Embed Size (px)

Citation preview

- 1 -

Ghana

HIPC Assessment and Action Program

Prepared by the World Bank and IMF Staff

October 2001

Contents

I. Introduction

II. Assessment of existing capacity to track poverty-reducing expenditures

III. List of the main ongoing and planned technical assistance

IV. Additional short-term measures to help upgrade capacity prior to the HIPC completion point

V. Summary of Action Program

Text Tables Table 1: Summary of Assessments of Public Expenditure Management Table 2: Overview of Donor and Technical Assistance Table 3: Recommended Short-Term Reforms Table 3: Functional Breakdown of Spending by Ministries, Departments and Agencies Text Boxes Box 1 Features of Budget Formulation in 2000 Box 2 Establishing an interim coding structure for tracking of poverty-related spending Appendix I Content of Proposed PUFMARP II

Appendix II Tracking HIPC-funded Expenditures

Appendix III The Existing Chart of Accounts

- 2 -

Abbreviations and Acronyms

ADMU Aid and Debt Management Unit BPEMS Budget and Public Expenditure Management System BOG Bank of Ghana CAGD Controller and Accountant General’s Department CIDA Canadian International Development Agency DFID Department of Foreign International Development (check) FAR Financial Administration Regulations 1979 FAD Financial Administration Decree 1979 EPCC Economic Policy Coordinating Committee GPRS Ghana Poverty Reduction Strategy HIPC Heavily Indebted Poor Countries IFMS Integrated Financial Management System IMF International Monetary Fund MDAs Ministries, Departments and Agencies NFPEs Nonfinancial public enterprises NPIs Nonprofit institutions MOF Ministry of Finance PEDM Public Expenditure and Debt Management PFIs Public financial institutions PRGF Poverty Reduction and Growth Facility PRSP Poverty Reduction Strategy Program PUFMARP Public Financial Management Reform Programme QFAs Quasi-fiscal activities SAI Supreme Audit Institution SSNIT Social Security and National Insurance Trust

- 3 -

GHANA

TRACKING POVERTY-REDUCING EXPENDITURES ASSESSMENT AND ACTION PLAN (AAP)

I. Introduction A joint Bank-Fund mission 1 visited Accra from August 6 to 15, 2001 to prepare a draft HIPC Assessment and Action Plan (AAP).2 The draft AAP prepared discusses Ghana’s public expenditure and debt management needs (PEDM) under the following three sections. (i) An assessment of Ghana’s capacity to track poverty reducing expenditures. This section presents a joint assessment by the team and the authorities relative to specific benchmarks in the areas of budget preparation, execution and reporting. These are shown in Table 1.3 (ii) A list of the main ongoing and planned technical assistance. This section is organized in two key parts. The first section provides a description of relevant projects now under way or proposed by the Bank, the Fund, and other relevant bodies—including bilateral donors--that would contribute to improvements in the capacity of the public expenditure management system. Table 2 provides a list of these projects and a summary of the enhancement that might be expected in the capacity to track poverty reducing spending over the next three years. The second part of this section describes in some detail aspects of these projects likely to be important for improvements in the capacity to track poverty-related spending in the near term. (iii) Additional short-term measures to help upgrade PEDM capacity prior to the HIPC completion point. Some of the main reforms included in Table 3—particularly those expected to make the most substantial contribution to improved tracking capacity—are likely to have a substantial impact only after Ghana reaches the HIPC completion point (2004). These include the principal investments in the development of a Budget and Public Expenditure Management System (BPEMS), and the introduction of a Medium-Term Expenditure Framework (MTEF). Given the weak capacity at present to track expenditures, these medium-term reforms will need to be

1 The mission consisted of Ms. Dawn Rehm (Fund) and Mr. Guenter Heidenhof (Bank).

2 HIPC Assessment and Action Plans are designed to assess the capacity of the authorities to track poverty-reducing public spending; to list planned and ongoing assistance that will upgrade that capacity; to identify any gaps that could be filled by additional assistance; and to prepare an Action Plan comprising ongoing, planned, and proposed new measures to enhance tracking capacity.

3 As there was no proposal for Ghana to participate in a HIPC arrangement when the Bank/Fund AAP program commenced, there was no prior desk assessment of the country’s capacity to track poverty related spending and this mission constituted the first formal assessment for Ghana.

- 4 -

complemented by short-term measures to upgrade tracking capacity over each of the next three years. These recommended short-term reforms are set out in Table 3. A fourth section presents a summary of the proposed actions to be agreed with the authorities. II. Assessment of existing capacity to track poverty-reducing expenditures This section provides an assessment of existing practices and capacity in key areas of the budget process—preparation, execution, and monitoring—in Ghana relative to a set of 15 benchmarks identified in a paper approved by the Fund and Bank Boards in early 2001.4 Before outlining the agreed assessment of Ghana’s PEM capacity against these benchmarks, it is important to mention two sources of uncertainty concerning the requirements for tracking poverty-reducing expenditure in Ghana. First, the particular procedures for the programs and activities will to some extent determine tracking poverty-reducing expenditures identified as specifically directed at poverty reduction. These programs—and the activities within each program that will be funded from HIPC resources—will be set out in the Ghana Poverty Reduction Strategy (GPRS), which will be finalized in October 2001. The second uncertainty pertains to the role of subnational governments in implementing the GRPS. The 1992 Constitution created a subnational layer of government--consisting of 110 Districts and 10 regional councils—which are largely funded from the 5 percent share of total central government tax revenues allocated to the District Assemblies Common Fund. These resources are used mainly to fund development projects, most of which are likely to be classified as being specifically poverty related. At present, there is no systematic reporting on the use of these resources. There are proposals to expand the role of subnational government, but the timing and extent of such activity requires further consideration. In preparing the GPRS, the authorities have recognized that close working relationships between local governments, communities, NGOs, Civil Society Organizations and the local private business sector are important for mobilizing human and physical resources for poverty reducing efforts. They are also aware that public expenditure management capacity at the local level is very weak, and that moves to increase participation of this level of government will require substantial technical assistance to monitor, control and report on expenditure of these governments. Budget preparation Discussions with the authorities resulted in the following evaluations in the area of budget preparation: • Benchmark: Budget reporting follows GFS definition of consolidated central government.

4 “Tracking Poverty Reducing Public Expenditures in HIPCs.” IMF and IDA Board Paper, March 27, 2001, SM/01/16.

- 5 -

There is no comprehensive measurement of general government operations in Ghana, nor has there been an attempt to systematically apply GFS definitions to determine which institutional data would be covered by such a concept. Substantial problems exist with regard to the measurement of consolidated central government operations.5 The national budget presented by the Government of Ghana to Parliament purports to cover the general operations of the central government, including external loans and grants from donors.6 There are, however, a number of deviations from a definition of consolidated central government consistent with GFS standards. Fiscal activities that would normally be included in central government operations--such as petroleum and utility subsidies and assistance to failing banks or institutions--have been effectively undertaken in Ghana through entities that are outside the budget, including nonfinancial public enterprises (NFEs) and public financial enterprises PFIs. In addition, number of agencies undertaking quasi-fiscal activities are also excluded from the budget.7 Equally important, operations of the central government cannot be monitored from available information on “above the line” items. The financial information prepared by the Controller and Accountant General Department (CAGD) covers only a “narrow based budget concept”.8 These reports exclude all project loans and grants--as well as expenditures financed by own account revenues (e.g. from health and education fees)—which are not paid into the central CAGD accounts.9 In order to build a complete picture of poverty related spending, it would be essential to collect information on these latter activities. 10 A separate problem concerns the fact that performance under the “broad based budget” concept presented by government to Parliament is largely measured and monitored on the basis of “below

5 Consolidated central government would cover all general government units controlled by the central government, including the MDAs, the subvented agencies as well as all nonprofit institutions that provide mainly nonmarket services and are both controlled and mainly financed by government units government but would exclude general government activities undertaken by subnational levels of government.

6 This presentation includes grants to subnational governments, but not own revenues raised and spent by that sector.

7 The Social Security and National Insurance Trust (SSNIT) and the Cocoa Board operate outside the budget as independent PFI/NFPE, but also conduct quasi-fiscal activities (provision of student loans by SSNIT, provision of rural extension services by the Cocoa Board).

8 Information prepared by the CAGD includes domestic statutory (mainly debt payments, pensions and gratuities to public servants) and discretionary expenditures by 33 Ministries, Departments and Agencies (MDAs), five major extrabudgetary funds, transfers paid from the budget to subvented agencies, and external program loans and grant flows.

9 Detailed information from the Ministry of Health indicates that internally generated funds accounted for about 11 percent of total expenditures on health. Similar data for the Ministry of Education is not available.

10 Information available from the Aid and Debt Management Unit (ADMU) of the Ministry of Finance (MOF) is not yet fully comprehensive, particularly with regard to grants that are not channeled through the budget.

- 6 -

the line” data on external and domestic financing. There has been no attempt to ensure that the units captured are consistent with the GFS concept of general government. For example, the net movements in about 3,000 government accounts appear to include some operations of several nongovernmental organizations (NFIs), such as Red Cross, which, depending on the nature of the transactions covered, may or may not qualify to be included in general government. 11 Similarly, there has also been no assessment as to whether the activities of about 235 subvented agencies (independently operating agencies some of which have substantial own revenue resources) captured in these accounts are properly classified. Benchmark: Government activities are not funded through extrabudgetary sources to a significant degree. The operations of the major extrabudgetary funds are consolidated within the “narrow budget concept” used by the CAGD.12 The CAGD also maintains some Trust Funds through which nongovernmental operations (e.g., car and housing advances to public servants) are transacted. These are shown as below the line transactions and may contribute temporary financing to the budget sector. • Benchmark: Budget outturn data are quite close to the original budget.

The budget outturn data for the year 2000 varied significantly from the original budget estimates both for the “broad based” general government coverage employed in the Fund PRGF program and for the “narrow based” data reported by they CAGD. The discrepancy can be attributed to both the externally financed and the domestically financed components of the budget. On the external side, there has been a tendency to overstate the project financing inflows (largely matched by under spending on the projects concerned). Within the domestically financed component, expenditures for both wages and debt payments have been significantly understated in the budget. Higher spending for these items has generally been accommodated through reductions in administrative and domestically financed capital expenditures. While present evidence points to a better performance in 2001, there is a continuing need to make initial budget estimates more realistic and to work closely with donors to build more appropriate expectations of project implementation and financing capabilities during the year.13

11 It is possible that, on closer inspection, it will be found that these NGO accounts are used to channel external grants to the government and therefore are properly included in general government.

12 There are presently five major extrabudgetary funds—Roads, Energy, Oil Exploration, Education, and the District Assembly Common Fund—some of which are financed by earmarked taxes: the Education Fund receives 2.5 percentage points of the VAT (currently equal to 20 percent of VAT revenues), while the District Assemblies Common Fund receives a 5 percent share of total taxes. Social security arrangements are also channeled through a separate PFI outside the budget. 13 DFID has pointed out that there is a need for the initial budget estimates to better reflect expected variations in awards during the coming year and then to hold managers directly responsible for variations during the year.

- 7 -

• Benchmark: Budget includes capital and current expenditure financed by donors

As noted above, the national budget estimation presentation to the parliament conceptually includes all donor-financed capital and recurrent expenditures channeled through the budget. These estimates are generally overstated, and the system available to monitor these grant, loan and expenditure flows during the year is inadequate, relying on notifications from individual donors to the ADMU of the MOF. Project grants delivered directly to commercial bank accounts held by MDAs are a particular problem. As indicated above, expenditures monitored through the CAGD do not cover most donor-financed activities or the use of own revenues by budget beneficiaries.14

• Benchmark: Budget classified on an administrative, economic, and functional basis.

A highly aggregated functional and economic type transaction classification–covering both domestic and externally financed expenditures—was used for the 2001 budget. This information, however, is based solely on a reclassification of administrative data on aggregate MDA expenditures, and does not extend to sub-functional groupings. As such, the classification is unsuitable for analyzing poverty related programs such as basic education or health in rural areas, rural roads, power and electricity projects etc. 15

• Benchmark: Poverty-reducing expenditures clearly identified in the budget.

Poverty-reducing expenditures were not separately classified in the 2001 budget and there will need to be a special analysis of the budget to define and then measure such expenditures, as reported expenditures have not included information on a substantial range of donor-financed activities—most of which would be classified as poverty-reducing. In the initial phase it is likely that the base for the analysis (probably 2001) will have to be estimated. The authorities are conscious of the need to quantify the poverty related spending and have established a special Project Implementation and Monitoring Unit within the Ministry of Finance which has been compiling data on such spending for the past there to four years.16 14 The need for improved reporting on donor disbursements has been emphasized, and a number of donors have been asked directly to provide information on disbursements to the ADMU. The response from donors to date has been limited.

15 There are also weaknesses with regard to the classification of revenues: while the main taxes can be distinguished, comprehensive information on nontax revenues is not available. 16 The classifications developed are crude at this stage but offer an initial insight into the usage of spending for poverty-related spending. The data produced was used in the I-PRSP document (paragraph 37 and Table 4) and referred to in the 2001 budget statement (paragraph 338), which states that in 2001 the government allocated “31.3 percent of total discretionary expenditure to improve access to basic social services and infrastructure for the poor. About 60 percent of this allocation is earmarked for basic education, primary health care and provision of safe drinking water for rural areas.”

- 8 -

• Benchmark: Multi-year expenditure projections integrated into the budget cycle.

The MTEF was used to prepare multiyear projections for domestic and external revenues and expenditures within a macroeconomic framework as part of the official budget process in 1999 and 2000. In this context, ministries were required to prepare their budgets within a single capital and recurrent envelope, and major programs included a statement of objectives as part of a gradual shift toward a more output-oriented budget. In support of the MTEF initiative, a budget formulation and presentation software (ACTIVATE) was developed, large-scale training exercises undertaken, and a number of new processes introduced. The following box sets down the timetable that was followed in the 2000 budget preparation.

Box 1. Features of Budget Formulation in 2000

MDA policy reviews and cross-sectoral meetings 31 July, 1999 Policy hearings 24–27 August, 1999 Circulation of three-year ceilings 17 September, 1999 Finalization of submission of three-year estimates 30 September, 1999 Budget hearings between MDAs and MOF 5–22 October, 1999 Finalization of estimates 12 November, 1999 Presentation of MDA estimates to Parliament 30 November, 1999 Presentation of Budget Statement to Parliament 9 February, 2000 Consideration of estimates at parliamentary committees and debate Appropriation Act passed by Parliament 30 March, 2000 BMAs allocate budget details within Ministries Until June, 2000 There were a number of desirable features in the MTEF introduced at that time. First, the concept of shifting from a narrow Government of Ghana to a broad-based total source of funds approach was commendable. Second, the idea of integrating strategic planning and budget making offered the opportunity of shifting resources to where they are most needed. Third, the medium-term focus provided an opportunity to improve sequencing of projects and to draw out the out-year consequences of current policies. Fourth, the arrangements offered the prospect of an increased focus on performance, specifically the specification of outputs and their associated activity costs. Fifth, the MTEF perspective could have been used to achieve better integration of the capital and recurrent budgets. Sixth, there is an explicit attempt to bring nontax revenues into the budget preparation process, irrespective of whether the MDA has been granted the right to retain the receipts automatically.

Notwithstanding these potential benefits, a number of factors undermined the usefulness of the process in this early period including over-optimistic revenue estimates, an inadequate prioritization of expenditures, lack of integration with the budget execution process and excessive use of detail

- 9 -

undermined its usefulness. As a result, the framework was difficult to adapt to changing circumstances—such as the 2000 budget crisis--and was temporarily abandoned in 2001.17 There is an intention to restore and revamp the MTEF in 2002 with assistance from donors and, in doing so, to take into account the Ghana Poverty Reduction Strategy document which is about to be finalized. Budget execution In terms of budget execution, the main benchmarks evaluated are: • Benchmark: Small stock of expenditure arrears, little accumulation of arrears over the past

year.

Weaknesses in expenditure commitment control and payroll management have led to substantial increases in domestic arrears, particularly with regard to road construction contracts. Arrears accumulated in the period to December 2000 have now been documented and forwarded for audit to the Auditor General. A survey of arrears accumulated in the period to June 2001 is currently being completed for subsequent audit. A timetable for liquidation of these arrears will be announced once the audits are completed in late 2001. • Benchmark: Internal Audit is active.

The Internal Audit function in Ghana—which is the responsibility of the CAGD—has not been adequately legislated or developed. While some ministries have established separate internal audit units, there is no consistent methodology, and efforts are largely restricted to routine verification (especially pre-checking of payment vouchers) and inspection work.18 Effectiveness is hampered by resource constraints and lack of follow-up to the findings from investigations. In the absence of effective internal controls, existing rules and regulations are not systematically applied or enforced; instead, they are often replaced by non-transparent informal rules. • Benchmark: Tracking surveys supplement internal control.

Tracking surveys have been limited to the formal tracking surveys in the Ministries of Health and Education conducted by the World Bank: as such they have not been used by the authorities as a mechanism for internal control. Because of the strong sector program being implemented by the Ministry of Health (with the support of several donors, including the World Bank), the accounts, reporting, and auditing for this Ministry have improved greatly, as have internal controls and procurement procedures. An analysis of the incidence of public expenditures using data from the Ghana Living Standards Survey has been completed. Some initial studies have been conducted to

17 These weaknesses are discussed in “Ghana: Country Financial Accountability Assessment,” World Bank, June 2001. 18 DFID has been involved in providing internal audit to the Ministry of Education that could prove a model for wider reform of the internal audit.

- 10 -

try to determine the extent to which existing budget expenditures flow to population groups living in poverty; there are plans for pilot surveys in future (with assistance from donors). The World Bank tracking survey for the Ministry of Education indicated substantial problems with the actual use of funds and a need for reforms similar to those implemented in the Ministry of Health. • Benchmark: Fiscal and banking reconciliation undertaken routinely.

There has been no comprehensive reconciliation of fiscal and banking data for over two years. Some ministries (for example, the Ministry of Health) undertake regular reconciliation of their ministry fiscal accounts with their own bank accounts.19 But these examples are limited and there is no government–wide effort at reconciliation through the CAGD. (However, PRGF program structural benchmarks do specify that an attempt will be made to complete such an exercise in the course of fiscal year 2001).

Budget reporting In terms of budget reporting, the position is as follows: • Benchmark: Internal budget reports from line ministries received within four weeks of the

end of the relevant period.

After a two-year hiatus, the CAGD has recently recommenced the preparation of internal monthly reports on “a narrow budget” coverage. The reports are available with a lag of 4 to 5 weeks, and efforts are under way to reduce the lag to 3 weeks. Delays are caused, in part, by a heavy reliance on hand tabulations that must be transported from the 125 treasuries (110 of which are outside Accra) to the central office for processing. Once received in Accra, the information must be keyed into computers before reports can be assembled using accounting software. Plans are under way to have a substantial share of this processing completed within the regional treasuries, allowing for a more timely compilation of the aggregate reports in Accra.

• Benchmark: Functional classification is reflected in the in-year budget reports.

As noted above, there is no comprehensive functional classification covering both domestic and externally financed expenditures for within year reporting. While a functional report on domestic expenditure by MDA can be constructed on a monthly basis, such a classification would not be adequate to track poverty-related spending. Meanwhile, the data produced by the CAGD does not cover external grants and loans and a special functional analysis of the data compiled by the ADMU would be necessary to complete a comprehensive functional analysis.

• Benchmark: Closure of the accounts occurs within two months after the end of the fiscal year.

19 The Ministry of Health does not, however, routinely reconcile GOG spending with records held at local treasuries.

- 11 -

Existing budget regulations require the CAGD to present a set of annual public accounts and financial statements to the Auditor General and the Parliament within three months of the end of the financial year. However, no annual accounts have been prepared for two years, and only four MDAs submitted completed accounts in 2000. • Benchmark: Audited accounts presented to the legislature within 12 months of the end of the

fiscal year.

The Supreme Audit Institution (SAI) has not presented an audit of the consolidated accounts to the legislature since 1997. The World Bank has noted that “weaknesses in internal controls and in MDAs accounting and reporting systems, the failure of MDAs to produce timely accounts, the general erosion of civil service salaries (making it hard to retain professional staff), diminished resources for the Accountant General, and the lack of follow up of audit findings by the MDAs, have all contributed to the diminished effectiveness of the external audit function in recent years.” 20

Parliament enacted the Audit Service Law in 1999 in an effort to strengthen the AG’s independence and expand his authority--including the authority to carry out economy, efficiency and effectiveness audits—thus allowing the AG to focus on both performance and compliance. The law also allows the AG to submit his budget, via the President, directly to the Parliament, where it becomes a charge on the Consolidated Fund (thus ensuring some independence in funding allocations). The law also creates Audit Implementation Committees in all MDAs, with responsibility for pursuing matters raised by the AG or by parliament and for providing annual reports on the AGs’ recommendations and proposed remedial actions.

Summary of Assessments Although the new administration has made some important strides in resuscitating PEDM arrangements in Ghana--which had virtually been allowed to collapse under the previous government--much remains to be done to build on this initial work. The agreed rankings shown in Table 1 suggest that Ghana is among a substantial group of other HIPCs countries in Africa that require considerable upgrading of their PEDM capacity, especially in the area of tracking poverty-reducing expenditures. The absence of adequate reporting of expenditures financed by donors and own revenues poses a particularly severe problem for estimating the base level of poverty reducing expenditure in Ghana, and for ensuring that in-year reporting is reliable. III. Ongoing and planned assistance to upgrade capacity to track poverty-reducing expenditures While a wide range of donors and multilateral institutions are active in providing assistance that will directly or indirectly enhance capacity to track pro-poor spending, there are four major providers in

20 See “Ghana: Country Financial Accountability Assessment,” World Bank, June 2001, page 11.

- 12 -

particular whose ongoing and planned programs and projects should serve to augment the capacity to track expenditures over the next three years.21 Table 2 sets out the main ongoing and planned assistance in capacity building in the area of public expenditure management relevant to the ability to track poverty-reducing spending. 22 • The World Bank has been the primary provider of assistance in capacity building that will

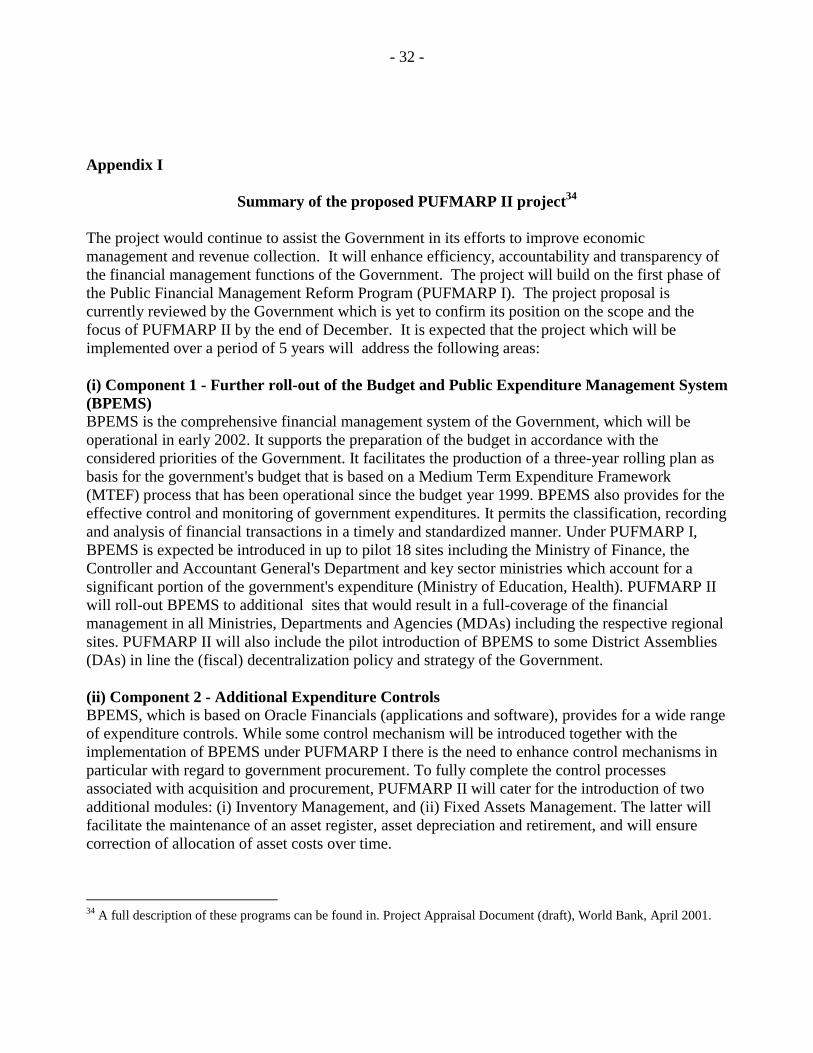

enhance the ability to track expenditures. The main vehicle has been the Public Financial Management Reform Program (PUFMARP), whose initial phase (PUFMARP I) is about to end. The second phase (PUFMARP II) is under discussion with the government, which is currently reviewing the proposed interventions. It is expected that PUFMARP II will cover a broad range of PEDM topics (Appendix I). Most important from a tracking viewpoint is the development of a Budget and Public Expenditure Management System (BPEMS) that will provide capacity for the CAGD and ultimately MDAs to provide timely reports on budget performance. Other PUFMARP II reforms touching on the HIPC process are likely to include programs to improve governance, accountability and transparency, as well as public expenditure reforms and assistance for the implementation of the revenue agency reform. Support will be provided for the development of a new procurement law that is expected to be approved by Parliament in the near future: PUFMARP II will provide assistance for its implementation and for the establishment of a new procurement oversight body.

• The UK DFID has provided assistance to improve information systems in the CAGD through the development and implementation of an integrated payroll and personnel management database (IPPD) system. 23 DFID has recently reviewed its involvement in the project. Further engagement will depend on a clear implementation plan, and revised consultancy arrangements that, inter alia, will involve close supervision and vetting of developments to ensure proper quality control. DFID has also provided assistance in the development of the MTEF under the PUFMARP I umbrella. Delays in implementing the BPEMS contributed to a general loss of momentum in further developing the MTEF, and the project must now be rejuvenated and remodeled to accommodate the poverty reducing initiatives to be set down in the GPRS. DFID is presently considering a proposal to assist in this task in the context of formulation of the 2002 budget.

21 There are also some sector specific initiatives in health, education and agriculture supported by donors that may also involve new financial management and tracking techniques which will also enhance tracking capacity. These could not be thoroughly reviewed during the mission but resident Bank and Fund staff should examine their possible contribution further.

22 Although most of this assistance is directed to the central government and its decentralized entities in the provinces and districts, some programs are aimed at strengthening capacity among subnational levels of government.

23 DFID support for the IPPD has terminated. Further support depends on the formulation of a mutually acceptable implementation plan.

- 13 -

• The EU (under the umbrella of PUFMARP I) has financed work by the Swedish and British

National Audit Offices to strengthen the Supreme Audit Institution (training, capacity building, modernization, the development of a consistent methodology and the harmonization of procedures). The project will run till 2003. Assistance from the EU also supported a review of the internal audit system, and recommendations aimed at a rationalization of the regulatory framework for public sector financial management have recently been submitted to the government for review.24 It is expected that the work on the adjustment of the regulatory framework will be completed in late 2001 or early 2002.

• CIDA has provided assistance for the recently completed design phase of the fiscal decentralization project included under PUFMARP I. The draft report is currently under review by the various stakeholders. World Bank support for the fiscal decentralization project under PUFMARP II is anticipated in the form of support for implementation of a modified BPEMS system at the district assembly level.

• The Fund has installed a resident budget expert in the Ministry of Finance in August 2001.

His principal role is to assist in the improvement of the existing expenditure, aid and debt management processes. A major focus will be the implementation of cash and commitment control systems and the monitoring and management of payment arrears. The expert will also assist with improvement of budget preparation and reporting arrangements and in the compilation and reporting of external and domestic debt. His terms of reference also envisage a role in assisting the authorities to develop interim systems that can help track poverty-reducing spending.

A consortium of donors has been assisting in the development of public expenditure management and information systems in the Ministry of Health. DFID has indicated an interest in extending its present involvement in the development and analysis of public expenditures to the Ministry of Education. Progress—both to date and planned—with regard to the main projects that will most directly contribute to improvements in the capacity to track poverty reducing spending is as follows: (i) BPEMS The introduction of the computerized, integrated financial management system (BPEMS) has been complicated by some key implementation difficulties and delays that should be resolved by mid

24 Current regulations comprise the Financial Administration Decree (FAD, 1979) and the Financial Administration Regulations (FAR, 1979)

- 14 -

December 2001. Pending final resolution of the issues that have caused delays, the project will be extended for another year and has been adjusted to take account of the delays and practical constraints. The roll out of the new system will now center on the Ministry of Finance and the CAGD, and will concentrate on an early start up in the Accra region—which accounts for about 80 percent of total budget transactions. The initial rollout phase will include up to18 sites (15 sub-treasuries of the CAGD, plus the Accra sites of the Ministries of Health and Education). In order to meet the indicated timeframe, decisions will need to be made and implemented much more quickly and decisively than in the past. In a second phase, expected to commence in late 2002, the BPEMS roll out will be extended to 42 key sites. There will then be a consolidation phase to evaluate the experience to date and to allow adjustments and refinements. Discussions between the World Bank and the Government concerning a continuation of the Bank’s technical assistance under the umbrella of PUFMARP II, however, have progressed much more slowly than envisaged and are still awaiting a final response from the Government. Potential sources of financing from the World Bank for the second stage roll-out are therefore unlikely to be available before mid-2002.

While training and capacity building activities for the BPEMS pilot sites (CAGD and Ministries of Health and Education) are progressing satisfactorily, much remains to be done. A trial stage, during which the new systems and existing systems are run in parallel, will extend through 2002. While the new system could be operational in 2003 (at the earliest), it will not initially have full coverage, and will need to be temporarily supplemented by other processes.

There are also a number of managerial issues to be resolved before the BPEMS can be fully implemented. For example, financial reporting in the Ministry of Education is not organized in an efficient manner, and the processes will need to be streamlined prior to the roll-out of BPEMS. The CAGD may also need to consider revisions to the accounting systems used, including to the classification system, which is presently complex and unsuited to tracking poverty related spending (see further discussion in Section IV below). Given the delays in the implementation of the BPEMS, the World Bank has been working with the Fund and the authorities to implement an interim PEDM system featuring quarterly control of cash releases and commitments to facilitate achievement of fiscal targets within the PRGF program. This interim system is discussed further under Section IV below.

(ii) Integrated Payroll and Personnel Management Database (IPPD) The integrated payroll and personnel management database (IPPD) system (implemented with assistance from DFID) has also experienced delays, some of which relate to hardware issues and some to management issues. As noted above, DFID support for IPPD has now terminated. On the basis of a recent review further support is dependent on a revised implementation plan prepared by the government coupled with a clear division of roles and responsibilities between suppliers, GOG and the necessary technical support. At this stage, it seems unlikely that the new systems will be fully operational until the middle of 2002, at the earliest.

(iii) Medium-Term Expenditure Framework (MTEF)

- 15 -

As noted, the Medium-Term Expenditure Framework requires rejuvenation. The main initial task will be to agree on a multi-year macroeconomic framework to guide policy over each of the next three years that will serve as the basis for continued PRGF support and HIPC relief. This will require extensive consultation between the Fund, Bank and the GOG team preparing the GPRS. This work must be completed by the time of the HIPC decision point, which is presently expected to take place in December 2001 or early 2002.

Consistent with the adopted macroeconomic framework, there will be a need to develop detailed revenue and expenditure plans, which take account both of the need to fund existing essential services and new poverty related spending initiatives contained in the GPRS. The annual budget appropriations developed within this framework will then have to be agreed by the parliament.

The budget preparation process must be scheduled to dovetail with this decision process. To this end, a budget call circular is presently being drafted with assistance from the IMF resident fiscal advisor. The circular will be directed to three main tasks: (i) determining the cost of existing government policies to be funded from existing sources of funding; (ii) identifying that portion of existing policies that are directed to addressing specific poverty related issues; and (iii) costing of any new policies being proposed by MDAs.

This approach would leave for separate consideration the costing of any new policies that are to be funded out of HIPC assistance, as proposed in the GPRS being developed by the GOG. The estimates prepared in this process would be prepared on the understanding that adjustments may be necessary to existing expenditure policy to make room for new policies proposed in the context of the GPRS. The Fund resident advisor will be available to assist this process and DFID has also indicated a willingness to fund an advisor to assist in the budget preparation process.

Notwithstanding this initial work, further assistance will be required to develop the MTEF into a useful fiscal management tool. The basic concept behind the MTEF is to provide decision-making discipline, so as allocate resources to where they are most valued within the context of an aggregate spending ceiling—to allocate according to needs constrained by availability. As noted earlier, the key improvements required in this process are greater high level involvement in the priority setting process and greater integration between the decisions made in the budget context and the subsequent budget execution process, including production of within year reports on the same coverage as used in the budget documents. No doubt, there are a number of measures that could be taken to strengthen budget preparation and gain greater benefit from the application of the MTEF. For example, a FAD technical assistance mission in 2000 25 made a number of recommendations for improving the MTEF including:

25

See “Ghana: Reforming Budget Execution” by Barry H. Potter, James Brumby, Pokar D. Khemani, and Michael Woolley, October 2000.

- 16 -

• The process and criteria for adjusting baselines in the face of shortfalls in available resources should be made clear.

• The classification logic of the split between objectives and outputs should be reviewed and improved to remove overlaps and to clarify the concepts.

• The development of a mid-year review to compare performance against current year budget track and to adjust out-year estimates should become a formalized part of the annual budget process.

• Revenue forecasting should be improved and benefits from levying nontax revenue should be shared.

• A system of limited carryovers (up to 10 percent of unused Item 4 allocations) should be introduced.

• Timing of budget preparation should be brought forward to allow better planning and execution by MDAs.

These and other measures need to be examined further by the Fund, Bank and other donors when planning the best method of rejuvenating the MTEF.

(iv) Other reforms under the PUFMARP I umbrella

It will also be important to continue other key reforms initiated under the PUFMARP I umbrella, in particular the procurement reforms and the reform of the internal/external audit functions. It will be critical for the Government to review the respective reform proposals and to ensure that they are subsequently implemented without undue delay.

Some intended reforms will require further analysis and discussion between the Government and the donor community, which should commence soon to ensure that implementation can proceed quickly. This refers in particular to the need for a new legal and regulatory framework for financial management to complement the arrangements specified in the Constitution. The Financial Administrative Regulations (FAD) and the Financial Administrative Decree (FAD) were adopted in 1979. These documents are complex and sometimes difficult to follow and are not properly enforced. The adequacy of the exiting Chart of Accounts also needs investigation. A new chart has been drafted as part of the BPEMS project that utilizes a 37-digit code. Such changes will require careful consideration. Whilst they may offer additional scope for finer dissections of information (which may assist in the tracking of poverty related spending) they also add complexity of the processing task (and hence could jeopardize the timely production of essential reports). Past experience with code structure changes in Ghana has not yielded favorable outcomes and it may

- 17 -

ensure the new computer system can operate with the existing chart of accounts structure before moving ahead with further reforms.

In the circumstances, it is desirable for the authorities to consider the introduction of bridging mechanism approaches, building on what they have already initiated to date, to enhance the capacity to track over the next three years. IV. A program of short-term reforms While there is general support for the proposed focus on the MTEF, BPEMS and other measures indicated in Section III, it is important to acknowledge that progress in upgrading the capacity to track poverty-reducing spending, as a result of work on these essentially medium-term projects, will be limited over the next two to three years. In this context, there are three main tasks to be dealt with in the short term. First, it is essential that the PEDM systems are adequate to ensure macro fiscal targets can be met, arrears are avoided, and broad budget allocations respected. Second, it is important to develop a capacity to track poverty related spending initiatives, including those funded by HIPC relief. Third, other short-term initiatives are needed to improve PEDM management and the quality of public expenditure data generally. Each of these issues is considered further below. (i) Tasks required to meet macro fiscal targets in Fund/Bank PRGF programs This first task is presently being handled through an interim package of initiatives to improve PEDM being supported under Fund and Bank programs. There are two basic components to this interim package: (a) The establishment of an integrated cash planning and commitment control system involving: • The creation of an Economic Policy Coordinating Committee (EPCC) consisting of officials of the MOF, BOG, CAGD and the main revenue agencies to oversee the forecasting and monitoring of expenditure commandments and cash transactions month by month. • Preparation of a quarterly cash flow plan by the MOF, updated each quarter, which is used to determine a set of quarterly ceilings on cash releases to MDAs. The initial cash ceilings covering the September and December quarters of 2001 were released in July and are now in effect. • Reintroduction of a commitment control system linked to these quarterly cash ceilings (rather than, as previously, to departmental annual appropriations), with MDAs required to limit commitments to projected cash availability. • Central settlement of water and electricity utility bills by the CAGD to facilitate control of commitments and limit the possibility of arrears: these payments are netted against cash releases to MDAs.

- 18 -

• Monitoring of the performance of MDAs against ceilings by the EPCC through specially developed monthly reports prepared by the CAGD on budget outcomes, including cash expenditures and commitments. Two sets of reports will be provided with a lag of four weeks after the end of the reporting period: (i) a report on aggregate budget cash revenue and expenditure outcomes and commitments within a broad economic classification; and (ii) a report on cash expenditures and commitments by MDAs classified by function. Once these reports achieve a satisfactory quality, they will be published in the government gazette. • The CAGD and the BOG will put in train action to reconcile the aggregate monthly budget reports with banking data by the end of the year. The World Bank agreed to finance some equipment for this interim cash and commitment control system (mainly computers and fax machines) under the existing PUFMARP I credit. This equipment is directed to speeding the processing of the dates produced by the 125 sub treasury offices in Accra. One aim of the new system will be to encourage greater data preparation within the treasury offices themselves so as to minimize delays in transmission of data. The Bank has also agreed to fund a consultancy study to assist the authorities to operationalize the new system, in particular to establish adequate information flow and reporting mechanisms. It is unclear how long this interim system will need to function. As indicated in Section III, the BPEMS should be operative by 2003 (albeit without full coverage), and the interim system can then be merged with the BPEMS project. The details of the migration will need to be worked out in the next few months.

(b) Improvements in debt management procedures to ensure full and timely settlement of external debt obligations, including: • Weekly updates by the BOG to the ADMU and CAGD on payments made by the BOG for external debt obligations; • Daily updates from the BOG to the CAGD and ADMU on external payment requests awaiting funding at the BOG; • Requests to donors for advance notification of the exact amounts due for interest and charges; • Provision by the ADMU to donors of a register of existing external debt obligations, to be expanded to include all external obligations guaranteed by the government or the Bank of Ghana; • Provision by the ADMU to the budget unit of the MOF, CAGD, and BOG of projections updated monthly for debt service obligations coming due.

(ii) Developing capacity to track poverty related spending

- 19 -

This second task of monitoring the desired shift toward pro-poor spending and, in particular, use of HIPC resources will require three types of information: • Information on the proportion of the government budget (including donor-financed programs) going toward poverty-reducing expenditures—which is necessary to demonstrate that resources released under the HIPC initiative expand the total effort on poverty-reducing programs (rather than, for example, substituting for resources in the general government budget); • Information on the resources made available by donors under the HIPC initiative. • Data on the actual use of those resources. • Material—at least on a credible sample basis—that looks beyond accounting records to establish whether funds intended for a particular program reached the intended beneficiaries. To this end, it will be necessary for the authorities to:

• Determine what constitutes poverty-reducing spending—which is not necessarily synonymous with social sector spending—and then construct a budget for these expenditures as a subset of total spending plans, initially for 2002, and subsequently for the remaining forward years of the revised MTEF.

• Ensure that actual expenditures can be tracked against that poverty-reducing budget in some fashion. Initially some bridging mechanism may need to be used (possibly using estimation techniques) but a more permanent and accurate information system will have to be put in place before the HIPC completion point is reached.

• Arrangements to channel the resources to be released under the HIPC Initiative into a new sub-account to be established in the Bank of Ghana. It is expected that the authorities may also wish, for their own purposes, wish to implement arrangements to track spending on poverty related spending items that is funded from the HIPC sub-account;

Each of these steps is considered in more detail below.

•••• How to define and construct a budget for poverty-reducing spending The authorities are still developing their proposals, in the context of the PRSP process, on how Ghana would use prospective relief under the enhanced HIPC initiative. The government has stated an intention to use some of the relief for domestic debt reduction.27 However, some donors and HIPC creditors may not agree with such a proposal.

27 See GPRS document which mentions the possible use of 10 percent of HIPC relief to reduce domestic debt (page 24).

- 20 -

As noted earlier, the authorities have been conducting some preliminary work on this initiative over the last three to four years and have developed an approximate classification in the special Project Implementation and Monitoring Unit within the Ministry of Finance. However, the data compiled relates only to estimates and does not cover actual budget outcomes. It is recommended that further work be undertaken to attempt to define poverty-related spending within an overall functional analysis of spending for 2000 and, if available, 2001 data. This analysis would then serve as a base for assessing additionality in poverty related spending for the years 2002-04. If some funds are set aside for debt servicing these should be explicitly recognized in the classification. •••• Answering the basic question: is total poverty-reducing public spending in the economy

increasing? A basic problem that Ghana shares with a number of other African countries—albeit perhaps to a greater extreme—is the absence of a functional or program classification that would provide a suitable basis for tracking actual spending on poverty-related items in a comprehensive manner. As a result, it is difficult to put together a satisfactory assessment of poverty-reducing expenditures for 2000 and 2001, against which progress, in terms of a shift toward more pro-poor spending, can be assessed in the years 2002-04. The work done by the Project Implementation and Monitoring Unit may be able to be adapted to provide some crude estimate poverty-reducing expenditures in 2000 and 2001, to serve as a baseline for assessing the desired shift to more pro-poor spending. However there will then be a need to track spending in subsequent years within a similar framework, which will be difficult given the virtual absence of disaggregated information for most MDAs on actual domestic spending by program categories, and by the absence of comprehensive functional estimates on donor financed spending. Once the BPEMS system becomes fully operative the capacity to disaggregate data into finer dissection should improve, particularly if all donor funds are channeled through the accounts and changes are made to the Chart of Accounts and associated coding system. However, the present interim system can only handle a highly aggregated functional breakdown of spending by MDAs (see Table 3). It is true that the 15 digit code now in use (see Appendix 3) should be capable of providing a finer classification but the CAGD (and most ministries) do not presently maintain sufficient quality control over the coding and processing system to enable these dissections to be used with any assurance of accuracy. In these circumstances two alternative approaches seem possible. First, it may be able to adopt the existing 15-digit code to accommodate some additional disaggregation of MDA spending into, say, ten to twenty highly important poverty related categories of spending. One possible adaptation to the coding that could accommodate such information flows is discussed in Box 2 below. The CAGD would need to implement special arrangements to ensure that some quality control over the processing of this data. Donor flow data to complement this data on MDA operations would need to be compiled manually by the ADMU of the MOF and it may be necessary to approach donors to

- 21 -

obtain finer breakdowns of their loans and grants into the selected categories. This task is discussed further under (c) below. A second option would involve estimating this breakdown from a variety of sources of information. Within the domestic expenditures some attempt may be made to split up actual expenditures for each MDA using surrogate measures, such as number of persons employed on different programs, analysis of capital expenditure projects. As with the first option, special arrangements would be needed to obtain complementary data from donors. Whilst it is not regarded as essential to the HIPC tracking process, many countries have expressed a desire, for their own purposes, to measure the inflow and outflow of HIPC funds used to fund the poverty related budget. If the authorities decided that they wished to follow this process, it would be desirable to take two further steps: (i) to create a bank account at the Bank of Ghana into which resources calculated as being available under HIPC—that is, funds released by the reduction in debt service requirements, compared with the pre-HIPC debt service profile--are paid. The funds available would be transferred from the main consolidated fund account (using a separate code identified by the CAGD); 28 and (ii) to identify the relevant expenditures for poverty-related programs financed from HIPC, the authorities could employ either one of the existing coding classifications contained in the CAGD's chart of accounts as explained in Box 2 below. A description of the possible approach to tracking HIPC monies is also set out in Appendix II. It is recommended that the authorities, with assistance from Bank and the Fund staff, set in train the necessary arrangements, including coding changes to apply from January 1, 2002 29 to (i) monitor the portion of the total budget expenditures that flows into identified poverty-related programs within the functional classification developed under the first dot point above. (ii) to meet their own reporting needs, take steps to establish a separate sub-account at the BOG into which HIPC monies can be paid and to monitor payments from that account to meet portion of the total poverty-related spending budget.

28 Separate sub-accounts with unique identification codes will be needed in the event that funds made available under the HIPC are applied to efforts other than specific, identified poverty reducing activities—e.g. other debt or debt service reduction.

29 Assuming that the HIPC decision point is set for December 31, 2001.

- 22 -

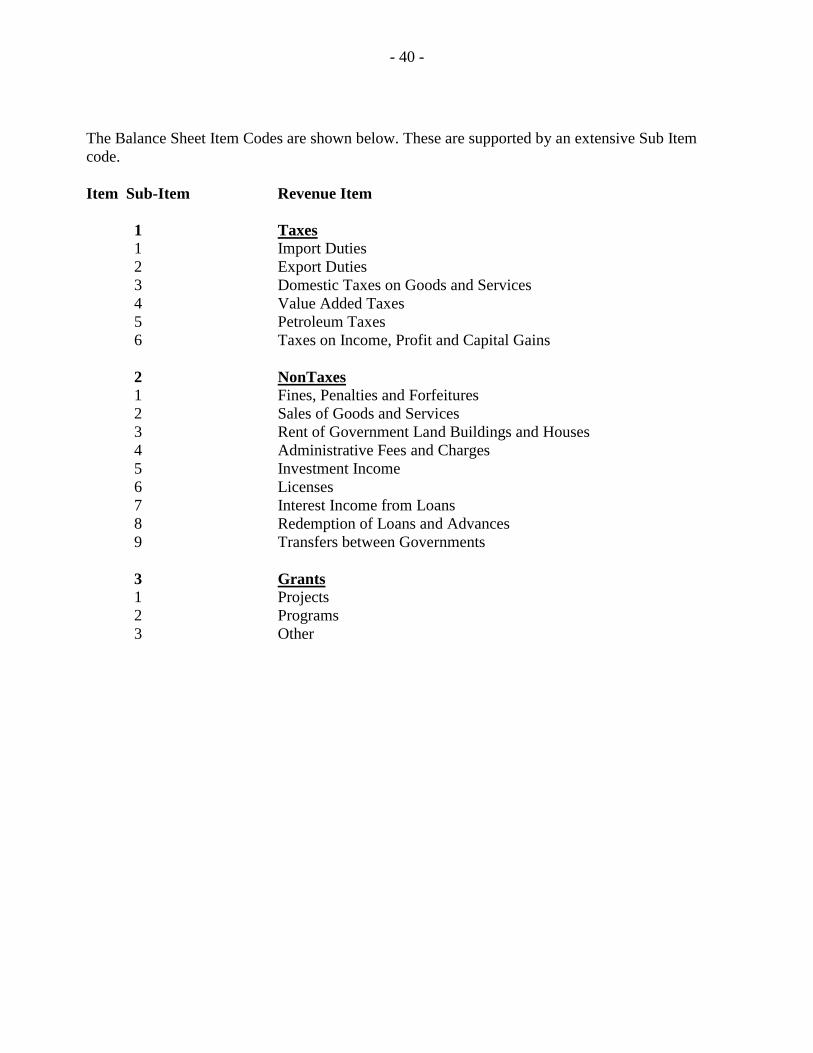

Box 2. Establishing an interim coding structure for tracking of poverty-related spending. Notwithstanding the weakness of the existing 15-digit revenue and expenditure code structure used in Ghana as a basis for GFS preparation (see Appendix III for details of these codes), the authorities could adapt it to identify the relevant expenditures for poverty related programs. There are a number of possible adaptations that could be made but it is important to keep the changes as simple as possible so as not to disrupt the existing (highly tenuous) flow of information. One possible adaptation would be to utilize the fourth digit of the existing code to designate the type of spending. There new codes could be inserted: The alphabetic code “O” (or if desired a numeric code) could be used to designate Ordinary spending (that is, spending that is not designated poverty related); the code “P” could then be used to designate special poverty related spending programs funded by the Government of Ghana; and the code “H” could be used, if desired, to designate that portion of poverty related spending that would be funded by the HIPC funds made available to the government. Another alternative would be to utilize the presently under-utilized seventh code, which is used to specify program objectives. A code could be inserted for poverty related programs financed by the government and another for the HIPC funding of such programs. Yet another possibility would be to utilize the last three codes –again underutilized—to track the source of funding (say a two digit code for GOG, World Bank and other donor funding plus a further single digit code to indicate whether the money was to be sued for poverty related sending or some other GOG purpose. Each possible approach has advantages and disadvantages. For example, if the first procedure were followed the present distinction in the coding structure between ordinary and subvented agencies would be lost. However, since the first three codes are available to code institutions, it should be possible to distinguish these two types of institutions using that code. Similar loss of flexibility would be associated with the second and third alternatives so this matter will need to be discussed and agreed with the authorities prior to the start of 2002. It is also recognized that some other changes to coding may be required. In particular, since the poverty related programs might need to be specially designated (e.g. rural roads, fresh drinking water, rural electricity projects) there may need to be a special codes inserted to specify these sub functions separately from the existing MDA and institutional descriptions (used in codes one to three) and the regional descriptions (used in codes five and six). Since the CAGD Chart already captures the region and the district codes in the 5th and 6th digits, the regional distribution of poverty or HIPC related funds is already catered for.

(c) Accelerating and extending reporting of expenditures on donor-financed projects.

- 23 -

It is in the interests of both donors and the authorities that a record of all poverty-reducing public spending in Ghana is captured. 30 Unfortunately, the CAGD accounting system does not capture information on donor funding and the information collected by the ADMU in the MOF is not comprehensive. Bank account information is also not reliable as some donor funds flow through commercial bank accounts, which are not easily tracked. Moreover, some expenditure is delivered in kind to the authorities (e.g., consultant services) and these flows are often not captured in accounting records. It is recommended that the ADMU of the MOF establish arrangements to more thoroughly monitor donor-financed projects—both the local and imported elements –on a more comprehensive and timely fashion. A common template has been developed by the ADMU to collect this information and it is now necessary to follow up collection of this information with donors. Other short-term initiatives that would improve PEDM management A third set of tasks related to improving the data and general PEDM environment concerns the need for supporting measures that would improve the overall quality of expenditure data (not just that on poverty-reducing spending). The main measures to be considered are as follows: • Action should be taken to properly define the general government sector. There is a need to define the institutional units that go into general government both within the central government (particularly the operation of subvented agencies) and subnational levels of government (including, for example, an analysis of expenditures out of own revenues). The coverage of the general central government also needs to be examined; in particular, consideration needs to be given as to whether the operations of the SSNIT and the some PFI and NFPEs operations (such as the Public Utilities Regulatory Commission and State Enterprise Commission) should be included in the budget. • Review and amendment of budget laws In Ghana, the legal basis to the Budget is principally determined by the following legal instruments: the Constitution, the Financial Administration Decree (1979), the Financial Administration Regulations (1979). There is a need to review the proposed amendments of the regulatory framework for budget and expenditure management (FAR/FAD). The relevant report was submitted to the Government in June and should be reviewed by the Fund and the Bank to ensure the adequacy of the proposed arrangements in the HIPC context. It is also critical to ensure that formal rules are properly applied, and that decisive actions are taken to address the informalities that govern the budget and expenditure management process.

30 From the donors’ viewpoint, as more resources are channeled into poverty projects, the demand for information on uses of the donor funds is likely to increase.

- 24 -

Nonapplication of current framework

It appears that, in several cases, the law is not being applied, and the regulations are not being complied with. For instance, the Auditor-General reported that at the end of 1998, only four MDAs provided annual reports, as they are required to do under the FAD. Three of the four MDAs interviewed by the mission indicated that the reporting requirements on accounts and unpaid bills were not being complied with. The Budget Director confirmed that, despite notification earlier this year of the need to furnish quarterly reports to MOF and the Select Committee, this requirement was not being followed (although, no reporting format had been issued by the MOF.) It was also clear in our discussions that aspects of the FAD, such as the power to revote funds, had not been applied and was not a known feature of the PEM system. There is also some evidence that in order to manage the transition from one year to the next, some MDAs engaged in deliberate breaches of due processes through the use of improper procurement and payment procedures so as not to lose funding. Where the MOF has become concerned, for instance, about the evidence of “ghost” projects, it has responded specifically to that, adding another layer of regulatory requirement with the certificate for the commencement to start work. The current framework is cumbersome, involving more than 900 regulations. Communication from the MOF has suggested that substantial additional changes will be made to the operation of the regulations for instance to make cost center managers, rather than Vote Controllers, the designated responsible officer for financial management. Accordingly, there seems to be both a high degree of uncertainty about the applicability of the existing stock of rules, and also some ignorance of the regulations. In such circumstances, the choices are either to enforce the current framework or amend it to reflect the new priorities associated with public financial management and ensure that these are communicated and enforced. The MTEF has represented something of a shock to the structure and form of the budget. Not surprisingly, aspects of the legal and regulatory framework are now at odds with this new approach. Examples include the following: • The general warrant no longer includes all recurrent expenditures, but instead relates to

Items 1 and 2 only (so-called overhead expenses relating to personal emoluments and administrative expenses).

• The broad-based budget concept does not appear in the regulations, but was announced via circulars.

• Other aspects of the PUFMARP-related projects, such as the introduction of a power for the audit service to conduct value for money audits, are also resulting in change to the core budgetary laws.

• Measures to monitor and audit arrears.

- 25 -

It is vital that the data on recorded expenditures and the proportions devoted to poverty-reduction are not distorted by the existence of payment arrears. A comprehensive in-year reporting system needs to be developed by the Accountant General.

• Action to bolster internal audit capacity remains critical to making the budget execution process more effective.

There is a need to expand the resources devoted to this function beyond the present pre-audit work by building up the systemic audit inspections, and developing performance audits.31 The findings and recommendations of EU-financed study should be discussed and an action plan developed to strengthen the internal audit function over the medium term. At present, the internal audit service is not in receipt of assistance from donors or the multilateral institutions. Training, the development of detailed up-to-date manuals, as well as investment in equipment could considerably augment capacity and effectiveness. This would give more assurance on the quality of all expenditure data, including that on poverty-reducing spending.

• Consideration needs to be given to ways to make the external audit more effective. While the legal framework and resources available to the external audit may be considered adequate, 32 there is a need to make the work of the SAI more effective, including by restoring CAGD reports as a basis for external audits. It is also necessary to strategically focus the activities of the SAI on areas that are deemed critical for achieving the Government’s objectives.

• Actions to continue and institutionalize procurement reforms.

The procurement reforms should be continued on a priority basis. In particular, the new procurement law should be put in place by the end of 2001. It will be critical to ensure compliance with the new regulations based on comprehensive training and capacity building activities once the new law is approved by Parliament.

Many of these measures could be undertaken with the support of donors and the multilateral institutions, perhaps building on their respective comparative advantage in different areas of public financial management. In many cases, however, it is also quite feasible for the authorities themselves to take the necessary actions—for example by increasing the share of budget resources allocated to internal audit activities.

31 One consequence of the emphasis on pre-audit is a weakening of the incentive for the accountant to undertake efficient pre-checking on transactions. Thus its removal on a selective basis could release resources for more work on inspections etc, without damage to the effectiveness of expenditure control.

32 See “Ghana: Country Financial Accountability Assessment,” World Bank, June 2001. In footnote 4, page 11, the Bank points out that the budget ceiling in 2000 of 1.5 percent of total expenditures audited is well above international norms.

- 26 -

The above list is intended to help the MOF consider priorities for upgrading their capacity to track poverty-reducing expenditures: it is for the MOF to take the lead in discussions with the multilateral institutions and individual donors, where they wish to seek help. V. The proposed action plan The proposed action plan is designed to improve the authorities’ overall public expenditure management capacity, with a particular emphasis on the improvements needed to ensure tracking of poverty-reducing expenditures.

(i) The Short-Term Reforms to be implemented before the HIPC decision point 33

• Top priority to be placed on fully implementing the cash and commitment control and expenditure and debt reporting arrangements set down as structural conditions in the PRGF. As part of this program the authorities should implement the interim computer arrangements outlined under section IV above.

• Develop a poverty alleviation budget within the context of the overall 2002 budget. The initial budget may include an allocation for debt relief and only a limited number of additional items that can be tracked with the interim computer arrangements.

• Set in train the necessary arrangements, including coding changes to apply from January 1, 2002 to monitor the portion of the total budget expenditures that flows into identified poverty-related programs.

If the authorities wish, for their own purposes, to track the inflow and usage of HIPC monies, they should (i) establish a separate account at the Bank of Ghana into which HIPC monies can be paid; and (ii). develop procedures to track the use of HIPC monies within the overall poverty related budget to be developed (as described above).

(ii) The Short-Term Reforms to be implemented by end-2002

• Top priority should be addressed to monitoring poverty related spending using the same classification developed for the GPRS and the 2002 budget.

• Work should be started on development of estimates of actual spending in 2000 and 2001 within the special classification sue to develop the poverty related budget for 2002. This will serve as a base for assessing additionality in the subsequent period prior to the completion date,

33 For the purposes of this report the short term has been defined as improvements that need to be implemented in the period before the end of 2003.

- 27 -

• The definition of the institutional units to be covered by the general government sector in Ghana and the subsequent derivation of more comprehensive general government expenditure data, including by coverage of expenditures financed from fees and charges and spending by local assemblies from the Common Fund and own revenues sources.

• Develop more comprehensive and timely expenditure data on donor-financed projects to improve the overall coverage of poverty-reducing public spending in Ghana. This information should be funneled into improved data on poverty-related spending within the budget mentioned above.

• Implementation of a pilot PETS tracking exercises to cover some specific poverty-reducing programs financed by donors, by the HIPC sub account.

• The pilot introduction of the BPEMS integrated financial management system in the MOF, CAGD and key sector ministries

• The development of a new Chart of Accounts in the context of the introduction of the new BPEMS integrated financial management system with a view to providing finer disaggregation of spending, including for poverty-related items

• The amendment of the legal and regulatory framework for the budget and expenditure management in Ghana

• A reformed and augmented internal audit capacity with increased human resource capacity, that operates under clear guidelines and under a consistent methodology and focuses more on selective audit, systems audit, and inspections, and less on pre-audit.

• A strengthened external audit capacity.

• The introduction of a new procurement law with subsequent training and capacity building to help institutionalize the new regulations.

(iii) The Medium-Term Reforms

• The implementation of the BPEMS integrated financial management system and of the integrated payroll and personnel management system.

• The rejuvenation of the MTEF initially implemented in 1999.

• The strengthening of internal and external audit functions and the enforcement of compliance with rules and regulations

• The improvement of governance and accountability as envisaged under the economic governance component of the PUFMARP II project.

• The implementation of a PETS project.

- 28 -

BUDGET MANAGEMENT Benchmark Agreed AssessmentCOMPREHENSIVENESS1. Budget reporting follows GFS definition of consolidated general government. A C2. Government activities are not funded through extrabudgetary sources to a significant degree. A B

3. Budget outturn data (levels, functional allocation) are quite close to that of the original budget. B C4. Budget includes capital and current expenditure financed by donors. A BCLASSIFICATION5. Budget classified on an administrative, economic, functional basis. B C6. Poverty-related expenditure clearly identified in the budget . A CPROJECTION 7. Multi-year expenditure projections integrated into the budget cycle . A B

INTERNAL CONTROL

8. Small stock of expenditure arrears; little accumulation of new arrears over past year. A C9. Internal audit is active. A C10. Tracking surveys supplement internal control. B BRECONCILIATION

11. Fiscal and banking reconciliation undertaken routinely. A C

REPORTING

12. Internal budget reports from line ministries/Treasury received within four weeks of the end of the relevant period. B C13. Functional classification is reflected in the in-year budget reports. A CFINAL AUDITED ACCOUNTS

14. Closure of the accounts occurs within two months after the end of the fiscal year. A C15. Audited account presented to the legislature within 12 months of the end of the fiscal year. B C

Notes: Shading: Meets benchmark

Table 1: GHANA: TRACKING POVERTY-RELATED SPENDING IN HIPCsFo

rmul

atio

nEx

ecut

ion

Rep

ortin

g

- 29 -

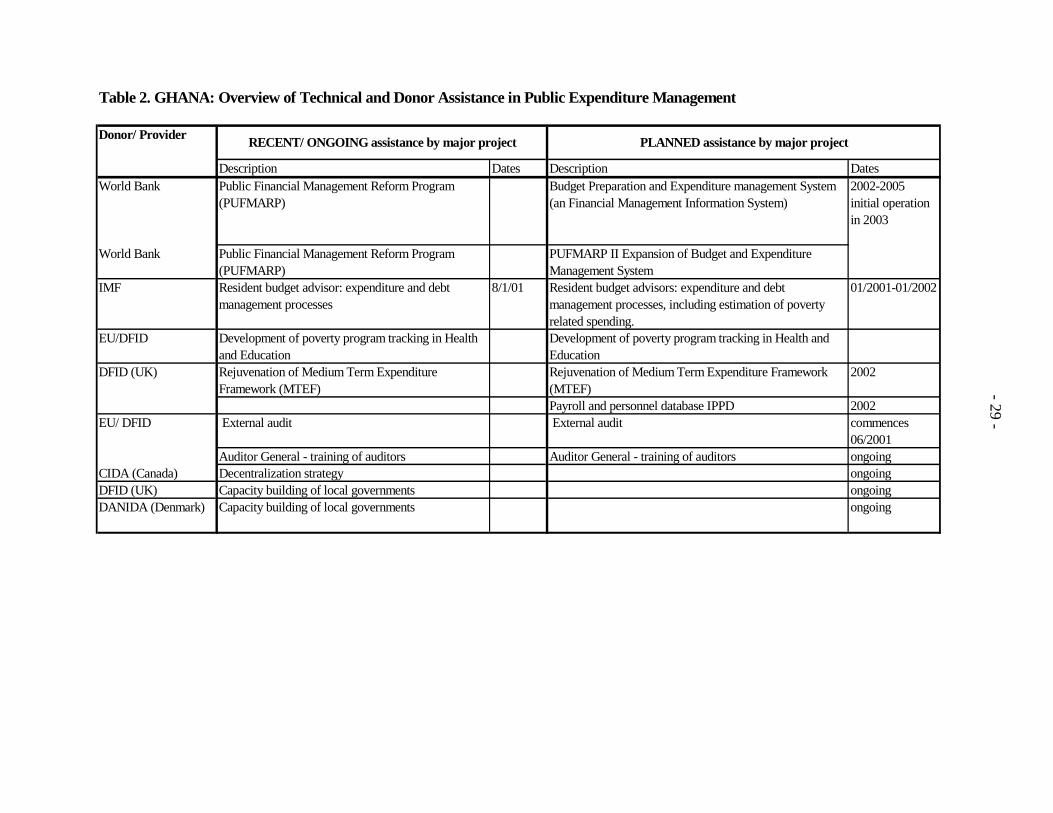

Table 2. GHANA: Overview of Technical and Donor Assistance in Public Expenditure Management

Donor/ Provider

Description Dates Description DatesWorld Bank Public Financial Management Reform Program

(PUFMARP)Budget Preparation and Expenditure management System (an Financial Management Information System)

2002-2005 initial operation in 2003

World Bank Public Financial Management Reform Program (PUFMARP)

PUFMARP II Expansion of Budget and Expenditure Management System

IMF Resident budget advisor: expenditure and debt management processes

8/1/01 Resident budget advisors: expenditure and debt management processes, including estimation of poverty related spending.

01/2001-01/2002

EU/DFID Development of poverty program tracking in Health and Education

Development of poverty program tracking in Health and Education

DFID (UK) Rejuvenation of Medium Term Expenditure Framework (MTEF)

Rejuvenation of Medium Term Expenditure Framework (MTEF)

2002

Payroll and personnel database IPPD 2002EU/ DFID External audit External audit commences

06/2001Auditor General - training of auditors Auditor General - training of auditors ongoing

CIDA (Canada) Decentralization strategy ongoingDFID (UK) Capacity building of local governments ongoingDANIDA (Denmark) Capacity building of local governments ongoing

RECENT/ ONGOING assistance by major project PLANNED assistance by major project

- 30 -

T a b le 3 . G h a n a : A c t io n P la n to U p g ra d e th e P E M C a p a c ity to T ra c k P o v e rty -R e la te d E x p e n d itu re

S H O R T - T E R M M E A S U R E SA c tio n T A p r o v id e r a n d t im in g A c t io n T A p r o v id e r a n d

t im in g

D e v e lo p m e n t o f e s t im a tes o f p o v e r ty b u d g e t G o G (M O F w i th M in o f P la n n in g a n d R eg io n a l D e v e lo p m e n t) a n d IM F /W o r ld B a n k /D F ID

Im p r o v e r e p o r t in g o n d o n o r a c t iv i t ie s

T a g e x p en d i tu r es to b e fin a n c ed fr o m H IP C m o n ie s th r o u g h sp ec ia l ly d ev e lo p ed c o d e a t th e le v e l o f su b h ea d

Im p lem e n ta tio n b y C A G D o f G o G w i th M O F

D e v e lo p a n e w c o m p r e h e n s iv e b u d g e t c la s s i fic a t io n fo r u se w i th H IP C a n d n o n H IP C ex p e n d i tu r e s .

C A G D / IM F /W o r ld B a n k a s p a r t o f P U F M A R P I I

C r ea te s ep a r a te a c co u n t a t B O G fo r H IP C m o n ies T o b e im p le m e n te d b y C A G D o f G o G

P r o je c t io n s

In teg r a t io n o f G P R S p r o g r a m s in a n n u a l b u d g e t G o G (M O F w i th M in o f P la n n in g a n d R eg io n a l D e v e lo p m e n t) a n d IM F /D F ID

M ed iu m T er m E x p e n d itu r e F r a m ew o r k : C o m p o n e n t o f P U F M A R P II

IM F / D F ID /W o r ld B a n k

E n fo r ce co m p l ia n ce w i th r eg u la t io n s o n co m m itm e n ts to co n t r o l b e t te r ex p e n d i tu r e p a th a n d a r r ea r s

G o G B P E M S P U F M A R P I I

S tr e n g th e n in te r n a l a u d i t in c lu d in g r ed i r e c t io n o f r e so u r c es to sys tem a u d i t s , r a n d o m ch e ck ; a n d t r a in in g

P U F M A R P I I S t r e n g th e n in te r n a l a u d it in c lu d in g r e d ir e c tio n o f r e so u r ce s to sys te m a u d i t s , r a n d o m c h e c k ; a n d t r a in in g

P U F M A R P I I

E s ta b l i sh su b a c co u n t (# 4 9 ) o f m a in g o v e r n m e n t a c co u n t in w h ich a l l m o n ie s s a v e d d u e to th e H IP C in i t ia t iv e a r e b e in g c h a n n e le d , a n d m a k e i t o p e r a t io n a l .

U n d e r im p le m e n ta t io n b y G o G

R ev ie w a n d im p r o v e s t r u c tu r e o f g o v er n m e n t b a n k a c co u n ts

Im p r o v e r e p o r t in g o n o w n r eso u r ce s o f d e p a r tm e n ts a n d a p p r o p r ia t io n s in a id