Embed Size (px)

DESCRIPTION

Master thesis

Citation preview

Economic Scenario Generators

Mark Plomp

November 10, 2013

Msc thesis Stochastics and Financial Mathematics

Supervisors:Yulia Bondarouk (KPMG)

Jeroen Gielen(KPMG)Peter Spreij (UvA)

AcknowledgmentsThis thesis is the result of my master project carried out at the Fi-nancial Risk Management and Risk Actuarial Services department ofKPMG in Amstelveen. I would like to thank everyone who has en-couraged me and supported me in writing this thesis. At KPMG YuliaBondarouk was my main supervisor and Jeroen Gielen was my secondsupervisor. I want to thank the both of them for all the time they putin helping me with the thesis, all the great feedback and encouragingme to look at the subject from an actuarial and economical point ofview in stead of only looking at the mathematics. My supervisor atthe university was Peter Spreij. I also want to thank him for the greatguidance I got from him, especially with getting all the mathemati-cal details right. Further, I am very grateful to all the colleagues atKPMG; for all the help, the interesting discussions and the informaltalk from time to time.

AbstractIn 2009 the European Union agreed upon introducing a new regulatoryframework, called Solvency II, for insurance companies operating inthe EU. One of the requirements of the Solvency II directive states thatthe valuation of assets and liabilities needs to be market consistent.For most insurance companies the only practical method to achievea market consistent valuation is using a so called economic scenariogenerator (ESG). An ESG generates future scenarios for different riskfactors by Monte Carlo simulation of stochastic models correspondingto these risk factors.

In this thesis the construction and use of a market consistenteconomic scenario generator is investigated. The main question un-der investigation is what the sensitivities are in calibrating the ESGand simulating the future scenarios and what their impact is on theestimation of the market consistent value. Four risk factors are mod-elled for the ESG: interest rates, stocks, real estate and inflation rates.The Hull-White one factor model is used for the modelling of interestrates; stocks and real estate are modelled by the Black-Scholes-Hull-White model and the inflation rates are modelled with the Vasicekmodel. First on the basis of available literature the stochastic modelsare discussed and option pricing formulas corresponding to these mod-els are derived. Subsequently the calibration of the stochastic modelsto market data is discussed; matching the market prices of optionsto the option pricing formulas derived in the first part is one of themain parts of the calibration. Afterwards, for the analysis of the ESG,two types of insurance policies are modelled. The analysis includes:the impact of the characteristics of the policies on the value, the cal-ibration to different market data, estimation errors due to the MonteCarlo simulation and the impact of changes in the way the models arecalibrated.

Contents

I Background 6

1 General background 71.1 Solvency II . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 71.2 Market Consistent Valuation . . . . . . . . . . . . . . . . . . . . . . 81.3 Economic Scenario Generator . . . . . . . . . . . . . . . . . . . . . 10

2 Technical background 12

II Theory 18

3 The interest rate model 193.1 The bond price . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 20

3.1.1 Alternative representation of the short rate . . . . . . . . . . 243.2 Bond option . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 24

3.2.1 Bond option under the Hull-White model . . . . . . . . . . . 29

4 The equity model 314.1 change of measure . . . . . . . . . . . . . . . . . . . . . . . . . . . . 33

5 The real estate model 385.1 Unsmoothing . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 39

6 The inflation model 41

7 Simulation 437.1 Euler Scheme . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 437.2 Discretisation and distributional error . . . . . . . . . . . . . . . . . 44

1

III Analysis and results 47

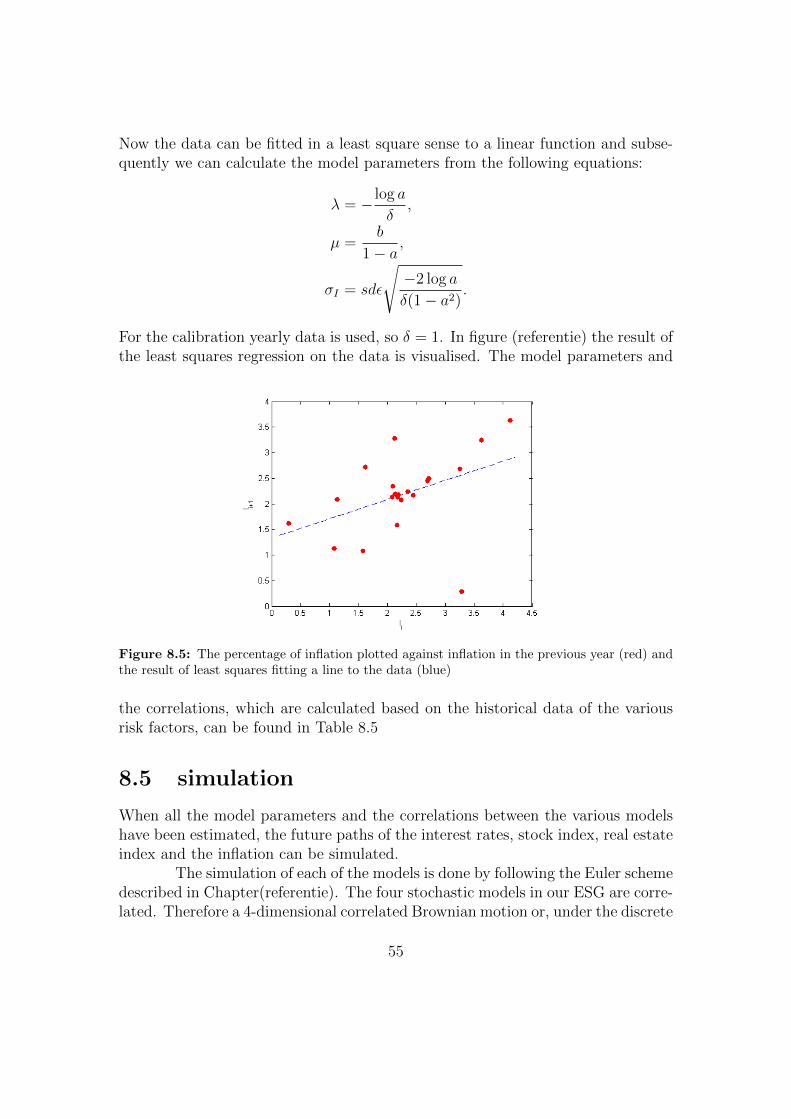

8 Calibration and simulation 488.1 Interest rate model . . . . . . . . . . . . . . . . . . . . . . . . . . . 488.2 Equity model . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 508.3 Real estate model . . . . . . . . . . . . . . . . . . . . . . . . . . . . 528.4 Inflation model . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 548.5 simulation . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 55

9 Insurance Products 59

10 Analysis of the technical provisions 6310.1 Policy conditions . . . . . . . . . . . . . . . . . . . . . . . . . . . . 6310.2 Market conditions . . . . . . . . . . . . . . . . . . . . . . . . . . . . 6810.3 Estimation error . . . . . . . . . . . . . . . . . . . . . . . . . . . . 6910.4 Changes in the calibration . . . . . . . . . . . . . . . . . . . . . . . 73

11 Summary, Conclusions and Discussion 7711.1 Improvement of the ESG . . . . . . . . . . . . . . . . . . . . . . . . 78

A Derivation of Black’s formula 82

B Abstract Bayes’ Formula 84

C Geltner’s real estate unsmoothing method 86

2

Introduction

The goal of this thesis is to discuss the construction and use of a market consistenteconomic scenario generator (ESG) by insurance companies. A market consistentESG consists of various stochastic models and produces risk-neutral future sce-narios. It is a tool for insurers with which they can calculate the present value oftheir assets and liabilities, also called technical provisions. In this thesis we willbuild our own ESG, which will be programmed in Matlab.

The construction of an ESG requires one to make a choice of asset classes(or risk factors) to be modelled, which stochastic models we want to use to simulatethese classes and how these models are going to be calibrated. Subsequently,economic scenarios can be generated for the various asset classes and used tocalculate the technical provisions for various insurance products.

Typically many risk factors play a role in the asset management of aninsurer; for example, interest rates, inflation, credit spreads, equity movements,real estate prices and exchange rates. However, to control the complexity of themodel not all of these factors will be modelled. The most important assets inan insurance company’s portfolio are generally bonds, stocks and real estate [33].Also, inflation can be an important factor for the liabilities of an insurer, becauseoften guarantees embedded in insurance contracts are indexed yearly with theinflation rate. Therefore, we restrict ourselves to modelling these four risk factors,where bonds will be modelled by modelling interest rates.

During the last fifty years a large variety of stochastic models has beendeveloped for the three asset classes. Here the choice is made to use the Hull-Whiteone factor model for the stochastic interest rates, the Hull-White-Black-Scholesmodel for equity and real estate and the Vasicek model for inflation rates. Thischoice was made to get realistic results while controlling the complexity of theESG.

The Hull-White model is chosen because it can give an exact fit to thecurrent term structure, we can derive analytical formulas for interest rate deriva-tives, like swaptions, which makes it easier to calibrate the model accurately tomarket data and it is fairly easy to use the equity model under Hull-White interestrates. Moreover, for options the implied volatilities are higher for out-of-the-money

3

strikes, which is consistent with the volatility skew/smiles implied from marketprices of floors and swaptions [26]. This is a very desirable feature of the modelsince interest rate options embedded in an insurance product are usually writtenon out-of-the-money strikes.

For equity the Hull-White-Black-Scholes model is chosen because it is easyto use simultaneously with the Hull-White model and it is analytically tractable,which makes calibration to options easy.

The choice for the Vasicek model for inflation rates was made, because itis easy to handle and shows mean reverting behaviour, which is a desirable featurefor inflation.

Another analytically tractable interest rate model which can be fitted tothe term structure is the CIR++ model [5]. However, the equity model loses itsanalytical tractability under the CIR++ model. Therefore, the Hull-White modelis chosen over the CIR++ model.

As will be discussed in more depth in Chapter 1, it is preferred thatthe calibration of the model is done with liquidly traded financial instruments ifpossible. Therefore the interest model and the equity model will be calibrated toswaptions resp. (European) call options. For real estate and inflation, no liquidlytraded options or other derivatives are available, therefore we have to resort tohistorical data to calibrate the models. For real estate we will calibrate the modelbased on the historical values of a so called appraisal index and for inflation thecalibration will be done based on historical euro zone inflation rates.

Two types of insurance contracts will be modelled and valuated in thisthesis, both of which are life insurance contracts in which at least a guaranteedsum is paid at time of maturity, e.g. at retirement age.

The first contract we will model is called a surplus interest sharing policy.For this policy the return on a portfolio of government bonds is compared to areference yield. If the return on the portfolio during a period of one year is higherthan the reference yield, then part of the excess return is shared with the policyholder resulting in a higher sum of money at time of maturity.

The second contract is called an endowment policy. For this contract thepolicy holder can choose a fund to invest in, e.g. a mixed fund with bonds, stockand real estate. If at maturity the fund is worth more than the guaranteed sum,then part of the profits are shared with the policy holder.

As will also be discussed in more depth in Chapter 1, under Solvency IIthe insurance companies are obliged to calculate their technical provisions in amarket consistent way. Doing these calculations by using an Economic ScenarioGenerator had become very popular in the insurance industry [44]. Hence, it isvery important for insurance companies, regulators and other parties like KPMGinvolved with insurance companies, to understand how these models work and

4

what choices can be made when using a scenario generator. Therefore, the mainquestion about the ESG we develop in this thesis is

What are the sensitivities in calibrating the Economic Scenario Generator andsimulating future scenarios and what is the possible impact of these sensitivities

on the outcome of the technical provisions?

It goes without saying that changes in the calibration and simulation methods haveto fall within the market consistent framework. However, often markets aren’tcompletely liquid and some assumptions have to be made when calibrating themodels, because of this we can investigate what reasonable changes we can maketo these assumptions and what impact they have on the technical provisions.

Layout of the thesis

In Part I the background behind the ESG is discussed. Chapter 1 discusses newregulations for insurance companies, called Solvency II, are discussed, explains inmore depth what an ESG is and gives reasons for the use of ESG’s by insurers.Chapter 2 introduces some mathematical concepts which we will use throughoutthis thesis and will provide a mathematical basis upon which we will build ourstochastic models.

Part II covers the mathematical theory behind the models and the optionpricing formulas we use in the ESG. This will be done based on literature, whichwill be referred to during the chapters.

Part III is where the programmed ESG will be analysed and discussed.Chapter 8 will discuss the way in which the ESG is calibrated and provides exam-ples of the outcome of the calibration. In Chapter 10 we will have a look at thetechnical provisions corresponding to the modelled insurance products, which areexplained in Chapter 9, and in what way they are influenced by changing underly-ing conditions. Finally in Chapter 11 a summary of the thesis is given, the resultsare discussed and we look at possible improvements of the ESG.

5

Part I

Background

6

Chapter 1

General background

1.1 Solvency II

In the wake of the subprime mortgage crisis that started in 2007, in 2009 theEconomic and Financial Affairs Council, in which the Economic and Finance min-isters of the European Union are seated, approved the Solvency II Directive [44].Solvency II is a new regulatory framework for the European insurance industry.The main aims of which are to enhance policyholders protection, the stability ofthe financial system and to unify the insurance market in the EU as a whole, byestablishing harmonised solvency requirements across all member states.

In addition, the Solvency II Directive is developed to reflect new andimproved risk management standards to define capital requirements and to managerisks and it is partially a response to the previous market turmoil during thefinancial crisis of 2007-2008.

The European Insurance and Occupational Pensions Authority(EIOPA) has defined three pillars as a way of grouping the Solvency II require-ments. Pillar 2 contains the requirements for good governance and risk manage-ment of insurers and covers the supervisory activities and powers of regulators.The centerpiece of pillar 2 is the Own Risk And Solvency Assessment (ORSA),which is an internal process the insurer has to undertake to assess the adequacy ofits risk management and current and future solvency positions under normal andalso under severe stress scenarios. Pillar 3 focusses on disclosure and transparencyrequirements.

Pillar 1 covers all the quantative requirements that insurers must satisfyto demonstrate that they have sufficient capital resources. It requires that an in-surance firm must maintain technical provisions against liabilities and it definestwo capital requirements: the Minimal Capital Requirement (MCR) and the Sol-vency Capital Requirement (SCR). The MCR is set as a minimal level below which

7

financial resources should never fall. It is a trigger for regulatory intervention. TheSCR is the amount of capital an insurance company should hold under Solvency IIand it corresponds to the Value-at-Risk (VAR) of the own funds of an insurer setat a confidence level of 99, 5% over a one year period. This can be interpreted asthe requirement that only once in 200 years a company won’t have enough fundsto meet their obligations.

Initially the Solvency II directive was meant to become effective January1, 2013. However due to delays the implementation of Solvency II is postponed atleast until January 1, 2014. A reason for this is that the negotiations about theOmnibus-2 guideline have come to a halt and will resume in the second half of2013. Omnibus-2 discusses the transition measures that have to be taken for theimplementation of Solvency II and the role EIOPA will have as a supervisor. An-other reason is that EIOPA has issued an impact study, the Long Term GuaranteeAssessment (LTGA), at the beginning of 2013, which investigates the impact ofSolvency II on long term insurance products. It can be expected that followingthe conclusion of the LTGA further adjustments to the Solvency II framework willbe made, this could lead to further postponement of the implementation.

1.2 Market Consistent Valuation

One of the requirements of the Solvency II directive is that insurance companiesvalue their assets and liabilities in a market consistent way [44]. In this section wewill look at the meaning of a market consistent valuation; we will generally followthe explanation given in [14].

Before we look at a market consistent valuation, we first have to dis-cuss deep and liquid markets. The Bank of International Settlements defines adeep market as a market where large volume transactions are possible without(drastically) affecting the market price and a liquid market as a market whereparticipants can execute large volume transactions rapidly with a small impacton market prices. In such a market buyers and sellers constantly trade and theobserved market price emerges as a consensus opinion of the asset’s value.

It is important to note that the observed market price cannot be identifiedwith the objective values of the traded objects. Sometimes the market can over-or undervalue an object; an example of an overvaluation is the ’dot-com’ bubble atthe end of the twentieth century in which the stock value of internet companies andrelated companies rose rapidly, causing a large overvaluation of these companies[42].

However, market prices have some attractive properties that make themvery suitable for assessing the value of an asset. Firstly, they react quickly tochanges in relevant information. Secondly, the values are additive; the price of two

8

securities is the sum of the prices. Thirdly, the price does not depend on who orwhat is the buyer or the seller. And finally, at any given moment the market priceis unique.

When a market is no longer deep or liquid the uniqueness property is lost.Since the number of transactions and the total volume of transactions in such asituation is low, there is uncertainty about the market price at any given pointin time. In stock markets this is reflected in the form of a large bid-offer spread,which is the difference between the prices for which an asset can be sold and forwhich an asset can be bought.

As can be expected, not all markets are deep and liquid. In fact, thenumber of stocks and bonds that are liquidly traded is very small compared to thenumber of bonds and stocks that you can trade in. Moreover, most assets aren’teven traded in such a manner, e.g. insurance liabilities. So a priori there seems tobe no market consistent value for an insurance liability, since there is no deep andliquid market for these liabilities. We could ask ourselves the question what a fairvalue for these liabilities is at a given point in time.

The definition for a market consistent value we will adopt here is thefollowing from [31].

A market consistent value of an asset or liability is its market value, if it isreadily traded in a deep and liquid market at the point in time that the valuation

is struck. For any other asset or liability, a market consistent value is a bestestimate of what its market value would have been had it been traded in a deep

and liquid market.

For an insurance liability the goal of the market consistent valuation is to transferthe valuation problem into a setting where we have reliable and useful marketprices.

The present value of the liabilities of a insurance company are often alsoreferred to as the technical provisions. This is the amount of money an insurancecompany has to maintain to meet its expected obligations.

An insurance liability is defined by its resulting future cash flows. Thesecash flows can depend on claims, expenses, changes in the environment and otherrandom events. It can even be argued that some cash flows also depend on theparticular insurer holding the liability, e.g. the financial strength and profitabilityof a company can be part of the agreement.

Thus, to value an insurance liability the cash flows associated to it haveto be determined and subsequently the cash flows have to be replicated by usingcash flows of deeply traded financial instruments as good as possible. For cashflows that cannot be replicated or only partially, a risk margin has to be taken.For example a cash flow that depends on the value of the value of some underlying

9

portfolio of stocks and bonds can be replicated perfectly in general, while a cashflow in which mortality rates are a factor might not be entirely replicable andtherefore a risk margin has to be taken.

In this thesis we concern ourselves with the replicable parts of the futurecash flows.

1.3 Economic Scenario Generator

There are several methods insurers can use to calculate the technical provisions ina market consistent way. One of the most intuitive ways to replicate cash flows,using deeply traded financial instruments, might be to construct a replicatingportfolio. Another efficient way would be to use a closed-form solution to calculatethe market consistent value. However, in practice it turns out that both methodsare often hard to implement because of technical issues, the most important ofwhich is that most insurance contracts contain options that are path-dependentand have high dimensions [44]. Here path-dependent means that the cash flowsdepend on the way in which the underlying asset value moves during the lifetimeof the policy, not just on what asset value is achieved at the end of the contract.High dimensionality means that the various cash flows depend on many underlyingrisk factors. In these cases it is often hard to find a good replicating portfolio orto derive a closed-form solution and every different insurance contract would needa different replicating portfolio resp. closed-form solution. Therefore, it is moreconvenient to look for other methods that are easier to implement. Currently oneof the most used methods to value insurance liabilities is using a so called economicscenario generator (ESG). We will now discuss what an ESG is and why it can beused for market consistent valuations.

Using an ESG is a simulation based approach to valuation. By usingMonte Carlo simulation and various stochastic models, future scenarios are gen-erated. The aim is to model the underlying risk factors of the insurance contractsas good as possible. Subsequently, after the scenarios are generated, they can beused to backward calculate the present value of the insurance liabilities.

An essential feature of the stochastic models and subsequently the gen-erated scenario is that they have to be risk-neutral. This is because the firstfundamental theorem of asset pricing implies that if we want to price a claim in away that avoids arbitrage then this should be done by calculating the expectationin a risk-neutral setting. In the case of a Monte Carlo simulation this means wehave to take the average value of what the price of the claim would be under eachindividual scenario, when the scenarios are generated in a risk-neutral way.

Worthy of addressing here is the fact that even though we generate a setof scenarios in a risk-neutral way, each individual scenario can be considered to be

10

a real world scenario. The difference between risk-neutral scenarios and real worldscenario is not the paths themselves. If a path is possible in a real world settingit is also possible in a risk-neutral setting and vice-versa. The difference is in theprobability of these scenarios occurring or more correctly the distribution of thescenarios [22].

As we noted above we would like the ESG to simulate the underlyingrisk factors of the insurance liabilities. There is a large variety of risk factors towhich the cash flows can be sensitive. For example interest rates, inflation, creditspreads, equity movements, real estate prices and exchange rates. Therefore, foran ESG to be market consistent it needs to be able to reproduce the current pricesof deep and liquidly traded assets related to these risk factors, e.g. it needs to beable to reproduce the prices of options on equity as good as possible.

There a two ways in which the model can be calibrated in a market con-sistent way. The first way is to match the model prices as good as possible to themarket prices; this is usually done in a least squares sense. The second way isto calibrate the model to historical data, e.g. historical volatility of a certain riskfactor.

The former method is the preferred one where liquidly traded assets areavailable, since this method reproduces the current market prices best. However,sometimes prices of claims related to a specific risk factor aren’t available or themarket for these claims is not deep and liquid. In these cases the latter calibrationmethod has to be used.

Sometimes the two methods can be combined. Life insurance liabilitiesoften stretch far into the future and claims with such long maturities generallyaren’t available on the market. For example the implied volatility surface of optionson equity can be extrapolated based on long time historical volatilities beforecalibrating the model to market prices.

11

Chapter 2

Technical background

This chapter provides some of the basic concepts that we will use throughout thisthesis. For a more complete introduction into portfolio theory and option pricingsee [4].

First, let us denote the stochastic processes, which correspond to valueprocesses of the financial instruments we want to model, by Y = (Y1, ..., Ym); lateron in this thesis we will change the notation to reflect the type of asset we aremodelling, e.g. equity will be denoted by S.

Let us assume we have a probability space (Ω,F ,P) on which Y is de-fined and let the filtration F = Ft = σ(Y (s) : 0 ≤ s ≤ t)|t ≥ 0 satisfy the usualconditions.

As was mentioned in Section 1.3, we want to generate risk-neutral scenar-ios. Therefore we want the dynamics of our models to operate under a risk-neutralmeasure in stead of the real world measure P. Hence, we assume the existance ofan equivalent martingale measure (EMM), or risk-neutral measure, Q, with respectto the numeraire B(t), which is called the money account and will be defined inDefinition 2.8. The dynamics of the stochastic models in this thesis will be givenunder the risk-neutral measure Q.

Portfolios and contingent claims

As we mentioned in the introduction of the thesis, we want to calibrate our modelsto options. To derive analytic formulas for these options we need to introduce somedefinitions and assumptions about the market. Before we introduce this definitions,we remind ourselves that a stochastic process X = X(ω, t) is a progressivelymeasurable process if Ω × [0, t] 3 (ω, s) → X(ω, s) is Ft

⊗B[0, t]-measurable for

all t ≥ 0.

Definition 2.1. Suppose we have an n-dimensional F-adapted price process Z =(Z1, .., Zn). Then

12

• a portfolio is any n-dimensional progressively measurable process h = h(t) :t ≥ 0.

• the value process Πh corresponding to the portfolio h is given by

Πh(t) =n∑i=1

hi(t)Zi(t).

• a portfolio h is called self-financing if the value process Πh satisfies the con-dition

dΠh(t) =n∑i=1

hi(t)dZi(t).

One of the main assumptions throughout this thesis is that the market is arbitragefree. This is in fact implied by the existence of a risk-neutral measure Q, which weassumed at the beginning of this technical introduction. However, it is still usefulto recall the definition of an arbitrage opportunity.

Definition 2.2. An arbitrage opportunities in a market is a self-financing portfolioh such that

Πh(0) = 0,

P(Πh(T ) ≥ 0) = 1,

P(Πh(T ) > 0) > 0.

A (European) call option X is a contract that is defined on the price Zi of someunderlying asset at a specified maturity time T and with a strike price K. At timeT the value of the call option is given by

ΠX(T ) = max(Zi −K, 0).

More general, a contract which is completely defined in terms of one or more under-lying assets is called a contingent claim or derivative; the mathematical definitionis given below.

Definition 2.3. A random variable X is called a contingent claim with maturityT or T-claim if it is FT -measurable. The corresponding price process is denotedby ΠX(t) for 0 ≤ t ≤ T , where ΠX(T ) = X P-a.s..

We would like the contingent claims to have a unique price, therefore we need thenext definition of attainability and the following proposition.

13

Definition 2.4. We say that a T-claim X is attainable, if there exists a self-financing portfolio h such that

Πh(T ) = X, P-a.s..

In this case we call h a replicating portfolio for X.

Proposition 2.5. Suppose that the T-claim X is attainable and let h be a repli-cating portfolio for X. Then the only price process ΠX(t) which is consistent withthe no arbitrage assumption is given by ΠX(t) = Πh(t). Furthermore, if g is alsoa replicating portfolio for X, then Πh(t) = Πg(t).

Proof. Suppose at some time t we have ΠX(t) < Πh(t) then we can make anarbitrage by selling the portfolio h and buying the claim X; vice-versa for ΠX(t) >Πh(t). The same argument can also be used to show that Πh(t) = Πg(t) under theno arbitrage assumption.

Bonds, interest rates and swaptions

The interest rate model plays an important role in the ESG and we will see var-ious types of interest rates and assets based on interest rates during this thesis.Therefore, these are introduced here.

The most basic, to interest rates related, asset is a zero-coupon bond,which is defined as follows.

Definition 2.6. A maturity T zero coupon bond or T -bond is a contract ensuringthe holder one unit of currency, e.g. one euro, at time T . The price of the bond attime t is denoted by P (t, T ), for 0 ≤ t ≤ T .

Based on the definition of a zero-coupon bond we can define some different typesof interest rates.

Definition 2.7. • The simple forward rate for [T, S] at time t is given by

F (t, T, S) =1

S − T

(P (t, T )

P (t, S)− 1

).

• The simple spot rate for [t, T ] is

F (t, T ) =1

T − t

(1

P (t, T )− 1

).

• The continuously compounded forward rate for [T, S] at time t is given by

R(t, T, S) = − logP (t, S)− logP (t, T )

S − T.

14

• The instantaneous forward rate with maturity T at time t is defined as

f(t, T ) = limS↓T

R(t, T, S) = −∂ logP (t, T )

T − t

• The (instantaneous) short rate at time t is defined by

r(t) = f(t, t)

With this definition we can define the money account B(t).

Definition 2.8. The money account is defined by the dynamics

dB(t) = r(t)B(t)dt, B(0) = 1,

or equivalently

B(t) = exp

(∫ t

0

r(u)du

).

It can be interpreted as a bank account in which the profits are continuouslycompounded at the prevailing short rate of interest.

Since we want to calibrate our interest rate model to swaptions, we need to definewhat an interest rate swap is and what a swaption is, but before we do this wewill define a coupon bond.

Definition 2.9. A coupon bond is a contract specified by a number of futuredates T0 < T1 < T2 < ... < Tn, a sequence of coupons c1, .., cn and a nominal valueN , such that the owner receives ci at Ti for i = 1, ..., n and receives N at timeTn. The coupons can either be some fixed amount or floating, in which case thecoupons are determined at Ti−1 as ci = (Ti − Ti−1)F (Ti−1, Ti)N . Here F (Ti−1, Ti)is the simple spot rate defined in Definition 2.7.

It is not hard to determine the t ≤ T0 price of ci. In the fixed coupon case we canbuy ci P (t, Ti) bonds to get a payoff of ci at Ti. Therefore the t ≤ T0 price of ci isciP (t, Ti). For the floating case we first have to note that, from the definition ofF (Ti−1, Ti) we have at Ti

ci =1

P (Ti−1, Ti)− 1.

At time t the value of getting −1 at Ti is −P (t, Ti). The time t ≤ T0 value of1

P (Ti−1,Ti)is P (t, Ti−1), since if we buy at t a Ti−1-bond for P (t, Ti−1), we get 1 paid

15

out at Ti−1 and we can use this to buy 1P (Ti−1,Ti)

Ti-bonds. Therefore the time

t ≤ T0 value of ci is

P (t, Ti−1)− P (t, Ti). (2.1)

An interest rate swap is a contract in which floating rate interest payments areexchanged for fixed rate interest payments. We can see this as an agreementbetween two parties in which one party has a coupon bond which pays a fixedinterest rate and the other party has a coupon bond which pays a floating rate.The two parties then decide to exchange the coupons they receive for some periodof time, without exchanging the underlying bonds.

Definition 2.10. A payer interest rate swap settled in arrears is a contract whichis defined as follows. There are a number of future dates T1, T2, ..., Tn with usuallyTi−Ti−1 = δ, a fixed rate K and a nominal value N . At dates T1, ..., Tn the ownerof the contract pays KδN and receives floating F (Ti−1, Ti)δN .

At time Ti the net cash flow is equal to

Nδ(F (Ti−1, Ti)−K),

for which, by using the result we derived in (2.1), the t ≤ T0 value can be computedas

N(P (t, Ti−1)− P (t, Ti)−KδP (t, Ti)).

Now we can compute the t ≤ T0 value of the payer swap by summing over i =1, ..., n:

Πp(t) = N

(P (t, T0)− P (t, Tn)−Kδ

n∑i=1

P (t, Ti)

). (2.2)

A receiver interest rate swap is a swap in which the holder pays a floating rateand receives a fixed rate. Note that in this case the signs of the cash flows aboveare changed and as a consequence its t ≤ T0 value is Πr(t) = −Πp(t).

The remaining question now is how the swap rate K is determined. Bydefinition it is chosen such that at the time the contract is written, the value ofthe swap equals zero.

Definition 2.11. The forward swap rate at time t ≤ T0 is the fixed rate whichgives Πp(t) = −Πr(t) = 0 and is denoted by Rswap(t)

We thus get

Rswap(t) =P (t, T0)− P (t, Tn)

δ∑n

i=1 P (t, Ti).

16

We can use this equation to rewrite (2.2) to

Πp(t) = Nδ(Rswap(t)−K)n∑i=1

P (t, Ti). (2.3)

Now we can define a (payer) swaption, which is an option on a payer swap.

Definition 2.12. A payer swaption with strike rate K is a contract which givesthe owner the right at maturity date T (but not the obligation) to enter into apayer swap with fixed rate K. Usually the maturity date is set to coincide withthe first reset date of the onderlying swap, i.e. T = T0.

An equivalent definition can be given for a receiver swaption. If we use(2.3) for t = T0 we can see that the T0 payoff of the payer swaption is equal to

Nδ(Rswap(T0)−K)+n∑i=1

P (T0, Ti) (2.4)

The market prices of swaptions are given in terms of swaption volatilities thatare derived from Black’s formula for swaptions. Therefore we will need Black’sformula to calculate the market prices.

Theorem 2.13 (Black’s Formula for Swaptions). Black’s formula for the t ≤ T0price of a payer swaption is given by

Nδ(Rswap(t)Φ(d1(t))−KΦ(d2(t)))n∑i=1

P (t, Ti),

where

d1(t) =log(Rswap(t)

K) + 1

2σ(t)2(T0 − t)

σ(t)√T0 − t

,

d2(t) = d1 − σ(t)√T0 − t.

Here Φ denotes the standard normal distribution function. σ(t) is known as Black’sswaption volatility.

A justification for Black’s formula can be found in Appendix A.

17

Part II

Theory

18

Chapter 3

The interest rate model

In this chapter we will discuss the interest rate model we will use in our ESG. Wewant to calibrate our model to market prices of at-the-money swaptions. Therefore,we will derive an explicit formula for the price of a swaption under the chosen Hull-White model.

The Hull-White model is a short rate model, it defines the dynamics ofthe short rate. Short rate models were the earliest stochastic short rate models.The relation between the bond prices P (t, T ) and the short rate can be derivedfrom the time t value of P (T, T ) = 1. That is,

P (t, T ) = B(t)EQ[

1

B(T )

∣∣∣∣Ft]= EQ

[e−

∫ Tt r(s)ds

∣∣∣Ft] .The need for an arbitrage free model let Hull and White [24] to an extension of theVasicek model [45], which can be described by the stochastic differential equation:

dr(t) = λ(µ− r(t))dt+ σdW (t), r(0) = r0.

The Vasicek model on it’s own is a arbitrage free model, however when used in areal market situation an exact fit of the model to the market term structure is notpossible in general. Hence, bond options and other derivatives priced under theVasicek model would not be consistent with the market prices of bonds and wouldtherefore lead to arbitrage opportunities.

The extension of Hull and White allows for an arbitrage free calibrationsince it is possible get an exact fit to the currently observed term structure ofinterest rates. Under the risk-neutral measure Q, with the money market accountas numeraire, the dynamics of r(t) under the Hull-White extended Vasicek model

19

are described by

dr(t) = (θ(t)− a(t)r(t))dt+ σ(t)dW (t), r(0) = r0.

Not only can this model be fitted to the term structure with the θ(t) term, itcan also give an exact fit to the spot or forward volatilities with the σ(t) term.However, these high degrees of freedom make the model hard to handle analyticallyin general. Since we want to fit observed market prices of swaptions to modelprices in order to calibrate the ESG, it is convenient if we can derive an analyticalformula for the swaption prices under te model. Therefore we restrict ourselvesto the model known as the Hull-White one factor model [25], where a(t) = a andσ(t) = σ are constants in stead of functions of time. Thus, the dynamics of theHull-White one factor model are given by:

dr(t) = (θ(t)− ar(t))dt+ σdW (t), r(0) = r0. (3.1)

An exact fit to the volatility term structure is not possible anymore in this model,but we are still able to exactly fit the term structure and we now can derive ananalytic formula for the price of a swaption. Moreover, one of the great strengthsof this model is that we can also derive analytical formula’s for put and call optionson equity under Hull-White interest rates.

We will proceed as follows. First we will deduce an explicit formula forthe price of a bond P (t, T ) under the model and subsequently we will use it to geta formula for the price of a European option on a bond. This formula, togetherwith the so called Jamshidian’s trick [27], will get us the formula for the price ofa swaption under the Hull-White model.

3.1 The bond price

The first step to deriving a formula for the price of a bond is by analysing thesolution of the Hull-White SDE (3.1).

Proposition 3.1. The solution to the short rate dynamics in the Hull-White modelis given by

r(t) = e−a(t−s)(r(s) +

∫ t

s

θ(u)eaudu+ σ

∫ t

s

eaudW (u)

). (3.2)

Proof. The result can be verified by applying the Ito-formula to (3.2).

20

From this result it follows that r(t), conditional on Fs, is Gaussian withconditional expectation and conditional variance

E [r(t)|Fs] = e−a(t−s)(r(s) +

∫ t

s

θ(u)eaudu

),

Var [r(t)|Fs] = E[(σe−a(t−s)

∫ t

s

eaudW (u))2∣∣∣∣Fs]

= E[σ2e−2a(t−s)

∫ t

s

e2audu

∣∣∣∣Fs]=σ2e2as

2a

(1− e−2a(t−s)

).

Here we have used the Ito isometry to calculate the variance. Recall that (underour risk-neutral measure Q) we can represent bond prices as

P (t, T ) = EQ[e−∫ Tt r(s)ds|Ft

]Since r(t) is a Gaussian process, one can show that

∫ Ttr(s)ds is normally dis-

tributed, which means the bond price is an expectation of a lognormal distributionand of the form

P (t, T ) = exp

(E[−

∫ T

t

r(s)ds] +1

2Var[−

∫ T

t

r(s)ds]

). (3.3)

Now we remind ourselves that (3.1) is just a short hand notation for

r(t) = r0 +

∫ t

0

θ(s)ds− a∫ t

0

r(s)ds+

∫ t

0

σdW (s).

By rearranging terms and taking the expectation on both sides we get that

E[

∫ t

0

r(s)ds] =r0a

+1

a

∫ t

0

θ(s)ds− 1

aE[r(t)]

=r0a

+1

a

∫ t

0

θ(s)ds− e−at

a

(r0 +

∫ t

0

θ(s)easds

)=r0a

(1− e−at) +1

a

∫ t

0

θ(s)(1− ea(s−t))ds.

Moreover, from (3.2) we can derive

Cov[r(t), r(u)] = σ2e−a(t+u)E[

∫ t

0

easdW (s)

∫ u

0

easdW (s)]

= σ2e−a(t+u)∫ t∧u

0

e2asds

=σ2

2ae−a(t+u)(e2a(t∧u) − 1),

21

where we have made use of the Ito isometry and the independence of disjointBrownian increments. We can use this formula to calculate the variance

Var[

∫ t

0

r(s)ds] = E[(

∫ t

0

r(s)ds− E[

∫ t

0

r(s)ds])2]

=

∫ t

0

∫ t

0

E[(r(s)− E[r(s)])(r(u)− E[r(u)])]ds du

=

∫ t

0

∫ t

0

Cov[r(s), r(u)]ds du

=

∫ t

0

∫ t

0

σ2

2ae−a(t+u)(e2a(t∧u) − 1)ds du

=σ2

2a3(2at− 3 + 4e−at − e−2at).

For notational convenience, let us now define

B(t, T ) =1

a(1− e−a(T−t)) (3.4)

and insert the results in (3.3). Then

P (t, T ) = exp

(−r(t)

a(1− e−a(T−t))− 1

a

∫ T

t

θ(s)(1− ea(s−t))ds

+σ2

2a3(a(T − t)− 3

2+ 2e−a(T−t) − 1

2e−2a(T−t))

)= exp

(−r(t)B(t, T )−

∫ T

t

θ(s)B(T, s)ds

+σ2

2a2

∫ T

t

1− 2e−a(T−s) + e−2a(T−s)ds

)= exp

(−r(t)B(t, T )−

∫ T

t

θ(s)B(T, s)ds

+σ2

2

∫ T

t

B2(s, T )ds

). (3.5)

The function θ(t) gives us the opportunity to fit the theoretical bond prices tothe market prices. It follows from the definition of the instantaneous forward ratef(t, T ) = −∂log(P (t,T ))

∂Tthat

P (t, T ) = e−∫ Tt f(t,s)ds,

22

which implies there is a one-to-one correspondance between bond prices P (0, T ) | T >0 and the forward rate curve f(0, T ) | T > 0. Because of convenience we chooseto fit the forward rate curve to our model, which results in

f(0, T ) = − ∂

∂Tlog(P (0, T ))

=∂

∂TB(t, T )r0 +

σ2

2

∫ T

0

∂

∂TB2(s, T )ds−

∫ T

0

θ(s)∂

∂TB(s, T )ds

= e−aT r0 −σ2

2a

(1− e−aT

)2+

∫ T

0

θ(s)e−a(T−s)ds.

Here we implicitly used the fact that ∂∂TB(s, T ) = − ∂

∂sB(s, T ) to get the last

expression. We can solve the last equation for θ(t) by writing

f(0, T ) = y(T )− g(T ),

where

g(T ) =σ2

2a

(1− e−aT

)2and

y(T ) = e−aT r0 +

∫ T

0

θ(s)e−a(T−s)ds

= E [r(t)]

We can describe y(T ) = E [r(T )] by the ordinary differential equation

d

dty(t) = −ax(t) + θ(t), y(0) = r(0).

This leads us to the following expression for θ(t)

θ(t) =d

dty(t) + ay(t)

=d

dtf(0, t) +

d

dtg(t) + a (f(0, t) + g(t))

=d

dtf(0, t) + af(0, t) +

σ2

2a

(1− e−2at

). (3.6)

Now we can insert θ(t) into (3.5) and, skipping some tedious calculations, we arriveat the following result

23

Proposition 3.2. Under the Hull-White short rate model, with θ(t) chosen suchthat theoretical forward rate curve matches the observed forward rate curve, thetheoretical bond price is given by

P (t, T ) =P (0, T )

P (0, t)exp

(B(t, T )f(0, t)− σ2

4aB2(t, T )

(1− e−2at

)−B(t, T )r(t)

),

(3.7)where B(t, T ) is given by (3.4).

3.1.1 Alternative representation of the short rate

Equation (3.6) gives us the means to derive an alternative representation for theshort rate r(t). This representation will be used in the next chapter, in which theequity model is discussed, and it will also be used for the simulation of the shortrate.

Let us look at (3.2) again and insert (3.6) for θ(t). This results in

r(t) = f(0, t) +σ2

2a2(1− e−at)2 + σ

∫ t

0

e−a(t−s)dW (s).

Now we can write the short rate as r(t) = x(t) + φ(t) where

φ(t) = f(0, t) +σ2

2a2(1− e−at)2 and

x(t) = σ

∫ t

0

e−a(t−s)dW (s).

Here is φ(t) the deterministic part of the short rate and x(t) is a solution to

dx(t) = −ax(t)dt+ σdW (t), x(0) = 0. (3.8)

3.2 Bond option

In this section we will derive an analytic formula for the price of an option on azero coupon bond. First we take a look at a general option pricing formula whichwe will derive by using a change of measure technique. Here, for the most part,we will follow the arguments presented by German et al (1995) [21]. Afterwardsthe formula is applied to the Hull-White setting.

From the first fundamental theorem of asset pricing we know that a marketis arbitrage free if and only if there exists a (local) equivalent martingale measure

24

Q.1 Moreover, if the market is also complete or a contingent claim is attainable,we know it has a unique arbitrage free price, which we can calculate by takingthe expectation of the discounted claim under the risk-neutral measure. Whatwe should realize, however, is that this is a risk-neutral measure or EMM onlyrelative to a chosen numeraire. The classical choice for this numeraire is themoney account B(t) = e

∫ t0 r(s)ds. In fact, we have assumed that the dynamics of

our short-rate model are under the EMM with B as numeraire. However, we couldimagine that, under stochastic interest rates, the money account is not the mostconvenient choice for a numeraire. Suppose, for example, we have a T -claim X,then the price of X at t = 0 is given by

ΠX(0) = EQ[X(T )

B(T )

]= EQ

[e−∫ T0 r(t)dtX(T )

]. (3.9)

Since we’re dealing with stochastic interest rates, we would need to consider thejoint distribution of X and B and integrate with respect to that distribution. Thiscan turn out to be rather hard work. We might want to consider an alternative

numeraire. Because P (0, T ) = EQ[e−∫ T0 r(t)dt], which is observable in the market,

P (t, T ) might be a good choice of numeraire, therefore we introduce a new measurecorresponding to this numeraire.

Definition 3.3. T -forward measure For some fixed time T > 0 the T -forwardmeasure QT is the equivalent martingale measure for the numeraire P (t, T ).

As we will see in Corollary 3.5 the fair value of X at t = 0 can be calculated as

ΠX(0) = P (0, T )EQT [X(T )] ,

which looks more manageable than the expectation in (3.9).The first objective now is to find what the corresponding Girsanov-transformation

is when we change from Q to QT .To prove the following proposition, we need a result on conditional expec-

tations known as the Abstract Bayes’ Formula, which is given in Appendix B.

Proposition 3.4. If Q is the risk-neutral measure relative to the money accountB, then the likelihood process

LT (t) =dQT

dQ

∣∣∣Ft, 0 ≤ t ≤ T

1In fact this is not completely true in a continuous time setting, where we need a strongerconcept as ’no free lunch with vanishing risk’ to replace the arbitrage free condition. For more in-formation on this subject see Bjork [4] or the more technical paper of Delbaen and Schachermayer[12].

25

which makes QT a risk-neutral measure for numeraire P (t, T ) is given by

LT (t) =P (t, T )

P (0, T )B(t). (3.10)

Proof. For QT to be a martingale measure, we have to show that every (sufficientlyintegrable) price process X(t) normalized by P (t, T ) is a QT martingale. For sucha price process, we already know X(t)/B(t) is a Q-martingale and in particularso is LT (t). Applying the Abstract Bayes’ Formula, we can derive the requiredresult:

EQT[X(t)

P (t, T )

∣∣∣∣Fs] =EQ[LT (t) X(t)

P (t,T )

∣∣∣Fs]EQ [LT (t)|Fs]

=EQ[

P (t,T )P (0,T )B(t)

· X(t)P (t,T )

∣∣∣Fs]LT (s)

=

1P (0,T )

EQ[X(t)B(t)

∣∣∣Fs]LT (s)

=

1P (0,T )

· X(s)B(s)

LT (s)=

X(s)

P (s, T ).

Corollary 3.5. Let X be a T -claim s.t. EQ[|X|B(T )

]<∞, then

EQT [|X|] <∞

and the price of X under QT at time t is given by

ΠX(t) = P (t, T )EQT [X|Ft] .

Proof. Both follow from Proposition 3.4, since

EQT [|X|] = EQ [LT (T ) · |X|]

= EQ[

|X|P (0, T )B(T )

]<∞

and using Bayes’ Formula and the fact that B(t)P (t,T )

is a martingale under QT

ΠX(t) = B(t)EQ[

X

B(T )

∣∣∣∣Ft] = B(t)EQT

[1

LT (T )· XB(T )

∣∣∣Ft]EQT

[1

LT (T )

∣∣∣Ft]= P (t, T )EQT [X|Ft] .

26

Proposition 3.6. Suppose the Q-dynamics of a T -bond are of the form

dP (t, T ) = r(t)P (t, T )dt+ v(t, T )P (t, T )dW (t),

where W is a Q-Brownian Motion, then the dynamics of LT are given by

dLT (t) = v(t, T )LT (t)dW (t)

and as a consequence the dynamics of W under QT are given by

dW (t) = v(t, T )dt+ dW T (t)

where W T is a QT -Brownian Motion.

Proof. Remembering that dB(t) = r(t)B(t)dt, the first result follows from apply-ing the Ito formula to LT (t) (3.10) and the second result follows from applying theGirsanov Theorem, see for example [4].

We can use the change of measure to derive a general formula for pricing Europeancall option X with strike K maturing at time T on an S-bond with S > T . Thetime T value of X is thus

X = max (P (T, S)−K, 0) .

To ensure the existence of a unique arbitrage-free price, we assume that the optionis attainable in the sense of Definition 2.4.

Proposition 3.7. Let X be a European call option as above, then the t = 0 pricecan be written as

ΠX(0) = P (0, T )EQT[(

P (T, S)

P (T, T )−K

)+]

or

ΠX(0) = P (0, S)QS (P (T, S) > K)−KP (0, T )QT (P (T, S) > K). (3.11)

Here QS denotes the S-forward measure corresponding to numeraire P (t, S).

Proof. The first expression is a direct result from Corollary 3.5. The second resultfollows from using an indicator function and changing the measure as follows

EQ[

(P (T, S)−K)+

B(T )

]= EQ

[P (T, S)

B(T )1P (T,S)>K

]−KEQ

[1

B(T )1P (T,S)>K

]= P (0, S)EQS

[P (0, S)B(T )

P (T, S)· P (T, S)

B(T )1P (T,S)>K

]−KEQT

[P (0, T )B(T )

P (T, T )B(T )1P (T,S)>K

]= P (0, S)QS (P (T, S) > K)−KP (0, T )QT (P (T, S) > K) .

27

Now the task at hand is to find conditions under which we can evaluate the prob-abilities in (3.11). As it turns out, deterministic volatilities are sufficient for com-putability. So let us assume that the process

Z(t) =P (t, S)

P (t, T )for t ≤ S ∧ T

has a stochastic differential under Q of the form

dZ(t) = Z(t)µ(t)dt+ Z(t)σ(t)dW (t) for t ≤ s ∧ t, (3.12)

where σ(t) is deterministic (and µ(t) is sufficiently integrable). Note that Z isa QT -martingale and since the volatility process is unaffected by a Girsanov-transformation the dynamics of Z(t) are

dZ(t) = Z(t)σ(t)dW T (t)

under QT . Moreover, by applying the Ito-formula we can see that an explicitsolution is given by

Z(t) =P (0, S)

P (0, T )exp

(−1

2

∫ t

0

σ2(s)ds+

∫ t

0

σ(s)dW T (s)

).

The exponent has a normal distribution with variance

Σ2(T ) =

∫ T

0

σ2(t)dt

and we see that Z(T ) has a lognormal distribution. This leads us to the followingcalculation for the second probability in (3.11)

QT (P (T, S) > K) = QT

(P (T, S)

P (T, T )> K

)= QT (Z(T ) > K)

= Φ

log(

P (0,S)KP (0,T )

)− 1

2Σ2(T )√

Σ2(T )

=: Φ(d2),

where Φ is the cumulative distribution function of a standard normal randomvariable. Now the first probability in (3.11) is calculated in a similar fashion.First note that

QS (P (T, S) > K) = QS

(P (T, T )

P (T, S)<

1

K

)= QS

(Y (T ) <

1

K

).

28

So Y (t) = P (t,T )P (t,S)

= 1Z(t)

and it is a martingale under QS. Applying the Ito-formula

to 1Z(t)

results in

Y (t) =P (0, T )

P (0, S)exp

(−1

2

∫ t

0

σ2(s)ds−∫ t

0

σ(s)dW T (s)

),

andQS (P (T, S) > K) = Φ

(d2 +

√Σ2(T )

)=: Φ(d1)

3.2.1 Bond option under the Hull-White model

We want to apply the general bond option formula we derived in the previoussection to the Hull-White model. Therefore we need to check if the assumptionswe made in the derivation of the option formula are compatible with the Hull-White model. That is, we need to check if Z(t) = P (t,S)

P (t,T )has an SDE of the form

(3.12) where σ(t) is deterministic. From the explicit formula we derived for thebond price P (t, T ), equation (3.7), we can write Z(t) in the form

Z(t) = exp (A(t, S)− A(t, T )− (B(t, S)−B(t, T ))r(t)) ,

where

A(t, T ) = B(t, T )f(0, t)− σ2

4aB2(t, T )

(1− e−2at

).

Applying the Ito-formula gives us the dynamics of Z(t), which are of the form

dZ(t) = Z(t)(. . . )dt− Z(t)σ [B(t, S)−B(t, T )] dW (t),

where−σ [B(t, S)−B(t, T )] =

σ

aeat[e−aS − e−aT

]=: σ(t).

Thus σ(t) is deterministic and we can apply the previous results to get

Proposition 3.8. Hull-White bond option In our (restricted) Hull-Whitemodel, the price of a put option at time t ≤ T , with strike K and maturity Ton a zero-coupon bond maturing at S, is given by

ZBp(t, T, S,K) = KP (t, T )Φ(d1)− P (t, S)Φ(d2),

where

d1 =ln(KP (t,T )P (t,S)

)+ 1

2Σ2

√Σ2

d2 =√

Σ2 − d1

Σ2 =σ2

2a3(1− e2a(T−t)

) (1− e−a(S−T )

)2.

29

The swaption formula

We want to configure our model to swaption prices, so we still need to find anexplicit formula for swaptions. As it turns out, because of a clever trick developedby Jamshidian in 1989 [27], it possible for us to write a swaption as a portfolio ofput options on bonds.

Proposition 3.9. Let the definition of a swaps and a swaption be as in Defini-tion 2.10 and Definition 2.12. Then, under the Hull-white short rate model, theprice of a payer swaption strike K at time t ≤ T0 is given by

Swaptp(t, T0, T1, ..., Tn, N,K) = N

(ZBp(t, T0, Tn, Kn) +Kδ

n∑i=1

ZBp(t, T0, Ti, Ki)

),

whereKi = P (T0, Ti; r

∗)

and ZBp is given by Proposition 3.8.

Proof. Recall the formula for the price of a swap (2.2), which leads to the followingT0 value of a swaption

Π(T0) = N

(1− P (T0, Tn)−Kδ

n∑i=1

P (T0, Ti)

)+

. (3.13)

To express the dependence of the bond prices on the short rate of interest r we writeP (T0, Ti) = P (T0, Ti; r). The following two steps that finish the proof together areknown as Jamshidian’s trick. The most important observation of this trick is thatP (T0, Ti; · ) is monotone decreasing in r as we can see from (3.7). We can definer∗ as the rate for which

P (T0, Tn; r∗) +Kδ

n∑i=1

P (T0, Ti; r∗) = 1. (3.14)

Plugging this into (3.13) and using the monotonicity we get

N

((P (T0, Tn; r∗)− P (T0, Tn; r)) +Kδ

n∑i=1

(P (T0, Ti; r∗)− P (T0, Ti; r))

)+

= N(P (T0, Tn; r∗)− P (T0, Tn; r))+ +KδN

n∑i=1

(P (T0, Ti; r∗)− P (T0, Ti; r))

+.

30

Chapter 4

The equity model

In this chapter we will discuss the equity model we will use in our ESG. In agree-ment with what we did with the short rate model we want to calibrate our modelto market prices of (European) options on equity. Therefore, we will derive an ex-plicit formula for the price of an option in our model. In this chapter we basicallyfollow the derivation presented in [5].

We would like our equity model to be consistent with the stochastic shortrate we modelled in the previous chapter. Moreover, we would like our model tobe analytically tractable. We will see that both of these properties are met by theHull-White-Black-Scholes model; this is the classic Black-Scholes equity model,but with the stochastic Hull-White interest rates in stead of a constant rate. Thedynamics under Q for this equity model are thus given by

dS(t) = S(t)r(t)dt+ σSdWS(t), S(0) = S0,

where r(t) is the short rate under the Hull-White model, so

dr(t) = (θ(t)− ar(t))dt+ σrdWr(t), r(0) = r0.

Here the two Brownian motions are correlated with

d〈Wr,WS〉t = ρdt

for −1 ≤ ρ ≤ 1.

Proposition 4.1. A solution to the dynamics of the equity model is given by

S(t) = S(s) exp

(∫ t

s

r(u)du− 1

2σ2S(t− s) + σS(WS(t)−WS(s))

)(4.1)

Proof. The result can be verified by applying the Ito-formula to (4.1).

31

Because (Wr(t),Ws(t)) is a jointly Gaussian process, one can see from (4.1)that logS(t) has a normal distribution conditional on Fs and we can calculate itsconditional expectation and conditional variance. Recall that in Section 3.1.1 wesaw that we can write r(t) = x(t) + φ(t). From the SDE of x(t), equation (3.8),we can see that ∫ t

s

x(u)du =x(s)− x(t)

a+σra

∫ t

s

dWr(u)

and the explicit solution for x(t) is given by

x(t) = x(s)e−a(t−s) + σ

∫ t

s

e−a(t−u)dWr(u).

Combining the last two equations results in∫ t

s

x(u)du =1− e−a(t−s)

ax(s) +

σra

∫ t

s

(1− e−a(t−u)dWr(u).

Using the last equality, we have that

log

(S(t)

S(s)

)=

∫ t

s

r(u)du− 1

2σ2S(t− s) + σS(WS(t)−WS(s))

=1− e−a(t−s)

ax(s) + σ

∫ t

s

e−a(t−u)dWr(u) +

∫ t

s

φ(u)du

− 1

2σ2S(t− s) + σS(WS(t)−WS(s)), (4.2)

From this we can derive the conditional expectation by inserting r(s) − φ(s) forx(s) and integrating φ(t)

E[log

(S(t)

S(s)

)∣∣∣∣Fs] =1− e−a(t−s)

a

(r(s)− f(0, s)− σ2

2a2(1− e−as)2

)− 1

2σ2S(t− s) + log

(P (0, s)

P (0, t)

)+

σ2

2a2

[t− s+

2

a(e−at − e−as)− 1

2a(e−2at − e−2as)

].

We can also derive the conditional variance from equation (4.2):

Var

[log

(S(t)

S(s)

)∣∣∣∣Fs] = Var

[σ

∫ t

s

e−a(t−u)dWr(u) + σS

∫ t

s

dWS(u)

∣∣∣∣Fs]=σ2

a2

[t− s− 2

a(1− e−a(t−s)) +

1

2a(1− e−2a(t−s))

]+

1

2σ2S(t− s) + 2ρ

σrσSa

[t− s− 1

a(1− e−a(t−s))

].

32

4.1 change of measure

As in the case of the bond options, it is convenient to change the measure tothe T -forward measure if we want to derive an explicit formula for an equityoption. Since we’re dealing with two correlated Brownian motion, we have totake this correlation in to account when applying a Girsanov-transformation forthe Brownian motions. However, recall that any multivariate normal distributedrandom variable Z ∼ N(µ,Σ) can be written in the form Z = µ+L · Z where Z isa vector of independent standard normal random variables and Σ = L · L>. It istherefore easier for us to write our processes in terms of two independent Brownianmotions before we do a measure transform. Applying a Cholesky transformationleads us to

dWr(t) = dWr(t),

dWS(t) = ρdWr(t) +√

1− ρ2dWs(t)

where Wr and Ws are two independent Brownian motions and so

dr(t) = (θ(t)− ar(t))dt+ σrdWr(t),

dS(t) = S(t)r(t)dt+ S(t)σSρdWr(t) + S(t)σS√

1− ρ2dWs(t).

If we apply the Ito-formula to (3.7) we see that the dynamics of the bond priceare of the form

dP (t, T ) = P (t, T )(. . . )dt− P (t, T )σ

a

[1− e−a(T−t)

]dW (t)

and we can apply the Girsanov-transformation, which is similar to Proposition 3.6for multidimensional W . This results in two independent Brownian motions W T

r

and W Ts under the measure QT , defined by

dWr(t) = dW Tr (t)− σr

a

[1− e−a(T−t)

]dt

dWs(t) = dW Ts (t).

Hence, under the measure QT , the dynamics of r(t) and S(t) are described by

dr(t) =

(θ(t)− σ2

r

a

[1− e−a(T−t)

]− ar(t)

)dt+ σrdW

Tr (t), (4.3)

dS(t) = S(t)(r(t)− σrσSρ

a

[1− e−a(T−t)

])dt+ S(t)σSρdW

Tr (t) + S(t)σS

√1− ρ2dW T

s (t).

33

We can find solutions for these SDE’s which can be checked easily by using r(t) =x(t) + φ(t) and the Ito-formula. For all t ≤ T we have

r(t) = r(s)e−a(t−s) +

∫ t

s

θ(u)e−a(t−u)du

− σ2

a

∫ t

s

e−a(t−u)[1− e−a(T−u)

]du+ σ

∫ t

s

e−a(t−u)dW Tr (u)

= x(s)e−a(t−s) − σ2

a

∫ t

s

e−a(t−u)[1− e−a(T−u)

]du

+ σ

∫ t

s

e−a(t−u)dW Tr (u) + φ(t). (4.4)

and

S(T ) = S(t)exp

(∫ T

t

r(u)du− σrσSρ

a

∫ T

t

(1− e−a(T−u)

)du

−1

2σ2S(T − t) + σSρ

∫ T

t

dW Tr + σS

√1− ρ2

∫ T

t

dW Ts (u)

). (4.5)

From (4.3) we see that under QT we have

dx(t) = −(σ2r

a

[1− e−a(T−t)

]+ ax(t)

)dt+ σrdW

Tr (t),

which leads to∫ T

t

x(u)du =x(t)− x(T )

a− σ2

r

a2

∫ T

t

(1− e−a(T−u)

)du+ σrd

∫ T

t

W Tr (u)

and again since r(t) = x(t) + φ(t) from (4.4) we get∫ T

t

x(u)du =1− e−a(T−t)

ax(t)

− σ2r

a2

∫ T

t

(1− e−a(T−u)

)2du+

σra

∫ T

t

(1− e−a(T−u)

)dW T

r (u).

34

We can insert this into (4.5), which results in

S(T ) = S(t)exp

(1− e−a(T−t)

ax(t)− σ2

r

a2

∫ T

t

(1− e−a(T−u)

)2du

+σra

∫ T

t

(1− e−a(T−u)

)dW T

r (u) +

∫ T

t

f(0, u)du

+σ2r

2a2

∫ T

t

(1− e−au

)2du− σrσSρ

a

∫ T

t

(1− e−a(T−u)

)du

−1

2σ2S(T − t) + σSρ

∫ T

t

dW Tr (u) + σS

√1− ρ2

∫ T

t

dW Ts (u)

)Now the expectation of logS(t) conditional on Ft under QT can be calculated

EQT [log (S(T ))|Ft]

=1− e−a(T−t)

ax(t)− σ2

a2

(T − t+

2

ae−a(T−t) − 1

2ae−2a(T−t) − 3

2a

)+ log

(P (0, t)

P (0, T )

)+

σ2

2a2

(T − t+

2

a

(e−aT − e−at

)− 1

2a

(e−2aT − e−2at

))− σrσSρ

a

(T − t− 1

a

(1− e−a(T−t)

))− 1

2σ2S(T − t) + log(S(t))

=1− e−a(T−t)

ax(t)− V (t, T ) + log

(P (0, t)

P (0, T )

)+

1

2(V (0, T )− V (0, t))

− σrσSρ

a

(T − t− 1

a

(1− e−a(T−t)

))− 1

2σ2S(T − t) + log(S(t))

= B(t, T )(r(t)− φ(t))− V (t, T ) + log

(P (0, t)

P (0, T )

)+

1

2(V (0, T )− V (0, t))

− σrσSρ

a

(T − t− 1

a

(1− e−a(T−t)

))− 1

2σ2S(T − t) + log(S(t))

where

V (t, T ) :=σ2

a2

(T − t+

2

ae−a(T−t) − 1

2ae−2a(T−t) − 3

2a

).

By applying the bond price formula (3.7) to the last equation, we arrive at thefollowing result:

EQT [log (S(T ))|Ft] = log

(S(t)

P (t, T )

)− σrσSρ

a

(T − t− 1

a

(1− e−a(T−t)

))− 1

2σ2S(T − t)− 1

2V (t, T ) := m(t, T ). (4.6)

35

For the variance we get the following

VarQT

[log (S(T ))|Ft] = VarQT

[σra

∫ T

t

(1− e−a(T−u)

)dW T

r (u)

+σSρ

∫ T

t

dW Tr (u) + σS

√1− ρ2

∫ T

t

dW Ts (u)

∣∣∣∣Ft]= V (t, T ) + σ2

S(T − t)

+ 2σrσSρ

a

(T − t− 1

a

(1− e−a(T−t)

))=: v2(t, T ) (4.7)

Proposition 4.2. The price at time t for a European call option X with maturityT and strike K under the Black-Scholes-Hull-White model is given by

ΠX(t) = S(t)Φ

log(

S(t)KP (t,T )

)+ 1

2v2(t, T )√

v2(t, T )

−KP (t, T )Φ

log(

S(t)KP (t,T )

)− 1

2v2(t, T )√

v2(t, T )

Proof. From Corollary 3.5 we know that

ΠX(t) = P (t, T )EQT [(S(T )−K)+∣∣Ft] .

Since S(T ) has a lognormal distribution this expectation can be calculated asfollows:

EQT [(S(T )−K)+∣∣Ft] =

∫ ∞−∞

(ex −K)+√2πv2(t, T )

e− 1

2x−m(t,T )

v2(t,T ) dx

=

∫ ∞log(K)

(ex −K)√2πv2(t, T )

e− 1

2x−m(t,T )2

v2(t,T ) dx

=

∫ ∞log(K)−m(t,T )√

v2(t,T )

(em(t,T )+v2(t,T )y −K)√2π

e−12z2dz

= em(t,T )+ 12v2(t,T )

∫ ∞log(K)−m(t,T )√

v2(t,T )

1√2πe−

12(z−√v2(t,T ))2dz

−K∫ ∞

log(K)−m(t,T )√v2(t,T )

1√2πe−

12z2dz

36

= em(t,T )+ 12v2(t,T )Φ

(− log(K)−m(t, T ) + v2(t, T )√

v2(t, T )

)

−KΦ

(− log(K)−m(t, T )√

v2(t, T )

).

The result follows from the formula’s for m(t, T ), equation (4.6) and v2(t, T ),equation (4.7).

37

Chapter 5

The real estate model

In this chapter the real estate model is discussed. Unlike the equity and bondmarkets, there is no central regulated market for real estate transactions. Asis argued in [19] transactions in real estate are less frequent than on the bondand equity market and usually happen between two private parties. As a resultthe quality of information on real estate prices is considered to be poor. In thecase of real estate, the lack of information on transactions has led to the use ofappraisals as a basis for tracking price movements. Appraisals are often aggregatedto construct an appraisal index. Since real estate is a risky asset it assumed thatit has similar dynamics under Q as equity and because of that we choose to modelit by

dRE(t) = RE(t)r(t)dt+ σredWre(t), RE(0) = RE0. (5.1)

Since, except for the appraisal indices, there is almost no market data available,the model will be calibrated based on the historical volatility of real estate returns.For the remaining part of this chapter we will discuss appraisal indices and howto derive returns on real estate from these indices.

In an optimal setting, the appraisal index would give us an accurate re-flection of current market prices. However, there is substantial empirical evidenceimplying the existence of appraisal smoothing or ’appraisal lag’ [3][7][9] . It is sug-gested that market agents use information about previous appraisals of propertyas well as current market information, when appraising a property. On a individ-ual level this may be the optimal, if not the only, way to appraise a property, butwhen combined in an index this may not be optimal and its value may differ fromthe real market value. In addition to this, properties can be appraised at differentpoints in time, but are averaged out in the appraisal indices which are usuallyquoted quarterly or yearly. This implies an index value can be seen as a movingaverage of appraisal values.

Moreover, in [10] it is argued that the returns of appraisal indices havean abnormally low volatility compared to other risky assets, while the expected

38

returns are of the same order of magnitude. We can therefore argue that Economictheory suggests that the appraisal indices don’t reflect the real market prices. Thisis because market players show risk averse behaviour, this means that for a highervolatility of an asset they demand a higher average rate of return. But this alsomeans that if two traded assets have the same rate of return, they should also beequally volatile, because else no one would buy the most volatile asset.

5.1 Unsmoothing

To derive the real return series of estate and consequently the real historical volatil-ity of the returns, the appraisal index has to be unsmoothed. Over the years,various unsmoothing techniques have been suggested for appraisal indices and as-sets with similar characteristics as real estate. Two of the most well know andmost often used methods are developed by Geltner [18] and by Fisher, Geltnerand Webb [17]. In this thesis we choose to use the second unsmoothing method,because in comparison to the other method it allows for more information to beextracted from the data itself and because less assumptions are needed. We willnow discuss the model of Fisher et al. For the Geltner model, see Appendix C.

The method proposed by Fisher et al. is called the Full-Information Valueindex method. This name reflects that the unsmoothing of the appraisal index bythis method is done as if the real estate market is an efficient market i.e. theunderlying true returns are uncorrelated across time. The smoothing model isrepresented by

r∗t = w0rt + w(B)rt−1. (5.2)

Here w(B) is shorthand for

w(B) = w1 + w2B + w3B2 + . . . ,

where B is the lag operator i.e. Brt = rt−1, B2rt = rt−2, etc. Like before r∗t is the

smoothed index return and rt is the unsmoothed or real return. Substituting andexpressing r∗t in present and past values of r∗t−1, one can see that Equation (5.2)corresponds to an AR-model given by

r∗t = φ(B)r∗t−1 + et, (5.3)

where

φ(B) = φ1 + φ2B + . . .

and

et = w0rt.

39

Expression (5.3) can be inverted to obtain an explicit expression for rt as a functionof r∗t , r

∗t−1, . . . . This results in

rt =r∗t − φ(B)r∗t−1

w0

. (5.4)

We assumed unpredictable returns, which implies that et is white noise and givesus the opportunity to estimate the parameters φ trough standard univariate time-series estimation. However, to derive rt we need to make an additional assumptionto evaluate w0. In the paper of Fisher et al. an assumption on the volatility ofrt is made. It is widely perceived by institutional investors that the volatility oftrue commercial property returns is approximately half the real volatility of stockreturns σstock [18][17]. So

SD[rt] =σstock

2

and by taking the standard deviation on both sides in (5.4) this gives

w0 =2SD

[r∗t − φ(B)r∗t−1

]σstock

.

Where SD[r∗t − φ(B)r∗t−1

]is calculated as the empirical standard deviation based

on the historical smoothed return series r∗t and the estimated values of φ. Nowthe real returns rt can be derived.

One of the most important assumptions in this model is that the realestate market is informational efficient. However, as we argued before, the realestate market is not an efficient market. Thus, a way to interpret the resultingvalues are the values that would have prevailed if the market was efficient.

A simple extension of the model had been proposed by [8]. This is becauseit had been found that in the model by Fisher et al. the error term et not nec-essarily has a zero expectation and the derived series of return still show positiveautocorrelation. The solution that is proposed by Cho et al. is that a constantdrift term should be added to the model and two step differences ∆rt = rt − rt−2are used to get independent errors.

40

Chapter 6

The inflation model

The last risk factor that is modelled in the economic scenario generator is inflation.A lot of life insurance and pension products are ’indexed’ yearly on the basis ofinflation. This means that the payment at the maturity of the insurance contractis incremented each year with the inflation.

Unlike interest rates and stock indices, inflation rates are not constantlyobservable. The inflation rates in the eurozone are calculated monthly on the basisof changes in the consumer price index (CPI); for the inflation in the Netherlandsthis is done by the Dutch Central Bureau for Statistics (CBS) and for the infla-tion in the whole eurozone this is done by Eurostat, the statistics bureau of theEuropean Union. The CPI measures changes in the price level of a market basketof consumer goods and services purchased by households. The composition of themarket basket is standarised by EU guidelines. The most important categoriesin the CPI are housing, water, electricity and gas (24.5% of the total weight),transport (11.6%) and food and non-alcoholic beverages (11.3%).

There is strong evidence that suggests that inflation rates follow a meanreverting process [2][34]. Because the Vasicek model exhibits mean reverting be-haviour [45] and because it is not too hard to implement, given that we alreadydiscussed the extended Vasicek model of Hull-White for the modelling of interestrates, we choose to use it to model inflation in our ESG. The stochastic differentialequation is given by

dI(t) = λ(µ− I(t))dt+ σIdW (t), I(0) = I0.

Here µ is the long term mean, λ is the mean reverting speed and σI is the volatilityof the inflation.

Since there are no deep and liquid markets from which we can infer a termstructure of inflation or on which inflation derivatives are traded, the model willbe calibrated based on historical data. To do so we need the solution to the SDE.

41

Because the Vasicek model is a special case of the Hull-White model we can applyProposition 3.1 to get the solution to the short rate dynamics. So

I(t) = e−λt(I0 +

∫ t

0

λµeλsds+ σI

∫ t

0

eλsdW (s)

),

which gives us the following expectation and variance,

E[I(t)] = e−λtI0 + µ(1− e−λt

), (6.1)

Var[I(t)] = σ2I

(1− e−2λt

2λ

). (6.2)

In chapter (reference) we will discuss how these explicit formula’s can be used tocalibrate the inflation model to historical data.

42

Chapter 7

Simulation

When the parameters for each model and the correlation between the various riskfactors have been estimated, we want the economic scenario generator to generatefuture scenarios; this is done with Monte Carlo simulation. In this section thesimulation method is described and we will discuss two types of errors that canarise when doing such a simulation: discretisation errors and distributional errors.

7.1 Euler Scheme

If we want to simulate our stochastic models, we must discretise the stochasticprocesses, because we cannot generate continuous paths. While there are severaldiscretisation methods, we choose to use the Euler-Maruyama scheme [35], becauseit is the most straightforward to implement.

Let us assume we have a stochastic process of which the dynamics aredescribed by a stochastic differential equation of the form

dX(t) = µ(X(t), t)dt+ σ(X(t), t)dW (t), (7.1)

where W is a Brownian motion. We wish to simulate X over the interval [0, T ]and we have discretised the interval as 0 = t1 < t2 < ... < tm = T . Integrating theSDE from ti to ti+1 gives us

X(ti+1) = X(ti) +

∫ ti+1

ti

µ(X(s), s)ds+

∫ ti+1

ti

σ(X(s), s)dW (s). (7.2)

The starting point of any discretisation method should be to approximate thisexpression.

Now let us have a look at (7.2) in more depth. The first integral is aregular Riemann integral, but the second integral is a stochastic integral. Without

43

discussing the technical details, a convenient way to interpret a stochastic integralis ∫ t

0

σ(X(s), s)dW (s) = limh→0

∑σ(X(ti), ti)(W (ti+1)−W (ti)), (7.3)

where h = maxi |ti+1 − ti| is the width of the partition. Important to note is thatthe σ(X(ti), ti) are evaluated at the left-hand point of the time interval; this canbe interpreted as the inability to see into the future.

The Euler method is derived directly from the interpretation in (7.3). Itapproximates the integrals using the ’left point rule’. Hence (7.2) is approximatedby

X(ti+1) = X(ti) + µ(X(ti), ti)∆ti+1 + σ(X(ti), ti)∆Wi+1, (7.4)

where ∆ti+1 = (ti+1 − ti) and ∆Wi+1 = (W (ti+1) − W (ti)). Here the ∆Wi areincrements of a Brownian motion and thus the ∆Wi are independent randomvariables with a N(0,∆ti) distribution.

An alternative to the Euler method is given by the Milstein method [37].It is based on the expansion of the coefficients µ(X(t), t) and σ(X(t), t) by usingthe Ito formula. The Milstein discretisation method is given by

X(ti+1) = X(ti) + µ(X(ti), ti)∆ti+1 + σ(X(ti), ti)∆Wi

+1

2σ(X(ti), ti)

∂σ

∂x(X(ti), ti)

(∆Wi+1

2 −∆ti+1

). (7.5)

Generally the Milstein method has a higher order of convergence than the Eulermethod, but when the σ(X(t), t) term is a deterministic function of time equation(7.5) coincides with equation (7.4). For our ESG this is the case, since the volatilityterms of the stochastic models are all deterministic.

As was mentioned in the introduction of this chapter, all the stochasticmodels will be simulated using the Euler method. However, for the interest ratesmodel, we won’t directly simulate the Hull-White SDE in equation (3.1). We willuse the representation r(t) = x(t)+φ(t) derived in Section 3.1.1. The advantages ofsimulating r(t) by using the SDE for x(t) and adding φ(t) in stead of simulating theSDE of r(t) (3.1) directly is that we don’t need the derivative of the instantaneousforward rate f(0, t), which is part of θ(t).

7.2 Discretisation and distributional error

Recall that the purpose of the economic scenario generator is to calculate technicalprovisions of various insurance products. The technical provisions are defined as

44

the expected value (under the risk neutral measure) of the discounted future cashflows. Let X be a stochastic process, with a corresponding stochastic differentialequation as in (7.1), then calculating the technical provisions comes down to cal-culating expected values of the form EQ[f(X(T ))], for some given function f anddiscounting it with the current term structure.

Approximating the expectation by using the Monte Carlo simulation canresult in an error in the estimated value of the expectation. Generally this approx-imation error consists of two components: a statistical error and a discretisationerror.

The values realised by the Monte Carlo simulation are used to approximatethe expectation; that is

E[f(X(T ))] ≈N∑j=1

f(X(m)(T ;ωj))

N,

where X(m) is a discrete approximation of X, e.g. the result from the Euler method,corresponding to partition 0 = t1 < t2 < ... < tm = T . We can describe the errorof the Monte Carlo method as

E[f(X(T ))]−N∑j=1

f(X(m)(T ;ωj)

N(7.6)

= E[f(X(T ))− f(X(m)(T ))] +

(E[f(X(m)(T ))]−

N∑j=1

f(X(m)(T ;ωj))

N

). (7.7)

On the right hand side of (7.6) the first part of the error is what we call the timediscretisation error and the second part is the statistical error.