Embed Size (px)

Citation preview

The Use of Technology to Promote Voluntary Savings

Kenya’s Experience

Nzomo Mutuku Chief Executive Office

Retirement Benefits Authority

October 4, 2018

Mexico City, Mexico CONSAR

“A Dynamic and Secure Retirement Benefits Sector”

v

Agenda

v About Kenya and RBA

v Diagnosis

v Barriers

v Promoting Voluntary Savings through ICT

v Challenges

v Conclusion

2

v

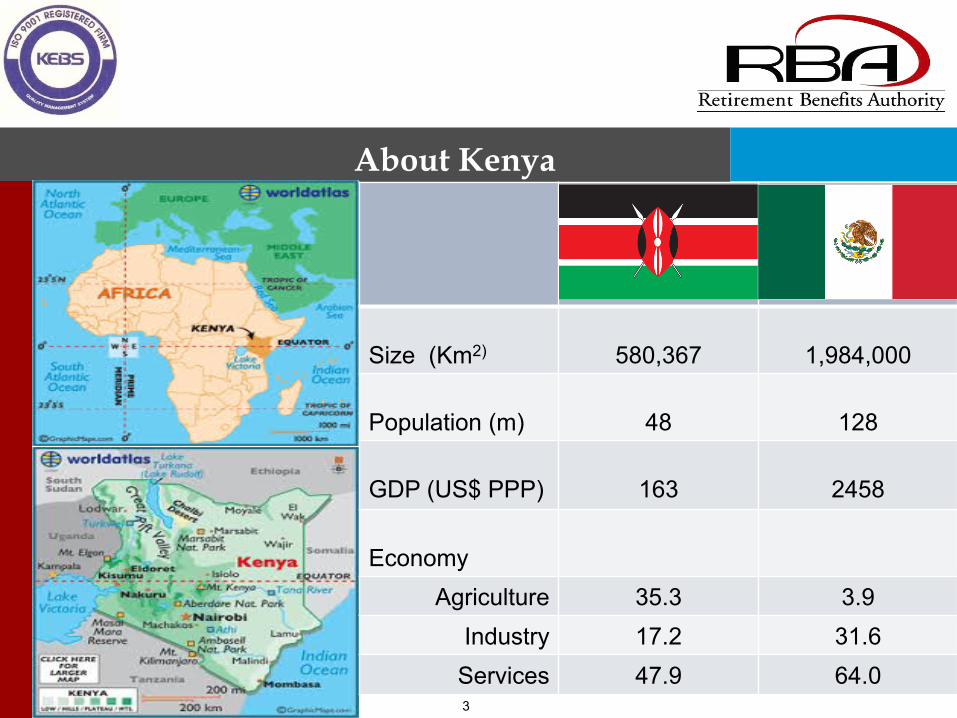

About Kenya

3

Size (Km2)

580,367

1,984,000

Population (m)

48

128

GDP (US$ PPP)

163

2458

Economy

Agriculture 35.3 3.9 Industry 17.2 31.6 Services 47.9 64.0

v

About RBA

v The Retirement Benefits sector in Kenya is covered under the

Retirement Benefits Act No. 3 of 1997 .

v The Act also established the Retirement Benefits Authority (RBA),

which is the retirement benefits regulatory body under the National

Treasury.

v RBA began its operations in October 2000 with the gazettement of

RBA Regulations & commencement of the Act

v Received is ISO 9001:2015 certification

4

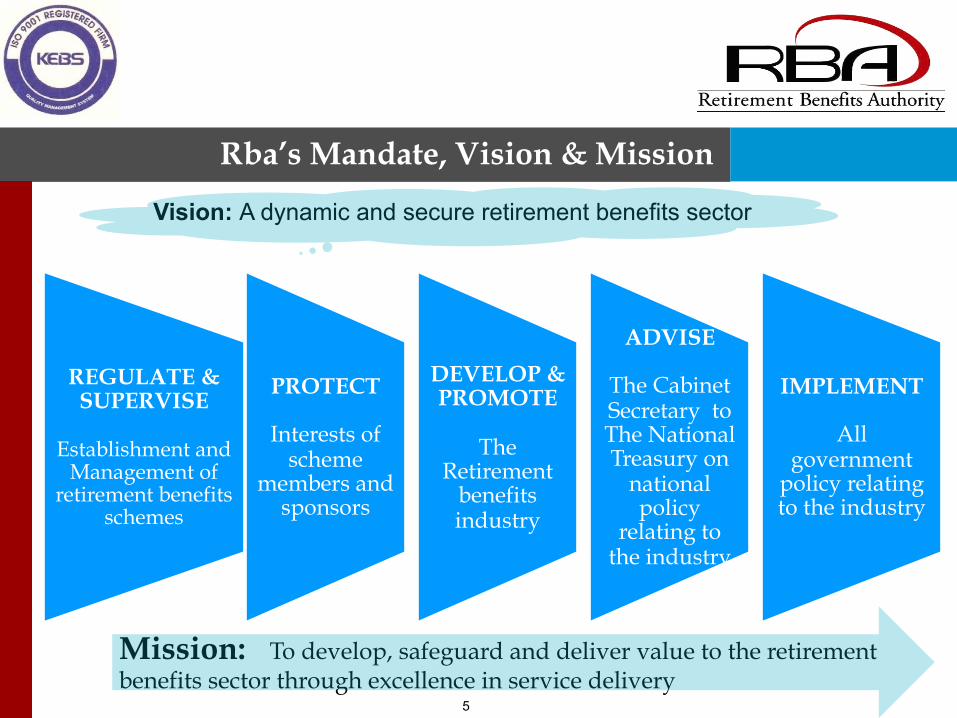

Rba’s Mandate, Vision & Mission

5

REGULATE & SUPERVISE

Establishment and

Management of retirement benefits

schemes

PROTECT

Interests of scheme

members and sponsors

DEVELOP & PROMOTE

The

Retirement benefits industry

ADVISE

The Cabinet Secretary to The National Treasury on

national policy

relating to the industry

IMPLEMENT

All government

policy relating to the industry

Vision: A dynamic and secure retirement benefits sector

Mission: To develop, safeguard and deliver value to the retirement benefits sector through excellence in service delivery

IOPS Membership

v RBA has been a member of IOPS almost from inception

v RBA is the immediate past President of IOPS for two terms ending April 2017

v RBA has benefited from many of IOPS activities including standards, principles, Risk Based Supervision and shared experiences from member jurisdictions and contributed also to the knowledge base through its own experiences.

v The same applies to the area of use of ICT in pensions

6

Diagnosis - Structure of the Retirement Benefits Sector

Pension System

Non Contributory/Pay

As You Go (PAYG)

Civil Service Pension

Scheme Members ->550,000

Asset Public Service

Superannuation Act 2012 - DC

Private Occupational – Employer Based

( Voluntary) Members >500,000

DB & DC

Individual Contributory Open

Schemes Members -200,000

DC

Mandatory National Social Security Fund Members >2.1m

DC NSSF Act 2013 – Pension

& Provident

7

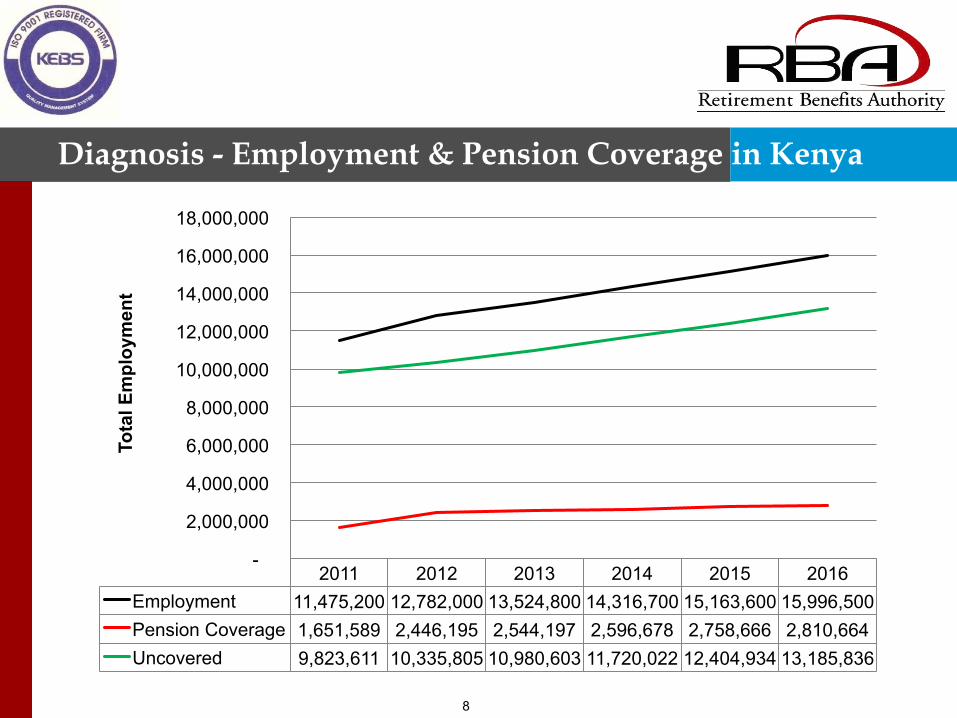

Diagnosis - Employment & Pension Coverage in Kenya

8

2011 2012 2013 2014 2015 2016 Employment 11,475,200 12,782,000 13,524,800 14,316,700 15,163,600 15,996,500 Pension Coverage 1,651,589 2,446,195 2,544,197 2,596,678 2,758,666 2,810,664 Uncovered 9,823,611 10,335,805 10,980,603 11,720,022 12,404,934 13,185,836

-

2,000,000

4,000,000

6,000,000

8,000,000

10,000,000

12,000,000

14,000,000

16,000,000

18,000,000

Tota

l Em

ploy

men

t

Barriers – Structure of Employment in Kenya

9

17.5 17.3 16.8

82.5 82.7 83.2

0.0

20.0

40.0

60.0

80.0

100.0

120.0

2012 2014 2016

SHAREOFEMPLOYMENT,%

FormalSector InformalSector

0

2000

4000

6000

8000

10000

12000

14000

2012 2014 2016

EMPLOYMENTINKENYA,000s

FormalSector InformalSector

Barriers – Characteristics of Informal Sector

v Informal Sector workers;

v Generally earn low and irregular incomes

v Change jobs & economic activities frequently thereby experiencing high labor mobility

v No monthly payroll to facilitate predetermined monthly contributions towards their retirement benefits.

v Exclusion from the formal financial system and lack of physical access to financial services

10

Promoting Voluntary Savings through ICT - I

v Given the low pension coverage [20%] of the total work force covered in registered existing retirement plans, new initiatives to extend pension coverage became profound.

v (RBA), working together with other stakeholders in the industry, has had to come up with initiatives to expand pension coverage, especially to the informal sector.

v The existing “pension gap” in the country require considerable measures to encourage supplementary personal pension savings

v Some of the measures include encouraging IPPs [36] where individuals can save voluntarily especially using mobile platforms

11

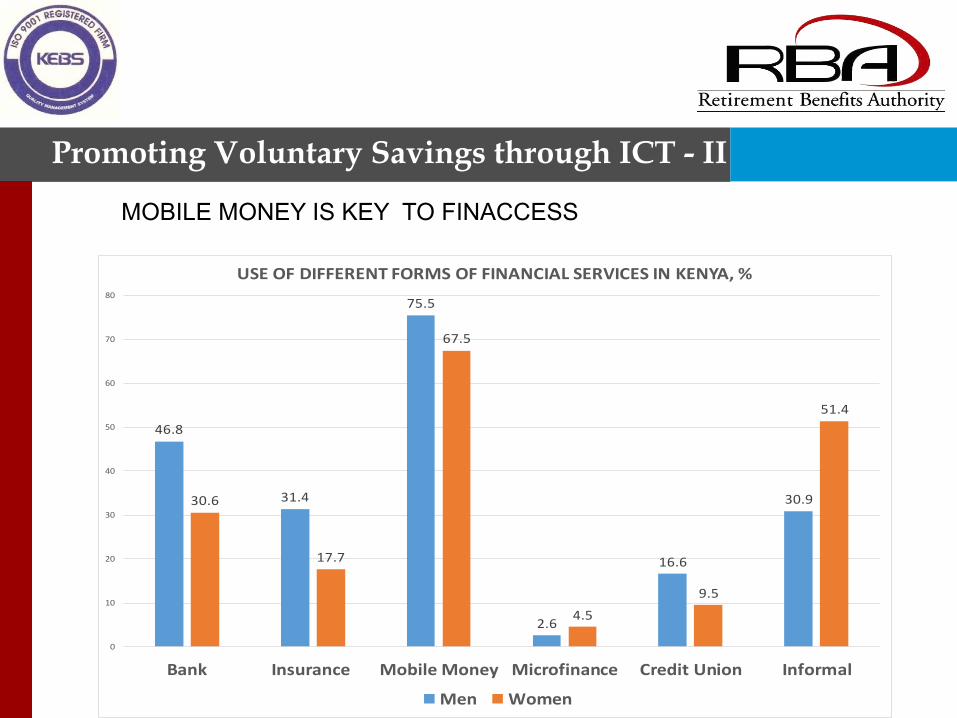

12

46.8

31.4

75.5

2.6

16.6

30.930.6

17.7

67.5

4.5

9.5

51.4

0

10

20

30

40

50

60

70

80

Bank Insurance MobileMoney Microfinance CreditUnion Informal

USEOFDIFFERENTFORMSOFFINANCIALSERVICESINKENYA,%

Men Women

MOBILE MONEY IS KEY TO FINACCESS

Promoting Voluntary Savings through ICT - II

Promoting Voluntary Savings through ICT - III

v Birth of Mbao Pension Plan;

v The Blue MSME Jua Kali Individual Retirement Benefits Scheme popularly known as the “Mbao Pension Plan” which targets the larger working population (85%) in the informal (Jua Kali) sector was conceptualized and officially launched in June 2011 and gained immense popularly among the population working in the informal sector and the self employed.

v Target workers in the informal sector who run micro, small and medium enterprises (MSMEs)

v It is a voluntary defined contribution provident fund.

v It began as a successful Corporate Social Investment (CSI) initiative.

13

14

v MBAO SME Individual Pension Scheme is one of 36 Independent Individual Pension Plans (IPPs) regulated by the RBA.

v “Mbao” is a colloquial term for twenty (20) shillings which is the minimum amount members are encouraged to contribute on a daily basis

v Mbao Pension Scheme, was the world’s first wholly mobile phone based pension scheme and specifically targets workers in the informal sector

v Mbao uses the mobile money transfer services offered by the two leading mobile phone networks in Kenya, namely, Safaricom and Airtel which allows real time transfers 24 hours a day from anywhere within the network coverage

Promoting Voluntary Savings through ICT - IV

15

v Like other IPPS Mbao has independent service providers including Corporate Trustee, Administrator, Custodian and Fund Manager

v Mbao model by allowing voluntary contributions by informal sector workers through the mobile phone overcomes the challenges informal sector workers face: v irregular income, v exclusion from the formal financial system and v lack of physical access to financial services

v Mbao scheme is the largest IPP in terms of members with over 100,000 members but is relatively small in terms of assets due to low level of contributions.

Promoting Voluntary Savings through ICT - V

Promoting Voluntary Savings through ICT - VI

v The contributions are reflected instantly on the members’ phones as receipted by the Fund and are able to check contribution balances.

v Mbao Pension Plan has helped address 3 things;

v Problem of low incomes - Kshs.20 per day is affordable to most people working in the informal sector.

v Seasonality/irregularity of incomes - in the sector for they can make bulk contributions to cover periods of no income

v high labor mobility - in the sector because by using mobile phones to make contributions, they can do it from anywhere any time, day or night.

v Mbao membership stands at over 100,000 members with a fund value of Kshs. 140 million by June 2018. It is currently the largest IPP by membership

16

In Summary Enable Informal Sector workers save for retirement by development and promoting

innovative pension products

17

MBAO INDIVIDUAL RETIRMENT BENEFITS SCHEME

Mobile Phone Based

(Mpesa)

Regulated by RBA

Independent Service

providers

Assets US$ 1.5m

Members 100,000

Founded by Informal Sector

Workers Groups

Challenges Facing Mbao

v Competing priorities of members such as medical and emergencies

v One size fits all approach yet informal sector very diverse

v High level of withdrawals from scheme

v Inconsistency and lack of sustainability of contributions- contributions taper off after time

v Competing savings vehicles perceived to offer value addition – Credit

v IT platform not robust – designed for formal sector scheme

v Questionable economic viability – perception as a Corporate Social Responsibility

v Need for sustained marketing campaigns which is very costly

18

Proposed Solutions

v Implement sub micro-pension schemes targeted at sub sectors of the informal sector

v Bundle pension with other financial services such as insurance and credit

v Implement a Specialized Micro-Pension Administration System v Strengthen Governance and capacity building to the Sponsor,

Trustee v Integration of financial literacy in school curriculum and

publicity campaign to promote old age savings by low income informal sector workers

v Matching contribution by the Government? v Auto-enrolment?

19

Conclusion

v Informality of employment is an established feature of working patterns on the African continent and in many other developing countries

v Informality makes the roll - out of centralized programs challenging, particularly those that require an active decision of citizens to participate, even more when such participation involves a financial contribution with pay - off only in the distant future.

v Substantial effort is therefore required to understand the needs and aspirations of informal sector workers before deploying a system for voluntary pension savings – based on our experience.

20

Asante

www.rba.go.ke

21