Embed Size (px)

Citation preview

_________________________________________________________________________________________________ The CGIAR Systemwide Program on Collective Action and Property Rights (CAPRi) is an initiative of the 15 centers that belong to the Consultative Group on International Agricultural Research. The initiative promotes comparative research on the role played by property rights and collective action institutions in shaping the efficiency, sustainability, and equity of natural resource systems. CAPRi’s Secretariat is hosted by the International Food Policy Research Institute’s (IFPRI) Environment and Production Technology Division (www.ifpri.org). CAPRi Working Papers contain preliminary material and research results and are circulated prior to a full peer review in order to stimulate discussion and critical comment. It is expected that most Working Papers will eventually be published in some other form, and that their content may also be revised. http://dx.doi.org/10.2499/CAPRiWP70. Copyright © August 2007. International Food Policy Research Institute. All rights reserved. Sections of this material may be reproduced for personal and not-for-profit use without the express written permission of but with acknowledgment to IFPRI. To reproduce the material contained herein for profit or commercial use requires express written permission. To obtain permission to reprint, contact the IFPRI Communications Division at [email protected]. _________________________________________________________________________________________________

CGIAR Systemwide Program on Collective Action and Property Rights (CAPRi) c/o INTERNATIONAL FOOD POLICY RESEARCH INSTITUTE

2033 K Street NW, Washington, DC 20006-1002 USA • T +1 202.862.5600 • F +1 202.467.4439 • www.capri.cgiar.org

CAPRi Working Paper No. 70 • OCTOBER 2007

The Role of Public-Private Partnerships and Collective Action in Ensuring Smallholder Participation in High Value

Fruit and Vegetable Supply Chains

Clare Narrod and Devesh Roy, International Food Policy Research Institute,

Julius Okello, University of Nairobi,

Belem Avendaño, Universidad Autónoma de Baja California,

Karl Rich, International Livestock Research Institute, and

Amit Thorat, Jawaharlal Nehru University

Research Workshop on Collective Action and Market Access for Smallholders October 2-5, 2006 - Cali, Colombia

ABSTRACT

Many developing countries have moved into the production of non-traditional

agricultural products to diversify their exports and increase foreign currency earnings. Accessing

developed country markets and urban domestic markets requires meeting the food safety

requirements due to several demand and supply side factors. Food retailers have developed

protocols relating to pesticide residues, field and packinghouse operations, and traceability. In this

changing scenario where food safety requirements are getting increasingly stringent, there are

worries regarding the livelihood of the poor since companies that establish production centers in

LDCs might exclude them. Poor producers face problems of how to produce safe food, be

recognized as producing safe food, identify cost-effective technologies for reducing risk, and be

competitive with larger producers with advantage of economies of scale in compliance with food

safety requirements. In enabling the smallholders to remain competitive in such a system, new

institutional arrangements are required. In particular, public-private partnerships can play a key

role in creating farm to fork linkages that can satisfy the market demands for food safety while

retaining smallholders in the supply chain. Furthermore, organized producer groups monitoring

their own food safety requirements through collective action often become attractive to buyers

who are looking for ways to ensure traceability and reduce transaction costs. This paper compares

how small producers of different fruit and vegetable products in different countries have coped

with increased demands for food safety from their main export markets. These commodities are

Kenyan green beans, Mexican cantaloupes, and Indian grapes.

Key words: food safety, supply chain management, public private partnerships, collective action,

public and private standards, traceability

TABLE OF CONTENTS

1. Introduction ................................................................................................................................ 1

2. Growth of the Supply of Fruits and Vegetables and the Response of LDCS .............................. 4

3. Development of Food Safety Standards and Regulations .......................................................... 6

4. Role of Supply Chains in the Delivery of Fruits and Vegetables ............................................... 8

5. Fruit and Vegetable Production and their Supply Chains from Three Case Studies................. 14

6. Difficulties Smallholders Have in Participating in these Supply Chains ................................. 26

7. Role of Various Institutions in Involving Smallholders in these Markets ................................ 29

8. Conclusions .............................................................................................................................. 36

References ..................................................................................................................................... 38

The Role of Public-Private Partnerships and Collective Action in Ensuring Smallholder Participation in High Value Fruit

and Vegetable Supply Chains

Clare Narrod and Devesh Roy,1 Julius Okello,2 Belem Avendaño,3

Karl Rich,4 and Amit Thorat5

1. INTRODUCTION

Many countries in Africa, Asia, and Latin America have moved into the production of

non-traditional agricultural products to diversify their agricultural exports and increase foreign

exchange earnings. High altitude regions in a number of African and Latin American countries

enable the growth of cool season crops year round, providing an opportunity to export these

products to developed countries. Similarly, tropical regions in many Latin American and Asian

countries enable the growth of high value fruits (like grapes, bananas, etc.).

Currently, most non-traditional crops in Africa are produced for export to the European

markets, while in Latin America most non-traditional crops are exported to North America.

Products from Asia go either to European or North American markets, depending on

transportation costs, market competition, and whether the product adheres to the food safety

requirements of the destination markets. Both national and international firms that source supplies

from these countries have high standards and provide technical assistance to their suppliers to

ensure the delivery of products with certain safety attributes to high-end markets.

Food safety has received heightened attention in developed and developing countries.

This has followed from an increased demand for safe food by households with rapidly rising

incomes, technological improvements in measuring contaminants, the expansion in the set of food

1 International Food Policy Research Institute, Markets, Trade, and Institutions Division, Research Fellow,

[email protected] and [email protected].

2 University of Nairobi

3 la Facultad de Economía Universidad Autónoma de Baja California, Profesor-Investigador de la Facultad

de Economía Universidad Autónoma de Baja California

4 International Livestock Research Institute, Scientist (Agricultural Economist)International Livestock

Research Institute

5 Jawaharlal Nehru University graduate student

CAPRI WORKING PAPER NO. 70 OCTOBER 2007

2

exporting countries, and increased media and consumer attention on the risks of food borne

illnesses associated with recent food scares (e.g., salmonella in cantaloupe, pesticide residues in

green beans and grapes). In response, food retailers and food service firms in developed countries

(DCs) have created private protocols relating to pesticide residues, field and packinghouse

operations, and traceability. Likewise, governments in both DC and LDCs have responded with

voluntary and occasionally mandatory programs for food safety. Among the examples of such

initiatives are the programs to register pesticides in Morocco (World Bank 2005) and the

implementation of Hazard Analysis Critical Control Points (HAACP) programs in China to

reduce sanitary and phytosanitary problems in canned food, aquatic products, meat and meat

products, frozen vegetables, fruit/vegetable juice, and frozen convenience food containing meat

or aquatic products (Dong and Jensen 2004).

While the development of food safety standards has reduced the risks from foods, it has

often come at the cost of temporary import bans, particularly of LDC food exports to DC markets.

During May 1999-April 2000, the number of detentions by the US originating from 52 countries

was 9,875, with India accounting for the most detentions. During December 2001-November

2002, 997 detentions from India resulted in 2.6 million dollars worth of rejections of Indian

exports (Mehta and George 2003). Recently, between February 2006 and January 2007, the

number of detentions was 16,818 (FDA 2007). India again faced the highest number of

detentions with a total of 2,085 detentions.

The increased food safety standards in both developed and developing countries can

potentially exclude small farmers who face four distinct problems: 1) how to produce safe food;

2) how to be recognized as producing safe food; 3) how to identify cost-effective technologies for

reducing risk; and 4) how to be competitive with larger producers (Narrod et al.. 2005). As supply

chains become more complex, supply chain management (SCM) plays an increasingly important

role in the delivery of high-value agriculture (HVA) products to distant markets. Given the

perishable nature of HVA and the demand for quality and safety attributes, relationships,

networks, skills, and coordination mechanisms are needed to manage the flow of products

between intermediaries and ensure that the quality specifications are met. A variety of

institutional arrangements such as collective action (CA) and forms of public-private partnerships

(PPPs) can play a key role in creating such links. Further, producer groups organizing through

CAPRI WORKING PAPER NO. 70 OCTOBER 2007

3

cooperatives and monitoring their own food safety requirements through CA often become

attractive to buyers who are looking for ways to ensure traceability.

This paper compares how small producers of fruits and vegetables (F & V) in different

countries have responded to increased demand for food safety from the markets they export to.

The three cases are green beans in Kenya, cantaloupe in Mexico, and grapes in India. These cases

differ in the ways in which they have adapted to the changes in international food safety standards

(IFSS) and the types of institutions that have emerged to ensure compliance with IFSS.

The green bean exports from Africa that go to the European supermarkets are mostly in a

pre-packed, pre-cut form, which normally requires a large investment to coordinate supply and

upgrade hygienic conditions at the farm/packing house. It moreover requires a mechanism such as

third party certification to ensure that specific standards are met. Findings from Okello (2005)

suggest that CA was helpful for small farmers in overcoming entry barriers created by IFSS.

A similar success story in horticultural exports from India is that of a marketing partner

named Mahagrapes to a collection of cooperatives that started exporting grapes to Europe in the

early 1990s. As reported by Roy and Thorat (2006), in the first five years of exports, the

cooperatives faced extremely high rates of rejection (at times greater than 80 percent). With the

aid of the public sector, the cooperatives were able to install cold chains and pre-cooling facilities,

and facilitate high rates of information dissemination related to IFSS. Consequently, the rejection

rates came down substantially to less than 10 percent in late 90s and to less than 1 percent after

2001.

The third case based on Avendaño et al. (forthcoming) relates to the cantaloupes from

Mexico exported to the US that were implicated in food safety concerns in 2000, 2001, and 2002.

This resulted in a ban on imports from all Mexican sources in 2002. Later, the US opened the

market to selected firms with Mexican and US government approval. When the US firms began

demanding Good Agricultural Practices (GAPs) and Good Manufacturing Practices (GMPs), to

minimize microbial contamination in fresh produce, the end result was a two-tier system where

larger farmers catered to export markets and the smallholders to domestic markets. Importantly,

given that very little time has elapsed since the food safety shock, there has been an absence of

both CA and PPPs in this case.

The paper is organized as follows. Section 2 briefly discusses the growth in supply of

fruits and vegetables throughout the world over the last several decades and how less developed

CAPRI WORKING PAPER NO. 70 OCTOBER 2007

4

countries have responded. Section 3 looks at the development of various domestic and

international food safety standards (such as HACCP, traceability, supermarket code of practices)

for these suppliers. Section 4 looks at the role of supply chains in the delivery of fruits and

vegetables, and the market outcomes that are likely to prevent smallholders from accessing these

supply chains. It also briefly discusses the role played by different institutions in enabling

smallholders to access the HVA chains. Section 5 focuses on the three cases involving

smallholders. Section 6 looks at the specific difficulties smallholders face in these chains. Section

7 discusses the institutional mechanisms that have facilitated smallholders in overcoming

constraints relating to the IFSS in these specific cases. Section 8 presents the conclusions.

2. GROWTH OF THE SUPPLY OF FRUITS AND VEGETABLES AND THE RESPONSE OF LDCS

Since 1971, global agricultural exports have grown at 3.0 percent per year in real terms

compared to production growth at 0.7 percent per year thus doubling the share of production to

exports (from 19 percent in 1971 to 40 percent in 2003).6 The composition of exports has also

changed for both developed and developing countries (Minot and Roy 2006) with a shift towards

HVA products like fruits and vegetables, fish, and livestock, even though these are highly

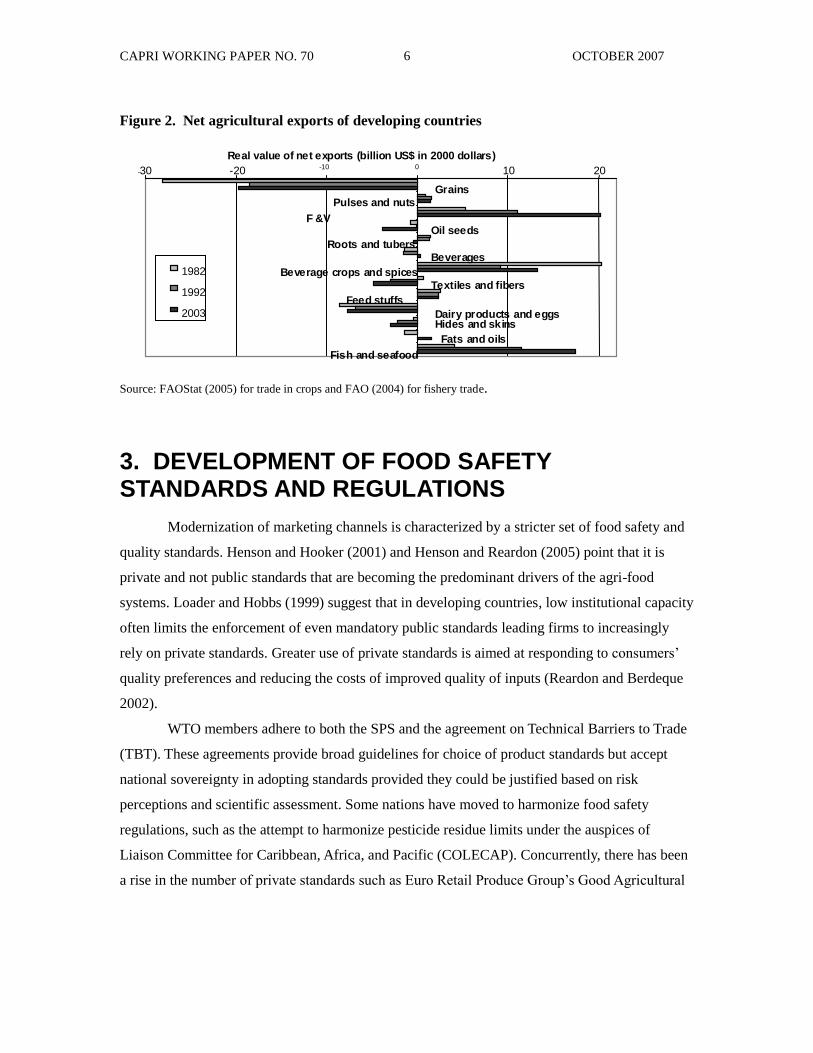

perishable and subject to stricter SPS requirements (Figures 1 and 2). In 1982, beverage crops and

spices (particularly coffee, tea, and cocoa) were the largest agricultural exports. Since then, net

exports of F&V and fish and seafood have increased almost four-fold (for F&V from US$5.3

billion in 1982 to US$20.1 billion in 2003). During this same period, fish and seafood exports

reached US$17.5 billion in 2003, becoming the second-largest component in exports. Currently,

fresh food exports account for half of all food and agriculture exports from LDCs to high income

countries; however, these products may be subject to greater food safety risks and trade barriers

arising from SPS regulations (Unnevehr 2000).

6 These calculations are based on FAO statistics for agricultural exports and the World Development

Indicators for agricultural value added and the US dollar GDP deflators.

CAPRI WORKING PAPER NO. 70 OCTOBER 2007

5

Figure 1: Composition of global agricultural exports (% of value)

10.8

0.6

9.6

4

12.9

5.7

8.5

11.4

36.4

0

5

10

15

20

25

30

35

40

45

Cer

eals

Pulse

s

Bever

ages

and

toba

cco

Anim

al veg

etable

oil

Fruits

and

veg

etab

les

Dai

ry p

rodu

cts & e

ggs

Mea

t

Fish

and

seaf

ood

Oth

er

1964-73

1974-83

1984-93

1994-2003

Source: FAOStat

Note: Crop and livestock exports from FAO statistics on primary agricultural products. Fish and seafood exports

include both processed and unprocessed

CAPRI WORKING PAPER NO. 70 OCTOBER 2007

6

Figure 2. Net agricultural exports of developing countries

-30 -20 -10 0 10 20

1

Real value of net exports (billion US$ in 2000 dollars)

1982

1992

2003

Grains

Oil seeds

Beverages

Textiles and fibers

Dairy products and eggs Hides and skins

Fats and oils

Pulses and nuts

F &V

Roots and tubers

Beverage crops and spices

Feed stuffs

Fish and seafood

Source: FAOStat (2005) for trade in crops and FAO (2004) for fishery trade.

3. DEVELOPMENT OF FOOD SAFETY STANDARDS AND REGULATIONS

Modernization of marketing channels is characterized by a stricter set of food safety and

quality standards. Henson and Hooker (2001) and Henson and Reardon (2005) point that it is

private and not public standards that are becoming the predominant drivers of the agri-food

systems. Loader and Hobbs (1999) suggest that in developing countries, low institutional capacity

often limits the enforcement of even mandatory public standards leading firms to increasingly

rely on private standards. Greater use of private standards is aimed at responding to consumers‘

quality preferences and reducing the costs of improved quality of inputs (Reardon and Berdeque

2002).

WTO members adhere to both the SPS and the agreement on Technical Barriers to Trade

(TBT). These agreements provide broad guidelines for choice of product standards but accept

national sovereignty in adopting standards provided they could be justified based on risk

perceptions and scientific assessment. Some nations have moved to harmonize food safety

regulations, such as the attempt to harmonize pesticide residue limits under the auspices of

Liaison Committee for Caribbean, Africa, and Pacific (COLECAP). Concurrently, there has been

a rise in the number of private standards such as Euro Retail Produce Group‘s Good Agricultural

CAPRI WORKING PAPER NO. 70 OCTOBER 2007

7

Practices (EUREPGAP), ChileGAP, KenyaGAP, ChinaGAP, Naturane [Spain], New Zealand

Fresh Produce Approved Supplier Program, and Mexico Supreme Quality GAP. Besides, major

supermarkets have their own standards like Tesco‘s Nature‘s Choice and Mark & Spencer‘s Farm

to Fork that require compliance via third party certification (Hatanaka et al. 2005).

The spurt in private standards has been partly driven by the events of food safety failures

in the eighties and nineties (Dolan and Humphrey 2000; Dolan et al.. 1999; Freidberg 2003 and

2004). With several standards in practice, there have been attempts to harmonize globally with the

formation of Global Food Safety Initiative (GFSI). The major goal of GFSI was to create a global

set of voluntary but universally accepted standards of food safety, quality and security (Freidberg

2005). In case of pesticide residue limits for example, the GFSI intended to eliminate situations

where some countries demand compliance with Codex Alimentarius, while other impose their

own limits.

As it is difficult for the supermarkets to identify products grown under specific protocols,

firms meeting guidelines try to distinguish themselves. Thus, in developed countries, retailers

have developed private food safety protocols. Reardon et al.. (2003) suggest the rise of private

standards as 1) strategic tools by the supermarkets to differentiate themselves; 2) instruments of

supply chain coordination by standardizing product requirements across suppliers; 3) substitutes

for missing or inadequate standards in less developed regions; and 4) strategic tools over the

informal sector by claiming better food safety.

CAPRI WORKING PAPER NO. 70 OCTOBER 2007

8

4. ROLE OF SUPPLY CHAINS IN THE DELIVERY OF FRUITS AND VEGETABLES

Types of markets available to producers in LDCs

Currently, in most developing countries producers supply to three different markets: the

domestic traditional markets, modern urban markets, and export markets. These markets differ in

several organizational respects but, most importantly, in their demand for food safety (World

Bank 2006 – Table 1). The food safety requirements are most stringent in the export markets (in

high income countries) followed by the modern domestic urban markets.

CAPRI WORKING PAPER NO. 70 OCTOBER 2007

9

Table 1. Three types of markets and their characteristics Types of market

Market

characteristics

Traditional local fruit

and vegetable markets

Emerging modern urban

domestic markets

(supermarkets, tourist

hotels/restaurants,

educated affluent

consumers)

Export markets in industrial

countries (retail markets,

modern food services

Food safety

control.

Little consumer

awareness, concern.

Little private effort.

Government control.

Emerging consumer

awareness, concern.

Retailers try to control and

sell ―safety‖.

High consumer concern.

High retailer requirements

imposed on suppliers.

Standardization,

grading, supply

Virtually absent.

Irregular supply.

Emerging importance of

grading, stable supply.

High requirements of grading,

consistency, supply schedule.

Supply-chain

organization

Supply-driven.

Transaction-based.

Little or no net benefit

from coordination.

Little durability in

relation between private

actors.

No technical

cooperation.

Efforts by retailers to

control quality, safety, and

reliability of supply.

Net financial benefits from

coordination still fragile.

Emerging coordination,

occasional technical

support.

Strongly demand-driven.

Durable relations within supply

chain, often on contractual basis.

Cooperation between buyers,

exporters, growers on

technology, information,

sometimes on finance.

Price level for

grower and

consumer

Relatively low.

Limited willingness to

pay for quality and

safety.

Moderate.

Moderate willingness to pay

for quality and safety.

Relatively high.

High willingness to pay for

quality and safety.

Value added Very low Low/moderate Moderate/high

Trust between

buyers and sellers

Not very important. Of emerging importance. Crucial factor for long-term

successful relations.

Competitiveness

depends mainly on.

Supply at low cost. Sufficient quantity of

improved quality.

Large quantity required.

Efficient, effective coordinated

supply chains.

Flexible response to changing

demand.

Market and product innovation.

Participation of

small-scale

producers.

No constraints. Emerging constraints in

meeting requirements of

quality, safety, consistency

of product, regular supply.

Only if well organized in out-

grower schemes and able to

guarantee safety and uniform

quality. Source: World Bank (2006)

CAPRI WORKING PAPER NO. 70 OCTOBER 2007

10

CONSTRAINTS FACING THE SMALLHOLDERS IN THE EMERGING FOOD SYSTEM

The new and emerging food system (dominated by domestic urban market and export

markets) with high demands for compliance with food safety and traceability disfavor the

smallholders due to high coordination costs. The problem is exacerbated by geographic

dispersion, low education, and poor access to capital and information (Poulton 2005; Humphrey

2005; Rich and Narrod 2005). Because of high transaction and marketing costs of sourcing from

smallholders, major exporters produce HVA on their own farms or source from medium and large

outgrowers trained and trusted to deliver on both traceability and food safety requirements.

The smallholders face problem in the two dynamic markets in meeting the standards as

well as in ensuring the delivery of a regular supply to their buyers. The list of constraints that

smallholders face in the HVA markets given below draws from Rich and Narrod (2005):

High fixed costs in production and marketing, especially due to the need to comply with

the standards given high perishability.

Difficulties in guaranteeing safe products. This can arise either in terms of the quality or

the misuse of inputs or the lack of knowledge about the introduction, growth, and

transport of pathogens, which can be magnified as products move along the supply chain.

For credence goods, reputation matters significantly for demand creation. Smallholders

usually have a small history of presence in the markets and lack branding.

Asymmetric and incomplete information and high transaction costs may exist between

actors in the supply chain. Lack of information regarding production and marketing can

especially deter smallholders as procurement and processing of information involves

large fixed costs.

Lack of incentives and resources to invest in quality improvement, low access to credit,

and the low returns from investing in quality (as they lack reputation) disadvantage the

small farmers.

The supply chain in most developing countries is often characterized by transactions in

spot markets, implying limited coordination among farmers, traders, and consumers. This lack of

coordination coupled with poor infrastructure (for example, absence of cold storage) imply that

participants lack incentive to reduce microbial pathogens, mycotoxins, and pesticide residues

since the penalties for low quality are not enforceable (Narrod et al. 2005).

CAPRI WORKING PAPER NO. 70 OCTOBER 2007

11

The economies of scale become prominent in the presence of FSS, thus disadvantaging

the smallholders. Consider, for example, the procurement of information regarding FSS. This

information, once obtained, can be disseminated at low marginal costs. Unless there is a large

volume of output over which the fixed costs can be distributed, it will not be economical to incur

these transaction costs defined broadly to include costs for the collection of market information,

negotiations, monitoring, and enforcement of business transactions (Jaffee and Morton 1995).

Additionally, marketing costs (such as requirement of cooling) require lumpy investments leading

to scale economies. In HVA chains, smallholders are thus likely to face problems in quality

control, handling, and storage (Bienabe and Sautier 2005). Moreover, once involved in HVA

chains, smallholders individually enjoy only limited bargaining power (Kaplinsky and Morris

2001).7

Role of Institutions in enabling smallholders market access in HVA chains

Given the constraints outlined above, the focus of this study is on CA and PPPs in

enabling smallholders to access the HVA chains with FSS. Conceptually, the role of CA arises

wherever there are economies of scale in production or in marketing. This includes the role of

farmer groups in being better able to ensure traceability. In these chains, the costs for the

establishment of traceability are lower for firms and farms with collective action than without it.

Similarly, collective action has a rationale if agents in the supply chain have different comparative

advantages. Thus, a producer group (with comparative advantage in production) could benefit

from collaboration with agents that have expertise in marketing.

Table 2 below presents a summary of the different processes and the role that CA plays in

each context. This list is not intended to be exhaustive but is aimed at presenting indicative cases

pointing to a basis for CA. In exporting, information about the demands of the markets and the

terms and conditions of the contract and the process of the establishment of contracts has to

7Some of these constraints remain unresolved owing to government over-regulation, taxes, or tariffs that

raise the cost of supply chain development and lower the benefits of participation. Limits or bans on

foreign investment reduce the benefits from technical expertise and coordination that foreign participants

can bring. Even when regulatory norms are appropriate, changes in consumer demand can have negative

impacts on smallholders if retailer‘s sourcing decisions change in response (Humphrey 2005).

CAPRI WORKING PAPER NO. 70 OCTOBER 2007

12

precede the production process. Procurement and processing of information clearly involves fixed

costs. Similarly, negotiation of contracts might involve a big component of costs not related to

output. Hence, these create a clear basis for grouping of small farmers to overcome diseconomies

of scale.

Table 2. Production processes in markets with IFSS and the role of collective action Supply Chain

Process

Role played by collective action

Pre-

production

Procurement of information about markets and the process of formation of

contracts

Dissemination of the information relating to IFSS

Undertaking of lumpy investments

Production Procurement of cheaper inputs through bulk buying

Use of extension services

Establishment of traceability system

Post harvest

and Marketing

Collective marketing leading to reduced costs (for example in transport)

Grading and certification for the farmer groups

Collaboration with marketing experts

Additionally, PPPs might be required to play a complementary role in linking small

farmers with HVA markets. The traditional public supply functions can be inadequate to meet the

needs of the HVA supply chains from the perspective of the smallholders. Traditional public

sector activities such as extension, research and development, and price and marketing policies

have been largely commodity-based and hence may not provide the support smallholders require

in a HVA supply chain. The private sector has traditionally been directly involved in the

production, marketing, and distribution of agricultural commodities, the rise in HVA commodities

giving an ever-larger and more specific role to the private actors.

Table 3 presents the different supply chain support processes and the institutional roles

played by the private and the public sectors. Wherever the public or the private sector by itself

cannot provide the supply chain support that caters to the needs of the smallholders, there arises a

need for partnerships. The last column in table 3 provides insights on the basis for PPPs in HVA

chains. For example, in the extension services relating to HVA, the public knowledge might be

limited while the access to private information might also be constrained owing to low

purchasing power of the smallholders.

CAPRI WORKING PAPER NO. 70 OCTOBER 2007

13

Table 3. Public and private sector roles in the supply chain management of HVA

Supply Chain Support

Processes

Needed Roles for

SCM

Traditional Institutional Roles Market or

government failures

affecting

smallholders Public Sector Private Sector

Extension services Knowledge of

specialized

techniques for HVA

Technical

assistance in

farming practices

Services to farmers

and firms linked to

private company

Low and variable

access to public or

private extension;

limited public

knowledge of new

techniques

Infrastructure

development

Management of flows

between chain links

quickly and

efficiently; Reduce

distribution costs to

remain competitive

Public

infrastructure

(roads, ports,

storage facilities);

public distribution

Private infrastructure

(processing, storage);

logistics

Uneven development

biased against

smallholders, private

development difficult

for smallholders or not

attuned to small

farmer‘s needs

Information services Integration of

information flows

across supply chain

Provision of

public statistics on

prices, production,

etc.; information

on varieties

through extension

Private marketing

information services

(MIS) and electronic

data interchange

(EDI)

Reliance on public

information systems

not tuned to market

needs, exclusion from

private sources for

inability to pay

Certification, grades,

and standards

Consistent, credible

application of

standards on food

safety and quality

specifications

Public

certification and

development and

enforcement of

public standards

and regulations

Private certification

and development and

enforcement of

private standards;

Smallholders‘ ability

to meet public or

private standards

limited; Development

not based on

smallholder needs

Coordination

mechanisms

Ensuring consistent

delivery of high-

quality products

Creation and

enforcement of

regulations to

ensure

competition;

mandatory

cooperatives

(centrally-planned

economies)

Development of

contracts and

marketing agreements

with suppliers

Limited enforcement

of contracts biased

against small farmers;

divergence in market

power between chain

actors

Source: Rich and Narrod (2005)

CAPRI WORKING PAPER NO. 70 OCTOBER 2007

14

CA and PPPs clearly play complementary roles in linking small farmers with HVA

markets. Where CA is necessary under many circumstances, it may not be sufficient. Consider a

group of small farmers that has to finance a lumpy investment. To this group, the private sector

loans might not be forthcoming at terms that the group finds economical. The private discount

rates tend to be high, while gestation lags in investments, especially with smallholders, tend to be

long. This creates a role for the public sector with lower discount rates (possibly with some

subsidy) in credit markets.

5. FRUIT AND VEGETABLE PRODUCTION AND THEIR SUPPLY CHAINS FROM THREE CASE STUDIES

Following on the discussions above, we focus on 3 supply chains involving smallholders

for fruit and vegetable exports in India, Kenya, and Mexico. In Kenya, the domestic market for

green beans hardly exists. The smallholders have been involved in producing beans for export for

some time even before the relatively recent demand for food safety. In the Mexican case,

smallholders were supplying both the domestic and the export markets with cantaloupes until the

outbreak of salmonella, which resulted in a total ban on all exports for a year. Exports only

resumed a year later when firms adopted voluntary best management practices. In the process

they began to source primarily from medium and large scale producers. In the Indian grape case,

Mahagrapes, the marketing partner of cooperatives, built upon an existing network of producer

organizations that were already producing good quality grapes (including organic farming) but

lacked the marketing expertise for export. Now, the smallholders are actively involved in exports

and successfully meet the FSS of the western markets. Below we discuss these cases.

Green Bean Production in Kenya8

8 From Okello et al. (forthcoming)

CAPRI WORKING PAPER NO. 70 OCTOBER 2007

15

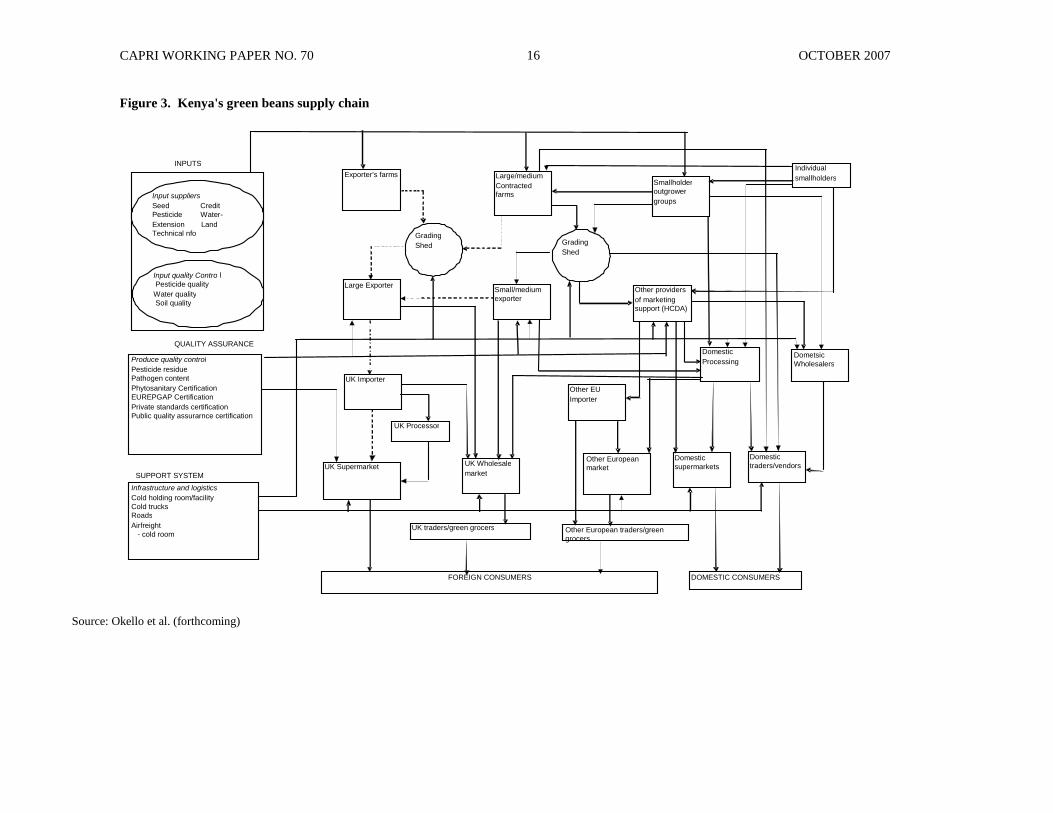

Kenyan green bean supply chains

Currently, green beans are marketed through three chains - the export supermarket chain,

the export wholesale chain, and the domestic chain (figure 3). These chains are distinguished by

the degree of coordination following the need to comply with IFSS and the demand for a

traceability system. The supermarket chain is the most closely coordinated and typically requires

establishment of a functional traceability system. In Figure 3, traceability requirements are

represented by a broken line.

CAPRI WORKING PAPER NO. 70 OCTOBER 2007

16

Figure 3. Kenya's green beans supply chain

Figure 4 Kenya's High Value Horticulture's Supply Chain

INPUTS

QUALITY ASSURANCE

SUPPORT SYSTEM

UK Importer Other EU Importer

Large Exporter Small/medium exporter

Other providers of marketing support (HCDA)

Exporter's farms Large/medium Contracted farms

Smallholder outgrower groups

UK Supermarket UK Wholesale market

Other European market

Domestic traders/vendors

Domestic Processing

Domestic supermarkets

FOREIGN CONSUMERS

Input suppliers Seed Credit Pesticide Water- Extension Land Technical nfo

Input quality Contro l Pesticide quality Water quality Soil quality

Produce quality control Pesticide residue Pathogen content Phytosanitary Certification EUREPGAP Certification Private standards certification Public quality assurarnce certification

UK traders/green grocers Other European traders/green grocers

DOMESTIC CONSUMERS

Dometsic Wholesalers

Infrastructure and logistics Cold holding room/facility Cold trucks Roads Airfreight - cold room

Grading Shed Grading

Shed

Individual smallholders

UK Processor

Source: Okello et al. (forthcoming)

CAPRI WORKING PAPER NO. 70 OCTOBER 2007

17

Supermarket chain

The UK supermarket chain has the most stringent food safety requirements (Singh 2002;

Jaffee 2003; Henson, et al. 2005). Green beans marketed through this chain must be certified (by

an accredited third party) as meeting EUREPGAP, BRC, and, in most cases, retailers‘ private

food safety protocols. The beans must be accompanied by a phytosanitary certificate issued by a

competent authority guaranteeing absence of prohibited pests. In addition, the beans must be

traceable from the retailer‘s shelf back to the grower‘s plot.

Handling and hygiene practices during harvesting, grading, and packing of green beans

are all closely monitored. Growers are required to have a toilet, pesticide storage unit, and a

facility for hand washing at the farm or the grading shed. Exporters to the EU supermarkets test

the water and soil twice a year for pathogens. The exporters also require farmers to keep records

of the type and quality of inputs (pesticide, water, or soil) used. These records accompany green

beans to the exporters‘ packhouses. Farmers keep records of production and handling practices

either individually or collectively (in case of a farmer group). In order to enforce compliance with

these practices, EU importers have increased their monitoring and coordination of input use. They

generally monitor the exporters expecting them to monitor growers in turn. Increasingly, some

EU importers have extended their monitoring to farm level through regular visits.

The most serious attention to the possibility of contamination occurs in the exporters‘

packhouses. Exporters in this chain have all invested in packhouses with good manufacturing

practices (GMPs). Workers are required to wear special clothing and rubber boots in the pack

houses and to wash their hands at regular intervals or when they change shifts. Some exporters

monitor worker hygiene (especially the washing of hands) in the packhouse. Such exporters

randomly swab the hands of workers and test for pathogens. If the swab tests positive for any of

the pathogens of concern, that worker is penalized. All containers used at various stages of the

processing are color-coded to avoid mixing and cross-contamination with pathogens. In addition

to strict adherence to hygiene during processing (sorting, chopping, and arranging beans into

trays), packing and bar coding are done under temperature-controlled conditions.

CAPRI WORKING PAPER NO. 70 OCTOBER 2007

18

Wholesale chain

Green beans from most small and medium farmers feed into the wholesale chain where

monitoring and coordination is less pronounced. Here the focus is often on the physical

characteristics (e.g., size, spotlessness) as opposed to the credence attributes (e.g., pesticide

residue content). However, meeting the EU‘s public standards is mandated, and consistency of

volume in supplies is desired. A large proportion of beans in this chain originate from the spot

market (hence do not satisfy traceability) and are usually not grown under supervision by the

exporter. Consequently, the quality (in terms of pesticide residues) cannot be ascertained even by

inspection at the market. Generally, the wholesale chain is used by exporters who find it

uneconomical to comply with the private FSS of the supermarkets. Such exporters are generally

the small and medium sized lacking adequate quality management systems (Humphrey 2002).

Domestic chain

The FSS are least pronounced in the domestic chain comprising fresh or processed beans.

The fresh green beans in domestic supermarkets tend to be the overflow from sales to UK

supermarkets. Some fresh beans are sold also to the wholesale markets and to open retail.

Currently, the supermarket buyers do not have any specific system of checking and verifying the

quality. There is also no system of preventing contamination of beans with pathogens. Five firms

in Kenya are involved in green bean canning and sell primarily to France. Since FSS is less

stringent in canned beans, the processing firms source the majority of their green beans from

smallholders. Indeed, the only FSS for processors is the pesticide residue limit. Thus, firms use

their own pesticide applicators and handle the purchase and storage of pesticides themselves.

Grape exports from India9

In 2005, India was the third biggest producer of fruits and second largest vegetable

producer in the world (FAO 2005). But India is a small horticultural exporter mainly because of

lack of off-farm competitiveness (World Bank 2005). Smallholder dominated agriculture restricts

the number of farmers able to adopt sophisticated farm practices and undertake the investments

(like cold storage) to meet stringent IFSS (Umali-Deininger and Sur 2006).

9 From Roy and Thorat 2006

CAPRI WORKING PAPER NO. 70 OCTOBER 2007

19

India’s grape supply chain

Figure 4 shows the supply chain for the three main varieties of grapes produced by the

grape farmers: viz. Thompson seedless, Sonaka, and Sharad seedless. The first variety is targeted

mainly for exports to European markets. The Sharad seedless variety is sold mainly in the

domestic market, while the Sonaka is marketed domestically and also exported to Gulf countries.

CAPRI WORKING PAPER NO. 70 OCTOBER 2007

20

Figure 4. Supply chain for Mahagrapes and independent grape producers

MAHAGRAPES

- Large farmers

- Medium Farmers

- Small farmers

INDEPENDENT Farmers & Other Coops.

- Large farmers

- Medium Farmers

- Small farmers

Mahagrapes Input Supply

Bio Fertilizers imported

From

Australia .

Bio pesticides under

Mahagrapes brand. Technical Assistance

Inputs - Commercial

Seeds

Fertilizers (Chemicals)

P esticides & Insecticides

(Chemical)

Water, Land etc

Independent Branding

Commission Agent

Domestic Retail

Domestic Consumption

Sorting & Primary

Packagin g

(Quality control)

Cooperative collection centers

Pre cooling , secondary packaging, grading and trace - back (quality control and cold storage.

Certification & marketing agents in Mumbai

Agent for supermarkets in Europe (Germany, Netherlands, U.K, Gu lf, Sri Lanka)

Supermarket

European Consumers

Wholesale Agents –

Europe (Germany, Great Britain & Netherlands)

Sonaka

Gulf Consumers

Exports

Agent in the Gulf

Whole Sellers

Shared Seedless

CAPRI WORKING PAPER NO. 70 OCTOBER 2007

21

Harvest and packing of grapes

There are stringent requirements in pruning and packing of the grapes. After harvesting,

the grapes are transported to a cooperative collection center where pre-cooling and cold storage

facilities exist. Some amounts of grapes are screened off based on initial damage, bunch

composition, etc. Some farmers, especially the small farmers, do the pruning near their farms and

then transport grapes to the cooperative centers. Some grapes after the second round of tests may

be rejected at the cooperative collection center. The grapes that are rejected at the collection

center are generally sold to middlemen and find their way to the local market. The post harvest

facilities have to meet the sanitation and hygiene requirements under the EUREPGAP. At the

packing station before the grapes are packed, the packages are coded for traceability.

Shipping

Shipping for exports is done by the cooperative in collaboration with Mahagrapes.

Refrigerated containers pick up grapes from the cooperative collection centers maintaining the

cold chain. The cooperatives charge a logistic fee per unit of grape supplied. The grapes rejected

for exports (similar to grapes intended for domestic markets) are shipped in non-corrugated boxes

to local markets. They are not packed in pallets nor are they labeled for traceback. The export

grapes are packed in pallets and covered with sulfur dioxide sheets (imported from China) to

preserve quality as grapes are shipped by sea over long distance. If shipped for local markets, the

mode of transport tends to be in open trucks with paper bags packed under wooden crates.

Mexico’s cantaloupe production10

A salmonella outbreak in 2002 detected in shipments from Guerrero led to the ban of

cantaloupe exports. Prior to the ban, almost 90 percent of Mexican F&V exports were to the U.S.

Following the ban, Mexican cantaloupe exports reduced by 97 percent, with a loss of 5,909

hectares under production (23.5 percent reduction) (Avendaño et al. forthcoming). Most U.S.

retail firms after the outbreak started demanding suppliers to meet GAPs and GMPs to minimize

microbial contamination in fresh produce. To meet this demand, the Mexican government tried to

10 From Avendaño et al. (working paper forthcoming)

CAPRI WORKING PAPER NO. 70 OCTOBER 2007

22

develop a strategy by signing a memorandum of understanding on actions needed to comply. This

was followed by the publication of an emergency regulation to develop a new FSS program for

FVs.

With this in place, the U.S. opened the market to selected firms that gained Mexican and

U.S. government approval, and a new program for imports of cantaloupe was announced in late

2005. To adopt GAPs, growers had to have technical assessments of their operations, make

investments to bring their farms up to standards, and pay for third-party audits certifying

compliance with GAPs.

Mexico’s cantaloupe supply chain

Mexico‘s cantaloupe chain comprises two different streams (figure 5): one associated

with export oriented large firms, and second involving smallholders catering to the international

markets before the salmonella outbreak (mainly through big firms with packing facilities).

CAPRI WORKING PAPER NO. 70 OCTOBER 2007

23

Figure 5. Mexico’s cantaloupe supply chain

Source: Avendaño et al. (forthcoming)

CAPRI WORKING PAPER NO. 70 OCTOBER 2007

24

Production

In production, firms usually rent land to smallholders for production and in some cases

contract with them. Nearly 825 hectares are used for this crop in Colima: 75 percent of the land

use in cantaloupe belongs to an ejido system (1 to 14 hectares with 6 hectares as the average per

grower), 25 percent to small property (up to 300 hectares); 29 percent of cantaloupe growers rent

land for production, and 71 percent are smallholders that work on owned land.11

Most growers (92 percent) use drip irrigation, plastic quilted beds, and certified seeds.

White fly is the main threat, but it is relatively under control with the techniques in use (drip and

bed). Only 4 percent of growers qualify for GAPs. Moreover, there is no evidence of other types

of microbiological risk reduction; thus, regaining of market access in the US seems unlikely in

the short run. To implement a food safety program, growers have to start with incorporation of

GAPs and pay attention to the quality of water, a major source of contamination.

Harvest and packing

Meeting GAPs during growing and harvesting can be difficult for small growers. They

must keep records of fertilizers, irrigation, pesticides and chemicals applications, and observe the

proper time to harvest (until chemicals are absorbed). Once harvested, big firms (export-oriented)

send the product to the packing facilities for post harvest treatment, which includes washing,

brushing, selection, pre-cooling, sizing, pre-packing, cold storage, and carton repacking. From

packing houses the product goes to the market. Only two packing houses are in process to obtain

a food safety certification to export to the USA. Small growers without a prior arrangement with

a packing house have the choice to sell to a middleman at the orchard. Once in the packing house,

if product does not meet the quality standards demanded by the packers, it can go to (fresh)

domestic market or to the process industry without packing. If packed, product goes to fresh

export market or domestic market.

Shipping

Shipping for export is usually done by the same growers (big firms that own transport

and can preserve the cold chain). Export is done mainly through brokers and wholesalers in the

11 The ejido is a tenure system through which the government promotes the use of communal land shared

by the people of the community.

CAPRI WORKING PAPER NO. 70 OCTOBER 2007

25

North American market, and gets to the institutional sector (supermarkets, hospitals, restaurants,

hotels, etc.) on the way to consumers. Product going to CEDA does not preserve the cold chain

and is usually transported in open trucks. Once in CEDA, product is distributed to small buyers

related to street markets, fruit stores, and public markets. Ninety percents of the produce goes to

domestic markets and the rest to export.

Marketing

The producer may sell directly to a middleman. Sometimes cantaloupe is bought directly

at the farm by a middleman, who can bring it to either the packing house, to the supply center, or

to a domestic processor. For products going directly into the domestic processing, no post harvest

processing is required. Domestic processors sell mostly in domestic markets in different forms:

frozen or canned. The packing process is one of the most important phases in the cantaloupe

chain. For export as well as for institutional markets, the facility must have a food safety program

and be certified by a third party. For example, if product is going to the EU, it must comply with

EUREPGAP; for the US, food safety certification is generally done by North American firms like

Primus Lab recognized by the market.

The institutional sector gets its supply from CEDA or directly from packers. When

products come from CEDA, it is difficult to trace back the origin. The supplies for the

institutional sector in the US require a system of traceability. Direct access to supermarkets is

recent for cantaloupe growers. Only 17 percent of Colima growers sell directly to supermarkets

since they need to have packing facilities. Though an important market, the need for packing

facilities and the delay in payments by supermarkets has obviated the participation of the small

growers. In a study by ANTAD (2005), 38 percent of fresh fruit and vegetables go to public

markets and 29 percent to supermarkets. The supply centers (CEDAs) are also the main importers

for fresh products which they also import from the U.S. Sometimes, they are just returned

exports. Most imports from the U.S. wholesalers go either to public markets, fruit stands, or to the

institutional sector.

CAPRI WORKING PAPER NO. 70 OCTOBER 2007

26

6. DIFFICULTIES SMALLHOLDERS HAVE IN PARTICIPATING IN THESE SUPPLY CHAINS

With these stringent requirements in the coordinated supply chains with IFSS, we now

focus on the difficulties that smallholders face in these specific chains.

Smallholders in Kenyan green bean supply chain

Prior to mid 1990s, Kenya‘s green bean industry was dominated by smallholders with

their share in output being greater than 60 percent (Kimenye 1993). Currently, this share is

believed to be less than 40 percent (Dolan et al. 1999; Dolan and Humphrey 2000; Jaffee 2003;

Jensen, n.d.). High value products are labor intensive, making it cheaper to grow on family farms

with self monitoring labor (Collins 1995). However, these advantages have generally been

outweighed by the higher transaction costs of working with smallholders, and exporters have

shifted from smallholders to medium and large scale, and own farms for green beans (Dolan and

Humphrey 2000; Jaffee 2003).

The dominant transaction cost in linking with smallholders is the cost of monitoring

compliance with IFSS and the insistence on traceability by importers. Medium and large

outgrowers also have access to own, debt, or venture capital to invest in costly facilities required

by IFSS including grading shed, cold storage, and pesticide storage unit (Jensen, n.d). The post

harvest facilities involve lumpy investment and entail economies of scale; hence, competitiveness

is achievable only with high volumes (Debertin 2002). The traceability and residue limit

requirements further disadvantage the smallholders as they are poorly educated and/or unskilled.

By comparison, larger farmers can invest in specialized skills needed to comply with FSS

(Collins 1995).

Smallholders in Indian grape supply chain

Several market failures plague the supply chain of Indian horticultural exports. Most

importantly, the Indian exports lack good reputation in external markets. Therefore, any private

sector investment in quality improvement or branding is unlikely to be adequately compensated.

CAPRI WORKING PAPER NO. 70 OCTOBER 2007

27

Indeed, the large farmers export independently under their own brand. In addition, certification is

expensive, and smallholders cannot individually bear the costs.

Several post harvest technologies (like cold storage) require lumpy investments, and

credit constrained farmers would not be able to make those investments. In the limited cold

storage facilities that exist, there is large monopoly power for the providers and, unless provided

by the cooperative, small farmers cannot afford it. Also, the private sector has not invested in pre-

cooling facilities given the small paying capacity and gestation lags in such investment.

The presence of middlemen in these chains accounts for another market failure. The

middlemen charge high commission costs ranging from 15 to 40 percent of the domestic

consumer price for grapes (based on field survey of grape farmers). To the extent that

smallholders rely more on middlemen, they are affected more adversely.

Smallholders in the Mexican cantaloupe chain

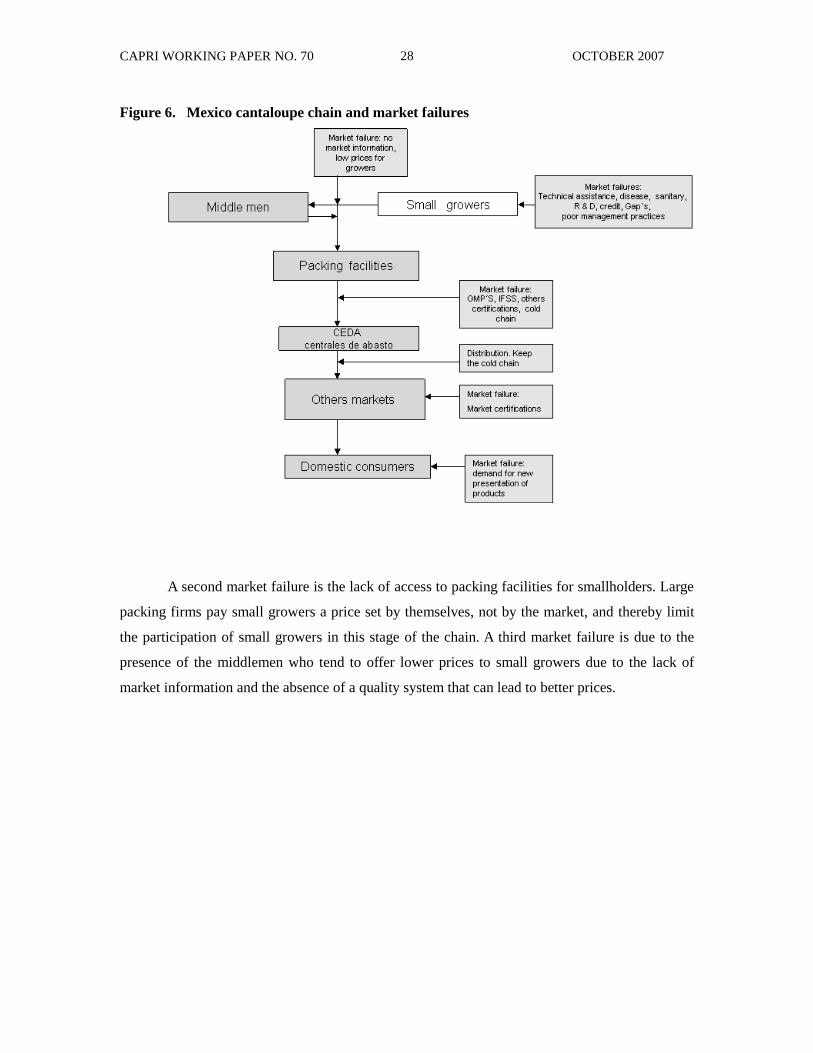

Several market failures arise also in Mexico‘s cantaloupe chain (figure 6). The first

relates to imperfect information and access to inputs. Most smallholders rely on input suppliers

for inputs on credit, but the cost of financing reflected in the final price is usually much higher

than market rates.

CAPRI WORKING PAPER NO. 70 OCTOBER 2007

28

Figure 6. Mexico cantaloupe chain and market failures

A second market failure is the lack of access to packing facilities for smallholders. Large

packing firms pay small growers a price set by themselves, not by the market, and thereby limit

the participation of small growers in this stage of the chain. A third market failure is due to the

presence of the middlemen who tend to offer lower prices to small growers due to the lack of

market information and the absence of a quality system that can lead to better prices.

CAPRI WORKING PAPER NO. 70 OCTOBER 2007

29

7. ROLE OF VARIOUS INSTITUTIONS IN INVOLVING SMALLHOLDERS IN THESE MARKETS

Thus, there are factors in these supply chains (some generic and some specific to the

chains) that would exclude the smallholders without any intervention. As discussed above, owing

to the nature of HVA export markets involving IFSS, there is rationale for CA and PPPs in

marking these markets more accessible for smallholders.

Collective action for sustainable management of resources among resource dependent

populations has been studied extensively (Bardhan and Dayton-Johnson 2002; Lam 1998; Kant

2000). The role of collective action in achieving market access through cooperatives has also

been widely documented (Baron 1978, Ranade 1983, and Wilkins 1983, for example). The

transaction cost approach to the determination of organizational and institutional structure

explains organizational forms as originating to minimize the transaction costs in a given

environment (Staatz 1984). The institutional structures and innovations that we discuss here aim

to minimize the transaction costs and exploit the economies of scale wherever applicable.

Coping strategies for smallholders in Kenyan green bean exports: The role of CA and PPP

Two forms of institutional arrangements have enabled market access for the small

farmers in fresh beans: contract production with individual farmers or with farmer groups (Okello

et al., forthcoming). The contracted outgrowers in farmer groups are usually smallholders with

weekly sales of fewer than 100 kilograms. Several of these farmer groups jointly invest in

facilities needed to comply with IFSS and also have technical assistants or trained leaders that

help members meet the standards. Buyers work very closely with groups in providing both

training and other technical support to members and facilitate their compliance with the FSS.12

12 One of the coping strategies adopted by small farmers as discussed above has been market switching.

Several smallholders have shifted to producing for the canning industry. In 2000, only a few hundreds of

farmers grew beans for the canning industry. Fintrac-Horticultural Development Center (a Kenyan NGO)

estimates that by 2004, thousands of smallholder farmers were growing beans for one of Kenya‘s leading

green bean canner, with 3000 having attained EUREPGAP certification. Less stringent FSS imply that the

farmers are not required to invest in long term facilities (pesticide storage unit, shower room, toilet in the

CAPRI WORKING PAPER NO. 70 OCTOBER 2007

30

Apart from this endogenous adjustment by the small farmers, institutions have emerged

to enable smallholders to access markets with IFSS. The arrangements comprise CA among

farmers or with different agents in the supply chain and formation of partnerships among NGOs,

donors, and the public sector. In Kenya, green bean farmer groups existed even prior to the IFSS.

The reason they existed was primarily for marketing, i.e. to find a buyer and negotiate better

prices for members. Beginning in the late 1990s (with IFSS), exporters began transforming the

way these smallholder groups operated (Jaffee 2003).

First, the groups were reorganized and their sizes reduced from as high as 350 farmers to

less than 30 farmers per group. The farmers were trained on IFSS and on the production practices.

The farmers were then subjected to close monitoring under more formal contracts than the

procurement arrangement that existed before. Some exporters supervised group members

individually and penalized the individuals for violation of practices, but most supervised the

group as a whole and penalized all the members for violations (Okello 2005). The farmer

organizations also conduct training for members and facilitate farmer to farmer monitoring in the

absence of the exporter‘s field technical assistant (TA) and/or to reinforce exporter‘s training. The

organizations invite experts to train farmers on GAPs, especially on the observance of pre-harvest

interval following application of pesticides, integrated pest management, packer hygiene, and

establishing and maintaining a functional traceability system.13

Some exporters require the farmer organizations to hire their own technical assistants

(TAs) who can respond to members‘ hygiene, pest, and disease problems readily, and a clerk. The

TA occasionally conducts field visits with an exporter‘s agronomist as part of the training and

also keeps records for all the members of the type, amount, and date of pesticides used. The clerk,

on the other hand, enforces compliance with hygiene requirements within the grading shed. This

strategy is used by a few leading exporters.

farm, grading shed) thus removing the scale-dependent determinants of competitiveness (Fintrac-

Horticultural Development Center 2004). 13

The main benefit from grouping has been the lowering of per capita costs of compliance with the IFSS

for the small farmers. Okello et al. (forthcoming) show that the costs of compliance with the IFSS for a

small farmer would be around 10 times higher if they were not a member of a farmer group. Several costs

of compliance involve fixed costs such as construction of grading sheds which, unless distributed over a

large output, would make it uneconomical to access markets with IFSS. For example, on average for an

individual small farmer, the costs of compliance with IFSS based on a conservative estimate would be

almost 70 percent of the income, while in a 15 member group it would be just 4 percent.

CAPRI WORKING PAPER NO. 70 OCTOBER 2007

31

Some producer organizations instead hire a team of expert pesticide applicators that spray

green bean fields for farmers under interlinked credit arrangements by the group. The TA

dispenses only the right kind and quantity of pesticide based on the growth stage of the crop and

outcome of pest scouting. Such producer organizations may also have their own pesticide stores.

To ensure traceability, producer organizations jointly hire field technical assistants and

depot/grading shed clerks who compile the records required under IFSS.

The organization of the producer groups and hence the CA among farmers as discussed

above is tuned to enabling the small farmers to comply with IFSS. Hiring a technical expert or

investing in facilities are possible because of joint sharing of costs. Most importantly, for the

buyers, having the producer groups enables them to implement a functional traceability system

whereby a clerk holds accounts from several small farmers at once and also creates a system of

farmer to farmer monitoring, akin to group liability system in microfinance.

Where does the partnership with the public sector play a role here? First, the formation of

producer organizations entails transaction costs related to search and screening of members.

Therefore, formation of some smallholder organizations has been facilitated by the governments,

exporters, non governmental organizations, and donors. Additionally, donor and NGO funding

has sponsored farmer‘s EUREPGAP training, audits, and certification.

The government moreover has adopted some policies aimed at promoting compliance

with IFSS such as i) partnering with donors and NGOs to provide training and physical

infrastructure; ii) partnering with the fresh export industry to lobby importers for adaptation of

EUREPGAP requirements to developing country conditions; and iii) conducting awareness

campaigns and limited training to smallholder farmers on importance of meeting IFSS. The

Government in partnership with Japanese International Cooperation Agency (JICA) established a

company that owns cold storage facilities. This partnership has also trained more than 100

smallholder farmer group leaders as IFSS service providers and many farmers belonging to

farmer groups on good agricultural practices (HCDA 2005). The government partnering with

USAID and major exporters conducts pest surveillance inspections on small green bean farms.

USAID has also funded capacity building in local government certification agencies through staff

training and establishment of pathogen and pesticide residue testing facilities that can bring down

the costs of certification for the smallholders. Further, USAID funding has also facilitated

partnership between Kenya Horticultural Development Project (KHDP) and green bean exporters.

The partnership provides management and business skills training and market advisory services.

CAPRI WORKING PAPER NO. 70 OCTOBER 2007

32

Donors and NGOs have also jointly established Africa‘s only indigenous certification

company aimed at making EUREPGAP certification cheaper and hence accessible to

smallholders. A PPP between UK Department for International Development (DFID) and HCDA

(Horticultural Crops Development Authority) has trained a pool of export horticulture service

providers. Three NGOs (namely, Care International (Kenya), Reach the Children Inc, and ICIPE)

are partnering with the private firms to train, audit, and/or financially help smallholders to obtain

EUREPGAP certification. Most of these NGOs are supported by donor agencies. In addition,

ICIPE is currently partnering with green bean exporters (e.g., Kenya Horticultural Exporters and

Woni) to train EUREPGAP trainers and other horticultural industry service providers. Reach the

Children Inc. has activities that involve 10 smallholder farmer groups in Machakos. The activities

include EUREPGAP certification, training in good agricultural practices, micro-credit services,

and market linkage program.

Another NGO, Pride Africa, works on creating linkages between various actors in the

horticultural industry aimed at i) training on good agricultural practices and access to technical

information; ii) access to credit; and iii) access to the export market. It has facilitated linkages

between farmer groups and EUREPGAP trainers, input sellers, banks, and exporters. The Pride

Africa-Donor partnership facilitates smallholders access to credit needed to finance IFSS

investments and transition from old to new but often costly pesticides. Pride Africa is sponsored

by international donors including IDRC, IFAD, and FORD Foundation. The Pesticide Initiative

Program, a European Union funded project run by the Liaison Committee for Europe, Africa,

Caribbean, and Pacific (COLEACP), supports capacity building among green bean exporters.

Compliance with standards by the Mahagrapes farmers through collective action and PPP14

Mahagrapes has enabled farmers in several ways to ensure their compliance with IFSS.

Kleinwechter and Grethe (2005), while analyzing the adoption of EUREPGAP standards by

mango exporters in Peru, differentiate the compliance process into three stages: the information

stage followed by a decision stage, followed subsequently by an implementation stage.

Mahagrapes and the cooperatives have been active in all the three stages of the compliance

process. Even before the actual creation of Mahagrapes, efforts were made by some of the leading

and educated farmers of the region to involve the numerous pre-existing grape growing farmer

14 This section is from Roy and Thorat (2006)

CAPRI WORKING PAPER NO. 70 OCTOBER 2007

33

groups under the umbrella of Mahagrapes. In order to convince the group leaders, a team of seven

people: five farmers, one scientist, and one government official visited Europe to see for

themselves how grape farming, processing, and marketing was done along with the nature and

form of inputs used and marketing methods followed. A part of the cost of this visit was funded

by the state government. These lead farmers were convinced that the grape produced by the

farmers was of quality good enough to be exported to Europe provided they could meet the

standards and safety regulations, and thus Mahagrapes came to be set up.

Mahagrapes holds workshops where information on the standards is disseminated to the

member farmers. Farmers and grape handlers/sorters (primarily women) are continuously

informed about and trained in the latest grape growing and handling methods and processes. The

cooperatives and Mahagrapes jointly update the list of banned and approved pesticides and

fertilizers continuously, which varies with time and across markets. Similarly, the changes in the

permissible levels of chemical residues are also provided by them regularly. All this information

is published in the form of a yearly handbook in the native language and distributed free of

charge to members. In addition, acquiring a EUREPGAP certificate individually is costly for the

small and medium grape farmers. However, Mahagrapes has managed to provide cooperatives

with this certification. Thus, member farmers now have to pay just Rs. 1200 (approximately $28)

for certification which is much less than the cost of individual membership.

Once the information on the standards is available, action is needed relating to the

decision on implementation. In the implementation stage, Mahagrapes provides materials and

technical help along with infrastructural support to facilitate the implementation of the standards.

Similar to the Kenyan case, some farmers are trained as technical experts and ensure that

implementation of production practices satisfies the FSS. Mahagrapes also provides the farmers

with packaging material which comply with international norms. Plastic bags and pallets in which

the grapes are first packed are imported from Spain and other places. Special sulphur dioxide

sheets are imported from China. In the purchase of inputs, the role of CA presents itself quite

distinctly. The production and marketing process requires several imported inputs where the

differences in prices for farmers because of bulk buying by cooperatives are substantial.15 Bio-

15 Most significant input from the point of view of cost reduction through CA is the case of bio-fertilizers

from Australia

CAPRI WORKING PAPER NO. 70 OCTOBER 2007

34

fertilizer and bio-pesticide are developed and produced by Mahagrapes and provided to member

farmers cheaper than market rates.16

Apart from CA on the part of farmers that has made farmers well informed about the

market requirements and has facilitated lower costs of production, partnerships with public

agencies have played a very important role. For example, regular monitoring of the grape plant by

the scientists from the National Research Centre (NRC) in Pune (a government agency) ensures

that the plant remains in sanitary condition throughout the year and not just in the fruiting season.

Also, during the initial time periods with high rates of rejection, the role played by the

government was critical. The role of the government over time has been akin to infant industry

protection and thereby is a good example of PPP. State bodies like Maharashtra State Agricultural

Marketing Board (MSAMB) deputed and paid the salaries of the first governing officers.

MSAMAB also provided funds for consultancy services from experts on agri-marketing,

packaging, and technical services such as refrigeration and cooling. The government body,

National Cooperative Development Commission (NCDC), was also of great help along with

Agriculture and Processed Food Products Export Development Authority (APEDA), and National

Horticulture Board. The agency provided subsidized credit for the installation of post harvest

facilities that were crucial in bringing down the consignment rejection rates substantially.17

Cooperatives linked with Mahagrapes with partial financial aid from the state government and

partial self-financing have installed pre-coolers and cold storages at all the 16 cooperative

headquarters (thus showing CA and PPPs in complementary roles).

Absence of collective action and PPP in the cantaloupe supply chain in Mexico18

In Mexico, for the smallholders export was the main reason they went into cantaloupe

production, and just a small share of the production earlier was sent to domestic market. After a

new regulation, small growers turned to the domestic market. In the domestic market,

smallholders also face a problem with poor technical support and low prices during the harvesting

season of cantaloupes. Currently, most technical support is provided by the inputs suppliers, but

16 These inputs are also sold to non-members but at higher prices, implying cross-subsidization.

17 In the early years of exports, consignment rejection rates were greater than 80 percent. At present the

Mahagrapes claims a negligible rate of rejection. The turnaround by Mahagrapes especially in light of the

struggle by Indian horticultural exports to meet the standards in the western markets makes an exciting case

study from a food safety and quality point of view. 18

This section is from Avendaño et al., forthcoming

CAPRI WORKING PAPER NO. 70 OCTOBER 2007

35

only 38 percent of the smallholders receive this type of assistance (from survey of farmers in

north-western Mexico in 2002). In the growing season, oversupply is a problem; 44 percent of the

Mexican production is in the summer, from the states of Durango, Coahuila, Chihuahua

Tamaulipas (Northern Mexico), and for the rest of the regions the growing season is in winter.

Low prices and the lack of certification on food safety restrict the options for the small growers.

In the survey, smallholders reported that it is not economical for them to absorb the

additional cost associated with FSS, and they lacked the skills to keep the registers; they also

need training and additional employees for the design of standard operations procedures. In the

survey, 71 percent of farmers had adopted some new food safety practices (Avendaño 2006). Of

this group, 9 percent were small farmers, 54 percent were medium, and 37 percent were large. Of

the non-adopters, 14 percent were small and 86 percent were medium. Another obstacle for

smallholders was the lack of administrative management; 90 percent of the small growers hardly

know their costs associated with production, and they do not keep accounting registers and do not

plan production in advance. Lack of management practices can be explained partly as a result of

the low educational level among farmers. About 60 percent farmers have primary education (6

years); 13 percent have secondary (9 years), and only 15 percent high school (11 years).

Apart from collective action that can help farmers establish packing facilities together

and afford the certification costs, PPPs can also play an important role. One form of CA and PPP

that can be useful is the organization of growers in an integrated firm that allows them to buy at

greater scale with better prices. Growers and government together like in case of Kenyan green

beans and grapes in India should develop a program to comply with IFSS. PPPs could also be

useful in supporting research and development activities targeted to the needs of smallholders.

Such partnerships can be encouraged through institutional agreements between government and

universities in the region. Cooperation among farmers and partnership with government can

facilitate the installation of a new packing facility run by small growers.