Embed Size (px)

Citation preview

THE WORLD IS MULTI-ASSET

1

2-DAY WORKSHOP ON ALTERNATIVE INVESTMENTS

JO MURPHY

MANAGING DIRECTOR, HEAD OF ASIA PACIFIC

FRIDAY, 9TH FEBRUARY, 2018

REBALANCE YOUR EDUCATION PORTFOLIO

Western India Regional Council of

The Institute of Chartered Accountants Of India

CONTENT

Professional Development

A Dive into the Global Hedge Fund Industry

Why Alternative Investments? …. Investor Appetite

Asia Pacific Investors …. Who are they?

What’s next?

Due Diligence

THE WORLD IS MULTI-ASSET

4

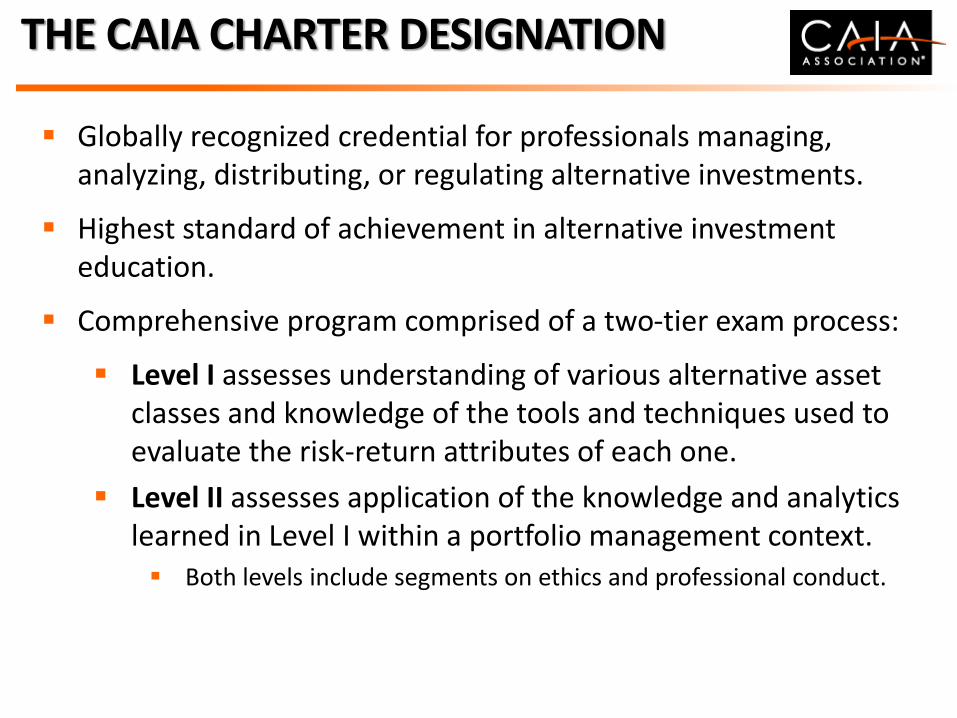

THE CAIA CHARTER DESIGNATION

Globally recognized credential for professionals managing, analyzing, distributing, or regulating alternative investments.

Highest standard of achievement in alternative investment education.

Comprehensive program comprised of a two-tier exam process:

Level I assesses understanding of various alternative asset classes and knowledge of the tools and techniques used to evaluate the risk-return attributes of each one.

Level II assesses application of the knowledge and analytics learned in Level I within a portfolio management context. Both levels include segments on ethics and professional conduct.

GLOBAL PRESENCE

Membership Growth

*2017 Data through May 2017

561

3,265

5,700

9,000

0

2,000

4,000

6,000

8,000

10,000

2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017*

CAIA Charter

Level I Curriculum – Third Edition

Core Concepts

Professional Standards & Ethics

Introduction to Alternative

Investments

Real Assets

Hedge Funds

Private Equity

Structured Products

Risk & Portfolio Management

Level I Curriculum Changes

New or Updated Topic Areas Liquid alternatives

New introduction chapter devoted to financial economics

Structured products expansion (equity, commodity, and fixed income

products)

Real asset expansion

Enhanced Applications on caia.org

Highlight and demonstrate numerical examples

Additional Review Questions

Review questions at the end of each chapter (Answers can be found in

the CAIA Level I Workbook)

CAIA TOPIC EVOLUTION: 2008 - 2017

As the Alternative Investment Universe expanded in both AUM and products, the curriculum evolved in tandem

Source: CAIA

0%

5%

10%

15%

20%

25%

30%

2008 2011 2014 2017

Hedge Funds Are Becoming A Smaller Topic Within The CAIA Curriculum

23%

26%

17%

Source: CAIA

Hedge Fund Topic Weight in 2008

Hedge Fund & Managed Futures in 2014

Hedge Fund & Managed Futures in 2017

Alternatives Are More Than Hedge Funds

Level II Curriculum – Third Edition

Advanced Core Concepts

Professional Standards & Ethics

Venture Capital & Private Equity

Hedge Funds & Managed Futures

Real Estate/Real Assets

Commodities

Structured Products

Manager Selection, Due Diligence &

Regulation

Research Issues & Current Topics

Risk & Risk Management

Asset Allocation & Portfolio Management

Level II Curriculum Recent Changes

The 3rd Edition of the CAIA Level II textbook provides comprehensive data models, due diligence processes, analysis, and strategies to keep you current

and relevant in the field of alternative investments.

New or Updated Topic Areas

Enhanced coverage of:

• Family offices and sovereign wealth funds.

• Alternative investment groups, such as structured products and

infrastructure• Private equity

• Real assets

• Hedge funds including credit strategies and operational due diligence• Structured products – featuring two sections focused on fixed-income

derivatives and asset-backed securities, and insurance-linked products

and hybrid securities

Resources for Success – Curriculum & Study Tools

67% 66% 66%

59%61%

63% 64%66%

68% 67%70%

66%

59%57%

50%

70%

90%

Level I

Level II

Pass Rates

Academic Partnerships - Americas

A complete list of CAIA’s academic partners globally can be found at caia.org.

Academic Partnerships - EMEA

Academic Partnerships - APAC

A complete list of CAIA’s academic partners globally can be found at caia.org.

Association Partnerships

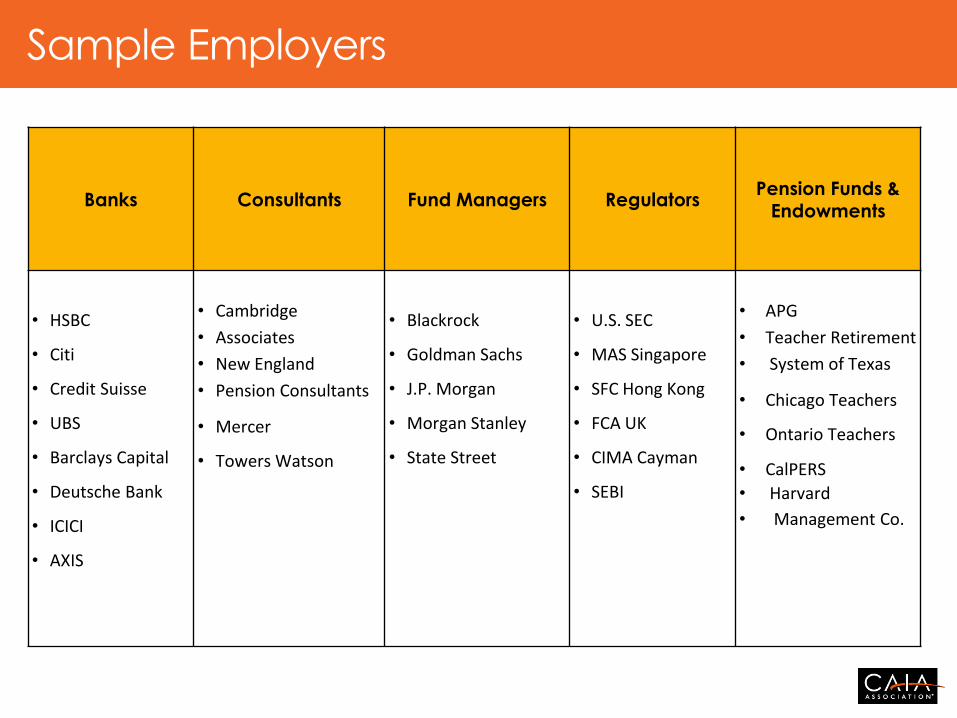

Banks Consultants Fund Managers RegulatorsPension Funds &

Endowments

• HSBC

• Citi

• Credit Suisse

• UBS

• Barclays Capital

• Deutsche Bank

• ICICI

• AXIS

• Cambridge

• Associates

• New England

• Pension Consultants

• Mercer

• Towers Watson

• Blackrock

• Goldman Sachs

• J.P. Morgan

• Morgan Stanley

• State Street

• U.S. SEC

• MAS Singapore

• SFC Hong Kong

• FCA UK

• CIMA Cayman

• SEBI

• APG

• Teacher Retirement

• System of Texas

• Chicago Teachers

• Ontario Teachers

• CalPERS

• Harvard

• Management Co.

Sample Employers

Top companies seek to hire CAIA Charterholders.Sample job postings from the CAIA Career Center

International Relationship Manager. CFA, CAIA or

working toward preferred.

Equity Investment Research -Manager. CIMA, CAIA, and/or CFA charter holders or candidates will be looked favorably upon.

International Trading ManagerMBA, CFA, CAIA or CMT preferred

CAIA is Preferred

Senior Quantitative Research Analyst. CFA, CAIA, CIMA

Senior Credit SpecialistCFA / CAIA / FRM / PRM is considered highly advantageous.

Risk Management - AssociateIndustry certifications, such as a CFA, CAIA, or FRM, are a plus.

Use of CAIA marks in professional documents

Chapter educational and networking events

Global network of more than 9,000 Members

Globally-recognized designation

Education and Research at CAIA.org

Self-evaluation Tool

Ongoing Education

CAIA Career Center

One Expiration Date – May 31st

Two-Year Membership Rate (April 2016)

New Member Outreach Initiatives

Member Benefits

REBALANCE YOUR EDUCATION PORTFOLIO

™

Fundamentals of Alternative Investments

The Fundamentals of Alternative Investments certificate program provides a foundation of core concepts in

alternative investments

Fundamentals fills a critical education gap for those who need to understand the evolving landscape of alternative investments.

Online, 20-hour, self-paced course Earns CE hours for the CIMA®, CIMC®, CPWA®, CPA ®, and CFP® designations Understand the core concepts in alternative investments Gain confidence in discussing and positioning alternatives

FAI Certificate

THE WORLD IS MULTI-ASSET

27

CONTENT

Professional Development

A Dive into the Global Hedge Fund Industry

Why Alternative Investments? …. Investor Appetite

Asia Pacific Investors …. Who are they?

What’s next?

Due Diligence

Why Alternatives? …. Investors are Increasing Allocations ….

INVESTOR PORTFOLIOS BECOMING EVER MORE DIVERSIFIED

AUM

• Global asset management industry about US$98tn

• Global AI about US$15tn

• Global ETF about US$3tn

Estimated revenue to managers

• Active management about $700bn

• AI about $200bn

• ETF about $13bn

Future Proofing : Does Your Skill Set Map Today’s Industry?

INSTITUTIONAL INVESTOR ALLOCATION

Source: Preqin Investor Outlook : Alternative Assets H2 2017

WHY INVEST IN ALTERNATIVES?

Source: Preqin Investor Outlook : Alternative Assets H2 2017

WHY INVEST IN ALTERNATIVES?

Source: Preqin Investor Outlook : Alternative Assets H2 2017

INSTO INVESTORS’ PLANS FOR THE COMING YEAR

Source: Preqin Investor Outlook : Alternative Assets H2 2017

INSTO INVESTORS’ PLANS FOR THE LONGER TERM

Source: Preqin Investor Outlook : Alternative Assets H2 2017

Asia Pacific Investors - who are they …. and, which assets classes are they interested in?

TOP 10 ASIA-PACIFIC-BASED P/E & VC INVESTORS

Investor Type CountryCurrent allocation

(USD bn)

GIC Sovereign Wealth Fund Singapore31,824

China Investment Corporation Sovereign Wealth Fund China20,000

National Pension Service Public Pension Fund South Korea19,365

Hong Kong Monetary Authority Sovereign Wealth Fund Hong Kong14,312

Future Fund Sovereign Wealth Fund Australia10,852

Gopher Asset ManagementPrivate Equity Fund of

Funds ManagerChina

9,261

Asia Alternatives ManagementPrivate Equity Fund of

Funds ManagerHong Kong

8,900

China Life Insurance Insurance Company China8,733

Export-Import Bank of China Bank China6,229

Oriza HoldingsPrivate Equity Fund of

Funds ManagerChina

6,124

Source: Preqin – July, 2017 / Market Info

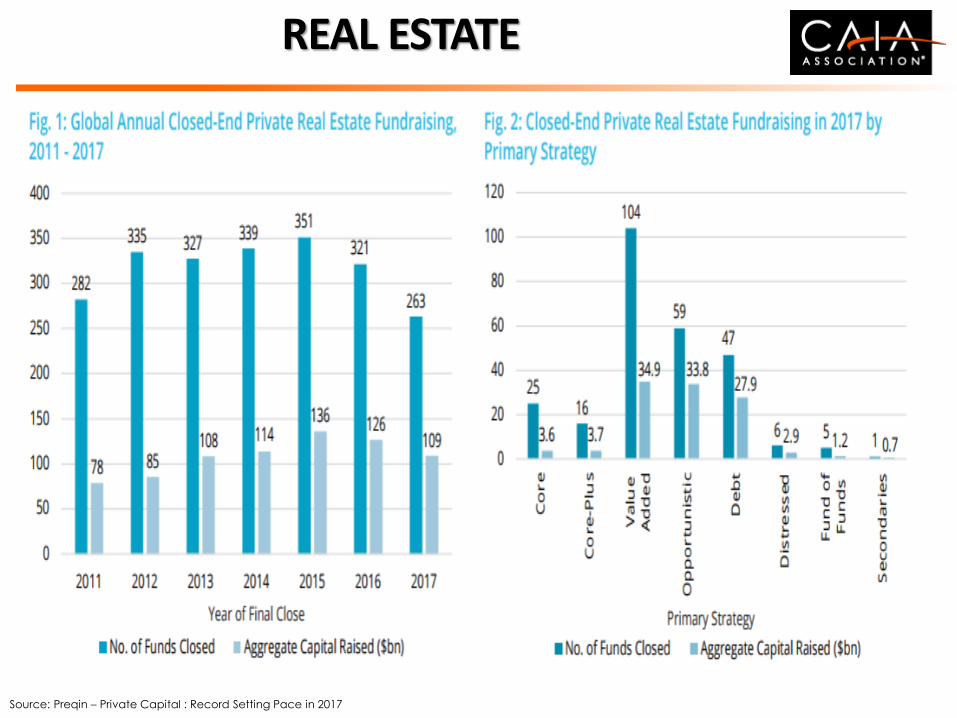

PRIVATE EQUITY

Source: Preqin – Private Capital : Record Setting Pace in 2017

VENTURE CAPITAL

2%

2%

4%

8%

10%

10%

10%

14%

14%

29%

35%

45%

51%

73%

0% 10% 20% 30% 40% 50% 60% 70% 80%

Interest Rates

Commodity Pricing

Public Perception of Industry

Availability/Pricing of Debt Financing

Regulation

Portfolio Management

Transparency

Ongoing Uncertainty in…

Governance

Fees

Deal Flow

Performance

Exit Environment

Pricing/Valuations

Investor Views on the Key Issues - Next 12 Months

29%

56%

15% IncreaseAllocation

MaintainAllocation

DecreaseAllocation

Allocation Intentions over the

Longer Term

Source: Preqin Investor Outlook : Alternative Assets H2 2017

Source: Preqin – July, 2017 / Market Info

TOP 10 ASIA-PACIFIC-BASED REAL ESTATE INVESTORS

Investor Type CountryCurrent allocation

(USD bn)

GIC Sovereign Wealth Fund Singapore24,752

National Pension Service Public Pension Fund South Korea21,249

Cathay Life Insurance Insurance Company Taiwan18,576

QIC Asset Manager Australia13,057

Samsung Life Insurance Insurance Company South Korea8,667

Hong Kong Monetary Authority Sovereign Wealth Fund Hong Kong8,038

AustralianSuper Superannuation Scheme Australia7,935

Fubon Life Insurance Insurance Company Taiwan6,978

Daiwa Securities Group Investment Company Japan6,976

Great Eastern Life Assurance Insurance Company Singapore6,566

REAL ESTATE

Source: Preqin – Private Capital : Record Setting Pace in 2017

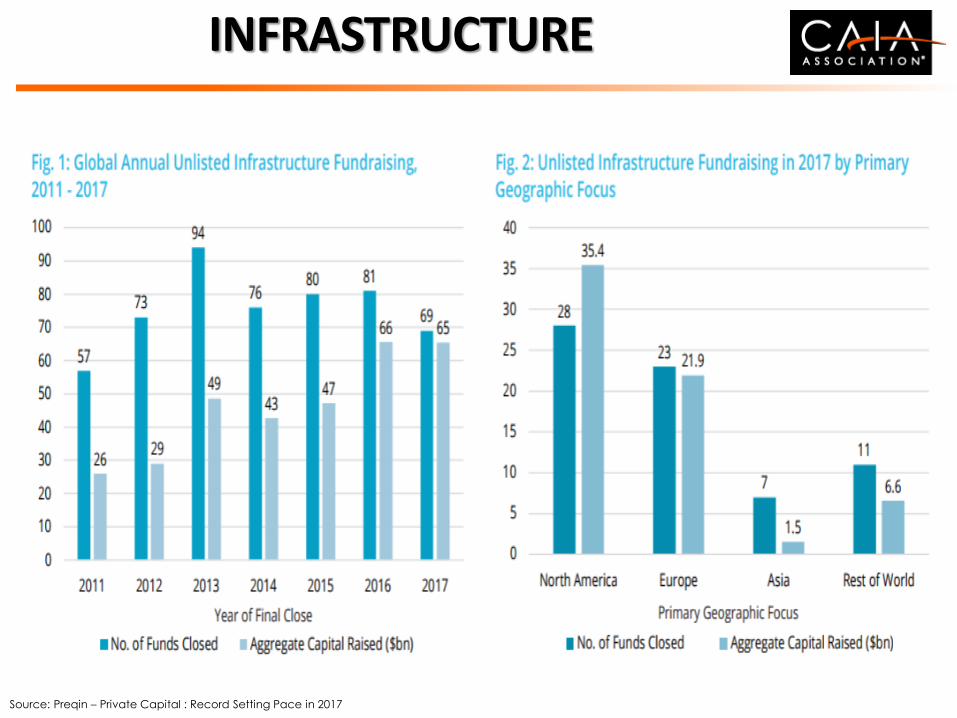

TOP 10 ASIA-PACIFIC-BASED INFRA INVESTORS

Investor Type CountryCurrent allocation

(USD bn)

National Pension Service Public Pension Fund South Korea16,434

Khazanah Nasional Sovereign Wealth Fund Malaysia8,660

AustralianSuperSuperannuation

SchemeAustralia

7,977

Future Fund Sovereign Wealth Fund Australia7,818

Fubon Life Insurance Insurance Company Taiwan5,644

QIC Asset Manager Australia5,539

Harris Fraser Wealth Manager Hong Kong5,250

Kyobo Life Insurance Insurance Company South Korea5,014

First State SuperSuperannuation

SchemeAustralia

4,558

QSuperSuperannuation

SchemeAustralia

4,371 Source: Preqin – July, 2017 / Market Info

INFRASTRUCTURE

Source: Preqin – Private Capital : Record Setting Pace in 2017

TOP 10 ASIA-PACIFIC-BASED HF INVESTORS

Investor Type CountryCurrent allocation

(USD bn)

China Investment Corporation Sovereign Wealth Fund China 34.168

Future Fund Sovereign Wealth Fund Australia 15.534

GIC Sovereign Wealth Fund Singapore 10.608

Korea Investment Corporation Sovereign Wealth Fund South Korea 4.986

Pension Fund Association Asset Manager Japan 4.287

Japan Post Bank Bank Japan 4.270

Gopher Asset Management Family Office - Multi China 3.891

Dai-ichi Life Insurance Insurance Company Japan 3.042

CMBC Private Banking Wealth Manager China 2.250

Victorian Funds Management Corporation

Asset Manager Australia 2.196

Source: Preqin – July, 2017 / Market Info

HEDGE FUNDS

20%

31%

49%

Allocation Intentions over the Longer Term

IncreaseAllocation

MaintainAllocation

DecreaseAllocation

69%

56%

41%39%

31%

24%20%

19%

11% 11%

0%

10%

20%

30%

40%

50%

60%

70%

80%

Perf

orm

ance

Fees

Ongoin

g V

ola

tility

in G

lobal M

ark

ets

Public P

erc

epti

on

of

Indust

ry

Regula

tion

Nota

ble

Invest

ors

Exit

ing t

he A

sset

Cla

ss

Tra

nsp

are

ncy

Port

folio M

anagem

ent

Pri

cin

g/Valu

ati

ons

Govern

ance

Pro

port

ion o

f Resp

ondents

Investor Views on the Key Issues - Next 12 Months

Source: Preqin Investor Outlook : Alternative Assets H2 2017

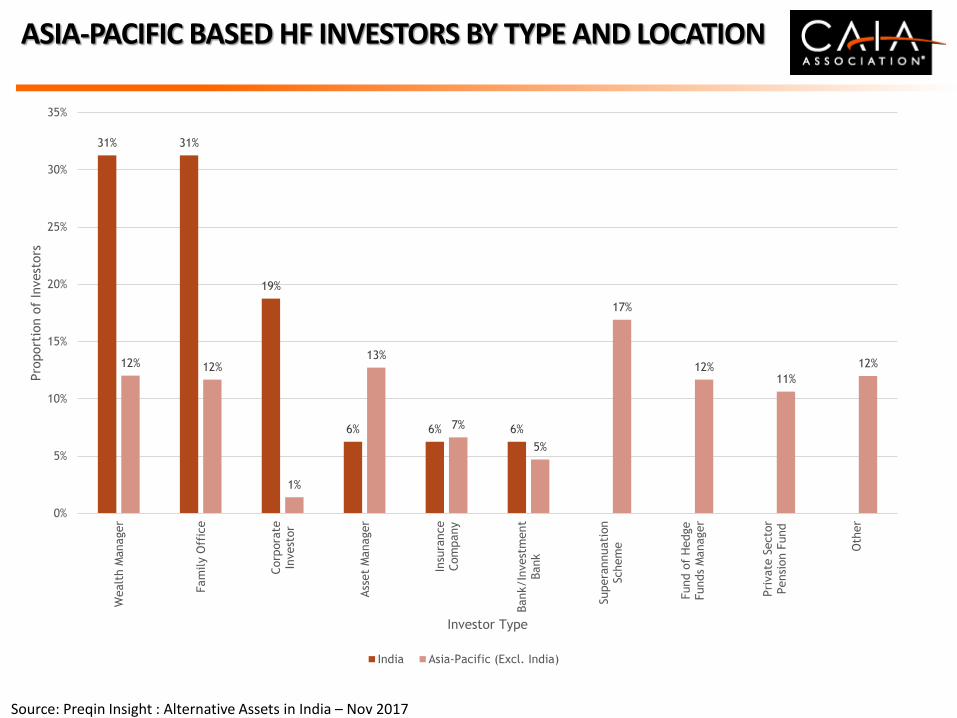

ASIA-PACIFIC BASED HF INVESTORS BY TYPE AND LOCATION

31% 31%

19%

6% 6% 6%

12% 12%

1%

13%

7%

5%

17%

12%11%

12%

0%

5%

10%

15%

20%

25%

30%

35%W

ealt

h M

anager

Fam

ily O

ffic

e

Corp

ora

teIn

vest

or

Ass

et

Manager

Insu

rance

Com

pany

Bank/In

vest

ment

Bank

Supera

nnuati

on

Schem

e

Fund o

f H

edge

Funds

Manager

Pri

vate

Secto

rPensi

on F

und

Oth

er

Pro

port

ion o

f In

vest

ors

Investor Type

India Asia-Pacific (Excl. India)

Source: Preqin Insight : Alternative Assets in India – Nov 2017

STRATEGY PREFERENCES OF AP BASED HF INVESTORS

88%

38%

13%

38%

68%

62%

40%

44%

48%

19%

67%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

Equity Strategies Macro Strategies Event DrivenStrategies

Credit Strategies Relative ValueStrategies

Niche Strategies Multi-Strategy

Pro

port

ion o

f In

vest

ors

Strategy Preference

India Asia-Pacific (Excl. India)

Source: Preqin Insight : Alternative Assets in India – Nov 2017

TOP 10 GLOBAL HEDGE FUNDS : BILLION DOLLAR CLUB

Fund Manager Location Year

EstablishedTotal AUM (USD mn)

AUM Date

Bridgewater Associates US 1975 $161,900 30-Jun-17

AQR Capital Management US 1998 $106,200 30-Jun-17

Man Group UK 1983 $57,900 30-Jun-17

J.P. Morgan Asset Management US 1974 $49,000 30-Jun-17

Renaissance Technologies US 1982 $47,900 30-Jun-17

Millennium Management US 1989 $34,300 1-Jul-17

Standard Life Investments (Part of Aberdeen Standard Investments)

UK 1998 $33,200 30-Jun-17

Och-Ziff Capital Management US 1994 $31,800 1-Jul-17

Elliott Management US 1977 $31,400 31-Dec-17

Two Sigma Investments US 2002 $30,400 1-Jan-17

Source: Preqin – October, 2017

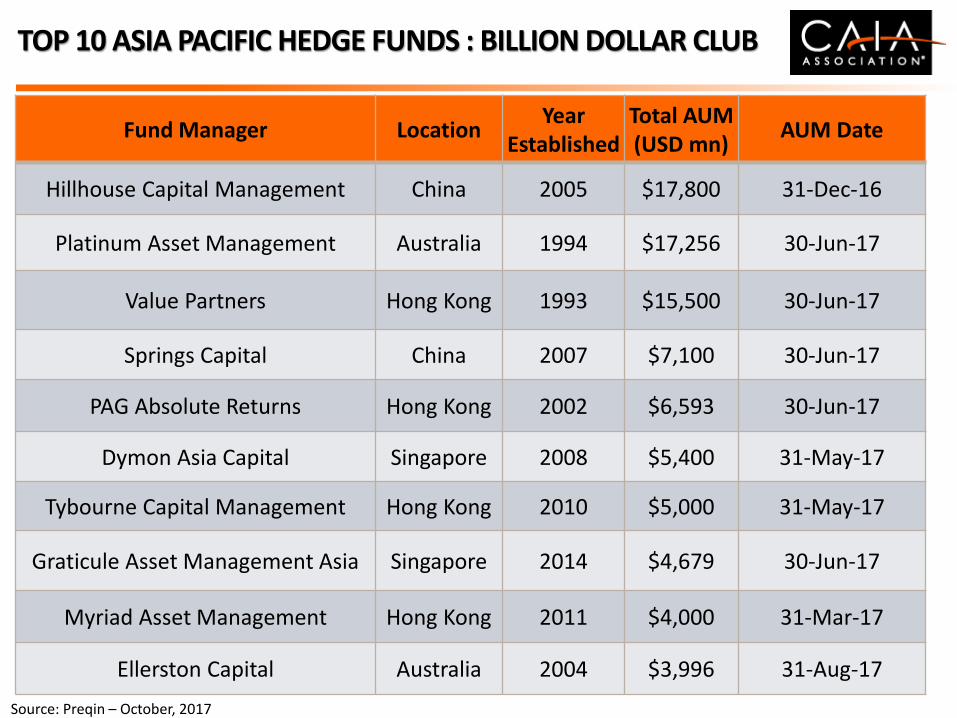

TOP 10 ASIA PACIFIC HEDGE FUNDS : BILLION DOLLAR CLUB

Fund Manager Location Year

EstablishedTotal AUM (USD mn)

AUM Date

Hillhouse Capital Management China 2005 $17,800 31-Dec-16

Platinum Asset Management Australia 1994 $17,256 30-Jun-17

Value Partners Hong Kong 1993 $15,500 30-Jun-17

Springs Capital China 2007 $7,100 30-Jun-17

PAG Absolute Returns Hong Kong 2002 $6,593 30-Jun-17

Dymon Asia Capital Singapore 2008 $5,400 31-May-17

Tybourne Capital Management Hong Kong 2010 $5,000 31-May-17

Graticule Asset Management Asia Singapore 2014 $4,679 30-Jun-17

Myriad Asset Management Hong Kong 2011 $4,000 31-Mar-17

Ellerston Capital Australia 2004 $3,996 31-Aug-17

Source: Preqin – October, 2017

TOP 10 GREATER CHINA BASED HEDGE FUNDS : BILLION DOLLAR CLUB

Fund Manager Location Year

EstablishedTotal AUM (USD mn)

AUM Date

Hillhouse Capital Management China 2005 $17,800 31-Dec-16

Value Partners Hong Kong 1993 $15,500 30-Jun-17

Springs Capital China 2007 $7,100 30-Jun-17

PAG Absolute Returns Hong Kong 2002 $6,593 30-Jun-17

Tybourne Capital Management Hong Kong 2010 $5,000 31-May-17

Myriad Asset Management Hong Kong 2011 $4,000 31-Mar-17

Symmetry Investments LP Hong Kong 2014 $3,600 1-Jul-17

Cephei Capital Management Hong Kong 2006 $3,331 30-Jun-17

Greenwoods Asset Management Hong Kong 2004 $2,688 31-Jul-17

BFAM Partners Hong Kong 2012 $2,611 31-Aug-17

Source: Preqin – October, 2017

HEDGE FUND CUMULATIVE RETURNS IN 2017

6.58%

8.36%

15.41%

0.00%

2.00%

4.00%

6.00%

8.00%

10.00%

12.00%

14.00%

16.00%

18.00%

Jan Feb Mar Apr May Jun Jul Aug Sep Oct

Cum

ula

tive N

et

Retu

rn

North America 0% Europe 0% Asia-Pacific 0%

Source: Preqin – October, 2017

GLOBAL BILLION DOLLAR CLUB - FOHF

Fund Manager Location Year EstTotal AUM (USD mn)

AUM Date

Blackstone Alternative Asset Management US 1990 $72,000 30-Jun-17

UBS Hedge Fund Solutions US 2000 $37,400 30-Jun-17

Goldman Sachs Asset Management US 1997 $29,200 30-Jun-17

Grosvenor Capital Management US 1971 $25,900 30-Jun-17

EnTrustPermal US 1971 $24,400 30-Jun-17

HSBC Alternative Investments UK 1994 $24,200 1-Jul-17

Morgan Stanley Alternative Investment Partners US 2000 $23,300 30-Jun-17

BlackRock Alternative Advisors US 1995 $22,900 1-Jul-17

PAAMCO Prisma* US 2000 $16,900 31-Dec-17

Man FRM UK 1991 $16,200 1-Jan-17

Source: Preqin – September, 2017

KEY CHALLENGES FOR FUND MANGERS

Private Equity

Venture Capital

Real Estate InfrastructureHedge Funds

Pricing Pricing Pricing Pricing Performance

Deal Flow Exit Deal Flow Deal FlowFees

Exit Performance Performance Performance Ongoing Vol

INDIA BASED ALTERNATIVE ASSETS AUM (AS AT DEC 2016)

23.6

1.4

10.2

4.4

3.3

0

5

10

15

20

25

Private Equity & VentureCapital

Hedge Funds(As at Jul-17)

Real Estate Infrastructure Private Debt

Ass

ets

under

Managem

ent

($bn)

Source: Preqin Insight : Alternative Assets in India – Nov 2017

INDIA BASED PRIVATE CAPITAL (2006 - 2016)

Source: Preqin Insight : Alternative Assets in India – Nov 2017

7.4

11.312.8 11.9

10.2 11.08.4

13.6

10.511.7

13.5

3.2

7.5

9.3 11.2 13.8

17.921.9

25.5

28.3

30.128.0

0

5

10

15

20

25

30

35

40

45

Dec-06 Dec-07 Dec-08 Dec-09 Dec-10 Dec-11 Dec-12 Dec-13 Dec-14 Dec-15 Dec-16

Ass

ets

under

Managem

ent

($bn)

Unrealized Value ($bn)

Dry Powder ($bn)

INDIA BASED PRIVATE CAPITAL FIRMS – 2000 – YTD SEPT 2017

Source: Preqin Insight : Alternative Assets in India – Nov 2017

205

16

0

50

100

150

200

250

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017YTD

No

. of

Act

ive

Firm

s

Existing Firm New Firm

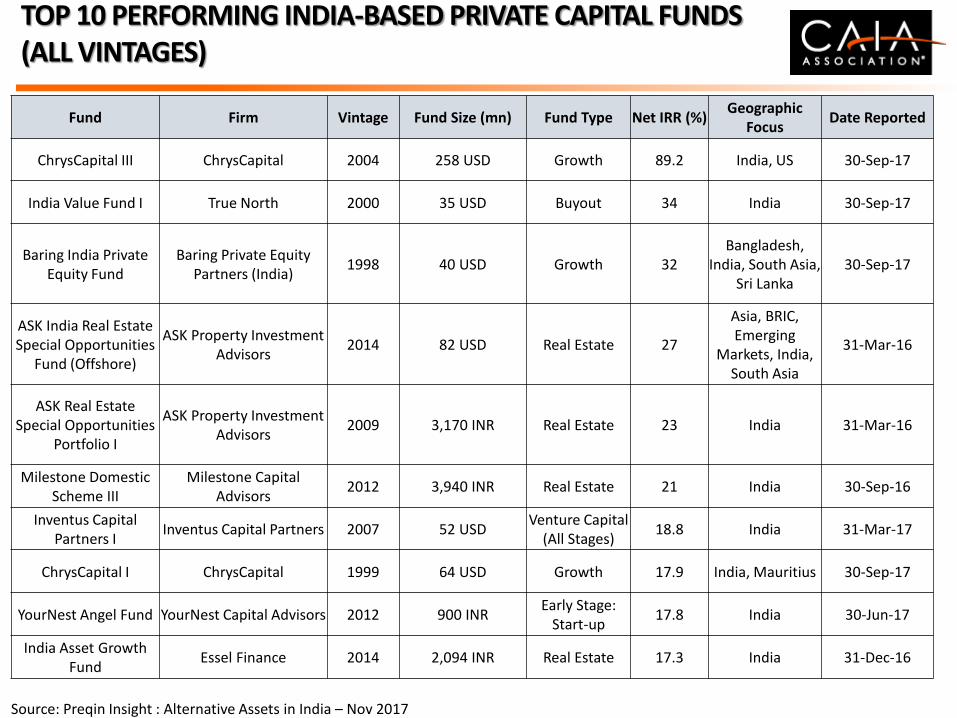

TOP 10 PERFORMING INDIA-BASED PRIVATE CAPITAL FUNDS (ALL VINTAGES)

Source: Preqin Insight : Alternative Assets in India – Nov 2017

Fund Firm Vintage Fund Size (mn) Fund Type Net IRR (%)Geographic

FocusDate Reported

ChrysCapital III ChrysCapital 2004 258 USD Growth 89.2 India, US 30-Sep-17

India Value Fund I True North 2000 35 USD Buyout 34 India 30-Sep-17

Baring India Private Equity Fund

Baring Private Equity Partners (India)

1998 40 USD Growth 32Bangladesh,

India, South Asia, Sri Lanka

30-Sep-17

ASK India Real Estate Special Opportunities

Fund (Offshore)

ASK Property Investment Advisors

2014 82 USD Real Estate 27

Asia, BRIC, Emerging

Markets, India, South Asia

31-Mar-16

ASK Real Estate Special Opportunities

Portfolio I

ASK Property Investment Advisors

2009 3,170 INR Real Estate 23 India 31-Mar-16

Milestone Domestic Scheme III

Milestone Capital Advisors

2012 3,940 INR Real Estate 21 India 30-Sep-16

Inventus Capital Partners I

Inventus Capital Partners 2007 52 USDVenture Capital

(All Stages)18.8 India 31-Mar-17

ChrysCapital I ChrysCapital 1999 64 USD Growth 17.9 India, Mauritius 30-Sep-17

YourNest Angel Fund YourNest Capital Advisors 2012 900 INREarly Stage:

Start-up17.8 India 30-Jun-17

India Asset Growth Fund

Essel Finance 2014 2,094 INR Real Estate 17.3 India 31-Dec-16

INDIA-BASED INSTITUTIONAL INVESTORS BY NUMBER OF ALTERNATIVE ASSET CLASSES INVESTED (AS AT AUG 2017)

Source: Preqin Insight : Alternative Assets in India – Nov 2017

40%

20%

13%

11%

11%

5%

None

One

Two

Three

Four

Five

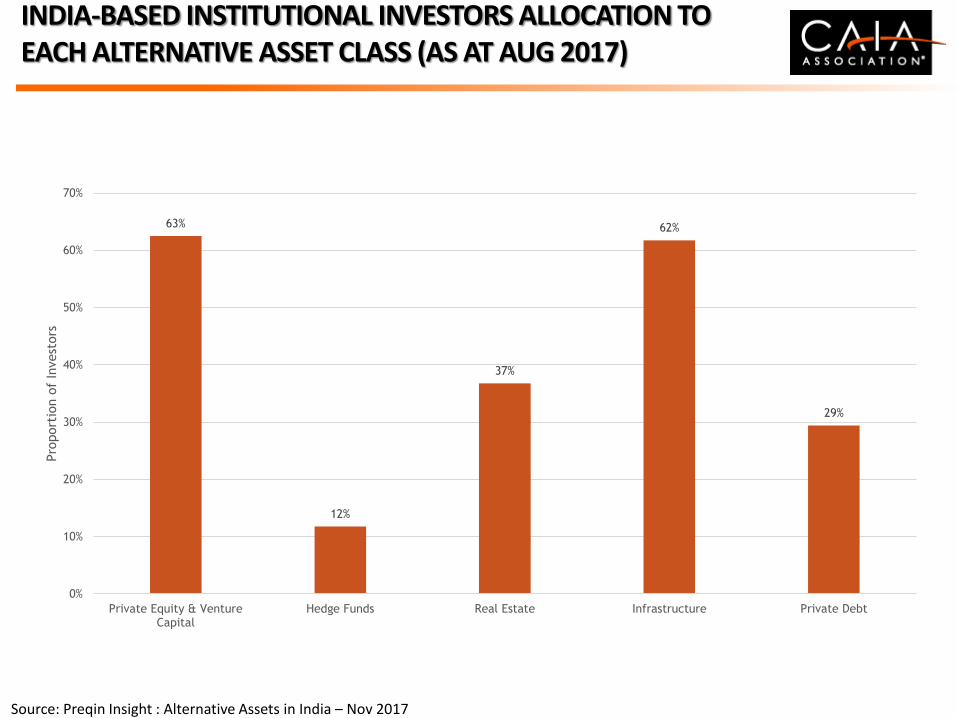

INDIA-BASED INSTITUTIONAL INVESTORS ALLOCATION TO EACH ALTERNATIVE ASSET CLASS (AS AT AUG 2017)

Source: Preqin Insight : Alternative Assets in India – Nov 2017

63%

12%

37%

62%

29%

0%

10%

20%

30%

40%

50%

60%

70%

Private Equity & VentureCapital

Hedge Funds Real Estate Infrastructure Private Debt

Pro

port

ion o

f In

vest

ors

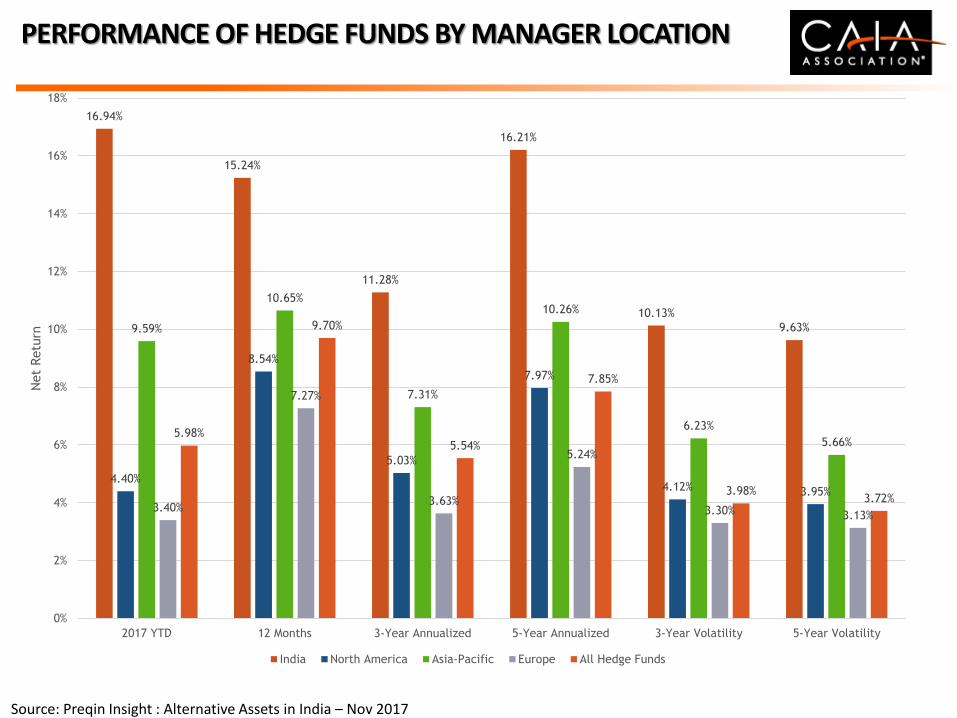

PERFORMANCE OF HEDGE FUNDS BY MANAGER LOCATION

Source: Preqin Insight : Alternative Assets in India – Nov 2017

16.94%

15.24%

11.28%

16.21%

10.13%

9.63%

4.40%

8.54%

5.03%

7.97%

4.12% 3.95%

9.59%

10.65%

7.31%

10.26%

6.23%

5.66%

3.40%

7.27%

3.63%

5.24%

3.30% 3.13%

5.98%

9.70%

5.54%

7.85%

3.98%3.72%

0%

2%

4%

6%

8%

10%

12%

14%

16%

18%

2017 YTD 12 Months 3-Year Annualized 5-Year Annualized 3-Year Volatility 5-Year Volatility

Net

Retu

rn

India North America Asia-Pacific Europe All Hedge Funds

THE WORLD IS MULTI-ASSET

61

CONTENT

Professional Development

A Dive into the Global Hedge Fund Industry

Why Alternative Investments? …. Investor Appetite

Asia Pacific Investors …. Who are they?

What’s next?

Due Diligence

A Dive into the Global Hedge Fund Industry

WHAT A HEDGE FUND IS NOT :

Numerous myths abound! : –

Hedge Funds were not the cause of the GFS in 2008, this was a banking crisis

Less than 1% of all hedge fund assets under management are from

pure/dedicated short selling

The Hedge Fund industry is regulated

The industry is NOT volatile and dangerous

Leverage levels employed by the Hedge Fund industry remains modest

The Industry is NOT shady and secretive!

The Global Financial Crisis …. How bad was it?

A RECAP : THE GREAT FINANCIAL CRISIS

Source: Altinvest

What Happened Performance Wise?

Hedge Funds ….

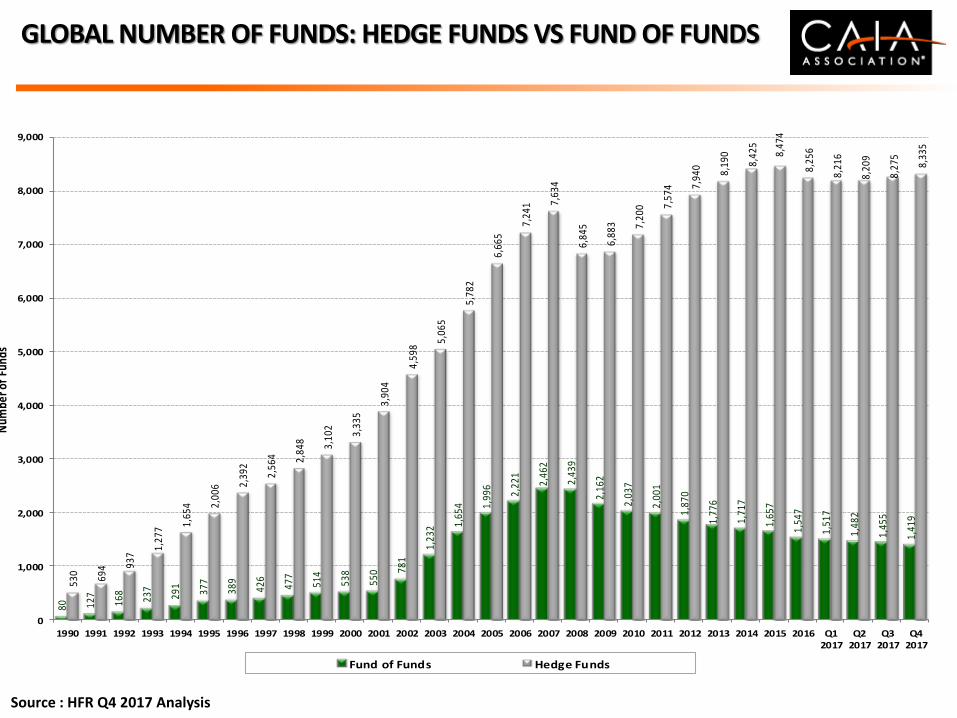

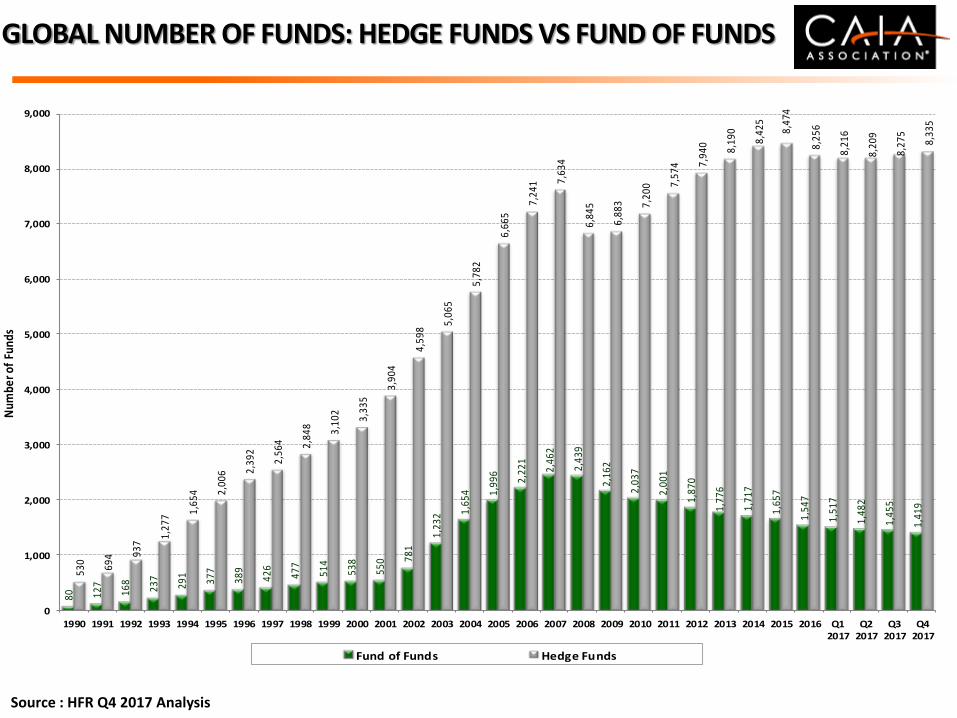

GLOBAL NUMBER OF FUNDS: HEDGE FUNDS VS FUND OF FUNDS

Source : HFR Q4 2017 Analysis

80 127

168

237

291

377

389

426

477

514

538

550 78

1

1,23

2 1,65

4 1,99

6

2,22

1

2,46

2

2,43

9

2,16

2

2,03

7

2,00

1

1,87

0

1,77

6

1,71

7

1,65

7

1,54

7

1,51

7

1,48

2

1,45

5

1,41

9

530 69

4 937

1,27

7 1,65

4 2,00

6 2,39

2

2,56

4 2,84

8 3,10

2

3,33

5

3,90

4

4,59

8

5,06

5

5,78

2

6,66

5

7,24

1 7,63

4

6,84

5

6,88

3 7,20

0 7,57

4 7,94

0 8,19

0

8,42

5

8,47

4

8,25

6

8,21

6

8,20

9

8,27

5

8,33

5

0

1,000

2,000

3,000

4,000

5,000

6,000

7,000

8,000

9,000

1990 1991 1992 1993 1994 1995 1996 1997 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 Q12017

Q22017

Q32017

Q42017

Num

ber o

f Fu

nds

Fund of Funds Hedge Funds

GLOBAL HEDGE FUND - GROWTH OF ASSETS / NET ASSET FLOW

Source : HFR 4Q 2017 Analysis

$38.9 $58.4 $95.7

$167.8 $167.4

$185.8 $256.7

$367.6 $374.8

$456.4 $490.6

$539.1

$625.6

$820.0

$972.6

$1,105.4

$1,464.5

$1,868.4

$1,407.1

$1,600.2

$1,917.4

$2,008.1

$2,252.4

$2,628.3

$2,845.1 $2,896.8

$3,018.3

$3,210.7

$8.5 $27.9 $36.9

($1.1)

$14.7 $57.4

$91.4

$4.4 $55.3 $23.3 $46.5

$99.4 $70.6 $73.6 $46.9 $126.5

$194.5

($154.4)($131.2)

$55.5 $70.6

$34.4 $63.7

$76.4 $43.8

($70.1)

$9.8

($500)

$0

$500

$1,000

$1,500

$2,000

$2,500

$3,000

$3,500

1990 1991 1992 1993 1994 1995 1996 1997 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017

Ass

ets

($BN

)

Estimated Assets Net Asset Flow

GLOBAL HF – DISTRIBUTION OF ASSETS BY FIRM AUM

By # Firms By Firm AUM Size

Source : HFR 4Q 2017 Analysis

1.01%1.76%

2.68%3.64%

22.05%

68.86%

46.11%

15.51%

10.77%

7.46%

13.70%

6.45%

< $100 Million $100 to $250 Million

$250 to $500 Million $500M to $1 Billion

$1 to $5 Billion > $5 Billion

GLOBAL HF - DISTRIBUTION OF ASSETS BY FUND AUM

By # Funds By Fund AUM Size

Source : HFR 4Q 2017 Analysis

0.08%

0.27% 0.58%1.22%

2.39%5.94%

6.80%

82.70%

56.01%

6.34%

6.26%

6.56%

6.45%

7.14%

3.73%

7.50%

< $10 Million $10 to $25 Million

$25 to $50 Million $50 to $100 Million

$100 to $200 Million $200 to $500 Million

$500M to $1 Billion > $1 Billion

GLOBAL HF – STRATEGY COMPOSITION BY AUM

Source : HFR 4Q2017 Analysis

Q4 1990 Q4 2017

Equity Hedge

37.07%

Event-Driven9.75%

Macro39.30%

Relative Value

13.88%

Equity Hedge29.26%

Event-Driven

25.90%

Macro

18.66%

Relative Value

26.18%

DISTRIBUTION OF INDUSTRY BY REGION INVESTMENT FOCUS

By # Funds By Assets

Source : HFR 4Q 2017 Analysis

Americas47.89%

Asia

13.93%

Europe10.69%

Other

27.49%

Americas

33.83%

Asia3.81%

Europe7.31%

Other55.05%

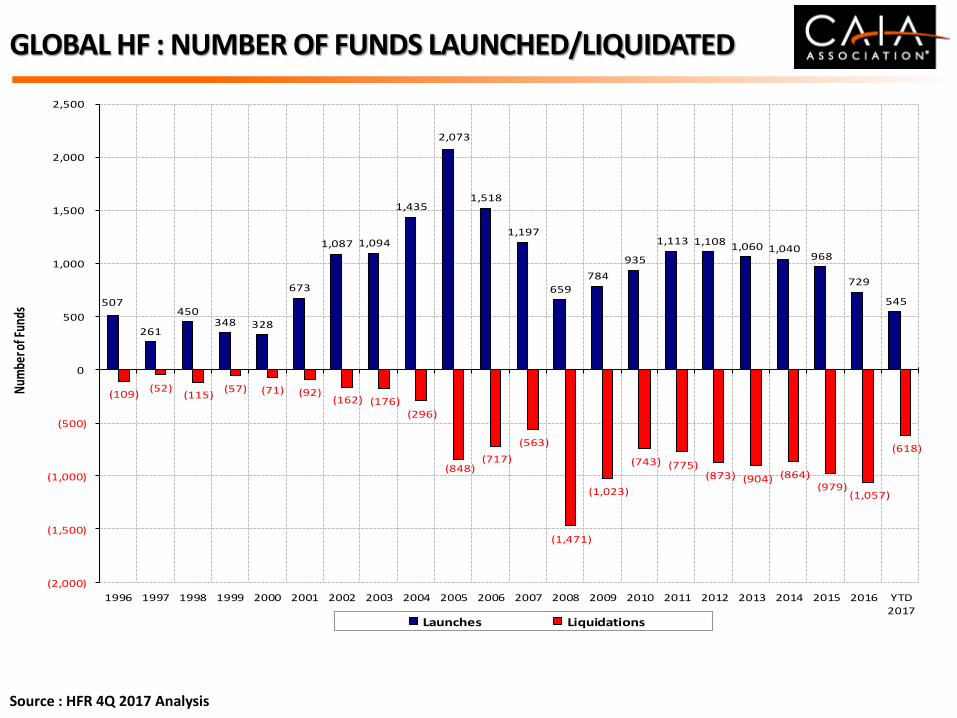

GLOBAL HF : NUMBER OF FUNDS LAUNCHED/LIQUIDATED

Source : HFR 4Q 2017 Analysis

507

261

450 348 328

673

1,087 1,094

1,435

2,073

1,518

1,197

659 784

935

1,113 1,108 1,060 1,040 968

729

545

(109)(52)

(115)(57) (71) (92)

(162) (176)(296)

(848)(717)

(563)

(1,471)

(1,023)

(743) (775)(873) (904) (864)

(979)(1,057)

(618)

(2,000)

(1,500)

(1,000)

(500)

0

500

1,000

1,500

2,000

2,500

1996 1997 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 YTD2017

Num

ber o

f Fun

ds

Launches Liquidations

TOP 10 GLOBAL HEDGE FUNDS : BILLION DOLLAR CLUB

Fund Manager Location Year

EstablishedTotal AUM (USD mn)

AUM Date

Bridgewater Associates US 1975 $161,900 30-Jun-17

AQR Capital Management US 1998 $106,200 30-Jun-17

Man Group UK 1983 $57,900 30-Jun-17

J.P. Morgan Asset Management US 1974 $49,000 30-Jun-17

Renaissance Technologies US 1982 $47,900 30-Jun-17

Millennium Management US 1989 $34,300 1-Jul-17

Standard Life Investments (Part of Aberdeen Standard Investments)

UK 1998 $33,200 30-Jun-17

Och-Ziff Capital Management US 1994 $31,800 1-Jul-17

Elliott Management US 1977 $31,400 31-Dec-17

Two Sigma Investments US 2002 $30,400 1-Jan-17

Source: Preqin – October, 2017

TOP 10 ASIA PACIFIC HEDGE FUNDS : BILLION DOLLAR CLUB

Fund Manager Location Year

EstablishedTotal AUM (USD mn)

AUM Date

Hillhouse Capital Management China 2005 $17,800 31-Dec-16

Platinum Asset Management Australia 1994 $17,256 30-Jun-17

Value Partners Hong Kong 1993 $15,500 30-Jun-17

Springs Capital China 2007 $7,100 30-Jun-17

PAG Absolute Returns Hong Kong 2002 $6,593 30-Jun-17

Dymon Asia Capital Singapore 2008 $5,400 31-May-17

Tybourne Capital Management Hong Kong 2010 $5,000 31-May-17

Graticule Asset Management Asia Singapore 2014 $4,679 30-Jun-17

Myriad Asset Management Hong Kong 2011 $4,000 31-Mar-17

Ellerston Capital Australia 2004 $3,996 31-Aug-17

Source: Preqin – October, 2017

TOP 10 GREATER CHINA BASED HEDGE FUNDS : BILLION DOLLAR CLUB

Fund Manager Location Year

EstablishedTotal AUM (USD mn)

AUM Date

Hillhouse Capital Management China 2005 $17,800 31-Dec-16

Value Partners Hong Kong 1993 $15,500 30-Jun-17

Springs Capital China 2007 $7,100 30-Jun-17

PAG Absolute Returns Hong Kong 2002 $6,593 30-Jun-17

Tybourne Capital Management Hong Kong 2010 $5,000 31-May-17

Myriad Asset Management Hong Kong 2011 $4,000 31-Mar-17

Symmetry Investments LP Hong Kong 2014 $3,600 1-Jul-17

Cephei Capital Management Hong Kong 2006 $3,331 30-Jun-17

Greenwoods Asset Management Hong Kong 2004 $2,688 31-Jul-17

BFAM Partners Hong Kong 2012 $2,611 31-Aug-17

Source: Preqin – October, 2017

TOP 5 ASIA PACIFIC BASED HEDGE FUNDS

Source : Preqin – September, 2017

Fund Name Firm NameFirm

CountryInception Date

Core Strategies

RegionPrefs

CountryPrefs

Methodsof

Investment

2017 Year-to-

date Return

12-Month

3-YearAnnu

Rtn Since Incep

CSV China Opportunities

Fund

CSV Capital Partners

China 1/4/2010Long Bias,

Long/Short Equity

ChinaDebt,

Equities80.95 66.45 16.58 130.91

UG Hidden Dragon Special

Opportunity Fund - Class A

UG Investment

AdvisersTaiwan 9/28/2007

Event Driven, Long/Short

Equity, Value-Oriented

Asia ChinaEquity & Currency

Derivs57.39 50.99 35.26 232.2

TAL China Focus Fund -

Class C (Unrestricted)

Trivest Advisors

Hong Kong 7/2/2010Long/Short

EquityGlobal China

Derivs / Equities

50.57 44.41 21.21 193.99

Foundation China

Opportunity Fund

Foundation Asset

Management (HK)

Hong Kong 1/1/2007Long Bias,

Long/Short Equity

Greater China, Global

China, Hong Kong

Debt, Equities

47.14 39.3 11.68 209.88

Chinese Mainland

Focus FundValue Partners Hong Kong 11/27/2003

Long Bias, Long/Short

EquityChina

Derivs, Equities, Currency

46.52 41.25 14.24 400+

TOP 5 ASIA PACIFIC INVESTED HEDGE FUNDS

Source : Preqin – September, 2017

Fund Name Firm NameFirm

CountryInception Date

Core Strategies

RegionPrefs

CountryPrefs

Methodsof

Investment

2017 Year-to-

date Return

12-Month

3-YearAnnu

Rtn Since Incep

UG Hidden Dragon Special

Opportunity Fund - Class A

UG Investment

AdvisersTaiwan 9/28/2007

Event Driven, Long/Short

Equity, Value-Oriented

Asia ChinaDerivs & Equities

57.39 50.99 35.26 232.2

KS Asia Absolute

Return Fund ICGen2 Partners Hong Kong 1/3/2010

Long/Short Equity, Multi-

StrategyAsia

South Korea

Debt & Equities

42.22 43.5 18.26 190.78

Telligent Greater China Master Fund

Telligent Capital

ManagementHong Kong 8/1/2004

Long/Short Equity

Greater China

China, Hong Kong,

Taiwan

Derivs & Equities

40.94 23.99 7.68 341.92

Value Partners Classic Fund -C Units (RMB)

Hedged

Value Partners Hong Kong 10/28/2015Long Bias,

Long/Short Equity

Greater China, Asia

China, Hong Kong

Equities 39.22 30.4 33.77

SPQ Asia Opportunities Fund - Class B

SPQ Asia Capital

Hong Kong 12/2/2013Long/Short

EquityGreater China

Equities 37.33 36.86 13.64 76.83

TOP 5 INDIA BASED HEDGE FUNDS

Source : Preqin – December, 2017

Fund Name Firm Name Firm Country Inception Date Core StrategiesCountry

Preferences

Methods of Investment Employed

2017 Return

Since Inception

Three-Year Annualiised

Redart Focus Fund Redart Capital India Sep-09Long/Short Equity,

Value-OrientedIndia

Derivative Markets,, Options

73.51 291.03 19.96

Malabar India Fund, Ltd.

Malabar Investment

AdvisorsIndia Sep-08 Long Bias India Equities 50.03 - 18.38

Banyan India Portfolio

Banyan Capital Advisors

India May-12Long Bias, Value-

OrientedIndia Equities 48.82 131.41 14.06

Karma STAR FundKarma Capital Management

India Feb-04 Long/Short Equity India Equities 45.95 618.23 12.99

Right Horizons Minerva Funds -

India Undervalued

Right Horizons Financial Services

India Nov-10 Long Bias India Equities 41.61 205.81 13.91

TOP 5 INDIA INVESTED HEDGE FUNDS

Source : Preqin – December, 2017

Fund Name Firm Name Firm CountryInception

DateCore Strategies

Country Pref

Methods of Investment Employed

2017 Return

Since Inception

Three-Year Annualiised

Atyant Capital India Fund-I

Atyant Capital Mauritius Jul-06 Long Bias India Equities 79.87 468.05 39.41

Redart Focus Fund Redart Capital India Sep-09Long/Short Equity,

Value-OrientedIndia Derivative Markets 73.51 291.03 19.96

Tantallon India FundTantallon Capital

AdvisorsSingapore Sep-15 Long Bias India - 59.15 50.28 -

SageOne India Growth Master Fund

Lighthouse Canton

Singapore Sep-14 Long Bias India Equities 53.55 - 19.73

Alchemy India Long Term Fund

Alchemy Investment

ManagementSingapore Jun-08 Long/Short Equity India

Derivative Equities, Commodities and

Warrants50.35 239.29 18.72

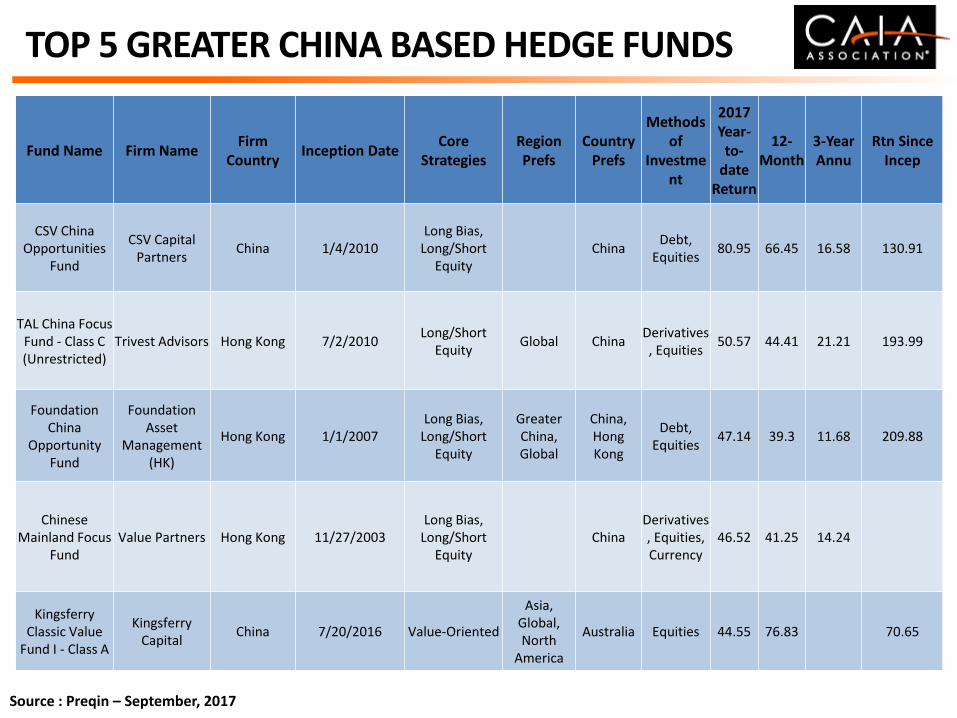

TOP 5 GREATER CHINA BASED HEDGE FUNDS

Source : Preqin – September, 2017

Fund Name Firm NameFirm

CountryInception Date

Core Strategies

RegionPrefs

CountryPrefs

Methodsof

Investment

2017 Year-to-

date Return

12-Month

3-YearAnnu

Rtn Since Incep

CSV China Opportunities

Fund

CSV Capital Partners

China 1/4/2010Long Bias,

Long/Short Equity

ChinaDebt,

Equities80.95 66.45 16.58 130.91

TAL China Focus Fund - Class C (Unrestricted)

Trivest Advisors Hong Kong 7/2/2010Long/Short

EquityGlobal China

Derivatives, Equities

50.57 44.41 21.21 193.99

Foundation China

Opportunity Fund

Foundation Asset

Management (HK)

Hong Kong 1/1/2007Long Bias,

Long/Short Equity

Greater China, Global

China, Hong Kong

Debt, Equities

47.14 39.3 11.68 209.88

Chinese Mainland Focus

FundValue Partners Hong Kong 11/27/2003

Long Bias, Long/Short

EquityChina

Derivatives, Equities, Currency

46.52 41.25 14.24

Kingsferry Classic Value

Fund I - Class A

Kingsferry Capital

China 7/20/2016 Value-Oriented

Asia, Global, North

America

Australia Equities 44.55 76.83 70.65

HFR FUND WEIGHTED COMPOSITE PERFORMANCE INDEX

0

1,000

2,000

3,000

4,000

5,000

6,000

7,000

8,000

9,000

10,000

11,000

12,000

13,000

14,000

15,000

06-1

990

12-1

990

06-1

991

12-1

991

06-1

992

12-1

992

06-1

993

12-1

993

06-1

994

12-1

994

06-1

995

12-1

995

06-1

996

12-1

996

06-1

997

12-1

997

06-1

998

12-1

998

06-1

999

12-1

999

06-2

000

12-2

000

06-2

001

12-2

001

06-2

002

12-2

002

06-2

003

12-2

003

06-2

004

12-2

004

06-2

005

12-2

005

06-2

006

12-2

006

06-2

007

12-2

007

06-2

008

12-2

008

06-2

009

12-2

009

06-2

010

12-2

010

06-2

011

12-2

011

06-2

012

12-2

012

06-2

013

12-2

013

06-2

014

12-2

014

06-2

015

12-2

015

06-2

016

12-2

016

06-2

017

12-2

017

VAM

I

HFRI Fund Weighted Composite Index S&P 500 w/ dividends Barclays Capital Government/Credit Bond Index 3-Month LIBOR USD

Index Net ROR StD Net ROR StD Net ROR StD Net ROR StD Net ROR StD

HFRI FWC 8.68 1.19 4.25 3.69 4.95 3.59 3.23 6.03 9.90 6.55

S&P 500 w/ dividends 21.80 3.93 11.39 10.06 15.77 9.49 8.49 15.06 9.80 14.20

Barclays Govt/Crdt Agg Bond 4.18 1.71 2.50 3.48 2.23 3.40 4.31 4.15 6.86 4.67

3-Month LIBOR 1.29 0.05 0.79 0.12 0.58 0.12 0.75 0.23 3.29 0.70

Since 19902017 3-Year Annualized 5-Year Annualized 10-Year Annualized

Source : HFR Q4 2017 Analysis

HFR MAIN STRATEGY INDICES PERFORMANCE ANALYSIS

Source : HFR Q4 2017 Analysis

0

1,000

2,000

3,000

4,000

5,000

6,000

7,000

8,000

9,000

10,000

11,000

12,000

13,000

14,000

15,000

16,000

17,000

18,000

19,000

20,000

21,000

22,000

23,000

06-1

990

12-1

990

06-1

991

12-1

991

06-1

992

12-1

992

06-1

993

12-1

993

06-1

994

12-1

994

06-1

995

12-1

995

06-1

996

12-1

996

06-1

997

12-1

997

06-1

998

12-1

998

06-1

999

12-1

999

06-2

000

12-2

000

06-2

001

12-2

001

06-2

002

12-2

002

06-2

003

12-2

003

06-2

004

12-2

004

06-2

005

12-2

005

06-2

006

12-2

006

06-2

007

12-2

007

06-2

008

12-2

008

06-2

009

12-2

009

06-2

010

12-2

010

06-2

011

12-2

011

06-2

012

12-2

012

06-2

013

12-2

013

06-2

014

12-2

014

06-2

015

12-2

015

06-2

016

12-2

016

06-2

017

12-2

017

VAM

I

HFRI Fund Weighted Composite Index HFRI Equity Hedge (Total) Index HFRI Event-Driven (Total) Index

HFRI Macro (Total) Index HFRI Relative Value (Total) Index

Index Net ROR StD Net ROR StD Net ROR StD Net ROR StD Net ROR StD

HFRI FWC 8.68 1.19 4.25 3.69 4.95 3.59 3.23 6.03 9.90 6.55

HFRI Equity Hedge Index 13.46 1.44 5.82 5.64 6.63 5.35 3.19 8.56 11.54 8.68

HFRI Event-Driven Index 7.73 1.68 4.73 4.73 5.49 4.31 4.17 6.44 10.45 6.51

HFRI Macro Index 2.21 2.88 0.65 3.88 1.40 3.67 1.95 4.49 10.15 7.12

HFRI Relative Value Index 5.11 1.26 4.11 2.80 4.68 2.61 4.81 4.98 9.23 4.17

Since 19902017 3-Year Annualized 5-Year Annualized 10-Year Annualized

Fund of Hedge Funds …. Dead …. Or …. Alive?

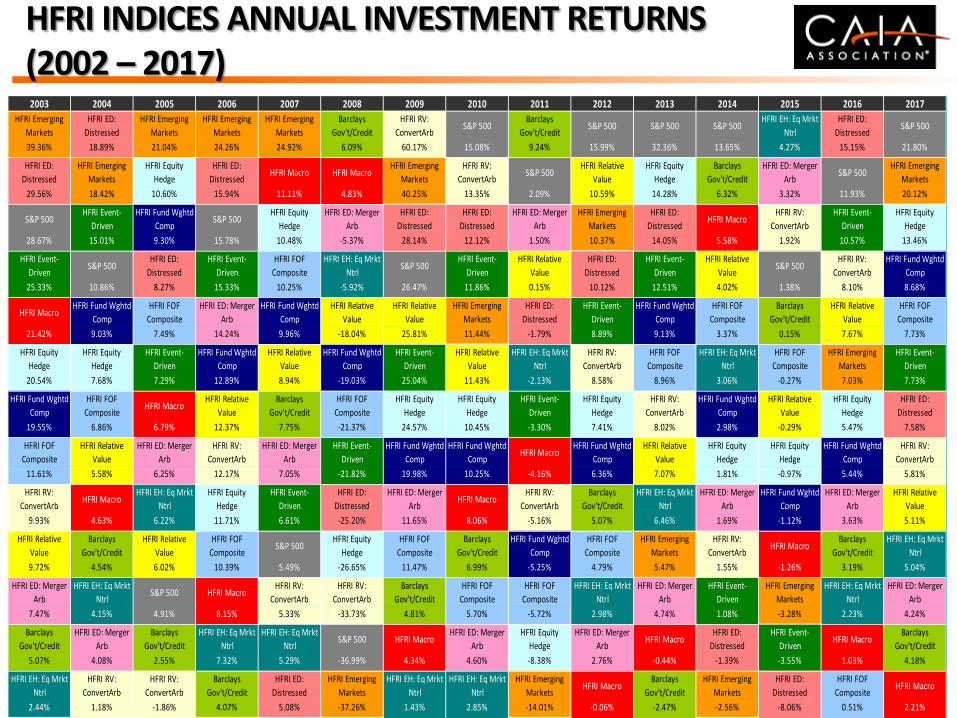

HFRI INDICES ANNUAL INVESTMENT RETURNS (2002 – 2017)

2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017

HFRI Emerging

Markets

HFRI ED:

Distressed

HFRI Emerging

Markets

HFRI Emerging

Markets

HFRI Emerging

Markets

Barclays

Gov't/Credit

HFRI RV:

ConvertArbS&P 500

Barclays

Gov't/CreditS&P 500 S&P 500 S&P 500

HFRI EH: Eq Mrkt

Ntrl

HFRI ED:

DistressedS&P 500

39.36% 18.89% 21.04% 24.26% 24.92% 6.09% 60.17% 15.08% 9.24% 15.99% 32.36% 13.65% 4.27% 15.15% 21.80%

HFRI ED:

Distressed

HFRI Emerging

Markets

HFRI Equity

Hedge

HFRI ED:

DistressedHFRI Macro HFRI Macro

HFRI Emerging

Markets

HFRI RV:

ConvertArbS&P 500

HFRI Relative

Value

HFRI Equity

Hedge

Barclays

Gov't/Credit

HFRI ED: Merger

ArbS&P 500

HFRI Emerging

Markets

29.56% 18.42% 10.60% 15.94% 11.11% 4.83% 40.25% 13.35% 2.09% 10.59% 14.28% 6.32% 3.32% 11.93% 20.12%

S&P 500HFRI Event-

Driven

HFRI Fund Wghtd

CompS&P 500

HFRI Equity

Hedge

HFRI ED: Merger

Arb

HFRI ED:

Distressed

HFRI ED:

Distressed

HFRI ED: Merger

Arb

HFRI Emerging

Markets

HFRI ED:

DistressedHFRI Macro

HFRI RV:

ConvertArb

HFRI Event-

Driven

HFRI Equity

Hedge

28.67% 15.01% 9.30% 15.78% 10.48% -5.37% 28.14% 12.12% 1.50% 10.37% 14.05% 5.58% 1.92% 10.57% 13.46%

HFRI Event-

DrivenS&P 500

HFRI ED:

Distressed

HFRI Event-

Driven

HFRI FOF

Composite

HFRI EH: Eq Mrkt

NtrlS&P 500

HFRI Event-

Driven

HFRI Relative

Value

HFRI ED:

Distressed

HFRI Event-

Driven

HFRI Relative

ValueS&P 500

HFRI RV:

ConvertArb

HFRI Fund Wghtd

Comp

25.33% 10.86% 8.27% 15.33% 10.25% -5.92% 26.47% 11.86% 0.15% 10.12% 12.51% 4.02% 1.38% 8.10% 8.68%

HFRI MacroHFRI Fund Wghtd

Comp

HFRI FOF

Composite

HFRI ED: Merger

Arb

HFRI Fund Wghtd

Comp

HFRI Relative

Value

HFRI Relative

Value

HFRI Emerging

Markets

HFRI ED:

Distressed

HFRI Event-

Driven

HFRI Fund Wghtd

Comp

HFRI FOF

Composite

Barclays

Gov't/Credit

HFRI Relative

Value

HFRI FOF

Composite

21.42% 9.03% 7.49% 14.24% 9.96% -18.04% 25.81% 11.44% -1.79% 8.89% 9.13% 3.37% 0.15% 7.67% 7.73%

HFRI Equity

Hedge

HFRI Equity

Hedge

HFRI Event-

Driven

HFRI Fund Wghtd

Comp

HFRI Relative

Value

HFRI Fund Wghtd

Comp

HFRI Event-

Driven

HFRI Relative

Value

HFRI EH: Eq Mrkt

Ntrl

HFRI RV:

ConvertArb

HFRI FOF

Composite

HFRI EH: Eq Mrkt

Ntrl

HFRI FOF

Composite

HFRI Emerging

Markets

HFRI Event-

Driven

20.54% 7.68% 7.29% 12.89% 8.94% -19.03% 25.04% 11.43% -2.13% 8.58% 8.96% 3.06% -0.27% 7.03% 7.73%

HFRI Fund Wghtd

Comp

HFRI FOF

CompositeHFRI Macro

HFRI Relative

Value

Barclays

Gov't/Credit

HFRI FOF

Composite

HFRI Equity

Hedge

HFRI Equity

Hedge

HFRI Event-

Driven

HFRI Equity

Hedge

HFRI RV:

ConvertArb

HFRI Fund Wghtd

Comp

HFRI Relative

Value

HFRI Equity

Hedge

HFRI ED:

Distressed

19.55% 6.86% 6.79% 12.37% 7.75% -21.37% 24.57% 10.45% -3.30% 7.41% 8.02% 2.98% -0.29% 5.47% 7.58%

HFRI FOF

Composite

HFRI Relative

Value

HFRI ED: Merger

Arb

HFRI RV:

ConvertArb

HFRI ED: Merger

Arb

HFRI Event-

Driven

HFRI Fund Wghtd

Comp

HFRI Fund Wghtd

CompHFRI Macro

HFRI Fund Wghtd

Comp

HFRI Relative

Value

HFRI Equity

Hedge

HFRI Equity

Hedge

HFRI Fund Wghtd

Comp

HFRI RV:

ConvertArb

11.61% 5.58% 6.25% 12.17% 7.05% -21.82% 19.98% 10.25% -4.16% 6.36% 7.07% 1.81% -0.97% 5.44% 5.81%

HFRI RV:

ConvertArbHFRI Macro

HFRI EH: Eq Mrkt

Ntrl

HFRI Equity

Hedge

HFRI Event-

Driven

HFRI ED:

Distressed

HFRI ED: Merger

ArbHFRI Macro

HFRI RV:

ConvertArb

Barclays

Gov't/Credit

HFRI EH: Eq Mrkt

Ntrl

HFRI ED: Merger

Arb

HFRI Fund Wghtd

Comp

HFRI ED: Merger

Arb

HFRI Relative

Value

9.93% 4.63% 6.22% 11.71% 6.61% -25.20% 11.65% 8.06% -5.16% 5.07% 6.46% 1.69% -1.12% 3.63% 5.11%

HFRI Relative

Value

Barclays

Gov't/Credit

HFRI Relative

Value

HFRI FOF

CompositeS&P 500

HFRI Equity

Hedge

HFRI FOF

Composite

Barclays

Gov't/Credit

HFRI Fund Wghtd

Comp

HFRI FOF

Composite

HFRI Emerging

Markets

HFRI RV:

ConvertArbHFRI Macro

Barclays

Gov't/Credit

HFRI EH: Eq Mrkt

Ntrl

9.72% 4.54% 6.02% 10.39% 5.49% -26.65% 11.47% 6.99% -5.25% 4.79% 5.47% 1.55% -1.26% 3.19% 5.04%

HFRI ED: Merger

Arb

HFRI EH: Eq Mrkt

NtrlS&P 500 HFRI Macro

HFRI RV:

ConvertArb

HFRI RV:

ConvertArb

Barclays

Gov't/Credit

HFRI FOF

Composite

HFRI FOF

Composite

HFRI EH: Eq Mrkt

Ntrl

HFRI ED: Merger

Arb

HFRI Event-

Driven

HFRI Emerging

Markets

HFRI EH: Eq Mrkt

Ntrl

HFRI ED: Merger

Arb

7.47% 4.15% 4.91% 8.15% 5.33% -33.73% 4.81% 5.70% -5.72% 2.98% 4.74% 1.08% -3.28% 2.23% 4.24%

Barclays

Gov't/Credit

HFRI ED: Merger

Arb

Barclays

Gov't/Credit

HFRI EH: Eq Mrkt

Ntrl

HFRI EH: Eq Mrkt

NtrlS&P 500 HFRI Macro

HFRI ED: Merger

Arb

HFRI Equity

Hedge

HFRI ED: Merger

ArbHFRI Macro

HFRI ED:

Distressed

HFRI Event-

DrivenHFRI Macro

Barclays

Gov't/Credit

5.07% 4.08% 2.55% 7.32% 5.29% -36.99% 4.34% 4.60% -8.38% 2.76% -0.44% -1.39% -3.55% 1.03% 4.18%

HFRI EH: Eq Mrkt

Ntrl

HFRI RV:

ConvertArb

HFRI RV:

ConvertArb

Barclays

Gov't/Credit

HFRI ED:

Distressed

HFRI Emerging

Markets

HFRI EH: Eq Mrkt

Ntrl

HFRI EH: Eq Mrkt

Ntrl

HFRI Emerging

MarketsHFRI Macro

Barclays

Gov't/Credit

HFRI Emerging

Markets

HFRI ED:

Distressed

HFRI FOF

CompositeHFRI Macro

2.44% 1.18% -1.86% 4.07% 5.08% -37.26% 1.43% 2.85% -14.01% -0.06% -2.47% -2.56% -8.06% 0.51% 2.21%

HEDGE FUND STRATEGY CLASSIFICATION TREE

Single-Manager Hedge Funds

Special Situations

Activist

Credit Arbitrage

Distressed /Restructuring

Merger Arbitrage

Private Issue /Regulation D

Multi-Strategy

DiscretionaryThematic

Active Trading

Commodity

Agriculture

Energy

SystematicDiversified

Currency

Discretionary

Systematic

Multi-Strategy

Short Bias

Equity Market Neutral

FundamentalGrowth

FundamentalValue

QuantitativeDirectional

Sector

Energy / Basic Materials

Technology /Healthcare

Multi-Strategy

Equity Hedge MacroEvent-Driven

Metals

Multi

EnergyInfrastructure

Real Estate

Relative Value

Fixed Income –Asset Backed

Fixed Income –Convertible Arbitrage

Fixed Income –Corporate

Fixed Income –Sovereign

Volatility

Yield Alternatives

Multi-Strategy

Multi-Manager Funds

Fund of Funds

Conservative

Diversified

Market Defensive

Strategic

Equity Hedge MacroEvent-Driven Relative Value

GLOBAL NUMBER OF FUNDS: HEDGE FUNDS VS FUND OF FUNDS

Source : HFR Q4 2017 Analysis

80 127

168

237

291

377

389

426

477

514

538

550 78

1

1,23

2 1,65

4 1,99

6

2,22

1

2,46

2

2,43

9

2,16

2

2,03

7

2,00

1

1,87

0

1,77

6

1,71

7

1,65

7

1,54

7

1,51

7

1,48

2

1,45

5

1,41

9

530

694 93

7

1,27

7 1,65

4 2,00

6 2,39

2

2,56

4 2,84

8 3,10

2

3,33

5

3,90

4

4,59

8

5,06

5

5,78

2

6,66

5

7,24

1 7,63

4

6,84

5

6,88

3 7,20

0 7,57

4 7,94

0 8,19

0

8,42

5

8,47

4

8,25

6

8,21

6

8,20

9

8,27

5

8,33

5

0

1,000

2,000

3,000

4,000

5,000

6,000

7,000

8,000

9,000

1990 1991 1992 1993 1994 1995 1996 1997 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 Q12017

Q22017

Q32017

Q42017

Num

ber o

f Fu

nds

Fund of Funds Hedge Funds

GLOBAL FOHF - GROWTH OF ASSETS / NET ASSET FLOW

Source : HFR Q4 2017 Analysis

$1.9

$19.9 $36.8

$75.4 $74.6

$56.3 $52.5

$74.0 $75.8

$76.1 $83.5

$102.5

$206.9

$293.3

$358.6

$394.6

$655.9

$798.6

$593.2 $571.3

$646.3

$629.6 $638.2

$663.1 $673.3

$657.4

$632.8 $637.5

$631.5 $639.4 $645.6

$15.4 $14.8 $28.5

($0.8)

($16.2)($3.3)

$18.0 $1.8 $0.2 $7.1

$18.5

$103.4

$59.4

$33.2 $9.5

$49.7 $59.2

($40.9)

($118.4)

($11.8)($7.9)

($22.2)

($20.2)($4.1)

($14.8)($26.4)

($6.0) ($8.1) ($4.3) ($3.0)

($200)

$0

$200

$400

$600

$800

$1,000

1990 1991 1992 1993 1994 1995 1996 1997 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 Q12017

Q22017

Q32017

Q42017

Ass

ets

($BN

)

Estimated Assets Net Asset Flow

GLOBAL FOHF – QUARTERLY PERFORMANCE

Source : HFR Q4 2017 Analysis

4.97

(0

.58)

(10.

02)

1.04

3.

29

7.08

0.

72

13.5

2 7.

08

(2.2

1)0.

60

(1.1

9)0.

73 1.54

(1

.83)

2.38

0.

98

0.20

(1

.45)

1.32

1.

15

4.01

2.

25

3.74

3.

16

(1.5

1)0.

29

4.86

0.

80

0.16

4.

18

2.20

5.

00

(0.7

8)0.

53

5.40

3.

16

4.53

0.

27

1.97

(4

.24)

1.90

(1

0.41

)(1

0.05

)0.

37

4.81

4.

43

1.47

1.

41

(2.5

9)3.

27

3.62

0.

88

(1.1

8)(4

.98)

(0.4

7)3.

37

(2.3

1)2.

42

1.32

3.

32

0.05

1.

67

3.67

0.

56 1.

54

0.28

0.

95

2.50

0.

21

(3.6

0)0.

73

(3.1

2)0.

56

2.29

0.

86

2.38

0.

81

2.32

2.

02

(15.00)

(10.00)

(5.00)

0.00

5.00

10.00

15.00

Q1-

1998

Q2-

1998

Q3-

1998

Q4-

1998

Q1-

1999

Q2-

1999

Q3-

1999

Q4-

1999

Q1-

2000

Q2-

2000

Q3-

2000

Q4-

2000

Q1-

2001

Q2-

2001

Q3-

2001

Q4-

2001

Q1-

2002

Q2-

2002

Q3-

2002

Q4-

2002

Q1-

2003

Q2-

2003

Q3-

2003

Q4-

2003

Q1-

2004

Q2-

2004

Q3-

2004

Q4-

2004

Q1-

2005

Q2-

2005

Q3-

2005

Q4-

2005

Q1-

2006

Q2-

2006

Q3-

2006

Q4-

2006

Q1-

2007

Q2-

2007

Q3

2007

Q4

2007

Q1-

2008

Q2-

2008

Q3-

2008

Q4-

2008

Q1-

2009

Q2-

2009

Q3-

2009

Q4-

2009

Q1-

2010

Q2-

2010

Q3-

2010

Q4-

2010

Q1-

2011

Q2-

2011

Q3-

2011

Q4-

2011

Q1-

2012

Q2-

2012

Q3-

2012

Q4-

2012

Q1-

2013

Q2-

2013

Q3-

2013

Q4-

2013

Q1-

2014

Q2-

2014

Q3-

2014

Q4-

2014

Q1-

2015

Q2-

2015

Q3-

2015

Q4-

2015

Q1-

2016

Q2-

2016

Q3-

2016

Q4-

2016

Q1-

2017

Q2-

2017

Q3-

2017

Q4-

2017

Retu

rn %

GLOBAL BILLION DOLLAR CLUB - FOHF

Fund Manager Location Year EstTotal AUM (USD mn)

AUM Date

Blackstone Alternative Asset Management US 1990 $72,000 30-Jun-17

UBS Hedge Fund Solutions US 2000 $37,400 30-Jun-17

Goldman Sachs Asset Management US 1997 $29,200 30-Jun-17

Grosvenor Capital Management US 1971 $25,900 30-Jun-17

EnTrustPermal US 1971 $24,400 30-Jun-17

HSBC Alternative Investments UK 1994 $24,200 1-Jul-17

Morgan Stanley Alternative Investment Partners US 2000 $23,300 30-Jun-17

BlackRock Alternative Advisors US 1995 $22,900 1-Jul-17

PAAMCO Prisma* US 2000 $16,900 31-Dec-17

Man FRM UK 1991 $16,200 1-Jan-17

Source: Preqin – September, 2017

CONTENT

Professional Development

A Dive into the Global Hedge Fund Industry

Why Alternative Investments? …. Investor Appetite

Asia Pacific Investors …. Who are they?

What’s next?

Due Diligence

Due Diligence

DUE DILIGENCE

Increased scrutinyIncreased fiduciary responsibility

Increased time and resource requirementsIncreased regulatory burdenIncreased potential liability

Increased accountabilityIncreased Cost

Leading to ….

How have due diligence requirements changed since 2008?

Operational Due Diligence Investment and Risk Due Diligence

Compliance Manual (including KYC checks, Money

Laundering procedures, trade errors, soft

commission policies etc.)

Prime Brokerage Agreement

Fund Administrator Agreement

Investment Management Agreement

Business Continuity documentation

Company accounts for last three years

Projected Budget for the next 5 years

Trading and Portfolio management system

verification

Authorisation, execution, confirmation,

settlement, reconciliation and accounting

policies. (Need for adequate segregation of

duties)

Detailed valuation policies or a pricing matrix

(maintaining transparency, consistency and

oversight)

Counterparty risk

Key person risk and insurance

DDQ

Prospectus

Fund Presentation

Risk Limits

Kroll reports and character references

Analysis of Market and product Liquidity,

volatility and credit risks

Modelling performance can be difficult:

Downside deviation, correlation, variance,

volatility, VAR, Sortino and Sharpe ratios

Back testing

Scenario analysis

Consistent approach to portfolio management

Definition and measurement of risk to the

portfolio

Investment in Non-listed Instruments

Best Execution

Conflicts of interest

Stock Borrowing

Personal Account Dealing

Investment Decision-making Process

Risk without return Risk with return

DUE DILIGENCE REQUIREMENTS WHEN INVESTING IN HEDGE FUNDS

CONTENT

Professional Development

A Dive into the Global Hedge Fund Industry

Why Alternative Investments? …. Investor Appetite

Asia Pacific Investors …. Who are they?

What’s next?

Due Diligence

Professional Business Education & Development

What’s needed to navigate and succeed in a complex workplace?

Our industry is shrinking – how does one stand out and survive?

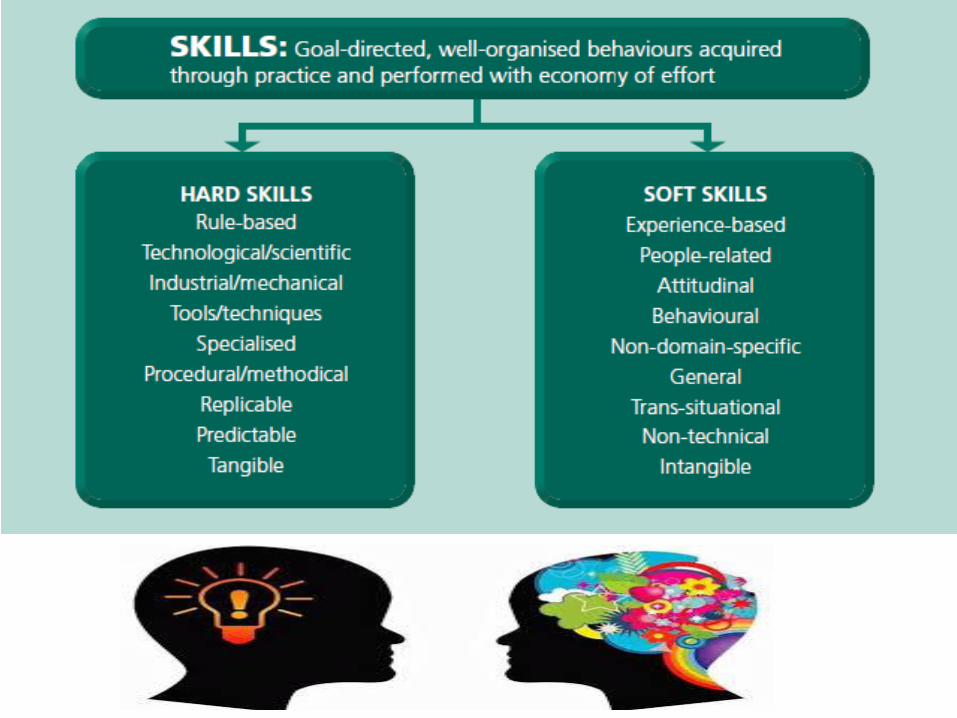

FINANCIAL SERVICES SKILLS

100

THE FINANCIAL SERVICE INDUSTRY IS SHRINKING

The number of Bloomberg terminals fell in 2016 for only the second time since the company was founded in 1981.

“A lot of the vendors [of financial information] are facing headwinds… The combination of machines replacing traders where they can and cutbacks overall in

financial institutions in terms of budgets has made it difficult for all vendors to maintain [terminal numbers].”

Financial Times – March, 2017

Stand Out To Survive!

THE FINANCIAL SERVICE INDUSTRY IS SHRINKING

Lawrence Wong: Minister for National Development, Singapore, 2016:

…. it’s very clear that the next decade will be a highly disruptive one for financial institutions worldwide …. will

have a significant bearing on the scale and nature of financial sector jobs in all financial centres …. FinTech alone will

impact one-third of employees at traditional banks over the next 10 years…we must all have a greater sense of urgency

towards reskilling, upskilling, and acquiring new skills.

The mindset must be:

“Train today, prepare for tomorrow”

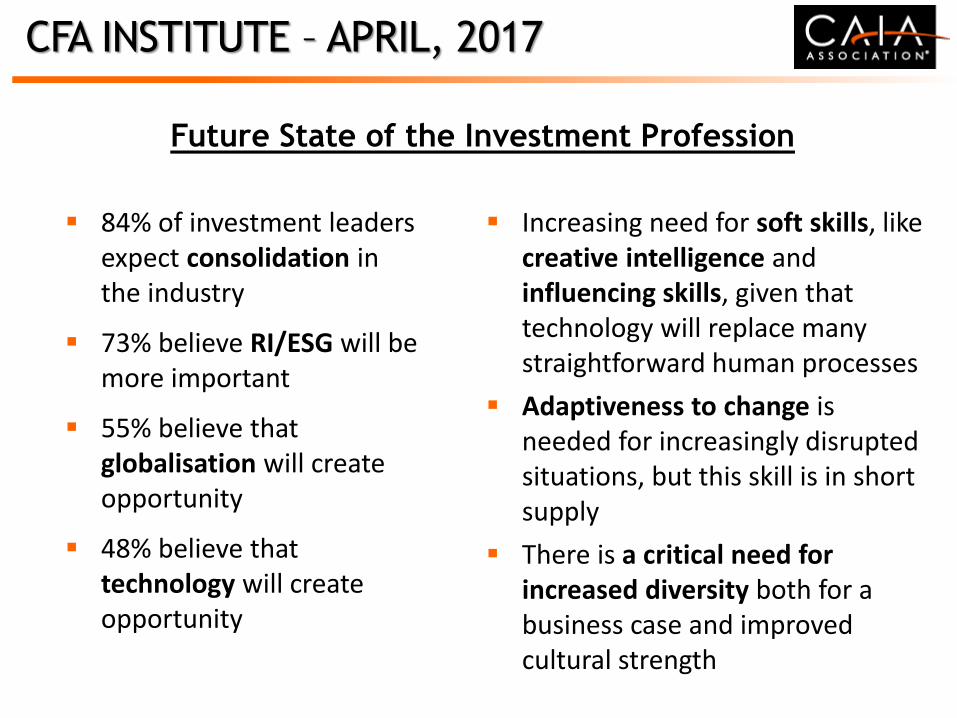

CFA INSTITUTE – APRIL, 2017

Future State of the Investment Profession

84% of investment leaders expect consolidation in the industry

73% believe RI/ESG will be more important

55% believe that globalisation will create opportunity

48% believe that technology will create opportunity

Increasing need for soft skills, like creative intelligence and influencing skills, given that technology will replace many straightforward human processes

Adaptiveness to change is needed for increasingly disrupted situations, but this skill is in short supply

There is a critical need for increased diversity both for a business case and improved cultural strength

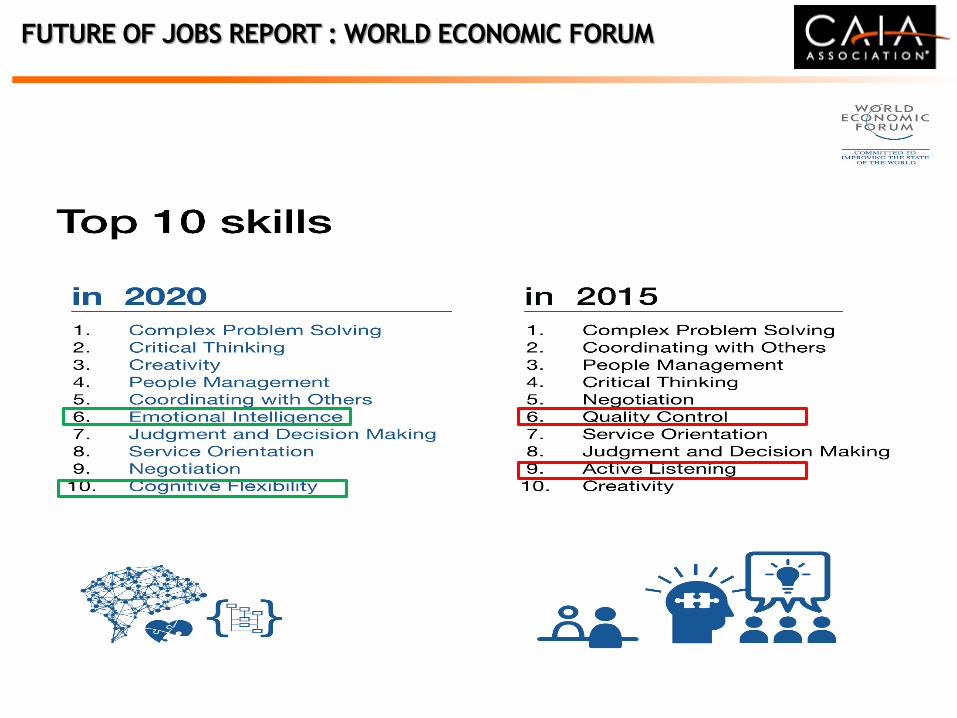

FUTURE OF JOBS REPORT : WORLD ECONOMIC FORUM

PROFESSIONAL DESIGNATIONS : THERE ARE A

LOT OF THEM!

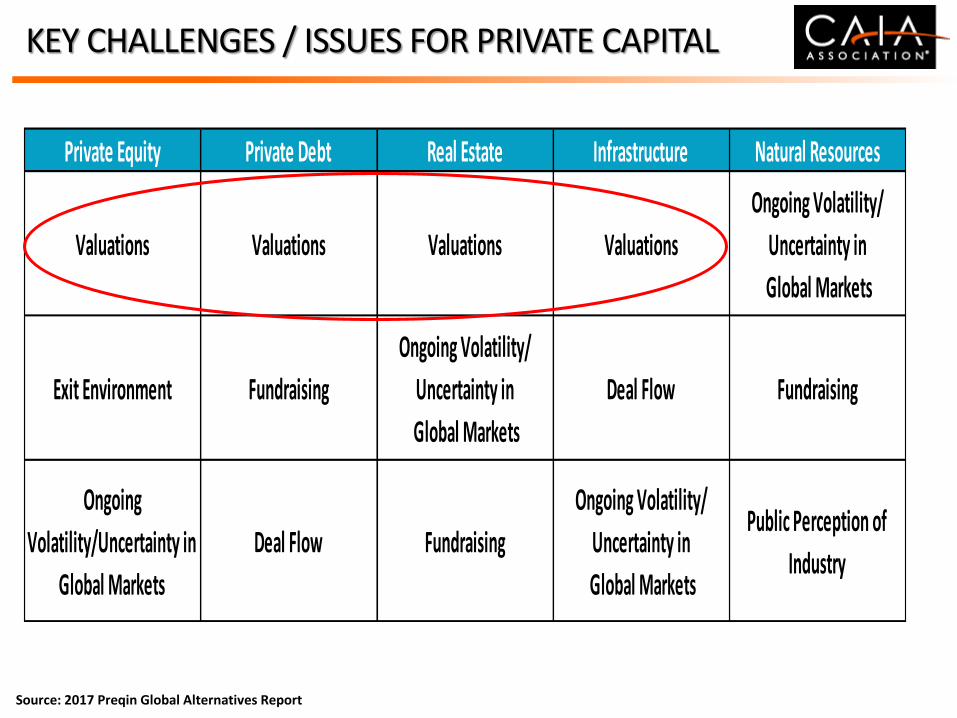

Source: 2017 Preqin Global Alternatives Report

Private Equity Private Debt Real Estate Infrastructure Natural Resources

Valuations Valuations Valuations Valuations

Ongoing Volatility/

Uncertainty in

Global Markets

Exit Environment Fundraising

Ongoing Volatility/

Uncertainty in

Global Markets

Deal Flow Fundraising

Ongoing

Volatility/Uncertainty in

Global Markets

Deal Flow Fundraising

Ongoing Volatility/

Uncertainty in

Global Markets

Public Perception of

Industry

KEY CHALLENGES / ISSUES FOR PRIVATE CAPITAL

CHINA ACCOUNTS FOR 21% OF ALL DEALS AND 36% OF AGGREGATE DEAL VALUE …. NOTE SIZE OF INDIA!

0

2,000

4,000

6,000

8,000

10,000

12,000

2007 2008 2009 2010 2011 2012 2013 2014 2015 2016

No

. o

f D

ea

ls

North America Europe Greater China India Israel Other

Source: Preqin Online Research Centre

THE WORLD IS MULTI-ASSET

113

CONTENT

Professional Development

A Dive into the Global Hedge Fund Industry

Why Alternative Investments? …. Investor Appetite

Asia Pacific Investors …. Who are they?

What’s next?

Due Diligence

Key Takeaways …. Crystal Ball Time!

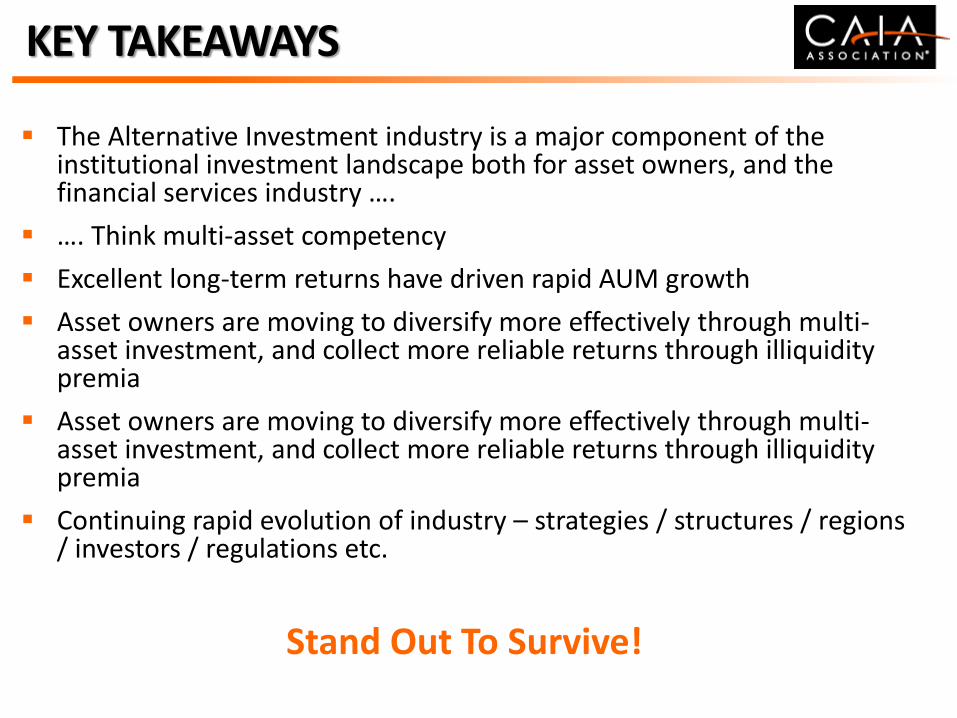

KEY TAKEAWAYS

The Alternative Investment industry is a major component of the institutional investment landscape both for asset owners, and the financial services industry ….

…. Think multi-asset competency

Excellent long-term returns have driven rapid AUM growth

Asset owners are moving to diversify more effectively through multi-asset investment, and collect more reliable returns through illiquidity premia

Asset owners are moving to diversify more effectively through multi-asset investment, and collect more reliable returns through illiquidity premia

Continuing rapid evolution of industry – strategies / structures / regions / investors / regulations etc.

Stand Out To Survive!

KEY TAKEAWAYS

Distinct investor motivations across different alternative asset classes

Excellent long-term returns have driven rapid AUM growth

PE mature, still growing strongly Infrastructure and private debt less mature, tremendous growth

prospects Natural Resources currently challenged

Current valuations high; investors and fund managers alike cautious about forward-looking prospects

But committed to further increasing allocations – risk/reward attractive as ever

Continuing rapid evolution of industry – strategies / structures / regions / investors / regulations etc.

Stand Out To Survive!

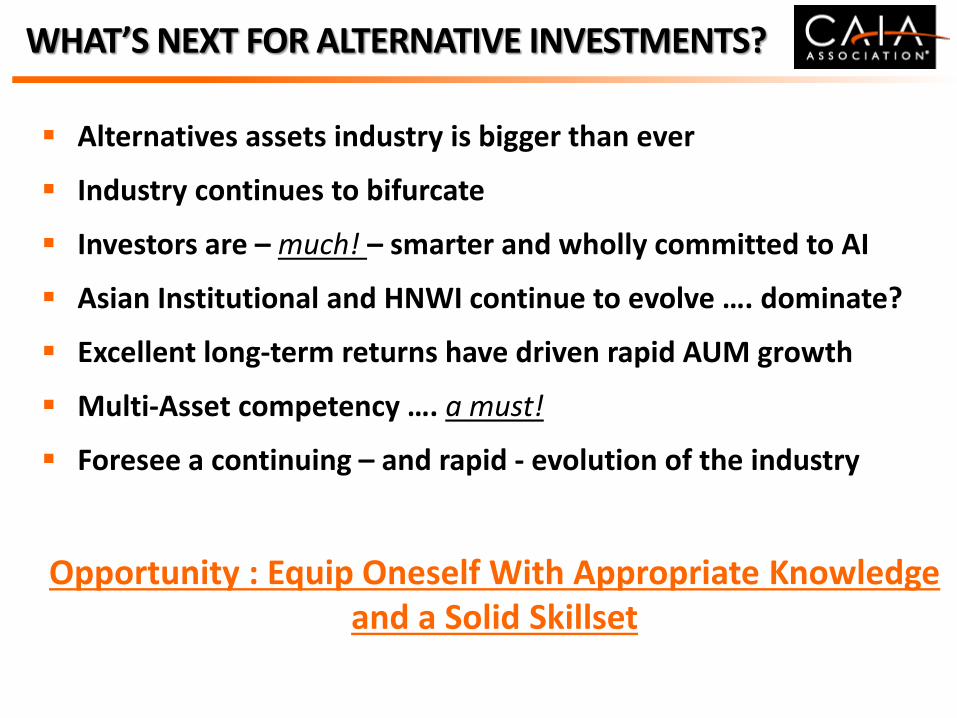

WHAT’S NEXT FOR ALTERNATIVE INVESTMENTS?

Alternatives assets industry is bigger than ever

Industry continues to bifurcate

Investors are – much! – smarter and wholly committed to AI

Asian Institutional and HNWI continue to evolve …. dominate?

Excellent long-term returns have driven rapid AUM growth

Multi-Asset competency …. a must!

Foresee a continuing – and rapid - evolution of the industry

Opportunity : Equip Oneself With Appropriate Knowledge and a Solid Skillset

Thank You!

THE WORLD IS MULTI-ASSET

121