Embed Size (px)

Citation preview

The South Ayrshire Economy and its Future

Prospects: A Strategic Review

Chris Doyle

Policy, Performance & Communication

South Ayrshire Council

24 August 2011

Pag

e2

Pag

e2

CONTENTS

Page

Executive Summary 4

Background to the Report 7

Chapter 1: Current and Future Economic Potential of the South Ayrshire Economy 8

The South Ayrshire Economy in 2011 8

Economic Growth 8

Productivity 9

Employment Structure and Business Base 11

Participation in the Labour Market 13

Unemployment and Economic Inactivity 15

Outlook for the South Ayrshire Economy in the Period 2011-2014 16

General Prospects for Employment 16

Prospects for Key Industrial Sectors 17

Prospects for Different Communities 20

Employment Blackspots 20

Vulnerable population groups 21

The Longer-Term Growth Prospects for the South Ayrshire Economy 23

The Resilience of the Local Economy 23

Diversifying the Employment Base 25

Increasing the Skills Level of the Local Workforce 27

Stimulating New Business Creation and Helping Existing Businesses

to Grow 28

Making the Area More Attractive to People and Businesses 28

Chapter 2: Future Opportunities for the South Ayrshire Economy 30

Fundamental Issues 30

Key Economic Drivers and Future Opportunities 30

Engineering: An Industry in Decline or transition? 31

Tourism: A Driver of Growth? 36

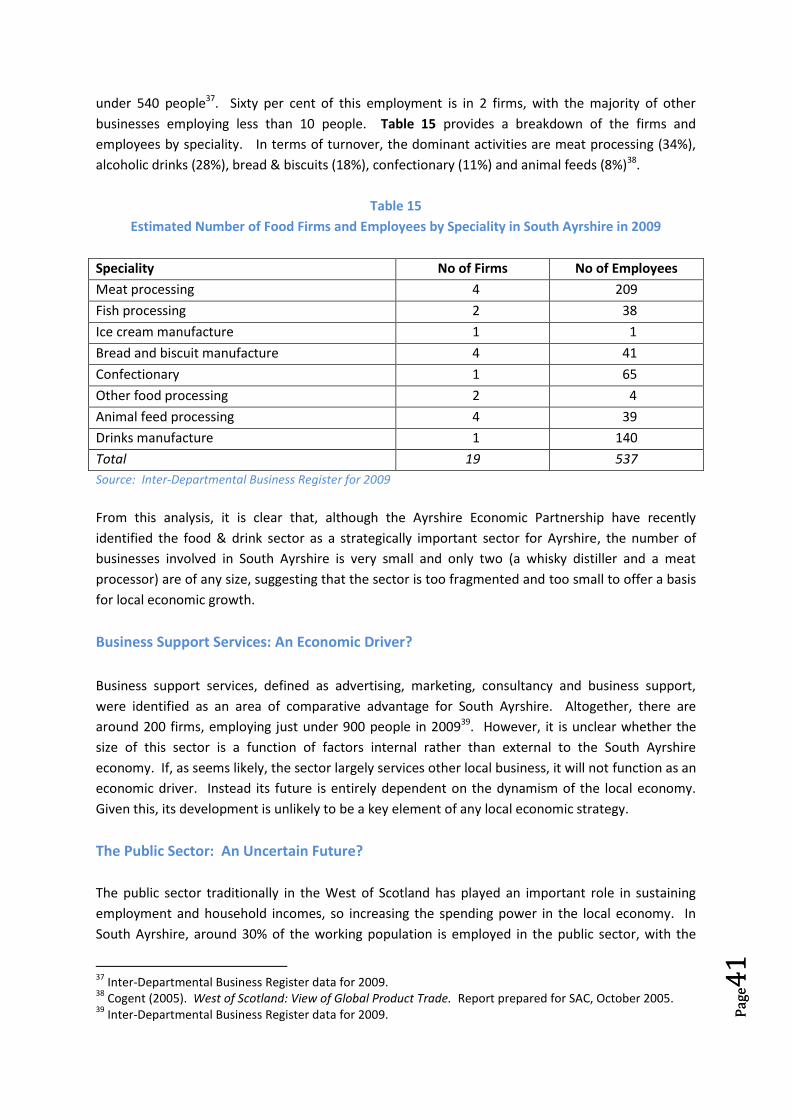

Food & Drink Processing: The Right Ingredients for Growth? 40

Business Support Services: An Economic Driver? 41

The Public Sector: An Uncertain Future? 41

Pag

e3

Pag

e3

Page

Inequality of Economic Opportunity 42

Urban Deprivation 42

Town Centre Re-Development 43

Rural Communities 44

Youth Unemployment 45

Concluding Remarks 46

Chapter 3: Challenges for the Future 47

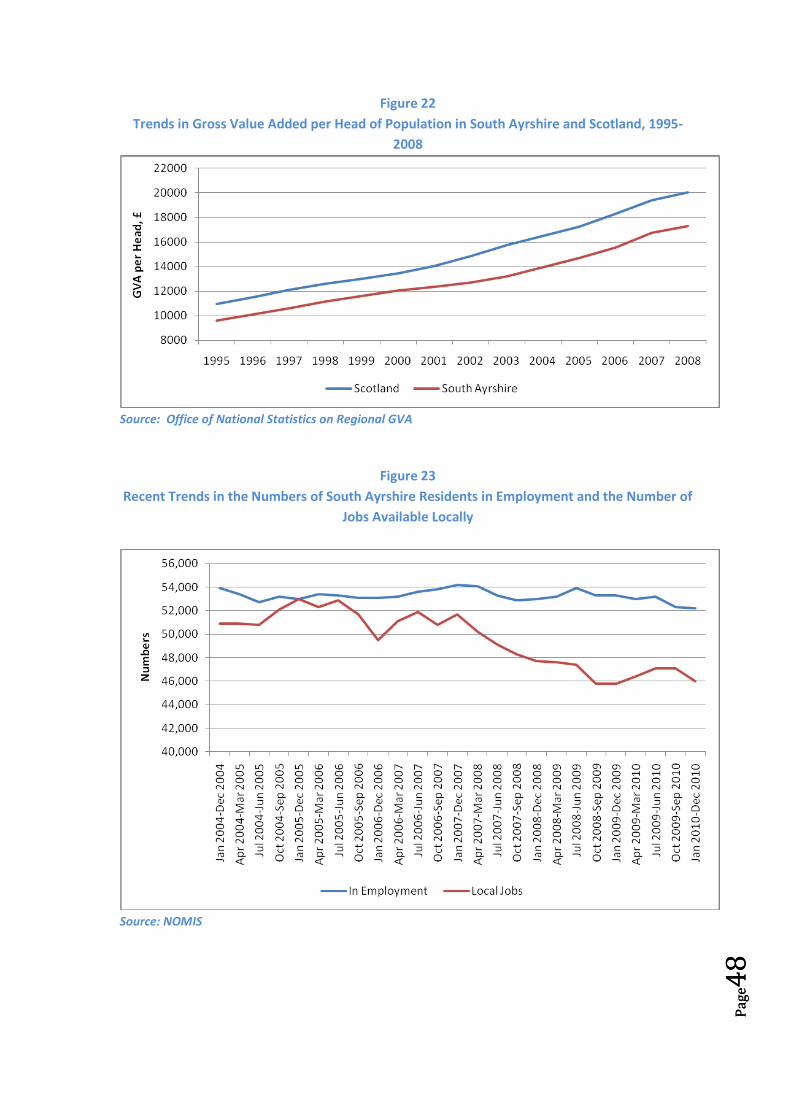

An Uncertain Future 47

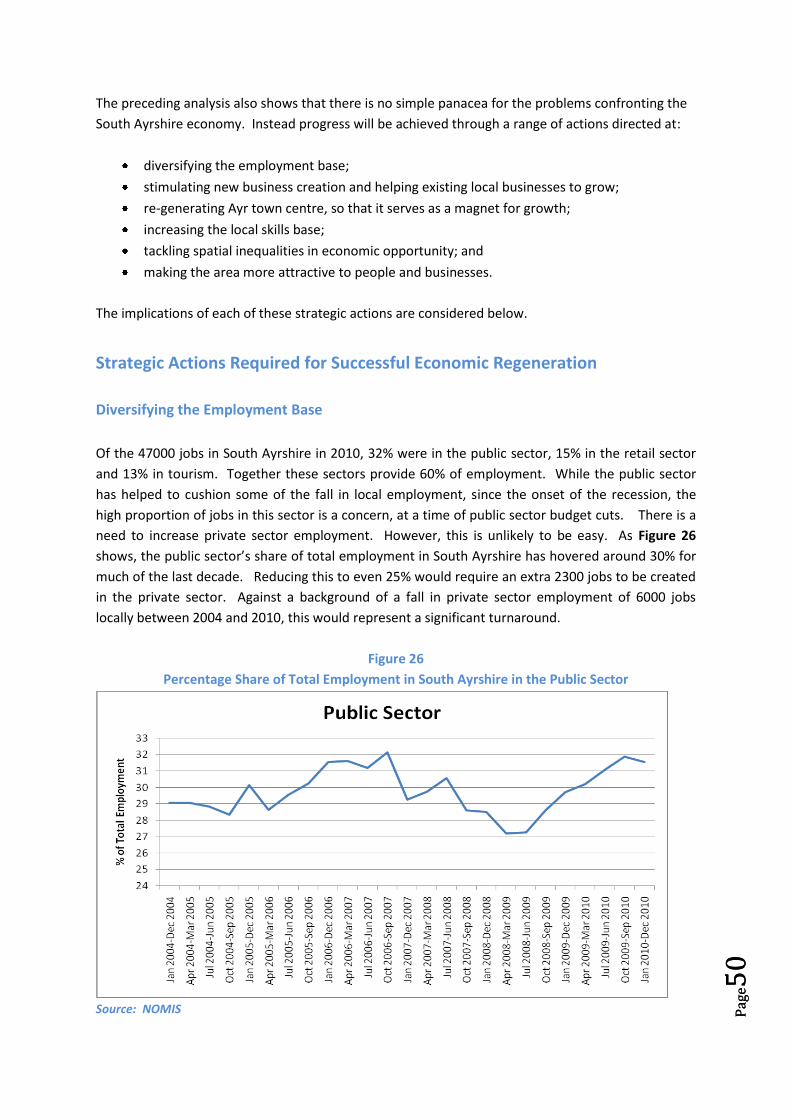

Strategic Actions Required for Successful Economic Regeneration 50

Diversifying the Employment Base 50

Stimulating New Business Creation and Help Existing Businesses

to Grow 51

Regenerating Ayr Town Centre 52

Increasing the Skill Levels of the Local Workforce 52

Tackling Spatial Inequalities in Economic Opportunity 54

Making the Area More Attractive to People and Businesses 55

Towards an Economic Strategy for South Ayrshire 56

What are the Key Objectives as Regards Local Economic Development? 56

How Far should the Economic Future of South Ayrshire be Linked to the

Glasgow City Region and what does this Imply for Levels of

Commuting? 56

What Industrial Sectors should Form the Focus of any Strategy? 57

What are the Potential Barriers to Economic Development and How

can the Partnership Assist Overcoming these? 58

With what Other Areas of Policy does any Economic Strategy Need to

Integrate? 58

Pag

e4

Pag

e4

EXECUTIVE SUMMARY

1. As a prelude to developing an economic strategy for South Ayrshire, this report attempts to

bring together the available information on South Ayrshire’s economy and to explore the

potential for growing economic output. To provide a strong evidence base for the strategy,

the study seeks to:

review recent trends in industrial output and employment to provide a profile of the

local economy;

examine the potential areas for economic growth; and

assess how the Economic Development Partnership can contribute to realising any

potential.

Specifically, the study examines 5 questions:

What are the key objectives as regards local economic development?

How far should the economic future of South Ayrshire be linked to the development

of the Glasgow city region and what does this imply for levels of commuting?

What industrial sectors should form the focus of any strategy?

What are the potential barriers to economic development and how can the

Partnership assist in overcoming these?

With what other areas of policy does any economic strategy need to integrate?

2. As far as the key economic objectives for the proposed economic strategy are concerned,

these are arguably fourfold:

to halt the current sharp decline in the number of jobs available in the local

economy. Between 2006 and 2010, the number of jobs in South Ayrshire fell by 8%;

most of this decline was in private sector employment.

to diversify the economic base of the local economy. Of the 47000 jobs in the local

area in 2010, 33% were in the public sector, 15% in the retail sector and 13% in

tourism. Together these three sectors provide 60% of all local jobs. This is an

immediate problem as the public sector is facing potential severe job losses as a

result of budget cuts, while both retail and tourism businesses are facing challenging

times as a result of a loss of consumer confidence.

to reverse the current decline in population and the contraction of the working-age

population by attracting more families and professional people to live in South

Ayrshire. This should boost consumer spending locally and assist the revival of

sectors like the retail trade and construction.

to ensure that any benefits from economic growth are equitably shared, so that

deprived areas in North Ayr and rural communities in the south of the local authority

share in any gains.

Pag

e5

Pag

e5

3. Inevitably the decline in the economic base of South Ayrshire and the contraction in the

number of local jobs has led to residents seeking work outside the local authority.

Commuting is now a key feature of the local employment market, with around 30% of the

working population resident in South Ayrshire commuting to other areas for employment.

Moreover, this trend has increased over the last decade. However, while this is directly a

response to the lack of local jobs, there is also a certain inevitability about the trend as more

jobs and investment are sucked into cities, like Glasgow. It may, therefore, be sensible to

recognise this inevitability and put in place strategies which capitalise on these commuting

flows, rather than trying to fight them. Even if the jobs are no created locally, the likelihood

is that the income generated will filter into the local economy. In this regard, South Ayrshire

has the potential to be an attractive place to live and building more homes for professional

people may be a way of attracting those working in places like Glasgow to migrate to South

Ayrshire. However, people will only migrate to South Ayrshire if an attractive environment is

sustained. This means revitalising the town centre of Ayr, improving local leisure facilities

and schools, and generally providing a clean and attractive environment.

4. However, while the economic future of South Ayrshire can no longer be considered in

isolation from developments elsewhere in the West of Scotland, the area does need to

diversify its economic base, so as to provide a better market for local employment in the

future. In this study the sectors identified as having the greatest potential for development

are aerospace engineering, renewables and tourism. Each sector presents slightly different

challenges:

The aerospace industry in South Ayrshire is already fairly well established. However,

with 70% of its activity related to aircraft maintenance and repair, uncertainty over

the future of Prestwick Airport potentially affects the sector’s future. However,

some confidence can be drawn from a recent survey of local aerospace businesses

that suggested that firms would not relocate even if passenger and freight

operations ceased at Prestwick. Nevertheless, expanding the number of businesses

specifically connected with the fabrication of airframe components, which might be

less vulnerable to changes in activity at the airport, may be a key aim.

For renewable, the problem is that there are currently only a handful of local firms

currently supplying ‘low carbon’ goods and services. As such, for the potential of

this sector to be realised, a cluster of firms specialising in renewables needs to be

developed. Although the area’s strong engineering tradition might provide the basis

for such a cluster, at the moment this sector is in its infancy and its local

development will face strong competition from other areas in Scotland.

Tourism is a long-standing activity and a major employer in the area. The problem is

that there has been little growth in the sector’s income. The number of tourists and

day trippers visiting the area has stagnated and spending per trip remains low. The

area’s image as a tourism destination is not strong and what image that it has is of a

traditional seaside holiday destination. The area needs to transform its image and

increase the range of holiday ‘experiences’.

Pag

e6

Pag

e6

5. However, it is unlikely that any of these potential local economic opportunities will be

realised without some form of public intervention and facilitation. The majority of local

private sector businesses are small and experience elsewhere has shown that it is hard for

SMEs to find the time and resources to invest in the innovation, product development and

research needed to grasp new opportunities. In these circumstances the Economic

Development Partnership has a role in:

helping to identify and raise awareness among local firms of the business

opportunities that could potentially be exploited by them in the three target areas

of aerospace, renewable and tourism;

assisting local firms to develop networks, which offer the opportunity for

collaborative business development, the potential for more integrated supply chains

and a mechanism for jointly exploiting R&D;

targeting business support and investment on those businesses which are able to

increase net local employment;

encouraging a stronger dialogue between local businesses and local training

providers and educational establishments to ensure the supply of young graduates

with the required skills; and

ensuring local infrastructure plans and investments are aligned with the needs of the

key growth sectors.

6. While attracting new businesses and generating new jobs is central to any economic strategy

for the area, a secondary consideration has to be how any growth impacts on the economic

opportunities for different areas and communities. The existence of pockets of high

economic deprivation in North Ayr and Girvan has dominated attempts to regenerate parts

of the South Ayrshire economy. More recently, the growing problem of town centre decline,

especially in Ayr itself, has become an issue, while a concern has developed about the

emergence of a two-speed economy, with the southern, rural part of the Local Authority

experiencing the exodus of young people in response to limited job opportunities and a poor

transport infrastructure. Finally, there is increasing evidence that young adults have been

especially hard hit in terms of job opportunities by the recent recession in South Ayrshire.

Pag

e7

Pag

e7

BACKGROUND TO THE REPORT

The Economic Development Partnership of the South Ayrshire Community Planning Partnership

has decided to develop a new economic strategy for the local economy. As a prelude to this, the

current report attempts to bring together the available information on South Ayrshire’s economy

and to explore the potential for growing economic output. To provide a strong evidence base for

the strategy, the current study seeks to:

review recent trends in industrial output and employment to provide a profile of the

local economy;

examine the potential areas for economic growth; and

assess how the Economic Development Partnership can contribute to realising any

potential.

Specifically, the study examines five questions:

What are the key objectives as regards local economic development?

How far should the economic future of South Ayrshire be linked to the development

of the Glasgow city region and what does this imply for levels of commuting?

What industrial sectors should form the focus of any strategy?

What are the potential barriers to economic development and how can the

Partnership assist in overcoming these?

With what other areas of policy does any economic strategy need to integrate?

Pag

e8

Pag

e8

CHAPTER 1: CURRENT AND FUTURE ECONOMIC PROSPECTS OF THE SOUTH

AYRSHIRE ECONOMY

The South Ayrshire Economy in 2011

Economic Growth

Total economic output (measured as Gross Value Added or GVA) from the South Ayrshire area in

2008 was just over £1.9bn, representing around 1.8% of Scotland’s GVA of £103.5bn1. This is

commensurate with the area’s share of national employment. However, average growth rates at

1.7% in the decade 1998-2008 lagged behind the Scottish average of 2.2% and the UK average of

2.6% (see Figure 1). In particular, growth in the South Ayrshire economy stalled and reversed

between 2001 and 2003, largely due to the foot and mouth outbreak, which had a particularly

severe impact on agricultural output and tourism in the area. The figure also shows that there was a

fall in economic output across South Ayrshire in 2008, mirroring the falls in Scotland and the UK.

Figure 1

Trends in UK, Scottish and South Ayrshire Annual Growth Rates

Source: SLIMSconsulting ‘Towards a Wealthier & Fairer South Ayrshire’ June 2011

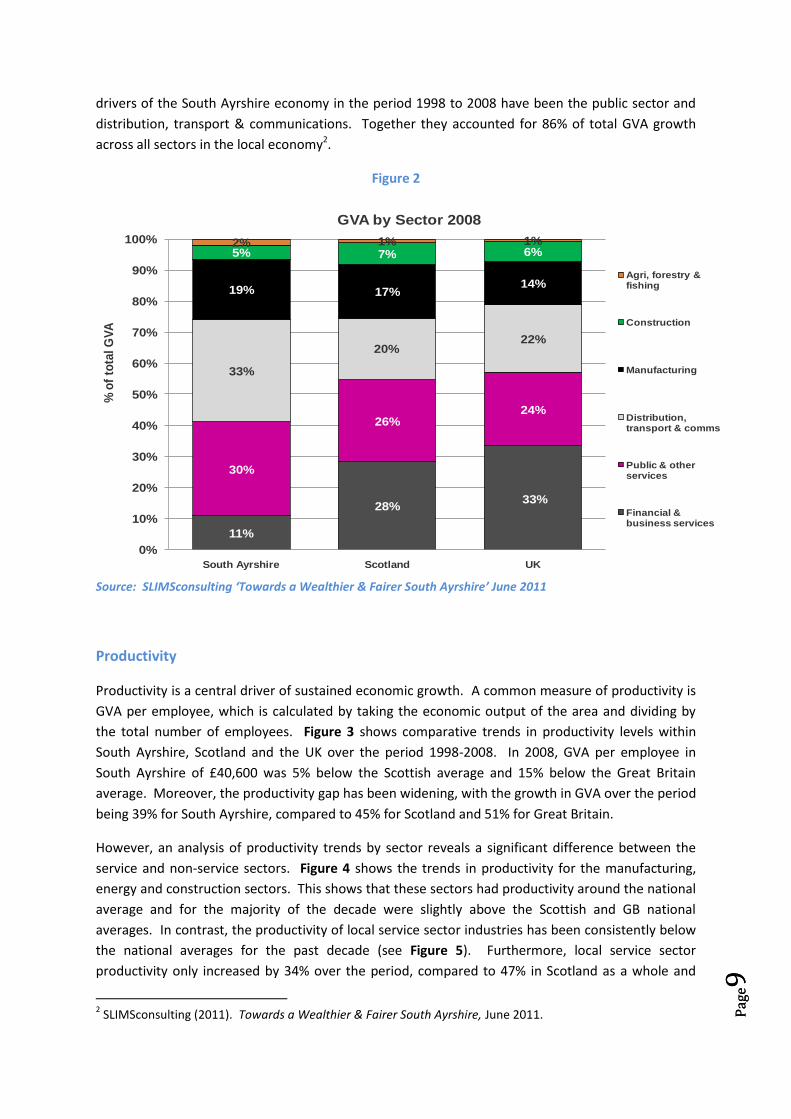

Almost three quarters of all economic output from the South Ayrshire economy is accounted for by

the service sector. In 2008, services accounted for 74% of the total GVA, while industrial activities,

including manufacturing and construction accounted for 24%. This is a similar proportion to the

Scottish average. As shown in Figure 2, the largest sectors in South Ayrshire are distribution,

transport & communications (33% of all output), public sector & other services (30%) and

manufacturing 19%. The area has a relatively small financial & business services sector, which

accounted for only 11% of GVA in 2008, compared to 28% nationally. In terms of output, the key

1 Office of National Statistics

-4%

-3%

-2%

-1%

0%

1%

2%

3%

4%

5%

6%

1997

-98

1998

-99

1999

-00

2000

-01

2001

-02

2002

-03

2003

-04

2004

-05

2005

-06

2006

-07

2007

-08

GVA

gro

wth

rate

GVA Growth Rates, 1998-2008

South Ayrshire

Scotland

UK

Pag

e9

Pag

e9

drivers of the South Ayrshire economy in the period 1998 to 2008 have been the public sector and

distribution, transport & communications. Together they accounted for 86% of total GVA growth

across all sectors in the local economy2.

Figure 2

Source: SLIMSconsulting ‘Towards a Wealthier & Fairer South Ayrshire’ June 2011

Productivity

Productivity is a central driver of sustained economic growth. A common measure of productivity is

GVA per employee, which is calculated by taking the economic output of the area and dividing by

the total number of employees. Figure 3 shows comparative trends in productivity levels within

South Ayrshire, Scotland and the UK over the period 1998-2008. In 2008, GVA per employee in

South Ayrshire of £40,600 was 5% below the Scottish average and 15% below the Great Britain

average. Moreover, the productivity gap has been widening, with the growth in GVA over the period

being 39% for South Ayrshire, compared to 45% for Scotland and 51% for Great Britain.

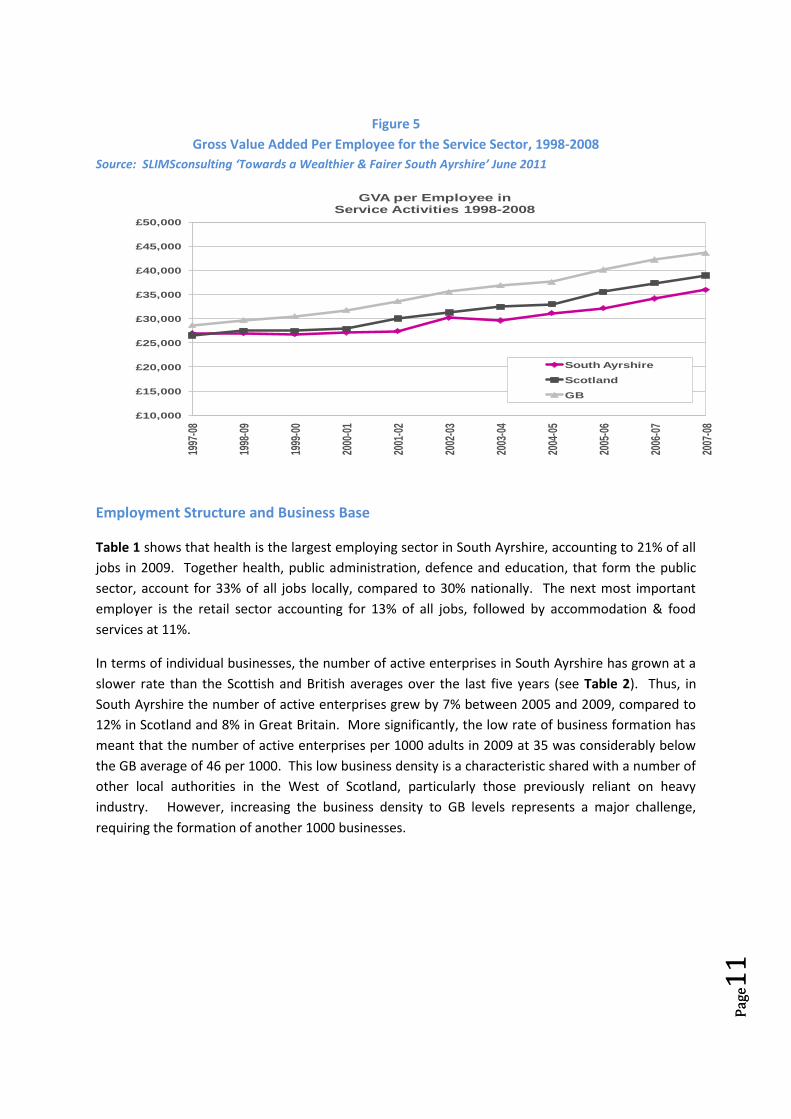

However, an analysis of productivity trends by sector reveals a significant difference between the

service and non-service sectors. Figure 4 shows the trends in productivity for the manufacturing,

energy and construction sectors. This shows that these sectors had productivity around the national

average and for the majority of the decade were slightly above the Scottish and GB national

averages. In contrast, the productivity of local service sector industries has been consistently below

the national averages for the past decade (see Figure 5). Furthermore, local service sector

productivity only increased by 34% over the period, compared to 47% in Scotland as a whole and

2 SLIMSconsulting (2011). Towards a Wealthier & Fairer South Ayrshire, June 2011.

11%

28%33%

30%

26%24%

33%

20%22%

19% 17%14%

5% 7% 6%2% 1% 1%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

South Ayrshire Scotland UK

% o

f to

tal G

VA

GVA by Sector 2008

Agri, forestry & fishing

Construction

Manufacturing

Distribution, transport & comms

Public & other services

Financial & business services

Pag

e10

P

age1

0

52% in Great Britain. As a result in this sector, there has been a widening productivity gap with the

rest of economy.

Figure 3

Comparative Productivity Trends

Source: SLIMSconsulting ‘Towards a Wealthier & Fairer South Ayrshire’ June 2011

Figure 4

Gross Value Added Per Employee for Manufacturing, Energy & Construction, 1998-2008

Source: SLIMSconsulting ‘Towards a Wealthier & Fairer South Ayrshire’ June 2011

£20,000

£25,000

£30,000

£35,000

£40,000

£45,000

£50,000

1997

-08

1998

-09

1999

-00

2000

-01

2001

-02

2002

-03

2003

-04

2004

-05

2005

-06

2006

-07

2007

-08

GV

A p

er E

mp

loye

e

GVA per Employee, 1998-2008

South Ayrshire

Scotland

GB

£20,000

£25,000

£30,000

£35,000

£40,000

£45,000

£50,000

£55,000

£60,000

£65,000

£70,000

1997

-08

1998

-09

1999

-00

2000

-01

2001

-02

2002

-03

2003

-04

2004

-05

2005

-06

2006

-07

2007

-08

GVA per Employee inIndustrial Activities 1998-2008

South Ayrshire

Scotland

GB

Pag

e11

P

age1

1

Figure 5

Gross Value Added Per Employee for the Service Sector, 1998-2008

Source: SLIMSconsulting ‘Towards a Wealthier & Fairer South Ayrshire’ June 2011

Employment Structure and Business Base

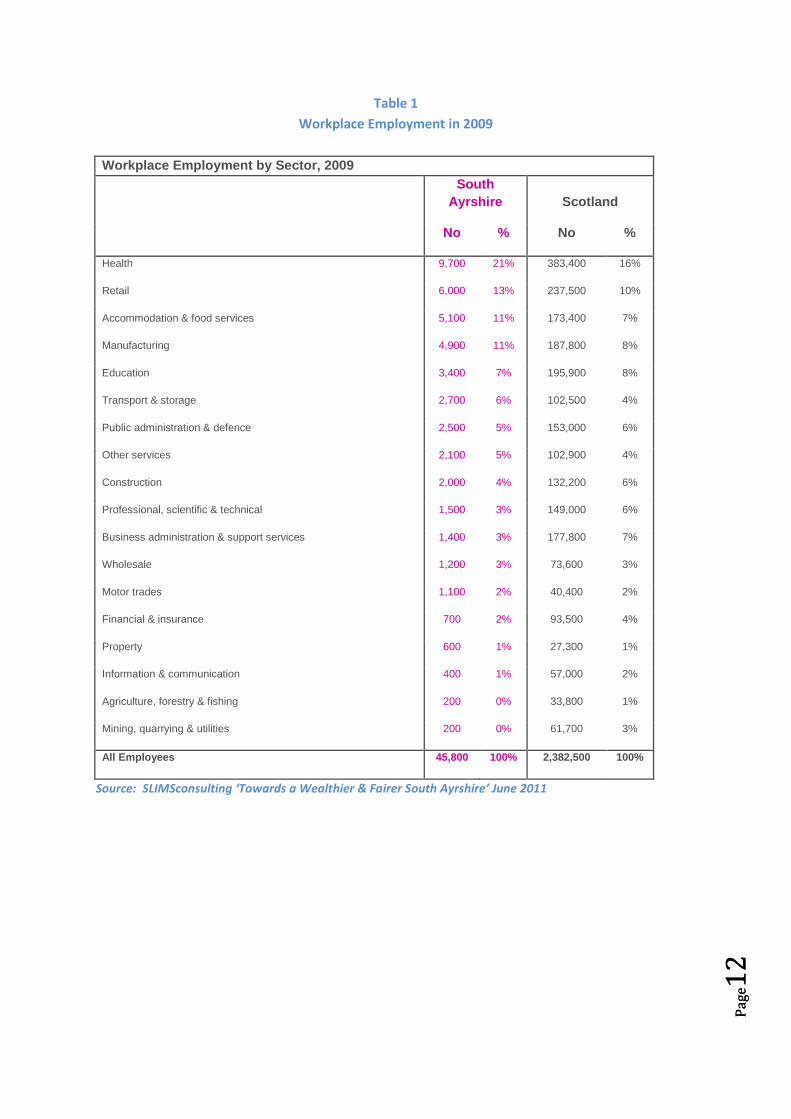

Table 1 shows that health is the largest employing sector in South Ayrshire, accounting to 21% of all

jobs in 2009. Together health, public administration, defence and education, that form the public

sector, account for 33% of all jobs locally, compared to 30% nationally. The next most important

employer is the retail sector accounting for 13% of all jobs, followed by accommodation & food

services at 11%.

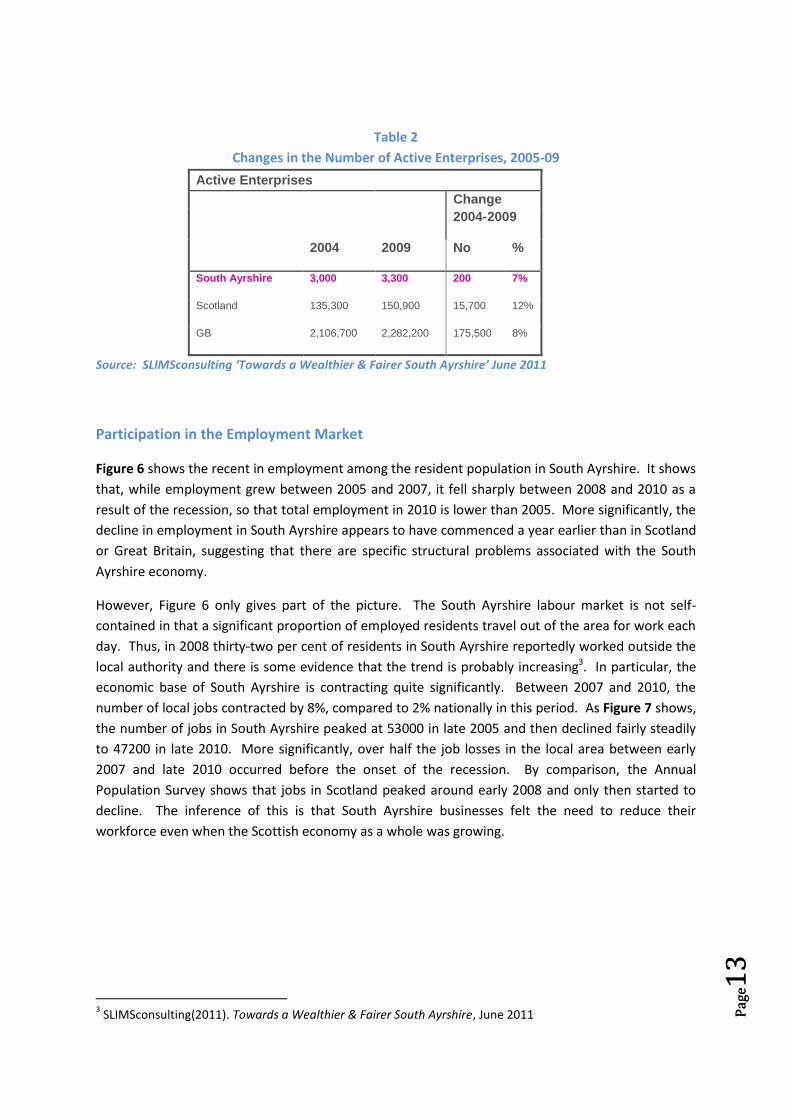

In terms of individual businesses, the number of active enterprises in South Ayrshire has grown at a

slower rate than the Scottish and British averages over the last five years (see Table 2). Thus, in

South Ayrshire the number of active enterprises grew by 7% between 2005 and 2009, compared to

12% in Scotland and 8% in Great Britain. More significantly, the low rate of business formation has

meant that the number of active enterprises per 1000 adults in 2009 at 35 was considerably below

the GB average of 46 per 1000. This low business density is a characteristic shared with a number of

other local authorities in the West of Scotland, particularly those previously reliant on heavy

industry. However, increasing the business density to GB levels represents a major challenge,

requiring the formation of another 1000 businesses.

£10,000

£15,000

£20,000

£25,000

£30,000

£35,000

£40,000

£45,000

£50,000

1997

-08

1998

-09

1999

-00

2000

-01

2001

-02

2002

-03

2003

-04

2004

-05

2005

-06

2006

-07

2007

-08

GVA per Employee inService Activities 1998-2008

South Ayrshire

Scotland

GB

Pag

e12

P

age1

2

Table 1

Workplace Employment in 2009

Workplace Employment by Sector, 2009

South

Ayrshire Scotland

No % No %

Health 9,700 21% 383,400 16%

Retail 6,000 13% 237,500 10%

Accommodation & food services 5,100 11% 173,400 7%

Manufacturing 4,900 11% 187,800 8%

Education 3,400 7% 195,900 8%

Transport & storage 2,700 6% 102,500 4%

Public administration & defence 2,500 5% 153,000 6%

Other services 2,100 5% 102,900 4%

Construction 2,000 4% 132,200 6%

Professional, scientific & technical 1,500 3% 149,000 6%

Business administration & support services 1,400 3% 177,800 7%

Wholesale 1,200 3% 73,600 3%

Motor trades 1,100 2% 40,400 2%

Financial & insurance 700 2% 93,500 4%

Property 600 1% 27,300 1%

Information & communication 400 1% 57,000 2%

Agriculture, forestry & fishing 200 0% 33,800 1%

Mining, quarrying & utilities 200 0% 61,700 3%

All Employees 45,800 100% 2,382,500 100%

Source: SLIMSconsulting ‘Towards a Wealthier & Fairer South Ayrshire’ June 2011

Pag

e13

P

age1

3

Table 2

Changes in the Number of Active Enterprises, 2005-09

Active Enterprises

Change

2004-2009

2004 2009 No %

South Ayrshire 3,000 3,300 200 7%

Scotland 135,300 150,900 15,700 12%

GB 2,106,700 2,282,200 175,500 8%

Source: SLIMSconsulting ‘Towards a Wealthier & Fairer South Ayrshire’ June 2011

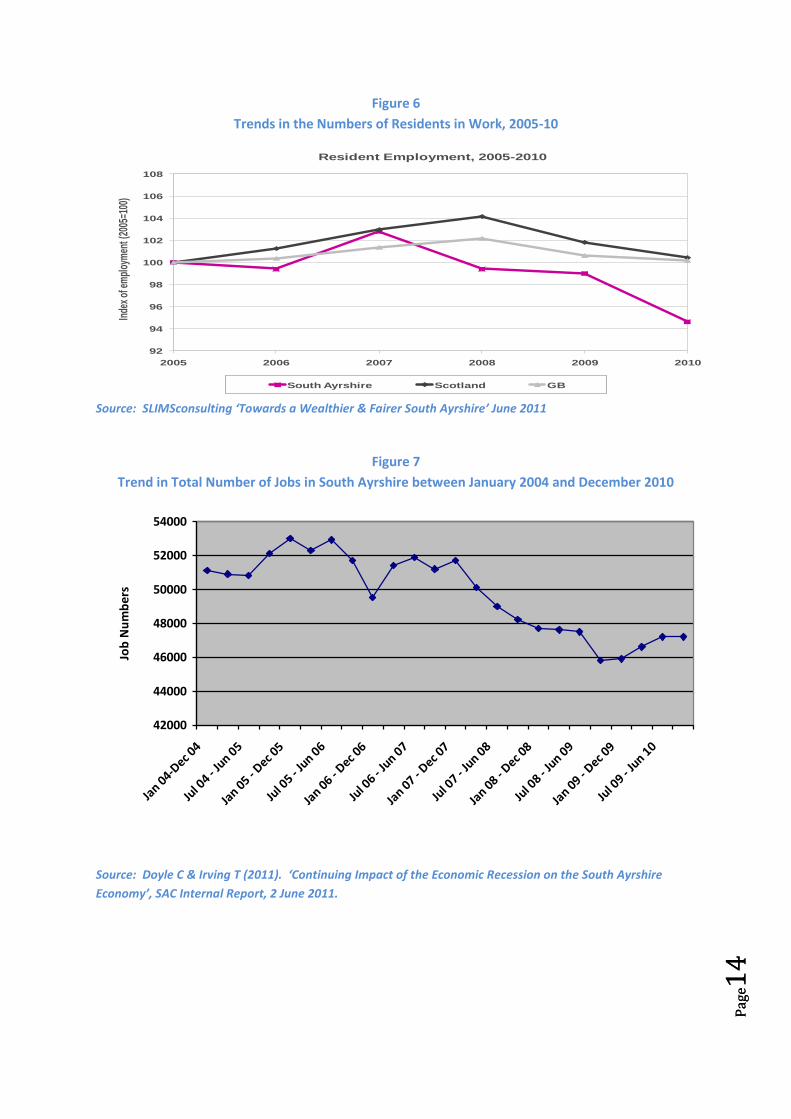

Participation in the Employment Market

Figure 6 shows the recent in employment among the resident population in South Ayrshire. It shows

that, while employment grew between 2005 and 2007, it fell sharply between 2008 and 2010 as a

result of the recession, so that total employment in 2010 is lower than 2005. More significantly, the

decline in employment in South Ayrshire appears to have commenced a year earlier than in Scotland

or Great Britain, suggesting that there are specific structural problems associated with the South

Ayrshire economy.

However, Figure 6 only gives part of the picture. The South Ayrshire labour market is not self-

contained in that a significant proportion of employed residents travel out of the area for work each

day. Thus, in 2008 thirty-two per cent of residents in South Ayrshire reportedly worked outside the

local authority and there is some evidence that the trend is probably increasing3. In particular, the

economic base of South Ayrshire is contracting quite significantly. Between 2007 and 2010, the

number of local jobs contracted by 8%, compared to 2% nationally in this period. As Figure 7 shows,

the number of jobs in South Ayrshire peaked at 53000 in late 2005 and then declined fairly steadily

to 47200 in late 2010. More significantly, over half the job losses in the local area between early

2007 and late 2010 occurred before the onset of the recession. By comparison, the Annual

Population Survey shows that jobs in Scotland peaked around early 2008 and only then started to

decline. The inference of this is that South Ayrshire businesses felt the need to reduce their

workforce even when the Scottish economy as a whole was growing.

3 SLIMSconsulting(2011). Towards a Wealthier & Fairer South Ayrshire, June 2011

Pag

e14

P

age1

4

Figure 6

Trends in the Numbers of Residents in Work, 2005-10

Source: SLIMSconsulting ‘Towards a Wealthier & Fairer South Ayrshire’ June 2011

Figure 7

Trend in Total Number of Jobs in South Ayrshire between January 2004 and December 2010

42000

44000

46000

48000

50000

52000

54000

Jan 0

4-Dec 0

4

Jul 0

4 - Ju

n 05

Jan 0

5 - Dec 0

5

Jul 0

5 - Ju

n 06

Jan 0

6 - Dec 0

6

Jul 0

6 - Ju

n 07

Jan 0

7 - Dec 0

7

Jul 0

7 - Ju

n 08

Jan 0

8 - Dec 0

8

Jul 0

8 - Ju

n 09

Jan 0

9 - Dec 0

9

Jul 0

9 - Ju

n 10

Job

Nu

mb

ers

Source: Doyle C & Irving T (2011). ‘Continuing Impact of the Economic Recession on the South Ayrshire

Economy’, SAC Internal Report, 2 June 2011.

92

94

96

98

100

102

104

106

108

2005 2006 2007 2008 2009 2010

Inde

x of

em

ploy

men

t (20

05=1

00)

Resident Employment, 2005-2010

South Ayrshire Scotland GB

Pag

e15

P

age1

5

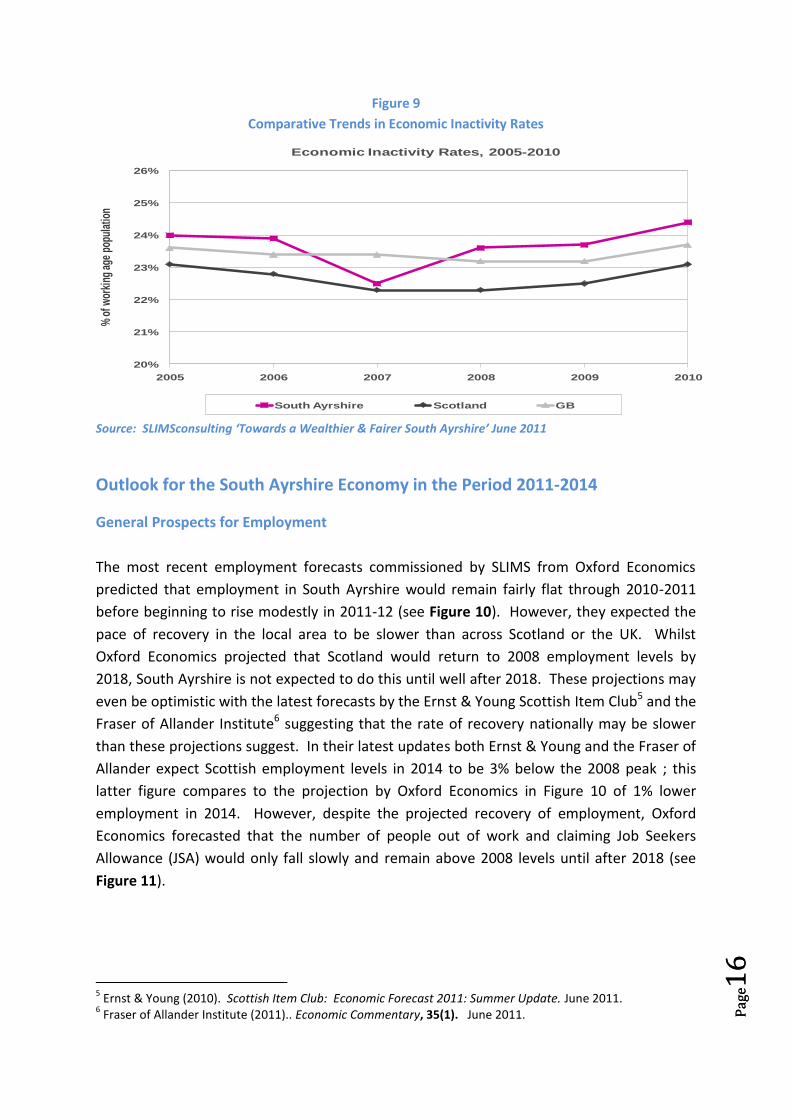

Unemployment and Economic Inactivity

Based on the wider definition of unemployment adopted by the International Labour Office4, in 2010

there were 4600 South Ayrshire residents who were unemployed; 12% higher than in 2000 (see

Table 3). This increase was broadly similar to that experienced in Scotland as a whole, but

considerably less than the rise in Great Britain. However, the lower increase in the unemployment

rate cannot disguise the fact that unemployment in South Ayrshire at 8.4% is higher than the

Scottish average of 7.4% and the GB average of 7.7%. Nevertheless, as shown in Figure 8, there has

been some contraction in the gap between the area and national averages. However, these figures

may not tell the whole story. The proportion of the working-age population not in work (the so-

called economic inactivity rate) in South Ayrshire has remained stubbornly above the Scottish and

Great Britain averages for the last 5-6 years (see Figure 9). Some of these may represent ‘hidden’

unemployment.

Table 3

Medium-Term Trends in Unemployment

Unemployment 2000 & 2010

Change

2000-2010

2000 2010 No %

South Ayrshire 4,100 4,600 500 12%

Scotland 178,000 200,900 22,900 13%

GB 1,641,000 2,344,600 703,600 43%

Source: SLIMSconsulting ‘Towards a Wealthier & Fairer South Ayrshire’ June 2011

Figure 8

Comparative Trends in Unemployment Rates

Source: SLIMSconsulting ‘Towards a Wealthier & Fairer South Ayrshire’ June 2011

4 Includes all those who want to work, are available for work and are actively seeking employment, not those

simply claiming Job Seekers Allowance.

0

1

2

3

4

5

6

7

8

9

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

% o

f eco

nom

ical

ly ac

tive u

nem

ploy

ed

Unemployment Rates, 2000-2010

South Ayrshire

Scotland

GB

Pag

e16

P

age1

6

Figure 9

Comparative Trends in Economic Inactivity Rates

Source: SLIMSconsulting ‘Towards a Wealthier & Fairer South Ayrshire’ June 2011

Outlook for the South Ayrshire Economy in the Period 2011-2014

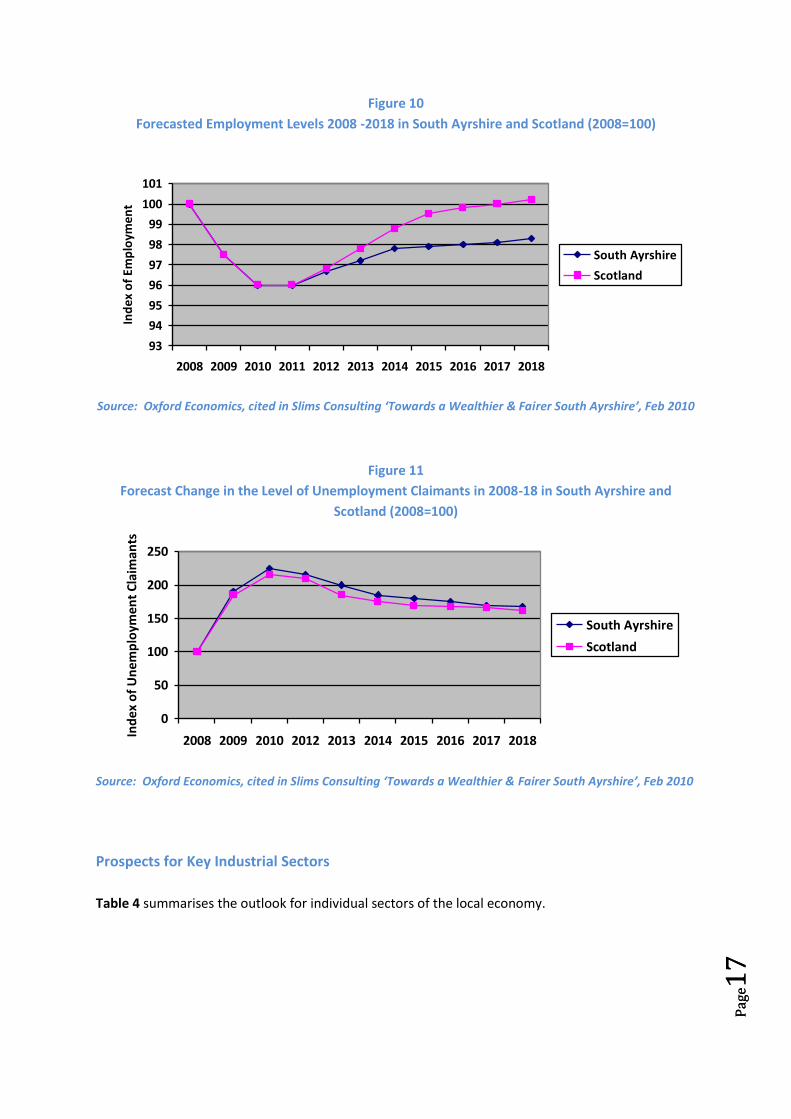

General Prospects for Employment

The most recent employment forecasts commissioned by SLIMS from Oxford Economics

predicted that employment in South Ayrshire would remain fairly flat through 2010-2011

before beginning to rise modestly in 2011-12 (see Figure 10). However, they expected the

pace of recovery in the local area to be slower than across Scotland or the UK. Whilst

Oxford Economics projected that Scotland would return to 2008 employment levels by

2018, South Ayrshire is not expected to do this until well after 2018. These projections may

even be optimistic with the latest forecasts by the Ernst & Young Scottish Item Club5 and the

Fraser of Allander Institute6 suggesting that the rate of recovery nationally may be slower

than these projections suggest. In their latest updates both Ernst & Young and the Fraser of

Allander expect Scottish employment levels in 2014 to be 3% below the 2008 peak ; this

latter figure compares to the projection by Oxford Economics in Figure 10 of 1% lower

employment in 2014. However, despite the projected recovery of employment, Oxford

Economics forecasted that the number of people out of work and claiming Job Seekers

Allowance (JSA) would only fall slowly and remain above 2008 levels until after 2018 (see

Figure 11).

5 Ernst & Young (2010). Scottish Item Club: Economic Forecast 2011: Summer Update. June 2011.

6 Fraser of Allander Institute (2011).. Economic Commentary, 35(1). June 2011.

20%

21%

22%

23%

24%

25%

26%

2005 2006 2007 2008 2009 2010

% o

f wor

king

age

pop

ulat

ion

Economic Inactivity Rates, 2005-2010

South Ayrshire Scotland GB

Pag

e17

P

age1

7

Figure 10

Forecasted Employment Levels 2008 -2018 in South Ayrshire and Scotland (2008=100)

93

94

95

96

97

98

99

100

101

2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 2018

Ind

ex o

f Em

plo

ymen

t

South Ayrshire

Scotland

Source: Oxford Economics, cited in Slims Consulting ‘Towards a Wealthier & Fairer South Ayrshire’, Feb 2010

Figure 11

Forecast Change in the Level of Unemployment Claimants in 2008-18 in South Ayrshire and

Scotland (2008=100)

0

50

100

150

200

250

2008 2009 2010 2012 2013 2014 2015 2016 2017 2018

Ind

ex o

f U

nem

plo

ymen

t C

laim

ants

South Ayrshire

Scotland

Source: Oxford Economics, cited in Slims Consulting ‘Towards a Wealthier & Fairer South Ayrshire’, Feb 2010

Prospects for Key Industrial Sectors

Table 4 summarises the outlook for individual sectors of the local economy.

Pag

e18

P

age1

8

Table 4

Prospects for Farming

Farming and fishing in 2010 provided only 900 jobs in

South Ayrshire, representing a little under 2% of the

workforce7. Livestock rearing and dairy farming are

still the predominant activities. Like the rest of

Scotland, farm incomes in the year to March 2010

rose by 18% in real terms. However, while specialist

sheep and cattle farms saw rises, dairy and arable

farmers suffered falls in income. Nevertheless, the

rise in cereal and milk prices in 2010/11, attributed to

global shortages, will have gone some way to

improving both arable and dairy farm incomes.

Unlike other sectors, the future is less likely to be

influenced by consumer spending and more by farm

support policies, inflationary cost pressures and world

food supplies.

Prospects for Construction

The downturn in construction activity in South

Ayrshire started in 2005-06, before the economic

recession began to impact on the rest of the

economy. In 2010-11, the construction industry

remained depressed with the Scottish Construction

Monitor reporting a 29% fall in private house

construction and a 41% fall in private commercial

construction in early 2011, compared to 2008.

However, it also hinted at a slight improvement in

business confidence, although there is continued

anxiety within the industry about reductions in public

construction work. Overall, nationally, the

expectations are that the turnover of the sector will

begin to rise. However, this is predicated on

continued investment in repair and maintenance in

the public housing sector. Whether this will

materialise will depend on the level and distribution

of public sector cuts from 2011 onwards.

Prospects for Manufacturing

Across Scotland, the gross value added (GVA) by

Scottish manufacturing has fallen since the first

quarter of 2008 by just over 6%. Although the Bank

of Scotland PMI index of business activity, published

in April 2010, suggested that manufacturing firms

were seeing a record rise in new orders, the latest

business survey conducted by the Scottish Chambers

of Commerce, published in early 2011, reported a

downward trend in business confidence by

manufacturing firms, fuelled by concerns about

inflationary cost pressures. However, it is noticeable

that productivity levels in Scotland in 2008 were

below those in the UK and placed her in the third

quartile of OECD countries, being 20% lower than the

USA. As a result, the advantage offered by the weak

Pound against both the Euro and the Dollar would

appear to be partly negated by any competitive

disadvantage and this goes some way to explain why

there has been no significant expansion of the volume

of manufactured exports in the last 12-18 months.

Prospects for Manufacturing (cont’d)

In South Ayrshire, the manufacturing sector continues

to contract. From providing 6800 jobs in 2006, this

has fallen to 4700 in late 2010. While it still accounts

for a sizeable component of total economic output

(18% of GVA in 2008), it is no longer the key driver of

growth in the local economy. Overall, the recession

simply seems to have accelerated the contraction of

the sector. .

Source: Doyle & Irving. ‘Continuing Impact of the Economic Recession on the South Ayrshire Economy’, June

2011

7 NOMIS

Pag

e19

P

age1

9

Table 4 (cont’d)

Prospects for the Retail & Catering Sector

About 15% of all employment in South Ayrshire is

accounted by shops and catering establishments.

How this sector copes with the impacts of the

recession in the next 2-3 years is critical to the local

economy. Recently, it has suffered from a drop in

consumer spending, leading to a rise in shop

vacancies in Ayr town centre. The first quarter of

2011 continued this trend, with like-for-like sales

down by 2.6% in the period January to March on a

year previously. Consumer confidence is likely to

remain weak, with customers continuing to be

worried about jobs, leading to the emergence of new,

lower spending patterns. As a result, Ernst & Young

are forecasting that jobs nationally in the retail sector

will be largely constant for the next 2-3 years.

However, the recession is not the only force at work

and the level of retail vacancy in South Ayrshire hints

at a longer term structural problem. Except for Troon

and Prestwick, which have a high proportion of small,

independent retailers, vacancy rates have increased

over the period 1999-2009 to 15-16%, significantly

above the UK average of 12% in the second quarter of

2009. The reasons for this include competition from

new retail centres at Silverburn and Braehead, the

diversification of out-of-town supermarkets into non-

food items, competition from internet sales and the

closure and consolidation of national chains, which

account for 7% of vacancies in Ayr. This raises issues

about what the future role of town will be in the

longer term.

Prospects for Tourism

Tourism provides about 13% of all employment in

South Ayrshire. Unlike the retail sector which is

focused on residents, tourism businesses look to

visitors. For that reason the forces shaping business

turnover and employment in this sector in the near

future are different. Across Scotland, the indications

are that the period January to September 2010 saw a

decline of about 4.6% in trips, of 9.6% in bed-nights

and of 9.0% in the average spend on the previous

year. Comparable information for South Ayrshire or

Ayrshire as a whole is currently not available for 2010.

The indication is that, despite favourable exchange

rates, after a slow start the number of overseas

visitors has remained flat, while domestic tourism has

been inhibited by depressed consumer confidence

and concerns about job losses. These challenging

conditions are expected to persist for the next 12-18

months.

Prospects for Financial and Business Services

Compared to Scotland as a whole, financial &

business services account for a very low proportion of

total employment in South Ayrshire; around 8%

compared to 19% nationally. As a result, while this

sector has taken a big knock nationally from the

recession, with around 16000 jobs lost in Scotland

between 2007 and 2010, the impact on employment

locally has been insignificant. In fact employment in

South Ayrshire in this sector has increased by 500

during the period 2006-2010.

Source: Doyle & Irving. ‘Continuing Impact of the Economic Recession on the South Ayrshire Economy’, June

2011

Pag

e20

P

age2

0

Table 4 (cont’d)

Prospects for Transport & Communication Services

Firms in the transport and communications sector in

South Ayrshire have shown strong long-term growth

and greater resilience in the face of the economic

recession than other businesses Between 1998 and

2008, employment in these industries locally grew by

57% or 1300 jobs. Even recently, there is some

evidence that the sector has been less vulnerable to

the economic downturn, with the number of jobs

rising slightly between 2008 and 2010 by 14% or 400

in South Ayrshire. Much of this employment is linked

with the aerospace industry centred on Prestwick

airport. However, this sector has not entirely escaped

the effects of the recession. Both passenger numbers

and freight volumes at Prestwick Airport have fallen

in recent years.

Prospects for the Public Sector

The public sector, including education and health

accounted for 33% of all jobs locally in the third

quarter of 2010, so what happens to public sector

budgets is likely to have significant implications for

the local economy. Contrary to the view often

expressed, there has already been contraction in job

numbers in the public sector within South Ayrshire

since 2006 of about 8%, though the numbers

employed in this sector locally are still 2% higher than

they were in 2000. However, it is the prospect of

large cuts in the public sector budget for Scotland

that raises the spectre of significant job losses in this

sector over the next 2-3 years.

It has been estimated that the local authorities are

likely to experience cuts of 14-16% between 2010-11

and 2014-15. This could translate into job cuts in

South Ayrshire Council alone during this period

equivalent to 800 full-time posts. Although enjoying

some budget protection, NHS Ayrshire & Arran,

another major employer, is also expected to cut staff

numbers in the period up to 2014-15.

Source: Doyle & Irving. ‘Continuing Impact of the Economic Recession on the South Ayrshire Economy’, June

2011.

Prospects for Different Communities

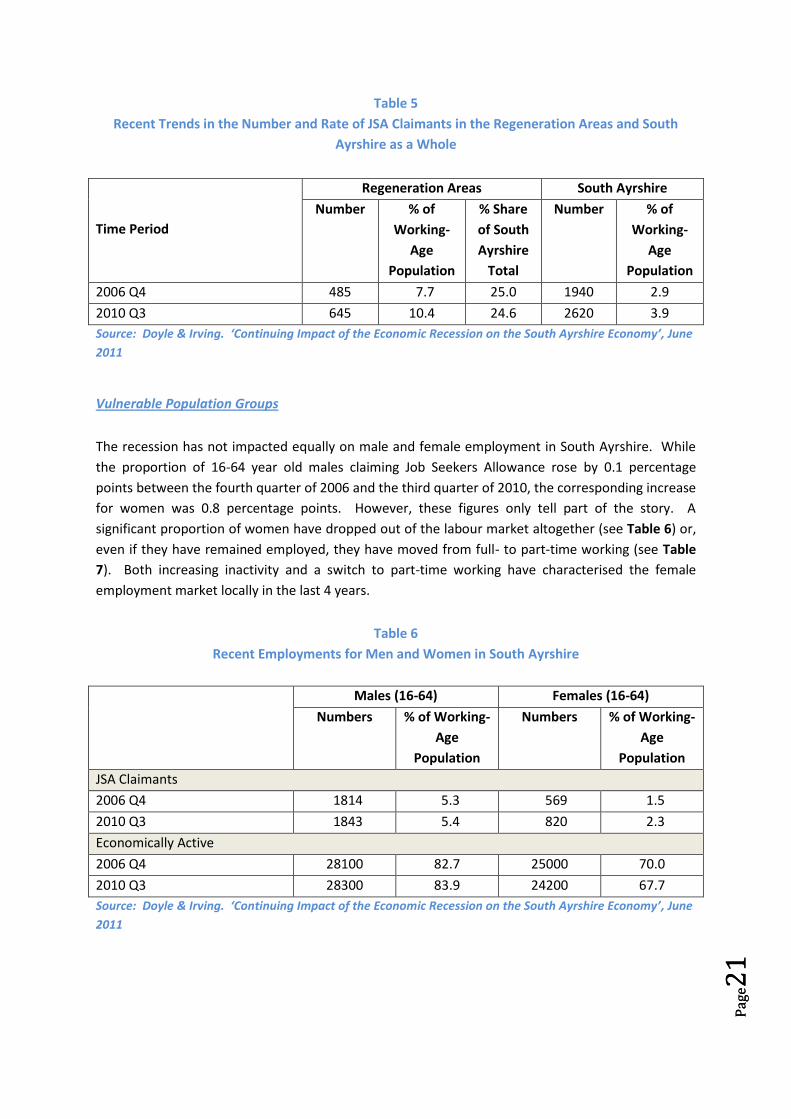

Employment Black-spots

Almost 25% of all those claiming Job Seekers Allowance (JSA) in the third quarter of 2010 were

resident in the Regeneration Areas of South Ayrshire, despite the areas only accounting for 9% of the

resident working-age population. Among 16-24 year olds the situation was more acute, with nearly

18% in this age group within these communities claiming JSA, compared 7% in South Ayrshire as

whole. However, while the gap between these areas and the rest of South Ayrshire in terms of the

percentages claiming JSA has widening in recent years, in terms of the Regeneration Area’s share of

the overall JSA claimants for both the 16-64 (see Table 5) and 16-24 age groups, this appears to be

unchanged.

Pag

e21

P

age2

1

Table 5

Recent Trends in the Number and Rate of JSA Claimants in the Regeneration Areas and South

Ayrshire as a Whole

Time Period

Regeneration Areas South Ayrshire

Number % of

Working-

Age

Population

% Share

of South

Ayrshire

Total

Number % of

Working-

Age

Population

2006 Q4 485 7.7 25.0 1940 2.9

2010 Q3 645 10.4 24.6 2620 3.9

Source: Doyle & Irving. ‘Continuing Impact of the Economic Recession on the South Ayrshire Economy’, June

2011

Vulnerable Population Groups

The recession has not impacted equally on male and female employment in South Ayrshire. While

the proportion of 16-64 year old males claiming Job Seekers Allowance rose by 0.1 percentage

points between the fourth quarter of 2006 and the third quarter of 2010, the corresponding increase

for women was 0.8 percentage points. However, these figures only tell part of the story. A

significant proportion of women have dropped out of the labour market altogether (see Table 6) or,

even if they have remained employed, they have moved from full- to part-time working (see Table

7). Both increasing inactivity and a switch to part-time working have characterised the female

employment market locally in the last 4 years.

Table 6

Recent Employments for Men and Women in South Ayrshire

Males (16-64) Females (16-64)

Numbers % of Working-

Age

Population

Numbers % of Working-

Age

Population

JSA Claimants

2006 Q4 1814 5.3 569 1.5

2010 Q3 1843 5.4 820 2.3

Economically Active

2006 Q4 28100 82.7 25000 70.0

2010 Q3 28300 83.9 24200 67.7

Source: Doyle & Irving. ‘Continuing Impact of the Economic Recession on the South Ayrshire Economy’, June

2011

Pag

e22

P

age2

2

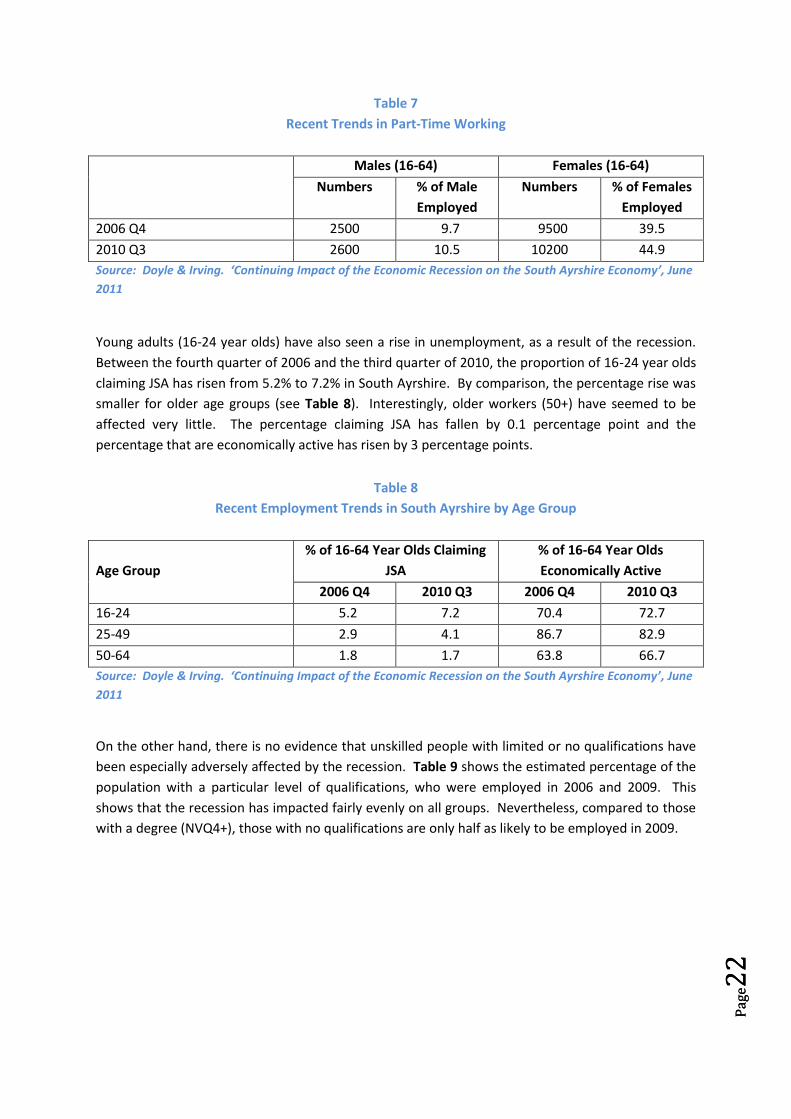

Table 7

Recent Trends in Part-Time Working

Males (16-64) Females (16-64)

Numbers % of Male

Employed

Numbers % of Females

Employed

2006 Q4 2500 9.7 9500 39.5

2010 Q3 2600 10.5 10200 44.9

Source: Doyle & Irving. ‘Continuing Impact of the Economic Recession on the South Ayrshire Economy’, June

2011

Young adults (16-24 year olds) have also seen a rise in unemployment, as a result of the recession.

Between the fourth quarter of 2006 and the third quarter of 2010, the proportion of 16-24 year olds

claiming JSA has risen from 5.2% to 7.2% in South Ayrshire. By comparison, the percentage rise was

smaller for older age groups (see Table 8). Interestingly, older workers (50+) have seemed to be

affected very little. The percentage claiming JSA has fallen by 0.1 percentage point and the

percentage that are economically active has risen by 3 percentage points.

Table 8

Recent Employment Trends in South Ayrshire by Age Group

Age Group

% of 16-64 Year Olds Claiming

JSA

% of 16-64 Year Olds

Economically Active

2006 Q4 2010 Q3 2006 Q4 2010 Q3

16-24 5.2 7.2 70.4 72.7

25-49 2.9 4.1 86.7 82.9

50-64 1.8 1.7 63.8 66.7

Source: Doyle & Irving. ‘Continuing Impact of the Economic Recession on the South Ayrshire Economy’, June

2011

On the other hand, there is no evidence that unskilled people with limited or no qualifications have

been especially adversely affected by the recession. Table 9 shows the estimated percentage of the

population with a particular level of qualifications, who were employed in 2006 and 2009. This

shows that the recession has impacted fairly evenly on all groups. Nevertheless, compared to those

with a degree (NVQ4+), those with no qualifications are only half as likely to be employed in 2009.

Pag

e23

P

age2

3

Table 9

Recent Employment Trends in South Ayrshire by Level of Qualification

Qualification Level % of Age Group in

Employment in 2006

% of Age Group in

Employment in 2009

NVQ4+ (degree) 87.2 81.6

NVQ3 81.7 74.3

NVQ2 68.9 71.3

NVQ1 (Standard Grades) 65.8 60.8

No Qualifications 51.1 44.5

Source: Doyle & Irving. ‘Continuing Impact of the Economic Recession on the South Ayrshire Economy’, June

2011

From this analysis it is clear that the recession has not impacted evenly on all communities

within the Local Authority. Young people (16-24 years of age) and women have been more

adversely affected than men and older people (50+). On the other hand, there is less

evidence that more deprived communities or lower skill groups have been affected

disproportionately.

The Longer-Term Growth Prospects for the South Ayrshire Economy

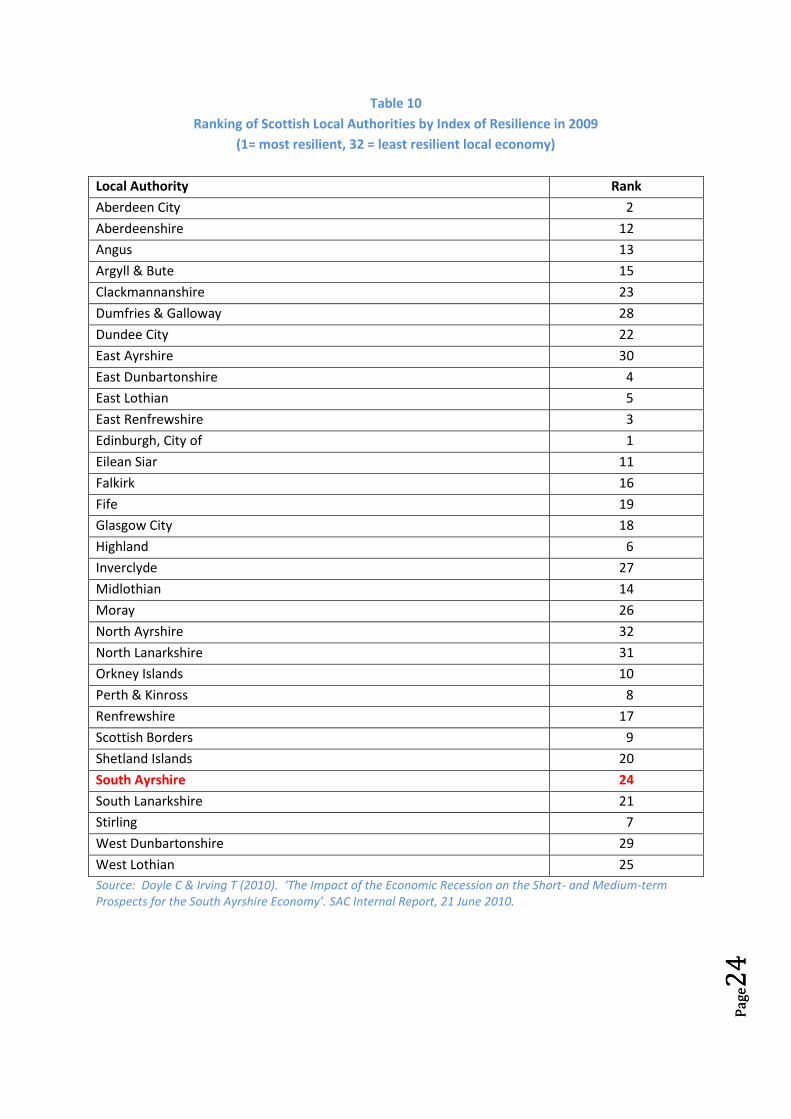

The Resilience of the Local Economy

In focussing on the short-term economic prospects and the effects of the recession, there is a danger

that attention is diverted from the underlying strengths and weaknesses of the economy, which are

central to determining the shape of any economic strategy. In particular, an analysis of the

‘resilience’ of the local economy carried out in June 2010 tended to confirm the impression that the

recession was revealing ‘hidden’ structural problems within the South Ayrshire economy8. As shown

in Table 10, using an index of ‘resilience’, in 2009 South Ayrshire appeared to be very nearly in the

bottom quartile of local authority economies in Scotland in terms of its ability to recover from the

impacts of the recession. It was perceived as being weak in terms of:

its dependence on a limited number of key growth sectors;

the skill base of its workforce;

the level of new business creation; and

the level of population and income growth.

8 Doyle C & Irving T (2010). The Impact of the Economic Recession on the Short- and Medium-term Prospects

for the South Ayrshire Economy. Sac Internal Report, 21 June 2010.

Pag

e24

P

age2

4

Table 10

Ranking of Scottish Local Authorities by Index of Resilience in 2009

(1= most resilient, 32 = least resilient local economy)

Local Authority Rank

Aberdeen City 2

Aberdeenshire 12

Angus 13

Argyll & Bute 15

Clackmannanshire 23

Dumfries & Galloway 28

Dundee City 22

East Ayrshire 30

East Dunbartonshire 4

East Lothian 5

East Renfrewshire 3

Edinburgh, City of 1

Eilean Siar 11

Falkirk 16

Fife 19

Glasgow City 18

Highland 6

Inverclyde 27

Midlothian 14

Moray 26

North Ayrshire 32

North Lanarkshire 31

Orkney Islands 10

Perth & Kinross 8

Renfrewshire 17

Scottish Borders 9

Shetland Islands 20

South Ayrshire 24

South Lanarkshire 21

Stirling 7

West Dunbartonshire 29

West Lothian 25

Source: Doyle C & Irving T (2010). ‘The Impact of the Economic Recession on the Short- and Medium-term Prospects for the South Ayrshire Economy’. SAC Internal Report, 21 June 2010.

Pag

e25

P

age2

5

More disturbingly, South Ayrshire had dropped 7 places in its ranking for economic resilience since

2001, suggesting that it had become less resilient in the last decade. The overall inference was that

the area needed to:

diversify its employment base;

increase the skills level of the local workforce;

stimulate new business creation and help existing small businesses to grow; and

make the area more attractive for people to move in and businesses to set up.

These issues are explored in more detail below.

Diversifying the Employment Base

Of the 47000 jobs in South Ayrshire, 33% are in the public sector, 15% in the retail trade and 13%

tourism. Together these three sectors provide over 60% of local jobs. The public sector is facing

potential job losses as a result of budget cuts, while both retail and tourism businesses are facing

challenging times as a result of a loss of consumer confidence. In the light of this, diversifying the

economic base would seem strategically important to the long-term vitality of the local economy.

Scottish Enterprise has identified six key growth sectors, namely i) creative industries, ii) energy, iii)

financial & business services, iv) life sciences, v) tourism and vi) food & drink. Using the definitions

of these industries, based on the SIC 2003 industrial classification used by Scottish Enterprise, earlier

this year an estimate was made of the numbers of firms and numbers of people employed in these

industries9. Figure 12 shows the estimated number of businesses locally in each of these key

sectors, together with the number that would be expected, if South Ayrshire’s share was

commensurate with its overall share of businesses in Scotland. Figure 13 shows the same

information, but this time for employment. In terms of the numbers of businesses, South Ayrshire

probably has its fair share of key sector businesses, but in terms of employment, except for tourism,

its share is significantly lower than expected. This reflects the fact that the majority of businesses in

the key sectors in South Ayrshire are small. As a result, while 31% of employment nationally is in

these 6 key growth sectors, in South Ayrshire the proportion is only 22%. Another measure of the

‘dynamism’ of the local economy is provided by employment in the so-called ‘knowledge-based

industries’ (KBIs). In 2007 44% of both public and private employment in Scotland was in KBIs, but

only 39% in South Ayrshire10.

9 Doyle C & Irving T (2011). Continuing Impact of the Economic Recession on the South Ayrshire Economy, SAC

Internal Report, 2 June 2011. 10 Doyle C & Irving T (2011). Continuing Impact of the Economic Recession on the South Ayrshire Economy, SAC

Internal Report, 2 June 2011.

Pag

e26

P

age2

6

Figure 12

Number of Firms in South Ayrshire in the Six Key Growth Sectors and the Expected Numbers in

South Ayrshire

050

100150200250300350400450

Nu

mb

er

of

Bu

sin

ess

Creativ

e

Energy

Financia

l & B

usiness

Life Sc

ience

s

Tourism

Food &

drin

k

Actual

Expected

Source: Doyle & Irving. ‘Continuing Impact of the Economic Recession on the South Ayrshire Economy’, June

2011

Figure 13

Number of People Actually Employed in South Ayrshire in the Six Key Growth Sectors and the

Expected Numbers in South Ayrshire

0

1000

2000

3000

4000

5000

6000

7000

Nu

mb

er

of

Bu

sin

ess

Creativ

e

Energy

Financia

l & B

usiness

Life Sc

ience

s

Tourism

Food &

drin

k

Actual

Expected

Source: Doyle & Irving. ‘Continuing Impact of the Economic Recession on the South Ayrshire Economy’, June

2011

Pag

e27

P

age2

7

Increasing the Skills Level of the Local Workforce

The Leitch Review in 2006 stated clearly that skills were a key driver of economic success and that

20% of the observed international differences in labour productivity was attributable to differences

in skill levels, with Scotland and the UK faring badly in international league tables11. However, these

observations are not the same as saying that there is an ever growing demand for degree-level staff.

In 2007 Oxford Economics made some forecasts of the demand in South Ayrshire for labour in the

period 2007-2017 by qualifications12. Of the 33,000 job openings anticipated over this 10-year

period, it expected that 8000 would be for graduates, 6000 would be for those with Highers, HNCs

and HNDs and a further 14000 would be for those with Standard Grades13. As Figure 14 shows,

relative to the numbers of people of working age with different qualifications in South Ayrshire, the

future shortages are not so much for degree-level staff, but for people with intermediate

qualifications. Thus, it is expected that 8000 staff with degree-level qualifications will be required,

compared to 21700 residents with degrees (NVQ4+). Comparable figures are provided for NVQs 1, 2

and 3 and for those with no qualifications. From this, it is possible to see that future labour demand

is greatest relative to the pool of those with sub-degree qualifications (NVQs 1-3). While the onset

of the recession may have reduced the job openings in the immediate future, it is unlikely to have

altered the pattern of demand by qualification level.

Figure 14

Estimated Demand for Labour by Level of Qualification between 2007 and 2017 in South Ayrshire

Relative to the Pool of Working-Age People Qualified to Given Levels

0

5000

10000

15000

20000

25000

Nu

mb

ers

No Qual

ifica

tions

NVQ1 & 2

NVQ3

NVQ4+

Anticipated DemandBetween 2007 and 2017

Working-AgePopulation

Source: Doyle & Irving. ‘Continuing Impact of the Economic Recession on the South Ayrshire Economy’, June

2011

11

HM Treasury (2006). Leitch Review of Skills: Prosperity for All in the Global Economy – World Class Skills. 12

SLIMS (2007). South Ayrshire 2007 Labour Market Statement 13

These figures are not based so much on an expansion of the total number of jobs available in South Ayrshire, but anticipated staff turnover, including retirements.

Pag

e28

P

age2

8

Stimulating New Business Creation and Helping Existing Businesses to Grew

While new business development has generally been shown to have a positive impact on economic

development, in Scotland the evidence suggests that stimulating new firm creation does not

increase sectoral employment14. The reason for this is that new firm creation both increases and

destroys jobs. The immediate impact of a new firm is to create new jobs, but in the longer term,

whether this increase is sustained depends on whether the new firm displaces existing firms or,

through increased competition, improves the performance of all firms locally in that sector. In

Scotland, and other areas characterised by comparatively low rates of business formation and low

entrepreneurial activity, the evidence is that the displacement effect predominates, resulting in no

long-term increase in employment. In the case of South Ayrshire, as noted earlier, the growth in the

number of businesses in recent years has trailed behind the Scottish average, suggesting that it is

likely that the contribution of new business growth to overall employment locally has been

negligible, as it has been for Scotland as whole.

Moreover, there is inherently no good reason to link new business formation to job creation. For

there to be real and significant employment benefits, the new businesses need to grow. Typically,

new businesses are one-person enterprises, so that the addition of 210 businesses to the total stock

of firms in South Ayrshire between 2004 and 2009 can only be expected to have increased job

opportunities by a maximum of 210, unless the new businesses grow fast. In reality more than 55%

of the new businesses created in South Ayrshire in 2004 had ceased to exist by 200915. This indicates

that far from growing many new businesses will quickly die. Real growth is achieved by getting a

new company to expand and in doing so take on more labour. The focus needs to be on the ‘quality’

of businesses created and not the number.

Making the Area More Attractive to People and Businesses

Trying to stimulate the local economy through creating new jobs is only one possible strategy. An

alternative that has attracted attention is the idea of consumer-led growth. In this case, rather than

focusing on jobs, the focus is on increasing the spending power in the local economy through

increasing the supply of housing and attracting more people to live in the area. Even if the in-

migrants continue to commute to other areas to work, the hope is that they will spend their money

locally and so indirectly boost local employment.

However, such a strategy would require a reversal of current trends. Between 2001 and 2009, the

population of South Ayrshire fell by 0.7%. The reason for this is that net in-migration to the local

14

Fritsch M & Mueller M (2005). How persistent are regional start-up rates? An empirical analysis. The Emergence of Entrepreneurial Economics: Research on Technological Innovation, Management and Policy, 9, 71-82; Helmers C and Rogers M (2007). Innovation and the survival of new firms across British regions. Discussion Paper, University of Oxford.; Lee S, Florida D and Arcs Z (2004. Creativity and entrepreneurship: A regional analysis of new firm formation. Regional Studies, 38, 879-971; Mueller P, van Stel A and Storey S (2008). The effects of new firm formation on regional development over time: The case of Great Britain. Small Business Economics, 30, 59-71 15

Office of National Statistics (2010). Business Demography 2009.

Pag

e29

P

age2

9

authority was only just over 350 per year in the period 2001-02 to 2008-0916. This was insufficient to

compensate for the natural fall in population, through declining births and rising deaths, which led

to an average annual decline in population of 410 per year in the same period. To achieve

population growth, average annual net in-migration would need to rise by about 18%. Even then, a

growth in the size of the local population would not necessarily guarantee that consumer spending

locally would rise proportionately. Residents may choose to spend some of their income outside the

area. A household shopping survey conducted in 2003 for example showed that over 20% of items

liking clothing and furniture by Ayrshire residents were made In Glasgow17. All this suggests that it

may be difficult in practice to engineer locally consumer-led economic growth, based around

increasing the local population.

16

General Register Office for Scotland 17

Doyle C & Clark E (2005). Implications of City Region Growth Models for South Ayrshire: A Re-Analysis. SAC Internal Paper, November 2005.

Pag

e30

P

age3

0

CHAPTER 2: FUTURE OPPORTUNITIES FOR THE SOUTH AYRSHIRE ECONOMY

Fundamental Issues

The preceding analysis suggests that the economy of South Ayrshire is stagnating. Between 2007

and 2010, there has been a dramatic (8%) fall in the number of jobs available locally. Increasingly,

the working population must find work in neighbouring areas, with nearly a third of all residents

employed in South Ayrshire commuting to other areas for employment in 2008. As a result, the area

is gradually becoming part of the ‘commuter zone’ for Greater Glasgow. More worryingly,

assessments of the resilience of the local economy are not promising, suggesting that the area may

not be able to cope very well with the challenges posed by prolonged economic recession. As a

consequence, although average household incomes in South Ayrshire remain above the national

average18, there are worrying signs that the incidence of poverty and worklessness is increasing over

time. Thus, even though the rates of poverty and worklessness are still lower than in the

neighbouring areas of North and East Ayrshire19, the widely held view that social and economic

problems in South Ayrshire are of a different order from those in neighbouring areas looks

increasingly suspect. For this reason the future of the South Ayrshire economy is likely to be bound

up with that of Ayrshire as a whole.

Against this background, this chapter explores 3 questions:

What are the main drivers of the local economy?

What are the opportunities for the future and how well placed is the local economy to take

up these opportunities?

Are all communities and areas with South Ayrshire equally well placed to avail themselves of

potential future opportunities?

Key Economic Drivers and Future Opportunities

In 2006, an attempt was made to estimate where the comparative advantage of the South Ayrshire

economy lay in terms of identifying those industrial sectors20:

which were net exporters, exporting a significant volume of goods and services to markets

outside of Ayrshire;

whose growth was likely to have a significant direct impact on the rest of the local economy

through purchases of raw materials, goods and services; and

that were dynamic and had the potential to grow, as reflected in above average gross

margins and their apparent comparative advantage.

18

SLIMSconsulting (2011). Towards a Wealthier & Fairer South Ayrshire, June 2011. 19

Scottish Neighbourhood Statistics 20

Doyle C & Clark E (2006). Growing the Ayrshire Economy: A ‘Polycentric’ Model of Economic Development. SAC Internal Report, March 2006.

Pag

e31

P

age3

1

This revealed that the industries that appeared to be the local economic drivers were:

the transport and equipment sector connected with Prestwick airport and the associated

aerospace complex;

the public sector, which is the area’s major employer;

the food processing sector; and

business support services (advertising, market research, tax consultancy and accountancy).

The significant omission in this list is tourism, which for much of the last decade has shown limited

growth. Nevertheless, this sector continues to attract attention as an industry, which has the

potential to grow21. At the same time, the development of the aerospace complex at Prestwick

Airport has grown out of the area’s engineering tradition. The engineering industry still accounts for

nearly 8% of the area’s economic output and so it may be a possible future economic driver. The

opportunities for expansion afforded by each of industrial sectors are examined below.

Engineering: An Industry in Decline or Transition?

There are just under 70 engineering businesses in South Ayrshire, employing 3390 in 200922. A

decade earlier, the sector employed 6000 people23. A very large part of these jobs (75%) are

connected with the aerospace sector (see Table 11), which saw a 6% growth in jobs in the last

decade24. Outside the aerospace industry, the majority of engineering firms are small, employing

around 20 people, and largely centred on the production and basic processing of metals. These

firms in this traditional engineering sector are vulnerable to global competition from low-cost

producers in Asia and the Far East, so that the future does not look bright for firms outside the

aerospace industry. Even in the case of the aerospace industry, there is a question mark over its

future. Firms congregated in the area attracted by the development of Prestwick Airport. In recent

years, both passenger numbers and freight volumes at Prestwick Airport have fallen. In 2010,

passenger numbers and freight volumes were both down by 9% on the previous year and much

more on 2008. A lot of this decline is only indirectly linked to the recession and is primarily driven

by the decision of airline operators, like Ryanair, to move activities elsewhere25. However, the

aerospace complex now seems sufficiently established that, in a recent survey, the majority of

businesses said that they would not re-locate away from Ayrshire, even if Glasgow Prestwick ceased

operating passenger and freight traffic26. Furthermore, training in the skills needed by the local

industry will be strengthened with the launch of a degree in aircraft engineering by the University of

21

See Report by the Chair of the Economic Development Partnership to the Community Planning Board of the South Ayrshire CPP on 23

rd February 2011.

22 Definition of engineering based on the classification employed by the Sector Skills Council for Science,

Engineering and Manufacturing Technologies. 23

Annual estimates of employment and output by manufacturing industries provided by the Office of National Statistics for Scottish Local Authorities. 24

Doyle C (2011). Engineering in Ayrshire: An Industry in Decline or Transition? SAC Internal Report, 9 August 2011. 25

Doyle C & Irving T (2011). Continuing Impact of the Economic Recession on the South Ayrshire Economy. Sac Internal Report, 2 June 2011. 26

SQWconsulting (2008). Economic Impact of Glasgow Prestwick Airport. Final Report to Glasgow Prestwick Airport, South Ayrshire Council and Scottish Enterprise, February 2008.

Pag

e32

P

age3

2

the West of Scotland at Ayr. Perhaps the one downside of the industry is the fact that locally the

industry has weak linkages with the rest of the economy, with very little of the inputs being

purchased locally27, so that the impact of the industry’s growth on the rest of the local economy is

limited.

Table 11

Estimated Employment in Engineering in South Ayrshire by Industrial Grouping in 2009

Industrial Grouping Employment Industrial Grouping Employment

Basic metals and metal

products (including wholesale

metals and scrap)

575 Electronics 125

Mechanical Equipment 46 Automotive 6

Electrical Equipment 2 Science and engineering R&D 5

Marine & aerospace 2625 Manufacture of medical and

surgical equipment and

orthopaedic appliances

6

Total 3390

Source: Doyle C ( 2011). Engineering in Ayrshire: An Industry in Decline or Transition? SAC Internal Report

9 August 2011

Given the area’s engineering base, there has been speculation about the potential to develop a new

economic base, built around renewables and the provision of low carbon goods and services28.

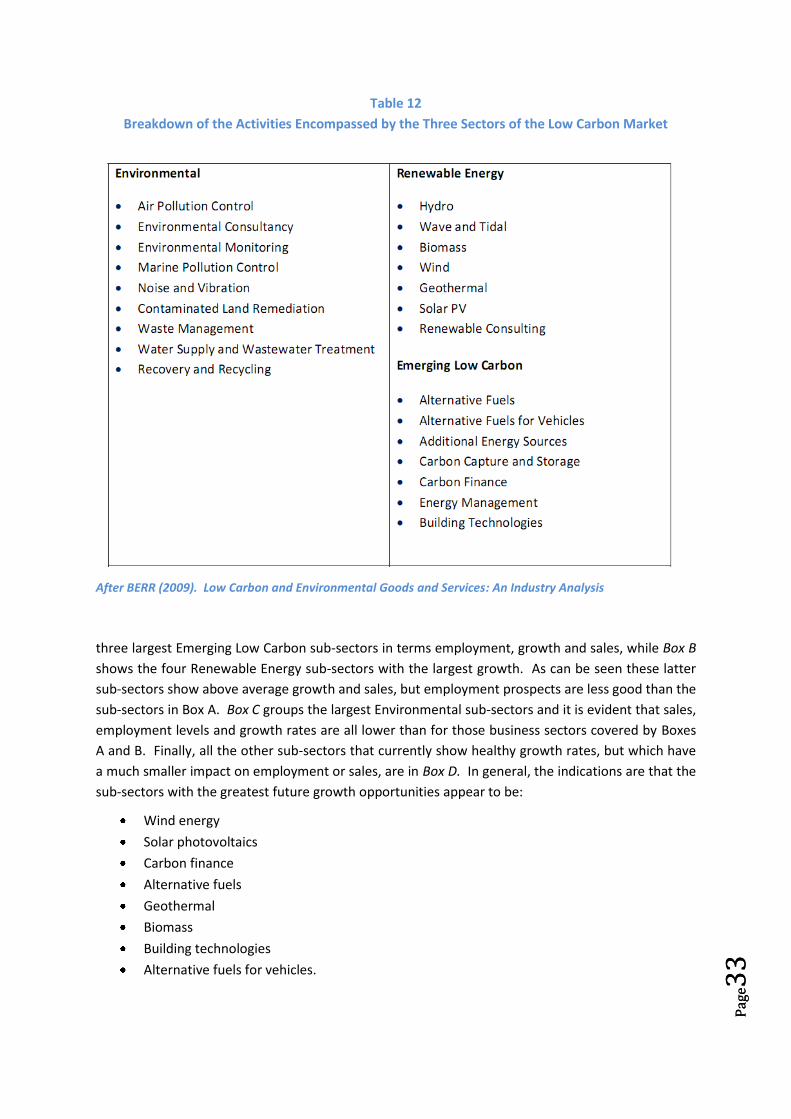

However, a ‘low carbon’ sector is about more than just engineering services. A recent report by the

Department for Business, Enterprise & Regulatory Reform (BERR) distinguishes three different

market segments29. First, there are the more traditional Environmental services, including activities

like waste management and recycling. Then there is a range of rapidly growing Renewable Energy

technologies, connected with hydro, wave and tidal power, geothermal energy generation and

power from wind and biomass. Lastly, there are a number of Emerging Low Carbon activities, such

as reduced emissions from within the transport and construction sectors, nuclear energy, energy

management and carbon capture and storage. A summary of the kinds of activities subsumed under

each market segment is presented in Table 12.

In terms of future opportunities, the BERR report assessed that the areas with the largest market

opportunities within the UK, reflected by sales growth, were in the Renewable Energy and Emerging

Low Carbon market segments rather than Environmental services. This can be seen in Figure 15.

Employment is shown on the horizontal axis, current (2007) growth on the vertical axis and market

value by the bubble size. Only the largest sectors by market size are labelled. Box A shows the

27

Doyle C & Clark E (2006). Growing the Ayrshire Economy: A ‘Polycentric’ Model of Economic Development. SAC Internal Report, March 2006. 28

Doyle C, Jarvie L & Irving T (2011). Implications of the Pursuit of a Low Carbon Economy for South Ayrshire. SAC Internal Report, March 2011 29

BERR (2009). Low Carbon and Environmental Goods and Services: An Industry Analysis. March 2009.

Pag

e33

P

age3

3

Table 12

Breakdown of the Activities Encompassed by the Three Sectors of the Low Carbon Market

After BERR (2009). Low Carbon and Environmental Goods and Services: An Industry Analysis

three largest Emerging Low Carbon sub-sectors in terms employment, growth and sales, while Box B

shows the four Renewable Energy sub-sectors with the largest growth. As can be seen these latter

sub-sectors show above average growth and sales, but employment prospects are less good than the

sub-sectors in Box A. Box C groups the largest Environmental sub-sectors and it is evident that sales,

employment levels and growth rates are all lower than for those business sectors covered by Boxes

A and B. Finally, all the other sub-sectors that currently show healthy growth rates, but which have

a much smaller impact on employment or sales, are in Box D. In general, the indications are that the

sub-sectors with the greatest future growth opportunities appear to be:

Wind energy

Solar photovoltaics

Carbon finance

Alternative fuels

Geothermal

Biomass

Building technologies

Alternative fuels for vehicles.

Pag

e34

P

age3

4

Figure 15

Sub-Sectors with the Greatest Future Opportunity for Growth

After BERR (2009). Low Carbon and Environmental Goods and Services: An Industry Analysis

In the case of Scotland, the most important market segments are connected with i) alternative fuels

and building technologies, ii) wind and geothermal energy generation, iii) carbon recovery &

recycling and iv) water & waste management. This can be seen from Figure 16, which provides a

breakdown of the sales, employment and growth of the Scottish low carbon sector in 2007/08. As in

Figure 15, sales are indicated by the size of the bubbles, growth rates are on the vertical axis and

employment is represented on the horizontal axis.

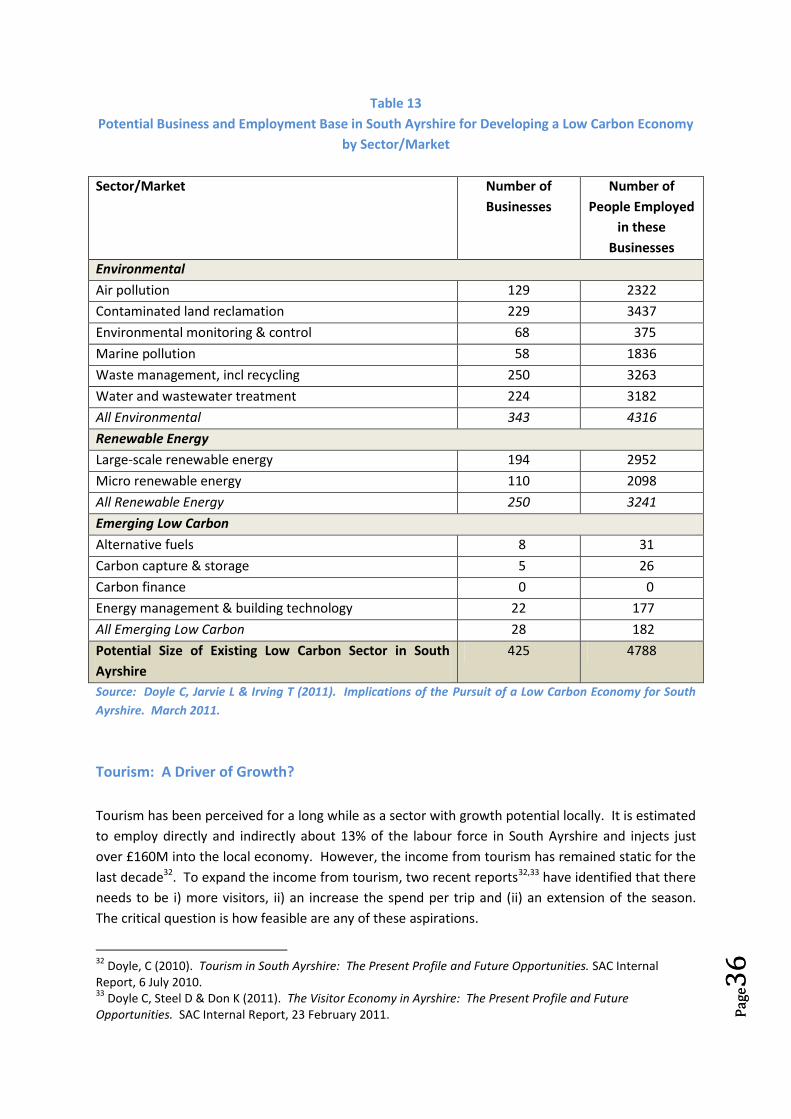

The number of businesses in South Ayrshire with the theoretical potential to expand into the

production of low carbon good and services has been put about 420 (see Table 13). Together these

companies employ around 4800 people. However, the gap between the potential and the reality is

illustrated by a detailed examination of the Yellow Pages and Thompson’s directories. Coupled with

web searches, this has revealed only a handful of Ayrshire businesses have any involvement in the

supply of low carbon goods and services. The significance of this is that, for a business sector

centred on the low carbon sector to evolve, there needs to be a core of ‘innovators’, who attract

other similar businesses to the local area. At the moment in South Ayrshire, it is very debatable

whether this exists. Moreover, some experts have questioned whether Scotland as a whole has

been fast enough in developing a low carbon economy. Germany’s early investment in renewable

energy is thought to have led it to capture a significant proportion of the global renewable energy

market30. This ‘first mover’ advantage could be difficult to compete with. Some experts have also

questioned the Scottish Government’s view that the low carbon economy is the key to future

30

UNEP (2007). Green Jobs: Sustainable Work in a Low-Carbon World.

Pag

e35

P

age3

5

economic growth, contending that, far from creating jobs, the renewable sector will destroy jobs by

displacing potential growth elsewhere. Thus, Verso Economics has suggested that for every job

created in the renewable sector in Scotland, 1.1 jobs will be lost31, largely because it would divert

investment away from other potential areas of growth. All this underlines that translating the

potential opportunities for developing a low carbon sector locally, centred on its existing expertise in

engineering, will require a focussed and concerted effort, as well as a high degree of commitment

from local businesses.

Figure 16

Sales, Employment and Growth in the Low Carbon Sector in Scotland

After BERR (2009). Low Carbon and Environmental Goods and Services: An Industry Analysis

31

Verso Economics (2011). Worth the Candle? See http://politics.caledonianmercury.com/2011/02/28/new-report-casts-doubt-on-scotland%E2%80%99s-role-as-the-%E2%80%98saudi-arabia-of-renewables%E2%80%99/#

Pag

e36

P

age3

6

Table 13

Potential Business and Employment Base in South Ayrshire for Developing a Low Carbon Economy

by Sector/Market

Sector/Market Number of

Businesses

Number of

People Employed

in these

Businesses

Environmental

Air pollution 129 2322

Contaminated land reclamation 229 3437

Environmental monitoring & control 68 375

Marine pollution 58 1836

Waste management, incl recycling 250 3263

Water and wastewater treatment 224 3182

All Environmental 343 4316

Renewable Energy

Large-scale renewable energy 194 2952

Micro renewable energy 110 2098

All Renewable Energy 250 3241

Emerging Low Carbon

Alternative fuels 8 31

Carbon capture & storage 5 26

Carbon finance 0 0

Energy management & building technology 22 177

All Emerging Low Carbon 28 182

Potential Size of Existing Low Carbon Sector in South

Ayrshire

425 4788

Source: Doyle C, Jarvie L & Irving T (2011). Implications of the Pursuit of a Low Carbon Economy for South

Ayrshire. March 2011.

Tourism: A Driver of Growth?

Tourism has been perceived for a long while as a sector with growth potential locally. It is estimated

to employ directly and indirectly about 13% of the labour force in South Ayrshire and injects just

over £160M into the local economy. However, the income from tourism has remained static for the

last decade32. To expand the income from tourism, two recent reports32,33 have identified that there

needs to be i) more visitors, ii) an increase the spend per trip and (ii) an extension of the season.

The critical question is how feasible are any of these aspirations.

32

Doyle, C (2010). Tourism in South Ayrshire: The Present Profile and Future Opportunities. SAC Internal Report, 6 July 2010. 33

Doyle C, Steel D & Don K (2011). The Visitor Economy in Ayrshire: The Present Profile and Future Opportunities. SAC Internal Report, 23 February 2011.

Pag

e37

P

age3

7

In 2009, South Ayrshire received just over 1.4M visitors and 3.1M tourist days. Nearly half the

visitors were day trippers. This underlines a problem that South Ayrshire does not have a strong

image as a tourism destination and what image that it has is of a traditional holiday area for those

living in Glasgow. With the development of the overseas holiday market in the 1970s, its market has

contracted and it has not managed to move on successfully. Despite efforts to rebrand and promote

the area as a tourism destination in the last decade, the position is essentially unchanged. In 2000,

between January and September, South Ayrshire attracted 1.29M tourists of which 0.77M were day

visitors; for the comparable period in 2009, 1.18M tourists, of which 0.66M were day visitors, visited

the area. To reverse the slide in visitor numbers, the area needs to identify what its comparative

advantage is in terms of tourism and the type of tourists that it is seeking to attract. In this regards

VisitScotland’s Ayrshire & Arran Visitor Survey for 2008-09 provides pointers, indicating that visitors

associate the area with Burns, golf, horse-racing and the sea. Table 14 shows the opportunities and

challenges connected with each of these. Essentially, this shows that it is unlikely that any one

activity or initiative will provide the basis for growth. Instead attracting more tourists will depend on

increasing the diversity of ‘experiences’ to be had and the development of ‘niche’ products. The

resultant growth in visitor numbers will be gradual.

Increasing the spend per trip will also be an important part of any tourism strategy. In 2009, the

average spend per day visitor to South Ayrshire was £28, while the average tourist, staying overnight

in the area, spent £42 per night34. The latter figure is markedly lower than the Scottish average for

tourists of £64 per night. This may be due to there being fewer high cost activities available within