Embed Size (px)

Citation preview

Tiger Brands:Tiger Brands: Africa ExpansionAfrica Expansion

22 March 201122 March 2011

Neil Neil BrimacombeBrimacombe: : Executive DirectorExecutive Director

2

1.

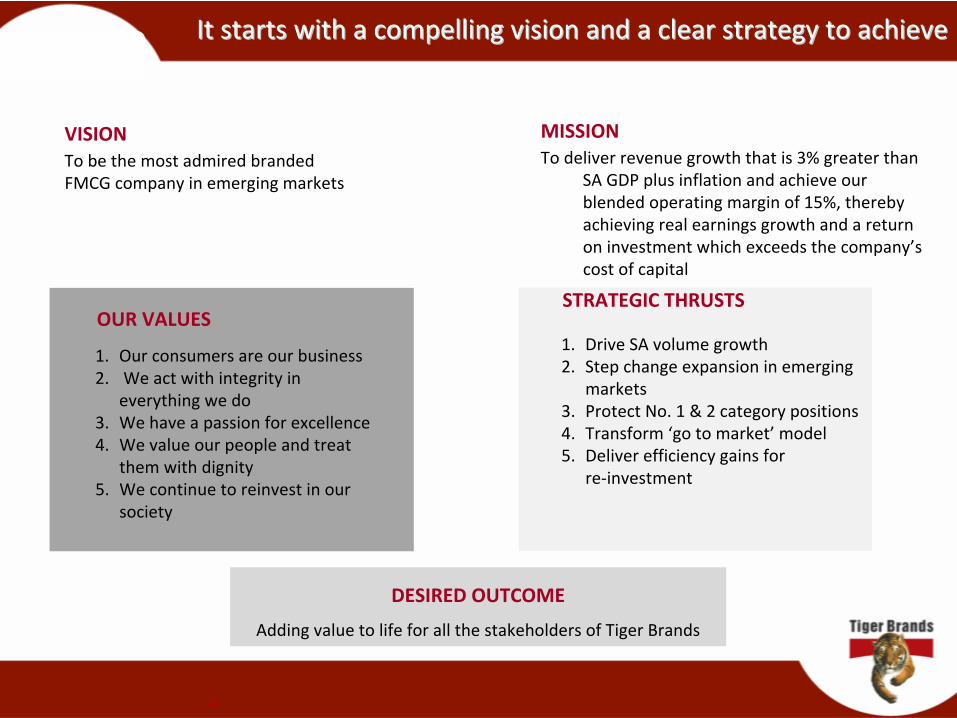

Drive SA volume growth2.

Step change expansion in emerging

markets

3.

Protect No. 1 & 2 category positions4.

Transform ‘go to market’

model 5.

Deliver efficiency gains for re‐investment

STRATEGIC THRUSTS

MISSION To deliver revenue growth that is 3% greater than

SA GDP plus inflation and achieve our

blended operating margin of 15%, thereby

achieving real earnings growth and a return

on investment which exceeds the company’s

cost of capital

1.

Our consumers are our business2.

We act with integrity in

everything we do

3.

We have a passion for excellence4.

We value our people and treat

them with dignity

5.

We continue to reinvest in our

society

OUR VALUES

DESIRED OUTCOME

Adding value to life for all the stakeholders of Tiger Brands

VISION To be the most admired branded FMCG company in emerging markets

It starts with a compelling vision and a clear strategy to achieIt starts with a compelling vision and a clear strategy to achieveve

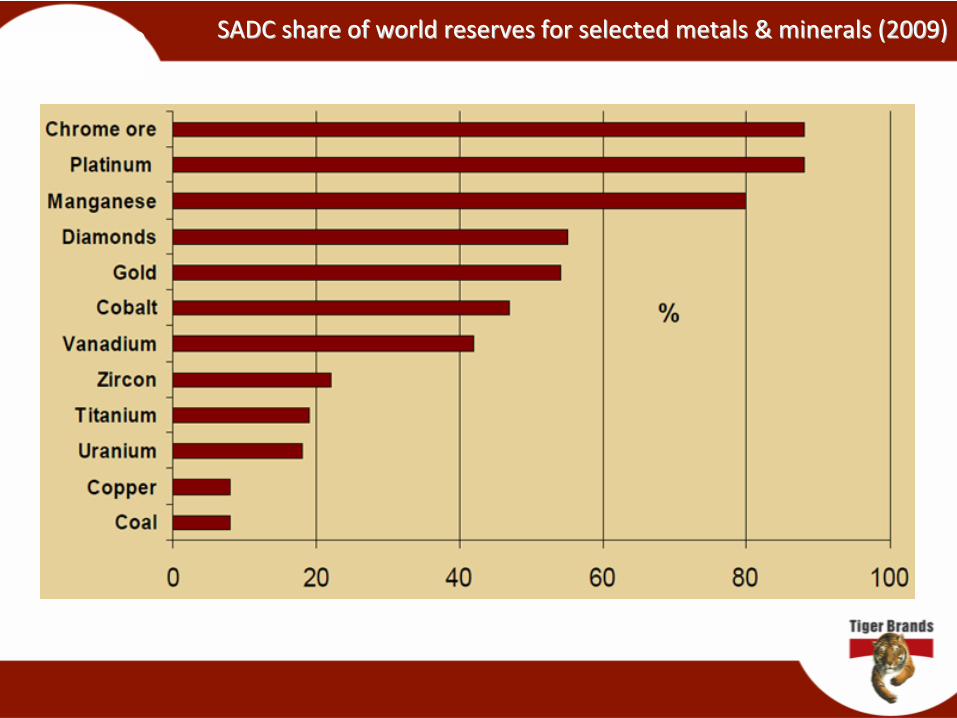

SADC share of world reserves for selected metals & minerals (200SADC share of world reserves for selected metals & minerals (2009)9)

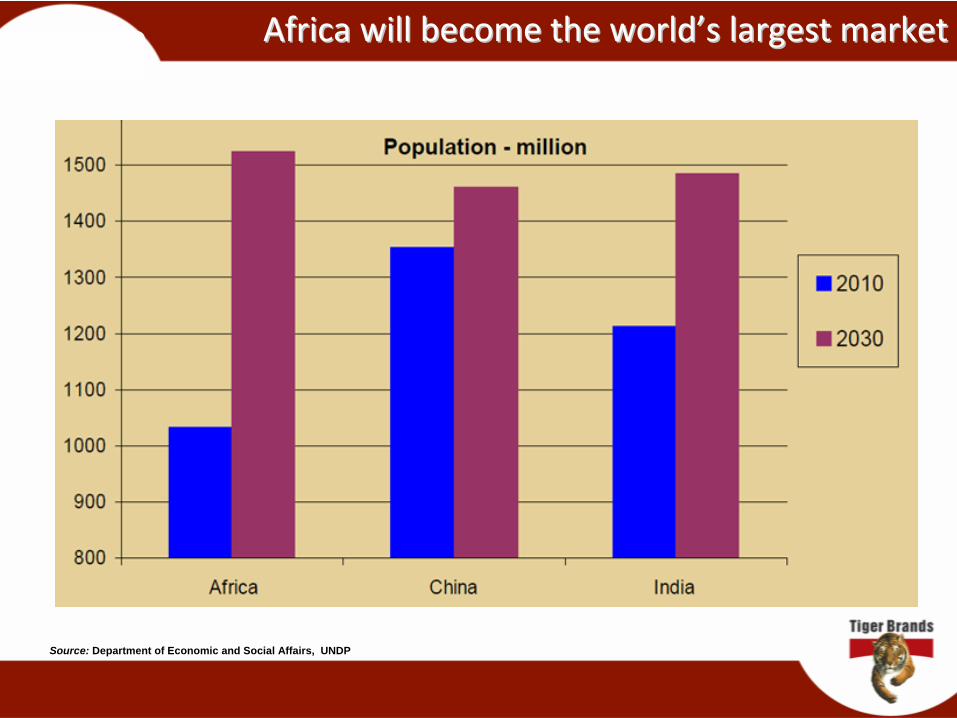

Africa will become the worldAfrica will become the world’’s largest markets largest market

Source: Department of Economic and Social Affairs, UNDP

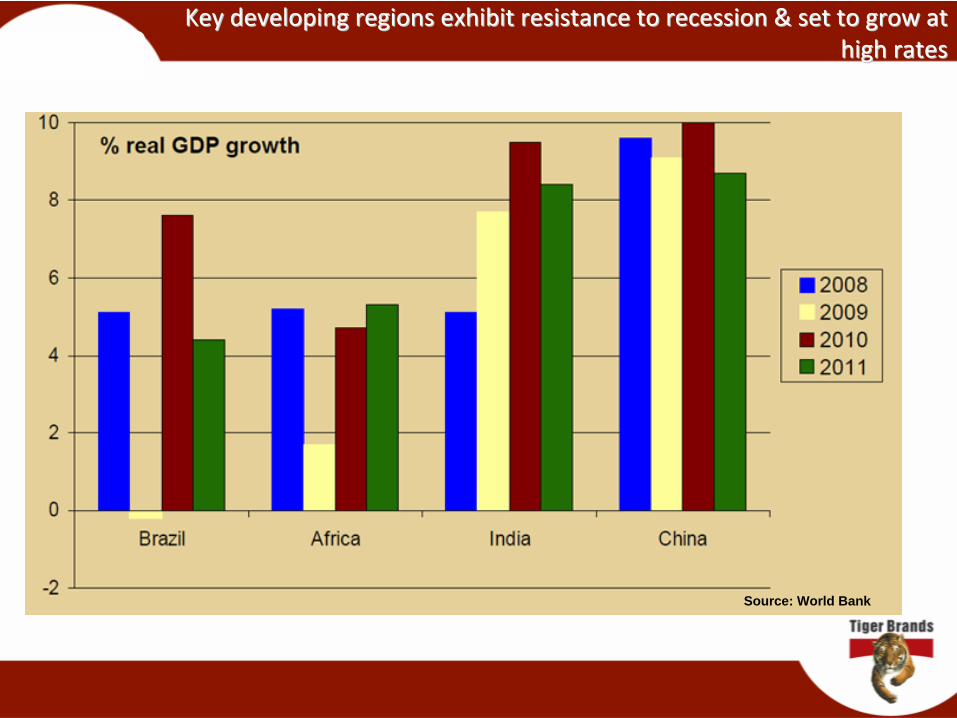

Key developing regions exhibit resistance to recession & set to Key developing regions exhibit resistance to recession & set to grow at grow at high rateshigh rates

Source: World Bank

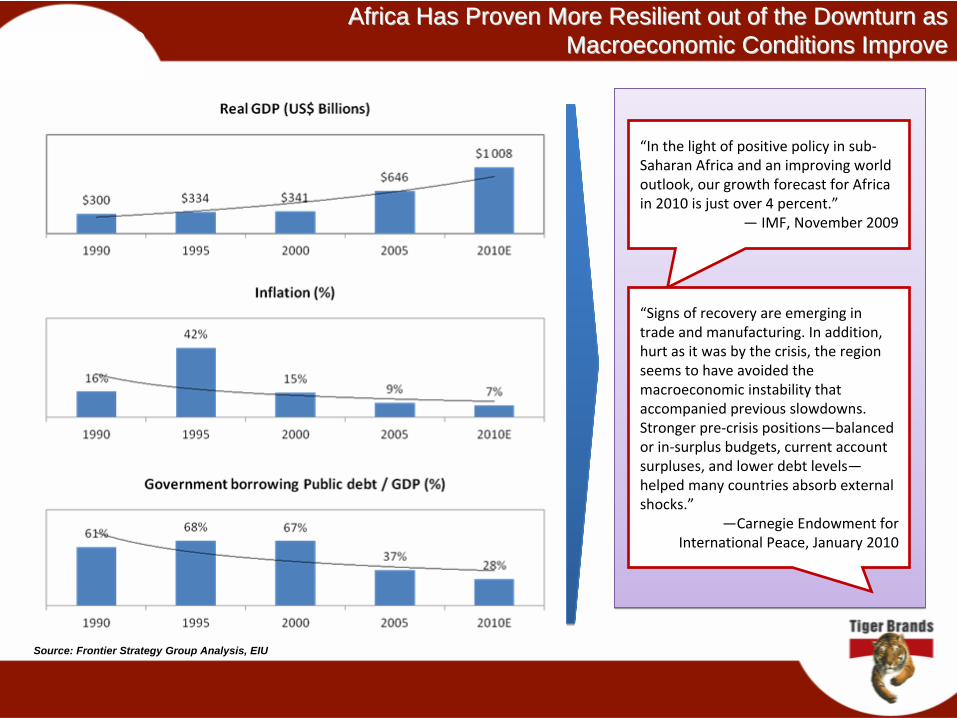

Africa Has Proven More Resilient out of the Downturn as Africa Has Proven More Resilient out of the Downturn as Macroeconomic Conditions ImproveMacroeconomic Conditions Improve

“In the light of positive policy in sub‐

Saharan Africa and an improving world

outlook, our growth forecast for Africa

in 2010 is just over 4 percent.”

— IMF, November 2009

“Signs of recovery are emerging in

trade and manufacturing. In addition,

hurt as it was by the crisis, the region

seems to have avoided the

macroeconomic instability that

accompanied previous slowdowns.

Stronger pre‐crisis positions—balanced

or in‐surplus budgets, current account

surpluses, and lower debt levels—

helped many countries absorb external

shocks.”

—Carnegie Endowment for

International Peace, January 2010

Source: Frontier Strategy Group Analysis, EIU

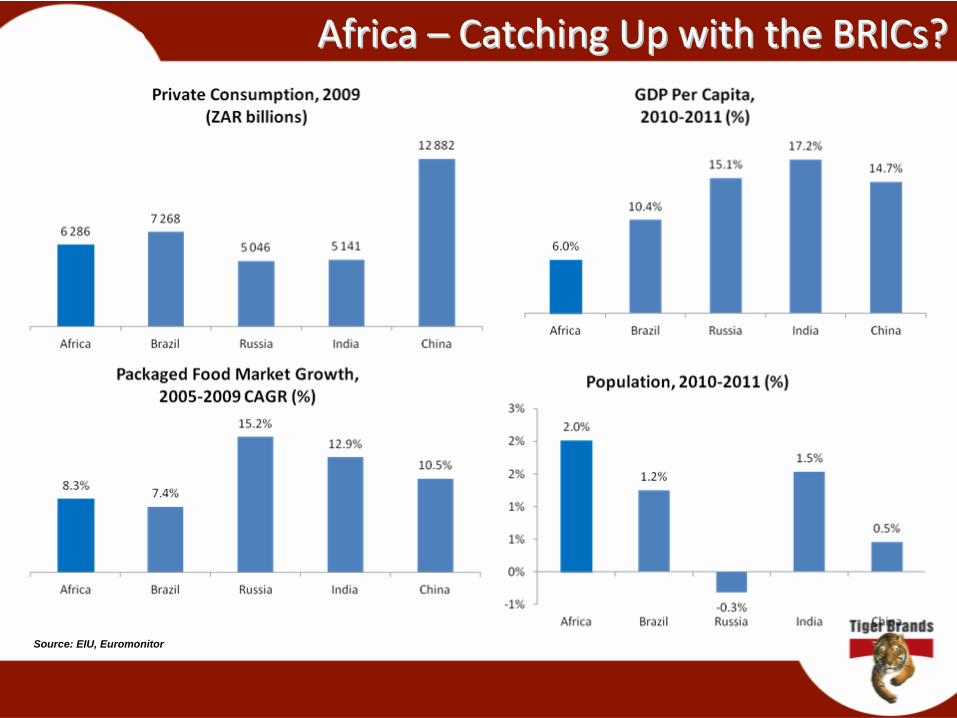

Africa Africa ––

Catching Up with the Catching Up with the BRICsBRICs??

Source: EIU, Euromonitor

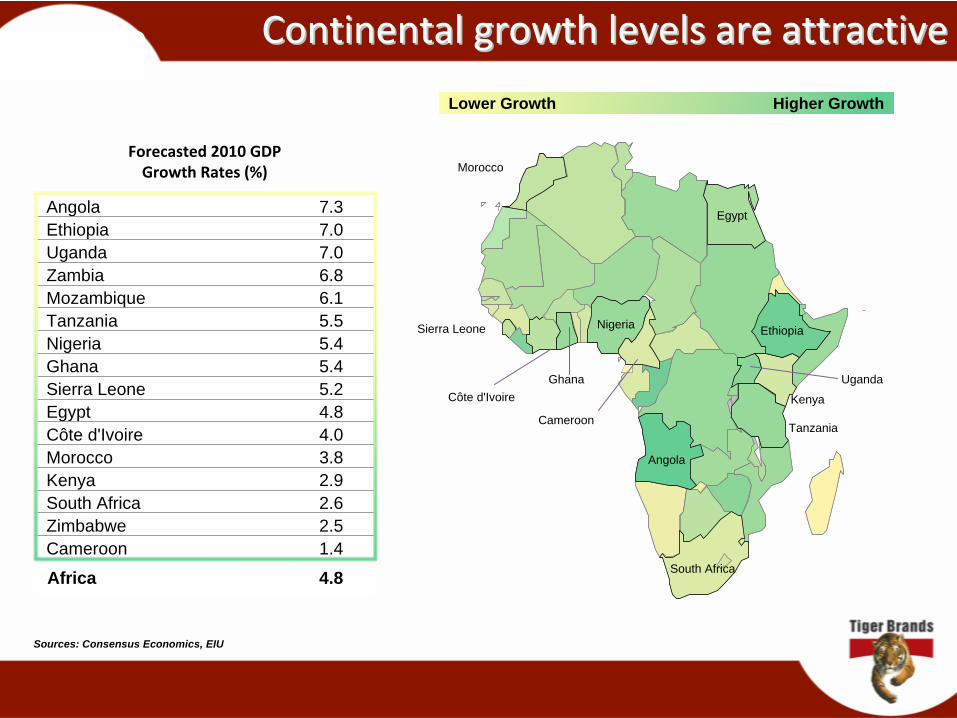

Continental growth levels are attractiveContinental growth levels are attractive

Sources: Consensus Economics, EIU

Lower Growth Higher Growth

Forecasted 2010 GDP Growth Rates (%)

Angola 7.3Ethiopia 7.0Uganda 7.0Zambia 6.8Mozambique 6.1Tanzania 5.5Nigeria 5.4Ghana 5.4Sierra Leone 5.2Egypt 4.8Côte d'Ivoire 4.0Morocco 3.8Kenya 2.9South Africa 2.6Zimbabwe 2.5Cameroon 1.4

Africa 4.8

Tanzania

Ethiopia

Uganda

Sierra Leone

Côte d'Ivoire

Cameroon

Kenya

Nigeria

Ghana

South Africa

Angola

Egypt

Morocco

Tiger Brands International: BackgroundTiger Brands International: Background

International expansion remains a key priority

Opportunity zones well understood

Our engagement in the markets has built real competencies

We continue to resource appropriately

Built on experience gained over the last 3 years

Our Priority Zones Our Priority Zones ––

no changes and focus remainsno changes and focus remains

BackgroundBackground

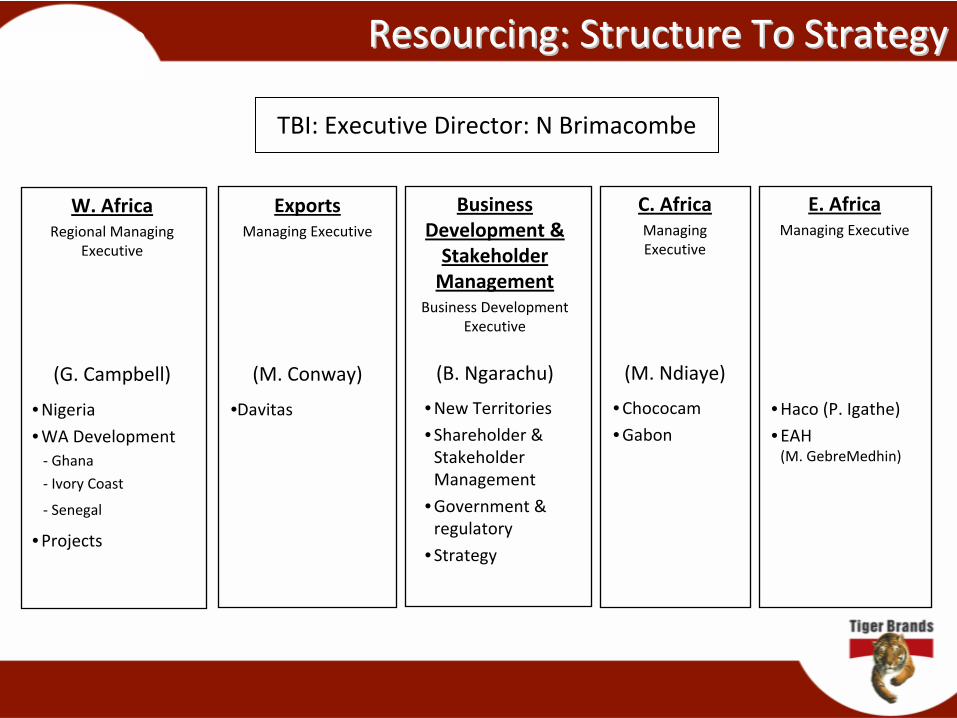

TBI: Executive Director: N Brimacombe

W. AfricaRegional Managing

Executive

(G. Campbell)

ExportsManaging Executive

(M. Conway)

Business

Development &

Stakeholder

ManagementBusiness Development

Executive

(B. Ngarachu)

C. AfricaManaging

Executive

(M. Ndiaye)

E. AfricaManaging Executive

• Nigeria• WA Development‐

Ghana‐

Ivory Coast

‐

Senegal

• Projects

•Davitas • New Territories • Shareholder &

Stakeholder

Management

• Government &

regulatory

• Strategy

• Chococam• Gabon

• Haco (P. Igathe)• EAH

(M. GebreMedhin)

Resourcing: Structure To StrategyResourcing: Structure To Strategy

Tiger Brands: Africa Footprint* Our on shore presence * Our on shore presence ……

Ethiopia

Kenya

Nigeria

South Africa

Zimbabwe

Cameroon

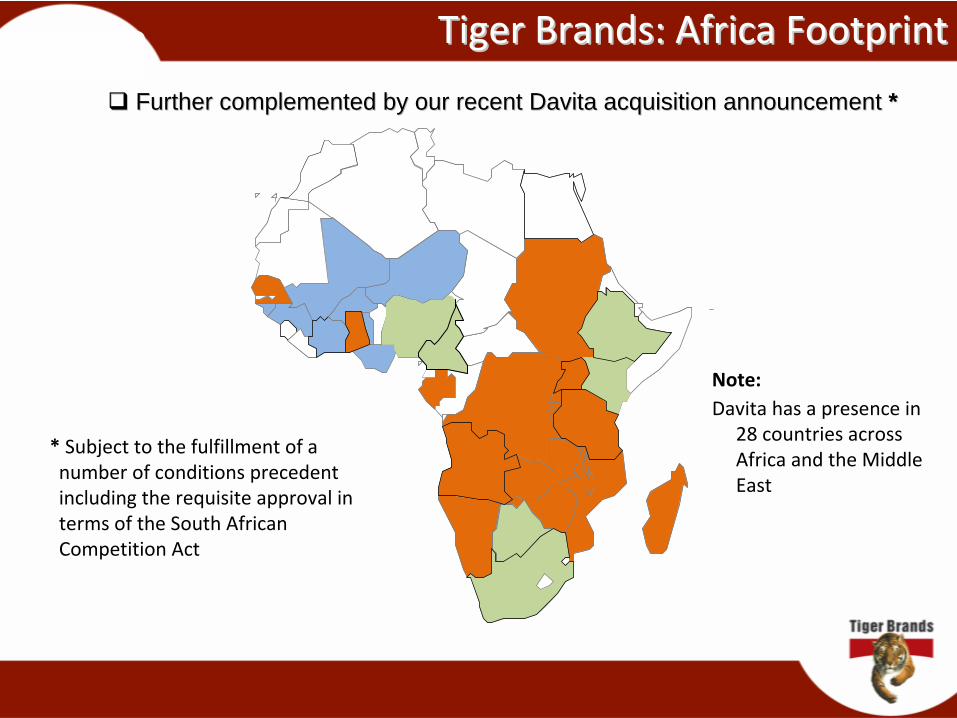

Tiger Brands: Africa FootprintTiger Brands: Africa Footprint

* Complemented by our export footprint* Complemented by our export footprint

Tiger Brands: Africa FootprintTiger Brands: Africa Footprint

Further complemented by our recent Davita acquisition announcemFurther complemented by our recent Davita acquisition announcement ent **

Note:Davita has a presence in

28 countries across

Africa and the Middle

East

*

Subject to the fulfillment of a

number of conditions precedent

including the requisite approval in

terms of the South African

Competition Act

14

HACO Industries (Kenya)HACO Industries (Kenya)

Brands

•BIC•Miadi•Motions•SoSoft•Jeyes•Palmer’s•TCB Naturals

2010

•Sales:

R189.5m•EBIT:

R20.1m

•Margin:

11%

Categories

•Stationary•Hair Care•Skin Care•Fabric Softeners•Bleach•Toilet Cleaners

15

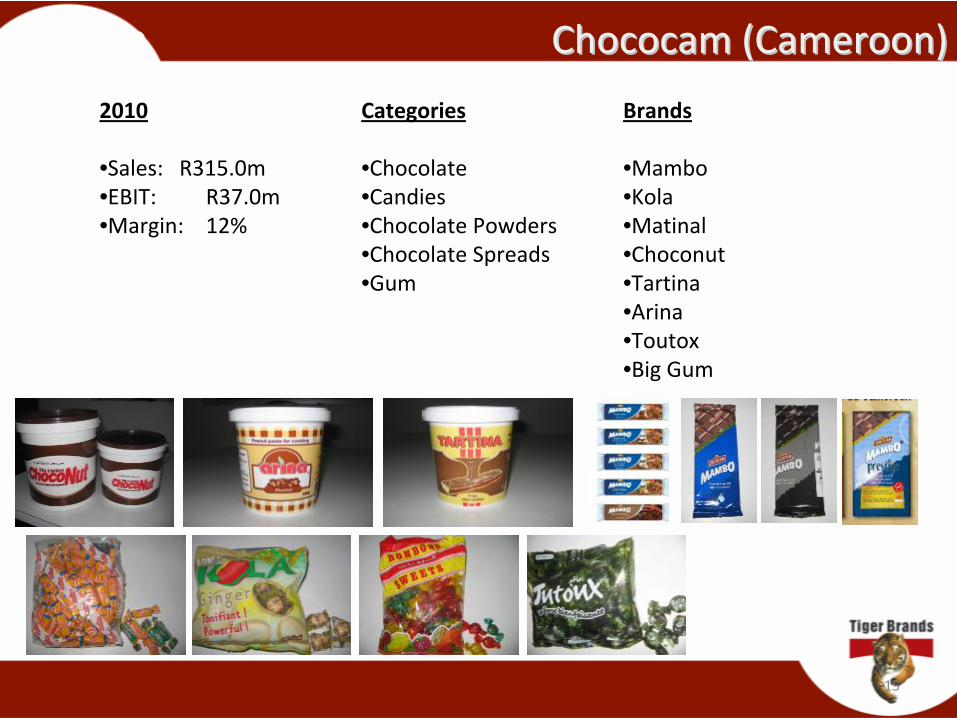

Chococam (Cameroon)Chococam (Cameroon)Brands

•Mambo•Kola•Matinal•Choconut•Tartina•Arina•Toutox•Big Gum

2010

•Sales:

R315.0m•EBIT:

R37.0m

•Margin:

12%

Categories

•Chocolate•Candies•Chocolate Powders•Chocolate Spreads•Gum

16

East Africa Tiger Brands Industries (Ethiopia)East Africa Tiger Brands Industries (Ethiopia)

Categories

•Biscuits•Laundry Soap•Detergent Soap•Pasta •Flour

17

Deli Foods (Nigeria)

*

EATBI & Deli Foods are expected to generate a combined annual turnover of c. 500m in the first year

Categories

•Biscuits•Crackers•Wafers

18

UAC / Tiger Brands (Nigeria)UAC / Tiger Brands (Nigeria)

Brands

•Gala•Funtime Cake•Coconut Chips•Snaps•Supreme•Funblast•Delite•Swan

Categories

•Water•Ice Cream•Fruit Juices•Snacks•Flavoured Milk•Carbonated Soft Drinks

2009

(31/12)

Sales: c.450m

19

Davita Trading (South AfricanDavita Trading (South African‐‐Based Export Company)Based Export Company)

Brands

•Jolly Jus•Benny •Davita

Categories

•Powdered Juices•Powdered Seasonings

2010

(28/2)Sales: R567m*

Enterprise Value:

R1. 625bn

* 99% Exports

Framing an Investment Case for AfricaFraming an Investment Case for Africa

• PESTEL Discontinuities ‐

Managing the Vagaries

• Appetite for Risk (Beta factor)

• Our defensive qualities – Brands and Categories

• Investment in enabling capabilities and competencies

• Balancing the Portfolio

• Investment horizons

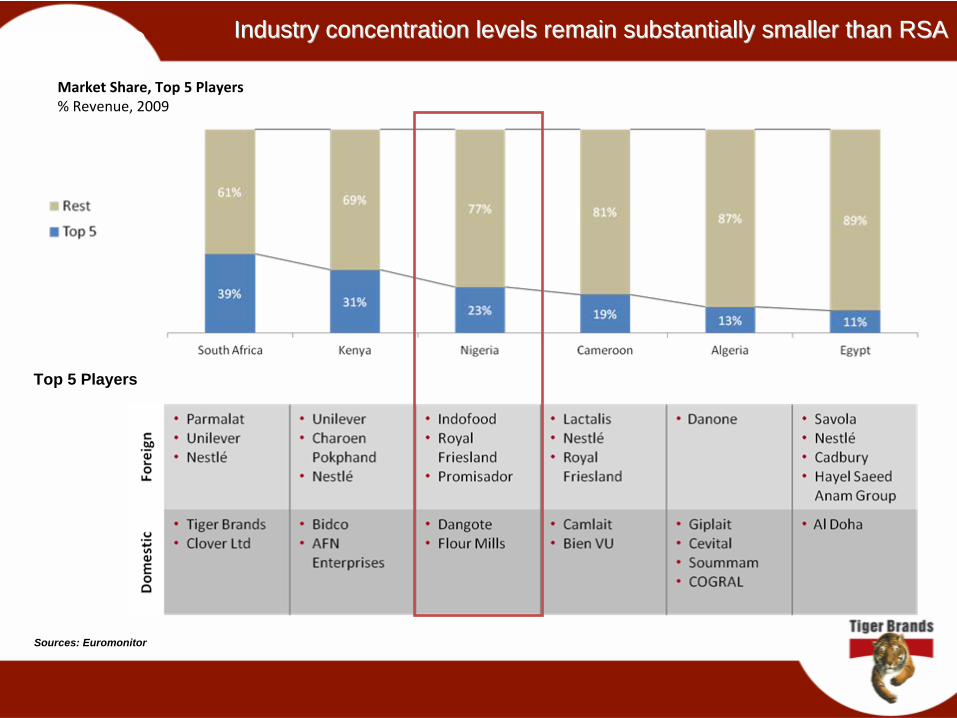

Industry concentration levels remain substantially smaller than Industry concentration levels remain substantially smaller than RSARSA

Sources: Euromonitor

Market Share, Top 5 Players% Revenue, 2009

Top 5 Players

Industry Consolidation increasing: Limited windowIndustry Consolidation increasing: Limited window

Source: Euromonitor

Total m

arket sha

re

%

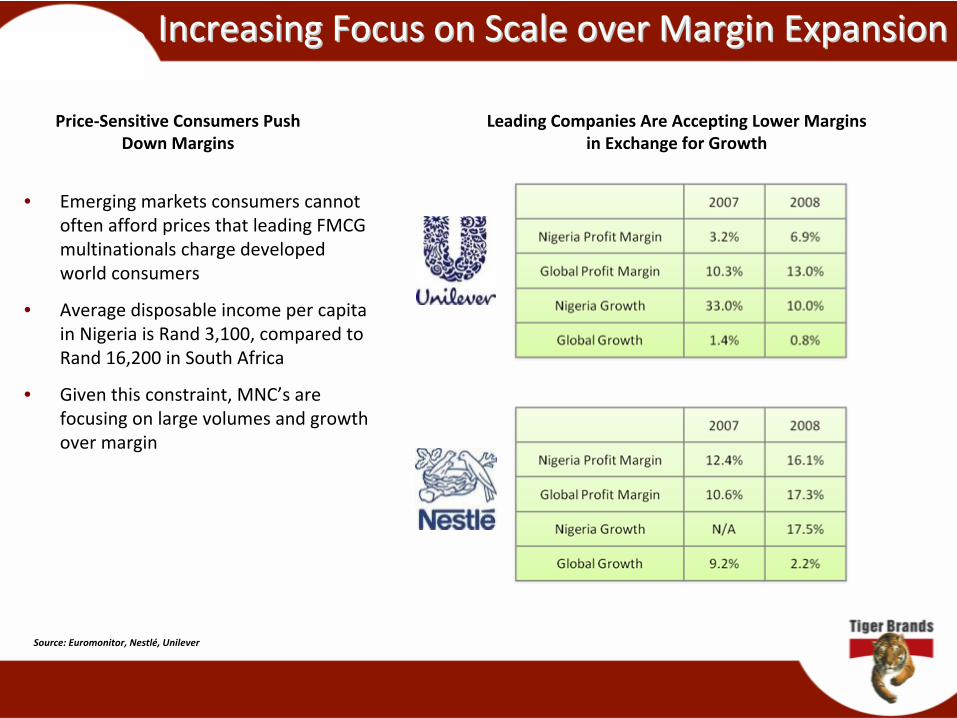

Increasing Focus on Scale over Margin ExpansionIncreasing Focus on Scale over Margin Expansion

• Emerging markets consumers cannot

often afford prices that leading FMCG

multinationals charge developed

world consumers

• Average disposable income per capita

in Nigeria is Rand 3,100, compared to

Rand 16,200 in South Africa

• Given this constraint, MNC’s are

focusing on large volumes and growth

over margin

Source: Euromonitor, Nestlé, Unilever

Leading Companies Are Accepting Lower Margins

in Exchange for Growth

Price‐Sensitive Consumers Push

Down Margins

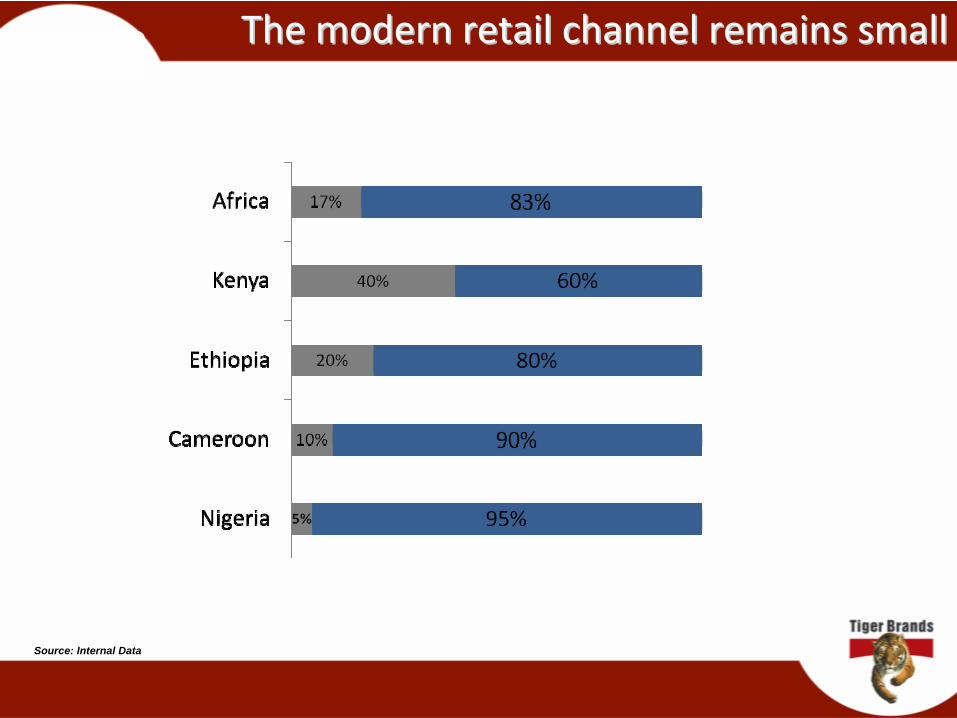

The modern retail channel remains smallThe modern retail channel remains small

Source: Internal Data

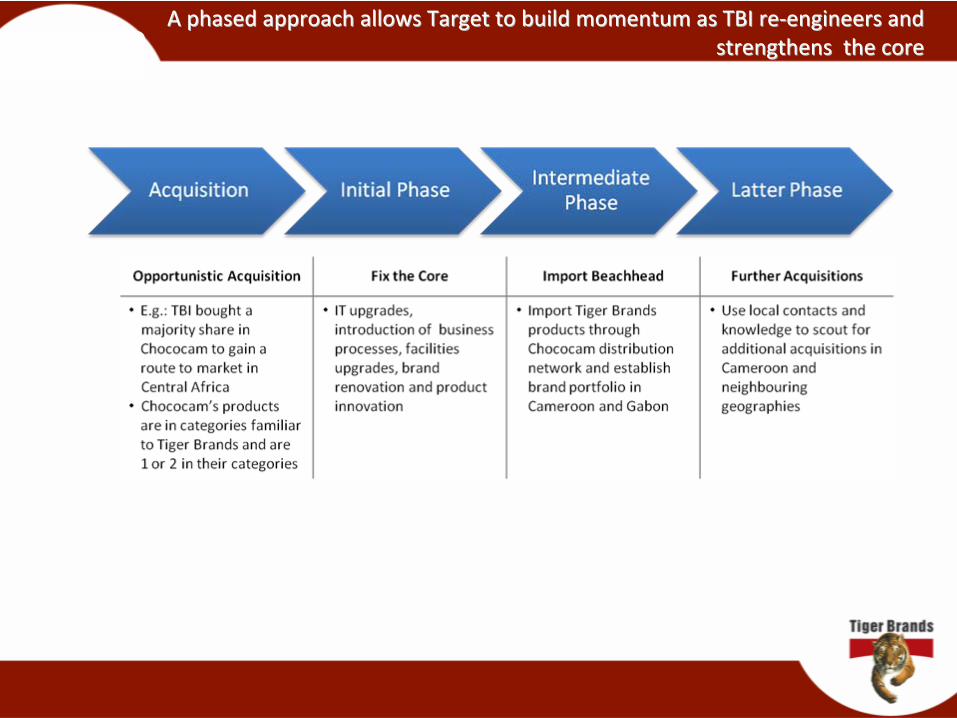

A phased approach allows Target to build momentum as TBI reA phased approach allows Target to build momentum as TBI re‐‐engineers and engineers and strengthens the corestrengthens the core

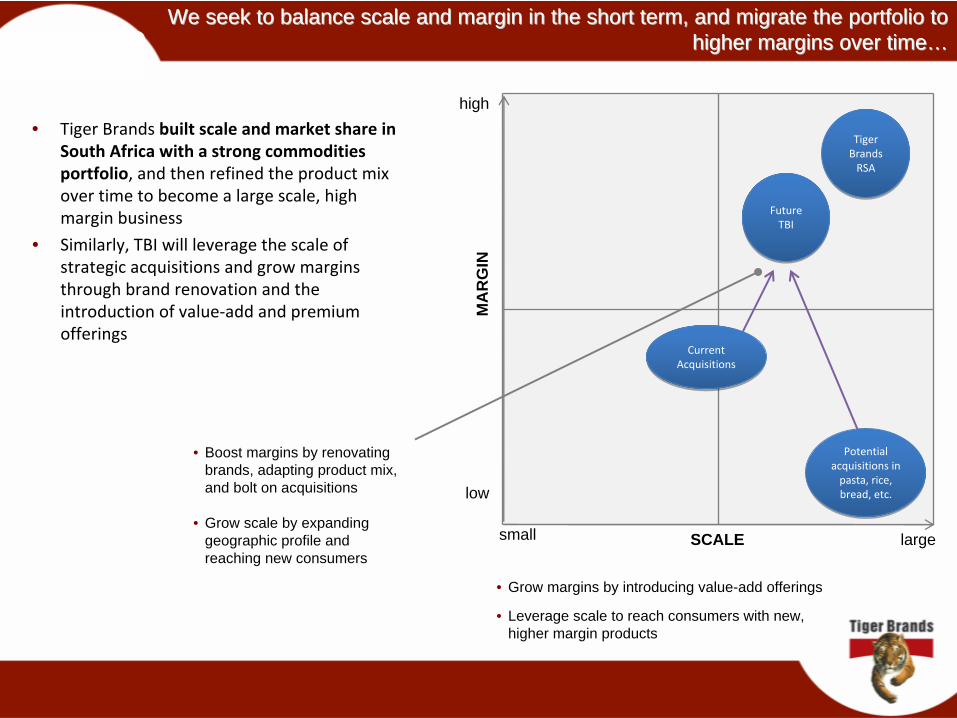

We seek to balance scale and margin in the short term, and migraWe seek to balance scale and margin in the short term, and migrate the portfolio to te the portfolio to higher margins over timehigher margins over time……

• Tiger Brands built scale and market share in

South Africa with a strong commodities

portfolio, and then refined the product mix

over time to become a large scale, high

margin business

• Similarly, TBI will leverage the scale of

strategic acquisitions and grow margins

through brand renovation and the

introduction of value‐add and premium

offerings

MA

RG

IN

SCALE largesmall

low

high

Current

Acquisitions

Current

Acquisitions

Potential

acquisitions in

pasta, rice,

bread, etc.

Potential

acquisitions in

pasta, rice,

bread, etc.

Tiger

Brands

RSA

Tiger

Brands

RSA

• Boost margins by renovating brands, adapting product mix, and bolt on acquisitions

• Grow scale by expanding geographic profile and reaching new consumers

• Grow margins by introducing value-add offerings

• Leverage scale to reach consumers with new, higher margin products

Future

TBI

Future

TBI

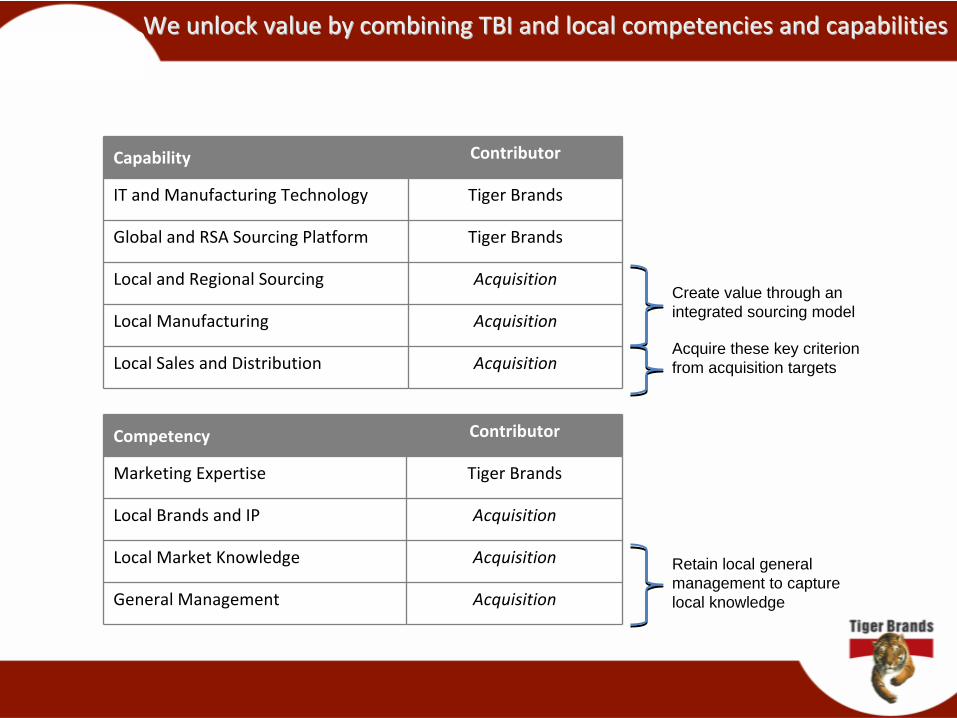

We unlock value by combining TBI and local competencies and capaWe unlock value by combining TBI and local competencies and capabilitiesbilities

Capability Contributor

IT and Manufacturing Technology Tiger Brands

Global and RSA Sourcing Platform Tiger Brands

Local and Regional Sourcing Acquisition

Local Manufacturing Acquisition

Local Sales and Distribution Acquisition

Competency Contributor

Marketing Expertise Tiger Brands

Local Brands and IP Acquisition

Local Market Knowledge Acquisition

General Management Acquisition

Create value through an integrated sourcing model

Retain local general management to capture local knowledge

Acquire these key criterion from acquisition targets

Brands that have regional appealBrands that have regional appeal

Tiger Brands Regional Brand Application

• Regional mother brands• Cross category evolution

Fix: Finished Goods WarehouseFix: Finished Goods WarehouseBefore

After

Fix: Fixed assets: KenyaFix: Fixed assets: Kenya

Fix: Power generation Fix: Power generation -- TransformersTransformers

NewOld

OldOld NewNew

Optimise Brand Renovation: Optimise Brand Renovation: MotionsMotions

Old New

Optimise Brand Migration: MamboOptimise Brand Migration: Mambo

Current

Tin Packaging

New

Plastic Container

with Shrink Sleeve

Optimise: Brand Renovation: MATINALOptimise: Brand Renovation: MATINAL

Purity Bill board – Nairobi

Engaging our consumers: Traditional mediaEngaging our consumers: Traditional media

Miadi promotion ‐

Uchumi North Rift road show

Engaging our consumers: NonEngaging our consumers: Non‐‐traditional mediatraditional media

Engaging our consumers: Kenya (Clinics)Engaging our consumers: Kenya (Clinics)

Beacon: In market samplingBeacon: In market sampling

Engaging our consumers: KenyaEngaging our consumers: Kenya

Engaging demand drivers: PaediatriciansEngaging demand drivers: Paediatricians

Annual Kenyan Paediatricians Conference

RTM Capability: CameroonRTM Capability: Cameroon

* Channel, occasion, format, pack* Channel, occasion, format, pack

Channel architecture and RTM capabilityChannel architecture and RTM capability

Strategic dealers

Streets Vendors

Boutiques or Convenience

Table TopKey Player in open market

Traditional trade, stores Traditional trade, stores and openand open--air marketsair markets

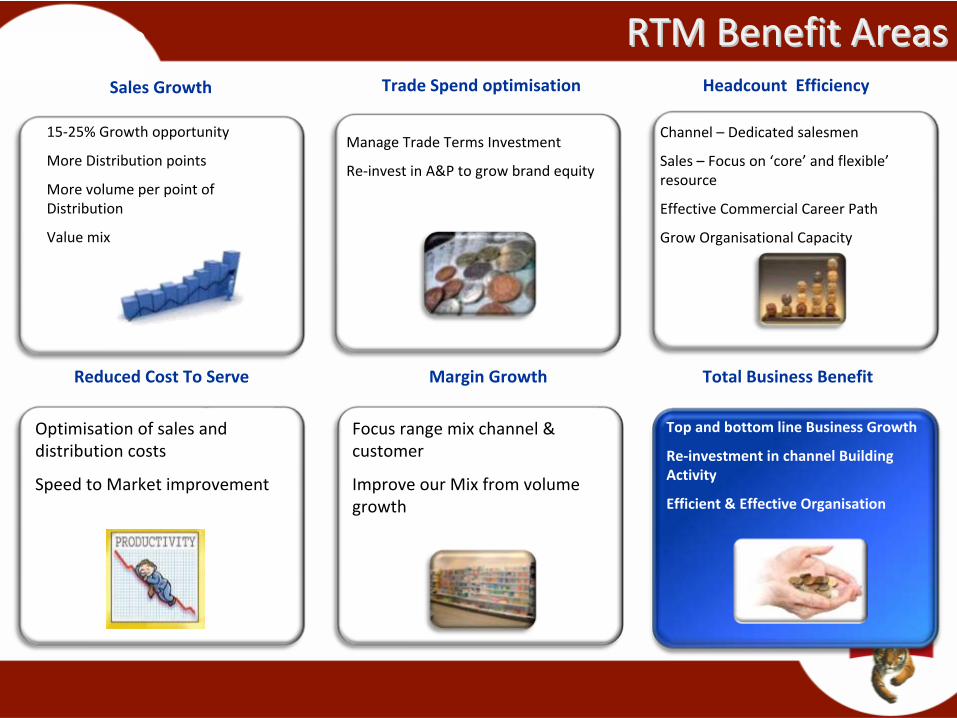

RTM Benefit AreasRTM Benefit AreasSales Growth Trade Spend optimisation Headcount Efficiency

Reduced Cost To Serve Margin Growth Total Business Benefit

Channel – Dedicated salesmen

Sales – Focus on ‘core’

and flexible’

resource

Effective Commercial Career Path

Grow Organisational Capacity

Manage Trade Terms Investment

Re‐invest in A&P to grow brand equity

Optimisation of sales and

distribution costs

Speed to Market improvement

Focus range mix channel &

customer

Improve our Mix from volume

growth

15‐25% Growth opportunity

More Distribution points

More volume per point of

Distribution

Value mix

Top and bottom line Business Growth

Re‐investment in channel Building

Activity

Efficient & Effective Organisation

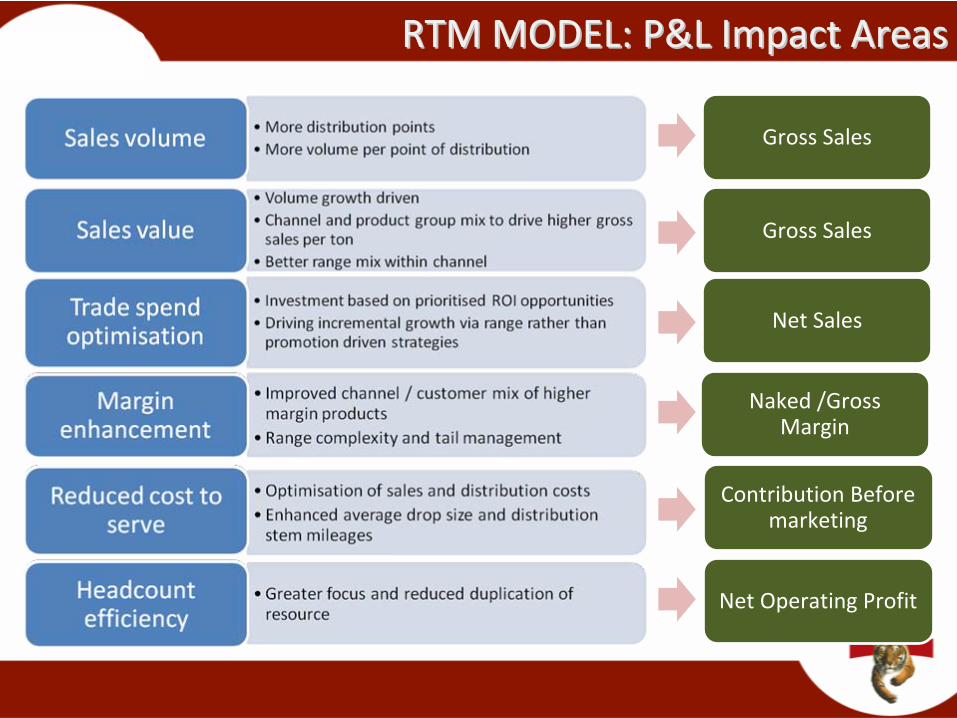

RTM MODEL: P&L Impact AreasRTM MODEL: P&L Impact Areas

Gross Sales

Gross Sales

Net Sales

Naked /Gross Margin

Contribution Before marketing

Net Operating Profit

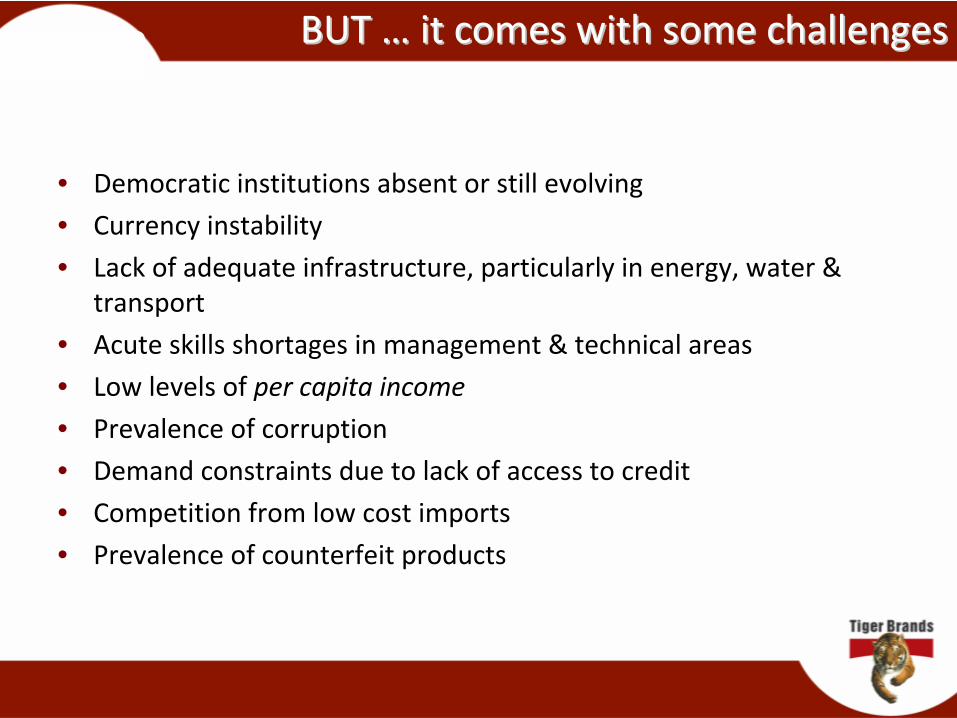

BUT BUT ……

it comes with some challengesit comes with some challenges

• Democratic institutions absent or still evolving• Currency instability• Lack of adequate infrastructure, particularly in energy, water &

transport• Acute skills shortages in management & technical areas• Low levels of per capita income• Prevalence of corruption• Demand constraints due to lack of access to credit• Competition from low cost imports• Prevalence of counterfeit products

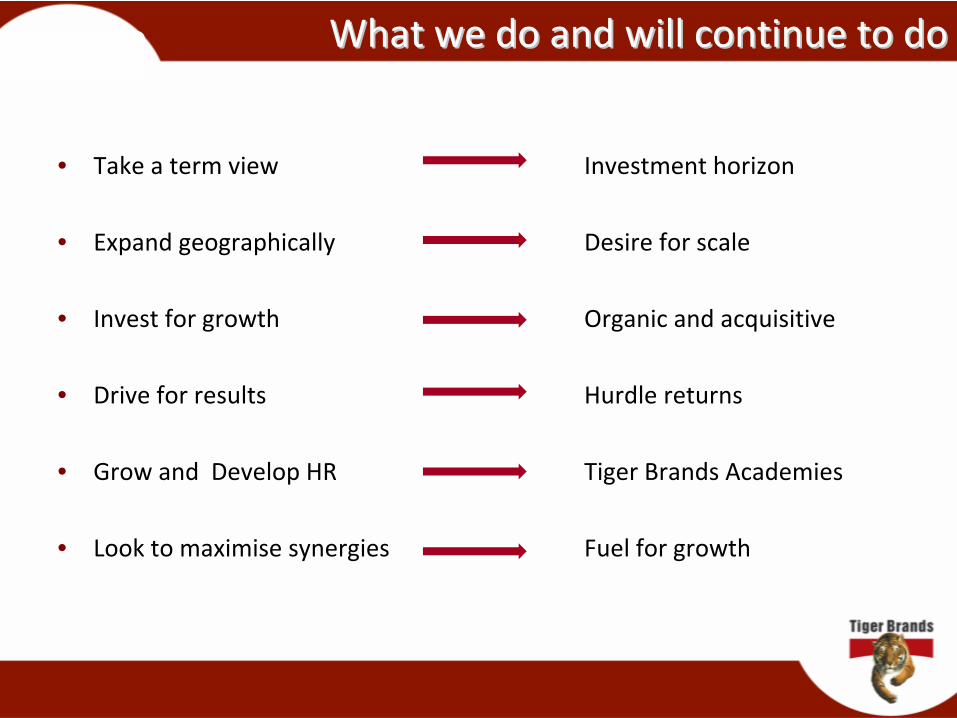

What we do and will continue to doWhat we do and will continue to do

• Take a term view

• Expand geographically

• Invest for growth

• Drive for results

• Grow and Develop HR

• Look to maximise

synergies

Investment horizon

Desire for scale

Organic and acquisitive

Hurdle returns

Tiger Brands Academies

Fuel for growth

• Unrelated diversification

• Expand at any cost

• Operate outside our stringent governance parameters

What we donWhat we don’’t do / wont do / won’’t dot do

Dilute value add

Shareholder returns

Corporate citizenship

Thank youThank you