Embed Size (px)

Citation preview

Copyright © 2011 by K&L Gates LLP. All rights reserved.

The Revolution in U.S. Law Governing Non-Resident Money Managers

April 27, 2011 – Webinar

Stuart E. Fross, Partner, K&L Gates, Boston, MACary J. Meer, Partner, K&L Gates, Washington, D.C.Ingrid Pierce, Partner, Walkers, Cayman IslandsJennifer Thomson, Partner, Walkers, Cayman Islands

DC-9204867 v1

1

I. Overview of U.S. RegulationU.S. federal regulation of money managers and collective investment schemes (“funds”) encompasses two inter-connected sets of laws:

Investment Advisers Act of 1940 (the “Advisers Act”) – regulates “investment advisers”

Provides for registration of advisers and regulation of their activities Includes advisers to separate accounts and/or fundsCan include U.S. or non-U.S. advisers - jurisdiction governed by “conducts and effects” test

Investment Company Act of 1940 (the “Investment Company Act”) – regulates collective investment schemes

Requires registration of some funds (such as mutual funds)Provides exemptions for other funds that meet certain requirementsNon-U.S. funds are ineligible to register as investment companies under the Investment Company Act

2

I. Overview of U.S. Regulation - Advisers

Definition of “investment adviser” in the Advisers Act is broad, and includes any person who:

for compensation, engages in the business of advising others, either directly or through publications or writings, as to the value of securities or as to the advisability of investing in, purchasing, or selling securities, or for compensation and as part of a regular business, issues or promulgates analyses or reports concerning securities

3

I. Overview of U.S. Regulation - Advisers

Includes exemptions from the definition for, among others:

Banks (not including non-U.S. banks)Certain FINRA-member broker-dealers (not including non-U.S. brokers that are not FINRA member firms)Publishers of newspapers, news magazines or business or financial publications of general and regular circulation Advisers providing advice solely with respect to U.S. government securities

4

I. Overview of U.S. Regulation - Advisers

Generally, an investment adviser must have a minimum amount of assets under management (subject to exceptions) to qualify for federal investment adviser registration (as discussed below)This minimum AUM requirement does not apply to an adviser without a place of business in the U.S.If an adviser does not register under the Advisers Act, it must consider whether it must register with one or more states

5

I. Overview of U.S. Regulation - FundsHedge funds, private equity funds, venture funds and similar investment schemes are generally structured to avoid registration under the Investment Company Act (“Private Funds”)

Private Funds are also offered and sold pursuant to an exemption (or combination of exemptions) from registration under the Securities Act of 1933 relating to the offer and sale of the securities issued by the Private Fund

Regulation D – private placement to U.S. or non-U.S. investorsRegulation S – offers made in an “offshore transaction”without “directed selling efforts” in the U.S.

6

I. Overview of U.S. Regulation - FundsRegistration as an investment company under the Investment Company Act is impractical for Private Funds

Registered investment companies are subject to, among other things:

Significant ongoing disclosure requirements including quarterly and annual public filingsRestrictions on debt issuance and preferred classes of equityRestrictions on transactions with affiliates and joint transactions

7

II. The Dodd-Frank Act The Act rescinds the “private adviser exemption” effective July 21, 2011 (unless postponed)

Many U.S. and non-U.S. advisers rely on the private adviser exemption to remain unregistered

Private adviser exemption (Section 203(b)(3) of the Advisers Act) exempts an adviser that:

during any rolling 12-month period had fewer than 15 clients does not serve as an adviser to a registered investment company or business development company (“BDC”) under the Investment Company Act and does not hold itself out to the public as an investment adviser

Generally, a fund counts as a single client

8

II. The Dodd-Frank Act (cont.)Many advisers that relied on the private adviser exemption will be required to register or qualify for an exemptionAdvisers that do not qualify for federal registration must register with one or more states

Does not apply to a non-U.S. adviser with no place of business in the United States – these advisers automatically qualify for federal registrationState regulatory regimes vary and may be similar to or very different than federal registration and Advisers Act regulation

9

III. New Exemptions

The Dodd-Frank Act creates or directs the SEC to create new exemptions from registration

Two most relevant to non-U.S. advisers are:Private fund adviser exemptionForeign private adviser exemption

These exemptions are mutually exclusive

10

IV. Private Fund Adviser Exemption

Section 408 of the Dodd-Frank Act provides an exemption from registration under the Advisers Act for:

An adviser that acts as an investment adviser solely to qualifying “private funds” with assets under management in the U.S. of less than $150 million

SEC proposed rules interpreting the exemption on November 19, 2010Proposed rules have not yet been adopted

11

IV. Private Fund Adviser Exemption (cont.)

The proposed rules define “qualifying private funds” for this purpose as collective investment schemes that are not registered under the Investment Company Act and have not elected to be treated as BDCs

12

IV. Private Fund Adviser Exemption (cont.)Private Fund Adviser Exemption

Under management in the U.S.– Proposed Rules

An adviser that has its principal office and place of business outside the U.S. but that does not have a U.S. place of business is treated differently from one with a U.S. place of business Place of business is defined in Advisers Act Rule 222-1 to mean:

An office at which the adviser regularly provides investment advisory services, solicits, meets with or otherwise communicates with clients andAny other location that is held out to the general public as a location at which the adviser provides investment advisory services, solicits, meets with or otherwise communicates with clients

13

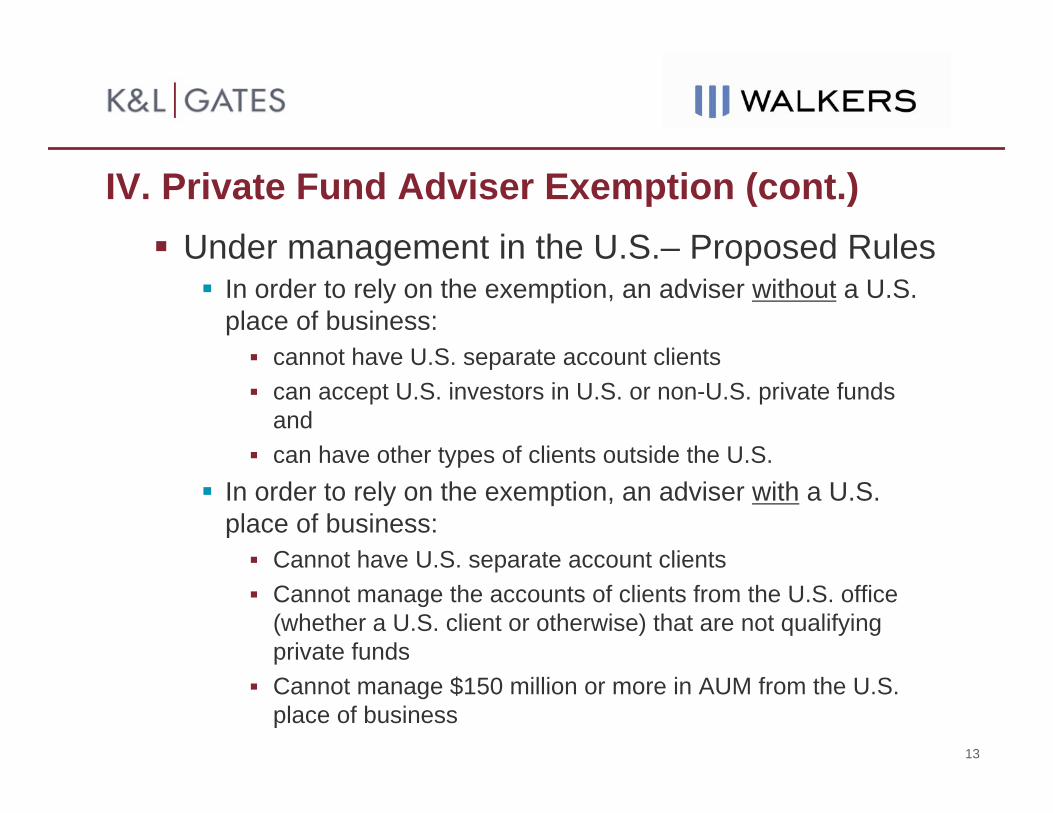

IV. Private Fund Adviser Exemption (cont.)Under management in the U.S.– Proposed Rules

In order to rely on the exemption, an adviser without a U.S. place of business:

cannot have U.S. separate account clientscan accept U.S. investors in U.S. or non-U.S. private funds andcan have other types of clients outside the U.S.

In order to rely on the exemption, an adviser with a U.S. place of business:

Cannot have U.S. separate account clientsCannot manage the accounts of clients from the U.S. office (whether a U.S. client or otherwise) that are not qualifying private fundsCannot manage $150 million or more in AUM from the U.S. place of business

14

IV. Private Fund Adviser Exemption (cont.)

$150 million AUM limit – Proposed RulesMust be calculated by reference to the AUM calculation method in proposed ADV Part 1A Item 5.F

Net asset value calculationAll assets of a qualifying private fund must be treated as a “securities portfolio”Must be calculated based on current market valueMust include assets of any qualifying private fund, even if it is:

Proprietary money and/orAssets managed without compensation

Must include any uncalled capital commitmentsCannot back out liabilities

15

IV. Private Fund Adviser Exemption (cont.)

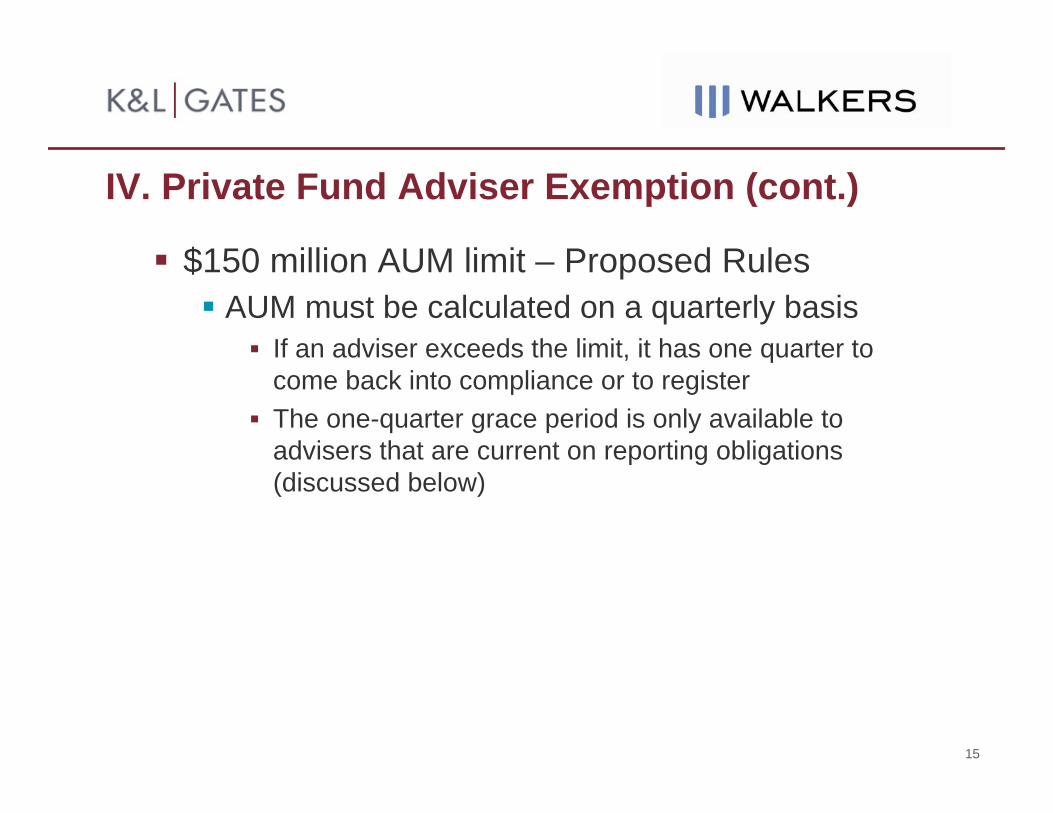

$150 million AUM limit – Proposed RulesAUM must be calculated on a quarterly basis

If an adviser exceeds the limit, it has one quarter to come back into compliance or to registerThe one-quarter grace period is only available to advisers that are current on reporting obligations (discussed below)

16

IV. Private Fund Adviser Exemption (cont.)

Subject to Reporting and InspectionAlthough exempt from registration, a private fund adviser:

Must make certain publicly-available reports through the Investment Adviser Registration Depository system (“IARD”)Is subject to inspection by the SEC staff as if it were registered

17

IV. Private Fund Adviser Exemption (cont.)Reporting

A private fund adviser must file a very limited subset information referenced on Form ADV Part 1A, including identifying information, form and state of organization, executive officers, direct and indirect owners, disciplinary history and information about private fundsAs proposed, unless postponed, a private fund adviser initially would have to file the sections of the amended Form ADV Part 1A no later than August 20, 2011

18

V. Foreign Private Adviser

Section 402(a) of the Dodd-Frank Act provides an exemption from registration under the Advisers Act for a non-US adviser that meets the definition of “foreign private adviser”“Foreign private adviser” means an adviser that:

has no place of business in the U.S.has fewer than 15 clients and investors in the U.S. in private fundshas less than $25 million AUM (subject to increase by SEC rule) attributable to such clients and investorsdoes not hold itself out generally to the public in the U.S. as an investment adviser anddoes not act as an investment adviser to any registered investment company or BDC

19

V. Foreign Private Adviser (cont.)

Place of businessDefined in the same way as in the context of the private adviser exemption, discussed above

“In the United States” means the United States of America, its territories and possessions, any State of the United States, and the District of Columbia

20

V. Foreign Private Adviser (cont.)Who is an investor?

A “beneficial owner”Must, however, count as investors its U.S. “knowledgeable employees” invested in a fund Must look through certain entities to underlying investors in some casesIncludes holders of any of the issuer’s securities, including both debt and equity

21

V. Foreign Private Adviser (cont.)

Who is an investor?Adviser must look through record holders of securities if the economic risk of the investment has been transferred by that record holder to a third-party U.S. person, such as through a total return swap, barrier call option or other derivative

Will require additional representations in subscription agreementsMay be difficult for adviser to discern

Look-throughs are intended prevent a foreign private adviser or a third party from creating nominee accounts or other vehicles in which U.S. investors pool money to keep the foreign private adviser from counting the underlying U.S. investors

22

V. Foreign Private Adviser (cont.)

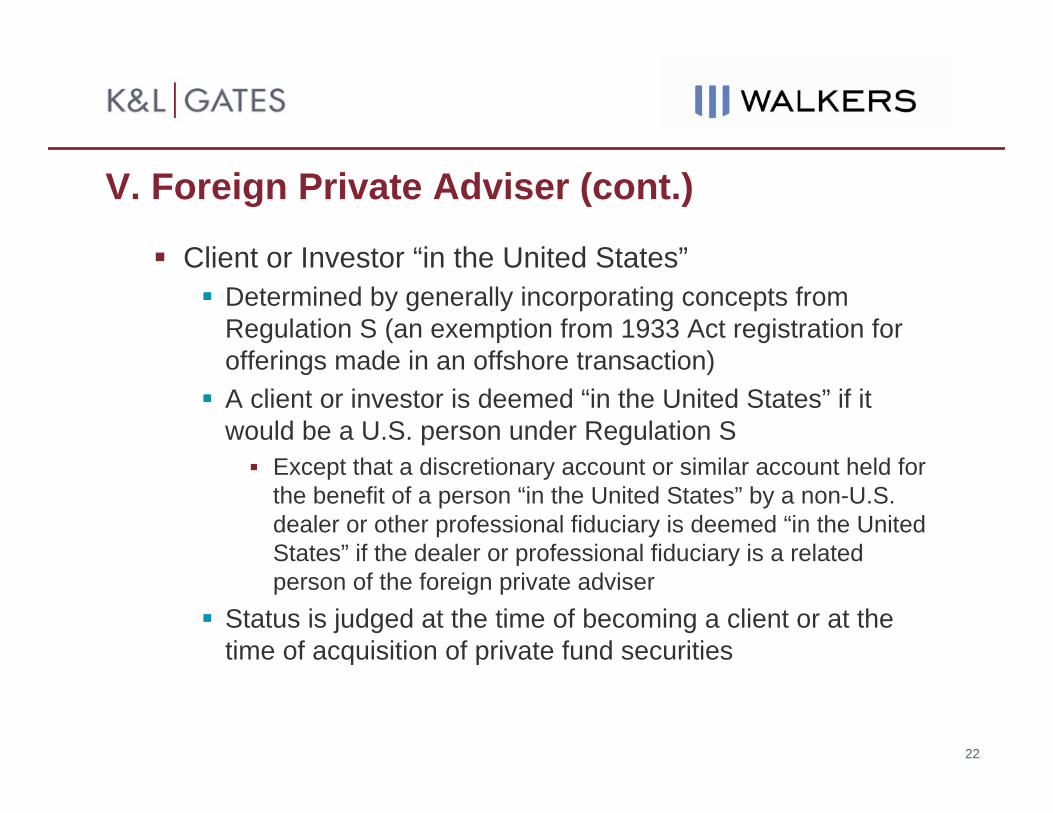

Client or Investor “in the United States”Determined by generally incorporating concepts from Regulation S (an exemption from 1933 Act registration for offerings made in an offshore transaction)A client or investor is deemed “in the United States” if it would be a U.S. person under Regulation S

Except that a discretionary account or similar account held for the benefit of a person “in the United States” by a non-U.S. dealer or other professional fiduciary is deemed “in the United States” if the dealer or professional fiduciary is a related person of the foreign private adviser

Status is judged at the time of becoming a client or at the time of acquisition of private fund securities

23

V. Foreign Private Adviser (cont.)Counting clients

Proposed rules borrow principles of client counting from private adviser exemptionA foreign private adviser must count a client even if the adviser receives no compensation from the client for its servicesIf an adviser were required to count one or more U.S. investors in a fund, it would not have to count separately the fund as a U.S. client

24

V. Foreign Private Adviser (cont.)

Calculating AUM for $25 million limitMust be calculated by reference to net asset value calculation in proposed ADV Part 1A Item 5.F

All assets of a qualifying private fund must be treated as a “securities portfolio”Must be calculated based on current market valueMust include assets of any qualifying private fund, even if it is:

Proprietary moneyAssets managed without compensation

Must include any uncalled capital commitmentsCannot back out liabilities

25

V. Foreign Private Adviser (cont.)Foreign private advisers are not subject to reporting, recordkeeping rules or inspection by SEC staff

SEC has the authority to raise the $25 million limit, but chose not to do so likely because of this lack of regulation

Key issuesLess flexible exemption than private fund adviser; lower AUM limitPermits separate account clients, but must count U.S. investors even in non-U.S. funds

26

VI. Exemption Application Chart CLIENTS/INVESTORS ASSETS UNDER

MANAGEMENTSEC REQUIREMENTS STATE REQUIREMENTS

Non-U.S. adviser to private funds and/or managed accounts with <15 US clients or investors and no place of business in the US

AUM (attributable to U.S. clients/investors) < $25M

Exempt from registrationNo record-keeping or reporting requirements

States are permitted to require registration, if meet minimum state nexus test

Non-U.S. adviser to private funds and/or managed accounts with 15 or more US clients or investors

Any amount SEC registration requiredSubject to record-keeping and reporting requirements required by Advisers Act (including SEC examination)

No state registration permitted

Non-U.S. adviser to private funds and/or managed accounts with US clients or investors

AUM (attributable to U.S. clients/investors) ≥ $25M

SEC registration requiredSubject to record-keeping and reporting requirements required by Advisers Act (including SEC examination)

No state registration permitted

Non-U.S. adviser solely to private funds (U.S. or non-U.S.)

AUM managed from an office in the U.S. < $150M

Exempt from registrationSubject to record-keeping and reporting requirements as SEC determines (including SEC examination)

States are permitted to require registration, if meet minimum state nexus test

Non-U.S. adviser solely to private funds (U.S. or non-U.S.)

AUM managed from an office in the U.S. ≥ $150M

SEC registration requiredSubject to record-keeping and reporting requirements required by Advisers Act (including SEC examination)

No state registration permitted

27

VII. Regulation Lite and Participating Affiliates

“Regulation Lite”Prior to the Dodd-Frank Act, the SEC took the position that the substantive provisions of Advisers Act regulation did not apply to a registered non-U.S adviser’s non-U.S. clients (including non-U.S. funds with U.S. investors)Position was based on no-action and interpretive guidance and was reaffirmed as recently as 2006

28

VII. Regulation Lite and Participating Affiliates (cont.)

“Regulation Lite”Under “Regulation Lite,” with respect to its non-U.S. clients:

The adviser was required to maintain and upon request provide records with respect to non-U.S. funds and clients and Its non-U.S. client activities would be subject to inspection but would not be governed by the Advisers Act

Regulation lite was based upon the conducts and effects test for extra-territorial application of the Advisers Act

29

VII. Regulation Lite and Participating Affiliates (cont.)

“Regulation Lite”It is unclear whether the staff will continue to apply “regulation lite” given that it is requiring non-U.S. advisers to look through non-U.S. funds to U.S. investors

Represents a shift in approach to non-U.S. funds

30

VII. Regulation Lite and Participating Affiliates (cont.)

Participating AffiliatesPrior to the Dodd-Frank Act, the SEC staff permitted unregistered, non-U.S. advisers to provide investment advice with respect to U.S. clients of an SEC-registered affiliate subject to certain conditions (discussed below)This was based on staff no-action and interpretive guidance

Most widely known of these no-action letters is the “Unibanco” no action letter – Uniao de Bancos de Brasileiros S.A., SEC No-Action Letter (July 28, 1992)

31

VII. Regulation Lite and Participating Affiliates (cont.)

Unibanco line of letters requirements:Registered adviser and participating affiliates must be (and act as) separate legal entitiesParticipating affiliate must appoint a U.S. agent for service of process (and must maintain such an agent until six years after it ceases providing advice to the registered adviser’s U.S. clients)Participating affiliate must submit to the jurisdiction of the U.S. courts for actions arising under the U.S. securities laws in connection with investment advisory activities for U.S. clients of registered adviser

32

VII. Regulation Lite and Participating Affiliates (cont.)

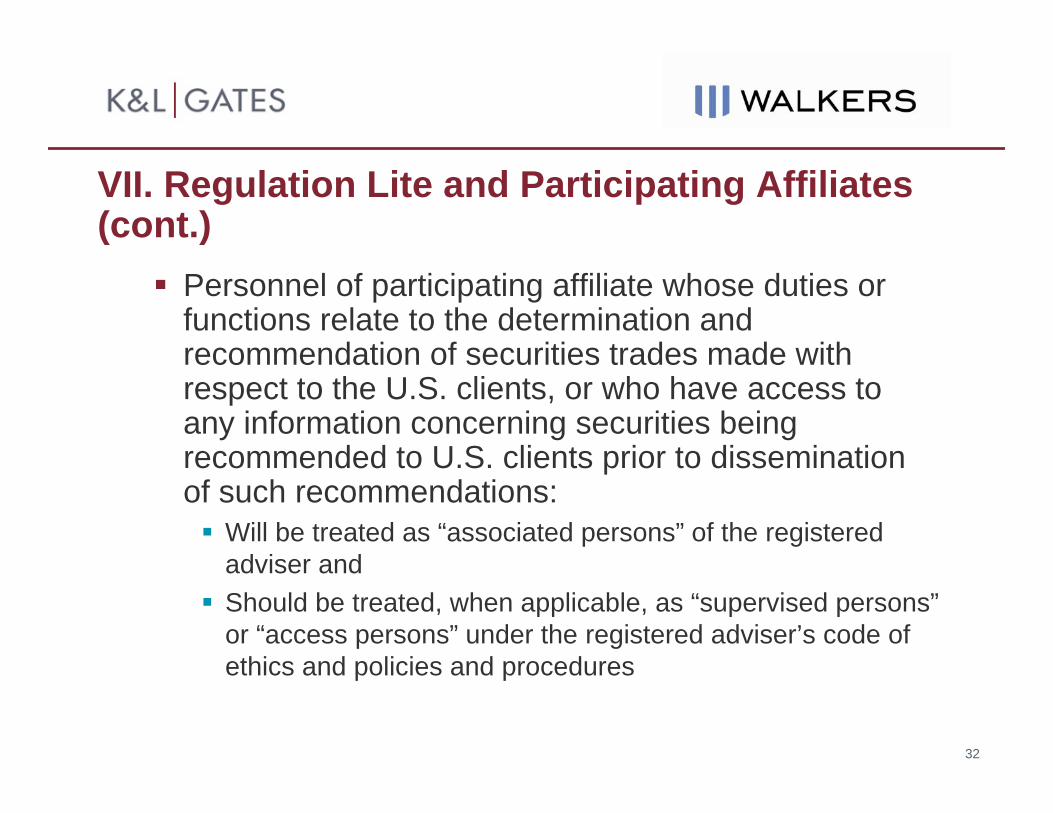

Personnel of participating affiliate whose duties or functions relate to the determination and recommendation of securities trades made with respect to the U.S. clients, or who have access to any information concerning securities being recommended to U.S. clients prior to dissemination of such recommendations:

Will be treated as “associated persons” of the registered adviser andShould be treated, when applicable, as “supervised persons”or “access persons” under the registered adviser’s code of ethics and policies and procedures

33

VII. Regulation Lite and Participating Affiliates (cont.)

Participating affiliate must maintain certain records required by the Advisers Act

For all transactions the participating affiliate must maintain the records required by Advisers Act Rule 204-2(a)(1), (2), (4), (5) and (6) With respect to transactions involving U.S. clients and all related transactions, the participating affiliate must retain records of the type described in Advisers Act Rule 204–2(a)(3) and (7)

All the books and records must be maintained and preserved:in an easily accessible place in the country where such records are kept andfor a period of not less than five years from the end of the fiscal year during which the last entry was made on such book or record

To the extent that any books and records are not kept in English, the participating affiliate must translate records intoEnglish upon reasonable advance request by the SEC

34

VII. Regulation Lite and Participating Affiliates (cont.)Participating affiliate must agree to:

Provide above records to the SEC staff upon receipt of an administrative subpoena, demand or a request for voluntary cooperation made during a routine or special inspection or otherwiseMake available for testimony or questioning by the SEC such personnel (other than clerical or ministerial personnel) identified by the SEC as having access to or having been involved in giving advice to be used for or on behalf of the registered adviser’s U.S. clients or related transactions

Testimony or questioning takes place at such place as the SEC may designate in the U.S. or, at the SEC’s option, in the country where the personnel resideDoes not require personnel to testify with respect to the identity of non-U.S. clients

Authorize all personnel to testify about all advice to be used for or on behalf of the U.S. clients of the registered adviser and any related transactionsNot to contest the validity of administrative subpoenas for testimony or documents (except with respect to the identity of non-U.S. clients of participating affiliate) under any non-U.S. laws or regulations

35

VII. Regulation Lite and Participating Affiliates (cont.)

Many registered advisers enter into agreements with participating affiliates that intend to provide advisory services with respect to the registered adviser’s U.S. clients These agreements specifically address each topic listed above and require the participating affiliate to make representations regarding such topics

36

VII. Regulation Lite and Participating Affiliates (cont.)

Participating AffiliatesIt is unclear whether the SEC staff will confirm that the Unibanco guidance continues to applyIn the release proposing the private adviser exemption and foreign private adviser exemption, the SEC requested comment on this guidance in light of the new exemptions

37

VIII. What’s Involved With SEC RegistrationThe SEC registration process will take 3-6 months, so advisers need to start planning now

Fund managers will have to be registered by July 21, 2011, and private fund managers will have to make the applicable filings by August 20, 2011, unless the deadlines are postponed

Once an adviser has filed with the SEC, the SEC has 45 days either to approve registration or take action to deny it

This means that, unless the deadline is postponed, you must submit your registration filing by no later than the beginning of June

Once your registration becomes effective, you must be in full compliance with the Advisers Act

38

VIII. What’s Involved With SEC Registration (cont.)

To prepare for registration, each adviser will have to prepare aForm ADV (SEC filing) as well as a compliance manual and code of ethics

These are complicated and interdependent documents that will have to be tailored to the adviser’s operations and implemented in practice

Larger and more complex advisers may have to restructure some of their business operations to complyFund documents may need to be reviewed and revised

e.g., subscription documents questionnaire must address “qualified client” status to receive performance allocation or carried interest

39

VIII. What’s Involved With SEC Registration (cont.)

Part 1 – SEC’s Examination BlueprintGeneral identifying information about your firm, advisory business (including employees, clients, compensation, assets under management, advisory activities and other business activities), financial industry affiliations, participation or interest in client transactions, custody, control persons and ownership and disciplinary history

Part 2 – Client BrochurePart 2A – plain English disclosure about your business practices, fees, investment strategies and risks, conflicts of interest and disciplinary informationPart 2B – supplement focused on advisory personnel

40

VIII. What’s Involved With SEC Registration (cont.)

Part 1A and 2A are filed and maintained online through the IARD, a national electronic depository

Requires setting up an account and getting a numberPart 1A and 2A are publicly available

Annual filing and delivery requirementsMust amend if materially inaccurate (and redeliver if change to disciplinary information)

41

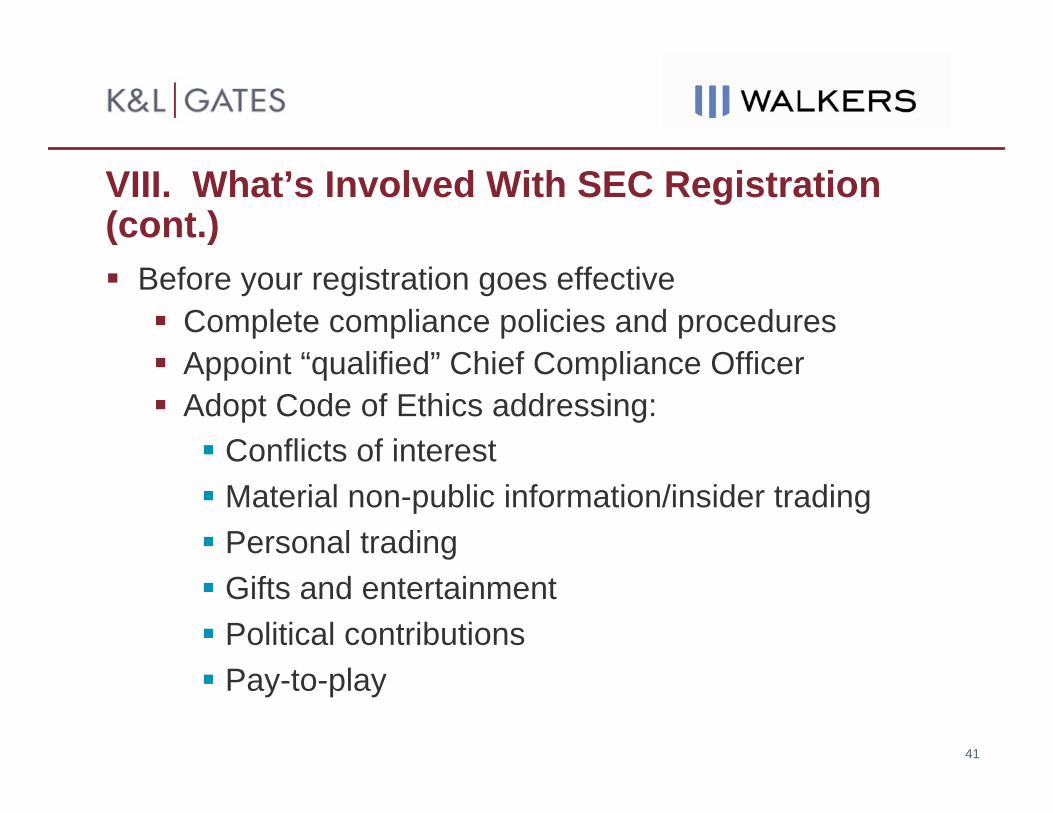

VIII. What’s Involved With SEC Registration (cont.)

Before your registration goes effectiveComplete compliance policies and proceduresAppoint “qualified” Chief Compliance OfficerAdopt Code of Ethics addressing:

Conflicts of interestMaterial non-public information/insider tradingPersonal tradingGifts and entertainmentPolitical contributionsPay-to-play

42

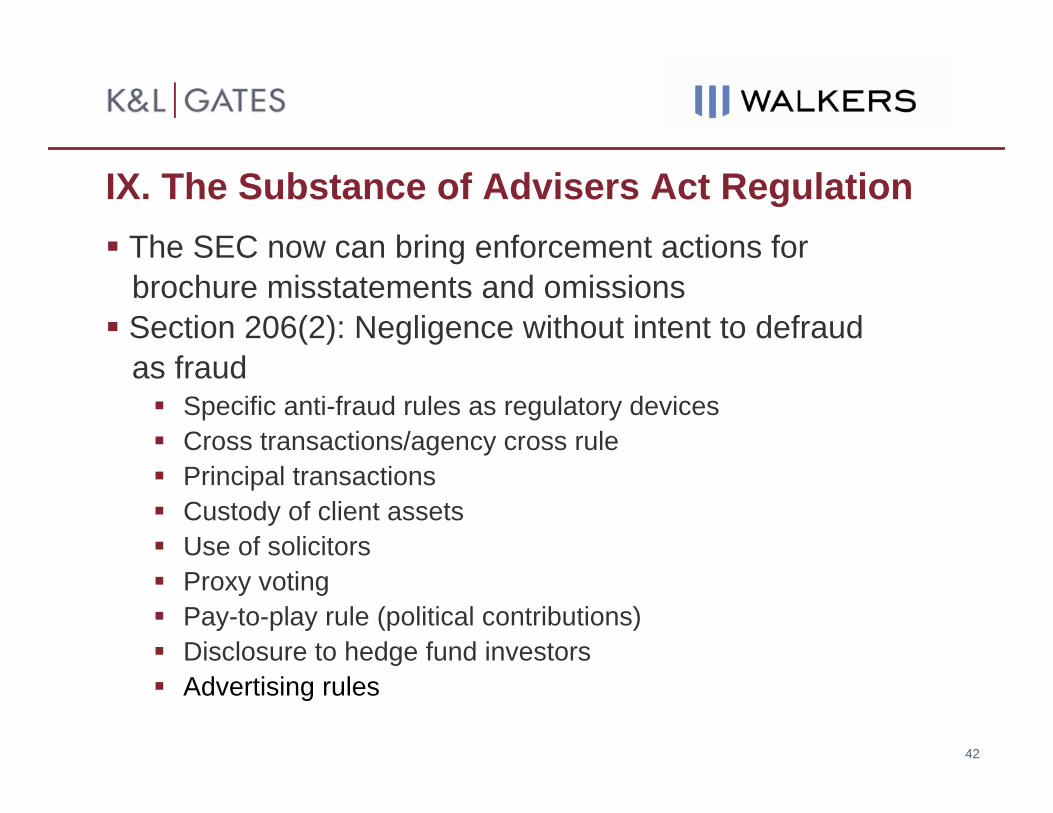

IX. The Substance of Advisers Act RegulationThe SEC now can bring enforcement actions forbrochure misstatements and omissionsSection 206(2): Negligence without intent to defraud as fraud

Specific anti-fraud rules as regulatory devicesCross transactions/agency cross rulePrincipal transactionsCustody of client assetsUse of solicitorsProxy votingPay-to-play rule (political contributions)Disclosure to hedge fund investorsAdvertising rules

43

IX. The Substance of Advisers Act Regulation (cont.)

Specific GuidanceSection 206 (general antifraud provision of Advisers Act)Rule 206(4)-1 (SEC advertising rule)No-action lettersEnforced through SEC inspections and enforcement actionsDisclosure rules not calculation rules

44

IX. The Substance of Advisers Act Regulation (cont.)What is an Investment Adviser Advertisement?

“Any written communication addressed to more than one person” that offers investment advisory services related to securitiesIncludes communications designed to maintain existing clients or solicit new clients Includes electronic and broadcast advertisementsExample enforcement action:

In re Seaboard Investment Advisers Inc.Advertised performance from a previous employer without disclosing the source or providing documentation

45

X. SEC Inspections

• Three Types of Inspections• A routine examination is conducted on a periodic basis• A “for cause” examination is conducted upon suspicion

of a problem at a firm and is typically unannounced and

• A sweep examination is a special review focusing on a specific industry issue

• A firm undergoing an examination will not typically be privy to the type of examination taking place, but the firm may inquire as to the nature of the exam in the entrance interview (discussed in more detail below)

• Examinations may be announced or unannounced

46

X. SEC Inspections (cont.)

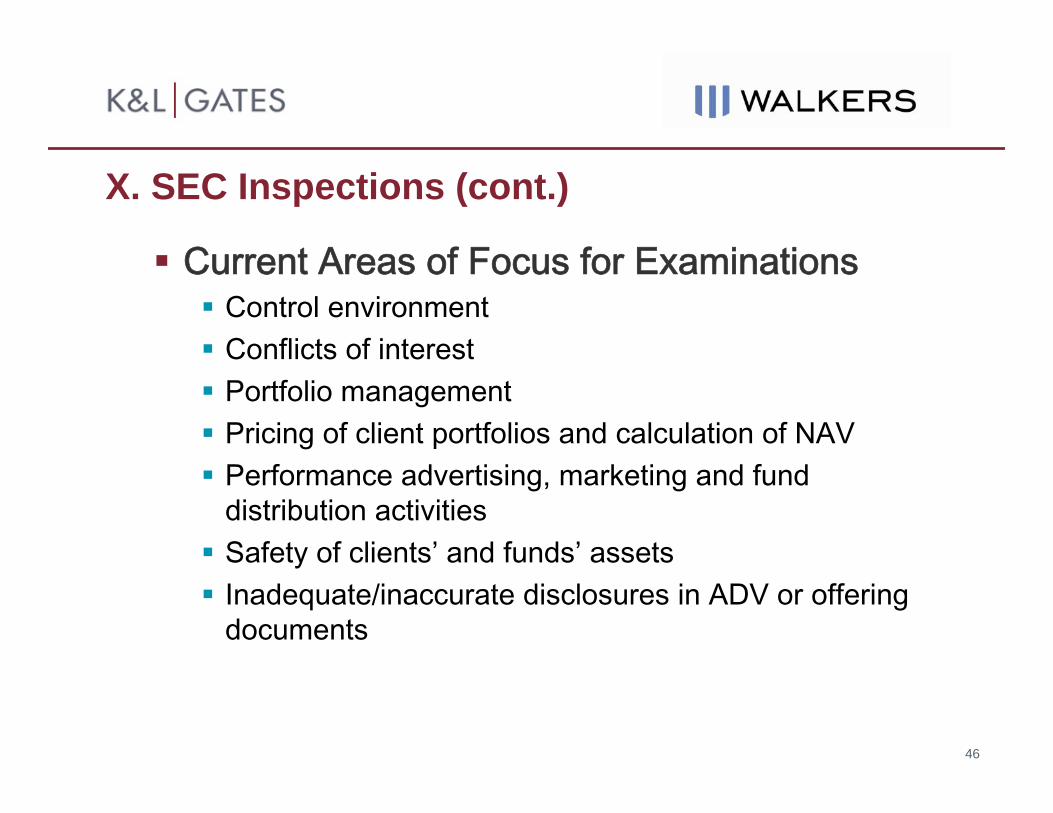

Current Areas of Focus for ExaminationsControl environmentConflicts of interestPortfolio managementPricing of client portfolios and calculation of NAVPerformance advertising, marketing and fund distribution activitiesSafety of clients’ and funds’ assetsInadequate/inaccurate disclosures in ADV or offering documents

47

X. SEC Inspections (cont.)

Other Areas of Interest for SEC ExamsBooks and recordsReferral arrangements (solicitors/consultants)Use of client commissions (soft dollars)Recidivism (breach logs)Prime brokerage arrangementsTrading and allocation proceduresRevenue sharingE-mail retention

48

X. SEC Inspections (cont.)

Producing Information to the SEC StaffSEC staff will request information in a number of forms including:

Document requestsInterviewsDemonstrations/walk-through

Important to request confidential treatment of materials produced

49

X. SEC Inspections (cont.)

Attorney-Client PrivilegeAn adviser is not required to produce documents that are subject to the attorney-client privilege Generally, the attorney-client privilege is applicable to:

CommunicationsBetween the attorney and clientMade in confidence andFor the purpose of seeking or obtaining legal assistance

50

X. SEC Inspections (cont.)

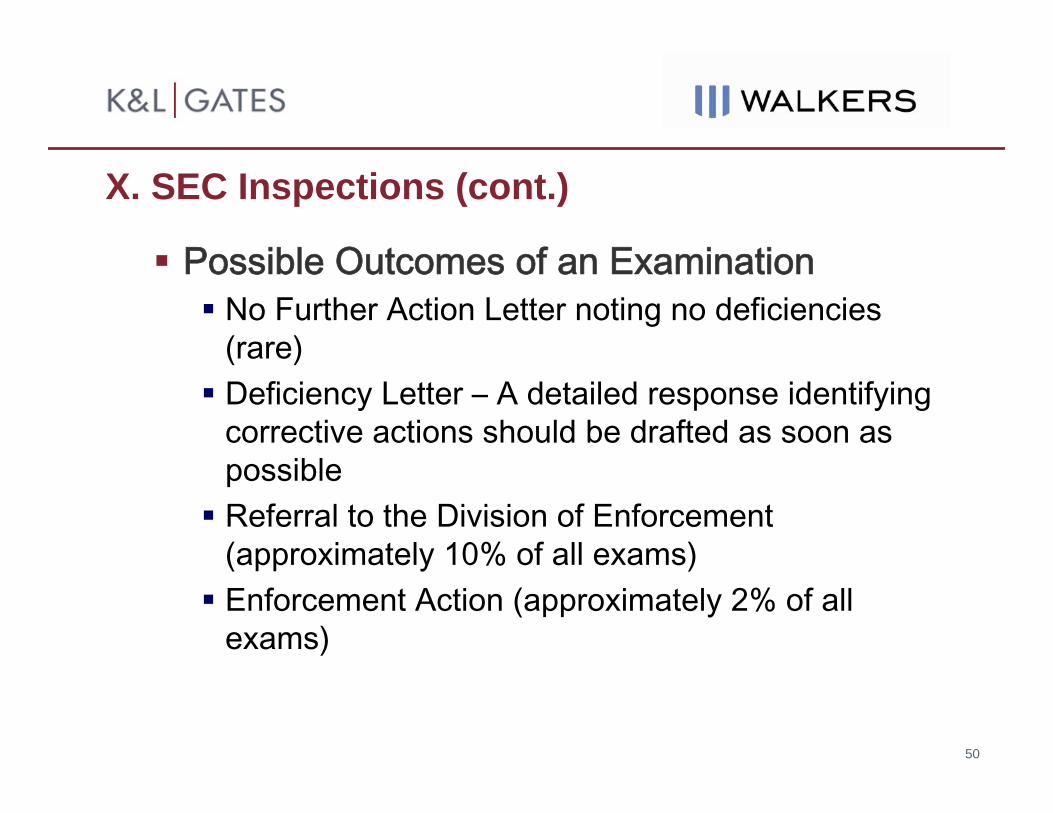

Possible Outcomes of an ExaminationNo Further Action Letter noting no deficiencies (rare)Deficiency Letter – A detailed response identifying corrective actions should be drafted as soon as possibleReferral to the Division of Enforcement (approximately 10% of all exams)Enforcement Action (approximately 2% of all exams)

51

X. SEC Inspections (cont.)

After the ExaminationRespond promptly to any deficiency letterTake any necessary corrective actionPrepare for next examination

52

XI. Conclusions – What Registration Means

Your personal affairs will be effected:Personal trading/giftsPolitical contributions to U.S candidates

Day-to-day conduct of your business will change:e.g., books and recordsConflicts of interest Living with your compliance policies

Client acquisition will change:Contractual provisions and feesAdvertising processThird-party solicitors

Accountability to a regulatorInspection/Enforcement

53

Stuart E. Fross, Partner, Boston, MAStuart Fross is a partner in K&L Gates' Boston office where he concentrates his practice on securities as part of the Investment Management Practice Group. Mr. Fross is involved in all aspects of fund management for both domestic and international funds, including formation of new funds, strategic planning and contract matters, with particular focus on securities regulatory compliance.

Mr. Fross assists clients with fund management operations, fund formation and fund distribution with respect to U.S. registered open-end funds, U.S. registered closed end funds, U.S. exchange traded funds, bank collective investment funds, Canadian 81-102 Funds, UCITS funds sold in the European Union, the U.S., South America, Japan, Taiwan and Hong Kong, as well as private funds, organized in the U.S. and offshore. Mr. Fross has extensive experience in equity, high-income and fixed income trading operations, as well as development of ETFs.

Email: [email protected]: (617) 261-3135

54

Cary J. Meer, Partner, Washington, D.C.Ms. Meer advises hedge fund and fund-of-funds managers on the organization and structuring of private investment funds, as well as on compliance issues, including under the Investment Advisers Act of 1940 and whether their futures-related trading or advice brings them within the regulatory structure of the Commodity Exchange Act. She also provides advice to non-U.S. managers and funds regarding marketing in the United States. She is also active innegotiating and structuring acquisitions and dispositions of hedge fund managers, investment advisers, broker-dealers, administrators and other financial services firms, and strategicalliances and joint-ventures with financial services.

Email: [email protected]: (202) 778-9107

55

Ingrid Pierce, Partner, Cayman IslandsIngrid Pierce is a partner in the Global Hedge Fund Group and is head of the Cayman Hedge Fund Practice of Walkers. She has over 18 years’ experience in advising fiduciaries and represents major institutions, fund managers, directors and trustees in allaspects of investment funds, including structuring and ongoing operations. Ingrid advises on directors’ duties and responsibilities, indemnities, confidentiality laws and issues related to electronic communication. She has particular expertise in advising funds onmanaging distress in volatile markets. She regularly advises some of the largest financial institutions on their stable of Cayman Islands funds and recently acted as counsel to significant investors and managers in connection with the restructuring and winding down of various high profile funds.

Email: [email protected]: +1 345 814 4667

56

Jennifer Thomson, Partner, Cayman IslandsJen Thomson is a partner in Walkers' Global Investment FundsGroup. She specialises in both hedge funds and private equity funds. Jen acts for several large UK and US-based investment managers, including fund-of-funds managers, in connection with the development, launch and operation of their Cayman Islands investment fund products, working extensively with their associated administrators, listing agents and other service providers.

Prior to joining Walkers in 1999, Jen practised for four years with Maclay Murray & Spens, a leading Scottish corporate firm.

Email: [email protected]: +1 345 914 4280