Embed Size (px)

Citation preview

1 People’s Republic of China – Business and Taxation Guide

Business and Taxation

Guide to

The People’s Republic of China

2 People’s Republic of China – Business and Taxation Guide

Preface This guide was prepared by Mazars Tax Service Limited of Mazars China in 2011. 42nd Floor, Central Plaza, 18 Harbour Road, Wanchai, Hong Kong Tel.: (+ 852) 2909 5555 Fax: (+852) 2581 1289 [email protected] www.mazars.cn Alexander Mak Managing Director Email: [email protected] Michael To Executive Director Email: [email protected] Dave Wong Senior Manager Email: [email protected] Other offices in China Beijing 1608, Tower E1 Oriental Plaza No.1 East Chang An Ave. 100738 Beijing Tel.: (+86 10) 8518 9780 Thierry Labarre Founding Senior Partner Email: [email protected] Joey Zhou Manager Email: [email protected]

Guangzhou 1308, Grand Tower No. 228 Tianhe Road Tianhe District 510620 Guangzhou Tel.: (+86 20) 3833 0235 Benoit Stos Managing Director Email: [email protected]

Shanghai 8th Floor, One Lujiazui No. 68 Yin Cheng Middle Road 200120 Shanghai Tel.: (+86 21) 6168 1088 Julie Laulusa Managing Partner Email: [email protected] Jean-Francois Salzmann Managing Partner Email: [email protected] Peter Law Senior Manager Email: [email protected] Flame Zheng Senior Manager Email: [email protected]

3 People’s Republic of China – Business and Taxation Guide

Mazars is an international, integrated and independent organisation specialising in audit, accountancy, tax, legal and advisory services. Mazars has 13,000 professionals in the 61 countries, making up a truly integrated partnership across all five continents. The firm also has correspondents and joint ventures in 21 additional countries. Mazars is one of the founding members of the Praxity Alliance. China has a dynamic legal and economic environment. Policies change from time to time. This booklet is intended as a general guide and professional advice is essential before any business is undertaken. The Special Administrative Regions of Hong Kong and Macau each has different laws and regulations in relation to business dealings and taxation. © Praxity 2011 This guide is intended as a general guide only and should not be acted upon without further advice.

4 People’s Republic of China – Business and Taxation Guide

Contents Page 1. General information 6 1.1 Opportunities and possible obstacles for foreign investors 1.2 Area and population 1.3 Government and law 1.4 Key economic indicators 1.5 Financial status 1.6 Currency 1.7 Immigration laws 2. Regulation of foreign investment 8 3. Government incentives 9 4. Business organisations available to foreigners 10 4.1 Wholly foreign-owned enterprise (WFOE) 4.2 Equity joint venture (EJV) 4.3 Co-operative joint venture (CJV) 4.4 Representative office (RO) 5. Setting up and running business organisations 11 5.1 Process for establishing a FIE 5.2 Registered capital for a FIE 5.3 Company management 5.4 Profits distribution 5.5 Accounting and audit requirements 5.6 Labour contract law 6. Corporate taxes and social charges 13 6.1 Corporate income tax 6.2 Income tax rates 6.3 Deductions 6.4 Transfer pricing 6.5 Social security contributions 7. Personal taxation 15 7.1 Income tax 7.2 Foreign tax credit 7.3 Assessment and filing 8. Double taxation agreements 17 9. Sales and use tax and other significant taxes and duties 18 9.1 Value Added Tax 9.2 Business Tax 9.3 Consumption Tax 9.4 Land Appreciation Tax 9.5 Resources Tax 9.6 Customs Duty 9.7 Stamp Duty 9.8 Real Estate Tax 9.9 Deed Tax 10. Portfolio investment for foreigners 22 10.1 Investment in PRC stocks

5 People’s Republic of China – Business and Taxation Guide

10.2 Investment in PRC real estate 11. Trusts 23 12. Practical information 24 12.1 Transport 12.2 Language 12.3 Time relative to Greenwich Mean Times (GMT) 12.4 Public holidays

6 People’s Republic of China – Business and Taxation Guide

1. General information 1.1 Opportunities and possible obstacles for foreign investors Foreign investment has been actively encouraged in the People’s Republic of China (PRC) since the early 1980s. In particular, Special Economic Zones with greater autonomy have been established to facilitate economic development. Some of the key attractions for foreign investors include: Since 2010 the PRC has been the second largest world economy after the United States PRC has experienced growth rates of around 10% per annum over the past 10 years Because of the size of its population, the PRC has direct access to a huge consumer market The PRC government encourages high technology or environmental friendly industries and

offers preferential treatments to the investors, upon fulfilment of certain stipulated requirements.

1.2 Area and population

The PRC is located in central and eastern Asia, with a total area of about 9.6 million square kilometres (3.7 million square miles) and is the world’s third largest country by land area. With 1.3 billion citizens, it is the most populous country in the world, representing about 22% of the world population. In terms of population density, there are major regional variations. The western and northern parts have a few million people, while ‘Inner China’ has about 1.2 billion. The PRC borders the Mongolian People’s Republic in the North; the Commonwealth of Independent States and North Korea in the North-East; the Yellow Sea and the East China Sea in the East; the South China Sea, Vietnam, Laos, Burma, India, Bhutan, Sikkim, Nepal and Pakistan in the South; and the Commonwealth of Independent States and Afghanistan in the West. Broadly speaking, the population is concentrated in Inner China, east of the mountains and south of the Great Wall, meaning the 11 eastern and coastal provinces are much more densely populated than the western interior. The most densely populated areas included the Yangtze River Valley, Sichuan Basin, North China Plain, Pearl River Delta, and the industrial area around the city of Shenyang in the northeast.

Major cities in the PRC include: Beijing Shanghai Chongqing Shenzhen Guangzhou.

The PRC has a diverse climate, with varied conditions. In the north it is bitterly cold in the winter, hot and humid in the summer. The climate in the south is sub-tropical.

7 People’s Republic of China – Business and Taxation Guide

1.3 Government and law

The People's Republic of China is a single-party state governed by the Party of China (CPC). The PRC exercises jurisdiction over 23 provinces, five autonomous regions, four directly controlled municipalities -Beijing, Tianjin, Shanghai, and Chongqing - and two special administrative regions (SARs), Hong Kong and Macau. Its capital city is Beijing.

The National People's Congress (NPC) is the highest state body and the only legislative house in the PRC. The NPC and its Standing Committee exercise the legislative power of the state.

1.4 Key economic indicators

In recent years, the PRC government has been taking measures that aim to achieve steady and moderate economic growth.

In 2010, GDP grew by 10.3% to around US$ 6,010 billion. 1.5 Financial status The People’s Bank of China (PBOC) is China’s central bank, which is responsible for establishing and implementing China’s national financial policies, and monitoring currency circulation as well as credit activities. PBOC also supervises China’s banking system which is composed of both state-owned and non-state owned domestic banks, plus branches of foreign banks in China. Banks are the main source of financing for most of the enterprises in China, although the PRC government has been tightening and closely monitors bank financing in recent years in view of the inflation pressure. 1.6 Currency The unit of currency in China is the Renminbi (abbreviated as RMB). The Renminbi is the legal tender in mainland China, but not in Hong Kong and Macau. The units for the Renminbi are the Yuan, Jiao and Fen (although the Fen has virtually disappeared from circulation. 1 Yuan equals 10 Jiao, which equals 100 Fen. 1.7 Immigration laws

In order for foreigners to live and work legitimately in the PRC, employment permits and residence permits are required.

The most common types of visa classifications that may interest non-resident investors are:

F Visa – issued to temporary business visitors

L Visa – issued to tourists

Z Visa – issued to foreigners coming to work in China, and their spouses

8 People’s Republic of China – Business and Taxation Guide

2. Regulation of foreign investment The PRC imposes controls on currency exchange. The State Administration of Foreign Exchange (SAFE), and its branches, is the main body responsible for supervising and monitoring foreign exchange transactions.

According to the PRC Foreign Exchange Control Regulations, foreign exchange transactions are categorised into:

Current account items, covering foreign exchange transactions that entail goods, services, remunerations, dividends, interest, gifts and compensations

Capital account items, covering foreign exchange transactions that entail direct investment, investment in securities, lending and transfer of fixed assets and intangible properties.

A Foreign Invested Enterprise (FIE) is required to register with the SAFE. It may open separate forex bank accounts with designated banks for current and capital account items.

For current account items, a FIE may receive and sell and purchase and remit foreign currency through its forex bank account. To substantiate transactions, a FIE is generally required to provide information and supporting documentation to the bank or SAFE.

For foreign exchange transactions of capital account items, a FIE is generally required to obtain prior approval from the SAFE, subject to certain exceptions.

From a foreign exchange control perspective, foreign investors should be aware that:

A FIE must have its export proceeds remitted back into the PRC

A FIE must register its foreign exchange borrowing with the SAFE

A FIE, with prior approval from the SAFE, may open a foreign exchange account with a bank outside the PRC

An expatriate is allowed to remit his or her PRC-sourced salaries and other legitimate income out of the PRC after tax clearance.

The PRC government has issued the Catalogue of Guidelines of Foreign Invested Industries (latest version: 2011) which classifies industries into categories of ‘Encouraged’, ‘Restricted’ and ‘Prohibited’.

In particular, foreign investment is not allowed in industries classified as ‘Prohibited’, for example the manufacturing of armaments. If an industry is not listed in the Catalogue of Guidelines, it is regarded as a ‘Permitted’ industry for foreign investment, with less or no preferential treatments, compared with those classified as ‘Encouraged’ industries. If an industry is classified as ‘Restricted’, then the form of investment is limited to a Sino-Foreign joint venture, whereby the Chinese party may be the majority shareholder for certain ‘Restricted’ industries.

9 People’s Republic of China – Business and Taxation Guide

3. Government incentives Corporate income tax incentives

Under the existing corporate income tax regime, tax incentives are mainly technology and industry oriented. For corporate tax incentives available under the previous Foreign Enterprise Income Tax regime, there are grandfathering rules supporting the transition up until 2012.

Local governments may offer certain financial subsidies to a foreign investment, depending on the corresponding location of the investment and/or the industry it is engaged in.

10 People’s Republic of China – Business and Taxation Guide

4. Business organisations available to foreigners

Common forms of business vehicles for inbound investments into the PRC include:

4.1 Wholly foreign-owned enterprise (WFOE)

A WFOE is a limited liability company, wholly owned by foreign investor(s). 4.2 Equity joint venture (EJV) An EJV is a limited liability company formed by one or more foreign parties, as well as Chinese party/parties. Foreign investors must together contribute at least 25% of the registered capital of the EJV. Representative of either the foreign investor or the Chinese investor can be appointed as the chairman of the Board of Directors. Profits are shared among the investors, according to their respective capital contributions.

4.3 Co-operative joint venture (CJV)

A CJV can be formed as a separate legal entity or on a contractual basis without being formed as a separate legal entity. Profits are shared among the investors in accordance with the terms prescribed in the CJV agreement, opposed to their respective capital contributions. Where the CJV is a separate legal entity, the foreign investors must collectively contribute at least 25% of the registered capital.

WFOEs, EJVs and CJVs are collectively referred to as a foreign investment enterprise (FIE).

4.4 Representative Office (RO)

A foreign company may establish a RO in the PRC to carry out market research, product display, promotion and business liaison activities in the PRC on behalf of its overseas head office. ROs are not allowed to engage in any business activities within the PRC. This can include, for example, the signing business contracts, the sale of goods, and the provision of services, collecting money and issuing invoices.

11 People’s Republic of China – Business and Taxation Guide

5. Setting up and running business organisations

5.1 Process for establishing a FIE

To set up a FIE, investors are required to submit an application to the Ministry of Commerce (MOC). The main supporting documentation required includes:

• Articles of association

• Feasibility study report and

• Joint venture (JV) agreement (for an EJV or CJV).

The articles of association establish the company's by-laws and stipulate the roles and responsibilities of the Board of Directors. The JV agreement covers the name and address of the proposed JV, the investing parties and each investor’s capital contribution, plus the nature of the JV’s business.

The MOC must reach a decision on the setting-up application within 90 days. Upon approval by the MOC, the investors must then apply for their FIE business license within 30 days. This is done through the State Administration of Industry and Commerce (SAIC).

Once the business license is issued, the FIE is officially established. The FIE should then register with the various government authorities (for example tax bureaus and customs) within 30 days from the date the business license was issued.

5.2 Registered capital for a FIE

The MOC will determine the minimum amount of capital that must be contributed into the FIE, depending on the proposed nature and scale of the FIE’s business. Foreign investors must collectively contribute at least 25% of the registered capital.

Contributions can be in:

Cash (in foreign currency or Renminbi), which needs to be at least 30% of the contribution

Fixed assets

Land use rights

Intellectual properties - these cannot exceed 20% of the registered capital.

5.3 Company management A FIE is managed by its Board of Directors and management office. The number of investor representatives on the board is generally proportional to its capital contribution. The board is responsible for major decisions undertaken by the company, plus strategic plans. The management office, which is run by a general manager appointed by the board, is responsible for the day-to-day operations of the FIE.

12 People’s Republic of China – Business and Taxation Guide

The chairman of the board and the general manager can be foreigners or PRC nationals.

5.4 Profits distribution

Dividends can be paid to foreign investors out of the FIE’s (after-tax) retained earning. Dividends distributed to foreign investors are subject to PRC withholding tax. 5.5 Accounting and audit requirements A FIE is required to maintain its own accounting records and prepare financial statements. It is also required to submit quarterly and annual financial statements to its local tax authority. The annual financial statements must be audited and certified by a Chinese Certified Public Accountant.

5.6 Labour contract law

Under the PRC’s Labour Contract Law:

An employer should enter into written employment contracts with all of its employees

The employment contracts should state the duration of employment, job description, compensation arrangement and working conditions - such as the maximum working hours (40 hours per week, excluding overtime), annual leave and maternity leave entitlements

Severance payment is set at one month’s salary for each year of employment, up to a maximum of 12 years.

13 People’s Republic of China – Business and Taxation Guide

6. Corporate taxes and social charges 6.1 Corporate income tax (CIT)

The current corporate income tax system was introduced and has been effective from 1 January 2008. The CIT law governs the income tax levied on domestic enterprises, FIE’s and foreign enterprises.

Resident enterprise An enterprise that is established under PRC laws, or an enterprise that is established under the laws of a foreign country/region but with its ’place of effective management’ maintained within mainland China, is considered a PRC tax resident enterprise and is subject to CIT on its worldwide income. The ‘place of effective management’ for an enterprise, refers to the place where the overall management and control of the production, operation, personnel, finance and properties of the enterprise are exercised. Non-resident enterprise An enterprise established under the laws of a foreign country/region that maintains its ‘place of effective management’ outside of mainland China is considered to be a non-PRC resident enterprise. As such, it is subject to CIT on its PRC-sourced income, plus non-PRC-sourced income that is effectively connected with its establishment (if any) in the PRC. 6.2 Income tax rates

The statutory CIT rate in the PRC is 25%. Certain types of enterprises may enjoy reduced CIT rates (see below).

Passive income (including dividends, interest, rental, royalties and capital gains) derived by non-resident enterprises is subject to PRC withholding tax at 10%, subject to reduction or exemption by applicable tax treaties. For example, under the tax arrangement between mainland China and Hong Kong, Hong Kong tax resident companies may enjoy a reduced PRC withholding tax rate, upon fulfilment of certain conditions, such as:

Dividends at 5% Interest and royalties at 7%.

6.3 Deductions According to the CIT law and Implementation Rules, deductions of certain expenses are capped. These expenses include staff welfare, labour union fund contributions, staff education, entertainment, advertising and promotion, charitable donations and depreciation. 6.4 Transfer Pricing (TP) In general, the TP concepts in the PRC follow the principles of the Organisation for Economic Co-operation and Development (OECD) Transfer Pricing Guidelines, with some variations. The CIT Law and regulations do not prescribe any preferred TP methods. Taxpayers may use any of the acknowledged methods to determine their transfer prices, providing the methods are defensible and commercially justifiable.

14 People’s Republic of China – Business and Taxation Guide

Corporate taxpayers in the PRC are required to file the following nine forms in relation to their related-party transactions, together with their annual CIT returns by 31 May of the following year:

Related parties

Related-party transactions

Sales and purchases

Services

Transfer of intangible assets

Transfer of fixed assets

Financing

Outbound investments

Outbound payments.

Corporate taxpayers are also required to prepare contemporaneous documentation with detailed content requirements, unless they have been specifically exempt. The five main categories include:

Organisational structure

Overview of business operations

Information on related-party transactions

Comparability analysis

Transfer pricing method selection and application.

The deadline for completing contemporaneous documentation is 31 May of the following year. The documentation must be retained for ten years, ready for submission to the tax authorities upon request. 6.5 Social security contributions Both the employer and employees make mandatory social security contributions, which cover the employees’ housing, pension and medical insurance. Each employer is also required to make social security contributions for the employees’ work injury and maternity insurance. The contribution rates vary across different locations in China.

Effective as of 15 October 2011, social security contributions in China are now applicable to foreigners who are based and work in China.

15 People’s Republic of China – Business and Taxation Guide

7. Personal taxation 7.1 Income tax

Individual Income Tax (IIT) is charged on income earned by individuals. PRC resident individuals are subject to IIT on their worldwide income.

For non-residents, the IIT treatment depends on the length of their stay in the PRC and the source of their income. An individual may be entitled to IIT exemptions under tax treaties between the PRC and their home country. Non-residents, who have stayed in China for more than 90 days in a year (or the specified

threshold periods in the tax treaties) and less than one year, are subject to IIT on their PRC-sourced income only.

Non-residents who have stayed in the PRC for one to five years are, in principle, subject to IIT on their PRC-sourced income and foreign-sourced income paid/borne by PRC entities/ establishments.

Non-residents who have stayed in the PRC for more than five consecutive years are subject to IIT on their worldwide income starting from the sixth year of their stay and thereafter.

Under the IIT Law, there are 11 types of taxable income, such as employment income, labour income, interest, dividend, rental, royalty and property disposal gain. The IIT calculation methods vary for different types of income.

Employment income is generally taxable, unless specifically exempt. Taxable employment income includes all wages, salaries, bonuses, annual bonuses, incentives, allowances, subsidies and benefits. Employment income is taxed at progressive rates, ranging from 3% to 45%. Every month the employer of the expatriate should:

Report the taxable employment income of the expatriate in an IIT return Withhold the IIT from the expatriate’s payroll, and Remit the IIT to the responsible tax authority.

Under the IIT regulations, some of employment benefits provided on a reimbursement basis to expatriates working in the PRC are not subject to IIT, for example:

Provision of accommodation or rental reimbursement

Reimbursement of transportation expenses incurred by the expatriate for travelling between the place of employment in the PRC and their family residences, which is limited to two trips a year

Reimbursement of relocation and moving costs upon commencement or end of the PRC assignment

Reimbursement of language training expenses for the expatriate

Reimbursement of education expenses incurred in the PRC for the children of the expatriate Reimbursement of meal and laundry expenses.

Such expenses should be in reasonable amounts. Also, expatriates will need to provide valid tax invoices for these expenses.

16 People’s Republic of China – Business and Taxation Guide

In addition, expatriates enjoy a statutory deduction of RMB 4,800 per month for employment income. 7.2 Foreign tax credit To avoid double taxation, the IIT Law and regulations state that individuals who have paid foreign income tax in respect of foreign income that is taxable in the PRC can be granted foreign tax credit. The credit cannot exceed the amount of IIT otherwise payable on such foreign income. If not fully utilised in one tax year, the foreign tax credit can be carried forward for five years to cover the IIT liability on future foreign income arising from that particular jurisdiction.

7.3 Assessment and filing

The PRC government requires taxpayers to file annual IIT returns in certain circumstances. Usually, expatriates should file annual IIT returns with the relevant tax authorities, unless:

They have stayed outside of the PRC for more than 30 consecutive days or 90 cumulative days in the calendar year concerned, or

Their annual income is lower than RMB 120,000. It is the legal responsibilities of the relevant individual expatriate (as opposed to the employer) to file the annual IIT return. The expatriate should file the annual IIT return, together with a copy of their valid personal identification document, with the relevant tax authority by 31 March of the following year. The employer should provide the expatriate with his/her monthly remuneration details and the reported IIT amounts.

7.4 Inheritance and gift tax As of the end of 2011, China does not have inheritance and gift tax laws.

17 People’s Republic of China – Business and Taxation Guide

8. Double taxation agreements With an aim to achieve greater economic integration in terms of investment and trade, the PRC has signed tax treaties with other countries. These tax treaties encourage businesses and individuals in other countries to invest and work in the PRC by reducing the potential double tax burdens imposed by the two jurisdictions. The treaties specify:

Whether the right to tax particular income is exercised by the country of residence or the country of source

To what extent tax credits will be granted by one country for taxes paid in another country Whether income is fully tax-exempt in one country or the other.

As of 2011, the PRC has signed tax treaties with more than 90 countries, including:

Australia Canada France Italy Japan New Zealand The Netherlands Singapore United Kingdom United States of America.

The PRC has also entered into tax treaties with the Special Administrative Regions of Hong Kong and Macau.

18 People’s Republic of China – Business and Taxation Guide

9. Sales and use taxes, other significant taxes and duties

9.1 Value Added Tax (VAT)

VAT is levied on all units and individuals engaged in the sale or importation of goods, or the provision of processing, repair or replacement services. VAT is calculated based on the sales value of the goods or the mentioned service.

There are two kinds of VAT taxpayers:

General taxpayers: Whose annual taxable sales value exceeds the threshold amount for small-scale taxpayers (see below). Generally, the applicable VAT rate is 17%. Certain goods (such as agricultural products and water) are taxed at 13%.

Small-scale taxpayers:

For taxpayers that are in the business of producing goods or providing taxable services, where annual taxable turnover is less than RMB 0.5 million

For taxpayers that are in the wholesale or retail business, where annual taxable turnover is less than RMB 0.8 million

The applicable VAT rate for small-scale taxpayers is 3%.Small-scale taxpayers are not allowed to issue VAT invoices.

Exports are exempt from output VAT in general. Input VAT incurred for the exports may be refunded according to special refund rates for the relevant exported goods, subject to fulfilment of various procedures and documentation requirements.

Different export VAT calculation methods are adopted for different types of exporting enterprises. For production enterprises, which export their self-manufactured goods, the ’Exempt, Credit and Refund’ method is applied to determine the export VAT refund. Using this method, some or all of the input VAT incurred for the exported goods may be recoverable, depending on the type of exported goods. A production enterprise may use the recoverable input VAT credit to offset the output VAT arising from its domestic sales. Any excess input VAT credit will be refunded or carried forward to offset future output VAT.

The PRC government adjusts the export VAT refund rates from time-to-time, as a means to exert its influence on economy.

9.2 Business Tax (BT)

BT is levied on all units and individuals that are engaged in the provision of taxable labour services, sale of immovable properties or transfer of certain intangible properties. Different tax rates (3%, 5% and 20%) may apply, depending on the nature of the transactions.

Typically:

Transportation, construction, telecommunications and cultural and sports services are taxed at 3%

19 People’s Republic of China – Business and Taxation Guide

Banking, insurance, tourist services, rental and leasing, advertising, consulting and transfer of intangible properties and immovable properties are taxed at 5%

Entertainment services are taxed at 5% or 20%.

BT is generally levied on the gross income. For certain industries (for example transportation, advertising agencies and tourist agencies), certain expenses can be deducted from the gross income when determining the BT liabilities.

Certain services are not subject to BT. These include medical services provided by hospitals and clinics, and educational services provided by educational institutions.

Starting on 1 January 2012, Shanghai implemented a pilot programme to transform certain designated services (i.e. transportation, modern services like R&D and technology, information technology, etc.) from BT payers to VAT payers.

9.3 Consumption Tax (CT)

CT is levied on manufacturers and importers of 14 types of consumer goods, such as motor cars, jewellery, tobacco, alcohol, cosmetics and petrol.

The CT rate ranges from 1% to 45%. For certain types of goods, CT is calculated by fixed amounts of CT per taxable unit.

9.4 Land Appreciation Tax (LAT)

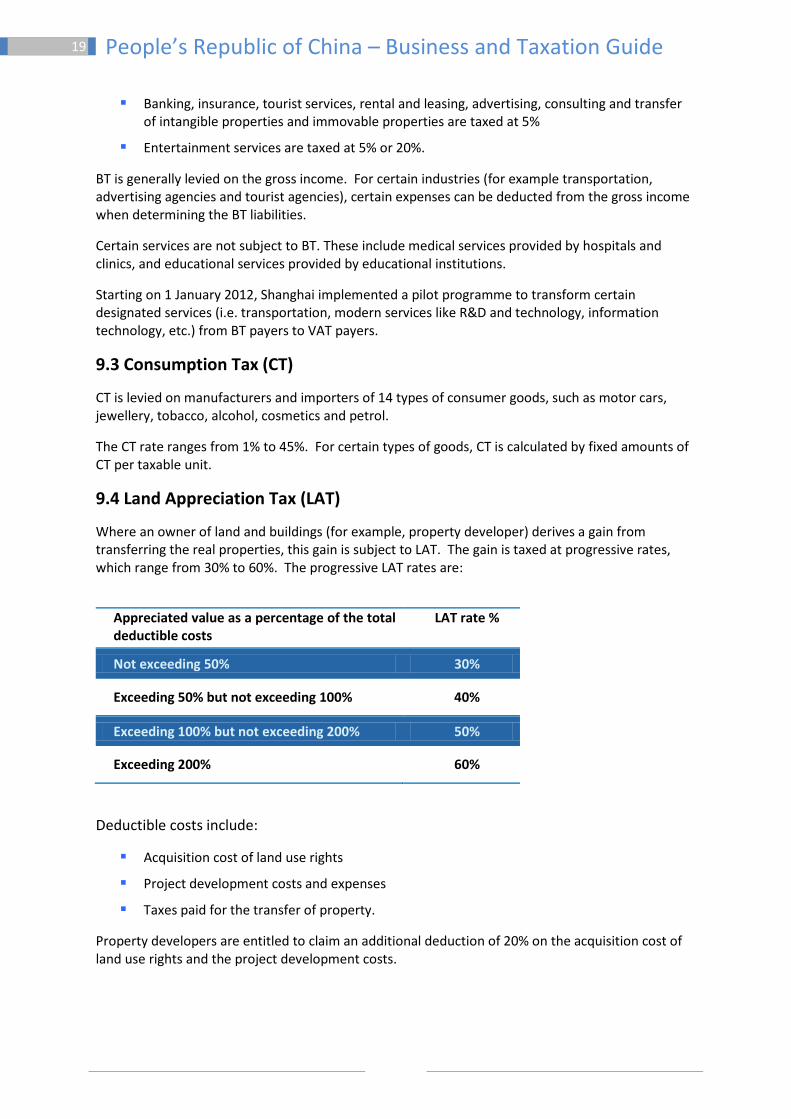

Where an owner of land and buildings (for example, property developer) derives a gain from transferring the real properties, this gain is subject to LAT. The gain is taxed at progressive rates, which range from 30% to 60%. The progressive LAT rates are:

Appreciated value as a percentage of the total deductible costs

LAT rate %

Not exceeding 50% 30%

Exceeding 50% but not exceeding 100% 40%

Exceeding 100% but not exceeding 200% 50%

Exceeding 200% 60%

Deductible costs include:

Acquisition cost of land use rights

Project development costs and expenses

Taxes paid for the transfer of property.

Property developers are entitled to claim an additional deduction of 20% on the acquisition cost of land use rights and the project development costs.

20 People’s Republic of China – Business and Taxation Guide

Also, a property developer may be required to file provisional LAT on a monthly or quarterly basis. The provisional LAT is calculated at 0.5% to 5% of the projects’ sales proceeds, depending on the type and location of the properties.

For a real estate development project , whereby construction has been certified as completed by various government authorities, the tax authorities may require the property developer to settle LAT when:

More than 85% of the saleable floor area of the whole project has been sold, or

85% or less of the saleable floor area has been sold and the remaining saleable floor area has been leased out, or is being used by the property developer themselves.

9.5 Resources tax

All units and individuals engaged in the extraction of mineral resources (for example, natural gas, crude oil and coal), or the production of salt within the PRC, are subject to Resources Tax. Resources Tax is calculated at different rates, either based on quantity or the dollar value.

9.6 Customs duty

General

Import duties vary, depending on any preferential tariff arrangements between the PRC and the country of origin. Customs duties are imposed on imported goods, independently of VAT and CT. VAT and CT are imposed on the customs-duty-inclusive value of the imported goods. Freight, insurance and other prescribed expenses are included as part of the duty value of the goods. Customs duty has to be paid within 15 days after Customs issues the duty payment notice.

Export duties are only imposed on limited types of goods, for example, certain mineral ores.

Exemptions

Enterprises that are engaged in contract processing or import processing arrangements may claim customs duty and VAT exemption on the importation of raw materials, providing that the products manufactured under the arrangement are for export. Importation of machinery and equipment for use under such arrangements may also be exempt from customs duty, if certain conditions are satisfied.

A FIE that is engaged in a project that is classified as ’Encouraged’ within the Catalogue of Guidance for Foreign Investment Industries, may be entitled to customs duty exemption for the importation of equipment, providing the:

Equipment is imported for self-use

Value of the equipment is covered by the total investment amount of the FIE, and

Equipment does not fall within the items listed in the ’Catalogue of Non-exempt Commodities Imported for Foreign-invested Projects’.

Importation of raw materials into Free Trade Zones and Export Processing Zones is exempt from customs duty and import VAT, providing the finished goods are not subsequently sold domestically. Importation of machinery and equipment for use within these zones are also exempt from customs duty and import VAT. The import and export declaration procedures in these zones are different from in the procedures in other locations.

21 People’s Republic of China – Business and Taxation Guide

Enterprises may claim customs duty exemption for machinery and equipment that are imported temporarily into the PRC (for instance, no more than six months, with possible extension to one year). However, the importer is required to make a guarantee payment. This is equivalent to the customs duty otherwise payable under general import.

9.7 Stamp duty

Stamp duty is levied on dutiable instruments that are executed, used or received in the PRC. These include sales and purchase contracts, leases and property title transfer agreements. The stamp duty rate ranges from 0.005% to 0.1%.

9.8 Real Estate Tax (RET)

Owners and individuals with a mortgage for buildings (plus in certain circumstances, custodians and users), are subject to RET. According to the national RET regulations (which are subject to local variations), RET may be imposed on:

Properties not rented out - original value of the property x (1 – statutory deduction %, ranging from 10% to 30% depending on the locality) x 1.2%

Properties rented out - rental income x 12%.

9.9 Deed Tax

The transferees (including purchasers and donees) of land and buildings are subject to Deed Tax. Deed Tax is imposed on the transaction price or the market value of the land and buildings, depending on the situations of how the land and buildings are transferred. The Deed Tax rate ranges from 3% to 5%, depending on the locality.

22 People’s Republic of China – Business and Taxation Guide

10. Portfolio investment for foreigners 10.1 Investment in PRC stocks

Foreigners are not allowed to buy and sell RMB-denominated ‘A’ shares in China's stock exchanges in Shanghai and Shenzhen, except for Qualified Foreign Institutional Investors (QFIIs) that have been specially approved by the PRC government. As of 28 November 2011, there were 108 QFIIs approved by the PRC government.

Limited numbers of USD or HKD-denominated ’B’ shares are traded in stock exchanges in Shanghai and Shenzhen, which enables foreigners to buy and sell. PRC State Owned Enterprises and domestic enterprises are also listed in overseas stock exchanges. Foreign investor dividends and capital gains derived from B shares and overseas listed shares of China Tax Resident Enterprises were exempt from income tax in the past based on a PRC circular Guoshuifa [1993] No. 45. However, this circular was cancelled in 2011. Currently, foreign investors would be subject to PRC income taxes on dividends and capital gains derived from B shares and overseas listed shares of China Tax Resident Enterprises. 10.2 Investment in PRC real estate Currently, the PRC government has implemented various measures to control speculations in the property market. In particular, an overseas individual (for example, a non-resident of the PRC) may purchase only one property for self-residence within the territory of China, and certain conditions apply. Other current measures include: An overseas entity that sets up a branch or representative office within the territory of

China may purchase a non-residence property for office purposes only. This would be in the city where the branch or representative office is registered.

An overseas entity that does not have an establishment within the territory of China cannot purchase a property in China.

23 People’s Republic of China – Business and Taxation Guide

11. Trusts The PRC government promulgated its first PRC Trust Law in 2001. Based on the Law, ’trust’ means the action in which the settler, with the trust in the trustee, entrusts certain property rights owned by the settler to the trustee. The trustee manages or disposes of the property rights in the name of the trustee, in accordance with the intentions of the settler and for the benefit of the beneficiary or for specific purposes.

However, there is no written tax regulation relating to trusts in the PRC. Consequently, the PRC tax position of a trust would be examined by tax authorities on a case by case basis.

24 People’s Republic of China – Business and Taxation Guide

12. Practical information 12.1 Transport

Air travel and train transportation are the most reliable and utilised means of passenger transport between the main centres in the PRC. Most international airlines services operate into and out of the main cities, including Beijing, Shanghai, Shenzhen and Guangzhou.

12.2 Language

Mandarin is the official language spoken in the PRC.

12.3 Time relative to Greenwich Mean Time (GMT)

The whole of the PRC is in one time zone, which is eight hours ahead of GMT.

12.4 Public holidays

The official public holidays observed by most businesses and government offices in the PRC are:

New Year’s Day – 1 January Spring Festival – 31 December, and the 1 and 2 of January, under Chinese Lunar Calendar Tomb Sweeping Festival – one day at the beginning of April (announced each year by the

government) Labour Day – 1 May Dragon Boat Festival – 5 May, under Chinese Lunar Calendar Mid-Autumn Festival - 15 August, under Chinese Lunar Calendar National Day - 1, 2 and 3 October