Embed Size (px)

Citation preview

426 n (2006) vol. 54, no 2

The Taxation of Strike Pay

Benjamin Alarie and Matthew Sudak*

P r é c i s

En 1990, dans l’arrêt Fries c. Sa Majesté la Reine, la Cour suprême du Canada a confirmé comme question de droit la pratique administrative de longue date de caractériser les allocations de grève comme un revenu non imposable compte tenu du fait qu’elles ne sont pas « un revenu […] dont la source » au sens de l’alinéa 3a) de la Loi de l’impôt sur le revenu. Aux États-Unis, par contre, les allocations de grève sont généralement assujetties à l’impôt sur le revenu, conformément à l’approche plus inclusive de la définition du revenu qui prévaut en vertu de l’article 61 de l’Internal Revenue Code. L’article examine en détail cette différence de politique fiscale. Dans le processus, les auteurs examinent la position d’autres pays devant des enjeux semblables, élaborent ce que l’on peut inférer à partir des conséquences fiscales et économiques probables de ne pas imposer les allocations de grève, et suggèrent certaines idées de réforme à l’intention des décideurs politiques canadiens.

A b s t r A c t

The Supreme Court of Canada in 1990 in Fries v. The Queen confirmed as a legal matter the longstanding administrative practice of characterizing strike pay as a non-taxable receipt by virtue of its not being “income . . . from a source” pursuant to paragraph 3(a) of the Income Tax Act. By contrast, in the United States, strike pay is generally subject to income tax, consistent with the more inclusive approach to defining income that predominates under section 61 of the Internal Revenue Code. This article examines in detail this tax policy difference. In the process, it canvasses the attitude of some other countries to similar issues, maps out what can be inferred about the likely fiscal and economic consequences of not taxing strike pay, and suggests some ideas for reform for Canadian policy makers.

KEYWOrDs: Income n labour dIsputes n strIkes n tax exemptIons n tax polIcy n unIons

* OftheFacultyofLaw,UniversityofToronto.WeareindebtedtoJimDinningforexcellentresearchassistance.WeextendthankstoChrisBruce,ArthurCockfield,DavidDuff,TimEdgar,EdwardIacobucci,AlanMacnaughton,FeliceMartinello,LisaPhilipps,DanielSandler,MichaelTrebilcock,DavidWhite,staffatStatisticsCanadaandtheDepartmentofFinance,thoseinattendanceatpresentationsofourearlierresearchpaperattheUniversityofBritishColumbiaFacultyofLawandatthe2005TaxPolicyResearchSymposiumoftheDeloitteCentreforTaxEducationandResearchattheUniversityofWaterloo,andtwoanonymousrefereesforhelpfulcommentsandsuggestions.Anyerrorsoromissionsareourown.

the taxation of strike pay n 427

intrO Duc tiO n

InNewYorkCityonSeptember15,2004,GaryBettman,thecommissioneroftheNationalHockeyLeague(nhl),announcedaleague-widelockout1onaccountofstalledcollectivebargainingnegotiationswiththeplayers’association(thenhlpa).OnNovember24,2004,thenhlpaannounceditsintentiontopaylargemonthlystipends to the locked-out players.2 Following the announcement, the nhlpaadviseditsplayersthatthosewhoweresubjecttoincometaxintheUnitedStateswouldhavetoreportthestipendsastaxableincome,butthestipendswouldnotbesubjecttoincometaxinCanada.

ThedifferenceintaxpolicybetweenCanadaandtheUnitedStatesinthisregardisarresting.InCanada,adeductionfromemploymentincomeisavailableforan-nualduespaidtounions.Unionsthemselvesaretax-exemptorganizations,soanyinvestmentincomegeneratedbyfundsdivertedfromannualduesforaccumulationinastrikefundistax-exempt.Finally,strikepayhasbeentreatedbyCanadianreve-nueauthoritiesasnotbeingtaxable.ThisviewwasexplicitlyupheldbytheSupremeCourtofCanadain1990inFries v. The Queen,3wherethecourtdecidedthatstrikepaywasnot“income...fromasource”withinthemeaningofparagraph3(a)oftheIncomeTaxAct.4Asaconsequence,inCanada,amountsreceivedasstrikepaywill

c O n t E n t s

Introduction 427Canadian Tax Treatment of Union Dues, Union Investment Income, and Strike Pay 428Comparison with Other Countries 434

Australia 434United States 435United Kingdom 438New Zealand 439

Data 440Economic Effects 441Analysis of Policy Alternatives 444Conclusion 447Appendix Estimating Strike Pay Tax Expenditures for 1993 to 2004 448

1 TheNHLworkstoppageoccurredbecausetheemployerpreventedemployeesfromworking;thus,itwasalockoutratherthanastrike(aworkstoppagewhereemployeesrefusetowork).Inthisarticle,theterm“strikepay”referstoanystipendorin-kindamountpaidbyauniontoitsmembersduringaworkstoppage(sometimesalsocalled“lockoutpay”or“picketpay”).

2 StrikepayinCanadianlabourdisputesisusuallyrathermodest,rangingupto$350perweek(seethediscussionbelowundertheheading“Data”andintheappendix).ThestipendannouncedbytheNHLPAwasanomalouslyhigh,atUS$10,000foreachofthefirsttwomonthswithsubsequentpaymentsexpectedtorangefromUS$5,000toUS$10,000permonth.

3 90DTC6662;[1990]2CTC439(SCC);rev’g.89DTC5240;[1989]1CTC471(FCA).

4 RSC1985,c.1(5thSupp.),asamended(hereinreferredtoas“theITA”).

428 n canadian tax journal / revue fiscale canadienne (2006) vol. 54, no 2

flowtax-freefromtheemployer(intheusualcase)onbehalfoftheemployeetotheunion,andthenbackfromtheuniontotheemployee,withoutbeingsubjectedtoincometaxatanypoint.Thetreatmentofstrikepayislessgeneroussouthoftheborder.IntheUnitedStates,unionduesareeligibleasmiscellaneousdeductions,butonlyiftaxpayersitemizetheirdeductions(insteadoftakingthestandarddeduc-tion).AsinCanada,unionstypicallydonothavetopayincometaxoninvestmentincome.ThestarkestdifferenceisthatintheUnitedStates,consistentwithitsmoreinclusiveapproachtodefiningincome,5strikepayhasconsistentlybeenheldtobesubjecttotaxundersection61oftheInternalRevenueCode.6

Thetaxpolicyissuesraisedbystrikepayappearnottohavebeenpreviouslyad-dressedatanylength,eitherinCanadaorabroad.7Accordingly,thisarticlefillsthisgapintheliterature.WebeginbydescribingthetaxrulesinCanadaforstrikepayandexaminingsomestatutoryinterpretationissuessurroundingtheleadingcaseinthisarea(Fries).Thisisfollowedbyacomparisonwiththerulesinothercountries;reportingofkeydata,includingstrikepayamountsandforgonetaxrevenue;analy-sisoftheeconomiceffects;areviewoftheadvantagesanddisadvantagesofthemainpolicyalternatives;andfinally,ourconclusion.

c A n A Di A n tA x trE AtmEnt O f uniO n DuE s , uniO n in v E s tmEnt incOmE , A nD s triK E PAY

Atfirstglance,itmightseemthattheissueofthetaxtreatmentofstrikepayisabinaryquestion:“Isstrikepaysubjecttotaxornot?”However,togetacompletepictureofthetaxtreatmentofstrikepay,itisnecessarytoconsiderthecontextinwhichstrikepayisreceived.Thereareactuallythreedistinctlevelsofanalysisthataresalienttosettingoutthetaxtreatmentofpaymentsfromlabourorganizationstotheirmembersduringlabourdisputes.Atthefirstlevelofanalysisistheissueofthedeductibilityofmembership feesorunionduespaid to labourorganizations.Atthesecondlevel,thetaxstatusandtreatmentofthevariousactivitiesofthelabourorganization itself—especially the aggregation, accumulation, and investment offunds held in reserve for use during potential labour disputes—is relevant. Thefinallevelofanalysisisconcernedwithpaymentsmadebylabourorganizationsforthesupportofworkerswhohavebeenlockedoutorareonstrike—thatis,thetaxconsequencestotherecipientofstrikepay.

5 Thisbroadapproachwasfirmlyestablishedin1955bytheUnitedStatesSupremeCourtinCommissioner v. Glenshaw Glass Co.,348US426(1955).WarrenCJremarked,ibid.,at429-30,“Congressappliednolimitationsastothesourceoftaxablereceipts,norrestrictivelabelsastotheirnature.AndtheCourthasgivenaliberalconstructiontothisbroadphraseologyinrecognitionoftheintentionofCongresstotaxallgainsexceptthosespecificallyexempted.”

6 InternalRevenueCodeof1986,asamended(hereinreferredtoas“theIRC”).

7 ThemostdetailedaccountappearstobeaparagraphinJonathanR.Kesselman,“BaseReformsandRateCutsforaRevitalizedPersonalTax”(1999)vol.47,no.2Canadian Tax Journal210-41,at223.

the taxation of strike pay n 429

Generallyspeaking,“annualdues”paidbyanofficeroranemployeetoaneli-gible“tradeunion”aredeductiblefromthetaxpayer’s incomefromtheofficeoremploymentunlessthepaymentscanbemoreaccuratelyconsideredtobepaymentsmadeforsomenon-unionpurpose(suchasestablishingorsupportingasuperan-nuationfund),fortheprovisionofinsurance,orforanypurposenotrelatedtotheunion’sordinaryoperatingexpenses.8Annualduespaidtoaneligibletradeunionarenotdeductibleiftheofficeroremployeehasbeen(orwillbe)reimbursedbyhisorheremployerforthefees9orifthefeesconstituteaninitiationfeeassociatedwithjoiningtheunionratherthanannualduesnecessarytomaintainmembership.10

Inordertobeconsideredaneligible“tradeunion,”anorganizationmustsatisfythedefinitionof“tradeunion”insection3oftheCanadaLabourCode11orthedefinitioninanyprovinciallabourrelationslegislation.Section3oftheclcdefines“tradeunion”as“anyorganizationofemployees,oranybranchorlocalthereof,thepurposesofwhichincludetheregulationofrelationsbetweenemployersandemployees.”Substantiallysimilardefinitionsof“union”and/or“tradeunion”canbefoundinprovinciallegislationaddressinglabourrelations.12

Withregardtotherequirementthattheduespaidtotheunionbe“annualdues,”Canadiancourtshaveanalyzedthemeaningofthetermonanumberofoccasions.13Therelevantcaselawmakesitclearthattheterm“annualdues”hasbeentreatedasratherporousbythecourts.Whilecontributionsearmarkedspecificallyforuseinastrikefundorforcertainspecificpensionorsimilarbenefitswillnotgenerallybedeductible,incaseswherethereisnosuchearmarking,Canadiancourtsappeartobewillingtoconsidercontributionstounionstobe“annualdues.”

Movingontothesecondstageoftheanalysis,unionsaregenerallyconsideredtobeexemptorganizationsunderparagraph149(1)(k)oftheita.Ostensiblysimilarinmotivationtothegeneraldeductibilityofunionduespaidbyofficersandem-ployees,paragraph149(1)(k)providesthatamountsreceivedbyaunionqualabour

8 ITAsubparagraphs8(1)(i)(iv)and(v),andsubsection8(5)securethisresult.SeealsoInterpretation BulletinIT-103R,“DuesPaidtoaUnionortoaParityorAdvisoryCommittee,”November4,1988.

9 IT-103R,supranote8,atparagraph3.

10 SeeBurke v. The Queen,76DTC6075(FCTD).

11 RSC1985,c.L-2,asamended(hereinreferredtoas“theCLC”).

12 Forexample,section1(1)oftheOntarioLabourRelationsAct,1995,SO1995,c.1,scheduleA,defines“tradeunion”as“anorganizationofemployeesformedforpurposesthatincludetheregulationofrelationsbetweenemployeesandemployersandincludesaprovincial,national,orinternationaltradeunion,acertifiedcounciloftradeunionsandadesignatedorcertifiedemployeebargainingagency.”Similarly,section1(x)ofAlberta’sLabourRelationsCode,RSA2000,c.L-1,asamended,defines“tradeunion”as“anorganizationofemployeesthathasawrittenconstitution,rulesorbylawsandhasasoneofitsobjectstheregulationofrelationsbetweenemployersandemployees.”

13 See,forexample,Burke,supranote10;Lucas v. MNR,84DTC1628(TCC);andHummel v. The Queen,[1997]2CTC2791(TCC).

430 n canadian tax journal / revue fiscale canadienne (2006) vol. 54, no 2

organizationwillnotbetaxable.ThepositionoftheCanadaRevenueAgency(cra)isthatlabourorganizationsdonothavetofileforstatusorregisterinanyparticularwayinordertobeexempt;thatis,theprovisionisself-assessing.ThecrastatedinatechnicalinterpretationissuedonSeptember10,2001thatwhetheraparticularentityconstitutesa labourorganizationinanygivenyear isaquestionof facttobedeterminedfromyeartoyearonthebasisoftheentity’sactivities.14Relevant,thoughnotdispositive,intheviewofthecraisthelistoforganizationscontainedinthe“DirectoryofLabourOrganizationsinCanada”maintainedbyHumanRe-sourcesDevelopmentCanada.15

Thetaxadvantagesextendalsotothethirdandmostvisible levelofanalysis:thetaxtreatmentofstrikepayitself.OnMay5,1989,inajudgmentthatwouldultimatelybeoverturnedbytheSupremeCourtofCanada,theFederalCourtofAppealinFries16heldthat$880.80receivedbyWallyFriesinstrikepayfromtheSaskatchewanGovernmentEmployees’Unionwastaxableas“income...fromasource”underparagraph3(a)oftheita,andthereforeshouldhavebeenreportedasincomebyFries.Inthisrespect,theFederalCourtofAppealupheldtheassessmentoftheminister,whohadgoneagainstestablishedadministrativepracticeinarguingthatthestrikepaywastaxableasincome,probablybecauseFrieswasonasympa-thystrikeandthestrikepaywasmuchhigherthannormal.Infact,thestrikepayreceivedwasintendedtoprovidefullafter-taxwagereplacement.FriesappliedforleavetoappealtotheSupremeCourtofCanada.TheSupremeCourtunanimouslyallowedtheappeal,reversingthejudgmentoftheFederalCourtofAppeal.Inwhatis almost certainly the shortestSupremeCourtofCanada judgment to reverse ajudgmentoftheFederalCourtofAppealinataxcase,Sopinkajrenderedthecourt’sreasons—whicharereproducedinfullinthefollowingexcerpt—fromthebench:

Wearenotsatisfiedthatthepaymentsbywayofstrikepayinthiscasecomewithinthedefinitionof“income...fromasource”withinthemeaningofs.3oftheIncome Tax Act.Inthesecircumstancesthebenefitofthedoubtmustgotothetaxpayers.Theap-pealisthereforeallowedandthedecisionoftheTaxReviewBoardisrestored.Theappellantsaretohavetheircoststhroughout.17

14 CRAdocumentno.2001-009077,September10,2001.

15 SeeHumanResourcesDevelopmentCanada,“DirectoryofLabourOrganizationsinCanada”(online:http://www110.hrdc-drhc.gc.ca/millieudetravail_workplace/ot_lo/index.cfm/doc/english).TheNHLPAislistedasalabourorganizationinthedirectory.

16 Supranote3.

17 Fries,supranote3,at6662;439(SCC).JudgmentsfromthebenchareinfrequentbutnotuncommonattheSupremeCourtofCanada.However,therearetwothingsthatmakethejudgmentinFriesstandout:first,thecourttendstoprovidemoredetailedreasonsintaxcases;andsecond,judgmentsfromthebenchareusuallyreservedforcasesinwhichanappealisbeingdismissed,notallowed.ThereversalofadecisionoftheFederalCourtofAppealsoswiftlyandwithsolittlefanfareisremarkable.

the taxation of strike pay n 431

TheSupremeCourt’sjudgmentinthecasehasbeencriticizedforitsbrevityandthereluctanceofthecourttoengagewithoranalyzetheproperapproachtoconstruingparagraph3(a)oftheita.Forexample,Krishnaremarksthat“theSupremeCourtbypassedthefundamentalissue:shouldsection3bereadexpansivelyonaglobal,ornarrowlyonaschedular,basis.”18Similarly,Hogg,Magee,andListate,“Inasurprisinglybriefjudgmentonanissueoffundamentalimportance,theCourtdidnotanalyzewhetherstrikepayhadthecharacterofincomeandthefactthataunionhadanobligationtomakepaymentstoitsmembersonstrike.”19

Inourview, it is indeedunfortunatethatthecourtdidnotprovideadetailedanalysisofthereferenceto“income...fromasource”inparagraph3(a)oftheita.Notonlydidthecourtbypassanopportunitytoengagewiththeappropriateinter-pretationoftheprovision;italsofailedtoundertakeameaningfulanalysisofthedecisionoftheFederalCourtofAppeal,whichdisallowedthetaxpayer’sargumentthatthe$880.80paymentwasmerelyareturnofincome,onthebasisthatthefundshadbeencommingledandheldinacommonfund.Inaddition,inourview,theSupremeCourtshouldhaveaddressedthefactthatunionmembers’contributionsofuniondueshadalreadybenefitedfromdeductibilityandthatinvestmentreturnsofthestrikefundwereexemptfromtax.Inchoosingnottoprovidesubstantialrea-sons,thecourtappearstohaveignoredthecautionarywordsofUriejattheFederalCourtofAppeal,whowrotewithrespecttotheimportanceofthecase:

Thepartiesheretohaveagreedthat,despitethesmallamountinvolved,thisappealisanimportantonesinceitisatestcaseforasubstantialnumberofotherpotentialappellantswhoseappealsfromassessmentsofincometaxarisingfromlargelysimilarfacts,dependontheoutcomeoftheappeal.20

Thedecisionisallthemorelamentablegivenitscursoryanalysisandproblem-aticreturntosupposedlybygonemethodsof statutory interpretation.AccordingtoDuff,

[w]hile statutory interpretationcannotproceedwithoutbackgroundnormsandas-sumptions, thesenormsandassumptionsshouldreflect thevaluesof thesocietyofwhichtheyareapart,notthoseofabygoneera.Forthisreason,aresidualpresump-tion in favour of the taxpayer, a lingering legacy of strict construction, is perhapslessconvincingthanaresidualpresumptioninfavourofpoliticalaccountabilityanddemocraticdecisionmaking....InFries v. The Queen,...wherethetaxpayerarguedsuccessfully that strike pay was not income from an unspecified source within themeaningofparagraph3(a)oftheAct,suchapresumptionwouldhavefavouredtheCrown,requiringlabourunionsandtheirmemberstojustifyaspecialexemptionforstrikepaynotwithstandingthatunionduesaredeductibleincomputingataxpayer’s

18 VernKrishna,The Fundamentals of Canadian Income Tax,8thed.(Toronto:Carswell,2004),133.

19 PeterW.Hogg,JoanneE.Magee,andJinyanLi,Principles of Canadian Income Tax Law,5thed.(Toronto:Carswell,2005),84.

20 Fries,supranote3,at5240;471(FCA).

432 n canadian tax journal / revue fiscale canadienne (2006) vol. 54, no 2

employmentincomeandtheinvestmentincomethataccumulatesinaunion’sstrikefundistax-exempt.21

Thus,thedecisionmayalsodemonstratehowtheSupremeCourtofCanadaalmostimmediatelybegandriftingawayfromtheso-calledmodernapproachtotheinter-pretationoftheita(theapproachemphasizedinthecourt’sjudgmentinStubart Investments Limited v. The Queen)22infavourofthemoretraditionalstrictapproach,pursuant towhich failure to enumerate a sourceof incomewithin the ita leadsalmostinexorablytoajudgmentinfavourofthetaxpayer.23

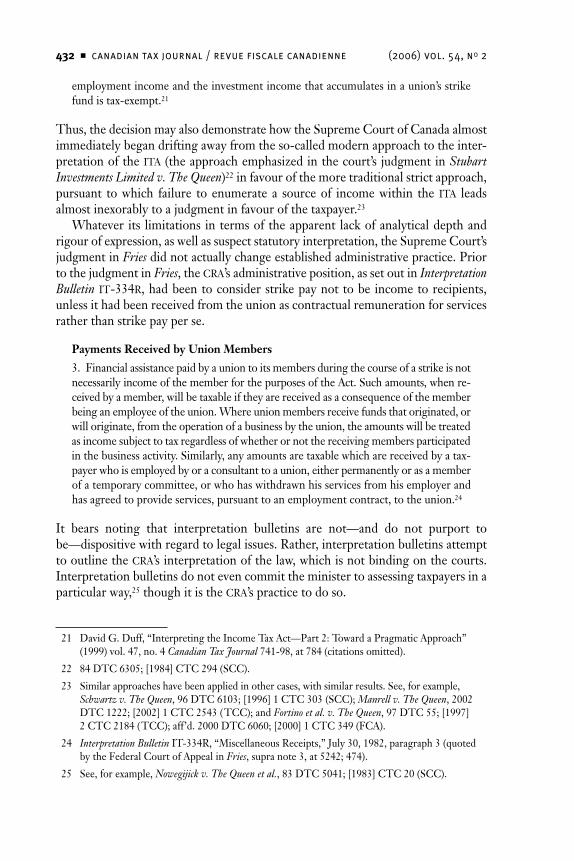

Whatever its limitationsintermsoftheapparent lackofanalyticaldepthandrigourofexpression,aswellassuspectstatutoryinterpretation,theSupremeCourt’sjudgmentinFriesdidnotactuallychangeestablishedadministrativepractice.PriortothejudgmentinFries,thecra’sadministrativeposition,assetoutinInterpretation Bulletin it-334r,hadbeentoconsiderstrikepaynottobeincometorecipients,unlessithadbeenreceivedfromtheunionascontractualremunerationforservicesratherthanstrikepayperse.

Payments Received by Union Members

3. FinancialassistancepaidbyauniontoitsmembersduringthecourseofastrikeisnotnecessarilyincomeofthememberforthepurposesoftheAct.Suchamounts,whenre-ceivedbyamember,willbetaxableiftheyarereceivedasaconsequenceofthememberbeinganemployeeoftheunion.Whereunionmembersreceivefundsthatoriginated,orwilloriginate,fromtheoperationofabusinessbytheunion,theamountswillbetreatedasincomesubjecttotaxregardlessofwhetherornotthereceivingmembersparticipatedinthebusinessactivity.Similarly,anyamountsaretaxablewhicharereceivedbyatax-payerwhoisemployedbyoraconsultanttoaunion,eitherpermanentlyorasamemberofatemporarycommittee,orwhohaswithdrawnhisservicesfromhisemployerandhasagreedtoprovideservices,pursuanttoanemploymentcontract,totheunion.24

It bears noting that interpretation bulletins are not—and do not purport tobe—dispositivewithregardtolegalissues.Rather,interpretationbulletinsattempttooutlinethecra’sinterpretationofthelaw,whichisnotbindingonthecourts.Interpretationbulletinsdonotevencommittheministertoassessingtaxpayersinaparticularway,25thoughitisthecra’spracticetodoso.

21 DavidG.Duff,“InterpretingtheIncomeTaxAct—Part2:TowardaPragmaticApproach”(1999)vol.47,no.4Canadian Tax Journal741-98,at784(citationsomitted).

22 84DTC6305;[1984]CTC294(SCC).

23 Similarapproacheshavebeenappliedinothercases,withsimilarresults.See,forexample,Schwartz v. The Queen,96DTC6103;[1996]1CTC303(SCC);Manrell v. The Queen,2002DTC1222;[2002]1CTC2543(TCC);andFortino et al. v. The Queen,97DTC55;[1997]2CTC2184(TCC);aff’d.2000DTC6060;[2000]1CTC349(FCA).

24 Interpretation BulletinIT-334R,“MiscellaneousReceipts,”July30,1982,paragraph3(quotedbytheFederalCourtofAppealinFries,supranote3,at5242;474).

25 See,forexample,Nowegijick v. The Queen et al.,83DTC5041;[1983]CTC20(SCC).

the taxation of strike pay n 433

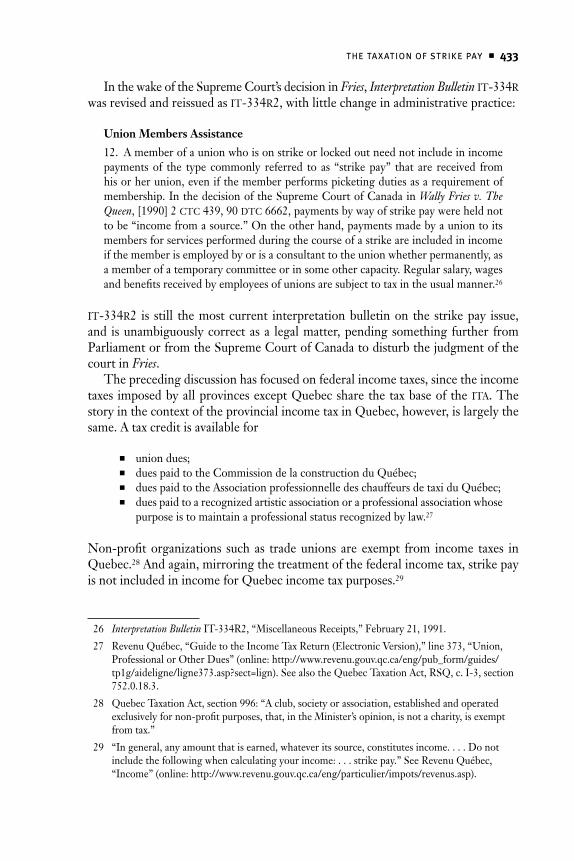

InthewakeoftheSupremeCourt’sdecisioninFries,Interpretation Bulletinit-334rwasrevisedandreissuedasit-334r2,withlittlechangeinadministrativepractice:

Union Members Assistance

12. Amemberofaunionwhoisonstrikeorlockedoutneednotincludeinincomepaymentsof the type commonly referred to as “strikepay” that are received fromhisorherunion,evenifthememberperformspicketingdutiesasarequirementofmembership.InthedecisionoftheSupremeCourtofCanadainWally Fries v. The Queen,[1990]2ctc439,90dtc6662,paymentsbywayofstrikepaywereheldnottobe“incomefromasource.”Ontheotherhand,paymentsmadebyauniontoitsmembersforservicesperformedduringthecourseofastrikeareincludedinincomeifthememberisemployedbyorisaconsultanttotheunionwhetherpermanently,asamemberofatemporarycommitteeorinsomeothercapacity.Regularsalary,wagesandbenefitsreceivedbyemployeesofunionsaresubjecttotaxintheusualmanner.26

it-334r2 is still themostcurrent interpretationbulletinon the strikepay issue,and isunambiguouslycorrectasa legalmatter,pendingsomething further fromParliamentorfromtheSupremeCourtofCanadatodisturbthejudgmentofthecourtinFries.

Theprecedingdiscussionhasfocusedonfederalincometaxes,sincetheincometaxesimposedbyallprovincesexceptQuebecsharethetaxbaseofthe ita.ThestoryinthecontextoftheprovincialincometaxinQuebec,however,islargelythesame.Ataxcreditisavailablefor

n uniondues;n duespaidtotheCommissiondelaconstructionduQuébec;n duespaidtotheAssociationprofessionnelledeschauffeursdetaxiduQuébec;n duespaidtoarecognizedartisticassociationoraprofessionalassociationwhose

purposeistomaintainaprofessionalstatusrecognizedbylaw.27

Non-profitorganizations such as tradeunions are exempt from income taxes inQuebec.28Andagain,mirroringthetreatmentofthefederalincometax,strikepayisnotincludedinincomeforQuebecincometaxpurposes.29

26 Interpretation BulletinIT-334R2,“MiscellaneousReceipts,”February21,1991.

27 RevenuQuébec,“GuidetotheIncomeTaxReturn(ElectronicVersion),”line373,“Union,ProfessionalorOtherDues”(online:http://www.revenu.gouv.qc.ca/eng/pub_form/guides/tp1g/aideligne/ligne373.asp?sect=lign).SeealsotheQuebecTaxationAct,RSQ,c.I-3,section752.0.18.3.

28 QuebecTaxationAct,section996:“Aclub,societyorassociation,establishedandoperatedexclusivelyfornon-profitpurposes,that,intheMinister’sopinion,isnotacharity,isexemptfromtax.”

29 “Ingeneral,anyamountthatisearned,whateveritssource,constitutesincome....Donotincludethefollowingwhencalculatingyourincome:...strikepay.”SeeRevenuQuébec,“Income”(online:http://www.revenu.gouv.qc.ca/eng/particulier/impots/revenus.asp).

434 n canadian tax journal / revue fiscale canadienne (2006) vol. 54, no 2

cOmPA risO n With OthEr cO untriE s

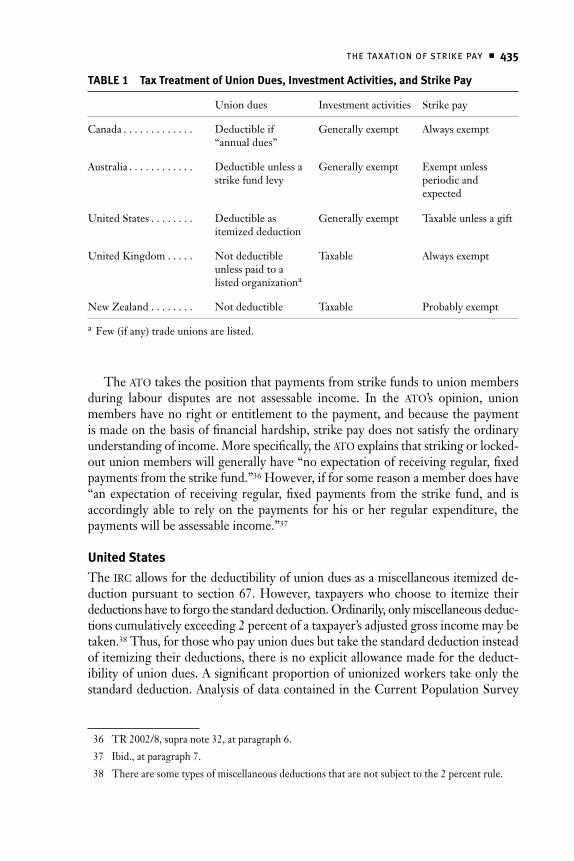

Canadianrulesforeachofthethreeaspectsdescribedabove—thedeductibilityofuniondues,thetaxationofinvestmentincomeofunions,andthetaxationofstrikepay itself—maybecomparedwithsimilarrules intheUnitedStates, theUnitedKingdom,NewZealand,andAustralia.Attemptstobroadenthecomparativesurveywerefrustratedbythefactthatthetaxationofstrikepayisrarelyaddressedwithexplicitstatutoryprovisions.30Table1,whichprovidesasummaryofthefindings,showsthatAustraliajoinsCanadainbothallowingadeductionforunionduesandnottaxingstrikepay,whileothercountrieseitherprovidenodeductionforuniondues(theUnitedKingdomandNewZealand)ortaxstrikepay(theUnitedStates).

Australia

TheAustralianapproachtothedeductibilityofunionduesandthetaxationofstrikepayhasbeenaddressedinapairoftaxationrulingsissuedbytheAustralianTaxationOffice(ato)inApril2002.Thefirstoftheserulingsdealswiththedeductibilityofpaymentsbyunionmemberstostrikefunds.31Thesecondaddresseswhetherpay-mentsfromstrikefundsreceivedbyworkersduringalabourdisputeareassessabletotax.32Withregardtothedeductibilityofcontributionstostrikefunds,theatohasdrawnadistinction(similartotheonedrawninCanada)betweenordinaryunionmembershipfees,whicharegenerallydeductible,andspecialstrikefundlevies,whicharenotdeductible.Theatostates,“Apaymentofalevytoastrikefundwillonlybeincurredingainingorproducingthecontributor’sassessableincomewherethestrikefundisusedtomaintainor improvethecontributor’spay.”33Theatoex-plainsinafootnotethatcontributionstostrikefundsarenotdeductibleonthebasisthat“[w]ehavebeenadvisedbyaleadingtradeunionthatstrikefundsarenotestab-lishedfor[the]purpose[ofmaintainingorimprovingthecontributor’spay].”34

TradeunionslocatedinAustraliathatoperateprincipallyinAustraliaareconsid-eredtobetax-exemptorganizations.However,thetaxexemptiondoesnotapplytoincomeearnedbyanotherwisetax-exempttradeunionfromanysuperannuation,lifeinsurance,oraccidentanddisabilityinsurancebusinessitcarrieson.35

30 Thelackofsuchprovisionsmakesonewonderwhetherstrikepayisuncommoninsomeoftheseothercountries.

31 AustralianTaxOffice,Taxation Ruling2002/7,“IncomeTax:DeductibilityofPaymentstoStrikeFunds,”April24,2002.

32 AustralianTaxationOffice,Taxation Ruling2002/8,“IncomeTax:AssessabilityofPaymentsReceivedfromStrikeFunds,”April24,2002.

33 TR2002/7,supranote31,atparagraph8.

34 Ibid.,atnote2.

35 AustralianTaxationOffice,“IsYourOrganisationExemptfromIncomeTax?IncomeTaxGuideforNon-ProfitOrganisations”(online:http://www.ato.gov.au/nonprofit/content.asp?doc=/content/34269.htm).

the taxation of strike pay n 435

tAblE 1 Tax Treatment of Union Dues, Investment Activities, and Strike Pay

Uniondues Investmentactivities Strikepay

Canada . . . . . . . . . . . . . Deductibleif“annualdues”

Generallyexempt Alwaysexempt

Australia . . . . . . . . . . . . Deductibleunlessastrikefundlevy

Generallyexempt Exemptunlessperiodicandexpected

UnitedStates . . . . . . . . Deductibleasitemizeddeduction

Generallyexempt Taxableunlessagift

UnitedKingdom . . . . . Notdeductibleunlesspaidtoalistedorganizationa

Taxable Alwaysexempt

NewZealand........ Notdeductible Taxable Probablyexempt

a Few(ifany)tradeunionsarelisted.

Theatotakesthepositionthatpaymentsfromstrikefundstounionmembersduring labour disputes are not assessable income. In the ato’s opinion, unionmembershavenorightorentitlementtothepayment,andbecausethepaymentismadeonthebasisoffinancialhardship,strikepaydoesnotsatisfytheordinaryunderstandingofincome.Morespecifically,theatoexplainsthatstrikingorlocked-outunionmemberswillgenerallyhave“noexpectationofreceivingregular,fixedpaymentsfromthestrikefund.”36However,ifforsomereasonamemberdoeshave“anexpectationof receivingregular,fixedpayments fromthestrike fund,and isaccordinglyable to relyon thepayments forhisorher regularexpenditure, thepaymentswillbeassessableincome.”37

United States

Theircallowsforthedeductibilityofunionduesasamiscellaneousitemizedde-ductionpursuant to section67.However, taxpayerswhochoose to itemize theirdeductionshavetoforgothestandarddeduction.Ordinarily,onlymiscellaneousdeduc-tionscumulativelyexceeding2percentofataxpayer’sadjustedgrossincomemaybetaken.38Thus,forthosewhopayunionduesbuttakethestandarddeductioninsteadofitemizingtheirdeductions,thereisnoexplicitallowancemadeforthededuct-ibilityofuniondues.Asignificantproportionofunionizedworkerstakeonlythestandarddeduction.AnalysisofdatacontainedintheCurrentPopulationSurvey

36 TR2002/8,supranote32,atparagraph6.

37 Ibid.,atparagraph7.

38 Therearesometypesofmiscellaneousdeductionsthatarenotsubjecttothe2percentrule.

436 n canadian tax journal / revue fiscale canadienne (2006) vol. 54, no 2

(cps)39 and tax statisticsproducedby the InternalRevenueService (irs)40 showsthatmorethan40percentofhouseholdswithatleastoneunionizedemployeetakethestandardizeddeduction.Thisnumberissubstantiallylowerthanthepercent-ageofhouseholdswheretherearenounionizedemployees.Inhouseholdswithoutaunionizedmember,approximately70percentoftaxpayerstakethestandardizeddeduction.41

Labourorganizationsareconsideredtobetax-exemptbyvirtueofsection501(c)(5)oftheirc.42Accordingtotheirs,tobealabourorganizationforthepurposesofsection501(c)(5),aparticularentityhastobe

1. anassociationofworkers 2. whohavecombinedtoprotectorpromotetheinterestsofthemembers 3. bybargainingcollectivelywiththeiremployers 4. tosecurebetterworkingconditions,wages,andsimilarbenefits.

Aspecial-purposelabourorganizationnotcontrolledbyprivateindividuals43andcreatedforthepurposeofoperatingastrikeorlockoutfundhasbeenheldbytheirstosatisfythefourprongsofthistest,sincestrikepayprovideddirectlytomembersfurthersa“union’sprimarypurposeofrepresentingitsmembersinmattersofwages,hoursoflabor,workingconditions,andeconomicbenefits.”44Althoughanyincome

39 UnitedStates,BureauofLaborStatisticsandtheBureauoftheCensus,“CurrentPopulationSurvey”(online:http://www.bls.census.gov/cps/).

40 InternalRevenueService,StatisticsofIncomeDivision,“SOITaxStats—IndividualStatisticalTablesbyAdjustedGrossIncome”(online:http://www.irs.gov/taxstats/indtaxstats/article/0,,id=96981,00.html).

41 Statisticsforthedistributionofgrossincomeforunionizedandnon-unionizedhouseholdsfromtheCPSwerecomparedwithstatisticsforthetypeofdeductiontakenamongtaxpayersindifferentincomebrackets.Thedataarefrom2001,themostrecentavailableyear.Theresultsshowthatapproximately57.8percentofhouseholdswithoneunionizedemployeeitemizedtheirdeductions,comparedwith28.1percentofnon-unionizedhouseholds.Therearethreeimportantcaveatstothesefindings.First,theCPSdatauseonlyhouseholdincome.TheIRSdataincludeallreturns(couplesfilingjointly,separately,etc.).However,whenIRSdataforjointfilingsonlyareexamined,nosignificantchangesresult.Second,theIRSdataincludeonlythosereturnsreportingatleast$1ofgrossincome.TheCPSdataincludehouseholdswithreportedincomeofzero.Third,theIRSdataincludenumerousbracketsforgrossincomelevelsabove$75,000.However,inordertocoincidewiththeCPSdata,thesebracketswerecombinedandaweightedaveragetaken.Asaresult,thedataonunionizedemployeesarelikelyskewed,becauseitisprobablethatalargerproportionofunionizedhouseholdswouldfallinthelowerendofthisbracketcomparedwiththegeneralpopulation.

42 ForanextendedtreatmentofIRCsection501(c)(5),seeJohnFrancisReilly,CarterC.Hull,andBarbaraA.BraigAllen,IRC 501(c)(5) Organizations,ExemptOrganizations—TechnicalInstructionProgramforFY2003(Washington,DC:InternalRevenueService,2003)(online:http://www.irs.gov/pub/irs-tege/eotopicj03.pdf ).

43 Fordetails,seeRev.rul.76-420,1976-2CB153.

44 Rev.rul.67-7,1967-1CB137.

the taxation of strike pay n 437

accruingtolabourorganizationsisgenerallyconsideredtax-exempt,section501(c)(5)entitiesmuststillreportandremittaxeson“unrelatedbusinessincome.”Inkeepingwithasection501(c)(5)entity’stax-exemptstatus,investmentincomegeneratedbythelabourorganizationandusedtosupportitsendsisgenerallynon-taxable.

Thedefinitionof“grossincome”insection61(a)oftheircstates,“Exceptasotherwiseprovidedinthissubtitle,grossincomemeansallincomefromwhateversourcederived.”Theprovisionthenlistsexamplesofspecificamountsincludedingrossincome,referstosections71andfollowingasprovisionsdetailingspecificinclu-sions,andreferstosections101andfollowingasprovisionsdetailingspecificexclusions.Strikepayisnotexplicitlymentionedanywhereintheirc.However,thebroadin-terpretationthattheUnitedStatesSupremeCourthasgiventothephrase“grossincomemeans all income fromwhatever sourcederived,” in cases likeGlenshaw Glass,45hasbeenappliedbylowercourtstoincludestrikeandlockoutbenefits.Theprimarytaxpayerargumentinthereporteduscaselawonstrikepaytendstobethatthe strikepaywasgratuitous—that is, agift46—andshould thereforebeexcludedfromgrossincomeonthebasisofsection102(1)oftheirc,aprovisionthatexpresslyexcludesgiftsand inheritances fromgross income.Sincethequestionwhetheraparticulartransferofpropertyisagiftisaquestionoffactthatturnsonwhetherthetransferorwasmotivatedtoactoutof“detachedanddisinterestedgenerosity,”itisperhapsnotsurprisingthatsomecourtshavecharacterizedstrikepayasagiftincertaincircumstances.47However,itismorecommonlyheldthatstrikepayisnotagift.48Inthe1975caseofMadonna J. Colwell,49theTaxCourtenunciatedsixrele-vantfactorsfordeterminingwhetherstrikepayshouldbeconsideredagift.Thesefactors50include

1. whethertherewasamoralorlegalobligationtomakethepayments; 2. whether the payments were made upon a consideration of the recipient’s

financialneed; 3. whetherthebenefitswouldcontinueduringthestrikeiftherecipientworked

elsewhere;

45 Supranote5. 46 TheUnitedStatesSupremeCourtaddressedthedefinitionof“gift”inCommissioner v.

Duberstein,363US278(1960). 47 Themostprominentofthedecisionsholdingthatstrikepayamountedtoagiftwasrendered

bytheUnitedStatesSupremeCourtinUnited States v. Kaiser,363US299(1960).ItshouldbenotedthatthecourtinKaiserwasconstrainedbythejury’sfindingattrialthattheassistancewasrenderedtoaclassofpersonsinthecommunityineconomicneedandthatthestrikepaywasmotivatedprimarilybygenerosityorcharity.AnothercasethatconsideredwhetherstrikepaywasagiftunderthetestarticulatedinDubersteinwasStone v. Lynch,325SE2d230(1985),wheretheNorthCarolinaSupremeCourtconcludedthatthestrikepayinquestionwasproperlyconsideredagiftforthepurposesofNorthCarolinaincometaxation.

48 See,forexample,Richard A. Osborne,69TCM1895(1995). 49 64TC584(1975). 50 AsdescribedinOsborne,supranote48,at1901.

438 n canadian tax journal / revue fiscale canadienne (2006) vol. 54, no 2

4. whethertherecipientwasamemberofthestrikingunion; 5. whether thepayments required the recipient toperformany strikeduties

suchaspicketing,ortowhatextenttherecipientwasunderamoralobliga-tiontopicket;and

6. whethertherewereanyrestrictions,suchaswhetherthebenefitswerere-strictedtobasicnecessities,orwhethertherecipienthadunfetteredcontroloveruseofthefunds.

United Kingdom

In the United Kingdom, annual subscription fees paid to specifically approvedorganizationsaredeductible fromemployment incomeunder section344of theIncomeTax(EarningsandPensions)Act2003(itepa).51AcurrentlistofapprovedorganizationsismaintainedbyhmRevenue&Customs(hmrc,formerlyInlandRevenue)andisavailableforpublicperusalontheInternet.52Whilethestatutoryframeworkseemstosuggestthattradeunionsmightbeabletogainhmrcapproval,few(ifany)tradeunionsappearontheapprovedorganizationslist.Thecurrentlistisdominatedbyprofessionalorganizations,suchasvarioussocietiesandorganiza-tionsforacademics,accountants,actuaries,architects,engineers,lawyers,medicalprofessionals,psychiatrists,psychologists,scientists,etc.

Historically,tradeunionsandemployees’associationshavebeenexplicitlyex-empted from income taxation—for example, by section 467 of the Income andCorporation Taxes Act 1988 (icta).53 However, trade unions are generally con-sidered to be companies for the purposes of the corporate tax.54 Under certainconditions,registeredtradeunionscanclaimrelieffromcorporatetaxinrespectofcertainnon-tradingincomeandchargeablegainsusedtomakeprovidentbenefitsavailable tomembers.55Registered tradeunionsare listedpursuant to theTradeUnionandLabourRelations(Consolidation)Act1992ortheIndustrialRelations(Northern Ireland) Order 1992.56 In practice, most trade unions are registeredunderoneoftheseacts.

51 IncomeTax(EarningsandPensions)Act2003(UK),2003,c.1.SeeUnitedKingdom,HMRevenue&Customs,“EIM32900—OtherExpenses:ProfessionalFeesandSubscriptions:AnnualSubscriptionstoApprovedBodies”(online:http://www.hmrc.gov.uk/manuals/eimanual/EIM32900.htm).

52 ThelistisavailablefordownloadfromHMRevenue&Customsathttp://www.hmrc.gov.uk/list3/list3.pdf.

53 IncomeandCorporationsTaxesAct1988(UK),1988,c.1.

54 UnitedKingdom,HMRevenue&Customs,“CT4710—TradeUnions”(online:http://www.hmrc.gov.uk/manuals/ct123manual/ct4710.htm).

55 UnitedKingdom,HMRevenue&Customs,“CT4711—TradeUnions:ProvidentBenefits—TitletoandExtentofRelief ”(online:http://www.hmrc.gov.uk/manuals/ct123manual/ct4711.htm).

56 TradeUnionandLabourRelations(Consolidation)Act1992(UK),1992,c.52andIndustrialRelations(NorthernIreland)Order1992,StatutoryInstrument1992no.807.SeeCT4710,supranote54.

the taxation of strike pay n 439

Strikepay isnot subject to tax in theUnitedKingdom.According tohmrc,section19(1)oftheicta(whichhasbeensupersededbytheitepa)didnotextendtotheinclusionofstrikepayinincome.“SomeTradeUnionsmakepaymentstomemberswhoareonstrike.Suchpaymentsarenotemolumentsfromtheemploy-mentandarenottaxable.”57Apparentlytheitepahasintroducednosubstantivechangestothelawregardingthetaxationofstrikepay.

Althoughstrikepayisnotdirectlysubjecttotax,itisindirectlytaxablebecauseitiscountedasincomeforthepurposeoftheincome-testedworkingtaxcredit.58ThisisunlikethesituationinCanada,wherestrikepayisneitherdirectlytaxablenorcountedasincomeincalculatingtheCanadachildtaxbenefitandthegoodsandservicestaxcredit.

New Zealand

InNewZealand,unionduesareconsideredanemployment-relatedexpense.TheIncomeTaxAct2004containsthefollowing“employmentlimitation”ruleinrespectofthedeductionofemployment-relatedexpenses:“Apersonisdeniedadeductionforanamountofexpenditureorlosstotheextenttowhichitisincurredinderiv-ingincomefromemployment.”59Thereisnospecificprovisionthatoverridesthisgeneralprovisiontoauthorizeadeductionforuniondues.

Asunincorporatedassociations,tradeunionsinNewZealandaregenerallytaxedasindividualsundertheIncomeTaxAct2004,andthereforeareassessabletotaxonincomeattributabletotheinvestmentofunionfunds.

NewZealand’sapproachtothetaxationofstrikepayisnotperfectlyclear,butamountsreceivedasstrikepayarelikelynotassessable.Inordertobeassessable,strikepaywouldhavetobecharacterizedas“income”accordingtotheapplicabletest. Section ca 1(2) of the Income Tax Act 2004 provides that in addition toamountsspecifiedinthelegislationasincome,areceiptwillbeconsideredincomegenerallyifitis“incomeunderordinaryconcepts.”Tobecharacterizedasincomeunder“ordinaryconcepts,”strikepaywouldhavetobereceivedregularly(forex-ample,weeklyorbi-weekly)andbeexpected.However,ifthepaymentwasalumpsumor if theunionmadein-kindprovisionforstrikers, the“ordinaryconcepts”requirement would probably not be satisfied. A further argument against thesepaymentsbeingconsideredincome,accordingto“ordinaryconcepts,”isthattheunionisreturningunionduespaidbyitsmembers.Giventhatemployeesarenotallowedadeductionforunionduesexante, it isnotunlikelythatthisargumentwouldbedecisive.

57 UnitedKingdom,HMRevenue&Customs,“SE06500—EmolumentsofEmployeesandOfficeHolders:StrikePayfromTradeUnions”(online:http://www.hmrc.gov.uk/manuals/senew/SE06500.htm).

58 CharteredInstituteofTaxation,“NewTaxCredits:QandAwithInlandRevenue”(online:http://www.tax.org.uk/showarticle.pl?id=1780).

59 NewZealandIncomeTaxAct2004,2004no.35,asamended,sectionDA2(4).

440 n canadian tax journal / revue fiscale canadienne (2006) vol. 54, no 2

DAtA

SinceourultimategoalistoaddressalternativestocurrentCanadiantaxpolicyonstrikepay,theabovelegalanalysisneedstobesupplementedwithdataonstrikepayamountsandtherevenuecostofthecurrentCanadiantaxtreatmentofstrikepay.

Strikepayisgenerallyconcernedwithprovidingworkersandtheirfamilieswithday-to-daysustenanceoverthecourseofagivenlabourdispute.Strikepayisnotusuallyconcernedwithincomereplacementassuch.Intheabsenceofcomprehen-sivecurrentdataonstrikepay,wemaycitesomerecentindividualfigures,rangingfrom$40to$350perweek:theCanadianAutoWorkersUnionpays$150perweek,escalatingto$200afterthefourthweek;60theCanadianUnionofPublicEmploy-eespays$200perweek,startingonthetenthdayofthestrike,althoughindividualdivisionsorlocalsmaysupplementthisamount;61theCanadianMediaGuildpaysus $200,escalatingtous $300afterthefourthweek;62theUnitedFood&Com-mercialWorkersUnionpaysatleast$240startingthesecondweekofastrike,withtheobjectiveofpayingatleast40percentofpre-strikeearnings;63theCommuni-cations,EnergyandPaperworkersUnionofCanadapays$250perweek(whichitsaidwasthehighestinCanada),althoughthiselevatedratedoesnotgenerallyapplyuntilthefourthweekofa labourdispute;64andthebcTeachersFederationpaid$350perweekinthe2005strike.65

Thefederalrevenuecost(taxexpenditureamount)ofthenon-taxationofstrikepay has not been officially estimated since 1992, when it was calculated in thegovernmentofCanada’s taxexpenditurereports tobe$9million.66However,by

60 CanadianAutoWorkersUnion,“MUSASurvey:UpdatedCAWResponses”(online:http://www.caw.ca/jointheCAW/campaigns/musa/survey.asp).

61 CanadianUnionofPublicEmployees,“SupporttoMembersonStrike,”September23,2003(online:http://cupe.ca/www/nationalstrikefundcampaigns/5977).

62 CanadianMediaGuild,“Negotiations”(online:http://www.cmg.ca/cbcnegsstrikepayEN.html).

63 UnitedFood&CommercialWorkersUnionLocal247,“InformationNotice,”May1,2003(online:http://ufcw247.com/global_news_template.cfm?page=05012003144453).

64 SeeCEPNationalUnion,“InformationforAllCEPMembers”(apparentlywritteninMay2004)(online:http://www.cep1129.ca/cepNews/Dues%20Increase.htm);andCEPNationalUnion,“Policy614:CEPDefenseFundRulesandStrikeAuthorizationProcedures”(online:http://www.cep.ca/policies/policy_614_e.pdf ),paragraph7.3.

65 CBCNews,“B.C.TeachersFaceLossofStrikePaybutNoFine,”October13,2005(online:http://www.cbc.ca/story/canada/national/2005/10/13/strike-bc-teachers051013.html).

66 Canada,DepartmentofFinance,Government of Canada Tax Expenditures 1995(Ottawa:DepartmentofFinance,1996),24.ThesefigureswerecalculatedbytheDepartmentofFinancewithreferencetoStatisticsCanada’sannualreportsonpartIIoftheCorporationsandLabourUnionsReturnAct(CALURA)(StatisticsCanadacatalogueno.71-202).StatisticsCanadastoppedcollectingtheCALURAinformationseriesin1995.From1997onward,StatisticsCanadahascollectedinformationsimilartothatcollectedunderpartIIofCALURAusingaredesignedmonthly“LabourForceSurvey”;however,theredesignedsurveydoesnotcollectstrikepayinformation.

the taxation of strike pay n 441

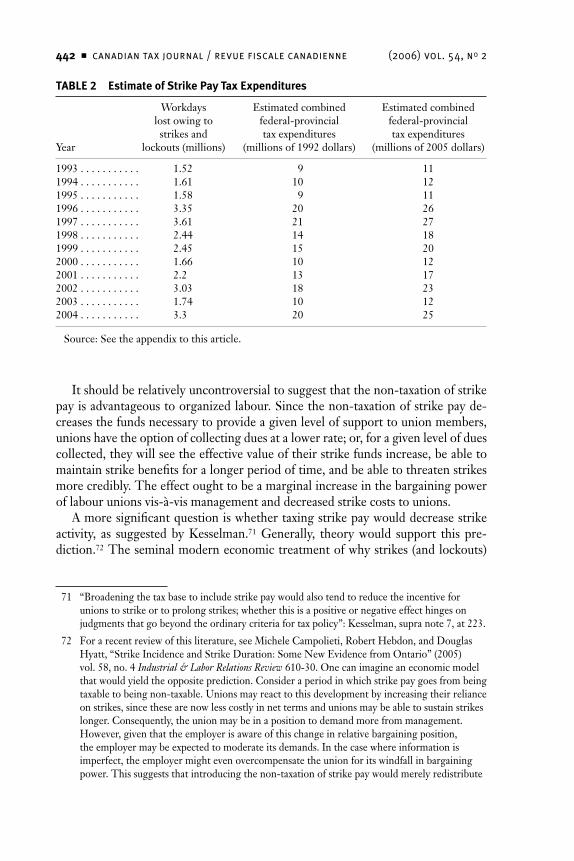

examiningtherelationshipof1988-1992taxexpenditurestoworkdayslostowingtostrikesandlockoutsinthatperiod,post-1992federaltaxexpenditureamountscanbeestimatedfrompost-1992figuresforworkdayslost.Provincialtaxexpenditurescanthenbeestimatedfromtherelationshipoffederaltoprovincialrevenues.Forfulldetails,seetheappendixtothisarticle.

Thesecondandthirdcolumnsoftable2providetheresultsofthisanalysis.Theaveragecombinedfederal-provincialtaxexpendituresrelatingtostrikepayareintherangeof$15-25millionin2005dollars,ofwhichapproximately60percentistherevenueforgonebythefederalgovernmentandtheremaining40percentbyalltheprovincialgovernmentscombined.

Foranygivenyear,theestimatesofthestrikepaytaxexpendituresareapttobesomewhatunreliablebecauseofthelargeyear-to-yearvariationinworkdayslostowingtostrikesandlockouts.Thefirstcolumnoftable2showsthatworkdayslostmaybealmostdoubledorhalvedfromoneyeartothenext.

Thereisalsoconsiderablevariationbycountryinthereportedfrequencyanddurationoflabourdisputes,partlyformethodologicalreasonsrelatingtothewaythedataarecollected,butalsoforvarioussocial,cultural,andeconomicreasons.67AccordingtostatisticscompiledbytheInternationalLabourOrganization,Canadawitnessedatotalof266strikesandlockoutsin2003,involvingalmost80,000work-ers.These interruptions accounted for a cumulative lossof1.74milliondaysofwork.68Bywayofcomparison,intheUnitedStatesin2003,therewere14strikesorlockoutslastingatleastonedayorshiftandinvolvingmorethan1,000workers,leadingto4.08millionlostworkdays.69In2003,theUnitedKingdomlost499,100daysofworkfrom133strikesandlockouts,andAustralialost439,400daysfrom643workstoppages.70

EcO nOmic EffEc t s

Inconsideringwhethertotaxstrikepay,onewouldliketoknowthebroadereco-nomiceffects,includingwhomthecurrentexemptionbenefitsorharms,andtowhatdegree.Althoughdetailedmodellingandempiricalexaminationofthesefactorsarewellbeyondthescopeof thiscommentary,a fewremarks indicatingthestateofknowledgeinthisareamaybeuseful.

67 Variationsattributedtosocialandculturalreasonsshouldnotbegivenundueweight,however,sincerecentempiricalworksuggeststhatthereisconsiderableinterdependenceinstrikeactivityamongOECDcountries.SeeL.J.PerryandPatrickJ.Wilson,“AnAnalysisofInternationalLinkagesinStrikeActivity”(2003)vol.11,no.2International Journal of Employment Studies47-74.

68 Thesefiguressomewhatunderestimatetheactualnumberofworkstoppagesandworkersinvolved,sincetheyincludeonlystoppageslastingforatleasthalfofaworkdayandresultinginthecumulativelossof10ormoredaysofwork.CompletestatisticsareavailablethroughtheInternationalLabourOrganizationLaborstaDatabase(online:http://laborsta.ilo.org/).

69 USdataonsmaller-scaleworkstoppagesarenotavailable.

70 StatisticsfromtheInternationalLabourOrganizationLaborstaDatabase,supranote68.

442 n canadian tax journal / revue fiscale canadienne (2006) vol. 54, no 2

Itshouldberelativelyuncontroversialtosuggestthatthenon-taxationofstrikepayisadvantageoustoorganizedlabour.Sincethenon-taxationofstrikepayde-creasesthefundsnecessarytoprovideagivenlevelofsupporttounionmembers,unionshavetheoptionofcollectingduesatalowerrate;or,foragivenlevelofduescollected,theywillseetheeffectivevalueoftheirstrikefundsincrease,beabletomaintainstrikebenefitsforalongerperiodoftime,andbeabletothreatenstrikesmorecredibly.Theeffectoughttobeamarginalincreaseinthebargainingpoweroflabourunionsvis-à-vismanagementanddecreasedstrikecoststounions.

Amoresignificantquestioniswhethertaxingstrikepaywoulddecreasestrikeactivity, as suggested by Kesselman.71 Generally, theory would support this pre-diction.72Theseminalmoderneconomictreatmentofwhystrikes(andlockouts)

tAblE 2 Estimate of Strike Pay Tax Expenditures

Workdays Estimatedcombined Estimatedcombined lostowingto federal-provincial federal-provincial strikesand taxexpenditures taxexpendituresYear lockouts(millions) (millionsof1992dollars) (millionsof2005dollars)

1993........... 1.52 9 111994........... 1.61 10 121995........... 1.58 9 111996........... 3.35 20 261997........... 3.61 21 271998........... 2.44 14 181999........... 2.45 15 202000........... 1.66 10 122001........... 2.2 13 172002........... 3.03 18 232003........... 1.74 10 122004........... 3.3 20 25

Source:Seetheappendixtothisarticle.

71 “Broadeningthetaxbasetoincludestrikepaywouldalsotendtoreducetheincentiveforunionstostrikeortoprolongstrikes;whetherthisisapositiveornegativeeffecthingesonjudgmentsthatgobeyondtheordinarycriteriafortaxpolicy”:Kesselman,supranote7,at223.

72 Forarecentreviewofthisliterature,seeMicheleCampolieti,RobertHebdon,andDouglasHyatt,“StrikeIncidenceandStrikeDuration:SomeNewEvidencefromOntario”(2005)vol.58,no.4Industrial & Labor Relations Review610-30.Onecanimagineaneconomicmodelthatwouldyieldtheoppositeprediction.Consideraperiodinwhichstrikepaygoesfrombeingtaxabletobeingnon-taxable.Unionsmayreacttothisdevelopmentbyincreasingtheirrelianceonstrikes,sincethesearenowlesscostlyinnettermsandunionsmaybeabletosustainstrikeslonger.Consequently,theunionmaybeinapositiontodemandmorefrommanagement.However,giventhattheemployerisawareofthischangeinrelativebargainingposition,theemployermaybeexpectedtomoderateitsdemands.Inthecasewhereinformationisimperfect,theemployermightevenovercompensatetheunionforitswindfallinbargainingpower.Thissuggeststhatintroducingthenon-taxationofstrikepaywouldmerelyredistribute

the taxation of strike pay n 443

occurcomesfromHicks,whopostulatedthatworkstoppagesarearesultoffaultyassessmentsofcostsandbenefitsbybothsides;thatis,strikesaretheproductofmutualmistakesandarethereforegenerallywasteful.73Thismodelandmorerecenteconomicmodels74predictthat“ifacertainfactororvariableincreasesthecosttoonlyoneoftheparties...incidenceanddurationarereducedeventhoughthecostofstrikesishigherforoneparty,sincethecosttothatpartyisacomponentofthetotalcosttobothparties.”75Agovernmentmovetotaxstrikepaywouldconstituteexactlysuchacostincrease.Also,inoneofthefewworkstoconsidertheissueofstrikepaydirectly,Goerkedevelopedatheoreticalmodelindicatingthattheavail-abilityofstrikepaywillgenerallyincreasetheincidenceofstrikes.76Ontheotherhand,theeffectsoftaxingstrikepayarelessclearinbehaviouralmodelsonstrikes,whichfocusonnon-economicvariables.77

Althoughnoempiricalworkhasexaminedtheeffectsofstrikepaytaxationonstrikeactivity,thebasicideathatanincreaseincoststoonepartydecreasesstrikeactivityhasbeentestedinthecontextofwhetherprovidingemploymentinsurancebenefits(unemploymentinsuranceintheUnitedStates)tostrikersincreasesstrikeactivity.Theevidenceisdecidedlymixed.Hutchens,Lipsky,andSternhavefounda positive correlation between strike activity and the availability of governmentemploymentinsuranceprograms(whichwouldpresumablydecreasestrikecosts);

wealthbetweenthetwoparties—thatis,unionswouldreceiveabiggerpartofthepie—butthatanincreasedpreferenceforstrikesonthepartofunionsmaybecompensatedforbyacountervailingdecreasedpreferenceforstrikesonthepartofemployers.

73 JohnR.Hicks,The Theory of Wages(London:MacMillan,1932),andJohnR.Hicks,The Theory of Wages,2ded.(NewYork:St.Martin’sPress,1966),specifically136-57.Kaufmanhasnotedthat“Hicks’stheoryhascometodominateeconomictheorizingonstrikes”:BruceE.Kaufman,“ResearchonStrikeModelsandOutcomesinthe1980s:AccomplishmentsandShortcomings,”inDavidLewin,OliviaS.Mitchell,andPeterD.Sherer,eds.,Research Frontiers in Industrial Relations and Human Resources(Madison,WI:IndustrialRelationsResearchAssociations,1992),77-83,at82.

74 Theseincludeasymmetricinformationmodels(inwhichunionsdifferentiatebetweenfirmsbyforcingthemtochoosebetweenlabourconcessionsandstrikes,onthetheorythatfirmsthatarehighlyprofitablearelikelytobemorewillingtomakesuchconcessions)andjointcostmodels(inwhichthegreaterthejointcostsofastrike,thegreateristheincentivetocompromisetoavoidtheexpensesassociatedwithaworkinterruption).

75 MorleyGunderson,AllenPonak,andDaphneG.Taras,Union-Management Relations in Canada,4thed.(Toronto:Addison-WesleyLongman,2001),331.

76 LaszloGoerke,“StrikePayandEmployers’StrikeInsurance”(2000)vol.51,no.3Metroeconomica284-303.

77 SeeJohnGodard,“StrikesasCollectiveVoice:ABehavioralAnalysisofStrikeActivity”(1992)vol.46,no.1Industrial & Labor Relations Review161-75.Godardarguesthatstrikesshouldberegardedas,primarily,theexerciseofcollectivevoiceandanexpressionofworkerdiscontent.Usingdatafrom1980-81,Godardfindsthatmanagerialpractices,operationssize,productmarketstructure,andunionpolitics,amongotherfactors,significantlyinfluenceddayslostowingtostrikeactivity.

444 n canadian tax journal / revue fiscale canadienne (2006) vol. 54, no 2

butanumberofresearchers,mostnotablyMaki,Ahmed,andIngram,Metcalf,andWadsworth,havefailedtoconfirmthisfinding.78

Thebroadesteconomicquestioniswhetherthenon-taxationofstrikepayim-provesbargainingoutcomesforunions,andfurther,whetherthisincreasessocietalwelfare.Clearlythisisunlikelytoberesolvedanytimesoon,asthebroadquestionoftheeffectofunionsontheeconomyisverymuchindebate.Inareviewoftheliteratureinthisarea,Kuhnconcludesonlythatthesocialwelfareimpactofunion-ization isuncertain,andthatallocative inefficienciescausedbyawagewedgeorstrikesareunlikelytocostmorethanaquarterpercentagepointofgrossdomesticproduct.79Similarly,Benjamin,Gunderson,andRiddellnotethat“evidenceontheaverageeconomy-wideimpactisinconclusive.”80

Ifthereisaconclusiontobedrawnfromareviewoftheeconomicliterature,itisthatalthoughthenon-taxationofstrikepayisatleastmarginallyabenefittoorganizedlabour,thebenefitisemphaticallysmall,thedirecteffectsofincreasedunionbargainingpowerontheincidenceanddurationofstrikesareunclear,andthebroaderoveralleffectsonsocialwelfareareuncertain.

A n A lYsis O f P O lic Y A ltErn Ati v E s

Onhorizontalequitygrounds,strikepayshouldbetaxable.AsKesselmannotes,

notonly is strikepaya receipt indirectly related toemployment services, it is alsofinancedoutofemployees’tax-deductibleuniondues.Hence,itisinconsistentwithbothhorizontalequityandthetaxdeductibilityofunionduestoomitstrikepayfromtaxableincome.81

Similarly,considerationsofeconomicefficiencywouldarguefortaxingstrikepay,sincethecurrentnon-taxationmaybeinducingunionstopaylargeramountsofstrikepaythantheyotherwisewould.82Argumentsforadeliberateincentive,such

78 SeeRobertM.Hutchens,DavidB.Lipsky,andRobertN.Stern,Strikers and Subsidies: The Influence of Government Transfer Programs on Strike Activity(Kalamazoo,MI:UpjohnInstituteforEmploymentResearch,1989);RobertM.Hutchens,DavidB.Lipsky,andRobertN.Stern,“UnemploymentInsuranceandStrikes”(1992)vol.13Journal of Labor Research337-54;D.R.Maki,“TheEffectoftheCostofStrikeActivityontheVolumeofStrikeActivity”(1986)vol.39,no.4Industrial & Labor Relations Review552-63;SyedM.Ahmed,“TheEffectsoftheJointCostofStrikesinCanadianManufacturingIndustries—ATestoftheReder-Neumann-KennanTheory”(1989)vol.21,no.10Applied Economics1353-67;andPeterIngram,DavidMetcalf,andJonathanWadsworth,“StrikeIncidenceinBritishManufacturinginthe1980s”(1993)vol.46,no.4Industrial & Labor Relations Review704-17.

79 PeterKuhn,“UnionsandtheEconomy:WhatWeKnow;WhatWeShouldKnow”(1998)vol.31,no.5Canadian Journal of Economics1033-56.

80 DwayneBenjamin,MorleyGunderson,andW.CraigRiddell,Labour Market Economics,5thed.(Toronto:McGraw-HillRyerson,2002),495.

81 Kesselman,supranote7,at223.

82 Kesselman,ibid.,at238,table6,citeseconomicefficiencyasanadditionalreasontotaxstrikepay.

the taxation of strike pay n 445

astheexternalityreasonsgivenforsubsidizingresearchanddevelopmentorCan-adianfilms,would appear tobe absent in this context.Even theDepartmentofFinanceseemsunabletofindareasonforthecurrentpolicy;thelistingofgoalsoftaxexpendituresintheannualtaxexpenditureaccountsdoesnotrefertoanygoaljustifying thenon-taxationof strikepay,but simplyrestates the legalconclusionreachedinFriesthatstrikepayisnot“income...fromasource.”83

Oneargumentthatcouldbeadvancedfornottaxingstrikepayisverticalequity.Strikepayundoubtedlyismainlyreceivedbylow-andmiddle-incometaxpayers.84Also,althoughpracticesofdifferentunionsvary,itiscommonforstrikepaytobedeterminedonthebasisofaformulathatgaugesneedratherthanincomereplace-mentoranequalamountpermember.Forexample,thestrikepayinsomecaseswillbelargerforpeoplewithchildrentosupport,orforthosepeoplewhohavenotbeenabletofindpart-timejobs.Inthatrespect,strikepaycouldbesaidtobeclosertoadistributionofbenefitsor“gifts”than“income.”85ThereissomesupportforthispositioninusjurisprudenceandintheopinionsoftheAustraliantaxauthori-ties,asdescribedabove.86

Onedifficultywiththeverticalequityargumentisthatnotallstrikepayisneed-based.Forexample,thefactsoftheFriescasesuggestedfullincomereplacement;andduringtherecentnhllabourdispute,thenhlpamadelargestipendpaymentsofuptous $10,000permonthtoitsplayers.Unfortunately,thereappeartobenodatatodeterminewhereonthiscontinuumbetweenneed-basedpaymentsandin-comereplacementmoststrikepayfalls.Morefundamentally,however,exemptingparticulartypesofincomerunscountertohorizontalequityandefficiencygoalsofthetaxsystem,andthereexistredistributionmechanisms,suchas increasingthebasicexemption,thatdonothavethesedrawbacks.87

83 Atleastonewriterhasdescribedthisexplanationas“puzzling.”SeeAlanMacnaughton,CurrentTaxReadingfeature(1998)vol.46,no.4Canadian Tax Journal929-39,at930-31.

84 Kesselman,supranote7,at221.

85 Thisobservationcouldbeusedtosupportalegalargumentfornon-taxationofstrikepay,eitheronthebasisofcharacterizingstrikepayassocialassistanceandeffectivelyexemptunderparagraph110(1)(f )oftheITA,oronthegroundsthatstrikepayisclosertothesustenancepoleandnot“income...fromasource.”

86 ThecriteriafromColwell,supranote49andtheaccompanyingtext,arehelpfulindeterminingwhereanygivensetoffactsisapttobeonthecontinuum.TheneedendofthecontinuumalsosupportstheconclusionoftheATOthatstrikepaywillnotordinarilybeassessablebecauseitisnot“income.”Seesupranote36andtheaccompanyingtext.

87 Kesselman,supranote7,at221,notesthisproblemforstrikepayandobservesthatitalsooccurswithexclusionsfromthetaxbaseforgovernmentcashtransferpaymentsandemployer-paidhealthbenefits.Also,StevenShavellandLouisKaplowofHarvardLawSchoolhavearguedinfavourofredistributingthroughtheincometaxratherthandirectlyregulatinginawaythatinefficientlyseekstopromotedistributivejustice.Putsimply,theideaistopromoteefficiency—thatis,maximizethesizeofthepie—andonlythentosplitupthepieusingtheincometax.SeeLouisKaplowandStevenShavell,“WhytheLegalSystemIsLessEfficientThantheIncomeTaxinRedistributingIncome”(1994)vol.23,no.2The Journal of Legal Studies667-81.

446 n canadian tax journal / revue fiscale canadienne (2006) vol. 54, no 2

Asecondargumentfornottaxingstrikepayistheincreaseincompliancecoststhattaxationwouldproduce.Thereareseveralreasons:manyunionsarenotsetuptoproducetaxslipsforlargenumbersofpeople;somepaymentsarein-kindandhavevaluationproblems;theamountoftaxableincomeperworkercouldbequitesmall;and,sincestrikesareinfrequentforanyoneunionlocal,theremightnotbemuchopportunityforreductionofcompliancecoststhroughlearning.Hence,theadditionalcompliancecostsfacedbyunionsmightrepresentanunacceptablepro-portionoftheassociatedtaxrevenues.Onesourcehassuggestedthatifstrikepayweretobecometaxable,theoutcrywouldbeatleastasmuchforthecomplianceburdenasfortheincreasedamountoftaxpayable.However,unionsalreadygener-allywithholdandremitincometaxforemployeesontheirpayroll,andpresumablycouldsimilarlywithholdtaxfrompaymentstostrikingworkerswithsomeefficacy.

Ifstrikepayistobetaxed,somepracticalissuesneedtobeaddressed.Inparticu-lar,unionssometimespayemployersorinsurancecompaniesforthecontinuationofemploymentbenefits,suchashealthanddentalplansorlifeinsurance,forthedurationof thestrike.Presumably,suchpaymentsshouldbenon-taxable, justastheywouldbeiftheemployerhadpaidtheamounts.Similarly,whereemploymentbenefitsaredisruptedbyastrike,paymentsbyaunioninlieuofdeathbenefitsfromemployer-providedlifeinsurancemightalsobeappropriatelyexemptedsincetheywouldreplacenon-taxableamounts.Finally,specialstrikelevies,whichcurrentlyarenon-deductiblebecausetheyarenot“annualdues,”shouldbecomedeductibletoavoiddoubletaxation.88

Onealternativetotaxationofstrikepayistoaddresstheproblemonthefrontend.Morespecifically,theremightbeareduceddeductionavailableforunionduesbasedontheproportionofunionduespaidintostrikefundsexante.Theideaisthatjustasspecialstrikeleviesarenotdeductible,theproportionofannualduesthatmakesitswayintostrikefundsshouldalsobenon-deductible.Thisnon-deductibleproportioncouldbecalculatedonaunion-by-unionandyear-by-yearbasis(withaone-or two-year lag); but for simplicity, a betteroptionwouldbe to create aCanada-widenon-deductibleproportionbasedon theaverageproportionofan-nual dues contributed to strike funds, which might be in the neighbourhood of5percent.89Professionalfees,whicharealsodeductible,wouldpresumablyretainafulldeductionsincenoprofessionsmaintainstrikefunds.Thisfront-endapproachisattractiveinthatitsolvesthecompliancecostproblem.However,itcreatesthewrongincentivesinthataCanada-widenon-deductibleproportioncouldnotaffectindividualunions’decisionsonstrikepay,andhencestrikepaywouldnotbetaxableatthemargin.

88 Seethecasescitedinnote13,supra.

89 Oneestimateofthisnumberistheratioofthefederaltaxexpenditureforstrikepay(say,$12million)tothetaxexpenditureforunionandprofessionaldues($585millionfor2004),whichis2percent.However,thisistoolowbecausethedenominatorinappropriatelyincludesprofessionaldues.

the taxation of strike pay n 447

AsecondalternativeistofollowtheapproachofFinland,whichexemptsthefirst€16(approximately$22)90receivedinstrikepayperday.Strikepayabovethislevelisincludedinincome.91AsimilarpolicyinCanadawouldexemptthefirst$150ofstrikepayperweek.Thiswouldexemptmoststrikepay,whichseldomexceeds$250perweek.Thespecialadjustmentsrequiredforthefulltaxationofstrikepaymightnotbenecessary,becauseitwouldapplyinonlyaverylimitednumberofsituations.Thisapproachwouldsolvethecompliancecostproblemsinceonlyafewpeoplewouldhaveataxableamount.However, itmightnotbeperceivedassolvingtheverticalequityproblem.The$150perweekexemptiontranslatesinto$7,800peryear,whichislessthanthebasicpersonalamount.Also,taxationabovetheexemptamountwould raise very little revenue, and thehorizontal equity and efficiencyproblemsnotedabovewouldnotbesolvedformoststrikepayamounts.

Althoughthisisnotataxissue,agovernmentcontemplatingthetaxationofstrikepaymightwishtoconsiderthechangeinthecontextoftheoverallroleofthestatein labourdisputes.ComparingCanadaandtheUnitedStates, theUnitedStatestaxesstrikepay,whileCanadadoesnot;butCanadianemploymentinsurancerulesdenybenefitstoworkerstakingpartinanytypeoflabourdispute,92whileusun-employmentinsurancerulesinmanystatesprovidebenefitstoworkerstakingpartincertainkindsoflabourdisputes,suchaslockouts.93Hence,amovetotaxstrikepayinCanadamightbeseenasremovingabenefitthatcompensatesforthelessfavourabletreatmentofemploymentinsurance.

cO nclusiO n

Thetaxtreatmentofuniondues,labourorganizations,andstrikepayinCanadaraisesbothhorizontalequityandefficiencyconcerns,sinceitprovidesamechanismthroughwhichemploymentincomecanreturntounionmemberswithoutincurringincometax liability.TheUnitedStates, theUnitedKingdom,andNewZealandhaveadoptedconsiderably lessgenerousapproaches to the implicated taxpolicyissuesthanCanada,althoughAustraliahassimilarrules.Ouranalysisindicatesthattheannualtaxexpendituresinthiscountryarecurrentlyintheneighbourhoodof$15millionto$25millionperyear,withabout60percentattributabletofederaltaxexpendituresandtheremaining40percenttotaxexpendituresattheprovincial

90 Convertedat€1=$1.36647,thereportedexchangerateathttp://www.xe.com/onNovember27,2005.

91 SeeFinland,MinistryofFinance,Taxation in Finland 2001(Helsinki:MinistryofFinance,2001),25(online:http://www.vm.fi/tiedostot/pdf/fi/15626.pdf ).In2001,theamountexemptedwas€12.Ithassincebeenincreasedto€16.

92 EmploymentInsuranceAct,SC1996,c.23,asamended,section36.SeethejudicialinterpretationsofthissectionprovidedbytheOfficeoftheUmpire(online:http://www.ei-ae.gc.ca/en/umpire/jud_interpretations/labour_1.shtml).

93 SeeHutchensetal.,supranote78,andGillianLester,“UnemploymentInsuranceandWealthRedistribution”(2001)vol.49,no.1UCLA Law Review335-93,at350,note56.

448 n canadian tax journal / revue fiscale canadienne (2006) vol. 54, no 2

level.Admittedly,taxingstrikepayraisesverticalequityconcernsinthatthesepay-mentsarereceivedmostlybylow-andmiddle-incomepeople.Compliancecostsarealsoanissue,becausealargenumberofpeoplecouldbetaxedonsmallamounts.Hence,thealternativesofpartiallydenyingthedeductibilityofunionduesortaxingonlystrikepayamountsaboveathresholddeserveseriousconsideration.

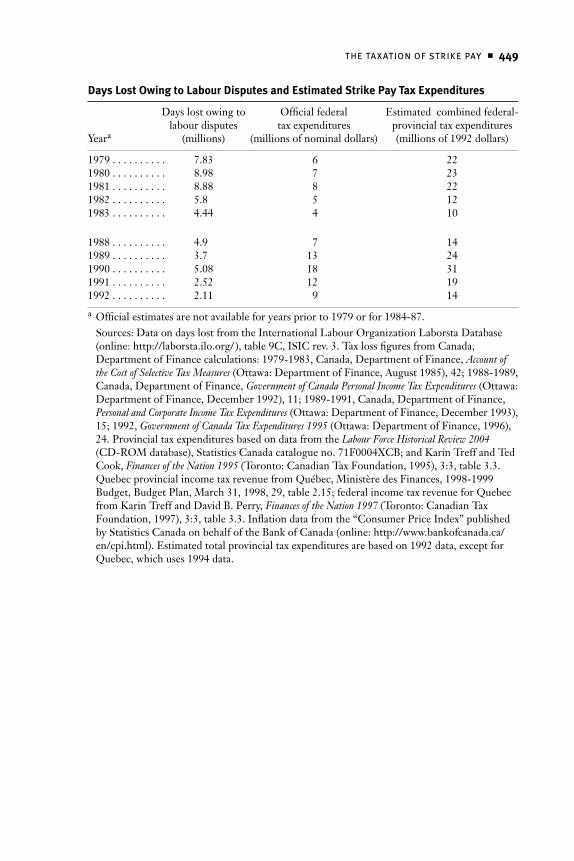

A PPEnDi x E s tim Ating s triK E PAY tA x E x PEnDit urE s fO r 19 93 tO 20 0 4

Theofficialfederaltaxexpenditureestimatesarepresentedinthetablebelow.Theunofficialestimatesareourown.TheyarebasedonfiguresfromtheLabour Force Historical Review 200494relatingtothenumberofdayslostowingtolabourdisputesineachprovince, theratioofprovincial to federal incometax revenues,and thefederaltaxexpenditureestimatesoftheDepartmentofFinance.95

Astraightforwardwaytomarshaltheinformationinthetable,inordertobetterestimatethemissingfederaltaxexpenditurefiguresfor1993to2004,istocalculateanaveragefederaltaxexpenditureperlostworkdayfor1988to1992($5.92in1992dollars),convertthisintocurrentdollars,andthenmultiplybythecurrentnumberoflostworkdays.Thecorrespondingprovincialexpendituresareestimatedinthesameway.Theresultsofthisprocedurearereportedintable2inthemainbodyofthearticle.

Onevaliditycheckonthedataistocalculatetheimpliedaveragestrikepay.A$5.92taxexpenditureperlostworkdayimplies$21.14instrikepayperday,assuminga28percentaveragemarginaltaxrate.Adjustingthisforinflationandmultiplyingby5producesaverageweeklystrikepayof$136in2005dollars.If10to30percentofunionsdonotissuestrikepay,thetrueaverageofpositivestrikepayamountsap-proximates$150to$195perweek.Thesefiguresseemreasonableascomparedwiththeindividualunionfigurescitedinthe“Data”sectionofthearticle,particularlyifitisassumedthatlowerstrikepayamountsarelesslikelytobepublicizedandsoarenotincludedinthislist.

94 StatisticsCanada,Labour Force Historical Review 2004(CD-ROMdatabase),StatisticsCanadacatalogueno.71F0004XCB.WhilethesestatisticsvaryinmagnitudefromtheLaborstadata,thetrendsaresimilar.

95 TaxrevenuedatagatheredfromKarinTreffandDavidB.Perry,Finances of the Nation 2004(Toronto:CanadianTaxFoundation,2004),chapter3.Therevenuesutilizedarefromthe2002taxationyear.Itisassumedthattherehasbeennosignificantchangeintheratioofprovincialtaxrevenuestofederaltaxrevenueswithinaprovincesincetheearly1990s.

the taxation of strike pay n 449

Days Lost Owing to Labour Disputes and Estimated Strike Pay Tax Expenditures

Dayslostowingto Officialfederal Estimatedcombinedfederal- labourdisputes taxexpenditures provincialtaxexpendituresYeara (millions) (millionsofnominaldollars) (millionsof1992dollars)

1979.......... 7.83 6 221980.......... 8.98 7 231981.......... 8.88 8 221982.......... 5.8 5 121983.......... 4.44 4 10

1988.......... 4.9 7 141989.......... 3.7 13 241990.......... 5.08 18 311991.......... 2.52 12 191992.......... 2.11 9 14

a Officialestimatesarenotavailableforyearspriorto1979orfor1984-87.Sources:DataondayslostfromtheInternationalLabourOrganizationLaborstaDatabase(online:http://laborsta.ilo.org/),table9C,ISICrev.3.TaxlossfiguresfromCanada,DepartmentofFinancecalculations:1979-1983,Canada,DepartmentofFinance,Account of the Cost of Selective Tax Measures(Ottawa:DepartmentofFinance,August1985),42;1988-1989,Canada,DepartmentofFinance,Government of Canada Personal Income Tax Expenditures(Ottawa:DepartmentofFinance,December1992),11;1989-1991,Canada,DepartmentofFinance,Personal and Corporate Income Tax Expenditures(Ottawa:DepartmentofFinance,December1993),15;1992,Government of Canada Tax Expenditures 1995(Ottawa:DepartmentofFinance,1996),24.ProvincialtaxexpendituresbasedondatafromtheLabour Force Historical Review 2004(CD-ROMdatabase),StatisticsCanadacatalogueno.71F0004XCB;andKarinTreffandTedCook,Finances of the Nation 1995(Toronto:CanadianTaxFoundation,1995),3:3,table3.3.QuebecprovincialincometaxrevenuefromQuébec,MinistèredesFinances,1998-1999Budget,BudgetPlan,March31,1998,29,table2.15;federalincometaxrevenueforQuebecfromKarinTreffandDavidB.Perry,Finances of the Nation 1997(Toronto:CanadianTaxFoundation,1997),3:3,table3.3.Inflationdatafromthe“ConsumerPriceIndex”publishedbyStatisticsCanadaonbehalfoftheBankofCanada(online:http://www.bankofcanada.ca/en/cpi.html).Estimatedtotalprovincialtaxexpendituresarebasedon1992data,exceptforQuebec,whichuses1994data.