Embed Size (px)

Citation preview

Tom Copeland [email protected] Director, Monitor Corporate Finance www.corpfinonline.comMonitor Group, Cambridge, Massachusetts www.monitor.com

For more reading see:Copeland, T, T. Koller, J. Murrin, Valuation: Measuring and Managing the Value of Companies

Copyright © 2001 by Monitor Company Group, L.P.

No part of this publication may be reproduced, stored in a retrieval system, or transmitted in any form or by any means — electronic, mechanical, photocopying, recording, or otherwise — without the permission of Monitor Company Group, L.P.

This document provides an outline of a presentation and is incomplete without the accompanying oral commentary and discussion.

COMPANY CONFIDENTIAL

Trends in Valuation

NIVRA, Amsterdam, June 1, 2001

Copyright © 2001 Monitor Company Group LP — Confidential — CAMZKN-MFR-NIVRA 6 01-TEC 2

Changes in Value are at the Heart of Economic Decision-Making

Discounted Cash Flow Valuation DCF

Expectations-Based Management

Real Options Analysis

Discounted Cash Flow Valuation DCF Discounted Cash Flow Valuation DCF

Copyright © 2001 Monitor Company Group LP — Confidential — CAMZKN-MFR-NIVRA 6 01-TEC 3

Discounted Cash Flow Definition

DCF has three components:

Free Cash Flow = EBIT - Cash taxes on EBIT + accrued taxes due

+ depreciation – Capital Expenditures – operating working capital

WACC =

Continuing Value =

V

SK

V

BK Sb )rate tax marginal1(

gWACC

rgEBIT

)/1)(ratecash tax 1(

Copyright © 2001 Monitor Company Group LP — Confidential — CAMZKN-MFR-NIVRA 6 01-TEC 4

Source: Value Line forecasts; Copeland, Koller, Murrin, Valuation, 2nd edition, 1994

0.0

2.0

4.0

6.0

8.0

10.0

12.0

0 1 2 3 4 5 6 7 8 9 10

35 Large U.S. Companies, 1988

1988 DCF / Book

19

88

Ma

rke

t /

Bo

ok

R2 = 0.94

DCF Works Well For Large Publicly Held Companies

R2 = 0.92

0

5

10

15

0 5 10 15

1999 DCF / Book Value1

99

9 M

ark

et

/ B

oo

k V

alu

e

Source: Value Line Forecasts, Monitor Analysis

31 Large U.S. Companies, 1999

Copyright © 2001 Monitor Company Group LP — Confidential — CAMZKN-MFR-NIVRA 6 01-TEC 5

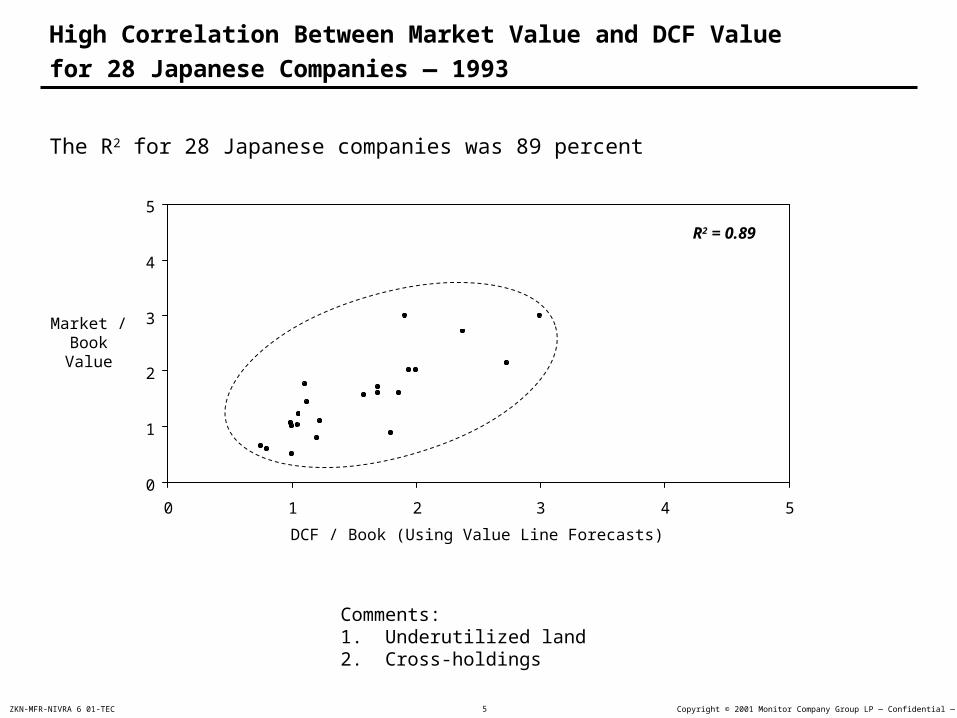

High Correlation Between Market Value and DCF Value

for 28 Japanese Companies — 1993

The R2 for 28 Japanese companies was 89 percent

Market / Book Value

0

1

2

3

4

5

0 1 2 3 4 5

DCF / Book (Using Value Line Forecasts)

R2 = 0.89

Comments:1. Underutilized land 2. Cross-holdings

Copyright © 2001 Monitor Company Group LP — Confidential — CAMZKN-MFR-NIVRA 6 01-TEC 6

. . . for 15 Italian companies (the R2 was 95.4 percent) . . .

DCF / Book

Market / Book Value

0.2

0.4

0.6

0.8

1.0

1.2

1.4

1.6

0.2 0.4 0.6 0.8 1.0 1.2 1.4 1.6

Correlation Between DCF and Market Value

for 15 Italian Companies* — 1990

Snia

Pirelli

Sip

Falk

Burgo

FiatMagneti M.

Montedison

Stet

FidenzaAuschen

Merloni

Cementir

Benetton

R2 = 0.954

2.0 3.0

2.0

3.0

Olivetti

Correlation between DCF and Market Value — Italy

* Using publicly available information** Capitalization on September 28, 1990 (Borsa valori di Milano), book value of companySource: Copeland, Koller and Murrin, Valuation

Comments:1. Mark to market inflation accounting2. Holder assets

Copyright © 2001 Monitor Company Group LP — Confidential — CAMZKN-MFR-NIVRA 6 01-TEC 7

Brazil

Copyright © 2001 Monitor Company Group LP — Confidential — CAMZKN-MFR-NIVRA 6 01-TEC 8

DCF Works Across Different Industries

16 banks

*5 banks are non-U.S. banksSource: Global Vantage; Value Line

Ma

rke

t /

Bo

ok

Va

lue

0.0

0.5

1.0

1.5

2.0

2.5

3.0

0.0 0.5 1.0 1.5 2.0 2.5 3.0

DCF / Book Value

R2 = 0.97

13 Insurance Companies

Mar

ket

/ Bo

ok

Val

ue

DCF / Book Value30 1 2

3

0

1

2

R2 = 0.92

1. Equity Approach2. Income model/ interest spread model

1. Equity Approach2. Unrealized capital gains

Copyright © 2001 Monitor Company Group LP — Confidential — CAMZKN-MFR-NIVRA 6 01-TEC 9

60

80

100

120

140

160

1804-

Jan-

99

13-J

an-9

9

25-J

an-9

9

3-F

eb-9

9

12-F

eb-9

9

24-F

eb-9

9

5-M

ar-9

9

16-M

ar-9

9

25-M

ar-9

9

6-A

pr-9

9

15-A

pr-9

9

26-A

pr-9

9

5-M

ay-9

9

14-M

ay-9

9

25-M

ay-9

9

4-Ju

n-99

15-J

un-9

9

24-J

un-9

9

6-Ju

l-99

15-J

ul-9

9

26-J

ul-9

9

4-A

ug-9

9

13-A

ug-9

9

24-A

ug-9

9

2-S

ep-9

9

14-S

ep-9

9

DCF Works for Robust Growth Companies

1999 Stock Price (AOL)

Note: 1999 elsewhere in valuation refers to FY 99 which ends in June Source: Compustat

Price Per Share

Volume(Millions)

0

10

20

30

40

50

60

4-Ja

n-99

13-J

an-9

9

25-J

an-9

9

3-F

eb-9

9

12-F

eb-9

9

24-F

eb-9

9

5-M

ar-9

9

16-M

ar-9

9

25-M

ar-9

9

6-A

pr-9

9

15-A

pr-9

9

26-A

pr-9

9

5-M

ay-9

9

14-M

ay-9

9

25-M

ay-9

9

4-Ju

n-99

15-J

un-9

9

24-J

un-9

9

6-Ju

l-99

15-J

ul-9

9

26-J

ul-9

9

4-A

ug-9

9

13-A

ug-9

9

24-A

ug-9

9

2-S

ep-9

9

14-S

ep-9

9

1999 Trading Volume (AOL)

Copyright © 2001 Monitor Company Group LP — Confidential — CAMZKN-MFR-NIVRA 6 01-TEC 10

AOL Revenue Assumptions for the Valuation Model Were Closely Tracked

to Analyst Estimates of Long Term Revenue Growth

$27,450

$25,183

$22,894

$20,260

$17,466

$12,233$9,945

$8,080$6,288

$4,777

$14,801

$0

$5,000

$10,000

$15,000

$20,000

$25,000

$30,000

1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009

Revenue Growth

* Most analysts did not forecast beyond 2003Note: FY for AOL ends in JuneSource: ING Barings; BankBoston Robertson Stephens; Donaldson, Lufkin, and Jenrette

$ Billions

Deviation fromAnalystProjections*

1.5% 1.9% 2.3% 0.1%

1999-2004 Average Growth Rate: 25.4%

2004-2009 Average Growth Rate: 13.2%

Long-Term Revenue Growth: 9%

Copyright © 2001 Monitor Company Group LP — Confidential — CAMZKN-MFR-NIVRA 6 01-TEC 11

AOL Projected Operating Margins Benefit From Both Significant Scale

Economies and Changes in Revenue Mix Toward Higher Margin Businesses

70% 67% 69% 65% 60% 55%

21% 25% 24% 29% 33% 38%

10% 8% 7% 7% 7% 7%

0%

20%

40%

60%

80%

100%

1999 2001 2003 2005 2007 2009

Enterprise

Advertising

Online Services

Revenue Mix

Source: ING Barings; BankBoston Robertson Stephens; Donaldson, Lufkin, and Jenrette

Percent of Revenue

Operating Margin 12.9% 22.0% 28.9% 32.1% 33.9% 34.8%

Analyst Projections* 13.1% 22.6% 28.1% 32.0%

* Average

Copyright © 2001 Monitor Company Group LP — Confidential — CAMZKN-MFR-NIVRA 6 01-TEC 12

AnalystProjections(CapEx)*

$355 $375 $375 $375

AOL: Increasing Capital Productivity

Capital Expenditures and Capital Turns (Rev / Invested Capital)

* Most analysts did not forecast beyond 2003Source: ING Barings; BankBoston Robertson Stephens; Donaldson, Lufkin, and Jenrette

Capital Turns

CapEx

$312

$409 $404$448

$489

$592

$699

$810

$916$1,007

$1,043

$0

$200

$400

$600

$800

$1,000

$1,200

1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009

0

1

2

3

4

5

6

7

8CapEx

Capital Turns

Copyright © 2001 Monitor Company Group LP — Confidential — CAMZKN-MFR-NIVRA 6 01-TEC 13

AOL: Matures Led to the Use of a Changing WACC

99.7%92.5%

85.4%

0.3%7.5%

14.6%0%

25%

50%

75%

100%

1999 2004 2009

Equity

Debt

AOL Capital Structure

Source: Compustat, Bloomberg, Monitor Analysis

Based on comparables taken from telecom, software, and news media

Equity Beta 1.69 1.38 1.06

Debt Rating B1 BBB3 A3

WACC 15.6% 13.5% 11.0%

Percent

Copyright © 2001 Monitor Company Group LP — Confidential — CAMZKN-MFR-NIVRA 6 01-TEC 14

AOL: Continuing Value

Return on New Investment

Continuing Value35% 40% 45%

8% $55,933 $58,038 $59,674

9% $80,934 $84,474 $87,228NOPLATGrowth

10% $155,025 $162,820 $168,883

In the base case shown below, continuing value contributes 85% of total operating value (approximately $76 out of $93 per share)

Continuing value growth rate has a particularly large impact because the growth rate is very close to the ending WACC of 11%

WACC = 11% in the long run

Copyright © 2001 Monitor Company Group LP — Confidential — CAMZKN-MFR-NIVRA 6 01-TEC 15

Example:

People in Network

2 3 4 5 6

Connections (graph)

Number of Connections

1 2 + 1 = 3 3+ 2 + 1 = 6 4 + 3 + 2 + 1 = 10 5 + 4 + 3 + 2 + 1 = 15

AOL: Metcalf’s Law (Interconnectivity) Makes Scale a Sustainable

Competitive Advantage Leading to Perpetually High ROIC

Metcalf’s Law:Metcalf’s Law: I =N2 - N

2

AOL has 18 million customers 1.62 x 1014 connections MSN has 2 million customers 2.00 x 1012 connections

AOL has roughly 10 times as many customers as MSN, but roughly 100 times the number of connections

Copyright © 2001 Monitor Company Group LP — Confidential — CAMZKN-MFR-NIVRA 6 01-TEC 16

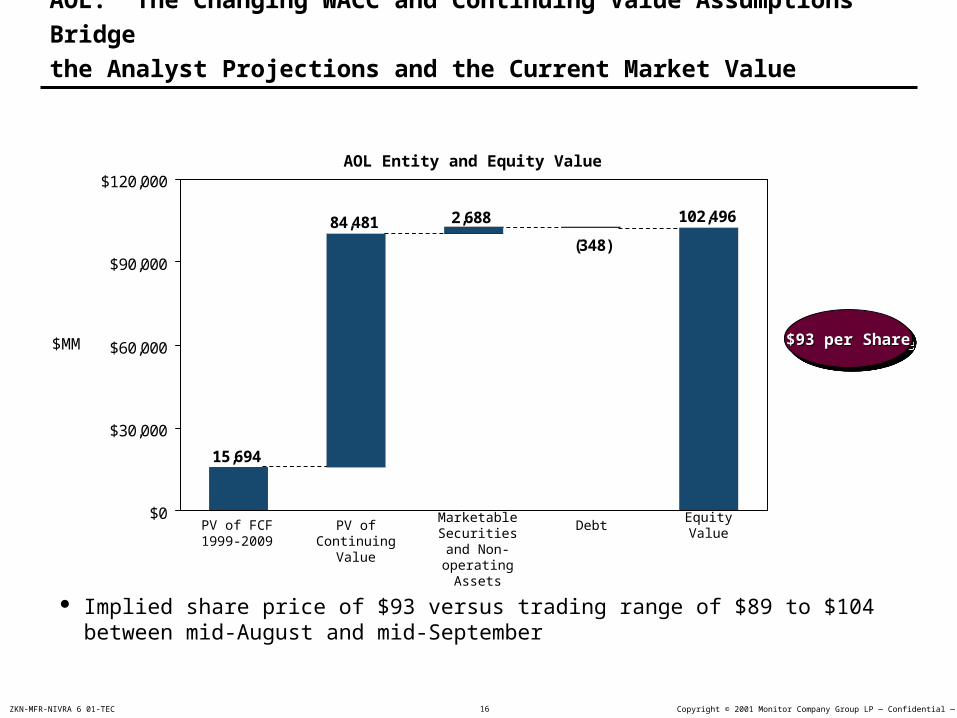

PV of FCF 1999-2009

PV of Continuing

Value

Marketable Securities and Non-operating

Assets

Debt Equity Value

AOL: The Changing WACC and Continuing Value Assumptions Bridge

the Analyst Projections and the Current Market Value

AOL Entity and Equity Value

Implied share price of $93 versus trading range of $89 to $104 between mid-August and mid-September

$MM $93 per Share$93 per Share$93 per Share$93 per Share

15,694

84,481 102,496

(348)

2,688

$0

$30,000

$60,000

$90,000

$120,000

Copyright © 2001 Monitor Company Group LP — Confidential — CAMZKN-MFR-NIVRA 6 01-TEC 17

AOL Market Ratios Decline Over Time as the Firm Matures

138.7

123.3

89.5

33.434.435.738.141.9

55.4

71.3

47.2

6.26.97.89.010.612.715.519.122.826.6

33.9

0

20

40

60

80

100

120

140

160

1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009

Price to Earning and Price to Book

P/E Ratio

P/B Ratio

Copyright © 2001 Monitor Company Group LP — Confidential — CAMZKN-MFR-NIVRA 6 01-TEC 18

Amazon.com: Amazon’s Stock* (up to August 1999)

$42

$64

$37

$124

$100

$125

$119

$172$172

$117$107 $128

$0

$50

$100

$150

$200

Sep-98 Oct-98 Nov-98 Dec-98 Jan-99 Feb-99 Mar-99 Apr-99 May-99 Jun-99 Jul-99 Aug-99

* On August 12, 1999 Amazon.com undertook a 2 for 1 stock split. As our valuation reflects the value of the company in July 1999 we will use the number of outstanding shares before the split.

Dollars

Copyright © 2001 Monitor Company Group LP — Confidential — CAMZKN-MFR-NIVRA 6 01-TEC 19

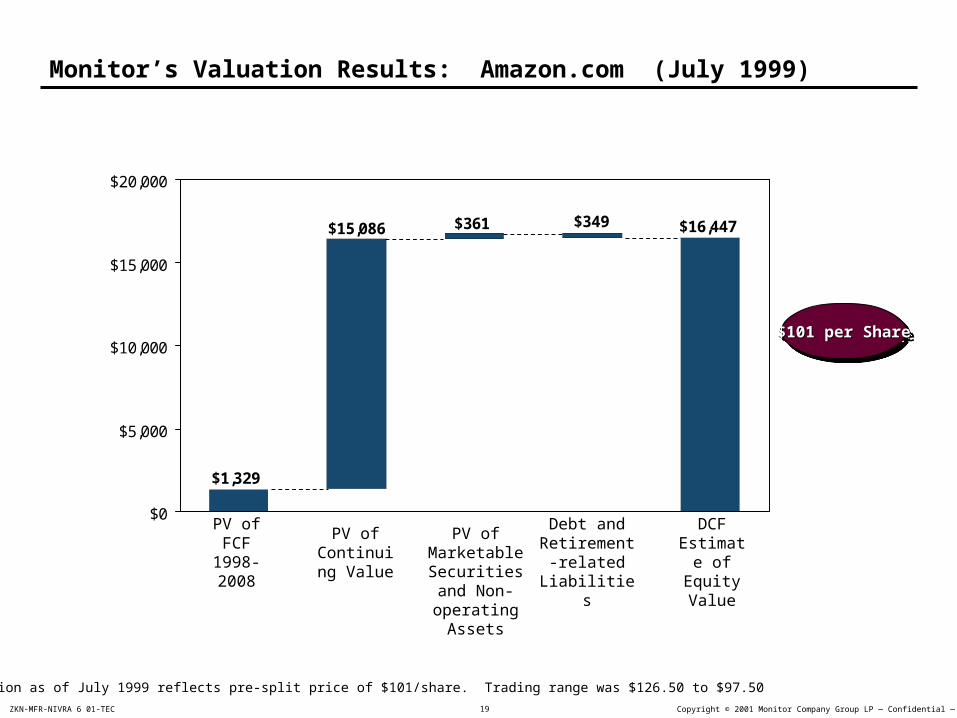

Monitor’s Valuation Results: Amazon.com (July 1999)

$361 $349 $16,447$15,086

$1,329

$0

$5,000

$10,000

$15,000

$20,000

PV of FCF 1998-2008

PV of Continuing

Value

PV of Marketable Securities and Non-operating

Assets

Debt and Retirement-

relatedLiabilities

DCF Estimate of Equity

Value

$101 per Share$101 per Share$101 per Share$101 per Share

Note: Valuation as of July 1999 reflects pre-split price of $101/share. Trading range was $126.50 to $97.50

Copyright © 2001 Monitor Company Group LP — Confidential — CAMZKN-MFR-NIVRA 6 01-TEC 20

Summary Operating Assumptions July 1999

Monitor

Revenue Growth 2000 – 50%

2001 – 39.2%

2002 onward 39.2% declining to 21%

COGS / Revenue 2000 – 77%

2001 – 76%

2002 – 74%

SG&A / Revenue 2000 – 28%

2001 – 22.4%

2002 – 15% declining to 10.5%

Capex / Revenue 2000 – 2%

2001 – 1.5%

2002 – 1.5%

Net Working Capital /Revenue

2000 – - 16%

2001 – -17.5%

2002 – - 17.5%

Copyright © 2001 Monitor Company Group LP — Confidential — CAMZKN-MFR-NIVRA 6 01-TEC 21

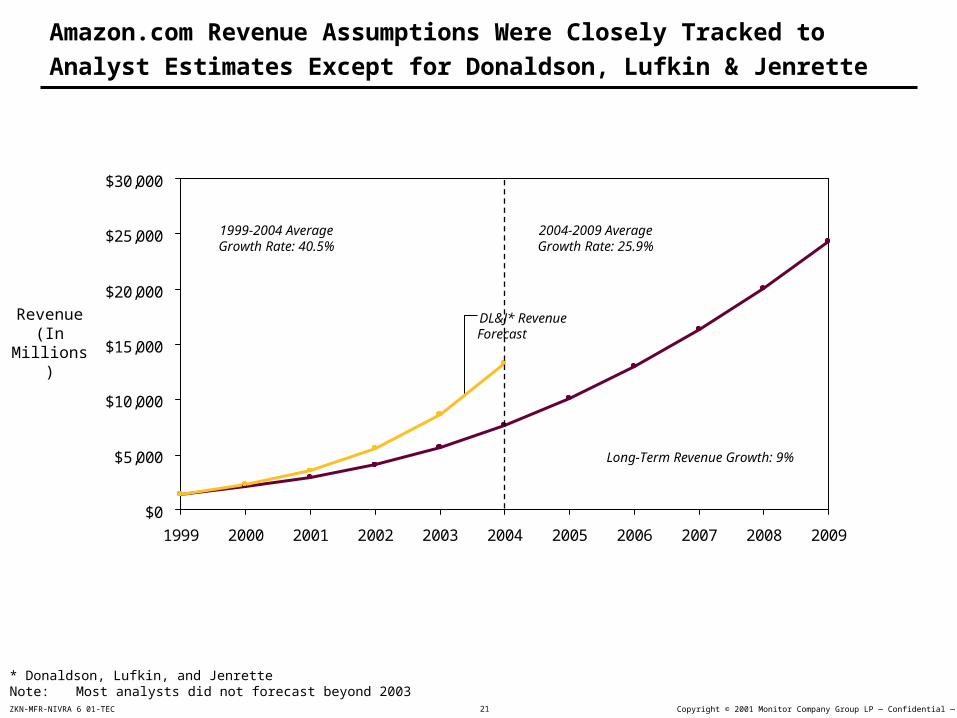

Amazon.com Revenue Assumptions Were Closely Tracked to Analyst

Estimates Except for Donaldson, Lufkin & Jenrette

$0

$5,000

$10,000

$15,000

$20,000

$25,000

$30,000

1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009

* Donaldson, Lufkin, and JenretteNote: Most analysts did not forecast beyond 2003

Revenue(In Millions)

1999-2004 Average Growth Rate: 40.5%

2004-2009 Average Growth Rate: 25.9%

Long-Term Revenue Growth: 9%

DL&J* Revenue Forecast

Copyright © 2001 Monitor Company Group LP — Confidential — CAMZKN-MFR-NIVRA 6 01-TEC 22

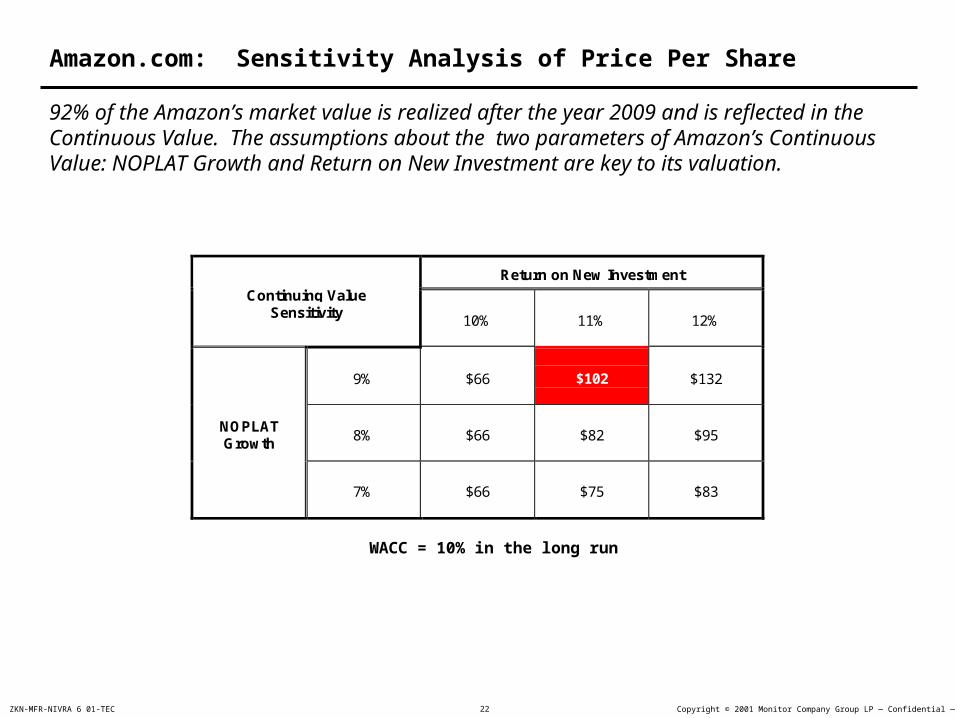

Amazon.com: Sensitivity Analysis of Price Per Share

Return on New Investment

Continuing ValueSensitivity 10% 11% 12%

9% $66 $102 $132

8% $66 $82 $95NOPLATGrowth

7% $66 $75 $83

92% of the Amazon’s market value is realized after the year 2009 and is reflected in the Continuous Value. The assumptions about the two parameters of Amazon’s Continuous Value: NOPLAT Growth and Return on New Investment are key to its valuation.

WACC = 10% in the long run

Copyright © 2001 Monitor Company Group LP — Confidential — CAMZKN-MFR-NIVRA 6 01-TEC 23

Amazon.com

Company TSR vs. S&P 500, 1999-2000

0

0.2

0.4

0.6

0.8

1

1.2

1.4

1.6

1.8

Dec-98

Jan-99

Feb-99

Mar-99

Apr-99

May-99

Jun-99

Jul-99

Aug-99

Sep-99

Oct-99

Nov-99

Dec-99

Jan-00

Feb-00

Mar-00

Apr-00

May-00

Jun-00

Jul-00

Aug-00

Sep-00

Oct-00

Nov-00

Dec-00

Jan-01

TR

S

Amazon

S&P 500

Copyright © 2001 Monitor Company Group LP — Confidential — CAMZKN-MFR-NIVRA 6 01-TEC 24

Amazon.com: Valuation Results July 1999 vs. January 2001

$ Million$ 15.3 per

share

$5,433

$2,114$1,045

$5,373

$1,130

0

1000

2000

3000

4000

5000

6000

7000

8000

9000

PV of FCF 2000 -2009

PV ofContinuing

Value

PV of ExcessCash and Non-

OperatingAssets

Total Debt DCF Estimate ofEquity Value

Value Build-Up January 2001

$15,086 $361 $349 $16,447

$1,329

$0

$5,000

$10,000

$15,000

$20,000

PV of FCF 1998-2008

PV of Continuing Value

PV of Marketable Securities and Non-operating Assets

Debt and Retirement-relatedLiabilities

DCF Estimate of Equity Value

$101 per Share$101 per Share$101 per Share$101 per Share

Note: Valuation as of July 1999 reflects pre-split price of $101/share.

Trading range was $126.50 to $97.50

Value Build-Up July 1999

Copyright © 2001 Monitor Company Group LP — Confidential — CAMZKN-MFR-NIVRA 6 01-TEC 25

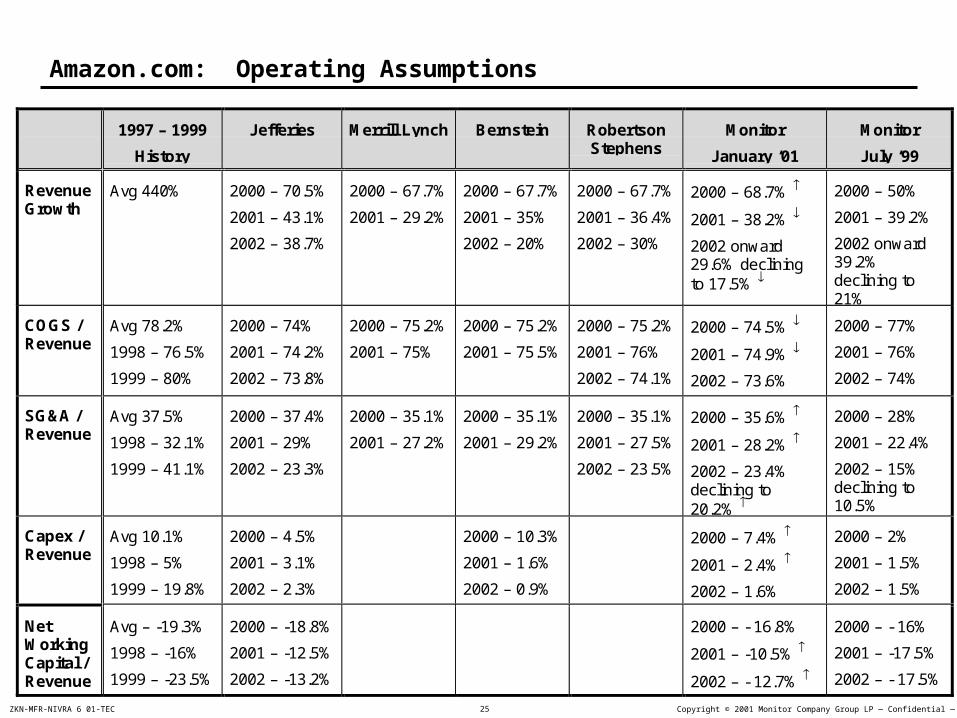

Amazon.com: Operating Assumptions

1997 – 1999

History

Jefferies Merrill Lynch Bernstein RobertsonStephens

Monitor

January ‘01

Monitor

July ‘99

RevenueGrowth

Avg 440% 2000 – 70.5%

2001 – 43.1%

2002 – 38.7%

2000 – 67.7%

2001 – 29.2%

2000 – 67.7%

2001 – 35%

2002 – 20%

2000 – 67.7%

2001 – 36.4%

2002 – 30%

2000 – 68.7%

2001 – 38.2%

2002 onward29.6% decliningto 17.5%

2000 – 50%

2001 – 39.2%

2002 onward39.2%declining to21%

COGS /Revenue

Avg 78.2%

1998 – 76.5%

1999 – 80%

2000 – 74%

2001 – 74.2%

2002 – 73.8%

2000 – 75.2%

2001 – 75%

2000 – 75.2%

2001 – 75.5%

2000 – 75.2%

2001 – 76%

2002 – 74.1%

2000 – 74.5%

2001 – 74.9%

2002 – 73.6%

2000 – 77%

2001 – 76%

2002 – 74%

SG&A /Revenue

Avg 37.5%

1998 – 32.1%

1999 – 41.1%

2000 – 37.4%

2001 – 29%

2002 – 23.3%

2000 – 35.1%

2001 – 27.2%

2000 – 35.1%

2001 – 29.2%

2000 – 35.1%

2001 – 27.5%

2002 – 23.5%

2000 – 35.6%

2001 – 28.2%

2002 – 23.4%declining to20.2%

2000 – 28%

2001 – 22.4%

2002 – 15%declining to10.5%

Capex /Revenue

Avg 10.1%

1998 – 5%

1999 – 19.8%

2000 – 4.5%

2001 – 3.1%

2002 – 2.3%

2000 – 10.3%

2001 – 1.6%

2002 – 0.9%

2000 – 7.4%

2001 – 2.4%

2002 – 1.6%

2000 – 2%

2001 – 1.5%

2002 – 1.5%

NetWorkingCapital /Revenue

Avg – -19.3%

1998 – -16%

1999 – -23.5%

2000 – -18.8%

2001 – -12.5%

2002 – -13.2%

2000 – - 16.8%

2001 – -10.5%

2002 – - 12.7%

2000 – - 16%

2001 – -17.5%

2002 – - 17.5%

Copyright © 2001 Monitor Company Group LP — Confidential — CAMZKN-MFR-NIVRA 6 01-TEC 26

Amazon.com: WACC & Continuing Value Assumptions

Monitor AssumptionsJanuary 2001

Monitor AssumptionsJuly 1999

WACC

Barra Beta

Risk Free Rate

Credit Rating

Pre-tax Cost of Debt

Cost of Equity

WACC

2.09

5.3%

B

10.9% (Debt / Total Capital(market value) 21.7%)

16.8% (Equity / Total Capital(market value) 78.3%)

14.5% declining to 10% by 2009

1.91

6.3%

B

11.8% (Debt / Total Capital(market value) 2.1%)

16.8% (Equity / Total Capital(market value) 97.9%)

16.6% declining to 10% by 2009

Continuing Value

Growth in NOPLAT

Return on Net NewInvestments

9%

11%

9%

11%

Copyright © 2001 Monitor Company Group LP — Confidential — CAMZKN-MFR-NIVRA 6 01-TEC 27

Changes in Value are at the Heart of Economic Decision-Making

Discounted Cash Flow Valuation DCF

Real Options Analysis

Expectations-Based Management Expectations-Based Management

Copyright © 2001 Monitor Company Group LP — Confidential — CAMZKN-MFR-NIVRA 6 01-TEC 28

Metric Critique

Sales Growth Ignores profitability, ignores balance sheet

EPS Ignores balance sheet

EPS Growth Ignores balance sheet

ROIC = EBIT / Invested Capital Encourages harvesting behavior

ROIC-WACC* Encourages harvesting

EVA=(ROIC-WACC) x Invested Capital Not correlated with TRS

Rational Expectations Best of short-term metrics

An Example:

Performance Measurement

Most traditional performance metrics create perverse incentives to management. Only Rational Expectations focuses on shareholder value creation

Copyright © 2001 Monitor Company Group LP — Confidential — CAMZKN-MFR-NIVRA 6 01-TEC 29

Sears** Wal-Mart

1994 1995 1996 1997 CAGR 1994 1995 1996 1997 CAGR

Sales Revenue (billions)

$54.6 $34.9 $38.2 $41.3 -8.9% $82.5 $93.6 $104.9 $118.0 12.7%

EBIT (billions) $3.4 $3.1 $3.5 $3.9 4.7% $3.6 $4.1 $4.1 $4.4 6.9%

Net Income (billions)*** $1.2 $1.0 $1.3 $1.2 0.0% $2.6 $2.7 $3.1 $3.5 10.4%

ROIC 19.5% -5.3% -4.2% -5.2% — 10.4% 8.9% 8.9% 9.8% —

WACC 9.1% 7.3% 8.1% 7.5% — 12.5% 10.0% 11.0% 10.6% —

ROIC-WACC 10.4% -12.6% -12.3% -12.7% — -2.1% -1.1% -2.1% -0.8% —

Invested Capital (billions)

$21.66 $28.20 $30.19 $34.22 16.5% $29.84 $33.54 $34.56 $36.60 7.0%

Economic Profit (billions)

$2.24 -$3.56 -$3.72 -$4.33 — -$0.63 -$0.36 -$0.73 -$0.28

Change in EP (billions)

-5.80 -0.16 -0.61 — 0.27 -0.37 0.45

* Sears “destroyed” on aggregate of $9.37 billion while Wal-Mart “destroyed” $2.00 billion** Excludes Allstate*** Before extraordinary items

Which Company Did Better?

Sears vs. Wal-Mart

A good example is found in the comparison between Wal-Mart and Sears over the 1994–1997 four-year interval. Can you tell from the data below which company had superior total return to shareholders?

Copyright © 2001 Monitor Company Group LP — Confidential — CAMZKN-MFR-NIVRA 6 01-TEC 30

0.0

0.5

1.0

1.5

2.0

2.5

3.0

1/94

3/94

5/94

7/94

9/94

11/9

41/

953/

955/

957/

959/

95

11/9

51/

963/

965/

967/

969/

96

11/9

61/

973/

975/

977/

979/

97

Sears Index

Wal-Mart Index

Total Returns to ShareholdersSears vs. Wal-Mart, 1994–1997

Total Return

Between January 1994 and December 1997 the Total Return to Shareholders of Sears

Was Consistently Higher Than the Total Return to Shareholders of Wal-mart

Copyright © 2001 Monitor Company Group LP — Confidential — CAMZKN-MFR-NIVRA 6 01-TEC 31

Sears

7/18/97 “Excluding unusual items, yesterday’s earnings report signals that the four-year old rebound at Sears stores is continuing . . . The better-than-expected results prompted several analysts to raise their Sears earnings forecasts.”

Wal-Mart

11/18/96 “They gradually recognize that the gap between expected and reported earnings has narrowed. Wal-Mart’s earnings fell off the table and its stock never fell way down. It just stopped going up as investors rotated into other types of names.”

5/17/94 “Wal-Mart Stores Inc.’s earnings soared in its first fiscal quarter while profit sank at Kmart Corp. Analysts had expected Wal-Mart to perform a bit better. . . . In Big Board composite trading yesterday, Wal-Mart shares fell $1.25 a share to close at $22.75.”

A Search of News Articles Provides a Clear Message That Sears Repeatedly Exceeded

the Market’s Expectations While Wal-Mart Met or Fell Short of Expectations

Quotations

Copyright © 2001 Monitor Company Group LP — Confidential — CAMZKN-MFR-NIVRA 6 01-TEC 32

Changes in Analyst Expectations Match Chevron’s TSR

Chevron CorpMarket-Adjusted TSR vs. Analyst Earnings Estimates, 1991-1998

1.5

2

2.5

3

3.5

4

4.5

5

5.5

Jan-

90

Jul-9

0

Jan-

91

Jul-9

1

Jan-

92

Jul-9

2

Jan-

93

Jul-9

3

Jan-

94

Jul-9

4

Jan-

95

Jul-9

5

Jan-

96

Jul-9

6

Jan-

97

Jul-9

7

Jan-

98

Jul-9

8

EP

S

0

0.2

0.4

0.6

0.8

1

1.2

1.4

Mar

ket-

Adj

uste

d TS

R

1991 1992

1993

1994

1995

1996

1997

1998

Note: EPS and analyst expectations exclude extraordinary items

Negative shareholder

return

Negative shareholder

return

Positive Earnings Growth

Positive Earnings Growth

Drop in Analyst

Expectations

Drop in Analyst

Expectations

During 1995, Chevron’s earnings rose, but shareholder return was negative. Why? Because during the year market expectations declined

Copyright © 2001 Monitor Company Group LP — Confidential — CAMZKN-MFR-NIVRA 6 01-TEC 33

Analyst’s expectations of Coca Cola remained fairly constant during 1995 and 1996. However, falling expectations during 1997 and 1998 resulted in below market stock performance

1.0

1.1

1.2

1.3

1.4

1.5

1.6

1.7

1.8

1.9

2.0

Analyst Expectations of Coca-Cola EPS, 1995–1998: The Asian Crisis

Earnings per Share(adjusted for splits)

2 Years Ahead 1 Year Ahead

1 Year Ahead

2 Years Ahead 1 Year Ahead

1.18

1.41

1.67

1995 1996 1997 1998

Number of Analysts: 25 2527 22 22 20 20 19

Source: IBES, Monitor Analysis

1 Year Ahead

Expectations for Current Year (1 Year Ahead)Expectations for Next Year (2 Years Ahead)Actual Earnings Reported (Annual) 2 Years Ahead

Copyright © 2001 Monitor Company Group LP — Confidential — CAMZKN-MFR-NIVRA 6 01-TEC 34

0.4

0.6

0.8

1.0

1.2

1.4

Jan-

95

Mar

-95

May

-95

Jul-9

5

Sep

-95

Nov

-95

Jan-

96

Mar

-96

May

-96

Jul-9

6

Sep

-96

Nov

-96

Jan-

97

Mar

-97

May

-97

Jul-9

7

Sep

-97

Nov

-97

Jan-

98

Mar

-98

May

-98

Jul-9

8

Coca-Cola Total Return to Shareholders Relative to the Market 1995–1998

Expectations Revised Downward

. . . And Its Total Return to Shareholders Relative to the Market

Copyright © 2001 Monitor Company Group LP — Confidential — CAMZKN-MFR-NIVRA 6 01-TEC 35

Total Shareholder Return (TSR) Regression Results*

Traditional Performance Measures

Performance Measure Number of

Observations Adjusted R-

squared

Basic EPS (Scaled by Lagged Share Price) 2,522 4.5 %

Change in Basic EPS 2,522 5.1%

EVA (Scaled by Lagged Market Value) 2,182 0.3 %

Change in EVA 2,182 3.0 %

*The dependent variable for all regressions is market-adjusted TSR. Sample includes S&P 500 firms during 1992–98

Traditional performance metrics like EPS and EVA® are very poor predictors of returns to shareholders

Copyright © 2001 Monitor Company Group LP — Confidential — CAMZKN-MFR-NIVRA 6 01-TEC 36

Multiple Regression Results*

* S&P 500 firms during 1992–98. Sample has 2,390 observations

Variable Representing Changes in Analyst

Expectations

Regression Coefficients (T-Statistics in Parentheses)

Percent Change in Analyst Forecasts of Current Year's Earnings (EPS)

-0.01 (-0.34)

Percent Change in Analyst Forecasts of Next Year's Earnings (EPS)

0.70 (21.3)

Change in Analyst Forecasts of Long-Term (3–5 year) EPS Growth

8.6 (12.9)

Adjusted-R2 41.6%

Expectations about current earnings have no significant

impact on TSR

Expectations about current earnings have no significant

impact on TSR

Expectations about next year and long-term earnings have

significant impact on TSR

Expectations about next year and long-term earnings have

significant impact on TSR

Multiple regressions of market-adjusted total shareholder return (TSR) vs. changes in analyst earnings (EPS) expectations indicate a strong correlation between expectations and returns

Correlation is much higher than traditional metrics (EPS, EVA®)

Correlation is much higher than traditional metrics (EPS, EVA®)

Copyright © 2001 Monitor Company Group LP — Confidential — CAMZKN-MFR-NIVRA 6 01-TEC 37

Two Examples

Actual ROIC 200x WACC

Business A 30% 10%

Business B 5% 10%

Market Expected ROIC 200x

Management’s Revised Expectations 200x

Project X 40% 40%

Project Y 40% 20%

Which business unit did better?

Two projects are expected to earn 40% each and the cost of capital is 10%

Should we invest?

Copyright © 2001 Monitor Company Group LP — Confidential — CAMZKN-MFR-NIVRA 6 01-TEC 38

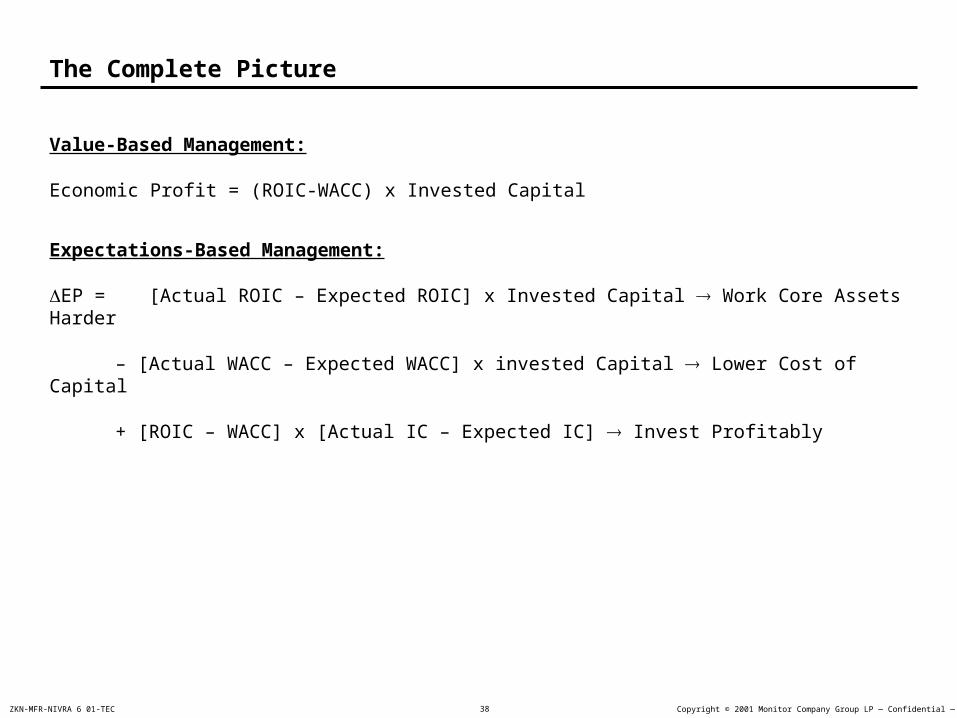

The Complete Picture

Value-Based Management:

Economic Profit = (ROIC-WACC) x Invested Capital

Expectations-Based Management:

EP = [Actual ROIC – Expected ROIC] x Invested Capital Work Core Assets Harder

– [Actual WACC – Expected WACC] x invested Capital Lower Cost of Capital

+ [ROIC – WACC] x [Actual IC – Expected IC] Invest Profitably

Copyright © 2001 Monitor Company Group LP — Confidential — CAMZKN-MFR-NIVRA 6 01-TEC 39

Integrated Framework for Expectations-Based Management

Operating Value Drivers, e.g.,

Cycle time

Customer retention rate

Churn rate

Non-performing loan rate

Operating Value Drivers, e.g.,

Cycle time

Customer retention rate

Churn rate

Non-performing loan rate

Actual vs. Expected

Annual Economic Profit

Actual vs. Expected

Annual Economic Profit

DCF ValueDCF ValueDrivesSummed

Over Time

Shareholder Value~~

Used by all levels of organization to set goals and measure

performance; used for benchmarking and sensitivity analysis

Measures short-term overall performance

by business

Value and compare strategies; measure long-term trade-offs

Together, DCF, EP, and value drivers form an integrated framework for value creation. DCF is comprehensive, long-term based, EP is a comprehensive, short-term measure, and value drivers are specific, short-term measures

EBM

Copyright © 2001 Monitor Company Group LP — Confidential — CAMZKN-MFR-NIVRA 6 01-TEC 40

Implications

Need to set expectations correctly with:

– Analysts, and shareholders

– Internal management team

Need to exceed expectations to have TRS exceed cost of equity

Take all new investments that are expected to have ROIC > WACC

Avoid the expectations treadmill with a two part incentive design

TRS = Cost of equity

+ Unexpected company performance

+ Unexpected market movements

Total Compensation = Salary + Bonus

Salaryt = f (Financial Performance in year t-1)

Bonust = f (Exceeding Expectations for year t )

Copyright © 2001 Monitor Company Group LP — Confidential — CAMZKN-MFR-NIVRA 6 01-TEC 41

Changes in Value are at the Heart of Economic Decision-Making

Discounted Cash Flow Valuation DCF

Expectations-Based Management

Real Options Analysis Real Options Analysis

Copyright © 2001 Monitor Company Group LP — Confidential — CAMZKN-MFR-NIVRA 6 01-TEC 42

Source: Dixit and Pindyck in Investment Under Uncertainty, Princeton University Press, 1994

Simple Investment Decision — Introduction

IllustrativeIllustrative

Facts:

Investment outlay = $1,600

Once made, the investment is irreversible

Replacement expense equals depreciation

Perpetual level cash inflows

Price level = $200 now

50 / 50 chance of price changing to $300 or $100 in one year

The price will stay at its new level forever

Cost of capital = 10%

200

(1.1)t

NPV = -1600 +

= -1600 + 2200

= 600

t=0

Consider the net present value approach to the following simple investment. When the expected cash flows are discounted at the cost of capital, the NPV is $600 and the decision is to invest. However . . .

Copyright © 2001 Monitor Company Group LP — Confidential — CAMZKN-MFR-NIVRA 6 01-TEC 43

. . . We have made an implicit assumption. We do not have to invest immediately, we can defer. If the project is deferred one year, it is possible to take advantage of price information. We would invest only if the price goes up. Regardless of whether it goes up or down, the NPV with deferral is $733 today

-1600

1.1NPV = .5

t=1

300

(1.1)t+ + .5

-1600

1.1

t=1

100

(1.1)t+

-1600 + 3300

1.1= .5 + .5

-1600 + 1100

1.1

= .5 + .5 [0]1700

1.1

= = $733850

1.1

Conclusion: Since the NPV of deferring is $133 higher than investing immediately, we would choose to defer, even though the NPV of investing immediately is large and positive

Do not invest if price falls to

$100

Do not invest if price falls to

$100

The Investment Decision as a Deferral Option

Copyright © 2001 Monitor Company Group LP — Confidential — CAMZKN-MFR-NIVRA 6 01-TEC 44

-1600

1.1NPV = .5

t=1

400

(1.1)t+ + .5

-1600

1.1

t=1

0

(1.1)t+

-1600 + 4400

1.1= .5 + .5

-1600 + 0

1.1

= .5 + .5 [0]2800

1.1

= = $1,2731400

1.1

Conclusion: The value of the deferral option goes up as there is greater uncertaintyPossible Macroeconomic Implication: Greater uncertainty in the economy (e.g., due to political unrest; uncertainty about taxes, interest rates or inflation) can cut investment because the deferral option becomes more valuable

Do not invest if price falls to $0Do not invest if price falls to $0

The value of deferral is a call option that is exercised when the irreversible investment is undertaken. The value of this option is affected by variance of prices (or costs), by the level of prices, by the scale of investment, by the level (and variance) of interest rates, and by the length of time that the deferral option lasts

Suppose the price in the previous example is equally likely to go to $400 or $0 (rather than $300 or $100)

The Value of a Deferral Option Increases with Variance

Copyright © 2001 Monitor Company Group LP — Confidential — CAMZKN-MFR-NIVRA 6 01-TEC 45

In environments with high uncertainty and room for managerial flexibility investments will have considerable option (strategic) value, which needs to be considered

An Option — Definition

Is the right but not the obligation to take an action (at a cost, called the exercise price) for a predetermined period of time (called the maturity of the option). Options capture the element of flexibility in decision-making

Financial Option

The option is contingent on the uncertain value of a financial security, e.g.,a CBOE call on a stock

Real Option

The option is contingent on the uncertain value of a real asset, e.g., an irreversible investment opportunity in a new project

An option:

Management Can Affect the Value of the

Underlying Real Asset

Management Can Affect the Value of the

Underlying Real Asset

A Side BetA Side Bet

Copyright © 2001 Monitor Company Group LP — Confidential — CAMZKN-MFR-NIVRA 6 01-TEC 46

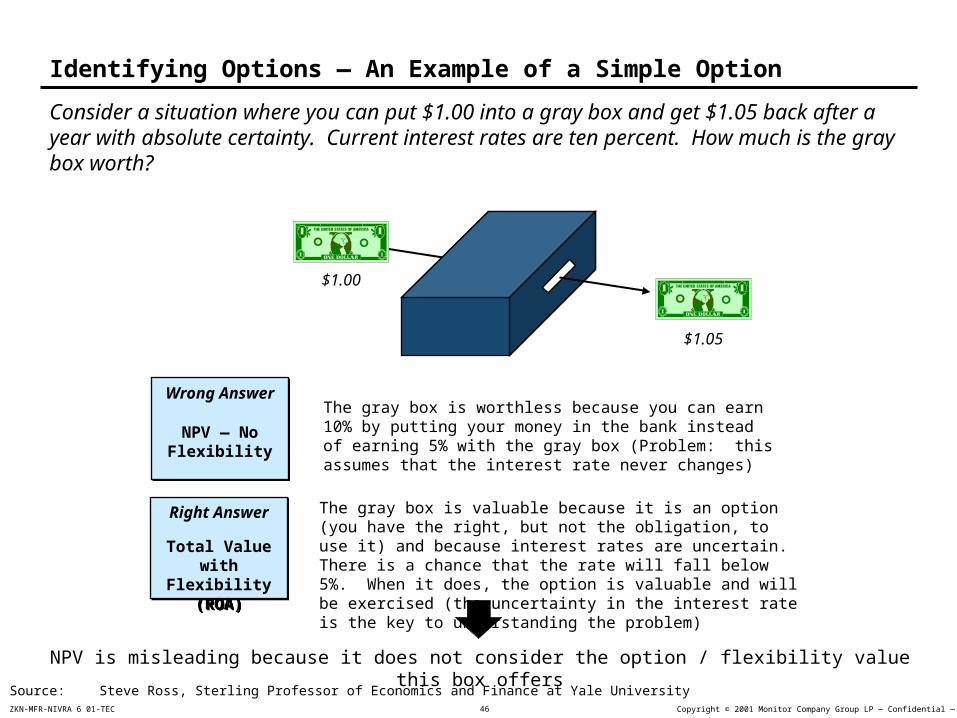

Identifying Options — An Example of a Simple Option

Wrong Answer

NPV — No Flexibility

Wrong Answer

NPV — No Flexibility

Right Answer

Total Value with Flexibility

(ROA)

Right Answer

Total Value with Flexibility

(ROA)

The gray box is worthless because you can earn 10% by putting your money in the bank instead of earning 5% with the gray box (Problem: this assumes that the interest rate never changes)

The gray box is valuable because it is an option (you have the right, but not the obligation, to use it) and because interest rates are uncertain. There is a chance that the rate will fall below 5%. When it does, the option is valuable and will be exercised (the uncertainty in the interest rate is the key to understanding the problem)

NPV is misleading because it does not consider the option / flexibility value this box offers

$1.00

$1.05

Source: Steve Ross, Sterling Professor of Economics and Finance at Yale University

Consider a situation where you can put $1.00 into a gray box and get $1.05 back after a year with absolute certainty. Current interest rates are ten percent. How much is the gray box worth?

Copyright © 2001 Monitor Company Group LP — Confidential — CAMZKN-MFR-NIVRA 6 01-TEC 47

When is Managerial Flexibility Valuable?

Moderate Flexibility Value

HighFlexibility Value

HighFlexibility Value

Low Flexibility Value

Low Flexibility Value

ModerateFlexibility Value

ModerateFlexibility Value

High

Low

Low HighLikelihood of Receiving New InformationLikelihood of Receiving New Information

Uncertainty

Ro

om

fo

rM

an

ag

eri

al

Fle

xib

ilit

y

Ab

ilit

y t

o r

es

po

nd

Flexibility Value Greatest When:

1. High uncertainty about the future Very likely to receive new

information over time2. High room for managerial flexibility

Allows management to respond appropriately to this new information

1. High uncertainty about the future Very likely to receive new

information over time2. High room for managerial flexibility

Allows management to respond appropriately to this new information

+

3. NPV without flexibility near zero If a project is neither obviously

good nor obviously bad, flexibility to change course is more likely to be used and therefore is more valuable

3. NPV without flexibility near zero If a project is neither obviously

good nor obviously bad, flexibility to change course is more likely to be used and therefore is more valuable

Under these conditions, the difference between ROA and other decision tools is substantial

Under these conditions, the difference between ROA and other decision tools is substantial

In every scenario flexibility value is greatest when the project’s value without flexibility is close to break evenIn every scenario flexibility value is greatest when the project’s value without flexibility is close to break even

The flexibility value comes from the ability to respond to information that may be received in the future. The greater the likelihood that this new future information will elicit a managerial response and alter the course of a project, the more value the option will have

Copyright © 2001 Monitor Company Group LP — Confidential — CAMZKN-MFR-NIVRA 6 01-TEC 48

ToToToTo

Applicability — Progress to Date

The complication is that although real options are valuable, up to now option valuation has been an esoteric subject accessible only to those trained in stochastic calculus and other advanced mathematics. Recent advances in theory and technology, however, have allowed us to implement option pricing capability in simple algebraic formulas in Excel spreadsheets. Moreover, we can now handle more complicated situations when there are multiple sources of uncertainty that are not necessarily traded world commodities

FromFromFromFrom

Source of uncertainty not necessarily market priced

Algebra and Excel spreadsheets

Multiple sources of uncertainty(rainbow options)

Options on options (compound options, learning options)

Many applications

Source of uncertainty not necessarily market priced

Algebra and Excel spreadsheets

Multiple sources of uncertainty(rainbow options)

Options on options (compound options, learning options)

Many applications

Uncertainty driven by world commodity product

Higher mathematics necessary for application

Single source of uncertainty

Simple options

Limited application

Uncertainty driven by world commodity product

Higher mathematics necessary for application

Single source of uncertainty

Simple options

Limited application

Copyright © 2001 Monitor Company Group LP — Confidential — CAMZKN-MFR-NIVRA 6 01-TEC 49

American Call — Deferral Option

Coal Lease Valuation

This first example is a simple deferral option on the development of a coal lease for up to five years after the lease was acquired

Comments

Single source of uncertainty — price of coal

NPV approach ignored flexibility

Option was particularly valuable because it was “near-the-money”* (options on deep in-the-money situations are not worth much because you invest immediately)

$116

$72

$59

0

25

50

75

100

125

NPV Valuation (NoFlexibility)

Successful Bid Option Value withDeferral

Dollars (Millions)

$57

* The price of coal was close to the cost of extraction

Copyright © 2001 Monitor Company Group LP — Confidential — CAMZKN-MFR-NIVRA 6 01-TEC 50

It was possible to value cancelable operating leases because there is a relatively active market in second hand aircraft

Comments

Single source of uncertainty — price of second hand aircraft

Option value significantly underestimated by management

Leasing strategy changed

19%3%

16%

0%

5%

10%

15%

20%

25%

Pre-DeliveryPut Option

Walk-AwayOption

Total

Percent of Engine Price

83%25%

58%

0%

30%

60%

90%

Pre-DeliveryPut Option

Walk-AwayOption

Total

Wide-Body Aircraft Narrow Body Aircraft

American Put — Cancelable Operating Lease

The Value of Cancelable Operating Leases on Aircraft

Percent of Engine Price

Copyright © 2001 Monitor Company Group LP — Confidential — CAMZKN-MFR-NIVRA 6 01-TEC 51

Switching Option

The Value of Switching Options in Mining

Switching options apply to any situation where it is possible to shut down then reopen an operation

Comments

Study provided insight into when to open up and shut down operations

Single source of uncertainty

Value depended on the quantity of mineral in the ground, extraction costs, and the fixed cost of startup or shutdown, in addition to the usual list of variables

FlexibilityValue

Dollars (Millions)

$1,160

$710

$447

0

500

1,000

1,500

Initial NPV Estimate Scenario BasedNPV

Total

Copyright © 2001 Monitor Company Group LP — Confidential — CAMZKN-MFR-NIVRA 6 01-TEC 52

Despite the strong growth, consumer PC assembly players have found their market participation to be mostly dissatisfying as they are not earning their cost of capital

-2.3%

-1.5%

8.2%

11.0%

12.5%

-6.0%

-10% 0% 10% 20%

Consumer PCAssembly

Automobiles

ConsumerElectronics

Sports Shoes

Commercial IT

Beverages

Consumer Markets

Switching Option

Exit and Reentry Decision

Source: Analyst Reports; Annual Statements

-7.0%

-4.1%

-2.0%

29.7%

-11.0%

-20% 0% 20% 40%

Packard Bell

Apple

Compaq

Acer

Gateway

Consumer PC Assembly

Spread: ROIC–WACC Spread: ROIC–WACC

Copyright © 2001 Monitor Company Group LP — Confidential — CAMZKN-MFR-NIVRA 6 01-TEC 53

ROA Gives Different Decisions Than NPV and Economic Profit

Scenario ROV NPVEconomic Profit(WACC = 13.7%)

In Operation, Gross Margin = 13% Continue Continue Exit (ROIC = 7.6%)

In Operation, Gross Margin = 11% Continue Exit Exit (ROIC = 5.6%)

Not in Operation Don’t Enter Don’t Enter Don’t Enter (ROIC = 7.6%)

Traditional valuation techniques give mixed decisions about whether the unprofitable players should immediately exit the business. However, ROA suggests that players should stay in the market and exit only if conditions do not improve

Valuation Methodologies

Copyright © 2001 Monitor Company Group LP — Confidential — CAMZKN-MFR-NIVRA 6 01-TEC 54

ROA Gives Different Values* of Staying in Business than NPV and EP

Gross Operating Margin ROA

NPV + Flexibility Value

NPV (Cash Flows)

Economic Profit

(Short Term)

(ROIC–WACC) x IC

15% $2.98 $2.62 $0.05

13% $1.71 $1.02 -$0.07**

11% $0.79 -$0.59 -$0.09

9% $0.36 -$1.79 -$0.11

ROA gives significantly different value to the business than EP and NPV approaches (1997, $Billions)

Valuation Methodologies

* Assume a volatility of 16% annually for the gross operating margin (GOM)** ROIC before taxes = 7.6%, tax rate = 30%, WACC = 13.7%, invested capital is 26% of sales of $3.6 billion

Copyright © 2001 Monitor Company Group LP — Confidential — CAMZKN-MFR-NIVRA 6 01-TEC 55

Today (year 0), management does not need to commit to the entire project; it can simply begin the design process (at a cost of $50 million) and learn more about the operating spread uncertainty. Six months later, management has a similar option, to begin the pre-construction process without a full commitment and learn more about the uncertainties. At the end of the year, management no longer has the flexibility to learn more about the uncertainty and must choose between a full commitment or abandonment

Year 0 Six Months End of Year 1

Decision Node

Invest $50 million for design process only

Invest $50 million for design process only

Full commitment — no flexibility Full commitment — no flexibility

Abandon — no flexibility Abandon — no flexibility

Invest $200 million only to start pre-construction work

Invest $200 million only to start pre-construction work

Full commitment — no flexibility Full commitment — no flexibility

Abandon — no flexibility Abandon — no flexibility

Full commitment — invest $400 million

Full commitment — invest $400 million

Abandon Abandon

Uncertainty evolves but we cannot react

Eliminated managerial flexibility, and therefore destroyed option value

Uncertainty evolves but we cannot react

Eliminated managerial flexibility, and therefore destroyed option value

Compound Option — Multiphase investment

The Value of Compound Options in Plant Construction

Copyright © 2001 Monitor Company Group LP — Confidential — CAMZKN-MFR-NIVRA 6 01-TEC 56

The Source of Uncertainty

0

200

400

600

800

1,000

1,200

1,400

1Q79 4Q79 2Q81 1Q81 1Q82 3Q83 2Q84 1Q85 4Q85 3Q86 2Q87 1Q88 4Q88 3Q89 2Q90 1Q91 4Q91 3Q92 2Q93 1Q94 4Q94 3Q95 2Q96 4Q96

Operating Spread = Output Price / Ton – Input

At first there seems to be two sources of uncertainty: the price of the output per ton, and the cost of the input per ton. However, these can be combined into a single source of uncertainty, the operating spread

Estimated Data Estimated Data

Output Price

Input Price

Price History — First Quarter 1979 to Fourth Quarter 1996

Copyright © 2001 Monitor Company Group LP — Confidential — CAMZKN-MFR-NIVRA 6 01-TEC 57

Summary — Phased Investment

$ Millions

The traditional NPV approach dramatically undervalues this investment since it does not consider the value of flexibility. Since this is a multi-staged investment, management has the flexibility to re-evaluate the project at each stage and refine their strategy based on new information. A full commitment (to either accept or abandon) eliminates managerial flexibility and destroys the option (flexibility) value

- $71.2

$354.5 $425.7

NPV Valuation: No Flexibility

Flexibility Value Total Value (ROA)

Copyright © 2001 Monitor Company Group LP — Confidential — CAMZKN-MFR-NIVRA 6 01-TEC 58

Planned

Abandon

Planned + 50%

Planned

Abandon

The decision tree below shows a stylized version of the decision to develop a large energy resource. There were two sources of uncertainty, the price of energy and the amount of resource in the ground, and there were compound options

Illustrative

* Simplified for illustrative purposes** Capacity planned before ROA analysis

11

11

11

11

11

11

Assumed decision nodes

Initial capacity decision

Year 3 initial capacity decision

Year 11 capacity addition decision

Exploration decision

Event nodes (uncertain outcomes) Prices go up or down? Reserves in existing fields are

higher or lower than EV? Resource quantity found in 4 add-

on fields worth developing or not?

1

3

11

E

OPM Cases

Capacity “lock-in”

Defer capacity decision and exploration

Defer capacity decision / explore today

1

2

3

Planned capacity 50% of planned capacity Abandon

Planned capacity 50% of planned capacity Abandon

11

11

11

1

Planned capacity** plus 50%

Planned capacity*

Abandon

Planned capacity** + 50%

Planned

Abandon

Planned + 50% 11

11

11

E

$ High

2

2

2

$ Low

Explore

E How much to invest in exploration during Year 1 through Year 3?

What capacity to lock-in in Year 3?

Do not explore in the near term

95

What capacity level to lock into today?

Lock in capacity now

1

3

Defer capacity decision

Explore in the interim? (Year 1-Year 3)

Lock in capacity today or defer decision until Year 3?

Add capacity in Year 11?

2

Compound Rainbow Option

Exploration and Development

Copyright © 2001 Monitor Company Group LP — Confidential — CAMZKN-MFR-NIVRA 6 01-TEC 59

OPM Case

A. Initial Capacity

Decision

B. Exploration

Decision

C. Add-on Capacity

Decision

No-options base case †

Capacity "lock-in"

Year 6

Defer capacity decision and exploration

Year 3 Year 6

Defer capacity decision / explore today

Year 3

ROA Model Valuation Results*

The optimal solution provided more than twice the value and was completely different from the client’s base case

225

200

150

100

0 100 200

Total Project Value Estimates**

Normalized Currency Units

* Throughout the document the results have been normalized and rounded off to provide general insights while maintaining client confidentiality** For comparison purposes and because of lack of information, each of the 4 cases assume a Year 1 exploration cost equal to 0; if “best-guess” exploration

cost of estimates of 40 is used, the NPV for the 3 option cases are 120, 175, and 185, respectively† Analogous to traditional DCF case (i.e., assumes deterministic inputs and no managerial flexibility)

11

22

33

+Value of reserve size information

Value of price information

Value of Better capacity

lock in decision Exploration option Expansion option

Today (planned capacity)

Today(No exploration)

Today(No exploration)

Today (planned capacity +50%)

TodayExplore

Most attractive operating plan

Year 11

Year 11

Year 11

Copyright © 2001 Monitor Company Group LP — Confidential — CAMZKN-MFR-NIVRA 6 01-TEC 60

Classic Questions and Their Answers

1. Option values are contingent on the current value and the expected volatility of the underlying security or asset. If one holds a call option on a share of stock, the market price is observable and we can estimate the expected volatility. But a real option is contingent on an asset that is not traded in a capital market (e.g., a cure for baldness). What do we do?Marketed Asset Disclaimer (MAD): We assume that the present value of the asset without flexibility is the same as the market price for which the underlying asset (without flexibility) can be bought or sold

2. Lattices (Binomial tress in particular) are a discrete approach to modeling the Gauss-Wiener continuous scholastic process that Black-Scholes assumed for the underlying security when they derived the closed-form solution For European call options. But, project cash flows do not follow, or even roughly approximate a “regularized” binomial latticeProperly Anticipated Process Fluctuate Randomly (PAP): Paul Samuelson proved that the bid of any pattern of the future cash flows contains all expectations and therefore moves randomly through time (obeying a Gauss-Wiener Process), deviating only with unexpected changes in the problem of cash flows

Copyright © 2001 Monitor Company Group LP — Confidential — CAMZKN-MFR-NIVRA 6 01-TEC 61

-20-10

2010

3020

1020

40

A Four-Step Process

Free Cash Flows

PV Free CashFlow

Year

0 1 2 3 4 5 6 7 8

PV

Value

Year

Cash In

Cash Out

Free Cash Flows1 2 . . . . . . 10 CV

Price

Quantity

Variable Cost

Interest Rates

The Year Spread Sheet

Evolution of Project Value

Value (t = 1) n (V1 / V0) = r

Monte CarloSimulation

V0

uV

dV

u2V

duV

d2V

u3V

u2dV

d2uV

d3V

Event Tree(Sans

Dividends)

Step One

Complete the base case present value (without flexibility) based on

– Expected future free cash flows– Cost of capital based on

comparables

Step Two Estimate the volatility of the value of

the project in order to derive the volatility of the rate of return

– A Monte Carlo approach can combine many uncertainties

– The volatility of the drivers of uncertainty may be estimated from internal data or from subjective estimates made by management

The output is a binomial lattice in value

Note that the expected value of the project evolves through time as shown in the figure to the right

udeu /1, T

WACC = 10%

Copyright © 2001 Monitor Company Group LP — Confidential — CAMZKN-MFR-NIVRA 6 01-TEC 62

Four Step Process (cont.)

Go, StopGo, Stop

Expand, AbandonExpand, Abandon

Expand, AbandonExpand, Abandon

Expand, ContractExpand, Contract

Expand, ContractExpand, Contract

Expand, AbandonExpand, Abandon

ROA0

Go

ROA2

Expand

ROA1

Abandon ROA2

Abandon

ROA1

GoROA2

Go

Step Three

Put decisions into the nodes of the event tree

– Can have multiple decisions per node

– Payouts may include cash flows as dividends

Step Four

Work backward in the tree (unless there is path dependency) to obtain values at each node and to make optimal decisions

– Use no arbitrage condition to conform to law of “one price”

– Output is the value of the project with flexibility and decision rules

Copyright © 2001 Monitor Company Group LP — Confidential — CAMZKN-MFR-NIVRA 6 01-TEC 63

Project Analysis

Overall Approach — A Four Step Process

Objectives

Comments

Compute base case present value without flexibility at t = 0

Value the total project using a simple algebraic methodology

Identify major uncertainties in each stage

Understand how those uncertainties affect the PV

Analyze the event tree to identify and incorporate managerial flexibility to respond to new information

Still no flexibility; this value should equal the value from Step 1

Explicitly estimate uncertainty

Incorporating flexibility transforms event trees, which transforms them into decision trees

The flexibility continuously alters the risk characteristics of the project, and hence the cost of capital

ROA includes the base case present value without flexibility plus the option (flexibility) value

– Under high uncertainty and managerial flexibility option value will be substantial

Steps

Output Project’s PV without flexibility

Detailed event tree capturing the possible present values of the project

A detailed scenario tree combining possible events and management responses

ROA of the project and optimal contingent plan for the available real options

Model theUncertainty

Using Event Trees

Identify and Incorporate Managerial

Flexibilities Creating a Decision Tree

Calculate Real Option Value (ROA)

Compute Base CasePresent Value withoutFlexibility Using DCF

Valuation Model

Copyright © 2001 Monitor Company Group LP — Confidential — CAMZKN-MFR-NIVRA 6 01-TEC 64

Step 4 — Valuation Using the “No Arbitrage” Condition

Using the traded twin security we can value our project in year 0 using either the traditional cost of capital approach, or the replicating portfolio method. Under the cost of capital approach we calculate the expected rate of return using the twin and then discount the cash flows from our project at this rate*. Alternatively, we can calculate how many shares (N) of the twin security would replicate the cash flow of our project** in any state, and calculate the value of those shares in year 0 (N shares x price / share). These two methods will yield the same result since the cost of capital approach is essentially a shortcut for the replicating portfolio method***

*Since the “twin security” is a traded security with the same risk characteristics as our project (by definition), its required rate of return (discount rate) must be equal to the discount rate on our project. CAPM simply generalizes this by claiming all securities with the same Beta (systematic risk) will have the same cost of capital (if all equity financing); therefore, identifying a security’s Beta is equivalent to finding a priced “twin security”**Typically the replicating portfolio will be a leveraged position that will also entail borrowing***Since the project and this portfolio provide the same future returns, to avoid risk-free arbitrage they must have the same value in year 0

Year 0

Twin Security

Our Project

P0 = 20 V0 = ?

Year 1

Twin Security

Our Project

$34 $170

Twin Security

Our Project

$13 $65

Probabilit

y = 50%

Probability = 50%

Calculating V0

Method 1:Cost of Capital Approach

Method 2:Replicating Portfolio**

1. Calculate cost of capital using “twin security”

20 = (0.5)(34)+(0.5)(13)1+k

k = 17.5%

2. Discount expected cash flows

V0 = (0.5)(170)+(0.5)(65)1.175

V0 = 100

1. Replicating cash flows of our security using a portfolio of “twin” and borrowing in year 1

34N + B = 170 13N + B = 65 N = 5; B = 0

2. Value of this portfolio in year 0

V0 = 20N + B V0 = 100

Copyright © 2001 Monitor Company Group LP — Confidential — CAMZKN-MFR-NIVRA 6 01-TEC 65

NPV / DCF Valuation — Flexibility Not Valued

* [(0.5) (170) + (0.5) (65)] / 1.175 = 100** 115 / 1.08 = 106.48: The investment is discounted at the risk-free rate because the decision to invest was made in Year 0

Using the NPV / DCF methodology, this project would be rejected since it has a negative NPV of -$6.5

100

-106.5

-6.5

Present Value ofCash Flows*

Present Value ofInvestments**

NPV

Decision Made in Year 0

Decision Made in Year 0

Probability = 50%

Probability = 50%

Cash Flows

170

65

Investment

-115

-115

Value in Year 0 Decision

Do NotInvest

Since the decision to invest was made in Year 0,

we are bound into a negative NPV project in the

unfavorable state

Since the decision to invest was made in Year 0,

we are bound into a negative NPV project in the

unfavorable state

Year 0 Year 1

Copyright © 2001 Monitor Company Group LP — Confidential — CAMZKN-MFR-NIVRA 6 01-TEC 66

Real Option Analysis — Flexibility Valued (cont.)

* To see derivation of this column see Decision Tree Analysis chart** See NPV / DCF valuation† Total value less NPV; this could be valued separately†† 2.62 shares X $20 / share -$31.43 = $20.95

27.4

-6.5

20.9

NPV** FlexibilityValue

Total Value

Decision Deferred

Until Year 1

Decision Deferred

Until Year 1

Probability = 50%

Probability = 50%

55

0

Invest;Based onFlexibility

Value

Value of N shares @ $34 / share

Value of loan (B) 34N+B(1+rf)=55

Value of N shares @ $13 / Share

Value of loan(B) 13N+B(1+rf )=0

Net CFs*

CFs Replicated UsingN Shares of “Twin

Security” and Borrowing

Replicating Portfolio in

Year 0

† ††

Year 0 Year 1

The ROA approach values the total project, with flexibility, at $20.95 ($2.54 less than the DTA value). Since the ROA method is calculated using replicating portfolios, this must be the correct value — otherwise there would be arbitrage opportunities

Value in Year 0 Decision

Buy 2.62 shares @ $20 / share

Borrow $31.43

Value = 20.95††

Copyright © 2001 Monitor Company Group LP — Confidential — CAMZKN-MFR-NIVRA 6 01-TEC 67

Real Option Analysis — Flexibility Valued

* To see derivation of this column see Decision Tree Analysis chart** See NPV / DCF valuation† Total value less NPV; this could be valued separately†† 0.52 shares X $100 / share -$31.42 = $20.95

27.4

-6.5

20.9

NPV** FlexibilityValue

Total Value

Decision Deferred

Until Year 1

Probability = 50%

Probability = 50%

55

0

Invest;Based onFlexibility

Value

Value of N shares @ $170 share

Value of loan (B) 170N+B(1+rf)=55

Value of N shares @ $65 / Share

Value of loan(B) 65N+B(1+rf )=0

Net CFs*

CFs Replicated UsingN Shares of “PV Type”

(without flexibility) and Borrowing

Replicating Portfolio in

Year 0

† ††

Year 0 Year 1

Rather than searching for a fictitious “twin security” we use the present value of the project itself, without flexibility, as the underlying risky asset. What is better correlated with the project that the project itself? We call this the Marketed Asset Disclaimer (MAD)

Value in Year 0 Decision

Buy 0.524 shares @ $100 / share

Borrow $31.53

Value = 20.95††

Copyright © 2001 Monitor Company Group LP — Confidential — CAMZKN-MFR-NIVRA 6 01-TEC 68

Marketed Asset Disclaimer Assumption

Both the replicating portfolio approach and the risk-adjusted method (as we will apply them in this section) rely heavily on the Marketed Asset Disclaimer assumption

Both the replicated portfolio approach and the risk-adjusted method rely on our ability to buy shares of the base case present value (without flexibility) when creating the replicating portfolios. If the present value is traded (as in the case of a stock) this will not be a problem; however when the present value is not explicitly traded (as will usually be the case with real options) our ability to build the replicating portfolio becomes dubious

The Marketed Asset Disclaimer assumption implies that we assume that even if the base case present value is not marketed we can still build the replicating portfolios, because if it were marketed, the value we calculated (with our DCF model) would be approximately equal to the publicly traded market value (if it existed); therefore the replicating portfolio approach (and equivalently the risk-adjusted method) would still produce the correct value

There are other approaches in the academic literature, however, noted academics Steve Ross and Eduardo Schwartz support the Marketed Asset Disclaimer method

Copyright © 2001 Monitor Company Group LP — Confidential — CAMZKN-MFR-NIVRA 6 01-TEC 69

20.9 = (0.5)(55)+(0.5)(0)

1+k

k = 31.9%

The original cost of capital was 17.5%

20.9 = (0.5)(55)+(0.5)(0)

1+k

k = 31.9%

The original cost of capital was 17.5%

The Correct Cost of Capital

The cost of capital, as calculated from correct ROA value is 31.9%. Since this differs from the original cost of capital for the project without flexibility (17.5%), flexibility has therefore altered the project’s riskiness

* To see derivation this column see Decision Tree Analysis chart

Net CFs*

55

0

Probabilit

y = 50%

Probability = 50%

Cost of Capital Year 0 Year 1

Value20.9

Value20.9

Copyright © 2001 Monitor Company Group LP — Confidential — CAMZKN-MFR-NIVRA 6 01-TEC 70

Step 3 — Decision Trees

Initial Conditions (No Flexibility) — Event Tree for Underlying Asset

Assumptions Risk-free rate of 5% WACC of 12% Initial investment of $105MM Five year time frame (analyzing one period

per year)

Underlying Asset A factory with a (no flexibility) present value of

$100MM The standard deviation of the rate of change of the

factory value (volatility) is 15%No Flexibility (NPV)

($5MM) = $100MM – $105MM

212182

157 157135 135

116 116 116100 100 100

86 86 8674 74

64 6455

47

t=0 t=1 t=2 t=3 t=4 t=5

Value =

– Investment = -105

-5NPV

Value-basedEvent Tree

Value-basedEvent Tree

Copyright © 2001 Monitor Company Group LP — Confidential — CAMZKN-MFR-NIVRA 6 01-TEC 71

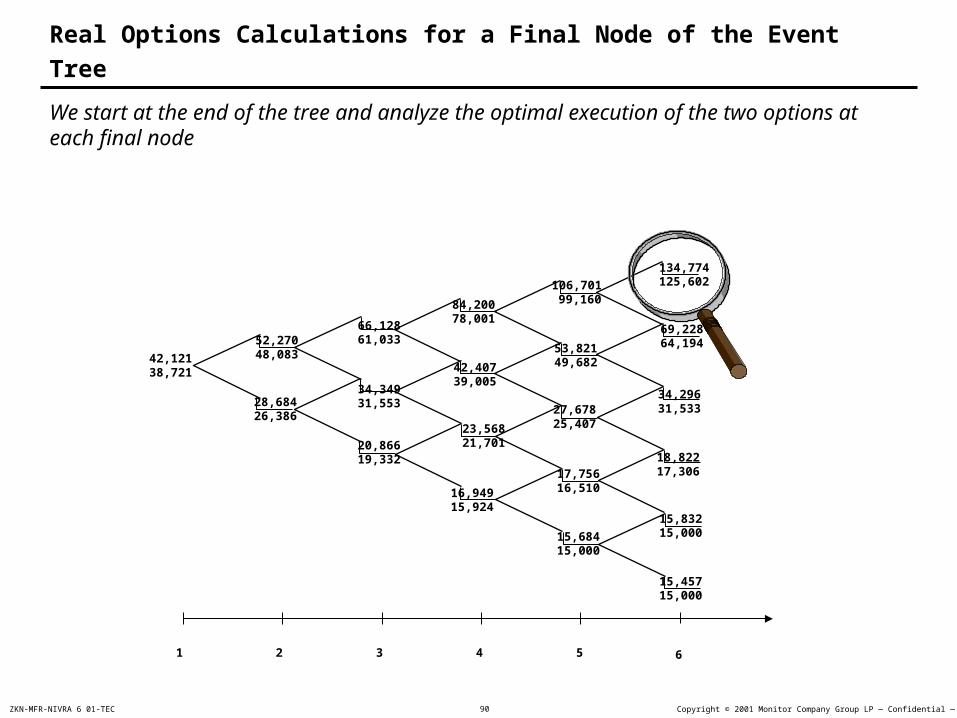

Step 3: Real Options Calculations Examples

Option to Expand

Management has the right to expand the scale and the value of the factory by 20% at any point in time by investing an additional $15MM

239204

175 173149 148

127 126 124108 107 106

91 90 8877 75

65 6455

47

t=0 t=1 t=2 t=3 t=4 t=5

Underlying Asset ValuesPV+ = 86PV- = 64PV = 74

Managerial Decisions (t=4,5)88 = Max (86, 86*1.2-15)64 = Max (64, 64*1.2-15)75 = Max (75, 74*1.2-15)

Portfolio Replicationn = (88 - 64) / (86 - 64)B = [88 - n (86) ] / (1+5%)n = 1.1, B = -5.54

Value of Option (ROA at t=4)ROA = n (74) + BROA = 75

Underlying Asset ValuesPV+ = 86PV- = 64PV = 74

Managerial Decisions (t=4,5)88 = Max (86, 86*1.2-15)64 = Max (64, 64*1.2-15)75 = Max (75, 74*1.2-15)

Portfolio Replicationn = (88 - 64) / (86 - 64)B = [88 - n (86) ] / (1+5%)n = 1.1, B = -5.54

Value of Option (ROA at t=4)ROA = n (74) + BROA = 75

Note: In this case management will never exercise its option prior to the five year expiration date. In general, a call option on a non-dividend paying asset will never be exercised early

= Decision to Expand

Copyright © 2001 Monitor Company Group LP — Confidential — CAMZKN-MFR-NIVRA 6 01-TEC 72

Step 3: Real Options Calculations Examples

Option to Abandon

At any point in time management has the option to abandon the factory. Abandonment will yield a salvage value of $100MM

212182

157 157135 135

118 118 116106 106 105

100 100 100100 100

100 100100

100

t=0 t=1 t=2 t=3 t=4 t=5

Underlying Asset ValuesPV+ = 116PV- = 86PV = 100

Managerial Decisions (t=4,5)116 = Max (116, 100) 86 = Max (86, 100)105 = Max (105, 100)

Portfolio Replicationn = (116 - 100) / (116 - 86)B = [116 - n (116) ] / (1+5%)n = 0.5, B = 51.5

Value of Option (ROA at t=4)ROA = n (100) + BROA = 105

Underlying Asset ValuesPV+ = 116PV- = 86PV = 100

Managerial Decisions (t=4,5)116 = Max (116, 100) 86 = Max (86, 100)105 = Max (105, 100)

Portfolio Replicationn = (116 - 100) / (116 - 86)B = [116 - n (116) ] / (1+5%)n = 0.5, B = 51.5

Value of Option (ROA at t=4)ROA = n (100) + BROA = 105

= Decision to Abandon

212182

157 157135 135

118 118 116106 106 105

100 100 100100 100

100 100100

100

t=0 t=1 t=2 t=3 t=4 t=5

Copyright © 2001 Monitor Company Group LP — Confidential — CAMZKN-MFR-NIVRA 6 01-TEC 73

Step 3: Real Options Calculations Examples

Option to Contract

At any point in time management has the option to decrease the scale and the value of the factory by 25%, generating savings of $25MM

212182

157 157135 135

117 117 116102 101 101

90 90 9081 81

73 7366

60

t=0 t=1 t=2 t=3 t=4 t=5

Underlying Asset ValuesPV+ = 116PV- = 86PV = 100

Managerial Decisions (t=4,5)116 = Max (116, 116*0.75+25)90 = Max (86, 86*0.75+25)101 = Max (101, 100*0.75+25)

Portfolio Replicationn = (116 - 90) / (116 - 86)B = [116 - n (116) ] / (1+5%)n = 0.87, B = 14.4

Value of Option (ROA at t=4)ROA = n (100) + BROA = 101

Underlying Asset ValuesPV+ = 116PV- = 86PV = 100

Managerial Decisions (t=4,5)116 = Max (116, 116*0.75+25)90 = Max (86, 86*0.75+25)101 = Max (101, 100*0.75+25)

Portfolio Replicationn = (116 - 90) / (116 - 86)B = [116 - n (116) ] / (1+5%)n = 0.87, B = 14.4

Value of Option (ROA at t=4)ROA = n (100) + BROA = 101

= Decision to Contract

Copyright © 2001 Monitor Company Group LP — Confidential — CAMZKN-MFR-NIVRA 6 01-TEC 74

239204

175 173150 148

129 127 124113 112 110

102 101 100100 100

100 100100

100

t=0 t=1 t=2 t=3 t=4 t=5

Underlying Asset ValuesPV+ = 116PV- = 86PV = 100

Managerial Decisions (t=4,5)124 = Max (116, 116*0.75+25,

116*1.2-15, 100)100 = Max (86, 86*0.75+25,

86*1.2-15, 100 )110 = Max (110, 100*0.75+25,

100*1.2-15, 100)

Portfolio Replicationn = (124 - 100) / (116 - 86)B = [124 - n (116) ] / (1+5%)n = 0.8, B = 29.7

Value of Option (ROA at t=4)ROA = n (100) + BROA = 110

Underlying Asset ValuesPV+ = 116PV- = 86PV = 100

Managerial Decisions (t=4,5)124 = Max (116, 116*0.75+25,

116*1.2-15, 100)100 = Max (86, 86*0.75+25,

86*1.2-15, 100 )110 = Max (110, 100*0.75+25,

100*1.2-15, 100)

Portfolio Replicationn = (124 - 100) / (116 - 86)B = [124 - n (116) ] / (1+5%)n = 0.8, B = 29.7

Value of Option (ROA at t=4)ROA = n (100) + BROA = 110

= Decision to Contract

= Decision to Abandon

= Decision to Expand

Step 3: Real Options Calculations Examples

Option to Expand, Contract or Abandon

At any point in time management has several options available: Expand the scale and the value of the factory by 20% by investing an additional $15MM Decrease the scale and the value of the factory by 25%, generating savings of $25MM Abandon the factory with a salvage value of $100MM

Copyright © 2001 Monitor Company Group LP — Confidential — CAMZKN-MFR-NIVRA 6 01-TEC 75

For the time being, assume that the uncertainties all move continuously through time and remember that the annualized volatility (we need to calculate is the volatility of the percent value which is usually hard to observe. Several factors combine to convert the uncertainty of the real market prices, quantities, and costs that feed into the company to the equity uncertainty that is manifested in the financial markets

PricePrice

QuantityQuantity

CostCost

PricePrice

QuantityQuantity

CostCost

Op

era

ting

Le

ve

rag

e

Div

ers

ifica

tion

Fin

an

cia

l Le

ve

rag

e

RealMarkets

Data

Project Uncertainties Asset Uncertainties

Equity Uncertainty

FinancialMarkets

Data

Not directly observable

Step 2 — Modeling Uncertainties and Building the Event Tree

Copyright © 2001 Monitor Company Group LP — Confidential — CAMZKN-MFR-NIVRA 6 01-TEC 76

The base-case present value without flexibility for the investment is estimated a thousand times to generate the standard deviation of the rate of return

Valuation Model DCF

Net present value for the investment

Net present value for the investment

Valuation Inputs Revenue growth rates Margin assumptions Capital expenditures

Ud

eU T

1

Monte Carlo

Random NumberRandom Number GeneratorGenerator

Random NumberRandom Number GeneratorGenerator

rV

Vn

0

1

based on r

Copyright © 2001 Monitor Company Group LP — Confidential — CAMZKN-MFR-NIVRA 6 01-TEC 77

Calculating Volatility Direct From Historic Market Data

If we have historical market data we can calculate the volatility of present value directly

Transform into Natural Logs

Calculate Variance

Compute Growth Rate

Jan ‘89:

Annualize

vart

Convert into Volatility (v)

SQRT (VAR) ( )

Date Value

Growth Rate LN (Growth Rate) Variance Volatility Annualize

Example:

Comments:

Feb ‘89:

Mar ‘89:

April ‘89:

2

4

3

5

G1=4/2

G2=3/4

G3=5/3

Ln4-ln2= .69

Ln3-ln4= -.29

Ln5-ln3= .51

.27 .271/12

= 3.26 SQRT (3.26) = 1.81

t is based on the time series data; in this example t = 1/12 since the data is monthly

Once we know the annualized volatility, we can use a different t in the building the tree

Get Time Series Data

Copyright © 2001 Monitor Company Group LP — Confidential — CAMZKN-MFR-NIVRA 6 01-TEC 78

Calculating Volatility from Management Estimates

What is the 95% confidence level in year 5?

$

100

20

o

ro

o

lower

i

P

Pn

lr

ePP

Pp

r

6

6

2

Expected

Copyright © 2001 Monitor Company Group LP — Confidential — CAMZKN-MFR-NIVRA 6 01-TEC 79

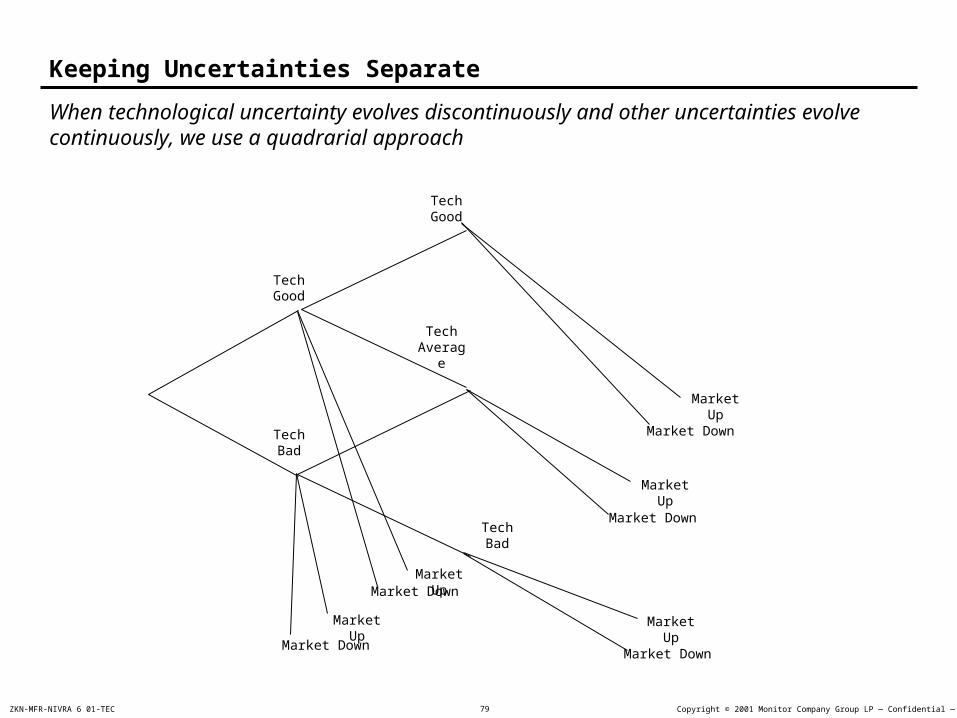

Keeping Uncertainties Separate

When technological uncertainty evolves discontinuously and other uncertainties evolve continuously, we use a quadrarial approach

Tech Good

Tech Bad

Tech Good

Tech Bad

Tech Average

Market UpMarket Down

Market Up

Market Down

Market Up

Market Down

Market Up

Market Down

Market Up

Market Down

Copyright © 2001 Monitor Company Group LP — Confidential — CAMZKN-MFR-NIVRA 6 01-TEC 80

Portes Case — Situation

1. Portes founded 10 years ago, 60 employees, CEO Diane Mullins

2. Slow growth of profitable systems recovery product, Recovery™

3. New high-end data recovery software — can be sold over the Internet

4. Bill, the CFO, finds that selling in France — The Portes Project — via the Internet, has a negative NPV. Monte Carlo analysis doesn’t help [see table 1 for the analysis]

Sales of 200 programs in year 1, doubles to 400 in 5 years Unit price starts at $30,000 and falls to $20,000 in 5 years COGS is $9,000 per program in year 1 and falls to $7,000 in 6th year Fixed cost $20,000 per year SG&A? is 10% of revenue Initial investment is $35 million, depreciated over 10 years No debt 40% tax rate 13% cost of capital Beyond year 10, FCF grows at 4%, and ROIC 12%

5. Risk estimates, in 6th year Unit sales, expected level is 400 programs and the lower 95% confidence limit is 190 Unit price, expected level is $20,000 and the lower 95% confidence limit is $25,000

6. Flexibility in decision-making Expansion (prevent loss product), invest $10.5 million and increase value 30% Abandonment value is $15 million

Copyright © 2001 Monitor Company Group LP — Confidential — CAMZKN-MFR-NIVRA 6 01-TEC 81

Table 1

NPV Analysis of the Investment Proposal

Item Year 0 Year 1 Year 2 Year 3 Year 4 Year 5 Year 6 Year 7

Quantity (units) 200 230 264 303 348 400Continuous Annual Growth Rate 13.9%

Price per unit 30.00 27.66 25.51 23.52 21.69 20.00Continuous Annual Growth Rate -8.1%

Cost per unit 9.0 8.6 8.1 7.7 7.4 7.0

Revenues 6,000 6,355 6,732 7,130 7,553 8,000Cost of Goods Sold 1,800 1,966 2,148 2,346 2,563 2,800

Gross Income 4,200 4,389 4,584 4,784 4,990 5,200Gross Margin% 70% 69% 68% 67% 66% 65%

Rent 200 200 200 200 200 200S&A expenses 600 636 673 713 755 800

EBITDA 3,400 3,554 3,711 3,871 4,034 4,200

Depreciation 3,500 3,500 3,500 3,500 3,500 3,500

EBIT (100) 54 211 371 534 700EBIT Growth -154% 294% 76% 44% 31%

Taxes 0 21 84 148 214 280

Net Income (100) 32 126 223 321 420

Depreciation 3,500 3,500 3,500 3,500 3,500 3,500

Initial Investment 35,000

Free Cash Flow (35,000) 3,400 3,532 3,626 3,723 3,821 3,920Change in FCF 4% 3% 3% 3% 3%

Continuous Value 50,960

Discount Rate 13%

PV 34,681 36,096 37,575 39,165 40,880 42,735 44,748TPV (319) 39,496 41,107 42,792 44,603 46,555 48,668FCF as a % of PV 8.6% 8.6% 8.5% 8.3% 8.2% 8.05%

Copyright © 2001 Monitor Company Group LP — Confidential — CAMZKN-MFR-NIVRA 6 01-TEC 82

Outputs of the Initial NPV Analysis

The free cash flow of the project has the usual profile with a significant initial investment followed by a small positive cash inflows and a considerable terminal value

Free Cash Flows

Dollars($ ‘000)

-40

-30

-20

-10

0

10

20

30

40

50

60

1 2 3 4 5 6 7

Continuous Value

Investment

Depreciation

Net Income

Year

Copyright © 2001 Monitor Company Group LP — Confidential — CAMZKN-MFR-NIVRA 6 01-TEC 83

Inputs for the Monte Carlo Simulation: Price per Unit

Price Uncertainty Range (95% confidence interval)

30

27.6

25.3

23.3

21.4

20.0

3031.5

30.629.4

28.1

30.0

24.3

21.3

18.8

16.815.0

26.7

10

20

30

40