Embed Size (px)

Citation preview

This is How You Can Beat the Market WithoutFail

January 10, 2020by Chuck Carnevaleof F.A.S.T. Graphs

Introduction

With this article I am going to present several ways that investors, especially retired investors, can beatthe market without fail. However, what I will be presenting may not be what you are expecting,particularly if you have a narrow notion of what beating the market means. In other words, one of myprimary objectives will be to expand your mind and attitudes regarding what investment performance istruly all about.

Moreover, this speaks to one of my biggest pet peeves as a financial professional, which is listening tothe common refrain that most active managers can’t beat the market (S&P 500). The reason thisaggravates me so much, is that I have never found it practical or useful as a professional manager toeven try to “beat the market.” Investors are unique, and as such, possess investment objectives thatare also unique to their own goals, objectives and risk tolerances.

Simply stated, investing is not a one-size-fits-all. Therefore, it has always made more sense – to me atleast – to manage portfolios that were designed to meet the individual client’s specific goals, objectivesand risk tolerances. In other words, I prefer to design portfolios that get the job done and often withoutregard to short-term price volatility.

More to the point, the market (S&P 500) simply may not be a suitable investment for every client. Onthe other hand, this does not simultaneously suggest that those investors should not invest in stocks atall. Instead, investors might be better served to build a portfolio of individual stocks that meets theirspecific goals, objectives and risk tolerances. A good example could be a portfolio of blue-chip dividendaristocrats with a long history of increasing their dividend every year. In contrast, the S&P 500 wouldalso include stocks that don’t even pay a dividend.

As I will illustrate later in the article, and in the accompanying video, a quality dividend growth stockwith a starting current yield that is higher than the S&P 500 and at the same time fairly valued willproduce more dividend income than the market the majority of time, if not over every timeframe. Inother words, it will beat the market based on total income produced, and is highly likely to meet or beatit on a capital appreciation basis over the long run as well. Superior businesses bought at fair value will

Page 1, ©2020 Advisor Perspectives, Inc. All rights reserved.

generally produce above-average (the market is an average) results over the long run.

Building Investment Portfolios to Meet Your Goals, Objectives and Risk Tolerances

To summarize, total return may not be the only criteria with which to judge a portfolio’s performanceby. The amount of income the portfolio is generating relative to the market may be a more importantobjective that is often overlooked. The amount of risk taken would be another. Nevertheless,generating more income than would be available from the market (S&P 500) is a relevant objective forinvestors in retirement that are fortunate enough to be able to live off their dividends.

This would further explain why investors might choose bonds, CDs or other fixed income securities.These are typically not purchased with the goal of beating the market. Instead, fixed incomeinvestments are normally purchased because of the safety and/or predictability they offer and forhigher current income if available. (Note: this can be difficult to accomplish today due to our long-running low interest rate environment).

Realized Versus Unrealized Gains and Losses

Additionally, performance calculations that include unrealized gains and losses can also be problematicand dangerous to an investor’s long-term financial security. For example, investors that were pouringmoney into technology stocks in 1998, 1999 and 2000 were crushing the market during thattimeframe. However, only two or three years later many of those same investors had lost 80 or 90% oftheir hard-earned money. The “false profits” (unrealized gains) of the technology bubble magically andin short order dissipated before their very eyes. Suddenly, the same investors who once were trouncingthe market, where suddenly substantially underperforming the market.

The lesson of the story is that unrealized gains can quickly turn into losses, while unrealized losses canquickly turn into gains. Stock prices are temporary in nature, but fundamentals are more enduring.Once again, it’s a fact that the market does not always correctly price stocks. This is precisely why Iam on record many times of stating that measuring performance without simultaneously measuringvaluation is a job half done. But more to the point, when I measure stock performance, I considerwhether I am measuring an undervalued opportunity or an overvalued risky investment.

This also empowers me to make a risk assessment of the total returns I may be receiving at any pointin time. In other words, are current market values justified by fundamental values or not? If not, Irecognize that my money is at risk and that inevitably true worth value will eventually and inevitablyrevert to the mean.

The point is that I first and foremost acknowledge the undeniable reality that the market does notalways price a common stock correctly. Consequently, in addition to measuring performance solely oncurrent market price, I also measure performance based on fundamental value. I will be elaboratingmore on this in the video portion of this article. I believe this approach provides a much clearerperspective of how a given stock portfolio is really performing relative to the specific needs of theinvestor.

Page 2, ©2020 Advisor Perspectives, Inc. All rights reserved.

Case Study: Dividend Income and Preservation of Capital

As a portfolio manager spanning many decades, I can tell you with absolute certainty that eachindividual investor’s case is unique and different. Consequently, as a portfolio manager, I consider itincumbent upon me to specifically design every individual’s portfolio relative to their unique situation,goals, objectives and risk tolerances. As previously stated, investing is not a one-size-fits-all exercise.

Just as an example, let’s consider two individuals where both desire maximum current and futureincome. However, one has enough money to meet their lifestyle needs and the other doesn’t.Therefore, even though they have the same objective, and possibly even the same risk tolerances,their situations would require a different strategy and approach.

Therefore, for the client that has adequate assets to meet their needs relative to the amount of incomethat can be achieved, I would focus more on the sustainability and growth of the income. For the otherinvestor I might prioritize the growth component because this investor does not have adequate assetsto simply live off their income alone. In other words, in order to meet their lifestyle, they would berequired to harvest a certain amount of principal each year. This creates many challenges. When youharvest principle, you have less assets with which to generate future income from.

Consequently, both growth (capital appreciation) and income growth (dividend growth) becomeprogressively harder to achieve over time. On the other hand, if your assets are large enough to meetyour current needs and your portfolio is designed to continue growing your income in the future, youcan live comfortably off of the income (and growth thereof) that your assets can generate over time.Having enough assets to live off the dividend income your portfolio produces is the ultimate dividendgrowth investor scenario. Not only can you maintain your lifestyle, but you can also look forward to araise in pay each year just as you did when you were working.

Therefore, the sad part of this scenario is that investor 1 (adequate assets) can take on less riskwhereas investor 2 (insufficient assets) must continue taking on greater risk in order to achieve growthso they do not eventually run out of money. The point here is that dividend income and growth is muchmore reliable and easier to predict and manage than capital appreciation. Therefore, the message toyounger investors is to save as much as you can as consistently as you can so that you can eventuallyaccumulate enough assets to be able to live off your dividends and continue enjoying growth of bothincome and principle over time.

Stock Prices Are Erratic and Unpredictable-Dividends Are Persistent and More Predictable

The title of this section is based on common sense; however, common sense is not always thatcommon. It becomes very easy to get caught up in all the hype and hysteria that goes with investing inliquid markets where we sometimes neglect or overlook the obvious.

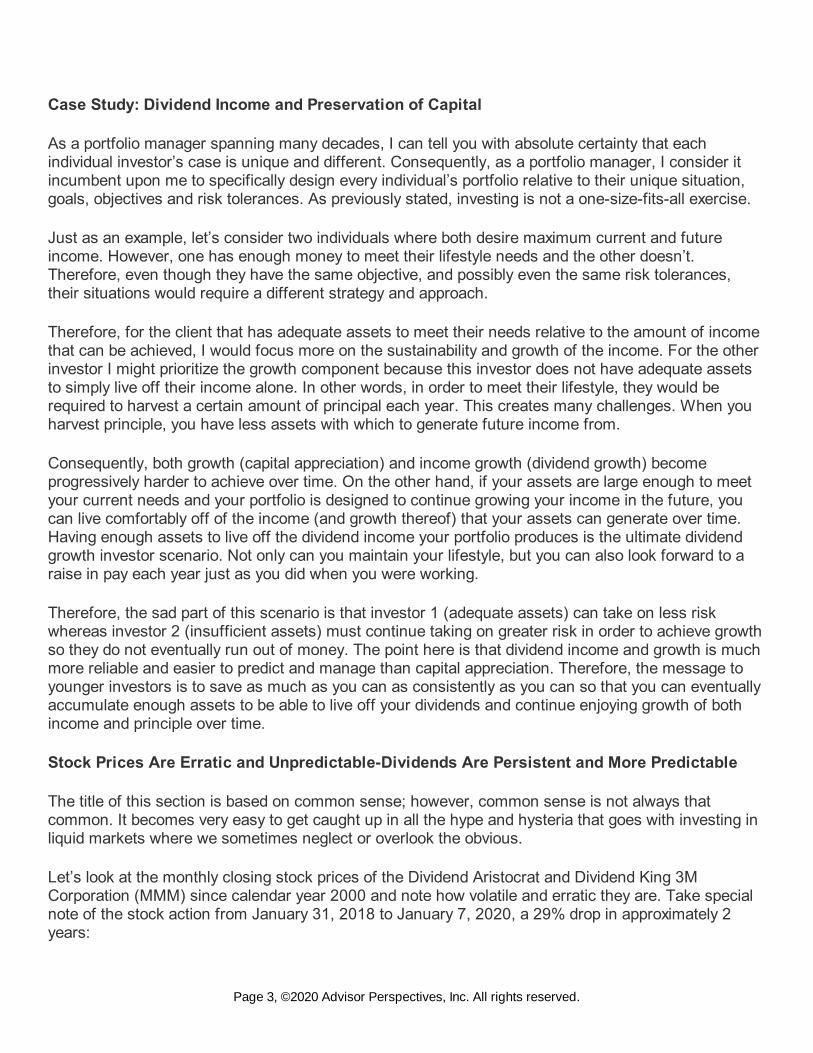

Let’s look at the monthly closing stock prices of the Dividend Aristocrat and Dividend King 3MCorporation (MMM) since calendar year 2000 and note how volatile and erratic they are. Take specialnote of the stock action from January 31, 2018 to January 7, 2020, a 29% drop in approximately 2years:

Page 3, ©2020 Advisor Perspectives, Inc. All rights reserved.

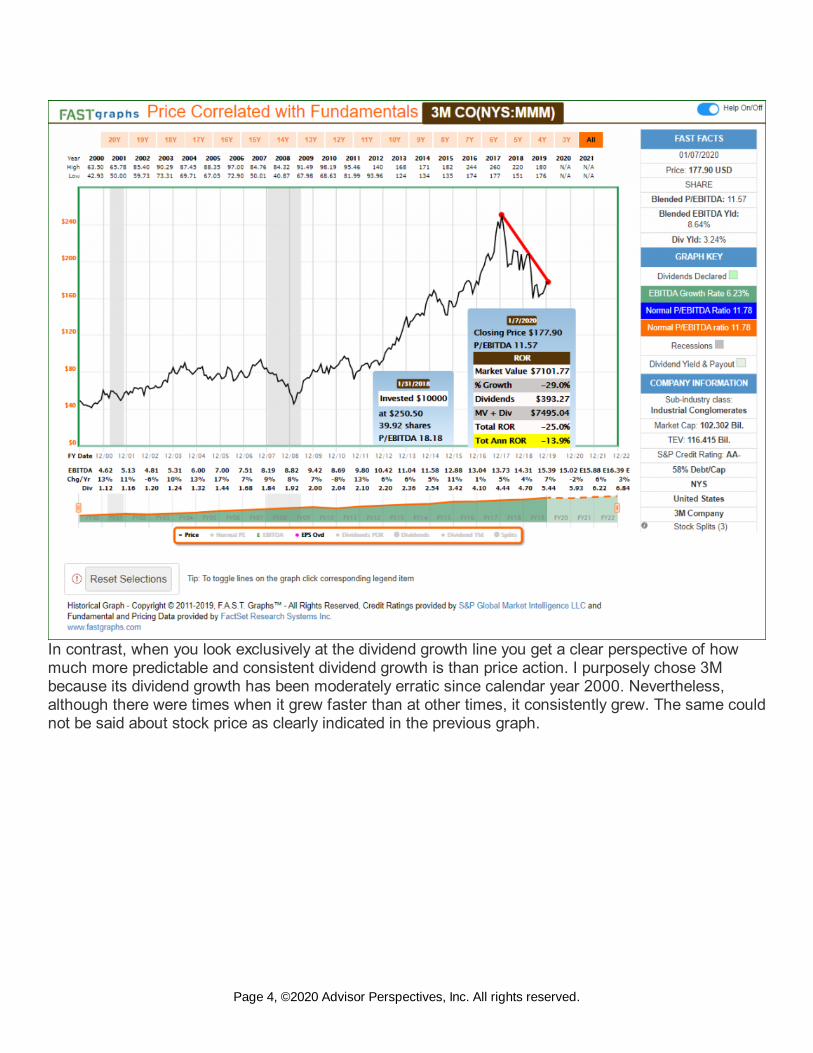

In contrast, when you look exclusively at the dividend growth line you get a clear perspective of howmuch more predictable and consistent dividend growth is than price action. I purposely chose 3Mbecause its dividend growth has been moderately erratic since calendar year 2000. Nevertheless,although there were times when it grew faster than at other times, it consistently grew. The same couldnot be said about stock price as clearly indicated in the previous graph.

Page 4, ©2020 Advisor Perspectives, Inc. All rights reserved.

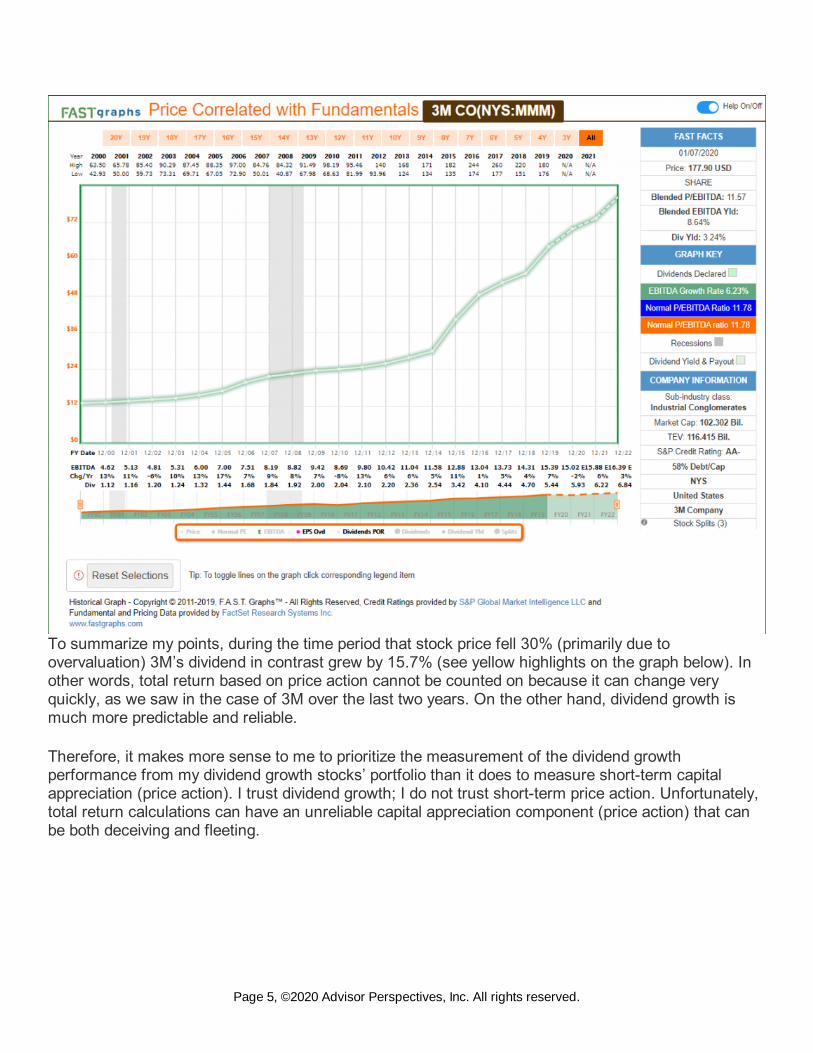

To summarize my points, during the time period that stock price fell 30% (primarily due toovervaluation) 3M’s dividend in contrast grew by 15.7% (see yellow highlights on the graph below). Inother words, total return based on price action cannot be counted on because it can change veryquickly, as we saw in the case of 3M over the last two years. On the other hand, dividend growth ismuch more predictable and reliable.

Therefore, it makes more sense to me to prioritize the measurement of the dividend growthperformance from my dividend growth stocks’ portfolio than it does to measure short-term capitalappreciation (price action). I trust dividend growth; I do not trust short-term price action. Unfortunately,total return calculations can have an unreliable capital appreciation component (price action) that canbe both deceiving and fleeting.

Page 5, ©2020 Advisor Perspectives, Inc. All rights reserved.

How You Can Beat the Market Without Fail

I want to start out by stating that I am confident that the strategy I’m about to share will outperform themarket (S&P 500) over the long run on a total return basis. However, I do not necessarily believe that itwill outperform the S&P 500 over the shorter run, although it is possible that it would. Nevertheless, mypoint is that from a total return perspective, all bets are off on the short run. The market is simply toounpredictable (volatile) and most often irrational over short periods of time to have any confidenceregarding how it might perform short-term.

On the other hand, there is a significant amount of evidence that suggests that the overall market, andmost importantly, each individual stock in the market will eventually reflect its fair value based on itsoperating success. In other words, whenever stocks become disconnected from fair value over orunder, they will eventually and inevitably revert to the mean. The exact timing is not precise, but theend result over time is virtually a certainty. In my experience, every great investor I have ever studiedbases their long-term decisions on those realities.

Nevertheless, I do believe that there are reliable ways to outperform the market without fail when your

Page 6, ©2020 Advisor Perspectives, Inc. All rights reserved.

focus is on those elements that are predictable such as dividends and dividend growth as discussedabove. Stated differently, I am supremely confident that investors can build a portfolio of dividendgrowth stocks that will produce more income than they can get from investing in an index fund (theS&P 500) without fail. What follows is a simple step-by-step common sense-based strategy that hasworked flawlessly for me.

1. Look for quality: Start out by identifying high quality blue-chip dividend growth stocks. TheDividend Aristocrats, Champions and Kings are great sources of potential ideas.

2. Identify attractive valuation: Next, screen the above lists for companies that are fairly valued,which to me means currently offering an earnings yield of 6 ½% or higher – and the higher thebetter. Also, the reader should recognize that an undervalued stock provides what I like to callnatural leverage. Future capital appreciation of an undervalued stock will be relative to futuregrowth plus the opportunity for multiple expansion. Consequently, with an undervalued stock youcan expect a lower future growth rate and still generate outsized returns.

3. Seek above-average current dividend yield: Then screen those attractively valued dividendgrowth stocks for those that offer current yields that are greater than the market average.Currently the S&P 500 offers a dividend yield of 1.85%. Therefore, I look for current yields of 2 ½% or better in order to provide a comfortable margin of safety or cushion.

4. Look for above-average future growth: After that, I turn my focus to operating growth, bothhistorical and expected future. With this step I am primarily looking at earnings growth, cash flowgrowth and EBITDA growth. Keep in mind that my focus is on sustainable dividends and dividendgrowth. Therefore, I am looking for confidence that the dividend is well covered and has thepotential to grow at above-average rates going forward.

To complement the above strategy, I also put emphasis on persistent or consistent growth. Althoughgood results can be accomplished with cyclical or quasi-cyclical businesses, the steady endings tend toengender confidence. Therefore, it is easier to stay the course with persistent growers, especiallyduring turbulent market environments.

FAST Graphs Analyze Out Loud Video: 9 Dividend Growth Stocks: Greater Income Than theMarket – Broadcom (AVGO), Bristol Myers Squibb (BMY), Caterpillar (CAT), Cummins (CMI),Omnicom (OMC), Principal Financial (PFG), Prudential Financial (PRU), Royal Bank of Canada(RY), Simon Property Group (SPG) and S&P 500

In the following analyze out loud video I present 9 dividend growth stocks that I believe can producemore dividend income than the S&P 500 going forward.

Summary and Conclusions

The key to understanding and appreciating the relevance of focusing on dividend income performanceover price performance is the recognition that dividends are paid on the number of shares you own.And are not adjusted by price changes. Therefore, you could go through a timeframe where stock priceis dropping and still maintain your lifestyle because your dividends are increasing.

This happened with virtually every Dividend Aristocrat and/or Dividend Champion during the GreatRecession of 2008. Even though stock prices were falling, investors in these blue-chip dividend growth

Page 7, ©2020 Advisor Perspectives, Inc. All rights reserved.

stocks were enjoying income growth. In other words, the dividend income portion of their portfolioswere insulated from the ravages of the bear market.

Furthermore, dividend growth investors, especially those in retirement, can rely on dividend growthstocks to provide them an inflation-fighting growing future dividend income stream. This is a primaryadvantage of investing in dividend growth stocks over fixed income. Although this advantage appliesunder all interest rate environments, it is especially advantageous when rates on fixed income are lowas they are today. To be clear, I am not against fixed income in the general sense if the coupons arehigh enough. However, I am not too keen on fixed income in an environment like today where I can gethigher current yields that are growing from quality dividend growth stocks.

For these reasons and others, I believe investors are best served by designing their portfolios so thatthey can meet their specific goals, objectives and risk tolerances. In my mind, this is a much morerational benchmark than something as vague as worrying about beating the market. Even if I beat themarket, my portfolio may not be meeting my needs. At the end of the day, stock price volatility –especially over the short run – is too unpredictable to bet my future on. A continuously rising stream ofincome makes much more sense to me.

© F.A.S.T. Graphs

Page 8, ©2020 Advisor Perspectives, Inc. All rights reserved.