Embed Size (px)

Citation preview

THE WORLD BANKWorld Bank Group Multilateral Investment Guarantee Agency

Key issues for designing presumptive tax regimes

Michael Engelschalk and Jan Loeprick

Investment Climate Advisory Services

World Bank Group

THE WORLD BANKWorld Bank Group Multilateral Investment Guarantee Agency

Summary of Key Issues

How simple is simple enough? When are we trying to be too simple?

What is “small”? – and should we differentiate “micro”?

Alignment is the key!

Including corporates?!

Avoiding/curbing abuses

Who administers – central, regional, local?

Aligning accounting requirements

Implementation and outreach – linking costs and benefits of compliance

2

THE WORLD BANKWorld Bank Group Multilateral Investment Guarantee Agency

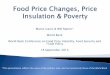

Significant improvements since 2005, but not for small firms

small medium large total0%

5%

10%

15%

20%

25%

30%

11%

17%

26%

16%

20%

8%

4%

15%

Share of Firms Who Rated Tax Administration as a Major Obstacle to Their Businesses

Georgia 2005Georgia 2008

(Source: Enterprise Survey 2008)

3

Example – exacerbating compliance costs for small businesses in Georgia

THE WORLD BANKWorld Bank Group Multilateral Investment Guarantee Agency

Example - How simple is simple enough? Indicators in Bulgaria

Bulgaria

Annual license tax - In 2005, the schedule had over 900 different rates, differentiated according to location and with more than 100 different kinds of services

4

Annual tax (BGL) per square meter of a retail trader in Sofia

Zone I Zone II Zone III Zone IV

Size of business premises less than 100 sq m

20 16 11 6

Size of business premises 100 sq m and above

50 40 30 20

THE WORLD BANKWorld Bank Group Multilateral Investment Guarantee Agency

Example – Misalignment in Kazakhstan

5

1

10

19

28

37

46

55

64

73

82

91

100

0

2,000,000

4,000,000

6,000,000

8,000,000

10,000,000

12,000,000 SR Service (Profit Margin 50%)

SR Construction (Profit Margin 15%)

SR Construction (Profit Margin 15%)

. SR Manufacturing (Profit Margin 30%)

SR Trade (Profit Margin 10%)

SR Trade (Profit Margin 20%)

Comparison of Liabilities for Firm in Different Regimes with Varying Profit Margins

Turnover, KZT (in million)

To

tal T

ax

Lia

bili

ty K

ZT

(In

co

me

Ta

x a

nd

So

cia

l Ta

x)

turnover = 100 million KZT

Difference in tax liability at the threshold of 40 million KZT for a high profitability firm in the simplified and standard regime

THE WORLD BANKWorld Bank Group Multilateral Investment Guarantee Agency

Example - The pitfall of simplicity: Side effects of patent regimes (Kyrgyz Republic)

A strong disincentive for graduation (and possibly formal growth) as patent payments are determined irrespective of the turnover of the individual businesses

The patent system opens the door for abuses

The SRS only collects information on patent contribution and not on the number of taxpayers registered under the patent scheme

→ impedes the monitoring of migration in and out of the patent regime

6Industry / production Wholesale trade Retail trade Hospitality and

cateringTransport Services, except

financial services

0%

20%

40%

60%

80%

42% 47% 45%53%

67%

45%

Share of IEs using the patent regime, per sector (out of those who are eligible for the patent regime)

Source: SME Survey 2009