Embed Size (px)

Citation preview

APPROVED: Mazhar Siddiqi, Major Professor James Conover, Committee Member Imre Karafiath, Committee Member Robert Pavur, Committee Member Niranjan Tripathy, Committee Member Marcia Staff, Chair, Department of

Finance, Insurance, Real Estate and Law

O. Finley Graves, Dean of the College of Business

James D. Meernik, Acting Dean of the Robert B. Toulouse School of Graduate Studies

THE REASONS FOR THE DIVERGENCE OF IPO LOCKUP AGREEMENTS

Fei Gao, B.A., M.B.A.

Dissertation Prepared for the Degree of

DOCTOR OF PHILOSOPHY

UNIVERSITY OF NORTH TEXAS

August 2010

Gao, Fei. The reasons for the divergence of IPO lockup agreements. Doctor of

Philosophy (Finance), August 2010, 107 pp., 22 tables, 1 figure, references, 61 titles.

Most initial public offerings (IPOs) feature share lockup agreements, which

prohibit insiders from selling their shares for a specified period of time following the IPO.

However, some IPO firms agree to have a much longer lockup period than other IPO

firms, and some are willing to lockup a much larger proportion of shares. Thus, the

primary research question for this study is: “What are the reasons for the divergence of

the lockup agreements?”

The two main hypotheses that this dissertation investigates are the signaling

hypothesis based on information asymmetry, and the commitment hypothesis based on

agency theory. This study uses methods that have not been applied by previous studies

in the literature relating to IPO lockups.

First, I directly use IPO firms operating performance as a proxy for firm quality.

The results show neither a negative nor a strong positive relationship between lockup

length and firm operating performance. Thus, based on operating performance, the

evidence does not support the agency hypothesis while showing weak support for the

signaling hypothesis.

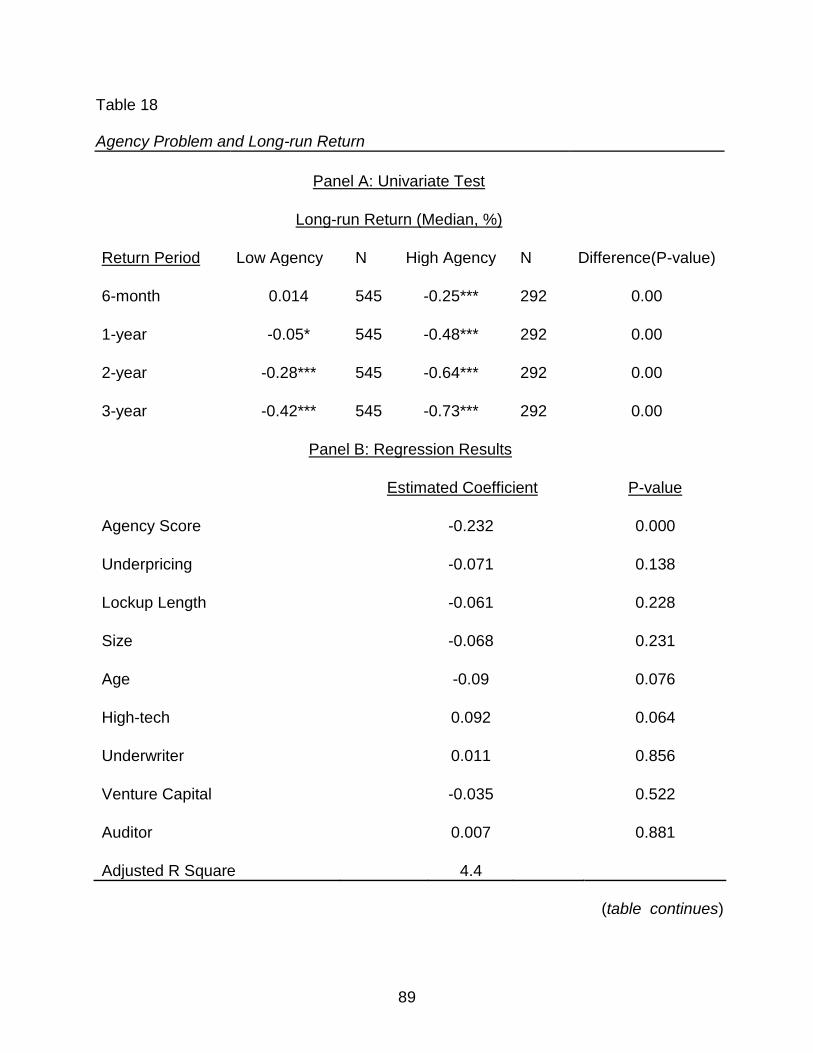

I then examine the long-run returns for IPO firms with different lockup lengths. I

find that firms with short lockup lengths have much better long-run returns than firms

with long lockup lengths. Therefore, the results reject the signaling hypothesis while

supporting the agency hypothesis. This dissertation further contributes to the IPO long-

run underperformance literature by showing that firms with a high agency problem have

much worse long-run returns than those with a low agency problem.

Finally, I investigate the short-term stock returns around lockup expiry. Generally,

I find that firms with short lockup periods experience better stock returns around lockup

expiry than firms with long lockup periods, though the returns are not significantly

different from one another. Overall, I conclude that the results reject the signaling

hypothesis while partially supporting the agency hypothesis. In addition, I show that

firms with high agency problems have much worse stock returns than those with low

agency problems around lockup expiry, even though the agency variable is not

significant in the regression analysis.

ii

Copyright 2010

by

Fei Gao

iii

ACKNOWLEDGMENTS

I wish to express my deepest gratitude to Dr. Mazhar Siddiqi, my Committee

Chairperson, whose guidance and patience make this dissertation possible. I also want

to thank Dr. James Conover, Dr. Imre Karafiath, Dr. Robert Pavur, and Dr. Niranjan

Tripathy, my committee members, and Dr. John Kensinger, for their contributions. Their

insights and discussions were essential for improving the dissertation.

I would like to thank my wife for her tremendous support and encouragement.

iv

TABLE OF CONTENTS

Page

ACKNOWLEDGMENTS………………………………………………………………………..iii

LIST OF TABLES……………………………………………………………………………….v

LIST OF FIGURES……………………………………………………………………….........vi

Chapters

1. INTRODUCTION…………………………………………………………………………1

2. LITERATURE REVIEW………………………………………………………………….5

IPO Underpricing…………………………………………………………………. 5 IPO Long-run Underperformance………………………………………………10 IPO Lockup Agreement……………………………………………………….. 16

3. HYPOTHESIS DEVELOPMENT………………………………………………………27

Signaling Hypothesis…………………………………………………………….27 Agency Hypothesis………………………………………………………………30

4. DATA COLLECTION AND RESEARCH DESIGN…………………………………..35

Signaling Hypothesis…………………………………………………………….35 Agency Hypothesis………………………………………………………………43

5. EMPIRICAL RESULTS………………………………………………………………...50

Summary Statistics……………………………………………………………....50 Signaling Hypothesis…………………………………………………………….51 Agency Hypothesis………………………………………………………………58

6. CONCLUSION AND DISCUSSION…………………………………………………99

REFERENCES…………………………………………………………………………….....

v

LIST OF TABLES

Page

1. Comparisons for the Predictions of Hypotheses…………………………………...34

2. Summary Statistics…………………………………………………………………....64

3. Accounting Numbers and Lockup Length…………………………………………..66

4. Regression for Length of Lockup (OLS)…………………………………………….68

5. Regression for Length of Lockup -- Binary Logistic……………………………….69

6. Regression for Length of Lockup -- Multinomial Logistic…………………………70

7. Accounting Numbers and Lockup Length -- Opaque Firms………………………72

8. Regression for Length of Lockup -- Opaque Firms………………………………..74

9. Accounting Numbers and Lockup Length -- High-tech Firms……………………76

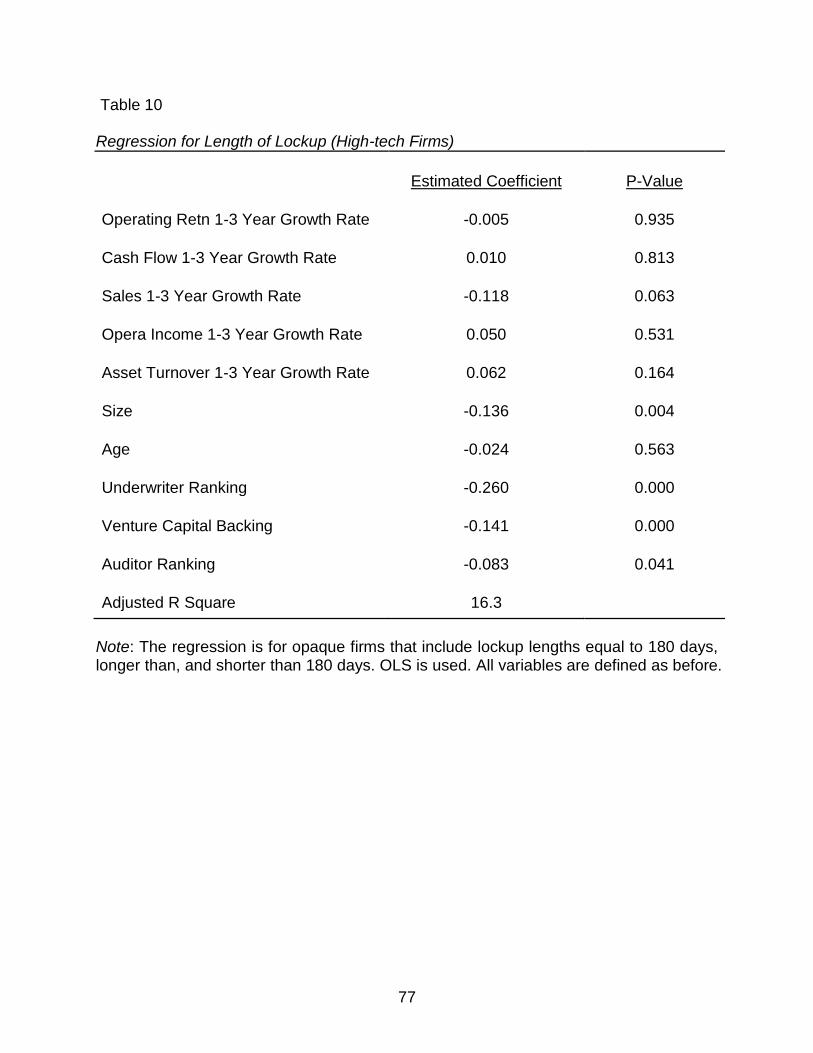

10. Regression for Length of Lockup (High-tech Firms)………………………………77

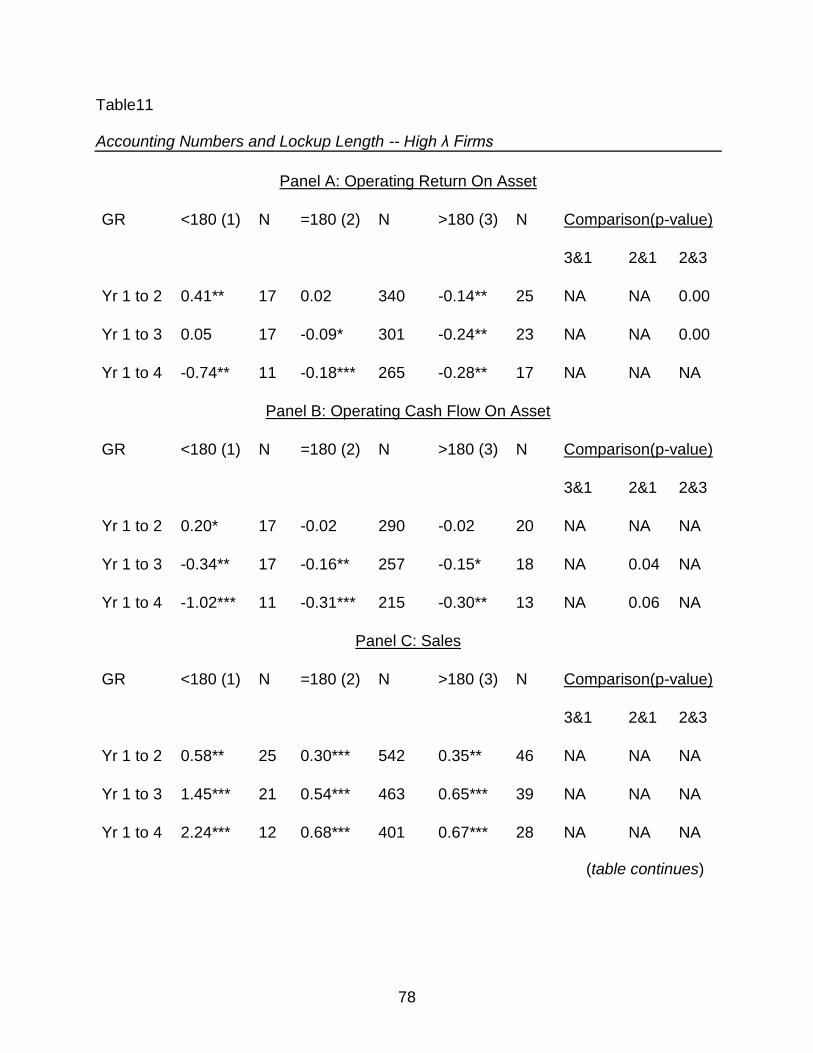

11. Accounting Numbers and Lockup Length -- High λ Firms………………………..78

12. Regression for Length of Lockup -- high λ…………………………………………80

13. Accounting Numbers and Lockup Length -- Low λ Firms…………………………81

14. Regression for Length of Lockup (Low λ)………………………………………….83

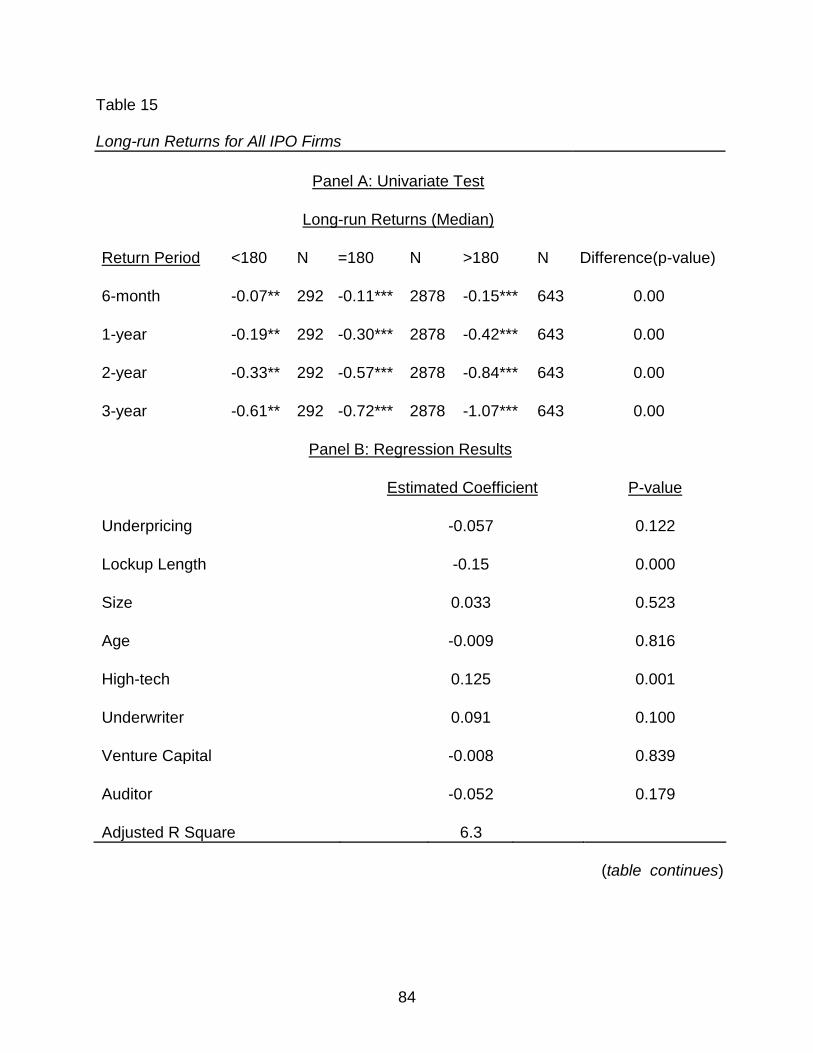

15. Long-run Returns for All IPO Firms…………………………………………………84

16. Abnormal Return around Lockup Expiry……………………………………………86

17. Percentage of Shares Locked……………………………………………………….88

18. Agency Problem and Long-run Return……………………………………………..89

19. Long-run Returns and Underwriter Reputation……………………………………91

20. Venture Capital Backing and Long-run Returns…………………………………..93

21. Auditor Reputation and Long-run Return………………………………………….94

22. Short-run Return and Agency Problem……………………………………………96

vi

LIST OF FIGURES

Page

1. Long-run Return for IPO Firms………………………………………………………97

1

CHAPTER 1

INTRODUCTION

When investment banks take a firm to an initial public offering (IPO), they sign an

underwriter agreement. This contract usually states that without the investment bank‟s

prior written consent, the issuer will not directly or indirectly sell any shares of common

stock for a certain period of time negotiated by the two parties following the public

offering of the stock. Such a contract is known as a share lockup agreement. Most

firms issuing IPOs voluntarily enter into a lockup agreement with their underwriters,

though the contract is not regulated by the Security and Exchange Commission. A

typical lockup lasts for 180 days, and the lockup agreement covers most of the shares

that are not sold in the IPO. The terms of the lockup and its expiration date are

disclosed in the IPO prospectus.

Some IPO firms agree to lockup their shares for a much longer period than other

firms, and some firms lockup more of their shares in the lockup agreement than other

firms. The research interest for this study is to explore the reasons for the divergence of

IPO lockup agreements. Several researchers have examined this topic, and they

approach the issue from two aspects. One aspect is the signaling hypothesis based on

information asymmetry. Courteau (1995) extends Leland and Pyle‟s (1977) signaling

model that focuses on retained ownership by introducing the length of lockup period to

which the owner commits in the prospectus as a signal of firm value. She develops a

model and shows that higher quality firms are more likely to have longer lockups as an

indication of their superior quality. Brav and Gompers (2003) test the signaling

hypothesis developed by Courteau by choosing IPO offer price revision, the probability

of dividend initiation, and frequency of seasoned equity offering (SEO) as measures of

2

firm quality. Their results reject the signaling hypothesis for lockups -- they do not find

that higher quality firms have longer lockup periods. However, Brau, Lambson, and

McQueen (2005) argue that the proxies for firm quality used in Brav et al. (2003) paper

are not appropriate.

Brau et al. (2005) present a theoretical model that shows how the incentives of

insiders, underwriters, and investors can interact with the nature of the firm‟s assets to

explain the existence of lockup agreements. Their results show that larger firms, older

firms, easy to value firms, firms with prestigious investment bankers, firms with venture

capital backing, and firms with well-known auditors have shorter lockup lengths.

However, their empirical evidence indicates only that lockups should be shorter when

the degree of asymmetric information is small. The authors, however, have not shown

that lockup length is a signal for firm quality, which is the main prediction of the signaling

hypothesis by Courteau (1995).

The second way to approach the lockup agreement issue is the commitment

hypothesis based on agency theory. Using Jensen and Meckling‟s (1976) theoretical

model of agency costs, Brav et al. (2003) argue that lockup agreements serve as a

commitment device to alleviate moral hazard problems. As a result, IPOs that have a

higher chance of experiencing agency problems should commit to longer lockup periods

during which the public is convinced to buy their stocks. Brav et al. empirical results

support the commitment hypothesis. But in their paper, the authors use variables of

information asymmetry to test agency hypothesis. For example, they find that smaller

firms, which have high information asymmetry, have longer lockup periods that they

attribute to a higher potential for an agency problem. However, this is not necessarily

3

the case. Insiders of small firms may work hard, while insiders of big firms may be more

likely to take advantage of outside shareholders.

I use different approaches from the papers discussed to test the signaling and

agency hypotheses. First, I directly use firm operating performance several years after

their IPO as a measure of firm quality as in Jain and Kini (1994) and in Zheng and

Stangeland (2007). Then I compare the operating performance for IPOs with long and

short lockup periods to determine whether there is a significant difference between the

two groups. According to the signaling hypothesis, long lockup IPOs, which have higher

quality, should have better operating performance after their offering compared to short

lockup IPOs, which have low quality. On the other hand, according to the agency

hypothesis, firms with longer lockup periods, which have a high agency problem, should

have worse operating performance after their IPO because of their high agency cost

compared to firms with short lockup periods, which have low agency cost.

Second, I investigate the long-run stock returns for IPO firms with different lockup

lengths. According to the signaling hypothesis, firms with longer lockup periods should

have higher quality than firms with shorter lockup periods. However, the information of

the quality of firms imbedded in the length of lockup should be priced into the offer price

of the IPO firms at the time of offerings. Therefore, the long-run returns of the firms with

long and short lockup periods should not be significantly different. Under a signaling

mechanism, only if investors consistently overestimate quality will long-run returns be

worse for longer lockups than shorter lockups. According to the agency hypothesis, in

order to attract investors to buy into their firms‟ shares, companies with a high agency

problem should have a longer lockup period than firms with a low agency problem. This

4

high agency cost will lead to poorer long-run returns for these firms with long lockup

periods compared to firms with short lockup periods.

Third, I examine the short-run stock returns around the lockup expiration date for

IPO firms with long and short lockup lengths. Since all the information about lockup

lengths should be priced into the stock at the time of IPO and since the expiration date

is known to public investors before IPO, there should be no short-run abnormal returns

for firms with long and short lockup lengths according to the signaling hypothesis.

According to the agency hypothesis, on the other hand, insiders of IPO firms may sell

their shares and start to cause an agency problem after lockup expiry. In order not to be

taken advantage of by insiders, investors who hold stocks of firms that have a high

potential for an agency problem will sell their holdings around lockup expiry, leading to

short-term negative returns for these stocks.

In the above mentioned tests, I primarily focus on the firms with short and long

lockup periods: those firms with lockup lengths shorter and longer than 180 days.

However, 75% of the firms in the sample have a lockup period that is exactly 180 days.

In order to investigate why the majority of IPO firms choose 180 days as their lockup

period, I run the multinomial logistic regression, comparing the characteristics of firms

with lockup periods equal to 180 days to those with lockup periods that are shorter and

longer than 180 days.

The remainder of the dissertation is organized as follows: Chapter 2 provides the

literature review. Chapter 3 develops the hypotheses. Chapter 4 discusses the data

collection and research design. Chapter 5 presents the results and chapter 6 concludes.

5

CHAPTER 2

LITERATURE REVIEW

Initial public offerings (IPOs) have attracted much attention from researchers in the

last two decades. Theoretical and empirical literature on IPO-related phenomenon is

extensive. I focus on several main issues of IPOs in this literature review.

IPO Underpricing

Underpricing is the first documented anomaly in the pricing of IPOs of common

stock. It refers to the systematic increase from the offer price to the first day closing

price for firms issuing IPOs. Some early studies documenting positive initial returns

include Ibbotson (1975), Ritter (1984), and Tinic (1988). In a sample of 6,249 IPOs from

1980 to 2001, Ritter and Welch (2002) show that the average first-day return is 18.8%.

Researchers have offered several possible explanations for this short-run IPO

underpricing.

Rock (1986) proposes the winner‟s curse hypothesis. He offers an equilibrium

model in which uninformed investors face a winner‟s curse when they submit an order

for IPO issues because some potential subscribers have superior information. Informed

investors do not subscribe to a new issue when it is priced above its value, leaving the

entire issue to uninformed investors. His model shows that this information asymmetry

may lead to a “lemons problem,” where uninformed investors end up primarily with the

less successful IPOs. Thus, firms are forced to underprice their IPOs in order to

compensate uninformed investors for this adverse selection. Beatty and Ritter (1986)

extend the model to show that the value of information and the necessary underpricing

are higher for issues in which there is greater uncertainty about their value. Michaely

and Shaw (1994) test the empirical implications of the winner‟s curse hypothesis, and

6

consistent with this hypothesis, find that IPOs are not underpriced in markets where

investors know a priori that they do not need to compete with informed investors.

Based on Rock‟s framework, Carter and Manaster (1990) investigate the role of an

investment banker‟s reputation in the IPO market. They show that to maintain their

reputation, prestigious underwriters always choose higher quality and less risky firms,

using information unavailable to the general public. This in turn reduces the uncertainty

and information asymmetry between informed and uninformed investors. Investors

know that by buying IPOs associated with high reputable underwriters, they face less

risk. Using investment bankers‟ capital as a proxy for underwriter reputation, Michaely

and Shaw (1994) show that reputation plays an important role in explaining the initial

day return; that is, IPOs underwritten by reputable investment banks experience less

underpricing.

Because most firms that go public are relatively young and new to general

investors, there are always information asymmetry problems between IPO firms and

outside investors. Welch (1989) presents a signaling model in which high-quality firms

underprice more at the IPO in order to obtain a higher price at a seasoned offering. Low

quality firms cannot imitate high quality firms by having greater underpricing because of

high imitation expenses and the possibility that this imitation is discovered between

offerings. Underpricing by high-quality firms can add sufficient imitation expenses to

induce low-quality firms to reveal their true quality voluntarily. Similarly, Allen and

Faulhaber‟s (1989) model shows that firms with the most favorable prospects will use

the signal of underpricing in an IPO to show their high quality to investors. Their model

predicts that firms that underprice more can recoup the cost of underpricing by going

back to the seasoned offering market more quickly and frequently.

7

In Grinblatt and Hwang‟s (1989) paper, the authors develop a signaling model with

two signals and two attributes to explain new issue underpricing. To overcome the

asymmetric information problem at IPO, the issuer signals the true value of the firm by

offering shares at a discount and by retaining some of the shares of the new issue in

their personal portfolio. This model can be regarded as a generalization of Leland and

Pyle‟s (1977) model, in which the issuer‟s retention ratio of his own company signals the

firm‟s future cash flows. Grinblatt and Hwang‟s results show that a firm‟s intrinsic value

is positively related to the degree its new issue is underpriced.

Underpricing could also be a mechanism to compensate outsiders for the cost of

information production. Chemmanur (1993) presents a model of IPO pricing in which

insiders have private information and sell stock in both the IPO and the secondary

market, and outsiders may engage in costly information production about the firm.

Knowing that they are going to pool with low-value firms, high-value firms induce

outsiders to engage in information production by underpricing, which in turn

compensates outsiders for the cost of producing information. The information is

reflected in the secondary market price of equity, giving a higher expected stock price

for high-value firms.

Michaely and Shaw (1994) test several signaling hypotheses mentioned above,

but do not find evidence supporting the signaling models for IPO underpricing.

Specifically, their results show that firms that underprice more return to the reissue

market less frequently and for lesser amounts than firms that underprice less. Also,

firms that underprice more experience lower earnings and pay fewer dividends.

Baron (1982) assumes that the value of a new issue is affected by market demand

and the investment banker‟s selling effort. In his model, the issuer is less informed

8

relative to its underwriters, not relative to investors. To address this moral hazard and to

induce the underwriter to put in the requisite effort to market shares, it is optimal for the

issuer to permit some underpricing, since the issuer cannot monitor the underwriter

without cost. Muscarella and Vetsuypens (1989) test Baron‟s agency model directly and

find that when underwriters themselves go public, their shares are just as underpriced

even though there is no monitoring problem. This evidence neither favors nor refutes

Baron‟s hypothesis.

There are three types of benefits that issuers find in liquid shares. First, greater

liquidity allows the opportunity to trade retained shares on more favorable terms.

Second, it is often hypothesized that increased liquidity reduces the required return to

investors, thus increasing the price that investors are willing to pay for shares. Third, it

has been shown that increased liquidity can reduce the issuing costs of subsequent

equity offerings. Several studies have investigated the relationship between IPO

underpricing and after-market liquidity.

Booth and Chua (1996) develop an explanation for IPO underpricing in which the

issuers‟ demand for ownership dispersion motivates underpricing and oversubscription.

In their framework, promoting oversubscription can allow broad initial ownership

dispersion and this in turn can achieve a liquid secondary market for the shares.

However, broad initial ownership requires an increase in investor-borne information cost,

which can be compensated by higher underpricing. Their findings suggest that issuers

intentionally underprice to promote oversubscription, which receives a broad initial

ownership, and in turn, increases secondary market liquidity for their stocks.

Reese (1998) studies the relationships between IPO underpricing, investor interest,

and trading volume. He finds that IPOs which appreciate in price during the first two

9

days of trading experience a significantly higher trading volume than those which do not

appreciate in price during the same time period. This difference in trading volume is not

only statistically significant during the first week of trading but persists for more than

three years beyond the issue date. Using the number of newspaper references of a firm

as a proxy for investor interest, Reese finds that there are significant relationships

between the pre-issue market interest in an IPO and its initial return, initial trading

volume, and long-term volume.

Employing 10 measures of liquidity, Hahn and Ligon (2004) explore whether

underpricing of IPOs boosts subsequent secondary market liquidity. They find that, in

general, there is a positive relationship between the two. The positive relationship holds

both prior to and after lockup expiration; thus, the influence of underpricing is not

restricted to the immediate post-issuance period. For three different volume-based

measures of liquidity -- the turnover ratio, Amihud‟s illiquidity measures, and the

average number of trades -- there is a consistent significantly positive relationship

between underpricing and liquidity. They conclude that insiders concerned about future

liquidity for their retained stakes in the issuing firm could benefit from the liquidity-

increasing effects of underpricing.

Zheng and Li (2008) examine a sample of 1,179 Nasdaq IPOs and find that

underpricing is positively related to the number of non-block institutional shareholders

after IPO. The authors also find evidence that the number of non-block institutional

shareholders is positively related to aftermarket liquidity. The relationship is robust and

significant, particularly when liquidity is measured by aftermarket trading volume.

Therefore, they conclude that underpricing is used to help increase the number of non-

block institutional shareholders, which improves secondary market liquidity.

10

Furthermore, the authors show that IPO underpricing is positively related to trading

volume in the secondary market, suggesting that underpricing does have some direct

effect on market liquidity.

In their 2002 paper, Aggarwal, Krigman, and Womack develop a model in which

managers strategically underprice IPOs to maximize personal wealth from selling

shares at lockup expiration. They argue that if IPO firms underprice more, which can

generate more information momentum, they can attract more attention to the firms‟

stock and thereby shift the demand curve for the stock outwards. As a result, this will

allow managers to sell their holdings at a higher price at lockup expiry than they could

otherwise obtain. Their results show that if managers hold more shares of their

company, their stocks will have greater underpricing at IPO. They find also that

underpricing is positively related to research coverage and research coverage is

positively associated with stock returns and insider selling at lockup expiry.

IPO Long-run Underperformance

Long-run underperformance is the second anomaly found in the IPO market, and

the topic has received substantial attention since the early 1990s. Researchers have

tried to find possible explanations for the anomaly by looking at the different

characteristics related to IPO firms.

Ritter (1991) uses a sample of 1,526 IPOs from 1975 to 1984 and finds that IPOs

substantially underperform the sample of matching firms for a three-year period after the

offering. Younger firms and firms going public in heavy volume years do worse than

average. After examining various cross-sectional and time-series patterns, Ritter

attributes this long-run underperformance of IPOs to investors‟ periodically

overoptimistic expectation about the earnings potential of young growth companies.

11

Firms take advantage of these windows of opportunity and go public near the peak of

industry-specific fads.

Schultz (2003) conducts 5,000 simulations of long-run aftermarket abnormal

returns of IPOs and SEOs from 1973 to 2000. He shows that the poor long-run

performance of equity-issuing firms in event-time is real in the sense that IPOs and

SEOs have underperformed relative to their expectations, but that it is not indicative of

any market inefficiency. More firms go public when they can receive a higher price for

their shares. As a result, there are more offerings at peak valuations than at lower

prices. However, the issuing firms do not know prices are at the peak when they issue

stock.

Venture capitalists specialize in providing funds to privately held companies, and

generate their profits from the companies that go public. According to Field and Lowry

(2007) and Megginson and Weiss (1991), prestigious underwriters prefer to deal with

IPOs backed by venture capitalists, as do institutional investors. As a result, the

presence of venture capital may signal a more successful IPO. Brav and Gompers

(1997) investigate the long-run underperformance of IPO firms by comparing a group of

IPOs with venture capital backing to a group without venture capital backing. They find

that the underperformance documented by Ritter comes primarily from small, non-

venture-backed IPOs. Returns on non-venture-backed IPOs are significantly below

those of venture-backed IPOs when returns are weighted equally. Value weighting

significantly reduces underperformance for non-venture-backed IPOs. Carter, Dark, and

Singh (1998) examine the role of underwriter reputation on IPO long-run

underperformance. Reputation concerns force high-ranked investment banks to choose

higher quality and less risky firms with which to do business. Their results show that, on

12

average, the long-run market-adjusted returns are less negative for the IPOs that are

brought to market by more prestigious underwriters.

As an explanation for the IPO long-run underperformance, Teoh, Welch, and

Wong (1998) try to explore a possible source for the over-optimism about the earnings

potential of IPOs found by Ritter. They argue that the IPO process is particularly

susceptible to earnings management, offering entrepreneurs both motivation and

opportunities to manage earnings. Because of information asymmetry between

investors and issuers at the time of the offering, investors must rely on current earnings

reports. As a result, high reported earnings would translate directly into a higher offering

price.

Total accruals can be decomposed into current and long-term components, and

studies have shown that entrepreneurs have more discretion over short-term than over

long-term accruals. Discretionary current accruals are the asset-scaled proxies for

manipulated earnings determined at the discretion of management. So, Teoh, Welch,

and Wong‟s hypothesis is that if marginal investors do not rationally discount for

earnings management in forming expectations about future cash flows, IPOs with

unusually high accruals in the IPO year experience underperformance relative to those

with conservative accruals after three years of the issue. The evidence in their paper

supports this hypothesis.

Miller (1977) argues that uncertainty implies that reasonable investors may differ in

their forecasts. Assuming investors seek to maximize the present value of their

investment, they will have different estimates of expected returns from the investment,

given uncertainty about the true return to the investment in the security. It follows, then,

that the shares will be owned by the investors with the highest evaluation of the return.

13

That is to say, a badly informed or excessively optimistic small group of investors can

bid a stock up to a value that most investors regard as unreasonable. This usually

occurs because they believe that the stock promises substantially better performance

than most other securities available. As a result, the higher the price of a security the

greater the divergence of opinion about the return from the security.

If the divergence of opinion about a stock changes, it follows that the market price

should also change. For instance, if risky stocks become less risky over time, their

prices should drop. This is because the divergence of opinion narrows over time; that is,

the passage of time resolves certain uncertainties about the future of a company. This

can explain the IPOs long-run underperformance. The prices of new issues are set not

by the appraisal of the typical investor, but by the small minority who think highly

enough of the investment merits of the new issue to include it in their portfolio. The

divergence of opinion about the new issue is greatest when the stock is issued,

because the information asymmetry is greatest. Over time, this uncertainty is reduced

as the company discloses more information, and the price of stocks decreases.

In their empirical test for Miller‟s hypothesis, Houge, Loughran, Suchanek, and

Yan (2001) find that all three variables measuring uncertainty -- percentage opening

spread, time of first trade, and flipping ratio (calculated as the sell-side block volume

divided by the total share volume on the IPO day) -- provide significant explanatory

power of IPO returns. A wide opening spread, late opening trade, and a high flipping

ratio are associated with poor long-run returns, suggesting that greater divergence of

opinion or uncertainty about an IPO can generate long-run underperformance.

Chemmanur and Paeglis (2005) empirically examine the relationship between the

quality and reputation of a firm‟s management and various aspects of its IPO return

14

performance. They argue that if a firm has higher management quality and reputation, it

is more likely to attract greater interest from institutional investors, who themselves are

less likely to be subject to over-optimism compared to individual investors. As a result,

such firms are likely to experience a smaller dispersion in beliefs among investors,

which in turn implies that management quality and reputation will be positively

associated with long-run stock price performance following a firm‟s IPO, in accordance

with Miller‟s theory. Their evidence shows that higher management quality is associated

with lower heterogeneity in investor valuations and firms with better managers have

greater long-run stock returns.

Jensen (1986) argues that conflicts of interest between shareholders and

managers over payout policies are particularly severe when the organization generates

substantial free cash flow and managers want to increase managerial benefits like

compensation or power and reputation, implying that there is negative information

contained in the new cash from IPOs. As Miller (1977) shows, the market may not

incorporate the opinion of pessimistic investors into stock valuation because of

divergent investor expectations and short sale constraints. As a result, Zheng (2007)

hypothesizes that the market may not incorporate the negative information contained in

the new cash into stock valuation; that is, the market may under-react to the free cash

flows from an IPO. Thus, Zheng predicts that firms getting more new cash from IPOs

should have poor long-term stock returns. Results indicate that raising more new cash

in an IPO is related to poorer long-term stock performance. IPO firms that receive more

new free cash flow and have large divergences of investor opinion would tend to be

more overvalued, leading to poor long-term returns.

15

Although studies have documented the IPO long-run underperformance, others

question the existence of such an anomaly. These researchers criticize the

methodology of measuring the long-run returns and conclude that different data, a

different study period, or a different methodology will give different answers. They not

only show that abnormal performance measurement is conditional on an asset-pricing

model, but also recognize that the method of measurement of abnormal performance

affects inferences. The method influences both the magnitude of the measured

abnormal performance as well as the size and power of the statistical test. Brav, Geczy,

and Gompers (2000) reexamine the robustness of IPO underperformance with respect

to various model specifications. In measuring event time returns, the authors use

various benchmarks such as the S&P (Standard & Poor‟s) 500, the Nasdaq composite

index, the CRSP (Center for Research in Security Prices) value weight index, and the

CRSP equal weight index. Size and book-to-market portfolios are also formed. The

paper computes the Fama-French three-factor model, the excess return on the value

weighted market portfolio, the return on a zero investment portfolio, and the return on a

portfolio of high book-to-market stocks less the return on a portfolio of low book-to-

market stocks. The authors conclude that value weighting cuts in half the

underperformance calculated from equal-weighting. Once IPO firm returns are matched

to size and book-to-market portfolios, there is no underperformance. Underperformance

is concentrated primarily in small issuing firms with low book-to-market ratios. Model

mis-specification is an important consideration in long horizon performance tests.

16

IPO Lockup Agreement

Rule 144 limits insider selling. It requires that restricted shares (unregistered

shares acquired directly or indirectly from the issuer from non-public offerings) be held

for a minimum of one year from the time that the shares were originally acquired. Before

1997, this minimum holding period was two years.

When an issuing firm and an investment bank enter into an agreement to offer

securities in an IPO, they sign an underwriter agreement. This contract usually states

that without the investment bank‟s prior written consent, the issuer will not directly or

indirectly sell any shares of common stock for a certain period of time negotiated by the

two parties following the commencement of the public offering of the stock. It is typically

a voluntarily agreement, and is not mandated by any SEC or state securities laws that

regulate insider trading.

Most IPOs feature share lockup agreements, which prohibit insiders and other pre-

IPO shareholders from selling any of their shares for a specified period. The typical

lockup lasts for 180 days, though lockups may range anywhere from three months to

three years. The lockup agreement covers most of the shares that are not sold in the

IPO. The terms and the expiration date of lockup are disclosed in the IPO prospectus.

Earlier, I mentioned that IPO underpricing could either be a device to solve the

information asymmetry problem or a device to reduce the agency problem. As outlined

in the papers reviewed below, IPO lockup agreements may also serve as either a

signaling device or a commitment device to solve the asymmetric information problem

and the agency problem in addition to underpricing. As a result, we can regard lockup

agreements as a complementary tool to underpricing that underwriters and issuers can

choose in the IPO process. Further, I try to shed light on the reasons for an IPO long-

17

run underperformance by examining the long-term stock returns for IPOs with different

lockup characteristics.

IPO Lockup Related Literature

Field and Hanka (2001) examine the IPO‟s stock price and trading volume around

the lockup expiration day. They find that while lockups are in effect, there is little selling

by insiders. Around the scheduled unlock day, there is on average a permanent 40%

increase in trading volume and a statistically prominent three-day abnormal return of

1.5%. Both of these effects are roughly three times larger in venture-backed firms than

in non-venture-backed firms. Venture capital investors sell more aggressively than other

pre-IPO shareholders. The authors find limited support for several hypotheses that may

explain the abnormal return, but do not provide a complete explanation. The abnormal

return is not caused by a change in the proportion of trades at the bid price, temporary

price pressure, or increased trading costs. Also, the abnormal return may be partly

caused by downward sloping demand curves or by consistently larger-than-expected

insider sales.

By examining market reaction to the expiration of IPO lockup, Brau, Carter,

Christophe, and Key (2004) find that the expiration of share lockups has important

share-price implications. Results show statistically significant negative abnormal returns

surrounding the lockup expiration. The authors argue that the negative abnormal returns

are consistent with theoretical predictions based on information asymmetries and

decreased incentive alignment between insiders and general shareholders. The results

of the cross-sectional regression also shed light on characteristics that affect market

returns around the lockup expiration date. The paper finds that greater uncertainty

about insiders‟ future actions is related to negative abnormal returns. Specifically,

18

percentage of shares in lockup, venture capital backing, the percentage of management

ownership in the firm after the offer, and the size of the firm are significantly related to

the cumulative abnormal returns.

Ofek and Richardson (2000) conduct a similar study about the volume and price

patterns around the lockup expiration day. Consistent with the previously mentioned

papers, the authors provide evidence that stock prices fall around the end of their IPO

lock-up period, but they also provide evidence that the lockup effect is not arbitrageable.

Trading costs, the difficulty of shorting newly-public stocks, and short-term capital gains

faced by original shareholder can help explain this fact. Furthermore, the paper argues

that the stock price fall is somewhat consistent with a downward sloping curve for

shares and certain variables, such as stock price volatility, have clear predictive power

for the magnitude of the fall.

Bradley, Jordan, and Yi (2001) find that the average abnormal return on the lockup

expiration day is -0.74%, and the cumulative abnormal return over the five-day

surrounding period is -1.61%. However, the negative abnormal returns are largely

concentrated in the 45% of the firms with venture capital backing. Such firms lose, on

average, 3% to 4% of their value. For the venture-capital-backed group, the largest

losses occur for high-tech firms and firms with the greatest post-IPO stock price

increases, the largest relative trading volume in the period surrounding expiration, and

the highest quality underwriters.

Cao, Field, and Hanka (2004) explore whether insider trading impairs market

liquidity around IPO lockup expiration. They show that officers and directors sell

substantial shares of their own at lockup expiration, but those selling have little effect on

effective spreads. Instead they find that quote depth -- the average of ask depth (the

19

number of shares offered for sale at the ask price) and bid depth (the number of shares

offered for sale at the bid price) -- average trade size, and number of trades per day all

increase. Overall, lockup expiration seems to improve liquidity. The authors explain that

the increase in asymmetric information costs is obscured by the liquidity benefits from

increased trading volume.

Using a different approach, Gao (2005) uses intraday data to explore the trading

activity and the information environment around IPO lockup expiration. He finds that the

price drop around lockup expiration is significantly positively correlated with venture

backing, analyst earnings forecast bias, and forecast dispersion. Further, results show

that information asymmetry of IPO stocks experience little change after the unlock day.

This suggests that insider trading on lockup expiry is unlikely to be driven by private

information; instead, insiders sell their holding for the purpose of diversification.

Even though a normal lockup agreement lasts for several months, in some

situations, some underwriters do allow restricted shareholders to sell a small portion of

the restricted shares early according to the lockup agreement between underwriter and

issuers. While the scheduled lockup expiration day is stated in the prospectus prior to

the firms‟ IPO, the early release represents new information to the market. Keasler

(2001) examines the influence of an underwriter‟s early lockup release on shareholders

wealth. The author finds that most of the firms receiving early release are backed by

venture capital and experience an increase in market capitalization after their IPO.

There are significantly negative abnormal returns associated with the early lockup

release announcement, and negative returns are greater for venture backed IPOs.

Further, negative abnormal returns at the lockup expiration day are reduced for firms

announcing the early lockup release.

20

Brav and Gompers (2003) also explore the extent of insider equity sales prior to

lockup expiration. They argue that if lockup agreement is a commitment device, then

only those firms that have greatly reduced the potential for insiders to take advantage of

shareholders will be released from the lockup restriction. Their results show that firms

that are associated with less moral hazard, such as larger firms, firms with higher

turnover, firms backed by venture capitalists, firms with high reputable underwriters, and

firms with higher post-IPO abnormal returns, are more likely to have an early release.

Both of the above papers conclude that their findings are consistent with the

commitment hypothesis.

The Reasons for the Divergence of IPO Lockup Agreements

Some IPOs have a three-month lockup period, while others lockup their shares for

more than three years. Some IPOs lock 60% of their shares, while others lock only 10%.

Thus far, researchers exploring the reasons for the existence of lockup agreements

have focused on two hypotheses, the signaling hypothesis and the agency hypothesis.

In the market for real assets where the quality of projects is highly variable, we

observe a scenario in which entrepreneurs know the quality of their own projects, while

lenders cannot distinguish between them. In order to solve this information asymmetry

problem, Leland and Pyle (1977) show that if the owner remains under-diversified, this

may communicate private information about the value of the firm to prospective

investors. The willingness of the owner to invest in his firm may serve as a signal to the

lending market of the true quality of the project. Lenders will place a value on the project

that reflects the information transferred by the signal. The authors use a signaling model

to come up with the conclusion that the market reads higher entrepreneurial ownership

as a signal of a more favorable future project.

21

However, Gale and Stiglitz (1989) argue that under-diversification at the time of

IPO is not sufficient for fully communicating private information. If the entrepreneur can

sell the retained shares on the secondary market immediately after the issue, the

signaling strategy will not be convincing to investors. Courteau (1995) extends Leland

and Pyle‟s signaling model that focuses on the retained ownership, and introduces the

length of lockup period to which the owner commits in the prospectus as a signal of firm

value. She develops a model and shows that the length of the holding period, in a

signaling mechanism, complements ownership retention. Also, she finds that higher

quality firms are more likely to have longer lockups to show their quality.

Brav and Gompers (2003) test the firm quality signaling hypothesis. The authors

designate the IPO offer price revision, the probability of dividend initiations, and the

frequency of seasoned equity offerings (SEOs) as measures of firm quality. They argue

that firms that signal their higher quality through longer lockups would be more likely to

raise their offering price in order to garner greater proceeds at the time of their IPO, or

they would have a higher chance to initiate dividend payment after IPO, or else they

would be more likely to issue equity in a subsequent seasoned equity offering. The

authors‟ results reject the signaling hypothesis of lockup, because they do not find that

higher-quality firms possess longer lockup periods. However, as argued by Brau,

Lambson, and McQueen (2005), the proxies for firm quality used in Brav et al. paper are

not appropriate.

Brau, Lambson, and McQueen (2005) present a theoretical model that shows how

the incentives of insiders, underwriters, and investors can interact with the nature of the

firm‟s assets to explain the existence of lockup agreements. Their model shows how

lockups can be a signaling solution to the adverse selection problem resulting from

22

information asymmetries at the time of the stock issue. Specifically, insiders cannot only

retain some fraction of shares of their firm, but also sign a lockup agreement not to sell

the shares for a period of time. Their results indicate that lockups should be shorter

when the degree of asymmetric information is small, and when the cost of mimicking is

high. Specifically, larger firms, older firms, easy to value firms, firms with prestigious

investment bankers, firms with venture capital backing, and firms with well-known

auditors have shorter lengths of lockup.

The problem in the findings of Brau et al. (2005) is that the signal is not a valid

signal by definition. For a signal to be valid, there should be a higher cost to mimickers

for sending a false signal. If their conclusion is true, then opaque firms can mimic

transparent firms by setting a shorter lockup period, a false signal, at a lower cost. This

is because with a shorter lockup period, they can cash out, and make themselves

diversified sooner. The authors realize this problem, and try to solve it by showing that

shorter lockup periods are associated with higher idiosyncratic risk. However, the result

for the test is just marginally significant (p-value = 0.0954). Even if their conclusion is

true, the authors have not shown whether lockup length is a signal for firm quality.

Jensen and Meckling (1976) develop a theoretical model of agency costs. Agency

costs arise when the manager‟s interests are not aligned with firm owners‟ interests,

and these costs increase as the equity share of the manager declines. Managers can

have on-the-job perks, shirking, and self-interested and entrenched decisions that might

reduce shareholders wealth.

In their paper, Brav and Gompers (2003) argue that these lockup agreements

serve as a commitment device to alleviate moral hazard problems. After a firm‟s IPO,

interests of insiders may not align with interests of outside shareholders due to the

23

separation of ownership and management. As a result, IPOs that have a higher chance

of having agency problems should have a longer lockup period to convince the public to

buy their stocks. The authors argue that for a firm with high information asymmetry, the

agency problem should be high because outsiders do not know the actions of the

managers. The results support the commitment hypothesis that unprofitable firms, low

book-to-market ratios firms, firms with low reputation underwriters, and firms without

venture backing have significantly longer lockup periods. These firms suffer from a

greater potential for insiders to take advantage of shareholders, therefore they need a

longer lockup to induce investors to buy into the offering. One concern regarding their

conclusion is that the authors use variables of information asymmetry to test agency

hypothesis. For example, they find that smaller firms, which have high information

asymmetry, have longer lockup period because of higher potential for an agency

problem. This is not necessarily true. Insiders of small firms may work hard, and

insiders of big firms may be more likely to take advantage of outside shareholders.

Using underwriter reputation, Yung and Zender (2008) separate their IPO sample

into two groups, one group with high reputation underwriters and the other with low

reputation underwriters, and test whether signaling hypothesis and agency hypothesis

work separately for these different groups. For the group of high reputable underwriters,

the authors argue that these IPOs will have low information asymmetry. Therefore, the

lockup is a device to solve agency problem for these firms. For the group of low

reputable underwriters, the authors argue that these IPOs cannot find high reputable

underwriters to solve information asymmetry problem, so they must use lockups to

solve this problem. One potential problem for this paper is choosing underwriter

reputation as a standard to divide the whole sample into two groups. Yung and Zender

24

(2008) argue that “underwriter certification has been argued to reduce information

asymmetry; however, this certification should have no impact on moral hazard

problems.”

But underwriters do have a monitoring function in reducing the firms‟ agency

problems after the IPO. According to Krigman, Shaw, and Womack (2001), only 30% of

firms completing an SEO within three years of their IPO switched their lead underwriters.

In addition, in the event of a switch, firms will choose more reputable underwriters. Thus,

we can see that IPO firms keep a relatively long and stable relationship with their

underwriter in order to extract more services from these investment banks. As a result,

a firm with a reputable underwriter will have fewer agency problems even after their IPO

due to the monitoring function of underwriters. To keep their reputation, highly reputable

underwriters will set stricter standards to do business with firms. If a firm has a high

agency problem, which lowers operating performance, a highly reputable underwriter

may refuse to do business with this firm rather than hurting its own reputation. This

could motivate such firms to reduce agency problems in order to keep and/or acquire

the services of highly reputable underwriters. In this way, a highly reputable underwriter

could serve as both a resolution to the information asymmetry and the agency problem

(at least to some extent). Thus, choosing this as a standard to divide the whole sample

into two groups is not appropriate.

My Approach to the Reasons of Divergence of IPO Lockup

Even though several studies mentioned above have investigated the reasons for

the divergence of IPO lockup, the results are mixed. Further, those studies have limited

their research to examining the relationships between lockup length and proxies for

information asymmetry and agency problems. They completely ignore both short-term

25

and long-term stock price behaviors from which we can get rich insight for the reasons

in the divergence of IPO lockup agreements. For example, according to signaling

hypothesis, all the information about the lockup length should be valued into the offering

price of firms at the time of their IPO, thus there should not be a significant difference

between the long-run stock returns for IPOs with long and short lockup lengths. On the

other hand, if the agency hypothesis is true, then firms with a long lockup period, which

have high potential for an agency problem will experience long-run underperformance

due to the high agency cost. Therefore, examining long-run stock returns may give us a

clearer idea for the reasons in the divergence of IPO lockup agreements.

At the lockup expiration day, insiders are given their first chance to sell a

substantial proportion of the shares they hold. Since the lockup expiration day is known

to the public, the short-term returns around lockup expiry should not be different for

stocks with long and short lockup lengths according to signaling hypothesis. But for

agency hypothesis, investors will heavily sell their holdings for firms with high potential

for agency problems, in order not to be taken advantage of by insiders of the firms after

the lockup expires. As a result, there should be a greater negative short-term return for

this group of stocks than those with fewer agency problems. Thus, the short-run returns

around lockup expiry may allow us to differentiate between the signaling and agency

hypotheses.

In choosing the proxies for firm quality, prior studies ignore the most direct

measures, the operating performance of IPO firms. Thus we can examine the operating

performance several years after firms‟ offerings to see whether there is a significant

difference between the group with long lockup periods and the group with short lockup

periods. By doing this, we can determine whether lockup length is a signal for firm

26

quality or is a mechanism to solve an agency problem. According to the signaling

hypothesis, firms with long lockup periods should have better operating performances

since they have better quality than short lockup IPO firms. But according to the agency

hypothesis, firms with long lockup periods should have worse operating performances

after their offering because of their high agency cost.

27

CHAPTER 3

HYPOTHESES DEVELOPMENT

Signaling Hypothesis

By signing a lockup agreement with underwriters, insiders of initial public offering

(IPO) firms bear the cost of non-diversification. Insiders of higher quality firms can bear

these costs to show their firms‟ quality to outside investors, while insiders of low quality

firms cannot give the false signal of committing to a long lockup period because of their

expected negative future performance. Therefore, we can predict that high quality firms

should have a long lockup period, while low quality firms should have a short lockup

period. Brav and Gompers (2003) use the probability of SEOs, offer price revision, and

the probability of dividend initiations as proxies for firm quality in their testing of this IPO

lockup signaling hypothesis. But, as argued by Brau et al. (2005), their measures of firm

quality are not appropriate.

Jain and Kini (1994) investigate whether equity retained by the original

entrepreneurs is a signal of firm quality. The authors use firms‟ operating performance

after the IPO as a proxy for firm quality. They find that there is a positive relationship

between the two variables – a higher retention ratio means a higher operating

performance after the firm‟s IPO. Zheng and Stangeland (2007) test whether

underpricing is a signal for firm quality. They also use the operating performance as a

proxy for firm quality and conclude that IPOs with greater underpricing are of better

quality. This dissertation intends to examine whether lockup is a signal for firm quality.

Therefore I use operating performance as a measure of firm quality, a proxy not

previously used in the literature of IPO lockups, thus leading to my first hypothesis.

28

Hypothesis 1: Firms with a longer lockup period should have higher quality, and

therefore higher operating performance for several years after their IPO.

Brau et al. (2005) find that lockups should be shorter when the degree of

asymmetric information is small. I can extend their paper, and partition the whole

sample into two groups, with one group including transparent IPOs, the other including

opaque IPOs. Both groups include high quality firms and low quality firms, because both

types of firms can be either opaque or transparent. Since opaque firms have a higher

degree of asymmetric information problems, high quality firms belonging to this group

have a strong motive to use lockup length to differentiate their quality from other firms.

On the other hand, for transparent firms, it is easier for investors to differentiate high

quality and low quality firms because of less information asymmetry, meaning there may

not be a strong relationship between firm quality and lockup length. Therefore, we

should observe that the relationship between firm quality and lockup length is stronger

for opaque firms than for transparent firms.

Hypothesis 1A: The positive relationship between operating performance and lockup

length (Hypothesis 1) is stronger for opaque firms than for transparent firms.

When partitioning the whole sample into opaque and transparent firms in

Hypothesis 1A, I use the asymmetric-information variables according to Brau et al.

(2005). However, some of those variables are proxies for both information asymmetry

and agency problem. For example, the reputation of an underwriter, as a third party

certification, is a good proxy for information asymmetry (Ritter, 1986; Michaely and

Shaw, 1995; Megginson and Weiss, 1991). But underwriters do have a monitoring

function in reducing the firms‟ agency problems after the IPO. To keep their reputation,

highly reputable underwriters will set strict standards to do business with firms. This

29

could motivate such firms to reduce agency problems in order to keep and/or acquire

the services from highly reputable underwriters. As a result, a firm with a reputable

underwriter will have fewer agency problems. Instead, I will use “high-tech” as a

criterion to separate the sample into opaque and transparent firms. High-tech firms will

have more research and development and know-how, which makes them hard to be

valued due to high information asymmetry. On the other hand, it is not necessarily true

that the managers of high-tech firms will cause more agency problems compared to

non-high-tech firms. Thus, high-tech is a good proxy for information asymmetry, and

can be used to partition the whole sample into opaque and transparent firms, providing

the impetus for my third hypothesis:

Hypothesis 1B: The positive relationship between operating performance and lockup

length (Hypothesis 1) is stronger for high-tech firms than for non-high-tech firms.

A third criterion may be used to separate firms with high information asymmetry

from firms with low information asymmetry. This third criterion is λ, the proportion of the

bid-ask spread due to adverse selection. Firms with a high λ have high information

asymmetry and firms with a low λ have low information asymmetry, therefore:

Hypothesis 1C: The positive relationship between operating performance and lockup

length (Hypothesis 1) is stronger for firms with a high λ than for firms with a low λ.

Brau et al. (2005) argue that the reason they do not examine the long-term stock

returns is that at the time of IPO good firms and bad firms are both fairly priced.

According to the signaling hypothesis, firms with a longer lockup period should have

higher quality than firms with a shorter lockup period. But the information of firm quality

imbedded in the lockup lengths has been incorporated into the stock price at the time of

a firm‟s IPO. In other words, the offer prices of IPO stocks are set according to their

30

quality. As a result, even though IPO firms experience long-run underperformance

compared to the market, we should not observe a difference between long-run stock

returns for firms with long lockup periods, which have high quality, and short lockup

periods, which have low quality. Previous research has not examined the long-run stock

returns for IPOs with different lockup lengths. I propose the following hypothesis:

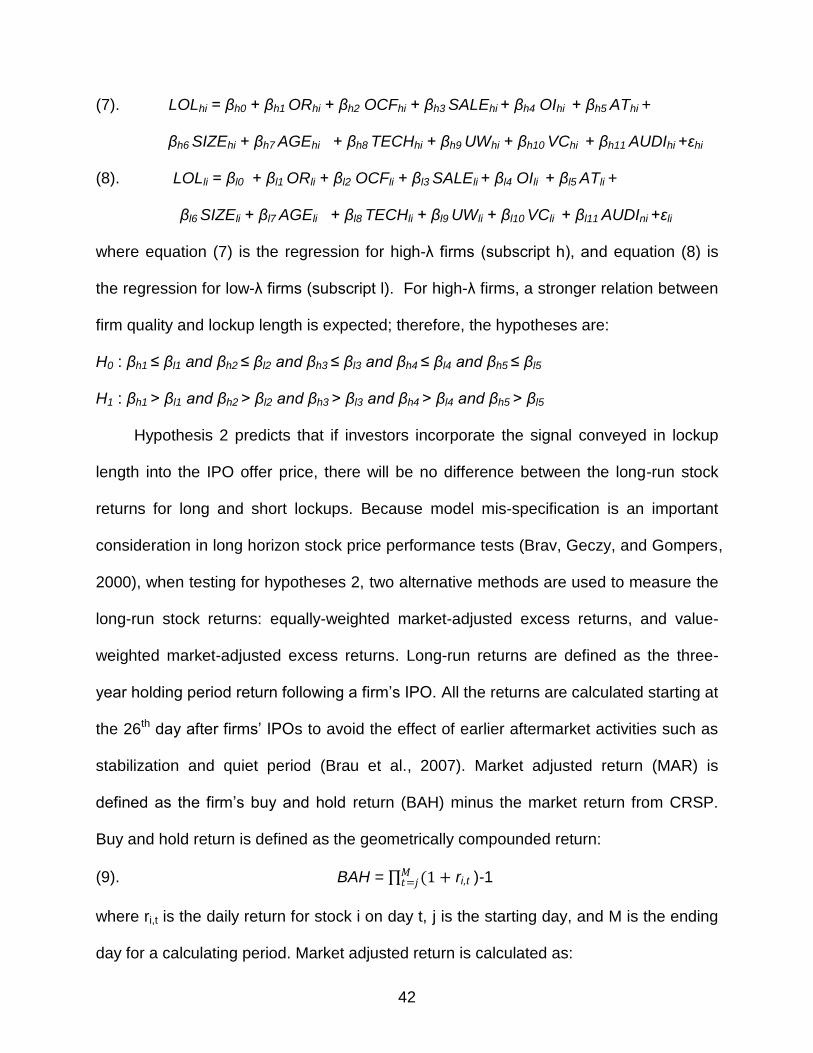

Hypothesis 2: If investors incorporate the signal of lockup into the IPO offer price, there

will be no difference between the long-run returns for long and short lockups.

Starting from the lockup expiration day, insiders of the IPO firms who are

previously restricted from selling their holdings have the first chance to sell a large

proportion of their shares. However, the dates of IPO lockup expiration and the number

of shares that can then be sold by insiders are well known by investors at the time of

firms‟ IPO from their prospectus. In addition, as Field and Hanka (2001) point out, IPO

lockup expiry is a relatively clean event to study because few companies make

important announcements around lockup expiry, such as earnings, dividend, mergers or

acquisitions. Therefore, there should be no significant abnormal returns for IPO firms

around their lockup expiry. The hypothesis is as follows:

Hypothesis 3: There are no significant abnormal returns for IPO firms around their

lockup expiration dates.

Agency Hypothesis

For IPOs with a high potential for agency problems, investors require more shares

to be locked to avoid being taking advantage of by insiders. This is because if insiders

of high agency firms hold only a very small portion of the firm then even with the lockup

agreement it is hard to align the interests of insiders with the interests of shareholders.

Brav and Gompers (2003) use variables such as firm size and industry to measure

31

agency costs. These variables are not appropriate because they are also proxies for

information asymmetry. Instead, I will use free cash flow, expense ratio, asset utilization

ratio, and debt level to measure the degree of agency problem (McKnight and Weir,

2008) in testing the following:

Hypothesis 4: Higher agency problem IPOs should lock up more shares.

Agency costs arise when the manager‟s interests are not aligned with firm owners‟

interests, and these costs increase as the equity share of the managers declines

(Jensen and Meckling, 1976). As the insiders of high agency IPO firms sell their shares

and therefore reduce their interests in the firm after lockup expiry, they can start to have

on-the-job perks, shirking, and self-interested and entrenched decisions. These agency

costs have a negative impact on the firm‟s operating performance and reduce

shareholders‟ wealth (Jain et al., 1994). As a result, I predict that firms with longer

lockup periods will have greater agency problems, which will lead to worse operating

performance after their IPO.

Hypothesis 5: IPO firms with longer lockup periods will have worse operating

performance for several years after their offerings compared to firms with shorter lockup

periods.

According to the agency hypothesis, firms with a high agency problem should

have a longer lockup period than firms with a low agency problem. At the time of lockup

expiry, Insiders have the chance to sell their holdings of the firm and to cause agency

problems thereafter. In order not to be taken advantage of by insiders, some investors

will sell their shares of high agency firms around lockup expiry, leading to a price drop.

Other investors may still hold their shares, probably due to their underestimate of the

agency problem of the firm. As insiders of these firms continuously cause agency

32

problems, leading to the deterioration of operating performance, more investors will sell

the firms‟ shares. Thus, this high agency cost will lead to poor long-run returns (Harris

and Glegg, 2009) for firms with long lockup periods. On the other hand, for firms with a

low agency problem, investors may not worry too much about the agency problem.

Therefore, they may not sell the shares of the firm as intensively as investors do in high

agency firms.

Hypothesis 6: Firms with long lockup periods will experience worse long-run stock

returns after their offerings compared to firms with short lockups.

As discussed in Hypothesis 1B, high reputation underwriters may be good

monitors and therefore reduce the agency problem for IPO firms. As a result, for firms

with high reputation underwriters, there should be a low agency problem. The lockup

length of these firms is not used to differentiate the agency problem among them. I

predict that there will be no difference between the long-run returns for this group of IPO

firms with long and short lockup lengths. On the other hand, for firms with low reputation

underwriters, agency problems may not be effectively reduced, so these firms still need

to use lockup length to differentiate the agency problems among them. Thus I predict

that the long-run returns for firms with short lockups will be better than firms with long

lockups. The reputation of underwriters works as a complimentary tool for lockup length.

By the same reasoning, venture capital backing and the reputation of auditors may also

work as a mechanism to reduce agency problems, so I have the following hypotheses:

Hypothesis 6A: For firms with high reputation underwriters, auditors, or with venture

capital backing, there is no difference between long-run stock returns for long and short

lockups.

33

Hypothesis 6B: For firms with low reputation underwriters, auditors, or without venture

capital backing, longer lockups are associated with worse long-run stock returns than

shorter lockups.

On the IPO lockup expiration date, insiders of the firm have the chance to sell their

holdings of the firm. Under agency hypothesis, if insiders sell their shares at the lockup

expiration day, they have more incentive to cause agency problems and may start to

expropriate wealth from shareholders. For long lockup IPOs, which have higher

chances of experiencing agency problems, investors will sell their shares around IPO

lockup expiry to avoid wealth expropriated by insiders. Therefore, we should observe a

big price drop for firms with long lockup periods around lockup expiration. On the other

hand, for IPOs with short lockup periods, we should observe no price drop or a smaller

price drop. This is because insiders in these firms will always try to maximize

shareholders wealth, and investors know that there are fewer agency problems in these

firms. As a result, investors will sell the shares for these IPO firms less intensively.

Previous research has not explored the short-run price behavior of IPOs around lockup

expiration for IPOs with different lockup lengths. Therefore, I propose:

Hypothesis 7: There are significant negative abnormal returns for IPO firms around their

lockup expiry, and firms with longer lockups, which have high chances of experiencing

agency problems, will experience worse returns than firms with shorter lockups.

I can use these hypotheses to examine whether the IPO lockup length is a solution

to the agency problem or a signaling mechanism, as shown in Table 1. The predictions

for the signaling hypothesis and the agency hypothesis are quite different. For example,

when examining the operating performance after firms‟ IPOs, the signaling hypothesis

predicts that firms with long lockups will have better performances than firms with short

34

lockups, while the agency hypothesis predicts that, on the contrary, short lockups will

have better performances. For the long-run stock returns, the signaling hypothesis

predicts that there are no differences between the long-run returns for firms with long

and short lockup periods, while the agency hypothesis predicts that firms with short

lockup periods will have better returns than firms with long lockup periods. For the short-

term returns around lockup expiry, the signaling hypothesis predicts that there are no

abnormal returns for IPO firms, while the agency hypothesis predicts that there should

be bigger negative abnormal returns for firms with long lockup periods than firms with

short lockup periods.

Table 1

Comparisons for the Predictions of Hypotheses

Hypotheses Signaling Agency

Operating performance after

IPO

H1: Long lockups will have

better performance

H5: Short lockups will

have better performance

Long-run returns after IPO H2: No difference between

long and short lockups

H6: Short lockups have

better long-run return

Short-run return around

lockup expiry

H3: No short-term

abnormal return

H7: There are short-term

abnormal returns and

long lockups have a

worse return

35

CHAPTER 4

DATA COLLECTION AND RESEARCH DESIGN

The data for this study is from the Thompson Securities Data Corporation (SDC)

database and consists of initial public offerings (IPOs) of equity for the period from 1989

through 2004. The end year, 2004, was chosen to ensure that four years worth of

operating performance data is available on Compustat. Information about each IPO is

collected, such as the IPO date, issuer name, symbol ticker, lead underwriter, IPO

proceeds, offer price, the number of primary shares and secondary shares, percentage

of shares locked up, auditor name, lockup expiration date, and total debt at the time of

the IPO. When SDC misses some data fields, the individual firm prospectus is searched

for the relevant information. Information on underwriter rankings is collected from Jay

Ritter‟s website based on Carter-Manaster (1990). Consistent with current research,

American depository receipts (ADRs), units offerings, closed end funds, real estate

investment fund (REITs), reverse leveraged buyouts (LBOs), and equity carve outs are

excluded. IPOs with offer price below $5 are excluded. Further firms must be listed on

the Center for Research in Security Prices (CRSP) after their offering. Thus daily stock

price, trading volume, and bid-ask spread for each IPO can be collected. Accounting

data is obtained from Compustat.

Signaling Hypotheses

Hypothesis 1 predicts that firms with a longer lockup period should have higher

quality, and therefore have higher operating performance for several years after their

IPO. Following Jain and Kini (1994) and Zheng and Stangeland (2007), growth rates of

several accounting variables are used to measure the operating performance of IPO

firms, which in turn proxy for firm quality. Specifically, two cash flow variables are

36

calculated. First is operating return on assets (OR), which is defined as operating

income before depreciation and taxes divided by total assets at the end of the fiscal

year. This variable provides a measure of the efficiency of asset utilization. The second

operating performance measure is defined as operating cash flows deflated by total

assets (OCF) at the end of the fiscal year. This ratio equals operating income minus

capital expenditures divided by total assets, and is a useful measure since operating

cash flow is a primary component in net present value calculations used to value a firm.

Other performance measures included are sales (SALE), operating income (OI), and

asset turnover (AT), which is defined as the ratio of sales to total assets. Earnings is not

used as a performance variable since managers may adopt a strategy that inflates

earnings initially at the expense of earnings growth rates in future years (Zheng et al.,

2007).

Growth rates are calculated for each performance measure by comparing their

values at the end of each fiscal year following the IPO (Year +2 to +4) to their values at

the end of the fiscal year of IPO (Year +1). The changes in operating performance are

measured as the median changes because the performance measures may be skewed

and the mean is particularly sensitive to outliers (Jain et al., 1994). Only those firms

with positive measures in Year +1 are included in our calculation of growth rates.

Different industries grow at different rates in the economic cycle. IPO firms tend to be

concentrated in high growth industries, thus their growth rate may reflect industry-wide

growth patterns. Industry-adjusted changes are calculated to reduce the effect of such

patterns in IPO growth rates. The industry-adjusted performance for a particular IPO

firm is the difference between its growth rate and the median growth rate in all firms in

37

its industry during the same period. Each IPO firm is matched with firms in the same

industry based on three-digit Standard Industrial Classification (SIC) codes.

Performance growth rates are compared between firms with long lockups and

firms with short lockups in order to evaluate whether long lockup periods are associated

with higher quality. To do this, the entire sample is split into quartiles according to the

length of firm‟s lockup. Then the median growth rates are compared for the first and

fourth quartiles to see whether the growth rates for the fourth quartile (long lockup group)

are significantly higher than those for the first quartile (short lockup group). The

hypotheses are:

H0 : Ms ≥ Ml

H1 : Ms < Ml

where Ms is the median growth rate of performance measure for the short lockup group,

and Ml is the median growth rate of performance measure for the long lockup group.

Regression analysis is performed to control for other variables that may affect the

length of lockup (LOL).

(1). LOLi = β0 + β1 ORi + β2 OCFi + β3 SALEi + β4 OIi + β5 ATi + β6 SIZEi +

β7 AGEi + β8 TECHi + β9 UWi + β10 VCi + β11 AUDIi + εi

where

LOL: length of lockup (number of days);

OR: operating return on asset;

OCF: operating cash flow on asset;

SALE: net total revenue;

OI: operating income;

AT: asset turnover;

38

SIZE: proceeds of a firm‟s IPO;

AGE: the years from a firm‟s inception till IPO;

TECH: a dummy variable for high-tech firms;

UW: Carter-Manaster ranking for underwriter;

VC: a dummy variable for venture capital backing;

AUDI: a dummy variable for the well-known top six auditors.

Length of lockup is the number of days in a firm‟s lockup agreement. Besides

growth rates of the five accounting numbers, several variables that may affect the

lockup length of IPO firms are included. Large firms and older firms will have less

information asymmetry, so they may have a shorter lockup period (Brau et al., 2005).