Embed Size (px)

Citation preview

This Webcast Will Begin Shortly

If you have any technical problems with the Webcast or the streaming audio, please contact us via email at:

Thank You!

1

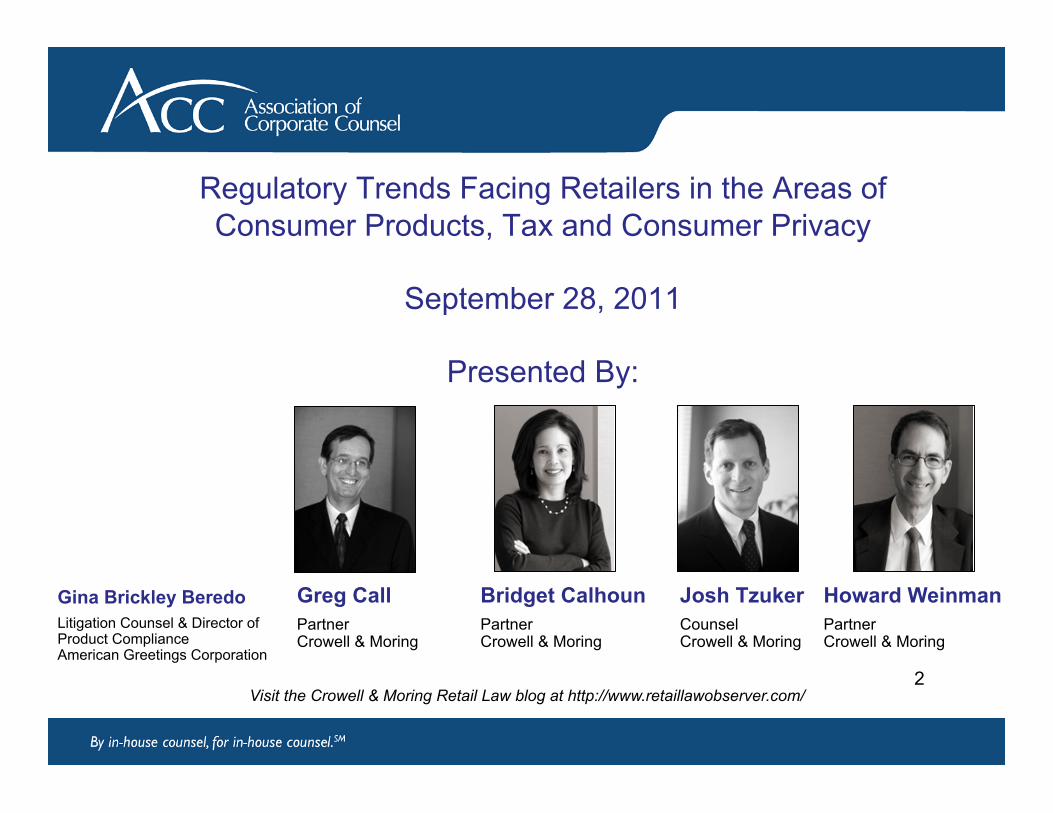

Regulatory Trends Facing Retailers in the Areas of Consumer Products, Tax and Consumer Privacy

September 28, 2011

Presented By:

Greg Call Partner Crowell & Moring

Gina Brickley Beredo Litigation Counsel & Director of Product Compliance American Greetings Corporation

Bridget Calhoun Partner Crowell & Moring

Howard Weinman Partner Crowell & Moring

Josh Tzuker Counsel Crowell & Moring

Visit the Crowell & Moring Retail Law blog at http://www.retaillawobserver.com/

2

CONSUMER PRODUCT SAFETY: HOT TOPICS FOR RETAILERS

3

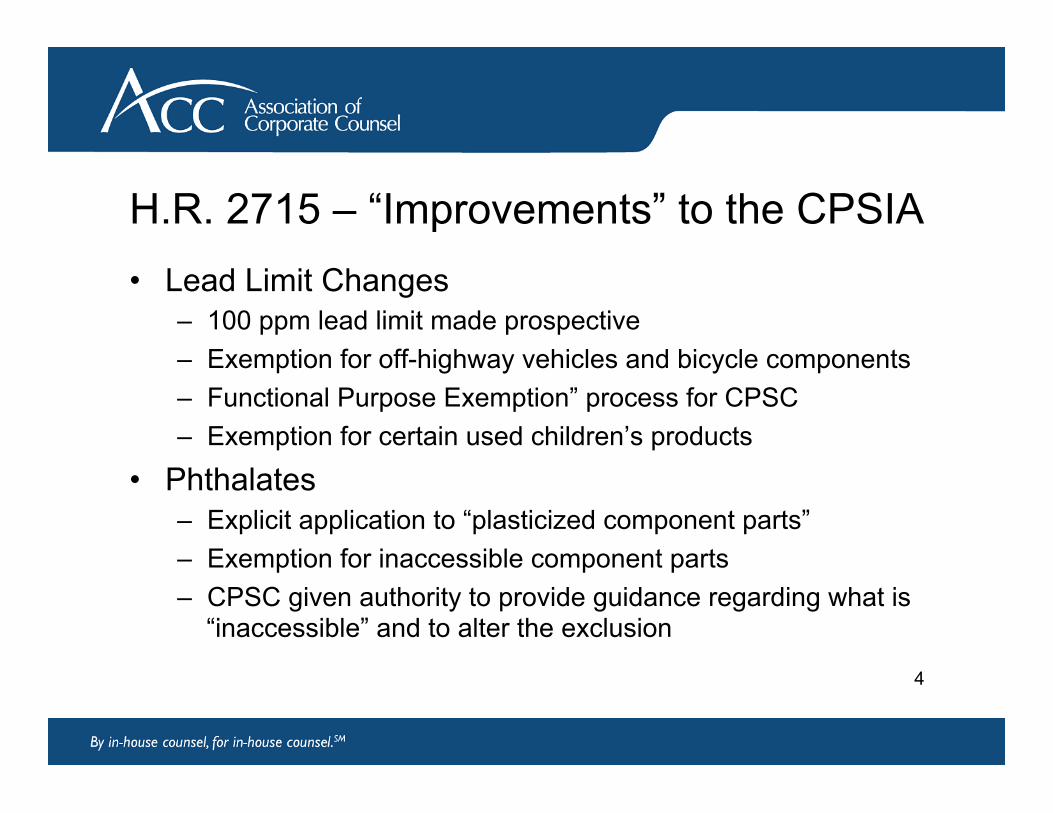

H.R. 2715 – “Improvements” to the CPSIA • Lead Limit Changes

– 100 ppm lead limit made prospective – Exemption for off-highway vehicles and bicycle components – Functional Purpose Exemption” process for CPSC – Exemption for certain used children’s products

• Phthalates – Explicit application to “plasticized component parts” – Exemption for inaccessible component parts – CPSC given authority to provide guidance regarding what is

“inaccessible” and to alter the exclusion

4

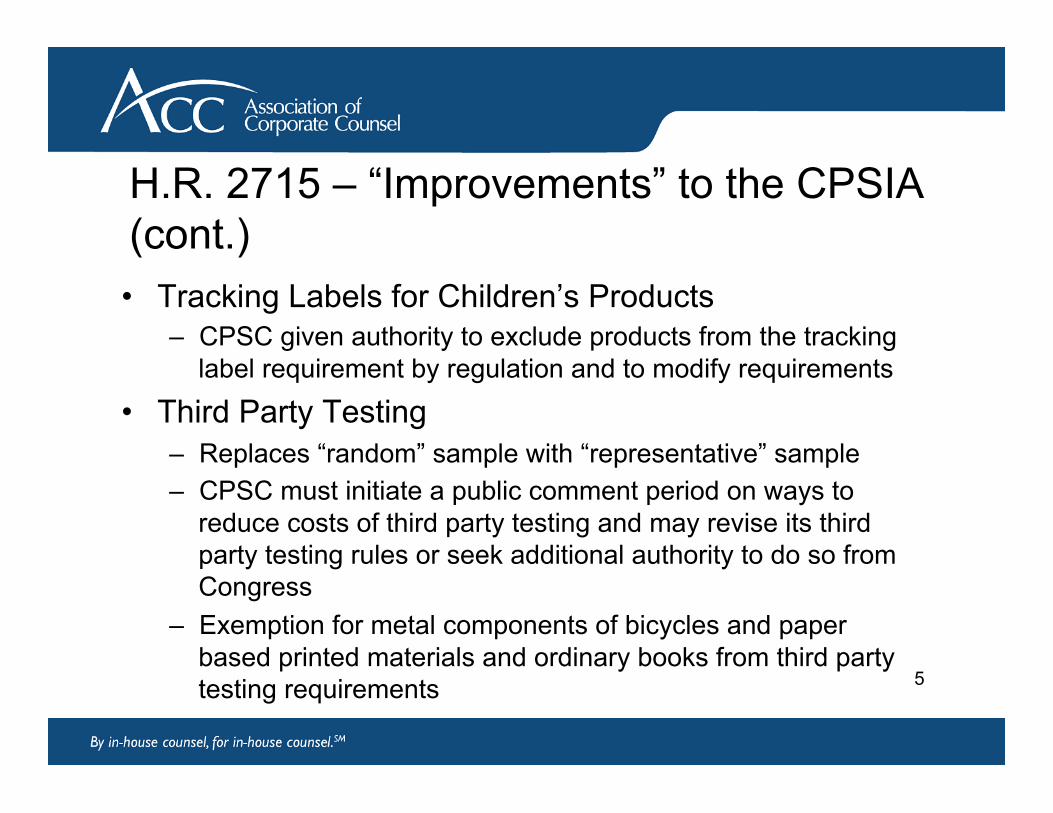

H.R. 2715 – “Improvements” to the CPSIA (cont.) • Tracking Labels for Children’s Products

– CPSC given authority to exclude products from the tracking label requirement by regulation and to modify requirements

• Third Party Testing – Replaces “random” sample with “representative” sample – CPSC must initiate a public comment period on ways to

reduce costs of third party testing and may revise its third party testing rules or seek additional authority to do so from Congress

– Exemption for metal components of bicycles and paper based printed materials and ordinary books from third party testing requirements 5

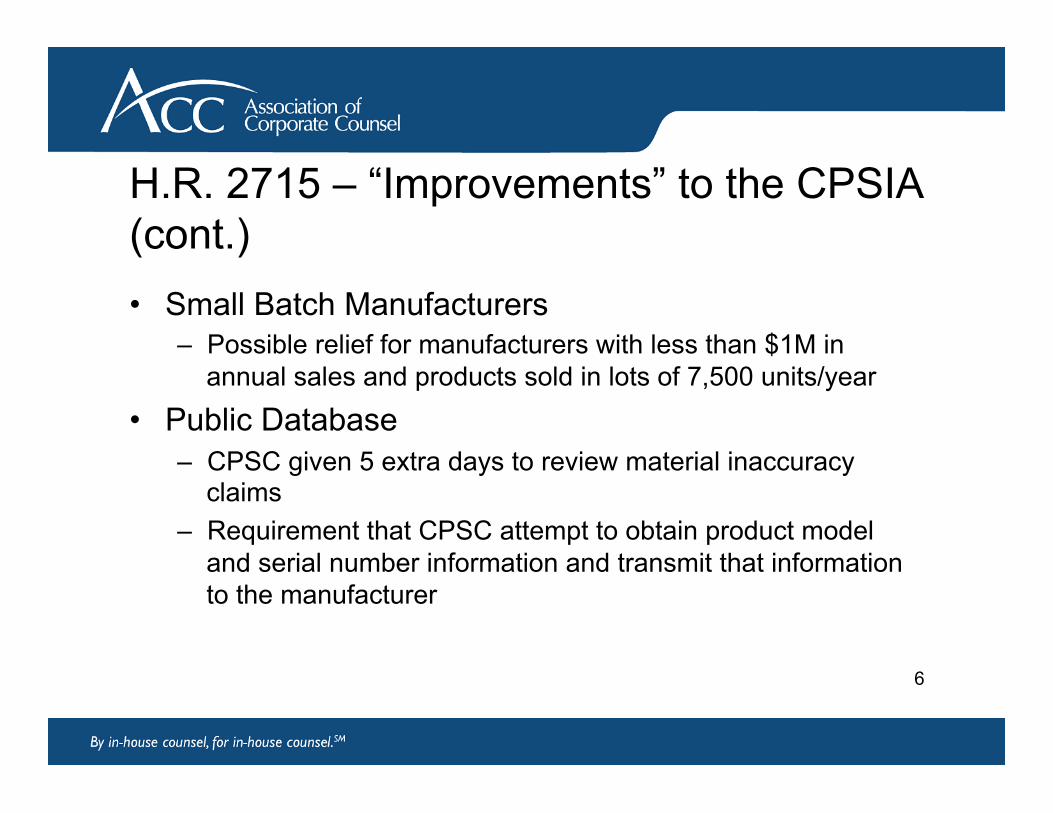

H.R. 2715 – “Improvements” to the CPSIA (cont.) • Small Batch Manufacturers

– Possible relief for manufacturers with less than $1M in annual sales and products sold in lots of 7,500 units/year

• Public Database – CPSC given 5 extra days to review material inaccuracy

claims – Requirement that CPSC attempt to obtain product model

and serial number information and transmit that information to the manufacturer

6

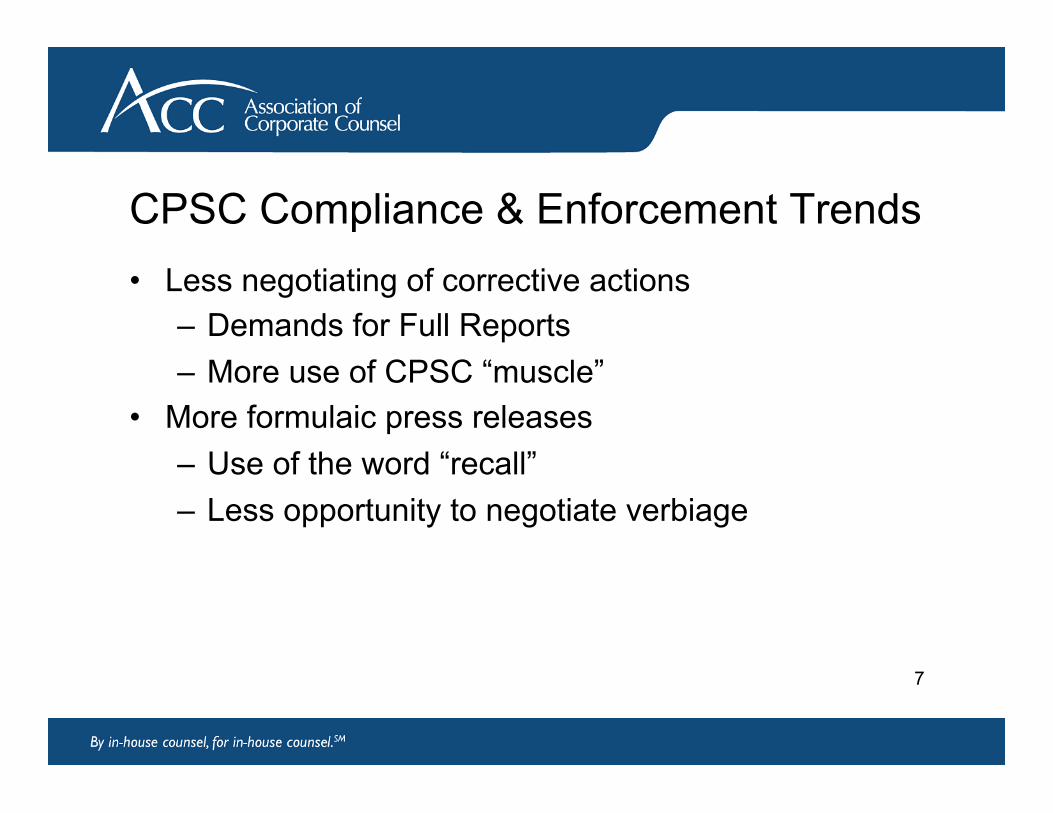

CPSC Compliance & Enforcement Trends • Less negotiating of corrective actions

– Demands for Full Reports – More use of CPSC “muscle”

• More formulaic press releases – Use of the word “recall” – Less opportunity to negotiate verbiage

7

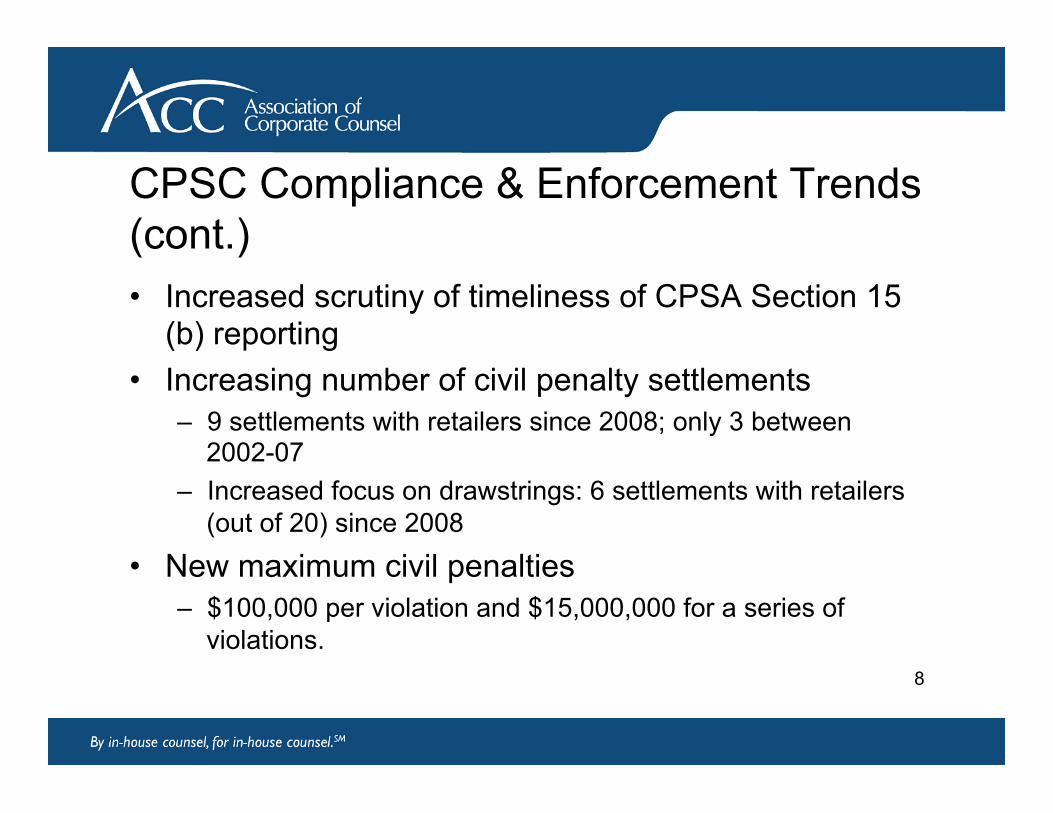

CPSC Compliance & Enforcement Trends (cont.) • Increased scrutiny of timeliness of CPSA Section 15

(b) reporting • Increasing number of civil penalty settlements

– 9 settlements with retailers since 2008; only 3 between 2002-07

– Increased focus on drawstrings: 6 settlements with retailers (out of 20) since 2008

• New maximum civil penalties – $100,000 per violation and $15,000,000 for a series of

violations. 8

Canada Consumer Product Safety Act: Reporting Triggers 1. an occurrence in Canada or elsewhere that resulted

or may reasonably have been expected to result in an individual’s death or in serious adverse effects on their health, including a serious injury;

2. a defect or characteristic that may reasonably be expected to result in an individual’s death or in serious adverse effects on their health, including a serious injury;

9

Canada Consumer Product Safety Act: Reporting Triggers (cont.) 3. incorrect of insufficient information on a label or in

instructions – or the lack of a label or instructions – that may reasonably be expected to result in an individual’s death or in serious adverse effects on their health, including serious injury; or

4. a recall or measure that is initiated for human health or safety reasons by a foreign entity or institution (or by other specified government bodies)

*For more information: http://www.hc-sc.gc.ca/cps-spc/pubs/indust/2011ccpsa_incident-lcspc/index-eng.php 10

PENDING FEDERAL TAX LEGISLATION OF

INTEREST TO RETAILERS

11

Federal Tax Reform • One reform concept is elimination of special tax

breaks, offset by an overall reduction of the 35% rate. • Large tax breaks that might be affected are

accelerated depreciation, the domestic production activities deduction, and the R&E credit.

• These breaks are most often used by manufacturers, not retailers, so reform could result in a net tax reduction for retailers.

12

“Amazon” Sales Taxes • Brick-and-mortar retailers must collect sales taxes,

but Internet out-of-state sellers need not. • Purchasers are supposed to pay use tax on Internet

purchases but seldom do. • States want the Internet sellers to collect sales tax. • Quill Corp. v. North Dakota, 504 U.S. 298 (1992)

prevents this.

13

Quill Corp. • Quill holds that a dormant commerce clause analysis

requires an Internet seller to have a physical presence in the state before a state can impose sales tax.

• Quill removed an additional due process clause impediment on taxation, and so opened the way for Congress to act.

• Almost 20 years later, Congress still has not acted.

14

State Strategies: Internet Affiliates • Some states have targeted Internet sellers with

“affiliates” (e.g., bloggers) in the state. • Under Scripto, Inc. v. Carson, 362 U.S. 207 (1960),

independent contractors who solicit in-state provide sufficient sales-tax nexus.

• New York presumes all in-state affiliates to be soliciting unless shown otherwise. If even one affiliate solicits, there is sufficient nexus.

• Amazon is litigating the New York law and has immediately cut off affiliates in all other states that passed this type of legislation.

15

State Strategies: Sister Companies • A sister company to the Amazon entity that makes

Internet sales had a distribution center in Texas. • The Texas Comptroller asserted Amazon tax liability

on the basis of the presence of the sister company. • Amazon promptly closed the distribution center and

cancelled plans for a second one. • Governor Perry opposed the Comptroller’s position.

16

Quill Update? • In Quill, the state argued that the Supreme Court

should allow state taxation of out-of-state sellers because the explosive growth of new technology (catalog sales!) had transformed commerce. The Court declined.

• It is unlikely that the Court would rule differently today. Three of the Quill Justices are still on the Court and emphasized stare decisis, so states would have to pick up 5 of the 6 remaining votes.

17

Main Street Fairness Act • The Main Street Fairness Act (S. 1452 and H.R.

2701) was introduced in July. There were similar bills in prior Congresses.

• Under the bill, states can tax remote sellers if a minimum number of states agree to specified common rules of taxation.

• The bill is designed to integrate with the Streamlined Sales and Use Tax Agreement, adopted by 24 states with 31% of the population.

18

Main Street Fairness Act • Under the bill, the agreement must provide for:

– One-stop multistate registration – Uniform definitions of products and exemptions – Uniform sourcing of transactions (no double tax) – Uniform tax return and tax payment requirements – State-level tax administration – Procedures to request a single, multi-state audit – Compensation to seller for costs of tax administration – Uniform small-seller exemption

19

Prospects for Enactment? • Prospects are uncertain. • Supported by National Retail Federation. • Amazon reportedly supports the bill. • eBay reportedly opposes it. • This type of legislation is supported by the Federation

of Tax Administrators. • Will any Republican vote for a bill that increases

taxes through improved enforcement?

20

Digital Goods and Services Tax Fairness Act of 2011 • The Digital Goods and Services Tax Fairness Act of

2011 would regulate state taxation of goods and services delivered electronically, e.g., downloads of software, music, and e-books.

• About half the states impose sales tax on digital goods and services.

• The bill would not apply to net income or ad valorem taxes.

21

Digital Goods and Services Tax Fairness Act of 2011 • The bill would prohibit:

– Multiple taxation (i.e., not allowing a credit for tax imposed by another state)

– Discriminatory taxation (a higher rate than is imposed on tangible property or non-digital services)

– Taxation at other than the customer’s stated address, where the seller does not know the actual point of delivery

– Interpreting existing laws to expand their application to digital goods and services (e.g., e-books as taxable information services)

– Applying discriminatory tax collection methods

22

Prospects for Enactment? • The bill received a hearing in a subcommittee of the

House Judiciary Committee. • Supported by Download Fairness Coalition

– Includes Amazon, Apple, Comcast, Cox, Time Warner, T-Mobile, Verizon, etc.

• Strongly opposed by the Federation of Tax Administrators.

23

Business Activity Tax Simplification Act of 2011 • Many states have read Quill as limited to sales taxes,

giving them more flexibility on other taxes. • For example, in KFC Corp. v. Iowa Dep’t of Revenue,

792 N.W.2d 308 (Iowa 2010), the court held that use of a franchisor’s intellectual property by franchisees in the state provides sufficient nexus for imposition of income tax.

• However, P.L. 86-272 prohibits state income tax on sales of tangible property where the only activity is solicitation of orders approved outside the state.

24

Business Activity Tax Simplification Act of 2011 • The Business Activity Tax Simplification Act of 2011

(H.R. 1439, “BATSA”) would impose further restrictions on state taxation.

• The bill applies to income and other business taxes, but not sales taxes.

• P.L. 86-272 protection would be expanded to apply to sales of intangible property and services.

• P.L. 86-272 would also prevent tax where the in-state contacts relate to purchasing property and the purchase decision is made outside the state.

25

Business Activity Tax Simplification Act of 2011 • Bright-line test for physical presence:

– Assigned employees – An agent who works only for you – Leased or owned real property – In all cases, not “limited or transient” – In all cases, for at least 15 days a year

• Where affiliated companies are taxed as a group, only income from companies having the required presence can be taxed.

26

Prospects? • H.R. 1439 was favorably reported by the House

Judiciary Committee. • Supported by Coalition to Protect Interstate

Commerce. – Includes Alcoa, Apple, Burger King, Caterpillar,

CBS, Citigroup, Dow, eBay, Gap, GE, Microsoft, Sony, Time Warner, Walt Disney, etc.

• This type of legislation is strongly opposed by the Federation of Tax Administrators.

27

Trash Reduction Act of 2011 • Many localities have imposed a tax on checkout bags

(usually plastic, but sometimes paper). The purpose is mostly environmental.

• The tax is usually 5¢ a bag. • Coverage often varies by type of retailer (e.g.,

grocery, department store, restaurant, convenience store).

• Sometimes, only large retailers are affected.

28

Trash Reduction Act of 2011 • The Trash Reduction Act of 2011 (H.R. 1628) would

impose a 5¢ tax on each carryout bag provided at checkout by a retailer, except reusable bags.

• There is no coordination with existing local taxes.

29

Prospects? • As a new tax, this is not going anywhere soon, but may

serve as a basis for future legislation. • Retailers do not necessarily oppose this legislation.

– Checkout bags are a cost that the bill could reduce. – Some retailers make a profit selling branded reusable

bags at checkout. – The bill would defray the retailer’s administrative costs. – For chain retailers, a uniform Federal law might be

better than a patchwork of local laws. • Bag manufacturers have strongly opposed similar

proposals at the state and local level.

30

IRS Circular 230 Disclosure • To comply with certain U.S. Treasury regulations, we

inform you that, unless expressly stated otherwise, any U.S. federal tax advice contained in this communication was not intended or written to be used, and cannot be used, by any taxpayer for the purpose of avoiding any penalties that may be imposed on such taxpayer by the Internal Revenue Service. To the extent that a state taxing authority has adopted rules similar to the relevant provisions of Circular 230, use of any state tax advice contained herein is similarly limited.

31

LEGISLATIVE CLIMATE ON PRIVACY ISSUES AND ITS

IMPACT ON RETAILERS

32

Protecting Consumer Privacy Enjoys Bi-Partisan Support

• Establishing a regulatory framework for data-security and consumer privacy is one of the few areas where there might be legislative progress

• The White House has established an inter-agency task force and working group with Congressional leaders in hopes of establishing a “baseline” for regulations

• More than 30 individual bills have been introduced in both chambers of Congress

33

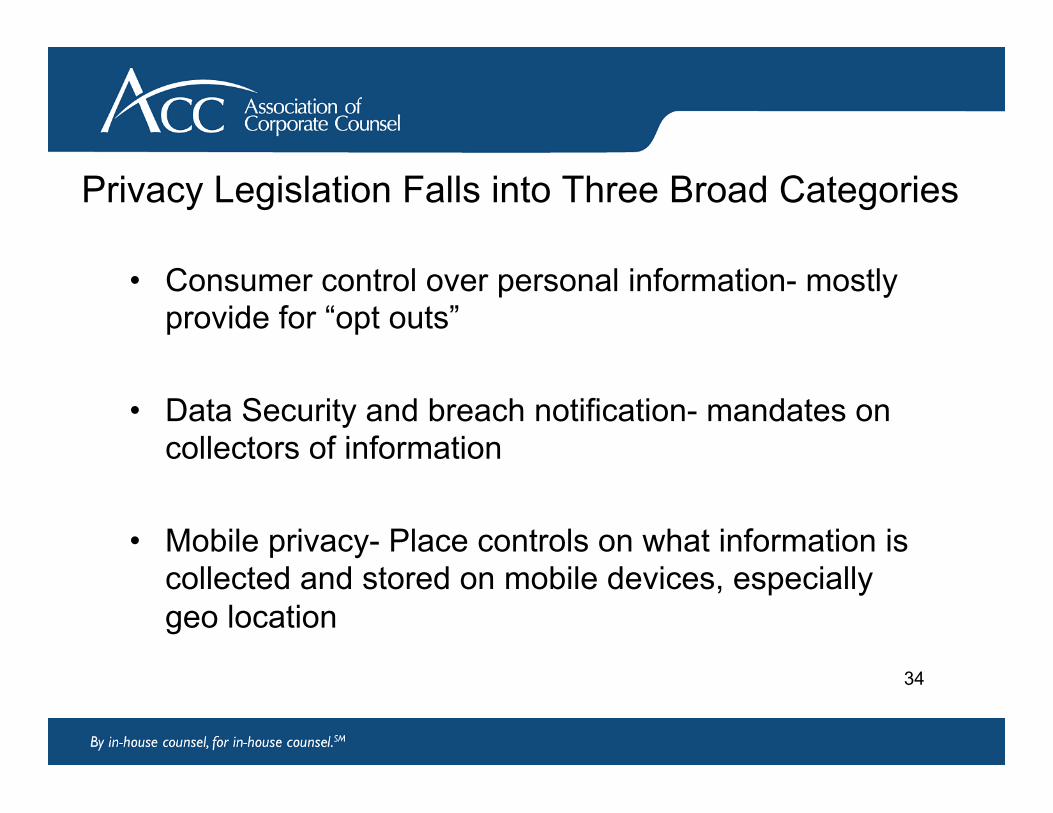

Privacy Legislation Falls into Three Broad Categories

• Consumer control over personal information- mostly provide for “opt outs”

• Data Security and breach notification- mandates on collectors of information

• Mobile privacy- Place controls on what information is

collected and stored on mobile devices, especially geo location

34

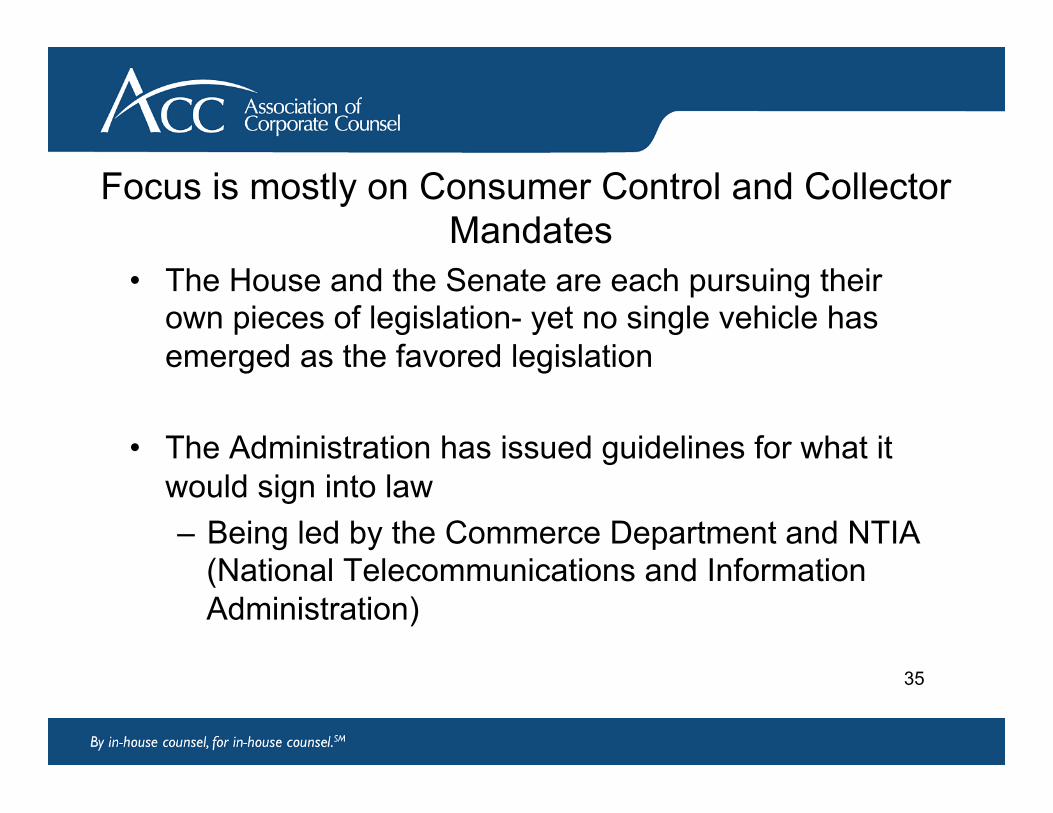

Focus is mostly on Consumer Control and Collector Mandates

• The House and the Senate are each pursuing their own pieces of legislation- yet no single vehicle has emerged as the favored legislation

• The Administration has issued guidelines for what it would sign into law – Being led by the Commerce Department and NTIA

(National Telecommunications and Information Administration)

35

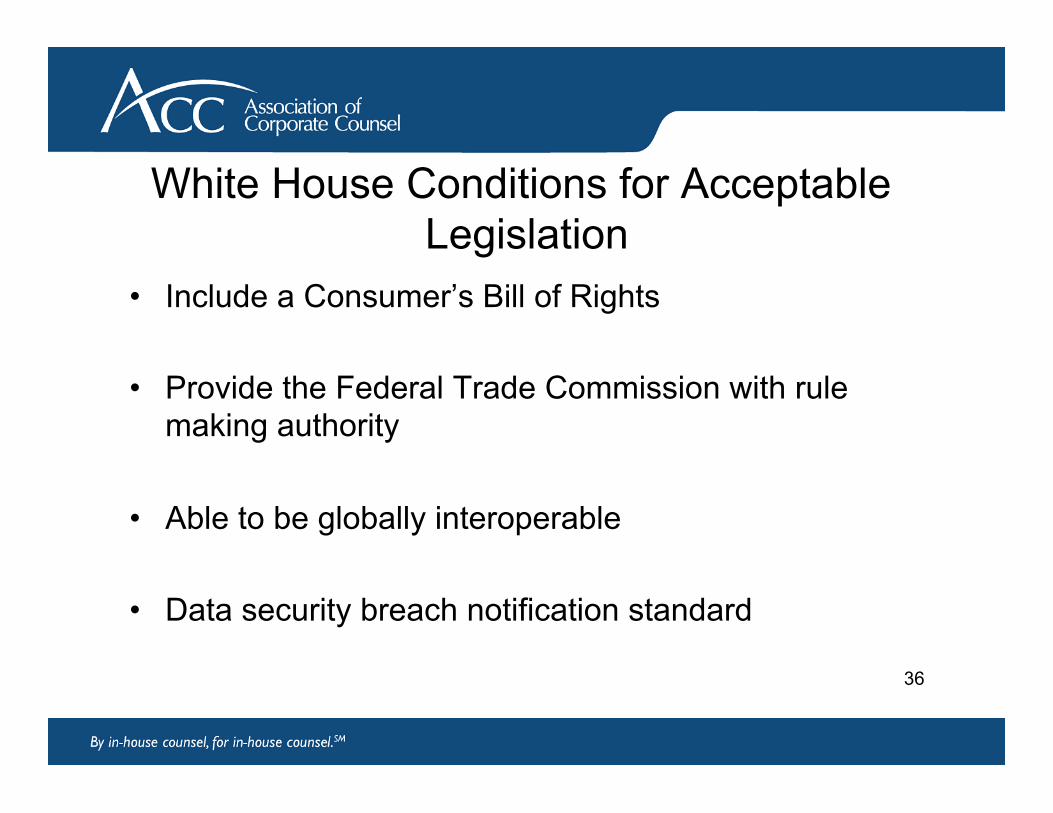

White House Conditions for Acceptable Legislation

• Include a Consumer’s Bill of Rights

• Provide the Federal Trade Commission with rule making authority

• Able to be globally interoperable

• Data security breach notification standard

36

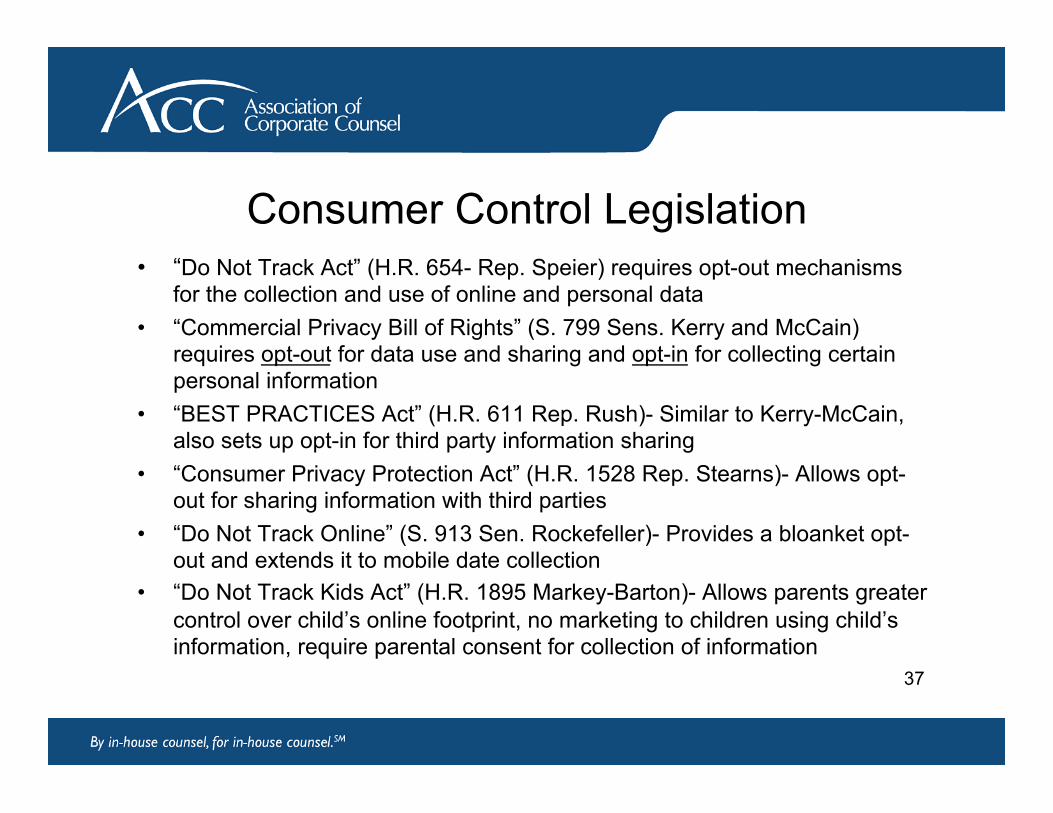

Consumer Control Legislation • “Do Not Track Act” (H.R. 654- Rep. Speier) requires opt-out mechanisms

for the collection and use of online and personal data • “Commercial Privacy Bill of Rights” (S. 799 Sens. Kerry and McCain)

requires opt-out for data use and sharing and opt-in for collecting certain personal information

• “BEST PRACTICES Act” (H.R. 611 Rep. Rush)- Similar to Kerry-McCain, also sets up opt-in for third party information sharing

• “Consumer Privacy Protection Act” (H.R. 1528 Rep. Stearns)- Allows opt-out for sharing information with third parties

• “Do Not Track Online” (S. 913 Sen. Rockefeller)- Provides a bloanket opt-out and extends it to mobile date collection

• “Do Not Track Kids Act” (H.R. 1895 Markey-Barton)- Allows parents greater control over child’s online footprint, no marketing to children using child’s information, require parental consent for collection of information

37

Data Security and Breach Notification • “Data Security and Breach Notification Act” (S. 1207 Sen. Rockefeller)-

Requires businesses and non-profits that store information to create security and consumer alert measures. Free credit monitoring for consumers if there is a breach.

• “Personal Data Privacy Act” (S. 1151 Sen. Leahy)- Creates federal standard for breach notification, establish baseline security procedures

• “SAFE Data Act” (Rep. Bono-Mack)- Businesses must notify consumers and FTC w/in 48hrs. of breach; minimize storage of personal information; free credit monitoring

• DATA Act (Rep. Rush and Stearns)- Mandates stricter data security policies; sets standards on notification if there is a breach

38

Likelihood of Action • The Senate Judiciary Committee has already begun to write it’s

legislation • The White House advisor on consumer privacy has said we should

follow an approach of, “Privacy law without regulation” – Create a recognized framework for consumers – Encourage businesses to create best practices

• “Businesses with responsible practices ought not to face additional burdens”

• Concern in Congress over whether efforts should be broad or contained to just the consumer space – One of the few areas where there is general bi-partisan agreement

39

What Action Could Mean for Business • Depending on scope of legislation could impact

retailers, ad networks, third party marketers, advertisers, mobile application developers etc.

• Could create hindrances for sharing information about consumer tastes

• Shorten the retention time of consumer information • Could decrease effectiveness of online or targeted

advertisements • Breached entities might lose consumer confidence

40

Questions?

41

Thank you for attending another presentation from

ACC’s Desktop Learning Webcasts

Please be sure to complete the evaluation form for this program as your comments and ideas are helpful in planning future programs.

If you have questions about this or future webcasts, please contact ACC at [email protected]

This and other ACC webcasts have been recorded and are available,

for one year after the presentation date, as archived webcasts at http://webcasts.acc.com.

42

![This Webcast Will Begin Shortly - Association of Corporate ...webcasts.acc.com/handouts/ACC_RCRA_Webinar[1].pdf · This Webcast Will Begin Shortly ... housekeeping and labelling is](https://img.pdfslide.net/doc/110x75/5ac16dd17f8b9ae45b8d59ff/this-webcast-will-begin-shortly-association-of-corporate-1pdfthis-webcast.jpg)