Embed Size (px)

Citation preview

Thriving In The As-a-Service Economy

Charles Sutherland

EVP, Research

Hema Santosh

Principal Analyst

HfS Blueprint Report

Procurement As-a-Service

Excerpt for Accenture

June 2015

© 2015 HfS Research Ltd. Accenture Excerpt 20150050 Proprietary │Page 2

TOPIC PAGE

Executive Summary 3

Research Methodology 8

Key Market Dynamics 16

Service Provider Grid 40

Service Provider Profile 44

Market Wrap-Up & Recommendations 46

About the Authors 51

Table of Contents

Executive Summary

© 2015 HfS Research Ltd. Accenture Excerpt 20150050 Proprietary │Page 4

Introduction to the HfS Blueprint Report:

Procurement As-a-Service

The Procurement As-a-Service HfS Blueprint Report a unique view of this dynamic market. Unlike other quadrants and matrices, the HfS Blueprint identifies relevant differentials between service providers across a number of facets under two main categories: innovation and execution.

HfS is emphasizing the focus on Procurement As-a-Service, with 47% of the Blueprint scoring being tied to proven innovation capability and performance is changing this market offering.

HfS Blueprint Report ratings are dependent on a broad range of stakeholders with specific weightings based on 1,109 stakeholder interviews from the 2014 State of Outsourcing Survey that covered:

• Procurement Outsourcing Enterprise Service Buyers

• Procurement Outsourcing Service Providers

• Procurement Outsourcing Industry Influencers (sourcing advisors and management consultants)

• HfS Sourcing Executive Council Members with Procurement engagements

• HfS Research Analysts with hands-on Procurement knowledge and experience

© 2015 HfS Research Ltd. Accenture Excerpt 20150050 Proprietary │Page 5

Key Highlights – State of the Procurement

Outsourcing Market

Moving To As-a-Service. We are certainly not there yet, but procurement outsourcing service providers have made extensive efforts over the last several years to further transform their offerings from “lift and shift” transactional procurement together with consulting led sourcing to more modular, integrated, technology based as-a-Service solutions.

Slowing Growth. Procurement outsourcing while still much smaller than F&A or HR is becoming a substantial multi-billion market and with that we have seen a slowdown in overall market growth from 10%+ a few years ago to something more in the 6% range and so the competition for new clients and renewing deals is greater than ever.

Procurian Acquisition Didn’t Change The Landscape. When we saw Accenture’s acquisition of Procurian in 2013, HfS expected to see follow-on acquisitions of sourcing/category service providers by the likes of Capgemini and Genpact in particular. That hasn’t happened and instead service providers have entered into many more partnerships for technology platforms and for sourcing and category management expertise.

The Nature Of Transactional Procurement Is Changing. Transactional Procurement for the last decade has often looked like a “lift and shift” model supplemented by post transition process excellence projects by service providers. In the last 18 months, we have seen a rapid evaluation of the potential first for robotic process automation and of late cognitive computing as well to this process in order to move away from the labor arbitrage heavy model of the past and to improve overall delivery speed and quality.

© 2015 HfS Research Ltd. Accenture Excerpt 20150050 Proprietary │Page 6

Key Highlights – State of the Procurement

Outsourcing Market (Continued)

Sourcing And Category Management Still In Demand. Client value creation and service provider differentiation often depend on the breadth and depth of the available sourcing staff in the service provider. The battle to hire and retain sourcing expertise is significant especially as clients in both North America and Europe are looking for the on-site availability of consultants from their outsourcing service providers. Many of the strategic actions undertaken over the last several years by the service providers including acquisitions and partnerships have been made in order to address gaps in organic indirect sourcing category coverage.

Procurement Technology And Technology Management Has Never Been More Important. Service provider technology has always played a role in procurement delivery but in the present market with the increased availability of SaaS solutions it has increased again in importance. We have increased the attention and weighting given to technology in this iteration of the Blueprint and spent even more time reviewing service provider capabilities and strategies for technology as well as what it feels like to be an enterprise client today that is increasingly reliant on technology they no longer control to deliver procurement results.

The Winner’s Circle Is Still Largely The Same. Through all of these changes in the market, the competitive environment remains similar today to what it was over the last few years. Some of the specialized service providers have come to the fore but overall, this is a market still dominated in size by Accenture, Capgemini, GEP, IBM, Infosys and Xchanging with other service providers either operating in specific niches or trying to move up to larger deals going forward.

© 2015 HfS Research Ltd. Accenture Excerpt 20150050 Proprietary │Page 7

What Has Changed Since the 2013 Blueprint on

Procurement Outsourcing

Post Procurian World. Accenture’s acquisition of Procurian in late 2013 certainly changed the Winner’s Circle creating one larger market leader and also forcing several service providers to seek new partners for their sourcing and category management capabilities. It did not lead to the further M&A activity in this market that we anticipated back at the beginning of 2014 however.

As-a-Service. Over the last two years we have seen previous solution models of end-to-end procurement lift and shift and sourcing consultancy become impacted by the arrival of more modular technology supported service delivery models. While still not the broad norm, this “As-a-Service” approach is setting roots in many service providers and we expect this to increasingly be the norm in the years to come.

Partnerships. Clearly partnerships between service providers born out of the transactional procurement market (e.g. TCS, Genpact, WNS) and those out of the technology (e.g. GEP) or strategic sourcing (e.g. Proxima, AT Kearney) are more prevalent in 2015 than they were back in 2013 as service providers construct end-to-end offerings to better compete with the largest players in the market.

Acquisition Integration. Over the last few years, past procurement acquisitions (e.g. MarketMaker4, Portland Group, Procurian) have all been well integrated into their new homes and have begun to significantly impact the strategies and capabilities of their acquirers.

Gradual Movement. Perhaps the biggest change since 2013 though is actually the lack of overall change. The market leaders of 2013 are generally still the market leaders of 2015 with some specialists providers becoming more noticeable but otherwise less revolution than we would have expected back in 2013.

Research Methodology

© 2015 HfS Research Ltd. Accenture Excerpt 20150050 Proprietary │Page 9

Research Methodology

Data Summary

More than 25,000 data points were collected from more than 900 live Procurement Outsourcing and Technology contracts, covering 18 major service providers.

Data was collected in Q1 2015, covering buyers, providers, and advisors/influencers of Procurement Outsourcing.

Participating Service Providers

This Report is Based On: Tales from the Trenches: Interviews were

conducted with buyers who have evaluated service providers and experienced their services. Some were supplied by service providers, but many interviews were conducted by HfS Executive Council members and participants in our extensive market research.

Sell-Side Executive Briefings: Structured discussions with service providers were intended to collect data necessary to evaluate their innovation, execution and market share, and deal counts.

HfS “State of Outsourcing” Survey: The industry’s largest quantitative survey, conducted with the support of KPMG, covering the views, intentions, and dynamics of 1,100+ buyers, providers, and influencers of outsourcing.

Publicly Available Information: Financial data, website information, presentations given by senior executives, and other marketing collateral were evaluated.

© 2015 HfS Research Ltd. Accenture Excerpt 20150050 Proprietary │Page 10

Procurement As-a-Service Process Value Chain

STRATEGIC SOURCING

• Spend Data Management

• Demand Management

• External Marketplace Analysis

• Sourcing Strategy

• Sourcing Event Management

• Proposal Evaluation

TRANSITIONAL PROCUREMENT

• Procurement Help Desk

• Accounts Payable

• Invoice/Receipt Match Reconciliation

• Asset Management

SUPPLIER MANAGEMENT

• Supplier Enablement

• Supplier Help Desk

• Supplier Accreditation

• SLA Monitoring

• Vendor Relationship Management

CONTRACT MANAGEMENT

• Contract Repository

• Contract Administration

• Contract Template Management

• Ongoing Contractual Negotiation Support

TECHNOLOGY MANAGEMENT

• Initial technology solutions

• Ongoing technology innovation

• Platform implementation

• Platform management

© 2015 HfS Research Ltd. Accenture Excerpt 20150050 Proprietary │Page 11

Key Factors Driving the HfS Blueprint

EVALUATION CRITERIA

Two major factors:

• Execution represents service providers’ ability to deliver services. It includes:

– Solutions in the Real World – Quality of Customer Relationships – Market Share

• Innovation represents service providers’ ability to improve services. It includes:

– Vision for End-to-End Process Lifecycle

– Integration of BPO and ITO – Vision to Tailor Solution for Specific

Industries – Leveraging External Drivers

CRITERIA WEIGHTING

Criteria are weighed by crowdsourcing weightings from the four groups that matter most:

• Enterprise Buyers [$5B+] (20%)

• Buyers (20%)

• Service Providers (30%)

• HfS Research Analysts Team (20%)

• Advisors, Consultants, and Industry Stakeholders (10%)

Weightings from this report come from HfS’s January 2013 State of Outsourcing Study

© 2015 HfS Research Ltd. Accenture Excerpt 20150050 Proprietary │Page 12

How the HfS Blueprint Scores Are Compiled

Provider G Provider J

Provider B Provider G

Provider A Provider B

vs.

vs.

vs. After service providers respond to HfS’s Blueprint RFI and client references and fact checking have been completed, HfS analysts conduct a paired comparisons survey of service providers in each category of evaluation. This can be as many as 1,100+ unique service provider comparisons.

The data/rankings are compiled and compared across all provider comparisons to identify inconsistencies within the scores.

After a further data refinement, the criteria weightings are used to give each service provider a score in each evaluation criteria component.

Once aggregation and scoring are complete, the service providers’ scores are plotted, producing the HfS Blueprint.

© 2015 HfS Research Ltd. Accenture Excerpt 20150050 Proprietary │Page 13

HfS Blueprint Scoring Percentage Breakdown

EXECUTION 52.69%

Quality of Customer Relationships 22.70%

Quality of Account Management Team 11.30%

How Service Providers Engage Customers and Develop Communities 4.67%

How Service Providers Incorporate Customer Feedback 6.73%

Real-World Delivery Solutions 21.45%

Actual Delivery of Services for Each Sub-Process 10.78%

Strategic Sourcing 4.00%

Transaction Procurement 4.00%

Supplier Management 1.00%

Contract Management 1.00%

Technology Management 0.78%

Geographic Footprint and Scale 3.18%

Usefulness of Services to Specific Client Needs of All Sizes 7.49%

Flexibility to Deliver End-to-End Solutions and Point Solutions 4.20%

Experience Delivering Industry Specific Solutions Including Direct Sourcing 3.29%

Flexible Pricing Models Including Gain Sharing To Meet Customer Needs 8.54%

INNOVATION 47.31%

Vision for End-to-End Process Lifecycle 15.10%

Concrete Plans to Deliver Value Beyond Cost and Investment in Future Capabilities 5.06%

Integration of As A Service Capabilities Into Procurement Outsourcing 5.93%

Continuous Improvement Methodology and Capability 4.11%

Vision for The Evolution of Procurement As A Service 16.86%

Ability to Leverage External Value Drivers 15.35%

Integration of New Technologies into Procurement Process 8.58%

Incorporate Regulatory Requirements Quickly and Proactively 6.77%

TOTAL 100.00%

© 2015 HfS Research Ltd. Accenture Excerpt 20150050 Proprietary │Page 14

Execution Definitions

EXECUTION How well does the service provider execute on it's contractual agreement and how well does the provider manage the client/provider relationship?

Quality of Customer Relationships How engaged are service providers in managing the client relationship based on the following metrics: quality of account management, service provider / client engagement, and incorporation of feedback?

Quality of Account Management Team What is the quality level of professional skills in the account management team?

How Service Providers Engage Customers and Develop Communities

How well does the service provider engage clients and develop client communities?

How Service Providers Incorporate Customer Feedback

How have service providers taken feedback and incorporated that feedback into their product/solution?

Real-World Delivery Solutions Does the solution provided compare favorably to the service agreed upon when taking into account delivery of services for each sub-process and geographic footprint and scale?

Actual Delivery of Services for Each Sub-Process

Taking into account each sub process and the entire macro process, does each sub-process sum to successful delivery of the service being provided For example in the Procurement Outsourcing macro process of Strategic Sourcing, are all sub-processes being delivered upon successfully?

Geographic Footprint and Scale Specific to the category, to what degree do service providers have geographic locations that offer strategic value and do they have scale?

Usefulness of Services to Specific Client Needs of All Sizes

How flexible and experienced are providers when tailoring solutions based on client size, location, and type of solution (end-to-end and single point)?

Flexibility to Deliver End-to-End Solutions and Point Solutions

How flexible are service providers with delivering multi-process end-to-end solutions vs. single point solutions?

Experience Delivering Industry Specific Solutions

How experienced are service providers at delivering solutions to the specific needs of different industries?

Flexible Pricing Models to Meet Customer Needs How flexible are service providers when determining pricing of contracts? Are they willing to make investments into the client’s firm for long term growth?

© 2015 HfS Research Ltd. Accenture Excerpt 20150050 Proprietary │Page 15

Innovation Definitions

INNOVATION Innovation is the combination of improving both services and business outcomes.

Vision for End-to-End Process Lifecycle The strategy for delivery services to each part of the processes "value chain". For example, in Finance and Accounting, the components of the value chain may include order to cash, record to report, and procure to pay. In Procurement Outsourcing, the components of the value chain include strategic sourcing, transactional procurement, supplier management, contract management and technology management.

Concrete Plans to Deliver Value Beyond Cost and Investment in Future Capabilities

Clear understanding of what value levers exist and how the service provider will deliver that value. Examples of value may include labor arbitrage, technology, analytics, quality, revenue, global scale, and flexibility.

Integration of Technology Into Business Process

How the service provider integrates applications with manual labor to improve value to clients. Service providers may provide cloud-enabled technology, SaaS, business platforms, BPaaS workflow, social , or mobility applications. Service provide may also develop in-house software and tools for providing point solutions for addressing specific procurement business challenges.

Continuous Improvement Methodology and Capability

How well does the service provider execute on improving business process and capabilities of their solutions?

Vision for the Evolution of Procurement As-a-Service

Does the service provider have a vision for how the mortgage market is developing and how they need to respond as a service provider to these changes both in terms of specific capabilities and in their commercial and operating approach?

Ability to Leverage External Value Drivers How well have service providers integrated external value drivers into their services?

Integration of New Technologies Into Procurement Process

How well does the the service provider integrate emerging new technologies (proprietary and third party) into the delivery of the procurement process?

Incorporate Regulatory Requirements Quickly and Proactively

How well does the service provider respond to the specific regulatory requirements by industry or cross-industry for Procurement related business processes?

Key Market Dynamics

© 2015 HfS Research Ltd. Accenture Excerpt 20150050 Proprietary │Page 17

Procurement As-a-Service is Based on Realizing the Eight

Ideals of the As-a-Service Economy

LEGACY OUTSOURCING AS-A-SERVICE ECONOMY

Resolve problems by looking first at the process

1. Design Thinking Generate creative solutions by understanding the business context

Complex, often painful technology and process transitions to reach steady state

2. Business Cloud “Plug and Play” business services

Fragmented processes requiring manual interventions, multiple technologies

3. Intelligent Automation Blending of automation, analytics, and talent

Operations staff doing mostly transactional tasks

4. Proactive Intelligence Operations focused on interpreting data, seeding new ideas

Ad-hoc analysis on unstructured data with little business context

5. Intelligent Data Real-time applied analytics models, techniques, and insights from big data

Legacy technology investments drain budgets to remain functional

6. Write Off Legacy Use of platform-based services makes many tech investments redundant

Governance staff manage contracts and service levels

7. Brokers of Capability Governance staff manage towards business-driven outcomes

Pricing and relationships based on cost, effort, and labor

8. Intelligent Engagement Pricing and relationships based on expertise, outcomes, and subscriptions

Simplification

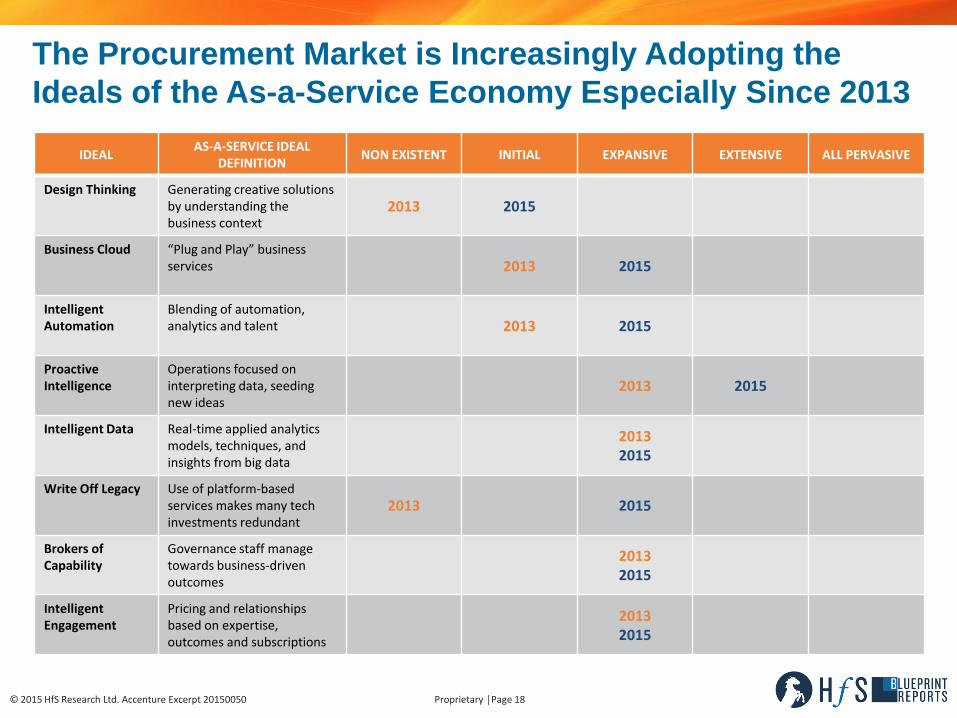

© 2015 HfS Research Ltd. Accenture Excerpt 20150050 Proprietary │Page 18

The Procurement Market is Increasingly Adopting the

Ideals of the As-a-Service Economy Especially Since 2013

IDEAL AS-A-SERVICE IDEAL

DEFINITION NON EXISTENT INITIAL EXPANSIVE EXTENSIVE ALL PERVASIVE

Design Thinking Generating creative solutions by understanding the business context

2013 2015

Business Cloud “Plug and Play” business services 2013 2015

Intelligent Automation

Blending of automation, analytics and talent 2013 2015

Proactive Intelligence

Operations focused on interpreting data, seeding new ideas

2013 2015

Intelligent Data Real-time applied analytics models, techniques, and insights from big data

2013 2015

Write Off Legacy Use of platform-based services makes many tech investments redundant

2013 2015

Brokers of Capability

Governance staff manage towards business-driven outcomes

2013 2015

Intelligent Engagement

Pricing and relationships based on expertise, outcomes and subscriptions

2013 2015

© 2015 HfS Research Ltd. Accenture Excerpt 20150050 Proprietary │Page 19

Procurement As-a-Service Process Value Chain

STRATEGIC SOURCING

• Spend Data Management

• Demand Management

• External Marketplace Analysis

• Sourcing Strategy

• Sourcing Event Management

• Proposal Evaluation

TRANSITIONAL PROCUREMENT

• Procurement Help Desk

• Accounts Payable

• Invoice/Receipt Match Reconciliation

• Asset Management

SUPPLIER MANAGEMENT

• Supplier Enablement

• Supplier Help Desk

• Supplier Accreditation

• SLA Monitoring

• Vendor Relationship Management

CONTRACT MANAGEMENT

• Contract Repository

• Contract Administration

• Contract Template Management

• Ongoing Contractual Negotiation Support

TECHNOLOGY MANAGEMENT

• Initial technology solutions

• Ongoing technology innovation

• Platform implementation

• Platform management

© 2015 HfS Research Ltd. Accenture Excerpt 20150050 Proprietary │Page 20

The Current Maturity of Procurement As-a-Service Offerings

STRATEGIC SOURCING

TRANSACTIONAL PROCUREMENT

SUPPLIER MANAGEMENT

CONTRACT MANAGEMENT

TECHNOLOGY MANAGEMENT

Spend Data Management

Procurement Help Desk Supplier Enablement Contract Repository Initial Technology

Solutions

Demand Management Accounts Payable Supplier Help Desk Contract Administration Ongoing Technology

Innovation

External Marketplace Analysis

Invoice/Receipt March Reconciliation

Supplier Accreditation Contract Template

Management Platform

Implementation

Sourcing Strategy Asset Management SLA Monitoring Ongoing Contractual Negotiation Support

Platform Management

Sourcing Event Management

Proposal Evaluation

Mature Competitive market with examples of service offerings and customer case studies from large number of service providers

Nascent Market in development with very few examples of service offerings and customer case studies

© 2015 HfS Research Ltd. Accenture Excerpt 20150050 Proprietary │Page 21

Strategic Issues for Procurement Service Providers

When Is Transactional Procurement Part of Procurement or Part of F&A BPO. For many service providers, transactional procurement opportunities are as likely to be part of their F&A offerings as they are part of a Procurement BPO offering HfS recognizes that the boundaries are fluid around Transactional Procurement (especially on accounts payable) when it often comes down to where in the organization the key buyer(s) sit in terms of how they actually describe the solution that has been purchased from a service provider.

Is It BPO or Consulting. One issue for Procurement BPO service providers with consulting strength in strategic sourcing is that many client requirements could be addressable with either BPO based or consulting based solutions. This creates internal confusion (and sometimes client confusion as well) in the sales and solutioning process and is one of the key reasons why those service providers need to invest in strong offering skills so that the boundaries of different possible client solutions can be shaped and well communicated to all.

Durability of Partnerships. Many service providers have entered into significant partnerships over the last several years either for access to technology or access to sourcing and category management expertise in order to build end-to-end capabilities across the value chain. Some of these partnerships have delivered real results but others remain largely limited to being paper alliances without substance. Because many of these partnerships are with potential competitors there are questions in our mind about their long term durability and whether this is a sustainable model or if these partner dependent service providers will just need to step up and make more substantial investments in capabilities in order to compete with the end-to-end service providers who make up the Winner’s Circle of 2015.

Indirect or Direct Spend Focus. The dominant area of spend management for procurement outsourcing service providers is for indirect spend categories. While attempts have been made by many of the profiled service providers to develop direct category expertise in general this has not proven to be as successful for service providers or as compelling for the enterprise as would be believed. That said many clients especially in manufacturing, utilities and high tech verticals continue to ask for this support and service providers will continually need to evaluate how much attention they are going to put into this capability over time.

© 2015 HfS Research Ltd. Accenture Excerpt 20150050 Proprietary │Page 22

More Strategic Issues for Procurement Service Providers

The Role of Robotic Process Automation. Procurement delivery can be expensive and very manual with a reliance on specialized delivery resources. Many service providers are looking to robotic process automation as one way to increase delivery quality and reduced overall delivery costs for very rules based activities and transactions in procurement. It is still early days for RPA in Procurement but the initial pilots and case studies are coming in and they look promising so the question now for service providers is how far do they push automation in these processes and how willing are clients today to accept this greater automation.

Addressing Tail Spend Management. Solving for costly (or rogue) spend in the long tail of spend categories is relatively high on the mind of many CPOs and business unit leaders in the enterprise and hence it is a trendy topic for service providers as well. Unfortunately, its not that easy to manage the long tail of spend and especially to do so in a way that the client is happy and the service provider is actually making a profit on the operations. This issue of tail spend management isn’t going away and if anything it is becoming more prominent as more and more CPOs look for solutions, the strategic question for most service providers is whether they can use technology and automation in particular to solve this client issue in a profitable way going forward.

Market Intelligence. The role and delivery forms for market intelligence are changing fast. Monthly newsletters or quarterly published data books are fast being replaced by mobility based services and on-demand insights. Many of the service providers in this report still rely on third parties to deliver this capability and its not clear that many of these third parties are keeping up with some of the proprietary capabilities and therefore with client expectations either. Service providers across the board need to be looking at what market intelligence they are creating which is truly of value and what investments in proprietary insight should they be developing in order to keep up with the innovative leaders today.

How Hard to Go After As-a-Service. HfS believes that Procurement Outsourcing will increasingly move away from highly customized often initially “lift and shift” deals or pure sourcing consulting contracts towards a more modular set of technology (and automation) based services. The question is does this make sense as a strategy for all service providers to follow or should some just concentrate on owning more share of the transactional procurement market based on more traditional delivery solutions and let the market truly bifurcate based on client expectations and demands.

© 2015 HfS Research Ltd. Proprietary │Page 23

Q. How Will This Change in the Next Year? (Outsourcing)

Q. How Will This Change in the Next Year? (Shared Services)

-13% -5% -5% -4% -3% -3% -5% -1% -1%

31% 29% 28% 26% 21% 18% 17% 16% 16%

-20%

-10%

0%

10%

20%

30%

40%

Application Development &

Maintenance

Finance and Accounting

IT Infrastructure

Industry-specific Operations

Procurement Human Resources

Customer Service

Supply Chain and Logistics

Marketing Support

-9% -7% -6% -2% -3% -3% -4% -1% -3%

18% 26%

19% 17% 20% 20% 16% 16% 14%

-20%

-10%

0%

10%

20%

30%

Application Development &

Maintenance

Finance and Accounting

IT Infrastructure

Industry-specific Operations

Procurement Human Resources

Customer Service

Supply Chain and Logistics

Marketing Support

Strong Uptake of Procurement Continues Unabated in 2015

Decreasing Increasing

Source: 2014 State of Industry Study, May 2014. HfS Research in Conjunction with KPMG (Sample 312 Enterprises)

© 2015 HfS Research Ltd. Proprietary │Page 24

Providers and Third Party Advisors see Middle of the Pack

Growth Rates for Procurement

Aggregating the regions for which you are responsible, at what percentage rate do you expect the following services markets to grow (or shrink) over the next 12 months?

Source: HfS Research in Conjunction with KPMG. Note n=347 Advisers, n=420 Providers

3.7%

3.7%

3.1%

3.9%

4.0%

4.4%

4.7%

5.0%

5.1%

5.0%

5.9%

4.3%

4.5%

4.9%

5.0%

5.7%

5.9%

6.1%

6.4%

6.6%

6.9%

8.4%

0% 2% 4% 6% 8% 10%

Document & Print Operations Outsourcing

Legal Process Outsourcing

Marketing Operations Outsourcing

Contact Center Outsourcing

Human Resources Outsourcing

Procurement & Sourcing Outsourcing

IT Infrastructure Outsourcing

Finance & Accounting Outsourcing

Application Development & Maintenance Outsourcing

Industry-specific Processes (i.e. life sciences/banking)

Analytics & Knowledge Process Outsourcing

Providers Advisers

© 2015 HfS Research Ltd. Proprietary │Page 25

7%

5%

6%

10%

7%

6%

8%

5%

12%

7%

11%

11%

15%

15%

16%

17%

24%

28%

32%

33%

35%

40%

31%

33%

24%

24%

30%

26%

33%

23%

20%

31%

27%

2%

2%

2%

6%

2%

3%

2%

5%

4%

5%

48%

45%

52%

43%

43%

44%

25%

38%

28%

24%

17%

2%

2%

2%

2%

2%

0% 25% 50% 75% 100%

Marketing …

Customer …

Knowledge Process …

Industry-Specific …

Legal Process …

Supply Chain …

Human Resources …

Analytics / Big Data …

Procurement & …

Document & Print …

Finance & …

Will look to start outsourcing for the first time Will increase scope/volume

Will keep scope/volume at current level Will decrease scope/volume

Do not outsource and have no plans Are looking to insource in next 12 months

45% of Enterprises Plan to Start or Increase the Scope of

Outsource Procurement Services so will Growth be Higher?

Are you likely to increase or decrease your outsourcing activity across the following business operations areas in the next 12 months?

Source: HfS Research in Conjunction with KPMG. Note n=312

© 2015 HfS Research Ltd. Proprietary │Page 26

Procurement Remains One of the Least Offshored of Processes

In your estimation, how much offshore/nearshore support do you currently use to service your business and IT operations, whether with an outsourcing provider on within your own shared services?

Source: HfS Research in Conjunction with KPMG. Note n=312

34%

40%

44%

52%

58%

62%

62%

68%

70%

22%

31%

30%

25%

23%

24%

26%

18%

20%

14%

10%

14%

11%

3%

8%

4%

6%

3%

22%

8%

9%

9%

10%

4%

3%

4%

5%

7%

8%

3%

3%

5%

3%

3%

2%

2%

2%

3%

1%

0% 25% 50% 75% 100%

Application Development & …

IT Infrastructure

Finance and Accounting

Industry-specific Operations

Customer Service

Procurement

Human Resources

Supply Chain and Logistics

Marketing Support

No Offshore 1-24% 25%-49% 50%-74% 75%-99% 100%

© 2015 HfS Research Ltd. Proprietary │Page 27

Although Procurement Offshoring is Increasing Over Time How will this change in the next year? (Outsourcing)

Source: HfS Research in Conjunction with KPMG. Note n=312

1%

1%

5%

4%

3%

5%

5%

6%

12%

83%

83%

79%

79%

77%

71%

68%

64%

56%

16%

16%

17%

17%

21%

24%

27%

29%

32%

0% 25% 50% 75% 100%

Marketing Support

Supply Chain and Logistics

Customer Service

Human Resources

Procurement

Industry-specific Operations

Finance and Accounting

IT Infrastructure

Application Development & Maintenance

Decreasing Staying as is Increasing

© 2015 HfS Research Ltd. Proprietary │Page 28

Cloud/BPaaS is Becoming More Important in Procurement

In what areas are you considering cloud / as-a-service options to augment / replace traditional outsourcing?

2%

4%

6%

9%

11%

14%

15%

20%

22%

16%

13%

6%

9%

19%

12%

17%

8%

8%

37%

23%

29%

24%

28%

37%

37%

35%

39%

45%

60%

58%

59%

42%

37%

31%

37%

31%

Marketing

Legal

Supply Chain and Logistics

Sales

Procurement

Customer Service/Support

Finance and Accounting

Business-specific Operations

Human Resources

We have at least one cloud based service for this function

Starting to evaluate / test solutions

We are interested but yet to find anything suitable

Nothing in place & see no value

Source: HfS Research State of Industry Study 2014, conducted in conjunction with KPMG (Sample 312 Enterprises)

© 2015 HfS Research Ltd. Proprietary │Page 29

The Xchanging, Accenture, IBM, Capgemini, Genpact, GEP &

Infosys Dominate Two-Thirds of the Multi-Process PO Market

Service Provider Estimated

2014 % Total Share ACV

Estimated 2014 ACV

($M)

Accenture 26.1% 510

Xchanging 15.1% 250

IBM 12.0% 235

Capgemini 10.0% 195

Infosys 6.1% 120

GEP 5.6% 110

Genpact 4.9% 95

WNS 3.6% 70

Wipro 2.8% 55

Proxima 2.6% 50

TCS 2.5% 48

Optimum Procurement 1.8% 36

HCL 1.6% 30

DSSI 1.3% 25

IGATE 1.2% 24

Tech Mahindra 1.1% 22

Denali 1.0% 20

Aegis 0.06% 12

Total 100% $1,952

Source: HfS Research, 2015; n = 910 live multi-process PO Contracts; based on live PO contracts over $0.5M in TCV with a min. of two core PO processes bundled

Accenture 26%

Xchanging 15%

IBM 12%

Capgemini 10%

Infosys 6%

GEP 6%

Genpact 5%

WNS 4%

Wipro 3%

Proxima 3%

TCS 2%

Optimum 2%

HCL 2%

DSSI LLC 1%

IGATE 1%

TechM 1%

Denali 1%

Aegis 1%

© 2015 HfS Research Ltd. Proprietary │Page 30

0%

5%

10%

15%

20%

25%

30%

35%

The Market Leaders’ Success is Based on Large Deals

Percentage Share per Size of Deal Percent of Deal Count (Including Other)

Enterprise-level engagements

Mid-mkt-level engagements

% Market Share >25M TCV % Market Share <25M TCV

Source: HfS Research, 2015; n = 910 live multi-process PO Contracts; based on live PO contracts over $0.5M in TCV with a min. of two core PO processes bundled

© 2015 HfS Research Ltd. Proprietary │Page 31

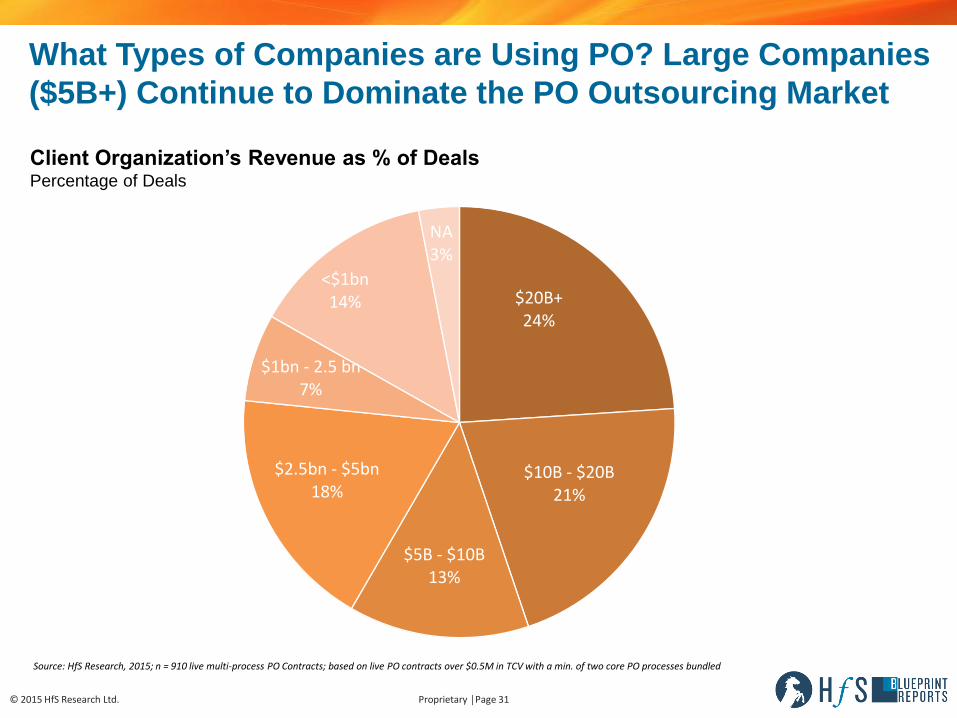

What Types of Companies are Using PO? Large Companies

($5B+) Continue to Dominate the PO Outsourcing Market

Client Organization’s Revenue as % of Deals Percentage of Deals

$20B+ 24%

$10B - $20B 21%

$5B - $10B 13%

$2.5bn - $5bn 18%

$1bn - 2.5 bn 7%

<$1bn 14%

NA 3%

Source: HfS Research, 2015; n = 910 live multi-process PO Contracts; based on live PO contracts over $0.5M in TCV with a min. of two core PO processes bundled

© 2015 HfS Research Ltd. Proprietary │Page 32

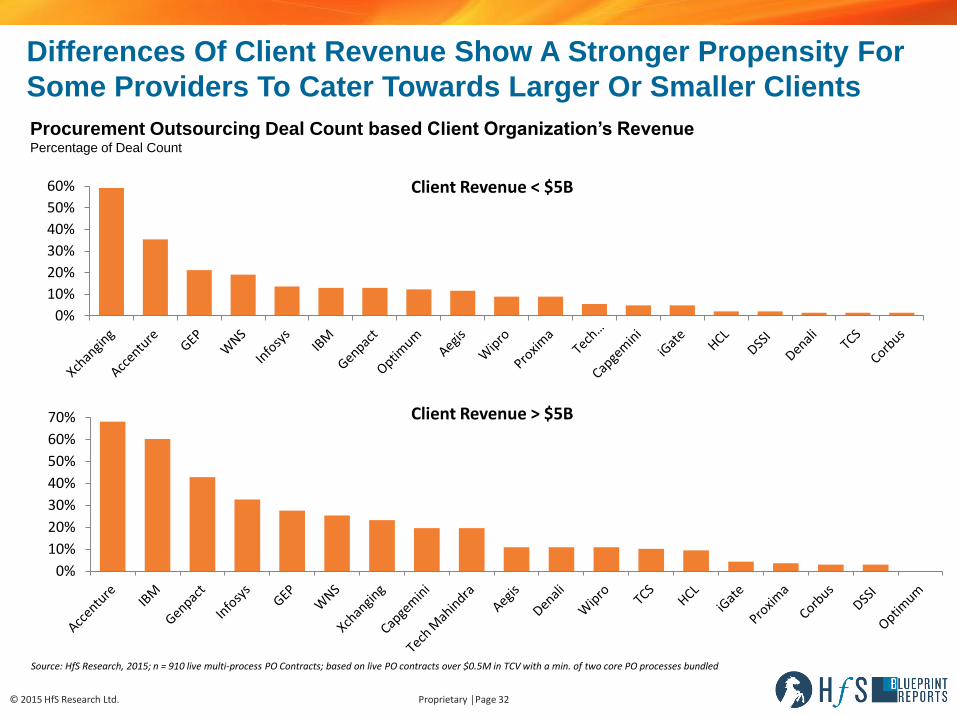

Differences Of Client Revenue Show A Stronger Propensity For

Some Providers To Cater Towards Larger Or Smaller Clients

Source: HfS Research, 2015; n = 910 live multi-process PO Contracts; based on live PO contracts over $0.5M in TCV with a min. of two core PO processes bundled

Procurement Outsourcing Deal Count based Client Organization’s Revenue Percentage of Deal Count

Client Revenue < $5B

Client Revenue > $5B

0%

10%

20%

30%

40%

50%

60%

0%

10%

20%

30%

40%

50%

60%

70%

© 2015 HfS Research Ltd. Proprietary │Page 33

20%

12% 12% 11% 11%

8% 7%

4% 3% 3% 3% 2% 2% 1%

Manufacturing, Retail & CPG, and Telecom & High Tech

Companies Continue to Dominate Deal Saturation in PAAS

Behind the Numbers

• Adoption mix outside of the top five industries shows generally low saturation levels.

Average % of PO Work Being Serviced by Industry Percentage of Deal Count

Source: HfS Research, 2015; n = 910 live multi-process PO Contracts; based on live PO contracts over $0.5M in TCV with a min. of two core PO processes bundled

© 2015 HfS Research Ltd. Proprietary │Page 34

23%

21%

18%

14%

12%

8%

4%

1%

North America

India Continental Europe

Latin America ANZ/APAC UK China Japan

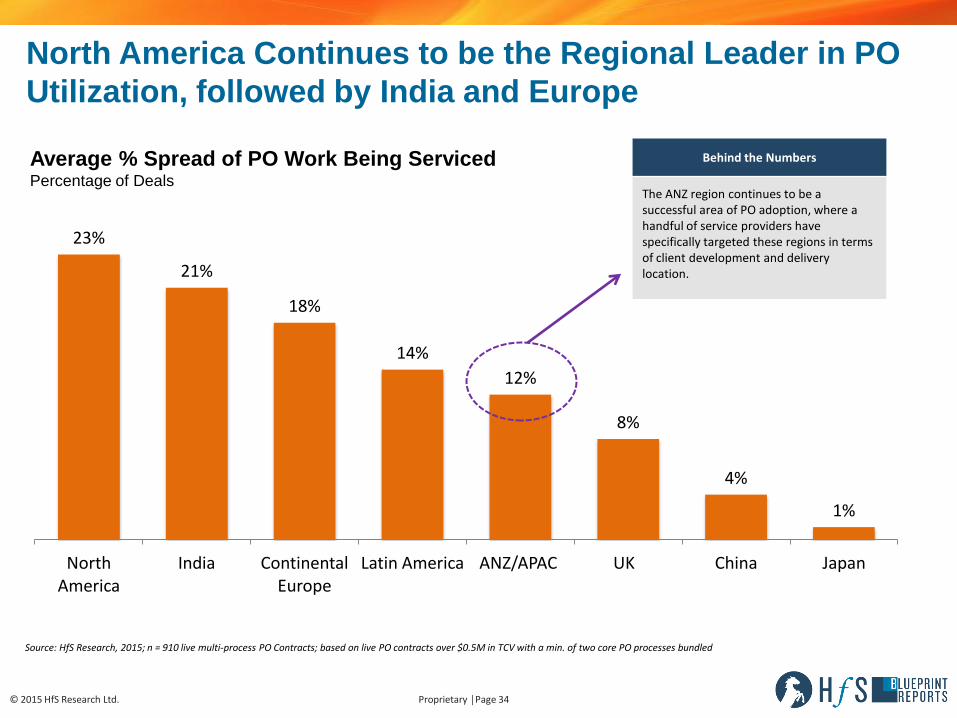

North America Continues to be the Regional Leader in PO

Utilization, followed by India and Europe

Average % Spread of PO Work Being Serviced Percentage of Deals

Behind the Numbers

The ANZ region continues to be a successful area of PO adoption, where a handful of service providers have specifically targeted these regions in terms of client development and delivery location.

Source: HfS Research, 2015; n = 910 live multi-process PO Contracts; based on live PO contracts over $0.5M in TCV with a min. of two core PO processes bundled

© 2015 HfS Research Ltd. Proprietary │Page 35

17%

35%

28%

15%

3% 2%

< 2 Years 2-3 Years 4-5 Years 6-7 Years 8-10 Years > 10 Years

Procurement Outsourcing Deal Length Consistently

Trends Towards 5 Years or Less

Length of PO Contract Term Number of Contracts

Behind the Numbers

Buyers prefer to remain flexible in their consistent choice for short-term deals. This is particularly true in non-multi-tower deals.

Source: HfS Research, 2015; n = 910 live multi-process PO Contracts; based on live PO contracts over $0.5M in TCV with a min. of two core PO processes bundled

© 2015 HfS Research Ltd. Proprietary │Page 36

61%

33%

42%

57%

49% 45%

36% 41%

33%

11%

38%

29% 24%

46%

33% 28% 28%

22%

Procurement As-a-Service Engagements Show a Mix of

Both Transaction and Strategic PO Process – Contract

Management Still Lags Behind

Strategic Sourcing Transactional Procurement Contract Management

Source: HfS Research, 2015; n = 910 live multi-process PO Contracts; based on live PO contracts over $0.5M in TCV with a min. of two core PO processes bundled

Supplier Management

© 2015 HfS Research Ltd. Proprietary │Page 37

FTE Models Remains Prevalent Choice, while Gainsharing is an

Attractive Option, Particularly Based on Savings Outcomes

Fee Structure Percentage of Contracts

Source: HfS Research, 2015; n = 910 live multi-process PO Contracts; based on live PO contracts over $0.5M in TCV with a min. of two core PO processes bundled

56%

33% 36%

14%

31%

Gain-sharing/Outcome based

FTE Based Transactional (Other than cost per PO or

Invoice)

Fixed Fee with Volume

Subscription based

(e.g. 1 cents per user)

© 2015 HfS Research Ltd. Proprietary │Page 38

35%

24%

61%

Buyer Owned Service Provider Owned Combination

Technology Platforms and Tools Play an Important Role

as the Buyers of Services Increasingly Move Towards the

Use of Combination of Tools in as a Service Economy

Core Technology Used Owned By Buyer/Supplier/Combination Percentage of Contracts

Source: HfS Research, 2015; n = 910 live multi-process PO Contracts; based on live PO contracts over $0.5M in TCV with a min. of two core PO processes bundled

© 2015 HfS Research Ltd. Proprietary │Page 39

50%

16%

12% 10%

5% 3% 3%

1% 1% 0%

North America

Continental Europe

UK ANZ India Latin America

Other APAC China Japan Africa

Procurement As-a-Service Market Penetration Continues

to be Dominated by the North American Market

Region Contract Signed Number of Contracts

Source: HfS Research, 2015; n = 910 live multi-process PO Contracts; based on live PO contracts over $0.5M in TCV with a min. of two core PO processes bundled

Service Provider Grid

© 2015 HfS Research Ltd. Proprietary │Page 41

To distinguish providers that have gone above and beyond within a particular line of delivery, HfS awards these providers a “Winner’s Circle” or “High Performer” designation. The below provides a brief description of the general characteristics of each designation:

Winner’s Circle and High Performers Methodology

WINNER'S CIRCLE:

Organizations that demonstrate excellence in both execution and innovation.

• From an execution perspective, providers have developed strong relationships with clients, execute services beyond the scope of hitting green lights, and are highly flexible when meeting clients’ needs.

• From an innovation perspective, providers have a strong vision, concrete plans to invest in future capabilities, a healthy cross-section of vertical capabilities, and have illustrated a strong ability to leverage external drivers to increase value for their clients.

HIGH PERFORMERS:

Organizations that demonstrate strong capabilities in both execution and innovation but are lacking in an innovative vision or execution against their vision.

• From an execution perspective, providers execute some of the following areas with excellence, but not all areas: high performers have developed worthwhile relationships with clients, execute their services and hit all of the green lights, and are very flexible when meeting clients’ needs.

• From an innovation perspective, providers typically execute some of the following areas with excellence, but not all areas: have a vision and demonstrated plans to invest in future capabilities, have experience delivering services over multiple vertical capabilities, and have illustrated a good ability to leverage external drivers to increase value for their clients.

© 2015 HfS Research Ltd. Proprietary │Page 42

HfS Blueprint 2015: Procurement As-a-Service IN

NO

VA

TIO

N

EXECUTION

High Performers

Aegis

OneSource Virtual

KPMG

Winner’s Circle

WNS

TCS

Wipro HCL

Tech Mahindra

Accenture GEP Xchanging

Capgemini

IBM

Infosys

Genpact Optimum Procurement

Proxima Denali

DSSI

IGATE

© 2015 HfS Research Ltd. Proprietary │Page 43

Major Service Provider Dynamics – Highlights

EXECUTION

• Geographic Footprint And Scale. All of the Winner’s Circle service providers (Accenture, Capgemini, GEP, IBM, Infosys and Xchanging) have built up a global presence in procurement delivery with a particular concentration on bringing sourcing expertise direct to the client site.

• Integration of Acquisitions. Since the last Procurement Blueprint in 2013 a significant effort has been completed by Accenture, Infosys and Xchanging to integrate key procurement acquisitions and bring their leaders to the head of the offerings.

• Strategic Sourcing and Category Management. Across the board we saw an increased investment in sourcing and category management within procurement outsourcing operations since 2013. In the past this was often more of a consulting delivery model with limited integration with transactional procurement but that older model is giving way to a more integrated and iterative capability.

• Process Automation in Procurement. Service providers are actively trialing process automation within procurement both in transactional procurement and in support of the other processes as well. HfS saw particular emphasis on this from IBM, Infosys and Genpact but many other service providers are close behind.

• Contract Management. We were especially impressed by the approach that Accenture is taking to enhancing their Contract Management offering with greater involvement of and access to included legal support for procurement clients. We expect this to be a areas of continued innovation and investment in 2015-16.

INNOVATION

• Integration of Procurement Specific Technology. All of the Winner’s Circle (and High Performer) service providers have made significant efforts since 2013 in expanding their technology deployment and management skills for procurement. With the much greater adoption of SaaS platforms for Procurement, leading service providers have realized that they need to have much greater in-house technology skills than in the past when procurement platforms were generally run on-premise by clients themselves.

• Creating a Vision for Procurement As-a-Service. HfS noted through our research, briefings and client discussions that a great many of the service providers have refreshed their offering strategies and solution models for procurement so that they include many more on-demand and As-a-Service components.

• Introducing Cognitive Computing Into Procurement. IBM Watson is being introduced in support of procurement process delivery and while its still early days and we are looking for more detailed use cases and client case studies, HfS believes that cognitive computing could be an important innovation for the support of procurement.

Service Provider Profile

© 2015 HfS Research Ltd. Proprietary │Page 45

Accenture Acquiring Procurian has put Accenture at the leading edge of

procurement outsourcing delivery with a wide breadth of capabilities

Client Industry Verticals Key Clients Global Operations Centers Technology

• Communications, Media, and Technology

• Financial Services • Health and Public Sector • Products • Resources • Public Services

120+ Procurement Outsourcing clients with US$ 95 billion in spend management including:

Headcount: 3,300+ professionals

• USA: King of Prussia, PA, Pittsburgh, PA; San Antonio, TX

• Costa Rica: San Jose • Brazil: Belo Hoizonte; Sao Paulo • Argentina: Buenos Aires • UK: London • Czech: Prague • Slovakia: Bratislava • Romania: Bucharest • India: Bangalore; Chennai; Delhi; Hyderabad • China: Shanghai; Shenzhen; Dalian • South Africa: Johannesburg

Accenture Proprietary Solutions include: • Radix • SavingsLink • The Buying Center Operations Suite (BCOS) • MySupplier and Buyer Portals • Accenture Insights – Category-specific benchmarking,

analysis, and cost modeling applications • Accenture Operations Navigator Key Third Party Solutions include: • SAP & Oracle • Tableau • Ariba

• Global Automotive Manufacturer

• Global Mining Operator

• Leading White Goods Manufacturer

• Major Cosmetics Retailer

• Global Automotive Parts Supplier

• Leading European Universal Bank

• Wireless Device Manufacturer

• Capital Markets Major • Global Tire and Rubber

Manufacturer

Strengths Challenges

• Successful Procurian Integration. Accenture has successfully integrated their legacy Procurement Outsourcing, Procurement Consulting, Ariba Services Acquisition and Procurian over the last several years and put key Procurian executives in charge to transform the business.

• Excellent Account Management. Clients were quick to highlight their delight with their account management leads (both Accenture and Procurian heritage) who made it easier to do business with what can at times seem like a giant firm.

• Strategic Sourcing And Category Management. Accenture leads the market in the breadth, depth and sophistication of its strategic sourcing and category management capabilities with innovative specializations in fields such as energy sourcing. Accenture has also brought on ex CMOs, CPOs and domain experts to lead categories across their global delivery network.

• Contract Management. Accenture is being quite innovative in the way that they have aligned legal and contract support resources to procurement outsourcing delivery teams. This approach is helping reduce sourcing cycle times for clients resulting in more rapid compliance to approved sourcing practices thereby reducing rogue spend.

• As-a-Service Capabilities. Accenture is advocating an As-a-Service approach to Procurement Outsourcing that allows clients to select the skills and technology needed to more effectively integrate into their retaining procurement functions than has traditionally been the case.

• Transformational Messaging Not For All. Accenture offers a wide set of Procurement offerings with a strong tilt towards transformational business outcomes. For some current clients and others who have chosen competitors, these transformational messages miss the mark and are perceived as being complicated to contract for and costly to implement. Even today, there are segments of buyers who just want simpler solutions in procurement outsourcing.

• Retaining Sourcing Staff. Accenture sourcing and category management staff are being targeted by other service providers who are looking to build up their capabilities in these high demand skills.

• Maintaining The Community. Several clients of a smaller size felt that while they heard about many programs to create communities of clients and share best practices, they weren’t able to take advantage of them and felt that perhaps they were really targeted at Accenture’s largest clients. We hope that the forthcoming release of “spend trends”, a collaborative site with premium content will be a significant development for clients of all sizes who are looking for greater community and collaboration.

Blueprint Leading Highlights

Execution • Account Management • Strategic Sourcing • Transactional Procurement • Contract Management • Geographic Footprint and Scale

Innovation • Integration of As-a-Service

Capabilities • Delivering Value Beyond Cost • Vision For The Evolution of

Procurement Outsourcing • Integration of Technology

Winner’s Circle

Strategic Sourcing

Transactional Procurement

Supplier Management

Contract Management

Technology Management

Market-Wrap and

Recommendations

© 2015 HfS Research Ltd. Accenture Excerpt 20150050 Proprietary │Page 47

Where Next For Procurement As-a-Service

All of the current service providers remaining in this market and further investing in procurement outsourcing capabilities and technologies

Some of the recent partnerships especially for sourcing and category management not lasting the test of time and leading to increased efforts to grow organic capabilities

A continued struggle to attract and retain sourcing and category management experts

Direct category spend management will come back and forth in vogue largely depending on which verticals service providers target for new logos and how much success they have in retaining the experts necessary to deliver in these difficult categories

The greater use of automation solutions to replace human agent involvement in procurement processing as well as in sourcing and category management activities

Further commercial adoption of As-a-Service solution and delivery models

We see the following as the major trends that will foster the future evolution of Procurement As-a-Service over the next 2-3 years:

© 2015 HfS Research Ltd. Accenture Excerpt 20150050 Proprietary │Page 48

HfS Expects to See Even Greater Adoption of the Ideals of

As-a-Service by Procurement Service Providers by 2017

IDEAL AS-A-SERVICE IDEAL

DEFINITION NON EXISTENT INITIAL EXPANSIVE EXTENSIVE ALL PERVASIVE

Design Thinking Generating creative solutions by understanding the business context

2013 2015 2017

Business Cloud “Plug and Play” business services 2013 2015 2017

Intelligent Automation

Blending of automation, analytics and talent 2013 2015 2017

Proactive Intelligence

Operations focused on interpreting data, seeding new ideas

2013 2015 2017

Intelligent Data Real-time applied analytics models, techniques, and insights from big data

2013 2015

2017

Write Off Legacy Use of platform-based services makes many tech investments redundant

2013 2015 2017

Brokers of Capability

Governance staff manage towards business-driven outcomes

2013 2015

2017

Intelligent Engagement

Pricing and relationships based on expertise, outcomes and subscriptions

2013 2015

2017

© 2015 HfS Research Ltd. Accenture Excerpt 20150050 Proprietary │Page 49

2015-16 Recommendations: Enterprise Buyers

Move To As-a-Service Offering Design and Execution. At HfS we are strong believers in the rapid move of BPO away from legacy “lift and shift” models towards an As-a-Service solution design and delivery world. This is especially true for Procurement which has always had some embodiment of the 8 Ideals of As-a-Service in how service providers have sold and delivered the offering. So as an enterprise buyer you should be pushing your service provider(s) to move to this new model and offer you a broader set of choices for what solutions you adopt and how they interact with your own retained organization. Don’t settle for a long term fixed model of solution delivery for procurement but push service providers to be modular and adaptable so that their future services better align to your future needs.

Move Categories In And Out Of Scope. Category expertise remains a fluid capability in many areas so if your service provider increases their capabilities move quickly to exploit that new breadth and if they seem to be flailing then also move quickly to shift that category elsewhere or bring it back into your own organization. Procurement scope definitions shouldn’t last 3 years anymore without change let alone 5 to 7 years.

Increase The Trust. Push your service provider to be more collaborative, more visionary, more inclusive and sharing with you and in turn provide that same approach back to them. The achievement of desired business outcomes via procurement outsourcing is far from guaranteed and making that transition from identified to realized savings and benefits comes easier in a close partnership than in a closed-off zero-sum mindset relationship so check that you are approaching your service provider in a manner that facilitates long term success as well and ask it always of them.

© 2015 HfS Research Ltd. Accenture Excerpt 20150050 Proprietary │Page 50

2015-16 Recommendations: Service Providers

Develop Expertise In Niche Categories. We recommended this back in 2013 and it remains every bit as valid today. Procurement outsourcing success (both in new logo wins and client value delivery) is won down in the trenches of helping to source and manage real client spend. The greater your depth and breadth as a service provider and the more you can do to help control spend across the board for your clients the more successful you will be.

Implement Robotic Process Automation In Procurement. Robotic Process Automation (RPA) is certainly the topic of the moment in BPO circles, but outside of invoice/accounts payable processes, its application inside end to end procurement processes still remains limited. HfS believes that RPA is a means to an end for procurement delivery by enabling a decoupling of labor and growth especially in transactional support and that service providers who adopt these technologies extensively will have a leg up for the next few years.

Prepare For The Rise Of Cognitive Computing. It isn’t here yet and may not be at scale for the next several years, but now is the time to start looking a cognitive computing solutions and seeing how they can be integrated into your existing procurement delivery operations. With talent availability remaining a concern for the future, the use of artificial intelligence to augment your specialists should be an area of ongoing investment and innovation.

Move To As-a-Service Offering Design and Execution. At HfS we are strong believers in the rapid move of BPO away from legacy “lift and shift” models towards an As-a-Service solution design and delivery world. This is especially true for Procurement which has always had some embodiment of the 8 Ideals of As-a-Service in how service providers have sold and delivered the offering. That said, there is still significant opportunity to move this further forward and bring a more modular yet end-to-end solution stack for procurement into the enterprise client so that there is a tighter integration between the service provider capabilities and those of the retained organization than we have seen so far.

About the Authors

© 2015 HfS Research Ltd. Proprietary │Page 52

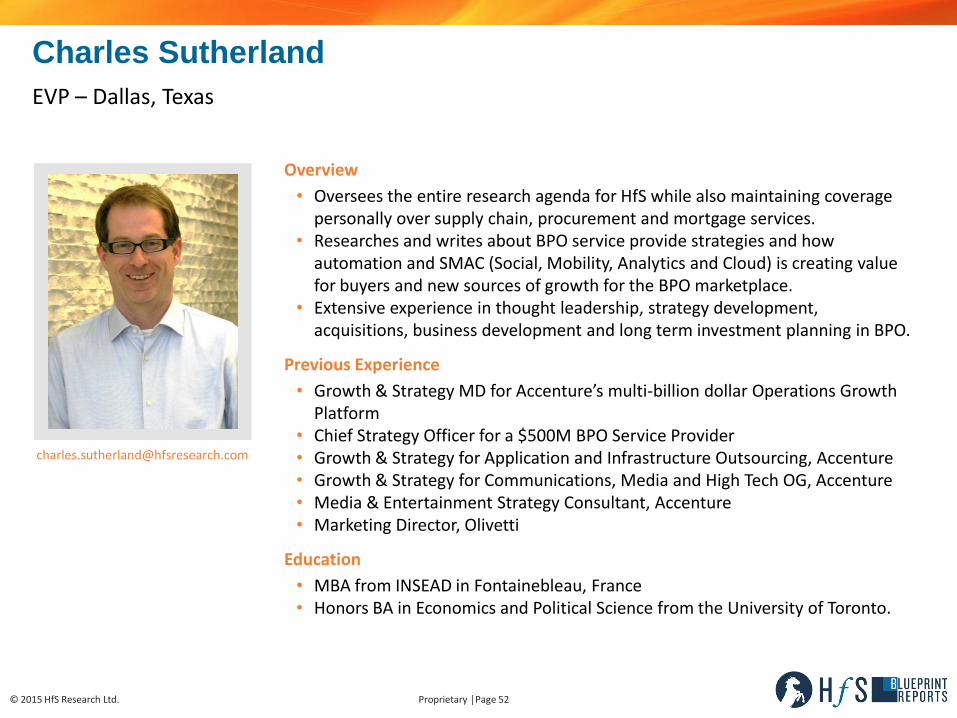

Charles Sutherland

EVP – Dallas, Texas

Overview

• Oversees the entire research agenda for HfS while also maintaining coverage personally over supply chain, procurement and mortgage services.

• Researches and writes about BPO service provide strategies and how automation and SMAC (Social, Mobility, Analytics and Cloud) is creating value for buyers and new sources of growth for the BPO marketplace.

• Extensive experience in thought leadership, strategy development, acquisitions, business development and long term investment planning in BPO.

Previous Experience

• Growth & Strategy MD for Accenture’s multi-billion dollar Operations Growth Platform

• Chief Strategy Officer for a $500M BPO Service Provider • Growth & Strategy for Application and Infrastructure Outsourcing, Accenture • Growth & Strategy for Communications, Media and High Tech OG, Accenture • Media & Entertainment Strategy Consultant, Accenture • Marketing Director, Olivetti

Education

• MBA from INSEAD in Fontainebleau, France • Honors BA in Economics and Political Science from the University of Toronto.

© 2015 HfS Research Ltd. Proprietary │Page 53

Hema Santosh

Principal Analyst – Bangalore, India

Overview

Hema Santosh is a principal analyst at HfS supporting research in finance and accounting and related business services, captives, and global in-house centers.

Over 14 years of research experience supporting leadership on strategic and critical business decisions.

Previous Experience

She has held senior research positions for organizations such as Information Services Group, Accenture, Wipro, and ITFinity Solutions.

Her journey as a research professional has evolved over 14 years by working across facets of MIS, business planning, market forecasting, market analysis, competitive intelligence, and large strategic initiatives for the organizations she has worked with.

Education

• Bachelor’s degree in Commerce from the University of Mumbai • MBA specializing in Marketing from Manipal University • Certificate in full-time “Management Program for Women Entrepreneurs”

from the Indian Institute of Management (IIM), Bangalore

© 2015 HfS Research Ltd. Proprietary │Page 54

About HfS Research

HfS Research is the leading analyst authority and global network for IT and business services, with a specific focus on global business services, digital transformation, and outsourcing. HfS serves the research, governance, and services strategy needs of business operations and IT leaders across finance, supply chain, human resources, marketing, and core industry functions. The firm provides insightful and meaningful analyst coverage of best business practices and innovations that impact successful business outcomes, such as the digital transformation of operations, cloud-based business platforms, services talent development strategies, process automation and outsourcing, mobility, analytics, and social collaboration. HfS applies its acclaimed Blueprint Methodology to evaluate the performance of service and technology in terms of innovating and executing against those business outcomes.

HfS educates and facilitates discussions among the world's largest knowledge community of enterprise services professionals, currently comprising 150,000 subscribers and members. HfS Research facilitates the HfS Sourcing Executive Council, the acclaimed elite group of sourcing practitioners from leading organizations that meets bi-annually to share the future direction of the global services industry and to discuss the future enterprise operations framework. HfS provides sourcing executive council members with the HfS Governance Academy and Certification Program to help its clients improve the governance of their global business services and vendor relationships.

In 2010 and 2011, HfS Research's Founder and CEO, Phil Fersht, was named “Analyst of the Year” by the International Institute of Analyst Relations (IIAR), the premier body of analyst-facing professionals, and achieved the distinctive award of being voted the research analyst industry's Most Innovative Analyst Firm in 2012.

In 2013, HfS was named first in rising influence among leading analyst firms, according to the 2013 Analyst Value Survey, and second out of the 44 leading industry analyst firms in the 2013 Analyst Value Index.

Now in its seventh year of publication, HfS Research’s acclaimed blog “Horses for Sources” is widely recognized as the most widely read and revered destination for unfettered collective insight, research, and open debate about sourcing industry issues and developments. Horses for Sources today receives over a million web visits a year.

To learn more about HfS Research, please email [email protected].