Embed Size (px)

Citation preview

The price of energy security in depressed electricity markets;

the case of Belgium

Prof.Dr. Johan AlbrechtFaculteit Economie & Bedrijfskunde

Second Summer School Economics of Electricity Markets 28/08/2014

Structure• The Belgian context• ‘Security of supply’ has two dimensions: follow peak

demand & avoid excessive overproduction (intermittent RES)

• ‘No Policy’ scenario; not sustainable• ‘Security of supply’ scenarios ; new assets, old

thermal assets, DSM & combinations• Surplus risk assessment• Conclusions

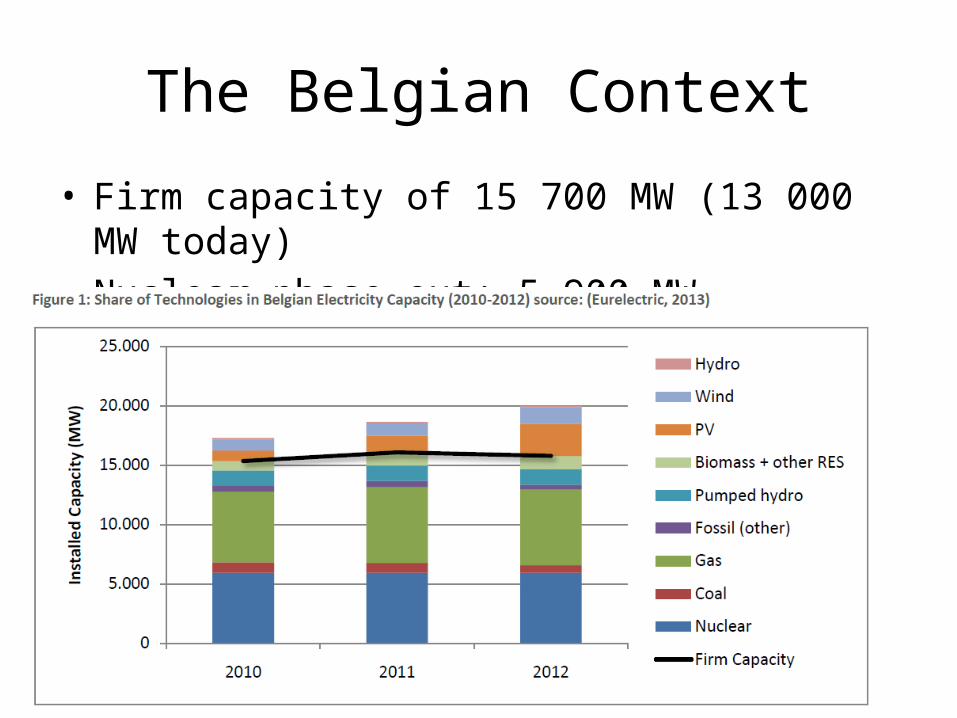

The Belgian Context

• Firm capacity of 15 700 MW (13 000 MW today)• Nuclear phase-out: 5 900 MW

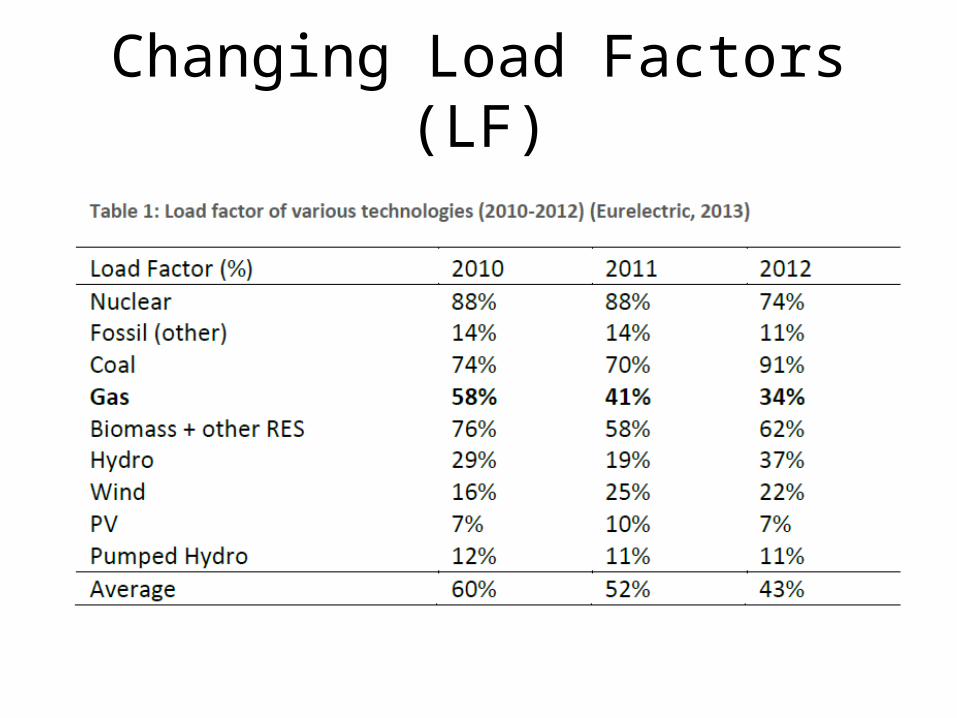

Changing Load Factors (LF)

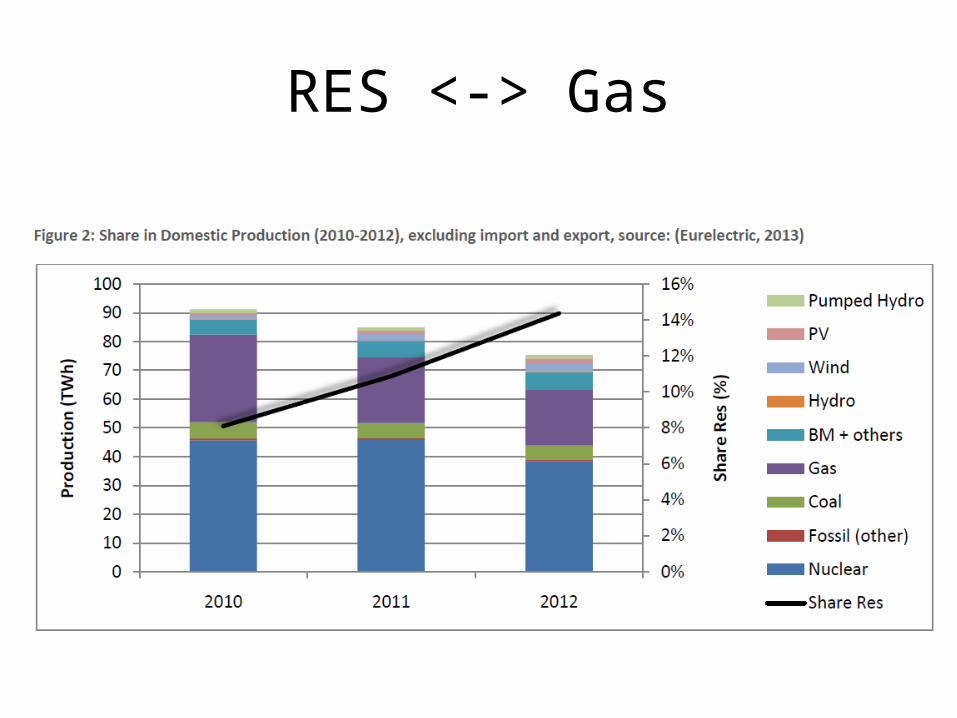

RES <-> Gas

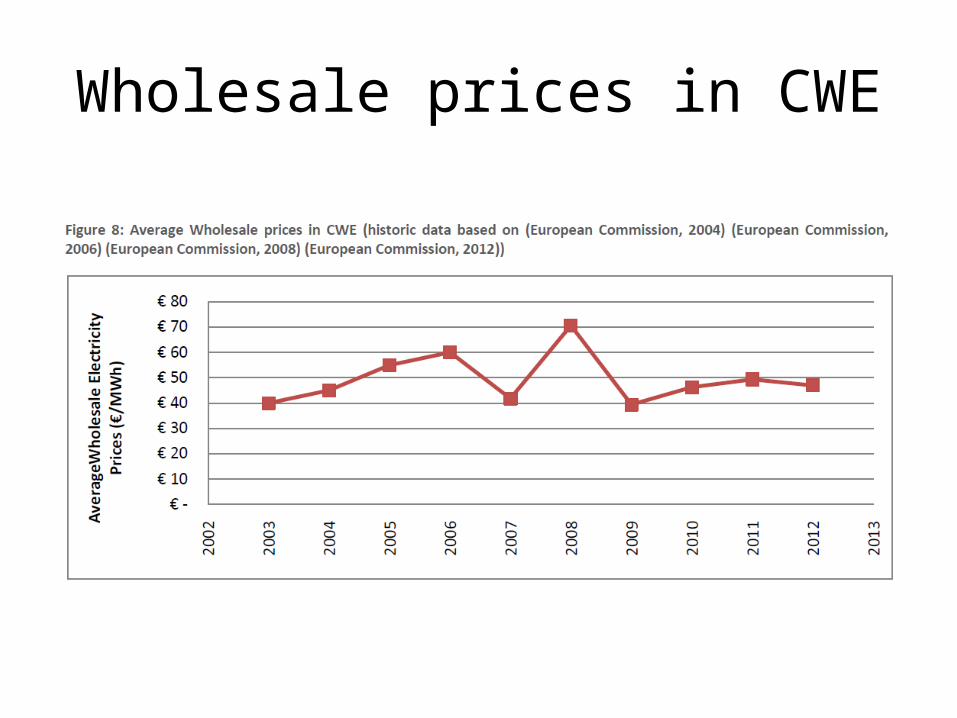

Wholesale prices in CWE

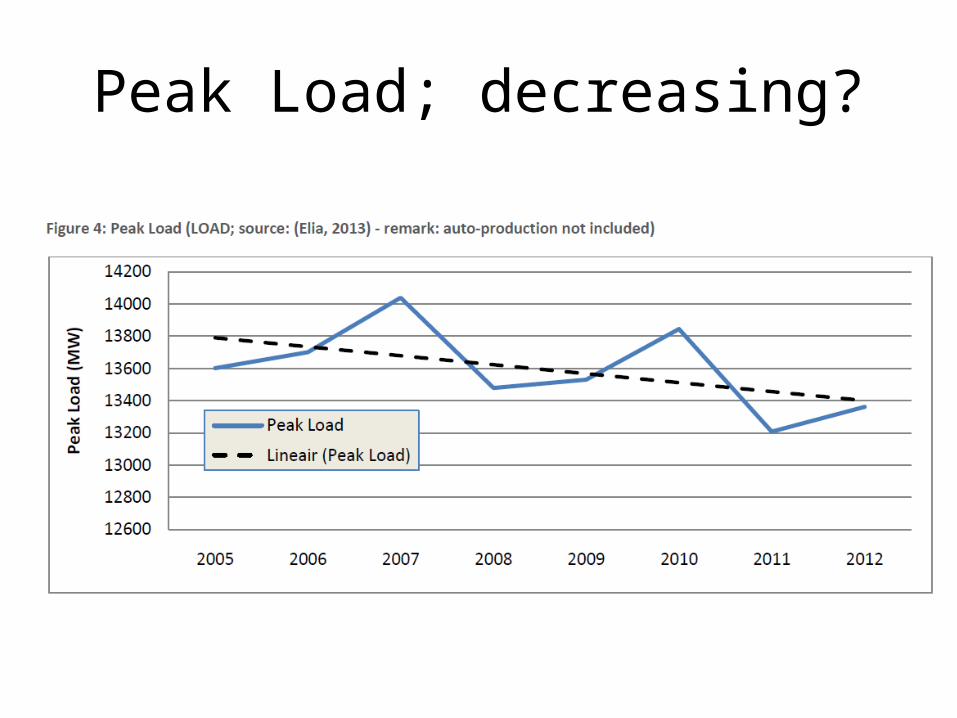

Peak Load; decreasing?

Plan Wathelet

• Extension Tihange 1, 800 MW CCGT, 400 MW DSM

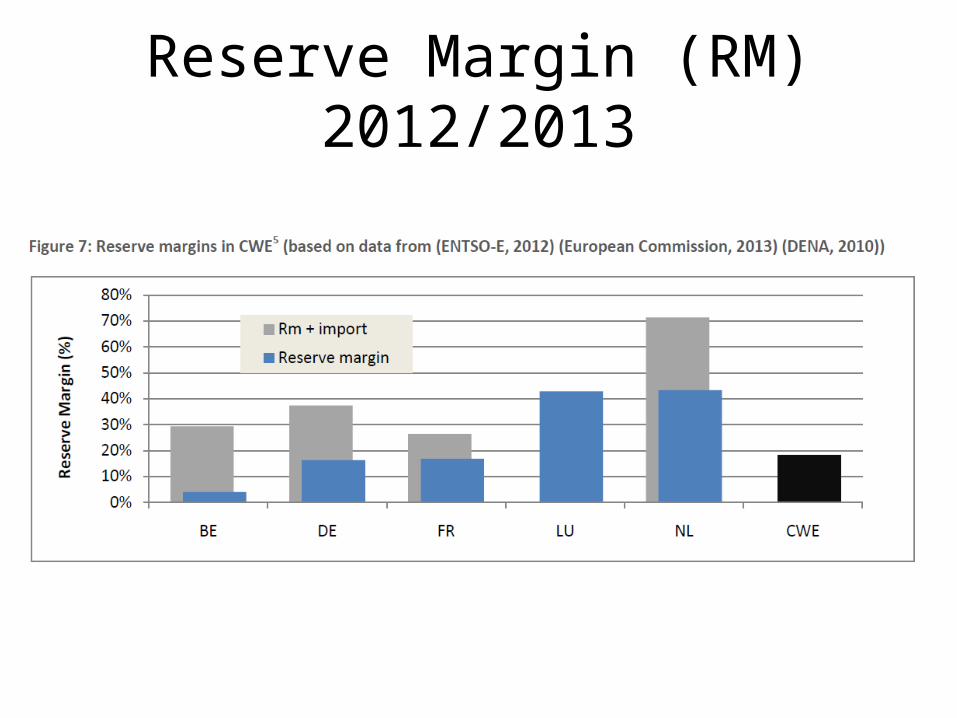

Reserve Margin (RM) 2012/2013

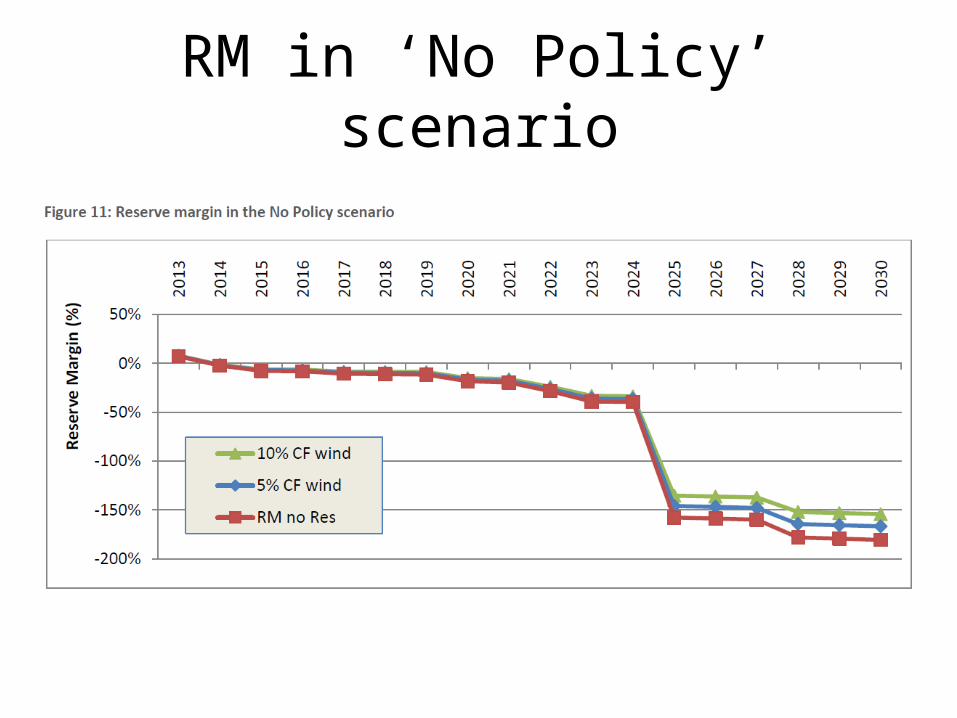

RM in ‘No Policy’ scenario

Supply scenarios for Belgium

• Policy options; incentives for flexible generation (new and old termal), DSM, CFD for RES (with/without Market Participation (MP))

• Investment and system cost of policy options? (with 8% discount rate, LCOE-approach)

• Assumptions on context; peak demand + 0,5%/yr, carbon price up to € 40 per ton CO2 in 2030, endogenous price model (more RES -> lower wholesale prices), network costs increase with RES share

LCOE assumptions

Endogenous price model

Prices in NEA for DE

Network costs as f(RES)

Security of supply; RM > 5% at all times• IF (‘No Policy’ RM < 5%) THEN model triggers CCGT,

OCGT & Biomass investments• Context: old thermal, DSM, BAU RES and High RES

New capacity; split up

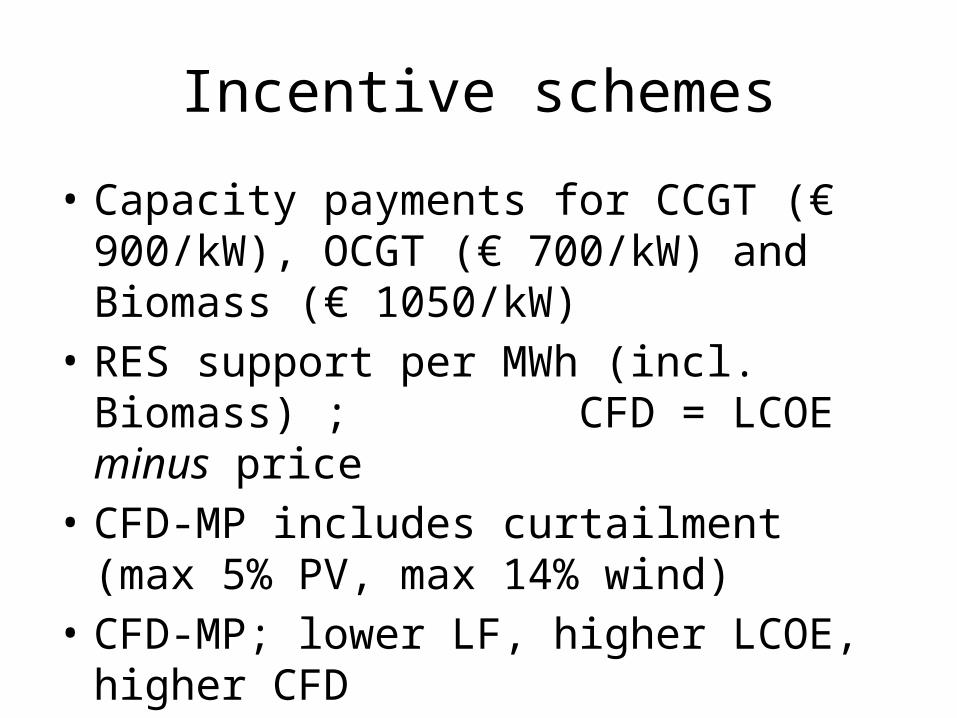

Incentive schemes

• Capacity payments for CCGT (€ 900/kW), OCGT (€ 700/kW) and Biomass (€ 1050/kW)

• RES support per MWh (incl. Biomass) ; CFD = LCOE minus price

• CFD-MP includes curtailment (max 5% PV, max 14% wind)

• CFD-MP; lower LF, higher LCOE, higher CFD

Old Thermal & DSM• end of 1 300 MW OT scheduled for 2014-2024; in

reserve capacity, 5% LF @ € 95/MWh (€ 50 to 60 mill)• DSM clearing prices of € 150/MW/day (based on UBS)

Firm capacity in 2030; 18 GW / RM 9%

Peak demand of 14,7 GW in 2030Gas dominates / old thermal; end of life in 2024Biomass; 3 000 – 3 500 MW in BAU RES / 4 000 – 4 500 MW in High RES

Total capacity in 2030; 25 – 30 GW

Electricity production in 2030

CFD-MP; Biomass used in flexible way -> higher LF for CCGTShare of RES in 2030: from 28% in BAU RES CFD-MP to 60% in High RES CFD

Generation portfolio LF

WP Bureau Fédéral du Plan, 2013

Annual subsidy cost: cap pay + CFD• All results: additional to subsidy cost of 2014• One-off capacity payments in year of investment

Cumulative cost up to 2030; € 21 and € 41 bill-> MP of RES matters!

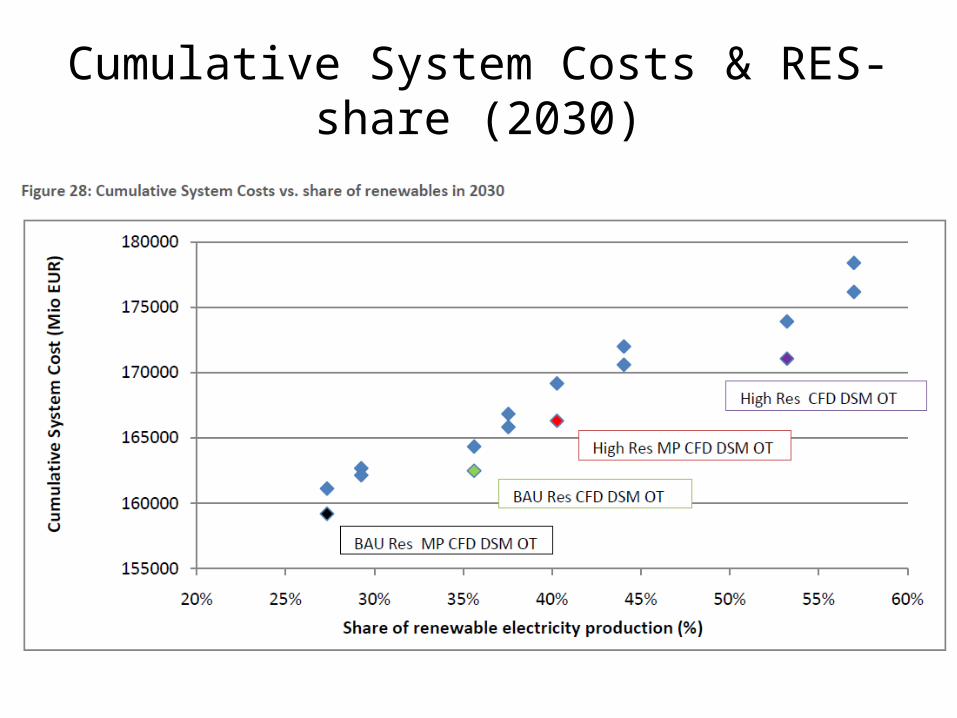

Optimal frameworks and RES share?

• Trade-off between RES share and costs is not linear

LCOE generation mix, 2012-2030

Total annual system costs (gen+netw)

Total costs and RES share

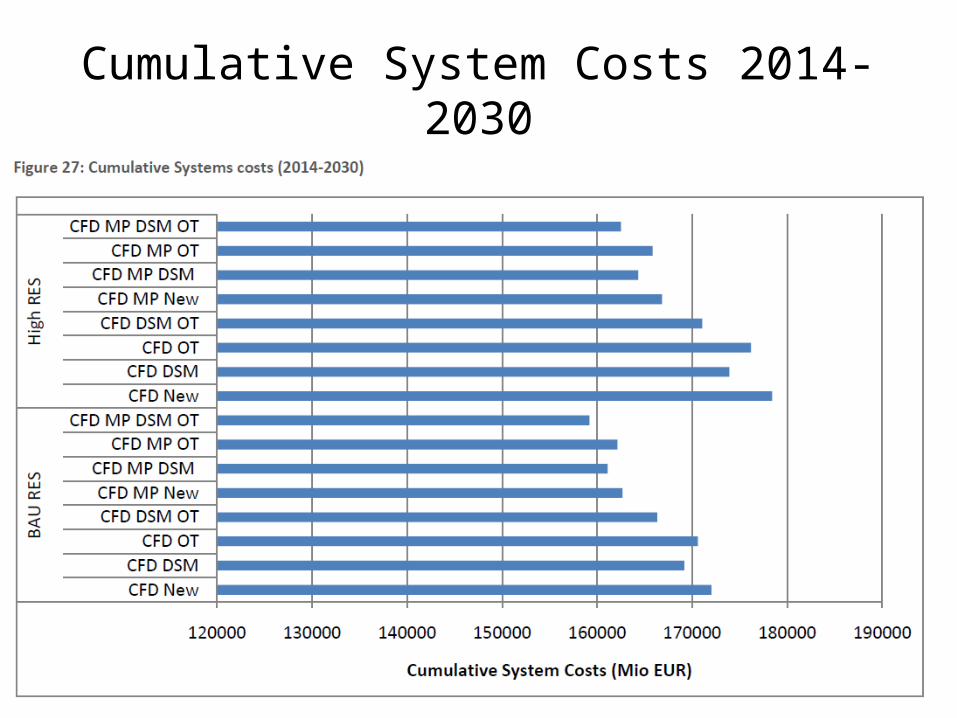

Cumulative System Costs 2014-2030

Cumulative System Costs & RES-share (2030)

Cumulative Subsidy Costs & Cumulative System Costs (2014-2030)

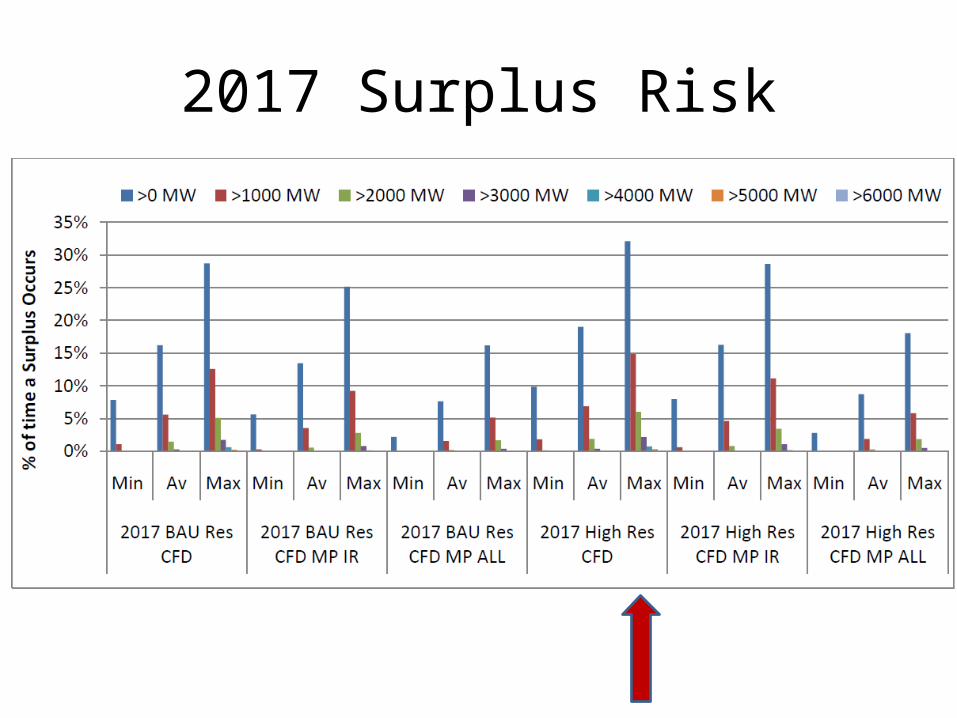

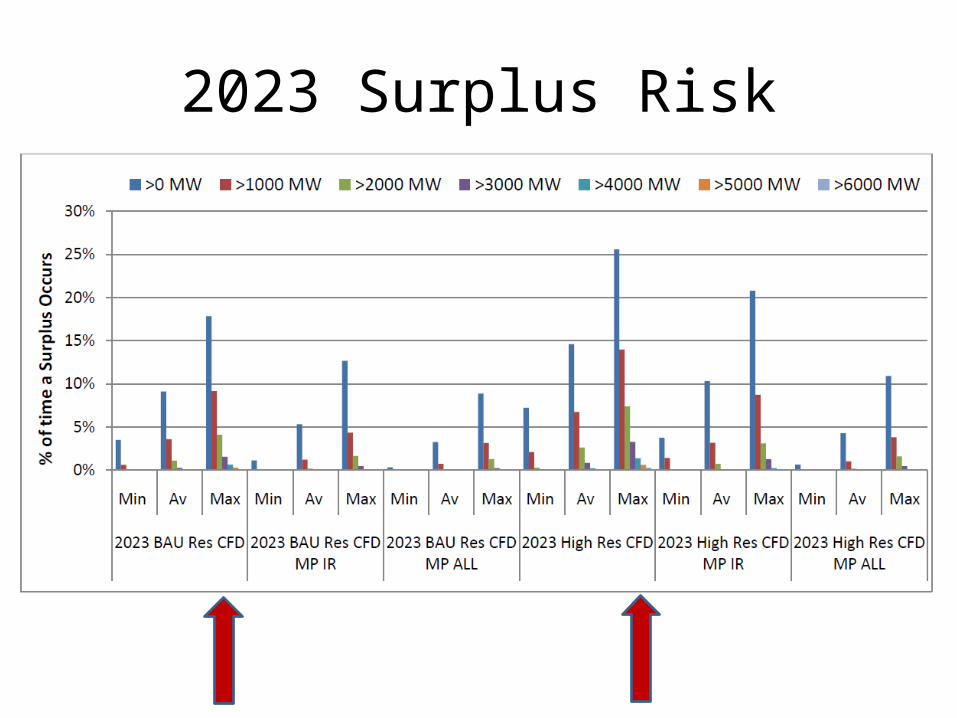

Surplus risks?• Only with ‘New Capacity’ scenarios• Random PV & wind generation in Matlab (10 000

patterns), based on Elia • ‘Must-run’; biomass (MP), CHP & nuclear• Compared to demand variation in 15 min intervals• Demand (15 min) <-> (RES + Must Run)• Export capacity of 3 500 MW; surplus of 3 000 is

problematic• DSM (to increase demand); here not included

Illustration of PV+wind output for 29 days

2014 Surplus Risk

2017 Surplus Risk

2023 Surplus Risk

2027 Surplus Risk

Overview Surplus Analysis

Nuclear prolongation; 3 GW NUC in 2030

Conclusions 1

Conclusions 2• To secure 5% RM, cumulative subsidy costs up to 2030

vary between € 21 and € 41 billion• Smart policy choices will lower costs for society, even at

relatively high RES shares• Market participation by RES is essential to facilitate

further expansion of RES• DSM lowers costs / Old thermal; limited relevance• limitations of this analysis; capacity payments as

institutional challenge (end of EOM?), recovery of demand, delocalisation energy-intensive industries, evolution of interconnection, arrival of smart grid, share of electric vehicles by 2030, EC climate policies,…

Thank you for your attention

• [email protected]• Second Summer School ‘Economics of Electricity

Markets’ @ Ghent University, August 25-29, 2014• http://

www.ceem.ugent.be/SummerSchools/2014/index.htm