Embed Size (px)

Citation preview

Transfer Pricing

Enrique Rayon, Ph.D.

McGladrey LLP

Outline

• What is Transfer Pricing?

• Transfer Pricing Methods

• Documentation

• Project Phases

• Applicability Review of TP Methods

• Selected Benefits from performing a TP Study

What is Transfer Pricing?

• Transfer pricing, the determination of prices charged

by one affiliated company to another in intercompany

transactions, is increasingly becoming a focus of

international tax inspectors around the world.

• Tax authorities around the world are increasing

cross-border dialogues and transfer pricing

enforcement abilities and have shifted their focus

from large taxpayers to small and midsize taxpayers.

What is Transfer Pricing?

• Authorities are not limiting their focus to transfer of

tangible goods.

• Transfers of intangible assets, services and funding

are also increasingly being closely scrutinized.

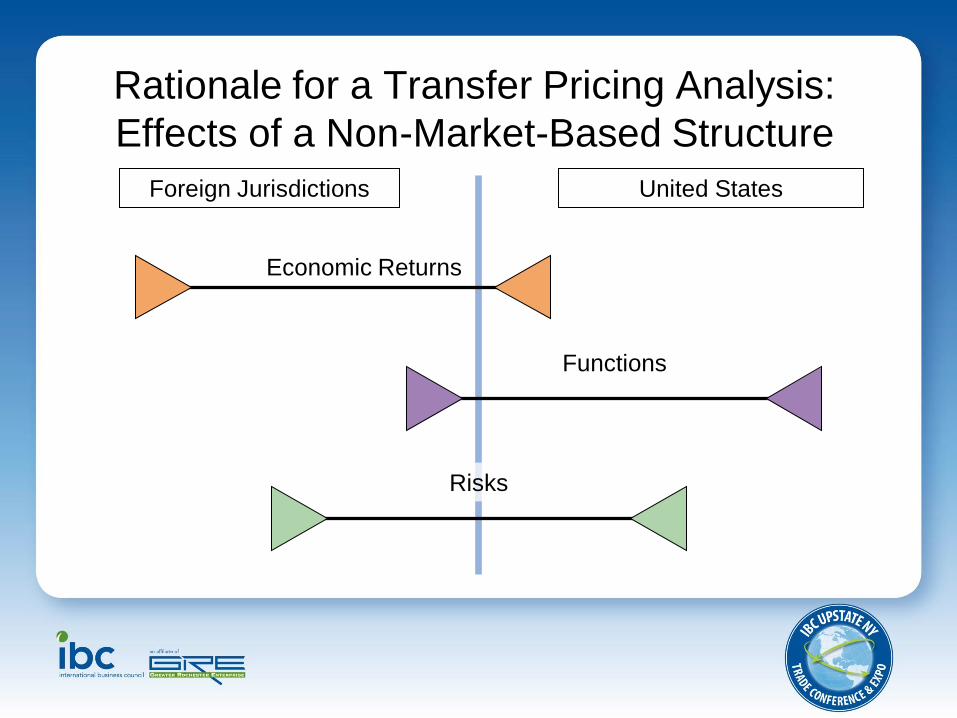

Rationale for a Transfer Pricing Analysis:

Effects of a Non-Market-Based Structure

Foreign Jurisdictions United States

Economic Returns

Functions

Risks

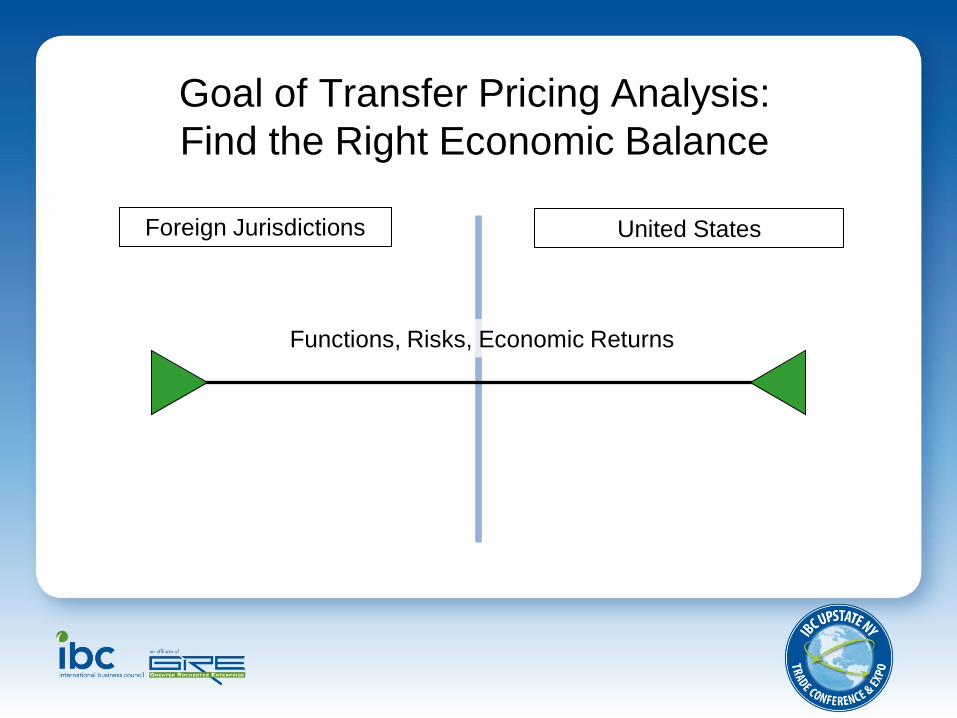

Goal of Transfer Pricing Analysis:

Find the Right Economic Balance

Foreign Jurisdictions United States

Functions, Risks, Economic Returns

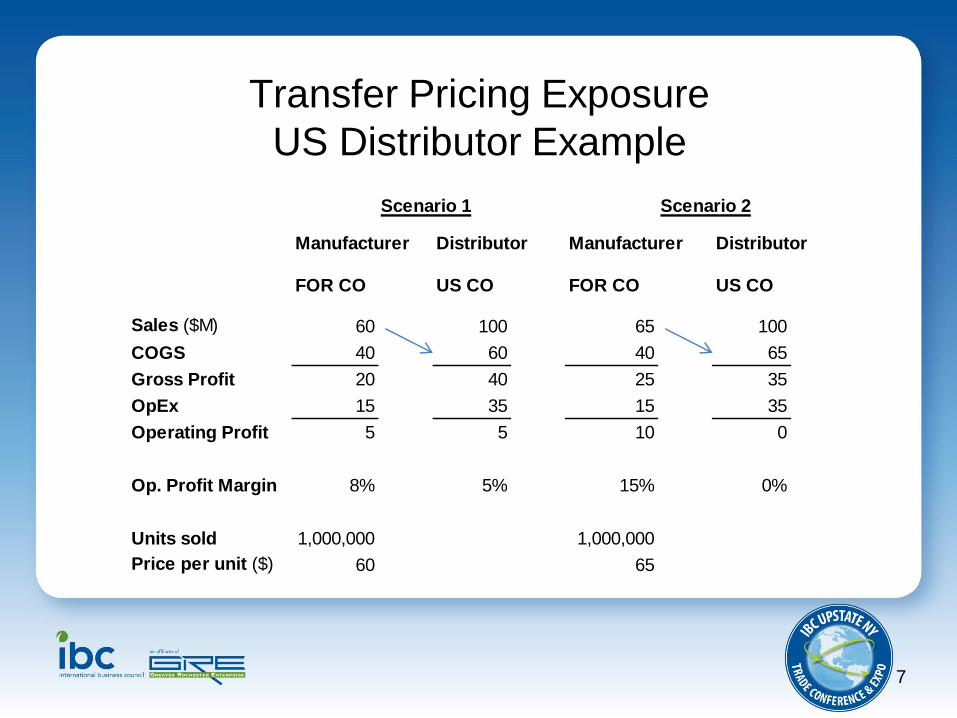

Transfer Pricing Exposure

US Distributor Example

7

Scenario 1 Scenario 2

Manufacturer Distributor Manufacturer Distributor

FOR CO US CO FOR CO US CO

Sales ($M) 60 100 65 100

COGS 40 60 40 65

Gross Profit 20 40 25 35

OpEx 15 35 15 35

Operating Profit 5 5 10 0

Op. Profit Margin 8% 5% 15% 0%

Units sold 1,000,000 1,000,000

Price per unit ($) 60 65

What is Transfer Pricing?

• Tax Risk

– Potential double taxation of intercompany income.

– Transfer pricing legislation almost always includes

a provision for the imposition of significant

penalties when adjustments are made to taxable

profits following an audit.

What is Transfer Pricing?

• Penalties – Substantial valuation misstatement, 20%

– Gross valuation misstatement, 40%

– Reporting penalties

• Failure to file Form 5471/5472

• $10,000 per occurrence

What is Transfer Pricing?

• Opportunity

– Effective transfer pricing can help minimize global

taxation.

– Adequate contemporaneous documentation of

transfer pricing strategy and implementation can

usually safeguard against the imposition of

penalties.

What is Transfer Pricing?

• Legislation

– Many countries follow the Organisation for

Economic Co-operation and Development’s

(“OECD”) guidelines.

– OECD and US legislation is based on the arm’s

length principle – related parties should conduct

business on arm’s length terms.*

* Arms’ length terms: terms that would result from the transfer of the same

property or services between two unrelated entities in similar circumstances.

Transfer Pricing Methods

• Two Approaches:

– Transactional analysis

– Profit based analysis

Transfer Pricing Methods

• Transactional Analysis

– Arm’s length prices are determined by comparison

with comparable uncontrolled prices – similar

transactions between unrelated parties.

Transfer Pricing Methods

• Profit Based Analysis

– Arm’s length prices are justified by comparison of

the enterprises profitability with that of comparable

uncontrolled legal entities.

Transfer Pricing Methods – US

• Relevant Methods (Best Method)

– Comparable Uncontrolled Price (CUP)

– Resale Price Method

– Cost Plus Method

– Profit Split

– Comparable Profits Method (CPM)

16

Transfer Pricing – Service Regulations

• (New) US regulations introduced the “services cost method” (SCM)

– Specified covered services

– Low margin covered services

• Rev. Proc. 2007-13 provides “evolving” list

17

Transfer Pricing - Service Regulations

• Services eligible for SCM (Rev. Proc. 2007-13) – Accounting and audit

– Tax

– Health, safety, environmental and regulatory

– Treasury

– Purchasing

– Information and technology

• Includes flexible, other “similar” activities category for each activity.

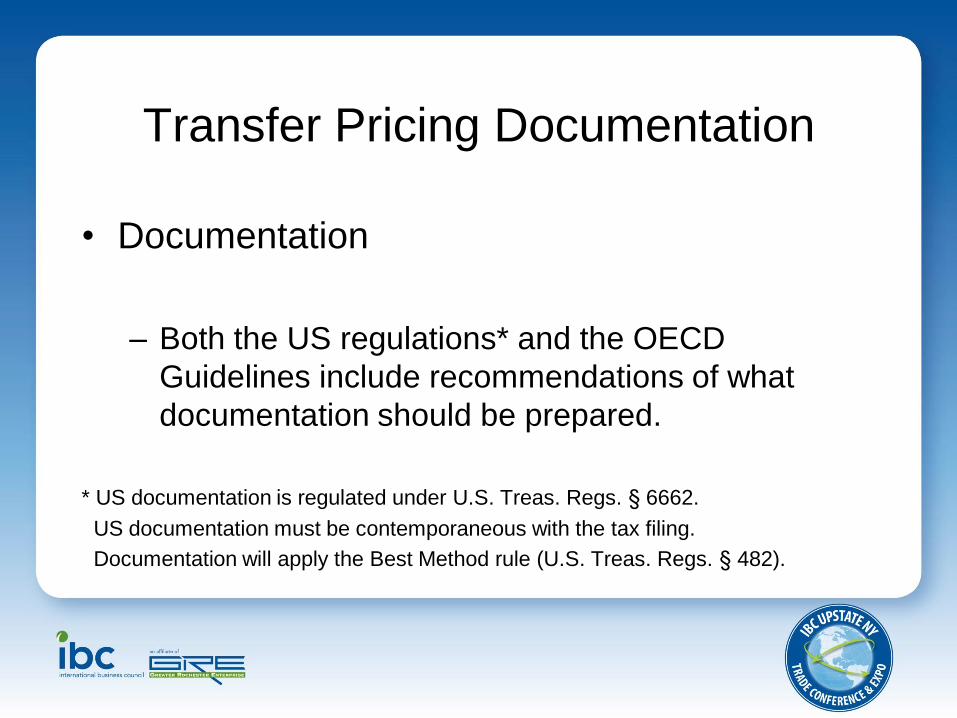

Transfer Pricing Documentation

• Documentation

– A key element of a transfer pricing strategy,

whether it is transaction or profit based, is it’s

documentation.

– The availability of contemporaneous transfer

pricing documentation is a fundamental

requirement of all transfer pricing legislation.

19

Global TP Documentation Challenges

Example

Transfer Pricing Documentation

• Documentation

– Both the US regulations* and the OECD

Guidelines include recommendations of what

documentation should be prepared.

* US documentation is regulated under U.S. Treas. Regs. § 6662.

US documentation must be contemporaneous with the tax filing.

Documentation will apply the Best Method rule (U.S. Treas. Regs. § 482).

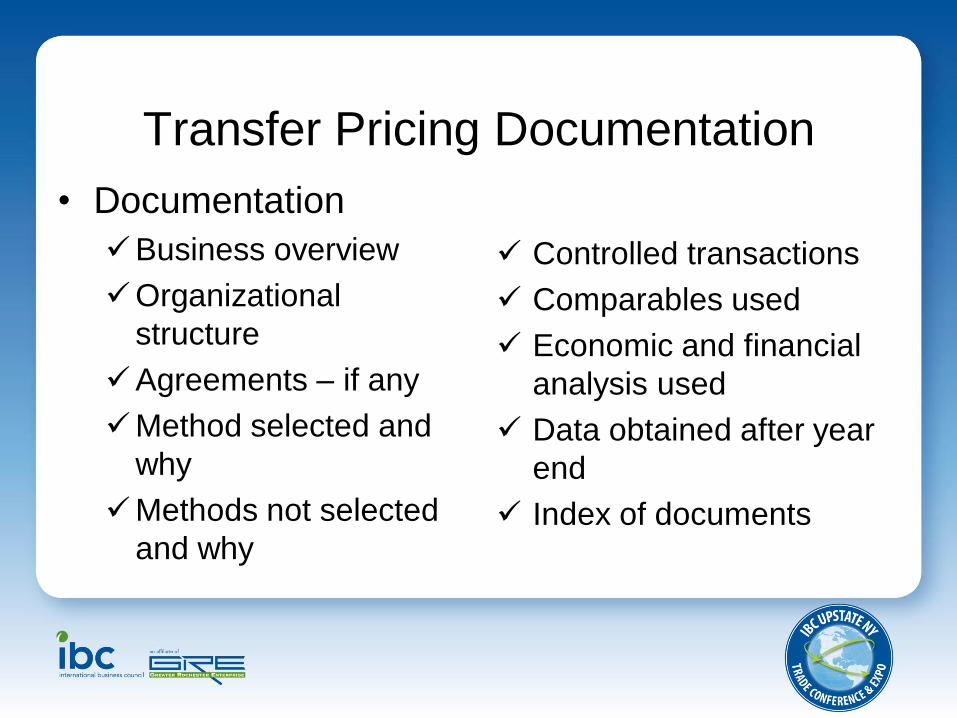

• Documentation

Business overview

Organizational

structure

Agreements – if any

Method selected and

why

Methods not selected

and why

Controlled transactions

Comparables used

Economic and financial

analysis used

Data obtained after year

end

Index of documents

Transfer Pricing Documentation

22

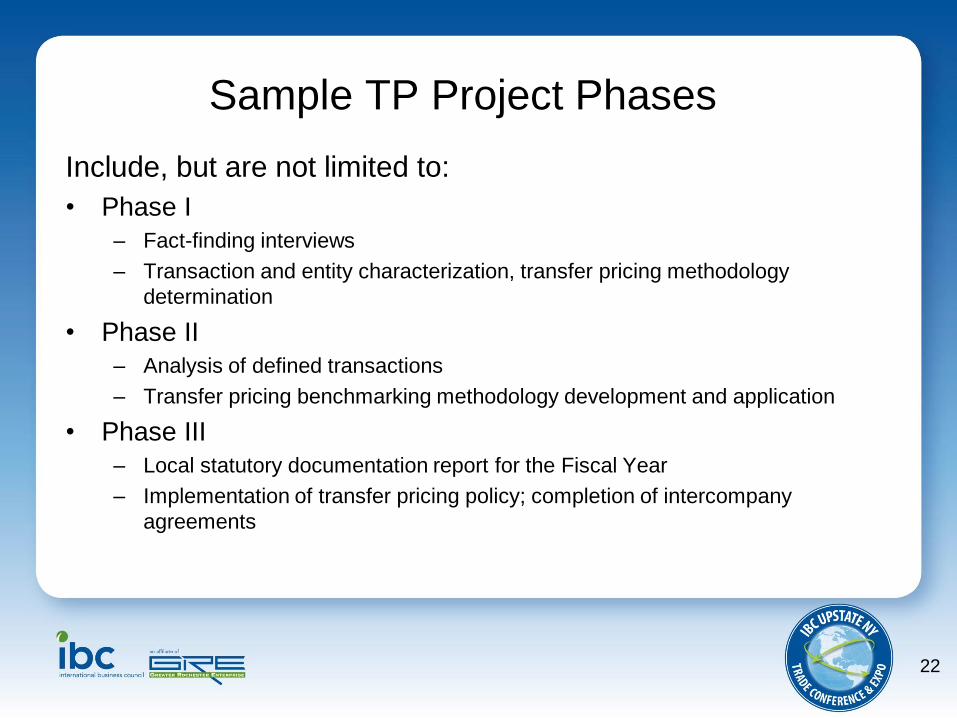

Sample TP Project Phases

Include, but are not limited to:

• Phase I

– Fact-finding interviews

– Transaction and entity characterization, transfer pricing methodology

determination

• Phase II

– Analysis of defined transactions

– Transfer pricing benchmarking methodology development and application

• Phase III

– Local statutory documentation report for the Fiscal Year

– Implementation of transfer pricing policy; completion of intercompany

agreements

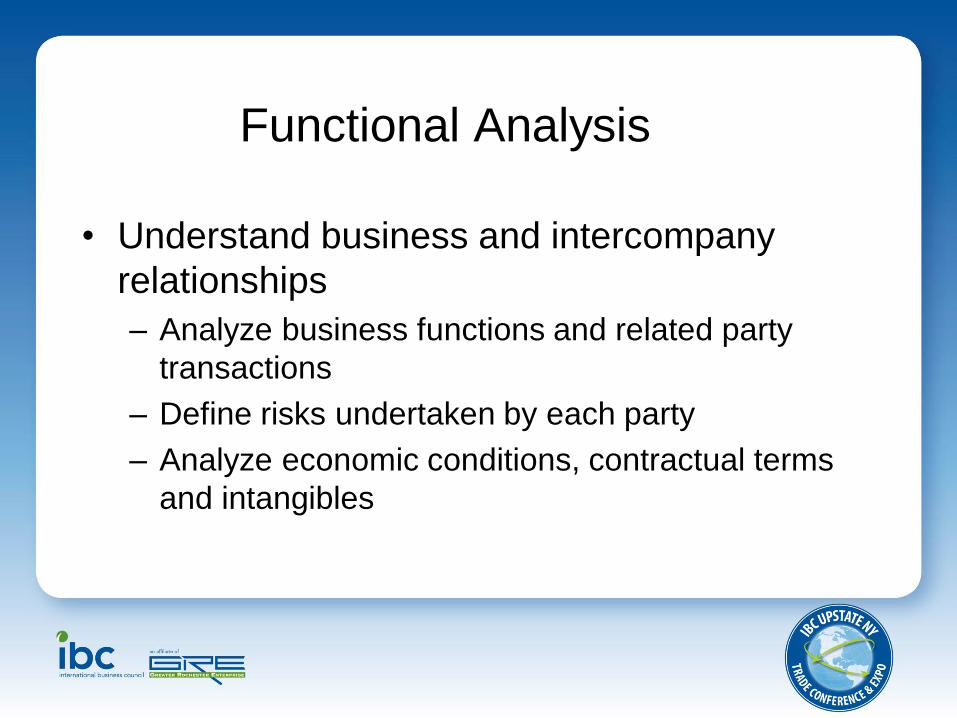

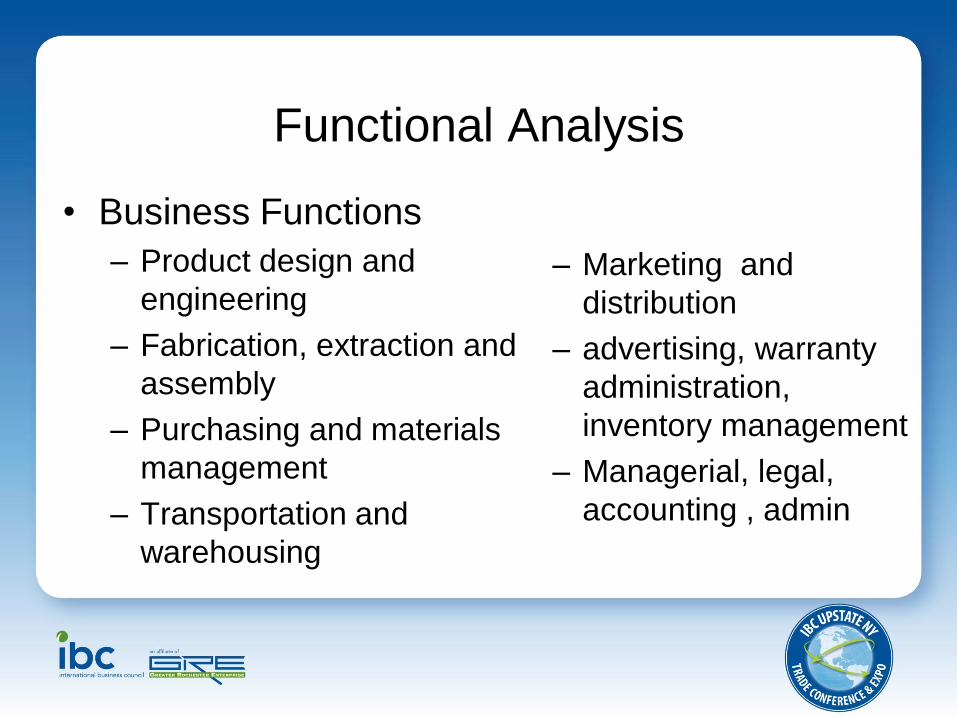

Functional Analysis

• Understand business and intercompany

relationships

– Analyze business functions and related party

transactions

– Define risks undertaken by each party

– Analyze economic conditions, contractual terms

and intangibles

• Business Functions

– Product design and

engineering

– Fabrication, extraction and

assembly

– Purchasing and materials

management

– Transportation and

warehousing

– Marketing and

distribution

– advertising, warranty

administration,

inventory management

– Managerial, legal,

accounting , admin

Functional Analysis

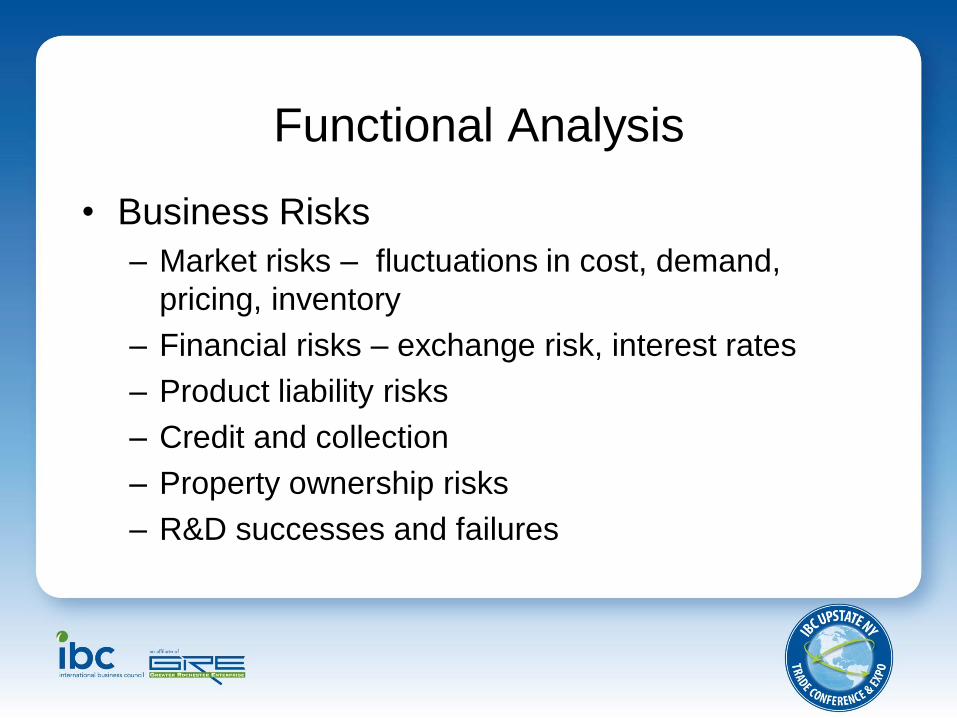

Functional Analysis

• Business Risks

– Market risks – fluctuations in cost, demand,

pricing, inventory

– Financial risks – exchange risk, interest rates

– Product liability risks

– Credit and collection

– Property ownership risks

– R&D successes and failures

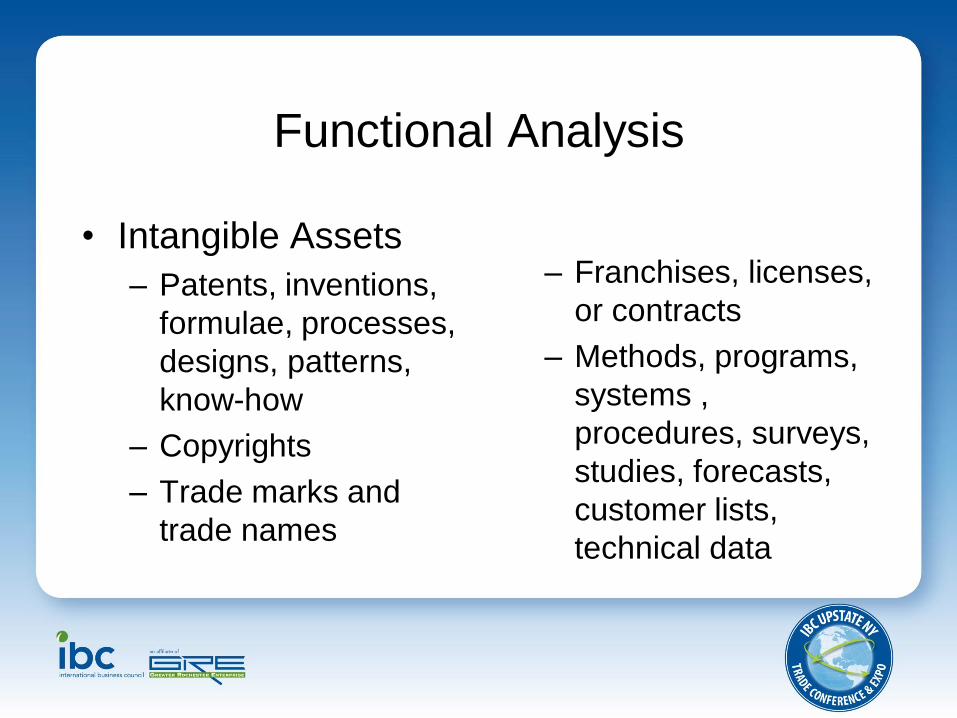

• Intangible Assets

– Patents, inventions,

formulae, processes,

designs, patterns,

know-how

– Copyrights

– Trade marks and

trade names

– Franchises, licenses,

or contracts

– Methods, programs,

systems ,

procedures, surveys,

studies, forecasts,

customer lists,

technical data

Functional Analysis

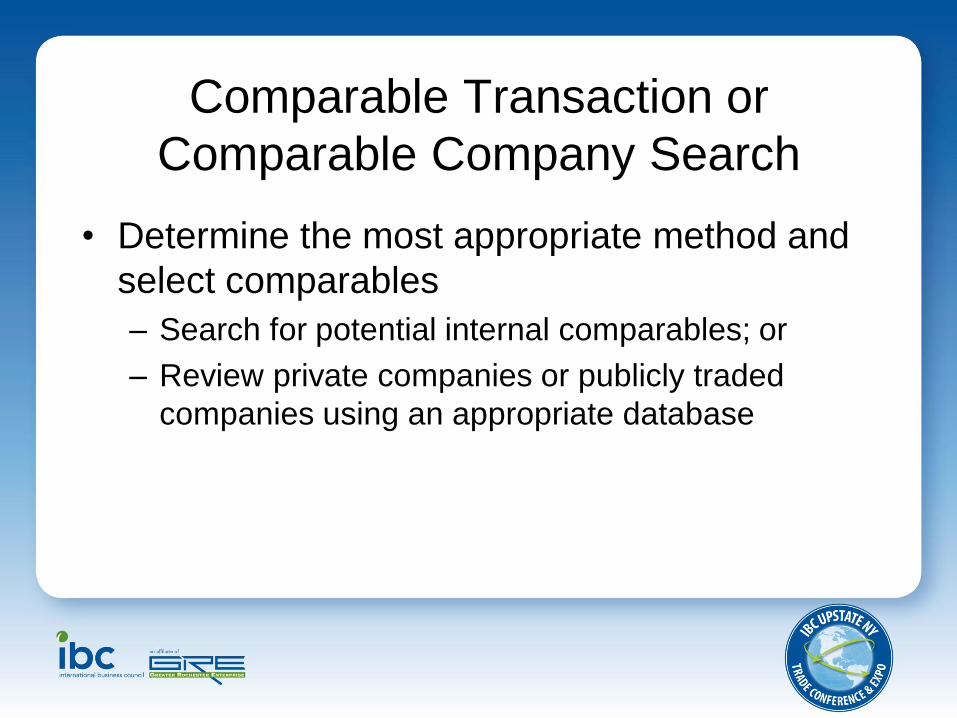

Comparable Transaction or

Comparable Company Search

• Determine the most appropriate method and

select comparables

– Search for potential internal comparables; or

– Review private companies or publicly traded

companies using an appropriate database

Final Steps

• Perform economic and financial analysis.

• Prepare the contemporaneous

documentation report.

29

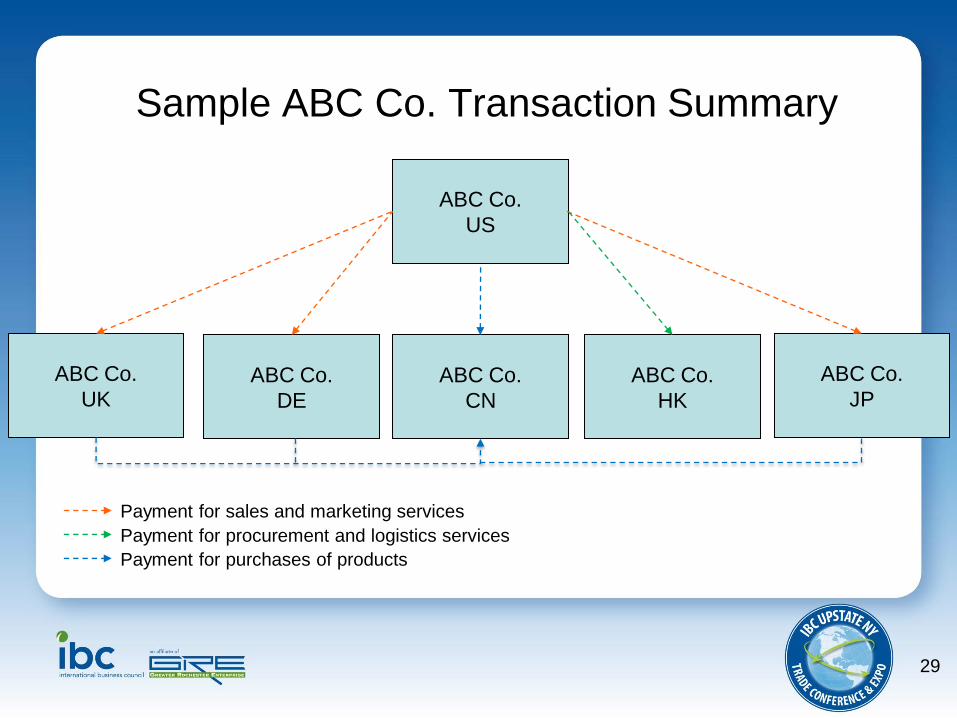

Sample ABC Co. Transaction Summary

ABC Co.

HK

ABC Co.

US

Payment for sales and marketing services

ABC Co.

DE

ABC Co.

CN

Payment for procurement and logistics services

Payment for purchases of products

ABC Co.

UK

ABC Co.

JP

30

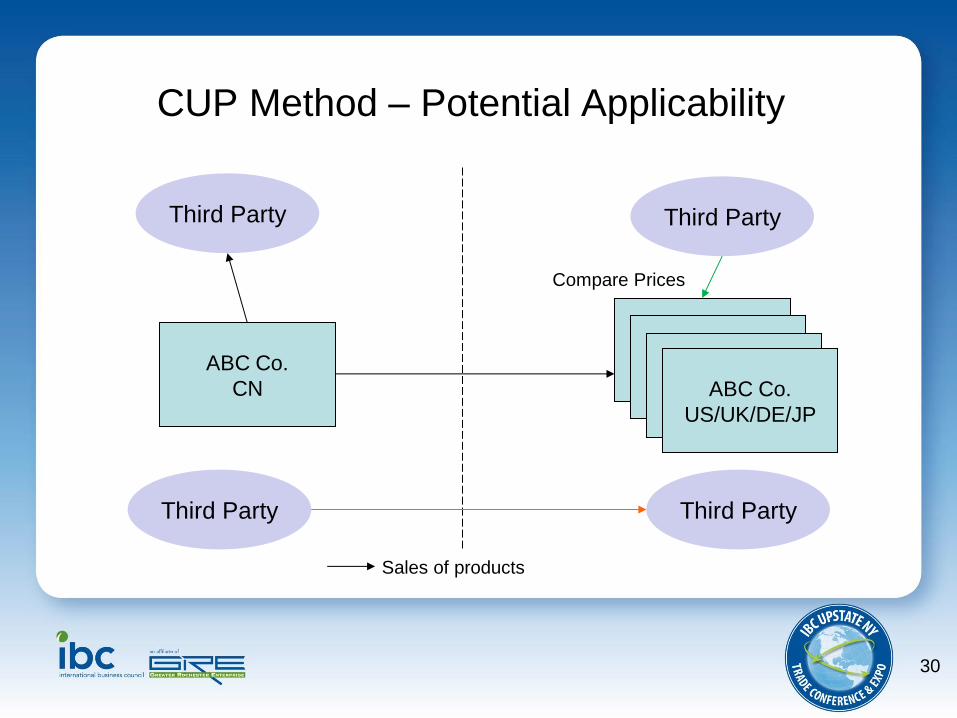

CUP Method – Potential Applicability

ABC Co.

CN

ABC Co.

US/UK/DE/JP

Sales of products

Third Party Third Party

Third Party Third Party

Compare Prices

ABC Co.

US/UK/DE/JP ABC Co.

US/UK/DE/JP ABC Co.

US/UK/DE/JP

31

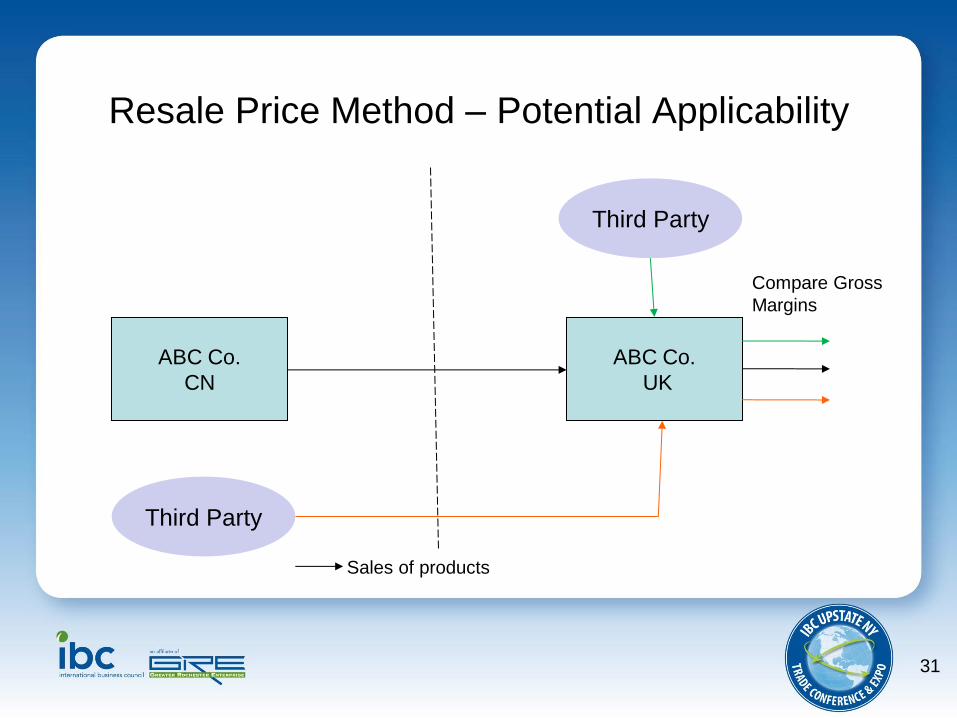

Resale Price Method – Potential Applicability

ABC Co.

CN

ABC Co.

UK

Sales of products

Third Party

Third Party

Compare Gross

Margins

32

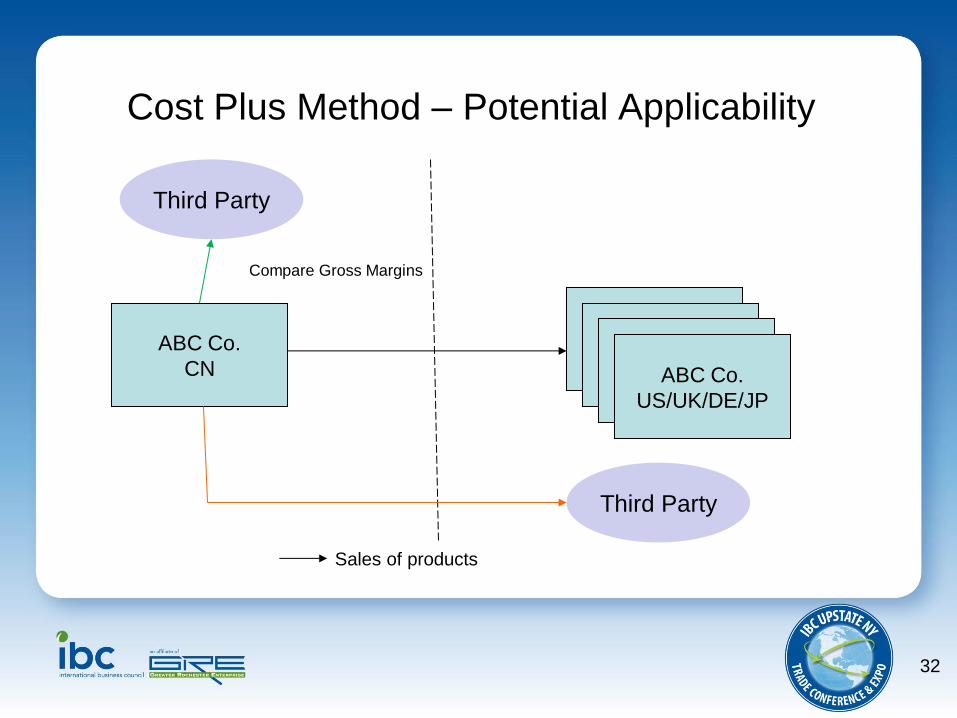

Cost Plus Method – Potential Applicability

ABC Co.

CN

ABC Co.

US/UK/DE/JP

Sales of products

Third Party

Third Party

Compare Gross Margins

ABC Co.

US/UK/DE/JP ABC CO.

UK/UK/DE/JP ABC Co.

US/UK/DE/JP

33

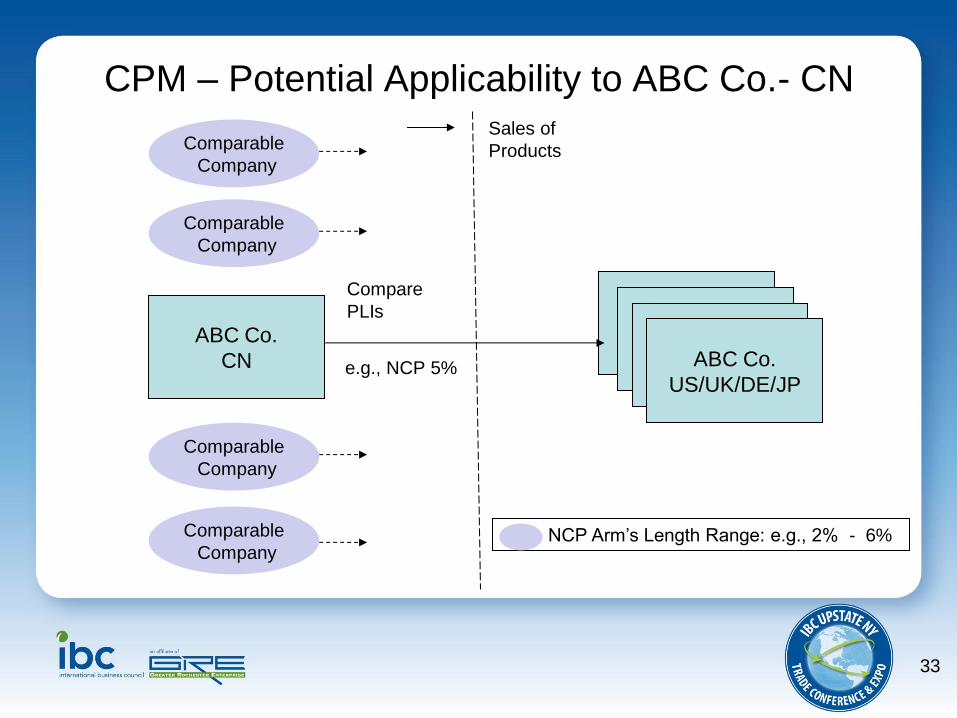

CPM – Potential Applicability to ABC Co.- CN

ABC Co.

CN

ABC Co.

US/UK/DE/JP

Sales of

Products Comparable

Company

Compare

PLIs ABC Co.

US/UK/DE/JP ABC Co.

US/UK/DE/JP ABC Co.

US/UK/DE/JP e.g., NCP 5%

NCP Arm’s Length Range: e.g., 2% - 6%

Comparable

Company

Comparable

Company

Comparable

Company

34

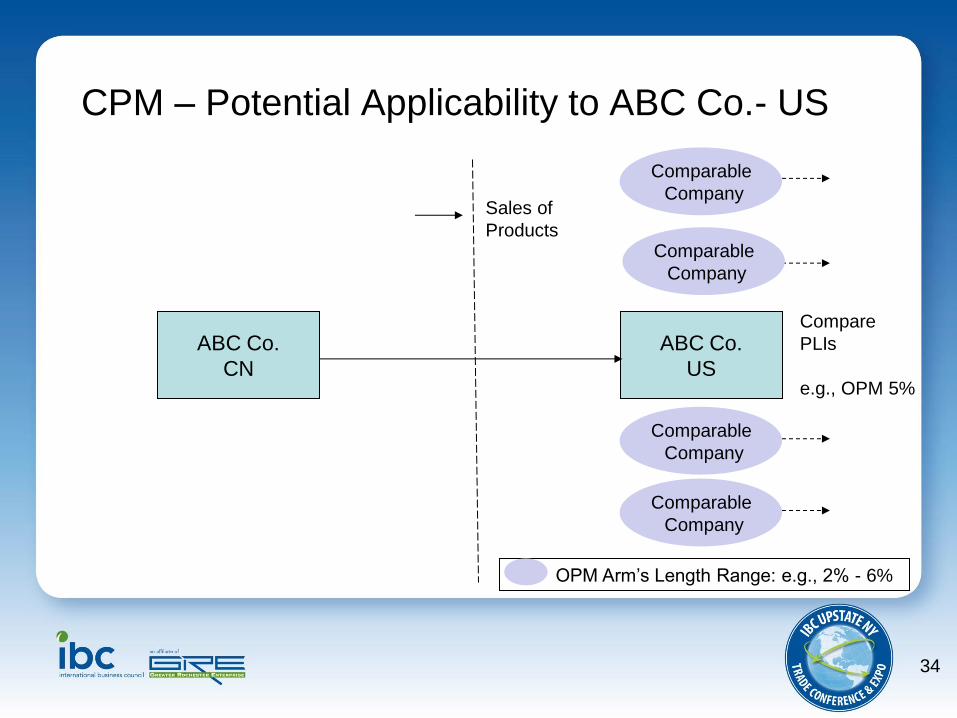

CPM – Potential Applicability to ABC Co.- US

ABC Co.

US

Sales of

Products

Comparable

Company

Compare

PLIs

e.g., OPM 5%

OPM Arm’s Length Range: e.g., 2% - 6%

Comparable

Company

Comparable

Company

Comparable

Company

ABC Co.

CN

35

Selected Benefits to a Company from

performing a Transfer Pricing Study

• Impact on the bottom line through:

– Tax risk management

• Stricter enforcement of Transfer Pricing rules, greater penalty

risks

• FIN 48 / ASC 740

– Financial risk management (e.g., notes to the audited

financial statements)

• Better information flow / audit trail, improved internal

controls / tying of various systems and accounts

36

Other Potential Benefits to the Company

from the Studies

• Prospective analysis to set pricing

• Analysis to understand existing pricing strategy

• Optimize global effective tax rate

• Review existing pricing strategy and supply chain review

• Resolve global management issues

• Compliance with foreign documentation requirements

• Penalty protection

• Audit defense

• Basis for APA preparation

Get your Upstate NY Trade Conference passport signed by at least 10 exhibitors for a chance to win the

following prizes, which will be raffled off and announced after the closing keynote

Exhibitors: 1 GRE/IBC/NYSERDA

2 Time Warner Cable Business Class

3 Advanced Language Translation

4 Freed Maxick CPAs, P.C.

5 Wells Fargo Bank, N.A.

6 KCI Engineering of New York, PC

7 JR Language Translation Services Inc.

8 RIT Saunders College of Business

9 Speed Global Services

10 RBS Citizens

11 FBI

12 US Small Business Administration

13 Mohawk Global Logistics

14 School of Business Administration and Economics,

The College at Brockport

15 Gallagher Benefit Services

16 U.S. Department of Commerce

17 U.S. Customs and Border Patrol

18 County of Monroe Industrial Development Agency (COMIDA)

Procurement Technical Assistance Center (PTAC)

19 Employer Support of the National Guard & Reserves (ESGR)

Exhibitor Passport Prizes:

• Advanced Language Translation, Inc.

$500 Gift Certificate towards translation services

• Hong Wah Restaurant – $10 Gift Certificate

• Mario's Via Abruzzi Restaurant – (2)

$50 Gift Certificates

• Mohawk Global Logistics

$100 Gift Card to Black & Blue Restaurant

• Richardson’s Canal House Restaurant – (2)

$25 Gift Certificates

• Speed Global Services

Dictionary of International Trade

& 50% off 2nd international shipment

• The Cheesecake Factory – $25 Gift Certificate

• The Spa at the Del Monte

50 minute Massage

• Wegmans – $100 Gift Card

• Wilmorite Inc. – $50 Mall Gift Card