Embed Size (px)

Citation preview

THE STATE OF GLOBAL PET FOOD:TRENDS AND GROWTH OPPORTUNITIES

JARED KOERTEN

SENIOR ANALYST

PFAC, OTTAWA, NOVEMBER 5, 2015

GLOBAL OVERVIEWDEVELOPED REGIONS

EMERGING REGIONS

THE FUTURE

© Euromonitor International

4

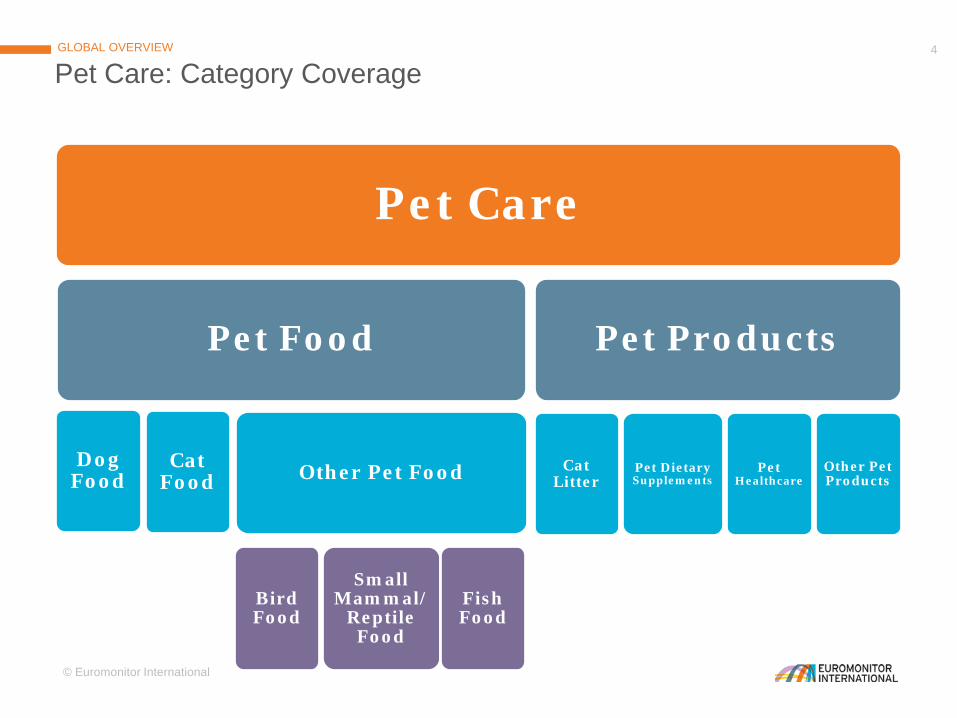

Pet Care: Category CoverageGLOBAL OVERVIEW

Pet Care

Pet Food

Dog Food

Cat Food Other Pet Food

Bird Food

Small Mammal/

Reptile Food

Fish Food

Pet Products

Cat Litter

Pet Dietary Supplements

Pet Healthcare

Other Pet Products

© Euromonitor International

5

Dog and Cat Food: Type and Price PlatformGLOBAL OVERVIEW

Pet Food by Type

Dog Food

Dry

Wet

Treats

Cat Food

Dry

Wet

Treats

Dog Food by Price Platform

Economy

Mid-Priced

Premium

Cat Food by Price Platform

Economy

Mid-Priced

Premium

© Euromonitor International

6

Global Pet CareGLOBAL OVERVIEW

US$ 105bnPet Care Sales in 2015

5%CAGRBetween 2010-2015

US$23BnIncremental Growth Last 5 years

© Euromonitor International

7

$0

$20

$40

$60

$80

$100

$120

2010 2011 2012 2013 2014 2015 (p)

Sale

s (U

S$, b

n, F

ixed

E-R

)

Global Spending on Pet Care: 2010-2015

Pet Products

Pet Food

A Large and Growing MarketGLOBAL OVERVIEW

© Euromonitor International

8

Dog FoodCat FoodOther Pet FoodPet Products

Global Pet Care By CategoryGLOBAL OVERVIEW

US$ 105 billion

© Euromonitor International

9

Pet Humanisation Drives GrowthGLOBAL OVERVIEW

-2.0

0.0

2.0

4.0

6.0

8.0

10.0

0

5

10

15

20

25

30

35

40

45

% C

AGR

(201

0-15

)

US$

billi

on

Global Value Sales and Growth by Category, 2010-2015

© Euromonitor International

10

A Story of PremiumisationGLOBAL OVERVIEW

0%

20%

40%

60%

80%

100%

2010 2011 2012 2013 2014 2015

% r

etai

l val

ue

Global Dog and Cat Food by Price Platform

Economy Mid-priced Premium

© Euromonitor International

11

Stark Differences by RegionGLOBAL OVERVIEW

© Euromonitor International

12

Asia Pacific

Australasia

Eastern Europe

Latin America

Middle East & Africa

North America

Western Europe

0%

2%

4%

6%

8%

10%

12%

14%

16%

18%

$0 $50 $100 $150 $200 $250 $300 $350

CA

GR

, 201

0-15

Per Household Sales, 2014

Pet Care: Per Household Sales and Growth, 2010-15

Two Distinct GroupingsGLOBAL OVERVIEW

GLOBAL OVERVIEW

DEVELOPED REGIONSEMERGING REGIONS

THE FUTURE

US$ 77bnPet Care Sales in 2015

US$ 216Per Household in 2015

3.6%CAGRBetween 2010-2015

© Euromonitor International

15

Leading MarketsDEVELOPED MARKETS

0.0

1.0

2.0

3.0

4.0

5.0

6.0

0

5

10

15

20

25

30

35

40

45

50

USA UnitedKingdom

France Germany Italy Australia Canada Spain Netherlands

% C

AG

R 2

010-

15 (F

ixed

E-R

)

US$

(bill

ions

, 201

5)

Leading Countries in Developed Regions, 2010-15

© Euromonitor International

16

Values over VolumesDEVELOPED MARKETS

-1%

0%

1%

2%

3%

4%

5%

2010-11 2011-12 2012-13 2013-14 2014-15

Y-on

-y g

row

th

Dog and Cat Food: Growth in Developed Regions

Value Sales(US$, Fixed E-R)

Volume Sales

© Euromonitor International

17

0

50

100

150

200

250

300

2010 2011 2012 2013 2014 2015

Popu

lati

on (i

n m

illio

ns)

Developed Regions: Dog and Cat Population, 2010-15

North America Western Europe Australasia

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

Shar

e of

Tot

al P

opul

atio

n

Developed Regions: Dog Population by Size: 2010-15

Large Dogs(Over 23 kg)

Medium Dogs(9 to 23 kg)

Small Dogs(up to 9 kg)

Weak Population Growth Hurts VolumesDEVELOPED MARKETS

0.2%CAGRBetween 2010-2015

© Euromonitor International

18

Growth: A Story of PremiumisationDEVELOPED MARKETS

0.0%

1.0%

2.0%

3.0%

4.0%

5.0%

6.0%

7.0%

0

2,000

4,000

6,000

8,000

10,000

12,000

14,000

16,000

Economy Mid-Priced Premium

CAG

R, 2

010-

15

Sale

s in

US$

(Mil)

North America: Dog and Cat Food by Price Tier, 2010-15

2010 2012 2015(p) CAGR 2010-15

0.0%

0.5%

1.0%

1.5%

2.0%

2.5%

3.0%

3.5%

0

1,000

2,000

3,000

4,000

5,000

6,000

7,000

8,000

Economy Mid-Priced Premium

CAG

R, 2

010-

15

Sale

s in

USD

(Mil,

Fix

ed E

-R)

Western Europe: Dog and Cat Food by Price Tier, 2010-15

2010 2012 2015(p) CAGR 2010-15

© Euromonitor International

19

Example: New Products in Canada Go UpscaleDEVELOPED MARKETS

Caru Naturals Stews by Caru Pet FoodPremium Wet Dog FoodLaunched June 2014

Resembles a stew that humans would eat: instantly-recognizable ingredients

Premium packaging: Recyclable Cartons; BPA-Free

All-Natural Formulation: No Artificial Colors, Flavors or Preservatives

Grain-Free, Gluten-Free, Soy-Free, No Animal By-Products

Fromm Four Star Beef Liva‘ttini Veg by Fromm Family FoodsPremium Dry Cat FoodLaunched April 2014

Grain-Free Recipe featuring beef liver, eggs, cheese, tomato, spinach, eggplant, zucchini

Premium packaging: Stand-Up pouch designed with fancy colors

Part of the company’s “Four Star Nutritionals” line

“An Italian Experience You Won’t Soon Forget”

“Pairs well with Chicken Duck and Salmon Pâté”

© Euromonitor International

20

0 5 10

Pet Products

Premium Cat Food

Premium Dog Food

Dog Treats

Cat Treats

% CAGR 2010-15

North America Top 5 Fastest Categories 2010-2015

Premium Foods and Treats LeadDEVELOPED MARKETS

0 10 20

Pet Products

Premium Dog Food

Premium Cat Food

Dog Treats

Cat Treats

% CAGR 2010-15

Western Europe Top 5 Fastest Categories 2010-2015

© Euromonitor International

21

Temptations Snacky Mouse by Mars IncCat TreatsUSA, 2015

Interactive toy and treat combination

Treat dispenser - Whiskas Temptations included in package

Entertaining for both cats and owners

Milk-Bone Brushing Chews by Big Heart Pet BrandsDog TreatsUSA, 2014

Helps clean teeth while chewed

Veterinary Oral Health Council’s (VOHC) seal of approval

Packaging looks like premium toothpaste

Innovation in US Pet TreatsDEVELOPED MARKETS

© Euromonitor International

22

Foodie Trends Come to TreatsDEVELOPED MARKETS

© Euromonitor International

23

0% 20% 40% 60% 80% 100%

WE

NA

AU

Value Share, 2015

Pet Food by Type, 2015Dog Food Cat Food Other Pet Food

Pet Preferences Vary SignificantlyDEVELOPED MARKETS

Key: WE – Western Europe; NA – North America; AU – Australasia

© Euromonitor International

24

38.1

50.2

64.7

27.8

21.4

25.3

6.15.8

2.9

3.5

4.8

1.124.5

17.8

6.0

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

North America Western Europe Australasia

Val

ue S

hare

, 201

5 (%

)

Developed Regions: Dog & Cat Food by Channel, 2015

Others

Internet Retailing

Veterinary Clinics

Pet Shops & Superstores

Supermarket & Hypermarkets

Significant Variation in Channel Distribution DEVELOPED MARKETS

© Euromonitor International

25

0% 20% 40% 60% 80% 100%

NA

AU

WE

Value Share, 2015

Dog & Cat Food: Pet Shops vs Superstores

Pet Shops Pet Superstores

Shops vs SuperstoresDEVELOPED MARKETS

Key: WE – Western Europe; NA – North America; AU – Australasia

Petco Photo Courtesy of: Mike Mozart (https://www.flickr.com/photos/jeepersmedia/14345603431/)Fressnapf Photo Courtesy of: Noebse (https://commons.wikimedia.org/wiki/Category:Fressnapf#/media/File:Fressnapf_Markt.JPG)

Pets at Home Photo Courtesy of: David Wright (https://commons.wikimedia.org/wiki/File:Pets_at_home_-_geograph.org.uk_-_485114.jpg)

47.5%

22.6%

12.2% 9.4%

© Euromonitor International

26

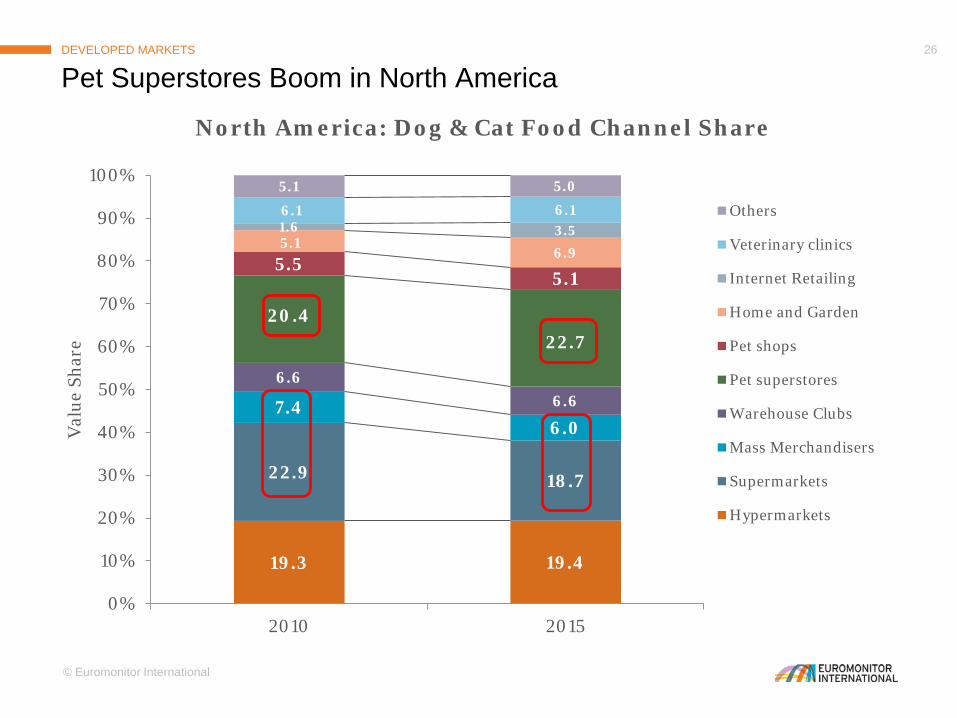

19.3 19.4

22.9 18.7

7.46.0

6.66.6

20.422.7

5.55.1

5.16.9

1.6 3.56.1 6.15.1 5.0

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

2010 2015

Val

ue S

hare

North America: Dog & Cat Food Channel Share

Others

Veterinary clinics

Internet Retailing

Home and Garden

Pet shops

Pet superstores

Warehouse Clubs

Mass Merchandisers

Supermarkets

Hypermarkets

Pet Superstores Boom in North AmericaDEVELOPED MARKETS

© Euromonitor International

27

Premium Manufacturers Gain SharePREMIUM PRODUCTS LEAD THE WAY

30.8 30.3

22.4 26.9

7.1

9.98.1

3.53.6

2.84.5

2.53.4

12.0 11.5

9.0 11.7

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

2009 2014

Val

ue S

hare

Canada: Dog & Cat Food Share by Company, 2009-14

Others

Private Label

Blue Buffalo Co Ltd

Champion Petfoods LP

Colgate-Palmolive Co

Big Heart Pet Brands

Procter & Gamble

Mars Inc*

Nestlé SA

*Note: Mars acquired Procter & Gamble’s Pet Business in April 2014

GLOBAL OVERVIEW

DEVELOPED REGIONS

EMERGING REGIONSTHE FUTURE

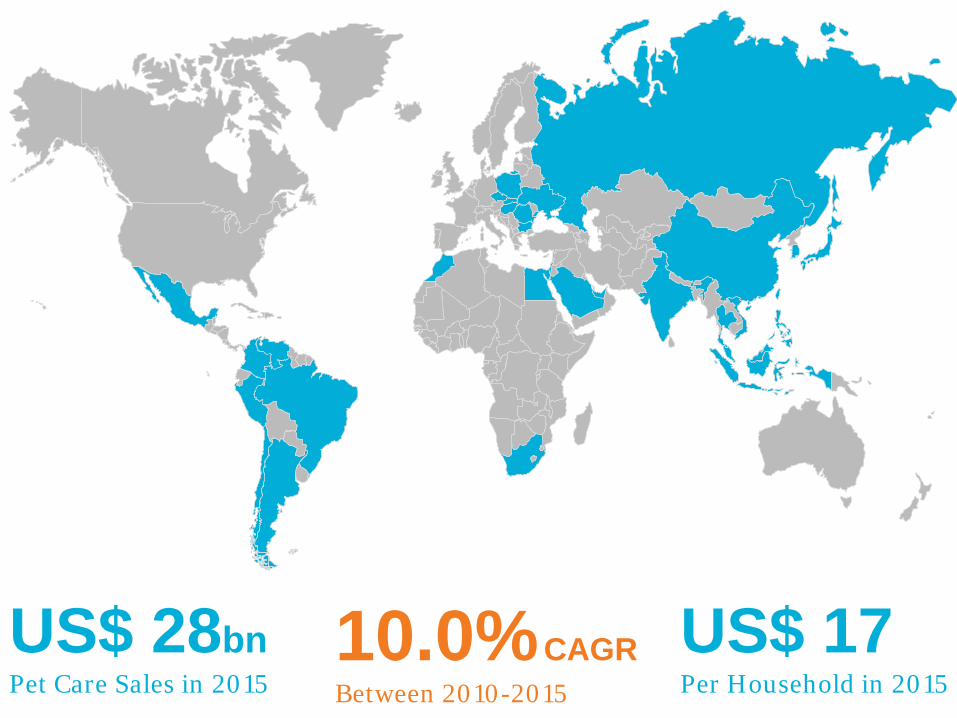

US$ 28bnPet Care Sales in 2015

US$ 17Per Household in 2015

10.0%CAGRBetween 2010-2015

© Euromonitor International

30

Leading MarketsEMERGING MARKETS

-2.0

0.0

2.0

4.0

6.0

8.0

10.0

12.0

14.0

0

1

2

3

4

5

6

Brazil Japan Mexico Russia Venezuela China Argentina South Korea Taiwan

% C

AG

R 2

010-

15 (F

ixed

E-R

)*

US$

(bill

ions

, 201

5)

Leading Countries in Emerging Regions, 2010-15

*Note: Growth in constant (real) terms are used in this case given high inflation rates in Venezuela and Argentina

© Euromonitor International

31

Values AND VolumesEMERGING MARKETS

0%

1%

2%

3%

4%

5%

6%

7%

8%

2010-11 2011-12 2012-13 2013-14 2014-15

Y-on

-y g

row

th

Dog and Cat Food: Growth in Emerging Regions

Value Sales (US$,Fixed E-R)*

Volume Sales

*Note: Growth in constant (real) terms are used in this case given high inflation rates some emerging markets

© Euromonitor International

32

0

50

100

150

200

250

300

350

400

2010 2011 2012 2013 2014 2015

Popu

lati

on (i

n m

illio

ns)

Emerging Regions: Dog and Cat Population, 2010-15

Middle East/Africa

Eastern Europe

Asia Pacific

Latin America

A Totally Different Trend in Pet PopulationsEMERGING MARKETS

3.0%CAGRBetween 2010-2015

© Euromonitor International

33

Asia-Pacific

Eastern Europe

Latin America

Middle East & Africa

0.0%

0.5%

1.0%

1.5%

2.0%

2.5%

3.0%

3.5%

4.0%

4.5%

5.0%

0 20 40 60 80 100 120 140 160

CA

GR

, 201

0-15

Dog & Cat Population (in millions, 2015)

Emerging Regions: Dog and Cat Population Growth

Growing Populations and OpportunityEMERGING MARKETS

© Euromonitor International

34

0%

2%

4%

6%

8%

10%

12%

14%

0

2

4

6

8

10

12

Economy Mid-Priced Premium

CAG

R, 2

010-

15, (

US$

, Fix

ed E

-R)

Sale

s in

US$

(Billi

ons)

Emerging Regions: Dog & Cat Food by Price Tier

2010 2012 2015(p) CAGR 2010-15

Growth: Across the BoardEMERGING MARKETS

© Euromonitor International

35

0 10 20

Cat Treats

Mid-Priced Dog Food

Economy Cat Food

Other Pet Food

Dog Treats

% CAGR 2010-15

Latin America Top 5 Fastest Categories 2010-2015

A Broader Base of GrowthEMERGING MARKETS

0 10 20

Mid-Priced Cat Food

Premium Dog Food

Economy Cat Food

Premium Cat Food

Cat Treats

% CAGR 2010-15

Eastern Europe Top 5 Fastest Categories 2010-2015

© Euromonitor International

36

0 10 20

Mid-Priced Cat Food

Pet Products

Premium Cat Food

Economy Dog Food

Cat Treats

% CAGR 2010-15

Asia-Pacific Top 5 Fastest Categories 2010-2015

A Broader Base of GrowthEMERGING MARKETS

0 10 20

Dog Treats

Pet Products

Mid-Priced Cat Food

Premium Dog Food

Premium Cat Food

% CAGR 2010-15

Middle East & Africa Top 5 Fastest Categories 2010-2015

© Euromonitor International

37

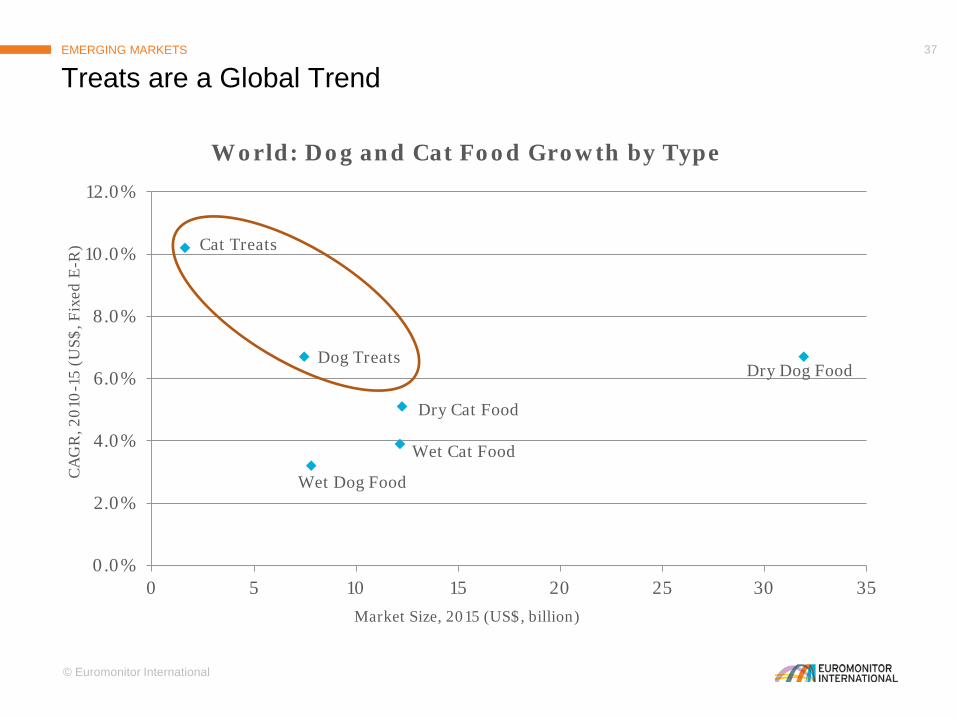

Treats are a Global TrendEMERGING MARKETS

Cat Treats

Dry Cat Food

Wet Cat Food

Dog TreatsDry Dog Food

Wet Dog Food

0.0%

2.0%

4.0%

6.0%

8.0%

10.0%

12.0%

0 5 10 15 20 25 30 35

CA

GR

, 201

0-15

(U

S$, F

ixed

E-R

)

Market Size, 2015 (US$, billion)

World: Dog and Cat Food Growth by Type

© Euromonitor International

38

Purina Dog Chow Abrazzos Integral Snaps by Nestlé Dog TreatsMexico, 2014

Made with whole wheat flour

Baked – reduced fat content

Fortified with essential vitamins and minerals

The Treat Boom Comes to Emerging RegionsEMERGING MARKETS

NoviPet Magic Treats by BioPet LtdDog TreatsSingapore, 2015

Fortified with DHA, Omega 6 and Multivitamins, Omega 3, Prebiotics or Glucosamine

Grain-free treats, no sugar

Available in blister and strip packs to maximize freshness

© Euromonitor International

39

0% 20% 40% 60% 80% 100%

AP

EE

LA

ME

Value Share, 2015

Pet Food by Type, 2015Dog Food Cat Food Other Pet Food

Pet Preferences Vary SignificantlyEMERGING MARKETS

Key: ME – Middle East & Africa; LA – Latin America; EE – Eastern Europe; AP – Asia Pacific

© Euromonitor International

40

43.9

30.2

25.3

30.2

5.8

6.8

3.9

3.9

21.1 29.0

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

Developed Regions Emerging Regions

Val

ue S

hare

, 201

5 (%

)

Dog & Cat Food by Channel, 2015

Others

Internet Retailing

Veterinary Clinics

Pet Shops & Superstores

Supermarket & Hypermarkets

Modern Grocery vs SpecialistsEMERGING MARKETS

© Euromonitor International

41

A Highly Fragmented ChannelEMERGING MARKETS

29,126 outlets

#1 global rank

55 m2/outlet

0% 20% 40% 60% 80% 100%

Developed

Emerging

Relative Value Share, 2015

Dog & Cat Food: Pet Shops vs SuperstoresPet Shops Pet Superstores

12,367 outlets

#2 global rank

84 m2/outlet

9,238 outlets

#3 global rank

666 m2/outlet

© Euromonitor International

42

The Potential for E-Commerce in Pet CareEMERGING MARKETS

US$839.6 bnInternet sales in 2014

169%Growth since 2009

5.8%Share total retail sales

© Euromonitor International

43

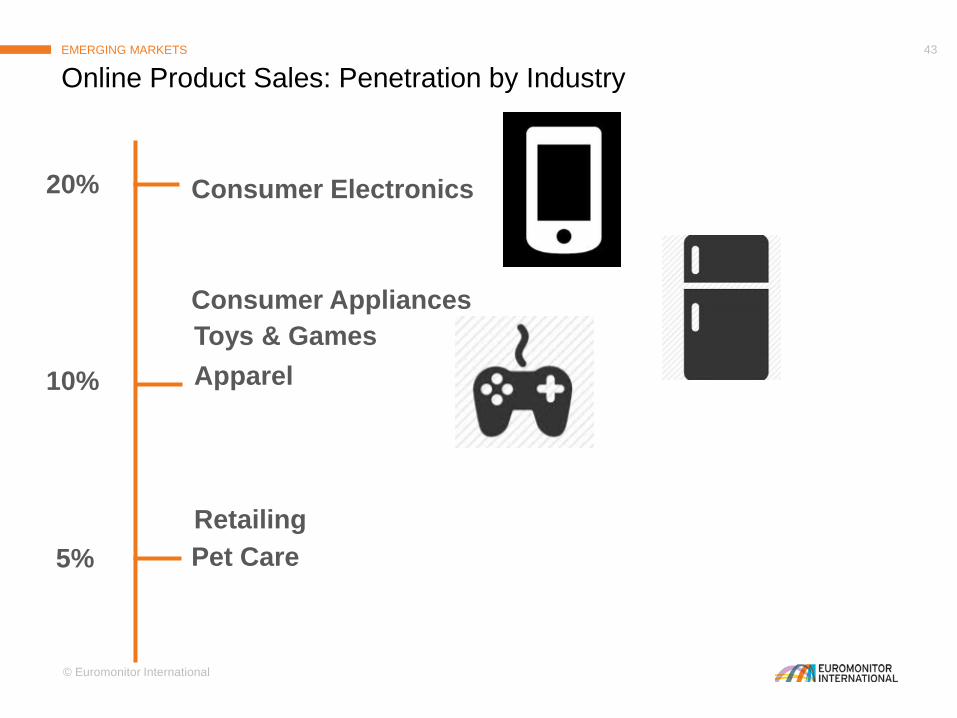

Online Product Sales: Penetration by IndustryEMERGING MARKETS

20%

10%

5%

Toys & Games

Consumer Electronics

Consumer Appliances

Apparel

RetailingPet Care

© Euromonitor International

44

Highest Internet Sales Share in Pet CareEMERGING MARKETS

15%

10%

5%

20%

GLOBAL OVERVIEW

DEVELOPED REGIONS

EMERGING REGIONS

THE FUTURE

© Euromonitor International

46

Pet Growth Expected to ContinueTHE FUTURE

© Euromonitor International

47

Cat Food 2010

AP EE LA Others

Cat Food by RegionTHE FUTURE AHEAD

Cat Food 2020

AP EE LA others

© Euromonitor International

48

Dog Food 2010

AP EE LA Others

Dog Food by RegionTHE FUTURE AHEAD

Dog Food 2020

AP EE LA Others

© Euromonitor International

49

0

100

200

300

400

500

600

700

800

2015 2016 2017 2018 2019 2020

Forecasted World Dog and Cat Population, 2015-20

Developing

Developed

Modest Population Growth ExpectedTHE FUTURE

1.4%CAGRBetween 2015-2020

© Euromonitor International

50

Growth to also Stem from Premium FoodsMARKET PERFORMANCE

0%

20%

40%

60%

80%

100%

2015 2016 2017 2018 2019 2020

% r

etai

l val

ue

Global Dog and Cat Food by Price Platform

Economy Mid-priced Premium

© Euromonitor International

51

Regional ContrastsTHE FUTURE

0.0%

0.5%

1.0%

1.5%

2.0%

2.5%

3.0%

3.5%

4.0%

4.5%

0

5

10

15

20

25

30

35

40

Dog Food Cat Food Other PetFood

PetProducts

CAG

R, 2

015-

20, (

US$

, Fix

ed E

-R)

Emerging Regions: Growth Forecast by Category

2015 2020 CAGR 2015-20

0.0%

0.5%

1.0%

1.5%

2.0%

2.5%

3.0%

3.5%

4.0%

4.5%

0

5

10

15

20

25

30

35

40

Dog Food Cat Food Other PetFood

PetProducts

CAG

R, 2

015-

20, (

US$

, Fix

ed E

-R)

Sale

s in

US$

(Bn)

Developed Regions: Growth Forecast by Category

2015 2020 CAGR 2015-20

© Euromonitor International

52

Global

• Consistent growth globally

• Stands out in stagnant CPG world

• Growth in both foods and treats

Developed Regions

• Pet population trends limit volume

• Growth a story of premiumisation

• Variations by pet type and channels

Emerging Regions

• Continued population growth

• Growth in all price platforms

• Small pet shops widespread

Treats Emerge

• A truly global trend: high-demand

• Innovation with value-added treats

• Cat treats with huge potential

E-Commerce Potential

• Ecommerce in pet care is limited

• Even developed regions modest

• Huge potential for growth

Beyond Food

• “Other Pet Products” has potential

• Apparel, Toys, “Pet tech”

• Small base in emerging regions

ConclusionTHE FUTURE

© Euromonitor International

53

THANK YOU FOR LISTENINGJared Koerten

Senior Analyst

Euromonitor Chicago224 S. Michigan Ave, 15th flChicago, IL 60604