Embed Size (px)

Citation preview

Tiffany Winters, Esq.Brette Kaplan Wurzburg, Esq.Brustein & Manasevit, PLLCwww.bruman.com

October 2014

Grants Management Top Best Practices For New Directors!

Ripped from the Headlines

• Former Director of Federal Programs of a State Dept of Ed arrested for ethics violations. Federal funds were awarded to husband’s company through the ARRA SIG grant competition. Possible 20 years in prison and $30,000 in

fines per each of 5 counts• ED/OIG addressed Conflicts of Interest

•School District of Philadelphia▫Did not have adequate fiscal controls in place▫$138,376,068 from grant funds were either unallowable or inadequately

supported Unallowable and inadequately supported personnel expenditures Unallowable and inadequately supported non-payroll expenditures Policies and procedures were not adequate and/or enforced No written policies and procedures for various fiscal processes Supplanting state and local funds with Federal funds

OIG Audit Findings

Top 10 Things Administrators Need to Know!!!

…in no particular order…

Develop and MaintainWritten Policies and Procedures!

Make sure they reflect what the entity is actually doing!

They are required!•OMB Circular A-87•EDGAR•A-133 Annual Single Audits •Changes and Transition of Staff•Uniform Grants Guidance▫Emphasis on internal controls▫Written policies and procedures required

Why Are Policies & Procedures Important?

•Compliant policies and procedures lead to:▫Administering compliant programs and complying with grants management

requirements

•Where to start?•Who should be involved?•What is the process?•How long does it take?• Incorporating changes

based on The Uniform Grants Guidance?

Developing Policies and Procedures

• Incorporate Rules and Regulations!▫Education Department General Administrative

Regulations (EDGAR)▫Office of Management and Budget Circulars▫Omni Circular ▫State/Agency Policies and Procedures▫Authorizing Statute

Developing Policies and Procedures

Describe:• Organization, Structure and Function• Grant Application Process • Financial Management System • Procurement• Inventory/Property Management• Time and Effort• Record Keeping • Monitoring• Audit Resolution • Programmatic Fiscal Requirements• Programmatic Requirements

Developing Policies and Procedures

•Training•Review and revise•Where are policies and

procedures located?

11

Regular Reviews and Updates

12

Know Your Lingo!

Subgrant v. ContractSubgrantee v. ContractorAn important distinction!

Subgrantee v. Contractor

Why is the distinction important?• Federal money spent by a subgrantees is subject to

audit.

• Payments to contractors are not federal awards and not subject to audit.

13

What is a Subgrant?

• Federal law dictates what a subgrant is and when it is allowed.• Therefore, subgrants are permitted when

mandated by statute!• Subgrantees (also known as Subrecipients) must

carry out responsibilities of the federal program• SEAs and LEAs must monitor subgrantees’

compliance with all federal program and fiscal requirements

14

What is a Contract?

• A contract provides goods or services as needed by the program.

• Contractors (also known as Vendors) are NOT responsible for carrying out the responsibilities of the federal program

• Contractors must carry out the terms of their contracts.▫Grantees and Subgrantees must have a contract

administration system to ensure contractors are complying with the terms of their contracts.

15

Subgrant v. ContractHow to Distinguish Between Them

• A subgrantee:• Determines who is eligible to participate in the

federal program• Measures performance against objectives of the

federal program• Is responsible for programmatic decision-making• Is responsible for complying with federal program

requirements• Uses federal funds to carry out the program (not just

provide specific goods/services)

16

Subgrant v. Contract (cont.) How to Distinguish Between Them

• A contractor:• Provides goods/services within normal business

operations• Provides similar goods/services to different

purchasers• Operates in a competitive environment• Provides goods/services ancillary to operation of

federal program• Is NOT subject to compliance requirements of the

federal program.

17

Subgrant v. Contract

•A public agency’s designation as a Contract or Subgrant is not binding▫Auditors are required to use their professional

judgment to determine the true nature of a document based on the previous criteria (OMB Circular A-133 and Compliance Supplement)

• In making the determination – the substance of the relationship is more important than the form of the agreement.

18

Ensure Costs are Allowable

Helpful Questions to Ask• Is the proposed cost consistent with applicable federal

cost principles?• Is the proposed cost allowable under the program?• Is the proposed cost consistent with program specific

fiscal rules?• Is the proposed cost consistent with EDGAR?• Is the proposed cost consistent with special conditions

imposed on the grant?

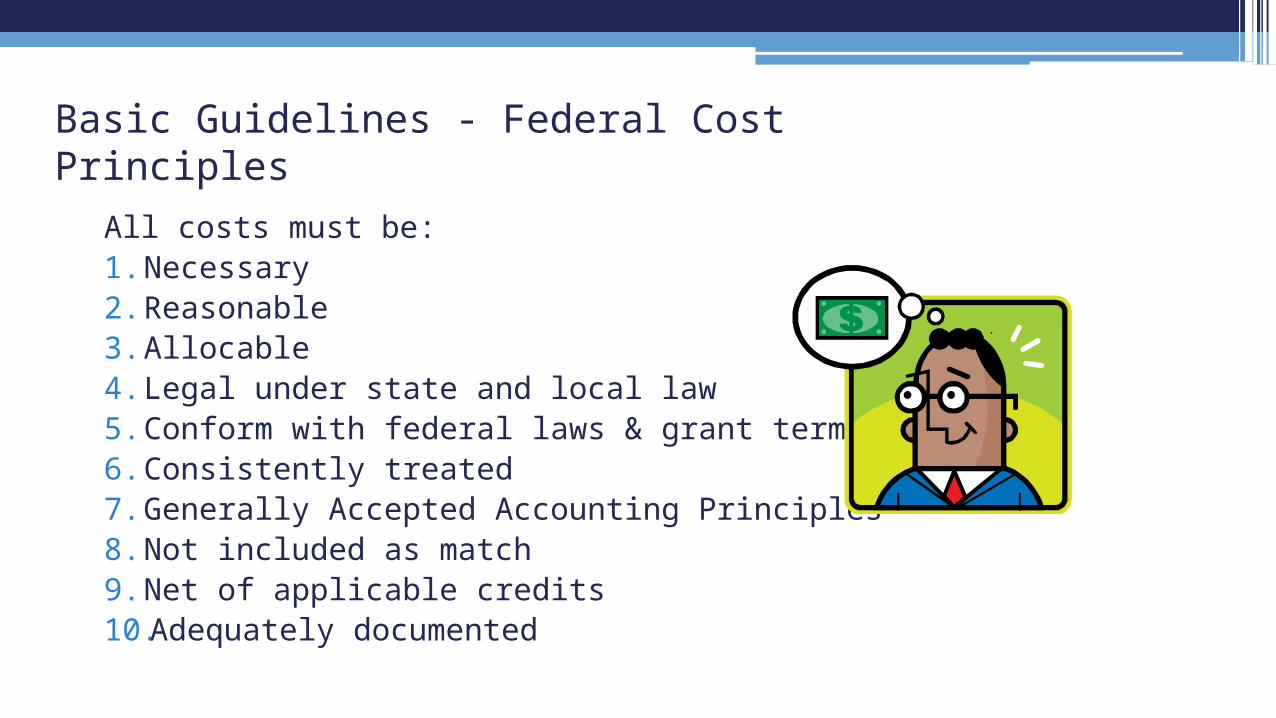

Basic Guidelines - Federal Cost Principles

All costs must be:1. Necessary2. Reasonable3. Allocable4. Legal under state and local law5. Conform with federal laws & grant terms6. Consistently treated7. Generally Accepted Accounting Principles8. Not included as match9. Net of applicable credits10. Adequately documented

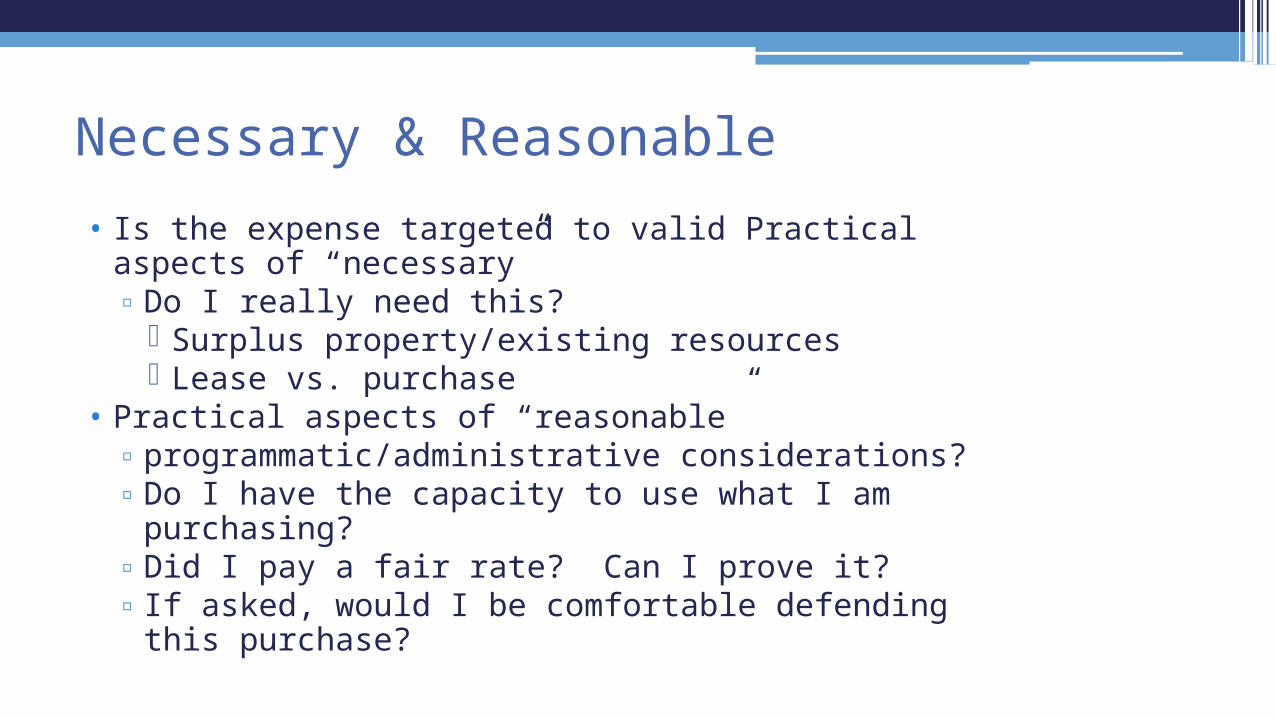

Necessary & Reasonable

•Must be necessary for the performance or administration (operation) of the institutions

•Must follow sound business practices▫Arm’s length bargaining

•Ensure receiving fair market prices•Act with prudence under the circumstances•No significant deviation from established prices

22

Necessary & Reasonable

• Is the expense targeted to valid Practical aspects of “necessary”▫Do I really need this?

Surplus property/existing resources Lease vs. purchase

• Practical aspects of “reasonable”▫programmatic/administrative considerations?▫Do I have the capacity to use what I am purchasing?▫Did I pay a fair rate? Can I prove it?▫ If asked, would I be comfortable defending this purchase?

23

Allocable• Can only charge in proportion to the value received by

the program• Example: If LEA purchases a computer to use 50%

in a federal program, then can only charge half the computer’s cost to that federal program

24

Properly Documented

Adequately documented Amount of funds under grant How the funds are used Total cost of the project Share of costs provided by

other sources Records that show compliance Records that show performance Other records to facilitate an effective audit

25

26

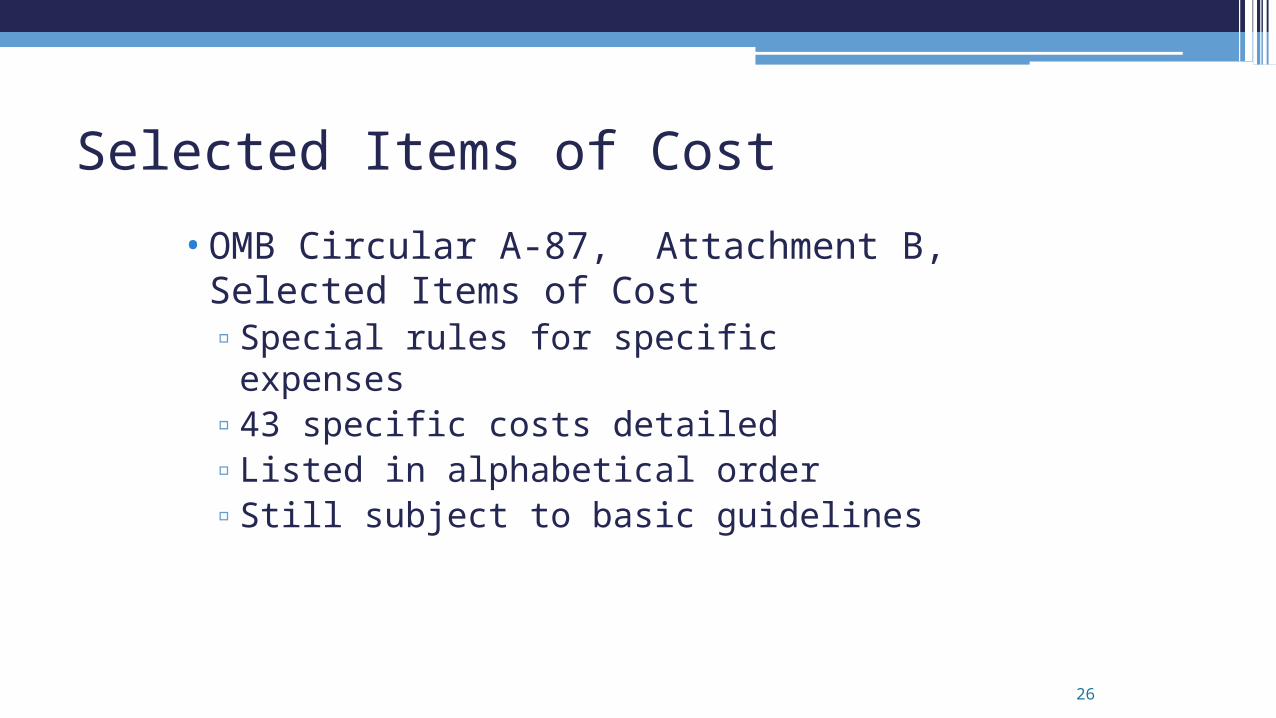

Selected Items of Cost

•OMB Circular A-87, Attachment B, Selected Items of Cost▫Special rules for specific expenses▫43 specific costs detailed▫Listed in alphabetical order▫Still subject to basic guidelines

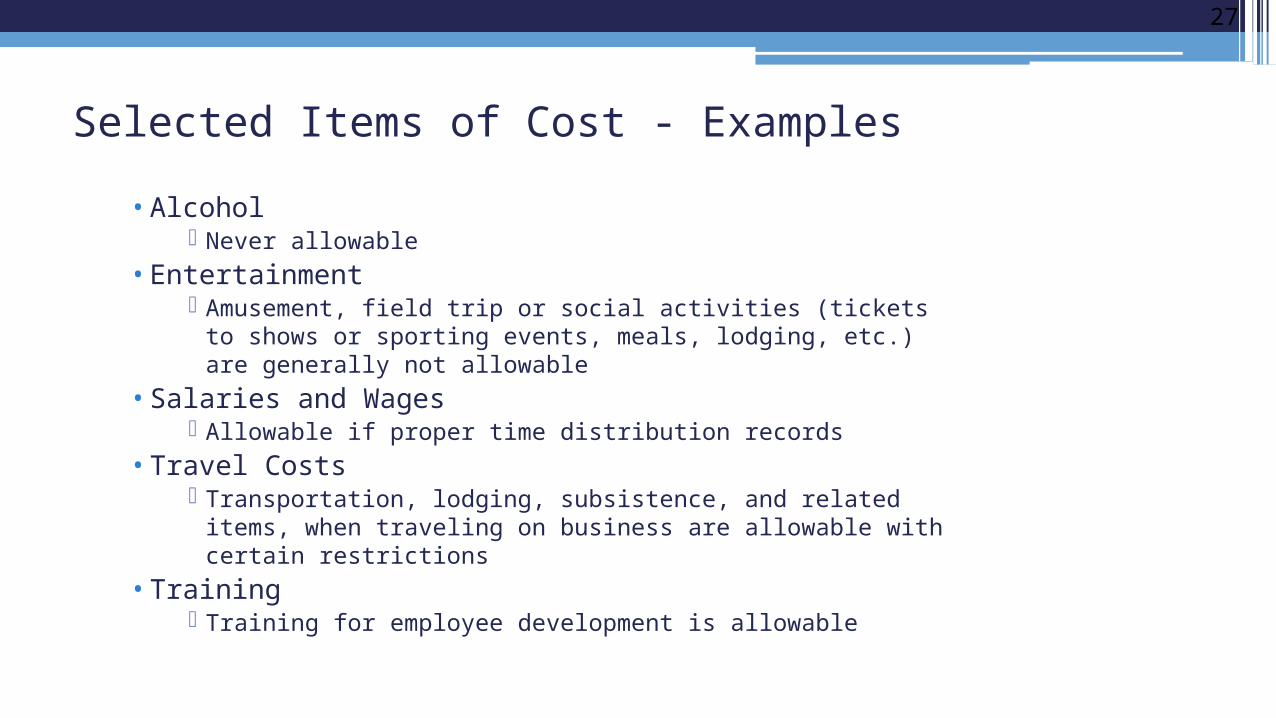

• Alcohol Never allowable

• Entertainment Amusement, field trip or social activities (tickets to shows

or sporting events, meals, lodging, etc.) are generally not allowable

• Salaries and Wages Allowable if proper time distribution records

• Travel Costs Transportation, lodging, subsistence, and related items,

when traveling on business are allowable with certain restrictions

• Training Training for employee development is allowable

27

Selected Items of Cost - Examples

Make Sure Expenditures Are Timely!

•All grants have a period of availability▫Federal Fiscal Year: July 1 through September 30th. (15 months)

Carryover Period: October 1st through September 30th. (12 months)

•Funds must be obligated during the Period of Availability▫An obligation is a transaction that requires payment

Allowability and Obligations of Funds

•An obligation is a transaction that requires payment

•Can only charge the federal award for obligations made during the period of availability

30

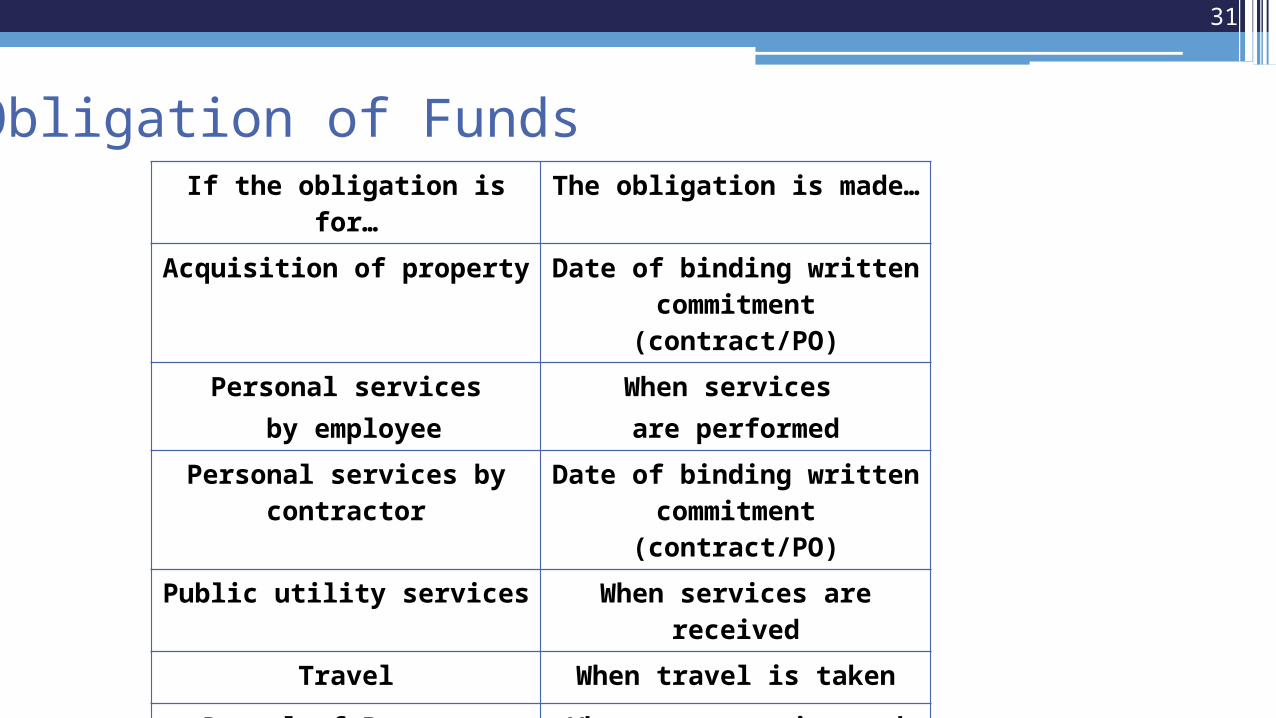

Obligations

31

If the obligation is for… The obligation is made…

Acquisition of property Date of binding written commitment (contract/PO)

Personal services by employee

When services are performed

Personal services by contractor Date of binding written commitment (contract/PO)

Public utility services When services are received

Travel When travel is taken

Rental of Property When property is used

Source: EDGAR Sections 75.707 and 76.707

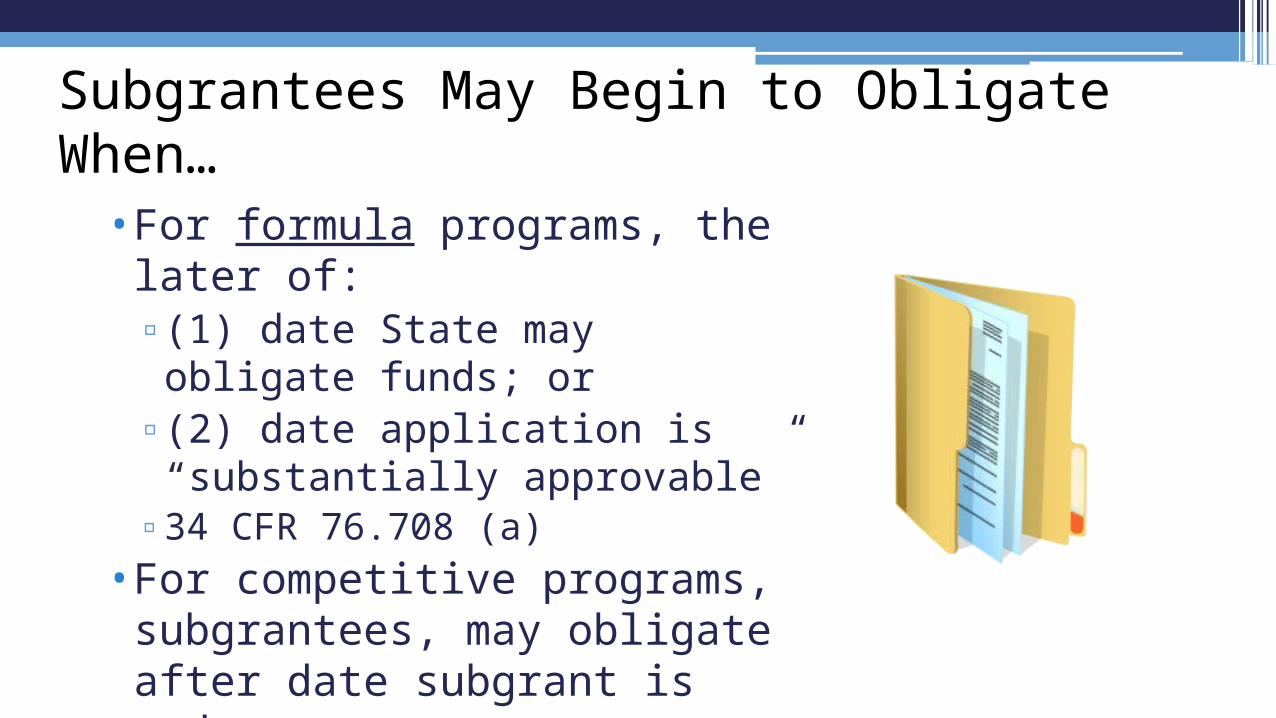

Obligation of Funds

•For formula programs, the later of: ▫(1) date State may obligate funds; or ▫(2) date application is “substantially

approvable”▫34 CFR 76.708 (a)

•For competitive programs, subgrantees, may obligate after date subgrant is made▫34 CFR 76.708 (c)

Subgrantees May Begin to Obligate When…

32

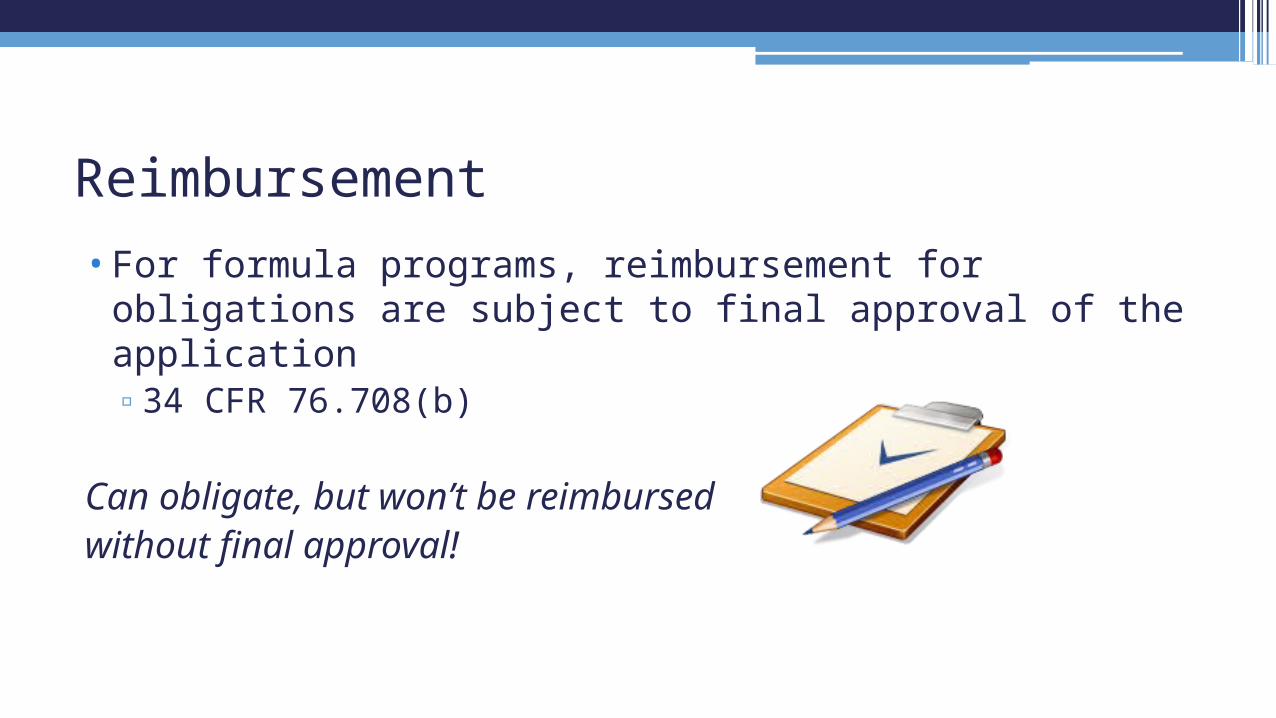

•For formula programs, reimbursement for obligations are subject to final approval of the application▫34 CFR 76.708(b)

Can obligate, but won’t be reimbursed without final approval!

Reimbursement

•Goal: To comply with methods and procedures for minimizing time elapsing between transfer of funds and disbursement by the LEA

•Generally, LEAs receive payment from SEA on a reimbursement basis▫If LEA receives advance, must remit interest on advance payment quarterly

to Federal agency. LEA may retain interest amounts up to $100/year for admin expenses (Uniform Grants Guidance = $500)

Cash Management Improvement Act (CMIA)

• LEA requests reimbursement for actual expenditures incurred under the federal grant on a regular basis (Ex: monthly)▫LEA follows SEA’s protocol for requesting reimbursement

Includes required details, uses appropriate form, provides adequate source documentation, submits to appropriate position/office

▫SEA processes reimbursement requests

Reimbursement

• LEA must maintain source documentation supporting federal expenditures (invoices, purchase orders, time sheets, payroll stubs, etc.)

•Maintain documentation for 3 5 years•Make documentation available for SEA/Federal review

upon request

Reimbursement – Maintain Documentation!

Establish Effective Internal Controls!

Internal Controls•Tools to help program and

financial managers achieve results and safeguard program integrity▫Includes processes for planning,

organizing, directing, controlling, and reporting on agency operations

Internal Controls

•Objectives of Internal Controls▫Effectiveness and efficiency of operations▫Reliability of financial reporting▫Compliance with applicable laws and

regulations▫Safeguarding assets

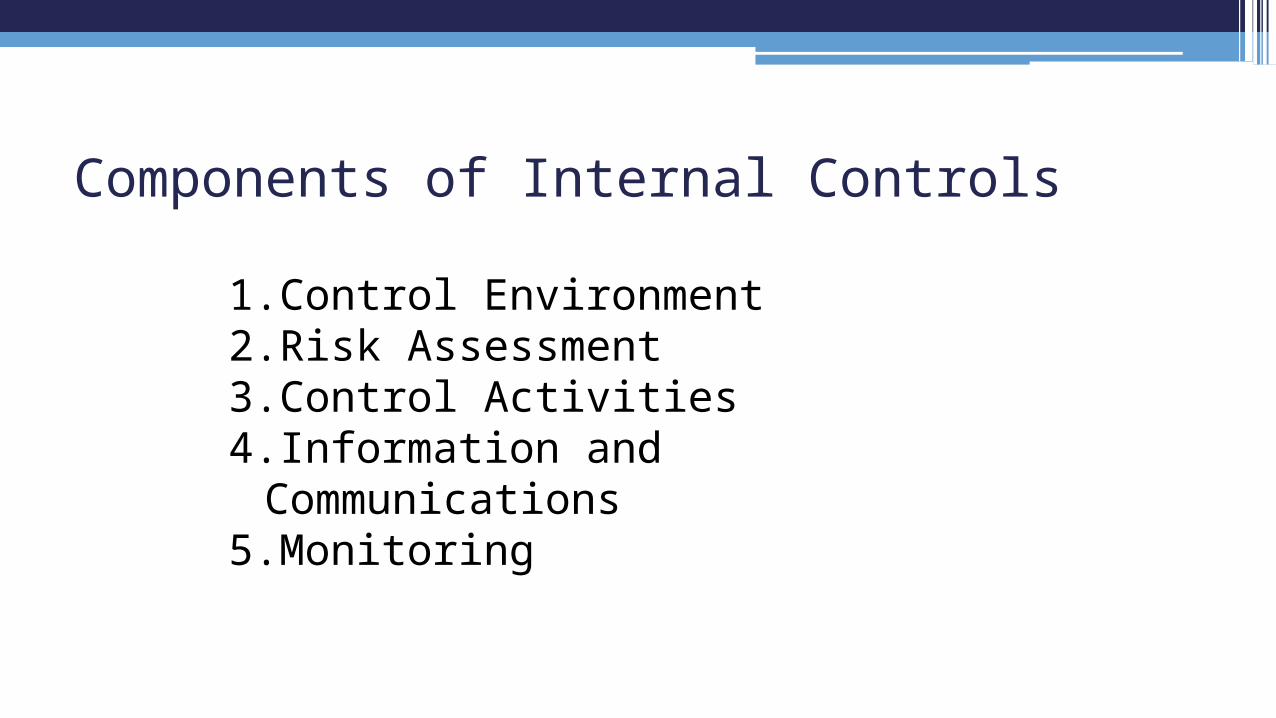

Components of Internal Controls

1.Control Environment2.Risk Assessment3.Control Activities4.Information and Communications5.Monitoring

Internal Controls – Control Environment

Goal: Sets the tone for the organization – allows management and employees to maintain a positive and supporting attitude toward compliance.

•Maintaining a level of competence that allows personnel to accomplish their assigned duties

•Clearly defined organizational structure•Proper amounts of supervision•Maintaining a good relationship with oversight agencies (like ED and OIG

for example!)

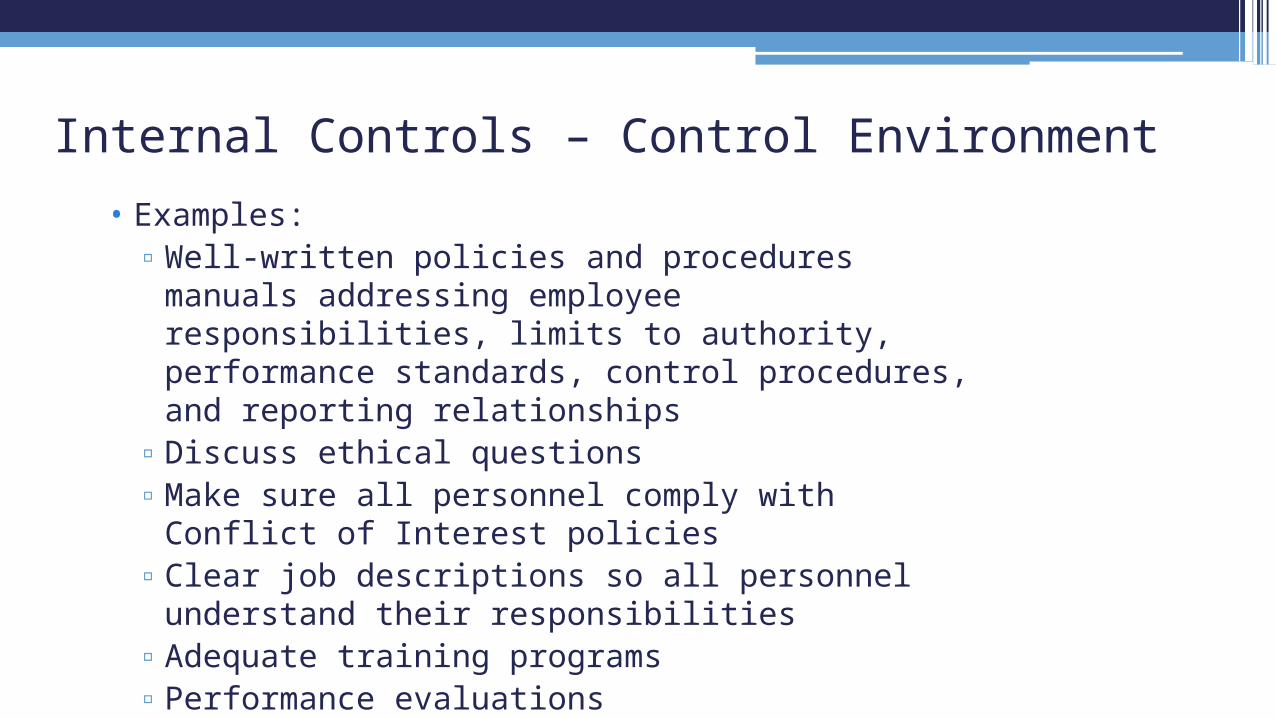

Internal Controls – Control Environment• Examples:▫Well-written policies and procedures manuals addressing

employee responsibilities, limits to authority, performance standards, control procedures, and reporting relationships

▫Discuss ethical questions▫Make sure all personnel comply with Conflict of Interest policies▫Clear job descriptions so all personnel understand their

responsibilities▫Adequate training programs▫Performance evaluations

Internal Controls – Risk AssessmentEvery Agency Has Problems and Risks!•Establish clear and consistent objectives ▫Operation objectives – pertain to achievement of

efficiency of operations, performance standards and safeguarding resources.

▫Financial reporting objectives – pertain to preventing fraudulent financial reporting.

▫Compliance objectives – pertain to adherence with applicable laws and regulations.

Internal Controls – Risk Assessment• Determine internal and external risks to obtaining those

objectives:▫What could go wrong?▫What assets do we need to protect?▫How could someone steal or disrupt operations?▫What information do we rely on?

• Examples:▫Changes in operating environment▫New personnel▫New or updated information systems or technology▫Rapid growth▫New programs, activities or grants▫ Lack of personnel

Internal Controls – Control ActivitiesGoal: Help ensure that management’s directives are carried

out • Examples:▫Segregating Key Responsibilities Among Different

People▫Restricting Access to Systems and Records

Authorizations / Passwords▫ Implementing Clear Written Policies in Key Areas▫Performance Reviews▫Maintaining Physical Control Over Valuable Assets

Maintenance of Security

Internal Controls – Control Activities•Examples▫Maintaining Appropriate Documentation

Approvals Record Retention

▫Data System Checks Check for accounting of transactions in numerical sequence.

▫Accurate and Timely Recording of Information

Internal Controls – Information and Communications

Goal: Ensure personnel receive relevant, reliable and timely information that enables them to carry out their responsibilities.

• Develop procedures for identifying pertinent information and distributing it in a form and timeframe that permits people to perform their duties efficiently.

• All personnel must receive a clear message from top down that control responsibilities must be taken seriously.

• Personnel must understand how they relate to one another in the system.

Internal Controls – Monitoring Goal: Assess the quality of internal controls over time

and ensure any findings are promptly resolved.• Ongoing program and fiscal monitoring • Regular oversight by supervisors• Record reconciliation• Formal program reviews / audits• OMB Circular A-133 audits

• Include policies and procedures for correcting any findings in a timely manner.

Always Follow Your Plan

District-level planSchool-level planModifications

• In order to receive Title I funds, LEAs must file a plan with SEA and obtain SEA approval. ▫Federal requirements in Section 1112 of ESEA.▫SEAs may require additional information

• LEA plan must be coordinated with other programs and services▫IDEA, Perkins, McKinney-Vento, Head Start, etc.

• LEA plan developed in consultation with teachers, administrators, parents, and other stakeholders

LEA Plan

•Consolidated Planning▫Permitted for most ESEA programs

•Consolidated Administration (ESEA, Section 9203)▫SEA approval

LEA Plan (cont)

•Allowability of costs▫E.g. Philly Audit: Costs disallowed because budget office moved

costs to federal funds without telling program office (inconsistent with plan – did not have necessary documentation)

•Modification to plan / budget may require prior approval▫See EDGAR 80.30 / Omni Circular 200.308

Why is LEA Plan important?

•Programmatic changes that require prior approval▫Revision of scope or objective (even if no budget revision)▫Need to extend period of availability of funds▫Changes in “key personnel” (specified in application or grant award)▫Contracting out, subgranting or otherwise obtaining services of a third

party “to perform activities which are central to purposes of the award”•Budget changes that require prior approval▫Additional funding needed▫Transfers among direct cost categories exceeding 10 % of budget or $100k

** SEA may impose additional modification requirements

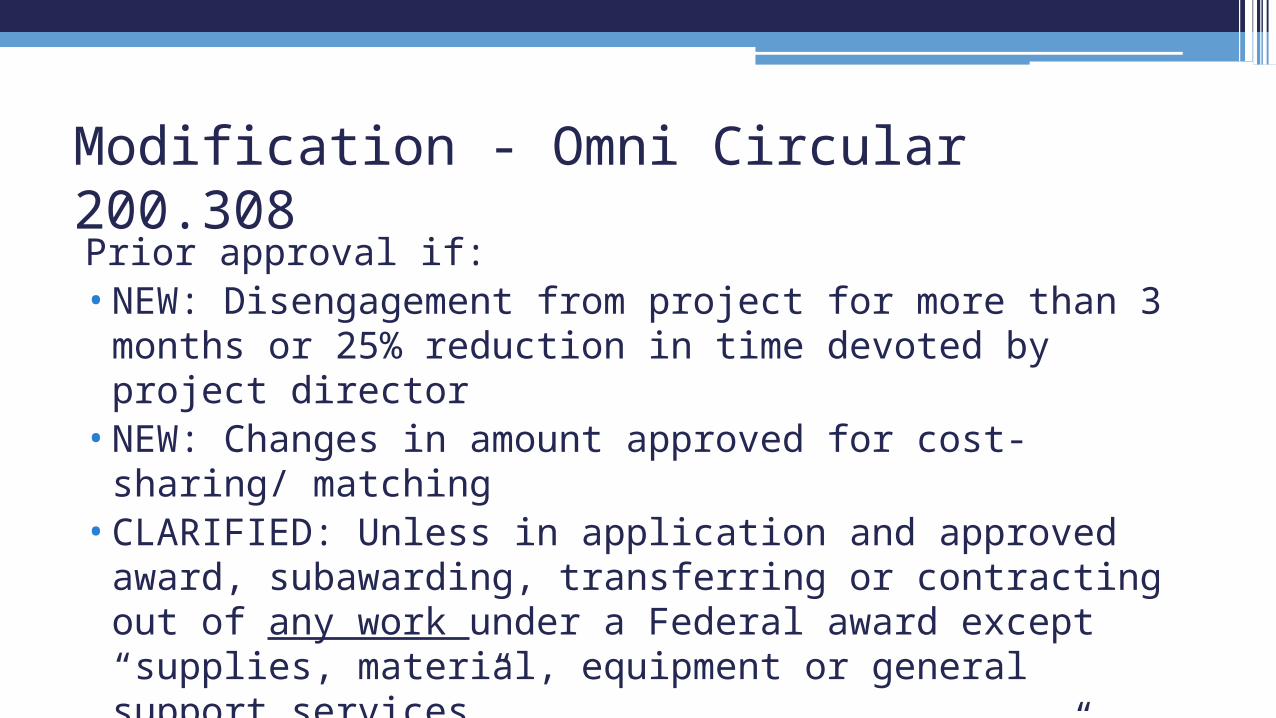

Modification (current rule, EDGAR 80.30)

Prior approval if:•NEW: Disengagement from project for more than 3 months or 25%

reduction in time devoted by project director•NEW: Changes in amount approved for cost-sharing/ matching•CLARIFIED: Unless in application and approved award, subawarding,

transferring or contracting out of any work under a Federal award except “supplies, material, equipment or general support services”

•CLARIFIED: Fed agency “may, at its option,” restrict transfer of funds across direct costs if exceeds 10% of budget or $150k

Modification - Omni Circular 200.308

•Targeted Assistance Program

Vs.

•Schoolwide Program

School level planning

1) Comprehensive Needs Assessment2) Plan3) Annual evaluation

56

Schoolwide Planning Requirements

Components of the SW Plan 1)Identify reform strategies, aligned with the needs assessment, that are

research-based and provide opportunities for all children to meet the State’s proficient or advanced levels of academic achievement;

2) Provide instruction by highly qualified teachers;

3) Offer high-quality, ongoing professional development;

4) Create strategies to attract highly qualified teachers;

5) Create strategies to increase parental involvement;

57

5) Develop plans to assist preschool students through the transition from early childhood programs to local elementary school programs;

6) Identify measures to include teachers in decisions regarding the use of academic assessments;

7) Conduct activities to ensure that students who experience difficulty attaining proficiency receive effective, timely, additional assistance; and

8) Coordinate and integrate Federal, State and local services and programs. Identify what funding sources are being consolidated

58

When In Doubt – Compete!

Procurement and the Importance of Competition

•All procurement transactions must be conducted in a manner providing full and open competition.▫34 CFR 80.36(c)

•Examples of restricting competition:▫Placing unreasonable requirements on vendors to qualify▫Requiring unnecessary experience and excessive bonding▫Specifying only a brand name product

Not allowing “an equal” product ▫In-state or local preferences

•Must have protest procedures in place to handle disputes

Full and Open Competition

Selecting a Vendor

61

•Can only contract with responsible contractors possessing the ability to perform successfully.

•Consider:▫Contractor integrity▫Compliance with public policy▫Record of past performance▫Financial and technical resources

•Soliciting proposals from only 1 source •Sole sourcing allowed only when:▫Item is available from only one source▫Public exigency or emergency▫Awarding agency authorizes it▫After solicitation of a number of sources, competition is deemed

inadequate

Noncompetitive Proposals

Noncompetitive Proposal

63

•As a practical matter, noncompetitive contract raises “red flags”▫Ensure persuasive and

adequate documentation to facilitate audit

Conflict of Interest • Must maintain written standard of conduct, including conflict of interest

policy.• A conflict of interest arises when any of the following has a financial or

other interest in the firm selected for award:▫Employee, officer or agent▫Any member of that person’s immediate family▫That person’s partner▫An organization which employs, or is about to employ, any of the

above or has a financial interest in the firm selected for award

64

• Include:▫Definition▫Chain for reporting potential conflicts

Alternative if reporting to employee involved in potential conflict▫Training▫Signed form attesting to receiving and understanding conflicts policy

Conflicts of Interest – Policies & Procedures

Know Where Your Inventory Is

67

Inventory Management•Different rules for equipment and supplies•Equipment▫Federal definition of equipment

Tangible personal property Useful life of more than one year Acquisition cost of $5,000 or more

▫May use own definition as long as it includes all property described above

Inventory Management

68

•Must have adequate controls in place to account for:▫ Location of equipment▫ Custody of equipment▫ Security of equipment

•34 CFR 80.32

Inventory Management

69

•Must have inventory management system▫Property records

Description, serial number or other ID, title info, acquisition date, cost, percent of federal participation, location, use and condition, and ultimate disposition

▫Physical inventory At least every 2 years Many states require it yearly

▫Control system to prevent loss, damage, theft All incident must be investigated!

Inventory Management

70

•When property no longer needed, must follow disposition rules:▫Transfer to another federal program▫Over $5,000 – Keep or sell, but must pay ED a share

based on percentage of federal ED participation in initial acquisition

▫Under $5,000 – May keep, sell, or dispose of it with no obligation to ED

Supplies71

•Supplies = Everything Else•EDGAR does not set out any specific tracking

requirements•But, as a practical matter, ED expects subgrantees to

track all property purchased with federal funds in order to prove there has been an allocable benefit to the federal program

• “Significant technological devices” and “Highly walkables”

• Omni Circular

▫Computing devices

Machines used to acquire, store, analyze, process, public data and other information electronically

Includes accessories for printing, transmitting and receiving or storing electronic information

Computing devices are supplies less than $5,000

Supplies

Keep Appropriate Time and Effort Documentation!

Time and Effort Rule

• If federal funds are used for salaries, then time distribution records are required.

• How staff demonstrate allocability• If employee paid in whole or in part with federal funds, then

must show employee worked on that specific federal program cost objective

• Used to meet a match/cost share requirement

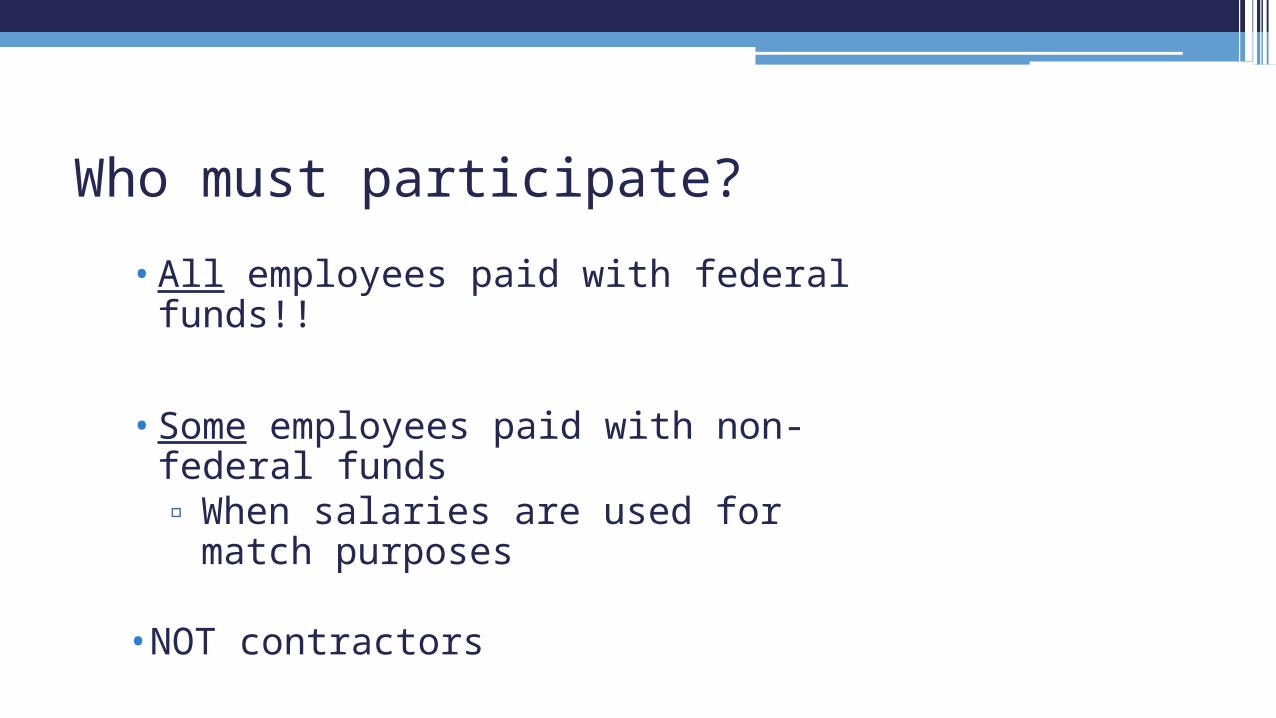

Who must participate?

•All employees paid with federal funds!!

•Some employees paid with non-federal funds▫ When salaries are used for match purposes

•NOT contractors

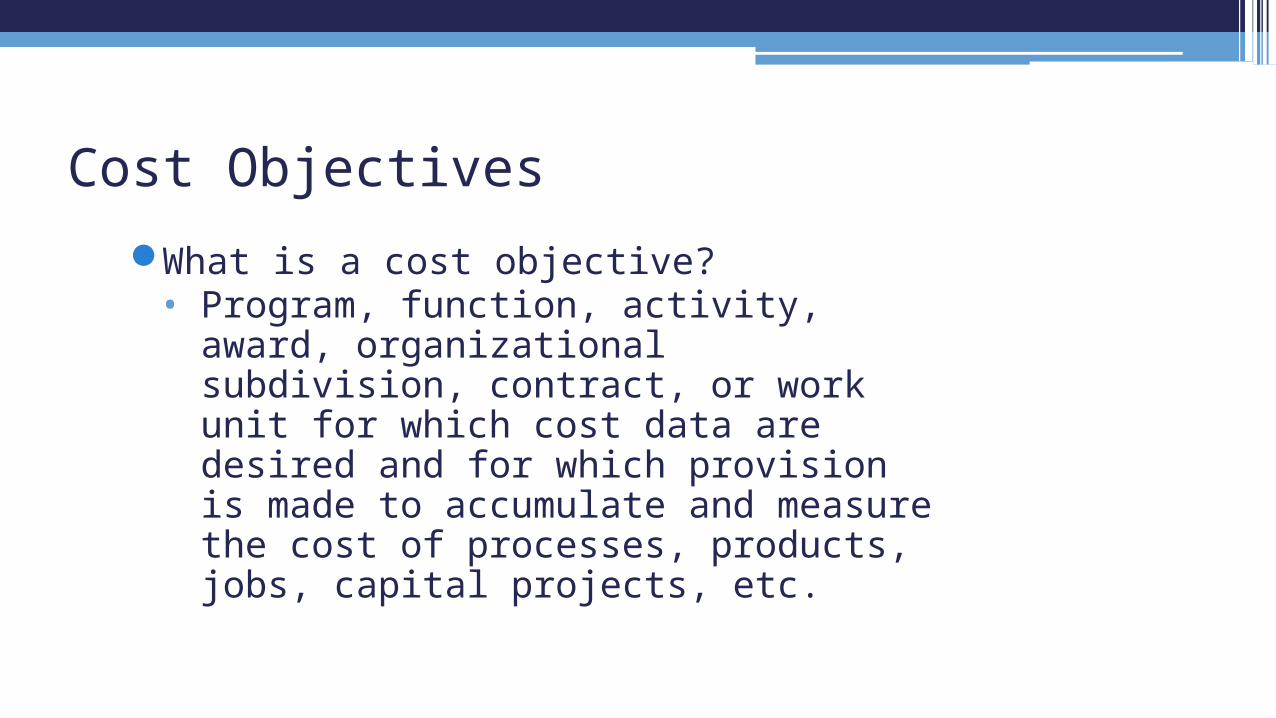

Cost Objectives

What is a cost objective?• Program, function, activity, award,

organizational subdivision, contract, or work unit for which cost data are desired and for which provision is made to accumulate and measure the cost of processes, products, jobs, capital projects, etc.

Does X employee have to keep time and effort records? Is she an employee?

Yes

Is she paid with federal funds?

Yes

T&E Required

No

Is her salary used for match?

No

No T&E Required

Yes

T&E Required

No

No T&E Required

I don’t know

Ask HR

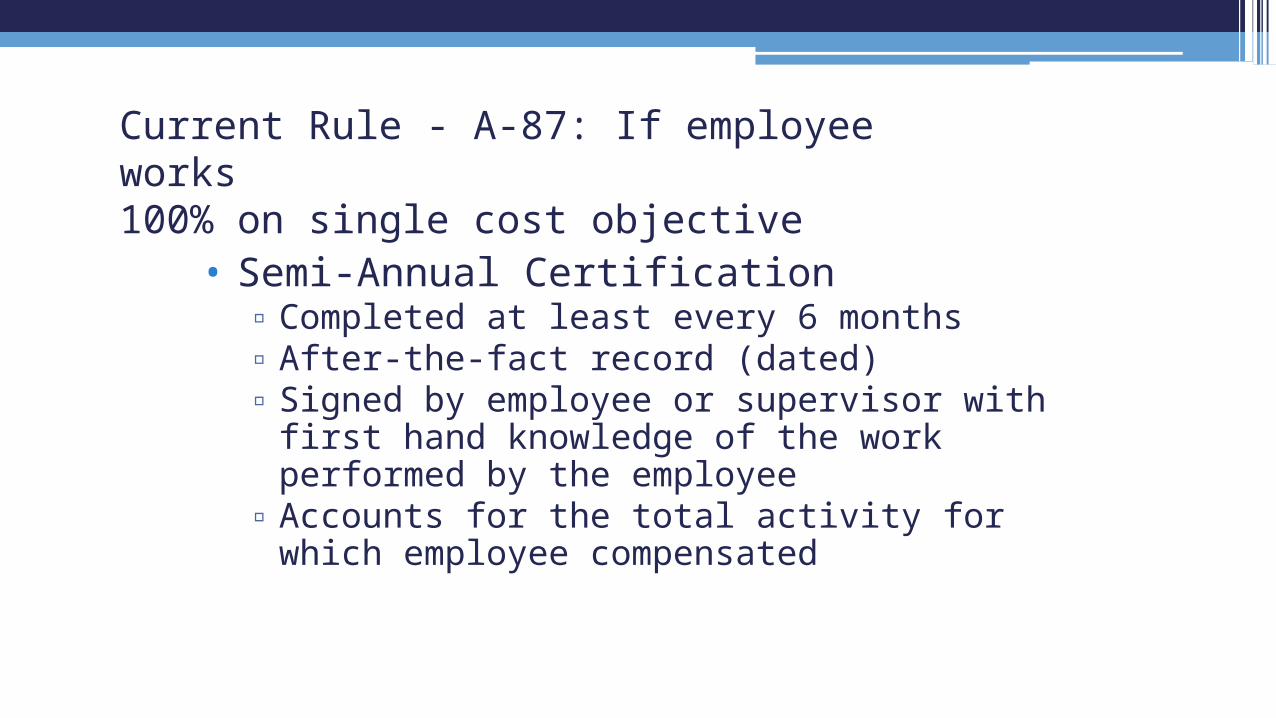

Current Rule - A-87: If employee works 100% on single cost objective

• Semi-Annual Certification▫ Completed at least every 6 months▫ After-the-fact record (dated)▫ Signed by employee or supervisor with first hand

knowledge of the work performed by the employee▫ Accounts for the total activity for which employee

compensated

Current Rule - A-87: If employee works 100% on single cost objective• Semi-Annual Certification

• “This is to certify that I, Blake Shelton, have worked 100% of my time for the period July 1, 2013 through December 31, 2013, on Title I Admin.”

Signature of employee: /s/Date: January 5, 2014

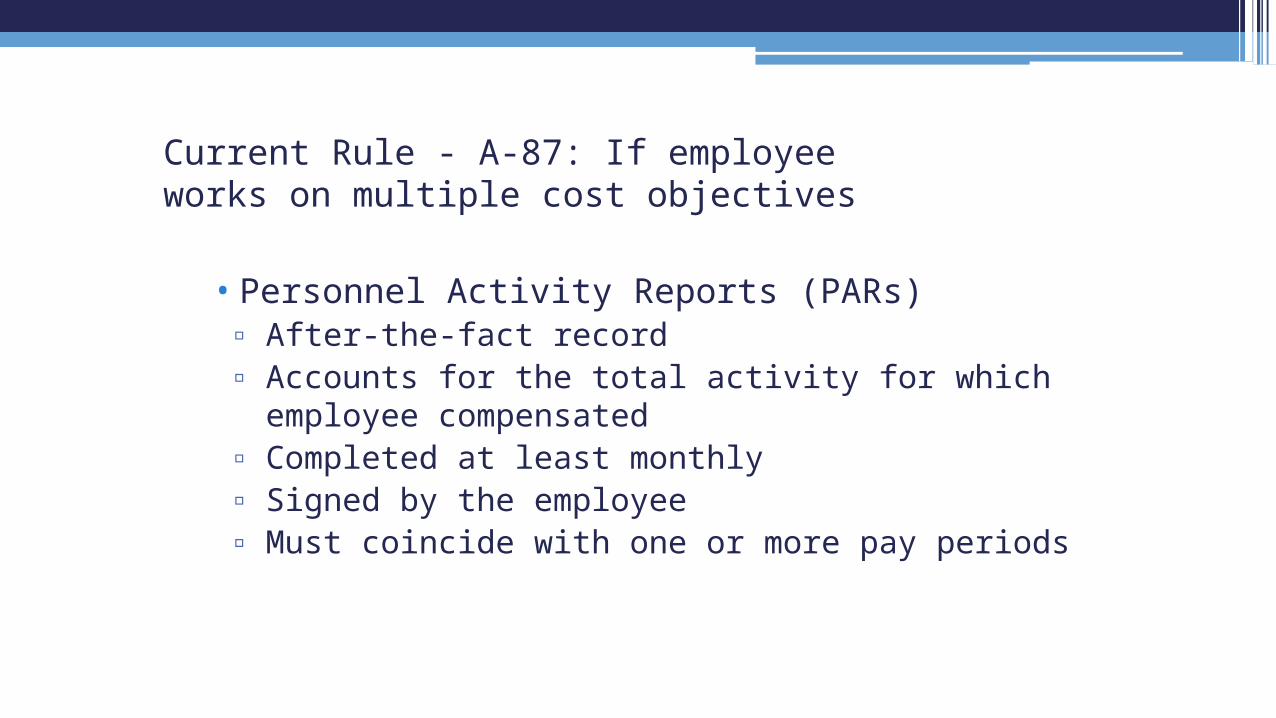

Current Rule - A-87: If employee works on multiple cost objectives

• Personnel Activity Reports (PARs)▫ After-the-fact record▫ Accounts for the total activity for which employee

compensated▫ Completed at least monthly▫ Signed by the employee▫ Must coincide with one or more pay periods

Current Rule - A-87: If employee works on multiple cost objectives

• Personnel Activity Reports (PAR)

• “For the month of August 2014, I, Miranda Lambert, spent my time 50% on Title I Program Services and 50% on non-federal programs.”

Signature of Employee: /s/Date: September 1, 2014

Examples: Right or Wrong?

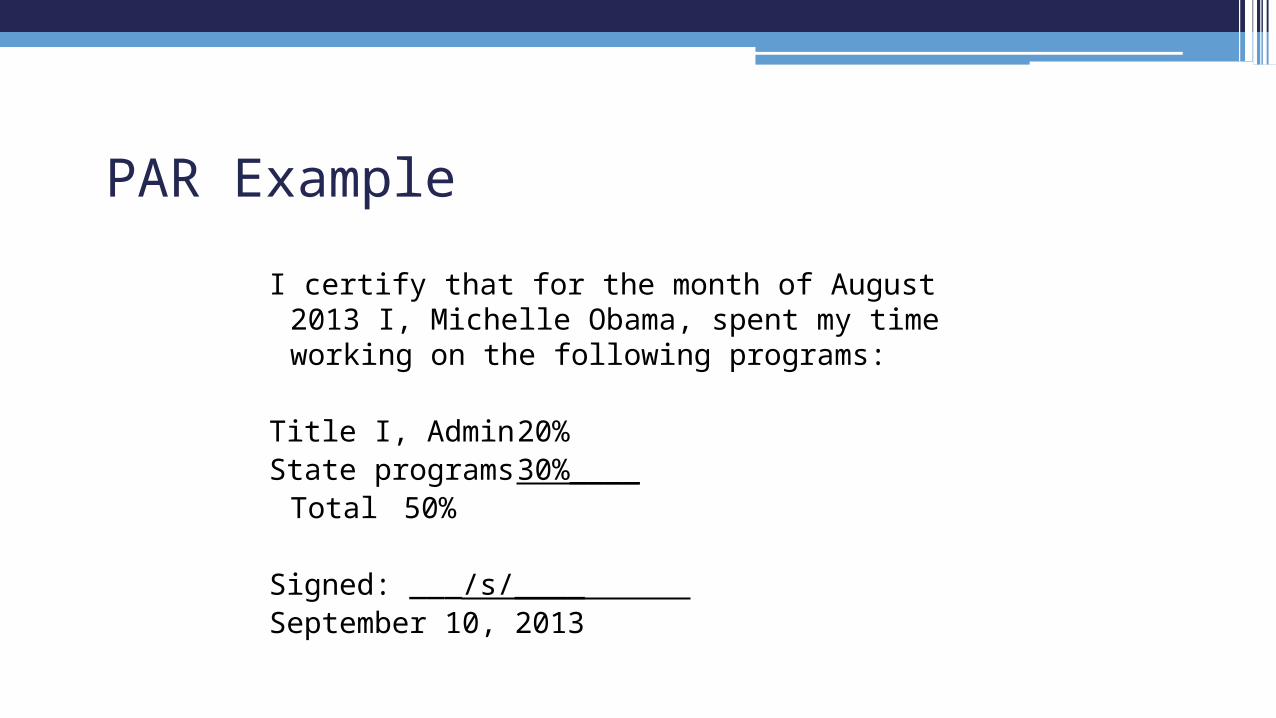

PAR Example

I certify that for the month of August 2013 I, Michelle Obama, spent my time working on the following programs:

Title I, Admin 20%State programs 30%____

Total 50%

Signed: ___/s/____ September 10, 2013

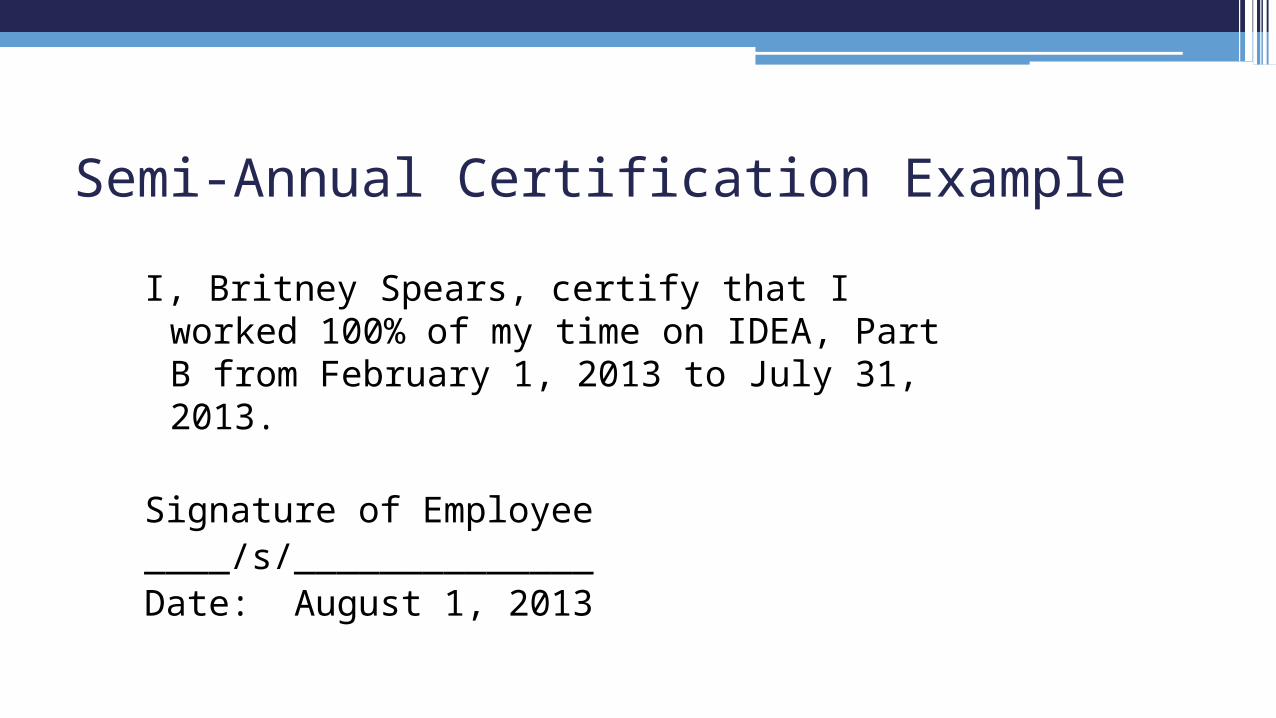

Semi-Annual Certification Example

I, Britney Spears, certify that I worked 100% of my time on IDEA, Part B from February 1, 2013 to July 31, 2013.

Signature of Employee ____/s/______________Date: August 1, 2013

Semi-Annual Certification Example

I, Taylor Swift, certify that I worked 100% of my time on Title I, Part A Administration from January 1, 2013 to June 30, 2013.

Signature of Employee ____/s/______________Date: June 20, 2013

Semi-Annual Certification

I certify that for the month of October 2013 I, Orlando Bloom, spent 60% of my time working on Title I, Admin.

I certify 100% that the above information is accurate.

Signed: ___/s/____ November 5, 2013

Beware of Supplanting!

Supplement not Supplant•Federal funds must be used to supplement

and in no case supplant (federal) state and local resources

“What would have happened in the absence of the federal funds???”

Auditors’ Tests for Supplanting

•OMB Circular A-133 Compliance Supplement

Auditors presume supplanting occurs if federal funds were used to provide services . . .

1. Required to be made available under other federal, state, or local laws

2. Paid for with non-federal funds in prior year

3. Same service to non-Title I students with state/local funds

Presumption Rebutted! If SEA or LEA demonstrates it

would not have provided services if the federal funds were not available

NO non-federal resources available this year!

What documentation needed?Fiscal or programmatic documentation to confirm

that, in the absence of federal funds, would have eliminated staff or other services in question

State or local legislative action

Budget histories and information

Must show:• Actual reduction in state or local funds

•Decision to eliminate service/position was made without regard to availability of federal funds (including reason decision was made)

Rebuttal Example•State supports a reading coach program

2012-2013•State cuts the program from State budget

2013-2014• LEA wants to support Title I reading coach

program 2013-2014

Rebuttal Example• LEA must document

a. State cut the programb. LEA does not have uncommitted funds available in

operating budget to pick upc. LEA would cut the program unless federal funds

picked it upd. The expense is allowable under Title I

QUESTIONS???

~ Legal Disclaimer ~

98

This presentation is intended solely to provide general information and does not constitute legal advice. Attendance at the presentation

or later review of these printed materials does not create an attorney-client relationship with Brustein & Manasevit. You should not take any action based upon any information in this presentation

without first consulting legal counsel familiar with your particular circumstances.