Embed Size (px)

Citation preview

The Risk of Reform: How US Healthcare Systems are Responding

Paul Posey CEO, Ascension Care Management & President, Risk Services

Transforming Healthcare - Health Policy, Digital Health and Data Privacy: Who pays the bill? Swiss Re Center for Global Dialogue

2

We’re going to make American Healthcare Great Again!!

Paul Posey @pposeyjr

4

Ascension - Continuum of Care

5

2,500 Sites of Care

1,798 Ambulatory

Care and Diagnostic

Sites 95

Emergency Service Sites

221 Post Acute

Service Sites

60 Senior Care and Living Facilities

231 Community

Services Sites and Programs

141 Hospitals

6

Ascension – US Healthcare Presence

Sites of Care 2,500

Acute Care Hospitals 111

Rehabilitation Hospitals 6

Behavioral Health Hospitals 9

Long-Term Acute Care Hospitals 2

Joint Venture Hospitals (<50% ownership) 13

Available Beds 22,416

Associates 160,000

Affiliated Physicians 36,000

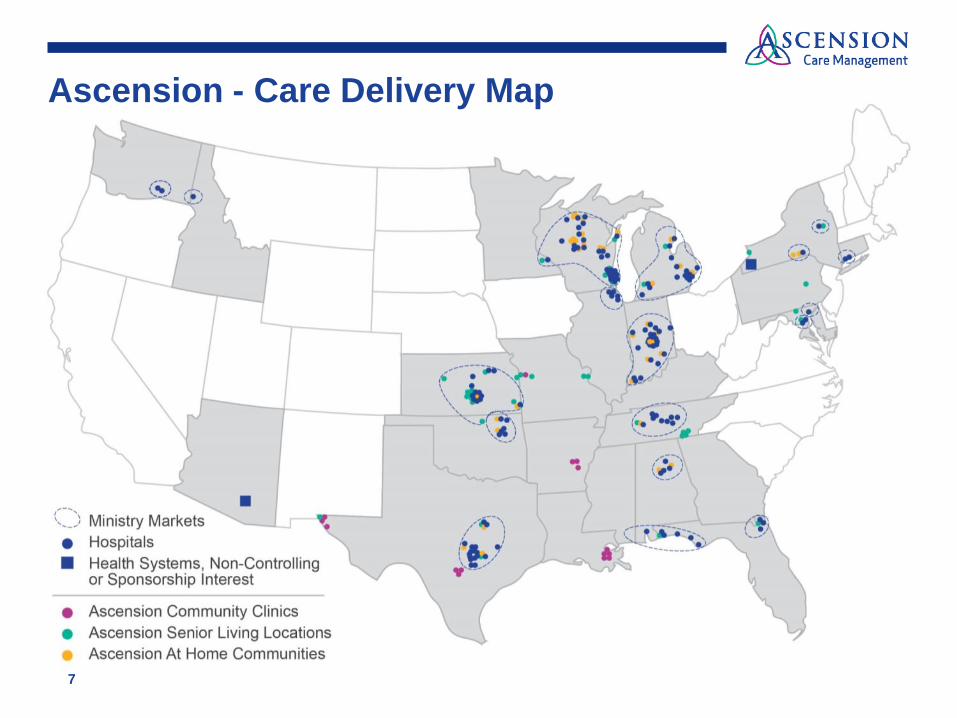

Ascension - Care Delivery Map

7

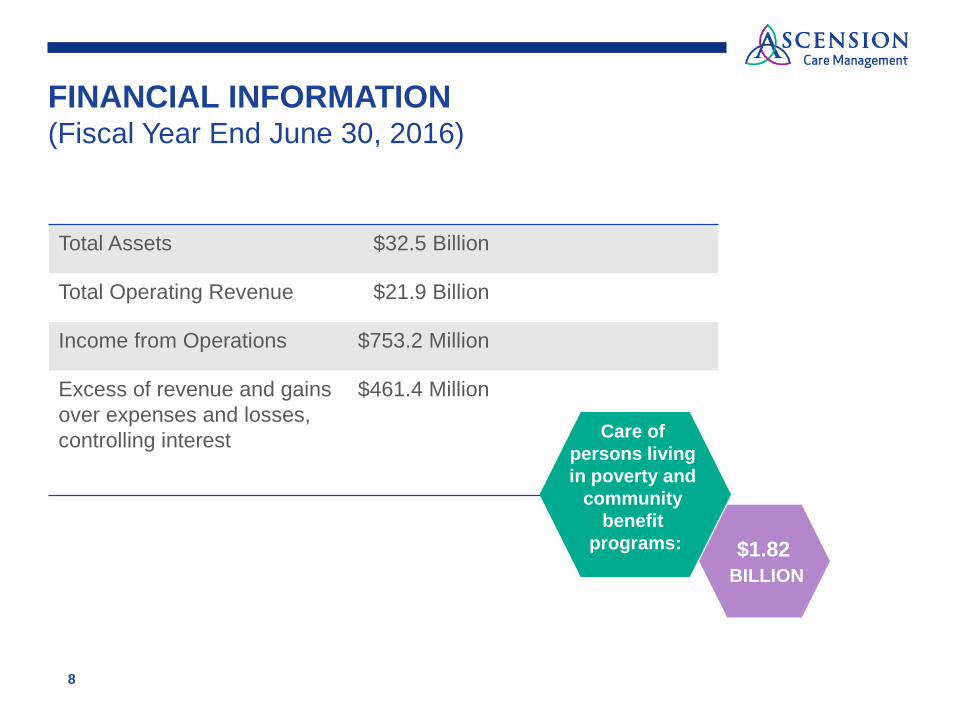

8

FINANCIAL INFORMATION (Fiscal Year End June 30, 2016)

Total Assets $32.5 Billion

Total Operating Revenue $21.9 Billion

Income from Operations $753.2 Million

Excess of revenue and gains $461.4 Million over expenses and losses, controlling interest

Care of persons living in poverty and

community benefit

programs:

$1.82 BILLION

*

U.S. Healthcare Trends Impacts on Payers and Providers

Spending Back on the Rise

© The Advisory Board Company - advisory.com 10

6.5% 6.3%

4.8% 3.8% 3.9% 3.9% 4.1%

3.6%

5.0% 5.8%

0%1%2%3%4%5%6%7%8%9%

10%

2006 2007 2008 2009 2010 2011 2012 2013 2014 2015

“U.S. Health-Care Spending Is on the Rise Again”

“Health care spending growth hits 10-year high”

“Health Spending Is Rising More Sharply Again”

US Healthcare - 2015 17.8% of GDP $3.2 Trillion

11

Crisis in the Making for Payers and Providers

12

2008 Stock Market Crash • Reserve positions deteriorate • Investment income erodes

2009-10 Economic Recession • Increasing unemployment • Employer-sponsored benefits cut

2010 “Obamacare” Passed • Substantial Cuts to Medicare Advantage Programs • Minimum Medical Loss Ratios Limit Profits • Long term reductions to hospital payments

Patient Protection and Affordable Care Act Obamacare

• Many More Americans Have Health Insurance

• Individuals Can Now Obtain Insurance

• Preventive and Wellness Visits under Medicare

• 30M (10%) of Americans Still Uninsured

• 40-50% lack liquid assets to cover deductibles1

• Carriers pulling out of Exchanges

13

1 Kaiser Family Foundation -Consumer Assets and Patient Cost Sharing Mar 11, 2015 | Gary Claxton, Matthew Rae, and Nirmita Panchal

Patient Protection and Affordable Care Act Health Plan Impacts

Children on Parents’ Plan

to Age 26

No Lifetime Limits on Coverage

Individual Mandates

Minimum MLR’s

No Pre-Existing

Condition Exclusions

No Health Based

Underwriting

14

15 Source: Oliver Wyman 2015

Healthcare Reform – Massive Shift to Risk Provider Impacts

16

Healthcare Reform – Medicare Risk Models Provider Impacts

Bundled Payments

Shared Savings

Shared Risk

Full Risk

• Comprehensive Primary Care Plus (CPC+)

• Medicare Shared Savings Program (MSSP) Track 1

• MSSP Track 1+4

• MSSP Track 2

• MSSP Track 3

• Next Generation ACO Model (NGACO) (80% share rate)

• NGACO (100% share rate)

PCMH Payments

• BPCI1

• CJR2

• The Oncology Care Model Two-Sided Risk Arrangement

• EPM3

Alternative Payment Models

Source: HHS, “Progress Towards Achieving Better Care, Smarter Spending, Healthier People,” available at: http://www.hhs.gov/, accessed February 2015; Health Care Advisory Board interviews and analysis. © The Advisory Board - 2017

1)Bundled Payments for Care Improvement. 2)Comprehensive Care for Joint Replacement Model. 3)Episode Payment Models. 4)MACRA Final Rule established Track 1+ with details to follow, set to start in 2018.

50% HHS goal for percent of

Medicare payment in alternative models by 2018

February 8, 2017 17

Medicare Value Based Care Purchasing Programs

3,087 hospitals in VBP program

1,700 hospitals received bonus payment

792 hospitals received net payment increases

After Accounting for Penalties1 Few Hospitals Receive Bonuses

Source: Rau J, “1,700 Hospitals Win Quality Bonuses From Medicare, But Most Will Never Collect,” Kaiser Health News, January 22, 2015, available at: kaiserhealthnews.org; Health Care Advisory Board interviews and analysis. © The Advisory Board - 2017

1)Hospital-Acquired Condition Reduction Program, Hospital Readmissions Reduction Program.

February 8, 2017 18

Accountable Care Organizations Mixed Results for Providers

30%

21%

48%

MSSP ACOs Share in Savings 2015

Held Spending Below Benchmark, Earned Shared Savings

Reduced Spending, Did Not Qualify

for Shared Savings

Did Not Hold Spending Below Benchmark

Source: CMS. “Fast Facts: All Medicare Shared Savings Program (Shared Savings Program) ACOs,” April 2016, “Pioneer ACO Model Frequently Asked Questions,” May 2016, available at www.cms.gov; Kocot and White. Health Affairs Blog. “Medicare ACOs: Incremental Progress, But Performance Varies,” September 2016, available at www.healthaffairs.org/blog; Health Care Advisory Board interviews and analysis.

1)Medicare Shared Savings Program. 2)Percentages may not add to 100 due

to rounding.

Medicare Access and CHIP Reauthorization Act “MACRA”

19 Source: McKinsey Medicare Growth Model. Includes Medicare and dual eligible

All providers will now be “at risk” with CMS for Medicare fee-for-service patients 1 Preparatory time is short—the first performance period starts in January 2017 2 Small providers will be disproportionately affected by the change in reimbursement 3 CMS wants other insurers to follow its lead and has incorporated many “all insurer” components 4 There will likely be second order implications (e.g., physician practice consolidation) 5

The Shift to Risk Old Ways of Looking at New Problems

Managing Complex Risk Systems is Not New

9,535

8,513

7,553

6,337 6,210 6,272 6,368 6,241 6,147 5,815 5,728 5,642 5,642

4,000

5,000

6,000

7,000

8,000

9,000

10,000

FY06 FY07 FY08 FY09 FY10 FY11 FY12 FY13 FY14 FY15 FY16 FY17 FY18

Ascension Professional Liability Cost Per Occupied Bed Equivalent

Loss cost per exposure (at $1 million)

40.8% Reduction

21

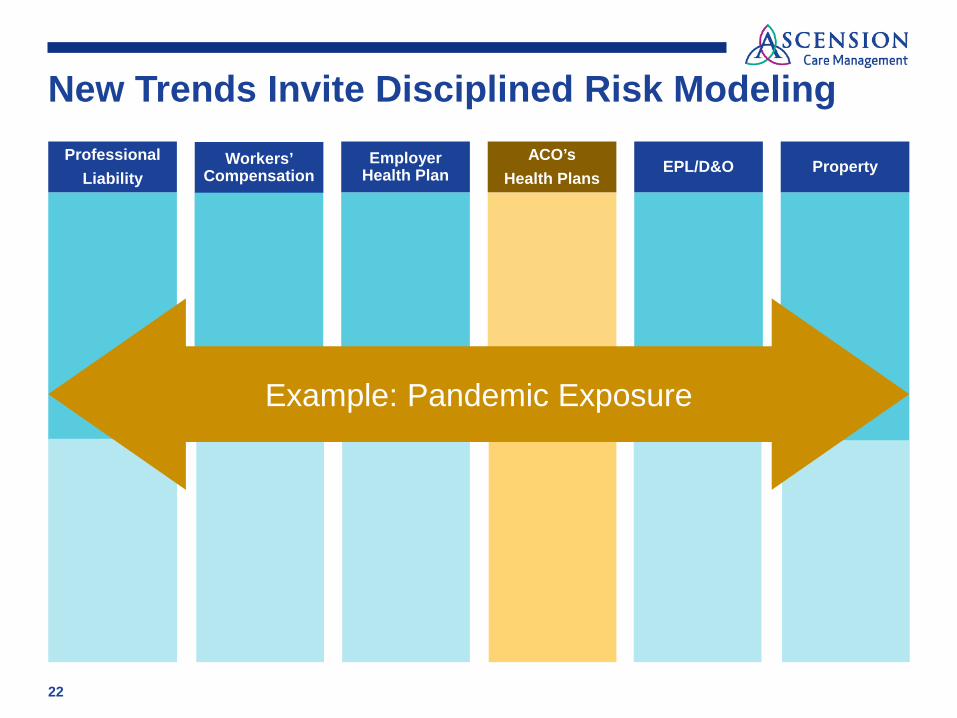

Professional Liability

Workers’ Compensation

Employer Health Plan

ACO’s Health Plans

EPL/D&O Property

Example: Pandemic Exposure

New Trends Invite Disciplined Risk Modeling

22

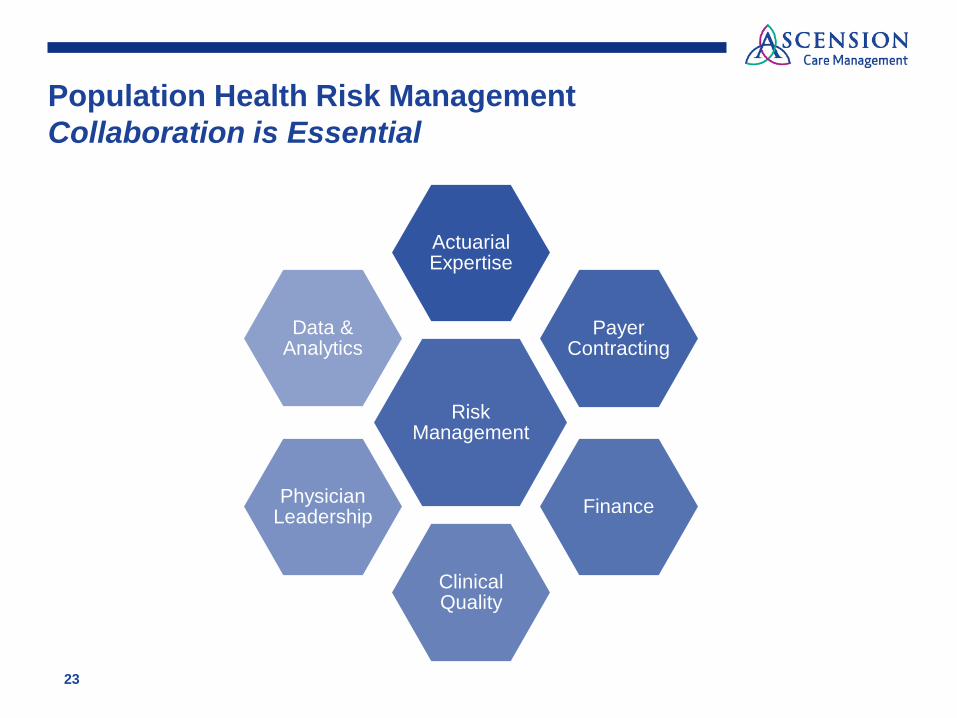

Population Health Risk Management Collaboration is Essential

23

Risk Management

Actuarial Expertise

Payer Contracting

Finance

Clinical Quality

Physician Leadership

Data & Analytics

24

The Path to Risk Sharing: System Integration ▪ Provider coordination and workflow technology

tools ▪ Chronic disease management programs with

standardized protocols

▪ Information and transparency tools

▪ Patient access tools ▪ Patient experience tools (e.g.,

satisfaction assessments) ▪ Customer service / navigation

(e.g., 24/7 hotline to answer patient clinical questions)

▪ Social service access and coordination

▪ Payer-provider incentive models & managements

▪ Provider-physicians incentive models & management

▪ Provider & physician performance management (e.g. performance reviews)

▪ Provider risk readiness assessment

▪ Foundational analytics – risk adjustment, risk stratification, patient attribution, care gap

▪ Governance, strategy and alignment across the network

▪ Ambulatory care management / practice transformation (e.g. care coordinators, practice coaches)

▪ Acute & post-acute care coordination (inpatient / discharge care protocols)

▪ Documentation and accurate coding (training, reports, reviews, and appropriate risk scoring)

▪ Cost and utilization analytics ▪ Quality and outcome analytics ▪ Physician reporting – e.g.,

performance reports, care gap reports, specialist profiles to PCPs

Source: McKinsey Medicare Growth Model. Includes Medicare and dual eligibles

What How Why

26

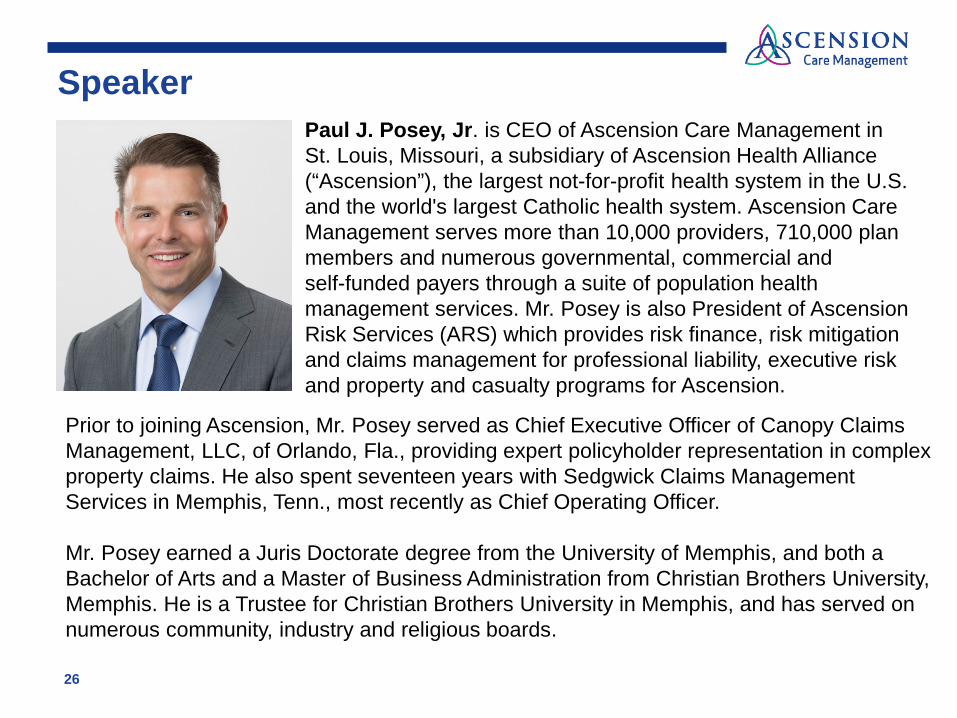

Paul J. Posey, Jr. is CEO of Ascension Care Management in St. Louis, Missouri, a subsidiary of Ascension Health Alliance (“Ascension”), the largest not-for-profit health system in the U.S. and the world's largest Catholic health system. Ascension Care Management serves more than 10,000 providers, 710,000 plan members and numerous governmental, commercial and self-funded payers through a suite of population health management services. Mr. Posey is also President of Ascension Risk Services (ARS) which provides risk finance, risk mitigation and claims management for professional liability, executive risk and property and casualty programs for Ascension.

Prior to joining Ascension, Mr. Posey served as Chief Executive Officer of Canopy Claims Management, LLC, of Orlando, Fla., providing expert policyholder representation in complex property claims. He also spent seventeen years with Sedgwick Claims Management Services in Memphis, Tenn., most recently as Chief Operating Officer. Mr. Posey earned a Juris Doctorate degree from the University of Memphis, and both a Bachelor of Arts and a Master of Business Administration from Christian Brothers University, Memphis. He is a Trustee for Christian Brothers University in Memphis, and has served on numerous community, industry and religious boards.

Speaker

Basic Copyright Notice & Disclaimer

©2017 This presentation is copyright protected. All rights reserved. You may download or print out a hard copy for your private or internal use. You are not permitted to create any modifications or derivatives of this presentation without the prior written permission of the copyright owner.

This presentation is for information purposes only and contains non-binding indications. Any opinions or views expressed are of the author and do not necessarily represent those of Swiss Re. Swiss Re makes no warranties or representations as to the accuracy, comprehensiveness, timeliness or suitability of this presentation for a particular purpose. Anyone shall at its own risk interpret and employ this presentation without relying on it in isolation. In no event will Swiss Re be liable for any loss or damages of any kind, including any direct, indirect or consequential damages, arising out of or in connection with the use of this presentation.