Embed Size (px)

Citation preview

The Pre-Great-Recession Slowdown in

Productivity Growth*

September 8, 2016

John G. Fernald

Federal Reserve Bank of San Francisco

Gilbert Cette and Benoit Mojon

Banque de France

* The views expressed here are our own and do not necessarily reflect the views of the Federal

Reserve Bank of San Francisco, the Banque de France, or anyone else associated with these

institutions

Diverging TFP performance 1995-2007

Source: Bergeaud, Cette, and Lecat 2015

Diverging TFP performance 1995-2007

Source: Bergeaud, Cette, and Lecat 2015

Diverging TFP performance 1995-2007

Source: Bergeaud, Cette, and Lecat 2015

Diverging TFP performance 1995-2007

• TOP DOWN/INDUSTRY

PERSPECTIVE

• U.S. Exceptional IT-fueled

1995-2004

• France/Germany Structural

rigidities

• Italy, Spain Rising

misallocation from capital

inflows

Source: Bergeaud, Cette, and Lecat 2015

Should same IT story apply equally everywhere?

• Not necessarily: Ideas flow across borders but have to be

implemented locally

– Timing of “intangible investments” (e.g., reorganizations

associated with IT) can differ

• Theory: Basu, Fernald, Oulton, Srinivasan (2003)

• Evidence: Corrado, Haskel, Jona-Lasinio, Iommi (2012)

Should same IT story apply equally everywhere?

• Not necessarily: Ideas flow across borders but have to be

implemented locally

– Timing of “intangible investments” (e.g., reorganizations

associated with IT) can differ

• Theory: Basu, Fernald, Oulton, Srinivasan (2003)

• Evidence: Corrado, Haskel, Jona-Lasinio, Iommi (2012)

• Industry data from EU-KLEMS

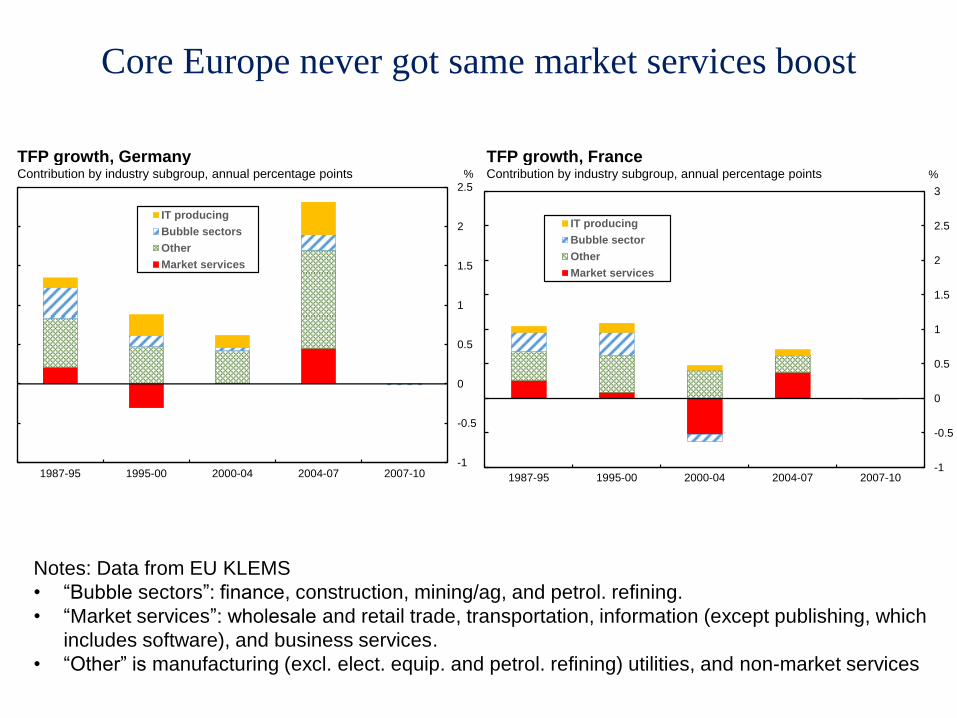

-1

-0.5

0

0.5

1

1.5

2

2.5

3

1987-95 1995-00 2000-04 2004-07 2007-10

IT producing

Bubble sector

Other

Market services

Contribution by industry subgroup, annual percentage points

TFP growth, France%

-1

-0.5

0

0.5

1

1.5

2

2.5

1987-95 1995-00 2000-04 2004-07 2007-10

IT producing

Bubble sectors

Other

Market services

Contribution by industry subgroup, annual percentage points

TFP growth, Germany%

Core Europe never got same market services boost

Notes: Data from EU KLEMS

• “Bubble sectors”: finance, construction, mining/ag, and petrol. refining.

• “Market services”: wholesale and retail trade, transportation, information (except publishing, which

includes software), and business services.

• “Other” is manufacturing (excl. elect. equip. and petrol. refining) utilities, and non-market services

Institutional barriers hold back continental Europe

• “Reallocations” and reorganizations that didn’t happen because

of labor and product market rigidities

• E.g., Van Reenen et al (2010), Bourlès, Cette, Lopez, Mairesse, and

Nicoletti (2013), Cette, Lopez, and Mairesse (2013)…

Diverging TFP performance 1995-2007

Source: Bergeaud, Cette, and Lecat 2015

-2.0

-1.5

-1.0

-0.5

0.0

0.5

1.0

1.5

2.0

1987-95 1995-00 2000-04 2004-07 2007-10

IT producing

Bubble sectors

Other

Market services

Contribution by industry subgroup, annual percentage points

TFP growth, Italy%

-2

-1.5

-1

-0.5

0

0.5

1

1.5

2

1987-95 1995-00 2000-04 2004-07 2007-10

IT producing

Bubble sectors

Other

Market services

Contribution by industry subgroup, annual percentage points

TFP growth, Spain%

“Great unlearning” in Spain and Italy

Notes: Data from EU KLEMS

• “Bubble sectors”: finance, construction, mining/ag, and petrol. refining.

• “Market services”: wholesale and retail trade, transportation, information (except publishing, which

includes software), and business services.

• “Other” is manufacturing (excl. elect. equip. and petrol. refining) utilities, and non-market services

Rising misallocation in peripheral Europe

E.g., Gopinath et al. (2015), Calligaris (2015), Garcia-Santana et. al. (2015)

Why did TFP in Southern Europe collapse?

Convergence of Euro nominal interest rates

0

2

4

6

8

10

12

14

16

18

20

1984 1987 1990 1993 1996 1999 2002 2005 2008 2011 2014

France

Germany

Italy

Spain

UK

10-year government bonds

Nominal interest ratesPercent

Convergence of Euro real interest rates

-4

-2

0

2

4

6

8

10

12

1984 1987 1990 1993 1996 1999 2002 2005 2008 2011 2014

France

Germany

Italy

Spain

UK

10-year gov. bond rate less 4-quarter percent change in GDP deflator

Real interest ratesPercent

16

-4

-2

0

2

4

6

8

10

12

1984 1987 1990 1993 1996 1999 2002 2005 2008 2011 2014

France

Germany

Italy

Spain

UK

10-year gov. bond rate less 4-quarter percent change in GDP deflator

Real interest ratesPercent

Real interest rates fell more in periphery

17

Real interest rates fell more in southern Europe

-4

-2

0

2

4

6

8

10

12

1984 1987 1990 1993 1996 1999 2002 2005 2008 2011 2014

France

Germany

Italy

Spain

UK

10-year gov. bond rate less 4-quarter percent change in GDP deflator

Real interest ratesPercent

18

Non-fin. corporate debt rose rapidly in Spain and Italy

30

40

50

60

70

80

90

100

110

120

1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014

United States

United Kingdom

Euro Area

Germany

France

Italy

Spain

Source:

Annual data

Non-Financial Companies' Debt as a Share of GDP%

Rising misallocation in peripheral Europe

E.g., Gopinath et al. (2015), Calligaris (2015), Garcia-Santana et. al. (2015)

Why did TFP in Southern Europe collapse?

Rising misallocation in peripheral Europe

E.g., Gopinath et al. (2015), Calligaris (2015), Garcia-Santana et. al. (2015)

Reis (2013), Gopinath et al. (2015), model capital inflows interacting

with financial frictions

Funds flow to less productive projects

E.g., large borrowers rather than productive ones

Increasing misallocation

Macro implication: Exogenous decline in real interest rates leads to low

productivity growth

Channel: Low-productivity firms get financed. Average productivity of firms falls.

Why did TFP in Southern Europe collapse?

Rising misallocation in peripheral Europe

E.g., Gopinath et al. (2015), Calligaris (2015), Garcia-Santana et. al. (2015)

Reis (2013), Gopinath et al. (2015), model capital inflows interacting

with financial frictions

Funds flow to less productive projects

E.g., large borrowers rather than productive ones

Increasing misallocation

Macro implication: Exogenous decline in real interest rates leads to low

productivity growth

Channel: Low-productivity firms get financed. Average productivity of firms falls.

=>VAR with labor productivity (or TFP growth) and real interest rates

Choleski identification with real interest rate last

Why did TFP in Southern Europe collapse?

Real interest rate “shock” raises labor productivity (Euro area)

Historical decomposition:

“Explains” some low periphery lab. prod. growth

Takeaways

• TFP growth in many advanced economies slowed prior to

Global Financial Crisis

– Negative TFP growth in periphery

• Factors: Technology, structural rigidities, and capital flows

– Challenge: Reforms work with long, uncertain lags

• Future is highly uncertain.

– Flexibility needed to advance/keep up with frontier

– Strong safety net needed to deal with individual risks

28

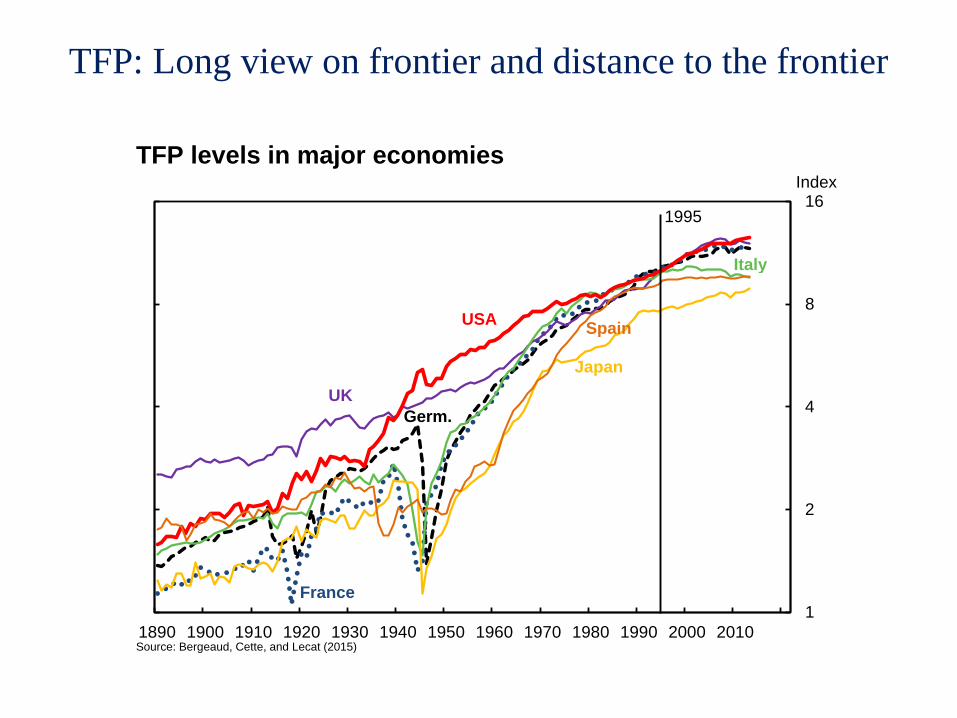

TFP: Long view on frontier and distance to the frontier

1

2

4

8

16

1890 1900 1910 1920 1930 1940 1950 1960 1970 1980 1990 2000 2010Source: Bergeaud, Cette, and Lecat (2015)

TFP levels in major economiesIndex

Germ.

France

UK

Italy

Japan

USASpain

1995

United States: The exceptional 1995-03 period

Rise and fall of TFP growth in IT-intensive market services

-0.5

0

0.5

1

1.5

2

2.5

1987-95 1995-00 2000-04 2004-07 2007-13

Contribution by industry subgroup, annual percentage points

Business-sector TFP growth, United StatesPercentage points

IT producing

Bubble sectors

Other

Market services

Notes: Data from BLS

• “Bubble sectors”: finance, construction, mining/ag, and petrol. refining.

• “Market services”: wholesale and retail trade, transportation, information (except publishing,

which includes software), and business services.

• “Other” is manufacturing (excl. elect. equip. and petrol. refining) utilities, and non-mkt. services

-0.5

0

0.5

1

1.5

2

2.5

1987-95 1995-00 2000-04 2004-07 2007-13

Contribution by industry subgroup, annual percentage points

Business-sector TFP growth, United StatesPercentage points

IT producing

Bubble sectors

Other

Market services

Rise and fall of TFP growth in IT-intensive market services

IT production had

late 1990s bulge

Notes: Data from BLS

• “Bubble sectors”: finance, construction, mining/ag, and petrol. refining.

• “Market services”: wholesale and retail trade, transportation, information (except publishing,

which includes software), and business services.

• “Other” is manufacturing (excl. elect. equip. and petrol. refining) utilities, and non-mkt. services

-0.5

0

0.5

1

1.5

2

2.5

1987-95 1995-00 2000-04 2004-07 2007-13

Contribution by industry subgroup, annual percentage points

Business-sector TFP growth, United StatesPercentage points

IT producing

Bubble sectors

Other

Market services

Rise and fall of TFP growth in IT-intensive market services

Market services had

2000-04 burst

(wholesale/retail trade,

info services, business

services)

Notes: Data from BLS

• “Bubble sectors”: finance, construction, mining/ag, and petrol. refining.

• “Market services”: wholesale and retail trade, transportation, information (except publishing,

which includes software), and business services.

• “Other” is manufacturing (excl. elect. equip. and petrol. refining) utilities, and non-mkt. services

Rise and fall of TFP growth in IT-intensive market services

-0.5

0

0.5

1

1.5

2

2.5

1987-95 1995-00 2000-04 2004-07 2007-13

Contribution by industry subgroup, annual percentage points

Business-sector TFP growth, United StatesPercentage points

IT producing

Bubble sectors

Other

Market services

Notes: Data from BLS

• “Bubble sectors”: finance, construction, mining/ag, and petrol. refining.

• “Market services”: wholesale and retail trade, transportation, information (except publishing,

which includes software), and business services.

• “Other” is manufacturing (excl. elect. equip. and petrol. refining) utilities, and non-mkt. services

Post-2004 slowdown

fairly broadbased

Rise and fall of TFP growth in IT-intensive market services

-0.5

0

0.5

1

1.5

2

2.5

1987-95 1995-00 2000-04 2004-07 2007-13

Contribution by industry subgroup, annual percentage points

Business-sector TFP growth, United StatesPercentage points

IT producing

Bubble sectors

Other

Market services

Notes: Data from BLS

• “Bubble sectors”: finance, construction, mining/ag, and petrol. refining.

• “Market services”: wholesale and retail trade, transportation, information (except publishing,

which includes software), and business services.

• “Other” is manufacturing (excl. elect. equip. and petrol. refining) utilities, and non-mkt. services

Why did continental Europe diverge?

Source: Bergeaud, Cette, and Lecat 2015