Embed Size (px)

Citation preview

The Performance of Underwriter Analyst Recommendations:

A Second Look

Maureen F. McNichols *Patricia C. O’Brien **Omer M. Pamukcu ***

Comments welcomeAugust 2004

* Contact author: Graduate School of Business, Stanford University, Stanford, CA 94305; (650) 723-0833; [email protected]** School of Accountancy, University of Waterloo, 200 University Ave. W., Waterloo, ON, Canada N2L 3G1; (519) 888-4567, ext. 5423; [email protected]*** School of Accountancy, University of Waterloo, 200 University Ave. W., Waterloo, ON, Canada N2L 3G1; (519) 888-4567, ext. 7119; [email protected]

The authors gratefully acknowledge the financial support of Stanford Graduate School of Business, the University of Waterloo, and the Social Sciences and Humanities Research Council of Canada. We are grateful to First Call for the use of recommendation data.

Abstract

We examine whether affiliated financial analysts’ buy recommendations after IPOs earn

lower returns than those of unaffiliated analysts during the 1994-2001 time period, when

analysts’ behavior is alleged to have been egregious. We extend the work of Michaely

and Womack (1999), who studied 1990-1991 IPOs. In contrast to Michaely and

Womack (1999), we do not see affiliated analyst recommendations earning lower

abnormal buy-and-hold returns than unaffiliated at intervals of three, six or twelve

months after the recommendations. Rather, in our pooled results we find that buy

recommendations from affiliated analyst generally earned significantly higher returns

than those from unaffiliated.

1

The Performance of Underwriter Analyst Recommendations: A Second Look

1. Introduction

In recent years, regulators, investors and the media have raised concerns that

analysts issued optimistically biased recommendations to maintain investment banking

ties between analysts’ employers and the companies that analysts cover.1 While the

anecdotal evidence is compelling that investment banking ties have influenced analysts’

research in recent years, we aim to explore the pervasiveness and nature of its influence

on the returns earned by investors in IPOs over the 1994-2001 period. We find that

investors did not generally earn lower returns following affiliated analysts'

recommendations for IPO companies than they did following unaffiliated analysts'

recommendations. We find that the difference in post-recommendation returns varies

substantially from year to year, without any obvious trend, lending no empirical support

to the notion that widespread investment-banking-related conflicts of interest cost

investors substantial sums.

The concern that investment banking ties could taint analysts’ research has led to

significant regulatory changes, including changes in New York Stock Exchange Rule 472

and NASDAQ Rule 2711. The revised rules aim to eliminate the influence of those

involved in investment banking over research analysts, by prohibiting supervision or

control of research analysts by any personnel engaged in investment banking activities,

by prohibiting research analysts in efforts to solicit investment banking, and by requiring

review of research analysts’ compensation at least annually by a committee that has no

1 These articles include Siconolfi (1992), Siconolfi (1995a), Siconolfi (1995b), and more recently, Feldman and Caplin (2002), Byrne (2002a), Byrne (2002b), Gasparino (2002) and Morgenson (2002).

2

representation of those involved in investment banking. (NYSE, 2003) In addition, the

SEC, NYSE and NASD and the New York Attorney General reached a global research

analyst settlement with ten Wall Street firms in the amount of $1.4 billion for failing to

ensure that the research they provided their customers was independent and unbiased.

The settlement requires that firms will separate research and investment banking,

including physical separation, completely separate reporting lines, separate legal and

compliance staffs, and separate budgeting processes. The firms will retain an

Independent Monitor who is acceptable to the SEC to review the firms’ compliance with

the structural reforms. (Donaldson, 2003)

In light of the sweeping changes in regulation of analyst research in response to

allegations of abuse in recent years, we believe it is useful to assess how the findings of

academic research might differ for the 1994-2001 period relative to the earlier sample

periods studied. Prior research by Dugar and Nathan (1995), Lin and McNichols (1998),

Dechow, Hutton and Sloan (2000) and Michaely and Womack (1999) has documented

systematic differences between the reports issued by analysts with and without

investment banking ties to the companies they cover. These studies are consistent in

finding that analysts who serve as lead underwriter of an equity offering, or affiliated

analysts, issue more optimistic earnings growth forecasts and more favorable

recommendations than unaffiliated analysts.2

However, the findings of these studies concerning the implications of greater

optimism in recommendations for return behavior are less consistent. Michaely and

Womack (1999), hereafter MW, find that the returns earned following lead analysts’ buy

2 These studies are less consistent in finding that analysts’ earnings forecasts differ, with Lin and McNichols (1998) finding no significant differences for one-year and two-year ahead forecasts, but Dugar and Nathan (1995) finding greater optimism for one-year ahead forecasts.

3

recommendations for a sample of companies going public in 1990 and 1991 are

significantly lower than those earned following non-lead analysts’ buy recommendations.

Dechow, Hutton and Sloan (2000) find that post-offering under performance is most

pronounced for firms with the highest growth forecasts made by affiliated analysts, for

their sample of IPO and SEO firms in the 1981-1990 period. Dugar and Nathan (1995)

find no difference in the returns earned by following the investment recommendations of

investment banker analysts and non-investment banker analysts for the 1983-1988 sample

period. Lin and McNichols (1998) find no difference in the returns earned following

affiliated and unaffiliated analysts’ buy or strong buy recommendations after seasoned

equity offerings from 1989-1994. An open question regarding the differences in return

results is whether they are due to differences in the time period studied, differences in the

offering studied (IPO vs. SEO), differences in the data on analysts’ recommendations or

forecasts, or differences in how affiliation is defined.

The aim of this study is to examine recent evidence concerning whether the

returns to following unaffiliated analysts’ recommendations exceed those associated with

following affiliated analysts’ recommendations. If affiliated analysts systematically bias

their recommendations relative to unaffiliated analysts and investors do not correctly

discount this bias, then we expect the returns to following unaffiliated analysts’

recommendations to be significantly greater. On the other hand, if affiliated

recommendations are not systematically biased relative to unaffiliated recommendations,

or if investors undo the bias in affiliated analysts’ recommendations, we expect returns to

affiliated recommendations to be similar to those from following unaffiliated

recommendations.

4

Our study is most closely related to MW in design. Their study examines the

return behavior associated with buy recommendations for a sample of 200 IPO’s

occurring in 1990 and 1991. Similar to their study, our recommendations data come from

First Call. However, the database available for academic subscription begins in 1994 so

it is not feasible for us to include the 1990-1991 period.

MW conclude that the recommendations by underwriter analysts show significant

evidence of bias. They also conclude that the market does not recognize the full extent of

this bias, because they find that the mean difference in post-recommendation returns to

the lead underwriter and non-underwriter buy recommendations is significantly negative.

They state:

For “buy” recommendations, the performance of the two groups diverges immediately. The price impact difference after three months is 8.9 percentage points, with a t-statistic of 2.43. This divergence continues for a year, with non-underwriter recommendations outperforming underwriters’ by an average 18.4 percentage points after one year (t-statistic = 2.29). The median one-year size-adjusted returns are 3.5% versus 11 .6% for a 15.1 percentage point difference.

Given the extensive anecdotal evidence concerning analyst conflicts in the late

1990’s, we believe it is interesting to examine the effect of affiliation on returns for this

later sample period. Similar to MW, we ask whether an underwriting relationship leads

to recommendations that are more favorable. Second, we test whether the market

correctly discounted the overly positive recommendations of affiliated underwriters.

Our study is also related to a recent working paper by Iskoz (2003). He examines

the return implications of bias in lead analyst recommendations for investors in IPO’s and

SEO’s in the 1993-2000 time period. His study differs from ours in three key respects.

First, our study uses First Call as a source of recommendation data rather than I/B/E/S.

5

Because First Call is the transmission channel that many investment banks use to

communicate research to their clients, we believe the timing of First Call

recommendations is very accurate. Second, we compare the behavior of lead analysts to

that of unaffiliated as well as non-lead affiliated analysts. The non-lead affiliated

category includes analysts employed by co-underwriter banks that some prior researchers

classified as unaffiliated, whereas we exclude co-underwriter analysts from the

unaffiliated classification. This is motivated by the findings of Lin and McNichols

(1998) that analysts affiliated with co-underwriters issue more favorable

recommendations than those of unaffiliated analysts and similar to those of lead

underwriter analysts. Third, we present our findings for each year of our sample period,

to assess the consistency of our findings through time.

Our preliminary findings are intriguing. First, we find that investors consistently

viewed the recommendations of lead underwriter analysts as less favorable news than

those by unaffiliated analysts, as measured by the size-adjusted returns in the three-day

period centered on the recommendation announcement. These findings suggest that

investors consistently viewed the buy recommendations of lead underwriter analysts with

some skepticism in our 1994-2001 sample period. These findings are substantially

stronger than those reported by MW, who find this effect is only marginally significant.

These findings also differ from those reported by Iskoz, who finds no significant

differences in the reaction to lead and non-lead buy recommendations.

We find that the mean three- and six-month returns following lead underwriter

buy recommendations are significantly more positive than the three- and six-month

returns following unaffiliated buy recommendations for our full sample period.

6

Furthermore, when we examine our findings for each year, we find that the difference in

three- (six-) month returns following lead underwriter buy recommendations is

significantly less positive than the returns following unaffiliated buy recommendations

only in 1998 and 2001 (1998). These findings hold when we separately focus on strong

buy recommendations rather than both strong buy and buy recommendations.3 In our

multivariate analyses, we find no significant differences in the three-, six- and twelve-

month returns following affiliated vs. unaffiliated analyst recommendations. These

findings suggest that the prior evidence of weaker performance following affiliated

recommendations vs. unaffiliated recommendations is not robust: it varies by year, and it

is sensitive to ?.

2. Hypotheses

As discussed above, prior studies have consistently documented that affiliated

analysts issue more favorable recommendations than unaffiliated analysts do. Consistent

with the prior findings, we expect that recommendations issued by affiliated analysts will

be more favorable for IPO companies than those issued by unaffiliated analysts in the

1994-2001 period. In particular, it will be of interest to assess whether the magnitude of

affiliated bias increased relative to that of prior sample periods.

In contrast, the evidence concerning the return implications of more favorable

investment recommendations is mixed. Ever-increasing media attention to conflicts of

interest throughout the 1990’s may have caused greater awareness and skepticism by

investors of affiliated analysts’ recommendations. If investors were sufficiently aware of

3 These findings contrast with Iskoz (2003), who finds that returns are significantly lower following lead analyst strong buy recommendations than non-lead strong buy recommendations, but does not find a significant difference for buy and strong buy recommendations taken together.

7

bias in affiliated analysts’ recommendations, the response to affiliated buy

recommendations would be less favorable than to the buy recommendations of

unaffiliated analysts. If the response at the announcement date fully reflects the

information in these recommendations, then we would not expect a difference in post-

recommendation returns to affiliated vs. unaffiliated buy recommendations. In contrast,

if investors do not fully discount the bias in analysts’ recommendations, then we expect

that the longer-term returns to following unaffiliated analysts’ recommendations will be

greater.

3. Sample and Design

Our sample includes U.S. companies that issued common stock in an underwritten

initial public equity offering between 1994 and 2001. We choose public offerings as a

starting point because the financing event allows us to distinguish affiliated from

unaffiliated analysts. Consistent with the prior literature on analysts’ banking affiliations,

we use the Securities Data Corporation (SDC) database, which includes only “firm

commitment” offerings, omitting “best efforts” offerings, so our sample is likewise

limited to firm commitment offerings. From our sample, we drop any IPO that (1) is a

unit offering, ADR, REIT or closed-end fund; (2) has a final offer price less than $5; (3)

does not have at least one analyst buy or strong buy recommendation in the calendar year

following the offer date; and (4) does not have data on the issue date from SDC database

that is sufficiently close to the beginning date of share prices on the Center for Research

in Security Prices (CRSP) database.4

4 Specifically, we remove 15 IPOs where the issue date on the SDC database is later than the appearance of the stock price on CRSP, or where the stock price does not appear on CRSP for three or more days after the issue date.

8

We obtain our analyst recommendations from the First Call database. We match

SDC underwriter names to First Call broker names by hand to link the two databases.

We define lead analysts as those serving as lead underwriter and affiliated non-lead

analysts as those serving as co-underwriter for a given equity offering; all others are

unaffiliated. For our tests, we examine the returns around the first buy or strong buy

recommendation for each analyst following the IPO, which gives us 8,306

recommendations.5

For our examination of excess returns before, at, and after the analyst

recommendation, we obtain return data from the daily CRSP files. We calculate excess

returns as the buy-and-hold returns on the stock minus the buy-and-hold return on the

appropriate CRSP market capitalization decile portfolio for the 30 days prior to the

recommendation, 3 (-1 to 1) day window around the recommendation and for 3, 6 and 12

months following the recommendation.6 Specifically, we measure cumulative excess

returns for each recommendation as:

, (1)

where is the raw return on stock i on day t, and is the return on the matching CRSP

market capitalization size decile for day t. is the excess return for firm i from time

a to time b. The excess return for the recommendation portfolios are the mean of the

cumulative excess return for each individual recommendation , :

5 Similar to Michaely and Womack (1999), we document that the lead underwriter and the affiliated non-lead underwriter analysts’ recommendations are available much sooner than the unaffiliated analysts’ recommendations. To see whether this influences our results, we also use affiliated recommendations that are closest in absolute time difference to the median unaffiliated analyst initial buy or strong buy recommendations. The results after accounting for the timing differences in this manner are consistent with the results presented in this paper.6 For recommendations made within 30 days after the IPO, we exclude the first-day return on the offer price from our calculation of the 30-days-prior excess return.

9

(2)

where n equals the number of recommendations in the event period with available

returns.

4. Results

Table 1 presents some descriptive statistics on our sample. Panel A shows that

the 1994-2001 period was associated with substantial offering activity, with the greatest

number occurring in 1996, at 471, and the fewest in 2001, at 72. The level of the

NASDAQ price index rose in each year from 1994 to 1999, and the number of IPO’s

declined along with the NASDAQ index in 2000 and 2001. MW document a similar

association between IPO activity and the level of the NASDAQ index in their 1990-1991

sample.

Panel B of Table 1 provides evidence on the market capitalization of IPO’s in the

1994-2001 period, and documents that offerings were substantially larger than in the

1990-1991 period. We find 50 % of IPO’s raise $200 million or more, as compared to

22% for MW’s sample period.

Panel C documents that the industry composition of our sample is fairly well

dispersed, with the greatest concentration of 26% in the Business services industry.

Approximately 10% of MW’s sample was comprised of firms in the Business Services

Industry, though it was the largest single industry in their sample as well.

Table 2 presents our initial replication and extension of MW concerning returns to

buy recommendations of affiliated vs. unaffiliated analysts. The mean excess return in

the 30 days prior to the recommendation release was significantly positive, at 4.8%. We

10

partition on three types of analysts, those issued by analysts employed by the lead

underwriter (L), those issued by analysts who were affiliated with a non-lead underwriter

(ANL), and those issued by analysts employed by investment banks that did not

underwrite the IPO (U). The mean ANL analyst’s buy recommendation was associated

with the highest prior return, at 5.6%, which is marginally significantly greater than the

returns preceding the U analysts’ recommendations. None of the other differences across

analyst categories are statistically significant.

Announcement returns for the three days surrounding the analysts’ first buy

recommendation are significantly positive, and are significantly greater for the U analysts

than for the ANL analyst (t=3.44) or the L analyst (t=3.38). This finding suggests that

investors view the buy recommendations of lead and co-underwriter analysts as less

favorable news than the buy recommendations of unaffiliated analysts, consistent with

MW. In contrast, the ANL return is not significantly different from the L analysts’

announcement returns (t=0.31), suggesting that aggregating ANL returns with U returns,

as MW did, will reduce the power to identify a difference in market reactions to affiliated

vs. unaffiliated analysts’ recommendations.

The number of days after the IPO date also corroborates the idea that ANL

recommendations are more similar to L recommendations than to U. ANL

recommendations occur in much greater proximity to the lead recommendations, at 49 vs.

51 days after the IPO, with medians of 27 and 28. Note the median days are just slightly

above the 25-day “quiet period” period required by law.7 In contrast, unaffiliated

analysts recommendations occur on average 183 (median 189) calendar days after the

IPO.

7 See Bradley, Jordan and Ritter (2003).

11

Excess returns for the three months following the analysts’ first buy

recommendation have significantly positive means and significantly negative medians,

suggesting longer-term return performance varied across IPO firms. Contrary to the

conventional view, the mean returns are significantly lower for the U analysts than for the

L or ANL analysts (t=-1.99 and t=-2.25 respectively). Relatedly, the ANL return is not

significantly different from the L analysts’ announcement returns (t=-0.03), consistent

with their similar timing, noted above. We observe similar findings for six-month

returns, where the means are now less positive for all groups than for three-month

returns, but L and ANL analyst returns remain significantly greater than U returns. Mean

and median excess returns for twelve months are significantly negative for buy

recommendations of L and U analysts, but there is no significant difference in the returns

between these two groups.

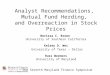

We plot the twelve month excess returns in figure 1, which shows the mean

returns following L, ANL and U analysts' buy recommendations are fairly similar

throughout the twelve month period, with slightly greater returns to the lead analyst

throughout the first eight months after the recommendation. The figure also illustrates

the loss of power from combining ANL with U analysts: the separation between L and U

is larger than the separation between L and non-lead (ANL + U).

Table 3 Panel A examines the distribution of ratings across analyst categories, for

the first recommendation following the IPO. Following the convention adopted by First

Call of assigning a 1 to "Strong Buy", a 2 to "Buy", a 3 to Hold, 4 to "Sell" and 5 to

"Strong Sell," we compute the mean and median ratings for each analyst category in

Panel B. The findings indicate a very small difference in the mean recommendation of L

12

and U analysts, with a mean recommendation of 1.45 by L analysts and of 1.49 by U

analysts. Furthermore, the median rating is 1 for each of the analyst categories. This

difference between L and U analysts' recommendations is substantially smaller than that

seen in prior studies, such as Lin and McNichols (1998). Although the difference in

recommendations appears small, there is still potential for overoptimism by lead analysts

if their recommendations are for stocks that unaffiliated analysts are unwilling to cover

because their recommendations would be less favorable.8 The data indicate that the

means and medians are significantly different across analyst categories for the sample as

a whole. Our year-by-year breakdown, however, shows that this is driven primarily by

differences in 1997and 2001.

Table 4 presents the mean and median returns centered on the recommendation

date by analyst category, similar to Table 2, for each sample year. The findings indicate

the results vary considerably from year to year. The results in Table 4 Panel A on prior-

30-day returns, which sample-wide are not significantly different across most analyst

categories, vary considerably over time. The magnitude of mean prior-30-day excess

returns varies from a low of 0.7% in 2001 to a high of 10.7% in 1999. Furthermore, U

analysts’ prior-30-day returns are significantly higher than L analysts’ in 1994, 1995, and

1997, but significantly lower in 1999 and lower but insignificant in 2000. These findings

do not suggest a consistent tendency of lead analysts to provide coverage after more

negative returns.

Table 4 Panel B presents the mean and median three-day announcement returns

by year. The signs are relatively consistent, though the differences are not always

statistically significant: the market reaction to U buy recommendations is usually greater

8 We plan to explore this further in the next version of the paper.

13

than that to L buy recommendations. The difference in mean three-day returns is positive

in all but 1998 and the median difference is positive in all but 2000. These findings,

though not strong, indicate that the market generally viewed the lead buy

recommendations as less favorable news than the unaffiliated buy recommendations,

throughout the 1994-2001 sample period. These results do not confirm those of Iskoz

(2003), although our sample periods substantially overlap. Iskoz (2003) found no

difference in investors’ three-day response to lead versus non-lead recommendations.9

Table 4 Panel C documents the distribution of days after the IPO date that the first

recommendation is issued by analyst category and year. The findings indicate that

analysts have reduced the time to issuing their first recommendation throughout the

sample period, with the mean (median) buy recommendation occurring 120 (77) days

after the IPO in 1994 but only 68 (28) days after the IPO in 2001. Much of the reduction

in time to the first recommendation occurred for L analysts by 1996, whereas the biggest

decline occurred for U analysts in 2001, dropping from a median of 172 to 98 days

between 2000 and 2001. The similarity between L and ANL analysts in number of days

between the IPO and the first recommendation is also quite striking, and supports the

design choice to treat co-underwriter analysts as affiliated rather than unaffiliated.

Table 4 Panel D presents the mean and median three-month excess returns to

following the analysts' first buy recommendations by year. The returns to L

recommendations are significantly lower than returns to U recommendations in only two

of the sample years, 1998 and 2001, and the 2001 mean result is not significant at

conventional levels. Furthermore, from Table 3 Panel B, the greatest difference in the

9 Two possible reasons for the difference in this result are: his aggregation of non-lead affiliated analysts with unaffiliated analysts may have obscured differences; or the IBES analyst database he uses has less precise dates than the First Call database we use.

14

favorableness occurred in 2001, with a mean of 1.45 and median of 1 for L versus a mean

of 1.67 and median of 2 for recommendations issued by U analysts. It is also interesting

to note that the findings for 2001 are based on 396 recommendations, where the typical

sample is substantially larger in other years. Three-month returns to L recommendations

are significantly higher only in 1999, and the differences in most years are statistically

insignificant. Therefore, the relations we observe overall in Table 2 are primarily

attributable to 1999, which has more analyst recommendations than any other sample

year. The bottom line, however, is that returns to analyst recommendations vary across

years, and no generalizable result on affiliation emerges from these data.

The findings for six-month returns in Panel E are generally consistent with those

of three-month returns, with significantly lower median returns in 1998 and marginally

significantly lower median returns in 2001. For both three-month and six-month returns,

lead analyst performance was significantly stronger than unaffiliated analyst performance

in 1999.

To ensure that our inferences are not influenced by correlated omitted variables,

we examine the relation between affiliation and returns around recommendation dates

through multivariate analysis. Following MW, the estimation equation is:

(3)

where is the excess return before, at or after the the recommendation

announcement; LEADi is an indicator variable equal to one if the analyst employed by the

lead underwriter makes the recommendation and zero if a non-lead analyst makes the

recommendation; Sizei is the log of market capitalization at the end of the quiet period;

15

Timei is the number of days between the IPO and the recommendation; DEARNi is an

indicator variable equal to one if an earnings announcement has occurred in the three

days around the recommendation date; DFIRSTi is an indicator variable that takes the

value of one if the recommendation is the first one to be issued on the IPO, and zero

otherwise; and LEADi × TIMEi is an interaction term between the source of

recommendation and the number of days between the IPO and the recommendation.

Table 5 presents the estimation results for the model, and includes each of the

return intervals in our previous analyses. The estimation results for the prior 30 days

indicate that SIZEi is positively associated with excess returns, suggesting larger IPO's

have more favorable returns prior to recommendations. The LEADi indicator is

insignificant, suggesting no difference between LEADi and NONLEADi analysts in their

tendency to issue buy recommendations following negative returns. These findings are

counter to the “booster shot” hypothesis and findings of MW, that lead analysts tend to

issue BUY recommendations to support offerings that are not performing well. The

findings also suggest that TIMEi since the offering is significantly negatively related to

prior 30-day returns. These findings suggest that later recommendations are significantly

associated with more negative prior returns.

Panel B presents the findings for the prior-30-day period when lead and co-

underwriter analysts are classified as affiliated. These findings are consistent with those

based on the LEAD/non-LEAD classification, and again do not support the booster shot

hypothesis.

The estimation results for the 3-day announcement excess returns confirm the

previous findings. The LEADi indicator is insignificantly different from zero in Panel A,

16

suggesting that control variables are responsible for some of the difference in mean 3-day

returns between lead and non-lead analysts documented in Table 2. The AFFILIATEDi

indicator is significantly negative, indicating that investors at least partially discount the

buy recommendations of lead and co-underwriter analysts.

The estimation results for the 3-, 6- and 12-month post-recommendation windows

are consistent across panel A and panel B. There are no significant differences in the

post-recommendation excess returns of lead vs. non-lead analysts or in the post-

recommendation excess returns of affiliated vs. unaffiliated analysts.

Finally, Panel C includes indicator variables for both LEADi and AFFILIATEDi.

With both these indicators in the model, AFFILIATEDi will capture the ANL differences

from U analysts, while LEADi will capture L differences from ANL. The findings

indicate that there are no significant return differences across any interval between L and

ANL analysts, but that 3-day excess returns continue to be significantly lower to

affiliated recommendations, consistent with investor discounting of all affiliated buy

recommendations, relative to unaffiliated.

5. Summary and conclusions

In this paper we have examined whether affiliated financial analysts’ buy

recommendations after IPOs earn lower returns than those of unaffiliated analysts

during the 1994-2001 time period, when analysts’ behavior is alleged to have been

egregious. We extend the work of Michaely and Womack (1999), who studied 1990-

1991 IPOs. Our extensions include examining a later time period with more years

17

and a larger number of recommendations; examining the issue year-by-year; and

studying different definitions of affiliation.

We find that investors appear to discount buy recommendations of affiliated

analysts, consistent with MW. In contrast to MW, however, we do not see affiliated

analyst recommendations earning lower abnormal buy-and-hold returns than

unaffiliated at intervals of three, six or twelve months after the recommendations.

Rather, in our pooled results we find that buy recommendations from affiliated

analyst generally earned significantly higher returns than those from unaffiliated. Our

year-by-year breakdown, however, reveals wide variation in this result across years,

from significant outperformance by affiliated analysts in 1999 to significant

underperformance in 1998 and 2001. No time trend is evident in these results, and

most years in our sample period show no statistically significant difference between

affiliated and unaffiliated analysts’ abnormal returns. We also find co-underwriters

similar to lead underwriters, and different from unaffiliated analysts, both in their

behavior (timing and optimism of recommendations) and in investors’ responses to

their recommendations.

Our results also fail to confirm those of Iskoz (2003), whose sample period

substantially overlaps ours. Alhough (similar to our findings) he did not find a

difference in post-recommendation returns when he aggregated buys and strong buys

together, he did find underperformance of lead analysts’ recommendations for strong

buy recommendations alone. In untabulated analysis, we replicate our tests using

only strong buy recommendations, without altering our conclusions.

18

Our results do not mean that no investors were harmed by investment banking

conflicts of interest, nor do they necessarily imply that the recent regulatory changes

were unwarranted. Our results do suggest, however, that the widely-cited MW result

that affiliated analysts’ buy recommendations lead to lower excess returns than those

of unaffiliated analysts may have been specific to their relatively limited sample

period, 1990-1991. In particular, that result does not generalize to the 1994-2001

period when affiliated analysts allegedly succumbed to more extreme conflicts of

interest and egregiously misled investors. We note as well that our investigation of

different definitions of affiliation suggests that MW’s decision to pool non-lead

affiliated analysts with unaffiliated analysts reduced the power of their tests, lending

support to the idea that their results were time-period-specific.

One potential explanation for the difference between our results and MW’s, and a

potential area for further investigation, is that investors learned from the earlier time

period and were more wary in the later time period. Possibly, investors impound any

information in the analyst’s recommendation fully at its announcement, leaving no

predictive value afterwards, regardless of affiliation.

19

References

Bradley, D., Jordan, B. and J. Ritter. 2003. “The Quiet Period Goes Out with a Bang.”

Journal of Finance, 58 (1), 1-36.

Byrne, John. “Analysts.” BusinessWeek online (May 6, 2002).

<http://www.businessweek.com/magazine/content/02_18/b3781706.htm>

Byrne, John. “How to Fix Corporate Governance.” BusinessWeek online (May 6, 2002).

<http://www.businessweek.com/magazine/content/02_18/b3781701.htm>

Chen, H.-C. and J.R. Ritter. “The Seven Percent Solution,” Journal of Finance 55 (June

2000): 1105-1131.

Dechow, P., A. Hutton and R. Sloan. “The relation between analysts’ forecasts of long

term growth and stock price performance following equity offerings.” Contemporary

Accounting Research (Spring 2000): 1-32.

Donaldson, William. “Testimony concerning the global research analyst settlement.”

Before the Senate Committee on Banking, Housing and Urban Affairs, May 7, 2003.

Dugar, A., and S. Nathan. “The effects of investment banking relationships on financial

analysts’ earnings forecasts and investment recommendations.” Contemporary

Accounting Research (Fall 1995): 131-160.

20

Feldman, Amy, and Joan Chaplain. “Is Jack Grubman the worst analyst ever?”

CNNMoney (April 25, 2002). <http://money.cnn.com/2002/04/25/pf/investing/grubman>

Gasparino, Charles. “NASD expands inquiry to analysts’ bosses.” The Wall Street

Journal (January 6, 2003): C1.

Greenspan, Alan. “Corporate governance.” Remarks by Chairman Alan Greenspan at

the Stern School of Business, New York University, New York, New York, March 26,

2002.

<http://www.federalreserve.gov/boarddocs/speeches/2002/200203262/default.htm>

Lin, H. and M. McNichols (1998). “Underwriting relationships, analysts’ earnings

forecasts and investment recommendations.” Journal of Accounting and Economics 25

(February): 101-128.

McNichols, M. and P.C. O’Brien (1997). “Self-selection and Analyst Coverage,”

Journal of Accounting Research 35 (Supplement): 167-199.

Michaely, R., and K. L. Womack (1999). "Conflicts of Interest and the Credibility of

Underwriter Analyst Recommendations." Review of Financial Studies 12, no. 4, pp. 653-

86.

21

Morgenson, Gretchen. “Requiem for an Honorable Profession.” The New York Times

(May 5, 2002): section 3, p. 1.

New York Stock Exchange. “Information Memo 03-36: Rule 472 Amendments to

Disclosure and Reporting Requirements.” August 25, 2003.

Spitzer, Eliot (2002) “Institutional Investor Dinner, November 12, 2002.” Office of New

York State Attorney General Eliot Spitzer.

<http://www.oag.state.ny.us/press/statements/nov12_inst.html>

Siconolfi, M. “At Morgan Stanley, analysts were urged to soften harsh views.” The Wall

Street Journal (July 14 1992): A1.

Siconolfi, M. “A rare glimpse at how street covers clients.” The Wall Street Journal

(July 14 1995a): C1.

Siconolfi, M. “Incredible ‘buys’: Many companies press analysts to steer clear of

negative ratings.” The Wall Street Journal (July 19 1995b): A1.

22

Table 1: Description of IPO SamplePanel A: Distribution of firms conducting initial public offerings by year (with offer price greater than $5) and the year end NASDAQ price index

Year Number of IPOsNasdaq Price

Index1994 215 911.841995 291 1,282.721996 471 1,569.791997 343 1,922.351998 212 2,672.141999 378 4,957.772000 276 2,987.632001 72 2,361.62Total 2,258

Panel B: IPO firms differentiated by market capitalization in Millions

Market Capitalization Percent of IPOs Number of IPOsLess then $50 7 164$50 - $99.9 18 413$100 - $199,99 24 553$200 - $400 20 444Greater than $400 30 684All IPO firms 100 2,258

Panel C: Distribution of IPO firms across industry groups (by two-digit SIC code)

SIC code Percent of IPOsNumber of

IPOsBusiness services (73) 26.2 592Electronic equipment (36) 9.6 217Communications (48) 6.1 137Instruments (38) 5.9 133Chemicals and allied products (28) 4.9 110Industrial equipment (35) 4.8 108Engineering, Accounting, Research, Management, And Related Services (87) 4.0 90Miscellaneous Retail (59) 2.5 57Health services (80) 2.5 56Durable Goods (50) 2.3 52Non-depository Credit Institutions (61) 2.0 46Other Industries (Various) 29.2 660All IPO firms 100.0 2,258

23

Notes:Sample includes all firm commitment equity offerings that (1) have a final offer price greater than $5; (2) have at least one analyst buy or strong buy recommendations in the calendar year following the IPO; and (3) have data on the issue date from SDC database that is on or up to three days before stock prices appear on the CRSP database. Market capitalization is measured at the end of the 25-day SEC quiet period as shares outstanding times market price.

24

Table 2: Excess returns before, at, and after analyst buy recommendations of IPO firms, differentiated by underwriting relationships

All buy Recommendations

By Unaffiliated

(U)

By Affiliated Non-Lead

(ANL)By Non-

Lead (NL)By Lead

(L)t-stat/z-stat

U-ANLt-stat/z-stat

U-Lt-stat/z-stat

ANL-Lt-stat/z-stat

NL-L (N = 8306) (N = 3882) (N = 2644) (N = 6526) (N = 1780) Excess Return, Prior 30 Days mean 4.8% 4.2% 5.6% 4.8% 4.7% -1.84 -0.59 0.99 0.08median 0.9% 0.8% 1.2% 0.9% 0.7% -1.32 -0.14 0.99 0.37

Excess Return, 3-day Eventmean 2.0% 2.6% 1.6% 2.2% 1.5% 3.44 3.38 0.31 2.30median 0.7% 1.2% 0.3% 0.8% 0.3% 4.33 4.10 0.19 2.70

Days after IPO datemean 112 183 51 130 49 65.32 63.22 1.45 43.20median 51 189 28 90 27 49.33 44.52 2.90 29.73

Excess Return, event + 3 monthsmean 3.1% 1.5% 4.5% 2.7% 4.5% -2.25 -1.99 -0.03 -1.25median -3.9% -3.9% -4.1% -3.9% -3.8% -1.27 -1.43 -0.29 -1.05

Excess Return, event + 6 monthsmean -1.6% -4.0% 0.7% -2.1% 0.4% -2.61 -2.15 0.14 -1.26median -12.6% -13.9% -10.7% -12.7% -11.4% -2.33 -2.15 -0.06 -1.40

Excess Return, event + 12 monthsmean -6.5% -5.3% -7.3% -6.1% -7.9% 0.74 0.90 0.21 0.69median -31.2% -32.4% -29.5% -31.0% -31.8% -1.51 -0.73 0.54 -0.21

25

Notes:Excess returns (size adjusted mean and median buy-and-hold returns) are calculated for periods before, at, and after the buy or strong buy recommendation event date given by First Call for the 8,306 observations. The size adjustment is done by subtracting the buy-and-hold return from the appropriate value-weighted CRSP decile. We define “By Unaffiliated” as recommendations made by analysts from brokerage firms that were not lead or co-underwriter for the IPO. Affiliated Non-Lead recommendations are made by analysts from brokerage firms that were the co-underwriter for the IPO. Non-Lead recommendations, includes those made by analysts from Unaffiliated and Affiliated Non-Lead brokerage firms. Lead recommendations are made by analysts from brokerage firms that were the lead underwriter for the IPO. “Days after IPO date” is the number of calendar days between the IPO date and the recommendation date. The t-statistics use the pooled-variance in the excess returns and the z-statistics are calculated using the Wilcoxon ranked-sum test.

26

Table 3: Analyst recommendations by year, differentiated by underwriting relationships

Panel A: Distribution of recommendationsBy

Unaffiliated (U)

By Affiliated Non-Lead

(ANL)

By Non-Lead

(NL)

By Lead (L)

Strong Buy 2133 1354 3487 1010Buy 1613 1226 2839 739Hold 133 63 196 31Sell 2 0 2 0

Strong Sell 1 1 2 0Total 3882 2644 6526 1780

27

Panel B: Distribution of recommendations by year

All Recom-menda-

tions

ByUnaffili-ated (U)

By Affiliated Non-Lead

(ANL)

ByNon-Lead

(NL)By Lead

(L)

t-stat/z-stat

U-ANL

t-stat/z-stat U-L

t-stat/z-stat

ANL-L

t-stat/z-stat NL-L

Full Samplen 8306 3882 2644 6526 1780mean 1.49 1.49 1.51 1.50 1.45 -1.87 2.35 3.80 3.28median 1 1 1 1 1 -2.45 1.76 3.71 2.841994n 483 220 134 354 129mean 1.40 1.39 1.46 1.41 1.37 -1.15 0.25 1.31 0.78median 1 1 1 1 1 -1.35 -0.11 1.13 0.451995n 775 361 226 587 188mean 1.49 1.46 1.56 1.50 1.45 -1.78 0.30 1.88 1.07median 1 1 1 1 1 -2.08 -0.04 1.79 0.791996n 1341 599 425 1024 317mean 1.42 1.37 1.47 1.41 1.45 -2.75 -2.12 0.42 -1.14median 1 1 1 1 1 -3.14 -2.60 0.29 -1.481997n 1088 447 365 812 276mean 1.33 1.36 1.36 1.36 1.26 -0.01 2.68 2.59 3.03median 1 1 1 1 1 -0.12 2.34 2.37 2.601998n 876 397 286 683 193mean 1.48 1.49 1.48 1.48 1.46 0.24 0.50 0.28 0.45median 1 1 1 1 1 -0.03 0.32 0.33 0.361999n 2002 1082 605 1687 315mean 1.57 1.56 1.58 1.56 1.57 -0.70 -0.50 0.06 -0.31median 2 2 2 2 2 -0.99 -0.75 0.03 -0.492000n 1345 638 445 1083 262mean 1.57 1.58 1.58 1.58 1.53 -0.02 1.09 1.06 1.17median 2 2 2 2 2 -0.17 1.05 1.14 1.192001n 396 138 158 296 100mean 1.59 1.67 1.62 1.64 1.45 0.75 3.18 2.64 3.27median 2 2 2 2 1 -0.64 2.97 2.55 3.09

28

Table 4: Yearly examination of excess returns before, at, and after analyst buy recommendations of IPO firms, differentiated by underwriting relationships (cont’d)

Panel A: Excess return, prior 30 days

Year All buy

Recommendations

By Unaffiliated

(U)

By Affiliated Non-Lead

(ANL) By Lead (L)t-stat/z-stat

U-ANLt-stat/z-stat

U-Lt-stat/z-stat

ANL-L

1994 mean 2.5% 3.8% 2.6% 0.3% 0.79 2.17 1.20median 0.9% 1.7% 0.8% -0.5% 0.82 2.16 1.19

1995 mean 3.7% 4.8% 4.3% 1.0% 0.28 2.40 1.82median 1.6% 1.4% 2.8% 0.6% 0.15 1.79 1.51

1996 mean 2.4% 2.6% 2.2% 2.3% 0.33 0.19 -0.10median 0.1% 1.2% -0.5% -0.4% 0.92 0.33 -0.42

1997 mean 0.9% 2.7% -0.5% -0.2% 2.59 2.21 -0.19median -0.1% 0.7% -1.1% -0.3% 2.36 1.98 -0.28

1998 mean 3.3% 3.4% 3.9% 2.0% -0.29 0.66 0.86median -0.1% -0.2% 0.5% -1.3% 0.09 1.07 1.04

1999 mean 10.7% 6.6% 14.9% 16.9% -3.94 -3.73 -0.69median 2.9% 1.2% 4.9% 5.1% -4.02 -3.90 -0.72

2000 mean 4.9% 3.5% 5.9% 6.7% -1.19 -1.26 -0.29median 1.5% -0.5% 4.1% 4.1% -1.92 -1.50 0.18

2001 mean 0.7% 2.8% -0.6% 0.0% 1.96 1.39 -0.37 median 1.3% 1.2% 1.4% 1.0% -0.95 0.63 -0.29

29

Table 4: Yearly examination of excess returns before, at, and after analyst buy recommendations of IPO firms, differentiated by underwriting relationships (cont’d)

Panel B: Excess return, 3-day event

Year All buy

Recommendations

By Unaffiliated

(U)

By Affiliated Non-Lead

(ANL) By Lead (L)t-stat/z-stat

U-ANLt-stat/z-stat

U-Lt-stat/z-stat

ANL-L

1994 mean 1.3% 1.7% 1.2% 0.7% 0.67 1.42 0.69median 0.6% 0.9% 0.7% 0.4% 0.61 0.86 0.26

1995 mean 2.2% 3.0% 2.1% 0.8% 1.29 3.00 1.75median 1.2% 1.6% 1.3% 0.2% 0.76 2.82 1.92

1996 mean 1.6% 1.7% 1.8% 1.2% -0.19 0.93 0.98median 1.0% 1.3% 0.8% 0.3% 0.95 1.63 0.74

1997 mean 1.9% 2.3% 1.7% 1.4% 0.90 1.63 0.44median 0.8% 1.2% 0.5% 0.7% 1.76 1.88 0.19

1998 mean 2.3% 2.0% 2.2% 3.1% -0.30 -1.09 -0.86median 0.4% 1.0% 0.1% 0.2% 0.36 0.26 0.01

1999 mean 3.0% 4.0% 1.6% 2.5% 3.49 1.58 -0.85median 0.6% 1.4% -0.1% 0.3% 3.33 2.02 -0.56

2000 mean 1.6% 1.8% 1.4% 1.6% 0.38 0.17 -0.16median 0.0% 0.3% -0.5% 0.6% 1.16 0.17 -0.72

2001 mean 0.3% 2.2% -0.3% -1.5% 2.55 3.21 1.07 median 0.3% 1.6% -0.3% -0.8% -2.80 3.27 0.79

30

Table 4: Yearly examination of excess returns before, at, and after analyst buy recommendations of IPO firms, differentiated by underwriting relationships (cont’d)

Panel C: Days after IPO date

Year All buy

Recommendations

By Unaffiliated

(U)

By Affiliated Non-Lead

(ANL) By Lead (L)t-stat/z-stat

U-ANLt-stat/z-stat

U-Lt-stat/z-stat

ANL-L

1994 mean 120 177 80 64 10.11 12.95 1.96median 77 175 50 47 8.19 9.43 1.38

1995 mean 119 185 65 58 17.18 19.21 1.40median 69 196 42 40 12.35 12.49 0.95

1996 mean 114 180 59 66 22.02 18.07 -1.28median 55 187 33 29 17.16 15.07 0.83

1997 mean 114 190 64 56 20.16 21.57 1.62median 54 197 30 28 16.17 16.08 2.11

1998 mean 114 192 51 47 21.62 21.23 0.83median 47 203 28 27 16.11 14.82 2.22

1999 mean 120 192 38 33 45.23 44.86 1.84median 69 193 27 26 29.43 24.03 2.85

2000 mean 103 174 41 34 28.73 31.30 2.79median 35 172 27 27 21.04 18.84 2.40

2001 mean 68 131 36 31 10.20 11.09 1.90 median 28 98 28 27 -8.61 8.40 1.58

31

Table 4: Yearly examination of excess returns before, at, and after analyst buy recommendations of IPO firms, differentiated by underwriting relationships (cont’d)

Panel D: Excess return, event +3 months

Year All buy

Recommendations

By Unaffiliated

(U)

By Affiliated Non-Lead

(ANL) By Lead (L)t-stat/z-stat

U-ANLt-stat/z-stat

U-Lt-stat/z-stat

ANL-L

1994 mean 4.4% 5.1% 4.3% 3.4% 0.28 0.57 0.27median -0.2% 1.5% -1.6% -1.2% 0.60 0.93 0.36

1995 mean 6.1% 7.2% 4.6% 5.7% 0.92 0.45 -0.31median 1.7% 3.0% 1.3% -0.2% 0.66 0.86 0.25

1996 mean -1.2% -2.3% -0.1% -0.9% -1.15 -0.63 0.39median -2.6% -2.9% -2.6% -2.3% -0.76 -0.31 0.36

1997 mean 4.8% 3.6% 4.9% 6.6% -0.47 -1.01 -0.54median -1.0% -1.2% -1.4% 0.5% -0.32 -1.13 -0.84

1998 mean 3.8% 8.9% -2.2% 2.1% 2.56 1.25 -0.77median -7.4% -2.5% -10.9% -11.1% 2.90 2.07 -0.33

1999 mean 10.8% 3.5% 19.6% 18.9% -4.27 -2.90 0.13median -7.1% -9.8% -4.0% -6.5% -3.74 -2.22 0.68

2000 mean -8.8% -10.5% -8.1% -5.9% -0.74 -1.19 -0.52median -16.4% -17.6% -16.5% -14.2% 0.42 -0.41 -0.65

2001 mean 6.2% 10.3% 5.1% 2.3% 1.34 1.84 0.73 median 6.3% 10.7% 6.3% 1.2% -1.39 2.02 1.04

32

Table 4: Yearly examination of excess returns before, at, and after analyst buy recommendations of IPO firms, differentiated by underwriting relationships (cont’d)

Panel E: Excess return, event +6 months

Year All buy

Recommendations

By Unaffiliated

(U)

By Affiliated Non-Lead

(ANL) By Lead (L)t-stat/z-stat

U-ANLt-stat/z-stat

U-Lt-stat/z-stat

ANL-L

1994 mean 11.1% 10.7% 13.5% 9.1% -0.57 0.33 0.78median 3.0% 2.9% 4.2% -0.5% -0.11 0.57 0.63

1995 mean 5.9% 4.0% 9.3% 5.4% -1.23 -0.30 0.80median -0.8% -3.3% 0.6% -1.3% -1.72 -0.65 0.85

1996 mean -7.8% -6.3% -8.7% -9.4% 0.94 1.04 0.21median -11.7% -11.8% -10.9% -13.6% 0.54 0.88 0.43

1997 mean 0.4% -0.1% 0.5% 1.0% -0.16 -0.27 -0.13median -7.1% -9.7% -5.2% -2.3% -1.80 -2.14 -0.45

1998 mean 6.1% 11.5% -1.4% 6.0% 1.74 0.65 -0.74median -11.9% -5.3% -13.4% -16.4% 3.51 2.84 -0.10

1999 mean 3.6% -8.8% 19.0% 16.6% -5.20 -3.39 0.28median -25.2% -31.3% -15.0% -20.8% -4.92 -2.63 1.11

2000 mean -20.9% -18.5% -24.9% -20.1% 2.10 0.45 -1.23median -32.4% -29.2% -38.1% -32.8% 2.72 0.84 -1.25

2001 mean 6.8% 7.8% 9.7% 1.0% -0.43 1.37 1.82 median 7.8% 9.1% 11.6% 0.8% 0.30 1.47 1.87

33

Table 4: Yearly examination of excess returns before, at, and after analyst buy recommendations of IPO firms, differentiated by underwriting relationships (cont’d)

Panel F: Excess return, event +12 months

Year All buy

Recommendations

By Unaffiliated

(U)

By Affiliated Non-Lead

(ANL) By Lead (L)t-stat/z-stat

U-ANLt-stat/z-stat

U-Lt-stat/z-stat

ANL-L

1994 mean 16.6% 17.1% 20.9% 11.3% -0.38 0.62 0.84median -4.5% -4.7% -2.9% -8.2% 0.11 1.03 0.81

1995 mean -3.6% -8.8% 4.3% -3.0% -1.95 -0.85 0.95median -16.5% -21.3% -6.9% -16.6% -2.17 -0.89 0.95

1996 mean -12.8% -7.1% -18.6% -15.5% 2.57 1.64 -0.63median -21.5% -20.0% -23.0% -25.9% 1.52 1.39 0.04

1997 mean -8.6% 2.1% -15.3% -16.9% 2.05 2.07 0.26median -31.7% -31.5% -31.1% -34.4% -0.99 -0.03 1.00

1998 mean 26.1% 53.8% -3.8% 13.4% 4.41 2.75 -1.46median -24.6% -16.0% -31.6% -34.0% 3.55 2.34 -0.55

1999 mean -12.8% -24.0% 4.2% -6.8% -4.01 -2.03 1.07median -53.4% -58.4% -42.6% -53.4% -3.20 -0.56 1.62

2000 mean -23.6% -21.0% -27.4% -23.4% 1.92 0.60 -0.98median -43.6% -40.5% -47.6% -43.6% 1.99 0.61 -0.99

2001 mean 4.4% 1.8% 7.6% 2.8% -1.09 -0.17 0.87 median 9.5% 2.8% 20.6% 6.1% 1.10 -0.10 1.05

34

Notes:We report the yearly results using the year of the IPO. Excess returns (size adjusted mean and median buy-and-hold returns) are calculated for periods before, at, and after the buy or strong buy recommendation event date given by First Call for the 8,306 observations. The size adjustment is done by subtracting the buy-and-hold return from the appropriate value-weighted CRSP decile. We define “By Unaffiliated” as recommendations made by analysts from brokerage firms that were not lead or co-underwriter for the IPO. Affiliated Non-Lead recommendations are made by analysts from brokerage firms that were the co-underwriter for the IPO. Lead recommendations are made by analysts from brokerage firms that were the lead underwriter for the IPO. “Days after IPO date” is the number of calendar days between the IPO date and the recommendation date. The t-statistics use the pooled-variance in the excess returns and the z-statistics are calculated using the Wilcoxon ranked-sum test.

35

Table 5: Regression of excess returns before, at, and after analyst buy recommendations of IPO firms

Panel A: Lead vs. Non-Lead

Excess return, prior 30 days

Excess return, 3 day event

Excess return, event + 3 months

Excess return, event + 6 months

Excess return, event + 12 months

Coeff. t-stat Coeff. t-stat Coeff. t-stat Coeff. t-stat Coeff. t-statIntercept -1.73 -0.90 0.01 0.87 0.01 0.27 0.10 2.06 0.04 0.49LEAD -0.41 -0.50 -0.30 -0.68 0.02 0.02 -0.09 -0.05 -1.79 -0.58SIZE 1.36 5.10 0.05 0.43 1.35 2.84 1.40 2.12 3.08 3.09Time -0.02 -6.45 0.00 1.87 -0.03 -4.62 -0.04 -4.96 -0.01 -0.61Dearn 0.03 0.07DFirst 0.30 0.93 0.50 0.35 -2.07 -1.05 -2.29 -0.77LEAD*Time 0.00 -0.69Adj. Rsq 0.022 0.003 0.019 0.022 0.019

Panel B: Affiliated (Lead & Affiliated Non-Lead) vs. UnaffiliatedExcess return, prior 30 days

Excess return, 3 day event

Excess return, event + 3 months

Excess return, event + 6 months

Excess return, event + 12 months

Coeff. t-stat Coeff. t-stat Coeff. t-stat Coeff. t-stat Coeff. t-statIntercept -1.18 -0.58 0.01 0.87 0.01 0.27 0.10 2.06 0.04 0.49AFFILIATED -0.75 -0.92 -1.17 -2.54 -0.61 -0.41 0.53 0.26 -3.03 -0.97SIZE 1.35 5.07 0.04 0.33 1.34 2.81 1.41 2.14 3.06 3.07Time -0.02 -5.76 0.00 0.11 -0.03 -4.30 -0.04 -4.27 -0.01 -0.93Dearn 0.09 0.19DFirst 0.47 1.42 0.64 0.44 -2.20 -1.11 -1.96 -0.65AFFILIATED*Time 0.00 0.17Adj. Rsq 0.022 0.004 0.019 0.022 0.019

36

Panel C: Affiliated vs. Unaffiliated and Lead vs. Non-LeadExcess return, prior 30 days

Excess return, 3 day event

Excess return, event + 3 months

Excess return, event + 6 months

Excess return, event + 12 months

Coeff. t-stat Coeff. t-stat Coeff. t-stat Coeff. t-stat Coeff. t-statIntercept -1.15 -0.56 1.49 1.70 1.48 0.39 9.95 1.89 5.64 0.71LEAD -0.14 -0.16 -0.02 -0.04 0.28 0.17 -0.32 -0.15 -0.82 -0.25AFFILIATED -0.70 -0.79 -1.16 -2.35 -0.71 -0.45 0.64 0.29 -2.73 -0.82SIZE 1.35 5.05 0.03 0.32 1.34 2.82 1.41 2.13 3.05 3.05Time -0.02 -5.76 0.00 0.12 -0.03 -4.31 -0.04 -4.27 -0.01 -0.92Dearn 0.09 0.20DFirst 0.48 1.44 0.61 0.42 -2.16 -1.08 -1.88 -0.62LEAD*Time 0.00 -0.29AFFILIATED*Time 0.00 0.30Adj. Rsq 0.022 0.004 0.019 0.022 0.019

Variable Definitions:EXCESS RETURN: Size adjusted buy-and-hold returns are calculated for periods before, at, and after the buy or strong buy

recommendation event date given by First Call for the 8,306 observations. The size adjustment is done by subtracting the buy-and-hold return from the appropriate value-weighted CRSP decile.

LEAD: Indicator variable that takes on the value of one if the recommendation is from a lead analyst and zero otherwiseAFFILIATED: Indicator variable that takes on the value of one if the recommendation is from a lead or an affiliated non-lead

analyst and zero otherwiseSIZE: Log of the market capitalization at the end of the 25-day SEC quiet periodTIME: Number of days between the IPO and the recommendationDEarn: Indicator variable that takes on the value of one if an earnings announcement has occurred in the three days

around the recommendation date and zero otherwiseDFirst: Indicator variable that takes on the value of one if the recommendation is the first one to be issued and zero

otherwiseLEAD*TIME: Interaction term between LEAD and TIMEAFFILIATED*TIME: Interaction term between AFFILIATED and TIME

The models in Panels A, B and C are estimated using ordinary least squares with year and industry fixed effects.

37

Figure 1Cumulative mean size adjusted event return for firms receiving buy recommendations within one year of their IPO

conditional upon the source of the recommendation

-0.1

-0.075

-0.05

-0.025

0

0.025

0.05

0.075

0.1

-2 -1 0 1 2 3 4 5 6 7 8 9 10 11 12

Month

Bu

y-an

d-H

old

Cu

mu

lati

ve R

etu

rn

Unaffiliated Affiliated Non-Lead Lead Non-Lead

38