Embed Size (px)

Citation preview

Page 1/21Page 1/21Bursa Malaysia : 7113 SGX : BVA Reuters : TPGC.KL Bloomberg : TOPG MK ADR CUSIP : 890534100

TOP GLOVE CORPORATION BHDInvestor Presentation

03 Sept 2018

Page 2/21

TG BUSINESS ETHICS CLAPS

Ready, 1 2 3

Claps, 2x 3x 2x

Prepared By: Ng Chin Yong @ 14/07/17

Checked & Verified By: Ng Yong Lin @ 14/07/17

Page 3/21

Top Glove Corporation Bhd (“Top Glove”) at a glance

60.5 billion gloves pa

40 factories

648 production

lines

2,000+ customers

across 195

countries

FY17 Revenue of RM3.4bn

and PATMI of RM0.3bn

Current market

capitalisation of

RM14.23bn

Global leader in

medical and

surgical gloves

World’s largest manufacturer of gloves

Over 17,000

employees

Page 4/21

1991

Started as a local business enterprise

2013Established first dedicated Group R&D Centre to drive innovation

Acquisition of the remaining minority stake in Medi-Flex and privatisation of the company

1994

First overseas foray

and established a

marketing arm in the

USA

2006

Acquisition of a majority

stake in Medi-Flex

2007

Revenues over RM1bn

2016

Secondary listing on

Singapore StockExchange (“SGX”)

2017Investment in new business line- condom projected to be operational by mid-2018

Revenues over RM3bn

(USD776mn)(1)

2018

Acquisition of Aspion

Acquisition of Eastern Press

Acquisition of Duramedical

2010

Revenues over RM2bn

2011Acquired a marketing arm in Germany to extend sales in Europe

2002

Commenced operations in

China

Established a second rubber

glove factory in Thailand

Transferred to the Main Board of

KLSE

2001

Commenced operations in Thailand

Listed on the Second Board of Kuala Lumpur Stock Exchange (“KLSE”)

From Humble Origins to Global Leader

Nearly 3 decades of track record of excellence

Page 5/21

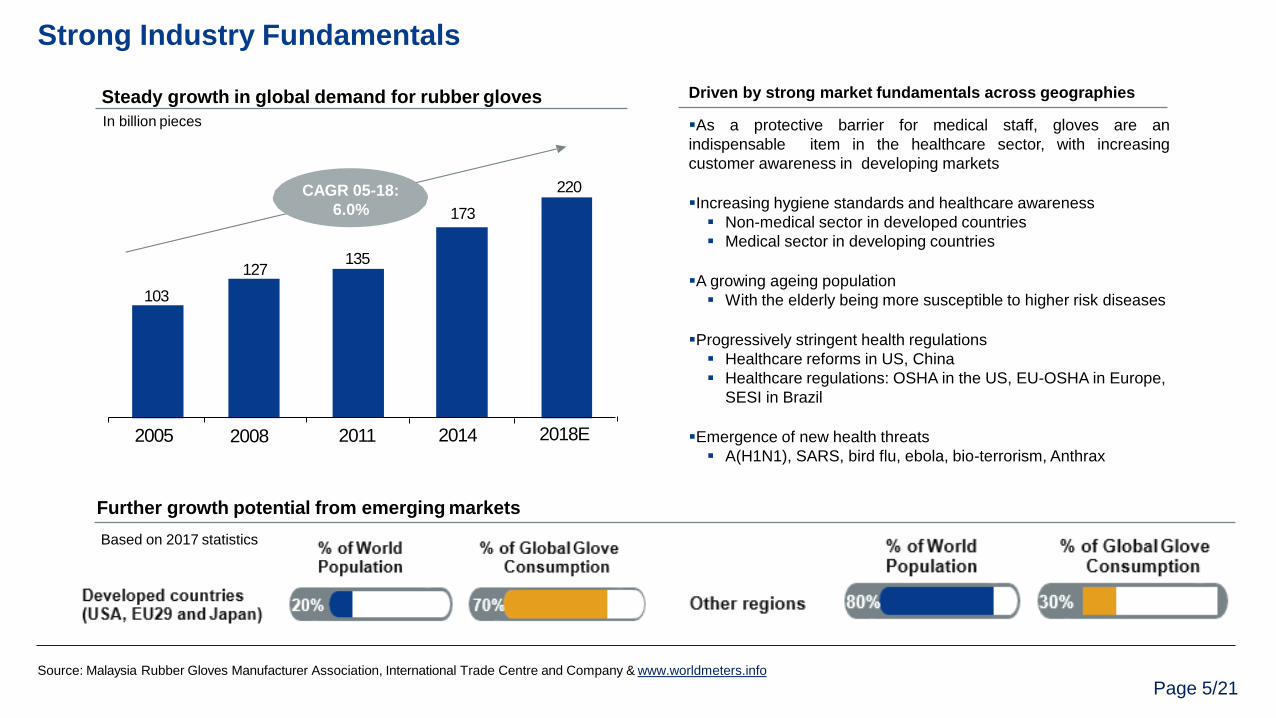

103

127135

173

220

2005 2008 2011 2014 2018E

Steady growth in global demand for rubber gloves

CAGR 05-18:

6.0%

Driven by strong market fundamentals across geographies

As a protective barrier for medical staff, gloves are an

indispensable item in the healthcare sector, with increasing

customer awareness in developing markets

Increasing hygiene standards and healthcare awareness

Non-medical sector in developed countries

Medical sector in developing countries

A growing ageing population

With the elderly being more susceptible to higher risk diseases

Progressively stringent health regulations

Healthcare reforms in US, China

Healthcare regulations: OSHA in the US, EU-OSHA in Europe,

SESI in Brazil

Emergence of new health threats

A(H1N1), SARS, bird flu, ebola, bio-terrorism, Anthrax

Further growth potential from emerging markets

Based on 2017 statistics

In billion pieces

Source: Malaysia Rubber Gloves Manufacturer Association, International Trade Centre and Company & www.worldmeters.info

Strong Industry Fundamentals

Page 6/21

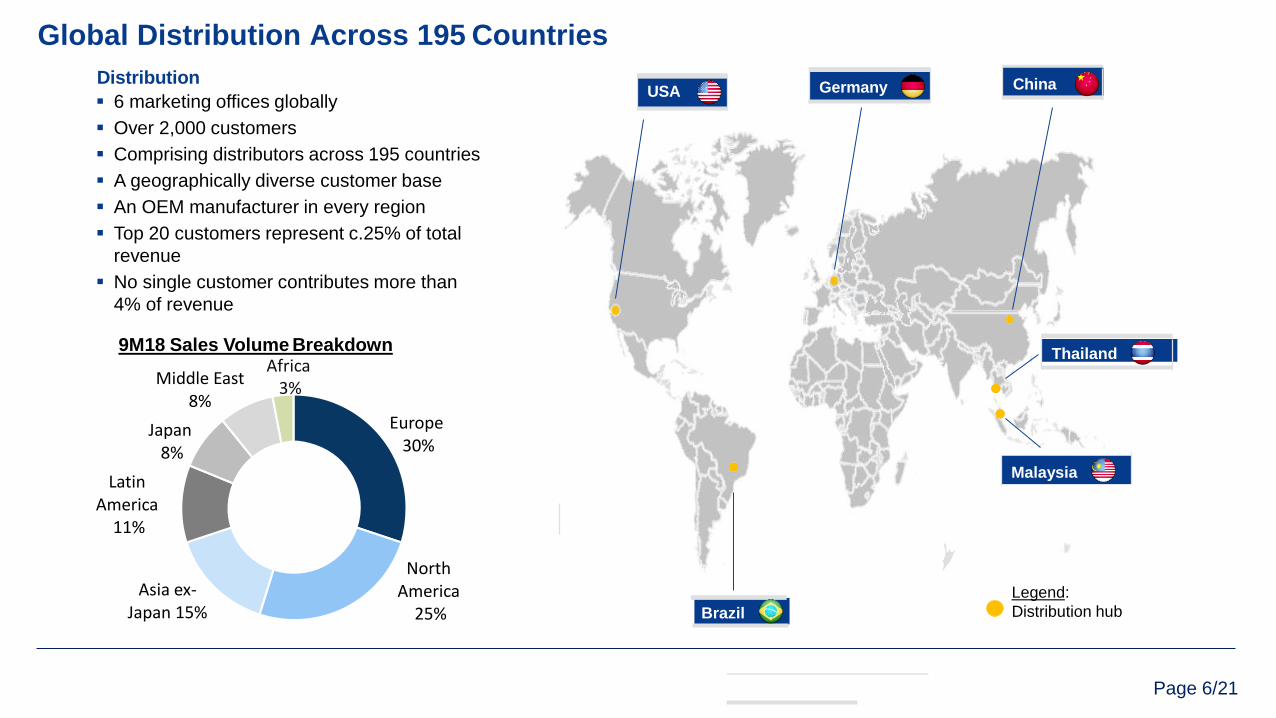

GermanyUSA China

Malaysia

Thailand

Legend:

Distribution hub

Distribution

6 marketing offices globally

Over 2,000 customers

Comprising distributors across 195 countries

A geographically diverse customer base

An OEM manufacturer in every region

Top 20 customers represent c.25% of total

revenue

No single customer contributes more than

4% of revenue

9M18 Sales Volume Breakdown

Brazil

Global Distribution Across 195 Countries

Europe30%

North America

25%

Asia ex-Japan 15%

Latin America

11%

Japan8%

Middle East8%

Africa3%

Page 7/21

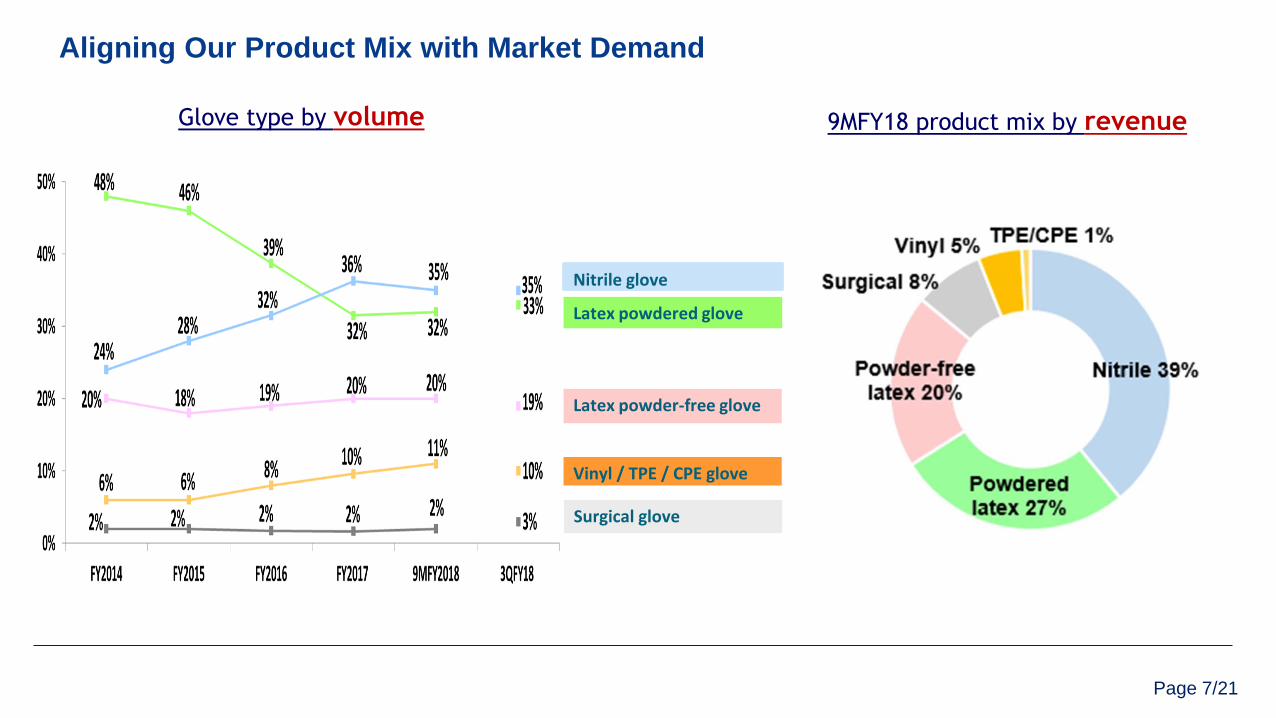

9MFY18 product mix by revenue

Latex powdered glove

Nitrile glove

Vinyl / TPE / CPE glove

Surgical glove

Latex powder-free glove

Glove type by volume

Aligning Our Product Mix with Market Demand

Page 8/21

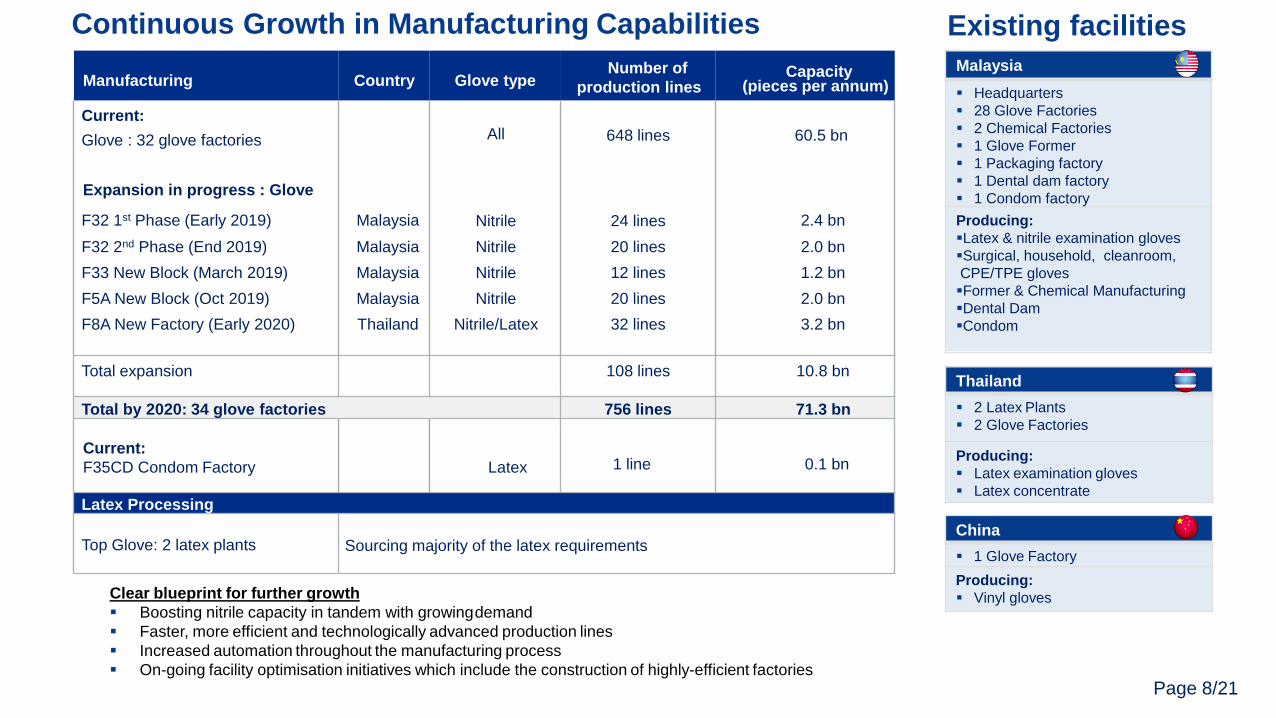

China

1 Glove Factory

Producing:

Vinyl gloves

Malaysia

Headquarters

28 Glove Factories

2 Chemical Factories

1 Glove Former

1 Packaging factory

1 Dental dam factory

1 Condom factory

Producing:

Latex & nitrile examination gloves

Surgical, household, cleanroom,

CPE/TPE gloves

Former & Chemical Manufacturing

Dental Dam

Condom

Thailand

2 Latex Plants

2 Glove Factories

Producing:

Latex examination gloves

Latex concentrate

Clear blueprint for further growth

Boosting nitrile capacity in tandem with growingdemand

Faster, more efficient and technologically advanced production lines

Increased automation throughout the manufacturing process

On-going facility optimisation initiatives which include the construction of highly-efficient factories

Continuous Growth in Manufacturing Capabilities

Manufacturing Country Glove typeNumber of

production linesCapacity

(pieces per annum)

Current:

Glove : 32 glove factories All 648 lines 60.5 bn

Expansion in progress : Glove

F32 1st Phase (Early 2019) Malaysia Nitrile 24 lines 2.4 bn

F32 2nd Phase (End 2019)

F33 New Block (March 2019)

F5A New Block (Oct 2019)

F8A New Factory (Early 2020)

Malaysia

Malaysia

Malaysia

Thailand

Nitrile

Nitrile

Nitrile

Nitrile/Latex

20 lines

12 lines

20 lines

32 lines

2.0 bn

1.2 bn

2.0 bn

3.2 bn

Total expansion 108 lines 10.8 bn

Total by 2020: 34 glove factories 756 lines 71.3 bn

Current:

F35CD Condom Factory Latex 1 line 0.1 bn

Latex Processing

Top Glove: 2 latex plants Sourcing majority of the latex requirements

Existing facilities

Page 9/21

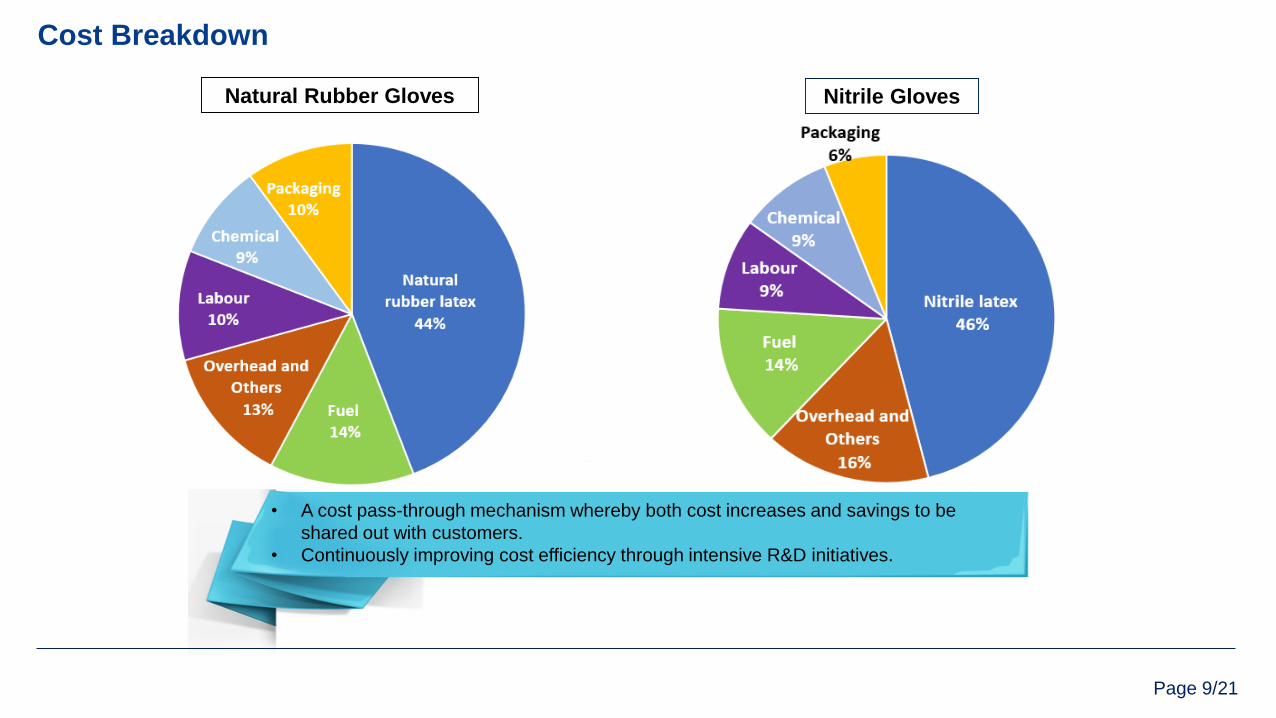

• A cost pass-through mechanism whereby both cost increases and savings to be

shared out with customers.

• Continuously improving cost efficiency through intensive R&D initiatives.

Natural Rubber Gloves Nitrile Gloves

Cost Breakdown

Page 10/21

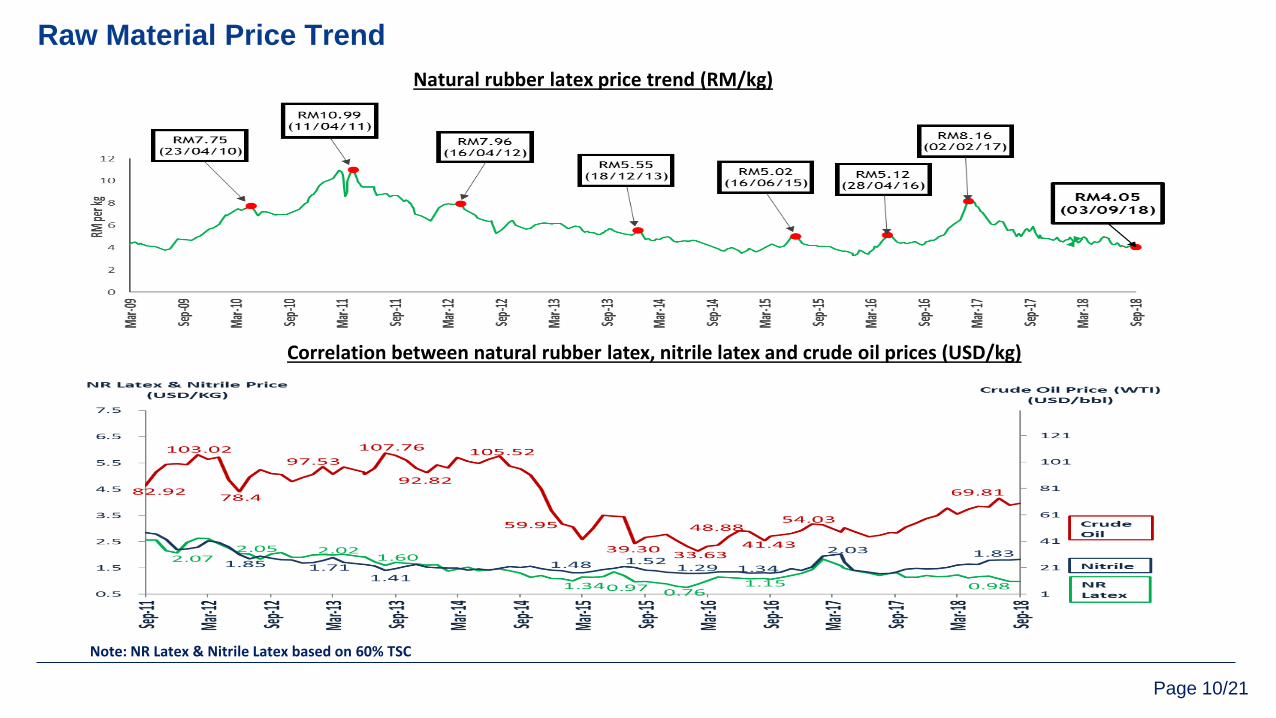

Note: NR Latex & Nitrile Latex based on 60% TSC

Natural rubber latex price trend (RM/kg)

Raw Material Price Trend

Correlation between natural rubber latex, nitrile latex and crude oil prices (USD/kg)

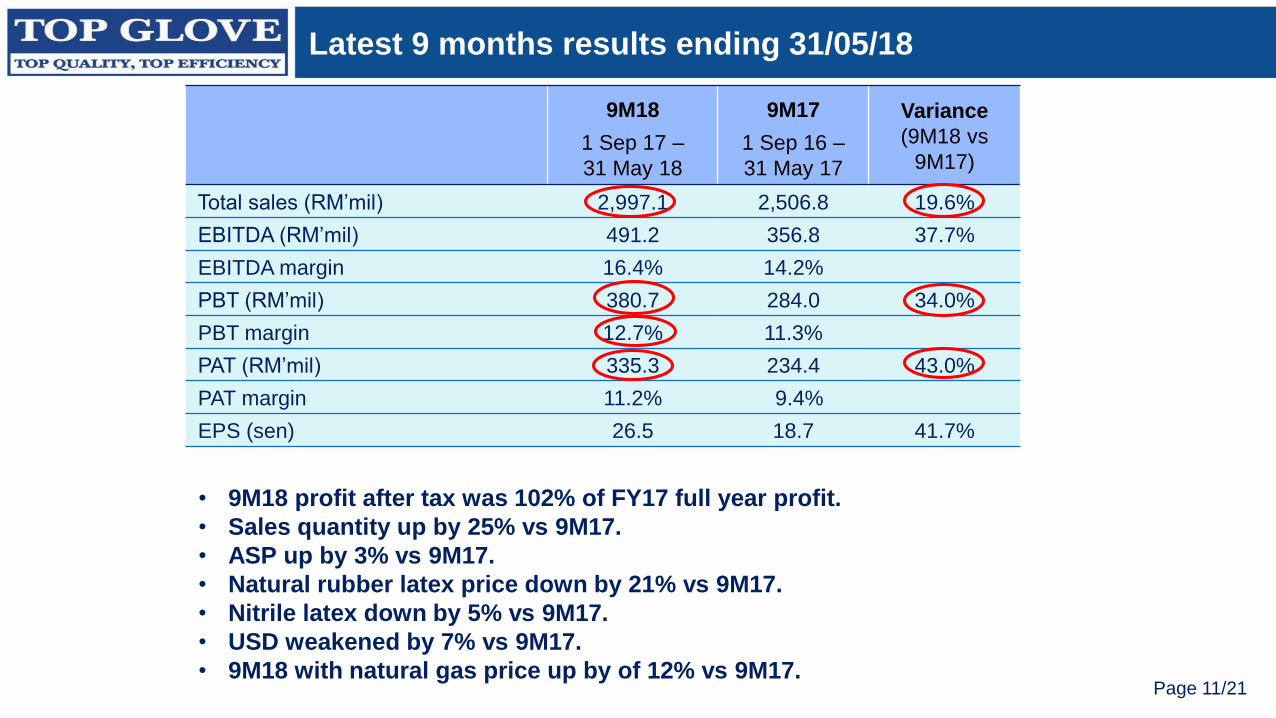

Page 11/21Page 11/21

9M18

1 Sep 17 –

31 May 18

9M17

1 Sep 16 –

31 May 17

Variance

(9M18 vs

9M17)

Total sales (RM’mil) 2,997.1 2,506.8 19.6%

EBITDA (RM’mil) 491.2 356.8 37.7%

EBITDA margin 16.4% 14.2%

PBT (RM’mil) 380.7 284.0 34.0%

PBT margin 12.7% 11.3%

PAT (RM’mil) 335.3 234.4 43.0%

PAT margin 11.2% 9.4%

EPS (sen) 26.5 18.7 41.7%

Latest 9 months results ending 31/05/18

• 9M18 profit after tax was 102% of FY17 full year profit.

• Sales quantity up by 25% vs 9M17.

• ASP up by 3% vs 9M17.

• Natural rubber latex price down by 21% vs 9M17.

• Nitrile latex down by 5% vs 9M17.

• USD weakened by 7% vs 9M17.

• 9M18 with natural gas price up by of 12% vs 9M17.

Page 12/21

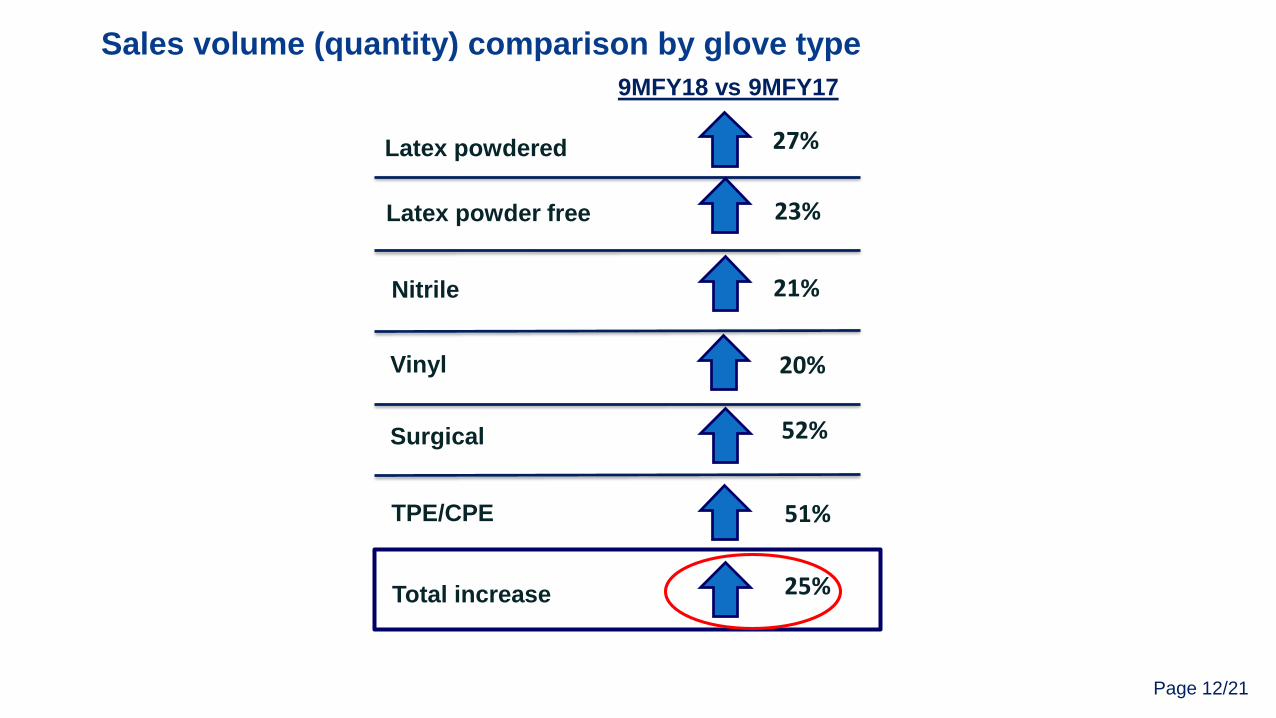

Sales volume (quantity) comparison by glove type

Latex powdered

Latex powder free

Nitrile

Surgical

Total increase

Vinyl

TPE/CPE

27%

23%

21%

52%

25%

9MFY18 vs 9MFY17

20%

51%

Page 13/21

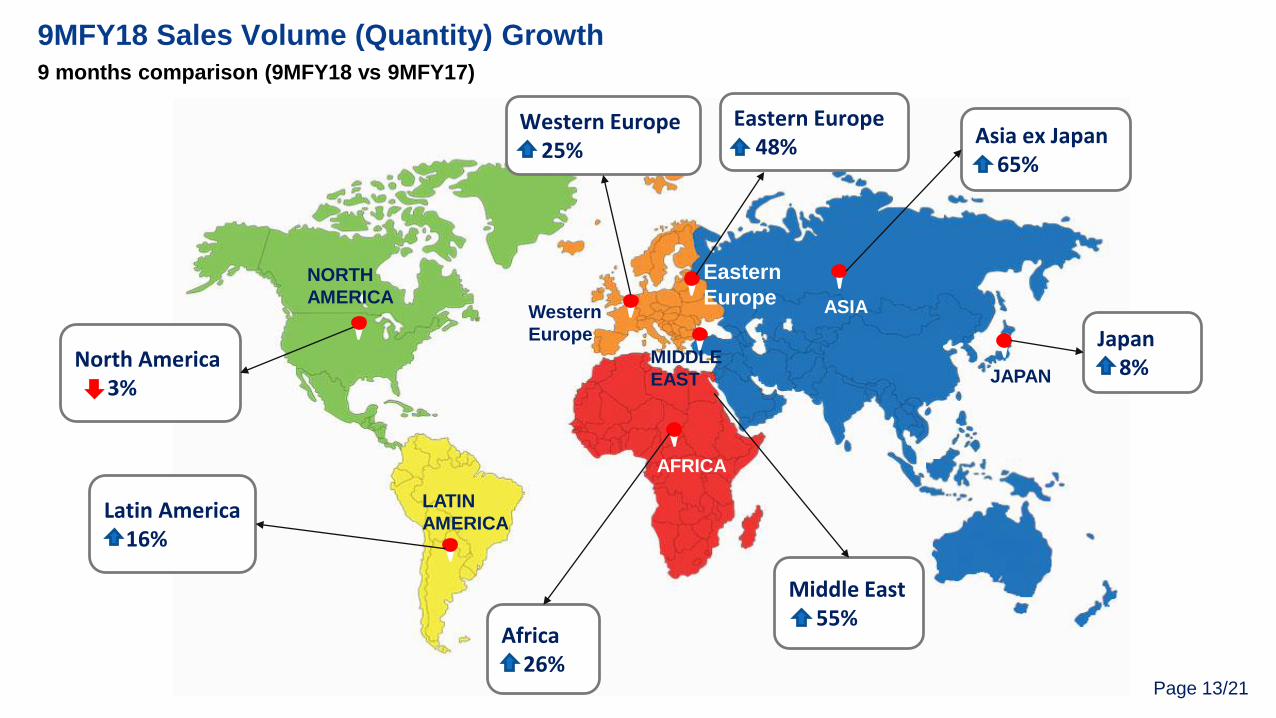

Middle East55%

North America 3%

Latin America16%

Africa26%

Western Europe25%

Eastern Europe48%

Japan8%

Asia ex Japan65%

NORTH

AMERICA

LATIN

AMERICA

AFRICA

MIDDLE

EAST

Western

Europe

Eastern

Europe ASIA

JAPAN

9MFY18 Sales Volume (Quantity) Growth

9 months comparison (9MFY18 vs 9MFY17)

Page 14/21Page 14/21

Steady growth since listing in 2001

(in RM’mil) 2010 2011 2012 2013 2014 2015 2016 20179MFY18

(unaudited)

Sales 2,079.4 2,053.9 2,314.5 2,313.2 2,275.4 2,510.5 2,888.5 3,409.2 2,997.1

EBITDA 364.7 196.7 297.7 310.6 301.8 441.7 524.7 484.0 491.2

EBITDA margin 17.5% 9.6% 12.9% 13.4% 13.3% 17.6% 18.2% 14.2% 16.4%

PBT 305.0 145.5 240.7 242.2 216.3 363.5 442.2 383.1 380.7

PBT margin 14.7% 7.1% 10.4% 10.5% 9.5% 14.5% 15.3% 11.2% 12.7%

Taxation 54.6 30.3 33.4 39.4 32.7 82.3 79.8 54.7 45.4

PAT 250.4 115.1 207.3 202.8 183.6 281.2 362.4 328.4 335.3

PAT margin 12.0% 5.6% 9.0% 8.8% 8.1% 11.2% 12.5% 9.6% 11.2%

# PAT Equity 245.2 113.1 202.7 196.5 180.5 279.8 360.7 328.6 332.0

ROE (%) 22.4 10.0 16.2 14.9 13.1 17.4 19.9 16.3 19.6

EPS (RM)** 0.20 0.09 0.17 0.16 0.15 0.23 0.29 0.26 0.35

Average PAT marginRevenue CAGR PAT CAGR

20.8%22.1% 9.5%For FY ended 31 August

Past 17 years since

listing in 2001 :Past 17 years since

listing in 2001 :Past 17 years since

listing in 2001 :

* Annualised **Adjusted for bonus issue

*

*

Page 15/21Page 15/21

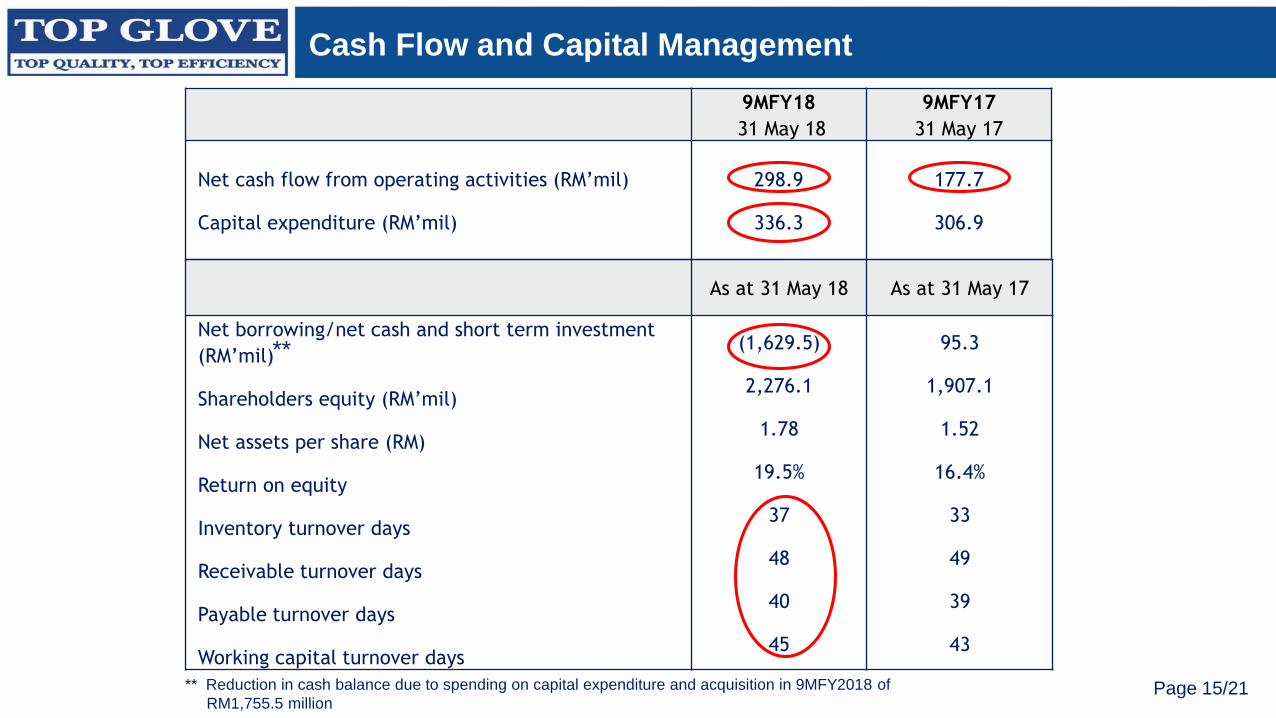

Cash Flow and Capital Management

As at 31 May 18 As at 31 May 17

Net borrowing/net cash and short term investment

(RM’mil)

Shareholders equity (RM’mil)

Net assets per share (RM)

Return on equity

Inventory turnover days

Receivable turnover days

Payable turnover days

Working capital turnover days

(1,629.5)

2,276.1

1.78

19.5%

37

48

40

45

95.3

1,907.1

1.52

16.4%

33

49

39

43

9MFY18

31 May 18

9MFY17

31 May 17

Net cash flow from operating activities (RM’mil)

Capital expenditure (RM’mil)

298.9

336.3

177.7

306.9

** Reduction in cash balance due to spending on capital expenditure and acquisition in 9MFY2018 of

RM1,755.5 million

**

Page 16/21Page 16/21

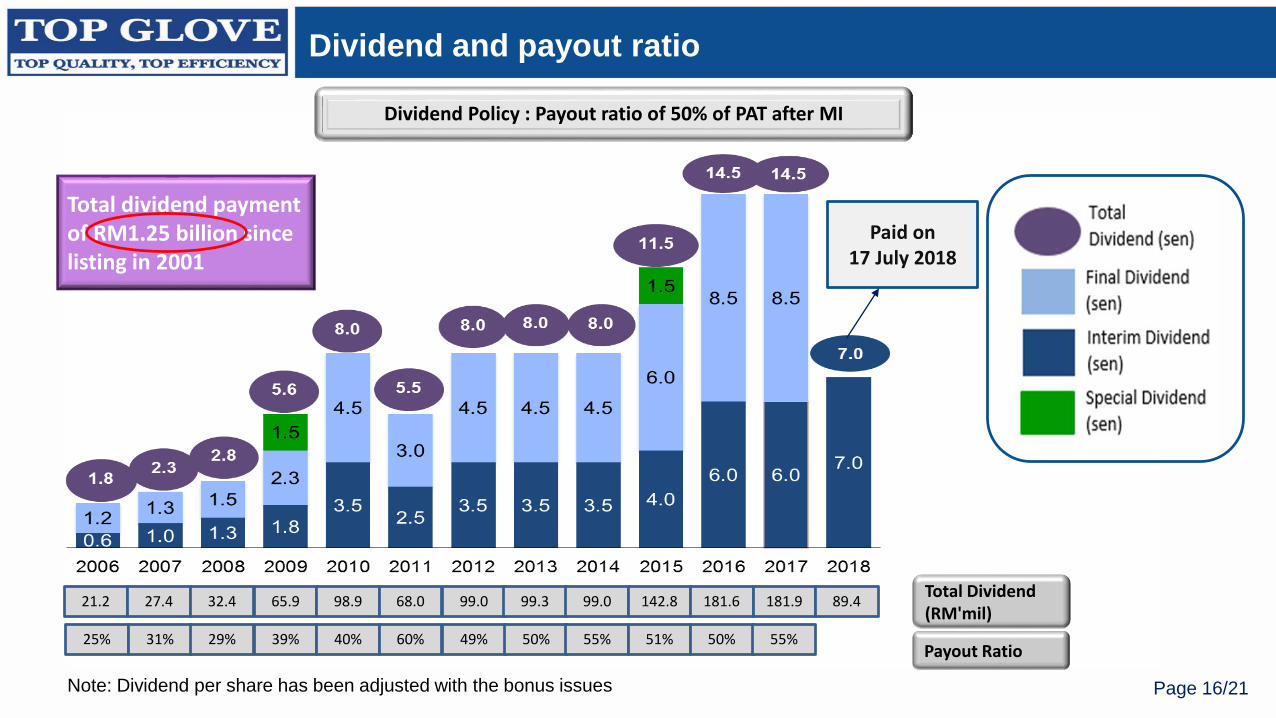

Dividend and payout ratio

Dividend Policy : Payout ratio of 50% of PAT after MI

Note: Dividend per share has been adjusted with the bonus issues

Total dividend payment of RM1.25 billion since listing in 2001

Payout Ratio

Total Dividend (RM'mil)

21.2 27.4 32.4 65.9 98.9 68.0 99.0 99.3 99.0 142.8 181.6

25% 31% 29% 39% 40% 60% 49% 50% 55% 51% 50%

181.9

55%

89.4

Paid on 17 July 2018

Page 17/21

4 310 12 14

2127

32

66 68

99 99 99

143

182 182

0

20

40

60

80

100

120

140

160

180

200

0.0

2.0

4.0

6.0

8.0

10.0

Mar-01 Mar-02 Mar-03 Mar-04 Mar-05 Mar-06 Mar-07 Mar-10 Mar-11 Mar-12 Mar-13 Mar-14 Mar-15 Mar-16 Mar-17 Mar-18Mar-08 Mar-09

Annual Dividends TopGlove

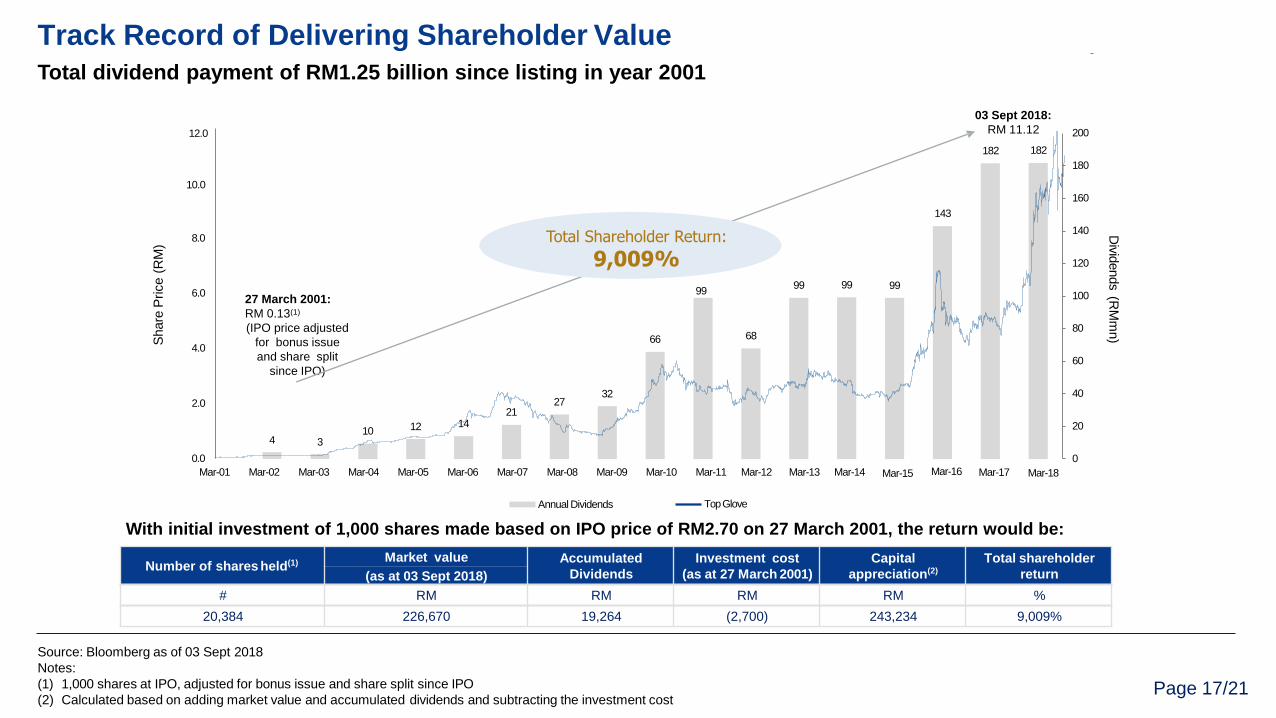

03 Sept 2018:

RM 11.12

27 March 2001:

RM 0.13(1)

(IPO price adjusted

for bonus issue

and share split

since IPO)

Share

Price

(RM

)

Total Shareholder Return:

9,009%

Number of shares held(1) Market value Accumulated

Dividends

Investment cost

(as at 27 March 2001)

Capital

appreciation(2)

Total shareholder

return(as at 03 Sept 2018)

# RM RM RM RM %

20,384 226,670 19,264 (2,700) 243,234 9,009%

With initial investment of 1,000 shares made based on IPO price of RM2.70 on 27 March 2001, the return would be:

Div

idends

(RM

mn)

Source: Bloomberg as of 03 Sept 2018

Notes:

(1) 1,000 shares at IPO, adjusted for bonus issue and share split since IPO

(2) Calculated based on adding market value and accumulated dividends and subtracting the investment cost

Track Record of Delivering Shareholder Value

Total dividend payment of RM1.25 billion since listing in year 2001

12.0

99

Page 18/21Page 18/21

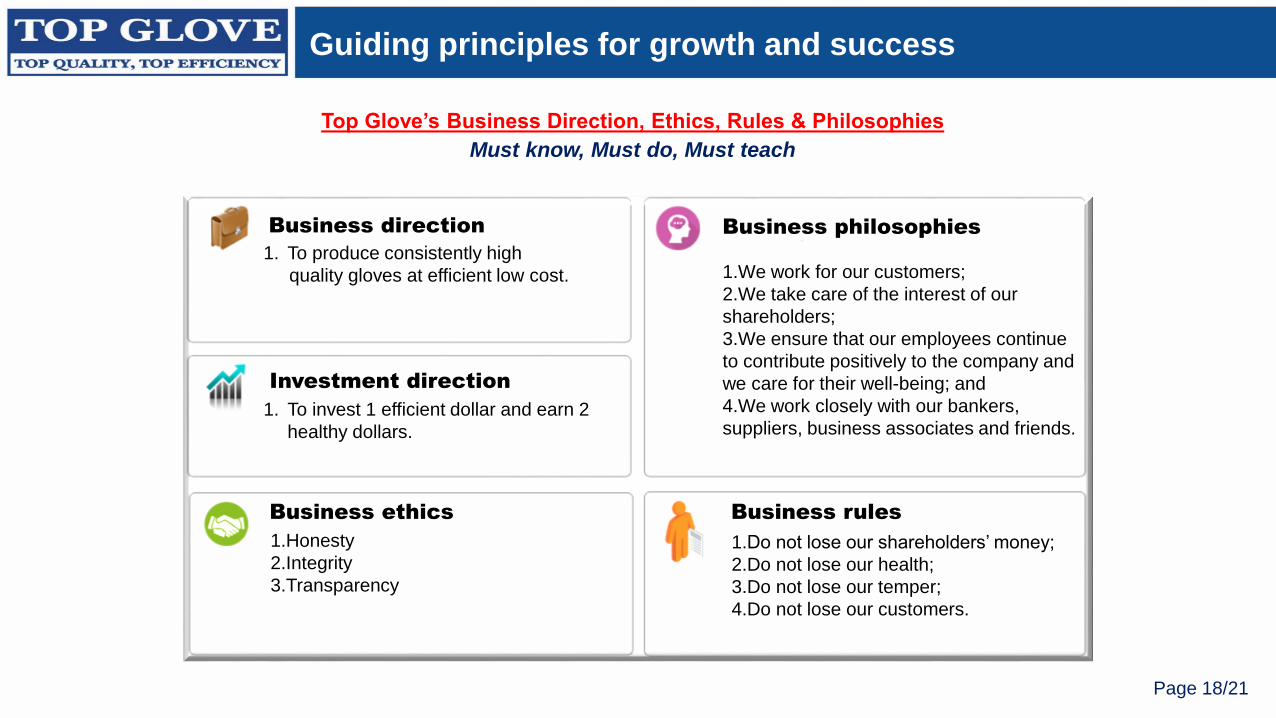

Must know, Must do, Must teach

Top Glove’s Business Direction, Ethics, Rules & Philosophies

1. To produce consistently high

quality gloves at efficient low cost.

1.Do not lose our shareholders’ money;

2.Do not lose our health;

3.Do not lose our temper;

4.Do not lose our customers.

1.We work for our customers;

2.We take care of the interest of our

shareholders;

3.We ensure that our employees continue

to contribute positively to the company and

we care for their well-being; and

4.We work closely with our bankers,

suppliers, business associates and friends.

1.Honesty

2.Integrity

3.Transparency

Business rules

Business direction Business philosophies

Business ethics

Investment direction

Guiding principles for growth and success

1. To invest 1 efficient dollar and earn 2

healthy dollars.

Page 19/21

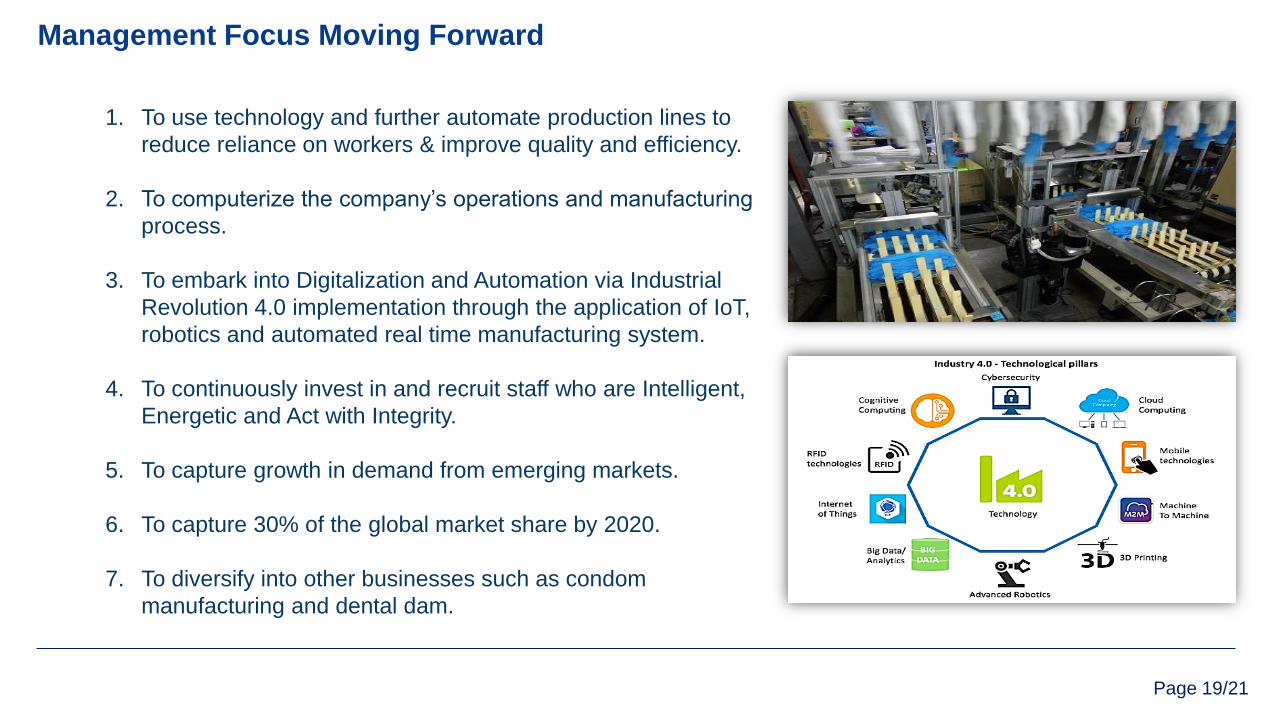

Management Focus Moving Forward

1. To use technology and further automate production lines to

reduce reliance on workers & improve quality and efficiency.

2. To computerize the company’s operations and manufacturing

process.

3. To embark into Digitalization and Automation via Industrial

Revolution 4.0 implementation through the application of IoT,

robotics and automated real time manufacturing system.

4. To continuously invest in and recruit staff who are Intelligent,

Energetic and Act with Integrity.

5. To capture growth in demand from emerging markets.

6. To capture 30% of the global market share by 2020.

7. To diversify into other businesses such as condom

manufacturing and dental dam.

Page 21/21

Ready, 1 2 3

TOP GLOVE

Claps, 2X 3X 2X

YES! YES! YES!

Top Quality

TOP GLOVE GROUP OF COMPANIES

Prepared by : QA Admin (Rev. 6, Date Prepared : 14/7/17)

Verified by : Ms. Loo Sun Nooi / QA DGM

Top Quality

Top Quality