Embed Size (px)

Citation preview

8/9/2019 Tocqueville Gold - 4Q 2012 Investor Letter

http://slidepdf.com/reader/full/tocqueville-gold-4q-2012-investor-letter 1/15

Tocqueville Asset Management L.P.

40 West 57th Street 19th Floor ● New York ● NY ● 10019-4001

Tel: (212)698-0800 ● Fax: (212)262-0154 ● www.tocqueville.com

Tocqueville Gold Strategy

Fourth Quarter 2012 Investor Letter

The bull market in gold remains intact. The metal rose approximately 7.14% in 2012 in U.S. dollar terms

and has increased in each of the last 12 years.

Negative real interest rates incentivize capital to move into gold. It is difficult to imagine a world of

positive real interest rates, absent a significant shift in monetary and fiscal policy in the Western democracies.

Gold and gold shares historically have been positively correlated. However, during the past few years,

gold mining stocks have underperformed the metal due a host of issues that we have discussed at length,

including in our website article A Golden Mulligan.(A Golden Mulligan | Tocqueville). Although the article was

published a few years ago, the issues afflicting gold mining stocks mentioned then still hold true.

Gold mining stock valuations are at the low end of the historical range since the introduction of the gold

ETF (GLD) in 2004, or roughly 10% (basis XAU/spot bullion.) This relationship is depicted on page 11 of the

appended data section to this report. Significant rallies in gold mining shares have occurred in the past few

years from this compressed valuation base.

We see evidence of fundamental change within the gold mining industry, which addresses many of the

concerns that have caused negative investor sentiment. For example, cost pressures are leveling off, which

should help margins. Investor pushback against major capital spending projects is leading to better capital

allocation decisions. There have been a number of departures at the CEO level due to investor dissatisfaction,

and this should heighten the sense of accountability to shareholder interests in the ranks of management. On

the other hand, resource nationalism remains a strong headwind. Only the better managed companies will be

able to deal successfully with these pressures.

Despite the steady rise in the gold price over many years, it has failed to exceed the 2011 high of

$1901/oz. achieved during the debt ceiling crisis and U.S. credit downgrade. This lack of direction has hurt gold

mining stocks, which do best when the upward trend of the gold price is clear. We believe that gold stocks will

respond favorably to a new high in the gold price.

Gold needs to rise only 15% to trade at a new high. We believe that this is in the cards for 2013, and that

such a move will be driven by the continuation of negative real interest rates and heightened concerns over the

direction of monetary and fiscal affairs in all western democracies. Such concerns would be exacerbated by the

continuation of extremely weak economic activity in 2013 and quite possibly the resumption of a recession,

anticipated by few.

8/9/2019 Tocqueville Gold - 4Q 2012 Investor Letter

http://slidepdf.com/reader/full/tocqueville-gold-4q-2012-investor-letter 2/15

Tocqueville Asset Management L.P.

40 West 57th Street 19th Floor ● New York ● NY ● 10019-4001

Tel: (212)698-0800 ● Fax: (212)262-0154 ● www.tocqueville.com

Most investors seem to expect a gradual acceleration of economic growth in 2013. We disagree and

believe that the recent tax hike, one of the largest in history, will dampen economic activity sufficiently to

widen the deficit and require the extension of debt monetization by the Federal Reserve for years to come.

We also believe that polarization of public opinion and the political process over austerity versus growth

agendas will also serve to paralyze economic activity. Not only will this require continued monetization of fiscal

deficits, but it will affect business and consumer behavior negatively. Intractable fiscal issues such as tax and

entitlement reform, in our opinion, will only be achieved through political consensus. In the absence of

effective political leadership, such a consensus seems achievable only in the aftermath of a financial and

economic meltdown on the order of 2008.

Once gold demonstrates that it can trade sustainably above $2000, or 20% above current levels, we

believe that gold mining stocks could trade at 13%-15% of spot bullion (basis XAU). That would translate into

appreciation of 60%-90% above the current XAU level of 160. Investor sentiment on gold is currently extremely

negative, comparable to the levels of mid-May 2012, when gold was trading approximately $100/oz. below

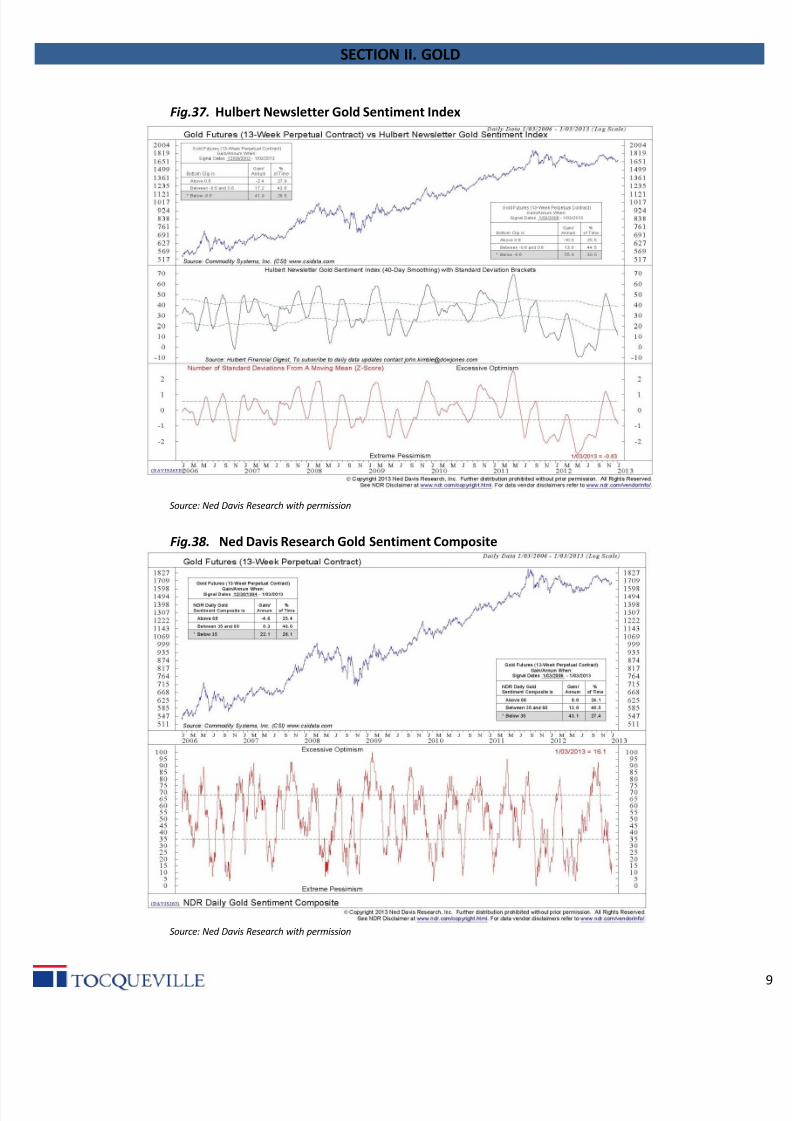

current levels (see Fig.35 - Fig.38 on pp. 8-9 of the appended data section). Historically, extreme negative

sentiment levels such as these have provided excellent entry points for new positions in bullion and the mining

shares.

Best regards,

John Hathaway

Portfolio Manager and Senior Managing Director

© Tocqueville Asset Management L.P.

January 8, 2013

This article reflects the views of the author as of the date or dates cited and may change at any time. The information should not be

construed as investment advice. No representation is made concerning the accuracy of cited data, nor is there any guarantee that any

projection, forecast or opinion will be realized.

References to stocks, securities or investments should not be considered recommendations to buy or sell. Past performance is not a guide

to future performance. Securities that are referenced may be held in portfolios managed by Tocqueville or by principals, employees and

associates of Tocqueville, and such references should not be deemed as an understanding of any future position, buying or selling, that

may be taken by Tocqueville. We will periodically reprint charts or quote extensively from articles published by other sources. When we

do, we will provide appropriate source information. The quotes and material that we reproduce are selected because, in our view, they

provide an interesting, provocative or enlightening perspective on current events. Their reproduction in no way implies that we endorse

any part of the material or investment recommendations published on those sites.

8/9/2019 Tocqueville Gold - 4Q 2012 Investor Letter

http://slidepdf.com/reader/full/tocqueville-gold-4q-2012-investor-letter 3/15

Macro charts show bloated and still expanding central bank balance sheets, negative real interest

rates in major currencies, and rapid growth of monetary aggregates. One could argue that thesefacts are well known, and that is certainly the case. However, the consequences of these facts are

still unknown, and therefore undiscounted by the markets. This in our opinion is the basis for

further upside in the gold price.

Charts 16 & 17 reveal a potential time bomb for US treasuries. Interest on the public debt is close

to historical lows, due in part to Fed manipulation, the “fear” trade, and old fashioned

momentum. Think of what 300 or 400 additional basis points across the yield curve would do to

the fiscal deficit. (Hint: what is 4% x $16 trillion as a percent of future fiscal deficits? Answer: it is

very high).

Charts 23 & 24 reflect the declining willingness of foreign investors to invest in US securities. It

may have something to do with the point above.

Charts 28, 32 & 32 indicate that despite all of the talk about gold, it remains very underowned.

Charts 35 & 38 show that sentiment is at, or approaching rock bottom levels from which rallies can

be reliably be expected.

Chart 47 shows that despite all of the sell side whining about rising costs (see Chart 48), profits are

at record levels.

The consequence of Chart 47 is reflected in Chart 51, a steady decline in equity issuance. We

believe declining equity dilution is an important positive fundamental change in the industry that

will help lead to expanding valuation of gold mining equities.

8/9/2019 Tocqueville Gold - 4Q 2012 Investor Letter

http://slidepdf.com/reader/full/tocqueville-gold-4q-2012-investor-letter 4/15

SECTION I. MACRO

-3%

-2%

-1%

0%

1%

2%

3%

4%€ 0

€ 200

€ 400

€ 600

€ 800

€ 1,000

€ 1,200

€ 1,400

1999 2001 2003 2005 2007 2009 2011

Fig.3. ECB Real Rates and Gold in EURGold

ECB Real Rates

Source: Bloomberg

-5%

-4%

-3%

-2%

-1%

0%

1%

2%

3%

4%

5%2,000

4,000

6,000

8,000

10,000

12,000

14,000

1999 2001 2003 2005 2007 2009 2011

Fig.5. Chinese Real Rates and Gold in RMBGold

Chinese Real Rates

Source: Bloomberg

-5%

-4%

-3%

-2%

-1%

0%

1%

2%

3%

4%

5%$0

$200

$400

$600

$800

$1,000

$1,200

$1,400

$1,600

$1,800

$2,000

2000 2002 2004 2006 2008 2010 2012

Fig.1. Gold and US Real Rates

Gold Price

US Real Rates

Source: Bloomberg

$0

$500

$1,000

$1,500

$2,000

$2,500

$3,000

$3,500

1994 1998 2002 2006 2010

Fig.2. Fed Balance Sheet ($B)

Source: Bloomberg

€ 0

€ 500

€ 1,000

€ 1,500

€ 2,000

€ 2,500

€ 3,000

€ 3,500

1999 2001 2003 2005 2007 2009 2011

Fig.4. ECB Balance Sheet ( €B)

Source: Bloomberg

0

5,000

10,000

15,000

20,000

25,000

30,000

35,000

2003 2005 2007 2009 2011

Fig.6. PBC Balance Sheet (RMB B)

Source: Bloomberg

8/9/2019 Tocqueville Gold - 4Q 2012 Investor Letter

http://slidepdf.com/reader/full/tocqueville-gold-4q-2012-investor-letter 5/15

SECTION I. MACRO

$0

$10

$20

$30

$40

1999 2001 2003 2005 2007 2009 2011

$0

$5

$1,

$1,

$2,Fig. 8. Gold and Combined M2

($T; Fed, ECB, PBC)

Gold

M2

Source: Bloomberg

0%

4%

8%

12%

16%

1970 1975 1980 1985 1990 1995 2000 2005 20

Fig. 10. US M2 YoY%

Source: Bloomberg

-5%

0%

5%

10%

15%

20%

25%

1970 1975 1980 1985 1990 1995 2000 2005 2010

Fig. 9. US M1 YoY%

Source: Bloomberg

0%

4%

8%

12%

16%

1999 2001 2003 2005 2007 2009 2011

Fig. 11. ECB M1 YoY %

Source: Bloomberg

0%

4%

8%

12%

1999 2001 2003 2005 2007 2009 2011

Fig. 12. ECB M2 YoY %

Source: Bloomberg

0%

10%

20%

30%

40%

1996 1998 2000 2002 2004 2006 2008 2010 2012

Fig.13. PBC M1 YoY %

Source: Bloomberg

0%

10%

20%

30%

1996 1998 2000 2002 2004 2006 2008 2010 2

Fig.14. PBC M2 YoY %

Source: Bloomberg

$0

$2

$4

$6

$8

$10

$12

$14

$16

2006 2007 2008 2009 2010 2011 2012

Fig.7. The Biggest 6 Central Bank Balance

SheetsUS, UK, Japan, China, EU & Switzerland (US$T)

Source: Bloomberg

8/9/2019 Tocqueville Gold - 4Q 2012 Investor Letter

http://slidepdf.com/reader/full/tocqueville-gold-4q-2012-investor-letter 6/15

SECTION I. MACRO

Fig.15. Inflation

US Euro Area China

Headline CPI 1.80% 2.20% 2.00%

Core CPI 1.90% 1.40% n/a

Shadowstats 9.41% n/a n/a

Source: Bloomberg; Shadow Government Statistics

Fig 19. Total credit Market Debt as % of GDP

Source: Ned Davis Research with permission

Dec-12

$0

$2

$4$6

$8

$10

$12

$14

$16

$18

1980 1990 2000 2010

Fig.17 . US Public Debt Outstanding ($T)

Source: Bloomberg

0%

1%

2%

3%

4%

5%

6%

7%

2000 2002 2004 2006 2008 2010 2012

F ig.16. Average Annual Interest Rate Pai

on US Debt

Source: Bloomberg; US Treasury

10%

12%

14%

16%

18%

20%

22%

24%

1988 1992 1996 2000 2004 2008 20

Fig.18 US Interest Expense as % of Total

Government Outlays

Source: Bloomberg; US Treasury

8/9/2019 Tocqueville Gold - 4Q 2012 Investor Letter

http://slidepdf.com/reader/full/tocqueville-gold-4q-2012-investor-letter 7/15

SECTION I. MACRO

Fig.21. The Debt Ceiling ($T) Fig.22. Global Forex Accumulation. 12 months sum

Source: MacroMavens, LLC

Source: Bianco Research

Fig.23. China Net Purchases of LT US Securities (annual $B)

Source: MacroMavens, LLC Source: MacroMavens, LLC

Fig.24. Share of Global Forex Accumulation Recycl

into US Securities

0

50

100

150

200

250

300

350

400

1999 2001 2003 2005 2007 2009 2011

$0

$500

$1,000

$1,500

$2,000Fig. 20. Quality Spread and Gold

Gold Price

Moody's Seasoned Corp Aaa vs Baa

Source: Bloomberg

8/9/2019 Tocqueville Gold - 4Q 2012 Investor Letter

http://slidepdf.com/reader/full/tocqueville-gold-4q-2012-investor-letter 8/15

SECTION II. GOLD

Fig. 25. Gold Supply and Demand(tonnes)

Source: World Gold Council

0

500

1000

1500

2000

2500

2004 2005 2006 2007 2008 2009 2010 2011 2012

Fig. 27 . Gold Held By Gold ETFS (tonnes)

Other

GLD

Source: Company Filings, World Gold Council

20%22%

6%

0%

5%

10%

15%

20%

25%

1934 1982 Q3'2012

Fig. 26. Market Cap of Above Ground Gold as % of Total US

Financial Assets

Source: Federal Reserve, World Gold Council

2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 Q32012

Supply

Mine production 2,591 2,592 2,478 2,550 2,481 2,476 2,409 2,584 2,739 2,827 2,101

Old gold scrap 835 944 829 886 1,107 956 1,217 1,672 1,723 1,669 1,237

Traditional supply 3,426 3,536 3,307 3,436 3,588 3,432 3,626 4,257 4,463 4,495 3,337 Net producer hedging (412) (279) (445) (86) (373) (444) (349) (252) (108) 10 (12)

Official sector sales 545 617 497 662 367 484 236 30 - - -

Total supply 3,559 3,874 3,359 4,012 3,582 3,472 3,513 4,034 4,355 4,505 3,326

Demand

Jewellery 2,680 2,522 2,673 2,707 2,283 2,405 2,187 1,760 2,017 1,972 1,410

Other 360 385 416 431 458 462 436 373 466 453 327

Total fabrication 3,040 2,907 3,089 3,138 2,741 2,867 2,623 2,134 2,483 2,425 1,738

Bar & coin retail investment 373 314 396 412 421 446 649 743 1,205 1,519 942

Official sector purchases - - - - - - - - 77 457 374

ETFs & Similar 3 39 133 208 260 253 321 617 382 185 189

Implied net investment 143 614 (259) 254 160 (94) (80) 541 207 (81) 83

Total demand 3,559 3,874 3,359 4,012 3,582 3,472 3,513 4,034 4,355 4,505 3,326

8/9/2019 Tocqueville Gold - 4Q 2012 Investor Letter

http://slidepdf.com/reader/full/tocqueville-gold-4q-2012-investor-letter 9/15

SECTION II. GOLD

Fig.30. Notable Transactions in 3Q12

Source: World Gold Council

Investment

Adviser,

19.3%

Broker, 7.4%

Private

Banking, 0.9%

Pension Fund,

0.5%

Hedge Fund,

10.2%Mutual Fund,

3.6%

Insurance

Company,

0.2%

Non-Institutional,

57.9%

Fig. 28. GLD Ownership by Type

Source: Factset

00 01 02 03 04 05 06 07 08 09 10 11 3Q12

-600-500

-400

-300

-200

-100

0

100

200

300

400

500

600 Fig.29. Central Banks Net Purchases (tonnes)

Source: World Gold Council

29,500

30,000

30,500

31,000

31,500

32,000

32,500

33,000

33,500

34,000

2000 2002 2004 2006 2008 2010 2012

Fig. 31. Central banks Holdings of Gold (tonnes)

Source: World Gold Council

1.0%

1.1%

1.2%

1.3%

1.4%

1.5%

1.6%

2000 2002 2004 2006 2008 2010 2

Fig. 32. Gold as % of Total Reserves

Source: World Gold Council

Country Tonnes Transaction

Kazakhstan 2.45 Purchase

Korea 16.00 Purchase

Russia 16.48 Purchase

Turkey 58.13 Addition

8/9/2019 Tocqueville Gold - 4Q 2012 Investor Letter

http://slidepdf.com/reader/full/tocqueville-gold-4q-2012-investor-letter 10/15

SECTION II. GOLD

0

20

40

60

80

100

Aug-05 Aug-06 Aug-07 Aug-08 Aug-09 Aug-10 Aug-11 Aug-12

Fig.33. Web searches for "Gold Bubble"

Source: GoogleTrends

0

20

40

60

80

100

2004 2006 2008 2010 2012

Fig.34. Web searches for "Gold Investment"

Source: GoogleTrends

$0

$500

$1,00

$1,50

$2,00

0

20

40

60

80

100

2006 2007 2008 2009 2010 2011 2012

Fig. 35. Bernstein's Daily Sentiment Index

DSI Gold

Source Bloomberg, Bernstein's DSI

$400

$600

$800

$1,00

$1,20

$1,40$1,60

$1,80

$2,00

0

20

40

60

80

100

2006 2007 2008 2009 2010 2011 2012

Fig. 36. Market Vane Bullish Consensus

Market Vane Gold

Source: Bloomberg; Market Vane

8/9/2019 Tocqueville Gold - 4Q 2012 Investor Letter

http://slidepdf.com/reader/full/tocqueville-gold-4q-2012-investor-letter 11/15

SECTION II. GOLD

Fig.37. Hulbert Newsletter Gold Sentiment Index

Source: Ned Davis Research with permission

Fig.38. Ned Davis Research Gold Sentiment Composite

Source: Ned Davis Research with permission

8/9/2019 Tocqueville Gold - 4Q 2012 Investor Letter

http://slidepdf.com/reader/full/tocqueville-gold-4q-2012-investor-letter 12/15

SECTION II. GOLD

-20%

80%

180%

280%

380%

480%

2000 2002 2004 2006 2008 2010 2012

Fig.40. Gold vs Continuous Commodity Index

CCI Index

Gold

Source: Bloomberg

$0

$200

$400

$600

$800

$1,000

$1,200

$1,400

$1,600

$1,800

$2,000

-1000

-800

-600

-400

-200

0

200

400

600

800

2006 2007 2008 2009 2010 2011 2012

Fig. 41. Comex Gold Futures Activity (tonnes)

Net Large Speculators

Net Hedgers/Commercials

Gold

Source: CFTC

$0

$200

$400

$600

$800

$1,000$1,200

$1,400

$1,600

$1,800

$2,000

800

1000

1200

1400

1600

1800

2000

2006 2007 2008 2009 2010 2011 2012

Fig. 39. Comex Gold Futures Open Interest

(tonnes)

Open

Interest

Source: Bloomberg

$900

$1,100

$1,300

$1,500

$1,700

$1,900

0.30%

0.40%

0.50%

0.60%

0.70%

0.80%

0.90%

1.00%

07-10 09-10 11-10 01-11 03-11 05-11 07-11 09-11 11-11 01-12 03-12 05-12 07-12 09-12 11-12

Fig.42. Commercial Net Shorts as % of Total Open Interest

Net Short/Open Interest

Gold

Source: Bloomberg; The McClellan Market Report

More Net Short

Less Net Short

8/9/2019 Tocqueville Gold - 4Q 2012 Investor Letter

http://slidepdf.com/reader/full/tocqueville-gold-4q-2012-investor-letter 13/15

SECTION III. MINING EQUITIES

0%

10%

20%

30%

40%

50%

60%

70%

1994 1996 1998 2000 2002 2004 2006 2008 2010 2012

Fig.43. XAU and HUI as a Ratio of Gold

HUI/Gold

XAU/Gold

Source: Factset

-$1,500

-$1,000

-$500

$0

$500

$1,000

$1,500

$2,000

$2,500

$3,000

$3,500

1 H 0 7

2 H 0 7

1 H 0 8

2 H 0 8

1 H 0 9

2 H 0 9

1 H 1 0

2 H 1 0

1 H 1 1

2 H 1 1

1 H 1 2

2 H 1 2

Fig.44. Net Fund Flows For Lipper's Equity

Precious Metals Fund Universe ($M)

Source: Morningstar

2H12 - as of 11/30/12

15%

20%

25%

30%

35%

40%

03 04 05 06 07 08 09 10 11 12

Fig.46. Gold Miners Dividend Payout Ratio

Source: Factset

Universe: ABX, NEM, GG, AU, GFI, KGC, NCM, BVN, HMY, AUY, IAG, CG,

EGO, GOLD

$0

$2

$4

$6

$8

$10

$12

$14

$16

2006 2007 2008 2009 2010 2011 2012

Fig.45. Market Cap of Van Eck Gold

Equity ETFs ($B)

Source: Factset

$0

$200

$400

$600

$800

$1,000

$1,200

$1,400

$1,600

$1,800 Fig.47. Senior Producers Cash Costs and

Margin

Cash Margin

Cash Costs

Source: Bloomberg

8/9/2019 Tocqueville Gold - 4Q 2012 Investor Letter

http://slidepdf.com/reader/full/tocqueville-gold-4q-2012-investor-letter 14/15

SECTION III. MINING EQUITIES

Fig. 48. Total Cash Outflow ($/oz)

Note: Operating = Operating costs + Exploration costs + Royalties;

ap ta= ngo ng+ xpans on cap ta ; t er = nance costs + t er costs

ource: o e s

0%

10

20

30

40

50

60

70

$0

$100

$200

$300

$400

$500

$600

2005 2006 2007 2008 2009 2010 2011 2012

Fig. 49. Average Cost of Acquisitions in the

Gold Sector ($/Oz)

Acquisition Cost As Ratio of Gold PriceSource: RBC Capital Markets

0

20

40

60

80

100

120

140

$0

$2

$4

$6

$8

$10

$12

$14

$16

$18

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012

Fig.51. Equity Capital Issued by Gold Miners

$B of Equty Issued

# of Transactions

Source: RBC Capital Markets

-2%

0%

2%

4%

6%

8%

10%

2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012

Fig. 50. Senior Producers Return On Capital

Source: Factset

Universe: NEM, ABX, GG, KGC, AUY, NCM, AU, GFI, HMY

Est

8/9/2019 Tocqueville Gold - 4Q 2012 Investor Letter

http://slidepdf.com/reader/full/tocqueville-gold-4q-2012-investor-letter 15/15

SECTION III. MINING EQUITIES

Fig. 52. Gold Price Discounted by Market

Source: BMO Capital Markets

Fig. 54. NAV Premiums - Senior & Intermediate producers (N.A.)

Source: BMO Capital Markets

Fig. 55. P/CF - Senior producers (N.A.)

Source: BMO Capital Markets

20072008

2009

2010

2011

2013

2012

$500

$700

$900

$1,100

$1,300

$1,500

$1,700

Yr 0 Yr 1 Yr 2 Yr 3 Yr 4

Fig.53. Consensus Forecast Gold Price ($/Oz)

Source: Scotiabank