Embed Size (px)

Citation preview

GeorgeAlogoskoufis,Interna'onalMacroeconomics,2016

TheMundell-FlemingModelandtheDornbuschModel

ProfessorGeorgeAlogoskoufisAthensUniversityofEconomicsandBusiness

1

GeorgeAlogoskoufis,Interna'onalMacroeconomics,2016

TheMundellFlemingModel

• This model has been the basis on which a large part of the short-term analysis of international macroeconomic phenomena has rested for several decades.

• It is an extension of the basic Keynesian model IS-LM, in an open economy with free capital mobility.

• The reference point of the model is that there is price rigidity in goods and services markets but that financial market prices adjust quickly in order to achieve equilibrium.

2

GeorgeAlogoskoufis,Interna'onalMacroeconomics,2016

TheStaFcFormoftheMundellFlemingModel

• We assume a small open economy, which takes international developments as exogenous, because of its small size.

• The demand for domestic goods and services depends on three factors: domestic income (positive), the domestic interest rate (negative) and the real exchange rate.

• The latter is defined as the relative price of international goods and services, expressed in domestic currency, and has a positive effect on domestic demand.

• These factors, together with fiscal policy, determine aggregate demand, which of course will be equal to total output.

3

GeorgeAlogoskoufis,Interna'onalMacroeconomics,2016

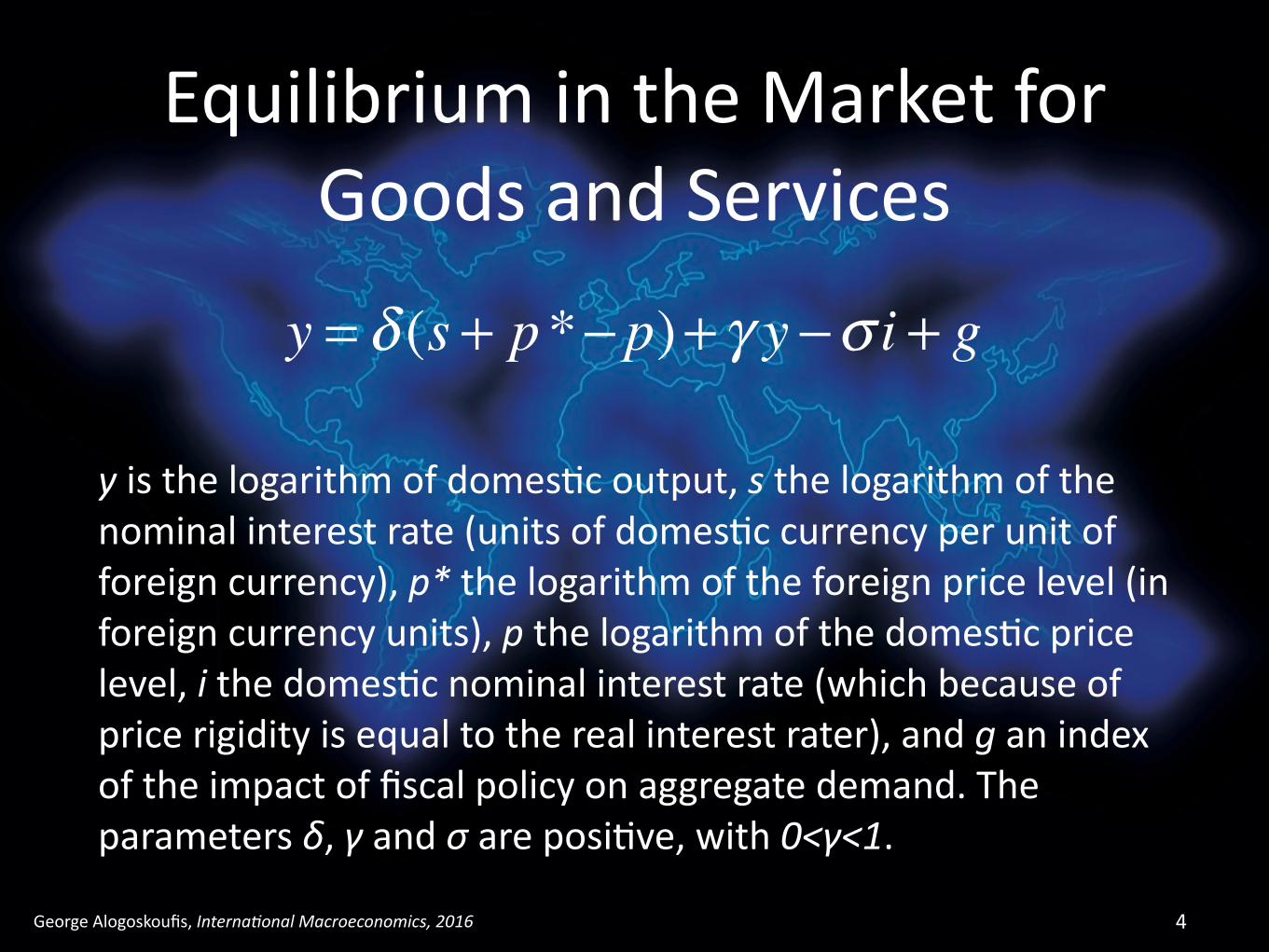

EquilibriumintheMarketforGoodsandServices

yisthelogarithmofdomesFcoutput,sthelogarithmofthenominalinterestrate(unitsofdomesFccurrencyperunitofforeigncurrency),p*thelogarithmoftheforeignpricelevel(inforeigncurrencyunits),pthelogarithmofthedomesFcpricelevel,ithedomesFcnominalinterestrate(whichbecauseofpricerigidityisequaltotherealinterestrater),andganindexoftheimpactoffiscalpolicyonaggregatedemand.Theparametersδ,γandσareposiFve,with0<γ<1.

4

y = δ (s + p*− p)+ γ y −σ i + g

GeorgeAlogoskoufis,Interna'onalMacroeconomics,2016

EquilibriumintheDomesFcMoneyMarket

misthelogarithmofthemoneysupply,φtheelasFcityofmoneydemandwithrespecttorealoutput,andλthesemi-elasFcityofmoneydemandwithrespecttothenominalinterestrate.

5

m − p = φy − λi

GeorgeAlogoskoufis,Interna'onalMacroeconomics,2016

EquilibriuminInternaFonalFinancialMarkets

WeassumethatthereisfreeinternaFonalcapitalmobility,andthatequilibriumintheinternaFonalfinancialmarketsimpliesuncoveredinterestparity.Withsta'cexpecta'onsaboutthefutureevoluFonoftheexchangerate,thismeansthatdomesFcinterestratesareequaltointernaFonalinterestrates.

6

i = i*

GeorgeAlogoskoufis,Interna'onalMacroeconomics,2016

ShortRunMacroeconomicEquilibriumintheMundellFlemingModel

7

GeorgeAlogoskoufis,Interna'onalMacroeconomics,2016

ARegimeofFixedExchangeRates

SubsFtuFnguncoveredinterestparityintheequilibriumcondiFonforthemarketsofgoodsandservicesandmoney,andtakingthetotaldifferenFalofthesystemofequaFonsobtained,weget,

8

dm = φδ1− γ

ds − λ + φσ1− γ

⎛⎝⎜

⎞⎠⎟di*+ φ

1− γdg

dy = δ1− γ

ds − σ1− γ

di*+ 11− γ

dg

GeorgeAlogoskoufis,Interna'onalMacroeconomics,2016

IneffecFvenessofMonetaryPolicyinaRegimeofFixedExchangeRates

9

GeorgeAlogoskoufis,Interna'onalMacroeconomics,2016

IneffecFvenessofMonetaryPolicyinaRegimeofFixedExchangeRates• AdomesFccreditexpansionhasnoeffectonthemoneysupply,ifthereisnochangeintheexchangerate,internaFonalinterestratesorfiscalpolicy.DomesFccreditexpansionwouldcauseforeignreserveouZlows,asdomesFcinterestratescannotfallbelowinternaFonalrates,andthecentralbankwillhavetointervenetosupportthefixedexchangerate.

• TheseouZlows,willbeequivalenttotheiniFalincreaseindomesFccredit,andtherewillbenoeffectonthedomesFcmoneysupply.

• TheMundellFlemingmodelpredictsthatdomesFcmonetarypolicyhasnoabilitytoinfluencetheeconomyunderaregimeoffixedexchangerates.

10

GeorgeAlogoskoufis,Interna'onalMacroeconomics,2016

EffectsofaDevaluaFon11

GeorgeAlogoskoufis,Interna'onalMacroeconomics,2016

EffectsofaDevaluaFon

AdevaluaFoncausesanincreaseinbothdomesFcincome,andthemoneysupply.Thisisduetotheshi]indemandinfavorofdomesFcproducts,theincreaseinnetexportsandtheconsequentaccumulaFonofforeignreservesthatincreasethemoneysupply.

Thus,adevaluaFoncausesbothanincreaseindomesFcincomeandanimprovementinthecurrentaccountinthismodel.

12

GeorgeAlogoskoufis,Interna'onalMacroeconomics,2016

EffectsofaFiscalExpansionunderFixedExchangeRates

13

GeorgeAlogoskoufis,Interna'onalMacroeconomics,2016

EffectsofaFiscalExpansionunderFixedExchangeRates

AfiscalexpansionincreasesbothdomesFcincomeandthedomesFcmoneysupply.ThisisbecauseitincreasesthedemandfordomesFcproducts,thisleadstoanincreaseinmoneydemand,which,withgivendomesFccredit,resultsininflowsofforeignexchangereserves,whichincreasethemoneysupply.

AlternaFvelyonecansaythatafiscalexpansioncausesupwardpressureondomesFcinterestrates,whichcauseforeigncapitalinflowstoequilibratethemoneymarket,asdomesFcinterestratesmaynotdifferfrominternaFonalrates.

WhereasadevaluaFonincreasesdomesFcincomebutcausesanimprovementinthecurrentaccount,iftheMarshallLernercondiFonissaFsfied,afiscalexpansioncausesadeterioraFoninthecurrentaccount.

14

GeorgeAlogoskoufis,Interna'onalMacroeconomics,2016

EffectsofanIncreaseinInternaFonalInterestRatesunderFixedExchangeRates

15

GeorgeAlogoskoufis,Interna'onalMacroeconomics,2016

EffectsofanIncreaseinInternaFonalInterestRatesunderFixedExchangeRates

Finally,anincreaseininternaFonalinterestratesleadstoadecreaseinbothdomesFcincome,andthemoneysupply.

TheincreaseininternaFonalinterestratescausecapitalouZlows,whichduetotheintervenFonsofthecentralbanktosupporttheexchangerate,reduceforeignexchangereservesandthemoneysupplyandincreasedomesFcinterestrates.

16

GeorgeAlogoskoufis,Interna'onalMacroeconomics,2016

DifferencebetweenFixedandFloaFngExchangeRates

WhenthemonetaryauthoriFesdonotinterveneintheforeignexchangemarket,ashappensunderfloaFngexchangerates,theendogenousvariablesaredomesFcincomeandtheexchangerate.Themoneysupply(anddomesFcinterestrates)canbeusedasapolicytool.

17

GeorgeAlogoskoufis,Interna'onalMacroeconomics,2016

FloaFngExchangeRates

SubsFtuFnguncoveredinterestparityintheequilibriumcondiFonsforthemarketsforgoodsandservicesandmoney,andtakingthetotaldifferenFalofthesystemofequaFonsobtained,weget,

18

ds = 1− γφδ

dm + λ(1− γ )+φσφδ

⎛⎝⎜

⎞⎠⎟di*− 1

δdg

dy = 1φdm + λ

φdi*

GeorgeAlogoskoufis,Interna'onalMacroeconomics,2016

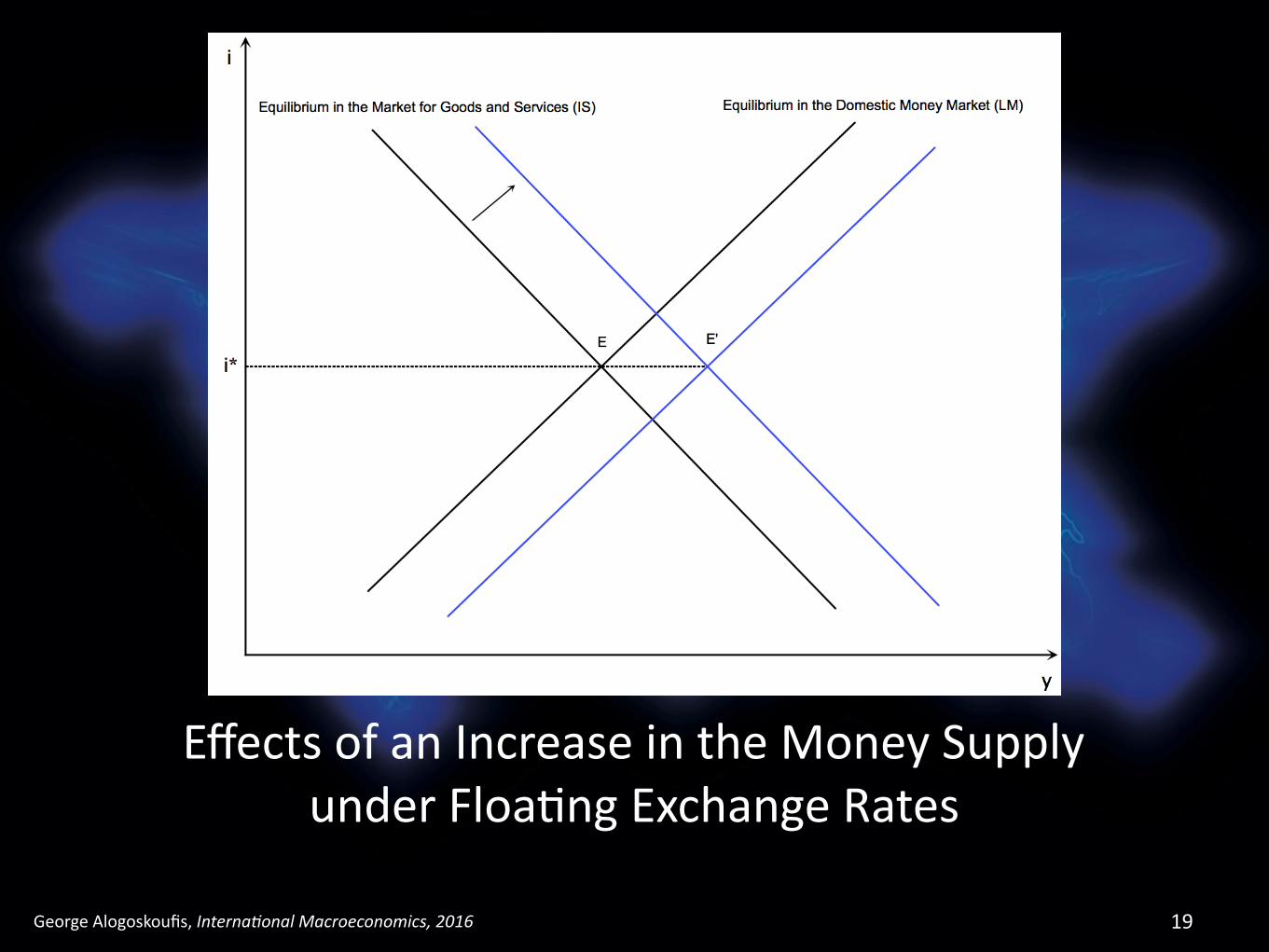

EffectsofanIncreaseintheMoneySupplyunderFloaFngExchangeRates

19

GeorgeAlogoskoufis,Interna'onalMacroeconomics,2016

EffectsofanIncreaseintheMoneySupplyunderFloaFngExchangeRates

AnincreaseinthemoneysupplythroughadomesFccreditexpansionleadstoadepreciaFonofthecurrency.ThedepreciaFoncausesanincreaseindomesFcdemandandhasaposiFveimpactondomesFcoutputandthecurrentaccount.

20

GeorgeAlogoskoufis,Interna'onalMacroeconomics,2016

EffectsofaFiscalExpansionunderFloaFngExchangeRates

21

GeorgeAlogoskoufis,Interna'onalMacroeconomics,2016

EffectsofaFiscalExpansionunderFloaFngExchangeRates

AfiscalexpansionputsupwardpressureondomesFcinterestrates,andcausesanappreciaFonoftheexchangerate.TheappreciaFonoftherealexchangeratereducesaggregatedomesFcdemandandcounteractsthedemandeffectsofthefiscalexpansion.Accordingly,afiscalexpansionisnotaccompaniedbymonetaryexpansion,hasnoimpactondomesFcoutputinafloaFngexchangerateregime.ItsonlyeffectistocauseanappreciaFonoftheexchangerateandadeterioraFoninthecurrentaccount.

22

GeorgeAlogoskoufis,Interna'onalMacroeconomics,2016

EffectsofanIncreaseinInternaFonalInterestRatesunderFloaFngExchangeRates

23

GeorgeAlogoskoufis,Interna'onalMacroeconomics,2016

EffectsofanIncreaseinInternaFonalInterestRatesunderFloaFngExchangeRates

AnincreaseininternaFonalinterestratesleadstoadepreciaFonofthedomesFccurrency.ThisleadstoanincreaseindomesFcdemand,astherestricFveeffectofrisinginterestratesisoutweighedbytheexpansionaryimpactofthedepreciaFonoftheexchangerate.TotheextentthatthedomesFcmoneysupplyisconstant,thedecreaseinmoneydemandcausedbytheincreaseininterestratesisoffsetbyanincreaseinmoneydemandduetoincreaseddomesFcoutputandincome.

24

GeorgeAlogoskoufis,Interna'onalMacroeconomics,2016

WeaknessesoftheMundellFlemingModel

• First,itignores,likeallshort-termmodelsofthistype,thedisFncFonbetweenstocks(suchasforeigndebt)andflows(suchasthecurrentaccount).

• Second,itassumescompletepricesFckiness,soitcannotsayanythingaboutpricechangesandinflaFonanditseffectsoninternalandexternalbalance.

• Third,itassumesstaFcexpectaFons.

• Finally,itsmicroeconomicfoundaFonsarenotbasedonopFmisingbehaviouronthepartofhouseholdsandfirms.

25

GeorgeAlogoskoufis,Interna'onalMacroeconomics,2016

TheDornbuschModelTheDornbuschmodelisasignificantimprovementoftheMundellFlemingmodel,inatleasttwodirecFons:

First,ithasalessextremeapproachtotheadjustmentofthepricelevel.Insteadofassumingconstantpricesitassumesthatthepricelevelgraduallyadjuststoequilibratethemarketforgoodsandservicesatfullemployment.

Second,insteadofstaFcexpectaFons,itassumesraFonalexpectaFonsaboutthefutureevoluFonoftheexchangerate,whichisassumedtobefloaFng.

Inthisway,themodelcanexplaintheovershooFngofnominalexchangeratestomonetarychanges,butalsotodescribetheadjustmentoftheeconomytowardslong-termequilibriumwithfullemployment.

26

GeorgeAlogoskoufis,Interna'onalMacroeconomics,2016

AssumpFonsoftheDornbuschModel

27

m − p = φy − λi

yd = δ (s − p)+ γ y −σ i + g

p•= π (yd − y)

i = i*+ se•

= i*+ s•

GeorgeAlogoskoufis,Interna'onalMacroeconomics,2016

SoluFonoftheDornbuschModel

28

s•= − 1

λ(m − p −φy + λi*) = − 1

λ(m − p −φy)− i*

p•= π δ (s − p)+ σ

λ(m − p)+ g − (1− γ )+ σφ

λ⎛⎝⎜

⎞⎠⎟ y

⎡⎣⎢

⎤⎦⎥

GeorgeAlogoskoufis,Interna'onalMacroeconomics,2016

LongRunEquilibriumintheDornbuschModelandtheAdjustmentPath

• First,thelong-runequilibriumcharacterizedbymonetaryneutrality.ApermanentchangeinthemoneysupplyhasnorealeffectbutmerelycausesachangeinthesameproporFontothepricelevelandtheexchangerate.

• Second,achangeinthemoneysupplyhasshort-termrealeffects,asthepricelevelcannotadjustimmediately,butonlygradually.Onlythenominalratecanchangeimmediately.

• Third,theeconomyconvergestoitslong-runequilibrium,fromanyiniFalstate.Thelongrunequilibriumisasaddlepoint,sincethetwofirstorderdifferenFalequaFonsofthemodelhaveoneposiFveandonenegaFveroot.Thereisauniquepaththatleadstothislong-termequilibrium.Thepathisuniquebecausethepricelevelisapredeterminedvariableandtheexchangerateisanonpredeterminedvariable.

29

GeorgeAlogoskoufis,Interna'onalMacroeconomics,2016

EquilibriumandAdjustmentintheDornbuschModel

30

GeorgeAlogoskoufis,Interna'onalMacroeconomics,2016

AnIncreaseintheMoneySupplyandExchangeRateOvershooFng

31

GeorgeAlogoskoufis,Interna'onalMacroeconomics,2016

TheInter-temporalEvoluFonoftheExchangeRate,PricesandInterestRates,FollowingaMonetaryExpansion

32

Χρόνος t

Χρόνος t

Χρόνος t

s

i

sE

sE'

s0

p

pE

pE'

i*

i0

t0

t0

t0

GeorgeAlogoskoufis,Interna'onalMacroeconomics,2016

TheInter-temporalEvoluFonoftheNominalandRealExchangeRate,FollowingaMonetaryExpansion

33

Χρόνος t

Χρόνος t

s

sE

sE'

s0

s+p*-p

t0

t00

GeorgeAlogoskoufis,Interna'onalMacroeconomics,2016

AFiscalExpansionintheDornbuschModel

34

GeorgeAlogoskoufis,Interna'onalMacroeconomics,2016

AnIncreaseinInternaFonalInterestRatesintheDornbuschModel

35

GeorgeAlogoskoufis,Interna'onalMacroeconomics,2016

ConclusionabouttheDornbuschModel

• TheDornbuschmodel,likemostmodelsbasedonthegradualadjustmentofthepricelevel,combineslong-runclassicalneutrality,withshort-runKeynesianfeatures.TheovershooFngofexchangeratechangeswouldnotoccurifthepriceleveldidnotadjustgradually,as,ifpricesalsoadjustedimmediately,theeconomywouldimmediatelyjumptoitslongrunequilibrium.

• TheDornbuschmodelexplainshowthecombinaFonofgradualadjustmentofthepricelevelandtheimmediateadjustmentofexchangeratesresultsinhighvolaFlityofbothnominalandrealexchangerates,asaresultofbothmonetary,andrealshocks.

• However,muchliketheMundellFlemingmodel,uponwhichitisanimprovement,theDornbuschmodellackssaFsfactorymicroeconomicfoundaFons.

36