Embed Size (px)

Citation preview

Report of Examination of

The Western and Southern Life Insurance Company Cincinnati, Ohio

As of December 31, 2012

Table of Contents Subject Page Salutation ............................................................................................................................ 1 Description of Company ..................................................................................................... 1 Scope of Examination ......................................................................................................... 1 Management and Control: Board of Directors ......................................................................................................... 2 Officers .......................................................................................................................... 3 Insurance Holding Company System ............................................................................ 4 Territory and Plan of Operations ........................................................................................ 4 Reinsurance ......................................................................................................................... 5 Financial Statements: Statement of Assets, Liabilities, Surplus and Other Funds ............................................ 6 Statement of Operations ................................................................................................. 8 Statement of Changes in the Capital and Surplus Account ............................................ 9 Notes to Financial Statements: Investments ..................................................................................................................... 9 Policy Reserves and Related Actuarial Items ................................................................. 9 Conclusion .......................................................................................................................... 10 Acknowledgement .............................................................................................................. 10

1

Columbus, Ohio August 9, 2013 Honorable Mary Taylor Lieutenant Governor/Director State of Ohio Department of Insurance 50 West Town Street 3rd Floor – Suite 300 Columbus, Ohio 43215 Dear Lieutenant Governor/Director: In accordance with Section 3901.07 of the Ohio Revised Code (“ORC”), the Ohio Department of Insurance (“Department”) conducted an examination of

The Western and Southern Life Insurance Company

an Ohio domiciled, stock, life insurance company, hereinafter referred to as the “Company.”

Scope of Examination The Department last examined the Company as of December 31, 2007. The Department’s current examination covers the period of January 1, 2008 through December 31, 2012. The examination was conducted in accordance with the National Association of Insurance Commissioners (“NAIC”) Financial Condition Examiners Handbook (“Handbook”). The Handbook requires that the Department plan and perform the examination to evaluate the Company’s financial condition and identify prospective risks including corporate governance, identify and assess inherent risks and evaluate system controls and procedures used to mitigate those risks. An examination also includes assessing the principles used and significant estimates made by management, as well as evaluating the overall financial statement presentation, management’s compliance with Statutory Accounting Principles and annual statement instructions when applicable to domestic state regulations. All accounts and activities of the Company were considered in accordance with the risk-focused examination process. For all years under examination, the Certified Public Accounting firm of Ernst & Young LLP provided an unqualified opinion on the Company’s financial statements based on Statutory Accounting Principles. The audited financial reports were reviewed during the examination.

2

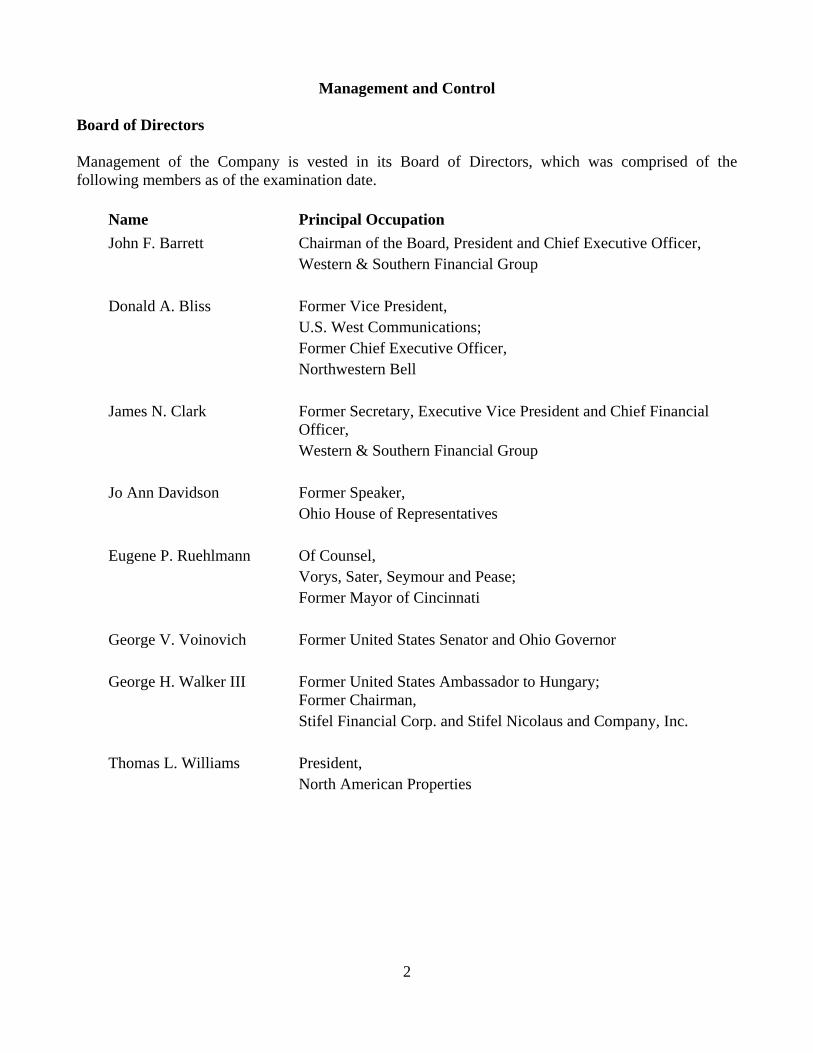

Management and Control Board of Directors Management of the Company is vested in its Board of Directors, which was comprised of the following members as of the examination date.

Name Principal Occupation John F. Barrett Chairman of the Board, President and Chief Executive Officer, Western & Southern Financial Group Donald A. Bliss Former Vice President, U.S. West Communications; Former Chief Executive Officer, Northwestern Bell James N. Clark Former Secretary, Executive Vice President and Chief Financial

Officer, Western & Southern Financial Group Jo Ann Davidson Former Speaker, Ohio House of Representatives Eugene P. Ruehlmann Of Counsel, Vorys, Sater, Seymour and Pease; Former Mayor of Cincinnati George V. Voinovich Former United States Senator and Ohio Governor George H. Walker III Former United States Ambassador to Hungary;

Former Chairman, Stifel Financial Corp. and Stifel Nicolaus and Company, Inc. Thomas L. Williams President, North American Properties

3

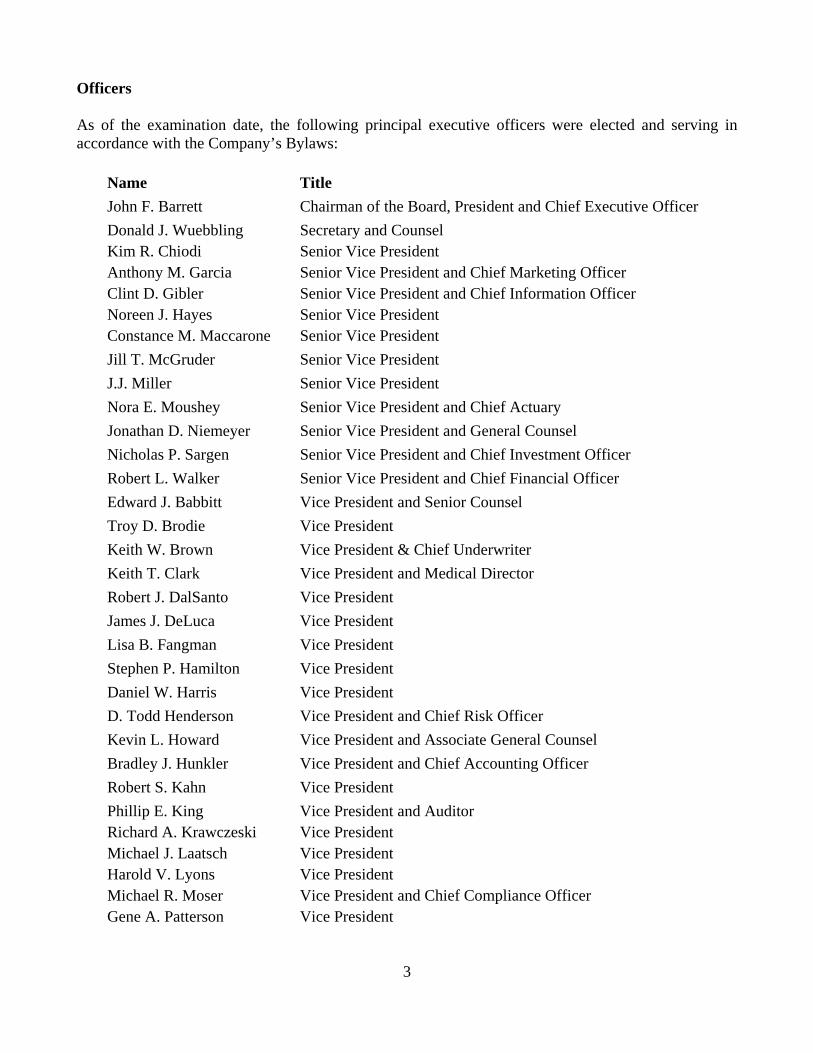

Officers As of the examination date, the following principal executive officers were elected and serving in accordance with the Company’s Bylaws:

Name Title John F. Barrett Chairman of the Board, President and Chief Executive Officer Donald J. Wuebbling Kim R. Chiodi Anthony M. Garcia Clint D. Gibler Noreen J. Hayes Constance M. Maccarone

Secretary and Counsel Senior Vice President Senior Vice President and Chief Marketing Officer Senior Vice President and Chief Information Officer Senior Vice President Senior Vice President

Jill T. McGruder Senior Vice President J.J. Miller Senior Vice President Nora E. Moushey Senior Vice President and Chief Actuary Jonathan D. Niemeyer Senior Vice President and General Counsel Nicholas P. Sargen Senior Vice President and Chief Investment Officer Robert L. Walker Senior Vice President and Chief Financial Officer Edward J. Babbitt Vice President and Senior Counsel Troy D. Brodie Vice President Keith W. Brown Vice President & Chief Underwriter Keith T. Clark Vice President and Medical Director Robert J. DalSanto Vice President James J. DeLuca Vice President Lisa B. Fangman Vice President Stephen P. Hamilton Vice President Daniel W. Harris Vice President D. Todd Henderson Vice President and Chief Risk Officer Kevin L. Howard Vice President and Associate General Counsel Bradley J. Hunkler Vice President and Chief Accounting Officer Robert S. Kahn Vice President Phillip E. King Richard A. Krawczeski Michael J. Laatsch Harold V. Lyons Michael R. Moser Gene A. Patterson

Vice President and Auditor Vice President Vice President Vice President Vice President and Chief Compliance Officer Vice President

4

Name Keith M. Payne Douglas I. Ross Mario J. San Marco Luc P. Sicotte Denise L. Sparks Jeffrey L. Stainton Thomas M. Stapleton Richard K. Taulbee David E. Theurich James J. Vance

Title Vice President Vice President and Chief Technical Officer Vice President Vice President Vice President Vice President and Associate General Counsel Vice President Vice President Vice President Vice President and Treasurer

Insurance Holding Company System The Company is a member of a holding company system as defined in Section 3901.32 of the ORC. The Company is a wholly owned subsidiary of Western & Southern Financial Group, Inc., which is a wholly owned subsidiary of Western-Southern Mutual Holding Company, the ultimate controlling person in the holding company system.

Territory and Plan of Operations

The Company’s main product offerings include whole life, juvenile term life, critical illness, accident insurance and personalized needs analysis. The Company’s products are sold through a captive agent distribution channel from 181 offices nationwide, plus an internet channel and a home office Client Relationship Center. Products are tailored towards individuals, families and businesses in the middle income markets. The Company is licensed in the District of Columbia and in all states except Alaska, Connecticut, Maine, Massachusetts, New Hampshire, New York and Vermont. During 2012, the largest states in terms of direct premium written allocable by state were as follows: Ohio, $64.6 million (28.3%); North Carolina, $23.9 million (10.4%); Illinois, $23.1 million (10.1%); Indiana, $20.0 million (8.8%); and Pennsylvania, $12.5 million (5.5%). The table below illustrates the Company’s 2012 direct and net premiums written, in thousands, by line of business:

Line of Business Direct Assumed Ceded Net Net %

Industrial life $ 14,583 $ - $ - $ 14,583 5.2 Ordinary life insurance 227,400 1,434 1,129 227,705 81.6 Ordinary individual annuities 172 4,523 - 4,695 1.7 Group life insurance 5,908 - - 5,908 2.1 Other accident and health 30,459 - 4,181 26,278 9.4 Totals $278,522 $ 5,957 $ 5,310 $ 279,169 100.0

5

Reinsurance The Company cedes business to various unaffiliated reinsurers pursuant to the terms of various agreements. Most of the Company’s cessions are existing ordinary life risks. The maximum amount of exposure retained on any one life is $2,000,000 on ordinary life risks. All contracts examined contained the necessary clauses to meet the guidelines prescribed by the NAIC.

Financial Statements

The financial condition and the results of its operations for the five-year period under examination as reported and filed by the Company with the Department and audited by the Company’s external auditors are reflected in the following:

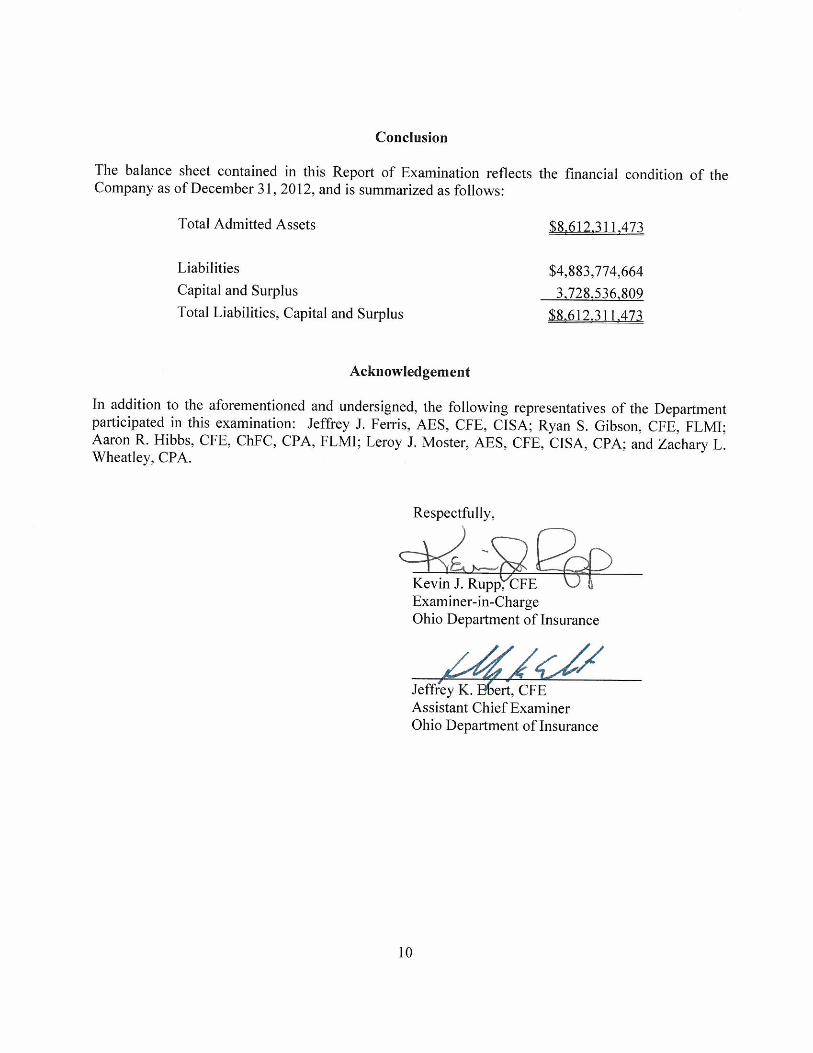

Statement of Assets, Liabilities, Surplus and Other Funds Summary of Operations Statement of Changes in the Capital and Surplus Account

6

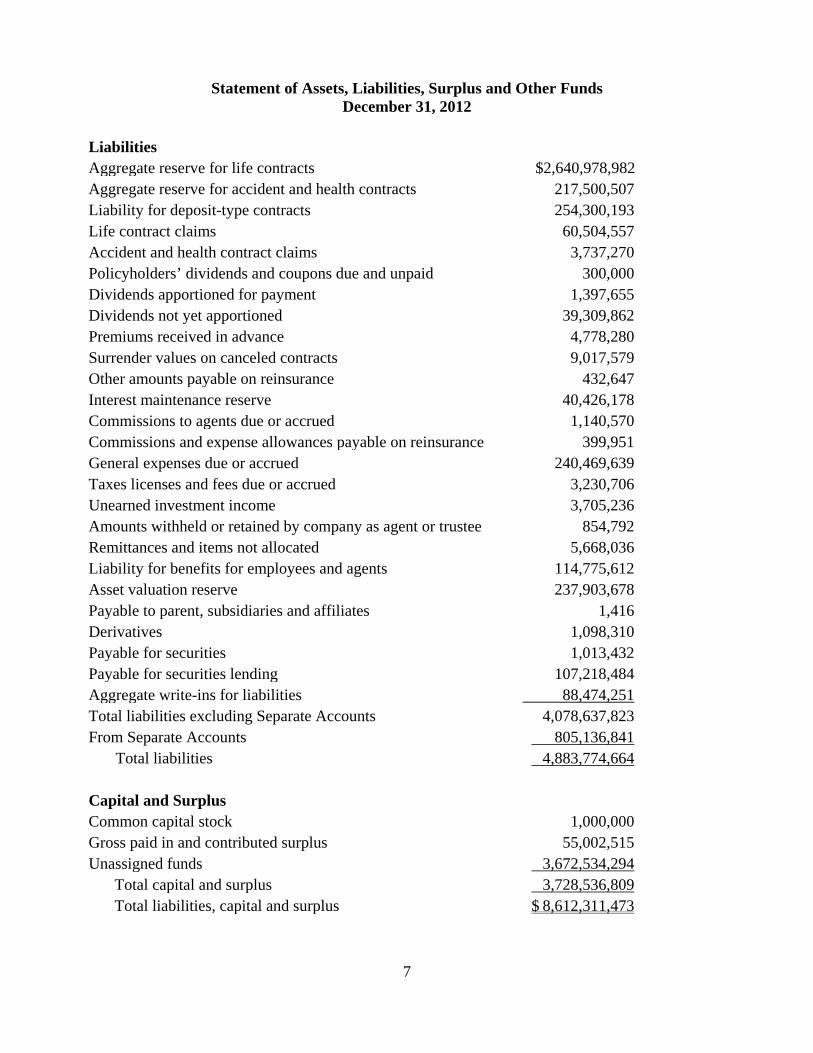

Statement of Assets, Liabilities, Surplus and Other Funds December 31, 2012

Assets Bonds $ 3,385,054,618 Preferred stocks 112,018 Common stocks 2,967,803,097 Mortgage loans on real estate 31,792,965 Properties occupied by the company 27,386,209 Properties held for the production of income 3,249,074 Properties held for sale 423,659 Cash and short term investments 118,438,134 Contract loans 175,189,761 Other invested assets 808,021,568 Receivable for securities 3,385,942 Securities lending reinvested collateral assets 21,522,427 Subtotal, cash and invested assets 7,542,379,472 Investment income due and accrued 42,407,215 Uncollected premiums in course of collection 3,169,131 Deferred premiums and installments booked but deferred 50,630,561 Amounts recoverable from reinsurers 316,196 Other amounts receivable under reinsurance contracts 21,016,951 Current federal income tax recoverable and interest thereon 15,082,499 Net deferred tax asset 75,635,273 Guaranty funds receivable or on deposit 1,317,766 Electronic data processing equipment and software 2,058,933 Receivable from parent, subsidiaries and affiliates 52,896,168 Health care and other amounts receivable 264,467 Total assets excluding Separate Accounts 7,807,174,632 From Separate Accounts 805,136,841 Total assets $ 8,612,311,473

7

Statement of Assets, Liabilities, Surplus and Other Funds December 31, 2012

Liabilities Aggregate reserve for life contracts $2,640,978,982 Aggregate reserve for accident and health contracts 217,500,507 Liability for deposit-type contracts 254,300,193 Life contract claims 60,504,557 Accident and health contract claims 3,737,270 Policyholders’ dividends and coupons due and unpaid 300,000 Dividends apportioned for payment 1,397,655 Dividends not yet apportioned 39,309,862 Premiums received in advance 4,778,280 Surrender values on canceled contracts 9,017,579 Other amounts payable on reinsurance 432,647 Interest maintenance reserve 40,426,178 Commissions to agents due or accrued 1,140,570 Commissions and expense allowances payable on reinsurance 399,951 General expenses due or accrued 240,469,639 Taxes licenses and fees due or accrued 3,230,706 Unearned investment income 3,705,236 Amounts withheld or retained by company as agent or trustee 854,792 Remittances and items not allocated 5,668,036 Liability for benefits for employees and agents 114,775,612 Asset valuation reserve 237,903,678 Payable to parent, subsidiaries and affiliates 1,416 Derivatives 1,098,310 Payable for securities 1,013,432 Payable for securities lending 107,218,484 Aggregate write-ins for liabilities 88,474,251 Total liabilities excluding Separate Accounts 4,078,637,823 From Separate Accounts 805,136,841 Total liabilities 4,883,774,664 Capital and Surplus Common capital stock 1,000,000 Gross paid in and contributed surplus 55,002,515 Unassigned funds 3,672,534,294 Total capital and surplus 3,728,536,809 Total liabilities, capital and surplus $ 8,612,311,473

8

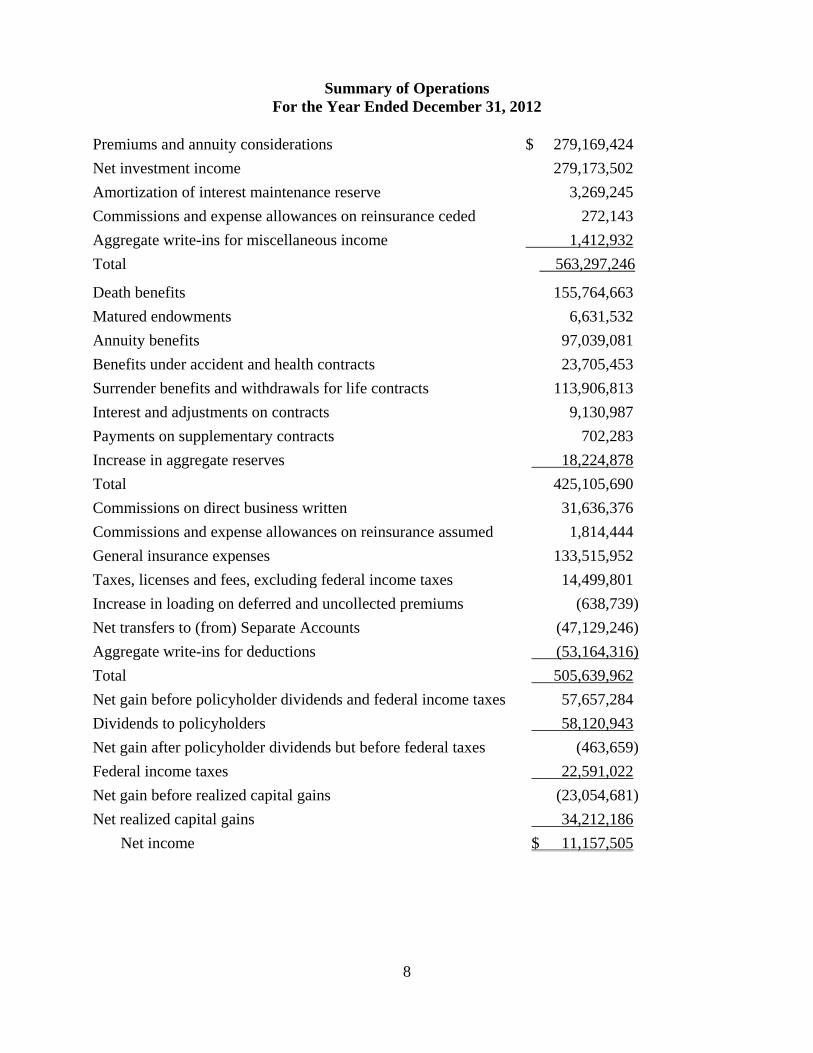

Summary of Operations For the Year Ended December 31, 2012

Premiums and annuity considerations $ 279,169,424 Net investment income 279,173,502 Amortization of interest maintenance reserve 3,269,245 Commissions and expense allowances on reinsurance ceded 272,143 Aggregate write-ins for miscellaneous income 1,412,932 Total 563,297,246

Death benefits 155,764,663 Matured endowments 6,631,532 Annuity benefits 97,039,081 Benefits under accident and health contracts 23,705,453 Surrender benefits and withdrawals for life contracts 113,906,813 Interest and adjustments on contracts 9,130,987 Payments on supplementary contracts 702,283 Increase in aggregate reserves 18,224,878 Total 425,105,690 Commissions on direct business written 31,636,376 Commissions and expense allowances on reinsurance assumed 1,814,444 General insurance expenses 133,515,952 Taxes, licenses and fees, excluding federal income taxes 14,499,801 Increase in loading on deferred and uncollected premiums (638,739) Net transfers to (from) Separate Accounts (47,129,246) Aggregate write-ins for deductions (53,164,316) Total 505,639,962 Net gain before policyholder dividends and federal income taxes 57,657,284 Dividends to policyholders 58,120,943 Net gain after policyholder dividends but before federal taxes (463,659) Federal income taxes 22,591,022 Net gain before realized capital gains (23,054,681) Net realized capital gains 34,212,186

Net income $ 11,157,505

9

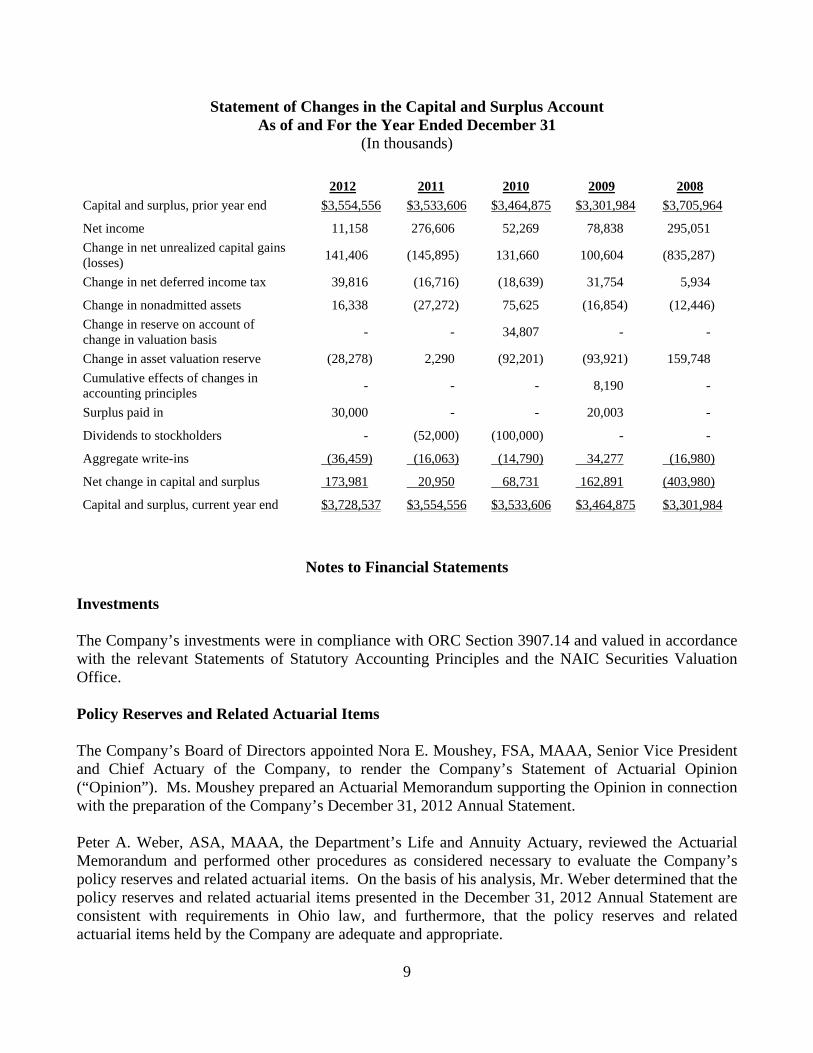

Statement of Changes in the Capital and Surplus Account

As of and For the Year Ended December 31 (In thousands)

2012 2011 2010 2009 2008

Capital and surplus, prior year end $3,554,556 $3,533,606 $3,464,875 $3,301,984 $3,705,964

Net income 11,158 276,606 52,269 78,838 295,051 Change in net unrealized capital gains (losses) 141,406 (145,895) 131,660 100,604 (835,287)

Change in net deferred income tax 39,816 (16,716) (18,639) 31,754 5,934

Change in nonadmitted assets 16,338 (27,272) 75,625 (16,854) (12,446) Change in reserve on account of change in valuation basis - - 34,807 - -

Change in asset valuation reserve (28,278) 2,290 (92,201) (93,921) 159,748 Cumulative effects of changes in accounting principles - - - 8,190 -

Surplus paid in 30,000 - - 20,003 -

Dividends to stockholders - (52,000) (100,000) - -

Aggregate write-ins (36,459) (16,063) (14,790) 34,277 (16,980)

Net change in capital and surplus 173,981 20,950 68,731 162,891 (403,980)

Capital and surplus, current year end $3,728,537 $3,554,556 $3,533,606 $3,464,875 $3,301,984

Notes to Financial Statements

Investments The Company’s investments were in compliance with ORC Section 3907.14 and valued in accordance with the relevant Statements of Statutory Accounting Principles and the NAIC Securities Valuation Office. Policy Reserves and Related Actuarial Items The Company’s Board of Directors appointed Nora E. Moushey, FSA, MAAA, Senior Vice President and Chief Actuary of the Company, to render the Company’s Statement of Actuarial Opinion (“Opinion”). Ms. Moushey prepared an Actuarial Memorandum supporting the Opinion in connection with the preparation of the Company’s December 31, 2012 Annual Statement. Peter A. Weber, ASA, MAAA, the Department’s Life and Annuity Actuary, reviewed the Actuarial Memorandum and performed other procedures as considered necessary to evaluate the Company’s policy reserves and related actuarial items. On the basis of his analysis, Mr. Weber determined that the policy reserves and related actuarial items presented in the December 31, 2012 Annual Statement are consistent with requirements in Ohio law, and furthermore, that the policy reserves and related actuarial items held by the Company are adequate and appropriate.