Embed Size (px)

Citation preview

THE "UNIFIED ACCOUNTING SYSTEM": HOW TO IMPLEMENT ON-LINECASH FLOW ACCOUNTING

by

Hervé StolowyAssociate-Professor of Accounting

Paris Graduate School of Management (Ecole Supérieure de Commerce de Paris)79 avenue de la République, 75543 - Paris Cedex 11, France.

Jean-Claude DormagenAccounting Manager

L'Oreal Group41, rue Martre, 92117 - Clichy, France.

and

Michel TernisienGeneral Secretary

Salustro-Reydel (C.P.A.) networkRSM International

2, avenue Hoche, 75008 - Paris, France.

Paper presented at the 16th Annual Congress of the European Accounting AssociationTurku, Finland, April 28-30, 1993

April 1993___________________________________________________________________________Simona Lardera, Associate-Professor of Information Systems at the Paris Graduate School of Management,

who programmed the case material supporting this paper, as well as to Nabil Elias, Professor at the University

of Manitoba, Visiting Professor at the Paris Graduate School of Management, for his helpful comments, John

Kennedy, Associate-Professor of Accounting at the Paris Graduate School of Management, and Paul Gillion,

International Department, Salustro-Reydel,

1

THE "UNIFIED ACCOUNTING SYSTEM": HOW TO IMPLEMENT ON-LINECASH FLOW ACCOUNTING

ABSTRACT

Corporate accounting information is sometimes organized in separate processing centers, eachone providing a specific kind of information. In France, for instance, as in many otherEuropean countries, there are often three separate data processing centers: financialaccounting, management accounting and cash flow accounting. In the United States, it wouldappear that such a separation between financial accounting and cash flow accounting alsoexists. The FASB (1987, § 109) recognizes that many providers of financial statements do notpresently collect information in a manner that will allow them to determine amounts such ascash receipts and payments directly from their accounting systems.

These divisions and dispersals of information entail laborious reconciliation and analysis work,reducing considerably the efficiency of accounting as a management tool.

Data processing has overcome these obstacles clearing the way for a more advancedbookkeeping technique: the Unified Accounting System (UAS), which helps to eliminatedivisions and dispersals and take optimum advantage of the available resources.

The purpose of this paper is to introduce the Unified Accounting System which unifies all theinformation needed for management needs; such a system is currently operating in severalsubsidiaries of an international French cosmetics group. The paper presents an application ofthe integration of financial accounting and cash flow accounting1. This is made possible by amajor innovation: the introduction of the concept of "object", i.e. the purpose of each entry.

We also show how this System which is "driven" by a software data base, can facilitate thepreparation of the Statement of Cash Flows (SFAS 95 model) using the direct method, whichdiscloses cash receipts and cash payments directly from the financial accounting entries,instead of reanalysing the accounts.

1 The integration of financial accounting and management accounting, also in practice, could be presented inan other paper.

2

THE "UNIFIED ACCOUNTING SYSTEM": HOW TO IMPLEMENT ON-LINECASH FLOW ACCOUNTING

Corporate accounting information is sometimes organized in separate processing centers, eachone providing a specific kind of information. In France, for instance, as in many otherEuropean countries, there are often three separate data processing activities:

• Financial accounting providing information about assets, liabilities, the determination of netincome - being the difference between revenues and expenses classified by type or nature.

• Management accounting determining the cost of goods with details of the composition of netincome, revenues and expenses being classified by function.

• Cash flow accounting generally provided by a separate processing center.

In the United States, it would appear that such a separation between financial accounting andcash flow accounting also exists. The FASB (1987, § 109) recognizes that many providers offinancial statements do not presently collect information in a manner that will allow them todetermine amounts such as cash receipts and payments directly from their accounting systems.

Such divisions and dispersals of information entail laborious reconciliation and analysis work,reducing considerably the efficiency of accounting as a management tool.

Data processing has overcome these obstacles clearing the way for a more advancedbookkeeping technique: the Unified Accounting System (UAS), which helps to eliminatedivisions and dispersals and take optimum advantage of the available resources.

Having noted the constraints of traditional accounting systems and the problems of calculatingthe net cash flows from operating activities using the direct method, this paper introduces theUnified Accounting System which unifies all the information needed for management andwhich is currently operating in several subsidiaries of an international French cosmetics group.

The paper presents an application of the integration of financial accounting and cash flowaccounting2. This is made possible by a major innovation: the introduction of the concept of

2 The integration of financial accounting and management accounting, also in practice, could be presented inan other paper.

3

"object", i.e. the purpose of each entry. In other words, the Unified Accounting Systemmodifies the structure of accounting entries and adds a new dimension to processing financialinformation.

At this stage, it is important to distinguish between the Unified Accounting System and theEvents Accounting approach introduced by Sorter (1969).

Thereafter, with the help of an example we show how this System which is "driven" by asoftware data base, can facilitate the preparation of the Statement of Cash Flows (SFAS 95model) using the direct method, which discloses cash receipts and cash payments directly fromthe financial accounting entries, instead of reanalysing the accounts.

The cash flow accounting protagonists like Lee (1987) saw a cash flow accounting as analternative to accrual accounting. The Unified Accounting System effectively combines bothapproaches, since by modifying the structure of accounting entries, one can obtain real-timecash-flow information from the basic financial records.

1 - BACKGROUND

1.1

The Unified Accounting System, as we will demonstrate, eliminates some of theweaknesses of the traditional accounting system whilst retaining its strengths.

1.1.1

are fully specified in a standard Chart of Accounts.

It is possible to distinguish between:

• collections and payments, thus determining cash variations• revenues and expenses, thus determining the income.

1.1.2 Weak points: the organization of accounting entries

4

Accounting entries record information in respect of transactions and provide the data neededto analyze accounts and draw up summaries. In current bookkeeping systems, the accountingentries:

• combine several movements under the same entry, preventing the direct reconciliation ofeach "source" with the related "use".

For example, the accounts receivable is debited with the total amount of an invoice, which includes

the sales value plus the sales tax.

• neglect elements of information by not indicating the reason or purpose of the accountingentries, thus, preventing direct explanations of account variations.

For example, "collection", i.e. the reason (or purpose or object) of the movement on the bank account,

when a check has been received from a customer in settlement of an account receivable, is not

entered.

Consequently, certain statements and certain analyses cannot be produced directly fromaccounting entries and lengthy and costly additional work needs to be done to producemeaningful analyses.

1.2 How to overcome problems encountered with the preparation of the Statement of CashFlows under the direct method

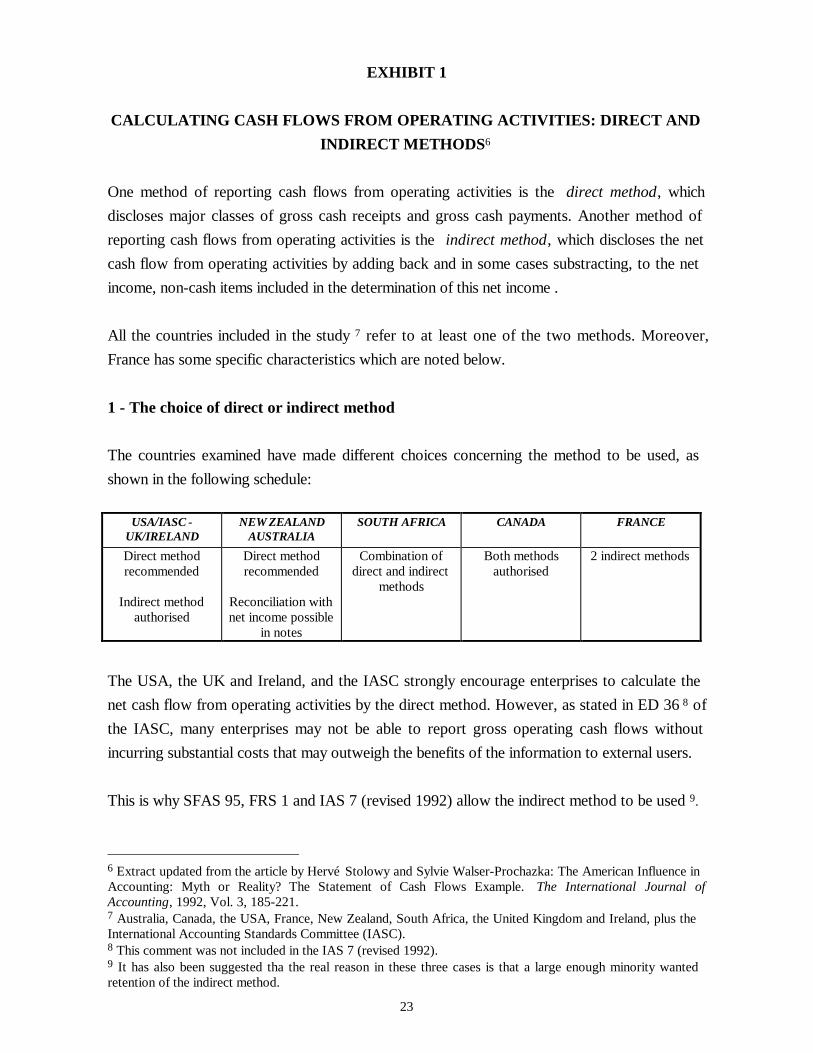

In taking the two methods of reporting cash flows from operating activities: the direct and theindirect methods, Stolowy and Walser-Prochazka (1992) carried out a comparative study onthe application of both methods in countries having adopted standards or exposure draftsdealing with the Statement of Cash Flows. A summary extract of this study is shown inexhibit 1.

INSERT EXHIBIT 1 HERE

These two direct methods are which is to provide information about cash receipts and cashpayments, than the indirect method.

5

In contrast, many providers of financial statements contend that the indirect method is lesscostly.

In practical terms, the information contained within a traditional accounting movement isoften insufficient for cash flow purposes. The basic information on cash flow is, however,required for the preparation and analysis of the Statement of Cash Flows. The constraints intraditional accounting give rise to two consequences:

• The Statement of Cash Flows becomes an imperfect representation of the underlyingconcepts: for example, purchases cash payments are calculated as the difference betweenpurchases and change in accounts payable balances at the beginning and the end of the period("semi-direct" method).

• the preparation of the Statement of Cash Flows requires prior analysis of accounts balancemovements and underlying transactions affecting the accounts, involving additional time andcosts.

The main question being raised is: "Why not analyse cash flows directly from their source -the accounting entries relating to receipts and payments?" The reply to this question isstraight-forward. It is difficult to analyse receipts and payments given the existing andtraditional structure of accounting entries. Once this is overcome, a "true" direct methodStatement of Cash Flows can be produced immediately.

2 - THE OBJECTIVES AND CONDITIONS OF CHANGE

The aim is to increase the effectiveness of accounting work by making it possible to draw upthe Statement of Cash Flows directly from the source accounting entries.

The Unified Accounting System proposes a change in the structure of accounting entries inorder to enable any one accounting entry to serve as a "data base" for further work oranalysis.

Two major innovation are proposed by Dormagen (1990): (1) to enter the purpose of eachentry, i.e. the reason for the movement in one or more accounts; (2) the creation of "junction"accounts allowing the liaison between accounts by nature and accounts by function.

We shall not be expanding on the second point as it lies outside of the scope of this paper.

6

2.1 The concept of object

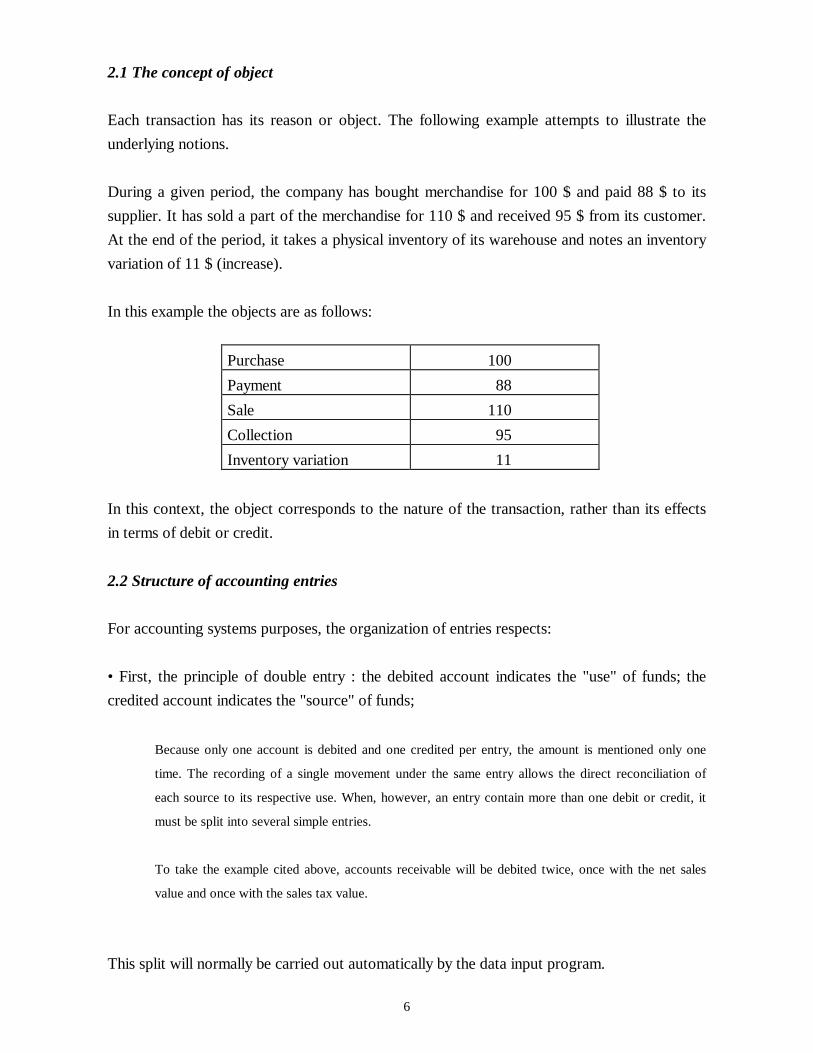

Each transaction has its reason or object. The following example attempts to illustrate theunderlying notions.

During a given period, the company has bought merchandise for 100 $ and paid 88 $ to itssupplier. It has sold a part of the merchandise for 110 $ and received 95 $ from its customer.At the end of the period, it takes a physical inventory of its warehouse and notes an inventoryvariation of 11 $ (increase).

In this example the objects are as follows:

Purchase 100Payment 88Sale 110Collection 95Inventory variation 11

In this context, the object corresponds to the nature of the transaction, rather than its effectsin terms of debit or credit.

2.2 Structure of accounting entries

For accounting systems purposes, the organization of entries respects:

• First, the principle of double entry : the debited account indicates the "use" of funds; thecredited account indicates the "source" of funds;

Because only one account is debited and one credited per entry, the amount is mentioned only one

time. The recording of a single movement under the same entry allows the direct reconciliation of

each source to its respective use. When, however, an entry contain more than one debit or credit, it

must be split into several simple entries.

To take the example cited above, accounts receivable will be debited twice, once with the net sales

value and once with the sales tax value.

This split will normally be carried out automatically by the data input program.

7

• Secondly, the need to know the object or purpose of the transaction to be codified in orderto permit automated processing.

3 - ORGANIZATION OF ENTRIES

3.1 Principle

We present below the standard accounting entries.

Use

(debited

account)

Source

(credited

account)

Object Amount

In the simplified example shown above (paragraph 2.1), the accounting entries can bepresented as follows:

8

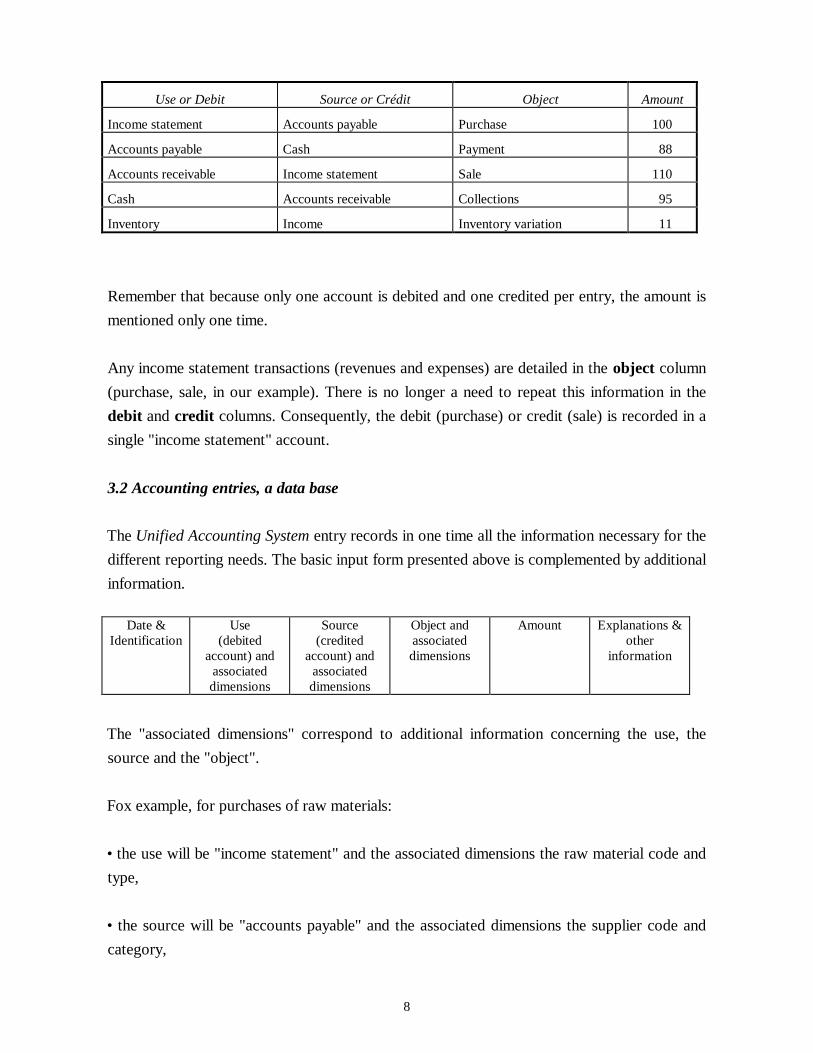

Use or Debit Source or Crédit Object Amount

Income statement Accounts payable Purchase 100

Accounts payable Cash Payment 88

Accounts receivable Income statement Sale 110

Cash Accounts receivable Collections 95

Inventory Income Inventory variation 11

Remember that because only one account is debited and one credited per entry, the amount ismentioned only one time.

Any income statement transactions (revenues and expenses) are detailed in the object column(purchase, sale, in our example). There is no longer a need to repeat this information in thedebit and credit columns. Consequently, the debit (purchase) or credit (sale) is recorded in asingle "income statement" account.

3.2 Accounting entries, a data base

The Unified Accounting System entry records in one time all the information necessary for thedifferent reporting needs. The basic input form presented above is complemented by additionalinformation.

Date &Identification

Use(debited

account) andassociateddimensions

Source(credited

account) andassociateddimensions

Object andassociateddimensions

Amount Explanations &other

information

The "associated dimensions" correspond to additional information concerning the use, thesource and the "object".

Fox example, for purchases of raw materials:

• the use will be "income statement" and the associated dimensions the raw material code andtype,

• the source will be "accounts payable" and the associated dimensions the supplier code andcategory,

9

• the "object" will be "purchases" and the associated dimensions the weight and volume...

Additional information could include the type of operation, payment conditions, the projectdetails...

All this information is linked and forms a whole.

All accounting data meet criteria which govern "data bases". The list of entries stores adescription of the transactions. Other lists store general data: the chart of accounts, thecustomers file, the suppliers file...

These lists include common items (accounts number, customers number, etc.) used to link thedata they contain.

They supply all data needed to draw up and analyse the statements peculiar to generalaccounting (balance sheet, income statement) and to cash (Statement of Cash Flows) from acommon source.

3.3 Actual implementation

Input of use, source and object at the same time does not cause any particular problem.

• The input format is designed to enter a datum needed or several entries only once. Forexample, the accounts payable account is entered first. The supplier code and invoicenumber are entered once for several entries concerning the invoice.

• Whenever possible, the object of the movement is automatically generated fromknowledge of the use and source concerned. If the source is a bank, and supplier is theuse, the object is payment.

3.4 Organizational aspects in the company

This organization of accounting entries facilitates the decentralization of accountingdepartments:

• because an entry describes all aspects of a transaction (source, use and object), it isimportant to input the data at a site close to the underlying transactions effected.

10

For example, to record an invoice properly, the payables accounting must be close to the supply and

reception departments, which have information about the order, the delivery, the result of checking,

etc.

• because the list of entries constitutes a common data source for different applications, datacan be input by those units which are directly responsible for the transaction.

For example, the payables accounting can be used to make and enter the payment, because it has the

necessary information and is in direct contact with the suppliers, even if the authorization to pay is

the final responsability of the treasurer.

Thus, the payables accounting can be made responsible for all aspects of operations involvedin processing an invoice, from purchase to payment.

4 - THE UNIFIED ACCOUNTING SYSTEM AND EVENT ACCOUNTING

5 - PREPARING A STATEMENT OF CASH FLOWS

We show below a limited example for pedagogical and demonstration purposes createdspecifically for this paper using the data base functions of Excel3. In practice, the UnifiedAccounting System, which is today in use, functions with data base software.

The following example shows how a Statement of Cash Flows can be prepared directly fromthe source accounting entries.

5.1 Example: transactions and accounting entries

Opening balance sheet

Assets Liabilities and stockholders'equity

Fixed assets("PPE")4 15 Capital stock 14

Less accumulated depreciation (5) Retained earnings 5

3 The choice of Excel was made simply because it is widely used and it is adequate for an illustration.4 Property, Plant and Equipment.

11

Inventories 9 Long-term debt 4

Accounts receivable 4 Accounts payable 8

Cash 8

Total 31 Total 31

During a given period, the following transactions are recorded (in $) :

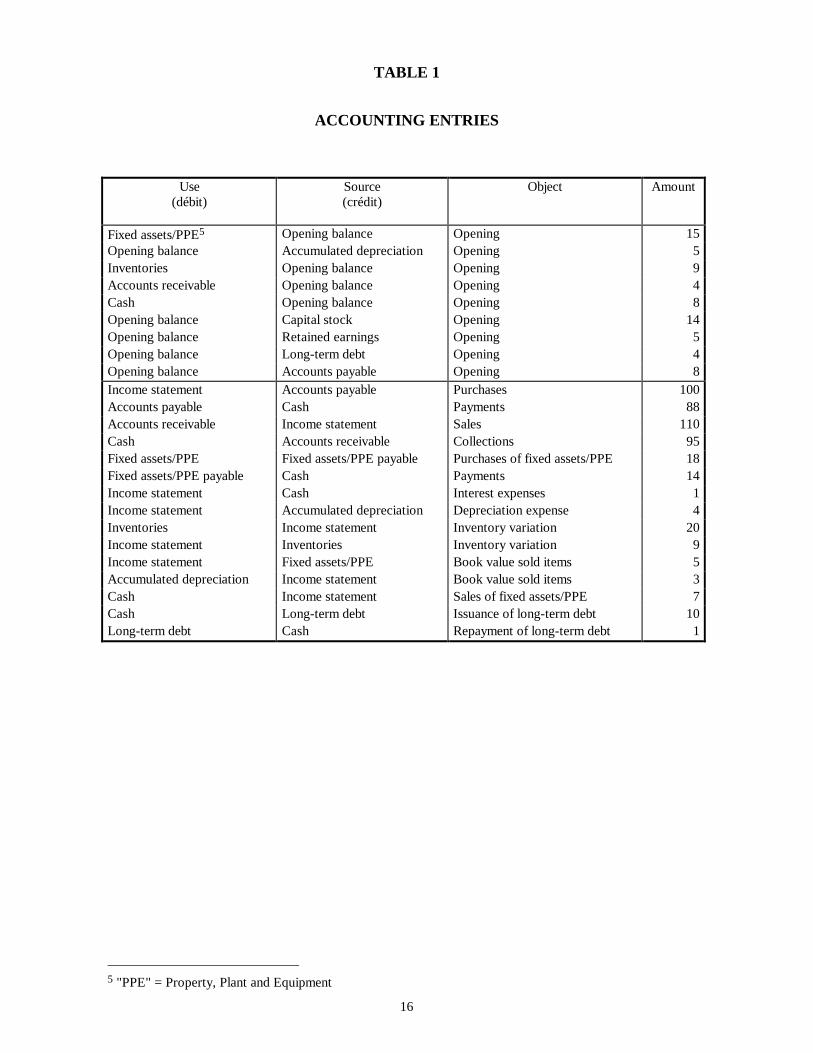

The accounting entries are shown in Table 1, as follows.

INSERT TABLE 1 HERE

Remember that the income statement accounting entries, debits or credits, are not at this stageanalysed or classified into expense or revenue types. The "object" of the original transactionand source accounting entry provides the detail composition of the income statement andindividual expense/revenue categories within the income statement.

5.2 Preparing the income statement

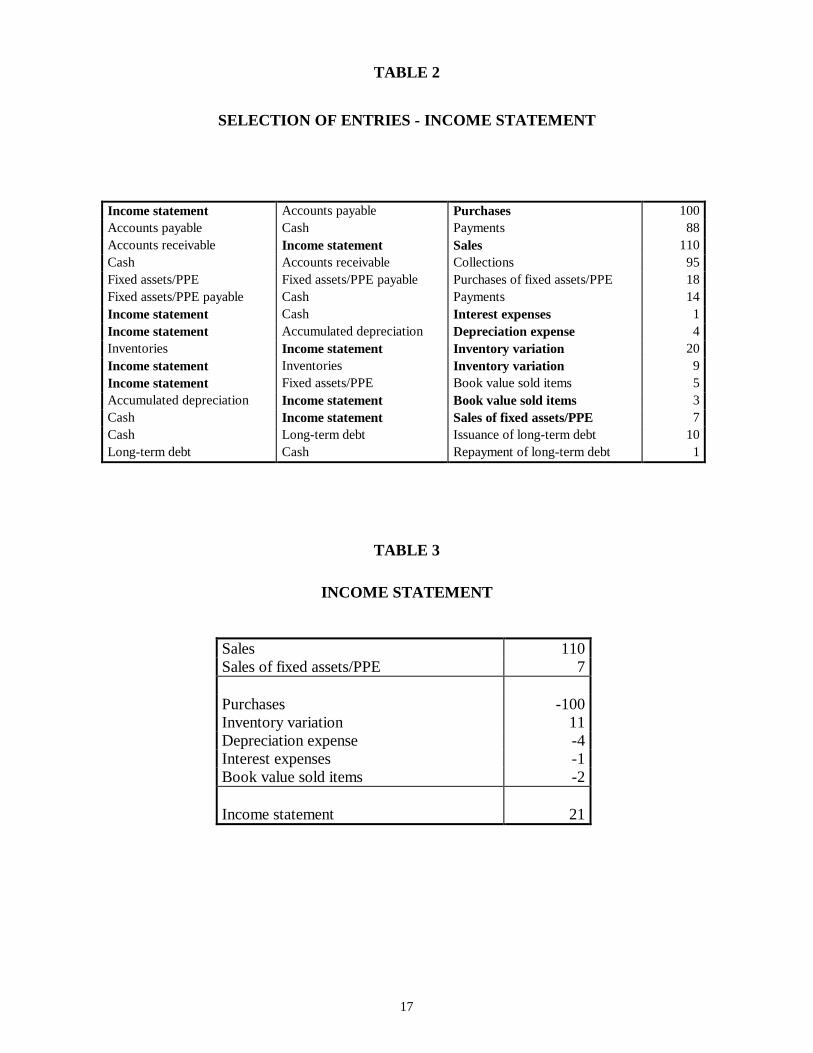

This step is not required for the preparation of a Statement of Cash Flows. For demonstrationpurposes, however, we show how the income statement is obtained by selecting entries whoseuse (debit) or source (credit) is "income", and sorting and grouping selected entries accordingto their object. Nonetheless, we are fully aware that an income statement can be obtainedusing a traditional accounting system.

The strength of the Unified Accounting System lies not in its ability to produce an incomestatement, but in its efficient use of accounting data to produce a direct method Statement ofCash Flows.

Table 2 gives the "selections" made by the program.

INSERT TABLE 2 HERE

As noted earlier, the object is expressed as expenses or revenues and corresponds to theaccounts by type (nature). The income statement is shown in table 3.

INSERT TABLE 3 HERE

12

In table 3, the entries are annoted as follows:

DEBIT (-) = USECREDIT (+) = SOURCE

5.3 The cash statement

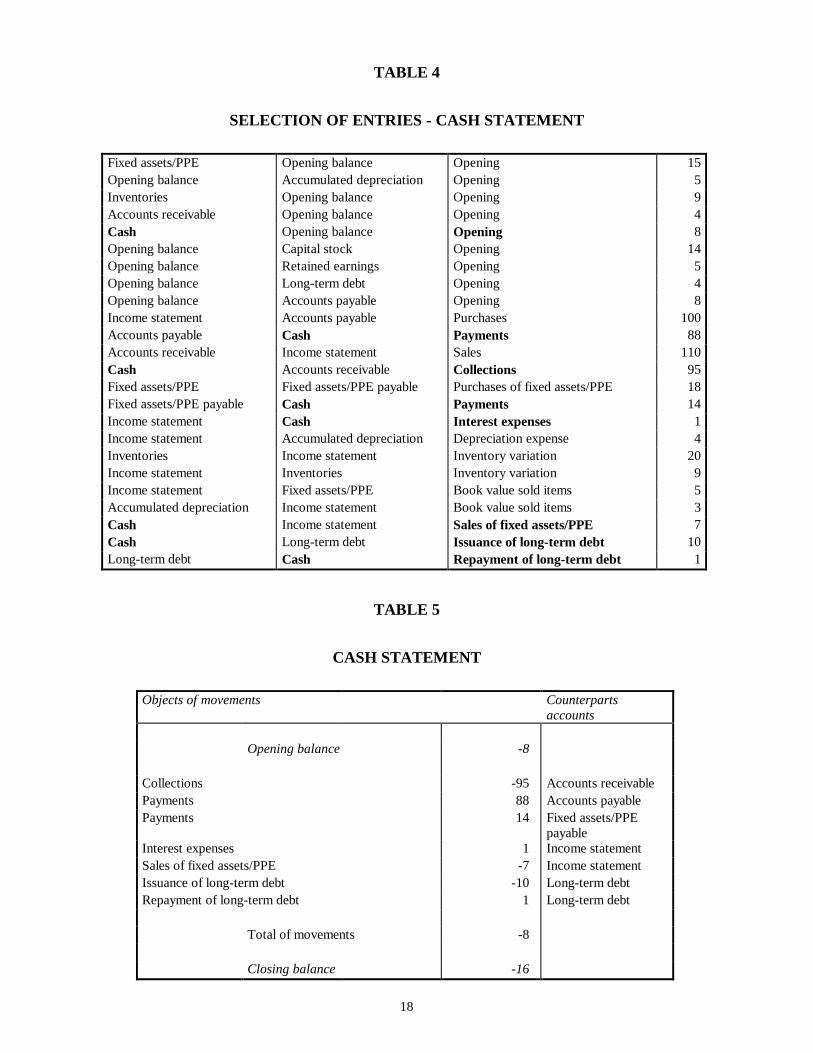

The connection existing between debit, credit and object of an entry, in the UnifiedAccounting System, means that movements affecting accounts may be analysed according tothe object of the movements but also the correlated accounts.

By selecting bank account entries, debits or credits, and then grouping the selected entriesaccording to:

• the object of the movements (collections, payments, etc.),• the correlated accounts (receivables, payables, etc.),

the entries can be used directly to analyse the cash variation giving the origin of the collectionor purpose of the payment for each type of movement (see table 4).

INSERT TABLE 4 HERE

The cash statement is now obtained (see table 5).

INSERT TABLE 5 HERE

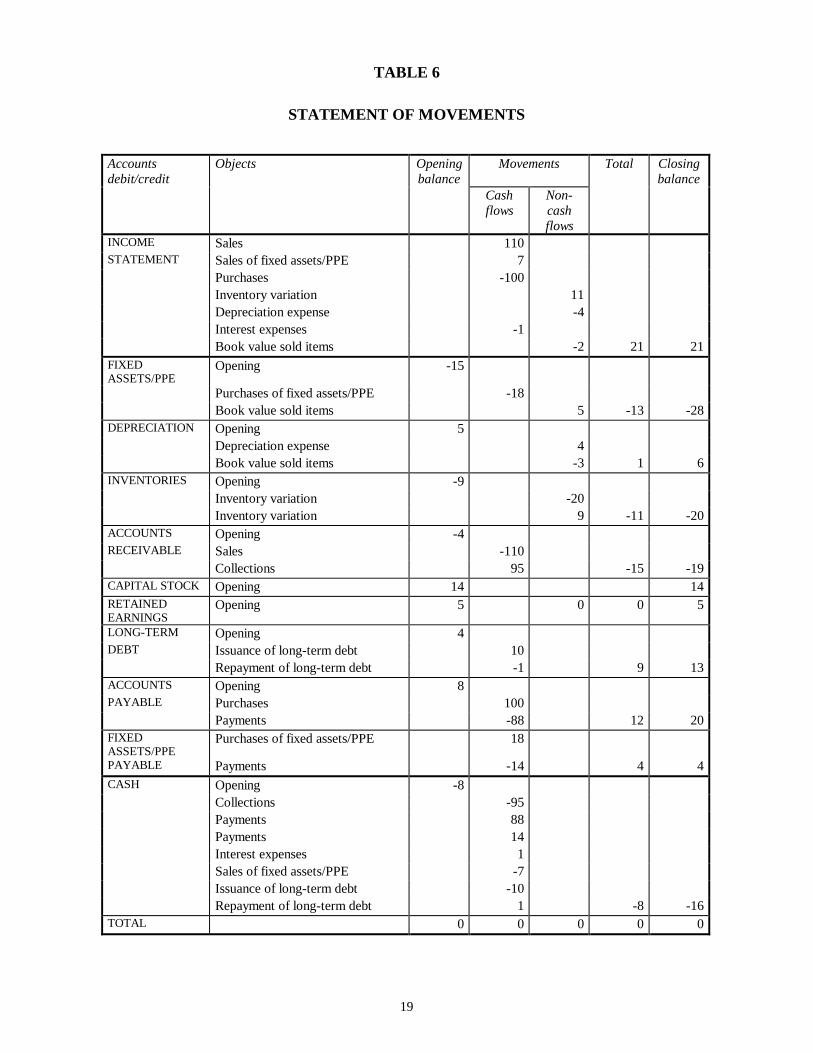

5.4 Statement of movements

Table 6 illustrates how all account balance movements may be summarized for analysis, i.e.

• by objects,• by cash-flow impacts,• by "non" cash-flow impact (depreciation, inventory variation, book value sold items) (seetable 6).

INSERT TABLE 6 HERE

13

5.5 Statement of cash flows (intermediary version)

Movements concerning funds flows are analysed according to the use (debit) or source(credit) they represent, i.e.:

• Income statement items - revenue and expenses column• Cash items - receipts and disbursements column• Other cases - other movements column (see table 7).

Account balance movements which stem from both income statement and cash relatedtransactions (cash revenues and expenses - financial costs; sale of assets), should normally bedealt with separately. However, since our objective is only to prepare a statement of cashflow, we have included both categories in the one column (receipts and payments).

INSERT TABLE 7 HERE

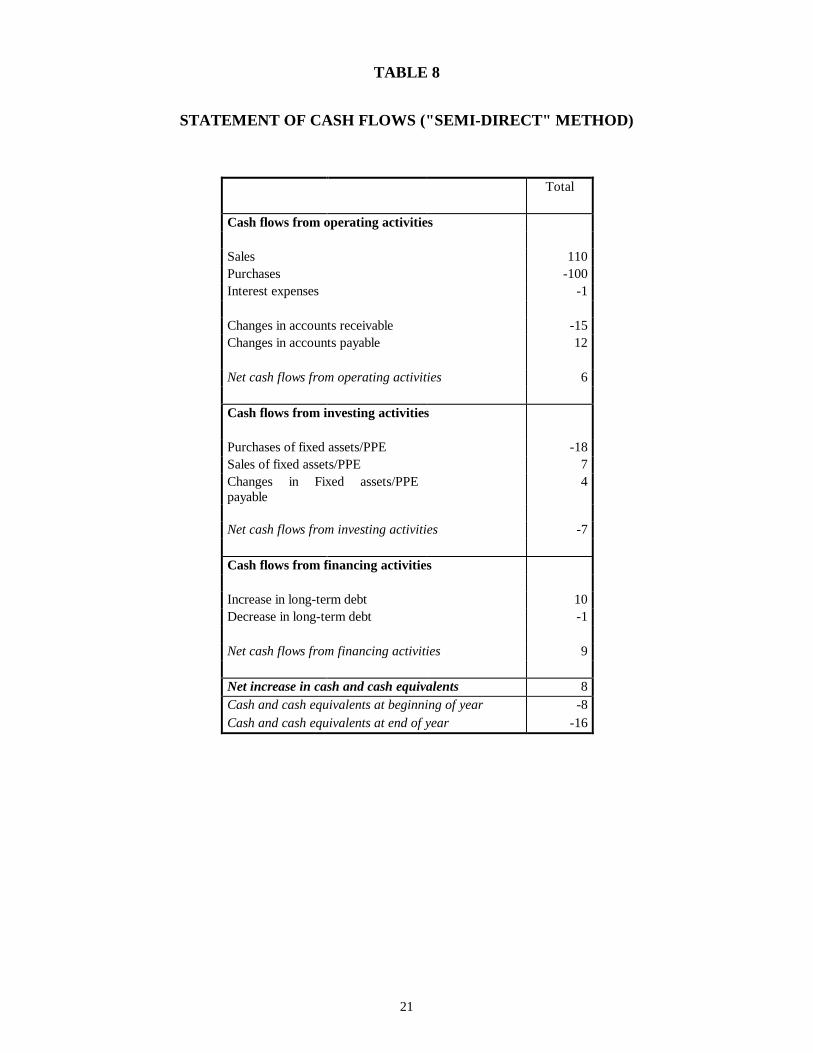

5.6 Statement of cash flows ("semi-direct" method version)

The "total" column of table 7 gives an unsatisfactory Statement of Cash Flows since the cashflow movements are reconstructed (sales cash receipts being the difference between sales andvariation in accounts receivable) (see table 8).

INSERT TABLE 8 HERE

5.7 Statement of cash flows ("true" direct version)

However in selecting the receipts and disbursements column only (in table 7), one obtains a"true" Statement of Cash Flows because each figure is an actual cash flow (table 9).

INSERT TABLE 9 HERE

CONCLUSION

The illustrated example can be applied for any cash flow model, since the data is sourceaccounting information which can be used in different ways, configurations, etc.

14

The integrated use of data processing has made it possible to develop these accountingtechniques which enable management to use more meaningfully the source accountinginformation and, thus, develop more effective information systems.

Thus, thanks to the Unified Accounting System, all statements and all analyses can now beproduced directly from book entries and more rapidly and more cheaply than in the traditionalaccounting system.

REFERENCES

FASB: Statement of Financial Accounting Standards (SFAS) No. 95 Statement of CashFlows, November 1987, 76 pages.

IASC: Exposure draft 36 Cash Flow Statements, 1991; IAS n° 7 Cash Flow Statements 1976,revised 1992.

Augustin, G.: La comptabilité et la révolution informatique. Masson, France, 1986, 173pages.

Degos, Jean-Guy: Histoire de la comptabilité matricielle : de l'amnésie à la réécriture. RevueFrançaise de Gestion n° 83, mars-avril-mai 1991, 18-28.

Dormagen, Jean-Claude: La comptabilité intégrée. La Villeguerin Editions, France, 1990.

Gensse, Pierre: Le renouvellement du modèle comptable : Evolution ou révolution ? RevueFrançaise de Comptabilité n° 139, October 1983, 374-383.

Gensse, Pierre: A propos de comptabilité multidimensionnelle... Revue Française deComptabilité n° 152, December 1984, 500-501.

Johnson O.: Toward an "Events" Theory Accounting. The Accounting Review, October 1970,641-653.

Kucic, A. Ronald and Samuel T. Battaglia: Matrix Accounting for the Statement of Changesin Financial Position. Management Accounting, April 1981, 27-32.

Lee, Tom A.: The Cash Flow Accounting Alternative for Corporate Financial Reporting. inFinancial Accounting Theory, edited by Stephen A. Zeff and Thomas F. Keller, Mc Graw-Hill, 3rd edition 1987, 275-282.

Leech, Stewart A.: The Theory and Development of a Matrix-Based Accounting System.Accounting and Business Research, Vol. 16, n° 64, 1986, 327-341.

Lieberman, A.Z. and A.B. Whinston: A Structuring of an Events - Accounting InformationSystem. The Accounting Review, April 1975, 246-258.

15

Mepham, M.J. : Matrix-Based Accounting: A Comment. Accounting and Business Research,Vol. 18, No. 72, 1988, 375-378.

Sorter, George H.: An "Events" Approach to Basic Accounting Theory. The AccountingReview, January 1969, 12-19.

Stepniewski J.: Principes de la comptabilité événementielle. Masson, France, 1987, 156pages.

Stolowy, Hervé and Sylvie Walser-Prochazka: The American Influence in Accounting: Mythor Reality? The Statement of Cash Flows Example. The International Journal of Accounting,1992, Vol. 3, 185-221.

16

TABLE 1

ACCOUNTING ENTRIES

Use(débit)

Source(crédit)

Object Amount

Fixed assets/PPE5 Opening balance Opening 15Opening balance Accumulated depreciation Opening 5Inventories Opening balance Opening 9Accounts receivable Opening balance Opening 4Cash Opening balance Opening 8Opening balance Capital stock Opening 14Opening balance Retained earnings Opening 5Opening balance Long-term debt Opening 4Opening balance Accounts payable Opening 8Income statement Accounts payable Purchases 100Accounts payable Cash Payments 88Accounts receivable Income statement Sales 110Cash Accounts receivable Collections 95Fixed assets/PPE Fixed assets/PPE payable Purchases of fixed assets/PPE 18Fixed assets/PPE payable Cash Payments 14Income statement Cash Interest expenses 1Income statement Accumulated depreciation Depreciation expense 4Inventories Income statement Inventory variation 20Income statement Inventories Inventory variation 9Income statement Fixed assets/PPE Book value sold items 5Accumulated depreciation Income statement Book value sold items 3Cash Income statement Sales of fixed assets/PPE 7Cash Long-term debt Issuance of long-term debt 10Long-term debt Cash Repayment of long-term debt 1

5 "PPE" = Property, Plant and Equipment

17

TABLE 2

SELECTION OF ENTRIES - INCOME STATEMENT

Income statement Accounts payable Purchases 100Accounts payable Cash Payments 88Accounts receivable Income statement Sales 110Cash Accounts receivable Collections 95Fixed assets/PPE Fixed assets/PPE payable Purchases of fixed assets/PPE 18Fixed assets/PPE payable Cash Payments 14Income statement Cash Interest expenses 1Income statement Accumulated depreciation Depreciation expense 4Inventories Income statement Inventory variation 20Income statement Inventories Inventory variation 9Income statement Fixed assets/PPE Book value sold items 5Accumulated depreciation Income statement Book value sold items 3Cash Income statement Sales of fixed assets/PPE 7Cash Long-term debt Issuance of long-term debt 10Long-term debt Cash Repayment of long-term debt 1

TABLE 3

INCOME STATEMENT

Sales 110Sales of fixed assets/PPE 7

Purchases -100Inventory variation 11Depreciation expense -4Interest expenses -1Book value sold items -2

Income statement 21

18

TABLE 4

SELECTION OF ENTRIES - CASH STATEMENT

Fixed assets/PPE Opening balance Opening 15Opening balance Accumulated depreciation Opening 5Inventories Opening balance Opening 9Accounts receivable Opening balance Opening 4Cash Opening balance Opening 8Opening balance Capital stock Opening 14Opening balance Retained earnings Opening 5Opening balance Long-term debt Opening 4Opening balance Accounts payable Opening 8Income statement Accounts payable Purchases 100Accounts payable Cash Payments 88Accounts receivable Income statement Sales 110Cash Accounts receivable Collections 95Fixed assets/PPE Fixed assets/PPE payable Purchases of fixed assets/PPE 18Fixed assets/PPE payable Cash Payments 14Income statement Cash Interest expenses 1Income statement Accumulated depreciation Depreciation expense 4Inventories Income statement Inventory variation 20Income statement Inventories Inventory variation 9Income statement Fixed assets/PPE Book value sold items 5Accumulated depreciation Income statement Book value sold items 3Cash Income statement Sales of fixed assets/PPE 7Cash Long-term debt Issuance of long-term debt 10Long-term debt Cash Repayment of long-term debt 1

TABLE 5

CASH STATEMENT

Objects of movements Counterpartsaccounts

Opening balance -8

Collections -95 Accounts receivablePayments 88 Accounts payablePayments 14 Fixed assets/PPE

payableInterest expenses 1 Income statementSales of fixed assets/PPE -7 Income statementIssuance of long-term debt -10 Long-term debtRepayment of long-term debt 1 Long-term debt

Total of movements -8

Closing balance -16

19

TABLE 6

STATEMENT OF MOVEMENTS

Accountsdebit/credit

Objects Openingbalance

Movements Total Closingbalance

Cashflows

Non-cashflows

INCOME Sales 110STATEMENT Sales of fixed assets/PPE 7

Purchases -100Inventory variation 11Depreciation expense -4Interest expenses -1Book value sold items -2 21 21

FIXEDASSETS/PPE

Opening -15

Purchases of fixed assets/PPE -18Book value sold items 5 -13 -28

DEPRECIATION Opening 5Depreciation expense 4Book value sold items -3 1 6

INVENTORIES Opening -9Inventory variation -20Inventory variation 9 -11 -20

ACCOUNTS Opening -4RECEIVABLE Sales -110

Collections 95 -15 -19CAPITAL STOCK Opening 14 14RETAINEDEARNINGS

Opening 5 0 0 5

LONG-TERM Opening 4DEBT Issuance of long-term debt 10

Repayment of long-term debt -1 9 13ACCOUNTS Opening 8PAYABLE Purchases 100

Payments -88 12 20FIXEDASSETS/PPE

Purchases of fixed assets/PPE 18

PAYABLE Payments -14 4 4CASH Opening -8

Collections -95Payments 88Payments 14Interest expenses 1Sales of fixed assets/PPE -7Issuance of long-term debt -10Repayment of long-term debt 1 -8 -16

TOTAL 0 0 0 0 0

20

TABLE 7

STATEMENT OF CASH FLOWS (INTERMEDIARY VERSION)

Revenues/ Receipts/ Other TotalExpenses Disbur-

sementsmovements

Cash flows from operating activities

Sales 110 110Purchases -100 -100Interest expenses -1 -1

Changes in accounts receivable -110 95 -15Changes accounts payable 100 -88 12

Net cash flows from operating activities 6Cash flows from investing activities

Purchases of fixed assets/PPE -18 -18Sales of fixed assets/PPE 7 7Changes in Fixed assets/PPEpayable

-14 18 4

Net cash flows from investing activities -7Cash flows from financing activities

Increase in long-term debt 10 10Decrease in long-term debt -1 -1

Net cash flows from financing activities 9Net increase in cash and cash equivalents 0 8 0 8

21

TABLE 8

STATEMENT OF CASH FLOWS ("SEMI-DIRECT" METHOD)

Total

Cash flows from operating activities

Sales 110Purchases -100Interest expenses -1

Changes in accounts receivable -15Changes in accounts payable 12

Net cash flows from operating activities 6

Cash flows from investing activities

Purchases of fixed assets/PPE -18Sales of fixed assets/PPE 7Changes in Fixed assets/PPEpayable

4

Net cash flows from investing activities -7

Cash flows from financing activities

Increase in long-term debt 10Decrease in long-term debt -1

Net cash flows from financing activities 9

Net increase in cash and cash equivalents 8Cash and cash equivalents at beginning of year -8Cash and cash equivalents at end of year -16

22

TABLE 9

STATEMENT OF CASH FLOWS ("TRUE" DIRECT METHOD)

Cash flows from operating activities

Cash receipts from sales 95

Cash payments for• Purchases -88• Interest Payments -1

Net cash flows from operating activities 6Cash flows from investing activities

Purchase of equipment -14Sale of equipment 7

Net cash flows from investing activities -7Cash flows from financing activities

Increase in long-term debt 10Decrease in long-term debt -1

Net cash flows from financing activities 9Net increase in cash and cash equivalents 8Cash and cash equivalents at beginning of year -8Cash and cash equivalents at end of year -16

23

EXHIBIT 1

CALCULATING CASH FLOWS FROM OPERATING ACTIVITIES: DIRECT ANDINDIRECT METHODS6

One method of reporting cash flows from operating activities is the direct method, whichdiscloses major classes of gross cash receipts and gross cash payments. Another method ofreporting cash flows from operating activities is the indirect method, which discloses the netcash flow from operating activities by adding back and in some cases substracting, to the netincome, non-cash items included in the determination of this net income .

All the countries included in the study 7 refer to at least one of the two methods. Moreover,France has some specific characteristics which are noted below.

1 - The choice of direct or indirect method

The countries examined have made different choices concerning the method to be used, asshown in the following schedule:

USA/IASC -UK/IRELAND

NEW ZEALANDAUSTRALIA

SOUTH AFRICA CANADA FRANCE

Direct methodrecommended

Direct methodrecommended

Combination ofdirect and indirect

methods

Both methodsauthorised

2 indirect methods

Indirect methodauthorised

Reconciliation withnet income possible

in notes

The USA, the UK and Ireland, and the IASC strongly encourage enterprises to calculate thenet cash flow from operating activities by the direct method. However, as stated in ED 36 8 ofthe IASC, many enterprises may not be able to report gross operating cash flows withoutincurring substantial costs that may outweigh the benefits of the information to external users.

This is why SFAS 95, FRS 1 and IAS 7 (revised 1992) allow the indirect method to be used 9.

6 Extract updated from the article by Hervé Stolowy and Sylvie Walser-Prochazka: The American Influence inAccounting: Myth or Reality? The Statement of Cash Flows Example. The International Journal ofAccounting, 1992, Vol. 3, 185-221.7 Australia, Canada, the USA, France, New Zealand, South Africa, the United Kingdom and Ireland, plus theInternational Accounting Standards Committee (IASC).8 This comment was not included in the IAS 7 (revised 1992).9 It has also been suggested tha the real reason in these three cases is that a large enough minority wantedretention of the indirect method.

24

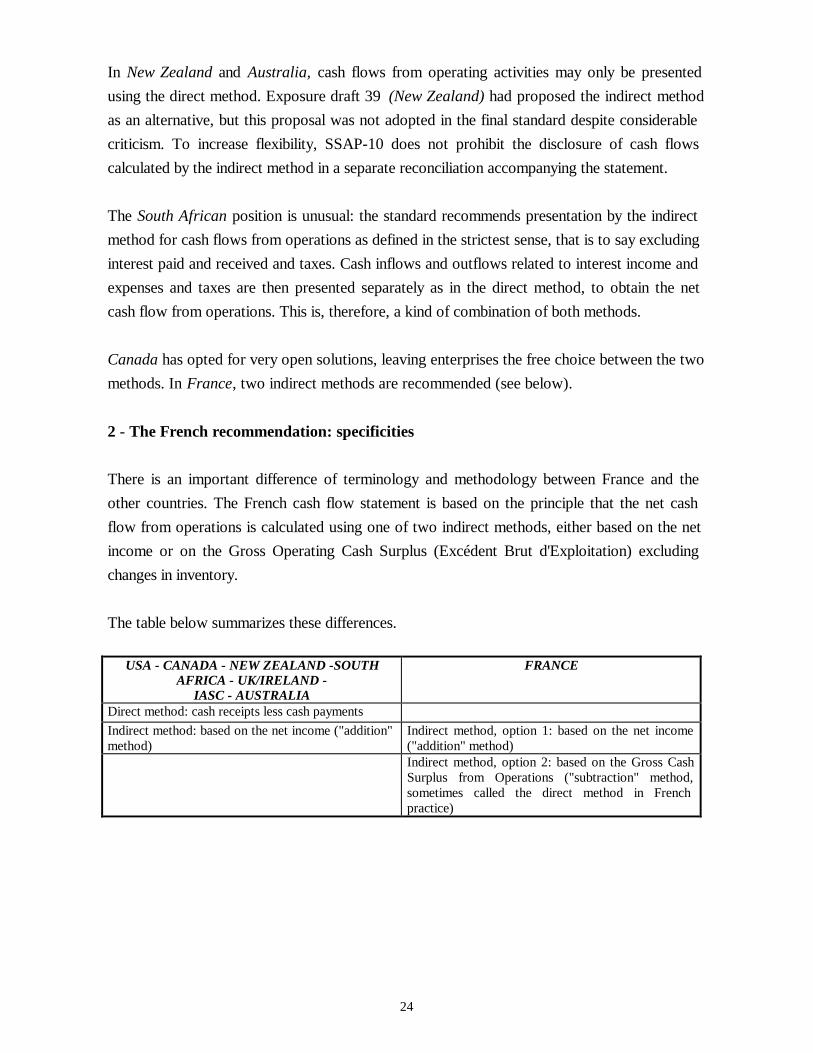

In New Zealand and Australia, cash flows from operating activities may only be presentedusing the direct method. Exposure draft 39 (New Zealand) had proposed the indirect methodas an alternative, but this proposal was not adopted in the final standard despite considerablecriticism. To increase flexibility, SSAP-10 does not prohibit the disclosure of cash flowscalculated by the indirect method in a separate reconciliation accompanying the statement.

The South African position is unusual: the standard recommends presentation by the indirectmethod for cash flows from operations as defined in the strictest sense, that is to say excludinginterest paid and received and taxes. Cash inflows and outflows related to interest income andexpenses and taxes are then presented separately as in the direct method, to obtain the netcash flow from operations. This is, therefore, a kind of combination of both methods.

Canada has opted for very open solutions, leaving enterprises the free choice between the twomethods. In France, two indirect methods are recommended (see below).

2 - The French recommendation: specificities

There is an important difference of terminology and methodology between France and theother countries. The French cash flow statement is based on the principle that the net cashflow from operations is calculated using one of two indirect methods, either based on the netincome or on the Gross Operating Cash Surplus (Excédent Brut d'Exploitation) excludingchanges in inventory.

The table below summarizes these differences.

USA - CANADA - NEW ZEALAND -SOUTHAFRICA - UK/IRELAND -

IASC - AUSTRALIA

FRANCE

Direct method: cash receipts less cash paymentsIndirect method: based on the net income ("addition"method)

Indirect method, option 1: based on the net income("addition" method)Indirect method, option 2: based on the Gross CashSurplus from Operations ("subtraction" method,sometimes called the direct method in Frenchpractice)