Embed Size (px)

Citation preview

THIN CAPITALIZATION AND COMPANIES INCOME TAX IN NIGERIA

FELIX OGHENEOCHUKO ALADE Department of Accounting

Western Delta University, Oghara Delta State

EIYA OFIAFOH PhD

Department of Accounting University of Benin, Benin City

ABSTRACT

The study involves an exploratory analysis of the relationship between thin capitalization and companies’ income tax in Nigeria. However, because Multinational Companies mostly employ thin capitalization in corporate tax avoidance, the focus of this study is on Multinational Companies. The study employed library research approach which formed the basis for drawing conclusion and making necessary recommendations by the researcher. From exploratory literature reviewed it was revealed that thin capitalization is a major strategy employed by companies, mostly multinationals to avoid tax and it reduces government revenue across the world. Also, the structure of multinationals and the need to encourage foreign direct investment and economic growth in Nigeria, pose a challenge to the tax authority to effectively introduce a specific thin capitalization rule. As a way foreword to dealing with thin capitalization and taxation of Multinational Companies (MNC) in Nigeria, Therefore we wish to make the following recommendations: introduction of specific thin capitalization rule. More so, unitary taxation should be adopted across the world to avoid multinational companies’ undue advantage of shifting profit from high tax jurisdictions to low tax jurisdictions. Keywords: Taxation, Thin Capitalization, Unitary taxation, Multinationals, Tax avoidance.

INTRODUCTION Companies employ debt and/or equity to finance its operations. How a company is

financed is purely the decision of management. However, when a company employs more debt than equity in its capital structure it is referred to as thin capitalization (Organisation for Economic Co-operation and Development [OECD], 2012). In Nigeria, section 24 (f) of the Constitution of the Federal Republic of Nigeria (1990) as amended, states that “it shall be the duty of every citizens to declare his income honestly to the appropriate and lawful agencies and pay his tax promptly” This provision makes it a constitutional responsibility for all income earners (both individual and Corporate) to pay tax in Nigeria. To this end, taxpayers can be defined as a person, group of persons or an entity that pays or liable to pay tax (National Tax Policy [NTP], 2016). Therefore, tax payers are classified as, Individual taxpayers and Corporate taxpayers. Individual taxpayers include individuals/citizens in paid employment and self-employed. On the other hand, Corporate taxpayers include companies (both domestic and non-resident). Domestic companies here, are companies incorporated in Nigeria under the

Companies and Allied Matter Act (CAMA). On the other hand, non-resident companies (Multinational Companies) are companies incorporated by other laws other than (1990) as amended but carrying on business in Nigeria. These multinationals, more often than not, employ different tax avoidance strategies to reduce tax liability.

Despite the aforementioned constitutional provision, rising tax avoidance scheme employed by multinational companies have become major causes of concern facing both developed and developing climes, which Nigeria is not an exception. Specifically, one of the policy drives of the present administration is seeking ways to increase tax revenue accruing to the government. Thus, there is absolute need for complete understanding of how these MNCs behave in Nigeria and developing countries, as many operate completely different standard in Africa to what obtains globally (Adeosun, 2018).

Over the past two decades in Nigeria, government revenue has been skewed in favour of oil revenue with little or no attention to taxation. For example, in Nigeria between 1999 and 2016, tax revenue to Gross Domestic Product (GDP) hit a record low of 1.5% and stayed at 6 % (National Bureau of Statistics (NBS), 2016). Between this periods, oil revenue to GDP hits a record high of 80% and stayed above 16% till 2016 (NBS, 2017). However, with the present economic challenges in Nigeria owning to dwindling crude oil price in international market and the weak value of Naira against the dollars necessitated the government to shift attention to taxation which has been described as a veritable tool for wealth creation (Udo, 2015). Consequently, governments across the world are in constant search of policies and law to discourage tax avoidance strategies employed by multinational companies that deprive the government of the much needed revenue for growth.

Eyitayo (2015) identified tax haven, transfer pricing, accounting technologies, contract manufacturing, double-Irish, thin capitalization and dutch sandwich, while Govendri, Lanis, and McClure (2016) identified base erosion profit shifting, loss creation, double Irish, dutch sandwich, debt loading or thin capitalization as the main strategies of tax avoidance by multinational companies. The impact of this strategy national companies cut across all countries but has a far reaching consequence on developing climes as they are confronted with policy and other conditions that reduce their abilities to address these corporate strategies (Eyitayo, 2015).

An important issue for policy purpose is to review the impact of thin capitalization on companies’ income tax in Nigeria. An understanding of thin capitalization and companies’ income tax, as well as the way MNCs employ thin capitalization in corporate tax avoidance may provide an important insight on the anti-avoidance policies and laws to be adopted to reduce tax revenue loss. The objective of this paper therefore, is to succinctly revived extant literature on the relationship between thin capitalization and companies’ income tax in Nigeria, with emphasis on MNCs. Considering the fact that, there is no specific thin capitalization rule in Nigeria, we also wish to identify anti-avoidance policies and laws available to Federal Inland Revenue Service (FIRS) to reduce or eliminate tax avoidance among corporate.

The study will be of significance by adding to the seemingly scarce researches on the subject matter in Nigeria. It will also be a source of useful reference to the government as well as Federal Inland Revenue Service (FIRS) in terms of policy formulation in relation to multinational taxation and thin capitalization rules. It may possibly serves as a starting point for upcoming researchers.

The remaining part of this paper is structured as follows: sections two (2) reviews relevant literature and section three (3) concludes the study with necessary recommendations made.

LITERATURE REVIEW This section reviews several studies on thin capitalization and companies’ income tax. It

specifically examines the impact of thin capitalization on companies’ income tax; Thin Capitalization rule approaches of selected countries; Anti-Avoidance rule and the relevant underlining theories.

Companies’ Income tax and multinational Companies in Nigeria National Tax Policy (NTP) (2016) sees taxation as the process by which taxes are

collected within a specific area. In the same vein, Anyaduba (1999:2) defined taxation as “the process or system of raising income through the levying of various types of taxes.” the fundamental objective of taxation therefore, is chiefly to generate revenue for government’s expenditure on social welfare (Uzonwanne, 2015). Tax is defined as a compulsory imposition by government on income, profit, gains or wealth of both individual and corporate bodies for the purpose of generating revenue (Alade, Eiya & Adu, 2016). From the above definition it suffices to say that taxation is a process of collecting revenue while tax is the product of the process.

The major taxes currently operational in Nigeria include: Personal Income Tax (PIT), Petroleum Profit Tax (PPT), Companies Income Tax (CIT), Value Added Tax( VAT), Education Tax (ET), Capital Gain Tax (CGT), Customer & Excise duties and stamp duties. Most critical to our discussion is companies’ income tax Act CAP C21 which mainly governed tax matter relating to multinational companies.

Companies income tax (CIT) is a direct tax on the profits of incorporated entities in Nigeria and non-resident companies (MNCs) carrying on business in Nigeria. The tax is paid by both limited liability and public limited liability companies. It is commonly refers to as, corporate tax. According to the FIRS Chairman, Babatunde Fowler (2016), CIT contributes a significant proportion to the revenue profile of the service. However, much revenue could be achieved from CIT with concerted efforts tailored towards eliminating or minimising corporate tax avoidance by companies, especially MNCs in Nigeria. Unlike purely domestic companies, MNCs are not limited to external borrowing but can also borrow from subsidiaries, thus optimize its financial structure over all subsidiaries to reduce the tax obligations of the company group.

Multinational companies (MNCs) are companies or corporations which are registered in one country but carry out business operation in one or two other countries. In some climes, a multinational company is also known as a Multination Enterprise (MNE) or as a transnational corporation [TNC], (Tatum, 2010). Tadaro (as cited in Ileoma, 2010), see MNCs as enterprises that operate and control means of production in more than one country. In Nigeria, the presence of MNCs predates independence. Their numbers and activities have grown over the years owing to Nigeria’s struggles to develop socio-economically as a nation (Abimbola & Dele, 2015). There exist in Nigeria ample of these multinational companies, top among these multinational companies in Nigeria are: Unilever, Nestle, Guinness, Chevron, Shell, Pocter and Gamble co. (P&G), British American Tobacco, Google, PrescoPlc (Obasanho, 2017). In the view,

of Otokiti (2012), most of the MNCs are attracted to Nigeria because of cheap labour and affordable transportation to deliver their markets.

Blouin (2010) opines that multinationals operate in several jurisdictions and not only subjected to several set of tax rates, but also sets of tax regulations. Thus, this interplay between rules and rates exposes MNCs to plethora of potentials tax obligations such transfer pricing and withholding tax. To this end, Organisation for Economic Co-operation and Development [OECD], (2013), identified the position of multinational corporation to heavily reduce their tax obligation and the harm it create for government struggling with dwindling tax revenue, for individual taxpayer who bears the burden for this cut in corporate taxes, as well as business with difficulty in competing. Similarly, Eyitayo (2015), while citing the case of IRC v. Duke of west minster, argues that every company has the option of engaging in different strategies within the contemplation of the law of the jurisdiction it operates to reduce its tax liability. However, the aggressive tax avoidance should be discouraged.

The Concept of Thin Capitalization As we earlier mentioned, corporations are basically financed or capitalized via debts and

equity. The way a company is capitalized is solely a financing decision of the company. However, the way and the intention behind the financial structure of a company especially within the multinational structure will often than not have a far reaching impact on the amount of profit it reports for tax purposes. According to OECD (2012), thin capitalization refers to a situation in which a company is financed through a relatively high debt compared to equity. It is usually refered to as “Debt loading” (Govendri et. al., 2016). A thinly capitalized company is referred to as highly geared or levered. Similarly, Sekar and Blushan (2012) opine that a company is said to be thinly capitalized when its capital structure is made up of a much greater proportion of debt than equity. That is the company’s gearing or leverage is too high. Furthermore, they stated that thin capitalization is commonly used to describe a situation where the proportion of debt to equity exceeds a certain limit. Thin capitalization is a tax avoidance scheme whereby multinational corporations capitalized their subsidiaries primarily with more debt vis-à-vis equity. It is often described as hidden capitalization or “hidden equity” (Tailor & Richardson, 2013). In the same vein, Dosai, Foley, and Hines (2004), opine that thin capitalization is one of the important elements of tax planning tool for multinational corporations, not only for the company as whole but also internally.

Flowing from the above assertions, we defined thin capitalization as a tax avoidance strategy whereby a company uses more debt than equity capital, with the intention retain ownership, as well as to reduce tax obligations having in mind that interest on loan is tax deductible. Thus, using more debt becomes more attractive to related or connected parties with the manipulative tendency to shift profits from one country to another or one subsidiary to another. This over reliance on debt financing by corporations is a tax planning strategy with a clear intention of tax avoidance. Tax avoidance therefore, is a mechanism of reducing tax liability in legally permissible way by structuring one’s affairs to take advantages of the law (Statement of Taxation Standards [STS] 9, 2016). In the view of Weisbach (2002), all tax rules defining tax base has inconsistencies and gaps that can be exploited, hence, the need for some anti-avoidance measures. The anti-avoidance measures are broadly classified below:

Approaches based on general principle: These are the philosophies and approaches of law but not codified in the legislation;

General Anti-Avoidance: these are rules which are codified and incorporated in the legislation; and

Specific Anti-Avoidance: This is an anti-avoidance measure which applies to specific situations such as Controlled Foreign Companies (CFC), Anti-tax Haven rule, Transfer pricing and thin capitalization rule.

Thin Capitalization and Anti-Avoidance Measures As earlier stated, the manner in which a company is capitalized may have a significant

impact on the profit it reports for tax purpose and consequently, the tax it pays. To this end, most countries more often than not, set acceptable debt to equity limits for corporations (OECD, 2012). However, in Nigeria presently, there is no specific rule that limits the level of debt to equity for companies. Hence, companies over reliance on debt. Most commonly used approach over the years among tax authorities is the Arm's Length Principle (Omoijiade, 2017). Arm's Length Principle (ALP) treats subsidiaries of multinationals as separate entities where transactions between them are adjusted to reflect independent market price for tax purpose. In Nigeria, the ALP has been domesticated in the tax laws as follows:

Section 17 Personal Income Tax (PTA) CAP P1;

Section 22, Companies Income Tax Act (CTA) CAP C21;

Section 15 Petroleum Profit Tax Act (PPTA) P8;

Section 22 Capital Gain Tax Act (CGTA) CAP C; and

Section 5 Value Added Tax Act (VATA) CAP VI.

The above provisions, in respect to Arm’s length transaction clearly guide Federal Inland Revenue Service (FIRS) to amend tax returns between related or connected persons not done at Arm’s length (Gbonjubola, 2015). However, more compelling arguments opine that the ALP create more opportunities for multinationals to engage in more complex structure to minimize taxes (International Commission for Reform of International Corporate Taxation [ICRICT], 2012). In the same vein, Segal (1994) argues that the Arm’s Length approach places the burden of proof on the taxing authority whether an Arm’s price has been set on transactions between related parties and what an arm’s length price should be. To further substantiate their point, the critics of the arm’s length principle, also argue that the arm’s length allows multinationals to engage in aggressive tax planning through creation of subsidiaries in a low tax jurisdiction or convenient countries and shift profit through or to them to reduce tax obligation to the detriment of the national tax authorities (Picciotto, 2012). Recent advocacies on strategies to discourage tax avoidance scheme by multinational corporations in most developing countries have been anchored on unitary taxation which tends to impose same tax rate across jurisdictions hence discouraging the creative games played by multinational corporations via thin capitalization (Sikka, 2013). Conversely, OECD (2012) is of

the view that tax injustices perpetuated by multinational companies are detrimental to revenue drive of most developing countries, hence the need to adopt rules designed to counter cross-border profit shifting.

Aside Unitary taxation, another anti-avoidance measure is thin capitalization rule. According to OECD (2012), thin capitalization rule (TC rule) is a rule or legislation put in place by countries tax administrations, essentially to place a limit or ceiling on the amount of interest that can be deducted in computing profit for tax purpose. Thin capitalization rule is designed to counter across–boarder profit shifting via ‘excessive debt’ hence protect a country tax base (OECD, 2012).

According to Ruf and Schindler (2012), Canada was at the fore front introducing thin capitalization rules (T.C rules) in 1971. However, implementations of T.C rules took off between mid-1990s and 2005, when the share of OECD countries with rules increased significantly from less than half to more than two third. In most cases, T.C rules, is to prevent apparent leakage of tax revenue, resulting from the way a corporation is financed (Sekar & Blushan, 2012). Furthermore, T.C rules help to prevent excessive “Captive” or “In house’ or friendly loans which would be detrimental to the revenue of the home country (where the borrower is resident), as the profit to this extent would be effectively shifted to a foreign lender, as interest payment. Similarly, Ruf and Schindler (2012) stated that the aim of T.C rules is to curb excessive debt financing and tax revenue losses from international debt shifting ( i.e, from shifting Income through Interest expenses into low tax jurisdictions). In the same vein, Blouin, Huizinga, Laeven, and Nicodeme, (2014) opine that to discourage the negative consequences of debt finance for tax purpose, countries' tax administrations have to institute a rule that restricts the deductibility of interest above a certain level. Despite the above assertions, the TC rule appears to create opportunities for tax competition among tax administration because of the different rules adopted by different tax jurisdictions. This led to the proponents of unitary taxation.

Flowing from the above, it can be deduced that the ALP is most prevalent because of its suitability to different tax jurisdictions, however to determine what constitute an arms' length price for a related party transaction requires competency and resources on the part of the tax authorities to apply the complex and time sapping check on transactions among related parties, which is lacking in most tax administration. In Nigeria, these challenges are evident. TC rules makes it relatively difficult for multinationals to erode tax base, although from what we can infer from the above assertions, most countries still depend on TC rule for ALP implementation Also the Unitary taxation appears tobe more simple to apply, as well as more equitable. The limitation on how to prepare common financial statements by multinationals has been overcome with the adoption of International financial Reporting Standards (IFRS). However, the bases of determining the extent of multinationals operation in a particular jurisdiction pose a challenge to its adoption across the world. Moreso, non-resident company with debt capital is considerably more tax efficient than financing with equity. The difference in the tax treatment of equity and debt is the motivation of resource owner to provide capital to a company in form of debt than equity. Thus, absence of T.C rules makes it relatively easy for Non-resident Corporations to advance funds to resident associates and christened it as debt such that the interest payment is tax deductible. Thin Capitalization Rules: Approaches and Effects on Tax Revenue

Kaserer (2008) asserts that categorization and classifications of T.C rules are used arbitrary without regard to supranational tax laws, while implementation in practice is limited to a few main approaches: the subjective approach; fixed ratio; hidden profit distributions; and earning stripping rules. In the same vein, Sekar and Blushan (2012) identified four approaches of T.C rules to include: Fixed Ratio approach; application of rule on hidden profit distributions, and "no rules"approach. In the light of the foregoing classification of T.C rule, the following explanations suffice: Subjective Approach: The subjective approach tends to view the teraprevailincircumstance of debt (loan) to ascertain whether the debt has been disguised as equity. Some countries us approach also have specific T.C legislation.

Fixed Ratio Approach: Under the fixed ratio approach, if the debt or loan exceeds a certain proportion to equity, the interest on the excess loan is either automatically disallowed or treated as dividend liable to dividend tax (withholding tax). Here, it is worthy of note that the disallowed interest may not reduce the income rate of loan provider (lender). Some countries that adopted this approach usually have specific T.C rule. Hidden Profit Distribution Approach: The hidden profit distribution approach tends to treat excess interest as dividend and taxed accordingly. Here, the general anti-avoidance rule (arm’s length principle) plays a major role. Also, in some countries the hidden profit distribution is applied alongside with specific T.C rules. Earning Stripping Approach: Under this approach, tax deductible interest expenses are limited not only for related party transaction but also unconnected parties.

It can be deduced from the above, that approaches of T.C rules are interrelated. Thus, OECD (2012) opines that T.C rule basically operates by means of one or two approaches: determining the amount of debt on which deductible interest payments are made and/or limiting the amount of interest that may be deducted by reference to its ratio to another variable.

Thin capitalization: Hypothetical Effect on Companies income Tax Revenue in Nigeria

Where there is no specific T.C Rule (scenario 1)

SOURCE: author’s computation

Nigeria XYZ MNC

(Borrower)

Parent

company of

XYZ in china

(Lender)

Loan 90m

Interest Repayment 10%

Financed by: Equity 10m: Debt 90m

-Profit before interest & Tax (PBIT) 15m -Interest payment (10% x 90m) (9m) -Profit after interest before Tax 6m -Tax Rate 30% - Corporate Tax (30% x 6m) 1.8m - Withholding Tax on interest (10% x 9m) 0.9m -Total Tax Revenue 2.7m -

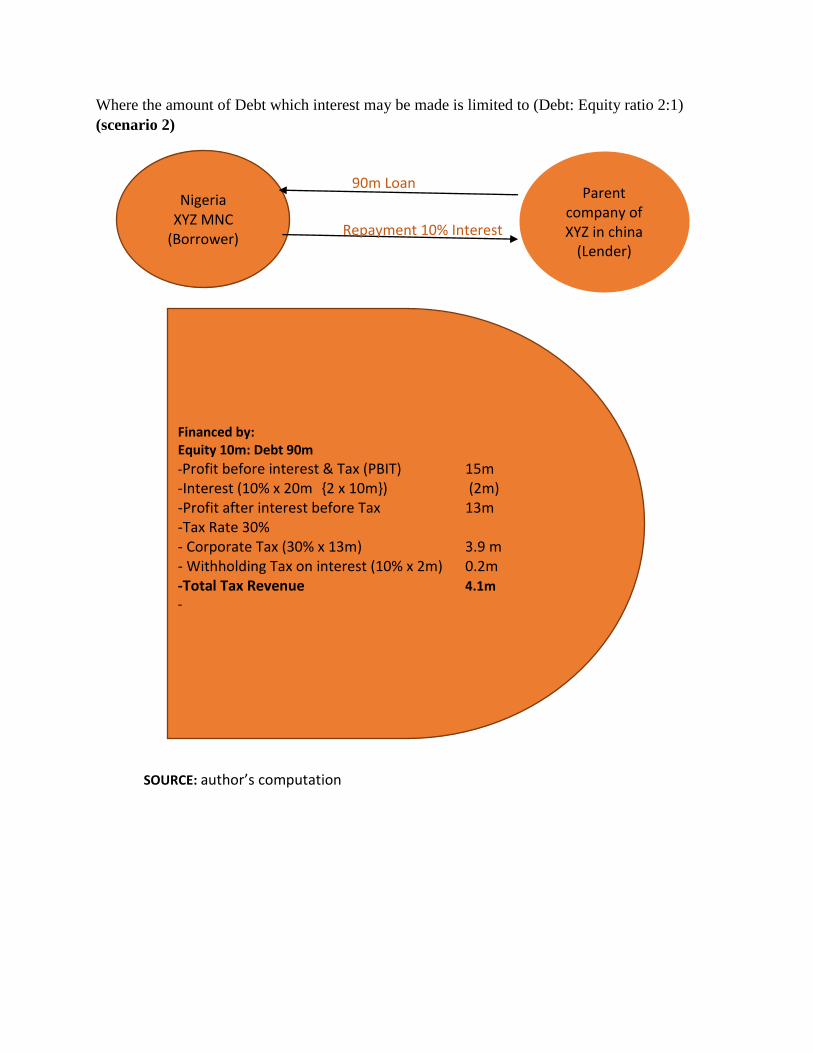

Where the amount of Debt which interest may be made is limited to (Debt: Equity ratio 2:1)

(scenario 2)

SOURCE: author’s computation

Nigeria XYZ MNC

(Borrower)

Parent company of XYZ in china

(Lender)

90m Loan

Repayment 10% Interest

Financed by: Equity 10m: Debt 90m

-Profit before interest & Tax (PBIT) 15m -Interest (10% x 20m {2 x 10m}) (2m) -Profit after interest before Tax 13m -Tax Rate 30% - Corporate Tax (30% x 13m) 3.9 m - Withholding Tax on interest (10% x 2m) 0.2m -Total Tax Revenue 4.1m -

Where the amount of Debt which interest deductible by reference to its ratio to

another variable is limited to 30% of profit before interest, tax, depreciation and

Amortisation (PBITDA) (scenario 3)

Nigeria

XYZ MNC

(Borrow)

Parent

company of

XYZ in china

(Lender)

Loan 90 millions

Repayment of Interest 10%

Financed by:

10m Equity: 90m Debt

-Profit before interest & Tax (PBIT) 15m

-Interest 10% x 4.5 {30% x 15m} (0.45m )

-Profit after interest before Tax 14.55m

-Tax Rate 30%

- Corporate Tax (30% x 14.55m) 4.37 m

- Withholding Tax on interest (10% x o.45m) 0.045m

-Total Tax Revenue 4.415m

SOURCE: Authors computation

ASSUMPTIONS There are no depreciation or amortisation charges. There is no tax treaty between Nigeria where the subsidiary of XYZ is located and China

where the parent of XYZ is resident XYZ loan capital is purely internally sourced.

Flowing from the above hypothetical analysis, it can be deduced that in scenario1 there is a tax revenue loss of over 1.4 million naira to China as interest repatriation. Conversely, in scenario 2, where interest on loan is limited to 2 million naira, there is a tax revenue gain of over 1.4m to Nigeria from XYZ MNC. In the same vein, where the interest deductibility is limited to 30% of the earnings before interest and tax, there is a further gain of tax of over 1.7 million from XYX to Nigeria government.

THEORETICAL FRAMEWORK The following theories are relevant to this study and are discussed below:

Fairness and Equity Theories Fairness and Equity theories draw its relevance from the “Canon of taxation” credited to

the earliest work of Adam Smith (1776). The theorists postulate that it is more likely for individuals to obey rules if they considered the system that determine that rule to be fair and equitable. Conversely, individual perceived of inequality in any system will result to disobediences. According to Bittker (1979), the standard, traditionally deployed by tax theorists in evaluating the structural details of corporate tax is equity. Equity theorists seek to ascertain whether an extant tax legislation treats equals equally (Horizontal equity) and whether it differentiate dispassionately among unequal’s (vertical equity). He further asserts that to answer the questions of whether a taxpayer or group of taxpayers are equals or unequal, equity theorists compare their earning before tax incomes. This theory indicates that taxes must not only be fair but also be seen as been fair by all taxpayers if the taxes must be accepted by taxpayers or the public. To this extent, there is high tendency of tax evasion and avoidance when the tax system is perceived inequitable, which Thin capitalization create between purely domestic companies and multinational companies

Structural Theory Structural theory is credited to the work of a sociologist Anthony Giddens (1984). He

argues that individual’s freedom is influenced by structure and structures are maintained and adopted via exercise of agency. In other words, agents and structure do not exist independently of each other and cannot be understood separately from one another.

According to Boden(cited in Otusanya, 2013), multinational corporations structure their operation to reflect a rational collectively of socials actions, despite the fact that there seems to be a separation in law between them which empowers each subsidiaries to sue and be sued.

EMPIRICAL REVIEW Despite the spread of thin capitalization by multinationals as a corporate tax avoidance

scheme, the empirical evidence on the consequence on company income tax is generally lacking, especially in developing countries like Nigeria.

In the case of Germany, Overesch, Shreiber, Buettner and Wamser (2006) conducted a study on thin capitalization for capital structure choice and investment of multinationals. The study employed a comprehensive micro panel-level datasets of almost all German multinational foreign affiliates combined with information about companies income tax including thin capitalization rule in all OECD and European union over a period of 9 years. The study revealed that thin capitalization is one of the major strategies employ by multinationals; thin capitalization is quite effective in reducing tax planning by means of intercompany loan.

In the case of U.S, Altshuler and Grubert (2006), provide data for the U.S showing that multinationals that use more debt than equity made it easier for such MNCs to avoid taxes on intercompany interest payment, hence significantly increased disparity in the reported profit of their subsidiaries in high tax jurisdiction and low tax jurisdiction. This is also consistent with the findings of Haufler and Runkel (2008) as they examined the impact of thin capitalization on multinational capital structure and companies income tax competition. Overesch and Wamser (2007), carried out a quasi-experimental study on corporate tax planning behaviour by means of intercompany finances and the effectiveness of government anti avoidance measures via thin capitalization rules using German inbound investment data from 1996 to 2004. The study revealed that with the introduction of specific thin capitalization rule in 2001, in 2002 Germany was able to retain corporate tax revenue on average 71,700 Euros per ordinary corporations and 1,807,000 Euros per holding corporation. They argue that considering the number of treated corporations, that tax revenue retain to Germany government between 2001- 2004 from the thin capitalization reform approximate 30 million Euros. Fuest and Hemmelgarn (2005) examined the impact of foreign firm ownership and international profit shifting through thin capitalization. They found that foreign firm ownership lead to reduction of corporate tax rates; the existence of international profit shifting through thin capitalization induces countries to reduce their tax rates to broader their tax bases and gain from unitary taxation ( coordinated corporate tax rate).

CONCLUSION The aim of this study is to review extant literature on the impact of thin capitalization on

companies’ income tax in Nigeria with emphasis on Multinational Companies which mostly employ thin capitalization in corporate tax avoidance. We also identified policies and laws available to tax authorities to eliminate or reduce this tax injustice that have deprived government its necessary revenue for growth. The motivation for the study therefore, resolves around the need to mitigate tax avoidance via thin capitalization by multinational companies, so as to increase revenue collection by government and close the revenue gap due to crash in crude oil price and weak value of naira to dollars in the global economic market. Literature revealed that thin capitalization is a major strategy employed by multinationals to avoid tax and the need to have a more sustainable measure to eliminate or reduce its impact on companies’ income Tax revenue. However, it must be stressed that recent advocacies to increase tax revenue in Nigeria is not equal with discouraging economic growth. Hence, the need to consider the dire needs of economic growth in introducing thin capitalization rules.

RECOMMENDATIONS

Flowing from the above, this study recommends the following as a way foreword to dealing with thin capitalization and taxation of Multinational Companies (MNCs) in Nigeria: introduction of specific thin capitalization rule. In the same vein, unitary taxation should be adopted across the world to avoid multinational companies’ undue advantage of shifting profit from high tax jurisdictions to low tax jurisdictions.

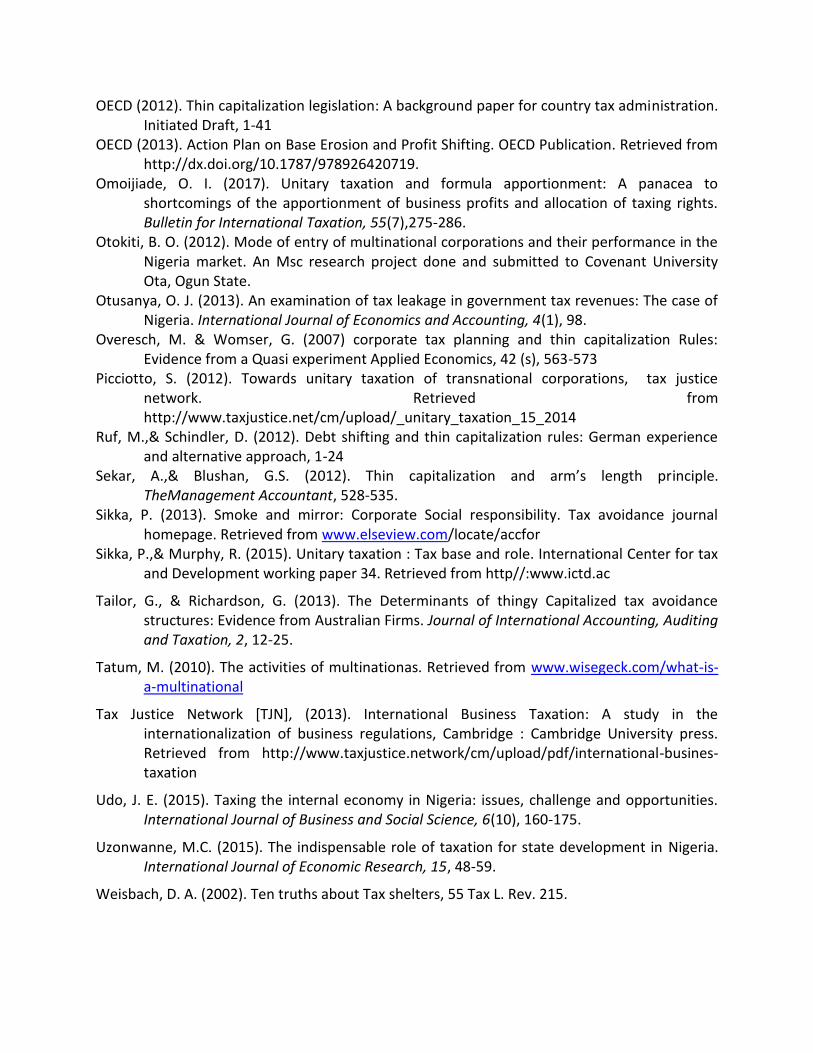

REFERENCES

Adam, S. (1776).Inquiry into the cause of the wealth of the nation. Journal of public Economics, 1(3-4), 323-38

Adeosun, K. (2018, February 20). Label tax malpractice by Multinationals as foreign corruption practices. An appeal by Nigeria Minister of finance at the platform for collaboration of Tax, (PCT) in New York, February 20th, 2018. Vanguard Newspaper. Retrieved from https//:www.vanguard.news/2018/02-oecd-world-bank-imf-label-tax-malpractices-multinationals-foreign-corruption-practices.

Alade, F. O, Eiya, O., & Adu, D. O. (2016). Tax audit and tax compliance in Nigeria. CARD International Jounal of Management Studies, Business & Entrepreneurship Research, 1(2), 2545-5907.

Altshuler, R. $ grubert, H. (2006). Government and multinational corporation in the race to the bottom. Tax note international, 41 (5), 459 -474

Ambibola, O.S., & Dele, A.O, (2015). Multinational corporations and economics development in Nigeria.America Journal of Environmental policy and management, 1 (2), 16-24

Anyaduba, J. O. (1999). Personal income taxation in Nigeria. Benin city, Nigeria: United City press

Ayi-Yonah, R. S., & Benshalom, I. (2010). Formulate apportionment: Myths and prospects-promoting better international tax policy and utilizing the misunderstood and under theorized formulary alternative. World Tax Journal, 2-3.

Babatunde, F. (2016, September 16). Understanding companies income Tax. The Nation's Newspaper. Retrieved from https//:nation.news/2016/16/tax-discurse-companies-income-tax.

Bittker, B.I. (1979). Equity, Efficiency, and income tax theory: Do Misallocation Drive out inequalities. Retrieved from http//:digitalcommons.law.yale.edu/fss-paper/2307

Blouin, J. (2011) Taxation of multinational corporations. Foundation and Trends in Accounting, 6(1), 1-64. Retrieved from http//:doi.org/10.1561/1400000017

Blouin, J., Huizinga, H., Laeven, & Nicodeme, G. (2014). Thin capitalization rules and multinational firm capital structure. IMF working paper Wp/14/12, 1-37.

Buettner, T, Overesch, M, Schreiber, U.S & Wamser, G. (2006). Taxation and the choice of capital structure: Evidence from a panel of Germany multinationals. CE.fo working paper 1841, Munich

Companies Income Tax Act, CAP C21, Laws of the Federation of Nigeria, 2004 (as amended by companies Income Tax (Amendment) Act, 2007.

Constitution of the Federal Republic of Nigeria, 1999

Desai, M. A. Foley, C. F., & Hines, J. R. (2004). A multinational perspective on capital structure choice and internal capital markets. The Journal of Finance, 59,2451-2487.

Eyitayo, O. (2015, December 2). Strategies employed by multinational companies to avoid Tax. Retrieved August 23, 2016 from unisedin: http//:www.linke.com

Gbonjubola, M. O. (2015). Transfer pricing and thin capitalization. 15th Annual tax conference of chartered Institute of Taxation of Nigeria (CITN).

Giddens, A. (1984). The constitution of Society: Outline of the Theory of Structuration. Cambridge:Polity Pres.

Havfler, A. & Runkel, M. (2008). Multinational capital Structure, thin Capitalization rules and Corporation tax competition. Payer prepared for the meeting of the European Tax policy forum, London. Retrieved from: http//havflerrunnkelpapet/London/2008

Hines, J. R (2010). International Taxation and Multinational activities. University of Chicago press, pagans 173-200

Ileoma, A. (2010). Accelerating economic growth in Nigeria: The rule of foriegnDirect investment. Current Research Journal of Economic Theory, 2(1), 11-15

Independent Commission for the Reform of International Taxation [ICRIT], (2017). Unitary Taxation Approaches. Being a paper Delivered at ICRIT AnnualConfernce, New York on September 18th, 2017. Retrieved from http//:ICRIT-HIGH-LEVEL-Roundtable-18-september-2017-conference-note.

IRC V. Duke of West minster (1936) A-C

Kaserer, C. (2008). Restricting Interest deductions in corporate tax systems: its impact on investment Decisions and Capital markets. Munich: CEFS.

laFuest, C. & Hemmelgain T. (2005) corporate tax policy, foreign firm ownership and thin capitalization Regional Science and Urban Economics 35, 508 – 526

McClure, R Lanis, R. &Govendir, B. (2016). Analysis of tax avoidance strategies of top forcing multinationals operating in Australia: AN Expose

National Tax policy of Nigeria (2012). Final Draft from the Federal Ministry of Finance

Obasanho, S. (2017). Multinational companies in Nigeria. Retrieved from http//www.naija.com

OECD (2008). Model of Tax Convention on Income and Capital. Condensed Version. Amsterdam:IBFD

OECD (2012). Thin capitalization legislation: A background paper for country tax administration. Initiated Draft, 1-41

OECD (2013). Action Plan on Base Erosion and Profit Shifting. OECD Publication. Retrieved from http://dx.doi.org/10.1787/978926420719.

Omoijiade, O. I. (2017). Unitary taxation and formula apportionment: A panacea to shortcomings of the apportionment of business profits and allocation of taxing rights. Bulletin for International Taxation, 55(7),275-286.

Otokiti, B. O. (2012). Mode of entry of multinational corporations and their performance in the Nigeria market. An Msc research project done and submitted to Covenant University Ota, Ogun State.

Otusanya, O. J. (2013). An examination of tax leakage in government tax revenues: The case of Nigeria. International Journal of Economics and Accounting, 4(1), 98.

Overesch, M. & Womser, G. (2007) corporate tax planning and thin capitalization Rules: Evidence from a Quasi experiment Applied Economics, 42 (s), 563-573

Picciotto, S. (2012). Towards unitary taxation of transnational corporations, tax justice network. Retrieved from http://www.taxjustice.net/cm/upload/_unitary_taxation_15_2014

Ruf, M.,& Schindler, D. (2012). Debt shifting and thin capitalization rules: German experience and alternative approach, 1-24

Sekar, A.,& Blushan, G.S. (2012). Thin capitalization and arm’s length principle. TheManagement Accountant, 528-535.

Sikka, P. (2013). Smoke and mirror: Corporate Social responsibility. Tax avoidance journal homepage. Retrieved from www.elseview.com/locate/accfor

Sikka, P.,& Murphy, R. (2015). Unitary taxation : Tax base and role. International Center for tax and Development working paper 34. Retrieved from http//:www.ictd.ac

Tailor, G., & Richardson, G. (2013). The Determinants of thingy Capitalized tax avoidance structures: Evidence from Australian Firms. Journal of International Accounting, Auditing and Taxation, 2, 12-25.

Tatum, M. (2010). The activities of multinationas. Retrieved from www.wisegeck.com/what-is-a-multinational

Tax Justice Network [TJN], (2013). International Business Taxation: A study in the internationalization of business regulations, Cambridge : Cambridge University press. Retrieved from http://www.taxjustice.network/cm/upload/pdf/international-busines-taxation

Udo, J. E. (2015). Taxing the internal economy in Nigeria: issues, challenge and opportunities. International Journal of Business and Social Science, 6(10), 160-175.

Uzonwanne, M.C. (2015). The indispensable role of taxation for state development in Nigeria. International Journal of Economic Research, 15, 48-59.

Weisbach, D. A. (2002). Ten truths about Tax shelters, 55 Tax L. Rev. 215.