Embed Size (px)

Citation preview

ThyssenKrupp

PresentationThyssenKrupp,CreditSuisseFieldTrip,April1,2009

ThyssenKrupp

PresentationThyssenKrupp,CreditSuisseFieldTrip,April1,2009

Disclaimer�ThyssenKrupp�AG

“Theinformationsetforthandincludedinthispresentationisnotprovidedinconnectionwithanofferorsolicitationforthepurchase

orsaleofasecurityandisintendedforinformationalpurposes only.

Thispresentationcontainsforward-lookingstatementsthataresubjecttorisksanduncertainties. Statementscontainedhereinthat

arenotstatementsofhistoricalfactmaybedeemedtobeforward-lookinginformation.Whenweusewordssuchas“plan,” “believe,”

“expect,” “anticipate,” “intend,” “estimate,” “may” orsimilarexpressions,wearemakingforward-lookingstatements.Youshouldnot

relyonforward-lookingstatementsbecausetheyaresubjecttoanumberofassumptionsconcerningfutureevents,andaresubjectto

anumberofuncertaintiesandotherfactors,manyofwhichareoutsideofourcontrol,thatcouldcauseactualresultstodiffer

materiallyfromthoseindicated.Thesefactorsinclude,butare notlimitedto,thefollowing:

-i.marketrisks:principallyeconomicpriceandvolumedevelopments,

-ii.dependenceonperformanceofmajorcustomersandindustries,

-iii.ourlevelofdebt,managementofinterestrateriskandhedgingagainstcommoditypricerisks;

-iv.costsassociatedwith,andregulationrelatingto,ourpensionliabilitiesandhealthcaremeasures,

-v.environmentalprotectionandremediationofrealestateandassociatedwithrisingstandardsforrealestateenvironmental

protection,

-vi.volatilityofsteelpricesanddependenceontheautomotive industry,

-vii.availabilityofrawmaterials;

-viii.inflation,interestratelevelsandfluctuationsinexchangerates;

-ix.generaleconomic,politicalandbusinessconditionsandexistingandfuturegovernmentalregulation;and

-x.theeffectsofcompetition.

Pleasenotethatwedisclaimanyintentionorobligationtoupdateorreviseanyforward-lookingstatementswhetherasaresultofnew

information,futureeventsorotherwise.”

ThyssenKrupp

PresentationThyssenKrupp,CreditSuisseFieldTrip,April1,2009

FY2007/08:Sales€53,426m• EBT€3,128m• TKVA€1,916m• Employees199,374

ThyssenKrupp�AG

Services

• MaterialsServicesInternational

• MaterialsServicesNorthAmerica

• IndustrialServices

• SpecialProducts

Sales €17.3bnEBT €750mTKVA €508mEmployees 46,486

•PlantTechnology

•MarineSystems

•MechanicalComponents

•AutomotiveSolutions

•Transrapid

• 4regionalbusinessunits

• Escalators/PassengerBoardingBridges

• Accessibility

Sales €12.4bnEBT €741mTKVA €502mEmployees 54,043

Elevator

Sales €4.9bnEBT €434mTKVA €314mEmployees 42,992

StainlessSteel

Sales €14.4bnEBT €1,540mTKVA €1,007mEmployees 41,311

Sales €7.4bnEBT €126mTKVA €-119.mEmployees 12,212

ThyssenKrupp�Group�FY�2007/08

Inter-segmentsalesnotconsolidated

• Corporate

• Steelmaking

• Industry

• Auto

• Processing

• Nirosta

• AcciaiSpecialiTerni

• Mexinox

• ShanghaiKruppStainless

• StainlessInt.

• VDM

Technologies

ThyssenKrupp

PresentationThyssenKrupp,CreditSuisseFieldTrip,April1,2009

� Group�Overview�and�StrategyUlrichMiddelmannViceChairmanoftheExecutiveBoardofThyssenKruppAG

� ThyssenKrupp�SteelPeterUrbanViceChairmanoftheExecutiveBoardofThyssenKruppSteelAG

� ThyssenKrupp Services�and�ThyssenKrupp�ElevatorEdwinEichlerMemberoftheExecutiveBoardofThyssenKruppAG

Agenda

1

ThyssenKrupp

PresentationThyssenKrupp,CreditSuisseFieldTrip,April1,2009

Current�Situation

� Economicsituationinalmostallcountries/industrieshasdeteriorated

inrecentweekswithevengreaterspeedandseverity

� StrategicreorganizationofThyssenKruppinresponseto

changedeconomicenvironment:

• StrongerpositioningofThyssenKruppasan

integratedmaterialsandtechnologygroup

• Leanerandmoreefficientstructure

• Additionalsustainablemid-termcostsavingsofupto€500mp.a.

• ReportinginnewstructureinFY2009/10;

today’stransparencylevelwillbeatleastmaintained

2

ThyssenKrupp

PresentationThyssenKrupp,CreditSuisseFieldTrip,April1,2009

Earnings

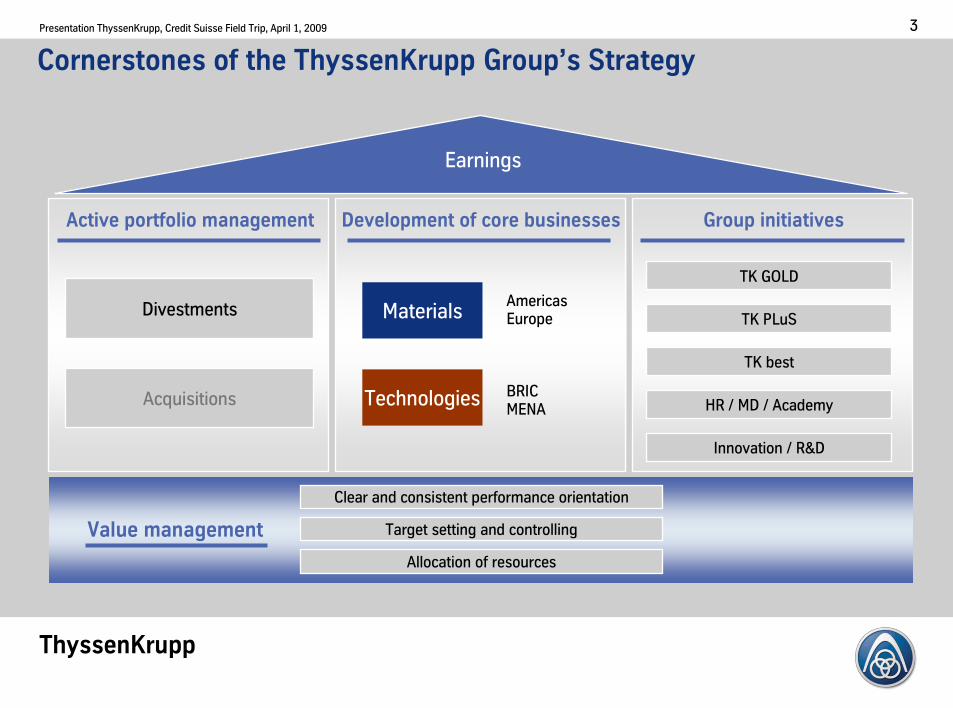

Active�portfolio�management Development�of�core�businesses Group�initiatives

Value�management

Clearandconsistentperformanceorientation

Targetsettingandcontrolling

Allocationofresources

Divestments

Acquisitions

Cornerstones�of�the�ThyssenKrupp�Group’s�Strategy

TKPLuS

TKbest

HR/MD/Academy

Innovation/R&D

TKGOLD

Materials

Technologies

AmericasEurope

BRICMENA

3

ThyssenKrupp

PresentationThyssenKrupp,CreditSuisseFieldTrip,April1,2009

Capture

marketopportunities

andrealize

costefficiencies

� Tight�coordination

� Lean�organization

� Fast�decision-making

� Consistent�value-based�management

� Pro-active�portfolio�optimization

� Selective�growth�&�focused�Group�initiatives

Strongerpositioningas

integratedmaterialsand

technologygroup

The�Integrated�Materials�and�Technology�Group�Concept

ThyssenKruppAG

SchulzCEO

MiddelmannVice CEO

HippeCFO

LabonteLaborDirector

EichlerCEOMaterials

BerlienCEOTechnologies

MaterialsDivision TechnologiesDivision

� Combining�the�Steel,�Stainless�and�Services�segments

� Pooling�and�expansion�of�materials�competence,�

related�services�and�sales�channels

� Consolidation�in�Europe

� Optimized�market�penetration�in�NAFTA

� Initial�focus�on�structural�optimization

� Combining�the�Technologies�and�Elevator�segments

� Pooling�and�expansion�of�technology�competence�

geared�to�infrastructure�and�mega-trends�

� Consolidation�in�Europe

� Development�MENA,�Asia

� Initial�focus�on�structural�optimization

4

ThyssenKrupp

PresentationThyssenKrupp,CreditSuisseFieldTrip,April1,2009

Target�Structure:�Strong�Corporate�Center�+�Strong�Divisions

MaterialsDivision

CEO CFOHead ofBU

1- xLaborDirector

TechnologiesDivision

CEO CFOHead ofBU

1- xLaborDirector

� Steelmaking

� Auto

� Industry

� HHO

� Rasselstein

� Elektroband

� CSA

� Compass

� MS�International

� MS�Americas

� Special�Products

� Industrial�Services

� Nirosta

� AST

� Mexinox

� SKS

� Stainless�International

� VDM

� Uhde� Polysius� Fördertechnik� System�Engineering�1DNK2

� Naval

� Services

� EMEA�1CENE�+�SEAME2

� Americas

� Asia-Pacific

� Rothe�Erde

� Berco

� Forging Group

� Presta Camshafts

� Waupaca

� Presta Steering

� Bilstein &�Automotive�Systems

BU1:SteelEurope

BU2:SteelAmericas

BU4:MaterialsServices

BU3:StainlessGlobal

BU2:PlantTechnology

BU4:MarineSystems

BU1:ElevatorSystems

BU3:Components Business

ThyssenKruppAG

SchulzCEO

MiddelmannVice CEO

HippeCFO

LabonteLaborDirector

EichlerCEOMaterials

BerlienCEOTechnologies

preliminarydraft

5

ThyssenKrupp

PresentationThyssenKrupp,CreditSuisseFieldTrip,April1,2009

Segment�Outlook�Q2�2008/09

� OrderintakeinFebruaryandMarchweakerthanexpected;

BF9shutdownaheadofschedule

� DecreaseinshipmentsandloweraveragerevenuescomparedtoQ1

� Furtherproductioncutsandunderutilization

� Orderintakeandshipmentstoremainatlowlevel

� Continuedproductioncutsandunderutilization

� Furtherwindfalllosses/inventorywrite-downsforeseeable

� Continueddecreaseinpricesandvolumesinmaterialstradingbusiness

� Furtherwindfalllosses/inventorywrite-downsforeseeable

� PlantTechnology,navalshipbuildingandwindenergycomponentsbusinessesstable

� Automotive,constructionequipmentandcivilshipbuildingbusinesses

tobeadragonperformance

� Restructuringchargesforeseeable

� Stablebusinessperformance

� Continuedgoodearningspictureexpected

Technologies

Stainless

Steel

Elevator

Services

6

ThyssenKrupp

PresentationThyssenKrupp,CreditSuisseFieldTrip,April1,2009

Group�Outlook�2008/09

� Providedtheeconomicsituationimprovesinthe2ndhalf,positiveoperatingEBTexpected

� Significanteffectsfrom:

• projectcostsforthenewsteelplants

• restructuringcharges

� SlightlypositiveoperatingEBT– beforeprojectandrestructuringcosts– expected

� Q2tobenegative

� Severecapacityunderutilizationandpricepressure

� Furtherwindfalllosses/inventorywrite-downsforeseeable

H1

FY

7

ThyssenKrupp

PresentationThyssenKrupp,CreditSuisseFieldTrip,April1,2009

Group�Initiatives�2008/09�Measurestostabilizeearningsandcashflow

Group�initiatives

Net�working capital Flexibility of�investmentsPerformance�improvement Portfolio�optimization

� Systematicnetworkingcapitalinitiativewillleadtosignificantdecreaseofworkingcapital

� Screeningofcapexprogram,prioritizationandpostponinginvestmentsinyearsafterFY2008/09

� Detailedprojectorganizationtodeliversignificantperformanceimprovement,e.g.reductionofSG&A

� Planneddivestments- IndustrialServices- SpecialProducts-minoritystake.

Significant�cash�and�cost�savings

Maintain financial flexibility

Target:Reductionby≈ €2.3bn within

fiscalyear2008/09

Target:Costsavingsof>€1bn within

fiscalyear2008/09

Target:Capex of≈ €4.5bn for

fiscalyear2008/09

8

ThyssenKrupp

PresentationThyssenKrupp,CreditSuisseFieldTrip,April1,2009

800

2003/04

2,623

2002/03 2004/05

1,477

Target

4,000-5,000*

mid-/long-term

Group�Targets

3,330

2005/06

Sales� 60�- 65

Sales,�EBT�and�EPS billion€ /million€ /€

EPS5.30-6.60

Tax�rate�33%

2006/07

*excl.majornonrecurringitems

EPS4.59

3,128

1,677

2007/08

9

ThyssenKrupp

PresentationThyssenKrupp,CreditSuisseFieldTrip,April1,2009

� Group�Overview�and�StrategyUlrichMiddelmannViceChairmanoftheExecutiveBoardofThyssenKruppAG

� ThyssenKrupp�SteelPeterUrbanViceChairmanoftheExecutiveBoardofThyssenKruppSteelAG

� ThyssenKrupp Services�and�ThyssenKrupp�ElevatorEdwinEichlerMemberoftheExecutiveBoardofThyssenKruppAG

Agenda

10

ThyssenKrupp

PresentationThyssenKrupp,CreditSuisseFieldTrip,April1,2009

Agenda

� OverviewandTrackRecordThyssenKruppSteel

� StrategicPositioning

� StrategicGuidelinesandImplementation

PeterUrbanViceChairmanoftheExecutiveBoardofThyssenKruppSteelAG

11

ThyssenKrupp

PresentationThyssenKrupp,CreditSuisseFieldTrip,April1,2009

Industry Auto ProcessingSteelmakingCorporate

Sales€14.4bn • EBT€1,540m• ROCE22.1%• TKVA€1,007m• Employees41,311

ThyssenKrupp�Steel�AG

Overview�ThyssenKrupp�Steel�FY�2007/08

Salesnotconsolidated;figuresasofFY2007/08;*ProfitCenterIDS-Industry,Distribution,SteelService.

Sales €7.0bn

Employees 9,199

• Industrydivision

• PCIDS*

• PCHeavyPlate

• CCColor/Construction

• SteelServiceEurope

• Autodivision

• TailoredBlanks

• SteelServiceNorthAmerica

• MetalForming

Sales €5.1bn

Employees 12,992

• Tinplate

• Medium-widestrip

• ElectricalSteel

Sales €2.9bn

Employees 5,325

Sales €1.5bn

Employees 7,653

• Metallurgydivision

• Transportation

Sales n/r

Employees 6,142

• CorporateCenter

• ThyssenKruppCSA

• ThyssenKruppSteelUSA

12

ThyssenKrupp

PresentationThyssenKrupp,CreditSuisseFieldTrip,April1,2009

EBT� million€

462

364

504

471

399

1,738

419

2007/08

534

470

excl.�major��nonrecurring�items

2006/07

1,885

335

2008/09

251

EBT�Track�Record�Steel

243

608

2004/05

2002/03

2003/04

2005/06

1,094

1,406

2006/07

364

428

471

399

as�reported

1,6621,540

2007/08

396

353

389

402

2008/09

13

ThyssenKrupp

PresentationThyssenKrupp,CreditSuisseFieldTrip,April1,2009

Q1�2008/09�Highlights�and�Outlook�Q2�2008/09

-66.

Steel:�Sharp�Drop�in�Orders�Indicates�a�Difficult�Fiscal�Year

Comments�Q1�2008/09 Outlook�Q2�2008/09�Bvs.�Q1C

� Solidearningswithlowershipments

� Sharpdropinorderintakecausedbyheavydestocking andreducedconsumptionacrossmainsteel-usingsectors

� Demandfortinplate,premiumelectricalsteelsandquartoplateholdingupwell

� EvenweakerordersinFebruaryandMarch;BF9shutdownaheadofschedule

� Largelyunchangedcostsforrawmaterialsagainstdecliningshipmentsandaveragerevenues

� Additionalefficiencyprogram“20/10” launchedtargeting>€400m/yearofsustainablecostsavingsbyFY2010/2011

EBTin€m

Q1 Q2 Q3 Q4 Q1

2007/08 2008/09

-66.

353 396 389 402 251

-145. -68.

-84.

419462

534470

335

Q1 Q2 Q3 Q4 Q1

2007/08 2008/09

Orderintakein€m

3,188 3,986 3,765 3,260 2,036

excl.majornonrecurringitems

14

ThyssenKrupp

PresentationThyssenKrupp,CreditSuisseFieldTrip,April1,2009

Averagerevenuesperton,indexed Q12004/2005=100

Shipments:Hot-rolledandcold-rolledproducts 1,000t/monthCrudesteeloutput-TKSincl.shareinHKM. 1,000t/month

251

604

Steel:�Output,�Shipments�and�Revenues�per�Metric�Ton

1,152

Fiscal�year

2004/05 2005/06

1,153

Q1

2007/08

1,239

319 334

757

349

822827

Fiscal�year

2004/05 2005/06

Cold-rolledHot-rolled

1,0761,161 1,171

338 388 337395

767872 913777

Q1

2007/08

1,115

160

133114

125

100116

136129111

133118118

138150

123115134

2007/08

Q1

2005/06

Q2 Q3 Q4Q1

2004/05

Q2 Q3 Q4 Q1

2006/07

Q2 Q3 Q4 Q1

1,129

Q2

1,260

Q2

Q2

Q3

1,196

Q3

1,308

Q3

1,174

Q4

1,104

Q4

Q4

2006/07

1,205

Q1

2008/09

1,064

2006/07 Q1

855

2008/09

2008/09

Q1

15

ThyssenKrupp

PresentationThyssenKrupp,CreditSuisseFieldTrip,April1,2009

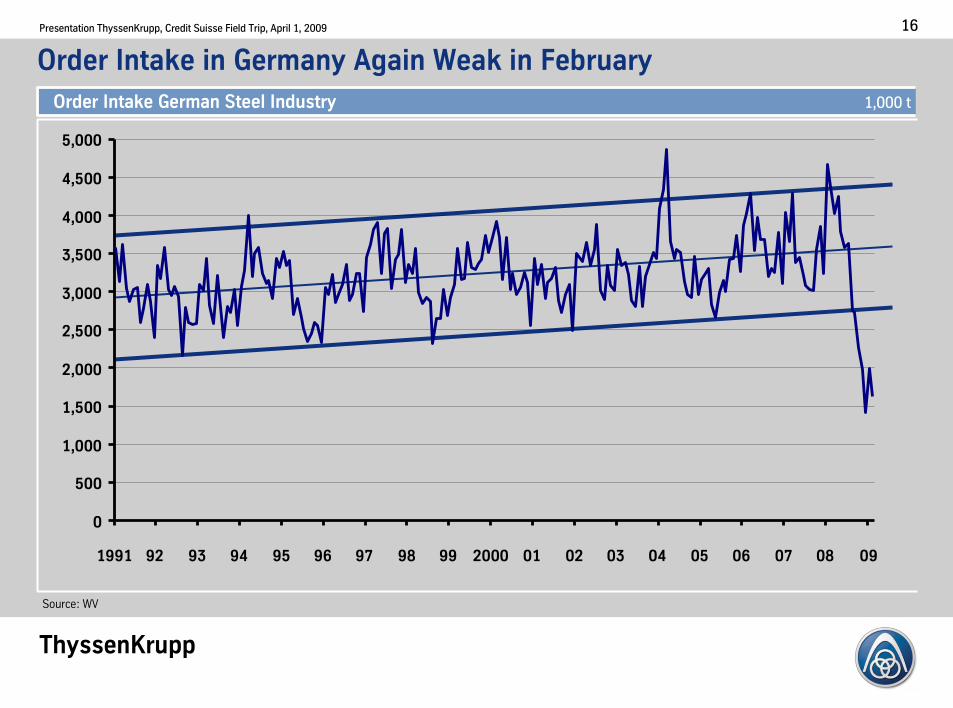

Order�Intake�German�Steel�Industry 1,000t

Order�Intake in�Germany�Again Weak in�February

Source:�WV

0

500

1,000

1,500

2,000

2,500

3,000

3,500

4,000

4,500

5,000

1991 92 93 94 95 96 97 98 99 2000 01 02 03 04 05 06 07 08 09

16

ThyssenKrupp

PresentationThyssenKrupp,CreditSuisseFieldTrip,April1,2009

0.0

0.5

1.0

1.5

2.0

2.5

3.0

J'05

J'06

J'07

J'08

J'09

1

2

3

4

5

6

7

0

1

2

3

4

5

6

7

8

9

10

J'05

J'06

J'07

J'08

J'09

1,5

2,0

2,5

3,0

3,5

4,0

Inventories�and�Months�of�Supply�- Europe

Inventories�and�Months�of�Supply�- USA

InventoriesChina

0

1

2

3

4

5

6

A�07

J�07

O�07

J�08

A�08

J�08

O�08

J�09

A�09

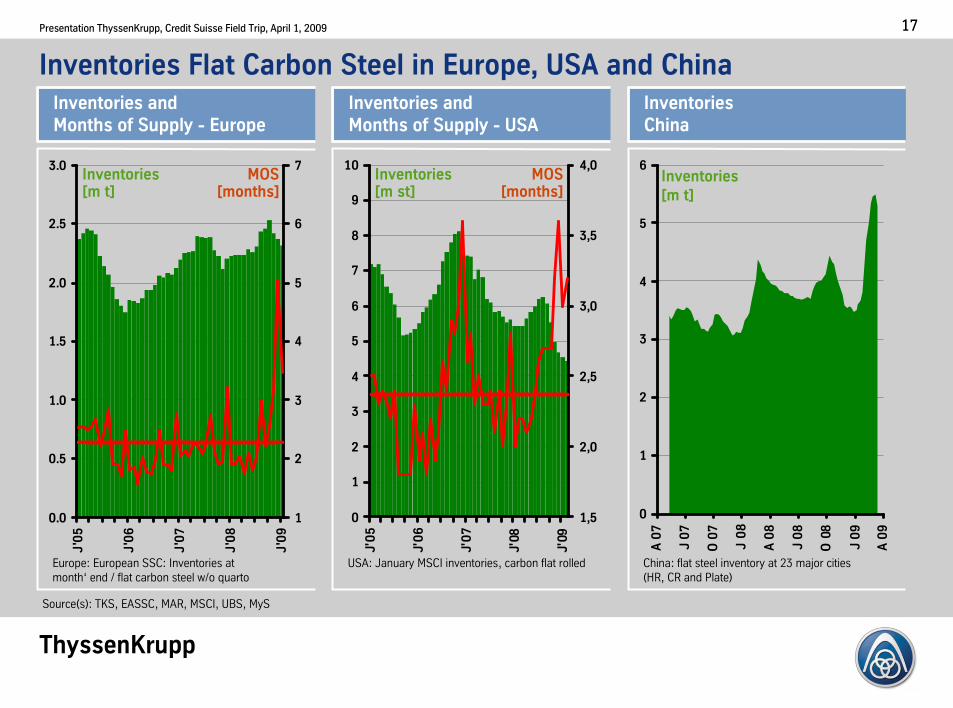

Inventories Flat Carbon Steel�in�Europe,�USA�and�China

Source1s2:�TKS,�EASSC,�MAR,�MSCI,�UBS,�MyS

Europe:�European�SSC:�Inventories at�

month‘ end�/�flat carbon steel w/o�quarto

InventoriesHm�tI

MOSHmonthsI

USA:�January MSCI�inventories,�carbon flat rolled

InventoriesHm�stI

MOSHmonthsI

China:�flat steel�inventory�at�23�major�cities�

1HR,�CR�and�Plate2

InventoriesHm�tI

17

ThyssenKrupp

PresentationThyssenKrupp,CreditSuisseFieldTrip,April1,2009

Agenda

� OverviewandTrackRecordThyssenKruppSteel

� StrategicPositioning

� StrategicGuidelinesandImplementation

PeterUrbanViceChairmanoftheExecutiveBoardofThyssenKruppSteelAG

18

ThyssenKrupp

PresentationThyssenKrupp,CreditSuisseFieldTrip,April1,2009

Current�Focus�of�Business�is�Europe

USA

Mexico

Germany

Spain

France

Brazil

Wuhan

Changchun

Dalian

Europe

Sweden

Poland

North-EastAsia

Turkey

Italy

Nashik

Projects/under�construction

Steel�mill Coating Tailored�blank�production

Steel�service�centerRolling�facilities�1USA�incl.�coating2

Strategic�Alliance

19

ThyssenKrupp

PresentationThyssenKrupp,CreditSuisseFieldTrip,April1,2009

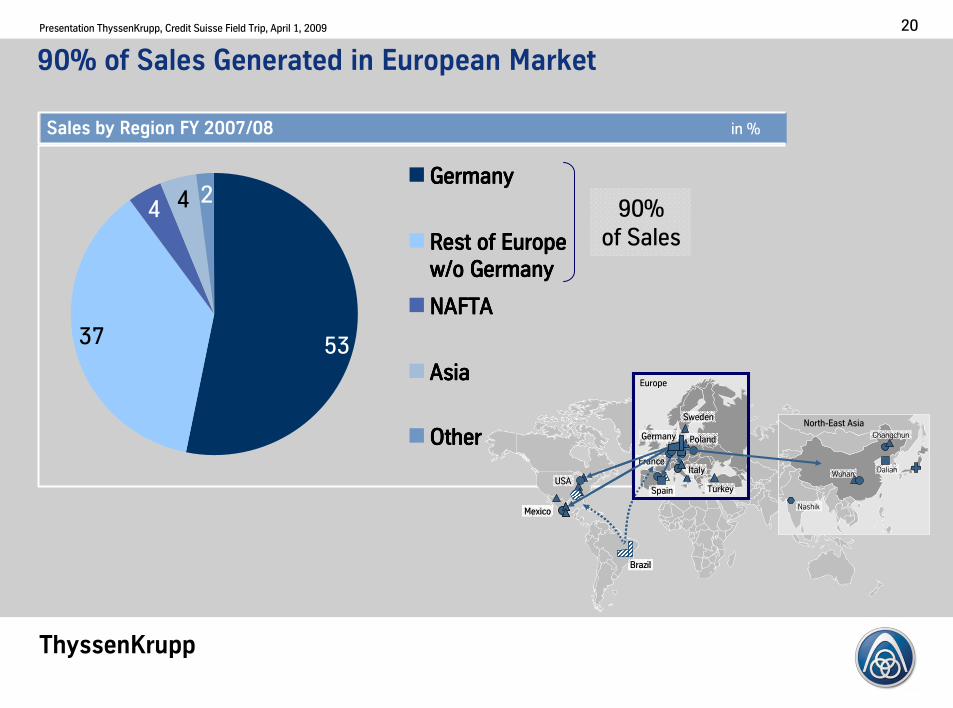

Sales�by�Region�FY�2007/08 in%

90%�of�Sales�Generated�in�European�Market

90%ofSales

5337

4 4 2GermanyGermanyGermanyGermany

RestofEuropeRestofEuropeRestofEuropeRestofEuropew/oGermanyw/oGermanyw/oGermanyw/oGermany

NAFTANAFTANAFTANAFTA

AsiaAsiaAsiaAsia

OtherOtherOtherOther

USA

Mexico

Germany

Spain

France

Brazil

Wuhan

Changchun

Dalian

Europe

Sweden

Poland

North-EastAsia

Turkey

Italy

Nashik

USA

Mexico

Germany

Spain

France

Brazil

Wuhan

Changchun

Dalian

Europe

Sweden

Poland

North-EastAsia

Turkey

Italy

Nashik

20

ThyssenKrupp

PresentationThyssenKrupp,CreditSuisseFieldTrip,April1,2009

Geared�to�the�Premium�Flat�Carbon�Steel�MarketSeparatemarketsegmentsofthesteelindustry

TotalFinished Steel

~1.2bn t

Flatproducts

Longproducts

FlatSteel

~0.5– 0.6bn t

Premiumproducts

Com-modities

PremiumFlat Carbon Steels

~0.2bn t

Superiorproduct andservice quality

Demandingcustomer groups /regionalpractices

Dedicatedtechnologiesandfacilities

Product�and�customer�specific�requirements�and�technologiesprovide�the�basis�for�the�successful�premium�strategy

21

ThyssenKrupp

PresentationThyssenKrupp,CreditSuisseFieldTrip,April1,2009

250

500

750

1,000

250

500

750

1,000

Product�portfolio�FY�2007/08*C in%

*2�sales�of�flat�products�only���

5%4%

13%

12%

15%

23%

2%9%

7%

10%

TailoredBlanks

ConstructionElements

SteelService

CoatedProducts

ElectricalSteel

Tinplate

ColdStrip

HeavyPlate

Medium-wideStrip

HotStrip

Revenue/t €/t

Premium�Product�Portfolio�Generates�Above-Average�Revenues

Source:�Company�reports,�own�estimates

12 data in�part preliminary 22 excl.�Metal�Forming

2001 20032002 2004

majorEuropeancompetitors

20062005 20082007

ThyssenKruppSteel�2.

1.

22

ThyssenKrupp

PresentationThyssenKrupp,CreditSuisseFieldTrip,April1,2009

Sales�by�industry�FY�2007/08 in%

60

80

100

120

140

160

180

200

220

240

260

Price�index Index-Q31997=100.Sales�by�maturity�FY�2007/08 in%

38

4

21

15

9

7

6

Quarterly

Half-year Annual�&>1�year

Spot

649

20

7

Long�Term�Customer�Relations�Reduce�Volatility

OthersAutomotive�industry�Bincl.�suppliersC

ConstructionPackaging

Trade

Mechanical�Engineering

Steel�and�steel-related�processing

All�data�incl.�Q4�2008

Sources:�CRU�and�own�calculations�based�on�CRU,�TKS

CRU

ThyssenKruppSteel

Price�index flat carbon steel ThyssenKrupp�Steel�

Price�index flat carbon steel,�global�market BCRUC

98 00 02 04 06 08

23

ThyssenKrupp

PresentationThyssenKrupp,CreditSuisseFieldTrip,April1,2009

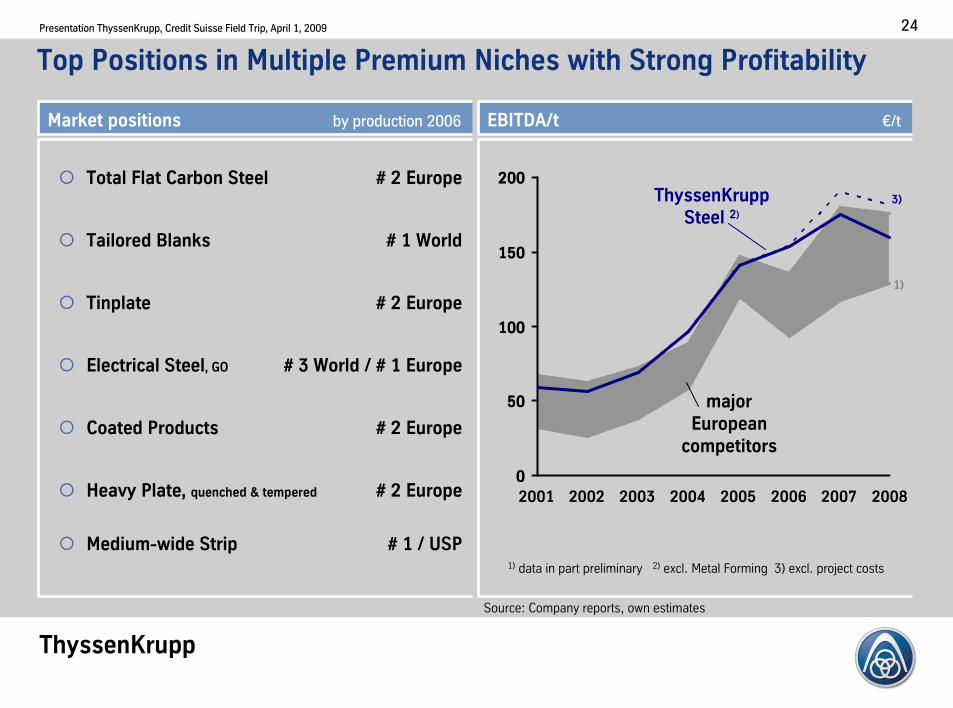

� Total�Flat�Carbon�Steel� #�2�Europe

� Tailored�Blanks� #�1�World

� Tinplate� #�2�Europe

� Electrical�Steel,�GO� #�3�World�/�#�1�Europe

� Coated�Products� #�2�Europe

� Heavy�Plate,�quenched�&�tempered #�2�Europe

� Medium-wide�Strip #�1�/�USP

Market�positions byproduction2006

Top�Positions�in�Multiple�Premium�Niches�with�Strong�Profitability

EBITDA/t €/t

Source:�Company�reports,�own�estimates

0

50

100

150

200

0

50

100

150

200ThyssenKrupp

Steel�2.

majorEuropeancompetitors

12 data in�part preliminary 22 excl.�Metal�Forming 32�excl.�project costs

2001 2006200520032002 20082004

1C

3C

2007

24

ThyssenKrupp

PresentationThyssenKrupp,CreditSuisseFieldTrip,April1,2009

Agenda

� OverviewandTrackRecordThyssenKruppSteel

� StrategicPositioning

� StrategicGuidelinesandImplementation

PeterUrbanViceChairmanoftheExecutiveBoardofThyssenKruppSteelAG

25

ThyssenKrupp

PresentationThyssenKrupp,CreditSuisseFieldTrip,April1,2009

Profitable

growth

Efficiency

improvement

Sustainable value growth

Technology

leadership

Focus�on�attractive marketsfor premium flat steel products

Strategic�Guidelines�ThyssenKrupp�Steel

26

ThyssenKrupp

PresentationThyssenKrupp,CreditSuisseFieldTrip,April1,2009

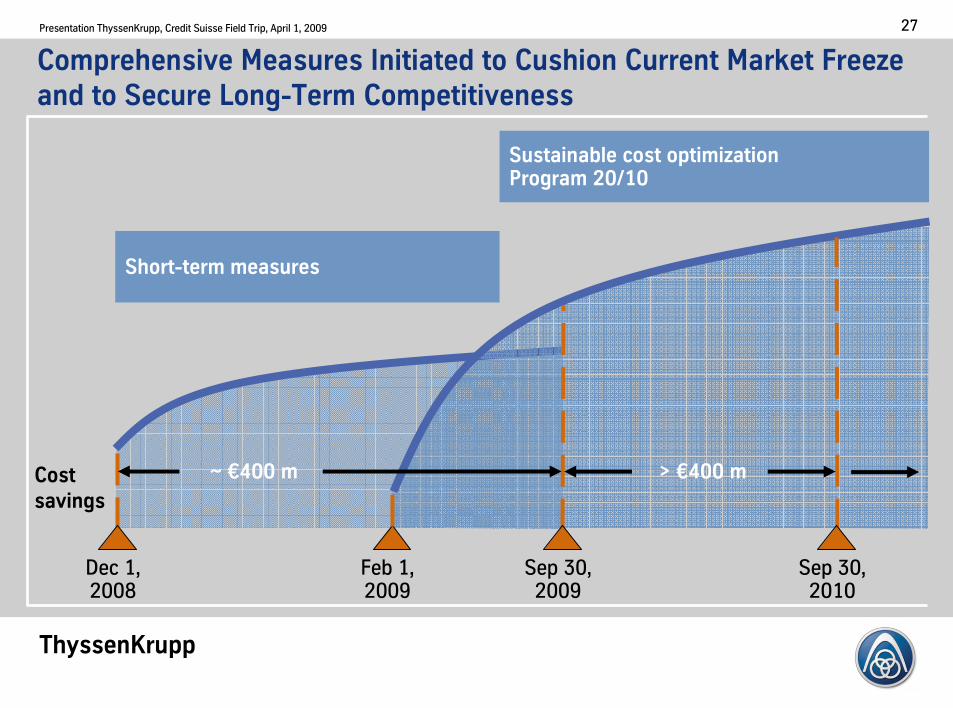

Sustainable�cost�optimizationProgram�20/10

Short-term�measures

Costsavings

Dec 1,2008

>�€400�m

Sep30,2009

Sep30,2010

Feb1,2009

~�€400�m

Comprehensive�Measures�Initiated�to�Cushion�Current�Market�Freeze�and�to�Secure�Long-Term�Competitiveness

27

ThyssenKrupp

PresentationThyssenKrupp,CreditSuisseFieldTrip,April1,2009

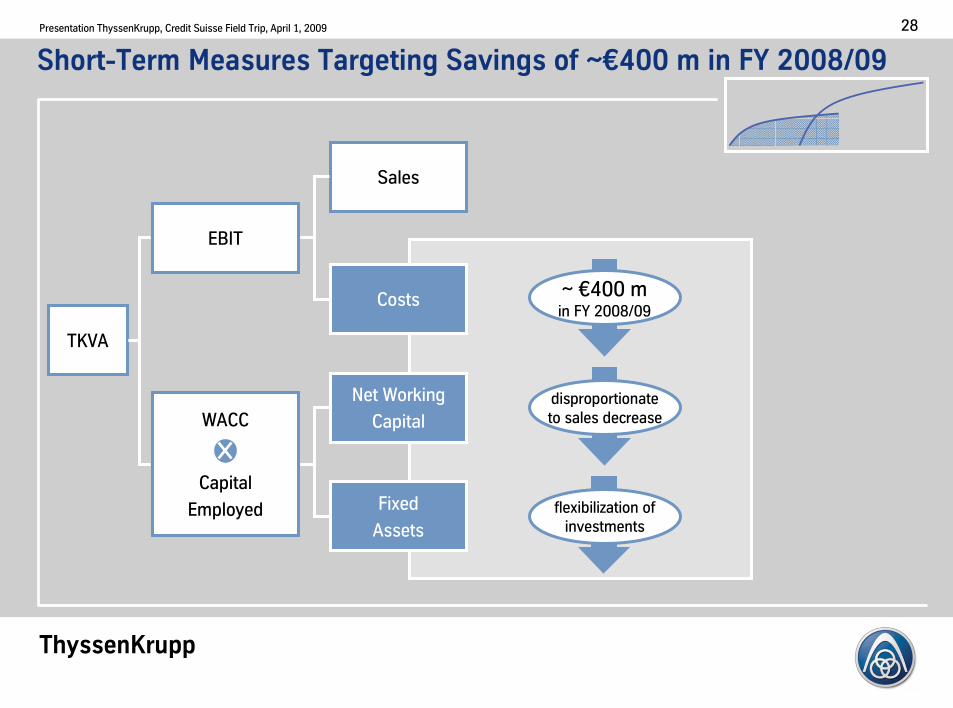

Short-Term�Measures�Targeting�Savings�of�~€400�m�in�FY�2008/09

Sales

Costs

NetWorking

Capital

Fixed

Assets

TKVA

EBIT

WACC

Capital

Employed

~€400minFY2008/09

disproportionatetosalesdecrease

flexibilization ofinvestments

28

ThyssenKrupp

PresentationThyssenKrupp,CreditSuisseFieldTrip,April1,2009

4 Purchasinginitiative2.01technical,�commercial�optimization2

5 Externalservices1increase�productivity,�insourcing,�…2

10�Initiatives�Geared�to�Sustainable�Cost�Savingsof�>�€400�m�per�year�by�FY�2010/11

Sales

Costs

NetWorking

Capital

Fixed

Assets

TKVA

EBIT

WACC

Capital

Employed

Energy

Materials/

Services

Labor

Production

Initiatives

1 Productmixoptimization1products,�customers,�costs2

2 Energycostoptimization1gas,�electricity,�steam,�…2

3 Rawmaterialcostoptimization1mix,�sourcing,�…2

6 Overheadefficiency1incl.�non-personnel�costs2

7 Expansionofsharedservices1functional�and�organizational�scope2

8 Leanproduction1benchmarking,�KPI,… 2

10 NWCinitiative1roll-out,�best�practices,… 2

9 Productionnetwork1configuration,�utilization,… 2

29

ThyssenKrupp

PresentationThyssenKrupp,CreditSuisseFieldTrip,April1,2009

Profitable

growth

Efficiency

improvement

Sustainable value growth

Technology

leadership

Focus�on�attractive marketsfor premium flat steel products

Strategic�Guidelines�ThyssenKrupp�Steel:�Technology�Leadership

30

ThyssenKrupp

PresentationThyssenKrupp,CreditSuisseFieldTrip,April1,2009

Unique�Network�of�R&D�Competence�Centers

WSK:Werkstoff-kompetenz-zentrum

MaterialsDevelopment

SE/AWT:SimultaneousEngineering/

Anwendungstechnik:

Concepts,Semi-finishedPartsandProcessingTechnologies

DOC:DortmunderOberflächenCentrum

SteelSurfaceEngineering

ProcessTechnology

FacilityandProcessTechnologyand

Simulation

Process Products

► Drivepremiumproductandserviceportfolio

31

ThyssenKrupp

PresentationThyssenKrupp,CreditSuisseFieldTrip,April1,2009

World-classmetallurgyenablesbroadportfoliowithpremiumquality

Premium�Product Portfolio�Based on�World-Class�Facilities

Cold-rolled,ultrahigh-strengthsheetinextremelythingauges TAKOpicklingline

&tandemmill

Hochwertige Oberflächen-veredelungen für höchsteQualitätsansprüche undoptimalen Korrosionsschutz

High-qualitycoatingsfordemandingqualityrequirementsandoptimizedcorrosionprotection

Hot-dipgalvanizing/coilcoatingline

Hot-rolled,ultrahigh-strengthsheetinextremelythingauges

Casting-rollingline

32

ThyssenKrupp

PresentationThyssenKrupp,CreditSuisseFieldTrip,April1,2009

► Overallcompetenceinautomobilemarketasabasisforleadershipintechnology

Materialsand

Surfaces

Technologyand

Engineering

� Innovative�steels

� New�materials

� Surface coatings

� Support�in�applications

� Simultaneous Engineering

� Tailored Blanks

� Parts�and�components

� Solutions�for auto bodies

� Chassis�systems

Innovations Leadershipintechnology

� T³ Technique®

� Tailored Blanks

� X-IP�Steels

� BONDAL®

� Zinc Magnesium

� Hot-rolled strip with

cold performance

� NewSteelBody®

Productionand

Service

Technology�LeadershipExample:Strongpartnertotheautomotiveindustry

33

ThyssenKrupp

PresentationThyssenKrupp,CreditSuisseFieldTrip,April1,2009

Tinplate�opens�up�innovation�potential�for�packaging

Can�wall�thicknesses�of�0.07�mm�place�extreme�demands�on�deep�drawing�properties

Hot�atrip with�thicker�gauges�in�sour�gas�quality

supports�economic�exploitation�of�gas�and�oil�resources�under�increasingly�adverse�conditions

Example�Applications�for�Premium�Flat�Carbon�Steels�Made�by�TKS

Water-quenched�heavy�plate�for�high-stress�applications

Mobile�cranes:�Ratio�of�load�capacity�to�operating�weight�increased�to�8�:�1.

Grain-oriented�electrical�steel�for�effective�energy�generation

Up�to�99%�efficiency

34

ThyssenKrupp

PresentationThyssenKrupp,CreditSuisseFieldTrip,April1,2009

Profitable

growth

Efficiency

improvement

Sustainable value growth

Technology

leadership

Focus�on�attractive marketsfor premium flat steel products

Strategic�Guidelines�ThyssenKrupp�Steel:�Profitable�Growth

35

ThyssenKrupp

PresentationThyssenKrupp,CreditSuisseFieldTrip,April1,2009

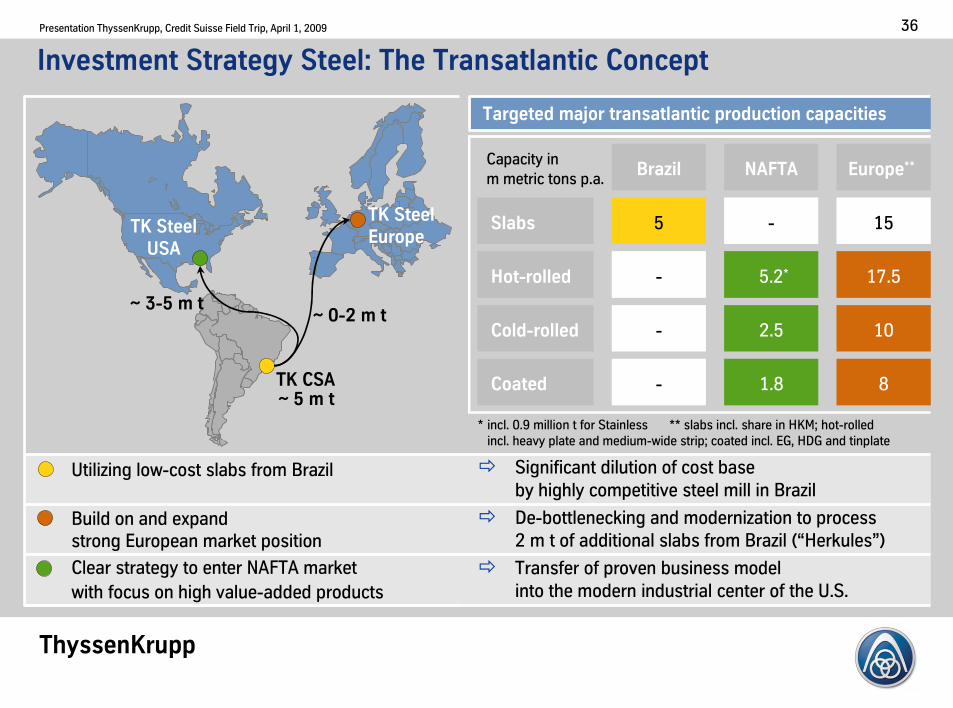

Investment�Strategy�Steel:�The�Transatlantic�Concept

Targeted�major�transatlantic�production�capacities

* incl.0.9milliontforStainless **slabsincl.shareinHKM;hot-rolledincl.heavyplateandmedium-widestrip;coatedincl.EG,HDGandtinplate

Utilizinglow-costslabsfromBrazil

BuildonandexpandstrongEuropeanmarketposition

ClearstrategytoenterNAFTAmarket

withfocusonhighvalue-addedproducts

� SignificantdilutionofcostbasebyhighlycompetitivesteelmillinBrazil

� De-bottleneckingandmodernizationtoprocess2mtofadditionalslabsfromBrazil-“Herkules”.

� TransferofprovenbusinessmodelintothemodernindustrialcenteroftheU.S.

Capacityin

mmetrictonsp.a.

Slabs

Hot-rolled

Cold-rolled

Coated

Brazil

5

-

-

-

NAFTA

-

5.2*

2.5

1.8

Europe**

15

17.5

10

8

TK�Steel�USA

TK�CSA

TK�SteelEurope

~�0-2�m�t~�3-5�m�t

~�5�m�t

36

ThyssenKrupp

PresentationThyssenKrupp,CreditSuisseFieldTrip,April1,2009

PortPowerplant

Outstanding�cost�position

Low-cost�and�high-quality�slabs�as�ideal�basis�for�further�processingin�Europe�and�North�America

Location

• Sepetiba,�Brazil

• Link�to�ore�logistics�from�Minas�GeraisBSouth�ore�mine�system�of�Vale�C

• Rail�connection�and�captive�port

• Ample�space�for�expansion

Blastfurnace

Sinterplant

Cokingplant

Melt-shop

ContinuouscasterPlant

configuration• Capacity:�~�5�million�tons�p.a.

• Capex:� ~�€4.5�billion

SOP • Q4�CY�2009�production�of�first�slab

• High-quality,�secure

ore�supply

• Site�advantages

• Modern�and�efficient�

technologies�and�

processes

• Excellent�logistics

Competitive

advantages

Slab�Facility�in�Brazil�Will�Create�Competitive�AdvantagesStartofproductioninQ4CY2009

37

ThyssenKrupp

PresentationThyssenKrupp,CreditSuisseFieldTrip,April1,2009

Key�facts�ThyssenKrupp�CSA

Full-Fledged�Steel�Mill�Geared�to�Maximum�Efficiency

� 9km² area

� ~22,000peoplecurrentlyworkingonsite

� Stockyardforironore:~900,000t

� Stockyardforcoal/coke:~800,000t

� Cleanaircokingplant:~1.9mtpy cokeandsteam

� Sinterplantcapacity:~5.7mtpy sinter

� Twoblastfurnaces:~5.3mtpy hotmetal

� Steelplant:2x330tconverterstopandbottomblowing

� Port,about3.5kmoff-land,connectedbybridgewithconveyorbeltforcoalintake

� Portintakefor4mtpy coal;shipmentof5mtpy slabs

38

ThyssenKrupp

PresentationThyssenKrupp,CreditSuisseFieldTrip,April1,2009

Aerial photo coke plant

Startup�of�Port�and�Coke�Plant�in�Q3�2009

Coke plant

39

ThyssenKrupp

PresentationThyssenKrupp,CreditSuisseFieldTrip,April1,2009

Melt shop

Blast�Furnace�and�Melt�Shop�Units�Start�Production�End�of�2009

Hot�blast�stoves #1-3

Blast�furnace #1

Sinter�plant

40

ThyssenKrupp

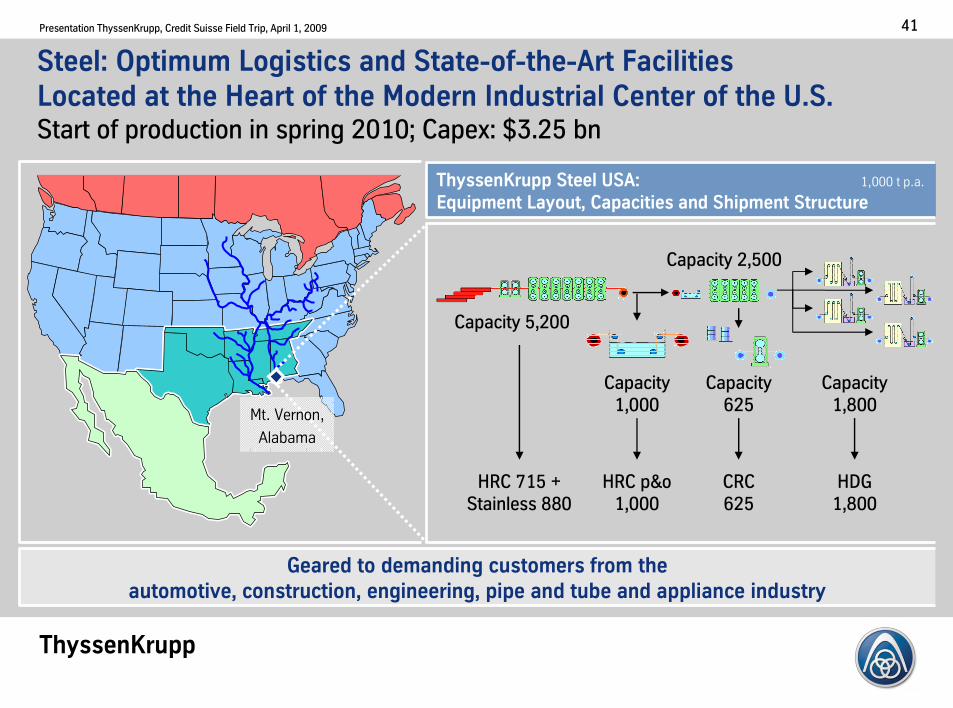

PresentationThyssenKrupp,CreditSuisseFieldTrip,April1,2009

ThyssenKrupp�Steel�USA: 1,000�t�p.a.

Equipment�Layout,�Capacities�and�Shipment�Structure

Steel:�Optimum�Logistics�and�State-of-the-Art�FacilitiesLocated�at�the�Heart�of�the�Modern�Industrial�Center�of�the�U.S.Startofproductioninspring2010;Capex:$3.25bn

Capacity5,200

Capacity1,000

Capacity625

Capacity2,500

HRC715+Stainless880

HRCp&o1,000

CRC625

HDG1,800

Capacity1,800

Mt.�Vernon,

Alabama

Geared�to�demanding�customers�from�theautomotive,�construction,�engineering,�pipe�and�tube�and�appliance�industry

41

ThyssenKrupp

PresentationThyssenKrupp,CreditSuisseFieldTrip,April1,2009

ThyssenKrupp�Steel�USA:�Implementation�Making�Good�Progress

� Capex:$3.25bn

� Ordersplacedforhot- andcold-rollingmill,coatingandinspectionlines,…-~$2.6bn.

� Riverterminal:pilingof1stpier

� HRM:foundationwork,arrivaloffirstequipment

� CRM:steelconstructiontandemmill

� Coatinglines:foundationwork,steelconstruction

� Salesconceptdeveloped

� Recruitingproceedstoschedule

42

ThyssenKrupp

PresentationThyssenKrupp,CreditSuisseFieldTrip,April1,2009

River�Terminal:�Piling Work

43

ThyssenKrupp

PresentationThyssenKrupp,CreditSuisseFieldTrip,April1,2009

Hot-Rolling Mill:�Foundation Work

44

ThyssenKrupp

PresentationThyssenKrupp,CreditSuisseFieldTrip,April1,2009

Cold-Rolling�Mill�and�Coating�LinesCold-rolling�mill:foundation�work

Coating�lines:foundation�work

45

ThyssenKrupp

PresentationThyssenKrupp,CreditSuisseFieldTrip,April1,2009

NAFTA�Sales�and�Marketing�Approach�Well�Advanced

� Salesorganizationestablished

� Potentialcustomersforramp-upphaseandsteadystateidentifiedandapproached

� Highinterestinspecifyingjointbusinessperspectives

� Volumepotentialsbycustomerforramp-upphasedefined

� PlannedshipmentvolumeinFY2009/10:~500,000t

� Continuousramp-upandsmoothpenetrationexpected

� HighdemandforThyssenKruppquality

� LocalTechCenterwithUSandGermanengineersestablished

� Developmentoffuturematerialconceptsforspecifictargetcustomershasstarted

� SuccessfulpositioningofThyssenKruppSteelaspremiumsupplier

46

ThyssenKrupp

PresentationThyssenKrupp,CreditSuisseFieldTrip,April1,2009

Transatlantic�Forward�Strategy Target�Structure�2012:�Slab�Production�and�Consumption

Increased�strategic�flexibility

Significant�cost�dilution

Optimized�sourcing�of�external�slabs

Optimized�cost�degressionthrough�mini�cycles

~5~2

~2

~15

~15

~5

� based�on�5�m�t�of�high-quality�and�low-cost�slabsfrom�TK�CSA

� based�on�logistics�cost�and�availability�Badjust�slab�supply�ex�CSA�to�Europe�and�U.S.C

� based�on�adjustment�of�external�slab�purchasesBat�optimized�utilization�of�own�upstream�facilitiesC

� based�on�transatlantic�production�network

Growth�Complemented�by�Significant�Cost�Dilution�and�Flexibility

TK�Steel�USA

TK�CSA~5�m�t

TK�SteelEurope

~0-2�m�t~3-5�m�t

million�t�p.a.

German

Operations

TK�CSA German�Operations

incl.�project “Herkules“

TK�Steel

USA

Slab Production Slab Consumption Ext.�Slabs

47

ThyssenKrupp

PresentationThyssenKrupp,CreditSuisseFieldTrip,April1,2009

� Comprehensivecostcuttinginitiated� Short-termmeasures: ~€0.4bn

-inFY08/09;predominantlyone-timeeffects.

� Program20/10: >€0.4bn/yr-byFY10/11;sustainablesavings.

� GrowthCapex� ForwardStrategyEurope: €0.4bn� ForwardStrategyNAFTA: $3.25bn� ForwardStrategyBrazil: €4.5bn

� Committedto� Reliableandsignificantprofitcontribution� DrivevaluefortheGroup!

Profitable

growth

Efficiency

improvement

Sustainable value growth

Technology

leadership

Focus�on�attractive marketsfor premium flat steel products

Strategy�Implementation�Based�on�Proven�Business�Model

Major�Transformation�Based�on�Cost�Optimization�and�Growth

Developing�the�future.�ThyssenKrupp�Steel.

48

ThyssenKrupp

PresentationThyssenKrupp,CreditSuisseFieldTrip,April1,2009

� Group�Overview�and�StrategyUlrichMiddelmannViceChairmanoftheExecutiveBoardofThyssenKruppAG

� ThyssenKrupp�SteelPeterUrbanViceChairmanoftheExecutiveBoardofThyssenKruppSteelAG

� ThyssenKrupp Services�and�ThyssenKrupp�ElevatorEdwinEichlerMemberoftheExecutiveBoardofThyssenKruppAG

Agenda

49

ThyssenKrupp

PresentationThyssenKrupp,CreditSuisseFieldTrip,April1,2009

ThyssenKrupp�Elevator�Organization

Escalators/PassengerBoardingBridges

Central/Eastern/NorthernEurope

SouthernEurope/Africa/

Middle East

Asia/PacificAmericas

Accessibility

Escalators/PassengerBoardingBridges

Central/Eastern/NorthernEurope

SouthernEurope/Africa/

Middle East

Asia/PacificAmericas

Accessi-bility

2007/08

Sales�€m*

Employees

1,482

11,251�

827

7,335

1,892

14,754

495

5,955

332

2,404

ThyssenKruppElevatorAGSales€4.9bn • EBT€434million • Employees 42,992

215

1,180

Servicebase:930,000units*not�consolidated

50

ThyssenKrupp

PresentationThyssenKrupp,CreditSuisseFieldTrip,April1,2009

Otis

ThyssenKrupp13%13%13%13%

Mitsubishi

Kone

Hitachi

Toshiba

Fujitec

Others

Schindler

Elevator:�World�Market�Marketsharesofoverallmarketforelevatorsandescalators-estimation.

Volume:�€35-40�bn

Asof2008

51

ThyssenKrupp

PresentationThyssenKrupp,CreditSuisseFieldTrip,April1,2009

Elevator�Track�RecordHighlights

EBTin€m

Q1 Q2 Q3 Q4 Q1

2007/08 2008/09

119 90 92 133 156

112139

excl.majornonrecurringitems

-20.-6.

Q1 Q2 Q3 Q4 Q1

2007/08 2008/09

Orderintakein€m

1,466 1,464 1,324 1,281 1,562

-2.

158

2002/03 2003/04 2004/05 2005/06

355 370 355 391

2006/07

>500e367*

2007/08

434

2008/09

EBTin€m

* excl.EUfine€480m

52

ThyssenKrupp

PresentationThyssenKrupp,CreditSuisseFieldTrip,April1,2009

New�Installation�BusinessPresent RegionalMarketDevelopment

SpainSharp�decline

residential market

FranceMarket�downturn

UKMassive�decline

ChinaSlower growth

Prospects:Infrastructure projects

DubaiBuilding�freeze

No�new�projects

IndiaStable

BrazilStable

RussiaBuilding�freeze

No�new�projectsGermanyStable

USMassive�decline

residential market,

condominiums

KoreaMarket�downturn

Eastern�EuropeBuilding�freeze

No�new�projects

ThyssenKrupp

53

ThyssenKrupp

PresentationThyssenKrupp,CreditSuisseFieldTrip,April1,2009

Marketvolume

MaintenanceService

Newequipment

Modernization

Infrastructureprojects

Strongbacklog

Downturn2nd HY

Margin pressure Recovery Growth

Reduction

DownturnDownturn

Recovery

Recovery

Growth

Bottomof crisis

Recovery

Begin

Boom

Stable

Reduction

Stable

Startdownturn

Q108/09Q108/09Q108/09Q108/09 today 08/09�����������09/10�������������10/11�����������long-term

Downturn�deferred

but�with�opportunities

Global�Financial�Crisis�Impactonmarketvolumeovertime

54

ThyssenKrupp

PresentationThyssenKrupp,CreditSuisseFieldTrip,April1,2009

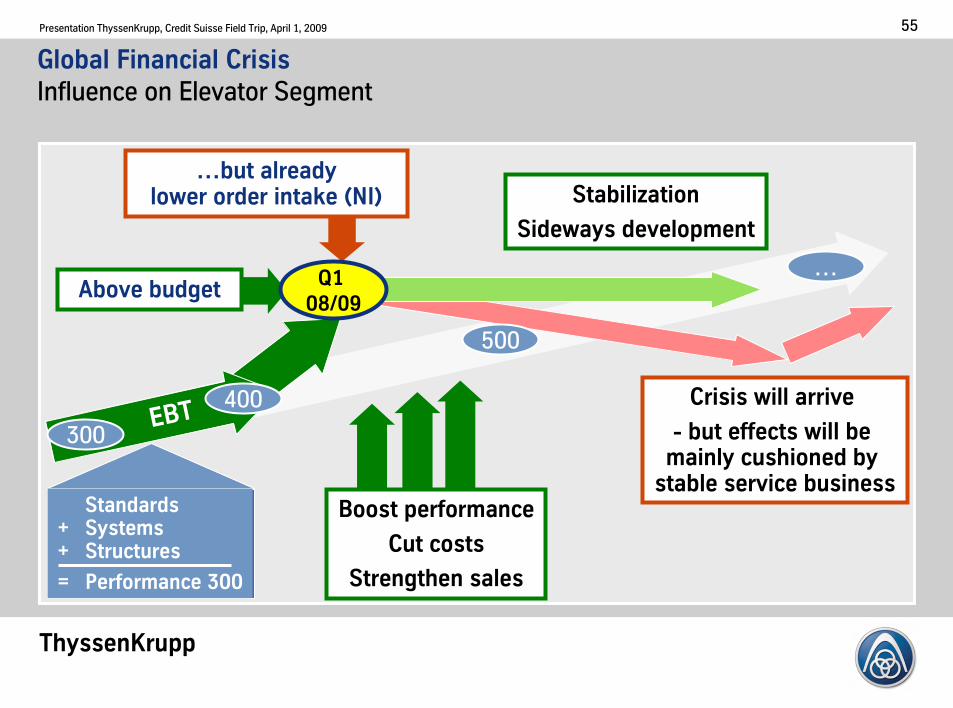

Global�Financial�Crisis�InfluenceonElevatorSegment

Standards+ Systems+ Structures

= Performance�300

Stabilization

Sideways�development

Crisis�will�arrive�

- but�effects�will�be�mainly�cushioned�by�stable�service�business

…Above�budget�

…but�alreadylower�order�intake�BNIC

500

Boost�performance

Cut�costs

Strengthen�sales

EBT

Q1�08/09

EBT300

400

55

ThyssenKrupp

PresentationThyssenKrupp,CreditSuisseFieldTrip,April1,2009

� StrengtheningPerformanceProgram300

� StrongCostReduction

� InvestSTOP

� SalesInitiative

� ReductionNWC

� Prospects:InfrastructureProjects

Measures+�PLUS

Howtopreparefordownturn?Current�overall�

situation

07/08

EBT�in�€ m

08/09asperSept 08

08/09asperMarch 09

� AMS outperforming

� Pretty�stable�develop-ment inEurope

� AP�stable,�slower�growth

� RestructuringUK�/�Korea�effective,butmarketdownturn

� EMC�implementation

� High�Order�Backlog�from�previous�years

� Currently�reduced�Order�Intake�

� Margin�pressure

434 ~500 >500e

Elevator:�Overview�development�Actualmeasurestoovercomethecrisis

56

ThyssenKrupp

PresentationThyssenKrupp,CreditSuisseFieldTrip,April1,2009

Service50%

R&D ProductManu-

facturing Installation Maintenance Modernization Repair

NewInstallation50%

Elevator:�Performance�Program�300Standards,SystemsandStructures

PersonnelManagement

OpportunitiesInfrastructureProjects

CutCostsLiquidity

NWCInitiative

StrengthenSales

R&DPlatform

StandardizationII

EMC

SCM-tocome. ModernizationPackage

ServiceAwareness

Sales&ServiceInitiative

ITPlatformPROGRESS

57

ThyssenKrupp

PresentationThyssenKrupp,CreditSuisseFieldTrip,April1,2009

Target�for�Platforms�A�and�B�defined

KeydriverforPlatformAis

product�cost

Elevator:�Performance�Program 300�Standardization II

KeydriverforPlatformBis

managing�product�complexity�at�lowest�possible�product�cost

PlatformformarketClusterA=basedonSynergy�layout

PlatformformarketClusterB=basedonEvolution�layout

58

ThyssenKrupp

PresentationThyssenKrupp,CreditSuisseFieldTrip,April1,2009

Specializedsalesunitforafter-salesservicesIndividualtargetsforownandthird-partyportfolio

Sales

TrainingSales

TechniquesMod&

Maintenance

MK&OperationalTools,Procedures&Documentation

FOBSeame Intranet

Individualtargets

SpecializedRenew&Service

SalesForce

CommercialPlan

Budgeting/Monitoring

Mod/RepKits

SupportActivities � ToolBoxes

Elevator:�Performance�Program�300RENEW Initiative,BUSouthernEurope,Africa&MiddleEast

FY05/06– FY09/10:Salesincrease:€132m• EBT:€33.5m-intotal.

59

ThyssenKrupp

PresentationThyssenKrupp,CreditSuisseFieldTrip,April1,2009

12

EBIT�%

EBT

700600500400

€700-800�m

300 800

>12% StrategicWindow

Elevator:�Definition�of�Clear�Profitability�TargetsSignificantriseofEBIT-margin

today€3.3bnsales

Performance

Program

300:

Product,

Invest-Ro

admap,E

XEast

60

ThyssenKrupp

PresentationThyssenKrupp,CreditSuisseFieldTrip,April1,2009

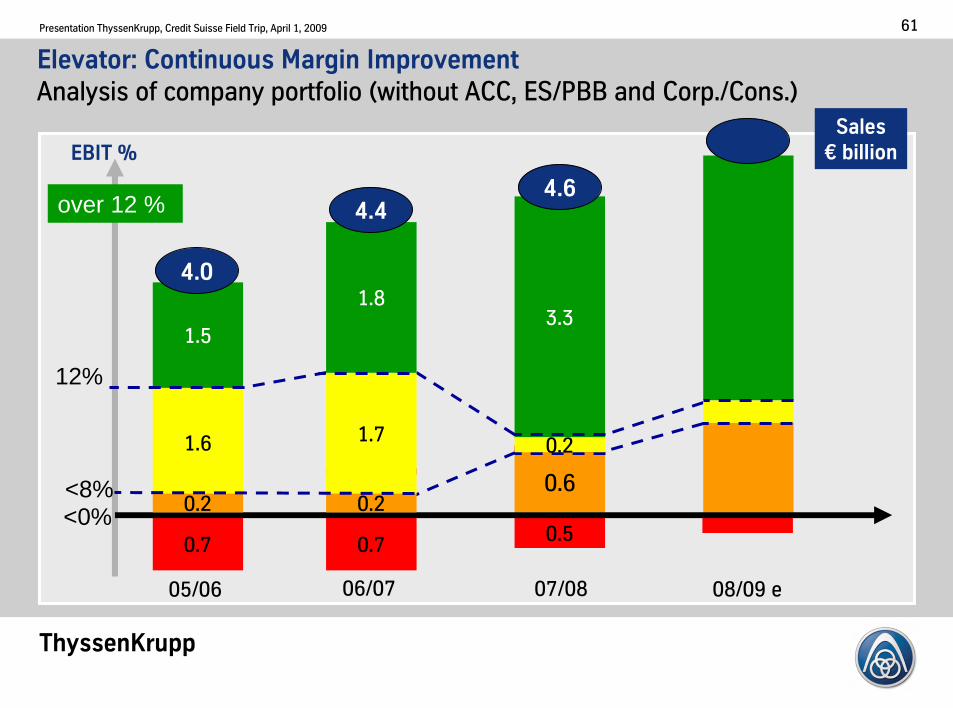

Elevator:�Continuous Margin�ImprovementAnalysisofcompany portfolio -withoutACC,ES/PBBandCorp./Cons..

Sales€ billionEBIT�%

1.6

1.5

12%

<8%

0.7

05/06

over 12 %

3.3

0.6

4.6

07/08 08/09e

1.8

0.7

06/07

0.5<0%

4.0

4.4

0.21.7

0.2 0.2

61

ThyssenKrupp

PresentationThyssenKrupp,CreditSuisseFieldTrip,April1,2009

Sales€m

07/0804/05 05/06 06/07

TKVA€m

EBT€m

355

244

3,773

4,298

391

314

434

4,930

EBIT�margin 9.6%10.1% 9.8% 8.6%

264

4,712

08/09�e

>500

244

375

*�exkl.�EMC*

Elevator:�Development�of�Key�DataFY2004/05� 2008/09

62

ThyssenKrupp

PresentationThyssenKrupp,CreditSuisseFieldTrip,April1,2009

3.8

4.9

4.34.7

04/05 05/06 06/07 07/08 08/09�e

Elevator: NWC�Management�Developmentofsales-billion€.andNWCas%ofsales

ReducedNWCby63%

Increasedsalesvolume

Sales NWCas%ofsales

63

ThyssenKrupp

PresentationThyssenKrupp,CreditSuisseFieldTrip,April1,2009

Elevator:�New�Important�Orders,�Q1�2008/09MetroLines

NI Rome,Italy 41 elevators88 escalators

NI Shenzhen,China 94 escalators

NI SaoPaulo,Brazil 65 escalators

Mod Madrid,Spain 181 escalators

Mod Barcelona,Spain 37 escalators

NI=Newinstallation • Mod =Modernization

Madrid

Barcelona

Rome,LineC

SaoPaulo,Linha Verde

Shenzhen,Line5

64

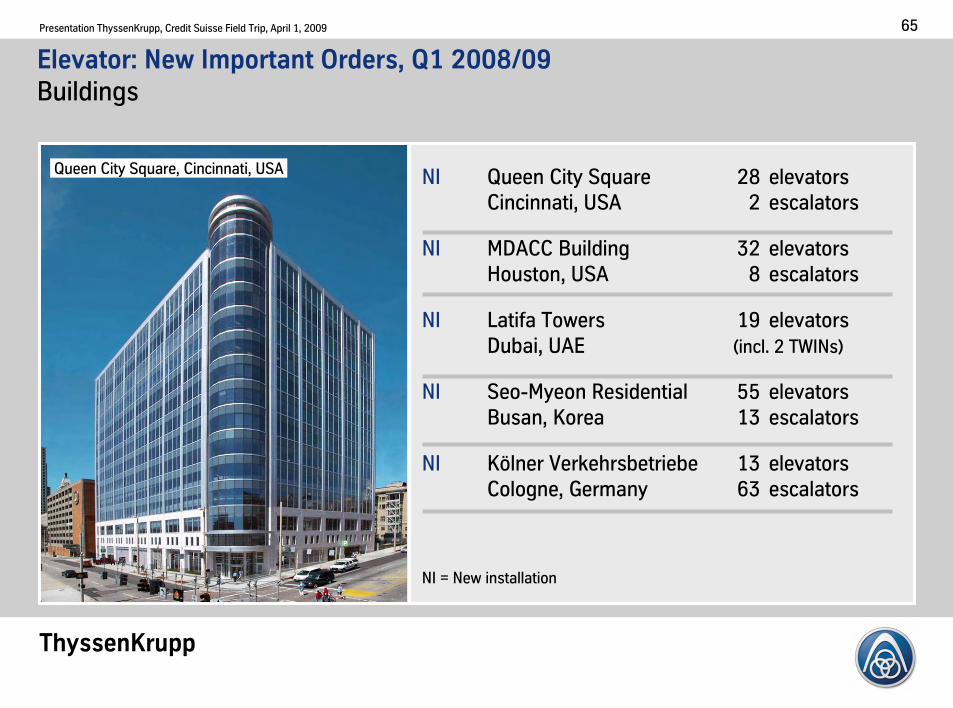

ThyssenKrupp

PresentationThyssenKrupp,CreditSuisseFieldTrip,April1,2009

NI QueenCitySquare 28 elevatorsCincinnati,USA 2 escalators

NI MDACCBuilding 32 elevatorsHouston,USA 8 escalators

NI Latifa Towers 19 elevatorsDubai,UAE-incl.2TWINs.

NI Seo-Myeon Residential 55 elevatorsBusan,Korea 13 escalators

NI Kölner Verkehrsbetriebe 13 elevatorsCologne,Germany 63 escalators

NI=Newinstallation

QueenCitySquare,Cincinnati,USA

Elevator:�New�Important�Orders,�Q1�2008/09�Buildings

65

ThyssenKrupp

PresentationThyssenKrupp,CreditSuisseFieldTrip,April1,2009

37�Airports Sep.,�2008�- 2010

Airport�projects in�ChinaPlannedconstructioncompletionby2010China

“stimulus�package”Infrastructure�programUSA

Positiveeffects from:

• Infrastructure projects-stations,airports.

• Publicbuildings,especially hospitals51 planned�2011-2020

Elevator:�Opportunities�in�the�Financial�Crisis:�Infrastructure�ProjectsWorldwide:Airports,metros,hospitals,otherpublicbuildings

66

ThyssenKrupp

PresentationThyssenKrupp,CreditSuisseFieldTrip,April1,2009

Performance:Product• Manufacturing• Service• SalesInvest.-Roadmap• EXEast

00/01

226

Long-termTarget

800Project�800

Perform�300

680

Mid-termTarget

06/07

367

280PerformanceProgram 300

08/09�e

>500

Invest.�Roadmap+�EX�East

excl.�EU�fine

Today

07/08

434

Elevator:�Performance�Program�300

67

ThyssenKrupp

PresentationThyssenKrupp,CreditSuisseFieldTrip,April1,2009

Liquidity

PersonnelManagement

Focus�on�Customers�and�Markets

Exploit�

OpportunitiesNew�Structures

Boost

Performance

EBTin08/09e:€>500mEBTin09/10:Stabilization

EffectPerform 300

Impetus�from backlog

Timetopreparefordownturn

Better�Performance

Weak�Competitors

Infrastructure�Projects

Elevator:�Conclusions

68

ThyssenKrupp

PresentationThyssenKrupp,CreditSuisseFieldTrip,April1,2009

355

390

434FY07/08

-113 1incl.�EU-fine2

FY06/07

>500e

We�will�reach�base�camp�and�survive�the�storm!

FY08/09

700

800

ThyssenKrupp

PresentationThyssenKrupp,CreditSuisseFieldTrip,April1,2009

ThyssenKrupp�Services�AG

Sales€17.3bn • EBT€750million • Employees 46,486

ThyssenKrupp�Services�– Business�UnitsFigures 2007/2008

Sales€1.8billionEmployees3,048

Sales€2.1billionEmployees30,181

Sales€4.9billionEmployees1,178

Sales€8.5billionEmployees11,889

Operatingandmaintenance services,production support,intraplant logistics,

outsourcing

Trading,logistics,project management

steel andpipes,raw materials,

energy andtechnics

Materials�ServicesNorth�America

IndustrialServices

Materials�ServicesInternational

SpecialProducts

Warehousing,processing,logistics,materials andinventory management,

supply chain management

steel,stainless steel,NF-metals,pipes andtubes,plastics

For�Sale

70

ThyssenKrupp

PresentationThyssenKrupp,CreditSuisseFieldTrip,April1,2009

Services:�Unique�Portfolio�in�Products�and�ServicesSalesbyproducts/services-%.,2007/08

CarbonSteel– fromTK8.6%

Pipes&Tubes

StainlessSteel– fromTK3.9%

NF-Metals

Plastics

RawMaterials

IndustrialServices

TechnicalProducts

13

4

14

15

5

29

6

14

ThyssenKruppProducts12.5%

Morethan 150,000�product items

Steel share below 50%,�continuingtodecline

Independent sourcing,notasalesorganizationforSteelandStainlesssegments

About300,000�customersworldwide

Services aredriving growth

71

ThyssenKrupp

PresentationThyssenKrupp,CreditSuisseFieldTrip,April1,2009

Services:�Track�RecordHighlights

EBTin€m

Q1 Q2 Q3 Q4 Q1

2007/08 2008/09

Q1 Q2 Q3 Q4 Q1

2007/08 2008/09

Orderintakein€m

EBTin€m

2002/03 2003/04 2004/05 2005/06

32

251 261

482

2006/07

750704

2007/08 2008/09

3,951 4,322 4,677 4,503 3,746132 135 248 23530

72

ThyssenKrupp

PresentationThyssenKrupp,CreditSuisseFieldTrip,April1,2009

2,000

2,500

3,000

3,500

4,000

4,500

3,248

4,338

1,830

06/07 07/08 08/09

O N D J FFFF M A M J J A SO N D J FFFF M A M J J A SO N D J F M A M J J A SO N D J F M A M J J A SO N D J F M A M J J A SO N D J F M A M J J A S

Stainless cold-rolled sheetsincl.alloy surcharge

Purchase price ThyssenKrupp�Schulte,�Central�warehouse stainless steel

300

400

500

600

700

800

06/07 08/0907/08

Freight RateChinaARA125

Coke,FOBChina

730

420

O N D J FFFF M A M J J A SO N D J F M A M J J A SO N D J F M A M J J A S

200

100 33

300

400

500

600

700

800

06/07 08/0907/08

Freight RateChinaARA125

Coke,FOBChina

730

420

O N D J FFFF M A M J J A SO N D J FFFF M A M J J A SO N D J F M A M J J A SO N D J F M A M J J A SO N D J F M A M J J A SO N D J F M A M J J A S

200

100 33

60,00052,161

10,000

20,000

30,000

40,000

50,000

31,217

10,404

O N D J FFFF M A M J J A SO N D J F M A M J J A SO N D J F M A M J J A S

06/07 07/08 08/09

60,00052,161

10,000

20,000

30,000

40,000

50,000

31,217

10,404

O N D J FFFF M A M J J A SO N D J FFFF M A M J J A SO N D J F M A M J J A SO N D J F M A M J J A SO N D J F M A M J J A SO N D J F M A M J J A S

06/07 07/08 08/09

06/07 07/08 08/09

O N D J F M A M J J A S O N D J FFFF M A M J J A SO N D J F M A M J J A S

Sections /broad flanged beamColdrolled sheetsGalvanized sheetsQuarto plates -R37-2.

ThyssenKrupp�Schulte,�PM�Walzstahl

245

955

630

480

480

940

800

855

1,000

400

500

700

800

900

600

300

06/07 07/08 08/09

O N D J F M A M J J A S O N D J FFFF M A M J J A SO N D J F M A M J J A S

06/07 07/08 08/09

O N D J F M A M J J A S O N D J FFFF M A M J J A SO N D J F M A M J J A SO N D J F M A M J J A SO N D J F M A M J J A S O N D J FFFF M A M J J A SO N D J FFFF M A M J J A SO N D J F M A M J J A SO N D J F M A M J J A S

Sections /broad flanged beamColdrolled sheetsGalvanized sheetsQuarto plates -R37-2.

ThyssenKrupp�Schulte,�PM�Walzstahl

Sections /broad flanged beamColdrolled sheetsGalvanized sheetsQuarto plates -R37-2.

ThyssenKrupp�Schulte,�PM�Walzstahl

245

955

630

480

480

940

800

855

1,000

400

500

700

800

900

600

300

Price�Developments

Delta2,508

Delta41,757

Stainless�Steel�€/tCarbon Steel�€/t

Coke,�Freight Rate�China�US$/tNickel�US$/t�Bmonthly averageC

73

ThyssenKrupp

PresentationThyssenKrupp,CreditSuisseFieldTrip,April1,2009

Present Regional�Market�Development

Russia

Construction�freeze

Business�standstill

Eastern�Europe

Building�freeze

Slump in�rolled steelGermanyStrongest devalua-tion volume

Southeast AsiaStrong decline

SpainDeep crisis

UKMassive�decline

DubaiConstruction�freezeNo�new projects

ChinaStill�growth

Prospectsinfrastructure

USASlumpalso�in�NF-metals

Safwaystable

AerospaceUSA/Europe�normal

Brazilstable

FranceStrong decline

74

ThyssenKrupp

PresentationThyssenKrupp,CreditSuisseFieldTrip,April1,2009

Market�EnvironmentSelected Sectors in�Germany

Mechanicalengineering

Steelindustry

Commercialvehicles

Autoindustry1cars2

Constructionindustry

Collapse inorders inJanuary 2009vs2008,biggest dropsince 1958

-42%

Collapse inorders in4thquarter 2008compared to2007,biggest dropsince 1945

Decline inoutput inJanuary - February 2009vs.prior year

Decline inoutput inJanuary- February2009vs.prioryear

Orderintake January 2009vs 2008,effect ofstimulus programs?!

-47%

-57%

-41%

-12%-24%

75

ThyssenKrupp

PresentationThyssenKrupp,CreditSuisseFieldTrip,April1,2009

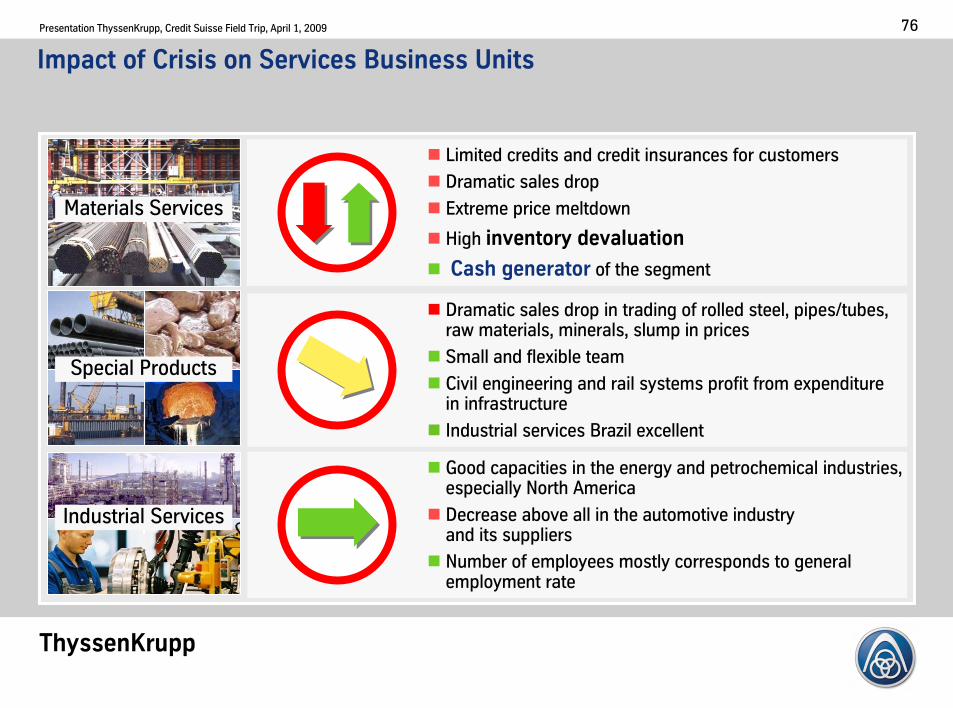

Impact�of�Crisis on�Services�Business�Units

� Dramaticsalesdropintradingofrolledsteel,pipes/tubes,rawmaterials,minerals,slump inprices

� Smallandflexibleteam

� Civilengineering andrail systems profit fromexpenditureininfrastructure

� Industrialservices Brazil excellent

� Limitedcreditsandcreditinsurancesforcustomers

� Dramatic sales drop

� Extremeprice meltdown

� Highinventory devaluation

� Cash�generator ofthe segment

� Goodcapacities inthe energy andpetrochemical industries,especially NorthAmerica

� Decrease above allinthe automotive industryandits suppliers

� Numberofemployeesmostlycorrespondstogeneralemploymentrate

IndustrialServices

SpecialProducts

MaterialsServices

76

ThyssenKrupp

PresentationThyssenKrupp,CreditSuisseFieldTrip,April1,2009

Materials�Services�Business�Model�Changeinearnings fromcyclic market/price developments

Sellingprice

Stock�value=�prime�cost

Purchaseprice

Margin

normal

higher lower

normal

Boom=�EBT

Slump=�Cash

Asset gains Asset losses

Loss fromlower ofcostor market principle

77

ThyssenKrupp

PresentationThyssenKrupp,CreditSuisseFieldTrip,April1,2009

Nearly�Every�Region,�Every�Industry�Hit�by�the�Economic�Crisis��Breakdown ofcompletevaluechains,standstillofpartsoftheeconomy

How�to�react?

� Postpone Growth

� Cut�Costs

� Adjust the Organization

� Concentrate on�Sales

� Motivate People

� Release�Working Capital

� Generate Cash

Keep on�trackwith strategy

78

ThyssenKrupp

PresentationThyssenKrupp,CreditSuisseFieldTrip,April1,2009

Services:�Mission�Statement�as�Construction�Kit for�Measures

IndustrialServices

SpecialProducts

MaterialsServices

� Salesinitiatives,markets/regions� Outsourcing� Reversefactoring program

Market

� FlexibleHRmanagement� Shorttimework/training� Work forcereduction

People

� Adjustment oforganization,warehousing,logistics,andadministration

Organization

� Inventories,debt,net working capital

� Performanceprograms

Profitability

79

ThyssenKrupp

PresentationThyssenKrupp,CreditSuisseFieldTrip,April1,2009

Services�Crisis Management:�Cost Reduction59measure packages

Effect on�EBT>€200�million

� Personnel

� Materialcosts

� Reducing M&R

� Reducing/optimizingtransport,logistics

� Reducing administration

� Reducing locations

� Optimization sourcing

� Assets

� NWCinitiative

� Investments

� Portfolio

ThyssenKruppPLUS Program

Reducing NWC>€800�million

80

ThyssenKrupp

PresentationThyssenKrupp,CreditSuisseFieldTrip,April1,2009

Services:�The�Whole�Spectrum�of�Personnel�Measures�

Avoidredundanciesif possible

Reducing overtime accounts/holidays

Freeze of�recruitments

Discharge external personnel

Use of�fluctuation

Early retirement

No�take-over�of�apprentices

Short�time�work

Reduced salary

Redundancies

Expiry temporary staff

Reduction of�variable�salary parts

Flexibly

Consistently

Immediately

81

ThyssenKrupp

PresentationThyssenKrupp,CreditSuisseFieldTrip,April1,2009

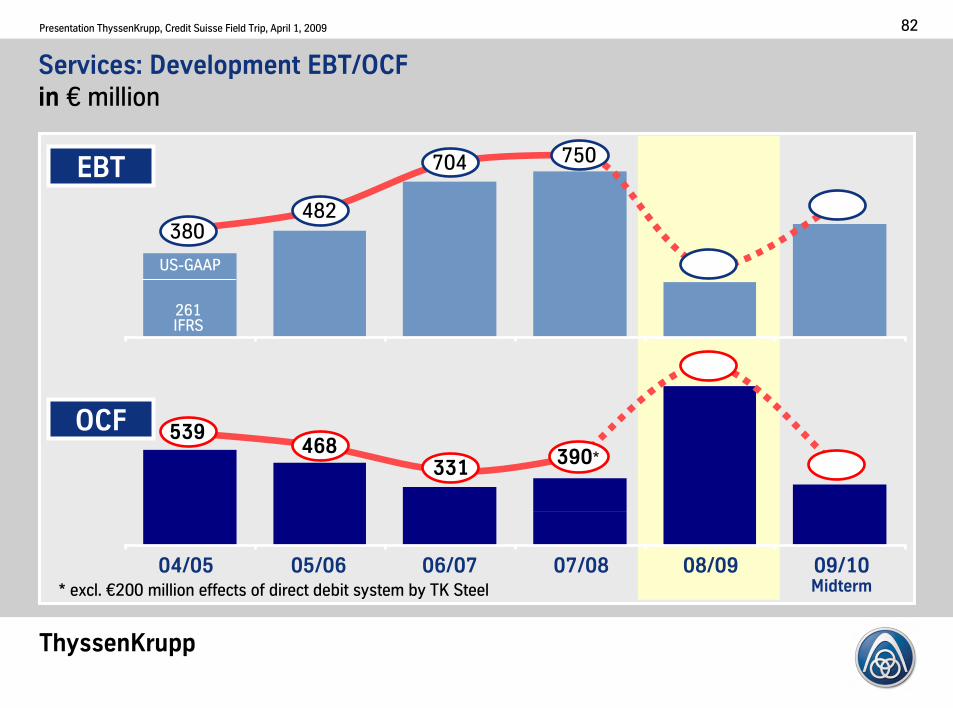

Services:�Development EBT/OCFin € million

04/05 05/06 06/07 07/08 08/09 09/10Midterm

380482

704EBT

OCF 539468

331

261IFRS

US-GAAP

750

390*

*excl.€200millioneffectsofdirectdebitsystembyTKSteel

82

ThyssenKrupp

PresentationThyssenKrupp,CreditSuisseFieldTrip,April1,2009

Key�Data�Segment�Services��

-100

0

100

200

300

400

500

600

700

800

900

1.000

EBT€m

Sales€bn 11.2

12.7

14.2

12.3

16.7

TKVA€ m

ROCE

02/03 04/05 05/06 06/07 07/08

32

251 261

482

704

23.6%

3.7%

12.9% 10.8%

19.2%

294

57105

-168

487

08/09

17.3

21.7%

750

508

09/10

Marketslump,adjustment

Norma-lization

US-GAAP,without

discontinued

03/04

83

ThyssenKrupp

PresentationThyssenKrupp,CreditSuisseFieldTrip,April1,2009

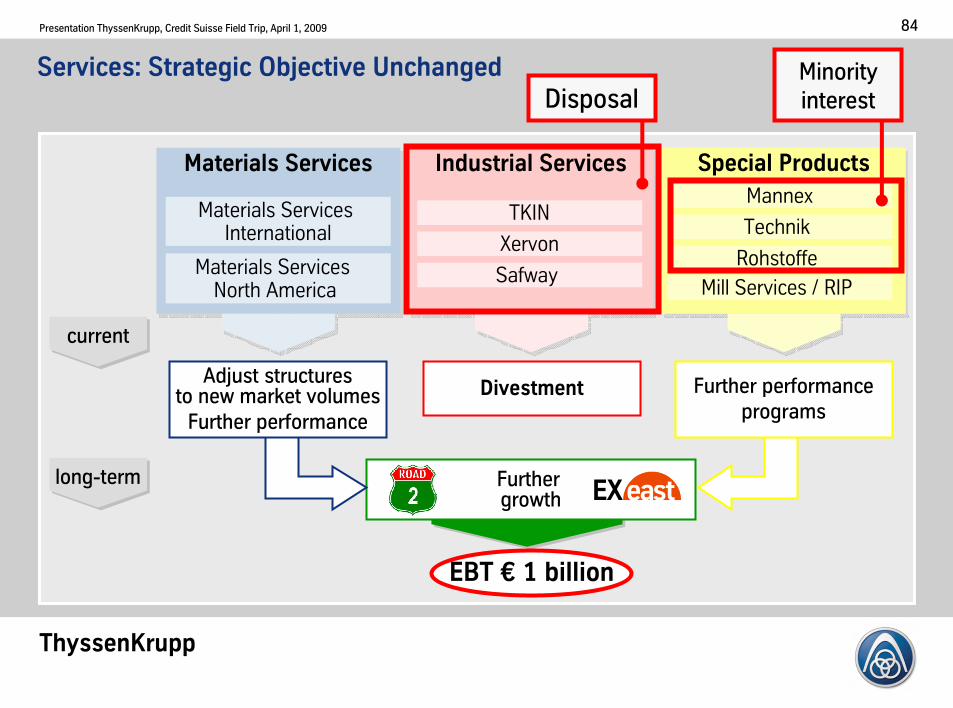

Services:�Strategic Objective Unchanged

Materials�ServicesMaterials�Services

Materials�Services�International

Materials�Services�North�America

Special�ProductsSpecial�Products

Mannex

Technik

Rohstoffe

Industrial�ServicesIndustrial�Services

TKIN

Xervon

Safway

Furthergrowth

Divestment

Mill Services�/�RIP

long-termlong-term

currentcurrent

Further performanceprograms

EBT�€ 1�billion

Adjust structurestonew market volumesFurther performance

MinorityinterestDisposal

84

ThyssenKrupp

PresentationThyssenKrupp,CreditSuisseFieldTrip,April1,2009

Chances

Strategy

Target

Chances Infrastructure InvestmentsOutsourcingWeakness ofCompetitors

Strategy

Target Long�Term:�EBT�€1bnWorld�Market�Leader�in�Materials�and�RawMaterials�Distribution

Tempor

arily

stoppe

d

Strive formarketopportunities

Divest IndustrialServices,stop growth

Keep strategyontrack

Services:�Our Tasks,�Our�Chances,�Our�Strategy,�Our�Targets

Tasks Cost,NWC,LiquidityStructures,OrganizationPerformance,Flexibility

Consistentadjustment

Tasks

85

ThyssenKrupp

PresentationThyssenKrupp,CreditSuisseFieldTrip,April1,2009

Inform:openlycompletelyclearly

Inform:openlycompletelyclearly

Quick adjustmentConsequent cost cutbackQuick adjustmentConsequent cost cutback

Keep strategy ontrackKeep strategy ontrack

Be�unshakably on�target!!!Be�unshakably on�target!!!

Being prepared for�the storm!!!Being prepared for�the storm!!!

Focuscash!!Focuscash!!Focuscash!!Focuscash!!Focuscash!!Focuscash!!Focuscash!!Focuscash!!