Embed Size (px)

Citation preview

This Valuation Report has been prepared by AAHCompany and contains information relating to the Company, and its subsidiaries and constituents. The material in this document is confidential and the property of Ajwaa Alalam Aviation Group and its subsidiaries and constituents. This document may not be copied, or transmitted to anyone without the prior written consent of Ajwaa Alalam Aviation Group.

VALUATION REPORT Page 2

ABBREVIATIONS

AAS AAS Company Limited

AAL AAL Company Limited

AAT AAT Company Limited

AAH AAH Company or AAH Group Companies

AOC Air Operator Certificate

CEO Chief Executive Officer

DCF Discounted Cash Flow

GACA General Authority of Civil Aviation, Saudi Arabia

IPO Initial Public offering

AA CONSULTING AA Consultants

MRO Maintenance, Repair and Overhaul

NAV Net Asset Value

OEM Original Equipment Manufacturer

PMA Parts Manufacturing Authority

SAMA Saudi Arabian Monetary Agency

SAR Saudi Arabian Riyals

SLA Service Level Agreement

VALUATION REPORT Page 3

3

TABLE OF CONTENTS

I. EXECUTIVE SUMMARY ............................................................................................................................. 7

A. Background to the Group ...................................................................................................................... 7

B. The Group’s philosophy, Vision and Mission Statements ...................................................................... 7

C. Business Description .............................................................................................................................. 8

D. Historical Financial Results .................................................................................................................... 9

E. Financial Projections ........................................................................................................................... 10

II. INTRODUCTION ..................................................................................................................................... 12

III. STATEMENT OF LIMITING CONDITIONS ................................................................................................. 13

IV. AJWA ALALAM HOLDING COMPANY ................................................................................................. 15

A. Overview ............................................................................................................................................. 15

B. Background to the Group .................................................................................................................... 15

C. The Group’s philosophy, Vision and Mission Statements .................................................................... 19

D. Summary of the Group's strengths ...................................................................................................... 23

E. Strategic Partnerships ......................................................................................................................... 25

F. Group Company structure, holding and shareholding patterns .......................................................... 30

G. Business Description ............................................................................................................................ 30

H. Historical Financial Results .................................................................................................................. 34

I. Summary ............................................................................................................................................. 38

V. INDUSTRY OVERVIEW ............................................................................................................................ 39

A. Introduction ......................................................................................................................................... 39

B. General Overview ................................................................................................................................ 39

C. Aircraft Operations .............................................................................................................................. 39

D. Aircraft Maintenance .......................................................................................................................... 41

E. Aircraft Spares ..................................................................................................................................... 45

F. Aviation Consulting ............................................................................................................................. 47

G. Understanding the Non-traditional Aviation Market .......................................................................... 48

H. Conclusion ........................................................................................................................................... 48

VI. ECONOMIC OVERVIEW ...................................................................................................................... 49

A. Review of key economic indicators ..................................................................................................... 49

B. Oil sector overview .............................................................................................................................. 50

C. Inflation ............................................................................................................................................... 51

D. Demography ........................................................................................................................................ 51

E. Employment ........................................................................................................................................ 52

F. Interest rates ....................................................................................................................................... 53

G. The Securities Market .......................................................................................................................... 53

H. Equity Markets .................................................................................................................................... 54

I. Industrial Scenario ............................................................................................................................... 56

J. Future economic outlook ..................................................................................................................... 56

VII. FINANCIAL PROJECTIONS................................................................................................................... 58

A. Income Statement Assumptions .......................................................................................................... 58

B. Balance Sheet Assumptions................................................................................................................. 70

VALUATION REPORT Page 4

VIII. GENERAL VALUATION METHODOLOGY ............................................................................................. 71

A. Income Approach ................................................................................................................................ 71

B. Asset Based Approach ......................................................................................................................... 71

C. Market Approach ................................................................................................................................ 72

D. Valuation Adjustment Factors ............................................................................................................. 73

IX. VALUATION ANALYSIS ........................................................................................................................... 75

A. Discount and Capitalization Rate ........................................................................................................ 75

B. Terminal Year Growth Factor .............................................................................................................. 76

C. Discounted Cash Flow ......................................................................................................................... 76

X. SUMMARY AND RECOMMENDATIONS .................................................................................................. 77

VALUATION REPORT Page 5

LIST OF TABLES

Table 1: Annualized Growth Rates of Group Companies ...................................................................... 10

Table 2: Market Value ........................................................................................................................... 11

Table 3: Shareholding Structure of the Group companies ................................................................... 30

Table 4: Historical Net Margins of group companies............................................................................ 35

Table 5: Historical Return on Capital for group companies .................................................................. 36

Table 6: Average Aircraft Age ............................................................................................................... 40

Table 7: Breakdown of status of private aircraft in the Middle East .................................................... 40

Table 8: Private aircraft by country of operation ................................................................................. 40

Table 9: Aircraft type operating in the region ...................................................................................... 41

Table 10: Key Aircraft maintenance players and their revenue estimates ........................................... 42

Table 11: Forecast for Air Transportation market ................................................................................ 42

Table 12: Maintenance industry breakdown by type ........................................................................... 43

Table 13: Economic Indicators for Saudi Arabia ................................................................................... 50

Table 14: Cost of Living Indices ............................................................................................................. 51

Table 15: Demographic breakdown of the Saudi Population ............................................................... 51

Table 16: Saudi Labor force .................................................................................................................. 52

Table 17: Interest rate data .................................................................................................................. 53

Table 18: Government securities subscription ..................................................................................... 53

Table 19: Capital market data ............................................................................................................... 54

Table 20: Sectoral value traded for Saudi Stocks .................................................................................. 55

Table 21: Growth estimates for the region ........................................................................................... 56

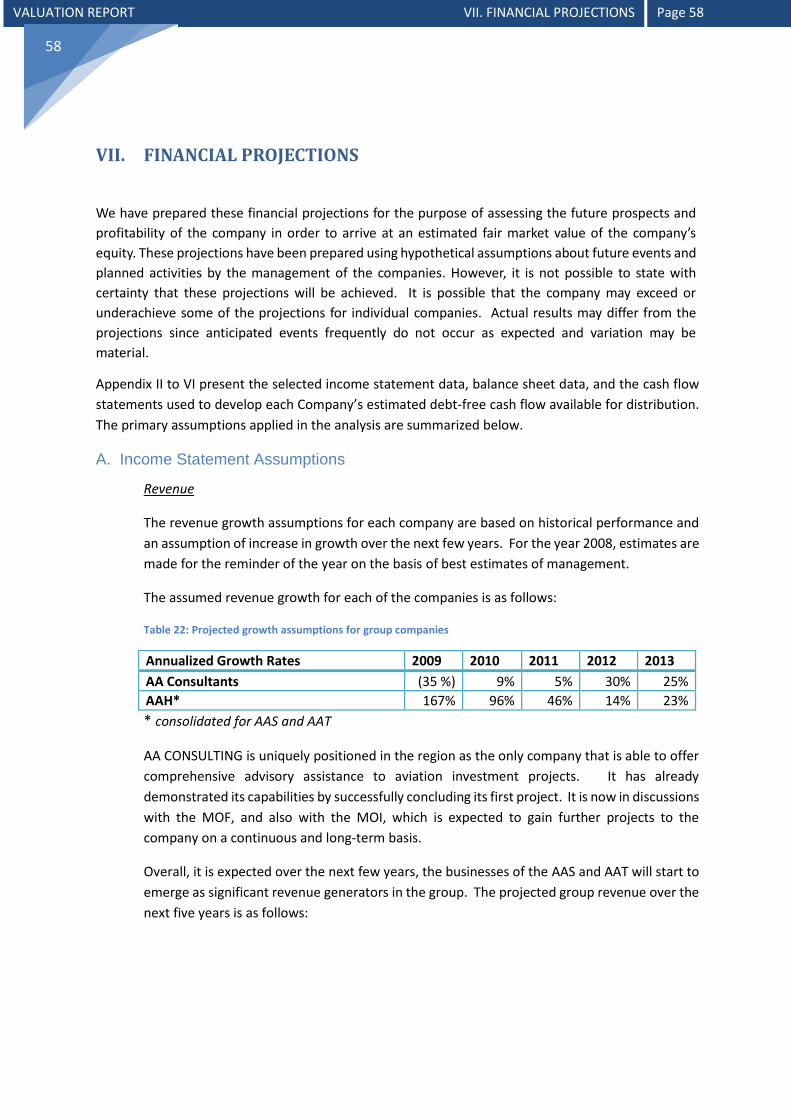

Table 22: Projected growth assumptions for group companies ........................................................... 58

Table 23: Price indicators of transportation companies on Saudi Stock Exchange .............................. 72

Table 24: Price indicators of multi-investment companies on Saudi Stock Exchange ......................... 72

Table 25: Valuation basis for companies in the group.......................................................................... 73

Table 26: Discount Rate assumptions for valuation ............................................................................. 75

Table 27: Terminal Growth rate assumptions ...................................................................................... 76

VALUATION REPORT Page 6

APPENDICES

APPENDIX I Summary CVs of the key management APPENDIX II Summary Consolidated historical and projected Financial Statements for AJWAA APPENDIX III Summary historical and projected Financial Statements for AASCompany APPENDIX IV Summary historical and projected Financial Statements for AATCompany APPENDIX V Summary historical and projected Financial Statements for AA Consultants

Company

VALUATION REPORT I. EXECUTIVE SUMMARY Page 7

7

I. EXECUTIVE SUMMARY

AAHGroup consists of four companies, which together constitute the group. In order to leverage this

position, AAHGroup now intends to offer its shares to prospective investors who will increase the pace

of growth of the companies in the group. We have performed a valuation analysis of the fair market

value of a 100% interest in the shares of AAHgroup companies as of 30 June 2008.

The private and specialized aviation market in the Middle East is one of the fastest growing markets.

With nearly 200 aircraft on order, the region will witness heightened private and specialized aviation

activities. The market for aviation services in the region is huge, but fragmented and there is no

established professional services company that has the capability or expertise to service the needs of

the market.

The AAHGroup of companies was started in 2006 as a business concept to serve the underserved

Middle Eastern private and specialized aviation market needs. Initially, two business entities were

created to serve the needs of the customer: AA Consultants, which operates as a professional office

offering purely advisory services, and Ajwaa Aviation, which operated as a specialized aviation services

company.

A. Background to the Group

AAHCompany Limited was established on 21 July 2008 (18 Rajab 1429 Hijri), as a holding

company for the AAHGroup in order to formalize and expand the services of the group into in

Kingdom certified aircraft operations, maintenance and logistics services. Through companies

in the Group, the Company offers end-to-end aviation support services to the private aviation

industry. AAHGroup’s “hands on” expertise spans all elements of the Aviation Industry

including, among others, Aviation Consulting, Aircraft Operation, Logistics and Maintenance,

Aircraft Acquisition and Financing, and Project Management.

Mr Founder Founder is the Chairman of the AAHGroup of Companies. Mr Founder Founder

is a recognized figure in the aviation industry, and more particularly in the business and

specialized aviation industry. Mr. Founder 's exposure to the international side of the aviation

business came while working initially at Al Salam Aircraft Company, and further as the

President and CEO at ABC(ABC).

B. The Group’s philosophy, Vision and Mission Statements

VALUATION REPORT I. EXECUTIVE SUMMARY Page 8

The Vision of the Group is:

To be recognized:

As the Middle East Leading provider of Specialized Aviation Services

and Aviation Investment Group

The Mission of the Group is:

To Establish

An integrated group of companies focused on serving its Employees ,

Clients and Being an added value to its Shareholders and Business

Partners

The Group’s strengths arise from its unique experience and market position, which gives the

group its ability to continually expand its business thus enhancing its market value.

AAHGroup has been recognized in the field of business and specialized aviation, and as a result

of this reputation, and its position in the Middle Eastern markets, the Group has attracted a

number of companies eager to establish a footprint in the region. Some of the well-known

strategic relationships are with Airbus and Comlux Group, and Studio E/motions.

C. Business Description

The business of the Group can be broadly classified into two areas: consulting, advisory and,

aircraft operations and technical support business. In order to service these two sectors, the

Group has been organized into four companies: each company in the Group has been formed

as a closely held company, with a unique business proposition and headed by a Chief Executive

Officer.

Each company is formed as a company which is held by Mr Founder Founder and

AAHCompany Limited as the key shareholders. AAHCompany Limited is the holding company

for the group, and does not perform any operations other than acting as the holding company,

and making strategic decisions to invest into new businesses or companies.

A brief description of each of the companies and their business is as follows:

VALUATION REPORT I. EXECUTIVE SUMMARY Page 9

AASCompany Limited (AAS): The Company was formed in 2008 and is headquartered in

Riyadh. The Chief Executive Officer of the Company is Captain Sultan AlDowaihy.

AAS specialized in providing services to the private and specialized aviation clients and shall be

responsible for operations of aircraft in the region, and turnkey aircraft management services

for individuals, government and corporate. The Company is already assisting in the operations

of an aircraft and is in negotiations with clients for operations of two other aircraft. AAS does

not directly own any aircraft, and currently assists customers by operating their aircraft for

them.

AAS has already obtained the 125 AOC certification, and is currently in the process of obtaining

its 121(S) AOC certification. These certifications will enable AAS to operate its own planes in

the future. For the purpose of this valuation, the implied investments and value realizable out

of these are not being considered.

AATCompany Limited (AAT): The Company was formed in 2008 and is headquartered in

Riyadh. AAT is in the business of providing aviation maintenance and technical services to

private and specialized aviation clients. The Company will provide line maintenance services,

including A, B and C checks for aircraft. In addition the company will provide VIP aircraft

interior upkeep services.

AAT has recently been awarded the 145 certification at Riyadh Airport as an approved repair

station. It is also in the process of setting up a private hangar facility at the King Khalid

International Airport at Riyadh, Saudi Arabia. For the purpose of this valuation, the implied

investments and value realizable out of these are not being considered.

AAL Company Limited (AAL ): The Company was formed in 2008 and is headquartered in

Riyadh. The company’s main business is to provide logistic support, including the purchase,

storage and sale of spare parts to support the needs of private aviation customers. AAL will

be actively involved in providing logistic support to aircraft that are being operated or

maintained by other companies in the group or other aircraft in the region.

The experience it gains in providing logistics support within the group will be leveraged to offer

logistic solutions to other businesses in the region.

AA Consultants (AA CONSULTING): The primary function of the company is to offer aviation

consulting, strategic advisory, investment advisory, and project management services to

companies in the region. Mr Ahmed Abdullah is the Chief Executive Officer of the company.

Its clients and relationships include high net-worth individuals, private companies and

government establishments and ministries, and virtually the who’s who of the Middle Eastern

private aviation industry. The company is involved mainly in aviation consultancy services and

aviation project management activities.

D. Historical Financial Results

VALUATION REPORT I. EXECUTIVE SUMMARY Page 10

The management of AAHGroup has reconstructed the financials statements of the group based

on the logical translation of businesses that belong to a specific line of activity to the company

that is expected to conduct that business.

AAHCompany provides significant strategic support to the companies in the Group, the value

of which cannot be easily estimated.

Total revenue for the AAHGroup of companies increased significantly from around SR 24

million in 2007 to more than SR 130 million in 2008.

Net margins, in general, have improved across all companies in the group. This is primarily

due to increased activity for the group, and also larger ticket business for the group.

The increased revenue for the group is a reflection of increasing confidence in the region for

the capabilities of the AAHGroup.

Each of the businesses of the group could grow through investment in related assets. For

example, obtaining GACA certifications for the operations and maintenance of aircraft and the

investments in hangar facilities are likely to significantly improve the performance of

AATCompany.

Net margins of most of the companies in the Group are superior to benchmark margins for companies in the region, and clearly demonstrate the potential for growth in these businesses.

E. Financial Projections

We have prepared these financial projections for assessing the future prospects and

profitability of the company in order to arrive at an estimated fair market value of the

company’s equity. It is possible that the company will exceed or underachieve some of the

projections for individual companies. These projections are not a substitute for business

planning, which will require detailed financial planning.

Revenue

The assumed revenue growth for each of the companies, over the previous year, is as follows:

Table 1: Annualized Growth Rates of Group Companies

Annualized Growth Rates 2009 2010 2011 2012 2013

AA Consultants (35 %) 9% 5% 30% 25%

AAH* 167% 96% 46% 14% 23%

* Consolidated for AAS and AAT

Valuation Analysis

In deriving values, we relied on: (i) historical financial data for the Companies (summary

provided in the section labeled “Historical Financial Results”), (ii) a Company-prepared

VALUATION REPORT I. EXECUTIVE SUMMARY Page 11

business plan for fiscal years 2009-13, and (iii) economic and industry data relating to the

business aviation industry and other related industries in which companies in the group

operate, as they impact the operations of the Companies.

The future business of the group has been broadly categorized as consulting related (MAZ

Aviation Consulting) and Aircraft operations related (AAS, AAT, and AAL ). The risks and the

returns expected on each of these businesses is different and moreover, a direct revenue and

cost linkage exists between financial performance for each of these two segments.

The discount rates for each of the companies was arrived at based on a combination of the

current rates of return based on risk free investments, the business risk premium associated

with the Company’s operations, and other relevant factors. The discount rate for each

company takes into account the risk free rate of return, country risk, industry risk and business

risk.

The valuation analysis estimates the fair market value of AAHGroup of companies using a

sum of parts method.

(all amounts in million Saudi Riyals) Table 2: Market Value

Company Name Valuation Basis

Total

Enterprise

Value

Less:

outstanding

loans/

(partner

advances)

Total

Equity

Value

AAH* DCF 645.58 0 645.58

AA Consultants DCF 595.84 0 595.84

Value

1,241.42 0 1,241.42

* Consolidated for AAS and AAT

Based on our analysis the fair market value of a 100% equity in the AAHgroup companies,

using the sum of parts valuation methodology as at 30 June 2008 is represented as Saudi

Riyals 1,241 million.

VALUATION REPORT II. INTRODUCTION Page 12

12

II. INTRODUCTION

The AAHGroup consists of four companies, which together make up the group. In a short span of less

than two years, the group has managed to gain a number of clients and established a formidable

reputation for the quality of its services, and the professionalism displayed by its team. The Group’s ability

to service the market in the Middle East is particularly strengthened due to some of the strategic

partnerships that it has entered into through its sister companies. As one of the few companies in the

region that has such significant partnerships, the Group occupies a position of strength. The Group is

poised for greater growth, and has over the past few months taken a number of steps to align the group’s

activities to maximize this growth potential.

The market for private and specialized aviation in the Middle East is fragmented, and poorly serviced due

to lack of adequate and professional manpower in the industry. In these conditions, the AAHGroup of

companies provides one of the best opportunities for growth and establishment of a dominant market

position. In order to leverage this position, AAHGroup now intends to offer its shares to prospective

investors who will increase the pace of growth of the companies in the group. This valuation exercise has

been prepared in order to assist in arriving at a value indication to guide in discussions with prospective

investors.

The objective of our valuation is to provide a recommendation for a possible stake sale or transfer in the

holding company to potential investors.

We have performed a valuation analysis of the fair market value of a 100% interest in the shares of

AAHgroup companies as of 30 June 2008. For the purpose of this analysis, fair market value is defined as:

…the price at which the 100% interest would change hands between a willing buyer and willing

seller, neither being under compulsion to buy or sell and both having reasonable knowledge of all

relevant facts as of the valuation date.

This valuation has been prepared based on a sum of parts method, whereby the value of the holding

company is derived based on the interest held by the holding company (either directly or indirectly) in

each of the subsidiary companies.

The recommendations in the report are based upon the information prepared internally and upon records

of events and contracts available with us, and other relevant sources. While we have carried out sufficient

procedures to ensure the accuracy of the information, it is possible that there could be some differences

between the audited financial statements and the historical financial statements used in this report.

Presentations of summaries of, or references to, the Valuation Report to third parties must be reviewed

by readers and they are cautioned to make their own evaluations.

VALUATION REPORT III. LIMITING CONDITIONS Page 13

13

III. STATEMENT OF LIMITING CONDITIONS

This valuation report is contingent on the following limiting conditions and assumptions made by us:

This valuation report is prepared by the management of AAHCompany and for the purpose of

assisting potential investors during discussions for a possible stake sale/transfer of the equity in

the Holding Company. This valuation report may not be distributed either in whole or in part to

any third party without the prior approval and written consent of the management of

AAHCompany.

Information used in this report and which forms a basis for the valuation is internally verified for

accuracy but has not been independently verified. This information primarily included: (i) the

proforma financial statements for years ended 31 December 2007 and 30 June 2008, and (ii)

financial projections and underlying assumptions for the five years ending 31 December 2013. The

performance of the companies in the group for the six month period ended 31 December 2008

are based on assumptions of business continuing on the same basis as on 30 June 2008.

This valuation report is not intended for use as investment, tax or accounting advice and does not

constitute a fairness opinion.

The valuation contained in this report is only to represent the estimated fair market value of

AAHgroup companies at 30 June 2008, i.e. the Valuation Date. Subsequent changes in market

conditions could result in a substantially different valuation. Specifically, it is assumed that the

business will maintain a status-quo position with respect to the methods of conducting business.

Any impact arising out of subsequent changes to the business including licensing and certifications,

establishment of hangars, and their impact on the potential revenues and profitability to the

companies in the group have neither been prepared nor are they being considered for the

purposes of this valuation.

Transaction prices may reflect specific circumstances and considerations other than the fair

market value. Such factors include, but are not limited to: (i) the profile of potential buyer, (ii)

potential synergy and strategic opportunities arising from business combination, and (iii) the

degree of urgency attached to the sale or acquisition. The user is responsible for making his/her

own determination of the fairness of any transaction.

Estimates of future events described herein represent our management’s general expectations

concerning such events as at 30 June 2008, the Valuation Date. These events may not occur as

anticipated, and actual operating results may vary materially from those projected by us.

Our report is prepared on the basis that AAHCompany Limited and its group companies and

associates have an unrestricted title to all property and other assets of the Company and that it

complies with local laws and regulations.

This report does not take into consideration the potential impact of some planned activities of the

group including, but not limited to establishment of hangar facilities, AOC certification (Part 125

VALUATION REPORT III. LIMITING CONDITIONS Page 14

and 121 (S) certification) and 145 certification for repair station operations. It is possible that the

inclusion of these facilities and certifications could significantly increase the value of the business.

Legal and financial impact, unless to the extent relevant for consideration of the valuation of

AAHCompany Limited, arising from any contractual and legal agreements between the Company,

its associates, and any of its principals that might affect the operations of the Company has not

been considered in our valuation analysis.

Except as specifically stated to the contrary, this Valuation Report has given no consideration to

the following matters to the extent they exist: (i) matters of a legal nature, including issues of

legal title and compliance with local laws, and (ii) litigation and other contingent liabilities that are

not recorded in the balance sheet. The user of this Valuation Report may be required to make his

own determination about the impact, if any, of these matters on the value reported in our report.

The prospective financial information has been prepared by us based on expectations of

competitive and economic environments as these may impact the future operations of the

Companies in the group. We have consistently applied key assumptions during the estimation

period and have not omitted any factors that may be relevant.

VALUATION REPORT IV. AAHCOMPANY Page 15

15

IV. AJWA ALALAM HOLDING COMPANY

A. Overview

The private and specialized aviation market in the Middle East is one of the fastest growing

regions. With nearly 200 aircraft on order, the region will witness heightened private and

specialized aviation activities. While the aircraft acquisition activity is in full swing, there are

very few companies in the region which have the capability of servicing the end-to-end needs

of private aviation players, right from initial aircraft purchase decision and negotiations to

purchase and outfitting, and to operations and maintenance of the aircraft.

The market for aviation services in the region is huge, but fragmented and there are few

established professional services company that had the capability or expertise to service the

needs of the market. Even where companies do exist, their quality of service leaves a lot to be

desired. Most of the existing aircraft owners typically relied on captains/pilots or other

technical support who had limited business exposure or understanding, or rely on expensive

services provided by European Service Providers.

The AAHGroup of companies was started as a business concept to serve the underserved

Middle Eastern private and specialized aviation market needs. In association with a group of

highly experienced and professional set of people, all of whom represent the best available

talent in the field of private aviation, AAHGroup has the privileged access to a combined talent

pool which is second to none.

Initially, two business entities were created to serve the needs of the customer: AA

Consultants, which operates as a professional office offering purely advisory services, and

Ajwaa Aviation, which operated as an aviation services establishment. The Ajwaa Aviation

business has now been further divided, for the purposes of strategic, administrative and

logistical convenience, into AAS, AAT, and AAL .

B. Background to the Group

AAHCompany Limited (“Subject” or the “Company”) was established on 21 July 2008 (18 Rajab

1429 Hijri), as a holding company for the AAHGroup in order to formalize and expand the

services of the group into in Kingdom certified aircraft operations, maintenance and logistics

services. The AAHGroup of companies offers end-to-end aviation support services to the

private aviation industry. AAHGroup’s “hands on” expertise spans all elements of the Aviation

Industry including, among others, Aviation Consulting, Aircraft Operation, Logistics and

Maintenance, Aircraft Acquisition and Financing, and Project Management.

Mr Founder Founder is the Chairman of the AAHGroup of Companies. Mr Founder Founder

is a recognized figure in the aviation industry, and more particularly in the business aviation

industry. Mr Founder is a Mechanical Engineer, having graduated from the University of New

Haven, CT, in 1984.

VALUATION REPORT IV. AAHCOMPANY Page 16

He has almost 25 years of hands on aviation experience that spans almost all aspects of the

aviation industry both commercial and military. For the first 22 years of his career Mr. Founder

worked on local, regional and global projects.

Mr. Founder was involved in obtaining one of the first licenses for an aircraft maintenance

facility in Saudi Arabia, in 1992.

Mr. Founder 's exposure to the international side of the aviation business came while working

at Al Salam Aircraft Company (Al Salam), a privately owned company which was formed as a

joint venture with Boeing as a part of the offset program.

In Al Salam, Mr Founder Founder was responsible for all business acquisition and contractual

activities, and in a span of 3 years, concluded contracts worth more than SR 1.5 Billion, with

almost 80% of it directly with the US government.

However, Mr Founder ’s is mostly recognized as the pioneer of organized private aviation

business in the Kingdom of Saudi Arabia. As the President and Chief Executive Officer of

ABC(ABC), he was responsible for redefining the landscape of business aviation in the region.

Under the leadership of Mr Founder , ABC became the first privately owned company to obtain

the first privately owned 135, 125 and 121 Aircraft Operator Certificates (AOC) and conduct

operations under these AOC's in the Kingdom. ABC also introduced and operated the Middle

East service of the global NetJets® program, the world’s first and largest fractional aircraft

ownership program.

In mid 2006, ABC was sold to a private equity fund for a market value seven times it original

capitalization. This was possible due to the significant value created under the leadership of

Mr. Founder during his tenure at ABC.

Immediately after the sale of ABC, Mr Founder , started the AAHGroup of companies in the

third quarter of 2006. Using his market experience, industry relationships, customer contacts

and understanding of the industry’s regulatory environment, Mr Founder put the initial

foundation for the AAHGroup with a clear vision driven by its objectives.

The objective was to establish an integrated group of companies each specialized in a certain

segment of the industry with a focus in three specific area of expertise which are:

• VIP and specialized aircraft services

• Specialized Aviation Consulting, and

• Selective Aviation Investment

The market potential in the aviation industry exists in the non-traditional markets, which is a

largely untapped segment. Other companies do not have the prior experience or the expertise

to address such needs, and the AAHGroup through its structure, is best equipped to serve this

market.

VALUATION REPORT IV. AAHCOMPANY Page 17

Recognizing the challenges of this industry, Mr. Founder recognized that to achieve success

two important risks that could result in failure, needed to be mitigated. These were:

1. Lack of financial support; and

2. Lack of competent team

To mitigate these two risks the following steps were undertaken:

In order to mitigate the financial stability risk; a long term corporate development strategy

was developed with a clear target of achieving a strong cash positive position within 18 months

of commencing operations (this target was, in reality, achieved within 6 months). Once this

target is achieved, plans for the group’s expansion could start. To achieve this target; all initial

activities were concentrated on the VIP aircraft activities since this market could be developed

based upon Mr Founder ’s reputation and industry contacts.

In order to mitigate the risk of failure due to the lack to competent team members, Mr Founder

recruited a group of highly experienced professionals all of whom had prior experience of

working in the Aviation industry outside the traditional domain.

Once the business stabilized and the initial targets were achieved, Mr. Founder and the team

started to activate the other two elements of the charter i.e. Aviation consulting and Aviation

Investment.

In early 2008, the team put together the foundation of the full structure. This took about 6

months to achieve and is designed to support the overall investment vision and also ensures

that the operational and business needs of the market are also addressed.

The goal of the structure creation is defined by a set of internal as well as external functions,

as described below:

Internal functions External functions

• To create clear lines of business that are distinct and separate from each other.

• To create a clear leadership and a performance orientation for each business line.

• To create a structure that relies on line leaders.

• To enable the rewarding of individuals within the company.

• To realize the full potential of business opportunities available in the aviation industry.

• To leverage the availability of external funding sources to rapidly accelerate growth of the business.

• To bring in partners, where necessary and possible.

A strategy was developed for the development of the group structure; this strategy revolves

around a basic principle that each company in the group adheres to four clearly defined

guidelines. These guidelines are:

VALUATION REPORT IV. AAHCOMPANY Page 18

Each company has to

• Have a clearly identified business line;

• Have synergies with other companies in the Group;

• Draw from the strengths of the Group; and

• Contribute to the strength and efficiency of the Group.

As a result, a group company structure was evolved with separate independent entities being

created to meet the vision of the group. In addition, the group has entered into a number of

strategic partnerships that further enhance the ability of companies within the group to deliver

better. The companies that constitute the group and their relationship with AAHCompany are:

The group’s principal facilities and corporate offices are located in Jeddah and Riyadh in Saudi

Arabia.

VALUATION REPORT IV. AAHCOMPANY Page 19

C. The Group’s philosophy, Vision and Mission Statements

The group’s philosophies closely are reflected in its functioning, which encourages

independent functioning of its staff, each of whom is expected to take decisions

independently, and in the best interests of the key stakeholders of the business.

The Vision of the Group is:

To be recognized:

As the Middle East Leading provider of Specialized Aviation Services

and Aviation Investment Group The Mission of the Group is:

To Establish

An integrated group of companies focused on serving its Employees ,

Clients and Being an added value to its Shareholders and Business

Partners The group plans to realize its Vision, and achieve its Mission by using the following strategies:

Use our market network & position and our understanding of the

Industry & Regulation to develop:

1) Unique solutions for our clients; and

2) Low risk high reward investments

Some of the core strengths of the group arise out of the dynamic management and leadership

skills of the key persons within the group.

Critical Elements of Success

The Group’s strengths arise from its unique experience and market position which gives the

Group its ability to continually expand its business in the most lucrative segment of the VIP

and Specialized aviation market thus enhancing its market value.

The Group has also leveraged its ability to take quick decisions even while carefully weighing

the implications of these decisions. This ability to react with rapidity gives it the advantage of

being able to close deals quickly.

For a business operating in the non-traditional aviation markets in the Middle East, some of

the critical elements of success include:

VALUATION REPORT IV. AAHCOMPANY Page 20

Leadership and Management:

One of the core strengths of the Group arises from its excellent Leadership, driven by its key

management team. Some of these leadership traits include the ability to motivate the team,

to deliver non-traditional solutions.

Greatest freedom is provided to each team member, thus encouraging innovative thinking,

and pride of ownership across all levels of management.

Professional competence and managerial skills:

Each member of AAHGroup has been selected based on their vast and diverse experience in

the field of aviation. The skill sets of the team members encompass all elements of the

Aviation Industry including, Operation, Command and Control, Logistics and Maintenance,

Quality Control and Standardization, Safety and accident investigation, Remote Site Operation,

Aircraft Acquisition and Financing, Aircraft Cost Analysis, and Project Management.

The combined work experience of the core team members, as individuals, spans more than

200 years and covers almost all major Commercial and Military aviation projects established

in the Kingdom during the last 30 years.

While a number of the team members have cut their teeth learning about the traditional

aviation business with reputed and established companies, in their subsequent career paths,

they have gained business experience that has enabled them to leverage this learning for

effecting far more professional solutions. Due to the vast experience of the team, they are able

to add value to projects way beyond what is possible by any other company in the aviation

business in the Middle East.

Please refer to the Appendix I for brief CVs of the key members.

In summary, AAH is the only Saudi Group

• To have aviation investment experience in Saudi as well as international aviation markets.

• To possess unique abilities to leverage the experience of our international partners.

• To have experience across all aspects of the aviation industry – commercial, private,

military, etc.

• To have experience in end-to-end servicing of the needs of the industry from advisory to

operations.

Networking:

AAHGroup has excellent networking within the customer community, the regulator and the

industry. The strength of this networking have been built on a believe that relationships are

the essence of being able to create sustainable business models, and continuously strengthen

them. The group leverages its networking to the benefit of its clients and its partners. As a

result, the group has won a number of key business on “sole sources” basis.

VALUATION REPORT IV. AAHCOMPANY Page 21

Strategic Alliances:

AAHGroup has been recognized in the field of business and specialized aviation, and as a result

of this reputation, and its position in the Middle Eastern markets, the Group has attracted a

number of companies eager to establish a footprint in the region. Some of the well known

relationships (see following pages) are with companies such as Airbus, Comlux Group, Hawker

Beechcraft, Indianapolis Jet Centre, etc.

Some of the reputed companies with which the Group has on-going relationships include:

• Legal Advisors: Clifford Chance

• Risk Management advisors: Willis Insurance Brokerage

• International Banks: UBS, Citibank

A number of international companies constantly keep approaching us for tie-ups or long term

relationships and we continuously evaluates such propositions.

Market Understanding and Positioning:

One of the biggest challenges facing users of private and specialized aviation services has been

the inability of one company to meet the end-to-end needs of its customers. Typically, a

customer requires approaching multiple vendors for each of its needs. For example, in order

to purchase an aircraft, he will require approaching one vendor, and for financing assistance,

he may need to approach a different vendor. The design and outfitting needs are then met by

a different set of vendor’s altogether, and finally for operations and maintenance, the same

customer has to approach a different company. All of this results in loss of efficiency, and

potentially ends up as a very expensive proposition for the customer.

The private and specialized aviation industry has traditionally remained highly fragmented,

with few centers of excellence, and disaggregated business models. The AAHGroup is one of

the first and perhaps the only company in the region that can offer end-to-end solutions to

meet customers’ needs, all under one roof.

Over the past 25 years members of the AAH have been involved as individuals, in almost all

fields of the aviation market, this has given it an excellent understanding of the opportunities,

risks and needs of the market. The group is therefore not a “me-too” service provider, but we

developed our Group to address the specific market needs. This, together with experience

ensures that the Group has hands-on operations and investment experience which help it

focus on the most lucrative opportunities within the VIP and Specialized opportunities in the

aviation industry.

VALUATION REPORT IV. AAHCOMPANY Page 22

Weaknesses

Some areas that require further strengthening include:

Number of years in business:

The Group is relatively young and has been in operation for barely a couple of years. The

opportunities that are available in the non-traditional aviation business have been so vast, that

the group has been working hard to meet the demands of the industry.

However, while the Group is young, individually most of the team members have long and

varied years of experience which more than makes up for this.

Being new in business also presents an opportunity to the Group to be dynamic and respond

to emerging needs better than long established aviation service companies in the region.

Geographical spread:

The group’s business activities remain largely restricted to the Middle East. The Group

continuously evaluates new business propositions for establishing or acquiring strategic stakes

in businesses all across the world. These decisions require careful consideration and also

evaluation to ensure strategic fit with the current business objectives of the Group.

However, the presence of strong international strategic partners helps in complementing the

strong local presence that the group has in the region.

A summary of the relative competitive position of the Group and the ability this has to impact

the markets are presented through the following Strategic Implications Matrix, below:

VALUATION REPORT IV. AAHCOMPANY Page 23

As is clearly evident, though the group is young in age, it has established a formidable reputation as a

provider of business aviation services in the Middle Eastern region.

D. Summary of the Group's strengths

A summary of the strengths of the group are as follows:

1. Excellent and comprehensive understanding of the Saudi and Middle East aviation markets.

2. Well established relationships - a critical success factor for any aviation business in the region.

3. Strong Team with practical hands-on Aviation Investment and Operational experience: We are

not first-timers.

4. Ability to Provide “Total In-House” solutions for VIP aircraft owners: Never done before in the

Middle East.

5. Local presence and capabilities: With offices in Riyadh and Jeddah we are well established with

local capabilities to support our clients.

6. Regional and international presence: We have capabilities to work under different

jurisdictions.

7. Excellent understanding of the regulatory, legal and cross-border issues: We can ensure that

these critical factors are accounted for in the clients’ requirements.

VALUATION REPORT IV. AAHCOMPANY Page 24

8. Extensive industry relationship and credibility: We can take an Idea to the Industry and get

them to at least listen.

9. Quick decision making process, giving us great business agility.

10. Excellent financial strength, which is a great support for our business expansion plans.

VALUATION REPORT IV. AAHCOMPANY Page 25

E. Strategic Partnerships

In addition to these direct holdings, the AAHGroup also has strategic partnerships with reputed

aviation companies. Some of these companies include:

Airbus Corporate Jet Centre:

Airbus’ Corporate Jet Centre, which was earlier

operating as a division of Airbus, had traditional

weaknesses in marketing and deliveries.

AAHGroup sister company MAZ Consultancy,

Bahrain entered into a joint venture agreement

with Airbus, by virtue of which, it agreed to MAZ

Bahrain become a shareholder in Airbus Corporate

Jet Centre. MAZ Consultancy, Bahrain also

committed to bringing business to the Centre. As a

result, the Airbus Corporate jet Centre has turned

around and shown a rapid increase in clientele.

AAHGroup has been rewarded through an

established relationship.

Airbus has shown appreciation of the

professionalism and competence of the

AAHManagement team in managing the entire

process, commencing with the review of the

business plans, to the due diligence and closure of

the deal.

Today, Mr Founder has board representation on the company. He also regularly reviews the

performance of the company, and provides advisory support.

About Airbus Corporate Jet

Centre

Airbus is one of the world's leading

aircraft manufacturers, and it

consistently captures approximately

half or more of all orders for airliners

with more than 100 seats.

Airbus' mission is to provide the

aircraft best suited to the market's

needs and to support these aircraft

with the highest quality of service. The

Airbus product line comprises 14

aircraft models.

Airbus' Corporate Jet Centre is based

in the former EADS Sogerma facilities

at Toulouse, and regroups most of the

company's experienced cabin-

outfitting personnel under a new

management team. It is a majority

owned subsidiary of Airbus.

VALUATION REPORT IV. AAHCOMPANY Page 26

Comlux Completions:

Comlux, through its Chairman, Mr Richard Goana,

showed interest in partnering with AAHGroup for

the Middle East business. Whereas Comlux had a

strong presence in the East European and Russian

markets, AAHGroup of companies had a strong

presence in the Middle Eastern markets. A new

company, Comlux Middle East is being created by

combining their strengths.

As a result of the first successful joint venture

between AAHGroup and Comlux, Comlux has

realized the skills and ability of the AAHGroup

management and has expressed its desire to

further deepen the relationship.

Comlux has agreed to the establishment of a

strategic relationship with AAHGroup for exploring the areas of aircraft management, charter

and completions business in the region.

Comlux and the AAHGroup are continuously evaluating possible business opportunities

together, that provide them a unique ability to leverage each of their areas of expertise.

About Comlux

Comlux The Aviation Group, is

managed by Comlux Management AG,

and provides its customer with the

ultimate business aviation solution at

the highest quality level. The group is

organized in divisions, covering all of

the customer needs under the lead of

Richard Gaona.

Mr Richard Gaona is the former Vice

President at Airbus Executive and VIP

Aircraft Division. Group companies

include Comlux Aviation, Comlux

Creatives, Comlux Transactions takes,

and Comlux Completions.

VALUATION REPORT IV. AAHCOMPANY Page 27

Indianapolis Jet Centre:

Indianapolis Jet Centre is one of the few companies that has an outfitting facility for a

wide variety of aircraft, which is based out of the

USA. In 2008, the company decided to expand its

activities to include Airbus Completions. The

company was hitherto operating in outfitting of

Learjets and Challengers. Aircraft manufactures

are currently experience a record breaking order

backlog creating record demand for completions.

The manufacturer of both the Lear and

Challenger lines, Bombardier, is experience a

backlog of $22.7 billion or roughly 1.9 years.

The company, operated by its Promoter, Randy

Keeler, required financing for its expansion

program. At the same time, AAH required

additional facilities available to service its clients’

outfitting requirements. While the ACJC facility

provided it with a facility in Europe, the

opportunity through IJC opened up a window to

the smaller aircraft as well as the US markets.

Along with Comlux, AAH’s sister company MAZ Bahrain has taken an investment in IJC,

resulting in a strategic equity stake in IJC.

About IJC

Indianapolis Jet Center, Inc. (“IJC”) is

a premier aircraft completion,

modification and maintenance

company, offering a broad array of

services to selected upper market

business jets. Over 600 aircraft

interiors have been completed

including six Boeings, one Russian

TU134, 28 Gulfstreams, 52

Challengers, 120 Learjets, 12 Hawkers

and 13 Citations.

IJC has held the Federal Aviation

Administration (“FAA”) air agency

repair station designation since 1979

and also holds European Aviation

Safety Agency (“EASA”) approvals. In

addition the Indianapolis Jet Center is

a prestigious FAA Diamond Award

facility.

VALUATION REPORT IV. AAHCOMPANY Page 28

Hawker/Beechcraft:

The Middle East offers Hawker/Beechcraft, a manufacturer of both small jets and

turboprops,a large market. In fact, with a market share of 16%, it has the largest share

of private aircraft in the region after Bombardier. However, the company has been

facing challenges of reaching to two of the largest markets in the region, both in

Kingdoms of Saudi Arabia and Bahrain.

While initially, the company approached MAZ Bahrain, a sister company of AAH group

for a sole representative arrangement for its Hawker aircraft only, it also decided to

award the sole representative arrangement to the group for its Beechcraft aircraft too.

The process of selection involved detailed due diligence by the company and several

rounds of discussions and evaluation.

VALUATION REPORT IV. AAHCOMPANY Page 29

Studio E/motions:

The strategic relationship between AAHcompany

Limited and Studio E/motions is aimed at providing

much needed aircraft design services to companies

in the region. Through this strategic partnership,

the Group can seamlessly offer aircraft design

solutions to its customers, combining the deep

knowledge that AAHGroup has of the requirements

of clients in the Middle East, and the expertise that

Studio E/motions has to offer in the area of interior

design.

Mr Francis Munch, the owner of Studio E/Motions

has established a formidable reputation in the field

of interior design for aircraft, especially with Airbus.

Studio E/motions is one of the few companies that

are recognized by Airbus as a provider of services to

private aviation customers of Airbus. Studio

E/motions has also entered into an MOU with Jet

Aviation to offer them design services.

Mr Francis Munch built his reputation while working with Jet Aviation. In the Middle East, one

of his projects includes the interior design for BBJs, 757, 767, 747, A320s and an A340s for Saad

Aviation.

About Studio E/motions

Studio E/motions is a company that is

owned by Mr Francis Munch, a French

national, and has its office in 1 Street's

Vineyard, Habsheim. The company

exists as a Sarl Unipersonnelle (single

person company) with a capital of

9,000 Euro, and operates out of

France.

Mr Francis Munch has also applied for

patent for one of his design works

relating to aircraft interiors that he has

undertaken (Application number:

11/109,677, Publication number: US

2005/0236523 A1, Filing date: 20 Apr

2005, Abstract: Internal arrangement

of the walls of the fuselage of an

aircraft).

VALUATION REPORT IV. AAHCOMPANY Page 30

F. Group Company structure, holding and shareholding patterns

All the group companies listed above have been formed as closely held companies, each with

a unique business proposition and headed by a Chief Executive Officer.

Each of the companies is fully funded, based on presented and anticipated future funding

requirements, out of the internal funds of the group. Each company is formed as a company

which is held by Mr Founder Founder and AAHCompany Limited as the key shareholders.

The Equity Capital and the shareholding pattern of each of the companies are as follows:

Table 3: Shareholding Structure of the Group companies

Company Name Equity Capital Shareholding Pattern

AASCompany Limited (AAS) SR 2 million 50% - Mr Founder Founder 50% - AAHCompany

AATCompany Limited (AAT) SR3 million 50% - Mr Founder Founder 50% - AAHCompany

AA Consultants SR 20 thousand 50% - Mr Founder Founder 50% - AAHCompany

AAL Company Limited (AAL ) SR 6 million 50% - Mr Founder Founder 50% - AAHCompany

The principal shareholders of AAHCompany Limited are Mr Founder Founder , who holds 95%

of the existing share capital, and Mr Hamad Founder who holds the remaining 5% of the

capital. The Share Capital of AAHCompany Limited is SR 10 million, consisting of one hundred

thousand shares of Saudi Riyals 100 each.

The executive management team for AAHCompany Limited includes:

Individual Position

Mr Founder Founder Chairman and Chief Executive Officer

Mr Ahmed Abdullah Director on the Board of the company

Mr Saleh Abdulrahman Director on the Board of the company

Mr Nasir Alsaaed Director on the Board of the company

Brief CVs of the team members are presented in the appendix to this document.

G. Business Description

As mentioned earlier, AAHCompany Limited is the holding company for the group, and does

not perform any operations other than acting as the holding company, and making strategic

decisions to invest into new businesses or companies. The holding company is guided in its

VALUATION REPORT IV. AAHCOMPANY Page 31

decision making process by the Board of Directors, and a Strategic Advisory Committee, which

consists of the CEOs of each of the companies of the group.

The Strategic Advisory Committee meets twice a year and discusses new business

opportunities and possible plans of action.

A brief description of each of the companies and their business is as follows:

AASCompany Limited (AAS): The Company was formed in 2008 and is headquartered in

Riyadh. The Chief Executive Officer of the company is Captain Sultan AlDowaihy. Captain

Sultan has more than 25 years of experience, having started his career with Saudi Arabia

Airlines. He subsequently joined ABC in 2004 as Director, Flight Operations. During his tenure,

he was responsible for obtaining 125 and 121 certifications for the company’s operations.

AAS specializes in providing services to the private and specialized aviation clients and shall be

responsible for operations of aircraft in the region, and turnkey aircraft management services

for individuals, government and corporate. The Company is already assisting in the operations

of one aircraft, and is in negotiations with clients for operations of two other aircraft. AAS does

not directly own any aircraft, and currently assists customers by operating their aircraft for

them.

AAS has already obtained the 125 AOC certification, and is currently in the process of obtaining

its 121(S) AOC certification. These certifications will enable AAS to operate its own planes in

the future. For the purpose of this valuation, the implied investments and value realizable out

of these are not being considered.

AATCompany Limited (AAT): The Company was formed in 2008 and is headquartered in

Riyadh. The Chief Executive Officer of the company is Mr Saleh Al Rasheed. Saleh is a graduate

in Aerospace Engineering and spent his initial career with Riyadh and Dahran Air bases, and

subsequently with the Royal Saudi Air Force. His previous position before joining the

AAHGroup was as Vice President Engineering and Maintenance at ABC.

AAT is in the business of providing aviation maintenance and technical services to private and

specialized aviation clients. The Company will provide line maintenance services, including A,

B and C checks for aircraft. It will also have some support shops such as tire, wheels and

brakes, avionics, electrical, battery and interior shops. In addition, the company will provide

VIP aircraft interior upkeep services.

The main business components of the company are as follows:

1. Aircraft survey, inspection and record review & acceptance: This service takes care of,

inspecting, and reviewing the records as a part of aircraft procurement activity.

2. Design review: This service involves reviewing of aircraft design that includes outfits and

interiors, entertainment system, avionics systems, etc., in compliance with the aviation

regulatory norms with regard to material used and the design.

VALUATION REPORT IV. AAHCOMPANY Page 32

3. Heavy Maintenance Projects: This service includes checks when major parts of the aircraft are

stripped and reassembled, with the services being offered either through outsourced partners

or, where possible through available resources within the company.

4. In-service aircraft line maintenance engineering support: This is a critical service. It involves

supporting the maintenance mechanics and liaison with the manufacturer when anything is

missing in the manual.

5. Engine monitoring: This service is related to regulatory requirement and hence critical. It takes

care of obtaining the real-time data or physical data of the engine and sending it to the

manufacturer.

6. Technical publication control and distribution: This is also a critical service as an aircraft

operation is done by technical manuals. It ensures that all the technical manuals are accurate

and up- to date.

7. Aircraft record keeping: This service includes maintaining a record of aircraft maintenance

activities, alterations, etc. It provides complete traceability relating to an aircraft.

By establishing a maintenance company, the company intends to fulfill a long felt need to have

a strong player in the region who can provide services without necessarily requiring moving

the aircraft to Europe or other regions. Clients will potentially reduce their time lost in service

as well as achieve more price effective solutions than were earlier possible.

AAT has recently been awarded the 145 certification at Riyadh Airport as an approved repair

station. It is also in the process of setting up a private hangar facility at the King Khalid

International Airport at Riyadh, Saudi Arabia. For the purpose of this valuation, the implied

investments and value realizable out of these are not being considered.

AAL Company Limited (AAL ): The Company was formed in 2008 and is headquartered in

Riyadh. Mr Saleh Al Rasheed is the Chief Executive Officer of AAL as well.

The company’s main business is to provide logistic support, including the purchase, storage

and sale of spare parts to support the needs of private aviation customers. The company

currently also has a small storage unit at the airport in Riyadh. On establishment of a larger

hangar and office support at the airport, the storage unit of the company will be transferred

to this location.

The company will primarily be dealing with two types of spares: Consumables, which are for

one-time use, and Ratable items, that are re-usable and could be sent for repairs.

AAL will be actively involved in providing logistic support to aircraft that are being operated

or maintained by other companies in the group. In order to provide support, the company will

stock items that are typically expected to be consumed by aircraft users.

Where necessary, the company will also enter into relations with established manufacturers

or other aircraft spares companies in order to augment its requirements, and to extend

VALUATION REPORT IV. AAHCOMPANY Page 33

services even where it does not have adequate spares. The company holds spares arising out

of allocation of the funds received by AAS for the purposes of spares for the aircraft. This has

been assumed at the rate of US$150 thousand per month per aircraft.

Eventually, the company will be able to provide logistic support to other industries in the

region, by leveraging its logistics capabilities and thereby:

• Reducing turnaround time for supplies

• Increasing logistic efficiencies

• Reducing logistic costs

AA Consultants (AA CONSULTING): AA Consultants was initially set up as a professional

office of Mr Founder Founder in 2006. It is fully certified by the Ministry of Commerce, with

offices in both Riyadh and Jeddah. Its certification was obtained based on recommendations

and approval from both the General Authority of Civil Aviation (GACA) and the Royal Saudi Air

Force (RSAF). The primary function of the company is to offer aviation consulting, strategic

advisory, investment advisory, and project management services to governments and aviation

companies in the region.

Since inception of services, AA CONSULTING has quickly gained a formidable reputation as

provider of quality consulting services in the field of aviation. As a result, it has established

strong relationships with clients as well as vendors who have appreciated the professionalism

as well as expertise that the company has shown.

AA CONSULTING’s unique approach to client relationship ensures not only repeated business

with the same clients, but also referrals to other clients. AA CONSULTING’s clients and

relationships include high net-worth individuals, private companies and government

establishments and ministries, and virtually the who’s who of the Middle Eastern private

aviation industry. Its key clients are:

• Government Clients: These mainly consist of the Ministry of Finance, and the Ministry of

Interior, Kingdom of Saudi Arabia.

• Private: AA CONSULTING has a total of 12 VIP clients, each one represent one aircraft

project, including one Head of State.

Based on its successful execution of the first contract with the Ministry of Finance (MOF), AA

CONSULTING is today poised to enter into a long term relationship with the Ministry whereby

all future AA CONSULTING will act in an advisory capacity for all future investment related

activities for the MOF.

AA CONSULTING has also submitted a proposal to the Ministry of Interior (MOI) for assistance

in aircraft management advisory.

Mr Ahmed Abdullah is the Chief Executive Officer of the company. Omar is a product of the

reputed Embry Riddle Aeronautical University. After starting his career with ABC, he was finally

VALUATION REPORT IV. AAHCOMPANY Page 34

responsible as the Managing Director of ABC Air, the Kingdom’s first low-cost airline. During

his tenure at ABC, he was also responsible for successfully launching the Al Khayala Services.

H. Historical Financial Results

As on the date of the valuation, the companies that form a part of the group have all not yet

been formed as legal entities.

At present, most of the business of the AAH Group is conducted primarily through two legal

entities: Ajwaa Aviation, which functions as an Establishment under the Saudi laws, and AA

Consultants, which operates as a professional office under Saudi laws.

The management of AAH Group has reconstructed the financials statements of the group

based on the logical translation of businesses that belong to a specific line of activity to the

company that is expected to conduct that business.

The reorganization of the historical financial statements have been performed using a basic set

of assumptions, which are expected to substantially form the fundamental and underlying

bases for all the transactions that are expected to be conducted between companies within

the group.

These assumptions are separately being agreed to as the Service Level Agreements (SLAs)

between the companies within the group. It is possible that there may be minor modifications

to the final SLAs that could result in a variation of the individual income statements and balance

sheets that are presented; however, the overall impact is not expected to be significant, if any.

The audit of the existing legal entities has not been completed as on the date of this valuation

report. It is possible that as a result of the audit there could be modifications that could be

effected to the financial statements, and these are expected to have minor impact, in terms of

the final valuation.

Basis for preparation of the historical financials

The key rules that were applied to prepare the historical financial statements for each of the

companies are as follows:

1. AAHCompany Limited, as the holding company, provides support services to all the companies

in the group. The costs incurred for this purpose of charged to each company in the group in

proportion to the revenues of its business. This charge is based on the fact that AAHCompany

provides significant strategic support to the companies in the group, the value of which cannot

be easily estimated.

2. Mr Founder , as the Chairman and the CEO of AAH, has been assumed to draw a gross salary

of SR 100 thousand per month. This amount is in compensation for his role as the Chairman of

the group. A revised salary package, in line with the new group structure, is being worked out.

In addition, as a majority shareholder, he reserves the rights to draw dividends in accordance

with the policies of each of the companies in the group.

VALUATION REPORT IV. AAHCOMPANY Page 35

3. Profits made by AA Consultants during the current year and the previous year have been drawn

out by the promoters for reinvestment mainly in creating AAHGroup and acquiring aircraft that

are used to support AAS operations.

4. In the year 2007, AAHAviation Services Company Limited charged a fixed amount of SR1 million

Saudi Riyals as compensation for services provided by it to AA Consultants. In the year 2008,

Ajwaa Aviation Services Company Limited charged 5% of the contract size for the costs it

incurred in assisting AA Consultants in fulfilling its obligations. Ajwaa Aviation Services

Company will draw revenues mainly from operations. The Company made revenues of around

$650,000 per month on the management of one aircraft. In addition, it is paid a monthly charge

of about $5,000 per hour on aircraft flight operations.

5. AATCompany charges a fixed amount of $175,000 per aircraft that is managed by AAHAviation

Services Company towards maintenance management of aircraft operated by it. In addition,

in 2008, it charged 2.5% of the contract value for a large consulting project undertaken by AA

Consultants for assistance provided to the company in fulfilling its obligations.

6. For providing support to AATCompany, AAL Company charges a fixed monthly amount of SR

125,000 per month. This is for inventory holding costs on behalf of AATCompany. It currently

has no other revenues.

The recast historical financial statements of each of the companies in the group were analyzed

in order to understand the past performance and operating trends. It should be noted that

this analysis is done entirely based upon the unaudited financial information, and it may not

be possible to develop audited financial statements for some of these companies.

The following narrative description includes an analysis of selected income statement items,

balance sheet items, cash flow items, and financial and operating ratios.

Income Statement Data

The summary income statements for each of the companies of the group are as provided in

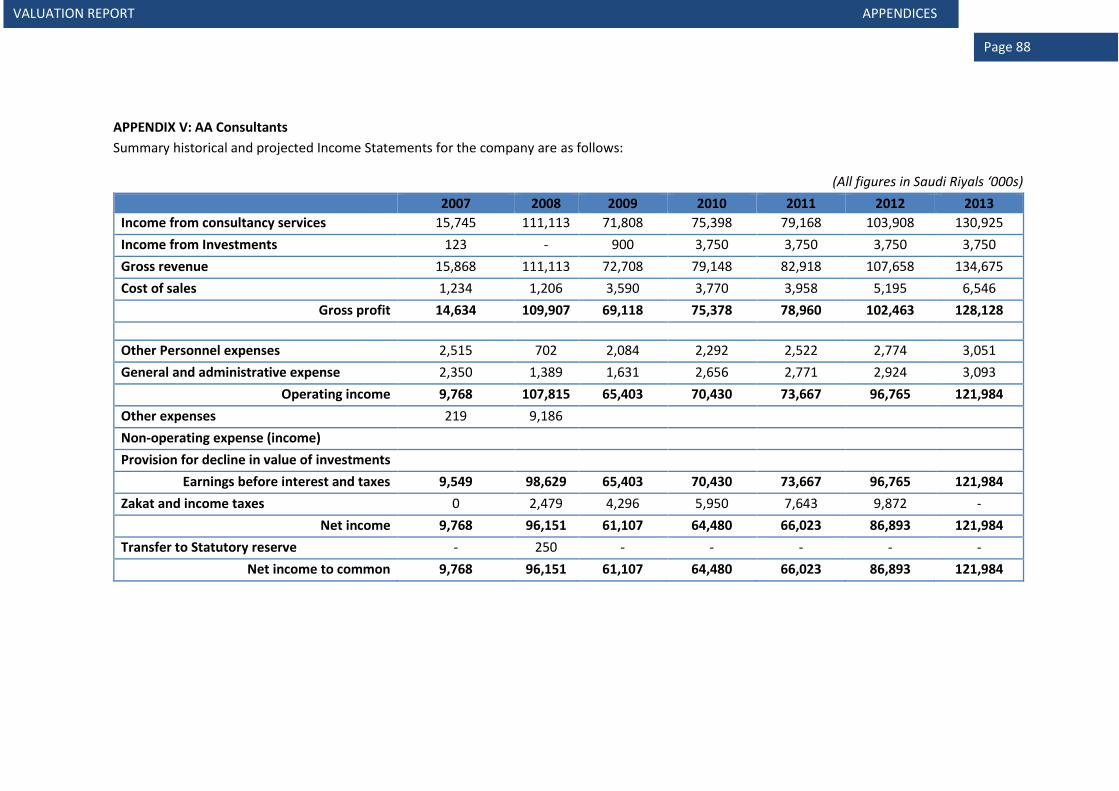

Appendix II to Appendix V.

Total revenue for the AAHGroup of companies increased significantly from 2007 to the first

half of 2008. Whereas in the entire year of 2007, the group had total revenue of around SR 24

million, in 2008, AAHGroup has already made revenues in excess of SR 130 million. This

represents a phenomenal of more than 437% growth in revenues. However, considering the

fact that 2007 was the first year of operations of the group, the revenues of the first year are

not entirely comparable with the revenues of 2008.

The historical net margins for each of the significant businesses in the group, and an

explanation of these returns are as follows:

Table 4: Historical Net Margins of group companies

Company Name Net Margin

2007 2008

VALUATION REPORT IV. AAHCOMPANY Page 36

AASCompany (AAS) 56% 54%

AATCompany (AAT) 33% 46%

AA Consultants (AA CONSULTING) 60% 89%

Net margins, in general, have improved across all companies in the group. This is primarily due to increased activity for the group, and also larger ticket business for the group.

The increased revenue for the group is a reflection of increasing confidence in the region for

the capabilities of the AAHGroup. Some of the revenues arose from new contracts with

existing customers, whereas others were a result of new contacts and references. In the year