Embed Size (px)

Citation preview

GLOBAL COMPACT NETWORK VIETNAM Office for Business Sustainable Development (SD4B)4th floor, VCCI building9 Dao Duy Anh Street, HanoiTel +84 4 3577 2700Fax +84 4 3577 2699 Email: [email protected]: www.globalcompactvietnam.org

THE TEN PRINCIPLES

HUMAN RIGHTS

Principle 1: Businesses shouldsupport and respect the protectionof internationally proclaimedhuman rights; and Principle 2: make sure that theyare not complicit in human rightsabuses.

LABOUR STANDARDS

Principle 3: Businesses shoulduphold the freedom of associationand the effective recognition ofthe right to collective bargaining; Principle 4: the elimination of allforms of forced and compulsorylabour; Principle 5: the effective abolitionof child labour; and Principle 6: the elimination ofdiscrimination in respect ofemployment and occupation.

ENVIRONMENT

Principle 7: Businesses shouldsupport a precautionary approachto environmental challenges; Principle 8: undertake initiatives topromote greater environmentalresponsibility; and Principle 9: encourage thedevelopment and diffusion ofenvironmentally friendlytechnologies.

ANTI-CORRUPTION

Principle 10: Businesses shouldwork against corruption in all itsforms, including extortion andbribery.

1

2

3

4

56

7

8

9

10

GLOBAL COMPACTNETWORK VIETNAM

The GCNV, launched in 2007, is acutting edge initiative developed inpartnership between the VietnamChamber of Commerce and Industry(VCCI) and the United Nations inVietnam (UN).

The GCNV aims to support itsmembers implement effectivecorporate social responsibility initiativein Vietnam.

The goal of the GCNV is to be thenational corporate social responsibilitycentre of excellence. Our job is toidentify, anticipate and diffuse thetensions between business andcommunities, business and theenvironment, business and thegovernment, business and theconsumer, leading to sustainablebusinesses in a prosperous society.

Printed on Recycle paper

A REVIEW OF THE SOCIAL AND ENVIRONMENTALCONDITIONS OF INDUSTRIES IN VIETNAM AGAINST

THE GLOBAL COMPACT PRINCIPLES

2010

A REVIEW OF THE SOCIAL AND ENVIRONMENTALCONDITIONS OF INDUSTRIES IN VIETNAM AGAINST

THE GLOBAL COMPACT PRINCIPLES

This research was conducted by CSR Asia in cooperation with the National Economics University in Vietnam for the Global Compact Network Vietnam

from September to December 2009

CBC-CSR Catalyzing Business Community’s role towardsgreater Corporate Social Responsibility throughGlobal Compact Principles in Vietnam

COCs Codes of ConductCSR Corporate Social Responsibility EU European UnionFDI Foreign Direct Investment GCNV Global Compact Network VietnamGDP Gross Domestic Product GSO General Statistics Office GSP Generalised Tariff of PreferencesHCMC Ho Chi Minh City IFC International Finance Corporate LEFASO Vietnam Leather and Footwear AssociationMPDF Mekong Project Development FacilityTOR Terms of ReferenceUNDP United Nations Development Programme UNIDO United Nations Industrial Development

OrganisationVCCI Vietnam Chamber of Commerce and Industry WTTC World Travel and Tourism Council

List of acronyms used in the report

Over the last 25 years Vietnam has transformed itselfthrough remarkable and sustained economic growthwhich has brought improvements to the quality of life formillions and a reduction in the number of poor. The

activities of the private sector and an enabling environment forentrepreneurship to grow and develop have been fundamental for thistransformation. Doi Moi and a vision of a “market economy withsocialist orientation” unleashed the potential of the private sector togenerate growth with a sustained commitment from the State to equityand poverty reduction.

In 2007 the GCNV was launched to support the government in theimplementation of its Sustainable Development Strategy (Agenda 21)and the development of responsible business practices. The GCNV isimplemented through the Vietnamese Chamber of Commerce andIndustry (VCCI), Office for Business Sustainable Development (SD4B)with funding from UNDP as part of the CBC-CSR project.

From September - December 2009, the GCNV commissioned areview of the current status of responsible business practices inVietnam. The main findings of this research demonstrate how businesshas successfully contributed towards sustainable development andpoverty alleviation in Vietnam and highlight the potential for businessto play an even great role in the future.

The report provides examples of initiatives which promote and addressgood labour, environment, human rights and transparency standards.It also outlines the ongoing risks which companies have to manage inorder to ensure sustainable economic growth in the future. This reportprovides a preliminary mapping of those issues in relation to differentindustries, based on various stakeholders perceptions.

While the views expressed in the paper do not necessarily reflect theofficial view of the GCNV, this paper forms part of our objective ofstimulating discussion in Vietnam on corporate social responsibilityand sustainable business practices. I would like to take this opportunityto congratulate the research team on this careful and thoughtprovoking paper, and to thank the companies involved intheir willingness to share information and views with us.

Fore

wor

dDr. Doan Duy Khuong, National Project Director, CBC-CSR ProjectVice Executive President of VCCI

““

This research was conducted by CSR Asia in cooperation with the National EconomicsUniversity in Vietnam. Michelle Brown managed the project with support and oversight fromNguyen Van Thang and Richard Welford. This project could not have completed withoutMichelle’s continuous commitment and dedication. The research was commissioned by theGCNV as part of the CBC-CSR project.

Special thanks are due to all the companies and non-government organisations thatparticipated in interviews in preparation of this report along with the governmentrepresentatives that gave the researchers their time and shared their perspectives on CSR andsustainable business practices as well.

The authors are solely responsible for remaining errors of fact or omission. While this is aGCNV paper, the views expressed here are the authors alone and do not necessarily reflectthe views of the GCNV or its members.

Acknowledgements

Executive Summary

Overview of the social and environmental issues for key industry sectors

Recommendations

Brief introduction to the project:

Our approach

Overall findings

The Industries

I Top tier recommendations: Food processing, construction and the extractive industries

1 Food processing2 Construction

THE EXTRACTIVE INDUSTRIES3 Oil and gas

4 Mining

II Manufacturing: Lots of risks and opportunities but other remediation efforts in place or starting…

5. Manufacturing:5.1 Garments, textiles and shoes5.2 Wood products and furniture

III Agriculture, fishing and forestry: Lots of risks but fewer opportunities

6. Agriculture7. Fishing

8. Forestry

III. Other industries we looked at but didn’t prioritise at this time: Tourism (including hotels andrestaurants) and real estate and telecommunications and post

9. Tourism, hotels and restaurants10. Real estate, renting and business activities

11. Post and telecommunications12. Finance and banking as a cross-cutting theme

Conclusion:

Appendix I: Key data on industry sectors Vietnam

Appendix II: Scorecard for Global Compact Issues by Industry in Vietnam

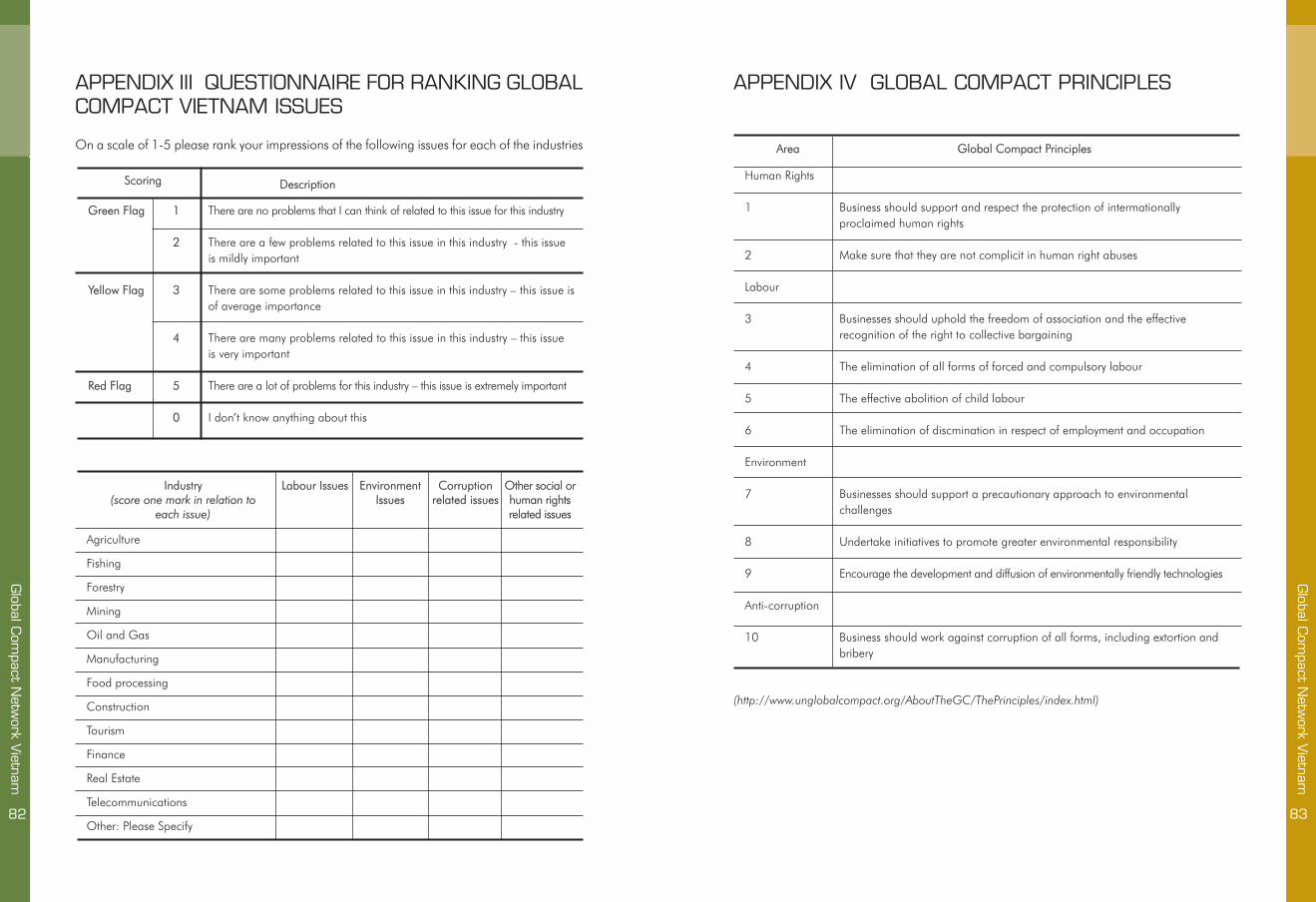

Appendix III: Questionnaire for Ranking Global Compact Vietnam Issues

Appendix IV: Global Compact Principles

Appendix V: General findings for Global Compact

Global Compact

6

10

22

26

27

30

32

32

3338434346

50

515557

58

596467

70

71727374

76

78

81

82

83

84

84

TABLE OF CONTENTS

4

Poverty Reduction, Business andSustainable Development

Over the last 25 years Vietnam hastransformed itself through remarkable andsustained economic growth which hasbrought improvements to the quality of lifefor millions and a reduction in the number ofpoor. The activities of the private sector andan enabling environment forentrepreneurship to grow and develop havebeen fundamental for this transformation.Doi Moi and a vision of a “market economywith socialist orientation” unleashed thepotential of the private sector to generategrowth with a sustained commitment from theState to equity and poverty reduction. Thecountry’s Socio-Economic Development Plan(SEDP) which is also the poverty alleviationstrategy sets a vision for Vietnam ofbecoming an industrialised country by 2020.The plan sets targets for the economy,society, the environment and for goodgovernance and sees the private sector asfundamental for providing resources, wealthand jobs which are needed for the country tomeet its own goals.

While Vietnam has not emerged unscathedfrom the global economic turmoil of 2009it has avoided a recession. It is on target tomeet its goal of becoming a middle incomecountry by 2020. However, the last 25 yearsof growth has not come without both socialand environmental costs and althoughmillions have lifted themselves out of povertythere are now growing concerns over thewidening income gap between the rich andthe poor as well as continued poverty inremote and mountainous areas, particularlyfor minority groups. Climate change,severe weather and other environmentalchallenges exacerbate social challengesand there is increasing recognition of theneed to protect Vietnam’s immense naturalresources in order for growth anddevelopment to be sustained. Recentanalysis from the General Statistics Office(GSO) Household survey shows that a largeproportion of people are ‘just above’ thepoverty line and pointed out that the nextphase of poverty alleviation strategies willbe more challenging1 . Vietnam is currentlyin the preparatory stages for its next Socio-Economic Development Plan which will set

targets and outline a vision and strategy forthe next five year period.

As the themes and discussions take root forsetting the framework for the next five yearSEDP, we believe that the work of the GCNVis timely and hope that this project cancontribute to considering how sustainabledevelopment can be achieved and theopportunities this provides for business. Asbusiness continues to be the driver of thegrowth and the main creator of wealth, jobsand employment, there is an opportunity forother sectors to work together with businessto identify ways in which this growth can bemore sustainable and bring benefits tobusiness and benefits for development. Whilesome costs will be involved, the benefits andthe risks and cost associated with not takingaction will be greater. The Global Compact’sframework for sustainable business through10 guiding principles on labour, environment,human rights and anti-corruption fit within thecontext of Vietnam’s development agendaand could be a rallying call for business tocontribute to the next SEDP.

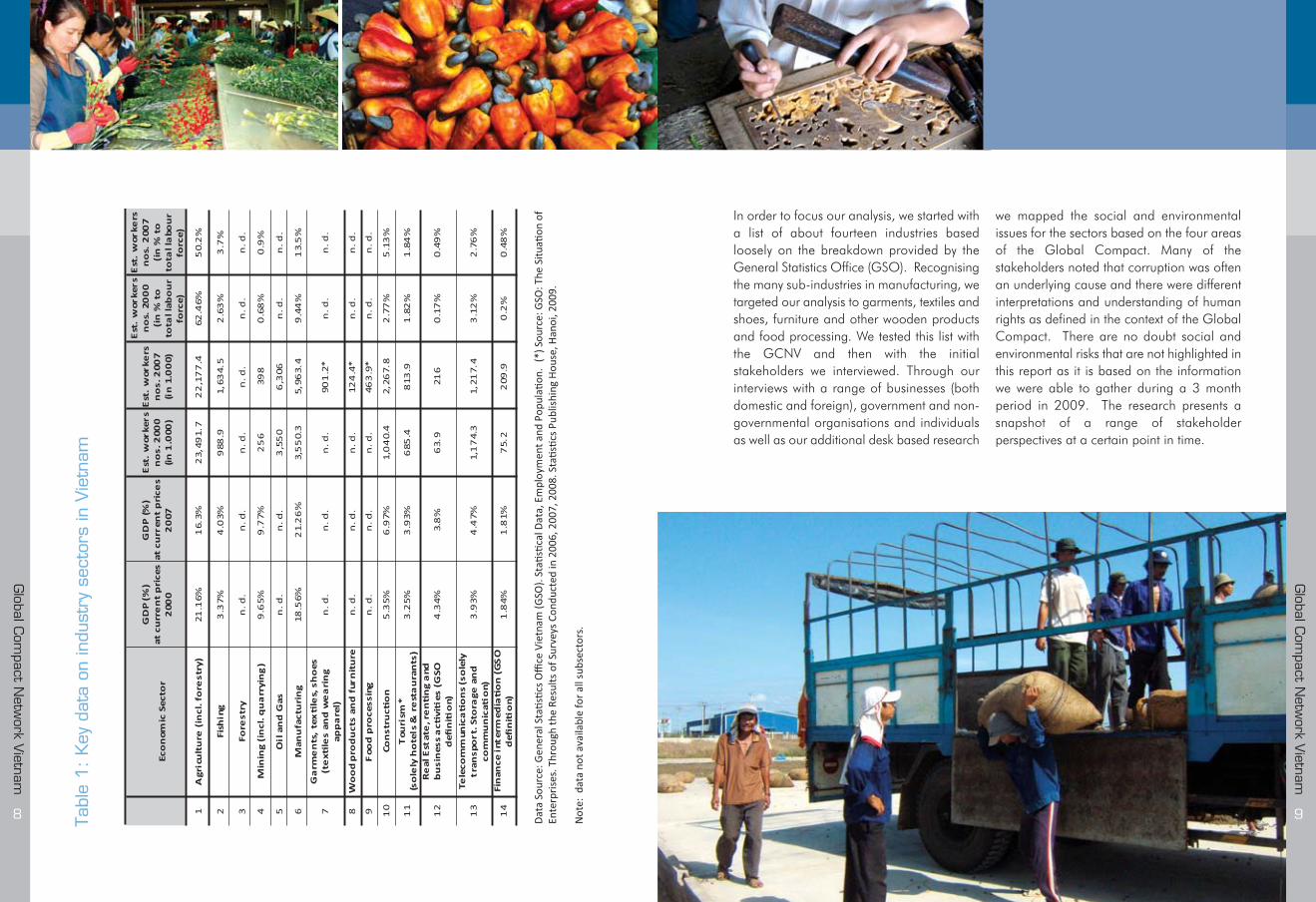

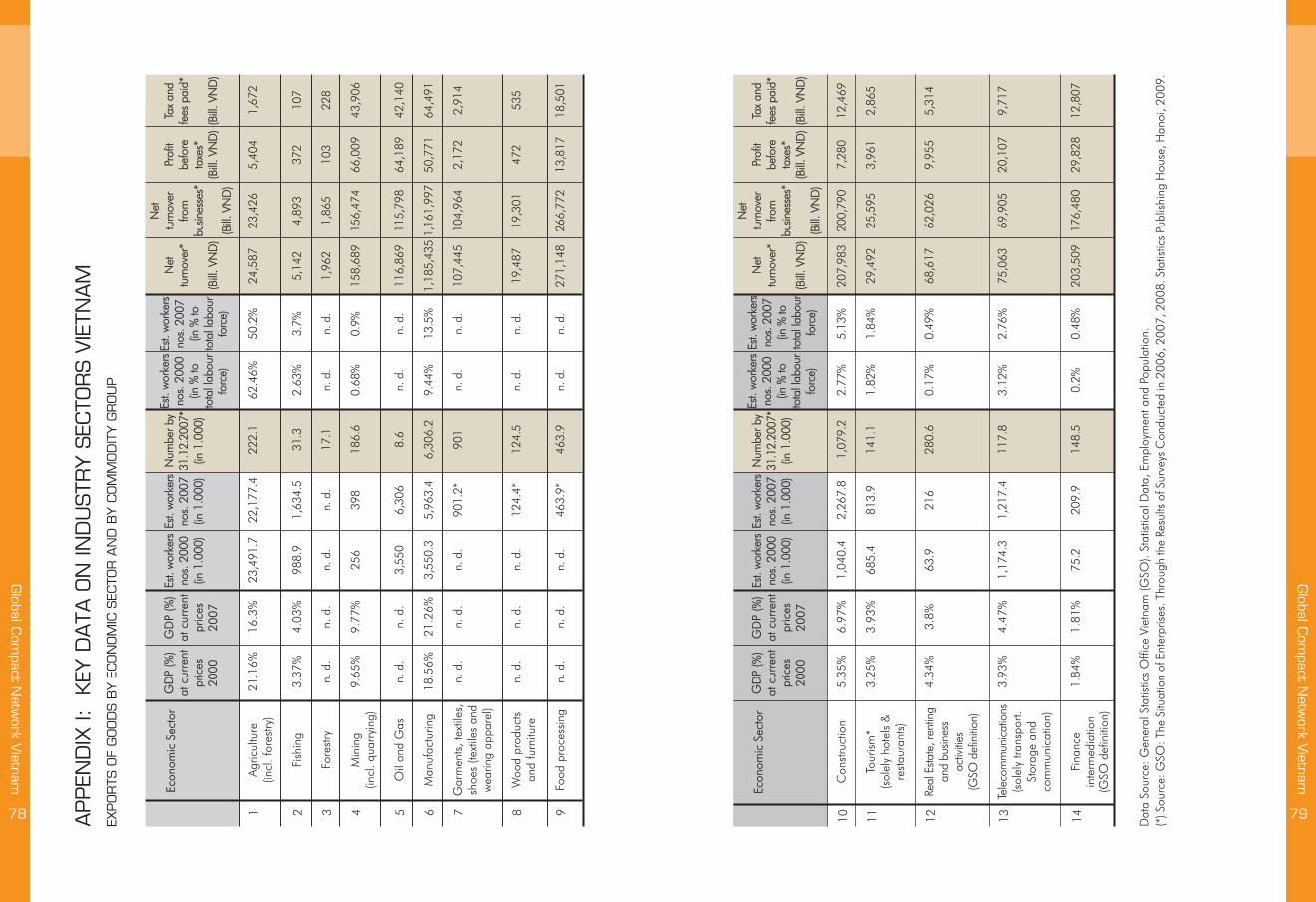

Since the Doi Moi reforms, Vietnam hastransitioned from an economy reliant onagriculture to one increasingly driven bymanufacturing. Table 1 below shows howmanufacturing has grown in terms ofcontribution to GDP from 18.56 percent in2000 to 21.26 percent in 2007 andcontinues to grow. The table provides asnapshot of some of the key data available

on the size and nature of the sector andfurther details are available in the body andappendix of the report. Apparel andfootwear, fish and food products, furnitureand wood products are key exports. Vietnamis endowed with significant natural resourcessuch as offshore oil and underground mineralreserves. Oil and gas exports are a key sourceof income. In recent years there have beenincreased opportunities for the extractiveindustries in the country. Over the years, theshare of the service sector to the economy hasalso grown considerably and is expected tobe a key driver in the years to come. Whileagriculture (including fishing and forestry)only contributes about 20 percent towardsGDP it is a substantial source of employmentand agricultural products account for nearly23 percent of all exports of the country2.Manufacturing is a critical source ofemployment and although affected by therecent global economy, there is a criticalshortage of workers in some areas3 .

Executive Summary

1 Vietnam Academy of Social Sciences. 2009. Reporton Rapid Impact Monitoring of Global Economic Crisis:Short-Term Vulnerability and Long-Term Measures forSustaining Poverty Reduction in Viet Nam. For 2009Consultative Group Meeting

2 Based on GSO data for agricultural, forest andaquatic products 2000 and 2007 data

3 Vietnam Academy of Social Sciences. 2009. Reporton Rapid Impact Monitoring of Global Economic Crisis:Short-Term Vulnerability and Long-Term Measures forSustaining Poverty Reduction in Viet Nam. For 2009Consultative Group Meeting.

This review of the social and environmental conditions of industries in Vietnam wascommissioned by the Global Compact Network Vietnam (GCNV) and carried out by CSR Asiain cooperation with the National Economics University in Vietnam. It aims to understand theCSR needs of different sectors. The objective was to identify the main social and environmentalproblems of the key industrial sectors in Vietnam and to rank these based on factors such asthe size of the sector and whether or not there are existing efforts to tackle the social andenvironmental challenges within the sectors.

Global C

ompact N

etwork Vietnam

7

Global C

ompact N

etwork Vietnam

6

Tabl

e 1:

Key

dat

a on

indu

stry

sec

tors

in V

ietn

am

Global C

ompact N

etwork Vietnam

9

Global C

ompact N

etwork Vietnam

8

In order to focus our analysis, we started witha list of about fourteen industries basedloosely on the breakdown provided by theGeneral Statistics Office (GSO). Recognisingthe many sub-industries in manufacturing, wetargeted our analysis to garments, textiles andshoes, furniture and other wooden productsand food processing. We tested this list withthe GCNV and then with the initialstakeholders we interviewed. Through ourinterviews with a range of businesses (bothdomestic and foreign), government and non-governmental organisations and individualsas well as our additional desk based research

we mapped the social and environmentalissues for the sectors based on the four areasof the Global Compact. Many of thestakeholders noted that corruption was oftenan underlying cause and there were differentinterpretations and understanding of humanrights as defined in the context of the GlobalCompact. There are no doubt social andenvironmental risks that are not highlighted inthis report as it is based on the informationwe were able to gather during a 3 monthperiod in 2009. The research presents asnapshot of a range of stakeholderperspectives at a certain point in time.

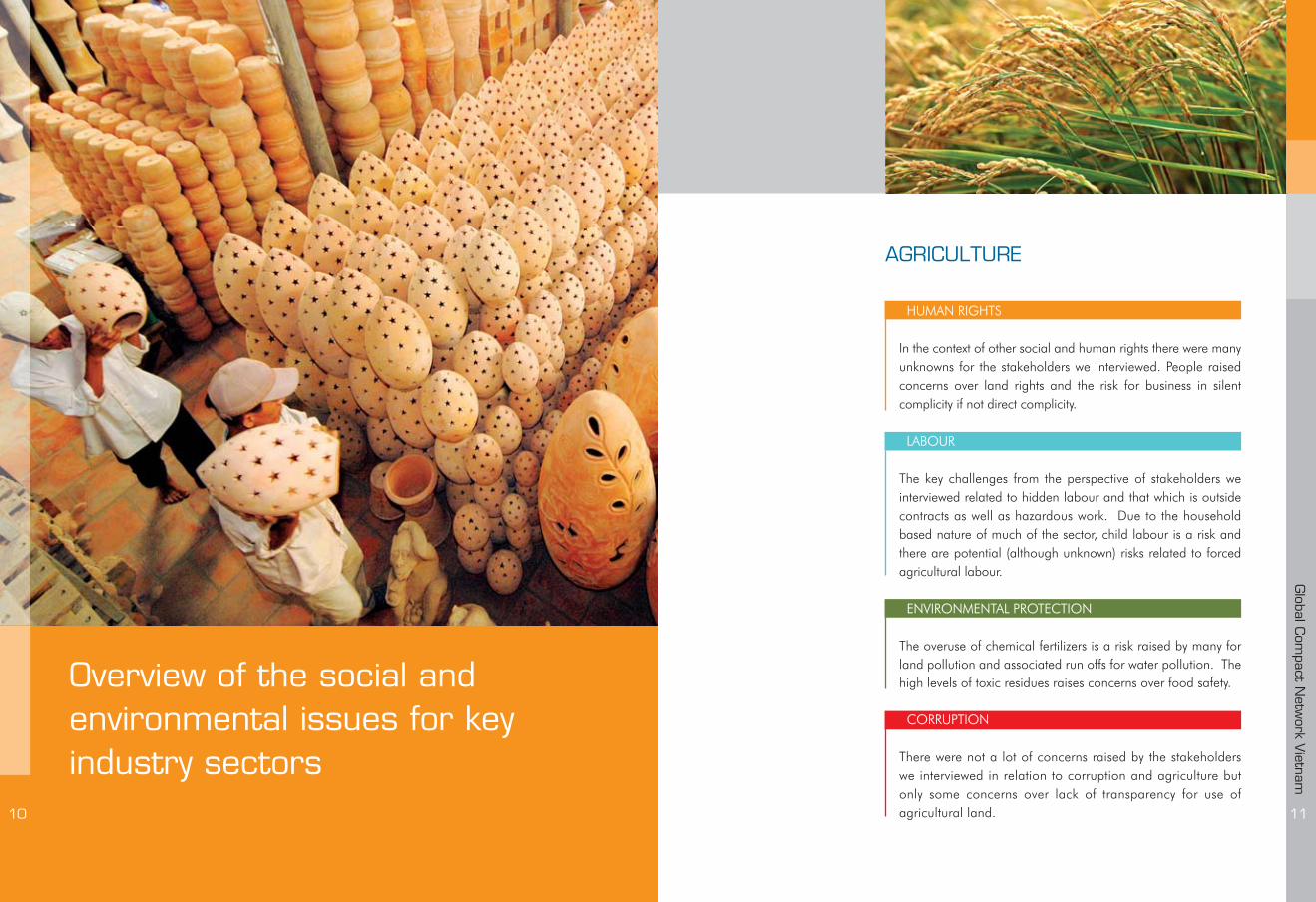

HUMAN RIGHTS

In the context of other social and human rights there were manyunknowns for the stakeholders we interviewed. People raisedconcerns over land rights and the risk for business in silentcomplicity if not direct complicity.

LABOUR

The key challenges from the perspective of stakeholders weinterviewed related to hidden labour and that which is outsidecontracts as well as hazardous work. Due to the householdbased nature of much of the sector, child labour is a risk andthere are potential (although unknown) risks related to forcedagricultural labour.

ENVIRONMENTAL PROTECTION

The overuse of chemical fertilizers is a risk raised by many forland pollution and associated run offs for water pollution. Thehigh levels of toxic residues raises concerns over food safety.

CORRUPTION

There were not a lot of concerns raised by the stakeholderswe interviewed in relation to corruption and agriculture butonly some concerns over lack of transparency for use ofagricultural land.

AGRICULTURE

Global C

ompact N

etwork Vietnam

11

Overview of the social andenvironmental issues for keyindustry sectors

10

Global C

ompact N

etwork Vietnam

13

Global C

ompact N

etwork Vietnam

12

FISHING

HUMAN RIGHTS

Land rights and conversion issues for aquaculture are a potentialrisk but there were many ‘unknowns’ generally for fishing.

LABOUR

Similar to agriculture, work often takes place at the householdlevel and there can be hidden issues. Stakeholders commentedthat there were many child labour issues for fishing and also alack of safe working conditions (i.e. sea fishing withoutcommunication devices as well as blast and cyanide fishing).

ENVIRONMENTAL PROTECTION

Aquaculture has relied on chemicals and antibiotics –particularly for shrimp and catfish and there are concerns overthe long term effects of chemical inputs. The destruction ofmangroves causes both environmental damage and can affectlocal livelihoods. Cyanide fishing is growing and blast fishingcauses irreparable damage to Vietnam’s precious ecosystems.

CORRUPTION

The primary concern related to access to fishing rights in someareas.

FORESTRY

HUMAN RIGHTS

There were no specific concerns raised by stakeholders weinterviewed.

LABOUR

The work is usually at a household level with land use rights toplant and cultivate forest trees. There were not a lot of labourissues flagged by stakeholders we interviewed.

ENVIRONMENTAL PROTECTION

Forest cover is increasing but the quality of forests (primarycover) is decreasing. The decrease in up-stream forests is aconcern with links to flooding and erosion. There are widerregional issues regarding deforestation.

CORRUPTION

Concerns related to land handover processes and illegalforest logging.

Global C

ompact N

etwork Vietnam

15

Global C

ompact N

etwork Vietnam

14

MINING

HUMAN RIGHTS

Risks and concerns related to relocation and lack of free priorand informed consent or consultation. In particular there wereconcerns for indigenous populations and cultural heritage(particularly in the highlands).

LABOUR

Risks and concerns related to hazardous and unsafe workingconditions. Although labour issues in mining get less mediaattention in Vietnam than say manufacturing, they areconsidered to be very serious and risks also relate to migrantand unprotected workers. Child labour is also a risk.

ENVIRONMENTAL PROTECTION

Mining brings with it severe environmental impacts which needto be carefully managed. The recent attention on Bauxitemining in the Central Highlands was noted by many.

CORRUPTION

Concerns over bribery and facilitation payments and a lack oftransparency and limited information available which raiseseven more concerns and fears over corruption.

OIL AND GAS

HUMAN RIGHTS

Nothing specific was raised by stakeholders we interviewed.

LABOUR

Stakeholders commented that there was a lack of informationover labour issues in the oil and gas industry but a perceptionthat people who worked in this industry were better off in termsof remuneration and benefits. However, as much is offshorethere is a risk of ‘hidden’ issues.

ENVIRONMENTAL PROTECTION

The biggest concern related to recent and potential oil spills.

CORRUPTION

This industry is perceived as ‘secretive’ with a lack oftransparency and some stakeholders assumed corruption butnoted that they had no clear evidence.

Global C

ompact N

etwork Vietnam

17

Global C

ompact N

etwork Vietnam

16

MANUFACTURING

HUMAN RIGHTS

The links to labour issues were the main concern.

LABOUR

Concerns were raised over the minimum wage vs. a ‘living’wage and rising inflation in 2008. Child labour continues to bea concern and although many brands have worked extensivelyon auditing and remediation this covers only a small percentageof factories in the apparel or footwear industries. While largerfirms may be better off, there is a lot ‘unseen’ in the next tier anda risk of sub-contracting. Lack of insurance for workers was aconcern as well as hazardous and safe working conditions.There are continued issues regarding child labour. Concernswere also raised about the quality of life in industrial parks.

ENVIRONMENTAL PROTECTION

Waste water and other forms of pollution are particularlyserious. There is a perception of limited enforcement and a lackof incentive for any enforcement. While the industrial parks aresupposed to manage this better, the systems are also notadhered to in these locations.

CORRUPTION

One stakeholder noted a risk regarding pay-offs to staff forwinning buyer orders. Other concerns were related to the non-enforcement of environmental or labour laws.

Manufacturing is broad and the risks and opportunities will be different given the differentnature of the industries. To manage the scope of this exercise we asked stakeholders aboutapparel and footwear, wood and furniture production and food processing (separately – seebelow) given their current contribution towards the economy of Vietnam. Electronics is growingin importance and is a prioritised industry in the country.

FOOD PROCESSING

HUMAN RIGHTS

Again the issues for most stakeholders related to labour issues.

LABOUR

The key concern is a lack of safety measures for workers whoare in contact with chemicals. Similarly with other manufacturingsectors, there are concerns for child labour and hazardouslabour as well as excessive overtime.

ENVIRONMENTAL PROTECTION

A lack of waste water treatment is a serious risk at the moment.Other concerns related to the overuse of chemicals in theprocessing.

CORRUPTION

The key concern was a perceived lack of enforcement ofenvironmental protection and concerns over corruption. If theright person is paid then a blind eye can be turned onenvironmental issues.

Global C

ompact N

etwork Vietnam

19

Global C

ompact N

etwork Vietnam

18

CONSTRUCTION

HUMAN RIGHTS

The concerns linked to land issues and labour issues.

LABOUR

Worker safety, overtime, unprotected labour, and child labourare risks and concerns for this industry in Vietnam. A largenumber of temporary workers from rural areas and an increasingnumber of migrant workers without any contract (and thereforeany formal protection) was another issue raised.

ENVIRONMENTAL PROTECTION

Dirt, noise, solid waste, transportation of materials to sites aswell as lax building standards and building safety were allconcerns that were flagged.

CORRUPTION

Stakeholders perceived corruption to be a big issue for thisindustry. Although Vietnam has a tender law and is workingon improvements in this area, the issue of ‘fake bidders’ andcorrupt practices in the tendering process is a big risk.

TOURISM

HUMAN RIGHTS

Some stakeholders raised concerns with ‘social evils’ associatedwith tourism such as prostitution, drugs loss of traditional valuesand heritage.

LABOUR

Overtime and potential child labour are risks for the tourismindustry.

ENVIRONMENTAL PROTECTION

The concern over lack of wastewater treatment, the use ofagricultural land for tourism and resorts such as golf resortswere all flagged. Logging of trees was also noted.

CORRUPTION

With any large infrastructure project in Vietnam the risk ofcorruption was noted. Who benefits and how with regards totourism can be affected by corrupt practices.

Global C

ompact N

etwork Vietnam

21

Global C

ompact N

etwork Vietnam

20

REAL ESTATE

HUMAN RIGHTS

Land rights are a sensitive issue as land belongs to thegovernment. Households who want to get the land use rightcertificate (the red book) need to go through many proceduresbut there are always “special cases” and there is uncertainty andlack of transparency.

LABOUR

Aside from concerns over poor management and poor buildingpractices, there were not a lot of concerns linked to labour issues.

ENVIRONMENTAL PROTECTION

Similar to construction some raised concern over how land istaken from farmers to build too many golf course and industrialparks without decent plans and proper waste water and solidwaste systems.

CORRUPTION

This industry is believed to be one of the worst in terms ofcorruption. Lack of transparency and lack of monitoring werekey concerns.

TELECOMMUNICATIONS AND POST

The main concerns raised in relation to this industry related tofacilitation payments for transporting materials through the postor through private companies. There was a concern thatfacilitation payments always needed to be made. No furtheranalysis was made in relation to this industry.

BANKING AND FINANCE AS A CROSS-CUTTING THEME

We initially looked at banking and finance alongside the otherindustries. While stakeholders did not raise concerns about socialand environmental issues directly in the financial institutions, it wasmore how banking and finance could play a pivotal role inpromoting and achieving sustainable development in otherindustries. We therefore see banking and finance as a cross-cutting theme across all of the industries. The direct concerns werein relation to corruption with a risk of insider trading andinformation asymmetry amongst powerful investors along withcredits being provided to unqualified borrowers.

Top tierrecommendations:

Food processing:

The food processing sector plays animportant role in Vietnam’s economy and isexpected to continue to do so. Based on ouranalysis there are substantial environmentalissues along with social issues that need to beaddressed. Given the transition from anagrarian to an industrial economy and therole that agricultural products play incontributing to exports, food processing hassome natural strength as an industry to focuson. Agriculture itself will be a bigger sourceof employment but there is more limitedcapacity for the GCNV to act (as in fishing).By moving one step up the value chain tofood processing there is a potential to addvalue to the development of Vietnam.

Construction:

While construction is lower in terms ofcontribution to GDP it links to other industriesand infrastructure. It is large in terms ofemployment and there are many issues toaddress throughout the industry. Some ofthese are critical with potential to causedisaster such as shoddy building materialsand unsafe infrastructure. There is currentlya lack of remediation efforts. VCCI couldleverage its government links and potentiallybring together some key players. The networkcan also leverage the support of key players

Recommendations

Global C

ompact N

etwork Vietnam

22

Global C

ompact N

etwork Vietnam

23

Based on a review of social and environmental related risks (including labour, environment,corruption and human rights), the presence of any ongoing remediation and the size of thesector and other opportunities, we ranked 14 industries in Vietnam and looked at these forfurther analysis. We came up with 3-4 industries for the Network to concentrate on (with bankingand finance as a cross-cutting theme). These recommendations by sector are as follows:

Cross-cutting theme: Banking and finance

High risk and lots ofopportunity but otherremediation effortsin place

•Manufacturing: •Garments, appareland textile andshoes •Wood productsand furniture

GCNV should workand liasie closelywith ongoingremediation efforts

Limited risk andlimited opportunity

•Tourism (Hotel andHospitality) •Real estate•Telecommunicationsand post

Not a priority at themoment for thenetwork

It should be stressed that we recognise the importance and severity of issues in the primaryindustries but that we see more potential for the GCNV to engage in the next step up the valuechain and focus on the manufacturing process (for example food processing).

Top tierrecommendations

•Food processing •Construction •Extractiveindustries: Oil & gasand mining

GCNV focus furtheron these sectors anddevelop tools forbrining to life theGlobal CompactPrinciples

High risk but morelimited opportunityto act

•Agriculture •Fishing •Forestry

Not a priority at themoment for thenetwork

Global C

ompact N

etwork Vietnam

24

Global C

ompact N

etwork Vietnam

25

in the construction materials industry who arelocal members.

The extractive industries:

Vietnam is now ranked South-East Asia’s thirdlargest oil producer. The profits from the oilbusiness have the potential to makesignificant contributions towards povertyalleviation and sustainable development inVietnam. However, experience and lessonslearned from other countries stress that theindustry must grow and develop in atransparent manner in order fordevelopmental gains to be realised. Thenetwork has potential with champions such asTalisman and interest shown from Embassiesand bilateral donors to help to take forwardsome work in this area. Clearly initiatives byorganisations such as TransparencyInternational are important and the GCNVcould help to legitimise and strengthen theirefforts. We would recommend that the GCNVgive serious consideration to leveraging itsstrengths and taking forward work related tothe extractive industries in Vietnam.

As mining is an industry which has thepotential to contribute to Vietnam’s economybut also one that needs to be managedresponsibly due to its significant environmentaland social impacts, it is an area we think anetwork such as the GCNV could add value.This could be in relation to decent work andlabour issues and providing businessstrategies for introducing occupational healthand safety measure’s for mining which couldalso include experiences from other countriesand ways to properly manage environmentalimpacts. Therefore we are recommendingthat mining be combined with oil and gas andthat the network do some further work onissues for the extractive industries. While manystakeholders were concerned with the‘sensitive’ nature of this industry, a multi-stakeholder network such as the GCNV isbetter placed than most to take forward workin this area.

Finance and banking as a cross-cutting theme:

The banking and finance sector initiallyemerged as one of our top-tierrecommendations. While some stakeholderswe interviewed felt that it was too early inVietnam’s reform process to talk aboutsustainable finance and that this would be tenyears later on, others disagreed. There is agreat opportunity now for Vietnam to embedsustainable lending practices in the bankingand finance sector in order to have a knock-on effect and positive influence elsewhere.There is further potential opportunity with

changes to the banking sector and stateowned banks as well as the growing influenceof the stock exchange. There is growinginterest globally and regionally in EquatorPrinciples, a benchmark for the financialindustry to manage social and environmentalissues in project financing. We generally seea lack of remediation efforts but also potentialchampions in country.

The other natural industries which have highrisks as well as opportunities are in otherareas of manufacturing and particularlygarments and shoes as well as wood andfurniture products and possibly electronics.As there has been some attention givenalready to these industries and there are someremediation efforts in place (such as the ILO

and IFC supported Better Work Programme)we recommend to the Network that they focuson those sectors which, as a multi-stakeholdernetwork (government, private sector andNGOs) they can leverage their strengths andadd additional value.

While the risks related to sustainable businessare numerous so are the opportunities.Experience and lessons learned from othercountries shows that a focus on sustainablebusiness can help to contribute to growth ina way that takes into consideration people,the environment and the economy. AsVietnam looks forward and considers its visionfor the future and next SEDP there is anopportunity for business to be a key partnerin sustainable development.

Global C

ompact N

etwork Vietnam

27

This project was initiated to identify the main social and environmental problems of the keyindustry sectors in Vietnam, in order to allow the Global Compact Network Vietnam to chooserationally which sectors to focus on. The Global Compact Network Vietnam (GCNV) is analliance of companies, government, trade unions and non-governmental organisations. Itexists to promote and improve the working and environmental conditions of Vietnameseworkers through the implementation of the Global Compact principles by companies. Itsultimate goal is to be the national corporate social responsibility (CSR) centre of excellence inthe country; supporting companies to identify, anticipate and diffuse the tensions betweenbusiness and communities, business and the environment and business and the consumer,leading to sustainable businesses in a sustainable society4. The GCNV was launched in 2007to support the government in the implementation of its Sustainable Development Strategy(Agenda 21). The project is implemented through the Vietnam Chamber of Commerce andIndustry (VCCI), Office for Business Sustainable Development (SD4B) with funding from UNDP.

4 Verbatim from terms of reference

Brief introductionto the project

Ourapproach

To rank the social and environmental issuesand prioritise key industries our approachincluded:

1.A mapping of the most important socialand environmental issues affecting eachindustrial sector in Vietnam (based on theGlobal Compact Principles) as well asimportant initiatives and activities supportedby companies and organisations at agovernment, factory, worker and civil societylevel, regarding the four areas of the GlobalCompact.

2.Developing a scorecard to rank the mostimportant social and environmental risks ofeach industrial sector against the GCNV’sability to influence them.

To develop the scorecard we looked at bothrisks and opportunities:

RISKS:

We mapped the social and environmentalproblem in each industrial sector in relation

to the four areas of the Global Compact. Inour interviews and our focus groups,stakeholders were asked to consider the keyindustries in Vietnam and share theirassessment of the severity of issues withineach of the industries. Appendix III has thetool that was used in the interviews. Basedon the collated answers we then attributed ascore of 0,1,2 or 3 to each of the issues.

OPPORTUNITIES:

For this part of the scorecard we considered:• The relevant size of each sector – relative26

Global C

ompact N

etwork Vietnam

29

Global C

ompact N

etwork Vietnam

28

to number of workers and value of thesector based on its contribution to GDP.

• The presence of ongoing remediationactions.

Ability to influence: Including:• GCNV’s ability to add-value and not

duplicate existing efforts.• External drivers including FDI and

proportion to export.

• Public awareness and interest in the sector.• Presence of local champions.

Again, for the purposes of benchmarking andthe scorecard, each of the areas was given ascore of 0,1,2 or 3 based on the datacollected. In each of the industries highlightedin this report the summary of the scorecardsare presented.

PROCESS: We engaged national companies,multinational companies working in Vietnam,government officials as well as others workingin international organisations, NGOs, localresearch organisations or as consultants. Wecarried out two focus group discussions withVietnamese companies (in the North and inthe South) and one focus group withmultinational companies.

In depth interviews were conducted withgovernment officials in various sectors (i.e.,Government Inspectorate - GI, Ministry ofLabour, Invalids, and Social Affairs - MOLISA,Ministry of Finance, Ho Chi Minh City’sDepartment of Resource and Environment),and several managers of organisations aswell as other stakeholders from a variety ofbackgrounds. Interviews were open-endedbased on a guideline. Each interview lastedfrom 40 to 60 minutes. Depending on the

sector of the interviewees, the interviews couldcover all or only some of the GC issues. Forexample, interviews with GovernmentInspectorate focused mainly on corruptionissues, while MOLISA talked more aboutlabour issues. All the interviews wereconducted from 15th September to 16thOctober, 2009.

The three focus groups were conducted withmanagers of domestic companies (13 inHCMC, and 10 in Hanoi) and multinationalcompanies (11 in HCMC). The focus groupslasted for more than 2 hours, with opendiscussions on key specific issues, pressingindustries, as well as any initiative orsuggestion to address these issues in eachGC area.

A final step was to walk through the researchprocess with the GCNV and test ourpreliminary findings (October, 2009). Theprinciple researchers were Michelle Brown(CSR Asia) and Nguyen Van Thang (NationalEconomics University). Oversight for thewhole project was provided by RichardWelford (CSR Asia and the University of HongKong) with some advisory support fromNicholas Freeman (CSR Asia representativeand affiliate consultant in HCMC) and someadditional research assistance from QuanMinh Chau (CSR Asia).

CHALLENGES AND LIMITATIONS:With regards to the ranking exercise, werecognise the challenge of applying a ‘score’or ‘flag’ to such complex issues as thoseenshrined in the Global Compact yet, at thesame time the tool proved useful as aconversation starter to further explore theissues with stakeholders. For our ranking, wealso took into consideration existing researchor analysis on the issues in Vietnam and thoserisks generally for the industries based on ourexperience in the region.

We were able to speak to and interview thosethat were interested in being engaged andwho we may have had easier access to. Wehave made attempts to compensate for thisby drawing on any alternative and existingresearch and continuously checking ourpreliminary findings with stakeholders andtesting and retesting as we go along.

In terms of the industries chosen to look at inthe study, we based this on our preliminaryassumptions and initial secondaryinformation. We also asked those weinterviewed to flag any additional ones thatweren’t covered in our research questions.

Global C

ompact N

etwork Vietnam

30

Global C

ompact N

etwork Vietnam

31

Figure 1 presents the overall findings based on the scorecard we developed and used for theresearch. Each industry examined was given a score for both risks (in relation to the severityof issues for the four areas of the Global Compact) as well as opportunities based on relativesize of the sector, remediation efforts already present, capacity of GCNV to add value as wellas other drivers such as FDI and contribution towards export, public awareness locally andpresence of any champions in country.

Figure 1: Risks and opportunities ranking

Presence of remediation efforts had been taken into account in the overall score (with equalweighting as the other industries). We originally looked at all industries in the top right quadrantand then prioritised those which had a lack of remediation efforts. Based on this assessmentour recommendations for the Global Compact Network Vietnam are presented in table 1:

Table 1: Recommendations

We recognise the importance and severity of issues in the primary industries but that we seemore potential for the GCNV to engage in the next step up the value chain and focus on themanufacturing process (for example food processing).

Overall findings

Cross-cutting theme: Banking and finance

High risk and lots ofopportunity but otherremediation effortsin place

•Manufacturing: •Garments, appareland textile •Wood productsand furniture

GCNV should workand liasie closelywith ongoingremediation efforts

Limited risk andlimited opportunity

•Tourism (Hoteland Hospitality) •Real estate•Telecommunications and post

Not a priority at themoment for thenetwork

Top tierrecommendations

•Food processing •Construction •Extractiveindustries: Oil & gasand mining

GCNV focus furtheron these sectors anddevelop tools forbrining to life theGlobal CompactPrinciples

High risk but morelimited opportunityto act

•Agriculture •Fishing •Forestry

Not a priority at themoment for thenetwork

1. FOOD PROCESSING

Based on our analysis of both the severity of issues and risks associated with the areas of theGlobal Compact as well as the opportunities and capacity to act on the issues within thesector, we have come up with three industries which are our ‘top tier’ recommendations. Thisdoesn’t mean there were not serious risks or problems in other sectors but based on a rangeof factors related to the opportunities certain industries were prioritised. A brief summary ofeach industry, the key GC issues and the opportunities within the sector are presented below.

The IndustriesI - TOP TIER RECOMMENDATIONS:FOOD PROCESSING, CONSTRUCTIONAND THE EXTRACTIVE INDUSTRIES

Global C

ompact N

etwork Vietnam

3332

5 Friedrich-Ebert-Stiftung. 2008. P.286 BMI research Vietnam Food and Beverage Report 7 BMI research

Food processing contributes significantly tothe overall GDP in Vietnam and is forecastedto maintain an average annual growth rate of10 to 15 percent for the short term. It is animportant source of employment. TheGovernment Statistical Office (GSO) datafrom 2007 shows that there are over 4.5million people working in the sector.However this may underestimate the truenature of the industry with others finding thatsugar factories alone are estimated to employaround 1 million laborers5.

The sector has attracted a significant level offoreign investment in recent years fromcompanies such as Unilever, Nestle and SanMiguel and P&G. At the same time, analystscomment that the requirement for jointventures is deemed to have deterred someforeign investors6.

The sector is made up primarily by micro,small and medium sized enterprises and isfragmented with the exception of the dairyand confectionary sector7. It is comprised of

Global C

ompact N

etwork Vietnam

34

Global C

ompact N

etwork Vietnam

358 BMI research

ENVIRONMENTAL PROTECTION • Waste water and water pollution critical issue • Perception that products in Vietnam competing on

price and waste treatment seen as too expensive • Overuse of chemicals • Food safety and sanitation

CORRUPTION • Concerns over lack of enforcement of environmental

protection and possible anti-corruption issues

HUMAN RIGHTS • Many ‘unknowns’• Food safety and human

rights • Land transfer issues for

manufacturing

LABOUR ISSUES • Safety and handling of

chemicals • Potential for other labour

issues – child labour,overtime, etc…

sea-food processing plants; slaughter houses;beverage plants; fruit and vegetableprocessing plants; instant noodlemanufacturers, confectionary manufacturersand many others. Like other parts ofmanufacturing, there are numeroushousehold and village level enterprises.

The global recession has impacted this sectorin Vietnam with reduced global prices and

falling demand with reports of some firmsreducing output by 50 to 60 percent8.

KEY ISSUES FOR THE GLOBALCOMPACT IN VIETNAM

Table 2 below provides an overview of the keyissues for the food processing Industry inrelation to the Global Compact.

OTHER HUMAN RIGHTS RELATED ISSUES For many stakeholders, human rights arelinked to labour issues. Concerns were notedon safe working conditions, overtime hours,gender issues and women’s rights.

KEY LABOUR ISSUESThe key concern here is the lack of safetymeasures for workers who are in contact withchemicals. Some stakeholders noted thatthere were also other potential labour issuessimilar for other manufacturing sectors rangingfrom: child labour and hazardous labour aswell as excessive overtime (although this is notas well researched or documented comparedwith the garments and shoe industries).

KEY ENVIRONMENTAL ISSUESEnvironmental issues in food processing wasa serious concern for nearly 80 percent of thepeople we spoke to. Recent media attentionaround cases such as Vedan and San Miguelhave helped to put environmental issues infood processing in the spotlight. Manystakeholders believed that food processingproducts in Vietnam are competing on price.Thus, investment in a proper waste treatmentcould be too expensive.

Table 2: Global Compact Issues in Food Processing

“Fish processing firms – if you visit you maysee that the premises are so clean, evencleaner than some hospitals. They used a lotof chemicals to clean the premises, then theyjust discard them it to the environment.”(A manager)

A lot of small, traditional food processingpremises use manual techniques andseriously pollute the environment. Wastewater discharge from village level enterprisesis a serious problem with high concentrationsof toxic substances exceeding permittedstandards.

There is a challenge with enforcement. Onestakeholder commented that “environmentalprotection certificates (in the food processingindustry) currently issued are not worth thepaper they are written on” (representativefrom a multinational).

CORRUPTION RELATED ISSUES There is a perceived lack of enforcement ofenvironmental protection linked to corruption.Basically questions were raised that if the rightperson is ‘facilitated’ then a blind eye can beturned on environmental issues.

8 In 2009 both of these companies were in the news forreported water pollution

Global C

ompact N

etwork Vietnam

36

Global C

ompact N

etwork Vietnam

37

OPPORTUNITIES ANDDRIVERS

SIZE, FDI AND EXPORT

As indicated above, the industry is quitesignificant for Vietnam in terms of size with agrowing level of foreign investment and animportant contributor to Vietnam’s globalexports. A combined estimate for foodprocessing and packaging is that it accountsfor about 40 percent of total export turnover 10.

SEAPRODEX controls the lion’s share offishing and aquaculture related exports. Thecompany appears to be taking a leadershiprole in relation to some aspects of CSR andhas recently worked with the National Instituteof Nutrition to reduce iron deficiencyanaemia, marking the “first time that thehealth sector and manufacturing anddistribution companies have joined forces tofight malnutrition in Vietnam.”11 The projecthas support from the Global Alliance forImproved Nutrition (GAIN). While this is notspecifically addressing the principles of theGlobal Compact it shows how somecompanies are looking to use their coreproduct and services to address developmentchallenges in the country.

10 Industry - Vietnamhttp://www.nationsencyclopedia.com/Asia-and-Oceania/Vietnam-INDUSTRY.html#ixzz0Xx4AZ8Sl

11 quote from NIN director Mr. Nguyen in VN news 215 08

12 http://xttmnew.agroviet.gov.vn/loadasp/tn/en/tn-spec-nodate-detail.asp?tn=tn&id=20801713 Huong. Huong, Bui Thi Lan. 2008 The Perspective on Corporate Social Responsibility in Emerging Countries:

The Case of Vietnam Ouverture International - International Vision CFVG Excellence Europeen en ManagementNo. 12 June 2008

13 List of priority industries and cutting edge industries for the period 2007 to 2010 with the outlook to year 2020(issued with Decision 55-2007-QD-TTG of the Prime Minister of the Government dated 23 April 2007).

ON-GOING REMEDIATION

Initiatives such as the cleaner production workof UNIDO have touched on the foodprocessing sector. Given the severity of theissues, we did not see a significant amount ofremediation in this industry. However, the sub-sector has recently had an injection of financingwith the ADB committed to a loan of USD 95million to support the industry to adhere tohealth, safety and quality requirements12.

PUBLIC INTEREST AND OTHERINFLUENCING FACTORS

While food safety has been a growingconcern in Vietnam, the milk scare whichbegan in the PRC in 2008 and also affectedVietnamese supplies, raised further concernsabout product safety13. In the first 6 monthsof 2009, the Food Safety and HygieneDepartment reported that food poisoningcases were up 55 percent compared with thesame period last year. Since November 2008,exporters to the United States have had toproduce certificates to the effect that theproducts are safe and not harmful to childrenand adult consumers. Manufacturers andimporters will announce their voluntary andmandatory standards, which must be certifiedby independent third parties through a test ofeach product or a reasonable testingprogram. The United States is Vietnam’s

biggest export market with 2008 exportstotalling $10.2 billion.

GCNV’S ABILITY TO ADD VALUE ANDRECOMMENDATIONS

Unilever has been an early signatory to theGlobal Compact Network in Vietnam and is arecognised leader from the perspective ofmany stakeholders in terms of CSR in Vietnam.Companies such as Duc Viet Foods Joint StockCompany, Hung Cuong Trading Company,Hung Trung Viet Joint Stock Company are allGC Vietnam signatories and food producers.Processing of agricultural, forestry andaquaculture products is a priority industry forthe periods 2007-2010, 2011-2015 and2016-2020 and will play a key role in helpingVietnam achieve its development goals14.

It is recommended that food processing is a(sub) sector that the GCNV should follow upwith. As noted above there are substantialenvironmental issues along with social issuesthat need to be addressed. Given the transitionfrom an agrarian to an industrial economy foodprocessing has some natural strength as anindustry to focus on. Agriculture itself will be abigger source of employment but there is morelimited capacity for the GCNV to act (as infishing). By moving one step up the value chainto food processing there is a potential to addvalue to the development of Vietnam.

Global C

ompact N

etwork Vietnam

38

Global C

ompact N

etwork Vietnam

39

2. CONSTRUCTION

While construction itself does not factor as highas other industries in terms of contributiontowards GDP, the construction material industryhas recorded an annual growth rate of morethan 17 percent higher than the wholeindustry’s average growth taking intoconsideration products such as cement,ceramic tiles, artificial granite, porcelain andglass15. As urbanisation continues to increasethe construction industry has boomed.Construction creates the infrastructure for themanufacturing and other industries. Some ofthe current large scale construction projectsinclude the Son La hydroelectric power plant,Dung Quat oil refinery, Ca Mau thermo-electric plant, Buon Lop hydroelectric powerplant, Thu Thiem Bridge, and Xekamanhydroelectric power plant No 3.

The Industry is a source of employment fornearly 2.2 million people and alsoparticularly for migrant and unskilled workers.According to the GSO, construction accountsfor 5.13 percent of the jobs for the workingpopulation although it is likely that this is nota true reflection of the size of the sector giventhe unofficial nature of much of the work. Italso provides an additional source of incomefor those predominantly reliant on agricultureduring the off-season. As noted below, the

unofficial nature of much of the work posessubstantial risks.

Larger companies such as Song DaConstruction Corporation, the NationalCement Corporation, the Hanoi ConstructionCorporation and numerous others are underthe Ministry of Construction. Since 2005 andthe enterprise law the number of privatecompanies and corporations has increasedsubstantially. According to the most recentavailable data from the GSO, nearly 97percent of ownership in the constructionsector is now national and private with only2.6 percent state ownership and less than onepercent foreign direct investment16.

While there has been a focus in recent yearson updating production techniques there is aheavy reliance on outdated machinery and16 percent of cement and half of all bricksare still produced manually17.

KEY ISSUES FOR THE GLOBALCOMPACT IN VIETNAM

Table 3 below provides an overview of the keyissues for the Construction Industry in relationto the Global Compact.

OTHER HUMAN RIGHTS RELATED ISSUES The issues on human rights linked to labourrights and issues around safe workingconditions, overtime hours, and child labour.There were also concerns over land use andhow land is taken and how communities arecompensated. As the Ministry of NaturalResources and the Environment’s websiterecently reported in late 2008, city inspectorsfound that Construction Company 623 in ThuDuc District of HCMC had used over 100mof a local canal, without Government’spermission18.

KEY LABOUR ISSUESThe key concern raised by stakeholders weinterviewed was in regards to safety onconstruction sites. Recent stories in the local presshave highlighted the health and safety risks inthe construction industry. Many workers aretemporary and unskilled and from rural areas.Overtime hours were a concern especially in abusy time when the construction needs to getfinished. Some stakeholders raised concernsregarding illegal migrant workers on large scaleinfrastructure sites. In such cases there are noformal contracts and there is limited ability of the

15 2008 Vietnam Country Report from the 14th Asia Construct Conference16 GSO17 BMI construction report 18 http://www.monre.gov.vn/monreNet/default.aspx?tabid=259&idmid=&ItemID=58333

ENVIRONMENTAL PROTECTION • Many stakeholders raised concerns

related to: dirt, noise, solid waste,transportation of materials

• Lax building standards and buildingsafety

CORRUPTION • Stakeholders perceive corruption to bea big issue for this industry • Tender law and fake bidders (red troopand blue troops)

HUMAN RIGHTS • Linked to land issues • Linked to labour issues

LABOUR ISSUES • Work safety • Overtime • Unprotected labour • Temporary workers from rural areas and• Increasing migrant workers (from abroad)• Child labour

Table 3: Global Compact Issues in Construction

Global C

ompact N

etwork Vietnam

40

Global C

ompact N

etwork Vietnam

41

labour inspectorate to follow up, monitor andensure labour protection.

Child labour is recognised as being an issue inconstruction. Even when a construction sitedoes not have children ‘on its books’, thepeople working may not be the same as onpaper. Participants cited the collapse of CanTho Bridge as an example: a lot of people arenot the same as the names in registered papers.

KEY ENVIRONMENTAL ISSUESThe construction industry has hugeenvironmental impacts. If properly managedthe construction industry has the potential tomake significant contributions towardsachieving Agenda 21 in Vietnam. Peoplecommented that there were few measures toprotect the environment in the constructionindustry and flagged concerns over dirt,

noise, solid wastes, etc. There are also clearlinks to health and safety issues in this respect.

CORRUPTION RELATED ISSUES This issue raised “red flags” for many of thestakeholders we interviewed who wereconcerned with corruption at all stages ofconstruction.

Bidding: Although Vietnam has a tender law, theimplementation of the law depends a lot on theindividual who manages the tender. In manycases, there are “red troops” and “blue troops”(red troops refers to the real bidder, while bluetroops refer to fake bidders, who are alsomanipulated by the red troop, but participate inthe tender to make the tender look lawful).

“The tender process has not been “clean” inpractice of many cases. It depends a lot onthe person in charge.” (A government official)

Implementation: The media have reported anumber of corruption incidents in theconstruction phase. Stakeholders pointed outthat these incidents are only part of the issue.Corruption happens in all phases: designing,monitoring, and construction. In thedesigning phase, if the “investor” (normally arepresentative of the government) iscorrupted, the designers could increase thespecification of the construction. Then, duringthe construction phase, they could take awaysome materials without worrying about thequality of the construction. Similarly, therewere concerns over land use during theconstruction phase and how this isappropriated by certain departments.

OPPORTUNITIES ANDDRIVERS

SIZE, FDI AND EXPORT

While the construction industry itself is not thebiggest industry in terms of contribution to GDP,when placed together with the constructionmaterials and related industries it has a verysignificant impact. The industry is mostlyinternal facing although some of Vietnam’scompanies have bid and won projects inneighbouring countries such as Laos.

ON-GOING REMEDIATION

A local green building council has beenlaunched with a Vietnam specific ratingsystem, Lotus, currently being developed. Therating includes credits for conservation (water,energy and materials); ecology andenvironment (site ecology and waste andpollution); health and well being; climatechange (adaptation and mitigation);community and social; along withmanagement approaches. Essentially it isadapting global standards such as LEED,

Global C

ompact N

etwork Vietnam

43

Global C

ompact N

etwork Vietnam

42

Green Star and BREAM for the VietnameseMarket. Founding members have mostly beeninternational property firms such as CBRE andarchitectural firms such as Woods Bagot andROK. The council is affiliated with the Ministryof Construction and other partners.

Other related work and initiatives include theConstruction Transparency Initiative (CoST)which Vietnam joined in 2008 which aims toenhance the accountability of procuring bodiesand construction companies for the cost andquality of public-sector construction projects19

along with work that is being undertaking bythe Ministry of Construction with the support ofDFID to provide more financial transparencyin the construction industry.

PUBLIC INTEREST AND OTHERINFLUENCING FACTORS

Given the significant attention to corruption ininfrastructure as well safety there has beenincreasing attention on linked issues in general.

GCNV’S ABILITY TO ADD VALUE ANDRECOMMENDATIONS

Based on the research and analysis webelieve that the GCNV could potentially addvalue in this industry. Holcim is an active

member of the GCNV. They are perceived bymany stakeholders to be playing a leadershiprole in the cement industry which is animportant part of the construction industry.They could help to champion work in thisarea in general.

While construction is lower in terms ofcontribution to GDP it links to otherindustries and infrastructure. It is large interms of employment and many issues toaddress throughout the industry. Some ofthese are critical with potential to causedisaster such as shoddy building materialsand unsafe infrastructure. There is currentlya lack of remediation efforts. VCCI couldleverage its government links and potentiallybring together some key players.Champions in the construction materialsindustry such as Holcim could also help toplay a pivotal role.

Crude oil was responsible for 17.5 percent ofVietnam’s exports in 2007 and the country isone of the largest producers in South-EastAsia. To date it has contributed nearly USD30 billion to the State’s budget and hasattracted large sources of foreign investment.The industry has been mostly upstream withoffshore oil sourcing. While it is significant interms of income it is not as significant in termsof employment. Mining and quarrying(including oil and gas) employ roughly 1.7million people according to recent GSOfigures but this is higher for coal and metalore mining and less substantial for extractionof petroleum and natural gas due to thenature of the work20.

In February 2009, the first downstream oilrefinery was opened in Quang Ngai provincewith another expected to be operational in2013 and a third is in preparation.

The industry is state-controlled withPetroVietnam playing the leading role who,together with Vietsovpetro are the principlepartners for foreign investment and controlthe country’s oil production. PetroVietnam isrequired to participate in all ventures. The

Russian state company Zarubezhneft is thebiggest foreign producer (via the VietsovpetroJV), while Petronas, Chevron andConocoPhillips are all significant investors.Between 2006 and 2008, Premier Oil andSOCO International along with Talisman allmade significant offshore discoveries.

The islands and surrounding waters in theSouth China Sea are disputed betweenVietnam and China (with other countries alsolaying claim). The oil reserves offshore havetherefore been a potential source of tensionbetween the countries and there have beenrumors in the press that China has putpressure on some companies over their oilexploration in Vietnam. In 2009 BPannounced a withdrawal from some of itsVietnam operations citing economic reasons.

19 CoST web page. URL: http://www.constructiontransparency.org/CountriesSupporters/Countries/Vietnam/ 19 GSO

3. OIL AND GAS

THE EXTRACTIVEINDUSTRIES

Global C

ompact N

etwork Vietnam

44

Global C

ompact N

etwork Vietnam

45

KEY ISSUES FOR THE GLOBAL COMPACT IN VIETNAM

Table 4 below provides an overview of the key issues for the Oil and Gas Industry in relationto the Global Compact.

Table 4: Global Compact Issues in Oil and Gas

ENVIRONMENTAL PROTECTION • Concern over spills

CORRUPTION • Nothing specific raised

HUMAN RIGHTS • Nothing specific raised

LABOUR ISSUES • Health and safety • Uncertainty over labour issues • Off shore issues

OTHER HUMAN RIGHTS RELATED ISSUESNothing specific was raised nor uncovered inthe additional research. Some NGOs haveraised concerns over how the indigenouspopulations on shore near the off shorediscoveries will benefit from the oil.

KEY LABOUR ISSUES A general perception exists that peopleworking in the oil and gas industry are betteroff in terms of remuneration and benefitshowever there is a lack of available data inVietnam. With offshore labour it is possiblethat many issues go undetected. Generally,the stakeholders we interviewed did not raisea lot of concerns in this area.

KEY ENVIRONMENTAL ISSUESThe biggest concern raised by stakeholdersrelated to potential oil spills. In 2007, an oilspill washed ashore along the central coast

near Danang (including the UNESCOheritage site of Hoi An) with spills affecting 20provinces damaging the environment andwreaking havoc on fisherman lives. The spillswhich were originally deemed to be fromoutside of Vietnam but conclusions wereunclear and may have also come from oil rigswithin the borders of the country.

CORRUPTION RELATED ISSUES The general perception of stakeholders weinterviewed was that this is an industry wherethere is not a lot that is known and is generallyquite secretive. Some were clear in voicingconcerns over lack of transparency and howthe benefits from the oil and gas industrywould be helping to address povertyalleviation. Business Monitor International’sreview of the Oil and Gas Industry for Vietnamhas flagged the fact that corruption and ruleof law is a major business risk in Vietnam.

OPPORTUNITIES ANDDRIVERS

SIZE, FDI AND EXPORT

Crude oil is the number one export forVietnam and a significant contribution to theGDP. It is not currently one of the largestemployers. Foreign investment is significantand always in partnership with a Vietnamesecompany.

ON-GOING REMEDIATION

Aside from some work around transparency,there is little remediation efforts in this industry.

Public interest and other influencing factors: Given the recent oil spills, the industry hasreceived a fair amount of press in the last year.However, other social and environmentalissues have received little coverage.

GCNV’S ABILITY TO ADD VALUE ANDRECOMMENDATIONS

Talisman has been an early founding memberof the GCNV. In addition the CanadianEmbassy with the involvement of Talisman

recently organised a workshop to share goodpractice in the extractive industries Althoughsome stakeholders have commented that thismay be an industry where it would be difficultto work in, given the nature of the GCNV webelieve there is potential for the network toadd value and work with others.

Vietnam is now ranked South-East Asia’s thirdlargest oil producer. The profits from the oilbusiness have the potential to make significantcontributions towards poverty alleviation andsustainable development in Vietnam.However, experience and lessons learned fromother countries stresses that the industry mustgrow and develop in a transparent manner inorder for developmental gains. The networkhas potential with champions such asTalisman and interest shown from embassiesand bilateral donors to help to take forwardsome work in this area. Clearly initiatives byorganisations such as TransparencyInternational are important and the GCNVcould help to legitimise and strengthen theirefforts. We would recommend that theNetwork give serious consideration toleveraging its strengths and taking forwardwork related to the extractive industries inVietnam.

Global C

ompact N

etwork Vietnam

46

Global C

ompact N

etwork Vietnam

47

OTHER HUMAN RIGHTS RELATED ISSUES The most pressing human rights related issuelinks to labour regarding safe workingconditions for miners. Other human rightsrelated issues which stakeholders commentedon were for land rights issues (when minesneed to be established) and cultural heritageissues for indigenous populations (particularlyin the highlands).

LABOUR ISSUESA lack of safe working conditions was the keyconcern raised. While there may not befrequent reports in the media of accidents, theparticipants in the focus groups and thepeople we interviewed suggested that safeworking conditions for mining workers is aserious issue in Vietnam. Labour accidentsand occupational diseases are still high in this

4. MINING

KEY ISSUES FOR THE GLOBAL COMPACT IN VIETNAM

For many of the issues there were lots of ‘unknowns’ from the perspectives of the stakeholderswe interviewed. This was matched with a lack of empirical research in many of the areas.

Table 5: Global Compact Issues in Mining

ENVIRONMENTAL PROTECTION • Severe environmental issues • Bauxite mining raised by numerous

stakeholders - untreatable caustic toxic redmud in area of significant biodiversity

CORRUPTION • Concerns over bribery and facilitation

payments • Limited information available• Lack of transparency raising concerns over

corruption

HUMAN RIGHTS • Relocation • Indigenous populations

LABOUR ISSUES • Health and safety • Hazardous and unsafe working

conditions • Less media attention but serious • Migrant and unprotected workers

In 2007, mining accounted for 10 percent ofGDP in Vietnam21. There was general declinein output in this sector in 2007 and 2008which has been partly attributed to a policyon conserving natural resources22. Theownership of the sector is 25.5 percent state,9.7 percent private and 64.8 percent isforeign investment23. In terms of statistics, theGSO defines the overarching sector asmining and quarrying which then includeswithin it: mining of coal; oil and gas; miningof metal ores and quarrying of stone andother mining. For the purpose of this research

we have initially separated out oil and gasfrom other types of mining and quarrying. Inaddition to petroleum, coal is a primarymineral export while antimony, bauxite,chromium, gold, iron, natural phosphates, tinand zinc are also mined in country.According to most recent figures roughly 1.7million people work in the mining andquarrying industry.

In 2009, mining was brought to the forefront ofthe national media due to the concerns over thebauxite mine in the central highlands. Vietnamhas one of the largest bauxite reserves which areused to produce aluminium. To tap this, thegovernment’s master plan calls for investmentsof around USD 15 billion by 2025. However,the reserves are situated in the central highlands- an area of rich biological and cultural diversity.Local and international concerns have beenraised over the potential adverse environmentalimpacts and on livelihoods and local crops suchas coffee and cacao. Presently, the VietnameseState Owned Enterprise Vinacomin has movedahead with operations and contracted asubsidiary of Chinalco for one mine and Alcoais working with them to ascertain feasibility fora second mine24.

21 GSO 2007 data 22 http://www.asiantechenterprise.co23 2007 GSO figures 24 http://blog.socialrisks.com/2009/05/vietnam-risk-

bauxite-mines-china-and.html

Global C

ompact N

etwork Vietnam

48

Global C

ompact N

etwork Vietnam

49

OPPORTUNITIES ANDDRIVERS

SIZE, FDI AND EXPORT

While the mining sector’s contributiontowards GDP has decreased somewhat inrecent years it is anticipated that it willcontinue to be significant for Vietnam in thecoming years and its growth is part of thestrategic plan of the Government.

ON-GOING REMEDIATION

Aside from the work of TransparencyInternational and embassies such as theCanadian Embassy, along with oneorganisation working specifically on theseissues, we did not encounter many championsfor driving the GC principles in the miningindustry in country.

Public interest and other influencing factors:Given the events over the last year particularlyin relation to the Bauxite mine there has beensome growing awareness and stakeholderinterest in mining and environmental andsocial issues in Vietnam.

GCNV’S ABILITY TO ADD VALUE ANDRECOMMENDATIONS

Some stakeholders raised concerns over theability of the GCNV to add value in this giventhe perceived sensitivity of some of the issues.

However, given the nature of the Network itmay be better placed than others to add valueand should seriously consider this. Given thepotential significant impacts on issues ofconcern to the global compact, the lack ofremediation efforts and ability to capitalise onthe nature of the network we think there issome potential.

In other countries, issues around transparencyhave been directly linked to mining andpoverty alleviation. There was interest in theapproach of the Extractive IndustriesTransparency Initiative and the benefits thatthis could bring to the industry in Vietnam.There have been some initial discussionsabout this in Vietnam. The CanadianEmbassy has also considered bringingtogether a working group to look at issuesrelated to CSR and the extractive industries inVietnam.

As mining is an industry which has thepotential to contribute to Vietnam’s economybut also one that needs to be managed welland has significant environmental and socialimpacts, it is an area we think a network suchas the GCNV could add value. This could bein relation to labour issues and providingbusiness strategies for introducing safetymeasure’s for mining which could alsoinclude experiences from other countries andways to properly manage environmentalimpacts. We therefore are recommendingthat mining be combined with oil and gas andthat the network do some further work onissues for the extractive industries.

sector and while the breaking of labourregulations may be widespread, investigationand supervision are inadequate25.

There were also concerns raised over migrantworkers who may be entering Vietnam ontourist visas (particularly Chinese migrantworkers on the Bauxite mine) and who maynot be protected by the national labour law.

KEY ENVIRONMENTAL ISSUESNearly 40 people we spoke to raised a ‘redflag’ for environmental issues in relation tomining. Due to the nature of the businessthere are adverse environmental impactswhich need to be carefully managed. InVietnam, traditional coal mining is well knownfor its pollution problems for the miners andthe people in the surrounding communities.

The current government decision on miningbauxite in the Highlands also triggered a lotof concerns about environmental issues.While the caustic red mud was flagged bysome interviewees most people we spoke towere not aware of the specific risks related tothis type of mining.

CORRUPTION RELATED ISSUES There were not a lot of specific concerns ordiscussion on this issue but it was an areawhere many stakeholders raised questionmarks and potential concerns. These relatedfrom concerns over bribery and facilitationpayments to a lack of transparency whichgenerally raises concern over corruption.One interviewee noted how rumours hadspread around regarding an allegedfacilitation payment for a mining project.

25 Friedrich-Ebert-Stiftung. 2008

Global C

ompact N

etwork Vietnam

5150

II - MANUFACTURING: LOTS OF RISKS AND OPPORTUNITIESBUT OTHER REMEDIATION EFFORTS INPLACE OR STARTING…

5. MANUFACTURING

In recent decades the share of manufacturingtowards GDP has increased significantly.Overall, manufacturing is responsible for 21percent of Vietnam’s GDP and employsroughly 6.4 million people accounting for 14percent of the working population.Productivity has increased 3.9 times over theyears since 1980 to VND11.4 million perworker in 200726. This has grown as the shareof labour in agriculture has declined and theeconomy has shifted from an agricultural toa manufacturing economy.

Manufacturing was responsible for 44percent of exports in 200727. Textiles,chemicals and electrical goods,cigarettes/tobacco and food processing areoverall the top manufacturing sectors inVietnam. For the purpose of this research wehave looked at general issues formanufacturing and then pulled out garments,textiles and shoes, as well as food processingand wood related manufacturing based oninitial assumptions of where there wereopportunities.

While manufacturing has been a source ofgrowth, industries which are often regarded

as competitive such as textiles, garments,furniture and footwear have a very low profitrate. For instance, the rate of profit for theseindustries in 2006 was as low as 0.11percent, 0.61 percent, 1.99 percent and even-0.05 percent (a minor loss), respectively.Most manufacturing in Vietnam involves athird party working on sub-contracts utilisingcheap labour to produce low value-addedproducts for large foreign-owned firms andare dependent on imported intermediateinputs. By and large, manufactured productsare not diversified, and product quality isrelatively poor compared with global norms.Overall, the structure of the manufacturingsector is mostly domestic non-state privateenterprises (86 percent), foreign ownership(11 percent) and state ownership (under 3percent)28. However this varies significantlybetween sub-sectors with 42 percent foreigninvestment in garments, 32 percent in textilesand 63 percent in leather products. Stateownership dominates the tobacco industry at99 percent of ownership. Furnituremanufacturing is approximately 47 percentfor both foreign ownership and local privateownership with the remaining being stateinvolvement29.

26 VIR article 27 GSO 28 GSO 29 GSO

Global C

ompact N

etwork Vietnam

52

Global C

ompact N

etwork Vietnam

53

KEY ISSUES FOR THE GLOBAL COMPACT IN VIETNAM

(Manufacturing in general: Food processing has been covered separately in Section 4 above.)

Table 6: Global Compact Issues in Manufacturing (General)

ENVIRONMENTAL PROTECTION • Severe issues • Concerns over industrial parks

where systems are supposed tobe in place but not adhered to

• Limited enforcement • Lack of incentives

CORRUPTION • Labour rights as human rights • Women with small children

HUMAN RIGHTS • Labour rights as human rights • Women with small children

LABOUR ISSUES • Minimum wage vs. living wage• Child labour still persists particularly in ‘non-

branded’ factories • Insurance avoidance: SMEs try to avoid paying

insurance • Hazardous work and safe working conditions• Sub-contracting. While larger firms may appear

better there is a lot unseen in next tier and sub-contracting

• Industrial parks and quality of life

issue is more linked to the concept of a livingwage – particularly with the rising inflation in2008. As one government official noted:“The minimum wage is too low. If we only relyon it as a measure to protect our labourers,we are not protecting them well.”

Child labour continues to be an issue. Whileimage conscious brands working extensivelyon auditing and remediation may have beenable to tackle this issue in their factories itcontinues to be a real issue for most othermanufacturers in the country.

Insurance for workers: Most of private smalland medium sized enterprises (SMEs) havetried to avoid paying insurance for theirworkers. In other cases, the “nominal” salary– as a basis for insurance payment – is verylow (to avoid paying insurance), while the realsalary was much higher. In many cases, eventhe workers themselves do not want to pay forinsurance and prefer to take the money asincome. This points to the fact that, one theone hand, the workers may not have goodknowledge of insurance purposes – they don’teven care or want it. On the other hand, theinsurance services in Vietnam may not beregarded as helpful.

Working conditions: Access to safe and cleanworking conditions was also a key issueraised by many stakeholders in thediscussions. This will vary between industrysub-sectors but was an issue in all.