Embed Size (px)

Citation preview

TILA Disclosures Lost at Sea?

Auto-Renewals under TILA and State Law

Annual ConferencePayday Loan Bar Association

November 13 – 15, 2013

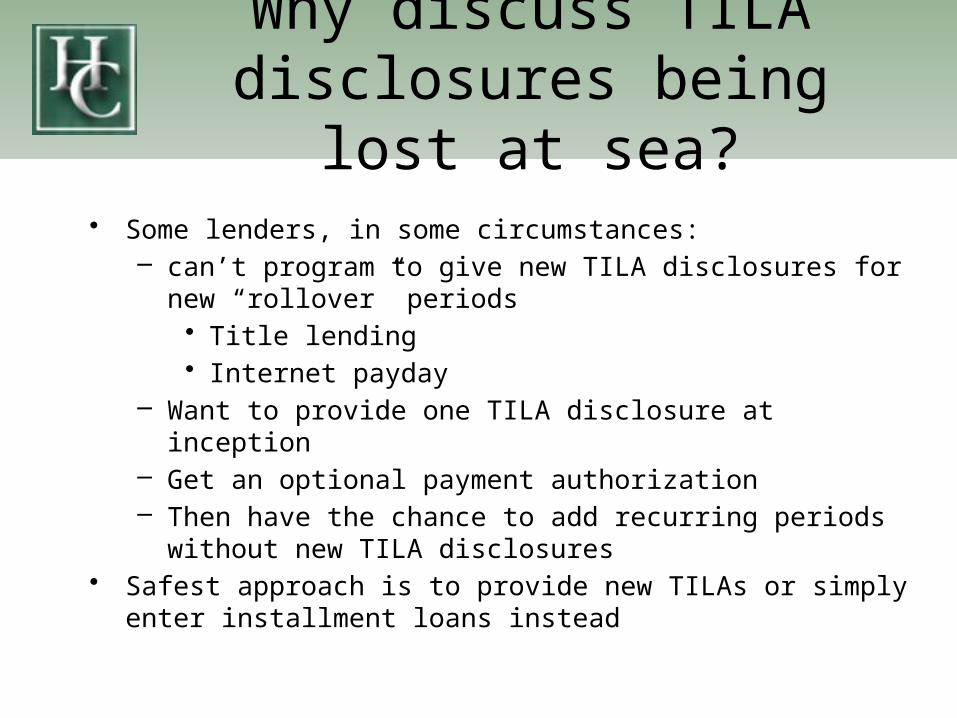

Why discuss TILA disclosures being lost at sea?

• Some lenders, in some circumstances:– can’t program to give new TILA disclosures for new “rollover”

periods• Title lending• Internet payday

– Want to provide one TILA disclosure at inception– Get an optional payment authorization– Then have the chance to add recurring periods without new TILA

disclosures• Safest approach is to provide new TILAs or simply enter installment

loans instead

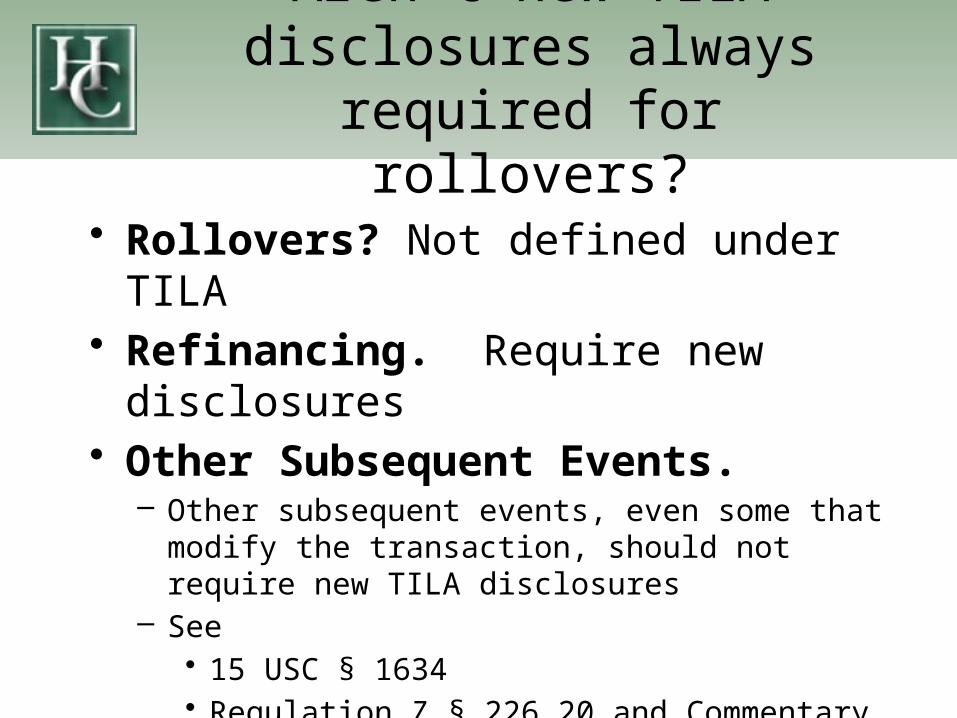

Aren’t new TILA disclosures always required for rollovers?

• Rollovers? Not defined under TILA• Refinancing. Require new disclosures • Other Subsequent Events.

– Other subsequent events, even some that modify the transaction, should not require new TILA disclosures

– See • 15 USC § 1634 • Regulation Z § 226.20 and Commentary

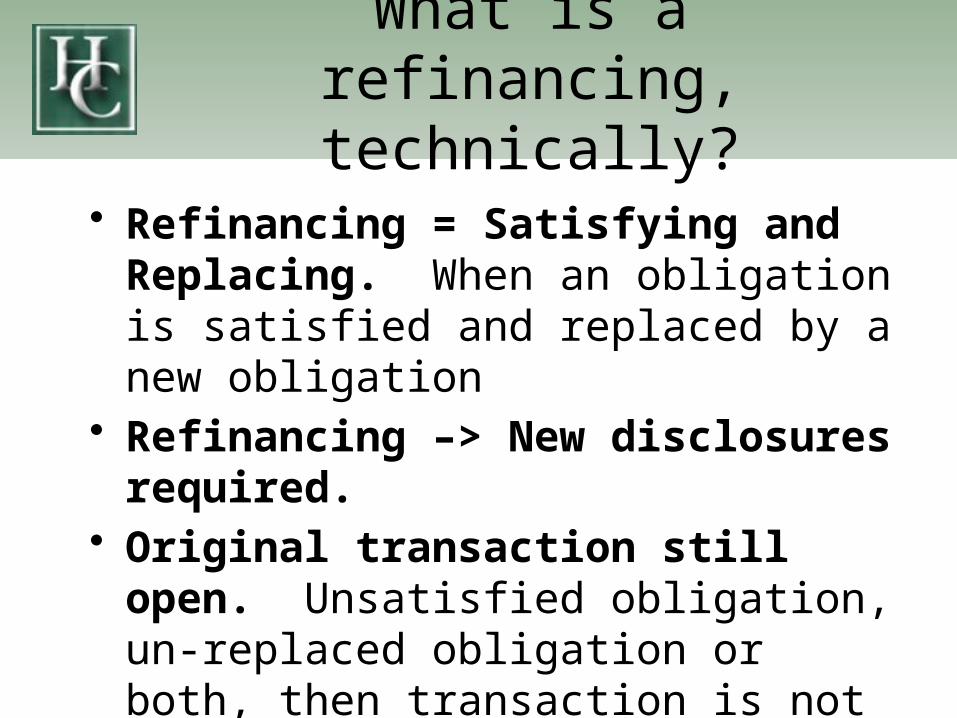

What is a refinancing, technically?

• Refinancing = Satisfying and Replacing. When an obligation is satisfied and replaced by a new obligation

• Refinancing –> New disclosures required. • Original transaction still open. Unsatisfied

obligation, un-replaced obligation or both, then transaction is not a refinancing

On a “rollover” isn’t the original obligation satisfied and replaced?

• It depends on the process. – Proceeds paying prior transaction = refinancing.

If the proceeds from the transaction in period 2 pay off the transaction in period 1, then this is a refinancing

– Payment to extend or renew transaction in period 1 ≠ refinancing. Period 2 can sometimes keep the original obligation open, and simply renew it in exchange for a fee

Are TILA disclosures required for post-consummation events that render the

original disclosures inaccurate?

• Not according to Congress– If TILA disclosure is subsequently rendered

inaccurate due to an act, occurrence, or agreement after delivering the disclosures, the resulting inaccuracy is not a violation

– 15 USC § 1634

So sign one agreement, then do anything you want, without new

TILA disclosures afterwards?

• No. Don’t do anything you want • Don’t Refinance. Don’t “substitute and

replace” an old obligation with a new obligation, unless you’re giving new TILA disclosures

• Be Careful. There are other technical nuances and agencies have clarified and taken actions providing guidance

What do the agencies say about refinancing?

• Look at the contract and applicable law. See whether the original obligation is satisfied and replaced

• Complete replacement. New obligation must completely replace the prior one

• More than merely changing terms. Changes in the terms and installment deferral shouldn’t be a refinancing unless they cancel the obligation and substitute a new one

• Reg Z 226.20 and Commentary

Any precautions to make sure something isn’t a refinancing?

• Yes. – Contemplate in the original contract. Contract should

contemplate the process, key terms, option for refinancing, and remain outstanding

– See regulatory examples. Look for explicit “non-refinancing” examples:• Single payment renewal with no change. Renewal of a single

payment obligation with no change in the original terms• Reduced APR (unless maturity lengthened). Reduction in the

APR with a payment schedule change (unless APR reduction is because maturity is lengthened –see the Commentary)

So, keep the original contract open and renew it?

• Generally yes. – Original contract remains open. Keep the original obligation

open– Clearly disclose renewal terms:

• Process to opt-in• Costs and key terms• “Subsequent events” that could lead to renewal, etc.

– Not changing terms is ideal. Renewing a single payment obligation, with no change in terms is ideal

– Duration change warning: Sometimes first payday loan is shorter than 14 days, but renewals are 14 days

• BUT …

But what?

• Plaintiffs, agencies, and courts• Positive cases:

– Payment holidays ≠ refinancing. They are “subsequent events.” Begala, April 2001, Begala, June 2000, and Begala, December 1998

– Payday extension fees ≠ refinancing. As long as loan’s terms, including “repayment obligation persist,” and the “agreement and note specify legal obligations even after a due date is extended” Jackson, December 2000

– Title pawn contemplating renewal ≠ refinancing. Title pawn ticket contemplating transaction renewal and maturity deferral deferred should not. Gunn, September 2008 and Gunn, March 2008

– Other positive cases exist

Has anything gone wrong for this approach?

• YES. • Disclosure is the safer approach. TILA is a

disclosure statute, intended to help consumers shop for the best cost of credit

• Assumption that the APR should be provided each period. Courts and agencies expect the industry to show the APR each period

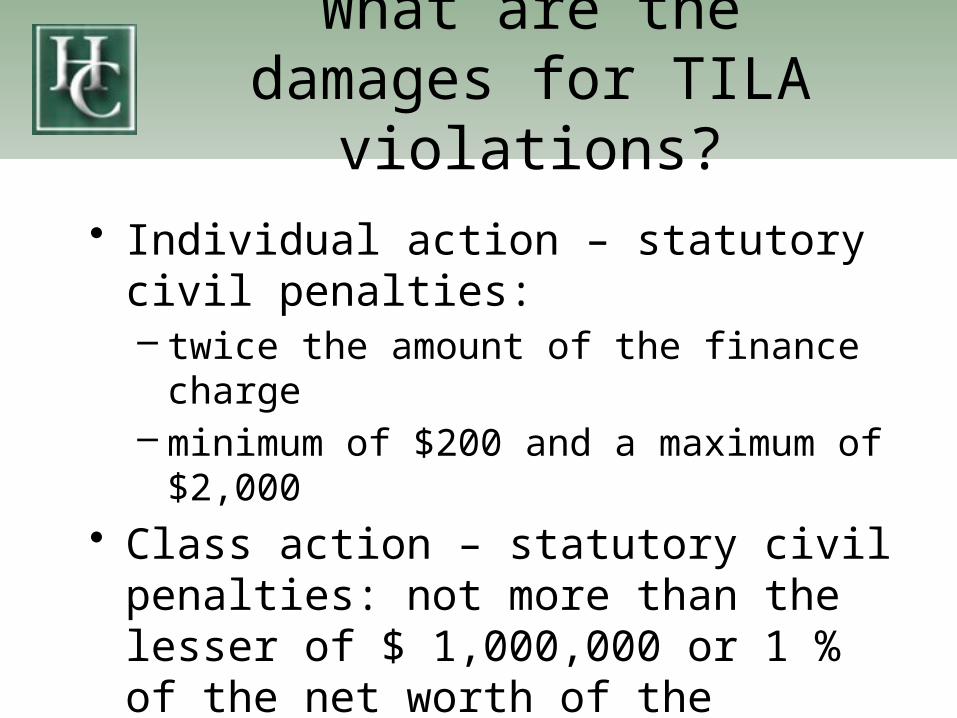

What are the damages for TILA violations?

• Individual action – statutory civil penalties: – twice the amount of the finance charge – minimum of $200 and a maximum of $2,000

• Class action – statutory civil penalties: not more than the lesser of $ 1,000,000 or 1 % of the net worth of the creditor.

• Actual damages, cost of the action, attorney’s fees

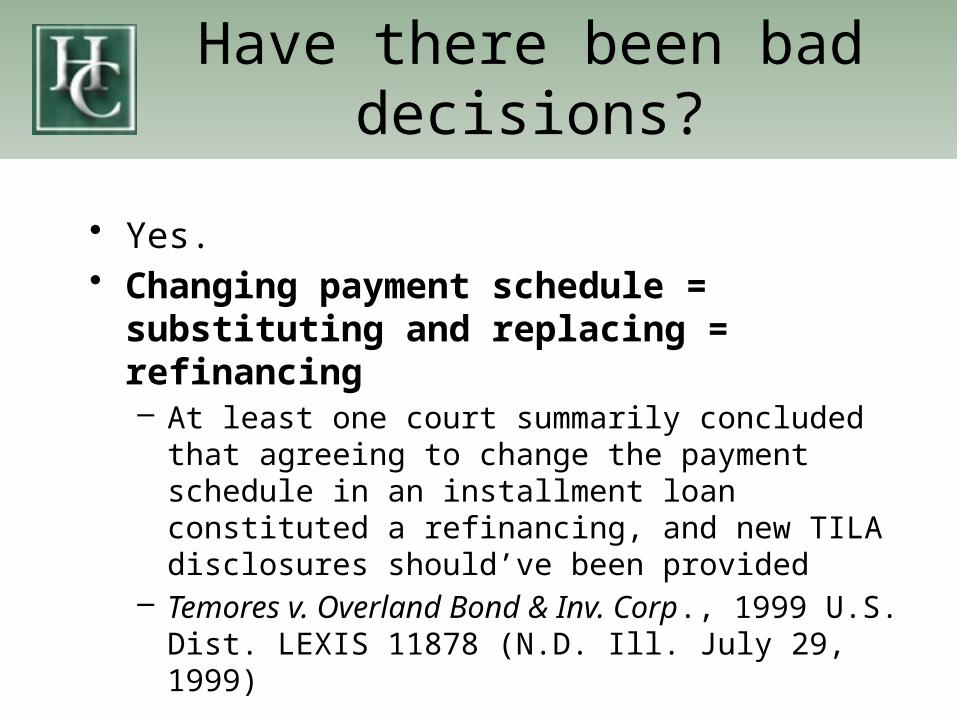

Have there been bad decisions?

• Yes.• Changing payment schedule = substituting and

replacing = refinancing– At least one court summarily concluded that agreeing to

change the payment schedule in an installment loan constituted a refinancing, and new TILA disclosures should’ve been provided

– Temores v. Overland Bond & Inv. Corp., 1999 U.S. Dist. LEXIS 11878 (N.D. Ill. July 29, 1999)

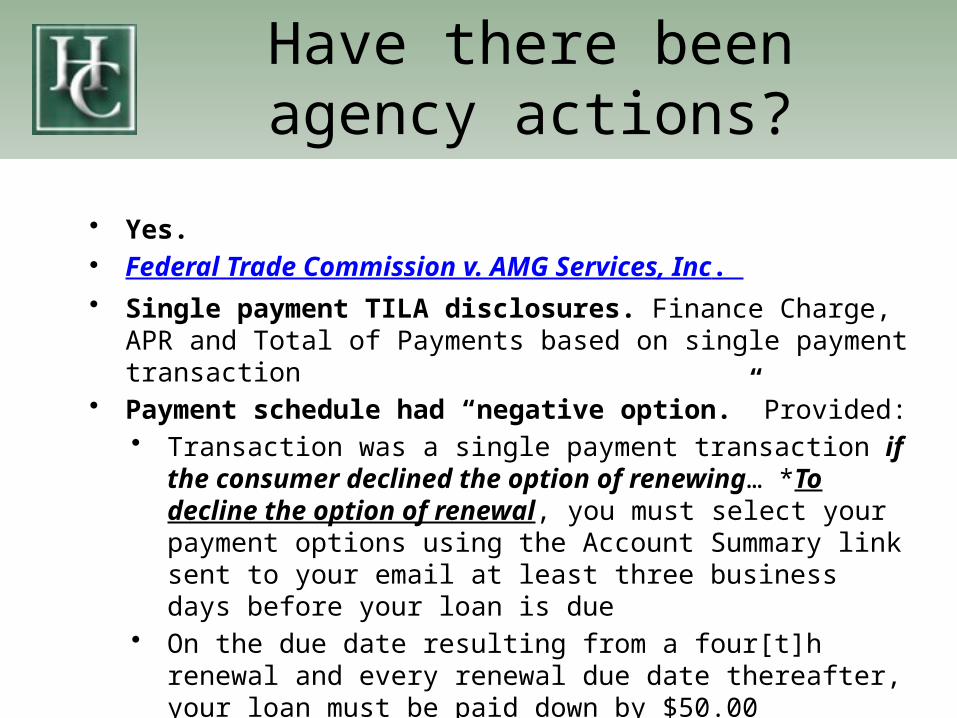

Have there been agency actions?

• Yes. • Federal Trade Commission v. AMG Services, Inc. • Single payment TILA disclosures. Finance Charge, APR and Total of

Payments based on single payment transaction• Payment schedule had “negative option.” Provided:

• Transaction was a single payment transaction if the consumer declined the option of renewing… *To decline the option of renewal, you must select your payment options using the Account Summary link sent to your email at least three business days before your loan is due

• On the due date resulting from a four[t]h renewal and every renewal due date thereafter, your loan must be paid down by $50.00

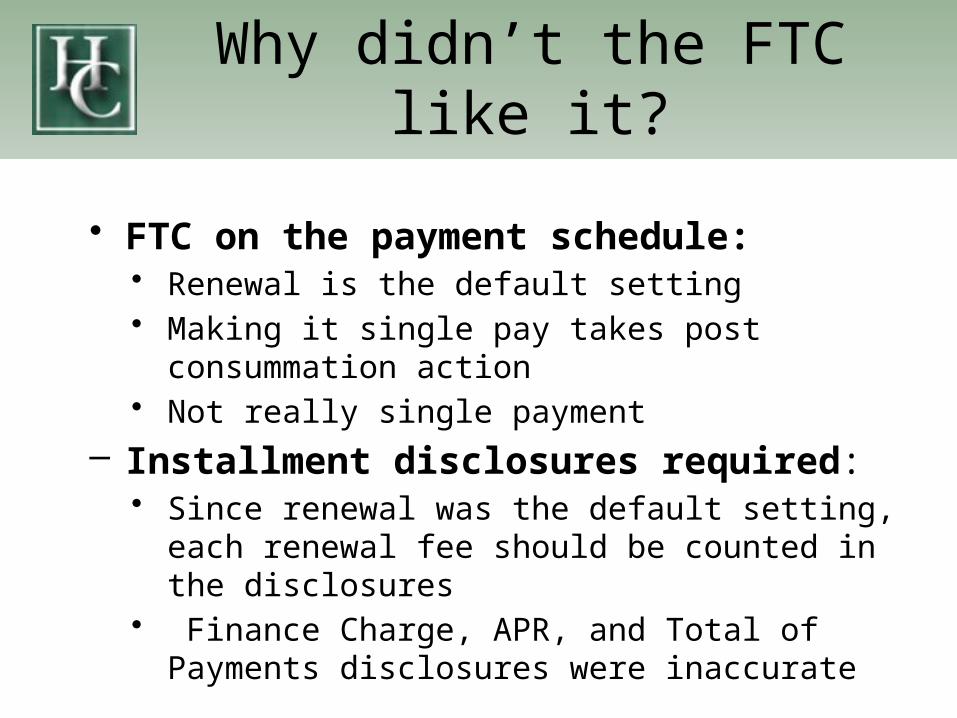

Why didn’t the FTC like it?

• FTC on the payment schedule:• Renewal is the default setting• Making it single pay takes post consummation action• Not really single payment

– Installment disclosures required:• Since renewal was the default setting, each renewal fee

should be counted in the disclosures• Finance Charge, APR, and Total of Payments disclosures

were inaccurate

What are the lessons from that action?

– Become an Installment Lender. If you have to auto-renew a single payment loan, without any post consummation action from the consumer:• Offer installment loans under applicable law• Follow the installment lending statutes and rules

– OR - Renew Carefully, Post Consummation. If you can’t give new TILA disclosures, but can get post-consummation assent to renewals:– Contemplate renewal possibility in the agreement– Contemplate subsequent events/options that would lead to such renewal– But, don’t put the transaction on “auto pilot.” Barring some consumer

action, payment as scheduled or default should occur– Follow licensing statute’s requirements

• OR – Change your program– Just give new TILA disclosures and get new agreement to replace the old one, each period. It’s the traditional approach in the industry, and reiterates the APR

Are there examples of other federal considerations?

• Yes – Consider UDAAP– Unfairness

• Standard: (1) It causes or is likely to cause substantial injury to consumers; (2) The injury is not reasonably avoidable by consumers; and (3) The injury is not outweighed by countervailing benefits to consumers or to competition

• Past agency actions:– Failing to be clear about price/cost – Explaining how consumers can avoid costs– Preventing consumers from exercising a choice – Not adhering to industry practices

What about “deception” claims?

• Deception

– Standard: (1) The act or practice misleads or is likely to mislead the consumer; (2) The consumer’s interpretation is reasonable under the circumstances; and (3) The misleading act or practice is material

– Past agency actions:• Pricing claims must be forthright and adequate • Pricing disclosures, such as APR and Finance Charge should

be conspicuous

What is the standard for “abusive” claims?

• Abusive Standard:– (1) Materially interferes with the ability of a consumer to

understand a term or condition of a consumer financial product or service; or

– (2) Takes unreasonable advantage of – • (A) a consumer’s lack of understanding of the material risks,

costs, or conditions of the product or service; • (B) a consumer’s inability to protect his or her interests in

selecting or using a consumer financial product or service; or• (C) a consumer’s reasonable reliance on a covered person to act

in his or her interests

What has the CFPB considered in “abusive” claims?

• Example action: American Debt Settlement Solutions, Inc. (ADSS) and its owner Michael DiPanni. CFPB noted:– financially vulnerable consumers– upfront fees without providing services– luring consumers deeply in debt and in dire circumstances– causing consumers to fall further into debt– Charging fees to vulnerable consumers who the defendants knew had

inadequate incomes to complete the programs• Suggestions – Explain the renewal:

– Terms, material risks, costs, and conditions– Emphasize ways the consumers can protect their interests: opt-out rights

(renewal, ACH, arbitration, privacy), prepayment, etc. – Warn the consumer that the Company’s interests are not the consumer’s

interests

How do licensing statutes address the subject?

• Different possibilities:– Expect Automatic renewals

• Certain title pledge/pawn explicitly expect “automatic renewal” unless certain conditions occur (default, surrender, redemption, etc.)

• Some examples: Alabama pawn, Georgia title pledge, Mississippi title pledge, Tennessee…

– Generally contemplate renewals with or without limitations• without statutory prohibition on post consummation automated

process• Some examples: Alabama (one rollover), Alaska (two consecutive

renewals) …– Prohibit Rollovers

• Some states prohibit any extension, deferral, rollover, etc.• Some examples: Florida deferred presentment …

Besides “rollover” provisions are there other state law

considerations?

• Yes. Some examples include:– Receipts. Receipts are required under several state laws. If

payments and renewals are automated, still must provide receipts

– Duration limits. If each new period is part of the initial transaction, and the transaction duration is limited, state regulators could deem an auto-renewal process “too long” of a transaction. Example: Alabama 31 day transaction limit, Alaska 14 day limit

– State regulator expectations. Many state regulators may be accustomed to seeing new TILA disclosures for each period, and assume an alternative process is a violation

So, what is the recap?

• Provide TILA disclosures early and often. The best approach is to provide TILA disclosures for each new “transaction.” This discloses the key terms to help assess the cost of credit

• Consider installment lending. If you can’t, consider operating as an installment lender

What if programming limitations prevent those options?

• Get new programmers. If you can’t …– Don’t automate. Don’t automate rollovers from inception– Post consummation option. Have a post-consummation option to automate

rollovers– Clearly disclose possibility in original agreement. Make sure the rollover

option (including cost) is contemplated as a possibility for extending the transaction, make this clear in the initial disclosures

– Remind consumer of continuing nature. Use post-consummation rollover procedures and documents that remind the borrower that it continues the current agreement, under its terms for optional rollover

– Clearly disclose key terms. Use post-consummation procedures and documents that that clearly discloses costs and key terms

– Avoid UDAAP. Be clear about price, conditions, risks, and interests.– Check licensing statute and with your regulator. Check your licensing

statute for provisions that could create issues

Questions & Answers

Questions?

Contact Information

Jennifer GallowayJennifer Galloway, P.A711 S. Howard Ave, Suite 200,

Tampa, Florida 33606 813-401-6161 [email protected]

Justin HosieHudson Cook, LLP6005 Century Oaks Dr.Chattanooga, TN 37416 423-490-7560 [email protected]

H. Blake SimsHudson Cook, LLP6005 Century Oaks Dr.Chattanooga, TN 37416 423-490-7560 [email protected]