Embed Size (px)

Citation preview

NSW Housing Outlook

The Outlook for the Housing

Industry in New South Wales

Harley Dale

HIA Chief Economist

HIA Industry Outlook Breakfast – Sydney

March 2011

NSW Housing Outlook

It’s (apparently) all about Europe

NSW Housing Outlook

What’s going on in Europe and what’s is got to do with

us?

• Europe is already back in recession.

• ‘Think’ Australia circa 1990 but with unemployment already at 10% (or in Spain’s case 22%).

• Europe is China’s largest trading partner (25 – 30% of exports).

• China’s net exports are at a more than two year low and manufacturing activity was falling sharply.

• Monetary policy (interest rates) is at its tightest for ten years, but ...

• ... the Chinese retail sector appears okay and fixed internal investment is still growing at over 20%.

• Remember, China takes 50% of the world’s steel.

• There is ample room to move to stimulate domestic demand and ...

• ... there is a change in leadership later this year.

• The most likely outcome is that Europe ‘muddles through’ and China is okay.

NSW Housing Outlook

The Australian Economy – too much focus on the

aggregate

• Economic growth is okay, but patchy and …

• … as HIA predicted from late 2010, nowhere near what was originally forecast.

-2.0

-1.0

0.0

1.0

2.0

3.0

4.0

5.0

6.0

Dec

-90

Dec

-91

Dec

-92

Dec

-93

Dec

-94

Dec

-95

Dec

-96

Dec

-97

Dec

-98

Dec

-99

Dec

-00

Dec

-01

Dec

-02

Dec

-03

Dec

-04

Dec

-05

Dec

-06

Dec

-07

Dec

-08

Dec

-09

Dec

-10

Dec

-11

% c

hang

e

Gross Domestic ProductSource: ABS 5206

Qtrly Annual

NSW Housing Outlook

HIA National Outlook, December 2010

• “(Official) economic growth rate forecasts for Australia in

2011 are too high ...”

• In terms of the resources boom mark II:-

• “… there may be little else to drive economic activity and we

will need a quick reversal in monetary policy settings and

potentially a revamping of some fiscal stimulus elements.”

NSW Housing Outlook

Interest rate relief appears to have been short-lived

NSW Housing Outlook

Interest rates are not going according to plan

• Interest rates fell in late 2011, but the banks dithered and businesses lost out.

• Banks lifting interest rates in 2012 changes the entire landscape.

2.00

3.00

4.00

5.00

6.00

7.00

8.00

9.00

10.00

11.00

Mar

-09

Apr

-09

May

-09

Jun-

09

Jul-0

9

Aug

-09

Sep

-09

Oct

-09

Nov

-09

Dec

-09

Jan-

10

Feb-

10

Mar

-10

Apr

-10

May

-10

Jun-

10

Jul-1

0

Aug

-10

Sep

-10

Oct

-10

Nov

-10

Dec

-10

Jan-

11

Feb-

11

Mar

-11

Apr

-11

May

-11

Jun-

11

Jul-1

1

Aug

-11

Sep

-11

Oct

-11

Nov

-11

Dec

-11

Jan-

12

*Feb

-12

Mar

-12

% In

tere

st R

ate

Interest Rates, Australia

Discounted Variable Mortgage Rate RBA Cash Rate Small Business Variable Term Loan

Source: RBA

NSW Housing Outlook

Consumers are feeling slightly better but still nervous

75

80

85

90

95

100

105

110

115

120

125

Feb-94 Feb-96 Feb-98 Feb-00 Feb-02 Feb-04 Feb-06 Feb-08 Feb-10 Feb-12

Inde

x

Consumer ConfidenceSource: Westpac-Melbourne Institute

NSW Housing Outlook

The NSW economy – a mixed bag like everywhere else

NSW ECONOMY

INDICATOR UPDATE

Gross State Product Steady

Interest rate outlook Steady/deteriorated

Manufacturing Steady

Unemployment Steady

Detached houses Deteriorated

Multi-units Improved

Renovations Deteriorated

NSW Housing Outlook

Housing indicators – up and down

8.6%

5.8%

-0.1%

-4% -4% -3.4%

-11.8%

0.9% 0.9%

-3.0%

-5.0%

-15.0%

-10.0%

-5.0%

0.0%

5.0%

10.0%

Land sales(Sydney)

Land prices(Sydney)

New homelending

Approvals -detached

Approvals -'total'

New homesales

Alts & adds Detachedhouse prices

(Sydney)

Multi-unitprices

(Sydney)

Detachedhouse prices

(regionalNSW)

Multi-unitprices

(regionalNSW)

% c

hang

e

Housing Indicators - Latest update for NSW Source: ABS, rpdata.com, HIA Economics

NSW Housing Outlook

The employment market is ‘okay’

-4.0

-3.0

-2.0

-1.0

0.0

1.0

2.0

3.0

4.0

5.0

6.0

3.0

4.0

5.0

6.0

7.0

8.0

9.0

10.0

11.0

12.0

Jan-

92

Jan-

93

Jan-

94

Jan-

95

Jan-

96

Jan-

97

Jan-

98

Jan-

99

Jan-

00

Jan-

01

Jan-

02

Jan-

03

Jan-

04

Jan-

05

Jan-

06

Jan-

07

Jan-

08

Jan-

09

Jan-

10

Jan-

11

Jan-

12

Per

cen

t

Per

cen

t

New South Wales' Labour MarketSource: ABS Labour Force

U/e rate (LHS) Annual Employment Growth Rate (RHS)

NSW Housing Outlook

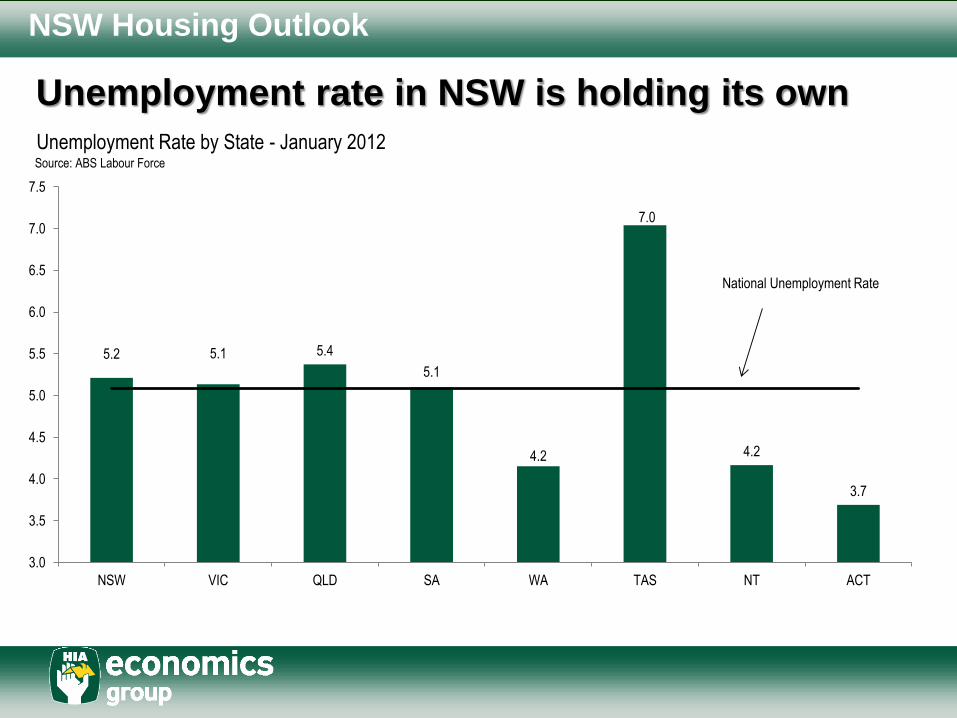

Unemployment rate in NSW is holding its own

5.2 5.1 5.4

5.1

4.2

7.0

4.2

3.7

3.0

3.5

4.0

4.5

5.0

5.5

6.0

6.5

7.0

7.5

NSW VIC QLD SA WA TAS NT ACT

Unemployment Rate by State - January 2012Source: ABS Labour Force

National Unemployment Rate

NSW Housing Outlook

Housing is the key to a

healthy NSW economy

NSW Housing Outlook

New Home Building

NSW Housing Outlook

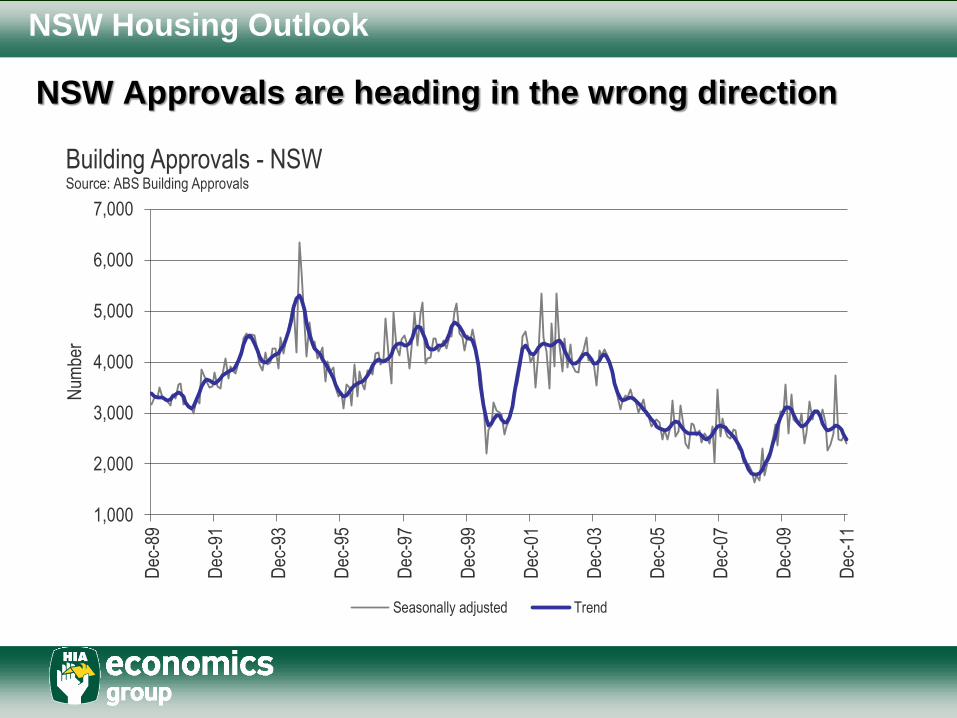

NSW Approvals are heading in the wrong direction

1,000

2,000

3,000

4,000

5,000

6,000

7,000

Dec

-89

Dec

-91

Dec

-93

Dec

-95

Dec

-97

Dec

-99

Dec

-01

Dec

-03

Dec

-05

Dec

-07

Dec

-09

Dec

-11

Num

ber

Building Approvals - NSWSource: ABS Building Approvals

Seasonally adjusted Trend

NSW Housing Outlook

Housing Affordability is improving and …

30.0

35.0

40.0

45.0

50.0

55.0

60.0

65.0

70.0

75.0

D06 M07 J07 S07 D07 M08 J08 S08 D08 M09 J09 S09 D09 M10 J10 S10 D10 M11 J11 S11 D11

HOUSING AFFORDABILITY INDEX, NSW

SYDNEY REST OF NSW

Sou

rce:

HIA

-Com

mon

wea

lthB

ank

Affo

rdab

ility

Rep

ort

HOUSING AFFORDABILITY INDEX, NSW

NSW Housing Outlook

… first home buyers are re-emerging and …

5.0%

10.0%

15.0%

20.0%

25.0%

30.0%

35.0%

40.0%

1000

2000

3000

4000

5000

6000

7000

Dec

-04

Mar

-05

Jun-

05

Sep

-05

Dec

-05

Mar

-06

Jun-

06

Sep

-06

Dec

-06

Mar

-07

Jun-

07

Sep

-07

Dec

-07

Mar

-08

Jun-

08

Sep

-08

Dec

-08

Mar

-09

Jun-

09

Sep

-09

Dec

-09

Mar

-10

Jun-

10

Sep

-10

Dec

-10

Mar

-11

Jun-

11

Sep

-11

Dec

-11

NSW First Home BuyersSource ABS Housing Finance

First home buyers - Dwellings financed (no.) Proportion

NSW Housing Outlook

... the trade-up buyer market has improved

6,846

33,060

11,194

35,337

0

5,000

10,000

15,000

20,000

25,000

30,000

35,000

40,000

FHB Non-FHB

Num

ber

of lo

ans

NSW First Home Buyer versus Non-First Home Buyer Loans - NSWSource: ABS Housing Finance

3mths to Dec 10 3mths to Dec 11

% change +64%

% change: +7%

NSW Housing Outlook

How are the regions faring?

Population growth 2009-10 Residential lot sales* NSW Building approvals** Ranking

Sydney 1.7 -9 -9 2

South Eastern 1.5 -25 13 1

Mid-North Coast 1.3 -36 -10 7

Illawarra 1.3 -32 -4 4

Hunter 1.2 -11 8 3

Central West 1.1 5 -12 5=

Richmond-Tweed 1.0 -51 -57 11

Northern 1.0 -42 3 9

Murrumbidgee 0.8 -41 -7 10

North Western 0.8 50 -38 8

Murray 0.7 -15 22 5=

*Annual % change - 6 mnths to Sep 2011

**Annual % change - December qtr 2011

NSW Housing Outlook

Housing prices, new housing,

and renovations activity

NSW Housing Outlook

Guess what? No housing crash

-0.9%

-6.8% -6.8%

-5.3%

-4.3%

-2.2%-2.5%

-4.3%

0.9%

-3.6%

-6.5%

-1.1%

-4.2%

-2.6%

-1.4% -1.5%

-10.0%

-8.0%

-6.0%

-4.0%

-2.0%

0.0%

2.0%

Sydney Melbourne Brisbane Adelaide Perth Darwin Canberra AustralianCapitals

Change in home values - year on year, December 2011Source: RP Data, Rismark International

Houses Units

NSW Housing Outlook

Dwelling prices – NSW regional centres

-2.2%

-4.7%

2.0%

15.7%

-5.5%

1.2%

-8.4%-10.2%

5.7%

-2.9%

20.8%

5.9%

2.1%

4.3%

-15.0%

-10.0%

-5.0%

0.0%

5.0%

10.0%

15.0%

20.0%

25.0%

Albury Armidale Bathurst Broken Hill Coffs Harbour Dubbo Lismore Maitland Orange Queanbeyan Tamworth Wagga Wagga Wollongong Sydney

Change in dwelling values - Annual change, 12 months to December 2011Source: Australian Property Investor, RP Data-Rismark

12 month % change

NSW Housing Outlook

Renovations activity has ‘re-disappointed’ and …

5,000

6,000

7,000

8,000

9,000

10,000

11,000

Dec

.198

9

Dec

.199

1

Dec

.199

3

Dec

.199

5

Dec

.199

7

Dec

.199

9

Dec

.200

1

Dec

.200

3

Dec

.200

5

Dec

.200

7

Dec

.200

9

Dec

.201

1

$ m

illio

n (m

ovin

g an

nual

tota

l)

Renovations Investment in New South Wales - Moving Annual TotalSource: ABS State Final Demand

NSW Housing Outlook

… major alts and adds haven’t done much

0

50,000

100,000

150,000

200,000

250,000

Dec

-04

Mar

-05

Jun-

05

Sep

-05

Dec

-05

Mar

-06

Jun-

06

Sep

-06

Dec

-06

Mar

-07

Jun-

07

Sep

-07

Dec

-07

Mar

-08

Jun-

08

Sep

-08

Dec

-08

Mar

-09

Jun-

09

Sep

-09

Dec

-09

Mar

-10

Jun-

10

Sep

-10

Dec

-10

Mar

-11

Jun-

11

Sep

-11

Dec

-11

The NSW Renovations and Additions MarketMonthly Lending and Monthly Council Approvals ($000)

Lending for Alts and Adds Value of Council Approved Alts and Adds

NSW Housing Outlook

NSW VIC QLD SA WA TAS NT ACT Aust

2003/04 (a) 9,741 6,424 6,358 1,934 3,078 684 204 376 28,799

2004/05 (a) 9,592 6,191 6,702 1,958 3,249 666 294 335 28,987

2005/06 (a) 8,962 5,842 7,159 1,956 3,255 695 322 354 28,545

2006/07 (a) 8,284 6,095 7,845 2,130 3,515 711 261 328 29,169

2007/08 (a) 8,262 6,639 7,565 1,829 4,244 769 202 367 29,877

2008/09 (a) 7,957 6,583 7,152 2,011 3,945 790 209 301 28,948

2009/10 (a) 8,263 6,338 7,363 2,026 4,536 751 254 392 29,923

2010/11 (a) 8,265 6,381 6,836 1,914 4,727 738 254 435 29,550

2011/12 8,004 6,495 7,349 1,956 4,557 799 243 431 29,835

2012/13 8,238 6,423 7,333 1,979 4,655 781 252 423 30,084

% change

2004/05 (a) -2% -4% 5% 1% 6% -3% 44% -11% 1%

2005/06 (a) -7% -6% 7% 0% 0% 4% 10% 6% -2%

2006/07 (a) -8% 4% 10% 9% 8% 2% -19% -7% 2%

2007/08 (a) 0% 9% -4% -14% 21% 8% -23% 12% 2%

2008/09 (a) -4% -1% -5% 10% -7% 3% 3% -18% -3%

2009/10 (a) 4% -4% 3% 1% 15% -5% 22% 30% 3%

2010/11 0% 1% -7% -6% 4% -2% 0% 11% -1%

2011/12 -3% 2% 8% 2% -4% 8% -4% -1% 1%

2012/13 3% -1% 0% 1% 2% -2% 4% -2% 1%

(a) = actual

HOUSING RENOVATIONS FORECAST: by state and territoryValue of investment, $ million, Chain Volume Measure

Source HIA Economics December 2011

The outlook for renovations is reasonable

NSW Housing Outlook

The outlook and what needs

to be done

NSW Housing Outlook

A recovery in new housing starts in 2012/13?

45.70

39.40

32.88

29.7431.49

23.62

31.87 30.8929.51

33.84

0.00

5.00

10.00

15.00

20.00

25.00

30.00

35.00

40.00

45.00

50.00

2003/04 (a) 2004/05 (a) 2005/06 (a) 2006/07 (a) 2007/08 (a) 2008/09 (a) 2009/10 (a) 2010/11 (a) 2011/12 2012/13

Tho

usan

d dw

ellin

gs c

omm

ence

d

NSW Housing Starts ForecastsSource: HIA Economics Group

Forecast

NSW Housing Outlook

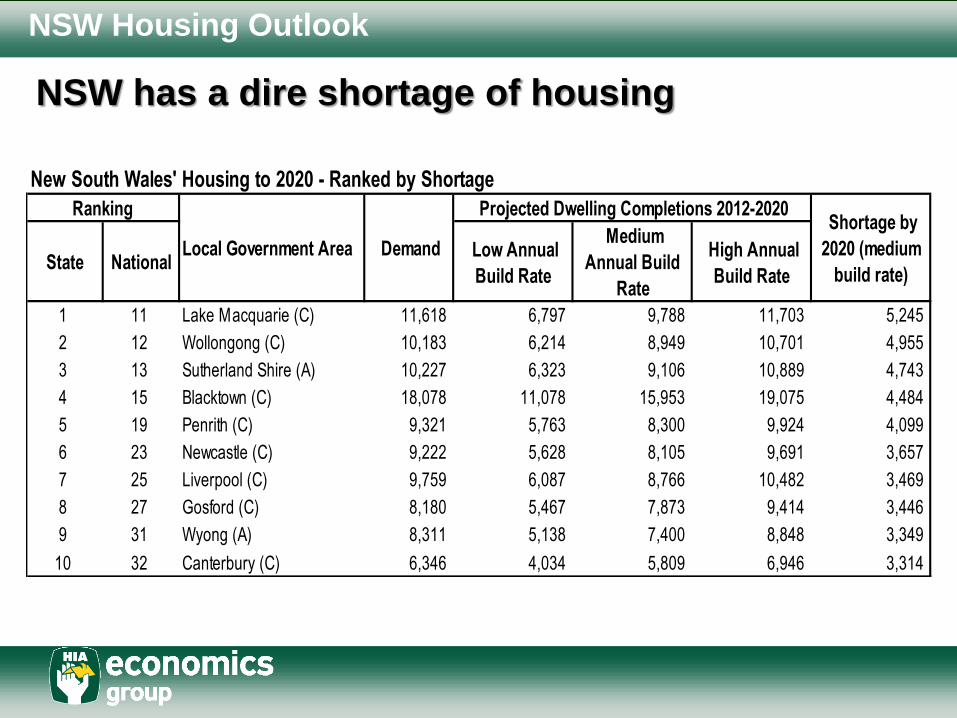

NSW has a dire shortage of housing

State National Low Annual

Build Rate

Medium

Annual Build

Rate

High Annual

Build Rate

1 11 Lake Macquarie (C) 11,618 6,797 9,788 11,703 5,245

2 12 Wollongong (C) 10,183 6,214 8,949 10,701 4,955

3 13 Sutherland Shire (A) 10,227 6,323 9,106 10,889 4,743

4 15 Blacktown (C) 18,078 11,078 15,953 19,075 4,484

5 19 Penrith (C) 9,321 5,763 8,300 9,924 4,099

6 23 Newcastle (C) 9,222 5,628 8,105 9,691 3,657

7 25 Liverpool (C) 9,759 6,087 8,766 10,482 3,469

8 27 Gosford (C) 8,180 5,467 7,873 9,414 3,446

9 31 Wyong (A) 8,311 5,138 7,400 8,848 3,349

10 32 Canterbury (C) 6,346 4,034 5,809 6,946 3,314

New South Wales' Housing to 2020 - Ranked by Shortage

Ranking

Local Government Area Demand

Projected Dwelling Completions 2012-2020 Shortage by

2020 (medium

build rate)

NSW Housing Outlook

So, what can be done?

• In December 2010 HIA Economics was the first group in Australia to point out that interest rates might need to fall in 2011 and that everybody was too bullish on the economy.

• In February 2011 this message was conveyed in person to the PM’s office and the need for assistance to residential building was conveyed.

• In March 2011 the same message was delivered to the Federal Treasurer’s office and a set of polices was provided to Commonwealth Treasury.

• HIA continued to communicate, in person and at arms-length, with the Treasurer and with Commonwealth Treasury.

• HIA also held two meetings with the Australian Bankers Association with regard to the lack of available finance for residential development.

NSW Housing Outlook

There needs to be a focus on taxation reform

• An independent report provides compelling evidence that:-

– New housing is one of the most heavily taxed sectors of the Australian economy.

– Among Australia’s 27 largest industrial sectors (> $10billion), the residential building sector is the second most heavily taxed sector.

– Including direct, indirect, and hidden taxes the tax on new housing is estimated at 44 per cent of a new house in Sydney, 38 per cent in Melbourne, and 36 per cent in Brisbane.

– Model simulations show that most of the burden of taxation falls on home buyers.

– Many of the taxes on housing are economically inefficient, ranging in value from $45,300 on a new apartment in Melbourne to $141,500 on a new house in Sydney.

NSW Housing Outlook

Total taxes on new houses and apartments

New homes New apartments

Sydney M elbourne Brisbane Sydney M elbourne Brisbane

Direct 75 422 63 312 55 170 73 694 55 607 52 238

Hidden/ambiguous 106 276 45 398 56 346 51 331 28 545 46 718

Indirect 86 180 75 071 79 265 84 598 73 058 72 504

Total 267 879 183 781 190 781 209 623 157 210 171 460

Data source: TheCIE 2011.

NSW Housing Outlook

Some wider findings

• The total taxes collected by governments for a new house is 44 per cent ($268,000) of the purchase price of a new home in Sydney.

• While Sydney houses yielded the highest figure, the other figures were also high.

• However, the tax burden of housing was found to be considerably higher in Sydney:-

– For houses the tax burden is 46 per cent higher in Sydney than in Melbourne; 40 per cent higher than in Brisbane.

– For apartments the tax burden is 33 per cent higher in Sydney than in Melbourne; 22 per cent higher than in Brisbane.

NSW Housing Outlook

Thank you for your time this

morning

Harley Dale

Chief Economist

HOUSING INDUSTRY ASSOCIATION

http://economics.hia.com.au