Embed Size (px)

Citation preview

February 2009

Report Series

Office of the Chief Economist Economics Department Samba Financial Group P.O. Box 833, Riyadh 11241 Saudi Arabia [email protected] +966 1 477 1060 +44 20 7355 4411 This and other publications can be Downloaded from www.samba.com

The UAE Economy: Sustainable in the Face of a Serious Global Recession Highlights

The UAE’s strong macroeconomic fundamentals and quick policy response to the global financial crisis should help support a positive growth momentum during 2009, despite the deep global recession and sharply lower oil revenues. Large external savings will provide the financial strength to inject liquidity into the banking system and to support fiscal stimulus packages. Together this should sustain GDP growth of around 0.5 percent, down from 6.8 percent in 2008.

The UAE has not escaped the impact of the current global financial

turmoil and has seen its stock prices slump, real estate sector weaken, access to external finance curtailed, and domestic liquidity conditions tighten. Dubai government related entities, in particular, are finding it hard to raise finance and have seen their CDS rates rise steeply. Government efforts to support domestic bank liquidity will certainly help, but it is inevitable that some of the UAE’s many large scale projects will be cancelled, and credit growth will slow.

The central bank’s focus has now shifted away from curbing record

inflation rates towards ensuring banks have adequate liquidity. The abrupt change in liquidity conditions has also meant that earlier concerns over the policy constraints of the exchange rate peg to the dollar have abated. Inflation is expected to slow sharply from 14 percent in 2008, to 4 percent in 2009 in response to a relative strengthening of the US dollar, falling international commodity prices, an easing of supply bottle necks as projects are cancelled, lower rents, and slower credit growth.

Lower prices and production will see oil revenues slashed during 2009,

but the fiscal and external balances are projected to remain in surpluses at 4.8 and 4 percent of GDP respectively. While sharply lower than the 20-30 percent of GDP achieved in 2008, these surpluses, augmented by recourse to large external assets, will help provide welcome financial ballast.

The extremely uncertain and fragile state of global financial markets and

the deepening global recession present significant downside risks to the outlook for the UAE. A more pronounced global downturn could see a protracted decline in tourism, foreign investment and credit flows to the UAE, and further falls in oil prices. This would curtail scope for public spending and investment, and promote a more pronounced contraction in business activity which in turn could put banks and financial institutions at risk.

Main Economic Indicators 2005 2006 2007 2008e 2009f Nominal GDP ($ bn) 135.3 164.0 200.5 272.7 215.3 GDP per capita ($ '000) 33.9 38.8 44.8 57.4 42.8 Real GDP (% change) 8.2 9.4 6.1 6.8 0.5 Hydrocarbon GDP 1.6 6.5 -1.2 3.3 -11.9 Non-hydrocarbon GDP 10.8 10.4 8.7 7.9 4.3 Nominal GDP (% change) 20.8 21.3 22.2 36.0 -21.1 Hydrocarbon GDP 40.5 37.4 18.3 61.2 -53.7 Non-hydrocarbon GDP 12.4 12.7 24.8 20.5 5.8 CPI inflation (% change) 6.2 9.3 11.1 14.0 4.0 Hydrocarbon exports ($ bn) 55.1 70.1 84.4 123.8 58.8 C/A balance ($ bn) 24.2 35.9 36.2 61.7 8.7 (% GDP) 17.9 21.9 18.1 22.6 4.0 External debt ($ bn) 41.0 82.3 133.3 150.0 150.4 (% GDP) 30.3 50.2 66.5 55.0 69.9 Fiscal balance (Dh bn) 101.5 163.9 196.4 304.7 37.8 (% GDP) 20.4 27.2 26.7 30.4 4.8 Cent gov debt (Dh bn) 70.0 91.2 117.9 138.0 159.9 (% GDP) 14.1 15.1 16.0 13.8 20.2 Memoranda: Oil price (WTI; $/b) 55.2 66.3 72.6 100.0 55.0 Crude oil prod (m b/d) 2.44 2.52 2.49 2.57 2.25 Nat gas prod (m boe/d) 803 828 865 900 936

3

February 2009

Table of Contents

The Global Context 4

The UAE: A Federation of Seven Dominated by Two 5

Economic Developments and Prospects: 2007-2009 7

Fiscal and External Positions 11

Monetary and Financial Sector Developments 14

Monetary Policy Challenges 18

Risks to the Outlook 21

4

The world is heading for a major recession amid financial crisis.

World GDP is expected to contract by 0.9 percent in 2009.

Spreads in funding markets remain high and credit flows constrained.

The Global Context A global recession amid financial crisis

The world is still grappling with the most dangerous financial shock in mature markets since the 1930s. Buffeted by this crisis which has seen the collapse of major international banks and extraordinary efforts by authorities to stabilize the turmoil in global financial markets, almost all advanced economies are now in, or moving into, recession. Output in advanced economies is expected to contract by 2 percent in 2009, with some pick up possible late in the year assuming financial markets recover, and that large fiscal stimulus packages have an impact. Growth in emerging markets is also slowing sharply, and this trend will continue through 2009. Overall emerging market growth rates should hold up better than during previous global downturns, but this will be insufficient to prevent a contraction in global GDP by 0.9 percent. This represents a sharp reversal from growth of 3.1 percent in 2008 and 5 percent in 2007. In addition, even this weak projection is subject to considerable downside risk, particularly if financial market conditions remain strained and emerging markets prove less resilient than currently assumed.

The World Economic Outlook 2006 2007 2008e 2009f Real GDP growth (percent, annual) World 5.1 5.0 3.1 -0.9 United States 2.8 2.0 1.2 -2.8 Japan 2.4 2.1 0.2 -3.5 Euro Area 3.0 2.6 0.9 -2.5 Emerging markets 7.3 7.5 5.9 1.0 Official policy rate (end period) United States 5.25 4.24 0.00 0.00 Japan 0.25 0.50 0.30 0.10 Euro area 3.50 4.00 2.50 0.80 ($/barrel, period average) WTI crude oil price 66.3 72.4 100 55 Financial conditions will remain very difficult

Financial conditions are expected to remain very difficult over the next 12 months. Despite wide-ranging policy measures to provide additional capital and reduce credit risks, spreads in funding markets remain high and credit flows constrained - emerging bond markets virtually shut down for a period of time during the fourth quarter of 2008. Advanced economies’ bank balance sheets are being cut back through asset sales and the retiring of maturing credits. Credit risks have risen as deteriorating economic and financial conditions have pushed up loan loses, and the IMF now estimates that write downs by European and US financial institutions will exceed $2 trillion.

Emerging markets are also feeling the effects of advanced economies’ financial difficulties, principally through the abrupt pull back from emerging market assets and higher financing costs. Borrowers in emerging markets, both corporate and to a lesser extent sovereign, remain vulnerable to continued deleveraging and credit retrenchment, and may struggle to roll over large amounts of existing debt in the coming years. Reduced access to capital markets has already pushed corporates to

5

Given the still uncertain outlook for financial markets, there remain significant downside risks to global growth projections.

O

30

50

70

90

110

130

150

Jan-

07

Mar

-07

May

-07

Jul-0

7

Sep-

07

Nov

-07

i l and Gas Prices

Jan-

08

Mar

-08

May

-08

Jul-0

8

Sep-

08

Nov

-08

Jan-

09

4

5

6

7

8

9

10

11

12

13

14

WTI (USD/bbl)Henry Hub Natural Gas S

This report has been prepared on the basis of a $55/b average oil price assumption for 2009 which represents a 45 percent drop over 2008.

pot Price (USD/MMBtu; rhs)

The UAE economy is the second largest in the Arab world after Saudi Arabia.

tap local banks for short-term loans, shortening the maturity structure of their debt and further raising roll over risks. This is particularly true in the UAE where banks and Dubai government related entities face challenges in rolling over large maturing loans in 2009-2010.

Significant downside risks remain

Given the still uncertain outlook for financial markets, there remain significant downside risks to global growth projections. Current financial stresses and credit constraints from deleveraging could be deeper and more protracted, and problems in US and European housing markets more extensive and long lived. In addition, emerging market growth prospects will depend significantly on a resumption of substantial capital flows.

Commodity prices, including oil, will fall in 2009

Following a sustained run-up over the last few years and extreme volatility over the last few months, commodity prices have fallen back in response to slowing global growth. Having hit a record high of over $145 a barrel (b) in mid-2008, oil prices plunged, ending the year at around $40/b. While in the longer-term oil markets are expected to remain tight, the dire outlook for demand and scheduled increases in non-OPEC production, are expected to result in sharply lower average oil prices in 2009.

Projecting oil prices under current global circumstances is extremely difficult. Much will depend on how severe the global recession turns out to be, how successful OPEC is in abiding by agreed production cuts, what happens to financial and credit markets, and whether and when markets start to worry about longer-term supply constraints again. While there are considerable downside risks, this report has been prepared on the basis of a $55/b average oil price assumption for 2009 which represents a 45 percent drop on the 2008 average of $100/b. The United Arab Emirates: A Federation of Seven Dominated by Two The United Arab Emirates (UAE) is a federation made up of seven emirates: Abu Dhabi, Dubai, Sharjah, Ajman, Umm al Qaiwan, Ras al Khaimah and Fujiarah with a total population of 4.5 million and an expanding economy approaching $273 billion in 2008 – the second largest in the Arab world after Saudi Arabia. Since the adoption of

6

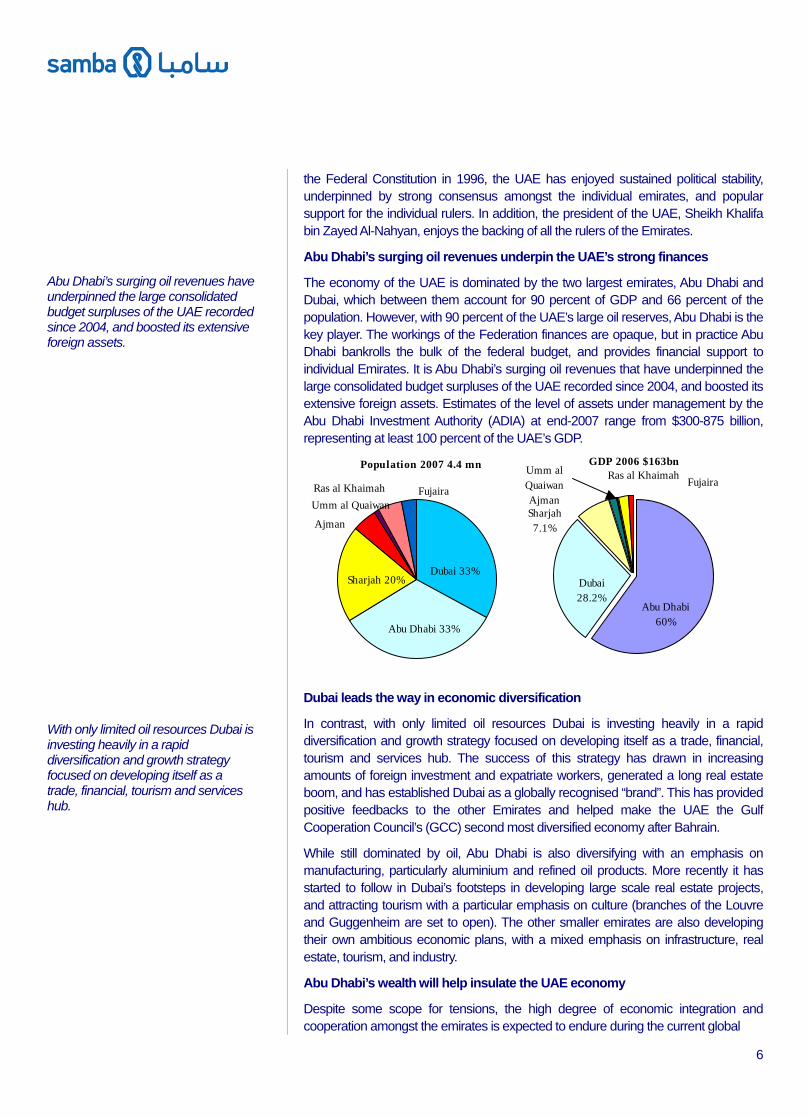

Abu Dhabi’s surging oil revenues have underpinned the large consolidated budget surpluses of the UAE recorded since 2004, and boosted its extensive foreign assets.

With only limited oil resources Dubai is investing heavily in a rapid diversification and growth strategy focused on developing itself as a trade, financial, tourism and services hub.

the Federal Constitution in 1996, the UAE has enjoyed sustained political stability, underpinned by strong consensus amongst the individual emirates, and popular support for the individual rulers. In addition, the president of the UAE, Sheikh Khalifa bin Zayed Al-Nahyan, enjoys the backing of all the rulers of the Emirates.

Abu Dhabi’s surging oil revenues underpin the UAE’s strong finances

The economy of the UAE is dominated by the two largest emirates, Abu Dhabi and Dubai, which between them account for 90 percent of GDP and 66 percent of the population. However, with 90 percent of the UAE’s large oil reserves, Abu Dhabi is the key player. The workings of the Federation finances are opaque, but in practice Abu Dhabi bankrolls the bulk of the federal budget, and provides financial support to individual Emirates. It is Abu Dhabi’s surging oil revenues that have underpinned the large consolidated budget surpluses of the UAE recorded since 2004, and boosted its extensive foreign assets. Estimates of the level of assets under management by the Abu Dhabi Investment Authority (ADIA) at end-2007 range from $300-875 billion, representing at least 100 percent of the UAE’s GDP.

Population 2007 4.4 mn

Dubai 33%

Abu Dhabi 33%

Sharjah 20%

Ajman

Umm al QuaiwanRas al Khaimah Fujaira

GDP 2006 $163bn

Dubai 28.2%

Abu Dhabi 60%

Sharjah7.1%

FujairaRas al Khaimah

Ajman

Umm al Quaiwan

Dubai leads the way in economic diversification

In contrast, with only limited oil resources Dubai is investing heavily in a rapid diversification and growth strategy focused on developing itself as a trade, financial, tourism and services hub. The success of this strategy has drawn in increasing amounts of foreign investment and expatriate workers, generated a long real estate boom, and has established Dubai as a globally recognised “brand”. This has provided positive feedbacks to the other Emirates and helped make the UAE the Gulf Cooperation Council’s (GCC) second most diversified economy after Bahrain.

While still dominated by oil, Abu Dhabi is also diversifying with an emphasis on manufacturing, particularly aluminium and refined oil products. More recently it has started to follow in Dubai’s footsteps in developing large scale real estate projects, and attracting tourism with a particular emphasis on culture (branches of the Louvre and Guggenheim are set to open). The other smaller emirates are also developing their own ambitious economic plans, with a mixed emphasis on infrastructure, real estate, tourism, and industry.

Abu Dhabi’s wealth will help insulate the UAE economy

Despite some scope for tensions, the high degree of economic integration and cooperation amongst the emirates is expected to endure during the current global

7

Abu Dhabi will continue to play a key role, and is expected to use its large oil revenues and foreign assets to support the federal government, and to provide a backstop to any temporary financial difficulties that might emerge in the other Emirates.

Despite a sharp deterioration in conditions during the third quarter of the year, real GDP growth is estimated to have risen to close to 7 percent in 2008.

UAE Sovereign Wealth Funds 2007 AUM ($ billion) Abu Dhabi Investment Authority (ADIA) 335-875 Investment Corporation of Dubai 82 Dubai International Capital 13 International Petroleum Investment Company 12 Mubadala Development Company 10 Istithmar 6 Emirates Investment Authority Na Dubai International Financial Centre Investments Na Source: UNCTAD, IIF Total 423-998

recession and financial crisis. Abu Dhabi will continue to play a key role, and is expected to use its large oil revenues and foreign assets to support the federal government, and to provide a backstop to any temporary financial difficulties that might emerge in the other Emirates. In particular, this includes Dubai which is highly leveraged and thus more exposed to problems stemming from the global financial crisis.

Economic Developments and Prospects: 2008-2009 An abrupt change in outlook

Up until the middle of 2008, the UAE economy continued to grow rapidly, with high oil revenues helping fuel an infrastructure and real estate boom which had turned the UAE into the GCC’s pre-eminent project centre with a reported $990 billion worth of projects announced, planned or underway according to statistics tracked by MEED Projects. Impetus was also coming from Dubai’s emergence as a financial and services centre, a growing population (estimated at 6 percent per annum), and rapid domestic credit growth. Despite a sharp deterioration in conditions during the third quarter of the year, real GDP growth is estimated to have risen to close to 7 percent in 2008, boosted by strong non-oil growth and a rebound in oil production.

However, this overall growth estimate masks a dramatic turnaround in the economy during the second half of 2008 when the UAE finally succumbed to the global financial crisis which had been gaining in intensity since the bursting of the US sub prime mortgage market in mid-2007. During this period access to international capital markets became severely curtailed which, combined with an outflow of funds

Projects $990 bill ion (MEED)

Construction

IndustryOil & gas

PetrochemicalsPower

Water & waste

GCC Investment Projects($ billion MEEDProjects O ct.08)

47.6 99.1202.2

296

585.2

990.2

0

200

400

600

800

1000

1200

Bah

rain

Om

an

Qat

ar

Kuw

ait

Saud

i Ara

bia

UA

E

8

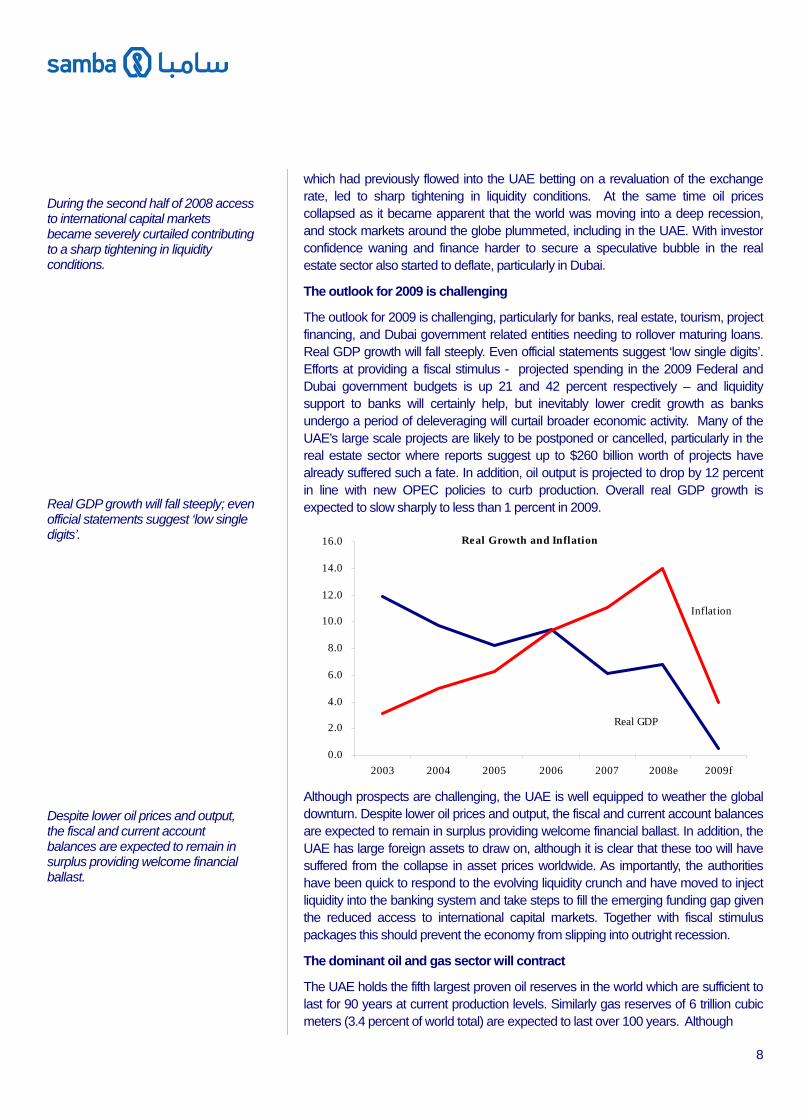

During the second half of 2008 access to international capital markets became severely curtailed contributing to a sharp tightening in liquidity conditions.

Real GDP growth will fall steeply; even official statements suggest ‘low single digits’. Real Growth and Inflation

0.0

2.0

4.0

6.0

8.0

10.0

12.0

14.0

16.0

2003 2004 2005 2006 2007 2008e 2009f

Real GDP

Inflation

Despite lower oil prices and output, the fiscal and current account balances are expected to remain in surplus providing welcome financial ballast.

which had previously flowed into the UAE betting on a revaluation of the exchange rate, led to sharp tightening in liquidity conditions. At the same time oil prices collapsed as it became apparent that the world was moving into a deep recession, and stock markets around the globe plummeted, including in the UAE. With investor confidence waning and finance harder to secure a speculative bubble in the real estate sector also started to deflate, particularly in Dubai.

The outlook for 2009 is challenging

The outlook for 2009 is challenging, particularly for banks, real estate, tourism, project financing, and Dubai government related entities needing to rollover maturing loans. Real GDP growth will fall steeply. Even official statements suggest ‘low single digits’. Efforts at providing a fiscal stimulus - projected spending in the 2009 Federal and Dubai government budgets is up 21 and 42 percent respectively – and liquidity support to banks will certainly help, but inevitably lower credit growth as banks undergo a period of deleveraging will curtail broader economic activity. Many of the UAE’s large scale projects are likely to be postponed or cancelled, particularly in the real estate sector where reports suggest up to $260 billion worth of projects have already suffered such a fate. In addition, oil output is projected to drop by 12 percent in line with new OPEC policies to curb production. Overall real GDP growth is expected to slow sharply to less than 1 percent in 2009.

Although prospects are challenging, the UAE is well equipped to weather the global downturn. Despite lower oil prices and output, the fiscal and current account balances are expected to remain in surplus providing welcome financial ballast. In addition, the UAE has large foreign assets to draw on, although it is clear that these too will have suffered from the collapse in asset prices worldwide. As importantly, the authorities have been quick to respond to the evolving liquidity crunch and have moved to inject liquidity into the banking system and take steps to fill the emerging funding gap given the reduced access to international capital markets. Together with fiscal stimulus packages this should prevent the economy from slipping into outright recession.

The dominant oil and gas sector will contract

The UAE holds the fifth largest proven oil reserves in the world which are sufficient to last for 90 years at current production levels. Similarly gas reserves of 6 trillion cubic meters (3.4 percent of world total) are expected to last over 100 years. Although

9

Following OPEC cuts, average oil production is projected to fall by over 12 percent in 2009.

Assuming government support to banks sustains positive credit growth and fiscal spending rises, the non-hydrocarbons sector should manage growth of around 4 percent.

currently hit by low oil prices, such resources will continue to underpin the financial health of the Emirates, providing funds for investment and consumption. In 2007, hydrocarbons production accounted for 40 percent of nominal GDP, 46 percent of exports and 75 percent of fiscal revenues.

Having dipped to 2.49 mb/d in 2007, oil production rose back to an average of 2.57 mb/d in 2008. However, OPEC agreed to steep new output cuts in December 2008 and, while not formally stated, we estimate that the UAE’s production target from January 2009 is now in the region of 2.2 mb/d. While there may some scope to raise output in the latter part of the year, average production is thus likely to be down by over 12 percent in 2009. Assuming that the global economy begins to recover in 2010, medium term production gains are expected as the state-owned Abu Dhabi National Oil Company (ADNOC) is committed to raising capacity to 3.5 mb/d by 2012, and plans to invest around $40 billion over the next five years to expand crude oil, gas and refining capacity.

Real GDP growth will slow

0

100

200

300

400

500

2005 2006 2007 2008 2009

Dh

bln

0

2

4

6

8

10

Nonhydrocarbon real GDP Hydrocarbon real GDP

Real GDP growth (rhs)

Non-hydrocarbons sector growth will slow

The UAE’s vibrant non-hydrocarbons sector has been growing rapidly, supported by the government’s active promotion of the private sector and successful efforts to attract foreign investment. The sector accounts for about three quarters of real GDP, and has been growing at an annual average rate of more than 10 percent for the last five years. While still rapid, this rate of expansion is likely to have slowed to around 8 percent in 2008, reflecting strong growth in the first 8-9 months before the liquidity crunch hit. Prospects are less favourable for 2009. Unemployment is rising (officially estimated at 12.7 percent for UAE citizens, and 2.6 percent for expatriates in 2008, although the latter is thought to be understated), and previously strong population growth, which had been a major contributor to demand, will falter. Nonetheless, assuming government support to banks sustains positive credit growth and state spending on development projects picks up some of the slack, the non-hydrocarbons sector should manage growth of around 4 percent.

Construction and real estate boom comes to an end

Supported by a rapidly expanding population and rising demand, the level of construction activity in the UAE has been extraordinary, driven mainly by large scale infrastructure and real estate projects. The opening up of the Dubai property market to

10

After nearly six years of rapid and unsustainable prices rises, the real estate sector is now undergoing a correction.

Banks and finance companies have been particularly active in providing credit for private sector real estate projects and have posted strong performances through Q3 2008.

foreign ownership in 2002 helped spur a surge in beachfront and island projects providing hotels, shopping malls and residencies. Office construction has also boomed as rising economic activity and foreign investment has pushed up demand. However, after nearly six years of extremely rapid prices rises, the sector is now undergoing a correction, and prices are likely to decline in the short-term as credit conditions tighten, the authorities take measures to rein in speculative activity, and projects are cancelled.

UAE Real Estate Price Index 2008 (Mazaya 2005=1000)

1200

1300

1400

1500

1600

1700

1800

1900

2000

2100

Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov

An expanding financial sector has supported rapid growth

One of the key measures supporting non-hydrocarbons growth has been the liberalisation and opening up of the financial markets, including the development of The Dubai International Finance Centre. This has allowed regional and international financial services companies to benefit from the opportunities generated by the economic boom. Banks and finance companies have been particularly active in providing credit for private sector real estate projects and have posted strong performances. However, operating conditions deteriorated markedly in the fourth quarter of 2008, and banks face a much tougher time in 2009 in the face of tightened liquidity, falling real estate and share prices, and sharply slower economic growth.

Global recession will dampen the tourism sector

The successful development of the UAE as a tourism destination, especially Dubai, has seen arrivals surge from 2.5 million in 2002 to 8.8 million in 2007. Emirates

Dubai: Source of Hotel Guests2006 6.95 million

Europe 32%

Asia pacific 26%

Arab countries

22%

Americas 8%

UAE 6%Africa 6%

11

Tourist arrivals will be hit by the global recession.

Lower oil prices and production are likely to result in a halving of hydrocarbon exports in 2009.

The current account surplus is projected to fall to 4 percent of GDP in 2009.

Airlines has been undergoing an unprecedented expansion as part of efforts to serve Dubai as a major tourism destination and global business centre. It has placed orders for close to 200 new planes, and a major expansion of the airport is underway. The authorities expected 10 million tourist arrivals in 2008 but, given the rapidly slowing global economy, this is unlikely to have been achieved (a third of Dubai hotel guests were from Europe in 2007). Arrivals are now expected to decline in 2009 reflecting the dire outlook for the global economy, and particularly advanced economies. However, the longer term prospects remain positive.

Fiscal and External Positions Fiscal and current account balances will remain in surplus

Surging oil and gas revenues ensured that the fiscal and external positions remained in large surplus through 2008. Based on estimates of the UAE’s consolidated fiscal balance made by the IIF, the fiscal surplus is estimated to have risen to 30 percent of GDP, while the current account surplus is estimated at around 23 percent of GDP. Hydrocarbon exports soared to an estimated $124 billion, while non-hydrocarbon exports performed strongly as well.

Surging current account and fiscal surpluses are set to fall in line with lower oil prices

-5.0

0.0

5.0

10.0

15.0

20.0

25.0

30.0

35.0

2001 2002 2003 2004 2005 2006 2007 2008e 2009f

% o

f GD

P

-18

2

22

42

62

82

102

122

$ bn

Oil exports (rhs $bn) Consolidated budget balanceCurrent account balance

The outlook for 2009 is considerably less rosy with lower oil prices and output likely to result in a halving of hydrocarbon exports to around $60 billion, while non-hydrocarbon exports will struggle in the face of the global recession. However, with import prices and volumes also likely to dip, the current account is still expected to remain in surplus at around 4 percent of GDP. Similarly, despite additional spending from fiscal stimulus packages at the federal and emirate level, the consolidated fiscal balance is also projected to remain in surplus at just under 5 percent of GDP. The fiscal accounts would, however, probably slip into deficit if average oil prices for the year stayed below the estimated breakeven budget oil price of $40/b.

While data is incomplete, the fiscal picture is reassuringly strong

Published data on the UAE’s fiscal accounts are not complete, and efforts to consolidate balances from individual emirates, the federal government, and estimated income flows from ADNOC and ADIA, are inevitably subject to some degree of error.

12

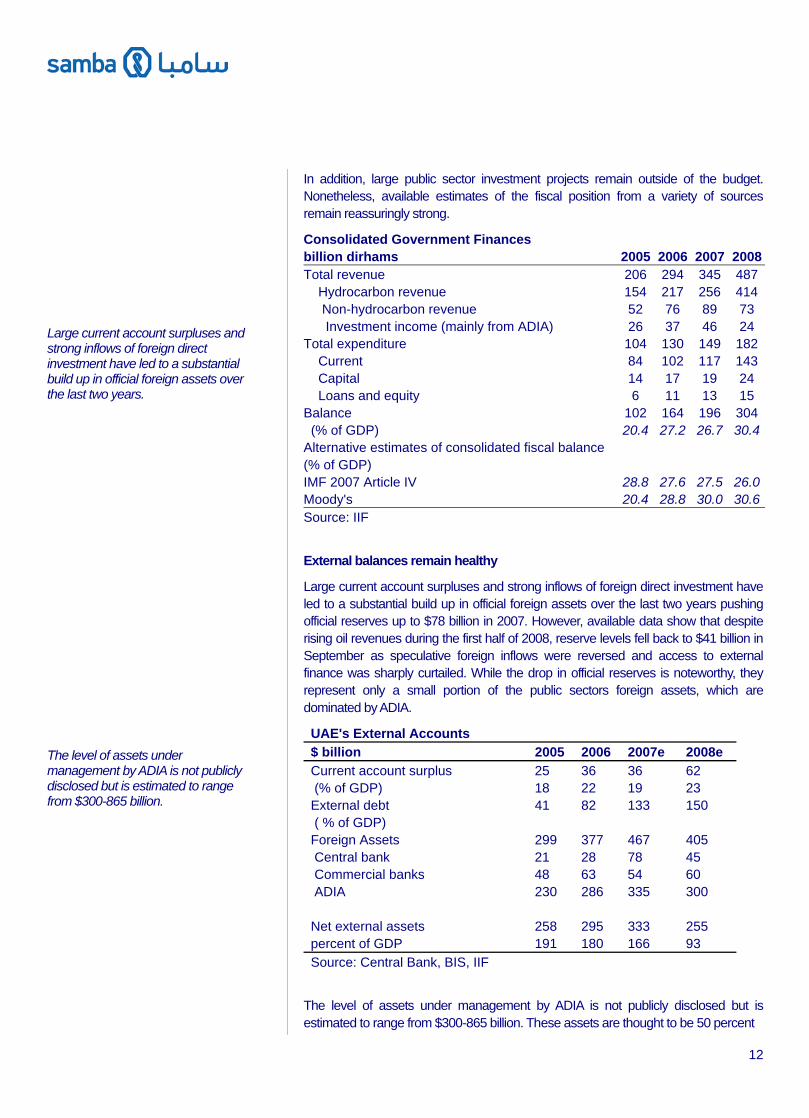

Large current account surpluses and strong inflows of foreign direct investment have led to a substantial build up in official foreign assets over the last two years.

The level of assets under management by ADIA is not publicly disclosed but is estimated to range from $300-865 billion.

In addition, large public sector investment projects remain outside of the budget. Nonetheless, available estimates of the fiscal position from a variety of sources remain reassuringly strong.

Consolidated Government Finances billion dirhams 2005 2006 2007 2008Total revenue 206 294 345 487 Hydrocarbon revenue 154 217 256 414 Non-hydrocarbon revenue 52 76 89 73 Investment income (mainly from ADIA) 26 37 46 24 Total expenditure 104 130 149 182 Current 84 102 117 143 Capital 14 17 19 24 Loans and equity 6 11 13 15 Balance 102 164 196 304 (% of GDP) 20.4 27.2 26.7 30.4 Alternative estimates of consolidated fiscal balance (% of GDP) IMF 2007 Article IV 28.8 27.6 27.5 26.0 Moody's 20.4 28.8 30.0 30.6 Source: IIF

External balances remain healthy

Large current account surpluses and strong inflows of foreign direct investment have led to a substantial build up in official foreign assets over the last two years pushing official reserves up to $78 billion in 2007. However, available data show that despite rising oil revenues during the first half of 2008, reserve levels fell back to $41 billion in September as speculative foreign inflows were reversed and access to external finance was sharply curtailed. While the drop in official reserves is noteworthy, they represent only a small portion of the public sectors foreign assets, which are dominated by ADIA.

UAE's External Accounts $ billion 2005 2006 2007e 2008e Current account surplus 25 36 36 62 (% of GDP) 18 22 19 23 External debt 41 82 133 150 ( % of GDP) Foreign Assets 299 377 467 405 Central bank 21 28 78 45 Commercial banks 48 63 54 60 ADIA 230 286 335 300 Net external assets 258 295 333 255 percent of GDP 191 180 166 93 Source: Central Bank, BIS, IIF

The level of assets under management by ADIA is not publicly disclosed but is estimated to range from $300-865 billion. These assets are thought to be 50 percent

13

Although private sector external borrowing has increased rapidly, the UAE retains a large net external creditor position.

International market perceptions of the UAE’s credit risk have deteriorated.

Markets are clearly differentiating between oil rich Abu Dhabi, and Dubai.

invested in equities, 20 percent fixed income, 10 percent real estate, and 20 percent in a mixture of cash, hedge funds, and strategic investments. The unprecedented crisis in the world financial markets during 2008 will certainly have had an adverse impact on the value of these assets. Such has been the poor performance of markets in 2008 that valuation declines are likely to have offset additions from sustained large fiscal and current account surpluses. However, even if we take the lower estimates of $335 billion in assets at end-2007, the level of ADIA’s assets at the end of 2008 is still likely to be close to $300 billion taking account additions and probable losses.

The UAE’s net external creditor position is strong

Although private sector external borrowing has increased rapidly, the UAE retains a large net external creditor position. Available estimates put the UAE’s total external debt at around $150 billion at end-2008, equivalent to 55 percent of GDP. Using conservative estimates of the UAE’s total foreign assets of $405 billion (official reserves plus bank foreign assets plus estimated ADIA’s assets); this gives a positive net external asset position of $255 billion, equivalent to 93 percent of GDP. Of course the position could be considerably larger depending on the true level of ADIA’s assets. Whatever the true figure, it is clear that the UAE has considerable assets to call upon to help cushion the economy from the global recession.

Lack of transparency mars market perceptions of UAE risk

Despite the strong external and consolidated fiscal positions, international market perceptions of the UAE’s credit risk have deteriorated, as revealed in rising rates for credit default swaps (CDS) for both sovereign and government related corporate entities. One of the main concerns weighing on the markets is the uncertainly over the level of public sector leverage in individual emirates, and the extent to which they can rely on the oil revenues of Abu Dhabi. While neither the federal government nor emirates governments have significant amounts of explicitly guaranteed debt, it is clear that contingent liabilities have risen rapidly as government owned companies issue debt on their own behalf, particularly in Dubai.

UAE 5 Year CDS Level (bps)

0

50

100

150

200

250

300

Jul-0

8

Aug

-08

Sep-

08

Oct

-08

Nov

-08

Dec

-08

UAE - Selected CDS Levels (bps)

0 500 1000 1500

Dubai Holding

Emirate of Abu Dhabi

National Bank of AbuDhabi

Emirates Bank IntlPJSC

Govt. of Dubai

Rollover risks have risen

Markets are clearly differentiating between oil rich Abu Dhabi, and Dubai where a lack of official data on the Dubai government’s finances has led to increasing concerns over its ability to meet mounting debt obligations given its limited oil resources and the severity of the global credit crunch. Such concerns can be seen in the elevated CDS

14

The Dubai government is actively working to ensure that all payment obligations are met, and to reassure capital markets of its financial strength.

Dubai’s total external debt is estimated at around 100 percent of GDP.

Since early 2007, domestic credit growth has soared on the back of the booming economy and increasingly negative real interest rates.

rates for Dubai entities. For some, rates have risen to levels which have effectively shut them out of the international capital markets. Thus a major challenge facing the UAE during 2009 is to ensure that the large funding needs of its quasi-public entities are met. These are thought to amount to around $16 billion in the form of maturing syndicated loans and bonds, with the overwhelming majority accounted for by Dubai government related entities.

Sovereign Credit Rating Moody's S & P Fitch UAE Aa2 Abu Dhabi AA AA

JP Morgan Broad EMBI Diversified UAE Index Level

85

90

95

100

105

110

115

120

Jul-0

8

Aug

-08

Sep-

08

Oct

-08

Nov

-08

Dec

-08

Jan-

09

Feb-

09

Support will be provided to prevent defaults

Recent unilateral moves by Abu Dhabi to recapitalise its own banks have caused disquiet as it begs the question as to whether and when such support may be provided to Dubai’s more exposed banks. Despite the uncertainty, we hold the view that, if necessary Abu Dhabi will step in to provide support to Dubai’s quasi government entities facing funding constraints, either through federal government channels, or other means. This appears to be borne out by the recent provision of $1 billion in federal funds to Borse Dubai to prevent it defaulting on a $2.4 billion loan it was having difficulty refinancing. However, it is likely that any support to Dubai will not be automatic and may involve tough negotiations and compromises.

For its own part the Dubai government is actively working to ensure that all payment obligations are met, and to reassure capital markets of its financial strength. In this regard, it has now publicly stated that its sovereign debt stands at $10 billion against assets (excluding key infrastructure installations) of $90 billion, and government affiliated companies debt stands at $70 billion against assets of $260 billion. Total external debt of Dubai is now put at around 100 percent of new 2007 GDP estimates.

The Dubai government is also seeking a sovereign credit rating by mid-year to provide more economic and financial data, and further reassurance to capital markets so as to facilitate lower cost and improved access to funds. In the meantime officials state that Dubai will seek a mix of repayments and rollovers to meet its debt obligations, using its own resources if necessary, and calling on its relationships with “numerous” financial institutions.

Monetary and Financial Sector Developments Credit growth soared in 2007-08

Since early 2007, domestic credit growth has soared on the back of the booming economy and increasingly negative real interest rates. Central bank data shows that annual private sector credit growth was running at an unsustainably high rate of nearly 60 percent in September 2008. Meanwhile commercial banks have increasingly tapped international markets for funds to support long-term project and

15

Banks have increasingly tapped international markets for funds to support long-term project and real estate lending.

Reduced and more costly access to international capital markets has had an adverse impact on banks and corporate entities’ long-term funding.

Loan growth which has exceeded deposit growth and contributed to elevated bank loan to deposit ratios.

real estate lending - mainly through Euro Medium Term Notes (EMTNs) and sukuks– raising their foreign liabilities to $89 billion at September 2008, and pushing their net external asset position into the red. This has made them more exposed to the intensification of the global financial crisis and the associated loss of access to international capital markets.

Credit to the private sector has soared

0

10

20

30

40

50

60

70

Jan-

07

Apr

-07

Jul-0

7

Oct

-07

Jan-

08

Apr

-08

Jul-0

8

y-o-y %

Broad money

Private sector

UAE commercial banks foreign assets & liabilities

0102030405060708090

100

2001

2002

2003

2004

2005

2006

2007

2008

Sep

.

$ bn

Assets Liabilit ies

Liquidity: from flood to drought

While the economy was awash with liquidity during the first half of 2008, three key factors combined to contribute to an abrupt and sharp tightening during the second half the year:

• Reduced and more costly access to international capital markets has had an adverse impact on banks and corporate entities’ long-term funding. This has constrained banks’ ability to lend in dollars, while at the same time pushing corporate entities into seeking funds in the local bank markets.

• Another key factor, unique to the GCC states, has been the withdrawal of large amounts of speculative funds which had flowed into the UAE betting on an exchange rate revaluation. This hurt bank deposits and added to shortages of dollar funds.

• Third has been the continued rapid increase in loan growth which has exceeded deposit growth and contributed to elevated bank loan to deposit ratios. In aggregate these reached 113 percent in September 2008, significantly above the 100 percent limit prescribed by the central bank. This shortfall in deposit growth is constraining banks’ ability to lend.

The combination of such factors ensured that the UAE has suffered its own credit crunch, leading to elevated interbank rates, a tightening of bank lending conditions, and the curtailment of credit flows with adverse consequences for economic activity.

The authorities have been quick to respond

Fortunately the government and central bank have been quick to respond to the evolving liquidity crunch and have implemented a number of measures to inject liquidity and shore of confidence in the banking system. Some of the more important measures include:

16

Measures have been introduced to support US dollar and dirham liquidity.

Interbank rates have fallen substantially from their peak, but they remain elevated.

The recent rapid rate of credit growth will slow sharply as a result of tighter liquidity conditions.

• Guaranteeing all bank deposits and interbank lending for three years.

• A phased injection of $19 billion into banks in the form of long-term deposits. Establishing a $13.6 billion short-term liquidity facility and a dollar swap facility at the central bank, and easing restrictions on accessing central bank funds.

• Lowering interest rates.

Such measures are aimed at improving both dollar and dirham liquidity. In addition, the government of Abu Dhabi has also unilaterally decided to inject a combined $4.4 billion worth of additional capital into five of its banks, with the funds coming from the emirate’s own budget. These fund injections will further reinforce those banks’ ability to meet balance sheet commitments and, in particular, could be channeled to selective infrastructure projects whose completion has been threatened by refinancing difficulties.

UAE v US 3 month interbank rates

1.0

1.5

2.0

2.5

3.0

3.5

4.0

4.5

5.0

Jan-

08

Feb-

08

Mar

-08

Apr

-08

May

-08

Jun-

08

Jul-0

8

Aug

-08

Sep-

08

Oct

-08

Nov

-08

Dec

-08

Jan-

09

Feb-

09

UAE

US

Interbank rates have begun to drop back

While interbank rates have fallen substantially from their peak in response to the various initiatives, they remain elevated. Three month rates were holding at 3.6 percent in February, compared with a similar US$ Libor rate of 1.2 and the central bank benchmark repo rate which was cut to 1 percent in January. Meanwhile, UAE banks are now offering up to 7 percent on time deposits compared with 2 percent a few months ago, as they try to boost their deposit base.

Credit growth will slow

Despite the measures taken by the authorities, the recent rapid rate of credit growth will slow sharply as a result of tighter liquidity conditions. The central bank has also set a cap of 10 percent lending growth for 2009, although this may not be necessary given that, without access to wholesale funding, many banks may need to deleverage their balance sheets. As well as high loans to deposit ratios, banks are also concerned about asset quality as the economy slows and real estate prices fall. Many are streamlining their lending operations and pursuing measures to boost their deposit base. Some have even stopped lending for apartment purchases in Dubai all together.

17

To-date banks have been resilient in the face of the international credit turmoil and US-sub prime crisis.

Banks face a tougher time in 2009 in the face of lower oil prices, weak stock markets, falling real estate prices, reduced access to capital markets, and an economic slowdown.

Banks need to manage their real exposure to real estate.

2008 bank results were generally positive but most saw sharp drops in the fourth quarter

To-date banks in the UAE have been resilient in the face of the international credit turmoil and US-sub prime crisis. There have been no bank failures, although the two largest mortgage finance companies, Amlak and Tamweel have been merged and effectively taken over by the federal government. Available bank results for 2008 show that profits held up for the year as a whole, and in some cases posted impressive gains. Capital adequacy ratios also remained relatively healthy and above the required 10 percent, although they have continued to trend down. However, most fourth quarter 2008 profits were sharply lower and offer a foretaste of the difficulties to come.

The outlook for banks is challenging

Banks face a tougher time in 2009 in the face of lower oil prices, weak stock markets, falling real estate prices, reduced access to capital markets, and the broad economic slowdown. In such circumstances, they face significant risks from asset quality deterioration, rising non-performing loans, inflated provisioning needs and decreased credit volumes. Reflecting the deteriorated operating conditions, international rating agencies have recently moved to downgrade the individual ratings of a number of UAE banks, although they have been quick to stress that the Long-Term Issuer Default ratings are unlikely to change as they remain driven by the probability of support by the federal government. Given the tough outlook, further such support to banks may be necessary, and there may also be scope for consolidation in the banking sector. Currently there are more than 50 domestic and international banks, many of them government controlled.

Bank Construction Loans

0.0

5.0

10.0

15.0

20.0

25.0

30.0

35.0

2004 2005 2006 2007 2008Sep.

0.0

5.0

10.0

15.0US$ billion (lhs)

% of deposits (rhs)

Bank Real Estate Mortgage Loans

0.0

5.0

10.0

15.0

20.0

25.0

30.0

35.0

2004 2005 2006 2007 2008Sep.

0.0

2.0

4.0

6.0

8.0

10.0

12.0

14.0

16.0US$ billion (lhs)

% of deposits (rhs)

Banks need to manage exposure to the real estate sector

According to an October 2008 press release from the central bank, bank loans to the real estate sector stood at the equivalent of 11 percent of total bank assets and 18 percent of total deposits, which is below the 20 percent maximum allowed by law. However, levels are likely to be significantly higher if construction related activities and personal lending which has been used to speculate in property are added. The latter is thought to have increased significantly as individuals evaded lending regulations on personal loan limits by posing as small businesses. This enabled them to secure larger loans which were often used to finance real estate investments.

18

UAE vs. Emerging Markets Stock Markets

0

1000

2000

3000

4000

5000

6000

7000

Feb-08 Apr-08 Jun-08 Aug-08 Oct-08 Dec-08 Feb-090

200

400

600

800

1000

1200

1400

DFMGI Index (LHS) ADSMI Index (LHS)MXEF Index (RHS)

The Dubai and Abu Dhabi stock markets fell by 72 and 48 percent respectively in 2008.

The market outlook for 2009 remains clouded by low oil prices and the weakening economy.

Inflation is estimated to have risen to a record 14 percent in 2008.

Stock markets have fallen steeply

Stock markets in Abu Dhabi and Dubai had already been falling steadily during 2008, when the massive global sell off saw markets around the world crash in early October. This dragged the UAE stock markets down further with the Dubai and Abu Dhabi market indices ending the year off 72 and 48 percent respectively. Real estate stocks were particularly hard hit reflecting concerns over the correction underway in the market after a long boom. Banking stocks were similarly dragged lower on concerns over their exposure levels to the real estate sector, and over increasing loan to deposit ratios.

During the first two months of 2009 UAE stock markets have continued to slide, with the Dubai index down 12 percent and the Abu Dhabi index down 9 percent. The outlook for the year is expected to remain sluggish as the global economy continues to struggle and oil prices remain weak, dampening investor sentiment.

Monetary Policy Challenges High inflation remains a concern

Inflation is estimated to have risen to a record 14 percent in 2008, from 11 percent in 2007. However, official figures are thought to understate the true level of inflation – which could be closer to 20 percent – as they are based on prices paid by UAE nationals who benefit from extensive subsidies and rent controls not available to the

UAE: O fficial Consumer Price Index (percent change)

0

2

4

6

8

10

12

14

16

18

20

2001 2002 2003 2004 2005 2006 2007

CPI Housing costs

19

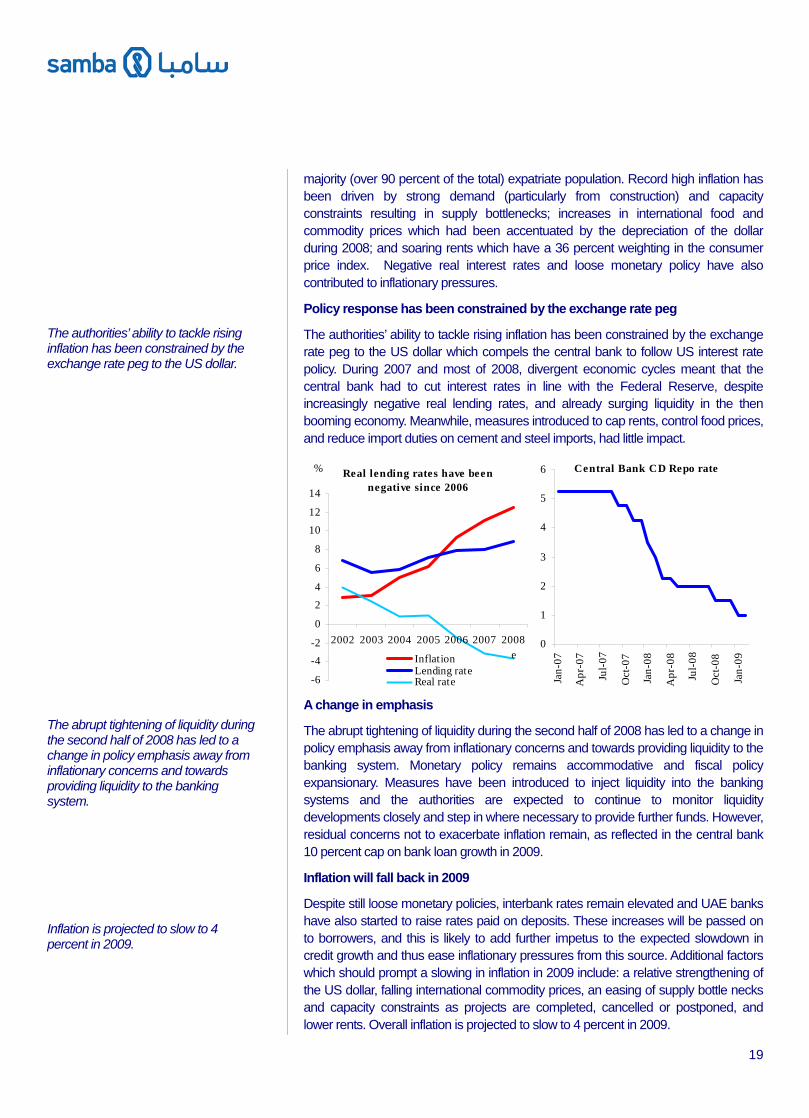

The authorities’ ability to tackle rising inflation has been constrained by the exchange rate peg to the US dollar.

The abrupt tightening of liquidity during the second half of 2008 has led to a change in policy emphasis away from inflationary concerns and towards providing liquidity to the banking system.

Inflation is projected to slow to 4 percent in 2009.

majority (over 90 percent of the total) expatriate population. Record high inflation has been driven by strong demand (particularly from construction) and capacity constraints resulting in supply bottlenecks; increases in international food and commodity prices which had been accentuated by the depreciation of the dollar during 2008; and soaring rents which have a 36 percent weighting in the consumer price index. Negative real interest rates and loose monetary policy have also contributed to inflationary pressures.

Policy response has been constrained by the exchange rate peg

The authorities’ ability to tackle rising inflation has been constrained by the exchange rate peg to the US dollar which compels the central bank to follow US interest rate policy. During 2007 and most of 2008, divergent economic cycles meant that the central bank had to cut interest rates in line with the Federal Reserve, despite increasingly negative real lending rates, and already surging liquidity in the then booming economy. Meanwhile, measures introduced to cap rents, control food prices, and reduce import duties on cement and steel imports, had little impact.

Central Bank CD Repo rate

0

1

2

3

4

5

6

Jan-

07

Apr

-07

Jul-0

7

Oct

-07

Jan-

08

Apr

-08

Jul-0

8

Oct

-08

Jan-

09

Real lending rates have been negative since 2006

-6

-4-2

0

24

6

8

1012

14

2002 2003 2004 2005 2006 2007 2008eInflation

Lending rateReal rate

%

A change in emphasis

The abrupt tightening of liquidity during the second half of 2008 has led to a change in policy emphasis away from inflationary concerns and towards providing liquidity to the banking system. Monetary policy remains accommodative and fiscal policy expansionary. Measures have been introduced to inject liquidity into the banking systems and the authorities are expected to continue to monitor liquidity developments closely and step in where necessary to provide further funds. However, residual concerns not to exacerbate inflation remain, as reflected in the central bank 10 percent cap on bank loan growth in 2009.

Inflation will fall back in 2009

Despite still loose monetary policies, interbank rates remain elevated and UAE banks have also started to raise rates paid on deposits. These increases will be passed on to borrowers, and this is likely to add further impetus to the expected slowdown in credit growth and thus ease inflationary pressures from this source. Additional factors which should prompt a slowing in inflation in 2009 include: a relative strengthening of the US dollar, falling international commodity prices, an easing of supply bottle necks and capacity constraints as projects are completed, cancelled or postponed, and lower rents. Overall inflation is projected to slow to 4 percent in 2009.

20

AED/$ 3 month forward spread-600

-500

-400

-300

-200

-100

0

100

200

300

400May-06 Sep-06 Jan-07 May-07 Sep-07 Jan-08 May-08 Sep-08 Jan-09

Inflow of 'speculative' funds

Outflow of speculative funds & curtailed access to capital markets

Speculative pressure on the Dirham betting on a revaluation has been eliminated, as reflected in movements in the forward exchange rate.

We do not expect a change in the current exchange rate peg to the dollar prior to the establishment of the GCC Monetary Union.

The exchange rate peg to the dollar will be maintained

While there has been considerable debate on the issue, we do not expect a change in the current exchange rate peg to the dollar prior to the establishment of the GCC Monetary Union. This is scheduled for 2010, although the timetable is likely to slip. In addition, with inflationary pressures now receding; the US dollar stronger against other major currencies, and domestic liquidity tight, the arguments for a change in the peg have abated. Speculative pressure on the Dirham betting on a revaluation has also been eliminated, as reflected in movements in the forward exchange rate. In fact a combination of the withdrawal of speculative funds and reduced access to capital markets sharply reduced US dollar availability and reversed spreads on the forward exchange rates to levels suggesting a large devaluation before the government intervened to provide liquidity support. Even so forward spreads continue to point to tightness in US dollar funding.

DXY (US$ spot index)

70

72

74

76

78

80

82

84

86

88

90

Sep-

06

Nov

-06

Jan-

07

Mar

-07

May

-07

Jul-0

7

Sep-

07

Nov

-07

Jan-

08

Mar

-08

May

-08

Jul-0

8

Sep-

08

Nov

-08

Jan-

09

21

While the UAE’s fundamentals are strong it remains vulnerable to a deeper and more protracted global recession.

Risks to the outlook Downside risks are prominent

While the UAE’s fundamentals are strong it remains vulnerable to a deeper and more protracted global recession. This could see oil prices slide further. At under $35/b the current account could shift into deficit, and at under $30/b so would the consolidated fiscal balance. This would mean fewer resources to fund investment and consumption, and a greater need to draw down external assets which in turn would likely to be adversely affected by a weaker global economy. Growth prospects would likely suffer as a result.

Even if oil prices hold up, real GDP projections are at risk from less benign assumptions on the real estate and banking sectors, and a generally more pronounced global slowdown which could see tourism, foreign investment and credit flows to the UAE more sharply curtailed. The tightening of liquidity conditions and the slump in UAE’s stock markets – led by real estate and banking shares – clearly illustrates that the UAE remains vulnerable to adverse global developments. A more pronounced contraction in business activity, particularly in real estate and infrastructure development, is a possibility, and this in turn could put banks and financial institutions at risk. Public funds may then need to be diverted to support banks and the real estate sector with adverse consequences for growth.

22

Howard Handy Chief Economist [email protected] Keith Savard Director Economic Research [email protected] James Reeve Senior Economist [email protected] Andrew B. Gilmour Senior Economist [email protected] Raza A. Agha Research Economist [email protected] Touheed Ahmed Management Associate [email protected] Disclaimer This publication is based on information generally available to the public from sources believed to be reliable and up to date at the time of publication. However, SAMBA is unable to accept any liability whatsoever for the accuracy or completeness of its contents or for the consequences of any reliance which may be place upon the information it contains. Additionally, the information and opinions contained herein:

1. Are not intended to be a complete or comprehensive study or to provide advice and should not be treated as a substitute for specific advice and due diligence concerning individual situations;

2. Are not intended to constitute any solicitation to buy or sell any instrument or engage in any trading strategy; and/or

3. Are not intended to constitute a guarantee of future performance. Accordingly, no representation or warranty is made or implied, in fact or in law, including but not limited to the implied warranties of merchantability and fitness for a particular purpose notwithstanding the form (e.g., contract, negligence or otherwise), in which any legal or equitable action may be brought against SAMBA.

Samba Financial Group P.O. Box 833, Riyadh 11421 Saudi Arabia