Embed Size (px)

Citation preview

THIS IS NEITHER AN OFFER TO SELL NOR A SOLICITATION OF AN OFFER TO BUY THE SECURITIES DESCRIBED HEREIN. AN OFFERING IS MADE ONLY BY PROSPECTUS. THIS LITERATURE MUST BE PRECEDED OR ACCOMPANIED BY A CURRENT PROSPECTUS. AS SUCH, A COPY OF THE CURRENT PROSPECTUS MUST BE MADE AVAILABLE TO YOU IN CONNECTION WITH THIS OFFERING AND SHOULD BE READ IN ORDER TO UNDERSTAND FULLY ALL OF THE IMPLICATIONS AND RISKS OF THIS OFFERING. No offering is made except by a prospectus filed with the Department of Law of the State of New York. Neither the Attorney-General of the State of New York nor any other state or federal regulator has passed on or endorsed the merits of this offering or these securities or confirmed the adequacy or accuracy of the prospectus. Any representation to the contrary is unlawful. All information contained in this material is qualified in its entirety by the terms of the current prospectus. The achievement of any goals is not guaranteed. An investment should only be made after a careful review of the prospectus. Realty Capital Securities, LLC One Beacon Street, 14th Floor, Boston, MA 02108 | 877-373-2522

Publicly Registered Non-Traded Real Estate Investment Trust*

*American Reality Capital Hospitality Trust, Inc., intends to elect and qualify as a real estate investment trust (“REIT”) commencing with the tax year ending December 31, 2013.

Investing in our common stock involves a high degree of risk. You should purchase these securities only if you can afford a complete loss of your investment. See the section entitled “Risk Factors” beginning on page 30 of the prospectus for a discussion of the risks which should be considered in connection with your investment in our common stock including:

• We have no prior operating history or established financing sources and will rely on our advisor to conduct our operations. Our advisor has no operating history and is a newly formed entity which has no experience operating a public company

• There is no guarantee that distributions will be paid. If distributions are declared and paid, the amount of the distributions paid may decrease or distributions may be eliminated at any time. Due to the risks involved in the ownership of real estate, there is no guarantee of any return on your investment, and you may lose all or a portion of your investment

• We are a “blind pool” offering because we currently do not own any properties and we have not identified any properties to acquire, other than the six hotel properties identified under “Description of Potential Real Estate Investments.” Since we have neither identified nor acquired any investments, other than the six hotel properties identified under “Description of Potential Real Estate Investments,” you will not have the opportunity to evaluate the merits and/or demerits of such investments prior to your purchase of our common stock

• Because we are dependent upon our advisor, our property manager, our sub-property manager and their affiliates to conduct our operations, any adverse changes in the financial health of such entities or our relationship with such entities could hinder our operating performance and the return on our stockholders’ investments

• No public market exists for our shares of common stock, nor may a public market ever exist and our shares are, and may continue to be, illiquid. Our share repurchase program may be the only way to dispose of your shares, but there are a number of limitations placed on such repurchases. See “Share Repurchase Program;”

• Market conditions and other factors could cause us to delay our liquidity event beyond the sixth anniversary of the termination of the primary offering. We also cannot assure you that we will be able to achieve a liquidity event

RISK FACTORS

American Realty Capital Hospitality Trust, Inc. 2

• We established the initial offering price on an arbitrary basis; as a result, the actual value of your investment may be substantially less than what you pay

• There are substantial conflicts among the interests of our investors, our interests and the interests of our advisor, property manager, our sub-property manager, our sponsor, our dealer manager and our and their respective affiliates, which could result in decisions that are not in the best interests of our stockholders

• The parent of our sponsor is the direct or indirect sponsor of twelve other publicly offered investment programs which invest generally in real estate assets, but not primarily in our target assets, most of which has more resources than we do

• We may change our investment objectives and strategies without stockholder consent• We are obligated to pay substantial fees to our advisor, which may result in our advisor recommending riskier investments• We are obligated to pay the special limited partner a subordinated distribution upon termination of the advisory agreement,

which may be substantial and therefore may discourage us from terminating the advisor• We may incur substantial debt, which could hinder our ability to pay distributions to our stockholders or could decrease the

value of your investment if income on, or the value of, the property securing the debt falls• Our organizational documents permit us to pay distributions from any source, including unlimited amounts from offering

proceeds and borrowings. Any of these distributions may reduce the amount of capital we ultimately invest in properties and other permitted investments and negatively impact the value of your investment, especially if a substantial portion of our distributions are paid from offering proceeds

• Our failure to qualify or remain qualified as a REIT would result in higher taxes, may adversely affect our operations, would reduce the amount of income available for distribution and would limit our ability to make distributions to our stockholders

• Commencing with the NAV pricing date, the offering price for shares in our primary offering and pursuant to our DRIP, as well as the repurchase price for our shares, will be based on NAV, which may not accurately reflect the value of our assets

• There are limitations on ownership and transferability of our shares. Please see “Description of Securities — Restrictions on Ownership and Transfer.”

RISK FACTORS

American Realty Capital Hospitality Trust, Inc. 3

FORWARD LOOKING STATEMENT DISCLOSURE

Certain statements made in this presentation are forward-looking statements. Those statements include statements regarding the intent, belief or current expectations of American Realty Capital Hospitality Trust, Inc. (“ARC Hospitality”) and members of its management team, as well as the assumptions on which such statements are based, and generally are identified by the use of words such as “may,” “will,” “seeks,” “anticipates,” “believes,” “estimates,” “expects,” “plans,” “intends,” “should” or similar expressions. Actual results may differ materially from those contemplated by such forward-looking statements. Further, forward-looking statements speak only as of the date they are made, and ARC Hospitality undertakes no obligation to update or revise forward-looking statements to reflect changed assumptions, the occurrence of unanticipated events or changes to future operating results over time, unless required by law. The following are some of the risks and uncertainties, although not all risks and uncertainties, that could cause ARC Hospitality’s actual results to differ materially from those presented in our forward-looking statements:

• While ARC Hospitality is raising capital and investing the proceeds of its on-going initial public offering, the competition for the type of properties it desires to acquire may cause its distributions and the long-term returns of its investors to be lower than they otherwise would be.

• ARC Hospitality depends on room occupancy for its revenue, and, accordingly, its revenue is dependent upon the success and economic viability of its hotel properties.

• No public market currently exists, or may ever exist, for shares of ARC Hospitality common stock and ARC Hospitality shares are, and may continue to be, illiquid.

• ARC Hospitality may be unable to pay or maintain cash distributions or increase distributions over time.• ARC Hospitality is obligated to pay substantial fees to its advisor and its advisor's affiliates, including fees payable upon the

sale of properties.• ARC Hospitality is subject to risks associated with the significant dislocations and liquidity disruptions currently existing or

occurring in the United States' credit markets.

American Realty Capital Hospitality Trust, Inc. 4

American Realty Capital Hospitality Trust, Inc. seeks to:

Acquire institutional-quality, strategically-located lodging properties in North America, partnering with premium national brands and

operated by its experienced management company,Crestline Hotels & Resorts, LLC

Capital Preservation

Capital Appreciation

Monthly Cash

Distributions

ARC Hospitality seeks to provide:

American Realty Capital Hospitality Trust, Inc. 5

INVESTMENT FOCUS

American Realty Capital Hospitality Trust, Inc. 6

INVESTMENT OBJECTIVES

Luxury Hotels & Resorts

Premium Hotels

Full-Service Hotels

Select-Service Hotels

Budget Hotels

ARC Hospitality Trust seeks to acquire select-service and full-service hotels:

Located in high barrier-to-entry, supply-constrained markets near stable and diverse demand generators

Well-maintained, with minimum deferred maintenance or capital required

Purchased at a discount to replacement cost

American Realty Capital Hospitality Trust, Inc. 7

REPRESENTATIVE SELECT-SERVICE HOTEL

Replacement Cost / Room ~$225,000

Rate Per Night $120

Room Size 300± Sq Ft

Select-Service

Customer Profile

• Business Traveler • Small group / conference /

events• Family / social• Extended stay

Level of Service Moderate to High

Room Rates Moderate

Operating Costs Moderate

Typical Amenities / Services

• Limited food & beverage• Complimentary breakfast• Lounge• Fitness room and pool• Limited meeting space

Hypothetical Floor Plan

Note: This slide is for illustrative purposes to showcase the type of properties which ARC Hospitality seeks to target for acquisitions. ARC Hospitality may not necessarily acquire properties with an identical floor plan to the one above.

American Realty Capital Hospitality Trust, Inc. 8

REPRESENTATIVE FULL-SERVICE HOTEL

Replacement Cost / Room ~$300,000

Rate Per Night(1) $173

Room Size 350± Sq Ft

Full-Service

Customer Profile• Business Traveler• Group / conference / events• Family / social

Level of Service Higher

Room Rates Higher

Operating Costs Higher

Typical Amenities / Services

• A la carte restaurant, three meals per day

• Lounge• Fitness facility and pool• Meeting and conference

support services• Room service, bellmen and

concierge services

Hypothetical Floor Plan

Note: This slide is for illustrative purposes to showcase the type of properties which ARC Hospitality seeks to target for acquisitions. ARC Hospitality may not necessarily acquire properties with an identical floor plan to the one above.(1) Source: PKF Hospitality Research, LLC

American Realty Capital Hospitality Trust, Inc. 9

TARGET BRAND PARTNERS*

* Companies listed above do not endorse the investment security sold. Crestline has been contracted to manage the properties or subsidiary properties that ARC Hospitality hopes to affiliate with through property acquisitions.

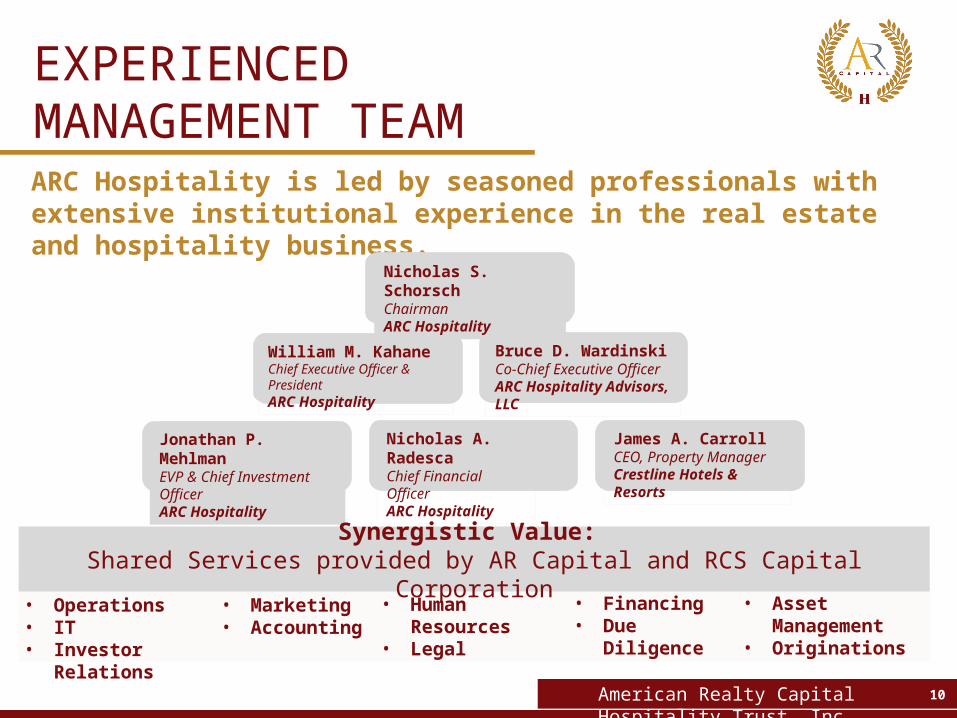

ARC Hospitality is led by seasoned professionals with extensive institutional experience in the real estate and hospitality business.

Bruce D. WardinskiCo-Chief Executive OfficerARC Hospitality Advisors, LLC

William M. KahaneChief Executive Officer & President ARC Hospitality

Nicholas A. RadescaChief Financial OfficerARC Hospitality

Jonathan P. MehlmanEVP & Chief Investment OfficerARC Hospitality

Nicholas S. SchorschChairmanARC Hospitality

James A. CarrollCEO, Property ManagerCrestline Hotels & Resorts

Synergistic Value: Shared Services provided by AR Capital and RCS Capital Corporation

• Operations• IT• Investor Relations

• Marketing• Accounting

• Human Resources• Legal

• Asset Management• Originations

• Financing• Due Diligence

American Realty Capital Hospitality Trust, Inc. 10

EXPERIENCED MANAGEMENT TEAM

• Has assisted its affiliates and its former affiliates in acquiring hotels with an aggregate value of over $3.4 billion. Such hotels include Marriott, Hilton, Starwood, Intercontinental Hotel Group, Wyndham and Hyatt.

• Crestline’s management team has been involved with structuring profitable exit strategies of assets through various means including initial public offerings and individual asset dispositions.

• Crestline’s executive team adopts a partnership approach with the hotel owners, investors and employees at each of its hotels, which ARC Hospitality believes enables them to maximize profitability in a hospitality-driven, guest-service-focused environment.

American Realty Capital Hospitality Trust, Inc. 11

Crestline Hotels & Resorts

EXPERIENCED PROPERTY MANAGERS

American Realty Capital Hospitality Trust, Inc. 12

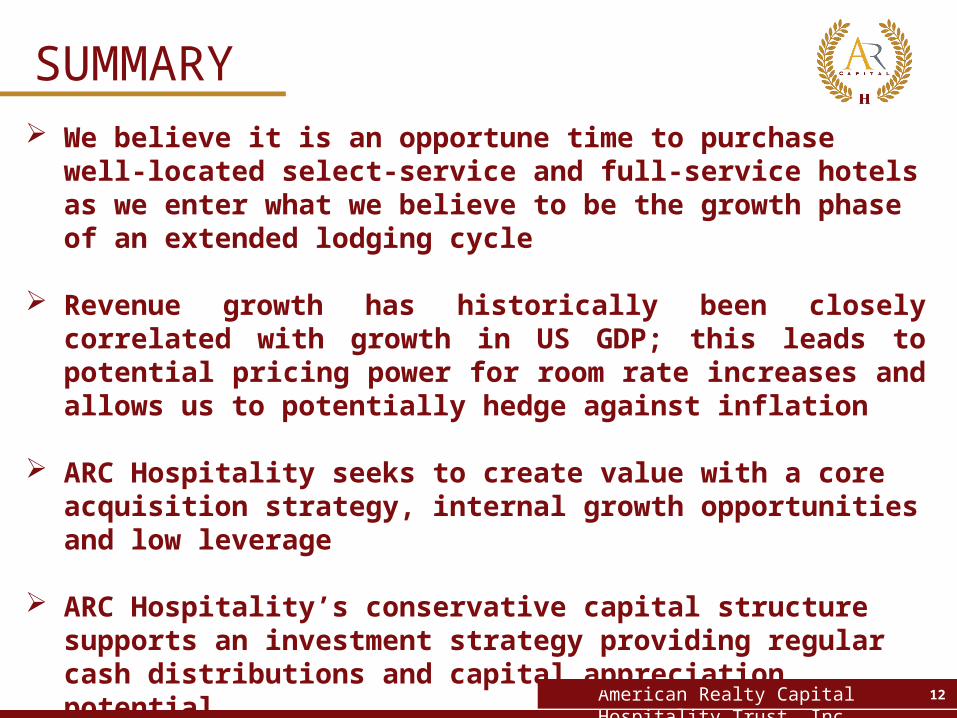

SUMMARY We believe it is an opportune time to purchase well-located select-

service and full-service hotels as we enter what we believe to be the growth phase of an extended lodging cycle

Revenue growth has historically been closely correlated with growth in US GDP; this leads to potential pricing power for room rate increases and allows us to potentially hedge against inflation

ARC Hospitality seeks to create value with a core acquisition strategy, internal growth opportunities and low leverage

ARC Hospitality’s conservative capital structure supports an investment strategy providing regular cash distributions and capital appreciation potential

American Realty Capital Hospitality Trust, Inc. 13

INVESTMENT OPPORTUNITY

Third Party Research on a Recovering Economy… Average Annual RevPAR* growth of approximately 6.4% from 2010 through 2013(1)

Pricing Power and “One Night Leases”… Economic growth drives demand as unemployment declines and spending and travel increase – creating pricing power

Limited Supply…Limited new construction since 2008 and lack of hotel construction financing leads to lower room supply, less competition and, we believe the ability to drive rates

ARC Hospitality Believes There are Strong Underlying Hotel Fundamentals:

Why Invest in the Hospitality Sector Now?

* A performance metric in the hotel industry, which is calculated by multiplying a hotel's average daily room rate (ADR) by its occupancy rate. (1) PKF Hotel Horizons, March-May 2014 Edition American Realty Capital Hospitality Trust, Inc. 14

MARKET OPPORTUNITY

Rising Occupancy

Rates

Increasing ADR

Metrics

Expanding RevPAR Metrics

Stable Demand Growth

15American Realty Capital Hospitality Trust, Inc. 15

2008 2009 2010 2011 2012 2013 2014E 2015E (3.5%)

(2.5%)

(1.5%)

(0.5%)

0.5%

1.5%

2.5%

3.5%

(0.3%)

(2.8%)

2.5%1.8%

2.8%

1.9%2.3%

3.4%

Jan-

08

Jul-0

8

Jan-

09

Jul-0

9

Jan-

10

Jul-1

0

Jan-

11

Jul-1

1

Jan-

12

Jul-1

2

Jan-

13

Jul-1

3

Jan-

14-1000

-800-600-400-200

0200400600

2006 2007 2008 2009 2010 2011 2012 2013 2014E

6,477

5,030

4,1104,340 4,190 4,260

4,660

5,0904,925

Jan-

05

Jan-

06

Jan-

07

Jan-

08

Jan-

09

Jan-

10

Jan-

11

Jan-

12

Jan-

13

Jan-

1430.0

40.0

50.0

60.0

70.0

80.0

90.0

100.0

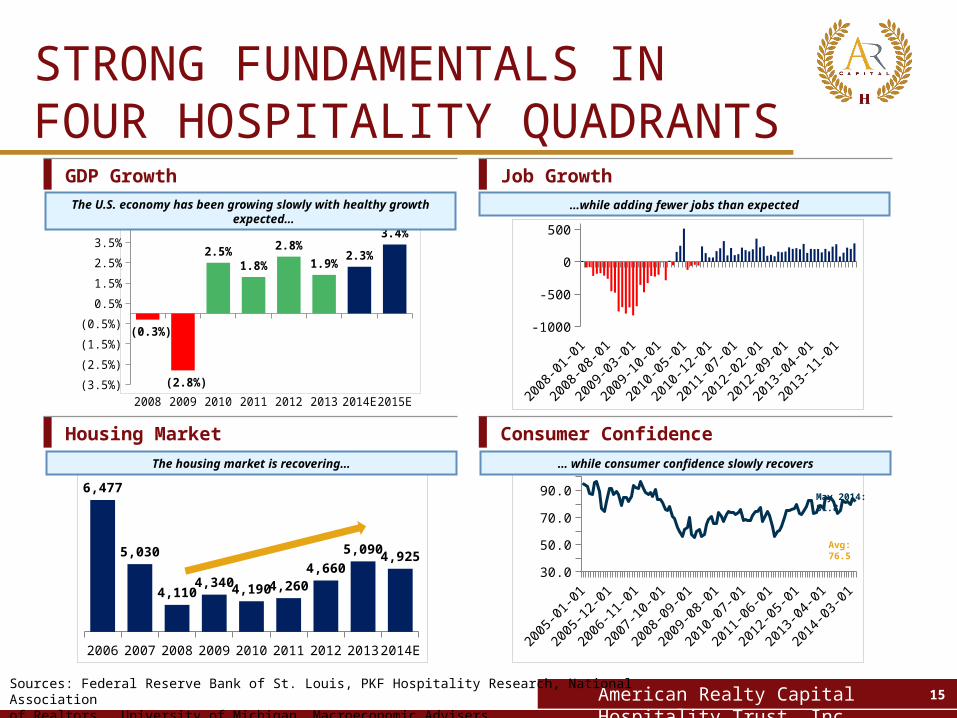

GDP Growth Job Growth

The U.S. economy has been growing slowly with healthy growth expected… …while adding fewer jobs than expected

The housing market is recovering… … while consumer confidence slowly recovers

Consumer ConfidenceHousing Market

Avg: 76.5

May 2014: 81.8

Sources: Federal Reserve Bank of St. Louis, PKF Hospitality Research, National Association of Realtors, University of Michigan, Macroeconomic Advisers

STRONG FUNDAMENTALS IN FOUR HOSPITALITY QUADRANTS

American Realty Capital Hospitality Trust, Inc. 16

ALTERNATIVE INDUSTRY FUNDAMENTALS

1998

1999

2000

2001

2002

2003

2004

2004

2005

2006

2007

2008

2009

2009

2010

2011

2012

2013

2014

-1.0%

0.0%

1.0%

2.0%

3.0%

4.0%

5.0%

6.0%

7.0%

1998

1999

2000

2001

2002

2003

2004

2004

2005

2006

2007

2008

2009

2009

2010

2011

2012

2013

2014

1.0%

2.0%

3.0%

4.0%

5.0%

6.0%

7.0%

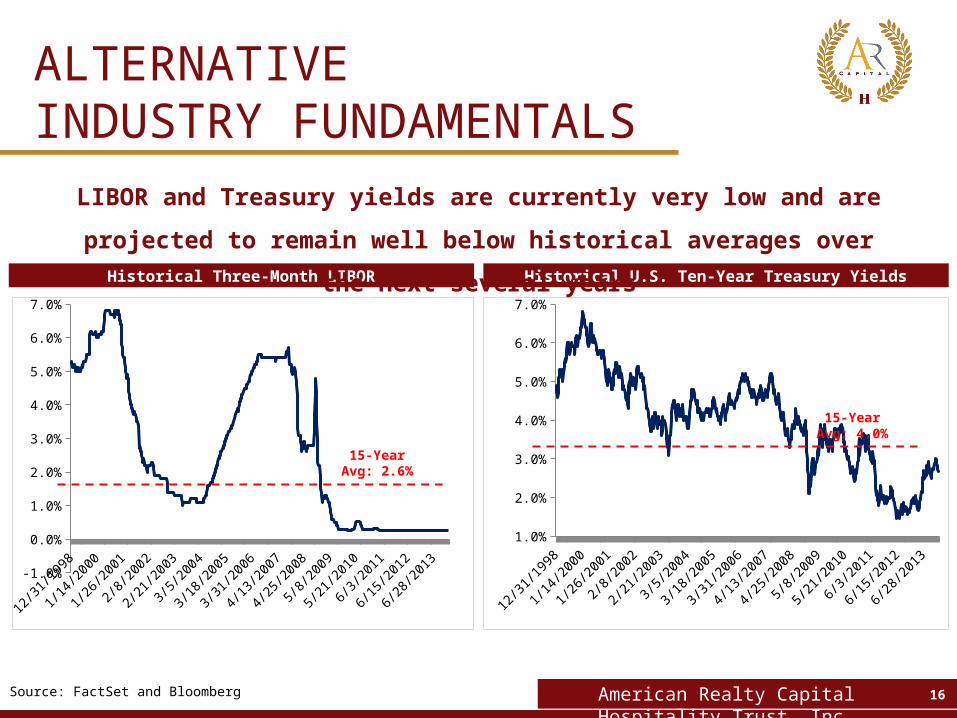

Historical Three-Month LIBOR Historical U.S. Ten-Year Treasury Yields

15-YearAvg: 2.6%

15-YearAvg: 4.0%

LIBOR and Treasury yields are currently very low and are projected to remain

well below historical averages over the next several years

Source: FactSet and Bloomberg

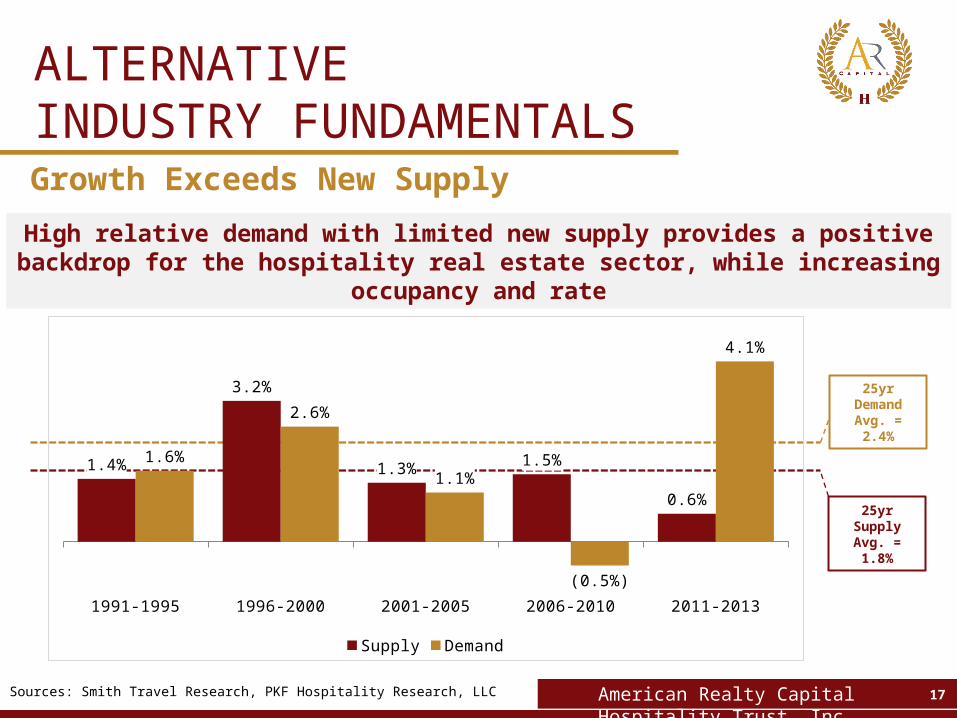

High relative demand with limited new supply provides a positive backdrop for the hospitality real estate sector, while increasing occupancy and rate

American Realty Capital Hospitality Trust, Inc. 17

Growth Exceeds New Supply

ALTERNATIVE INDUSTRY FUNDAMENTALS

Sources: Smith Travel Research, PKF Hospitality Research, LLC

1991-1995 1996-2000 2001-2005 2006-2010 2011-2013

1.4%

3.2%

1.3% 1.5%

0.6%

1.6%

2.6%

1.1%

(0.5%)

4.1%

Supply Demand

25yr Demand Avg. = 2.4%

25yr Supply Avg. = 1.8%

American Realty Capital Hospitality Trust, Inc. 18

Few Construction Starts = Low Supply Growth

ATTRACTIVE INDUSTRY FUNDAMENTALS

New hotel rooms under construction in the U.S. remain near historical lows, nearly 60% below 2007

Limited availability of construction financing is leading to fewer starts and more abandoned projects

2007 2008 2009 2010 2011 2012 Current

211,694185,119

97,302

51,914 54,103 67,92391,599

Historical Rooms Under Construction:

2007

Source: Smith Travel Research

2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013-0.8%

-0.6%

-0.4%

-0.2%

0.0%

0.2%

0.4%

0.6%

-15.0%

-10.0%

-5.0%

0.0%

5.0%

10.0%

15.0%

Monthly Job GrowthY/Y ADR Growth

*A metric widely used in the hospitality industry to indicate the average realized room rental per day.Source: Smith Travel Research and US Bureau of Labor Statistics

Good News for Lodging Given High Correlation Between Jobs and ADR* Growth

Job

G

row

thA

DR

G

rowth

American Realty Capital Hospitality Trust, Inc. 19

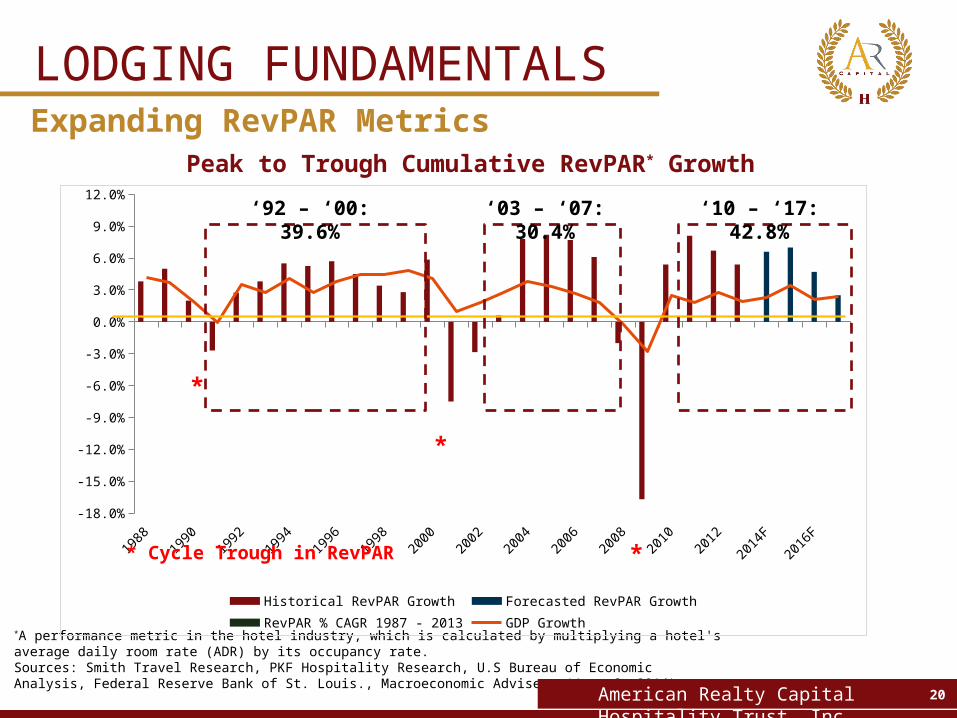

Increasing ADR Metrics

IMPROVING MACROECONOMIC FACTORS

*A performance metric in the hotel industry, which is calculated by multiplying a hotel's average daily room rate (ADR) by its occupancy rate.Sources: Smith Travel Research, PKF Hospitality Research, U.S Bureau of Economic Analysis, Federal Reserve Bank of St. Louis., Macroeconomic Advisers (June 6, 2014)

Peak to Trough Cumulative RevPAR* Growth

American Realty Capital Hospitality Trust, Inc. 20

Expanding RevPAR Metrics

LODGING FUNDAMENTALS

1988

1989

1990

1991

1992

1993

1994

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

2013

2014

F

2015

F

2016

F

2017

F-18.0%

-15.0%

-12.0%

-9.0%

-6.0%

-3.0%

0.0%

3.0%

6.0%

9.0%

12.0%

Historical RevPAR Growth Forecasted RevPAR Growth

RevPAR % CAGR 1987 - 2013 GDP Growth

*

*

** Cycle Trough in RevPAR

‘92 – ‘00: 39.6% ‘03 – ‘07: 30.4% ‘10 – ‘17: 42.8%

American Realty Capital Hospitality Trust, Inc. 21

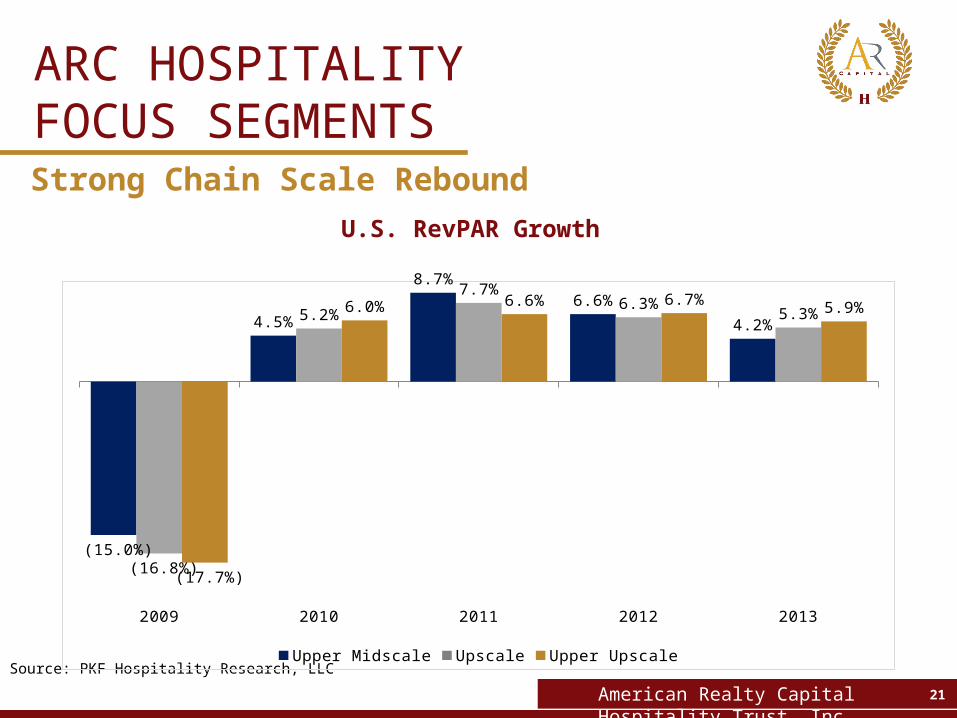

ARC HOSPITALITY FOCUS SEGMENTSStrong Chain Scale Rebound

Source: PKF Hospitality Research, LLC

2009 2010 2011 2012 2013

(15.0%)

4.5%

8.7%

6.6%

4.2%

(16.8%)

5.2%

7.7%6.3%

5.3%

(17.7%)

6.0% 6.6% 6.7% 5.9%

Upper Midscale Upscale Upper Upscale

U.S. RevPAR Growth

22

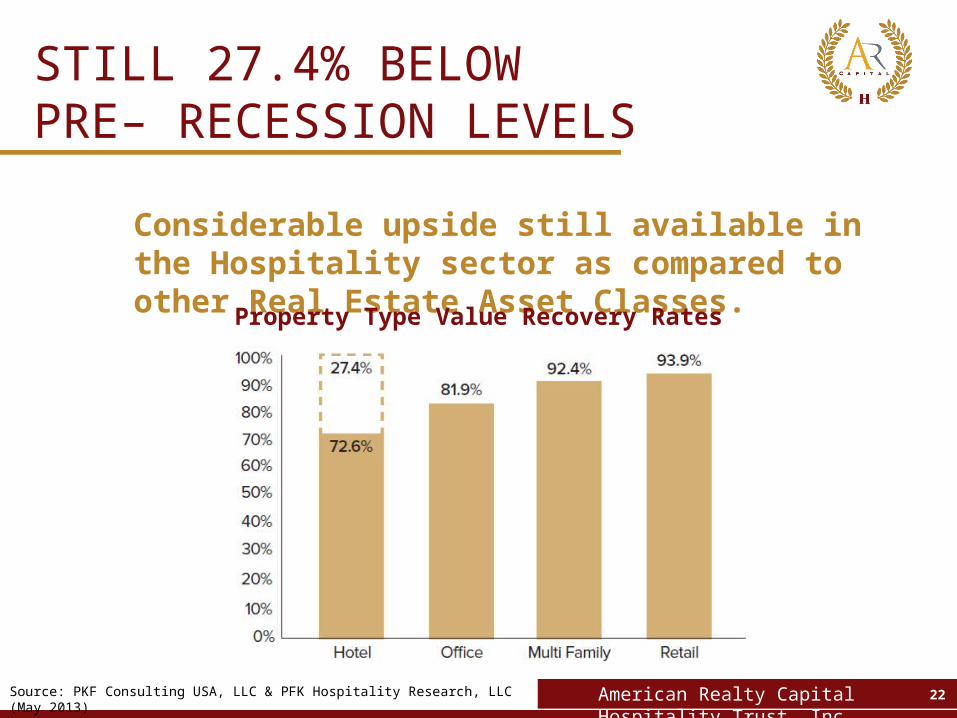

Considerable upside still available in the Hospitality sector as compared to other Real Estate Asset Classes.

American Realty Capital Hospitality Trust, Inc. 22

STILL 27.4% BELOW PRE– RECESSION LEVELS

Property Type Value Recovery Rates

Source: PKF Consulting USA, LLC & PFK Hospitality Research, LLC (May 2013)

Courtyard by Marriott

Location Baltimore, MD

Rooms 205

Courtyard by Marriott

Location Providence, RI

Rooms 216

Georgia Tech Hotel & Conference Center(1)

Location Atlanta, GA

Rooms 252

Hilton Garden Inn at Virginia Tech(2)

Location Blacksburg, VA

Rooms 137

Homewood Suites by Hilton

Location Stratford, CT

Rooms 135

Westin Hotel(2)

Location Norfolk/Virginia Beach, VA

Rooms 236

INITIAL HOTEL PORTFOLIO

(1) ARC Hospitality owns an operating leasehold interest in the property pictured (2) ARC Hospitality owns a minority interest in a joint venture for the property pictured American Realty Capital Hospitality Trust, Inc. 23

24

ARC Hospitality to Acquire Equity Inns Lodging Portfolio for $1.925 Billion

Purchase Creates One of the Largest Hospitality REITs in North America

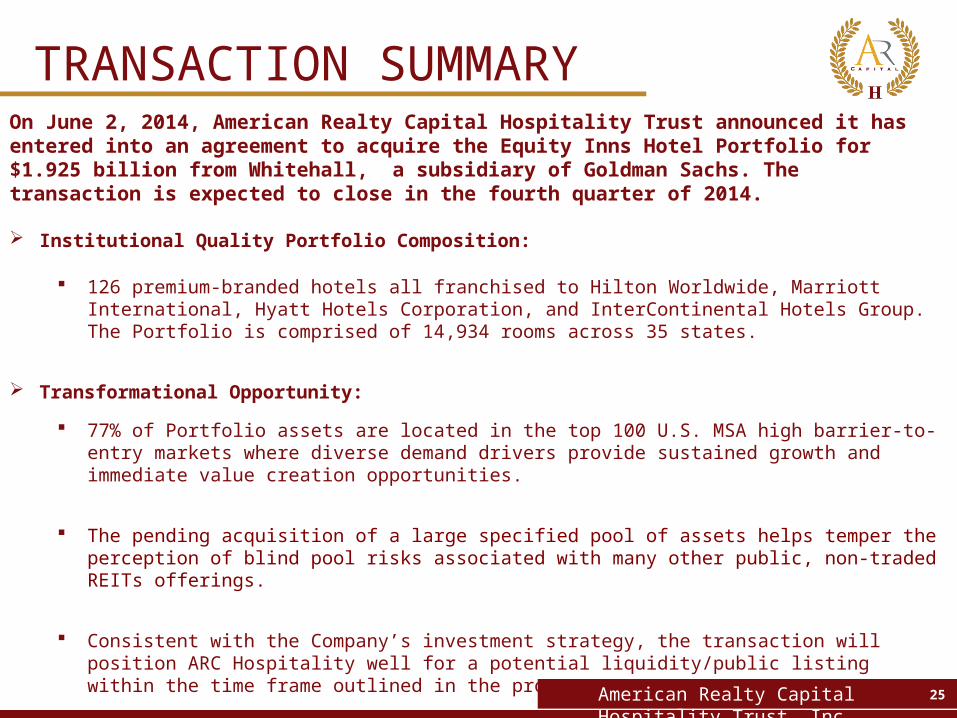

On June 2, 2014, American Realty Capital Hospitality Trust announced it has entered into an agreement to acquire the Equity Inns Hotel Portfolio for $1.925 billion from Whitehall, a subsidiary of Goldman Sachs. The transaction is expected to close in the fourth quarter of 2014.

Institutional Quality Portfolio Composition:

126 premium-branded hotels all franchised to Hilton Worldwide, Marriott International, Hyatt Hotels Corporation, and InterContinental Hotels Group. The Portfolio is comprised of 14,934 rooms across 35 states.

Transformational Opportunity:

77% of Portfolio assets are located in the top 100 U.S. MSA high barrier-to-entry markets where diverse demand drivers provide sustained growth and immediate value creation opportunities.

The pending acquisition of a large specified pool of assets helps temper the perception of blind pool risks associated with many other public, non-traded REITs offerings.

Consistent with the Company’s investment strategy, the transaction will position ARC Hospitality well for a potential liquidity/public listing within the time frame outlined in the prospectus.

TRANSACTION SUMMARY

American Realty Capital Hospitality Trust, Inc. 25

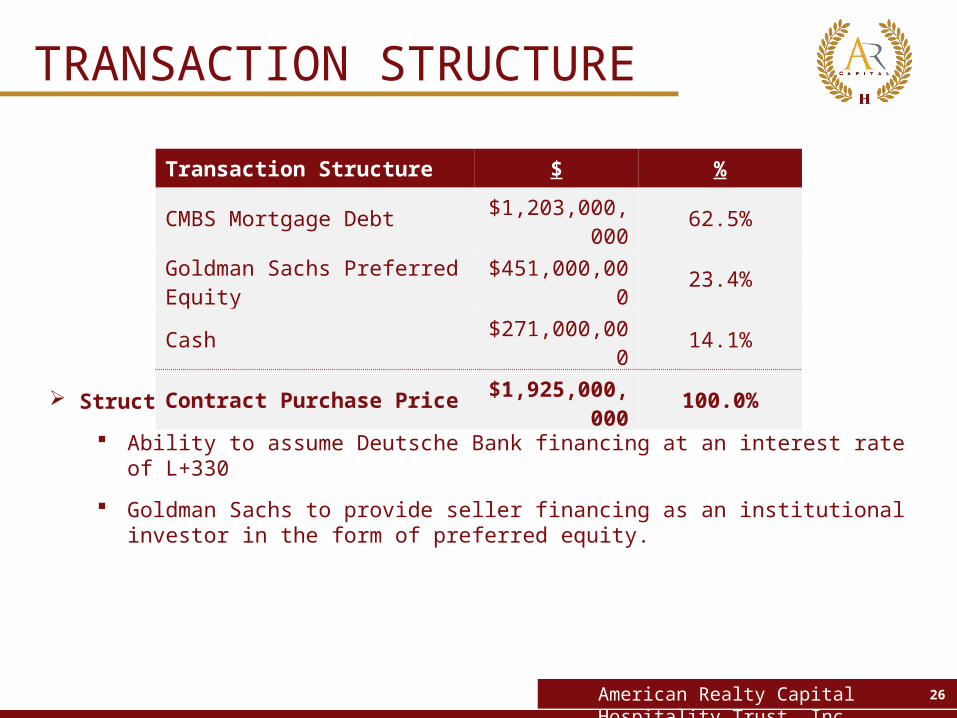

TRANSACTION STRUCTURE

Structure:

Ability to assume Deutsche Bank financing at an interest rate of L+330

Goldman Sachs to provide seller financing as an institutional investor in the form of preferred equity.

Transaction Structure $ %

CMBS Mortgage Debt $1,203,000,000 62.5%

Goldman Sachs Preferred Equity $451,000,000 23.4%

Cash $271,000,000 14.1%

Contract Purchase Price $1,925,000,000 100.0%

American Realty Capital Hospitality Trust, Inc. 26

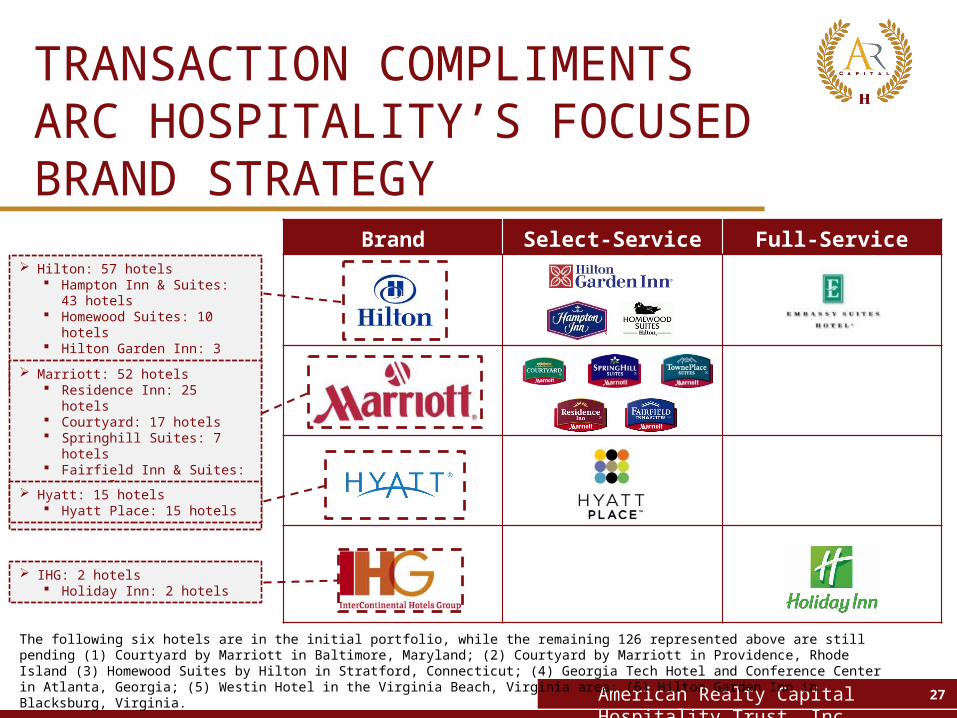

TRANSACTION COMPLIMENTS ARC HOSPITALITY’S FOCUSED BRAND STRATEGY

Brand Select-Service Full-Service Hilton: 57 hotels

Hampton Inn & Suites: 43 hotels Homewood Suites: 10 hotels Hilton Garden Inn: 3 hotels Embassy Suites: 1 hotel

Marriott: 52 hotels Residence Inn: 25 hotels Courtyard: 17 hotels Springhill Suites: 7 hotels Fairfield Inn & Suites: 2 hotels Towneplace Suites: 1 hotel

Hyatt: 15 hotels Hyatt Place: 15 hotels

IHG: 2 hotels Holiday Inn: 2 hotels

American Realty Capital Hospitality Trust, Inc. 27

The following six hotels are in the initial portfolio, while the remaining 126 represented above are still pending (1) Courtyard by Marriott in Baltimore, Maryland; (2) Courtyard by Marriott in Providence, Rhode Island (3) Homewood Suites by Hilton in Stratford, Connecticut; (4) Georgia Tech Hotel and Conference Center in Atlanta, Georgia; (5) Westin Hotel in the Virginia Beach, Virginia area; (6) Hilton Garden Inn in Blacksburg, Virginia.

SC

NJ

AL

NC

CA

IL

OH

MI

KY

GA

TX

TN

FL

3

3

4

4

4

5

5

5

6

8

11

11

22

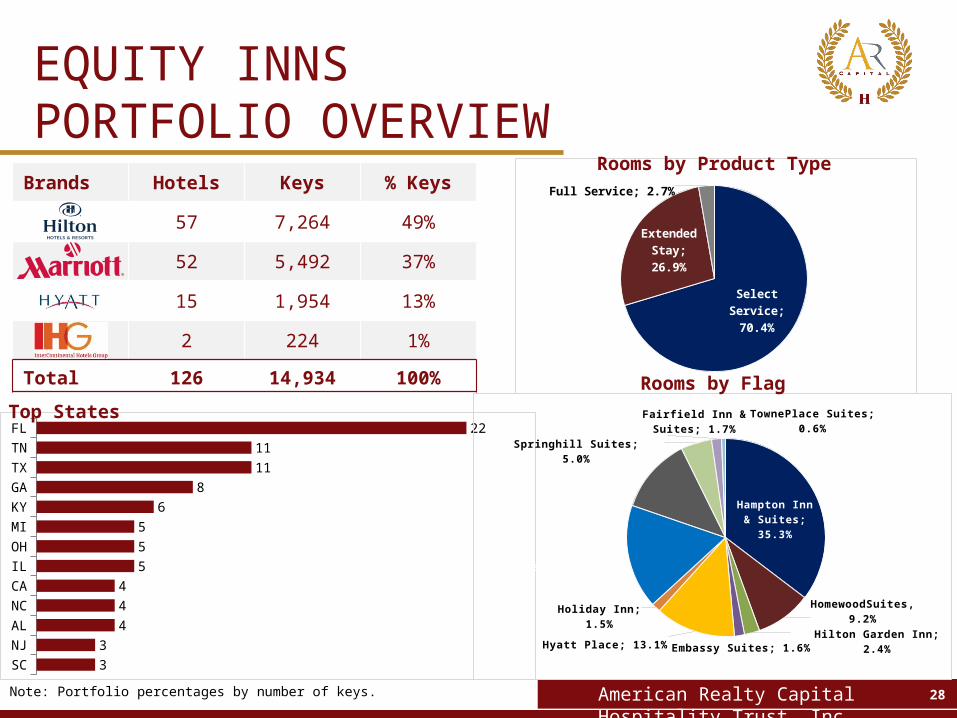

EQUITY INNS PORTFOLIO OVERVIEW

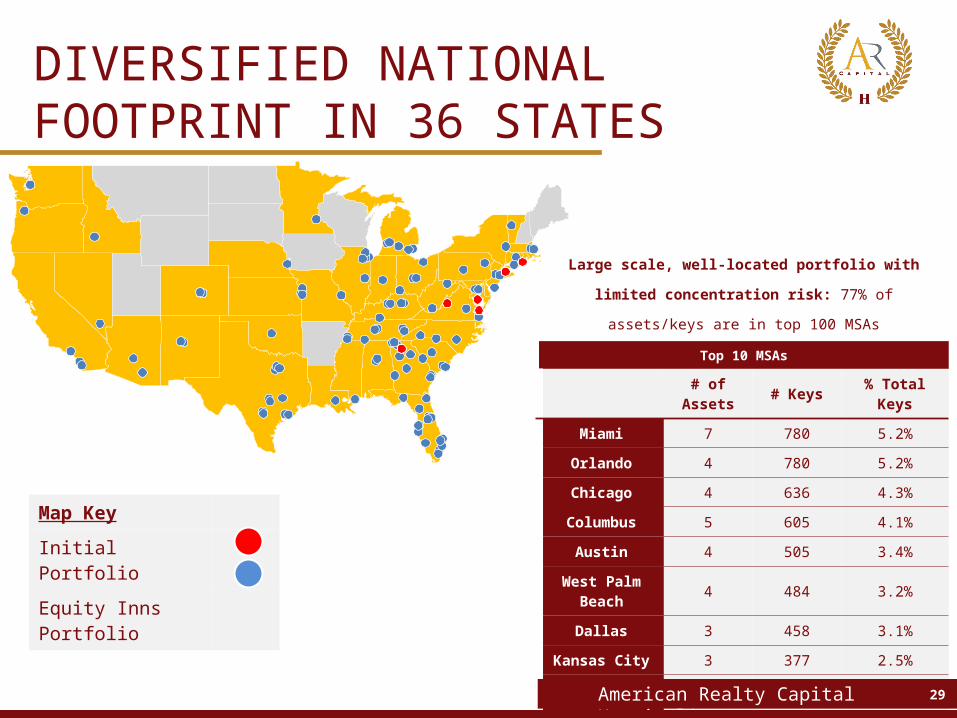

Note: Portfolio percentages by number of keys. American Realty Capital Hospitality Trust, Inc. 28

Hampton Inn & Suites; 35.3%

HomewoodSuites, 9.2%

Hilton Garden Inn; 2.4%Embassy Suites; 1.6%Hyatt Place; 13.1%

Holiday Inn; 1.5%

Residence Inn; 17.0%

Courtyard; 12.4%

Springhill Suites; 5.0%

Fairfield Inn & Suites; 1.7% TownePlace Suites; 0.6%

Select Ser-vice; 70.4%

Extended Stay; 26.9%

Full Service; 2.7%

Rooms by Product Type

Rooms by Flag

Brands Hotels Keys % Keys

57 7,264 49%

52 5,492 37%

15 1,954 13%

2 224 1%

Total 126 14,934 100%

Top States

Large scale, well-located portfolio with limited concentration

risk: 77% of assets/keys are in top 100 MSAs

Top 10 MSAs

# of Assets # Keys % Total Keys

Miami 7 780 5.2%

Orlando 4 780 5.2%

Chicago 4 636 4.3%

Columbus 5 605 4.1%

Austin 4 505 3.4%

West Palm Beach

4 484 3.2%

Dallas 3 458 3.1%

Kansas City 3 377 2.5%

San Diego 3 377 2.5%

Memphis 3 342 2.3%

29

Map Key

Initial Portfolio

Equity Inns Portfolio

˜̃̃̃

American Realty Capital Hospitality Trust, Inc. 29

DIVERSIFIED NATIONAL FOOTPRINT IN 36 STATES

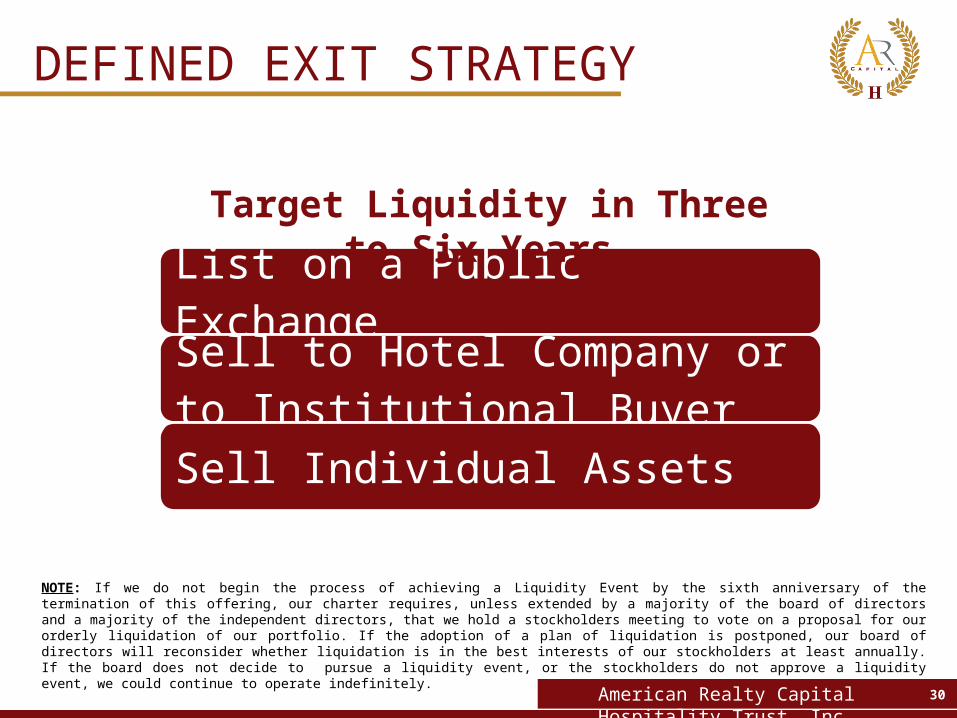

List on a Public Exchange

Sell to Hotel Company or to Institutional Buyer

Sell Individual Assets

Target Liquidity in Three to Six Years

NOTE: If we do not begin the process of achieving a Liquidity Event by the sixth anniversary of the termination of this offering, our charter requires, unless extended by a majority of the board of directors and a majority of the independent directors, that we hold a stockholders meeting to vote on a proposal for our orderly liquidation of our portfolio. If the adoption of a plan of liquidation is postponed, our board of directors will reconsider whether liquidation is in the best interests of our stockholders at least annually. If the board does not decide to pursue a liquidity event, or the stockholders do not approve a liquidity event, we could continue to operate indefinitely.

American Realty Capital Hospitality Trust, Inc. 30

DEFINED EXIT STRATEGY

American Realty Capital Hospitality Trust, Inc. 31

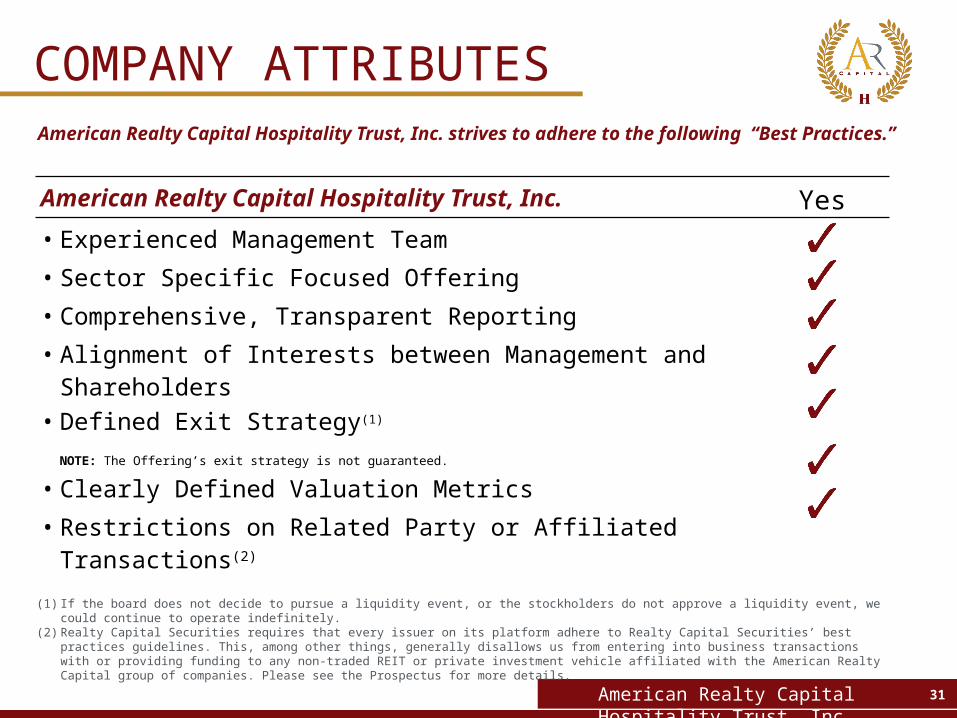

COMPANY ATTRIBUTES

American Realty Capital Hospitality Trust, Inc. Yes

• Experienced Management Team

• Sector Specific Focused Offering

• Comprehensive, Transparent Reporting

• Alignment of Interests between Management and Shareholders

• Defined Exit Strategy(1)

NOTE: The Offering’s exit strategy is not guaranteed.

• Clearly Defined Valuation Metrics

• Restrictions on Related Party or Affiliated Transactions(2)

American Realty Capital Hospitality Trust, Inc. strives to adhere to the following “Best Practices.”

(1) If the board does not decide to pursue a liquidity event, or the stockholders do not approve a liquidity event, we could continue to operate indefinitely.(2) Realty Capital Securities requires that every issuer on its platform adhere to Realty Capital Securities’ best practices guidelines. This, among other things, generally

disallows us from entering into business transactions with or providing funding to any non-traded REIT or private investment vehicle affiliated with the American Realty Capital group of companies. Please see the Prospectus for more details.

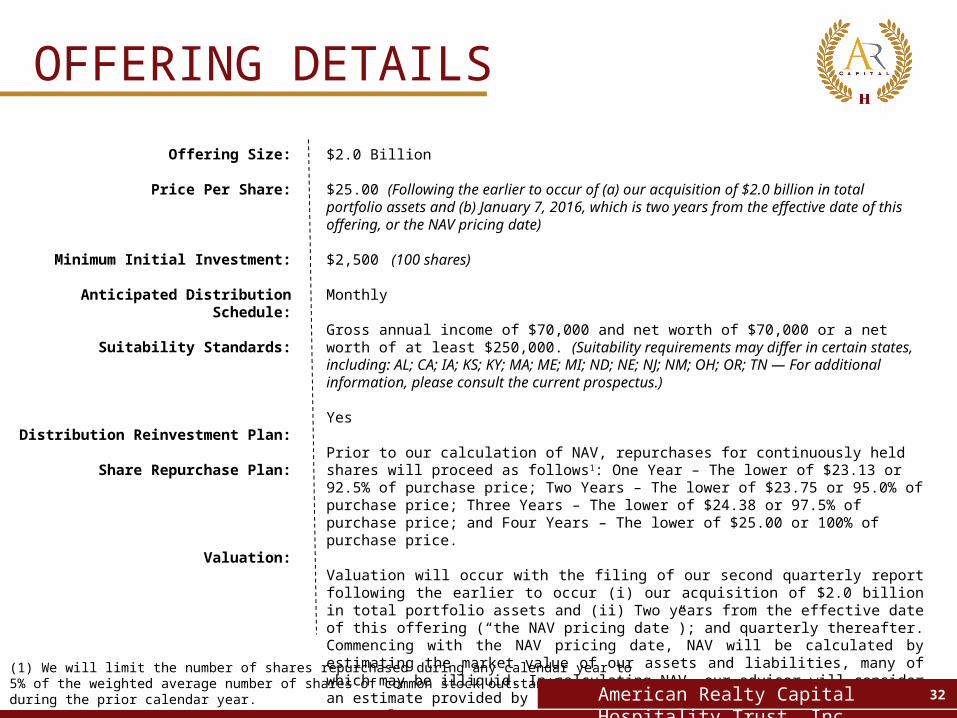

$2.0 Billion

$25.00 (Following the earlier to occur of (a) our acquisition of $2.0 billion in total portfolio assets and (b) January 7, 2016, which is two years from the effective date of this offering, or the NAV pricing date)

$2,500 (100 shares)

Monthly

Gross annual income of $70,000 and net worth of $70,000 or a net worth of at least $250,000. (Suitability requirements may differ in certain states, including: AL; CA; IA; KS; KY; MA; ME; MI; ND; NE; NJ; NM; OH; OR; TN — For additional information, please consult the current prospectus.)

Yes

Prior to our calculation of NAV, repurchases for continuously held shares will proceed as follows1: One Year – The lower of $23.13 or 92.5% of purchase price; Two Years – The lower of $23.75 or 95.0% of purchase price; Three Years – The lower of $24.38 or 97.5% of purchase price; and Four Years – The lower of $25.00 or 100% of purchase price.

Valuation will occur with the filing of our second quarterly report following the earlier to occur (i) our acquisition of $2.0 billion in total portfolio assets and (ii) Two years from the effective date of this offering (“the NAV pricing date”); and quarterly thereafter. Commencing with the NAV pricing date, NAV will be calculated by estimating the market value of our assets and liabilities, many of which may be illiquid. In calculating NAV, our advisor will consider an estimate provided by an independent valuer of the market value of our real estate assets.

Offering Size:

Price Per Share:

Minimum Initial Investment:

Anticipated Distribution Schedule:

Suitability Standards:

Distribution Reinvestment Plan:

Share Repurchase Plan:

Valuation:

(1) We will limit the number of shares repurchased during any calendar year to 5% of the weighted average number of shares of common stock outstanding during the prior calendar year. American Realty Capital Hospitality Trust, Inc. 32

OFFERING DETAILS

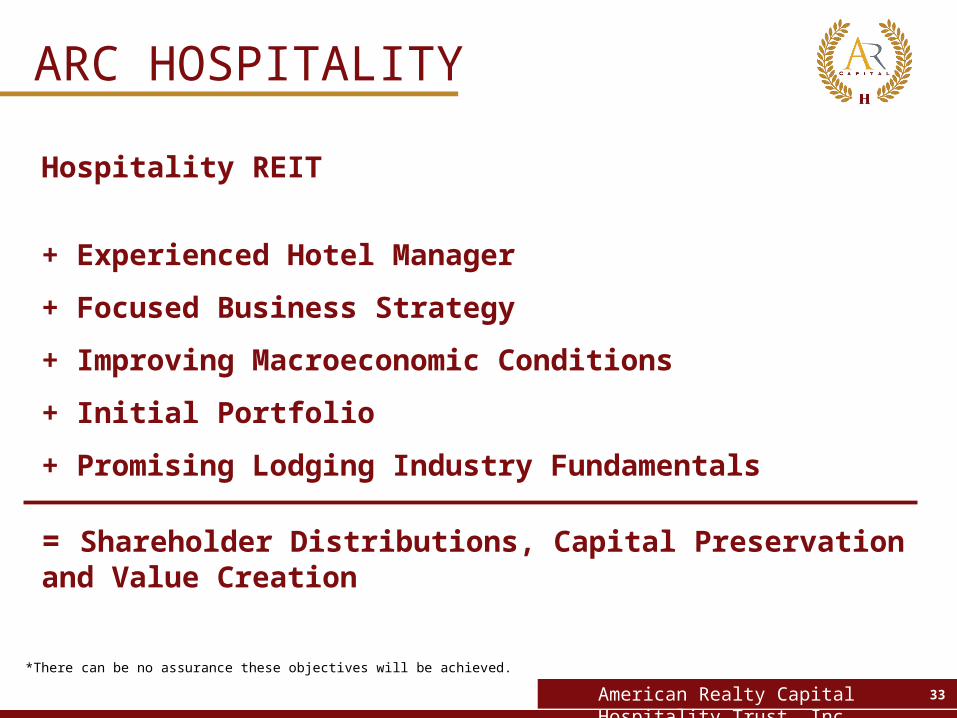

Hospitality REIT

+ Experienced Hotel Manager

+ Focused Business Strategy

+ Improving Macroeconomic Conditions

+ Initial Portfolio

+ Promising Lodging Industry Fundamentals

= Shareholder Distributions, Capital Preservation and Value Creation

American Realty Capital Hospitality Trust, Inc. 33

ARC HOSPITALITY

*There can be no assurance these objectives will be achieved.

American Realty Capital Hospitality Trust, Inc. 34

NOTES

American Realty Capital Hospitality Trust, Inc. 35

NOTES

36

INVESTOR INQUIRIES

For more information on American Realty Capital Hospitality Trust, Inc.

please contact your financial professional.

BROKER DEALER INQUIRIES

Realty Capital Securities, LLC One Beacon Street

14th Floor, Boston, MA 02108877-373-2522

www.rcsecurities.com

ALL OTHER INQUIRIES

American Realty Capital Hospitality Trust, Inc.

405 Park AvenueNew York, NY 10022

212-415-6500

Realty Capital Securities, LLC (Member FINRA/SIPC), is the dealer manager for American Realty Capital Hospitality Trust, Inc.

archospitalityreit.com

American Realty Capital Hospitality Trust, Inc.