Embed Size (px)

Citation preview

8/7/2019 The nationalization in the 21th century: The case of the hydrocarbons in Bolivia

http://slidepdf.com/reader/full/the-nationalization-in-the-21th-century-the-case-of-the-hydrocarbons-in-bolivia 1/43

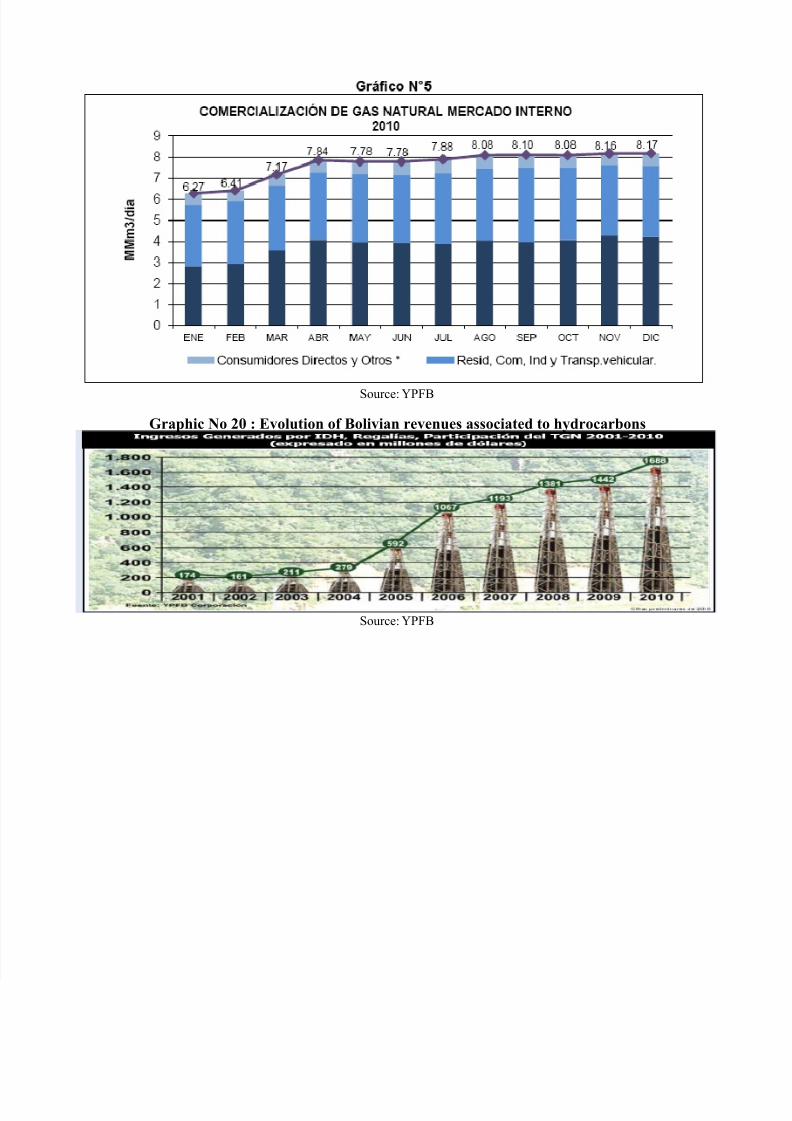

UNIVERSITÉ LAVAL

‘’LE PHÉNOMÈNE DE LA NATIONALISATION DANS LE SIÈCLE XXI : LE CAS DESHYDROCARBURES EN BOLIVIE’’

TRAVAIL PRÉSENTÉ À MONSIEUR MICHEL ROLAND DANS LE CADRE DU COURS DESÉMINAIRE DE FIN DE BACCALAURÉAT

17 MARS 2011

8/7/2019 The nationalization in the 21th century: The case of the hydrocarbons in Bolivia

http://slidepdf.com/reader/full/the-nationalization-in-the-21th-century-the-case-of-the-hydrocarbons-in-bolivia 2/43

SYNOPSISActuellement les politiques de nationalisation dans les pays en voie de développement sont regardées avec

scepticisme par la majorité d'économistes, pendant que pour les médias et la communauté internationale, elles

représentent des méthodes populistes et non-viables utilisées par certains politiques pour rester dans le pouvoir.

Ce travail propose étudier un des cas de nationalisation plus particuliers du siècle XIX: le cas de la

nationalisation de l'industrie d'hydrocarbures en Bolivie. Le travail s'intéresse d'abord en connaître l'industrie et

son contexte pour pouvoir trouver une façon de compréhension plus économique du processus de nationalisation

prenant comme bas des travaux théoriques sur l'économie de la régulation et l'information, et des modèles liés à

l'économie politique.

INDEX

SYNOPSIS(fr.)...........................................................................................................................................................................iINDEX................................................................................................................................................................

8/7/2019 The nationalization in the 21th century: The case of the hydrocarbons in Bolivia

http://slidepdf.com/reader/full/the-nationalization-in-the-21th-century-the-case-of-the-hydrocarbons-in-bolivia 3/43

......iiINTRODUCTION(fr.)..........................................................................................................................................iv

1. HYDROCARBONS IN CONTEXT 11.1. NATURAL GAS INDUSTRY 1

1.1.1. Overview and sources 1

1.1.2. The production chain of gas 11.1.3. World supply and demand 1

1.1.4. Prices 2

1.1.5. International trade 2

1.1.6. World reserves 3

1.1.7. Natural gas and other fuels 3

1.1.8 The South American regional market 3

2. BOLIVIA AND NATURAL GAS 42.1. BOLIVIA OVERVIEW 4

2.1.1. A landlocked country in the Andes 4

2.2. BOLIVIA'S GAS INDUSTRY 4

2.2.1. The natural gas and its importance for the country 4

2.2.2. A brief national history of natural gas 5

2.2.3. The natural gas industry before nationalization (1998-2006) 5

a. Regulatory structure 5

b. Infrastructure and operators 6

c. Domestic and international markets 6

d. Prices 7

e. Hydrocarbon revenues 7

f. Revenues distribution system and social conflicts 7

g. Social economic impacts of the boom: The Andersen CGE model for the Bolivian

economy 8

3. HYDROCARBONS NATIONALIZATION 9

3.1. UNDERSTANDING NATIONALIZATION 93.1.1. The Socialist State view of nationalization 9

3.1.2. The principal-agent dilemma to understand transitional economies 9

3.1.2. An empirical economic political approach to understand nationalization 12

3.2. THE NATURAL GAS INDUSTRY AFTER NATIONALIZATION (2006-2011) 14

3.2.1. Natural gas production and trade after nationalization 14

3.2.2. New revenues and distribution 15

8/7/2019 The nationalization in the 21th century: The case of the hydrocarbons in Bolivia

http://slidepdf.com/reader/full/the-nationalization-in-the-21th-century-the-case-of-the-hydrocarbons-in-bolivia 4/43

3.2.3. Allocation of hydrocarbon outputs and social benefits 15

3.2.4. Theoretical considerations 16

4. CONCLUSIONS 17

5. BIBLIOGRAPHY 19

6. APPENDIX

I.

OTHERS................................................................................................................................................

..

A. Public regulation versus public control

B. Matrix of nationalization

C. Guriev econometric results

II.

FIGURES...............................................................................................................................................

.......

II.

DIAGRAMS...........................................................................................................................................

.

III.

TABLES........................................................................................................................................................

IV.

GRAPHICS............................................................................................................................................

......

8/7/2019 The nationalization in the 21th century: The case of the hydrocarbons in Bolivia

http://slidepdf.com/reader/full/the-nationalization-in-the-21th-century-the-case-of-the-hydrocarbons-in-bolivia 5/43

INTRODUCTION

En 2003, le président bolivien Gonzalo Sanchez de Lozada a signé un contrat appelé ‘’Pacific LNG’’ pour

exporter le gaz naturel du pays au Mexique et aux États-Unis par son arche ennemi, le Chili. Ceci est amené le

pays à une grevé généralisée principalement motivée par les groupes plus marginalisés de la société. La Bolivie,

le pays avec une des sources gazières plus importantes de la région a cause de son niveau de intégration régional

avec ses voisins et le riches réserves encore inexplorées venait d'une crise politique et institutionnelle de dix ans

motivée par les intérêts particuliers des élites associées avec les gouvernement et les grosses entreprises

multinationales qui avaient simplement approfondi l'inégalité dans le pays.

Le période 2004 au 2006 était caractérisé par une forte transition économique, politique et sociale dans lequel

l'élément de fond et de changement était la volonté de la majorité de la population pour nationaliser l'industrie

d'hydrocarbures, cela qui apporte les plus grands revenus au gouvernement. Alors, la Bolivie en plein siècle XXI

décidait nationaliser son entreprise clé. Cela nous impose plusieurs questions comme économistes. En premier

lieu, on se demande sur la viabilité d'un processus comme tel dans une industrie ou les grandes transnationalesont montré être les plus efficients économiquement. Après, on se pose la question s'il existe quelque rationalité

économique et non seulement politique derrière d'un phénomène comme tel.

Ce travail intéresse à répondre à ces deux interrogations et autres. D'abord, on commencera par donner un bref

aperçu de l'industrie des hydrocarbures, toujours en se concentrant dans le gaz naturel, pour imaginer le contexte

auquel notre industrie doit s'affronter. Immédiatement, on passera à regarder des caractéristiques

socioéconomiques de base de la Bolivie. Après qu'on finisse avec ces deux tâches, on passera à montrer la

particularité de l'expérience de nationalisation bolivienne après et en avant du 2006 quand le président Evo

Morales a annoncé la politique officiellement. Pour comprendre la transition aussi sur une logique économique,

on essayera d'aborder le sujet de nationalisation en dehors du discours socialiste et sèchement politique, à partir

des travaux théoriques sur l'économie de la régulation et l'information, et quand même à partir des modèles

spécifiques liés à l'économie politique.

1. HYDROCARBONS IN CONTEXT

8/7/2019 The nationalization in the 21th century: The case of the hydrocarbons in Bolivia

http://slidepdf.com/reader/full/the-nationalization-in-the-21th-century-the-case-of-the-hydrocarbons-in-bolivia 6/43

1.1. NATURAL GAS INDUSTRY

1.1.1. Overview and sources

Today natural gas is seen as oil’s first cousin. Its importance has grown since the mid-1990s because it is the

cleanest, safest, and most readily useable of all energy sources.

The geophysical conditions where we find gas can be quite different (See figure No 1). The best-known sourceof natural gas is the conventional associated gas which is the gas found above an underground petroleum

deposit. Although when natural gas is found alone it is considered also a conventional source but of not

associated source. Conventional sources have been historically the most important. Various unconventional gas

sources also exist. Coalbed methane or coalbed gas is one of them and it is extracted from coal beds, as the

name suggests. There are important deposits of coalbed gas in the United States, Canada, and Australia.

Methane clathrate or ‘fire ice’ is another source but it has not been heavily exploited because its deposit sites

seem to be too dispersed for economic purposes. The only commercial source found today is located in Norilsk,

in Siberia. Tight gas is another source, which requires significant effort to extract because of its very deepgeological location. The only unconventional gas which has became an increasing source of natural gas is

derived from shale. It first began to be exploited in the US, but in recent years also by other OECD countries,

like Canada, which have a strong interest in this alternative source. Finally, natural gas isn't only found in

continental areas, but also under the sea. As such, the gas industry has recently developed an intensive offshore

gas drilling exploitation. The most important of these offshore gas sources are located in the Gulf of Mexico.

1.1.2. The production chain of gas (See diagram No 1).

1.1.3. World supply and demand

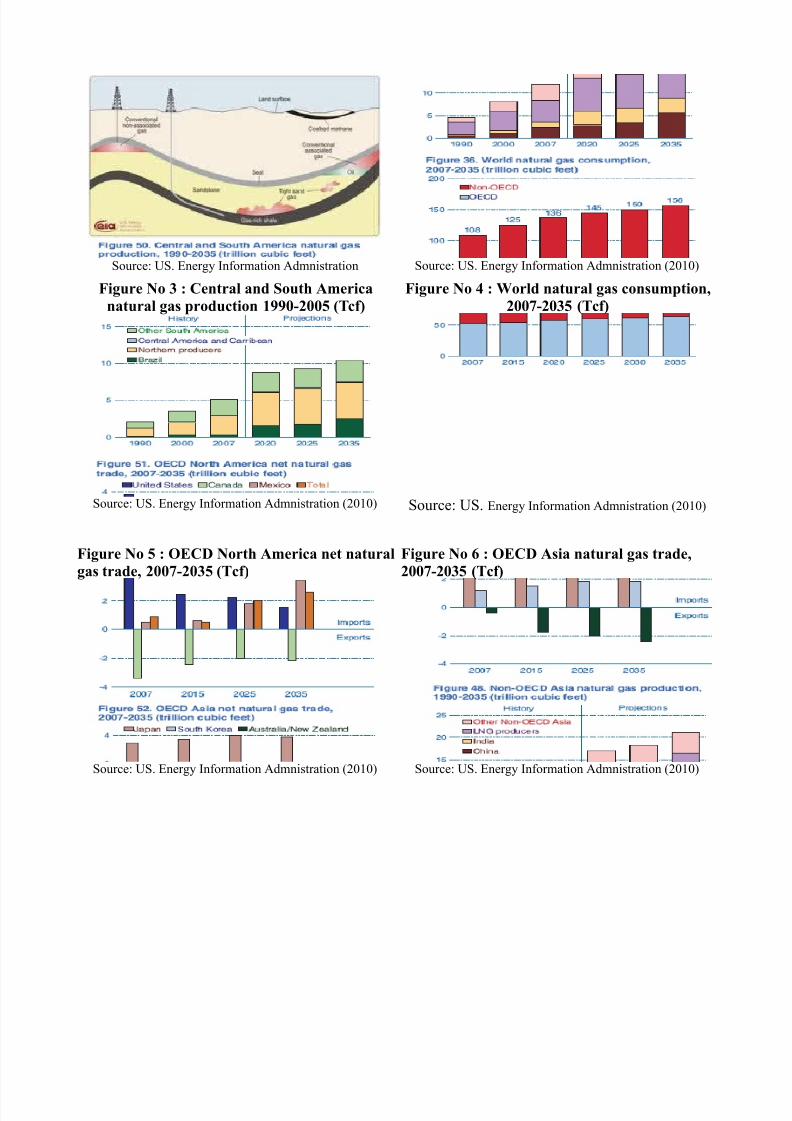

Originally, the US was the main supplier and innovator in the gas industry. However, the scenario is quite

diversified today. In 2007, according to the IEO2010 of the EIA (US Energy Information Administration), 106.6

trillon cubic feet (Tcf) were produced worldwide, with the US was responsible for only 19.2 Tcf of the total (See

table No 1) . Other OECD members with important natural gas productions were Western Europe and Canada

with 10.2 and 6.3 trillon cubic feet respectively. Outside of the OECD, in the same year, Russia was the

principal gas supplier in the world with 23.1 Tcf. Other non-OECD production included Asia (not including

China or Central Asia) and Eastern Europe, and Central Asia with 9.6 Tcf and 7.3 Tcf of natural gas respectively.

In general, most production was non-OECD. Moreover, future projections confirm this recent tendency; the blocexpected to have the fastest annual production growth in the next decades is non-OECD. So, in the year 2035

the non-OECD countries are forecast to produce 110.6 Tcf of the expected world total of 155.4 Tcf.

Furthermore, many non-OECD members are expected to boast strong production and growth, particularly Asia

(other than China and Central Asia) and Central and South America with 15.4 Tcf and 10.5 Tcf respectively (See

figures No 2 & No 3). About the consumption (See figure No 4).

8/7/2019 The nationalization in the 21th century: The case of the hydrocarbons in Bolivia

http://slidepdf.com/reader/full/the-nationalization-in-the-21th-century-the-case-of-the-hydrocarbons-in-bolivia 7/43

1.1.4. Prices

As the world market for natural gas is quite diversified in regional markets, it is difficult to speak in terms of a

single world price. Even though there is a trend for liberalization all over the world, natural gas markets are still

strongly regulated in many countries (e.g., Russia).

Price determination by public or private producers is quite complicated because it not only depends on the

specific costs of the natural production chain, but also on volatile market economic factors (e.g., the degree towhich the market is liberalized; expected economic growth), population changes, environmental legislation,

geographical factors (e.g., weather) and others. Nonetheless, according to the United Nations Conference on

Trade and Development (UNCTD, 2006), a simple understanding (with comparative purposes) of the gas price-

cost determination by a local industry could be done taking the three most important gas production associated

costs, as follows:

C = W + T + d

Where:

C: Price-cost per unitW: wellhead price (the cost of natural gas itself or commodity cost) per unit

T: long-distance transportation cost per unit

d: local distribution cost per unit

It is important to specify that this price-cost (C) is different from the market price. The price-cost represents an

abbreviated approximation of the variables costs associated with the extraction of the resource. In modern

resource economics theory, the difference between the market price and the price-cost (C) is understood as the

rent generated by the resource generated (i.e.,, Rent = Market price – Price-cost).

On the other hand, even the differences of markets, the Henry Hub natural gas spot prices, which is a pricing

point traded on the New York Merchantile Exchange (NYMEX), could considered the most acceptable indicator

of the industry internationally today. It measures the price of natural gas in USD per British thermal unit

(MMBtu).

1.1.5. International trade

In general, world natural gas trade suggests a growth in OECD natural gas demand from non-OECD productors.

In the OECD bloc in the year 2007, according to EIA, all their members were net importers, except for Canada

and Australia (See figures No 5 and No 6). In future, projections show that only the US will attempt to be less

dependent on the international natural gas trade, reducing its demand from almost 4 Tcf in 2007 to less than 2

Tcf in 2035.

In the year 2007, in the group of non-OECD producers, we distinguish the importance of Russia as a net

exporter with more than 6 Tcf exported mainly to the European market. Other important net exporters were

Qatar, Iran, North and West Africa, and South America (mainly Venezuela). EIA projects that this situation will

persist toward the year 2035. Moreover, the projections show a fast growth in natural gas demand by China and

8/7/2019 The nationalization in the 21th century: The case of the hydrocarbons in Bolivia

http://slidepdf.com/reader/full/the-nationalization-in-the-21th-century-the-case-of-the-hydrocarbons-in-bolivia 8/43

India, with both projected to become major net importers by 2035 (See figure No 7).

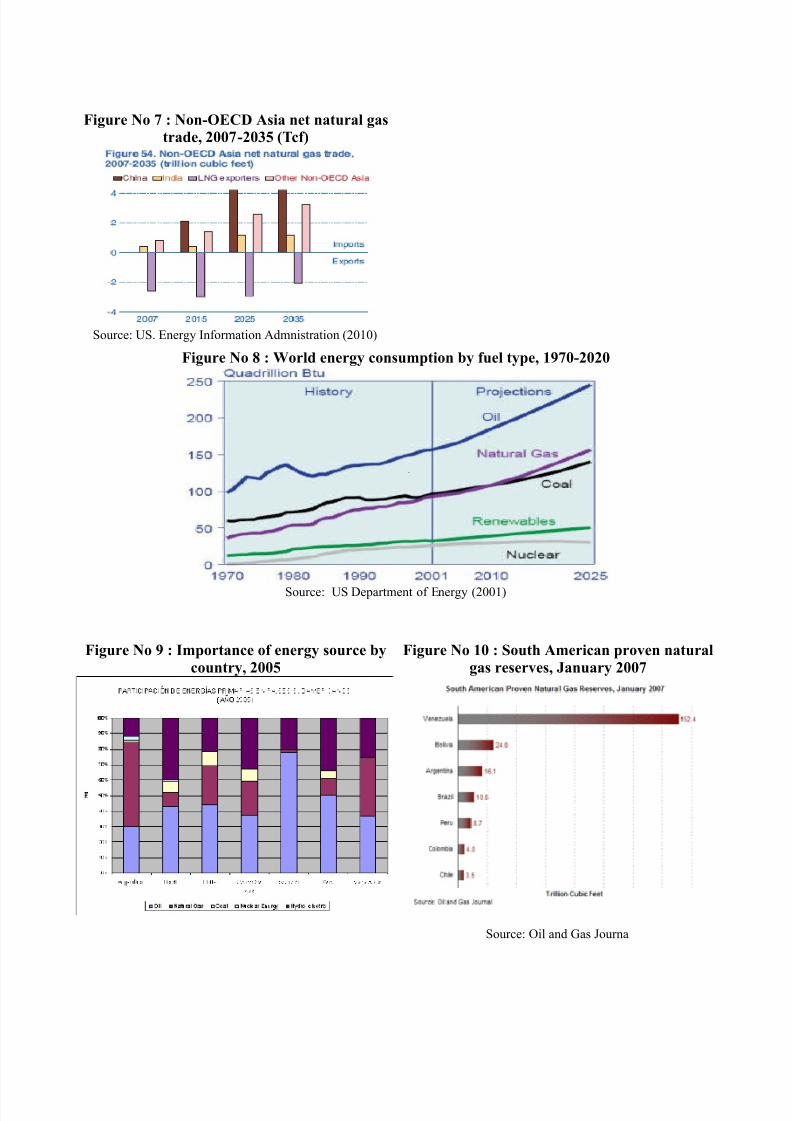

1.1.6. World reserves

In 2010, according to the Oil & Gas Journal , there was an estimated 6,609 Tcf of world reserves. According to

EIA, three-quarters of the world’s natural gas reserves were located in the Middle East and Eurasia. Russia

(1,680 Tcf), Iran (1,046 Tcf) and Qatar (899 Tcf) owned more than the 50% of the official reserves (See table No2).

1.1.7. Natural gas and other fuels (See figure No 8).

1.1.8. The South American regional market

In 2005, the most used energy resource in the region was oil (See figure No 9). However, natural gas held an

important second position. In market terms, the only two countries in a position of real net exporter were

Venezuela and Bolivia. Both also held the most important gas reserves in the year 2007 (See figure 10). It isimportant to notice that Bolivia (2010) held the highest non-associated gas reserves in the region, which means

that its reserves are mostly of free gas compared with Venezuela where half of its natural gas reserves were

associated with other gases that increases the overall cost to process of producing liquids. In terms of

infrastructure, the two main areas of gas production were Plataforma Deltana in the Orinoco river region

(Venezuela) and the region of Tarija (Bolivia). The best developed pipeline network was found in the Southern

side of South America, between Bolivia, Argentina, Brazil and Chile. Bolivia was the main exporter of this sub-

region, supplying the Argentinean and Brazilian markets. Nonetheless, there were also some natural gas

exchanges between Argentina and Chile. Meanwhile, in the north of the continent, the pipeline net extended

from Venezuela to Colombia and Panama (Central America). Regardless of this important infrastructure

integration, the most part of the Venezuelan production went to foreign markets to be commercialized through

OPEC, to which the country belongs.

Finally, according to OLADE (2006), under an scenario of low or high integration, the South American demand

for natural gas will tend to increase remarkably toward the year 2018, especially in the sub-region called Cono

Sur (Brazil, Paraguay, Uruguay, Argentina, and Chile).

2. BOLIVIA AND NATURAL GAS

2.1. BOLIVIA OVERVIEW

2.1.1. A landlocked country in the Andes

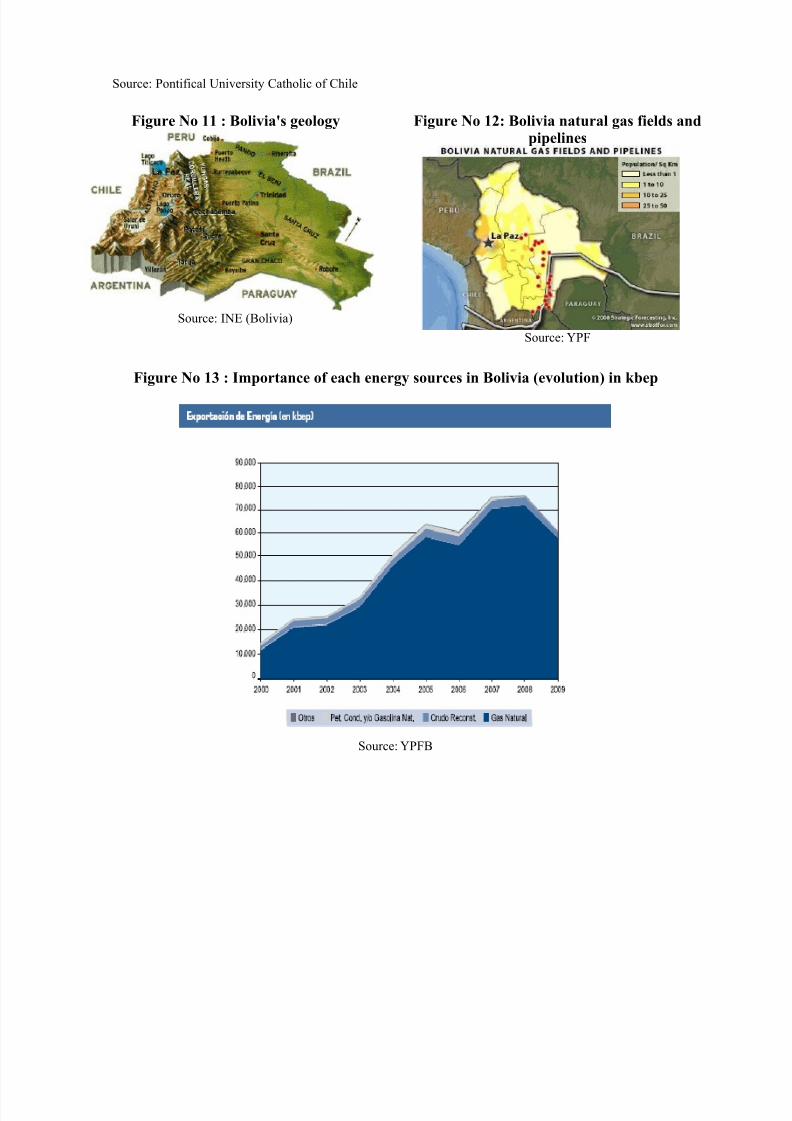

The Republic of Bolivia, founded in 1825, is a landlocked country located in the South American Andean

region. Bolivia's area represents 1,098,581 km2 and had a population of 10,027,643 inhabitants in 2009

according to estimates of the INE (National Institut of Statistics of Bolivia). The GDP and the GNI per capita

8/7/2019 The nationalization in the 21th century: The case of the hydrocarbons in Bolivia

http://slidepdf.com/reader/full/the-nationalization-in-the-21th-century-the-case-of-the-hydrocarbons-in-bolivia 9/43

were $17,339,992,191 and $1,630 respectively. Geographically, the country is composed of three main regions

(see figure No 11): the Altiplano (high plateau), the mountain valleys and the llanos (plains). The Altiplano, in

the west, is largely a high and desert region, but it contains important mineral resources. Meanwhile, the

mountain valleys contain mainly important fertile agricultural lands and are located in the heart of the country.

Finally, the llanos, at the east and north of the country are vast flat spaces where cattle farming has traditionally

been the main activity; however they also include important hydrocarbon deposits and wooded areas.Bolivia is characterized for being a quite unequal country due to rooted ethnic and economic differences. This

motivates a continuous political and social tension between the elites and the rest of the population, mainly

indigenous. According to be World Bank (2004), indigenous people represented the majority of the country at

62%. In rural areas, 72% of the population spoke a native language, compared to 36% in urban areas.

Meanwhile, in the llanos, 17% were indigenous compared to more than 60% in the Altiplano and mountain

valleys. Despite the internal differences and problems, Bolivia has undergone important economic and social

improvement in the last 10 years. The GDP has grown rapidly, driven mainly by the hydrocarbon industry (See

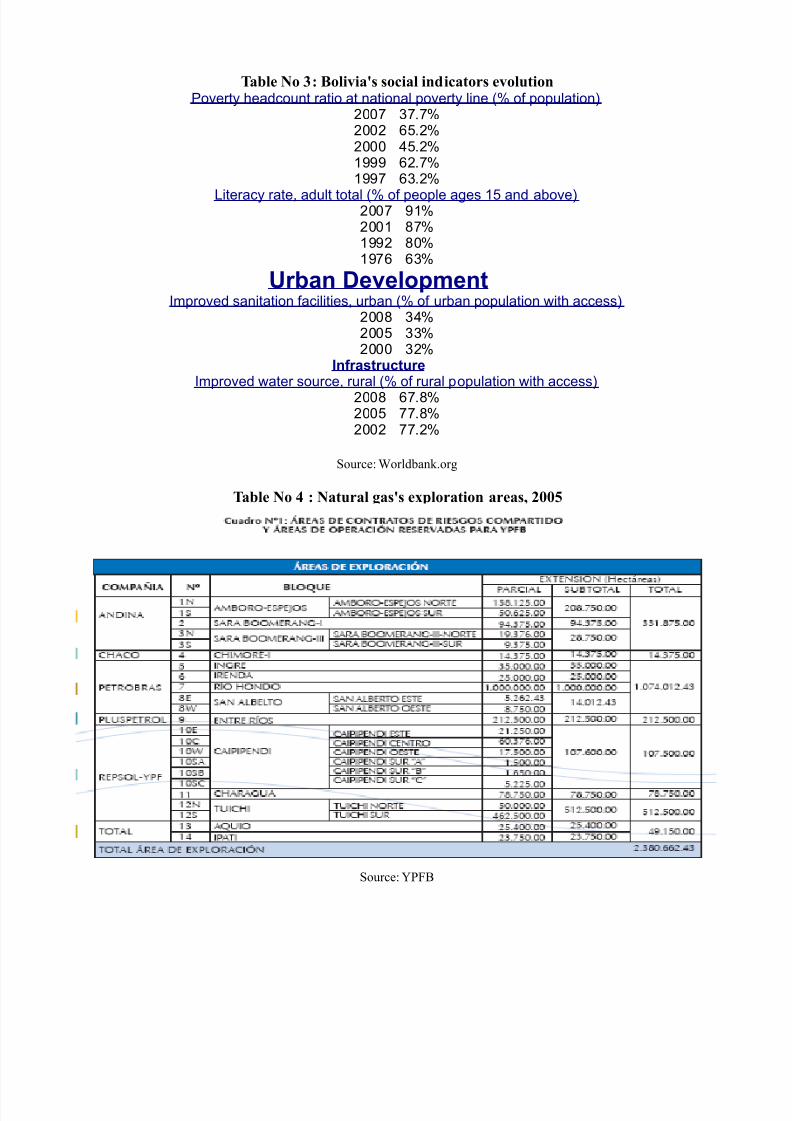

graphic No 1). While in the social aspect, poverty, literacy, urban development (such as sanitation facilities) andinfrastructure have improved remarkably (See table No 3).

The political and social instability, as with many other countries of the region, is the primary limiting factor in

the country’s economy. The recent instability started in 1993 when Gonzalo Sanchez de Lozada (also known as

Goni) assumed the presidency. Goni motivated by the Washington Consensus, brought an aggressive economic

and social reform for liberalizing the economy. The reforms were followed by the next civil presidents and

carried Bolivia to an ungovernable period of ten years. In 2003, during the second Sanchez de Lozada's

presidency, the most marginalized groups of the society held a general strike (known as The Gas War ) motivated

by the sale of natural gas to the US and Mexico through Chilean pipelines. This marked the fall of Gonzalo

Sanchez de Lozada and the beginning of a new period in Bolivian history.

2.2. BOLIVIA'S GAS INDUSTRY

2.2.1. The natural gas and its importance for the country

The importance of natural gas for the country is related mainly to two complex aspects: one economic and the

other social. In the economic realm, the recent natural gas boom represents an opportunity of important short-

term fiscal revenues for the government and economic growth in a context where world economies recover from

the recent downturn and the demand for fuels is on the rise. Meanwhile, in the social aspect, natural gas is themain factor of tension between the two recent identified groups which claim fair gas revenues distribution. We

refer to the eastern Bolivia which hold the majority of the rich lands in hydrocarbons and the western Bolivia

which claims for an egalitarian distribution of the resource revenues, also according to the population and

poverty of each region of the country.

2.2.2. A brief national history of natural gas

8/7/2019 The nationalization in the 21th century: The case of the hydrocarbons in Bolivia

http://slidepdf.com/reader/full/the-nationalization-in-the-21th-century-the-case-of-the-hydrocarbons-in-bolivia 10/43

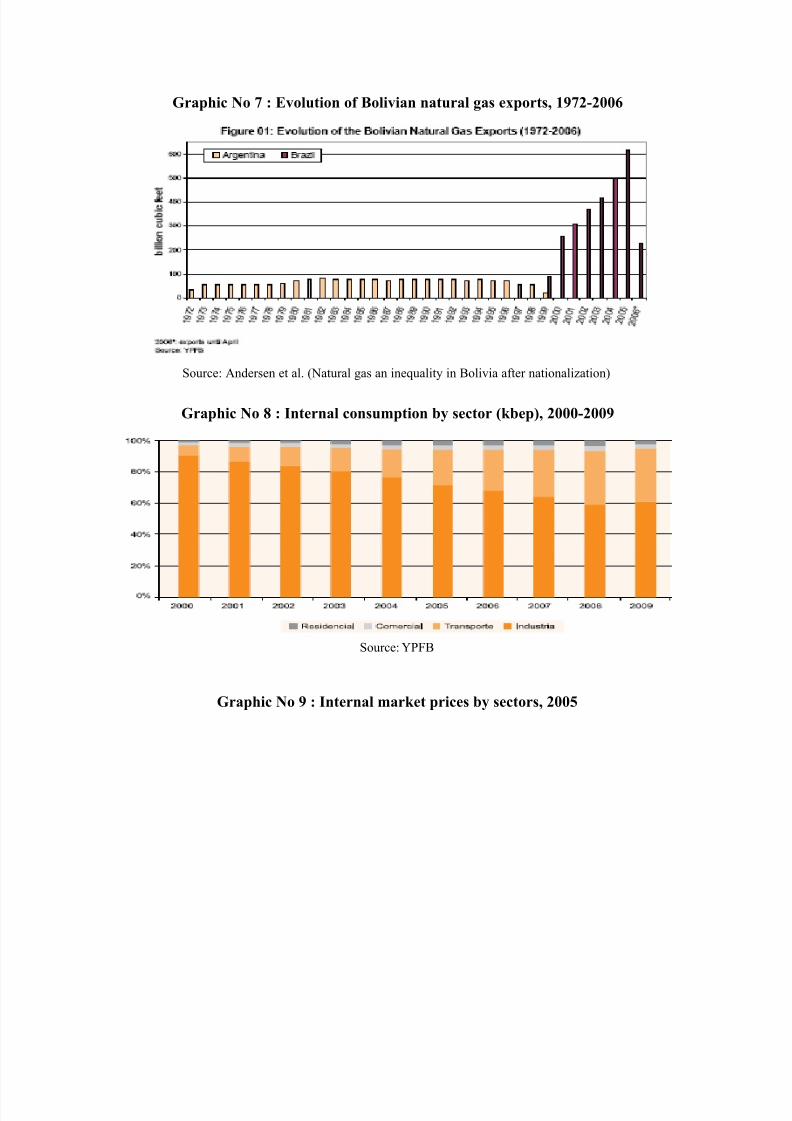

In the early 1970s, a contract was signed to supply Argentina with Bolivian natural gas. This was the beginning

of the Bolivian Gas Boom (See graphic No 2). The same oil companies managed the new natural gas

exploitation until the liberalization reforms of Sanchez de Lozada in 1996. The Goni government approved the

Ley de Capitalizacion (Law of Capitalization) for which YPFB was semi-privatized losing its power in the

hydrocarbons industry and big multinational corporations arrived to Bolivia. Petrobras, Repsol-YPF, BG, Enron

and Shell were some of the main companies that took position in the country. After the year 1996, thegovernment decided to fix the royalties and participations between 28%-48% of the companies’ revenues to

encourage the foreign investments. Since then, the industry underwent rapid growth, reaching 500,000 in 2004,

but also motivated by an important contract signed with Brazil to supply the country with 7.1 Tcf in 20 years.

Finally, in 2006, under the Evo Morales presidency the hydrocarbon industry was nationalized for a third time

and all the companies were obligated to renegotiate their contracts with YPFB, which again took control.

2.2.3. The natural gas industry before nationalization (1998-2006)

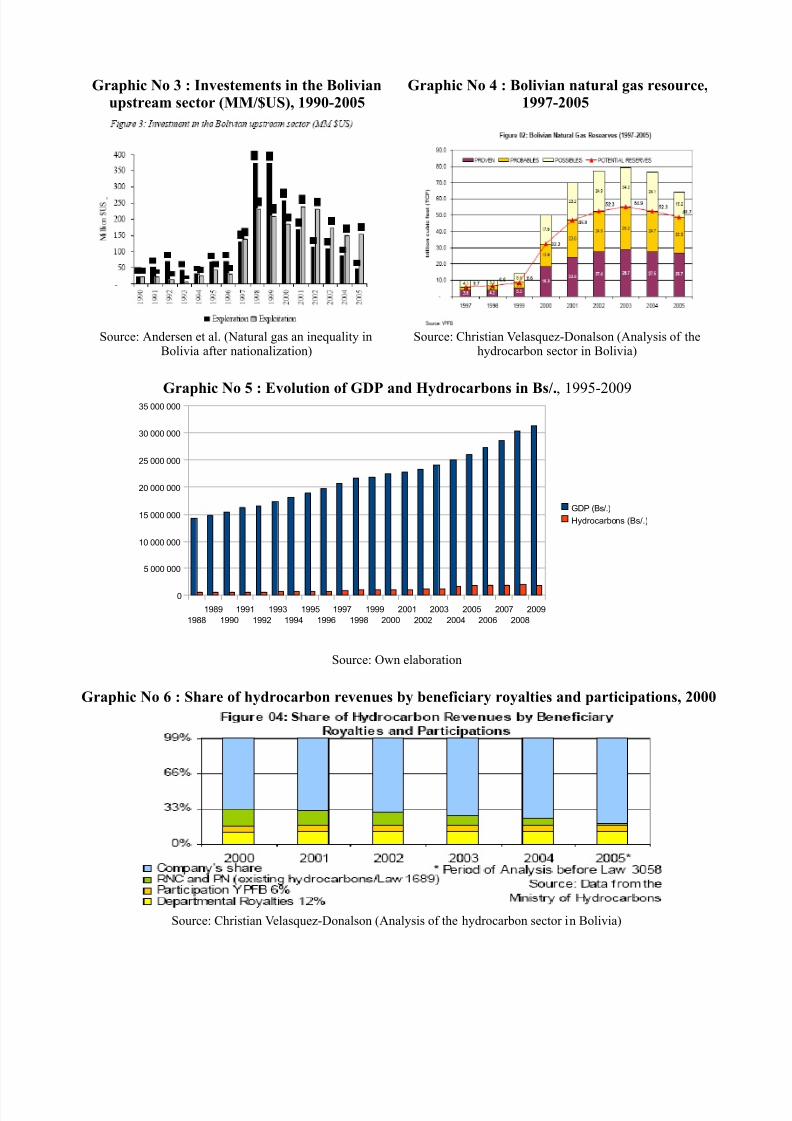

Between the contract to supply Argentina with natural gas (1972) and the nationalization (2006), the growth of the industry was unstoppable, despite the social and political problems. The liberalization reforms in the 1990s,

mainly the Law of Hydrocarbons, were the principal factor that stimulated the investments; explorations and the

growth of the industry (See graphic No 3). Thus, in the same period of reference the proved reserves increased,

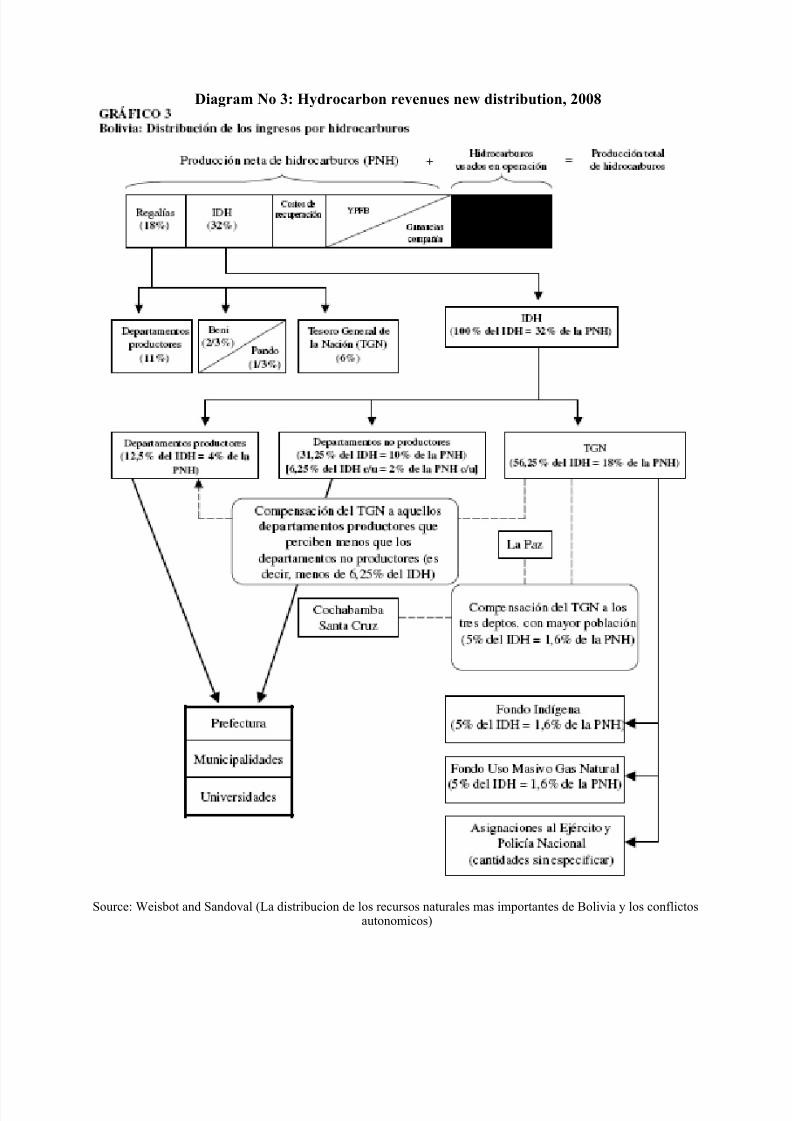

reaching 26.7 Tcf in 2005 (See graphic No 4) and the potential reserves were 48.7 Tcf. Moreover, the industry

enjoyed the fastest growth compared to GDP (See graphic No 5) and was the most representative between the

energy sources in the country (See figure No 13)

In 2006, Bolivia had a strategic position in the region because it held the second largest reserves in South

America, the interesting geographical location of the country in the heart of the South American region, and the

attractive increasing demand for fuels of North America before the economic downturn in 2008.

a. Regulatory structure

Until 2005, the only important change in legislation and regulation, after the Law of Hydrocarbons (1972), was

made by Sanchez de Lozada who promoted the Law of Capitalization (1996) which accelerated the

capitalization process of YPFB dividing the national company in three others (Andina, Chaco and Transredes)..

Law 1689 (1996) was also part of the reforms and banned YPFB from participating in any decision made in the

production chain of the industry. In the next years the industry became progressively more liberalized, so the

royalties and participations dropped in percentage until 2005 (See graphic No 6).

Finally, late 2005 under Meza's provisional government saw the introduction of Law 3058 or the Nueva Ley de

Hidrocarburos (New Law of Hydrocarbons) which was the legislative support to prepare the industry for the

nationalization some months later. The New Law of Hydrocarbons introduced the IDH (Direct Tax to

Hydrocarbons) which increased the government incomes from the industry and the FCD (Compensatory

Departmental Fund) which redistributed the revenues according to the population and production of each

Bolivian region.

b. Infrastructure and operators

8/7/2019 The nationalization in the 21th century: The case of the hydrocarbons in Bolivia

http://slidepdf.com/reader/full/the-nationalization-in-the-21th-century-the-case-of-the-hydrocarbons-in-bolivia 11/43

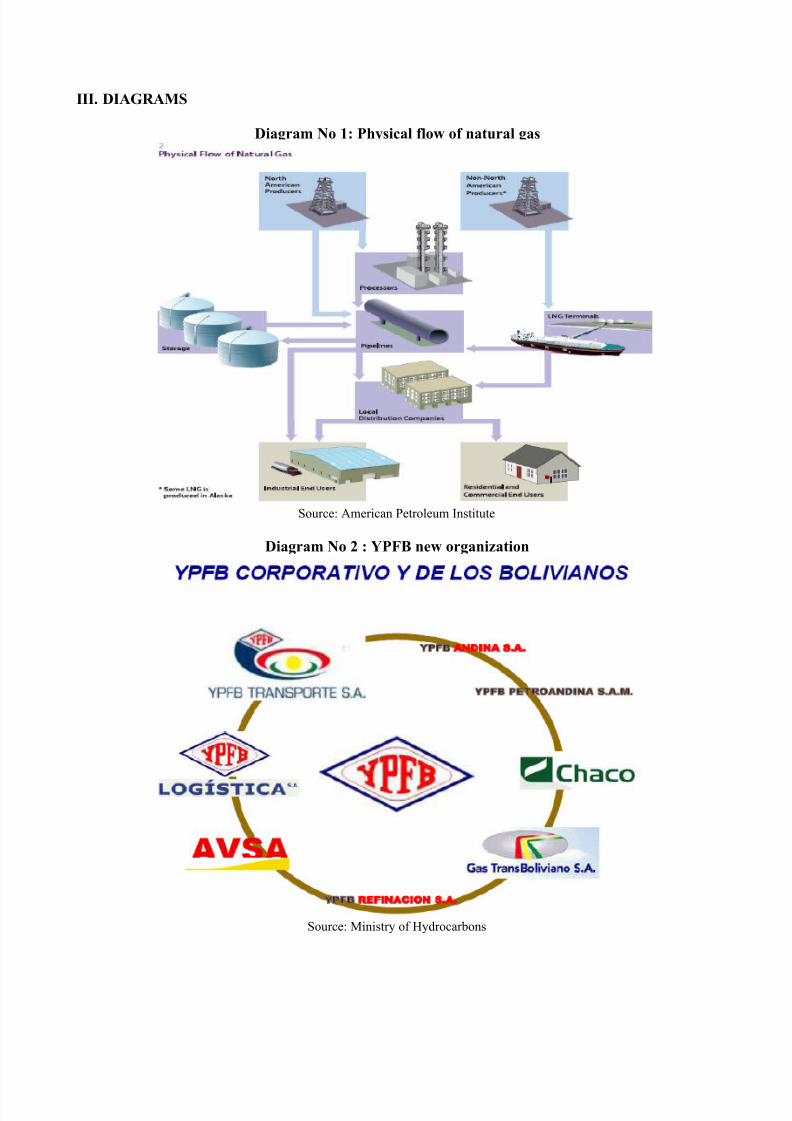

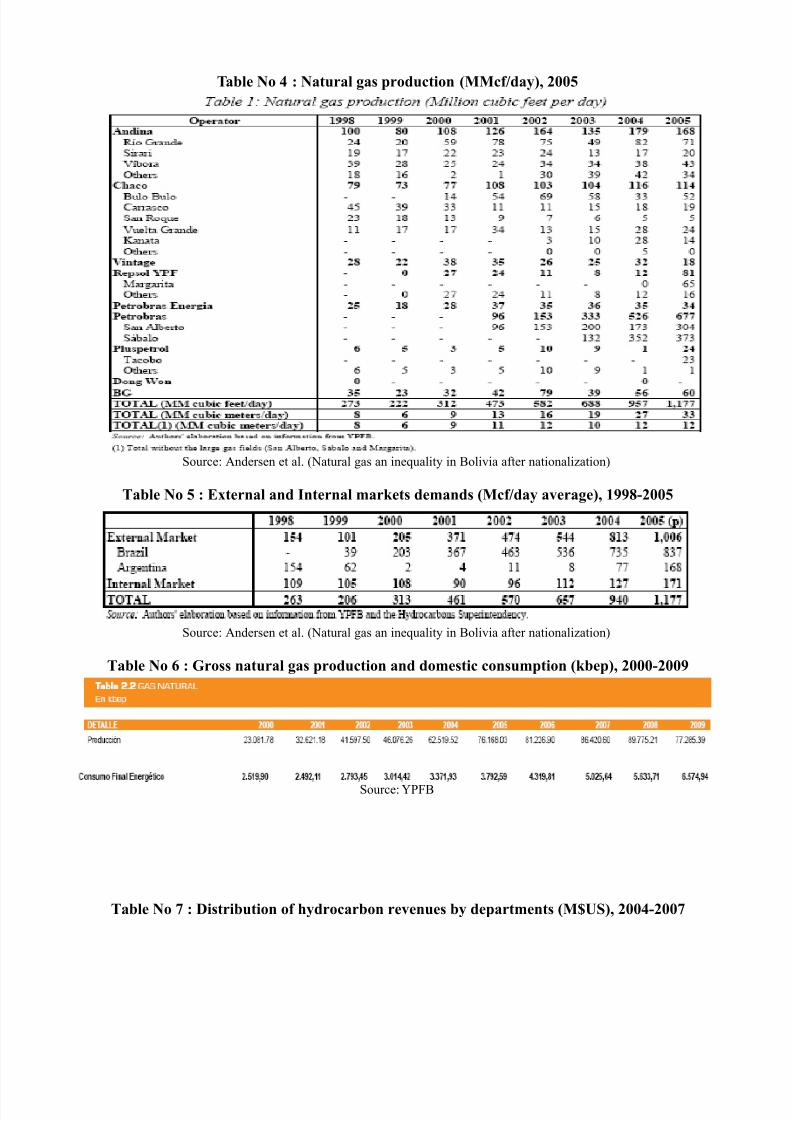

The majority of the hydrocarbons are concentrated in the eastern and northern provinces of Bolivia, mainly in

Beni, Santa Cruz and Tarija (see figure No 12). Thus, the main axis of the hydrocarbon infrastructure has been

developed in those regions. This is also one of the reasons for significant regional tensions and separatist

movements.

In 2005, there were five main companies operating in the country: Andina and Chaco (both mainly with foreign

investments), the Brazilian Petrobras, the American BG-Bolivia and the Spanish Repsol-YPF. Shell and Enroncontrolled the transportation system (Transredes) for the petroleum and natural gas. In exploitation, Repsol-YPF

was the largest company holding more than 152,900 hectares in concession. However, most important for the

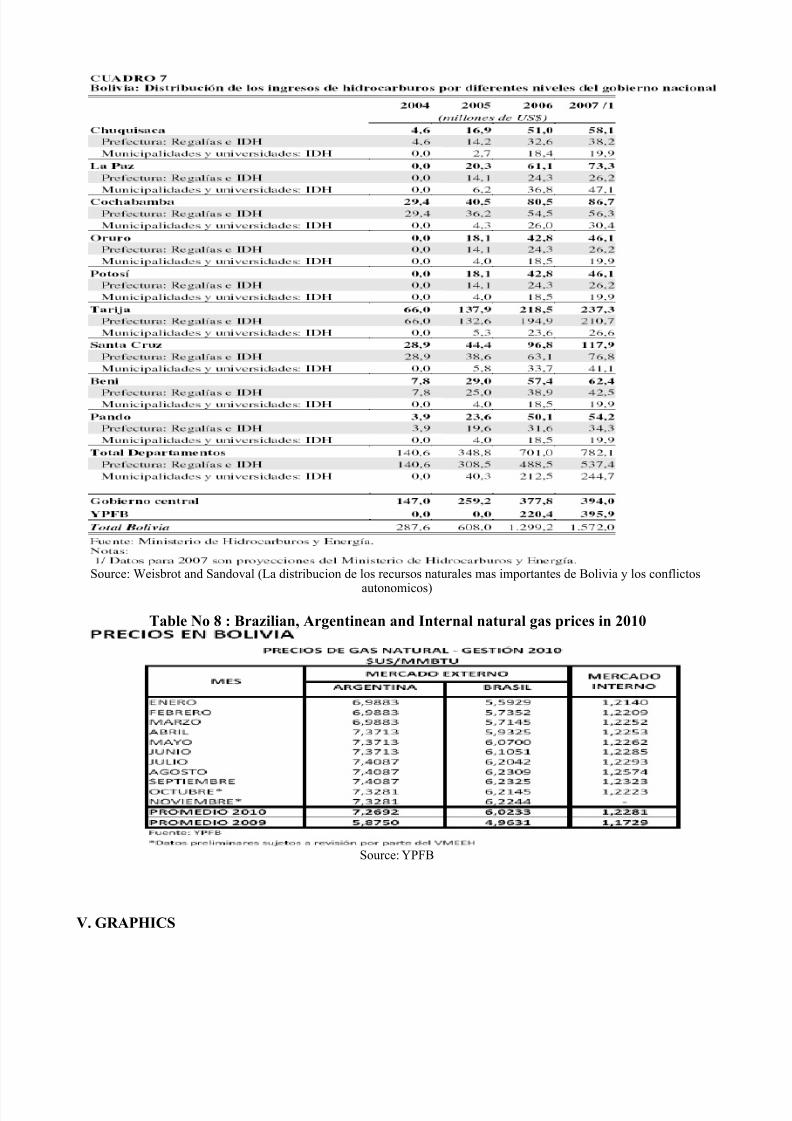

economy was Petrobras, which held more than 1 million hectares for exploration (See table No 5) and was the

most important productor with 677 MMcf per day (See table No 4). The two largest fields (San Alberto and

Sabalo) in Tarija were also held by Petrobras.

The production chain of the industry was organized as a typical North American circuit. The only important

difference in Bolivia was that the bulk of the production went to the international markets (Argentinean and

Brazilian markets) due to the profitability of these and the lack of infrastructure in the domestic market.c. Domestic and international markets

In the year 2005, in average more than 87% of the sales of natural gas were exported (Argentina and Brazil

markets), while only 13% were dedicated to the domestic market (See table No 5). According to CDDTA

(Center for democracy and development in the Americas) in the year 2006, more than the 50% of gas

consumption of Sao Paulo) depended on the Bolivian gas.

Until the year 1999, Argentina was the main international destination for these exports. The same year a GSA

contract was signed between YPFB and Brazil to supply its market (particularly the industrial market near Sao

Paulo) with a maximum of 30.08 MM cubic meters per day and around 7.1 Tcf in a period of 20 years, thereby

becoming the most important international market to date (See graphic No 7).

In terms of the domestic market, it consumption increased between the 2000-2005 period (See table No 6) from

2,519 kbep to 3,792 kbep, but this did not represent an important increase compared to the growth of the natural

gas production in the same period. In 2005, the main sector of consumption in the domestic market was

industrial, especially thermoelectric plants. However, an important growth of vehiicular natural gas (VNG)

(transport) was also observed (See graphic No 8).

d. Prices

According to Garron-Bozo (2002) the function for the Brasilian market (the principal market of Bolivia) was as

follows:W = P(i)*(0.5*(F01/F01o) + 0.25*(F02/F02o) + 0.25*(F02/F02o))

Where:

W: Wellhead price in USD per million of BTU (British thermal unit).

P(i): Price at the purchase and sale agreement which changes along the time.

F01, F02 and F03: Arithmetic averages of other fuel prices a trimester before the determination of W.

F01o, F02o, F03o:: Arithmetic averages of other fuel prices between January 1990 and June 1992.

8/7/2019 The nationalization in the 21th century: The case of the hydrocarbons in Bolivia

http://slidepdf.com/reader/full/the-nationalization-in-the-21th-century-the-case-of-the-hydrocarbons-in-bolivia 12/43

According to a study of the Pontifical Catholic University of Chile (2002), the average price-cost of Bolivian

natural gas in Sao Paulo in 2002 was 3.1 USD/MMBtu. So, if the wellhead price (W) was 1.19 USD/MMBtu,

we can deduce that the average transportation (t) more local distribution (d) was 1.91 USD/MMBtu. Meanwhile,

the cost of the Brazilian natural gas in Sao Paulo was 2.42 USD/MMBtu. This important difference would be an

economical reason which motivated the new elected president Luiz Inacio Lula Da Silva (2003) to stimulate the

(hydro) electricity industry to reduce its dependence on Bolivian gas.Concerning the domestic market, it was still harder to determine an approximate average value for the

transportation (t) and local distribution (d) costs, because the real final consumer prices were quite subsidized by

the Bolivian government. According to YPFB (2005), the final prices were relatively different depending on the

final sector of consumption. The industrial sector held the cheapest rate (See graphic No 9).

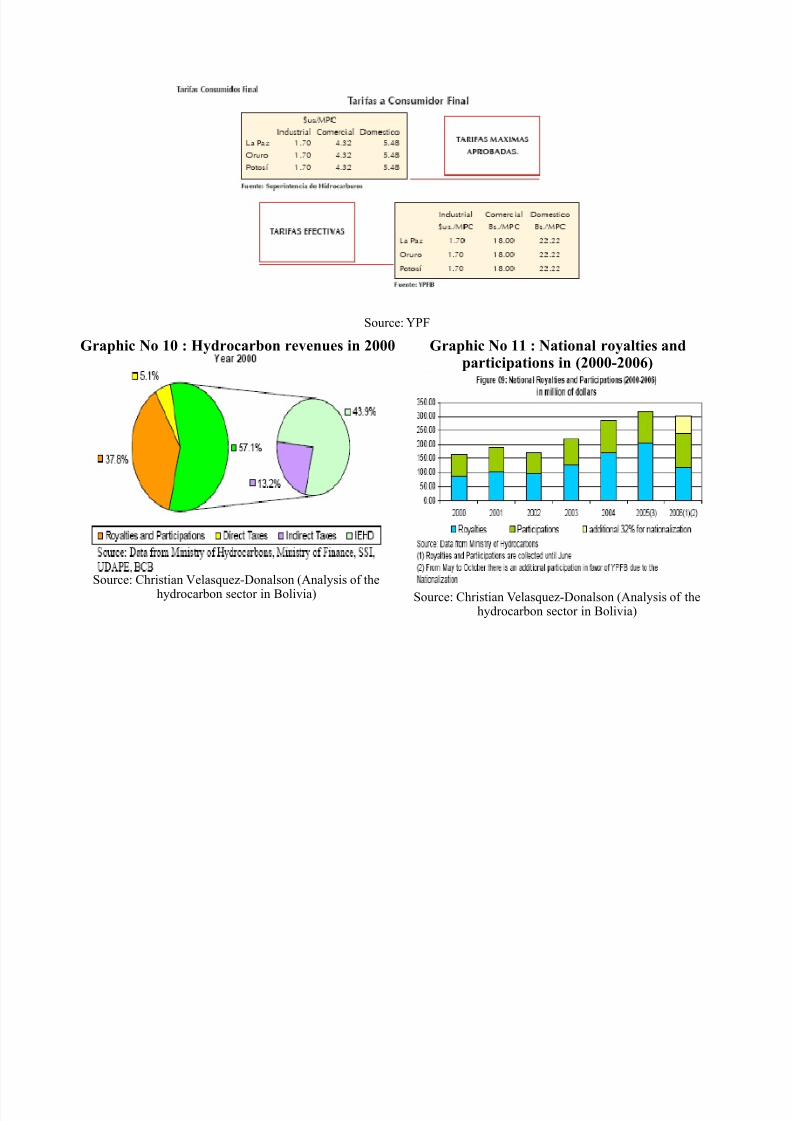

e. Hydrocarbon revenues

It is important to notice that the hydrocarbon revenues are not only limited to the pay of royalties and

participations by the fields’ operators. Actually, the tributary system for the hydrocarbons is composed by a

complex set of rates which covers all the production chain including the final consumer. Between 1994 andearly 2005, the tributary system didn't change remarkably, with the year 2000 serving as a good example (See

graphic No 10). We can see that the main components were the royalties and participations at 37.8%, as well as

the indirect taxes at 57.1%, standing up the IEHD (Special Tax to Hydrocarbons and Derivatives). The IEHD is

tax charged in the consecutive levels of the chain of natural gas production except to the fields’ operators.

As we saw before, although the royalties and participations dropped dramatically in percentage between the

2000-2005 period, the amount of taxes collected by the government passed from 150 millions USD to more than

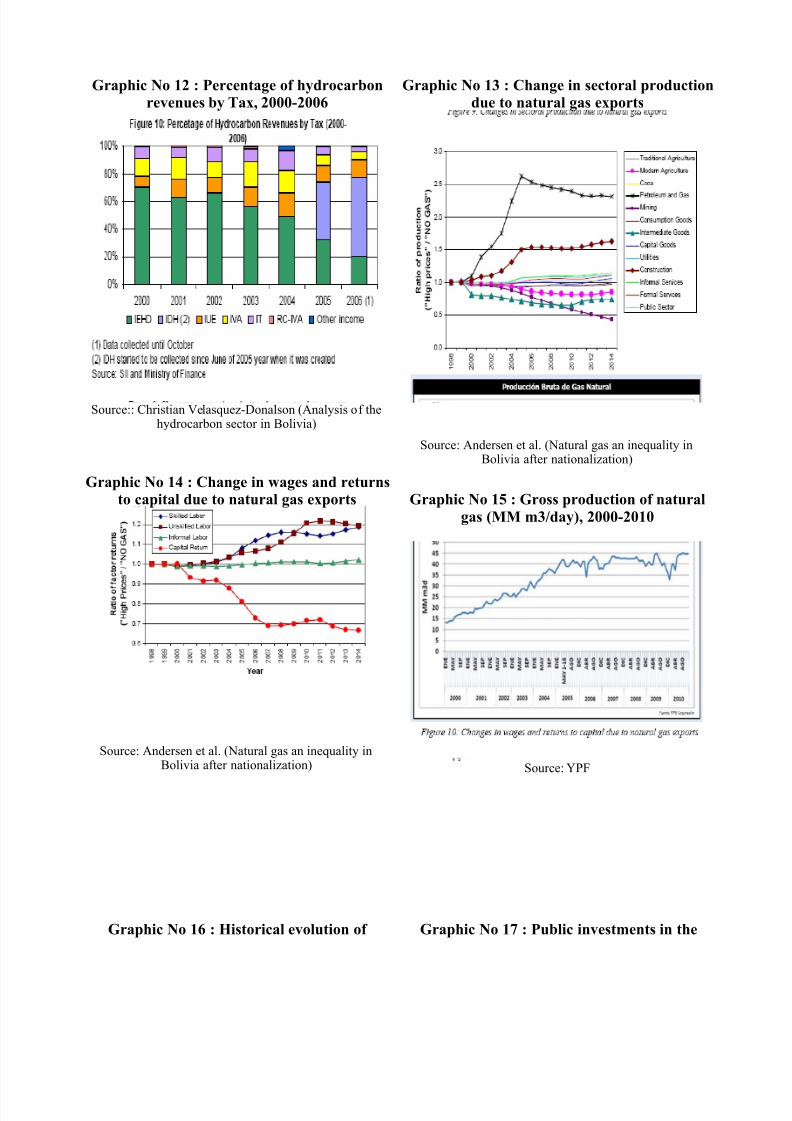

300 millions USD (See graphic No 11). As well, in the group of indirect taxes (See graphic No 12), we can see

that after 2000, the IEHD dropped progressively until 2005 when it was introduced the IDH as part of the New

Law of Hydrocarbons.

f. Revenues distribution system and social conflicts

Apart from the concession of gas exploitation and exploration to international investments, the revenues

distribution by region had been the second most important tension matter related to the natural gas industry for

the country.

Bolivia has three levels of administration. The central government is the main and the first one. The prefecturas

are like regional governments and there is one for each of the nine departments of Bolivia. The 352

municipalities represent the last level.

In terms of departments, royalties represent the only income-generation instrument related to the hydrocarbonindustry for the prefecturas. Central government transfers are another source of income, among there we found

funds provided by the Compensatory Departmental Fund (FCD) (since 2005), a share of 25 percent of the total

IEHD and the IDH (since 2005) in the year 2006.

In 2006, the eastern and northern provinces also called Media Luna (Cobija, Beni, Santa Cruz and Tarija) were

the main productors of natural gas, especially Tarija. Four years before, we could see that the only departments

which received royalties for natural gas were the Media Luna and Cochabamba (See table No 7). Since the

8/7/2019 The nationalization in the 21th century: The case of the hydrocarbons in Bolivia

http://slidepdf.com/reader/full/the-nationalization-in-the-21th-century-the-case-of-the-hydrocarbons-in-bolivia 13/43

introduction of the New Law of Hydrocarbons (2005) when the FCD and IDH were introduced, the situation

changed drastically. Thus, in 2006 the Media Luna had to share its natural gas income with those provinces that

had no such resources. The FCD was precisely accorded with the idea of a more equitable distribution based

also in the population of each department.

Although the eastern regions continued receiving the most important share of the gas rates, the new revenues

distribution provoked a strong controversy between western and eastern departments, two failed attempts of separatism via referendum and the general rejection of Morales in the Media Luna.

g. Social economic impacts of the boom: The Andersen CGE model for the Bolivian economy

Andersen et al. (2006) used a Computable General Equilibrium (CGE) model to measure the impacts of

hydrocarbon taxes and royalties in other production sectors and labor markets.

Firstly, according to the results of the model there are three important sectors (mining, modern agriculture and

intermediate goods) which suffer absolute reductions in their production levels in the long run as a direct

consequence of the natural gas boom (See graphic No 13). Also, it predicts that wages increase for both skilled

and unskilled workers. However, there is an import fall of capital returns due to the relative abundance of capitalin the assumed absence of productivity gains. Moreover the data shows that the agricultural workers, urban

informal and smallholders are the most affected by the growth of the industry (See graphic No 14).

Finally, according to Andersen et al., (2006), the decline of mining, the intermediate goods industry, and modern

agriculture (associated to a fall in the real income of agricultural workers) is a clear example of what is called

Dutch Disease in economics. While the fall of the real income of urban informal and smallholders, which

represent an important share of the Bolivian poor, could be understood as an increase of inequality due to the

gas boom. In general, the Andersen CGE model suggests that the boom generates a negative externality for an

important percentage of the poor population and theoretically they might prefer a no gas scenario.

8/7/2019 The nationalization in the 21th century: The case of the hydrocarbons in Bolivia

http://slidepdf.com/reader/full/the-nationalization-in-the-21th-century-the-case-of-the-hydrocarbons-in-bolivia 14/43

8/7/2019 The nationalization in the 21th century: The case of the hydrocarbons in Bolivia

http://slidepdf.com/reader/full/the-nationalization-in-the-21th-century-the-case-of-the-hydrocarbons-in-bolivia 15/43

in pursuit of social welfare.

Finally, years later emerged Socialism, as a product of the Marxism thesis, proposing a society where the

property and the production systems had to be controlled by the government (planned economy) ruled by the

majority working class. So, in a socialist country, the State Owned Enterprises (SOEs or public firms) became

the gears of economic machinery.

3.1.2. The principal-agent dilemma to understand transitional economies

Although that empirically the most part of Socialist countries have show theirs weakness to keep economic

targets (economic efficiency) and social targets (social welfare), the controversy between the use of private

enterprises or public firms is still alive, and motivated mainly by the current social democracy trend. However,

as we said before, the discussion today for an economic transition like nationalization is not more seen as part of

a planned economy (i.e., case of the Socialist State), but in a liberal context where the most part of countries

favor a free market economic approach. This discussion involves theoretical aspects of regulatory economics (a

branch of microeconomics), mainly related to the principal-agent dilemma and the asymmetric in formations.First, let's starts by making the difference between private enterprises and public firms, and why in modern

world an economic transition toward privatization (i.e., from public to private enterprises) has been mostly

preferred. De Allesi (1980) says about: 'The crucial difference between private and political (publicly owned)

firms is that ownership, in the latter effectively is nontransferable. Since this rules out specialization in their

ownership, it inhabits the capitalization of future consequences into current transfer prices and reduces owners'

incentives to monitor managerial behaviors. We refer now to two important fields of regulatory economics the

principal-agent theory and the property right.

Principal-agent theory (or the principal-agent dilemma) concerns the question of how to avoid an agent's

shirking behavior (it is a classic example of asymmetric information). According to privatization supporters one

of the objectives of privatization is to promote work incentive in public firms that SOEs don't do (i.e., they don't

have much incentive) to avoid shirking behavior. Holmstrom (1982) says that in this model of 'information

imperfection' (shirking behavior), the principal (owner) is required to regulate an agent who has private

knowledge about their production costs. So, if an audit is not implemented, the principal will grant the type of

agent who can exploit this private information a rent to stop his cheating behavior. This efficiency versus rent

trade-off has been proved robust in other extensions of the model.

In parallel, Grosman and Hart (1986) with their theory of 'incomplete contracts' see the principal agent dilemma

through the contract costs (which is a transactional cost). The contract costs for our case refers to the costsinvolved in a potential agent's shirking behavior. Hence, they defined the ownership of a firm as the acquisition

of 'residual rights of control' because when the contract is incomplete (i.e., the agent incur additional costs

caused by his behavior), the owner must afford it. So, in this case the allocation of property rights becomes

essential for efficiency considerations. All this lead us to model private and the public firms as two different

ownership structures. According to Suppington and Stiglitz (1987), the contract costs theoretically are less

costly in the public domain because the legal protection of private property is absent in this case. However, the

8/7/2019 The nationalization in the 21th century: The case of the hydrocarbons in Bolivia

http://slidepdf.com/reader/full/the-nationalization-in-the-21th-century-the-case-of-the-hydrocarbons-in-bolivia 16/43

authors suggest that it creates an important and harmful distortion of the behavior of the public firm; they refer

to the temptation of becoming a social planner.

Now let's generalize our case of shirking behavior to all asymmetric in formations in a principal-agent dilemma.

According to Shapiro and Willing (1990), the government is assumed to be able to collect data in the case of a

public firm, whereas in private firm some variables (i.e., information) cannot be verified by the government.

Hence, only in public firms the principal (government) and agent (public owner) are symmetrically informed.So, we can see clear different costs of intervention in public and private sectors.

Shapiro and Willing (1990) developed two agency models to compare the symmetry of information. In the first,

the public firm is owned by a public official (e.g., Minister), but run by a public manager on behalf of this first-

owner. Meanwhile, the private firm is composes by three players. On the top, an official is regulating the private

enterprise which belongs to a private owner. Below these two players, the private managers, who work for the

enterprise and are regulated by the official, have access to observe some exclusive information about the firm.

The main conclusion of this experience is that according to the authors the 'private information' that the manager

can obtain from the firm will be null as long as it arrives after an investment decision. So, this 'neutrality' leadsus that both models could be equivalents in a symmetrical information sense.

Returning to our interest of a nationalization or privatization policy, according to Schmidt (1996), the

government is interest if the costs and benefits of each policy. For the author, in a public firm scenario, the

principal (government) is well informed, but is unable to observe a technological factor and the manager's effort

level of a private firm. His main conclusion is: allocative efficiency is high but productive efficiency (economic

efficiency) is poor under nationalization. On the other hand, allocative efficiency is lower while economic

efficiency is higher under privatization due to a harder budget constraint.

We talked about the contract cost and the 'residual rights of control'. So, in the case of a financial distress in a

public firm, only the government will be the responsible for the loss. Hence, Coase supporters suggest that

private enterprises (privatization) are better when the property rights are well-defined because the invisible hand

will automatically sweep all barriers in the road to optimality. However, according to the Transactional Cost

School, this argument could be only valid when the ownership of the privatized firm can be allocated to a so-

called real 'economic man'. But in the real life huge and industrialized firms are the real actors in the economy,

so the separation (a problem) of ownership and managers (control) will always persist. Steinfeld (1999) says that

the key is not only in well-defined property rights, but also in building up a well-functioning market system.

Finally, it is important to distinguish that another important distinction between private and public enterprises

hinges on their respective objective functions. The owner of a private firm is only concerned with

profitability; its objective is profit maximization. As a property of the government, the objective

function of the public firm should subsume the interest of the public and the government officials, so

the public and the bureaucratic welfare will be the most important. This view is supported by the

Structure of Function scholars, and they also suggest that imperfect competitive market which involves

private and public firms, the economic system could be more efficient than in an only private

8/7/2019 The nationalization in the 21th century: The case of the hydrocarbons in Bolivia

http://slidepdf.com/reader/full/the-nationalization-in-the-21th-century-the-case-of-the-hydrocarbons-in-bolivia 17/43

enterprises system. Fershtman (1990) found empirical evidences to assure that in some of these cases

the private firm may not always be the one performing better. Moreover according to the author a

partly nationalized firm can earn a higher profit than a privatized firm in a duopolistic (Cournot)

market.

We have showed briefly the theoretical foundations of regulatory economics in a context of transitional

economies. In a private enterprise dominated economy, we know that according to modern public

economics that one of the functions of the government the regulation of market failures. The most typical

market failures are:

-Externalities (e.g., negative externalities)

-Public good (e.g., the fishery)

-Market powers (e.g., natural monopolies)

-Asymmetric information

Now, we want to clarify the role of the government with private and public enterprises in a context of

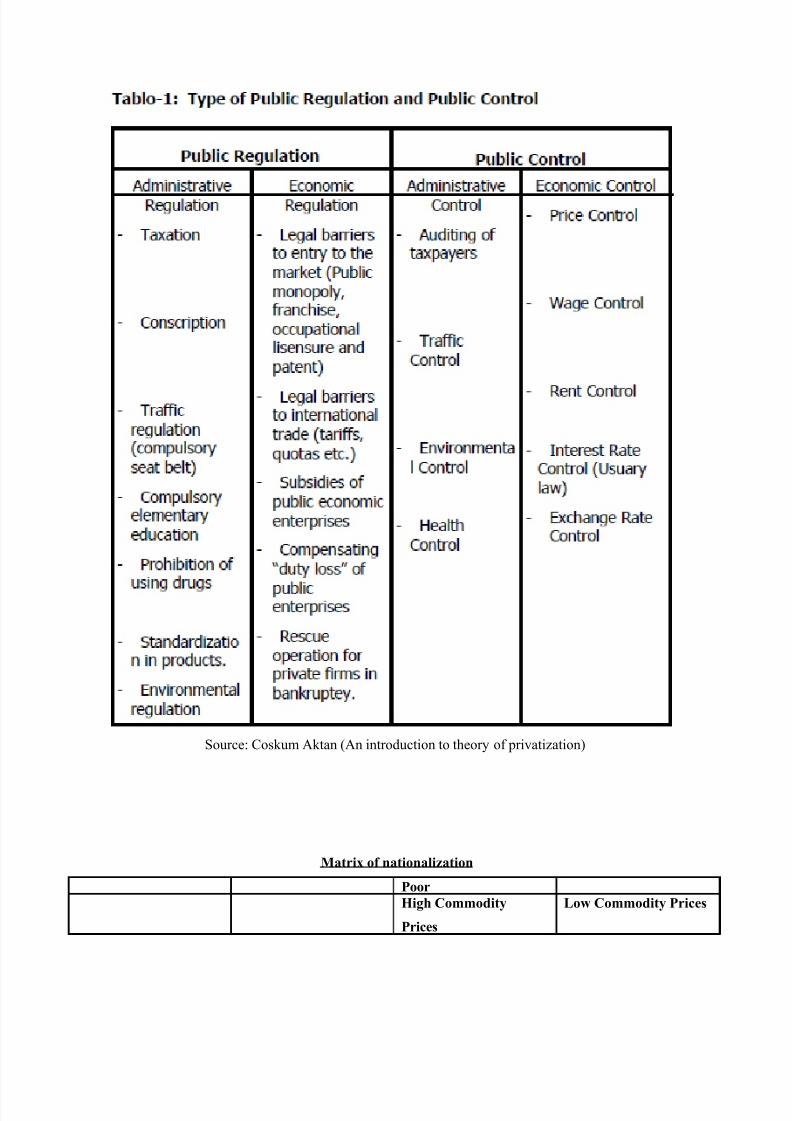

transitional economies. The regulation role of the government in a private enterprise finishes when it becomes

nationalized (public firms), because when it happens the government becomes a controller of the industry (See

Public regulation versus public control ).

3.1.3. An empirical economic political approach to understand nationalization

Boycko et al. (1996) suggest that public enterprises are inefficient because they are operated to pursue

certain objectives (e.g. excess employment, to satisfy the political parties). After privatization, the costs

for politicians to intervene in the firm in order to promote their personal goals become prohibitively

high, because privatization drives a wedge between the manager and the politician. So privatization

could render firms more efficient by controlling the politician’s discretion. But, what could happen in

cases where there are lobbies between private enterprises and government (politicians)? It would be

any incentive for a new re-nationalization? In the next paragraphs we will try to summarize the

econometric experience of Guriev and Kototilin (2009) about nationalization, which is very similar to

the Bolivian case, and some political economics notions, mainly from Acemoglu and Robinson (1999),

to understand how nationalisation could happen in some specific contexts.

Guriev and Kolotilin (2009) studied the nationalization in the oil industry around the world during 1960-2006.The authors develop an econometric model (using panel data) to show that in the majority of cases where the oil

industry was nationalized, the countries (130 countries) had a strong institutional weakness and there were

periods of high commodity prices (See Guriev econometric results). Moreover, this study was based in a

political economy study developed by Acemoglu and Robinson (1999) about political transitions.

The authors studies are concentrated in developing economies where there is a clear degree of inequality an

there is a key primary resource industry (e.g., mining, oil, gas). They imagine three actors: the government, the

8/7/2019 The nationalization in the 21th century: The case of the hydrocarbons in Bolivia

http://slidepdf.com/reader/full/the-nationalization-in-the-21th-century-the-case-of-the-hydrocarbons-in-bolivia 18/43

riches, who hold the key industry, and the poor who are the majority and can exert pressure in the government

through the median vote. The economy is mainly composed by private enterprises and the degree of the

dependance on the key industry is high. So, the principal role of the government in this economy is to regulate

the private enterprises that belong mainly to riches. Hence, we consider two firsts scenarios for this model: (i)

the government tax the enterprises (elites) fairly to compensate poors by the externalities generated

(environmental and social externalities), so the median vote intention is reflected in the decisions of thegovernment and it is perceived as democratic (strong institutions), (ii) the elites (enterprises) exert influence on

the government (lobbies), so the government don't tax fairly the companies, poors are affected and the

government is perceived as non-democratic (weak institutions). Moreover, we will introduce two more

scenarios: high commodity prices and stable commodities prices.

To understand this model, we will build a game chart with the four scenarios and the groups proposed ( see

Matrix of Nationalization). In the left we have the elites and the strong and weak institutions scenarios. While in

the right we have the poors and the high and stable commodities prices scenarios. According to our chart, in the

upper-left gap, the new revenues of the industry associated to the high prices are distributed equally (5, 5)between riches and poors. In the upper-right gap, the revenues are also distributed equally (2, 2) but they are

lower because the prices don't change. Meanwhile, in the lower-right gap, we see a clear inequality (3, 1) in the

distribution of the revenues when the prices are stables. However, in the lower-left gap, the situation is still more

unequal (8, 2) because when the revenues increase the elites take a more disproportionate share of the new

incomes. According to Acemoglu and Robinson (1999), this last gap represents the potential of a revolution, and

so the probable nationalization of the resource industry by the new government to gain the confidence of the

median voter. If it happens, the new distribution of revenues will be (0, 4). It means that the elite will loss every

income from the industry after the nationalization and the poor will receive a higher share from the taxation than

in (8, 2). It is importance to notice that this share of taxation for the poor will be lower than the income in a

democratic scenario (strong institutions) with private enterprises and high commodity prices.

According to Acemoglu and Robinson (1999) the riches could try to change the situation: 'The rich (elite) will

try to prevent revolution, by making concessions to the poor, for example in the form of income redistribution.

Because the threat of revolution is often only transitory, current redistribution does not guarantee future

redistribution. If this temporary redistribution is insufficient to prevent a revolution, as it will be in a very

unequal society, the elite will be forced to make a credible commitment to future income redistribution'

A strong economical argument which supports this view comes from the econometric experiences of Guriev and

Kolotilin (2009) that suggest that the immediate proceeds of nationalization (because of the high prices) couldcompensate the long-term losses in efficiency.

Some other real cases where nationalization happens because of the mediun voter like in the experience of

Guriev and Kototilin, are:

-When the private enterprise is weak and don't guarantee prices stability

-When the private enterprise have a macroeconomic importance for the economy (as the case of Guriev and

Kototilin).

8/7/2019 The nationalization in the 21th century: The case of the hydrocarbons in Bolivia

http://slidepdf.com/reader/full/the-nationalization-in-the-21th-century-the-case-of-the-hydrocarbons-in-bolivia 19/43

-Delivery of critical infrastructure (i.e., the construction of roads, dams, or public buildings).

-Strategic justifications (i.e., nuclear industries).

Moreover, before closing this theoretical framework part it is important to know that the nationalization of

private property can be classified into the four categories: (i) formal expropriation, (ii) intervention, (iii) forced

sale and (ii) contract renegotiation. The nationalization process is usually accompanied by the payment of compensation.

On other aspect, the main arguments against the SOE comes from the theory of Corporative Finances which

assures that under this type of organization there aren't important incentives for the maximization of enterprises

profits, the innovation and the free rider comportment (corruption) is stimulated.

3.2. THE NATURAL GAS INDUSTRY AFTER NATIONALIZATION (2006-2011)

The decree of hydrocarbons nationalization (28071), was promulgated on May 1st, 2006. According to this

document, YPFB recovers the ownership of resources as defined in the Law of Hydrocarbons (1972). Thegovernment will nationalize the necessary shares to control Chaco, Andina, Transredes and Petrobras-

Refinamiento controlling at least 51% of each enterprise. Moreover, the companies who want to continue to

operate in the country (exploration and production) must renegotiate their contracts with YPFB in the next 180

days. Finally, the decree suggests that YPFB will start a reorganization to become a corporate, clear and efficient

enterprise with the purpose of guaranteeing social welfare.

The hydrocarbon nationalization is a very complex process to analyze which involves different economic and

social variables in the short and long term. Under an economic view, we can recognize three main axes of

effects: (i) the new production organization of the industry (See diagram No 2), (ii) the economic short-term

effects (i.e., aggregate production, domestic and international trade changes, distribution of revenues and

allocation of outputs), and (iii) the social-microeconomic effects associated to the externalities (positives or

negatives) caused by nationalization. Because our analysis is concentrated in the economic spectrum and

Bolivian nationalization is too recent to allow discussion of associated socio-microeconomic effects or long-

term macroeconomic effects, we will center our attention mainly on the economic short-term consequences.

3.2.1. Natural gas production and trade after nationalization

Between the year 2004 and 2010, gross natural gas production underwent a slight stagnation, probably

associated to the economic downturn in 2008 and nationalization (2006). Moreover, the 2009 downturn wasmotivated by a contraction in the Brazilian demand. However, in general terms, the trend of the decade was

positive; increasing from 15.6 MM cubic meters per day in 2000 to 45 MM cubic meters per day in 2010 (See

graphic No 15).

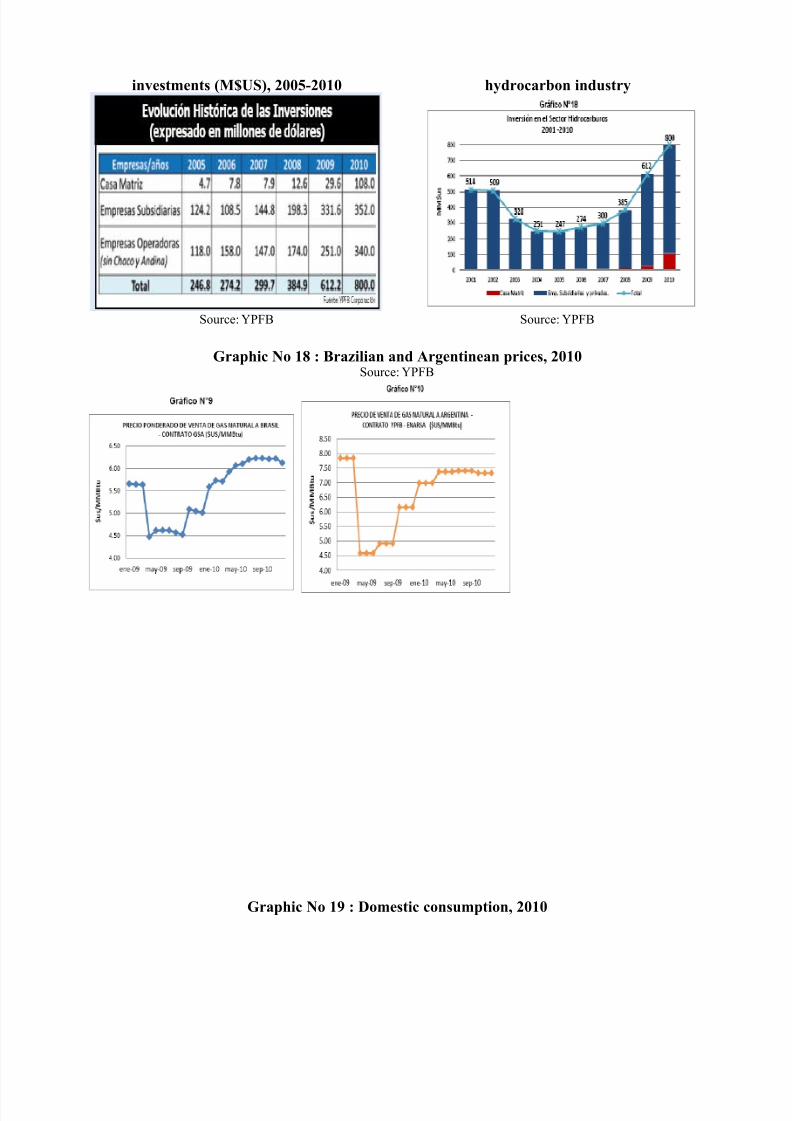

After the nationalization and the recovery of the basic productive structure of the industry, the investments grew

remarkably changing from USD$247 million in 2005 to USD$612 million in 2009 and USD$800 in 2010 (See

graphic No 16). This was closely related to the public investment that grew since 2004 (See graphic No 17).

8/7/2019 The nationalization in the 21th century: The case of the hydrocarbons in Bolivia

http://slidepdf.com/reader/full/the-nationalization-in-the-21th-century-the-case-of-the-hydrocarbons-in-bolivia 20/43

In terms of international trade, as we know Argentina officially ended its demand for Bolivian gas in 2006. But

last year, after a long dialogue between YPFB and ENASAR (National Enterprise of Energy of Argentina), a

new deal was signed and Bolivia compromised to supply the market with 5 MM cubic meters per day, to be

increased progressively until the year 2026. In 2010, the exportation was quite stable reaching more than 35

MMm3/day.

The price charts for the international markets for the years 2009 and 2010 (See graphic No 18) show that theBolivian natural gas prices, even after the nationalization, continued following a free market trend because they

fell during the periods of contraction (2009) and increased during the recovery (2010). So, the international

demand was elastic. Moreover, there was an important correlation between both prices and the Henry Hub

international price.

In the domestic market, between nationalization (2006) and the year 2009, domestic consumption increased

from 4,319 to 6,574 kbep. The domestic sector with the fastest-growing consumption was transportation, while

the industrial sector decreased. It was related to an aggressive post-nationalization policy for the use of

Vehicular Natural Gas (VNG). In 2010, the domestic consumption increased again, reaching, on average, morethan 8 MM cubic meters per day (See graphic No 19).

Regarding internal prices, we can distinguish that after the nationalization they became still more subsidized. As

an example, average prices for the year 2010 (See table No 8) show a clear difference compared to the

international prices.

Finally, another important consequence of the nationalization was that the government decided to expand the

production chain, introducing new structures to ensure the industrialization of the resource. So, the government

created the EBIH (Bolivian Enterprise for the Nationalization of Hydrocarbons) which would be responsible for

this task, and many associated projects were planned (Appendix minis). Also, the IBE (Bolivian Institute of

Energy) was created to cooperate with YPFB in the development of the industry.

3.3.2. New revenues and distribution

One of the most important effects of nationalization was the progressive increase of hydrocarbon revenues

reaching USD$1.688 billion in 2010, compared to just USD$279 million in 2004 (See graphic No 20). As we

have seen before, the main innovation in taxation was related to the introduction of the IDH (Direct Tax to

Hydrocarbons) in the year 2005. The only fundamental difference since its creation was that it has increased

progressively. Weisbrot and Sandoval (2008) summarize the new system of revenues related to the production of

hydrocarbons (see diagram No 3). According to their description, the government takes a share representingmore than 50% of private companies’ revenues. But, the new revenues aren't only assigned to the central

government and prefecturas; the municipalities and universities receive an important percentage also. Also, the

TGN (National Treasury of the Nation) was created in 2006 to compensate the production departments that do

not receive the FCD. The new system also incorporated a tax benefiting indigenous groups (Fondo Indigena) to

compensate the communities affected by the negative externalities of the industry.

On the other hand, the central government created new programs which were financed with the revenues of the

8/7/2019 The nationalization in the 21th century: The case of the hydrocarbons in Bolivia

http://slidepdf.com/reader/full/the-nationalization-in-the-21th-century-the-case-of-the-hydrocarbons-in-bolivia 21/43

industry as the Juanito Pinto bond which benefited more than 600,000 children at school and the Renta

Dignidad which benefited more than 600,000 elderly citizens.

3.3.3. Allocation of hydrocarbon outputs and social benefits

In the domestic market, the government has developed many socio-economic programs to ensure fair allocation

of the output. For this reason, consumption in the internal market has increased noticeably since nationalization.The most important aspect of this program was Gas Para Todos (2008): This program is focused on two main

groups, the residential (and commercial) and transportation. For the first group, through the National Plan of

Net Gas Supply, the government has increased the installation of natural gas home access in the six cities with

gas infrastructure. The planned project will complete over 100,000 connections per year starting in 2010.

Meanwhile in the transport sector, the government, through the Plan of Vehicle Conversion, seeks to accelerate

the change of the energy matrix from diesel toward the use of natural gas (VNG). The plan aims to change more

than 30,000 vehicles in the short term (2013).

3.3.4. Theoretical considerations

The reasons for the nationalization in Bolivia are quite clear. According to our empirical political framework

there were two important reasons. First, the negative externalities generated by the private companies who not

only generated important inequalities in the poorest groups of society as the CGE model suggests. Secondly, the

weak institutions of the country (lobbies) were another detonator and third, the intention of the government to

win the confidence of the median voter.

According to our regulation framework, it existed a strong principal-agent dilemma before the nationalization,

because the citizens or voter (owners) and government (agent) had important asymmetric information

differences. It was reproduces in the case of the government (owner) trying to regulate the natural gas

enterprises before the nationalization.

Until date, the nationalization experience seems very positive; it suggests some evidences to Fershtman (1990)

who says that when private and public firms work together there are incentives (in the public one) for the

economic efficiency.

8/7/2019 The nationalization in the 21th century: The case of the hydrocarbons in Bolivia

http://slidepdf.com/reader/full/the-nationalization-in-the-21th-century-the-case-of-the-hydrocarbons-in-bolivia 22/43

4. CONCLUSIONS

Despite the strong inequalities and poverty of the country, the natural gas industry is well-organized andcompetitive in the international market. Through the nationalization policy, the government sought that the

progress of the industry was also reflected in an improvement in the quality of life of the people and controlled,

by itself, the negative externalities generated. The new gas revenues have opened new opportunities to Bolivia,

such as a major investment in social programs, an egalitarian income distribution which also involves

municipalities and universities, and the possibility to develop an industrialization of the resource which will

generate new jobs and more revenues. Moreover, the nationalization has motivated the government to include

the environmental matter in the political agenda. The creation of the IBE and the Fondo Indigena are two clear

examples.

On the other hand, we can make two interesting microeconomic conclusions after this work. First, if the

government has show a trend to increase the taxes for the industry progressively, we ask ourselves, for the case

of the companies who renegotiated theirs contracts, which are theirs incentives to continue operating in the

country under that panorama. It can make us to suppose that the natural gas industry is a very profitable

business, so even with a very high taxation the companies can continue paying theirs marginal costs and

receiving important benefits. Secondly, the recent essay of the government to reduce the subsidies (2010)

suggests that Bolivia can't cover these costs even with the recent rise in commodity prices. It makes just three

years and the government sees that it is non-viable.

At this stage, we can distinguish that the Bolivian nationalization, in economic terms, does not follow a

precisely Socialist discourse. Although Morales won the presidency following such a discourse, we see that in

economics, Bolivia follows a likely social democratic discourse. As the reflected in the thesis of Garcia-Linera,

the new Bolivian experience starts from capitalism through a more inclusive economic model (in social terms).

For example, in the case of the nationalization it wasn't a forced expropriation, but an intervention and

renegotiation of the contracts, where the government sought to control the majority of shares of some

companies (e.g., Andina, Chaco and Transredes) and fixed new contracts with others (e.g., Petrobras, Repsol-

YPF and BG) to ensure a more important income from the gas industry. Moreover, the recent experience to

reduce subsidized prices is a clear example of the economic preoccupation of the government.We want to make an important attention call related to our subject, because since Morales assumed the

presidency of the country in 2006, every economic initiative, especially nationalization, has been excessively

politicized by the South American media. Although Morales’ policies have a significant degree of populism, we

have certified that there is also an important economic logic behind them. In general, we feel that the Bolivian

economic policy more closely follows the Brazilian social democratic model of Lula than the Hugo Chavez or

Fidel Castro models. Today we can assure that it is a model of mixed economy, instead of a Socialist planned

8/7/2019 The nationalization in the 21th century: The case of the hydrocarbons in Bolivia

http://slidepdf.com/reader/full/the-nationalization-in-the-21th-century-the-case-of-the-hydrocarbons-in-bolivia 23/43

economy.

Finally, in the year 2009 Morales was reelected president with 64.22% of the vote in the first round.

Nonetheless, there are still important socio-economic matters not completely solved such as eastern autonomy,

which was slightly accepted in the new Constitution approved in 2009, and others which need an immediate

solution, such as the coca cultivation. At this stage the context suggests that the key to integrate the traditional

Amazonian-Andean economy with the urban economy in a single socially inclusive capitalist model, as thevice-president Alvaro Garcia-Linear said, is found in the strengthening of institutions through a clear legal

system where urban poor, miners, informal, coca cultivators, the wealthy, private enterprise, public firms and the

whole society could the limits of their rights in the economic machinery as Hernando de Soto (2000) would say.

5. BIBLIOGRAPHY

8/7/2019 The nationalization in the 21th century: The case of the hydrocarbons in Bolivia

http://slidepdf.com/reader/full/the-nationalization-in-the-21th-century-the-case-of-the-hydrocarbons-in-bolivia 24/43

ACEMOGLU D. & J. ROBINSON, 'A Theory of Political Transitions' (paper). US: MIT & University of

California-Berkeley, 1999.

AMERICAN PETROLEUM INSTITUTE, 'Understanding Natural Gas Markets' (bulletin), American Petroleum

Institute, 2006.

ANDERSEN L. et al., 'Natural Gas and Inequality in Bolivia after Nationalization', Washington-La Paz:

Institute for Advanced Development Studies, 2006.COETZEE C., 'The proposed nationalization of mines in South Africa – A critical assesstment', South Africa:

Provincial Treasury (Province of KwaZulu-Natal), 2010.

GAMARRA E., 'Bolivia on the Brick', New York: COUNCIL ON FOREIGN RELATIONS, 2007.

GARRON-BOZO M., 'El negocio del gas natural y los Impactos esperados en Bolivia', La Paz (Bolivia),

Unidad de Analisis de Politicas Sociales y Economicas (UDAPE), 2007.

GURIEV S. & A. KOTOTILIN, 'Determinants of Nationalization in the Oil Sector: A Theory and Evidence from

Panel Data' (paper), US: New Economic School & MIT, 2009.

GURIEV, S. & W. MEGGINSON, 'Privatization: What have we learned?' (paper), St. Petersberg: ABCDEConference, 2005.

GUTIERREZ C., 'Analysis of Poverty and Inequality in Bolivia, 1999-2005: A Microsimulation Approach, The

Hague: Institute for Advanced Development Studies, 2008.

HALL V., 'Intermediate Microeconomics', US: W. W. Norton & Company; 5th edition (February 1, 1999).

Karl Marx (1818-1883), Course PHIL 329 (University of Waterloo), p. 192-225.

KAUP B., 'A Neoliberal Nationalization?: The Constraints on Natural-Gas-Led Development in Bolivia',

Department of Sociology and the Environmental Science and Policy Program at the College of William &

Mary: Latin American Perspective May 2010, p. 123-138.

MARTINEZ N., 'Bolivia’s Nationalization: Understanding the Process and Gauging the Results', Washington:

Institute for Policy Studies, 2007, p. 1-2.

MEDLOCK K. & P. HARTLEY, 'Exploiting Bolivia’s Natural Gas Resources', Rice University, 2010, p. 1-34.

MINISTERIO DE HIDROCARBUROS & ENERGIA, 'Balance Energetico Nacional 2000-2009', La Paz

(Bolivia): Estado Plurinacional de Bolivia, 2011.

MINISTERIO DE HIDROCARBUROS & ENERGIA, 'Reporte semanal de precios' (Bulletin), La Paz

(Bolivia): Estado Plurinacional de Bolivia, 3-11 March, 2011.

MINISTRIO DE HIDROCARBUROS & ENERGIA, 'De la nacionalizacion a la industrializacion' (Bullettin),

La Paz (Bolivia): Estado Plurinacional de Bolivia.MOREY E., (5 March), 'An Introduction to Market Failures',

http://www.colorado.edu/economics/morey/4545/introductory/marketfailures.pdf.

Policy Research, 2008.

PONTIFICIA UNIVERSIDAD CATOLICA DE CHILE (5 March), 'Abastecimiento de Gas Natural',

http://web.ing.puc.cl/~power/alumno07/gas/P01.htm.

SJOHOLM F., 'Stated Owned Enterprise and Equitazation in Vietnam' (paper), Stockholm:

8/7/2019 The nationalization in the 21th century: The case of the hydrocarbons in Bolivia

http://slidepdf.com/reader/full/the-nationalization-in-the-21th-century-the-case-of-the-hydrocarbons-in-bolivia 25/43

Stockholm School of Economics, 2006.

STEFANONI P., 'Alvaro Garcia-Linera: Pensando Bolivia entre dos siglos', Buenos Aires, 2008.

THE WORLD BANK (5 March), 'Bolivia Data', http://data.worldbank.org/country/bolivia .

Theories of Regulation (5 March), http://poli.haifa.ac.il/~levi/regutheories.htm.

US. INTERNATIONAL INFORMATION ADMINISTRATION, 'International Energy Outlook 2010' (Bulletin),

Chapter 3.VELASQUEZ-DONALSON C., 'Analysis of the Hydrocarbon Sector in Bolivia: How are the Gas and Oil

Revenues Distributed?', Washington: Institute for Advanced Development Studies, 2007.

WEISBROT M. & L. SANDOVAL, 'La distribución de los recursos naturales más importantes de Bolivia y los

conflictos autonómicos', Washington: Center for Economic and

YPFB, '2010 Ano de Inversion y Reactivacion' (bulletin), La Paz (Bolivia): Yacimiento Petroliferos Bolivianos,

2010.

YPFB, 'Boletin Estadistico Yacimientos Petroliferos Fiscales Bolivianos 2010', La Paz (Bolivia): Yacimiento

Petroliferos Bolivianos, 2011.YPFB, 'Memoria Anual 2005', La Paz (Bolivia): Yacimiento Petroliferos Bolivianos, 2005.

YPFB, 'Plan de Inversiones YPFB Corporacion 2009-2015', La Paz (Bolivia): Yacimientos Petroliferos Fiscales

Bolivianos, 2009.

APPENDIX

I. OTHERS

Public regulation versus public control

8/7/2019 The nationalization in the 21th century: The case of the hydrocarbons in Bolivia

http://slidepdf.com/reader/full/the-nationalization-in-the-21th-century-the-case-of-the-hydrocarbons-in-bolivia 26/43

Source: Coskum Aktan (An introduction to theory of privatization)

Matrix of nationalization

PoorHigh Commodity

Prices

Low Commodity Prices

8/7/2019 The nationalization in the 21th century: The case of the hydrocarbons in Bolivia

http://slidepdf.com/reader/full/the-nationalization-in-the-21th-century-the-case-of-the-hydrocarbons-in-bolivia 27/43

Rich (+) Institutions (5.5) (2,2)(-) Institutions (8,2) (3,1)

*Under (8, 2) it would be a revolution (nationalization) and the new income for the two groups will be (0,4).

Guriev econometric results

Source: Own elaboration

Source: Determinants of Nationalization in the Oil Sector: A Theory and Evidence from Panel Data'

II. FIGURES

Figure No 1 : Schematic geology of natural gasresources

Figure No 2 : Non-OECD Asia natural gasproduction, 1990-2005 (Tcf)

8/7/2019 The nationalization in the 21th century: The case of the hydrocarbons in Bolivia

http://slidepdf.com/reader/full/the-nationalization-in-the-21th-century-the-case-of-the-hydrocarbons-in-bolivia 28/43

Source: US. Energy Information Admnistration Source: US. Energy Information Admnistration (2010)

Figure No 3 : Central and South Americanatural gas production 1990-2005 (Tcf)

Source: US. Energy Information Admnistration (2010)

Figure No 4 : World natural gas consumption,2007-2035 (Tcf)

Source: US. Energy Information Admnistration (2010)

Figure No 5 : OECD North America net naturalgas trade, 2007-2035 (Tcf)

Source: US. Energy Information Admnistration (2010)

Figure No 6 : OECD Asia natural gas trade,2007-2035 (Tcf)

Source: US. Energy Information Admnistration (2010)

8/7/2019 The nationalization in the 21th century: The case of the hydrocarbons in Bolivia

http://slidepdf.com/reader/full/the-nationalization-in-the-21th-century-the-case-of-the-hydrocarbons-in-bolivia 29/43

Figure No 7 : Non-OECD Asia net natural gastrade, 2007-2035 (Tcf)

Source: US. Energy Information Admnistration (2010)

Figure No 8 : World energy consumption by fuel type, 1970-2020

Source: US Department of Energy (2001)

Figure No 9 : Importance of energy source bycountry, 2005

Figure No 10 : South American proven naturalgas reserves, January 2007

Source: Oil and Gas Journa

8/7/2019 The nationalization in the 21th century: The case of the hydrocarbons in Bolivia

http://slidepdf.com/reader/full/the-nationalization-in-the-21th-century-the-case-of-the-hydrocarbons-in-bolivia 30/43

Source: Pontifical University Catholic of Chile

Figure No 11 : Bolivia's geology

Source: INE (Bolivia)

Figure No 12: Bolivia natural gas fields andpipelines

Source: YPF

Figure No 13 : Importance of each energy sources in Bolivia (evolution) in kbep

Source: YPFB

8/7/2019 The nationalization in the 21th century: The case of the hydrocarbons in Bolivia

http://slidepdf.com/reader/full/the-nationalization-in-the-21th-century-the-case-of-the-hydrocarbons-in-bolivia 31/43

III. DIAGRAMS

Diagram No 1: Physical flow of natural gas

Source: American Petroleum Institute

Diagram No 2 : YPFB new organization

Source: Ministry of Hydrocarbons

8/7/2019 The nationalization in the 21th century: The case of the hydrocarbons in Bolivia

http://slidepdf.com/reader/full/the-nationalization-in-the-21th-century-the-case-of-the-hydrocarbons-in-bolivia 32/43

Diagram No 3: Hydrocarbon revenues new distribution, 2008

Source: Weisbot and Sandoval (La distribucion de los recursos naturales mas importantes de Bolivia y los conflictosautonomicos)

8/7/2019 The nationalization in the 21th century: The case of the hydrocarbons in Bolivia

http://slidepdf.com/reader/full/the-nationalization-in-the-21th-century-the-case-of-the-hydrocarbons-in-bolivia 33/43

IV. TABLES

Table No 1 : Wolrd natural gas production by region and country of Reference case 2007-2005(Tcf)

Source: US Energy Information Administration (2010)

Table No 2 : World natural gas reserves by country as of January 1, 2010

Source: US Energy Information Administration (2010)

8/7/2019 The nationalization in the 21th century: The case of the hydrocarbons in Bolivia

http://slidepdf.com/reader/full/the-nationalization-in-the-21th-century-the-case-of-the-hydrocarbons-in-bolivia 34/43

Table No 3: Bolivia's social indicators evolutionPoverty headcount ratio at national poverty line (% of population)

2007 37.7%2002 65.2%2000 45.2%1999 62.7%1997 63.2%

Literacy rate, adult total (% of people ages 15 and above)2007 91%2001 87%1992 80%1976 63%

Urban DevelopmentImproved sanitation facilities, urban (% of urban population with access)

2008 34%2005 33%2000 32%

InfrastructureImproved water source, rural (% of rural population with access)

2008 67.8%2005 77.8%2002 77.2%

Source: Worldbank.org

Table No 4 : Natural gas's exploration areas, 2005

Source: YPFB

8/7/2019 The nationalization in the 21th century: The case of the hydrocarbons in Bolivia

http://slidepdf.com/reader/full/the-nationalization-in-the-21th-century-the-case-of-the-hydrocarbons-in-bolivia 35/43

Table No 4 : Natural gas production (MMcf/day), 2005

Source: Andersen et al. (Natural gas an inequality in Bolivia after nationalization)

Table No 5 : External and Internal markets demands (Mcf/day average), 1998-2005

Source: Andersen et al. (Natural gas an inequality in Bolivia after nationalization)

Table No 6 : Gross natural gas production and domestic consumption (kbep), 2000-2009

Source: YPFB

Table No 7 : Distribution of hydrocarbon revenues by departments (M$US), 2004-2007

8/7/2019 The nationalization in the 21th century: The case of the hydrocarbons in Bolivia

http://slidepdf.com/reader/full/the-nationalization-in-the-21th-century-the-case-of-the-hydrocarbons-in-bolivia 36/43

Source: Weisbrot and Sandoval (La distribucion de los recursos naturales mas importantes de Bolivia y los conflictos

autonomicos)

Table No 8 : Brazilian, Argentinean and Internal natural gas prices in 2010

Source: YPFB

V. GRAPHICS

8/7/2019 The nationalization in the 21th century: The case of the hydrocarbons in Bolivia

http://slidepdf.com/reader/full/the-nationalization-in-the-21th-century-the-case-of-the-hydrocarbons-in-bolivia 37/43

Graphic No 1 : Bolivia GDP evolution

Source: Economywatch.com

Graphic No 2 : Natural gas production in Bolivia, 1953-2005

Source: Andersen et al. (Natural gas an inequality in Bolivia after nationalization)

8/7/2019 The nationalization in the 21th century: The case of the hydrocarbons in Bolivia

http://slidepdf.com/reader/full/the-nationalization-in-the-21th-century-the-case-of-the-hydrocarbons-in-bolivia 38/43

Graphic No 3 : Investements in the Bolivianupstream sector (MM/$US), 1990-2005

Source: Andersen et al. (Natural gas an inequality inBolivia after nationalization)

Graphic No 4 : Bolivian natural gas resource,1997-2005

Source: Christian Velasquez-Donalson (Analysis of thehydrocarbon sector in Bolivia)

Graphic No 5 : Evolution of GDP and Hydrocarbons in Bs/. , 1995-2009

Source: Own elaboration

Graphic No 6 : Share of hydrocarbon revenues by beneficiary royalties and participations, 2000

Source: Christian Velasquez-Donalson (Analysis of the hydrocarbon sector in Bolivia)

1988

1989

1990

1991

1992

1993

1994

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

0

5 000 000

10 000 000

15 000 000

20 000 000

25 000 000

30 000 000

35 000 000

GDP (Bs/.)

Hydrocarbons (Bs/.)

8/7/2019 The nationalization in the 21th century: The case of the hydrocarbons in Bolivia

http://slidepdf.com/reader/full/the-nationalization-in-the-21th-century-the-case-of-the-hydrocarbons-in-bolivia 39/43