Embed Size (px)

Citation preview

TRAVIS CENTRAL APPRAISAL DISTRICT

BOARD OFFICERS RICHARD LAVINE

CHAIRPERSON

KRISTOFFER S. LANDS

VICE CHAIRPERSON

ED KELLER

SECRETARY/TREASURER

MARYA CRIGLER

CHIEF APPRAISER

BOARD MEMBERS TOM BUCKLE

JAMES VALDEZ

BRUCE GRUBE

BRUCE ELFANT

ELEANOR POWELL

RICO REYES

BLANCA ZAMORA-GARCIA

July 28, 2017

NOTICE

Travis Central Appraisal District is accepting proposals from companies to provide printing and mailing services. The term of this contract is for the period beginning January 1, 2018 and ending December 31, 2018, plus the option to renew for two(2) additional 12-month periods . Each vendor must furnish all information required by the proposal and must propose a specific price for all requested years. Bids should conform to the specifications established by the District. A copy of the specifications is included in this packet. The proposal shall be delivered in a sealed envelope marked on the outside “2017-5: PRINTING AND MAILING SERVICES PROPOSAL- DO NOT OPEN” prior to 2:00 p.m. on Monday, August 28, 2017, to Mrs. Leana H. Mann, Finance & Facilities Director, Travis Central Appraisal District, 8314 Cross Park Drive, Austin, Texas 78754. The Board of Directors will consider all proposals at their regularly scheduled meeting on Tuesday, September 5, 2017. TCAD reserves the right to reject any or all proposals, to waive technicalities or formalities, and to accept the proposal deemed to be the best value for the TCAD. _______________________________ Leana H. Mann, C.G.F.O. Finance & Facilities Director Travis Central Appraisal District

REQUEST FOR PROPOSAL

TO PROVIDE PRINTING AND MAILING SERVICES

TRAVIS CENTRAL APPRAISAL DISTRICT

SECTION I:

General Provisions

1.0 Travis Central Appraisal District (TCAD) is a government agency, duly organized and existing

under the Constitution and Laws of the State of Texas as set forth in the Texas Property Tax Code and is a political subdivision of the State of Texas.

2.0 The principal governmental function and purpose of TCAD is to appraise property in Travis County for ad valorem tax purposes for each taxing units within Travis County. TCAD operates on a calendar year budget cycle.

3.0 TCAD is governed by a ten member Board of Directors, appointed by the taxing jurisdictions for which TCAD appraises property. TCAD has obtained such approvals and consents as are necessary (if applicable) to complete this RFP.

4.0 In accomplishing its public purposes, TCAD has the power and is subject to the limitations set forth in the Texas Property Tax Code and in other applicable laws and the Constitution of the State of Texas.

5.0 The chief administrative officer for TCAD is the Chief Appraiser. Day-to-day supervision of all consultants to TCAD will be performed by the Chief Appraiser.

6.0 The Texas State Legislature has enacted into law in previous years substantial and significant

changes concerning requirements for various notifications to the taxpayers. These changes for Appraisal Districts can be a significant change to notice form design which might require programming costs. As part of the proposal, the District requests that all proposers state a summary of previous Appraisal District experience and their ability to timely perform concerning the changes needed to comply with legislative mandates, quality laser printing, and subsequent mailing of appraisal notices. Proposer’s stated history of prior successful experience with notice printing, sorting and mailing, and all other aspects of this quote, will be an important factor in the District’s staff recommendations to the Board of Directors for awarding a contract to the proposer who provides the “best value”.

Please keep in mind changes are pursuant to the

Texas State Legislature and are REQUIRED. Failure to implement Legislatively mandated changes are grounds for

immediate termination of the contract as well as the ability for TCAD to recover any cost associated

with finding a new vendor.

7.0 Services and equipment will be used for governmental purposes and will be exempt from all

taxes presently assessed and levied.

8.0 All quotes must include a statement that they are valid for a minimum period of ninety (90)

days after closing date of the RFP.

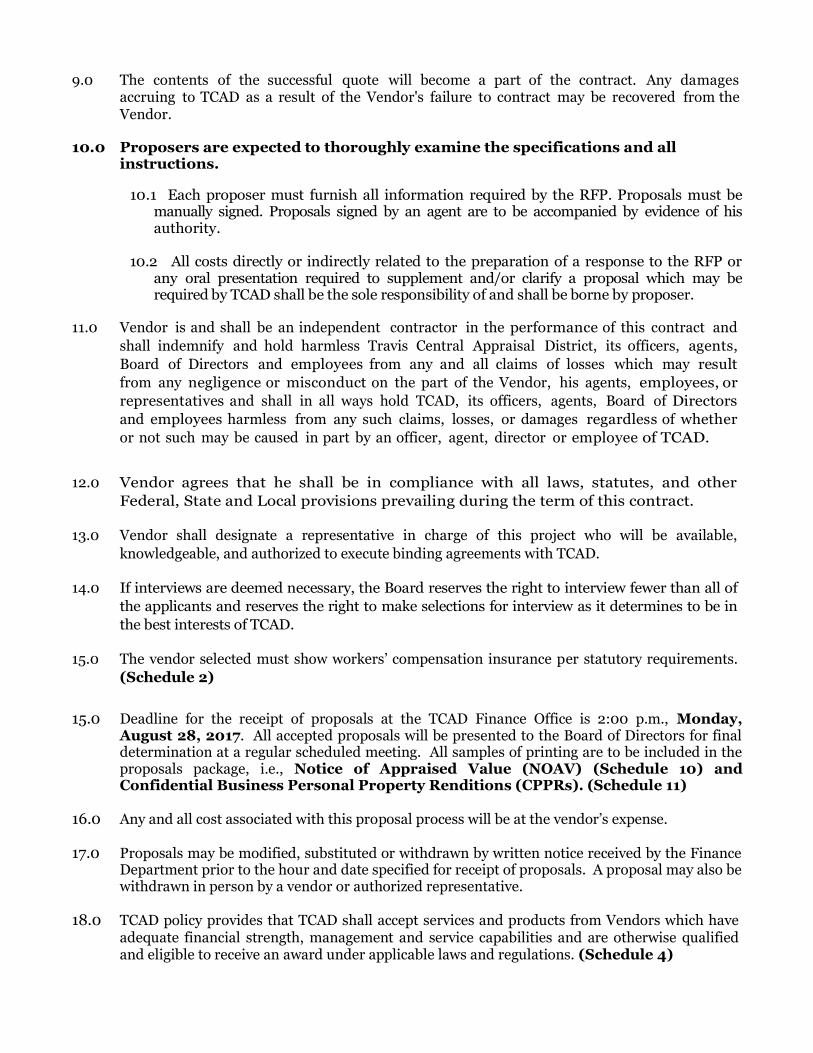

9.0 The contents of the successful quote will become a part of the contract. Any damages accruing to TCAD as a result of the Vendor's failure to contract may be recovered from the Vendor.

10.0 Proposers are expected to thoroughly examine the specifications and all instructions.

10.1 Each proposer must furnish all information required by the RFP. Proposals must be manually signed. Proposals signed by an agent are to be accompanied by evidence of his authority.

10.2 All costs directly or indirectly related to the preparation of a response to the RFP or any oral presentation required to supplement and/or clarify a proposal which may be required by TCAD shall be the sole responsibility of and shall be borne by proposer.

11.0 Vendor is and shall be an independent contractor in the performance of this contract and

shall indemnify and hold harmless Travis Central Appraisal District, its officers, agents,

Board of Directors and employees from any and all claims of losses which may result

from any negligence or misconduct on the part of the Vendor, his agents, employees, or

representatives and shall in all ways hold TCAD, its officers, agents, Board of Directors

and employees harmless from any such claims, losses, or damages regardless of whether

or not such may be caused in part by an officer, agent, director or employee of TCAD.

12.0 Vendor agrees that he shall be in compliance with all laws, statutes, and other

Federal, State and Local provisions prevailing during the term of this contract.

13.0 Vendor shall designate a representative in charge of this project who will be available,

knowledgeable, and authorized to execute binding agreements with TCAD.

14.0 If interviews are deemed necessary, the Board reserves the right to interview fewer than all of

the applicants and reserves the right to make selections for interview as it determines to be in

the best interests of TCAD.

15.0 The vendor selected must show workers’ compensation insurance per statutory requirements.

(Schedule 2)

15.0 Deadline for the receipt of proposals at the TCAD Finance Office is 2:00 p.m., Monday, August 28, 2017. All accepted proposals will be presented to the Board of Directors for final determination at a regular scheduled meeting. All samples of printing are to be included in the proposals package, i.e., Notice of Appraised Value (NOAV) (Schedule 10) and Confidential Business Personal Property Renditions (CPPRs). (Schedule 11)

16.0 Any and all cost associated with this proposal process will be at the vendor’s expense. 17.0 Proposals may be modified, substituted or withdrawn by written notice received by the Finance

Department prior to the hour and date specified for receipt of proposals. A proposal may also be withdrawn in person by a vendor or authorized representative.

18.0 TCAD policy provides that TCAD shall accept services and products from Vendors which have

adequate financial strength, management and service capabilities and are otherwise qualified and eligible to receive an award under applicable laws and regulations. (Schedule 4)

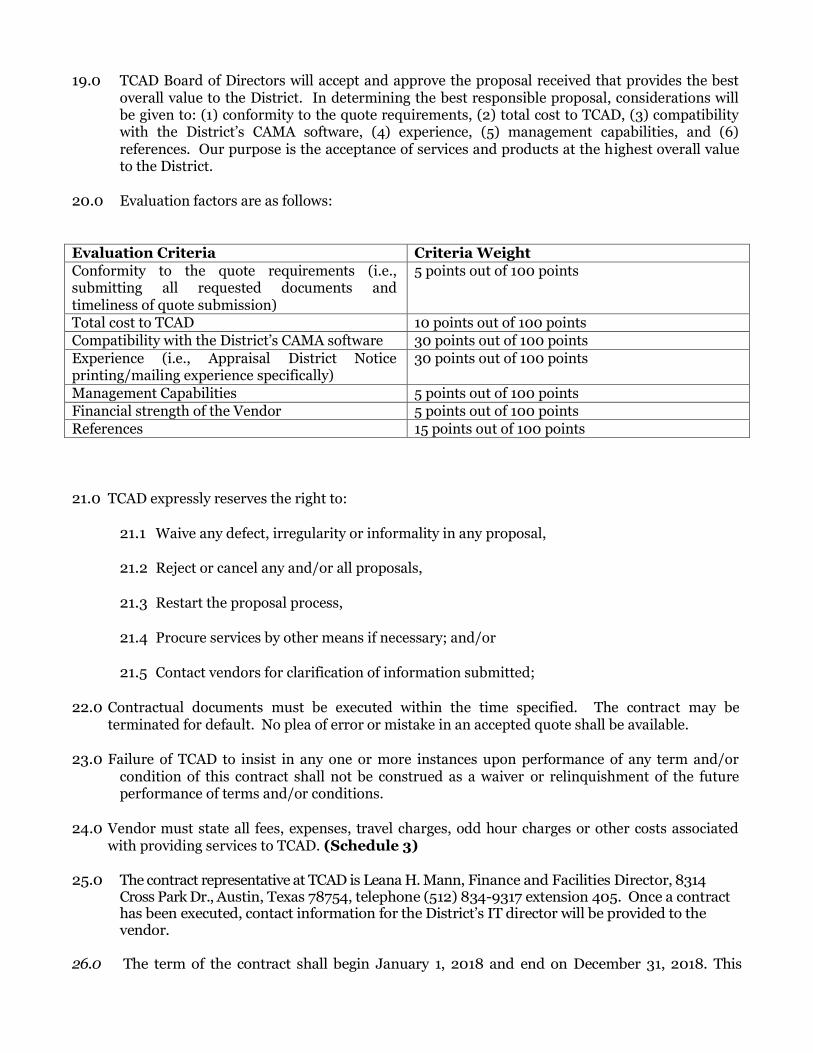

19.0 TCAD Board of Directors will accept and approve the proposal received that provides the best overall value to the District. In determining the best responsible proposal, considerations will be given to: (1) conformity to the quote requirements, (2) total cost to TCAD, (3) compatibility with the District’s CAMA software, (4) experience, (5) management capabilities, and (6) references. Our purpose is the acceptance of services and products at the highest overall value to the District.

20.0 Evaluation factors are as follows:

Evaluation Criteria Criteria Weight

Conformity to the quote requirements (i.e., submitting all requested documents and timeliness of quote submission)

5 points out of 100 points

Total cost to TCAD 10 points out of 100 points

Compatibility with the District’s CAMA software 30 points out of 100 points

Experience (i.e., Appraisal District Notice printing/mailing experience specifically)

30 points out of 100 points

Management Capabilities 5 points out of 100 points

Financial strength of the Vendor 5 points out of 100 points

References 15 points out of 100 points

21.0 TCAD expressly reserves the right to:

21.1 Waive any defect, irregularity or informality in any proposal, 21.2 Reject or cancel any and/or all proposals, 21.3 Restart the proposal process, 21.4 Procure services by other means if necessary; and/or

21.5 Contact vendors for clarification of information submitted;

22.0 Contractual documents must be executed within the time specified. The contract may be

terminated for default. No plea of error or mistake in an accepted quote shall be available. 23.0 Failure of TCAD to insist in any one or more instances upon performance of any term and/or

condition of this contract shall not be construed as a waiver or relinquishment of the future performance of terms and/or conditions.

24.0 Vendor must state all fees, expenses, travel charges, odd hour charges or other costs associated

with providing services to TCAD. (Schedule 3)

25.0 The contract representative at TCAD is Leana H. Mann, Finance and Facilities Director, 8314 Cross Park Dr., Austin, Texas 78754, telephone (512) 834-9317 extension 405. Once a contract has been executed, contact information for the District’s IT director will be provided to the vendor.

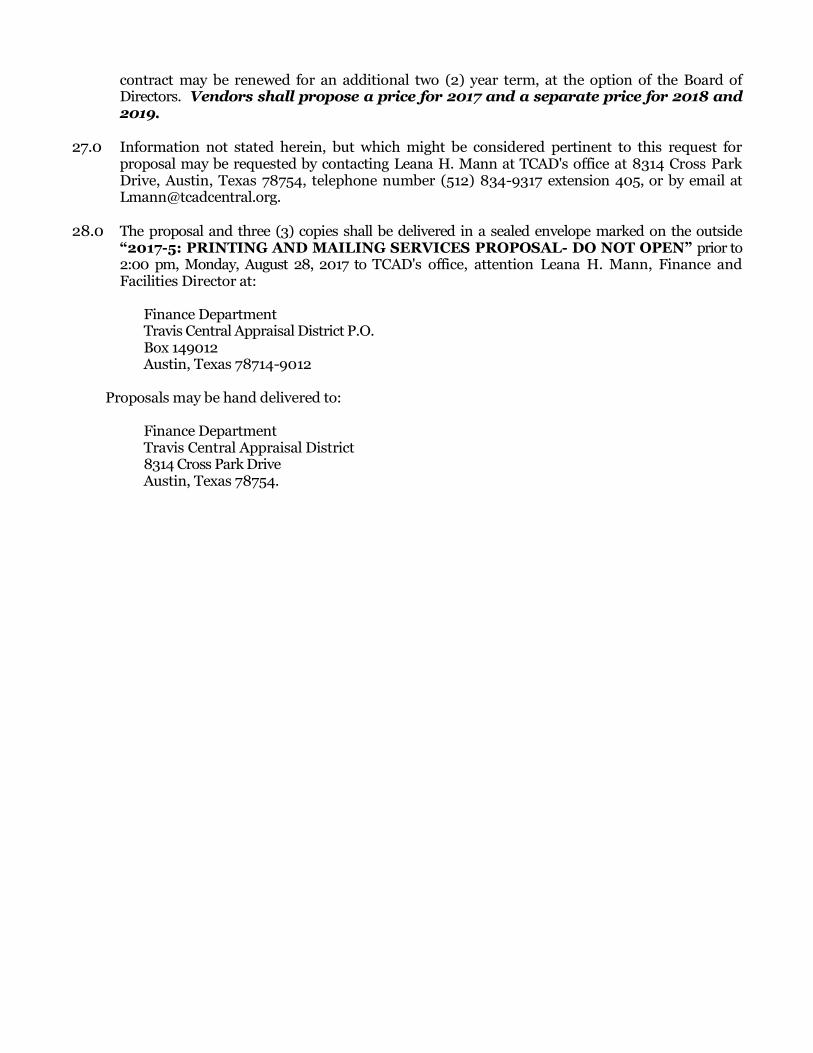

26.0 The term of the contract shall begin January 1, 2018 and end on December 31, 2018. This

contract may be renewed for an additional two (2) year term, at the option of the Board of Directors. Vendors shall propose a price for 2017 and a separate price for 2018 and 2019.

27.0 Information not stated herein, but which might be considered pertinent to this request for proposal may be requested by contacting Leana H. Mann at TCAD's office at 8314 Cross Park Drive, Austin, Texas 78754, telephone number (512) 834-9317 extension 405, or by email at [email protected].

28.0 The proposal and three (3) copies shall be delivered in a sealed envelope marked on the outside “2017-5: PRINTING AND MAILING SERVICES PROPOSAL- DO NOT OPEN” prior to 2:00 pm, Monday, August 28, 2017 to TCAD's office, attention Leana H. Mann, Finance and Facilities Director at:

Finance Department Travis Central Appraisal District P.O. Box 149012 Austin, Texas 78714-9012

Proposals may be hand delivered to:

Finance Department Travis Central Appraisal District 8314 Cross Park Drive Austin, Texas 78754.

REQUEST FOR PROPOSAL

TO PROVIDE PRINTING AND MAILING SERVICES

TRAVIS CENTRAL APPRAISAL DISTRICT

SECTION II:

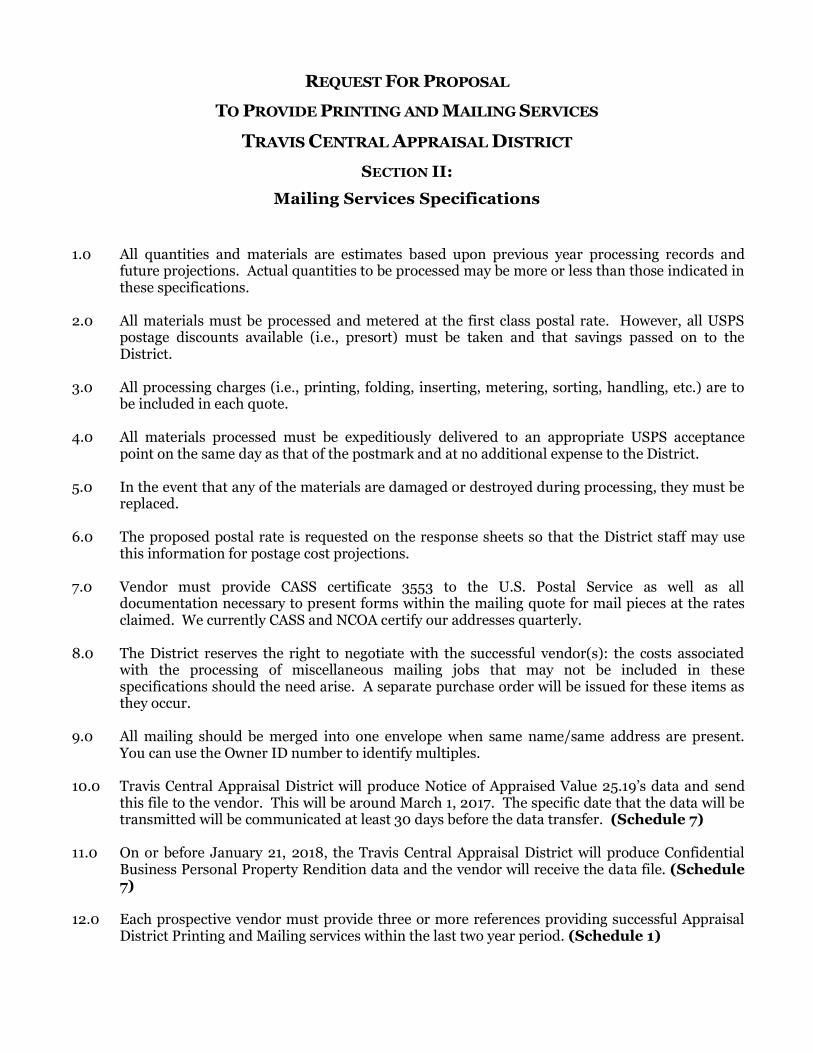

Mailing Services Specifications

1.0 All quantities and materials are estimates based upon previous year processing records and

future projections. Actual quantities to be processed may be more or less than those indicated in these specifications.

2.0 All materials must be processed and metered at the first class postal rate. However, all USPS

postage discounts available (i.e., presort) must be taken and that savings passed on to the District.

3.0 All processing charges (i.e., printing, folding, inserting, metering, sorting, handling, etc.) are to

be included in each quote. 4.0 All materials processed must be expeditiously delivered to an appropriate USPS acceptance

point on the same day as that of the postmark and at no additional expense to the District. 5.0 In the event that any of the materials are damaged or destroyed during processing, they must be

replaced. 6.0 The proposed postal rate is requested on the response sheets so that the District staff may use

this information for postage cost projections. 7.0 Vendor must provide CASS certificate 3553 to the U.S. Postal Service as well as all

documentation necessary to present forms within the mailing quote for mail pieces at the rates claimed. We currently CASS and NCOA certify our addresses quarterly.

8.0 The District reserves the right to negotiate with the successful vendor(s): the costs associated

with the processing of miscellaneous mailing jobs that may not be included in these specifications should the need arise. A separate purchase order will be issued for these items as they occur.

9.0 All mailing should be merged into one envelope when same name/same address are present. You can use the Owner ID number to identify multiples.

10.0 Travis Central Appraisal District will produce Notice of Appraised Value 25.19’s data and send

this file to the vendor. This will be around March 1, 2017. The specific date that the data will be transmitted will be communicated at least 30 days before the data transfer. (Schedule 7)

11.0 On or before January 21, 2018, the Travis Central Appraisal District will produce Confidential

Business Personal Property Rendition data and the vendor will receive the data file. (Schedule 7)

12.0 Each prospective vendor must provide three or more references providing successful Appraisal

District Printing and Mailing services within the last two year period. (Schedule 1)

13.0 The awarded vendor will generate samples from final data provided by the District prior to this production requirement. These samples must be presented for review and verification by the District’s Chief Appraiser. Changes to the form and/or data stream are possible up to the initial printing date. The vendor must have programming capability to handle the data stream and merge to the form. Vendor will have to create the form from the samples provided.

14.0 One complete printing sample of Data must to be included in the proposal package, i.e., Notice

of Appraised Value 25.19 (NOAV)(Schedule 10) and Confidential Business Personal Property Renditions (CPPRs)(Schedule 11). Submit all proposals to the address previously mentioned.

REQUEST FOR PROPOSAL

TO PROVIDE PRINTING AND MAILING SERVICES

TRAVIS CENTRAL APPRAISAL DISTRICT

SECTION III:

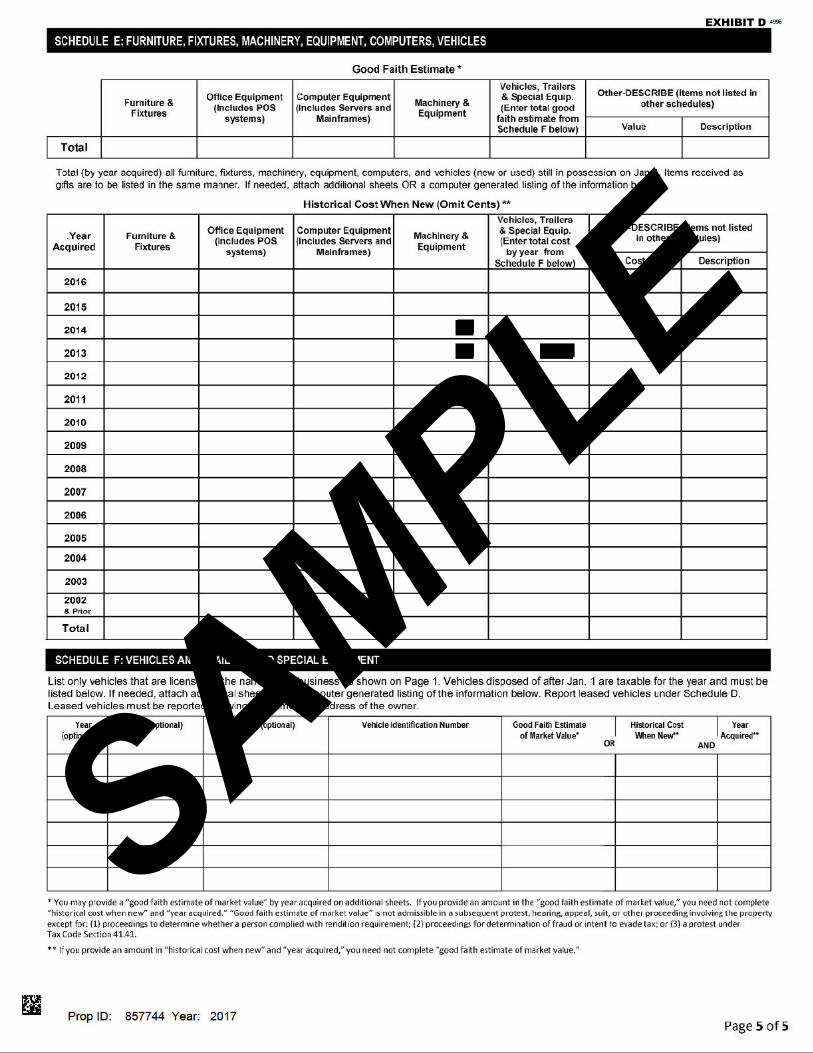

Notice of Appraised Value (NOAV) 25.19A Specifications

1.0 Data will be provided as input stream to be merged with the form. The preferred

method of data exchange is FTP server. The vendor would be responsible for the FTP server. Data input stream is a txt file that must be merged correctly for each form. Data may also be exchanged via CD/DVD.

2.0 Form length varies from 4 to 6 pages and the vendor must be able to handle both

form lengths within a single data stream.

3.0 Page 1 has general account information and a grid of variable data to be merged on the form. All variable data must be aligned to fit within the boundaries of the appropriate square. Page 2 has general account information and variable data to be merged in the form. Page 3 includes standard protest language. Only the Efile notices include a color picture on page 3. Page 4 has general accounting information and a barcode to be merged on the form.

4.0 Position of 3 of 9 barcode is essential to future forms processing and must be placed exactly in the same position as the sample.

5.0 The vendor must provide samples of the printed forms for forms processing testing of

the barcode. The sample must pass forms processing testing.

6.0 A two page insert “Taxpayers Rights and Remedies” is to be included in ALL Notice of Appraised Value mail envelopes. This document is printed in black and white ink, duplex, legal size paper. It is the vendors responsibility to provide this form with the Notices of Appraised Value mailing. The current version of Taxpayers Rights and Remedies is included as Exhibit E.

7.0 Vendor shall coordinate data specifications, format, and laser system programming

requirements with the District’s IT department. Vendor is to provide proofs of all documents to the District’s IT department for approval prior to printing. Proofs may be provided via email and/or FTP. The vendor shall correct any errors or omissions noted and return to the District for final approval.

8.0 Three (3) types of notices are generated in a single data stream: Standard, Agent and

Homestead. The vendor must be able to identify the type of notice based on indicators in the data and print the appropriate notice.

9.0 Standard notices should be grouped based on the owner ID in the data stream, and

all notices for a given owner should be put in a single envelope. Standard notices are four pages. Pages 1 and 2 are the Notice of Appraised Value and pages 3 and 4 are the property protest form (duplex).

10.0 Efile notices should be grouped based on the owner ID in the data stream, and all notices for a given owner should be put in a single envelope. Efile notices are four pages. Pages 1 and 2 are the Notice of Appraised Value and pages 3 and 4 are the property protest form (duplex). Page 3 includes a color graphic on the Efile notice ONLY.

11.0 Homestead notices should be identified and the fifth and sixth pages should be

printed as appropriate. Vendor may opt to sort input data for the type of notices and print in batches if they choose. Homestead Notices are eight pages. Pages 1 and 2 are the Notice of Appraised Value and pages 3 and 4 are the property protest form (duplex). The first four pages are the same as the standard Notice of Appraised Value. Homestead notices also include pages 5, Homestead Application Flyer, and page 6, Homestead application.

12.0 TCAD may make changes to the wording in the sample form provided.

13.0 Vendor must laser print Notice of Appraised Value 25.19’s with a 3 of 9 barcode with

selected data. The bar code will be tested for validity and it must pass for the proposal to be accepted. Positioning of the bar code is very important. You must laser print the complete form. Offset printing will not allow this positioning to work.

14.0 The District reserves the right to change the Notices of Appraised Value

from year to year. If changes are made, the District will negotiate the contract changes with the selected vendor for each required change.

15.0 No. 10 standard window envelopes will be provided by the District.

Request for Proposal

Travis Central Appraisal District

Section IV:

Confidential Business Personal Property Renditions (CPPRs) Specifications

1.0 Data will be provided as input stream to be merged with the form. The preferred method of data

exchange is FTP server. The vendor would be responsible for FTP server. Data input stream is a

series of txt files that must be merged correctly for each form. Data may also be exchanged via

CD/DVD.

2.0 The rendition form is 4 pages duplex (8 printed pages total).

3.0 There are three (3) types of data txt files for input that must be merged. Main property data,

Schedule A data, and Schedule B data. The control key used to merge the data form the different

files on to a single form is the Property ID number.

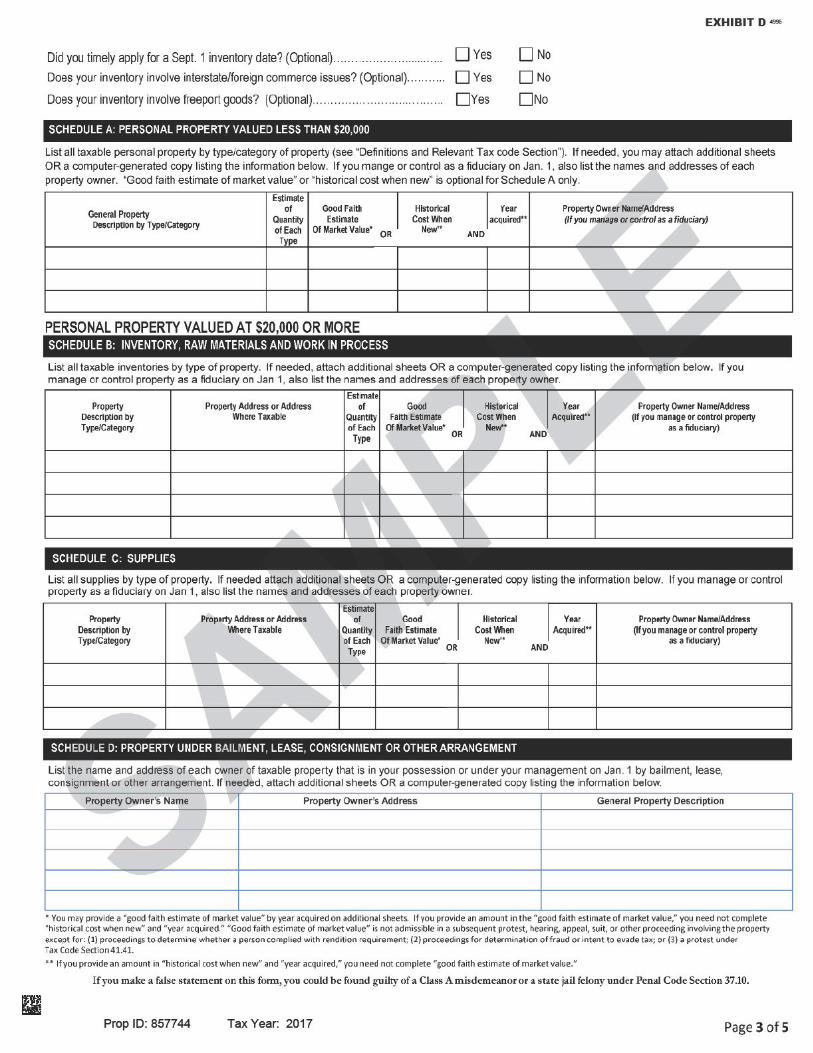

4.0 Page 1 has general information about the Confidential Business Personal Property Renditions

(CPPRs). General account information must be merged on page 1 in the address box. Please see

Exhibit D for a sample. The barcode information must appear exactly as it does on the sample in

the exact location. Page 2 is left blank.

5.0 Page 3 has general account information to be merged on the form. The main property data file is

used to complete page 3. Pages 4, 6, and 7 are static data. Page 8 is left blank.

6.0 Page 5, Schedule A and Schedule B contain a grids with variable data to be merged into the grid.

The Schedule A and Schedule D data file, respectively, is used to enter this data. There are

multiple line entries in this data used to complete the grid. All variable data must be aligned to fit

within the boundaries of the appropriate square.

7.0 Property ID and Year are to be printed in the bottom left corner of each page, and forms are to

be printed duplex.

8.0 A return No. 9 red border envelope and an instructional insert are to be included in the mail

envelope. No. 9 red border envelope will be provided by the District.

9.0 Vendors must have the ability to collate forms based on owner name and address and mail all

forms for a given owner in a single envelope.

10.0 Vendor shall coordinate data specifications, format and laser system programming requirements

with the District’s IT department. Vendor is to provide proofs of all documents to the District’s

IT department for approval prior to printing. Proofs may be provided via e-mail and/or FTP. The

vendor shall correct any errors or omissions noted and return to the District for final approval.

11.0 Vendor must supply the District with PDF copies of all renditions.

12.0 No. 10 standard window envelopes will be provided by the District.

P O BOX 149012 8314 CROSS PARK DRIVE AUSTIN, TEXAS 78714-9012 (512) 834 9317 TDD (512) 836-3328 FAX (512) 835-5371

WWW TRAVISCAD ORG

Section V:

Proposal Specifications

The vendor has carefully inspected the forms and documents and that from the Vendor’s own

investigation, the Vendor has satisfied itself as to the nature and location of the work and the character,

quality, quantities, materials and difficulties to be encountered; the kind and extent of equipment and

other facilities needed for the performance of the work and the general and local conditions and other

items which may in any way affect the performance of the services. The vendor understands and accepts

the difficulties and costs associated with the services and the potential delays, disruptions in work and

costs associated there with and has included such considerations in its work schedule and the proposed

amount.

The intent of the mailing is to get the Notice of Appraised Value 25.19 (NOAV) and Confidential

Business Personal Property Renditions (CPPRs) into the mail system in a timely manner, no later than

the due date established, and at the best possible 1st class postage rate available. Our addresses have been

CASS certified, but you may need to do it again to achieve your level of comfort with the process. The vendor’s current financial statement attached hereto as Schedule 4 is true and complete in all respects and reflects the true financial condition of the vendor. SCHEDULES: The following schedules must be completed for the requested quote to be considered and

potentially accepted.

Schedule 1: References Schedule 2: Workers’ Compensation Statement Schedule 3: Payment Terms and Discounts Schedule 4: Financial Statements Schedule 5: Detail Proposal Costs for Notice of Appraised Value 25.19 Schedule 6: Detail Proposal Costs for Business Confidential Personal Property

Renditions Schedule 7: Mail out schedule Schedule 8: Anticipated Timeline Schedule 9: Sample Form- Notice of Appraised Value 25.19 (NOAV) Schedule 10: Sample Form- Confidential Business Personal Property Rendition

(CPPRs

Vendor Name Signature of Owner or Authorized Agent

Print name of Owner or Authorized Agent

Title

TRAVIS CENTRAL APPRAISAL DISTRICT

BOARD OFFICERS RICHARD LAVINE

CHAIRPERSON

KRISTOFFER S. LANDS

VICE CHAIRPERSON

ED KELLER

SECRETARY/TREASURER

MARYA CRIGLER

CHIEF APPRAISER

BOARD MEMBERS TOM BUCKLE

JAMES VALDEZ

BRUCE GRUBE

BRUCE ELFANT

ELEANOR POWELL

RICO REYES

BLANCA ZAMORA-GARCIA

SCHEDULE 1 REFERENCES

Company Name:

Contact Person:

Address:

Telephone No.:

Facsimile No.:

E-mail:

Description of Contract (including size and type of services and dollar amount):

Company Name:

Contact Person:

Address:

Telephone No.:

Facsimile No.:

E-mail:

Description of Contract (including size and type of services and dollar amount):

TRAVIS CENTRAL APPRAISAL DISTRICT

BOARD OFFICERS RICHARD LAVINE

CHAIRPERSON

KRISTOFFER S. LANDS

VICE CHAIRPERSON

ED KELLER

SECRETARY/TREASURER

MARYA CRIGLER

CHIEF APPRAISER

BOARD MEMBERS TOM BUCKLE

JAMES VALDEZ

BRUCE GRUBE

BRUCE ELFANT

ELEANOR POWELL

RICO REYES

BLANCA ZAMORA-GARCIA

Company Name:

Contact Person:

Address:

Telephone No.:

Facsimile No.:

E-mail:

Description of Contract (including size and type of services and dollar amount):

TRAVIS CENTRAL APPRAISAL DISTRICT

BOARD OFFICERS RICHARD LAVINE

CHAIRPERSON

KRISTOFFER S. LANDS

VICE CHAIRPERSON

ED KELLER

SECRETARY/TREASURER

MARYA CRIGLER

CHIEF APPRAISER

BOARD MEMBERS TOM BUCKLE

JAMES VALDEZ

BRUCE GRUBE

BRUCE ELFANT

ELEANOR POWELL

RICO REYES

BLANCA ZAMORA-GARCIA

SCHEDULE 2

WORKER’S COMPENSATION INSURANCE

TRAVIS CENTRAL APPRAISAL DISTRICT

BOARD OFFICERS RICHARD LAVINE

CHAIRPERSON

KRISTOFFER S. LANDS

VICE CHAIRPERSON

ED KELLER

SECRETARY/TREASURER

MARYA CRIGLER

CHIEF APPRAISER

BOARD MEMBERS TOM BUCKLE

JAMES VALDEZ

BRUCE GRUBE

BRUCE ELFANT

ELEANOR POWELL

RICO REYES

BLANCA ZAMORA-GARCIA

SCHEDULE 3

PAYMENT TERM AND DISCOUNTS

TRAVIS CENTRAL APPRAISAL DISTRICT

BOARD OFFICERS RICHARD LAVINE

CHAIRPERSON

KRISTOFFER S. LANDS

VICE CHAIRPERSON

ED KELLER

SECRETARY/TREASURER

MARYA CRIGLER

CHIEF APPRAISER

BOARD MEMBERS TOM BUCKLE

JAMES VALDEZ

BRUCE GRUBE

BRUCE ELFANT

ELEANOR POWELL

RICO REYES

BLANCA ZAMORA-GARCIA

SCHEDULE 4

FINANCIAL STATEMENTS

TRAVIS CENTRAL APPRAISAL DISTRICT

BOARD OFFICERS RICHARD LAVINE

CHAIRPERSON

KRISTOFFER S. LANDS

VICE CHAIRPERSON

ED KELLER

SECRETARY/TREASURER

MARYA CRIGLER

CHIEF APPRAISER

BOARD MEMBERS TOM BUCKLE

JAMES VALDEZ

BRUCE GRUBE

BRUCE ELFANT

ELEANOR POWELL

RICO REYES

BLANCA ZAMORA-GARCIA

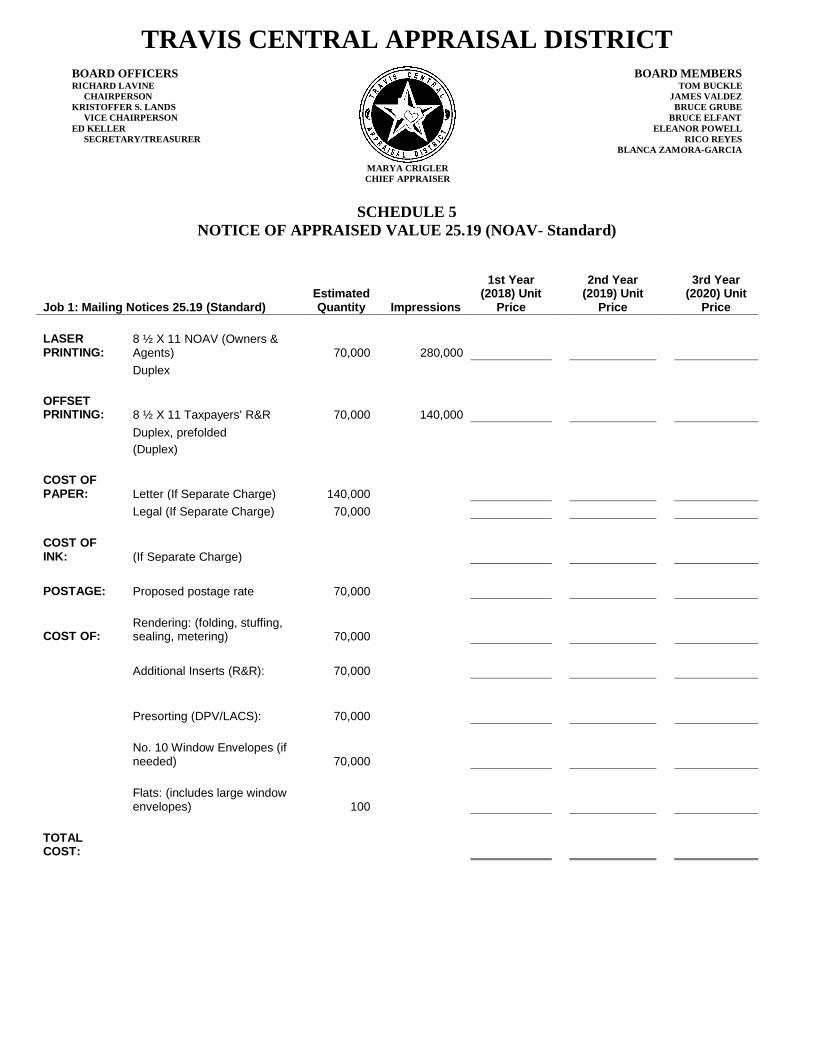

SCHEDULE 5

NOTICE OF APPRAISED VALUE 25.19 (NOAV- Standard)

Job 1: Mailing Notices 25.19 (Standard)

Estimated Quantity Impressions

1st Year (2018) Unit

Price

2nd Year (2019) Unit

Price

3rd Year (2020) Unit

Price

LASER PRINTING:

8 ½ X 11 NOAV (Owners & Agents)

70,000 280,000

Duplex

OFFSET PRINTING: 8 ½ X 11 Taxpayers' R&R

70,000 140,000

Duplex, prefolded

(Duplex)

COST OF PAPER: Letter (If Separate Charge)

140,000

Legal (If Separate Charge) 70,000

COST OF INK: (If Separate Charge)

POSTAGE: Proposed postage rate 70,000

COST OF: Rendering: (folding, stuffing, sealing, metering) 70,000

Additional Inserts (R&R): 70,000

Presorting (DPV/LACS):

70,000

No. 10 Window Envelopes (if needed) 70,000

Flats: (includes large window envelopes)

100

TOTAL COST:

TRAVIS CENTRAL APPRAISAL DISTRICT

BOARD OFFICERS RICHARD LAVINE

CHAIRPERSON

KRISTOFFER S. LANDS

VICE CHAIRPERSON

ED KELLER

SECRETARY/TREASURER

MARYA CRIGLER

CHIEF APPRAISER

BOARD MEMBERS TOM BUCKLE

JAMES VALDEZ

BRUCE GRUBE

BRUCE ELFANT

ELEANOR POWELL

RICO REYES

BLANCA ZAMORA-GARCIA

SCHEDULE 5

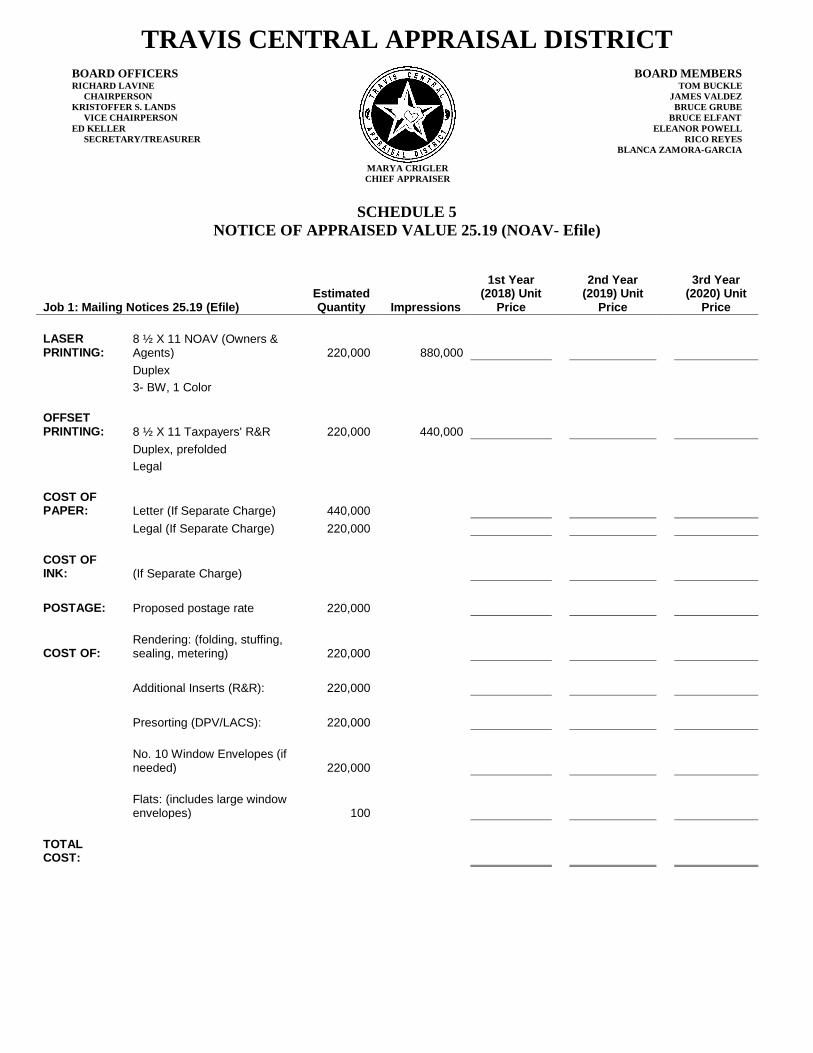

NOTICE OF APPRAISED VALUE 25.19 (NOAV- Efile)

Job 1: Mailing Notices 25.19 (Efile)

Estimated Quantity Impressions

1st Year (2018) Unit

Price

2nd Year (2019) Unit

Price

3rd Year (2020) Unit

Price

LASER PRINTING:

8 ½ X 11 NOAV (Owners & Agents)

220,000 880,000

Duplex

3- BW, 1 Color

OFFSET PRINTING: 8 ½ X 11 Taxpayers' R&R

220,000 440,000

Duplex, prefolded

Legal

COST OF PAPER: Letter (If Separate Charge)

440,000

Legal (If Separate Charge) 220,000

COST OF INK: (If Separate Charge)

POSTAGE: Proposed postage rate 220,000

COST OF: Rendering: (folding, stuffing, sealing, metering)

220,000

Additional Inserts (R&R): 220,000

Presorting (DPV/LACS): 220,000

No. 10 Window Envelopes (if needed)

220,000

Flats: (includes large window envelopes)

100

TOTAL COST:

TRAVIS CENTRAL APPRAISAL DISTRICT

BOARD OFFICERS RICHARD LAVINE

CHAIRPERSON

KRISTOFFER S. LANDS

VICE CHAIRPERSON

ED KELLER

SECRETARY/TREASURER

MARYA CRIGLER

CHIEF APPRAISER

BOARD MEMBERS TOM BUCKLE

JAMES VALDEZ

BRUCE GRUBE

BRUCE ELFANT

ELEANOR POWELL

RICO REYES

BLANCA ZAMORA-GARCIA

P O BOX 149012 8314 CROSS PARK DRIVE AUSTIN, TEXAS 78714-9012 (512) 834 9317 TDD (512) 836-3328

WWW TRAVISCAD ORG

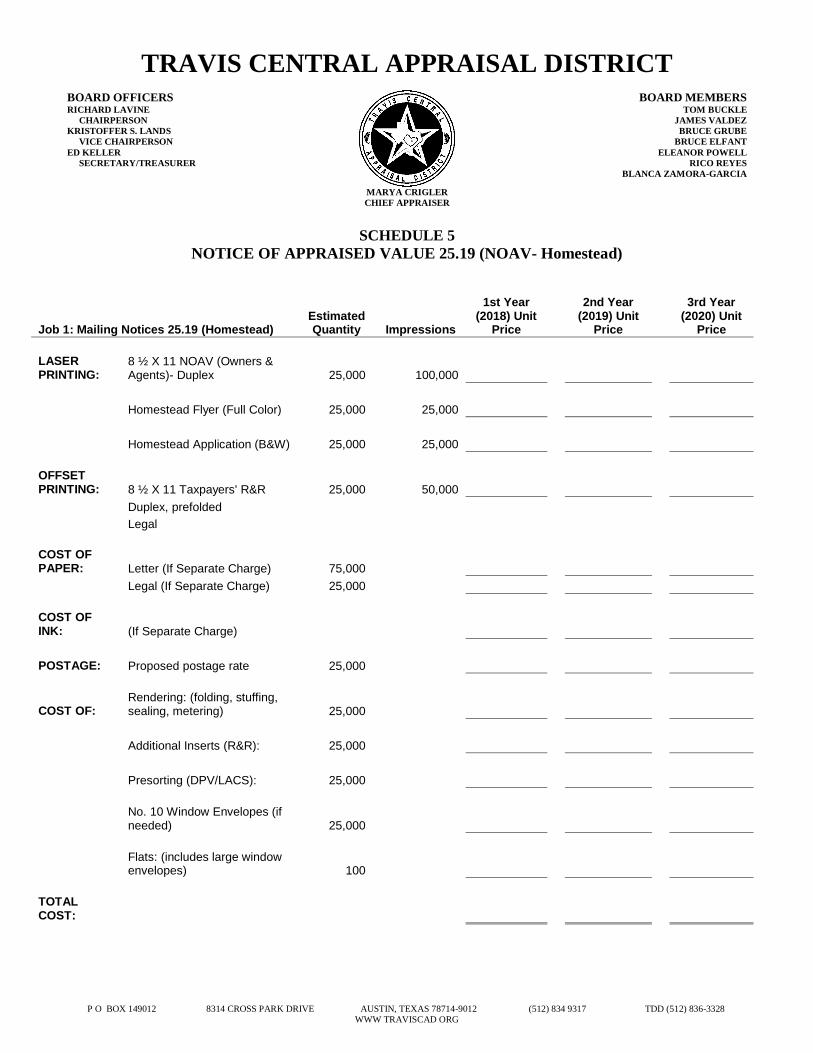

SCHEDULE 5

NOTICE OF APPRAISED VALUE 25.19 (NOAV- Homestead)

Job 1: Mailing Notices 25.19 (Homestead)

Estimated Quantity Impressions

1st Year (2018) Unit

Price

2nd Year (2019) Unit

Price

3rd Year (2020) Unit

Price

LASER PRINTING:

8 ½ X 11 NOAV (Owners & Agents)- Duplex

25,000 100,000

Homestead Flyer (Full Color) 25,000 25,000

Homestead Application (B&W) 25,000 25,000

OFFSET PRINTING: 8 ½ X 11 Taxpayers' R&R 25,000 50,000

Duplex, prefolded

Legal

COST OF PAPER: Letter (If Separate Charge)

75,000

Legal (If Separate Charge) 25,000

COST OF INK: (If Separate Charge)

POSTAGE: Proposed postage rate 25,000

COST OF: Rendering: (folding, stuffing, sealing, metering) 25,000

Additional Inserts (R&R): 25,000

Presorting (DPV/LACS): 25,000

No. 10 Window Envelopes (if needed) 25,000

Flats: (includes large window envelopes)

100

TOTAL COST:

TRAVIS CENTRAL APPRAISAL DISTRICT

BOARD OFFICERS RICHARD LAVINE

CHAIRPERSON

KRISTOFFER S. LANDS

VICE CHAIRPERSON

ED KELLER

SECRETARY/TREASURER

MARYA CRIGLER

CHIEF APPRAISER

BOARD MEMBERS TOM BUCKLE

JAMES VALDEZ

BRUCE GRUBE

BRUCE ELFANT

ELEANOR POWELL

RICO REYES

BLANCA ZAMORA-GARCIA

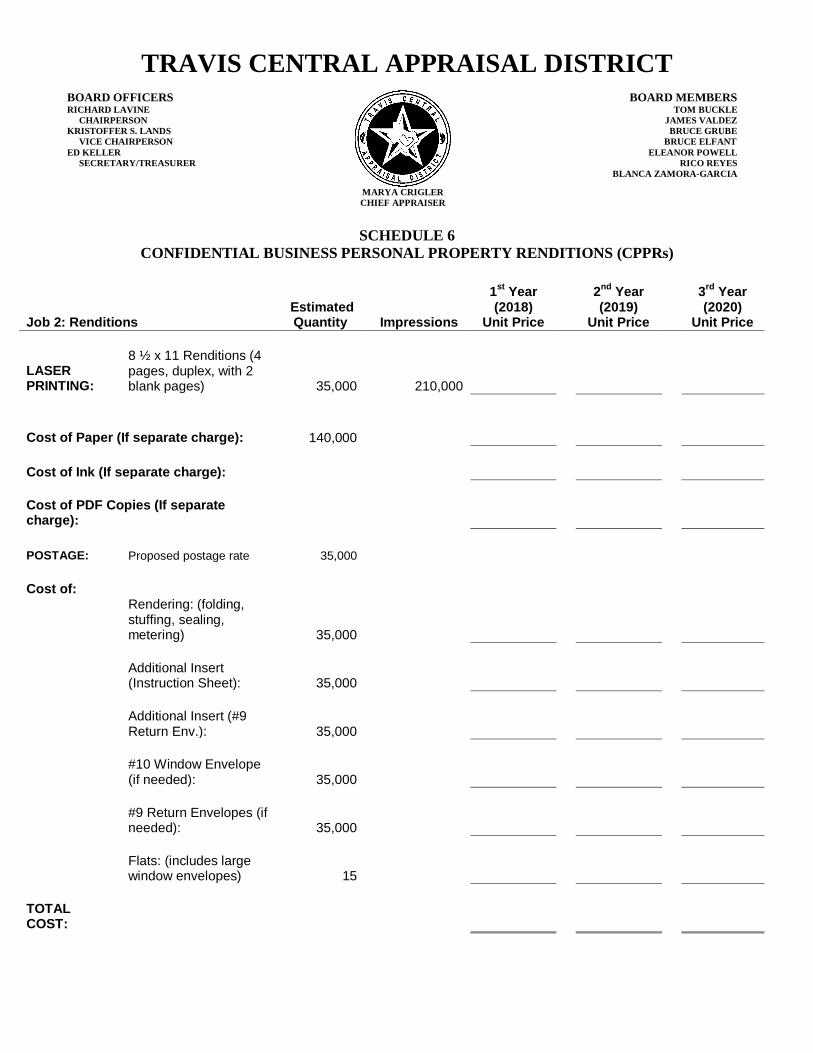

SCHEDULE 6

CONFIDENTIAL BUSINESS PERSONAL PROPERTY RENDITIONS (CPPRs)

Job 2: Renditions Estimated Quantity Impressions

1st

Year (2018)

Unit Price

2nd

Year (2019)

Unit Price

3rd

Year (2020)

Unit Price

LASER PRINTING:

8 ½ x 11 Renditions (4 pages, duplex, with 2 blank pages) 35,000 210,000

Cost of Paper (If separate charge): 140,000

Cost of Ink (If separate charge):

Cost of PDF Copies (If separate charge):

POSTAGE: Proposed postage rate 35,000

Cost of:

Rendering: (folding, stuffing, sealing, metering) 35,000

Additional Insert (Instruction Sheet): 35,000

Additional Insert (#9 Return Env.): 35,000

#10 Window Envelope (if needed): 35,000

#9 Return Envelopes (if needed): 35,000

Flats: (includes large window envelopes) 15

TOTAL COST:

TRAVIS CENTRAL APPRAISAL DISTRICT

BOARD OFFICERS RICHARD LAVINE

CHAIRPERSON

KRISTOFFER S. LANDS

VICE CHAIRPERSON

ED KELLER

SECRETARY/TREASURER

MARYA CRIGLER

CHIEF APPRAISER

BOARD MEMBERS TOM BUCKLE

JAMES VALDEZ

BRUCE GRUBE

BRUCE ELFANT

ELEANOR POWELL

RICO REYES

BLANCA ZAMORA-GARCIA

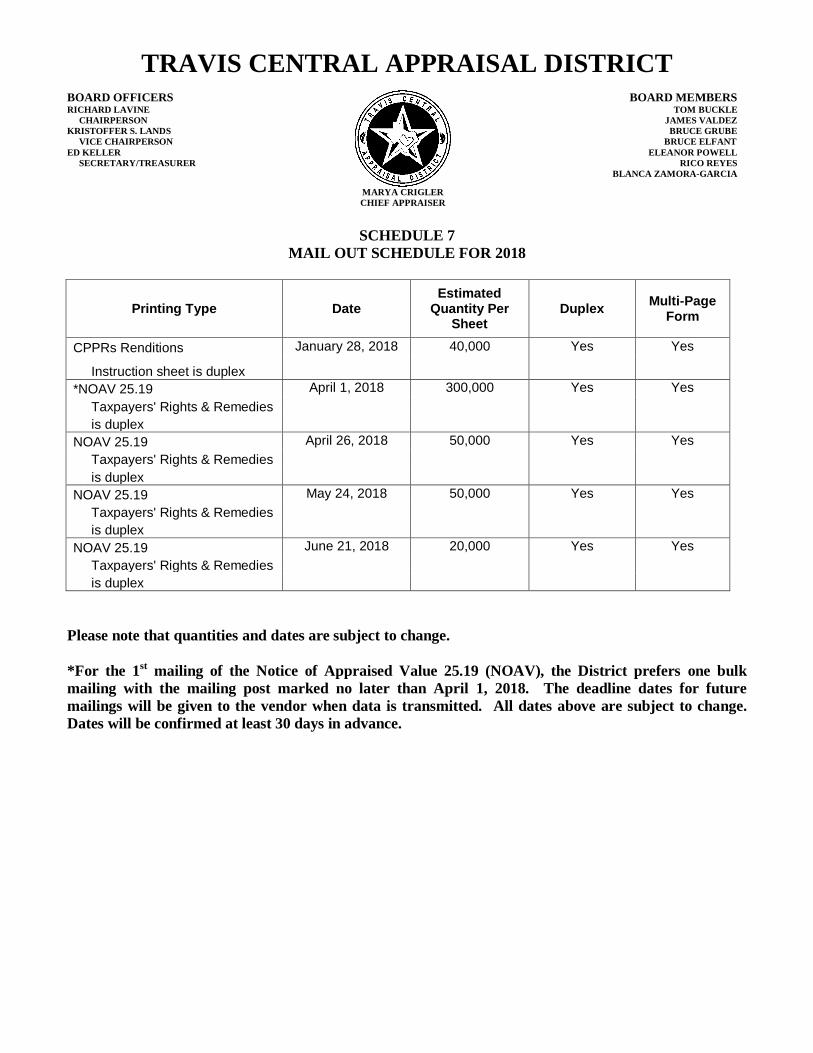

SCHEDULE 7

MAIL OUT SCHEDULE FOR 2018

Printing Type Date Estimated

Quantity Per Sheet

Duplex Multi-Page

Form

CPPRs Renditions January 28, 2018 40,000 Yes Yes

Instruction sheet is duplex

*NOAV 25.19 April 1, 2018 300,000 Yes Yes

Taxpayers' Rights & Remedies

is duplex

NOAV 25.19 April 26, 2018 50,000 Yes Yes

Taxpayers' Rights & Remedies

is duplex

NOAV 25.19 May 24, 2018 50,000 Yes Yes

Taxpayers' Rights & Remedies

is duplex

NOAV 25.19 June 21, 2018

20,000 Yes Yes

Taxpayers' Rights & Remedies

is duplex

Please note that quantities and dates are subject to change.

*For the 1st mailing of the Notice of Appraised Value 25.19 (NOAV), the District prefers one bulk

mailing with the mailing post marked no later than April 1, 2018. The deadline dates for future

mailings will be given to the vendor when data is transmitted. All dates above are subject to change.

Dates will be confirmed at least 30 days in advance.

TRAVIS CENTRAL APPRAISAL DISTRICT

BOARD OFFICERS RICHARD LAVINE

CHAIRPERSON

KRISTOFFER S. LANDS

VICE CHAIRPERSON

ED KELLER

SECRETARY/TREASURER

MARYA CRIGLER

CHIEF APPRAISER

BOARD MEMBERS TOM BUCKLE

JAMES VALDEZ

BRUCE GRUBE

BRUCE ELFANT

ELEANOR POWELL

RICO REYES

BLANCA ZAMORA-GARCIA

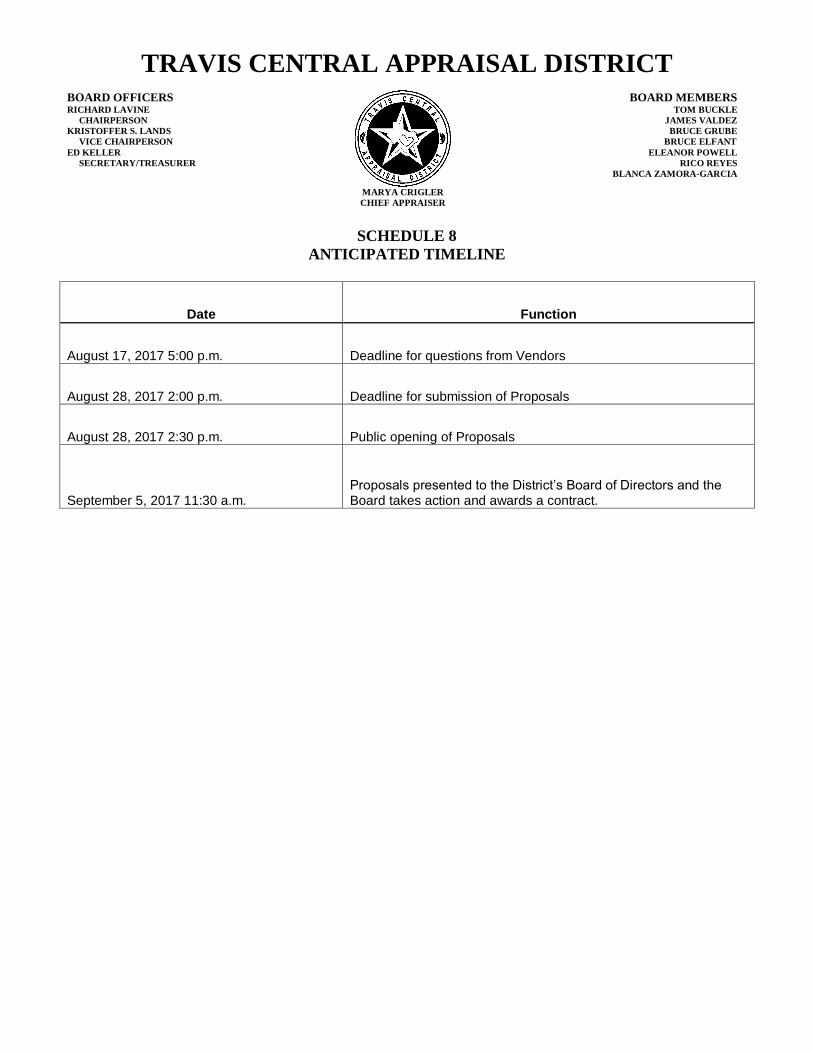

SCHEDULE 8

ANTICIPATED TIMELINE

Date Function

August 17, 2017 5:00 p.m. Deadline for questions from Vendors

August 28, 2017 2:00 p.m. Deadline for submission of Proposals

August 28, 2017 2:30 p.m. Public opening of Proposals

September 5, 2017 11:30 a.m. Proposals presented to the District’s Board of Directors and the Board takes action and awards a contract.

TRAVIS CENTRAL APPRAISAL DISTRICT

BOARD OFFICERS RICHARD LAVINE

CHAIRPERSON

KRISTOFFER S. LANDS

VICE CHAIRPERSON

ED KELLER

SECRETARY/TREASURER

MARYA CRIGLER

CHIEF APPRAISER

BOARD MEMBERS TOM BUCKLE

JAMES VALDEZ

BRUCE GRUBE

BRUCE ELFANT

ELEANOR POWELL

RICO REYES

BLANCA ZAMORA-GARCIA

SCHEDULE 9

SAMPLE FORM

NOTICE OF APPRAISED VALUE 25.19 (NOAV)

Please provide a sample of the Notice of Appraised Value 25.19 (NOAV). Exhibit A, B and C provide

our current notices and you should generate your sample based on the exhibits provided. Please provide

the following:

(1) Sample Notice- owner and agent regular NOAV

(2) Sample Notice- NOAV with Homestead Application

(3) Sample Notice- NOAV with E-file

TRAVIS CENTRAL APPRAISAL DISTRICT

BOARD OFFICERS RICHARD LAVINE

CHAIRPERSON

KRISTOFFER S. LANDS

VICE CHAIRPERSON

ED KELLER

SECRETARY/TREASURER

MARYA CRIGLER

CHIEF APPRAISER

BOARD MEMBERS TOM BUCKLE

JAMES VALDEZ

BRUCE GRUBE

BRUCE ELFANT

ELEANOR POWELL

RICO REYES

BLANCA ZAMORA-GARCIA

SCHEDULE 10

SAMPLE FORM

CONFIDENTIAL BUSINESS PERSONAL PROPERTY RENDITIONS (CPPRs)

Please provide a sample of the Confidential Business Personal Property Renditions (CPPRs) form.

Exhibit D provides our current notice and you should generate your sample based on the exhibit provided.

Please provide the following:

(1) Confidential Business Personal Property Renditions (CPPRs)

TRAVIS CENTRAL APPRAISAL DISTRICT

BOARD OFFICERS RICHARD LAVINE

CHAIRPERSON

KRISTOFFER S. LANDS

VICE CHAIRPERSON

ED KELLER

SECRETARY/TREASURER

MARYA CRIGLER

CHIEF APPRAISER

BOARD MEMBERS TOM BUCKLE

JAMES VALDEZ

BRUCE GRUBE

BRUCE ELFANT

ELEANOR POWELL

RICO REYES

BLANCA ZAMORA-GARCIA

EXHIBITS

Exhibit A Standard Notice of Appraised Value Exhibit B Homestead Notice of Appraised Value Exhibit C Efile Notice of Appraised Value Exhibit D Confidential Business Personal Property Rendition (CPPR) Exhibit E Taxpayer Rights & Remedies

00 4 68 0 00 6

261 of 2

524

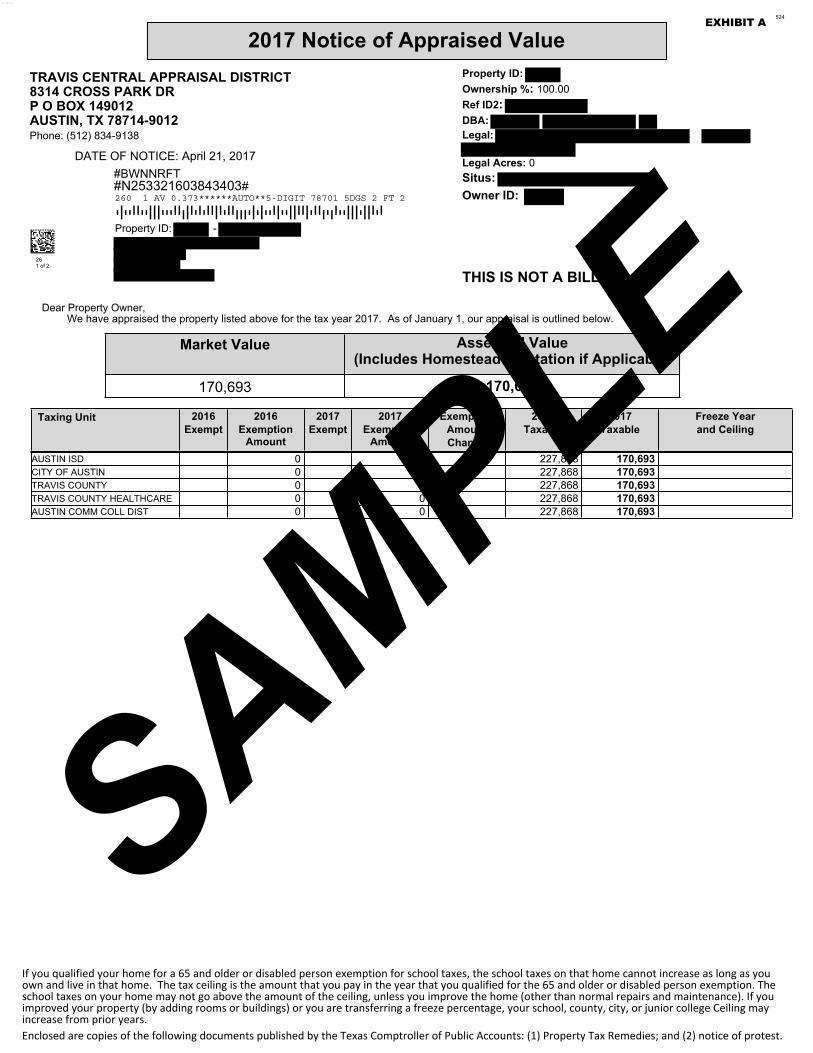

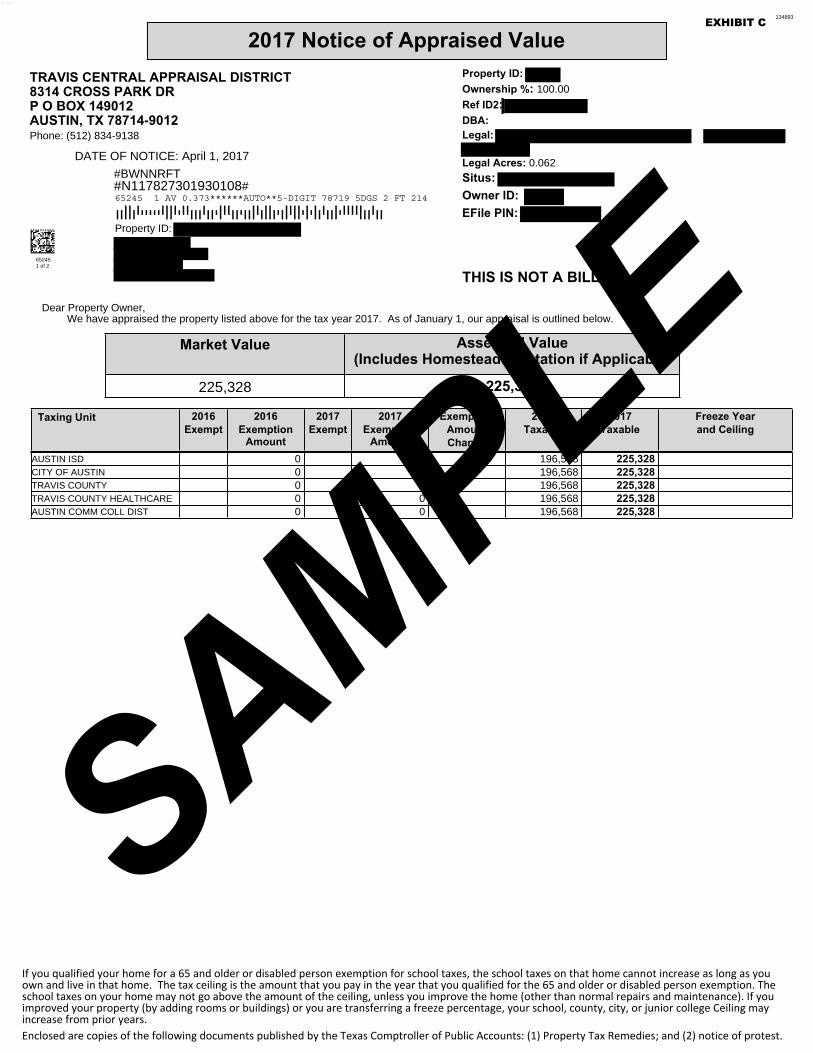

Property ID: -

2017 Notice of Appraised ValueProperty ID: Ownership %: 100.00Ref ID2: DBA: Legal:

Legal Acres: 0Situs: Owner ID:

THIS IS NOT A BILL

DATE OF NOTICE: April 21, 2017

TRAVIS CENTRAL APPRAISAL DISTRICT8314 CROSS PARK DRP O BOX 149012AUSTIN, TX 78714-9012Phone: (512) 834-9138

#BWNNRFT#N253321603843403#

Dear Property Owner,We have appraised the property listed above for the tax year 2017. As of January 1, our app aisal is outlined below.

Market Value Asse d Value(Includes Homestead tation if Applicab

170,693 170,6

Taxing Unit 2016Exempt

2016Exemption

Amount

2017Exempt

2017Exemp

Amo

ExempAmouChan

20Taxa

017Taxable

Freeze Yearand Ceiling

AUSTIN ISD 0 227,8 8 170,693 CITY OF AUSTIN 0 227,868 170,693 TRAVIS COUNTY 0 227,868 170,693 TRAVIS COUNTY HEALTHCARE 0 0 227,868 170,693 AUSTIN COMM COLL DIST 0 0 227,868 170,693

If you qualified your home for a 65 and older or disabled person exemption for school taxes, the school taxes on that home cannot increase as long as youown and live in that home. The tax ceiling is the amount that you pay in the year that you qualified for the 65 and older or disabled person exemption. Theschool taxes on your home may not go above the amount of the ceiling, unless you improve the home (other than normal repairs and maintenance). If youimproved your property (by adding rooms or buildings) or you are transferring a freeze percentage, your school, county, city, or junior college Ceiling mayincrease from prior years. Enclosed are copies of the following documents published by the Texas Comptroller of Public Accounts: (1) Property Tax Remedies; and (2) notice of protest.

260 1 AV 0.373******AUTO**5-DIGIT 78701 5DGS 2 FT 2

EXHIBIT A

SAMPLE

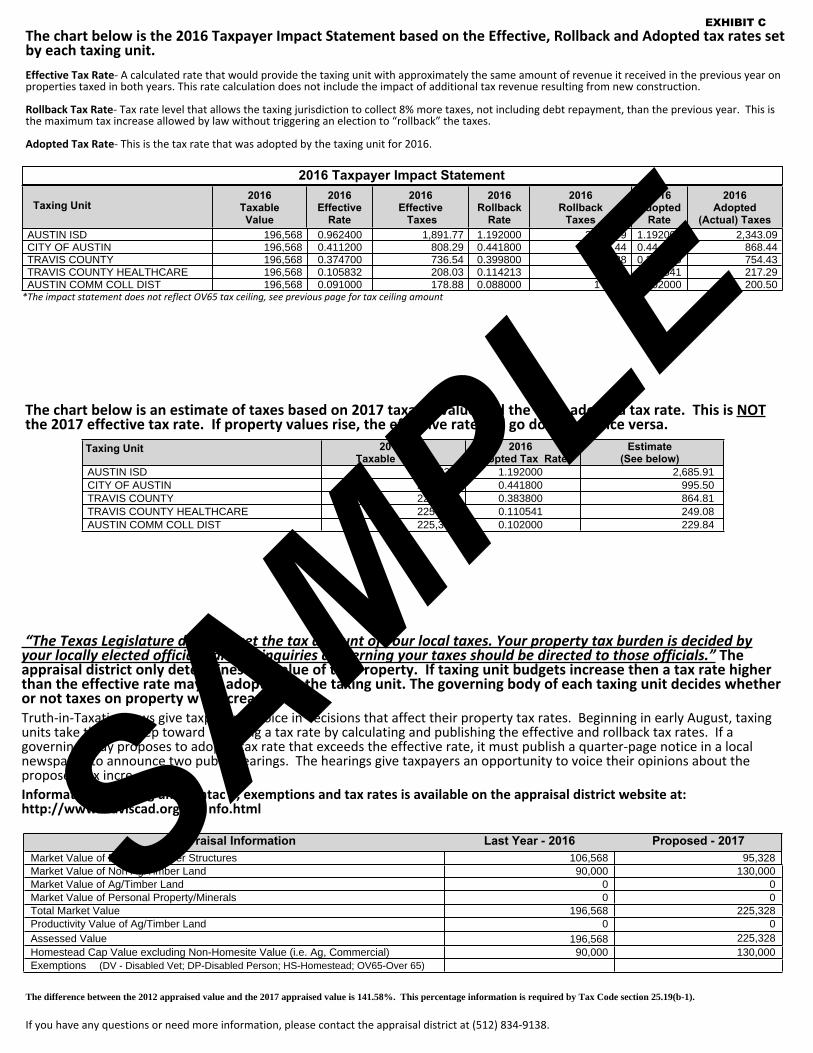

The chart below is the 2016 Taxpayer Impact Statement based on the Effective, Rollback and Adopted tax rates setby each taxing unit.

Effective Tax Rate- A calculated rate that would provide the taxing unit with approximately the same amount of revenue it received in the previous year onproperties taxed in both years. This rate calculation does not include the impact of additional tax revenue resulting from new construction.

Rollback Tax Rate- Tax rate level that allows the taxing jurisdiction to collect 8% more taxes, not including debt repayment, than the previous year. This isthe maximum tax increase allowed by law without triggering an election to “rollback” the taxes.

Adopted Tax Rate- This is the tax rate that was adopted by the taxing unit for 2016.

2016 Taxpayer Impact Statement

Taxing Unit2016

TaxableValue

2016Effective

Rate

2016Effective Taxes

2016Rollback

Rate

2016Rollback

Taxes

16doptedRate

2016Adopted

(Actual) TaxesAUSTIN ISD 227,868 0.962400 2,193.00 1.192000 2 9 1.19200 2,716.19CITY OF AUSTIN 227,868 0.411200 936.99 0.441800 .72 0.44 1,006.72TRAVIS COUNTY 227,868 0.374700 853.82 0.399800 02 0 3 0 874.56TRAVIS COUNTY HEALTHCARE 227,868 0.105832 241.16 0.114213 541 251.89AUSTIN COMM COLL DIST 227,868 0.091000 207.36 0.088000 20 02000 232.43

*The impact statement does not reflect OV65 tax ceiling, see previous page for tax ceiling amount

The chart below is an estimate of taxes based on 2017 taxa value d the ado d tax rate. This is NOTthe 2017 effective tax rate. If property values rise, the ef ive rate l go do ice versa.

Taxing Unit 20Taxable

2016opted Tax Rate

Estimate(See below)

AUSTIN ISD 69 1.192000 2,034.66CITY OF AUSTIN 0.441800 754.13TRAVIS COUNTY 17 0.383800 655.12TRAVIS COUNTY HEALTHCARE 170 0.110541 188.69AUSTIN COMM COLL DIST 170,6 0.102000 174.10

“The Texas Legislature d set the tax a unt of our local taxes. Your property tax burden is decided byyour locally elected officia an inquiries c erning your taxes should be directed to those officials.” Theappraisal district only dete ines alue of t roperty. If taxing unit budgets increase then a tax rate higherthan the effective rate may adopt the taxing unit. The governing body of each taxing unit decides whetheror not taxes on property w creaTruth-in-Taxati ws give taxp er oice in ecisions that affect their property tax rates. Beginning in early August, taxingunits take th ep toward ng a tax rate by calculating and publishing the effective and rollback tax rates. If agovernin dy proposes to adop tax rate that exceeds the effective rate, it must publish a quarter-page notice in a localnewspa to announce two pub earings. The hearings give taxpayers an opportunity to voice their opinions about thepropose x incre Informat g un ntac , exemptions and tax rates is available on the appraisal district website at:http://www. aviscad.org nfo.html

raisal Information Last Year - 2016 Proposed - 2017Market Value of B er Structures 0 0Market Value of Non Ag/Timber Land 0 0Market Value of Ag/Timber Land 0 0Market Value of Personal Property/Minerals 227,868 170,693Total Market Value 227,868 170,693Productivity Value of Ag/Timber Land 0 0Assessed Value 227,868 170,693Homestead Cap Value excluding Non-Homesite Value (i.e. Ag, Commercial) 0 0Exemptions (DV - Disabled Vet; DP-Disabled Person; HS-Homestead; OV65-Over 65)

The difference between the 2012 appraised value and the 2017 appraised value is -25.46%. This percentage information is required by Tax Code section 25.19(b-1).

If you have any questions or need more information, please contact the appraisal district at (512) 834-9138.

EXHIBIT A

SAMPLE

262 of 2

524

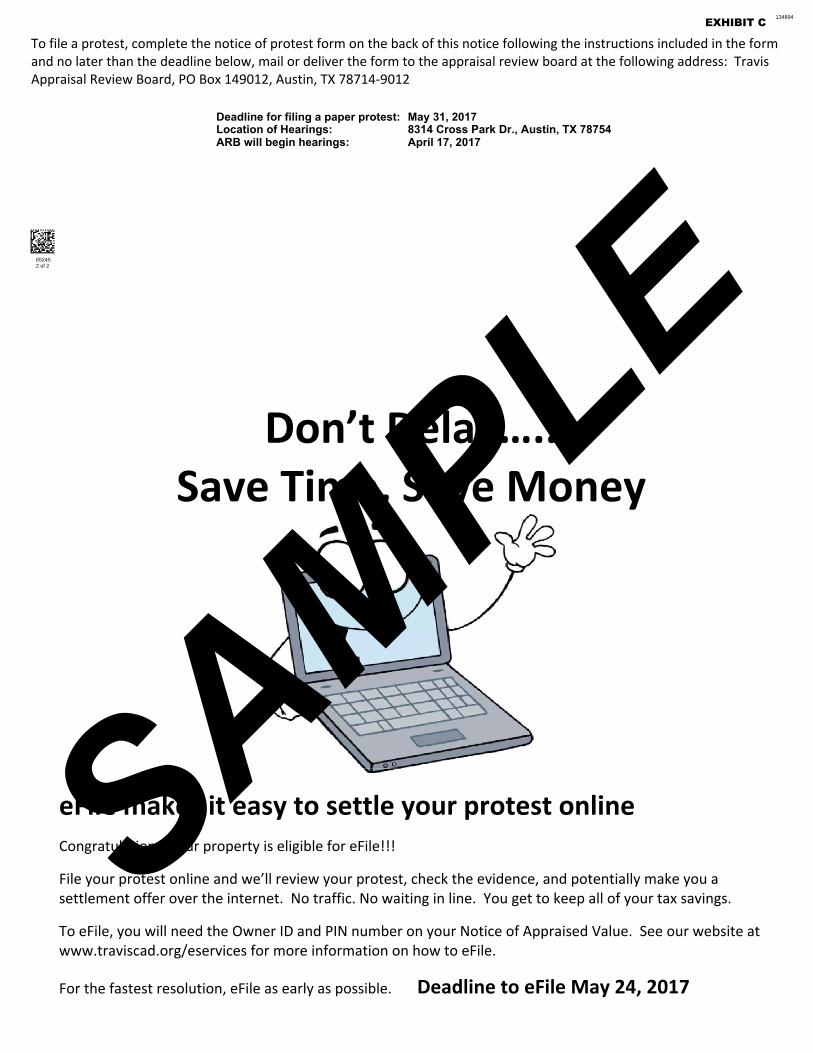

To file a protest, complete the notice of protest form on the back of this notice following the instructions included in the formand no later than the deadline below, mail or deliver the form to the appraisal review board at the following address: TravisAppraisal Review Board, PO Box 149012, Austin, TX 78714-9012

Deadline for filing a paper protest: May 31, 2017Location of Hearings: 8314 Cross Park Dr., Austin, TX 78754ARB will begin hearings: April 17, 2017

EXHIBIT A

SAMPLE

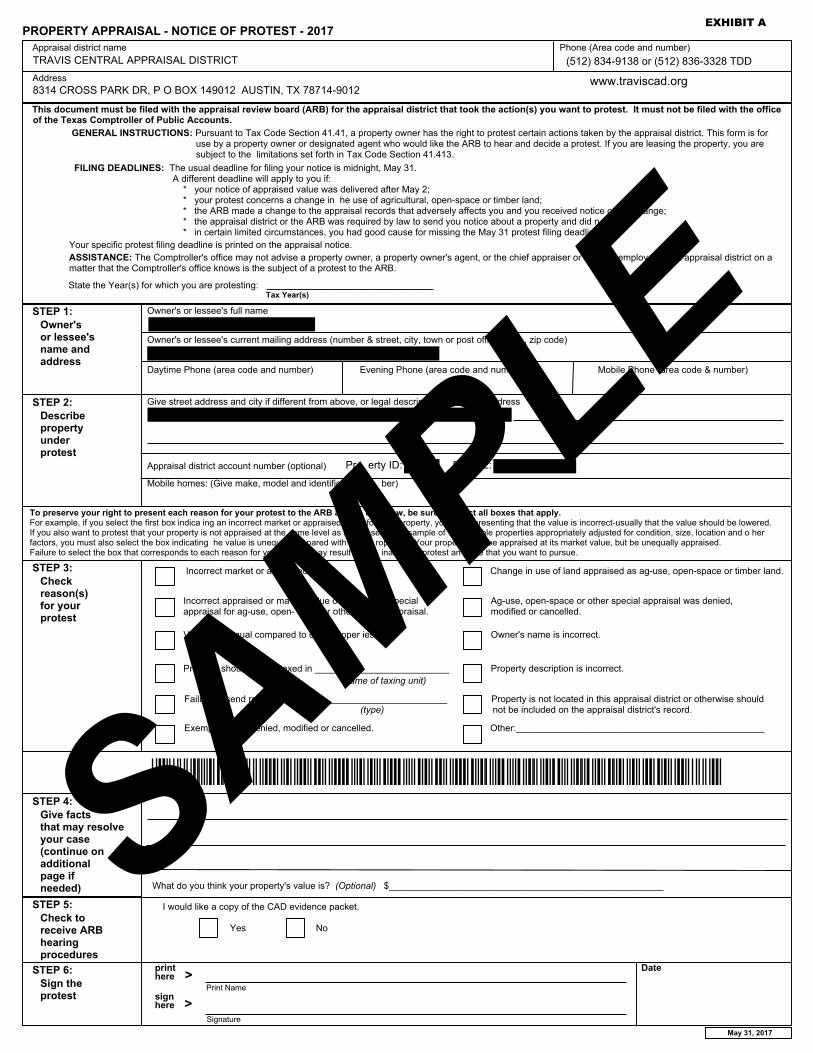

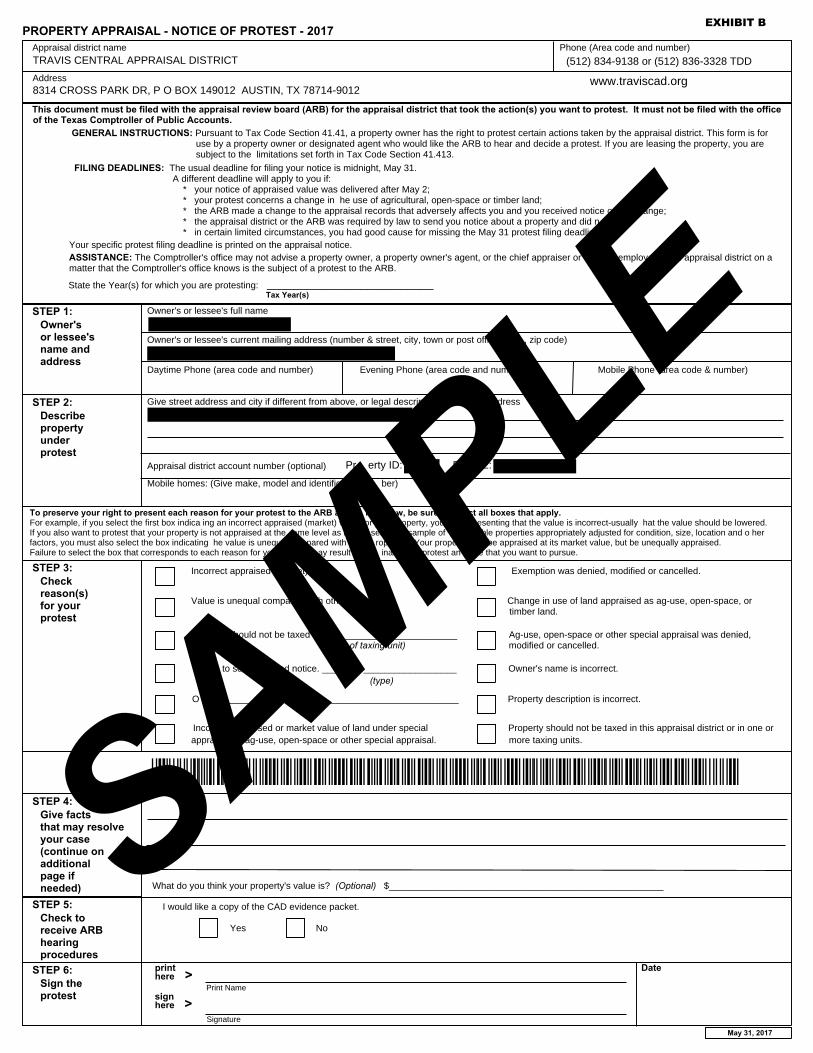

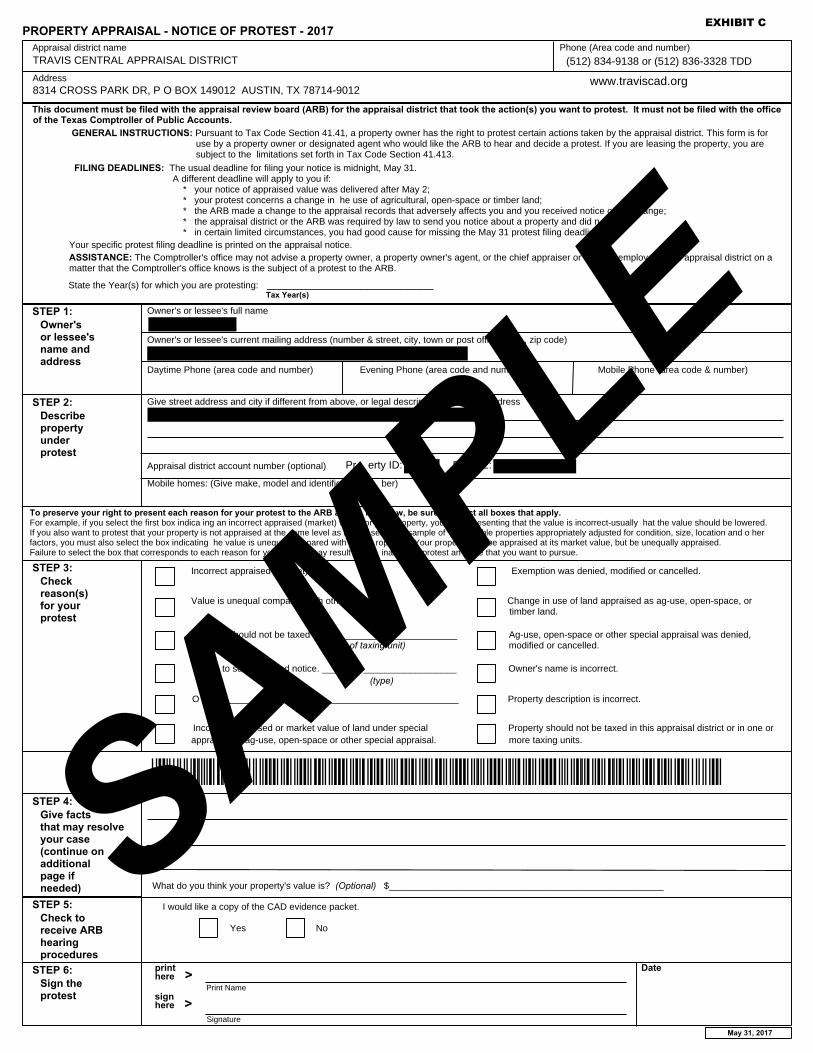

Appraisal district name Phone (Area code and number)

Address

This document must be filed with the appraisal review board (ARB) for the appraisal district that took the action(s) you want to protest. It must not be filed with the office of the Texas Comptroller of Public Accounts. GENERAL INSTRUCTIONS: Pursuant to Tax Code Section 41.41, a property owner has the right to protest certain actions taken by the appraisal district. This form is for use by a property owner or designated agent who would like the ARB to hear and decide a protest. If you are leasing the property, you are subject to the limitations set forth in Tax Code Section 41.413. FILING DEADLINES: The usual deadline for filing your notice is midnight, May 31. A different deadline will apply to you if: * your notice of appraised value was delivered after May 2; * your protest concerns a change in he use of agricultural, open-space or timber land; * the ARB made a change to the appraisal records that adversely affects you and you received notice o ange; * the appraisal district or the ARB was required by law to send you notice about a property and did n * in certain limited circumstances, you had good cause for missing the May 31 protest filing deadlin Your specific protest filing deadline is printed on the appraisal notice. ASSISTANCE: The Comptroller's office may not advise a property owner, a property owner's agent, or the chief appraiser or employe n appraisal district on a matter that the Comptroller's office knows is the subject of a protest to the ARB.

STEP 1: Owner's or lessee's name and address

Owner's or lessee's full name

Owner's or lessee's current mailing address (number & street, city, town or post offi , zip code)

Daytime Phone (area code and number) Evening Phone (area code and num Mobile Phone area code & number)

STEP 2: Describe property under protest

Give street address and city if different from above, or legal descrip dress

Appraisal district account number (optional)

Mobile homes: (Give make, model and identific ber)

To preserve your right to present each reason for your protest to the ARB ac ng w, be sure ct all boxes that apply. For example, if you select the first box indica ing an incorrect market or appraised v for roperty, yo presenting that the value is incorrect-usually that the value should be lowered. If you also want to protest that your property is not appraised at the ame level as a sen sample of ble properties appropriately adjusted for condition, size, location and o her factors, you must also select the box indicating he value is unequ pared with o rope Your prope be appraised at its market value, but be unequally appraised. Failure to select the box that corresponds to each reason for yo ay result i inab protest an e that you want to pursue.

STEP 3: Check reason(s) for your protest

Incorrect market or a ed Change in use of land appraised as ag-use, open-space or timber land.

Incorrect appraised or ma alue o n pecial Ag-use, open-space or other special appraisal was denied, appraisal for ag-use, open- or othe praisal. modified or cancelled.

V qual compared to o oper ies Owner's name is incorrect.

Pr shou taxed in ____ _________________ Property description is incorrect. ame of taxing unit)

Failu send re _______________________ Property is not located in this appraisal district or otherwise should (type) not be included on the appraisal district's record.

Exemp enied, modified or cancelled. Other:________________________________________________

STEP 4: Give facts that may resolve your case (continue on additional page if needed) What do you think your property's value is? (Optional) $_____________________________________________________

STEP 5: Check to receive ARB hearing procedures

I would like a copy of the CAD evidence packet.

Yes No

STEP 6: Sign the protest

print Date here > Print Name sign here > Signature

8314 CROSS PARK DR, P O BOX 149012 AUSTIN, TX 78714-9012 www.traviscad.org

TRAVIS CENTRAL APPRAISAL DISTRICT

_________________________ Tax Year(s)

May 31, 2017

State the Year(s) for which you are protesting:

(512) 834-9138 or (512) 836-3328 TDD

PROPERTY APPRAISAL - NOTICE OF PROTEST - 2017

Pr erty ID: R 2:

BfY:DwZwqu wYBww:duJVe:ffEJFZJfbZVwCJUKJJwUFbZbwYFveBwu:equBwBfVwBfY:DwX

EXHIBIT A

SAMPLE

00 4 72 0 00 1

11 of 4

40

Property ID:

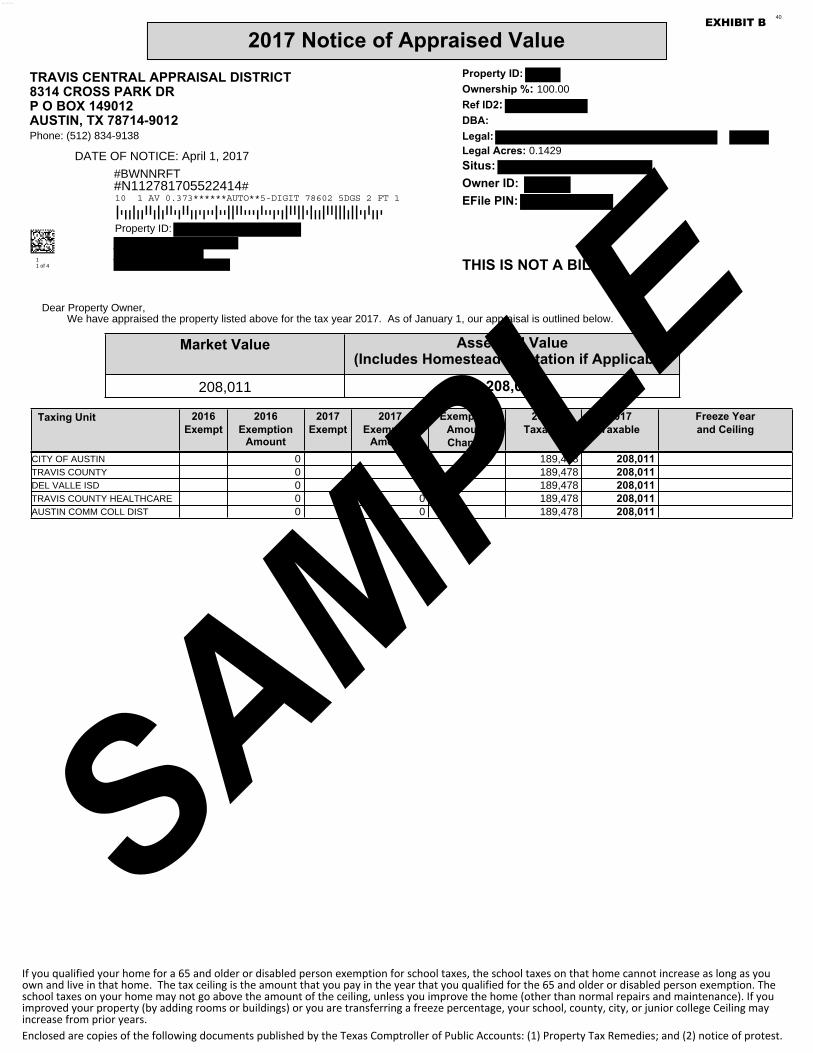

2017 Notice of Appraised ValueProperty ID: Ownership %: 100.00Ref ID2: DBA:Legal: Legal Acres: 0.1429Situs: Owner ID: EFile PIN:

THIS IS NOT A BIL

DATE OF NOTICE: April 1, 2017

TRAVIS CENTRAL APPRAISAL DISTRICT8314 CROSS PARK DRP O BOX 149012AUSTIN, TX 78714-9012Phone: (512) 834-9138

#BWNNRFT#N112781705522414#

Dear Property Owner,We have appraised the property listed above for the tax year 2017. As of January 1, our app aisal is outlined below.

Market Value Asse d Value(Includes Homestead tation if Applicab

208,011 208,0

Taxing Unit 2016Exempt

2016Exemption

Amount

2017Exempt

2017Exemp

Amo

ExempAmouChan

20Taxa

017Taxable

Freeze Yearand Ceiling

CITY OF AUSTIN 0 189,4 8 208,011 TRAVIS COUNTY 0 189,478 208,011 DEL VALLE ISD 0 189,478 208,011 TRAVIS COUNTY HEALTHCARE 0 0 189,478 208,011 AUSTIN COMM COLL DIST 0 0 189,478 208,011

If you qualified your home for a 65 and older or disabled person exemption for school taxes, the school taxes on that home cannot increase as long as youown and live in that home. The tax ceiling is the amount that you pay in the year that you qualified for the 65 and older or disabled person exemption. Theschool taxes on your home may not go above the amount of the ceiling, unless you improve the home (other than normal repairs and maintenance). If youimproved your property (by adding rooms or buildings) or you are transferring a freeze percentage, your school, county, city, or junior college Ceiling mayincrease from prior years. Enclosed are copies of the following documents published by the Texas Comptroller of Public Accounts: (1) Property Tax Remedies; and (2) notice of protest.

10 1 AV 0.373******AUTO**5-DIGIT 78602 5DGS 2 FT 1

SAMPLEEXHIBIT B

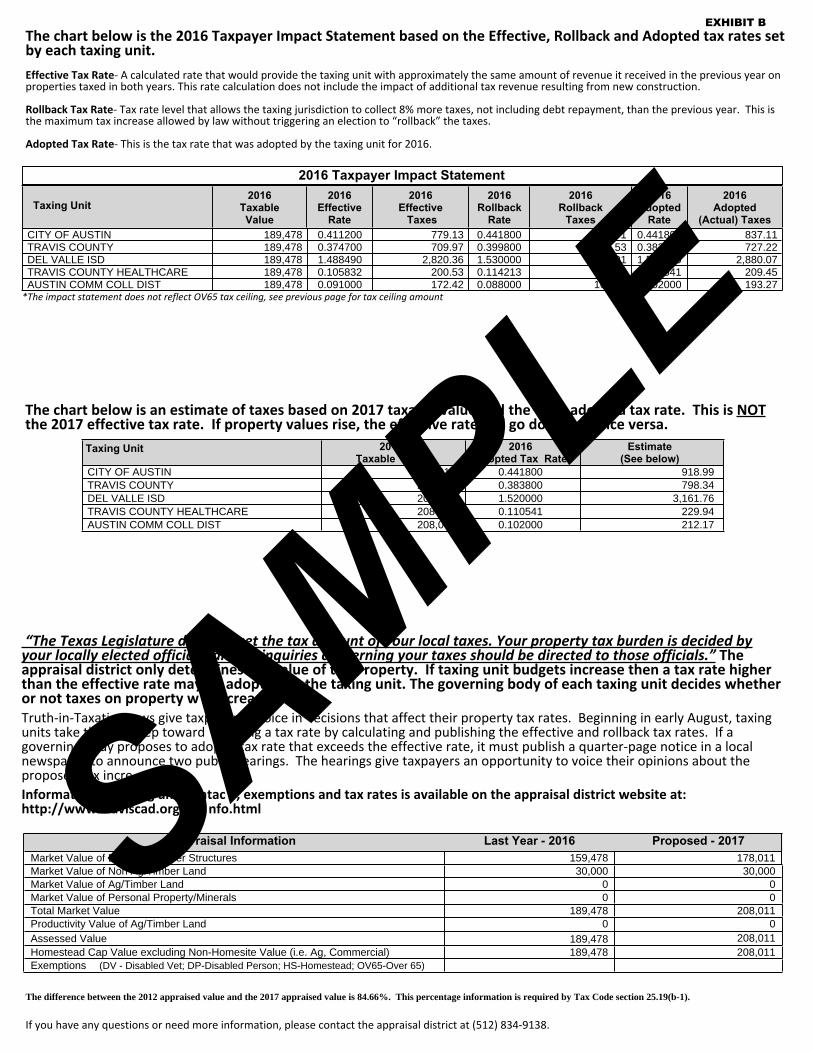

The chart below is the 2016 Taxpayer Impact Statement based on the Effective, Rollback and Adopted tax rates setby each taxing unit.

Effective Tax Rate- A calculated rate that would provide the taxing unit with approximately the same amount of revenue it received in the previous year onproperties taxed in both years. This rate calculation does not include the impact of additional tax revenue resulting from new construction.

Rollback Tax Rate- Tax rate level that allows the taxing jurisdiction to collect 8% more taxes, not including debt repayment, than the previous year. This isthe maximum tax increase allowed by law without triggering an election to “rollback” the taxes.

Adopted Tax Rate- This is the tax rate that was adopted by the taxing unit for 2016.

2016 Taxpayer Impact Statement

Taxing Unit2016

TaxableValue

2016Effective

Rate

2016Effective Taxes

2016Rollback

Rate

2016Rollback

Taxes

16doptedRate

2016Adopted

(Actual) TaxesCITY OF AUSTIN 189,478 0.411200 779.13 0.441800 1 0.44180 837.11TRAVIS COUNTY 189,478 0.374700 709.97 0.399800 .53 0.383 727.22DEL VALLE ISD 189,478 1.488490 2,820.36 1.530000 01 1 5 0 2,880.07TRAVIS COUNTY HEALTHCARE 189,478 0.105832 200.53 0.114213 541 209.45AUSTIN COMM COLL DIST 189,478 0.091000 172.42 0.088000 16 02000 193.27

*The impact statement does not reflect OV65 tax ceiling, see previous page for tax ceiling amount

The chart below is an estimate of taxes based on 2017 taxa value d the ado d tax rate. This is NOTthe 2017 effective tax rate. If property values rise, the ef ive rate l go do ice versa.

Taxing Unit 20Taxable

2016opted Tax Rate

Estimate(See below)

CITY OF AUSTIN 01 0.441800 918.99TRAVIS COUNTY 2 0.383800 798.34DEL VALLE ISD 20 1.520000 3,161.76TRAVIS COUNTY HEALTHCARE 208 0.110541 229.94AUSTIN COMM COLL DIST 208,0 0.102000 212.17

“The Texas Legislature d set the tax a unt of our local taxes. Your property tax burden is decided byyour locally elected officia an inquiries c erning your taxes should be directed to those officials.” Theappraisal district only dete ines alue of t roperty. If taxing unit budgets increase then a tax rate higherthan the effective rate may adopt the taxing unit. The governing body of each taxing unit decides whetheror not taxes on property w creaTruth-in-Taxati ws give taxp er oice in ecisions that affect their property tax rates. Beginning in early August, taxingunits take th ep toward ng a tax rate by calculating and publishing the effective and rollback tax rates. If agovernin dy proposes to adop tax rate that exceeds the effective rate, it must publish a quarter-page notice in a localnewspa to announce two pub earings. The hearings give taxpayers an opportunity to voice their opinions about thepropose x incre Informat g un ntac , exemptions and tax rates is available on the appraisal district website at:http://www. aviscad.org nfo.html

raisal Information Last Year - 2016 Proposed - 2017Market Value of B er Structures 159,478 178,011Market Value of Non Ag/Timber Land 30,000 30,000Market Value of Ag/Timber Land 0 0Market Value of Personal Property/Minerals 0 0Total Market Value 189,478 208,011Productivity Value of Ag/Timber Land 0 0Assessed Value 189,478 208,011Homestead Cap Value excluding Non-Homesite Value (i.e. Ag, Commercial) 189,478 208,011Exemptions (DV - Disabled Vet; DP-Disabled Person; HS-Homestead; OV65-Over 65)

The difference between the 2012 appraised value and the 2017 appraised value is 84.66%. This percentage information is required by Tax Code section 25.19(b-1).

If you have any questions or need more information, please contact the appraisal district at (512) 834-9138.

SAMPLEEXHIBIT B

12 of 4

40

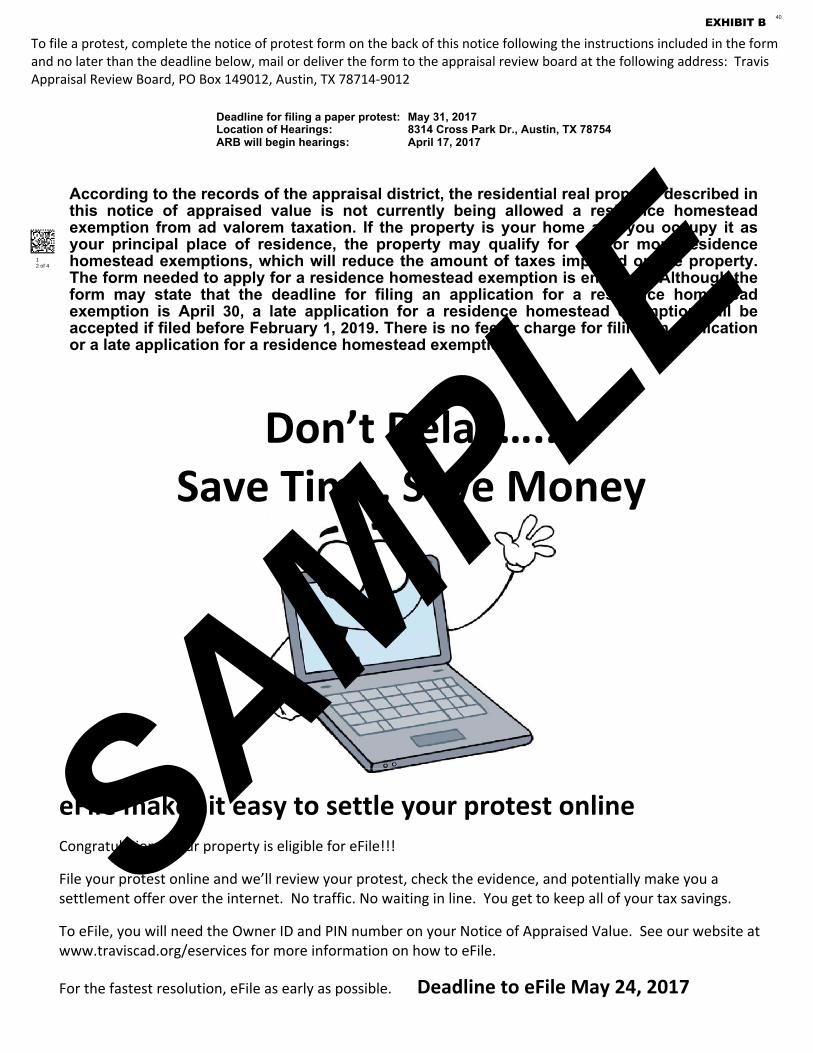

To file a protest, complete the notice of protest form on the back of this notice following the instructions included in the formand no later than the deadline below, mail or deliver the form to the appraisal review board at the following address: TravisAppraisal Review Board, PO Box 149012, Austin, TX 78714-9012

Deadline for filing a paper protest: May 31, 2017Location of Hearings: 8314 Cross Park Dr., Austin, TX 78754ARB will begin hearings: April 17, 2017

According to the records of the appraisal district, the residential real prop described inthis notice of appraised value is not currently being allowed a resi nce homesteadexemption from ad valorem taxation. If the property is your home a you oc upy it asyour principal place of residence, the property may qualify for o or mor esidencehomestead exemptions, which will reduce the amount of taxes imp d on e property.The form needed to apply for a residence homestead exemption is en Although theform may state that the deadline for filing an application for a res nce hom eadexemption is April 30, a late application for a residence homestead e mption ill beaccepted if filed before February 1, 2019. There is no fee r charge for filin n licationor a late application for a residence homestead exemptio

Don’t Dela …..Save Time, S ve Money

eFile make it easy to settle your protest onlineCongratul ion ur property is eligible for eFile!!!

File your protest online and we’ll review your protest, check the evidence, and potentially make you asettlement offer over the internet. No traffic. No waiting in line. You get to keep all of your tax savings.

To eFile, you will need the Owner ID and PIN number on your Notice of Appraised Value. See our website atwww.traviscad.org/eservices for more information on how to eFile.

For the fastest resolution, eFile as early as possible. Deadline to eFile May 24, 2017

SAMPLEEXHIBIT B

Appraisal district name Phone (Area code and number)

Address

This document must be filed with the appraisal review board (ARB) for the appraisal district that took the action(s) you want to protest. It must not be filed with the office of the Texas Comptroller of Public Accounts. GENERAL INSTRUCTIONS: Pursuant to Tax Code Section 41.41, a property owner has the right to protest certain actions taken by the appraisal district. This form is for use by a property owner or designated agent who would like the ARB to hear and decide a protest. If you are leasing the property, you are subject to the limitations set forth in Tax Code Section 41.413. FILING DEADLINES: The usual deadline for filing your notice is midnight, May 31. A different deadline will apply to you if: * your notice of appraised value was delivered after May 2; * your protest concerns a change in he use of agricultural, open-space or timber land; * the ARB made a change to the appraisal records that adversely affects you and you received notice o ange; * the appraisal district or the ARB was required by law to send you notice about a property and did n * in certain limited circumstances, you had good cause for missing the May 31 protest filing deadlin Your specific protest filing deadline is printed on the appraisal notice. ASSISTANCE: The Comptroller's office may not advise a property owner, a property owner's agent, or the chief appraiser or employe n appraisal district on a matter that the Comptroller's office knows is the subject of a protest to the ARB.

STEP 1: Owner's or lessee's name and address

Owner's or lessee's full name

Owner's or lessee's current mailing address (number & street, city, town or post offi , zip code)

Daytime Phone (area code and number) Evening Phone (area code and num Mobile Phone area code & number)

STEP 2: Describe property under protest

Give street address and city if different from above, or legal descrip dress

Appraisal district account number (optional)

Mobile homes: (Give make, model and identific ber)

To preserve your right to present each reason for your protest to the ARB ac ng w, be sure ct all boxes that apply. For example, if you select the first box indica ing an incorrect appraised (market) va or y operty, you esenting that the value is incorrect-usually hat the value should be lowered. If you also want to protest that your property is not appraised at the ame level as a sen sample of ble properties appropriately adjusted for condition, size, location and o her factors, you must also select the box indicating he value is unequ pared with o rope Your prope be appraised at its market value, but be unequally appraised. Failure to select the box that corresponds to each reason for yo ay result i inab protest an e that you want to pursue.

STEP 3: Check reason(s) for your protest

Incorrect appraised et) Exemption was denied, modified or cancelled.

Value is unequal compa th oth e Change in use of land appraised as ag-use, open-space, or timber land.

hould not be taxed _______ ____________ Ag-use, open-space or other special appraisal was denied, of taxing unit) modified or cancelled.

to se ed notice. ___ __________________ Owner's name is incorrect. (type)

O _____ _________________________ Property description is incorrect.

Inco sed or market value of land under special Property should not be taxed in this appraisal district or in one or appra ag-use, open-space or other special appraisal. more taxing units.

STEP 4: Give facts that may resolve your case (continue on additional page if needed) What do you think your property's value is? (Optional) $_____________________________________________________

STEP 5: Check to receive ARB hearing procedures

I would like a copy of the CAD evidence packet.

Yes No

STEP 6: Sign the protest

print Date here > Print Name sign here > Signature

8314 CROSS PARK DR, P O BOX 149012 AUSTIN, TX 78714-9012 www.traviscad.org

TRAVIS CENTRAL APPRAISAL DISTRICT

_________________________ Tax Year(s)

May 31, 2017

State the Year(s) for which you are protesting:

(512) 834-9138 or (512) 836-3328 TDD

PROPERTY APPRAISAL - NOTICE OF PROTEST - 2017

Pr erty ID: R 2:

BfY:DwZwqu wYBww:duJVe:fdeJJu:eUJVwYFUKJEu:e;KBeYFYKDfYFeUJVeYFYKCFYKDU:FdSAMPLEEXHIBIT B

00 4 73 0 52 5

652451 of 2

134893

Property ID:

2017 Notice of Appraised ValueProperty ID: Ownership %: 100.00Ref ID2:DBA:Legal:

Legal Acres: 0.062Situs: Owner ID: EFile PIN:

THIS IS NOT A BILL

DATE OF NOTICE: April 1, 2017

TRAVIS CENTRAL APPRAISAL DISTRICT8314 CROSS PARK DRP O BOX 149012AUSTIN, TX 78714-9012Phone: (512) 834-9138

#BWNNRFT#N117827301930108#

Dear Property Owner,We have appraised the property listed above for the tax year 2017. As of January 1, our app aisal is outlined below.

Market Value Asse d Value(Includes Homestead tation if Applicab

225,328 225,3

Taxing Unit 2016Exempt

2016Exemption

Amount

2017Exempt

2017Exemp

Amo

ExempAmouChan

20Taxa

017Taxable

Freeze Yearand Ceiling

AUSTIN ISD 0 196,5 8 225,328 CITY OF AUSTIN 0 196,568 225,328 TRAVIS COUNTY 0 196,568 225,328 TRAVIS COUNTY HEALTHCARE 0 0 196,568 225,328 AUSTIN COMM COLL DIST 0 0 196,568 225,328

If you qualified your home for a 65 and older or disabled person exemption for school taxes, the school taxes on that home cannot increase as long as youown and live in that home. The tax ceiling is the amount that you pay in the year that you qualified for the 65 and older or disabled person exemption. Theschool taxes on your home may not go above the amount of the ceiling, unless you improve the home (other than normal repairs and maintenance). If youimproved your property (by adding rooms or buildings) or you are transferring a freeze percentage, your school, county, city, or junior college Ceiling mayincrease from prior years. Enclosed are copies of the following documents published by the Texas Comptroller of Public Accounts: (1) Property Tax Remedies; and (2) notice of protest.

65245 1 AV 0.373******AUTO**5-DIGIT 78719 5DGS 2 FT 214

SAMPLEEXHIBIT C

The chart below is the 2016 Taxpayer Impact Statement based on the Effective, Rollback and Adopted tax rates setby each taxing unit.

Effective Tax Rate- A calculated rate that would provide the taxing unit with approximately the same amount of revenue it received in the previous year onproperties taxed in both years. This rate calculation does not include the impact of additional tax revenue resulting from new construction.

Rollback Tax Rate- Tax rate level that allows the taxing jurisdiction to collect 8% more taxes, not including debt repayment, than the previous year. This isthe maximum tax increase allowed by law without triggering an election to “rollback” the taxes.

Adopted Tax Rate- This is the tax rate that was adopted by the taxing unit for 2016.

2016 Taxpayer Impact Statement

Taxing Unit2016

TaxableValue

2016Effective

Rate

2016Effective Taxes

2016Rollback

Rate

2016Rollback

Taxes

16doptedRate

2016Adopted

(Actual) TaxesAUSTIN ISD 196,568 0.962400 1,891.77 1.192000 2 9 1.19200 2,343.09CITY OF AUSTIN 196,568 0.411200 808.29 0.441800 .44 0.44 868.44TRAVIS COUNTY 196,568 0.374700 736.54 0.399800 88 0 3 0 754.43TRAVIS COUNTY HEALTHCARE 196,568 0.105832 208.03 0.114213 541 217.29AUSTIN COMM COLL DIST 196,568 0.091000 178.88 0.088000 1 02000 200.50

*The impact statement does not reflect OV65 tax ceiling, see previous page for tax ceiling amount

The chart below is an estimate of taxes based on 2017 taxa value d the ado d tax rate. This is NOTthe 2017 effective tax rate. If property values rise, the ef ive rate l go do ice versa.

Taxing Unit 20Taxable

2016opted Tax Rate

Estimate(See below)

AUSTIN ISD 32 1.192000 2,685.91CITY OF AUSTIN 2 0.441800 995.50TRAVIS COUNTY 22 0.383800 864.81TRAVIS COUNTY HEALTHCARE 225 0.110541 249.08AUSTIN COMM COLL DIST 225,3 0.102000 229.84

“The Texas Legislature d set the tax a unt of our local taxes. Your property tax burden is decided byyour locally elected officia an inquiries c erning your taxes should be directed to those officials.” Theappraisal district only dete ines alue of t roperty. If taxing unit budgets increase then a tax rate higherthan the effective rate may adopt the taxing unit. The governing body of each taxing unit decides whetheror not taxes on property w creaTruth-in-Taxati ws give taxp er oice in ecisions that affect their property tax rates. Beginning in early August, taxingunits take th ep toward ng a tax rate by calculating and publishing the effective and rollback tax rates. If agovernin dy proposes to adop tax rate that exceeds the effective rate, it must publish a quarter-page notice in a localnewspa to announce two pub earings. The hearings give taxpayers an opportunity to voice their opinions about thepropose x incre Informat g un ntac , exemptions and tax rates is available on the appraisal district website at:http://www. aviscad.org nfo.html

raisal Information Last Year - 2016 Proposed - 2017Market Value of B er Structures 106,568 95,328Market Value of Non Ag/Timber Land 90,000 130,000Market Value of Ag/Timber Land 0 0Market Value of Personal Property/Minerals 0 0Total Market Value 196,568 225,328Productivity Value of Ag/Timber Land 0 0Assessed Value 196,568 225,328Homestead Cap Value excluding Non-Homesite Value (i.e. Ag, Commercial) 90,000 130,000Exemptions (DV - Disabled Vet; DP-Disabled Person; HS-Homestead; OV65-Over 65)

The difference between the 2012 appraised value and the 2017 appraised value is 141.58%. This percentage information is required by Tax Code section 25.19(b-1).

If you have any questions or need more information, please contact the appraisal district at (512) 834-9138.

SAMPLEEXHIBIT C

652452 of 2

134894

To file a protest, complete the notice of protest form on the back of this notice following the instructions included in the formand no later than the deadline below, mail or deliver the form to the appraisal review board at the following address: TravisAppraisal Review Board, PO Box 149012, Austin, TX 78714-9012

Deadline for filing a paper protest: May 31, 2017Location of Hearings: 8314 Cross Park Dr., Austin, TX 78754ARB will begin hearings: April 17, 2017

Don’t Dela …..Save Time, S ve Money

eFile make it easy to settle your protest onlineCongratul ion ur property is eligible for eFile!!!

File your protest online and we’ll review your protest, check the evidence, and potentially make you asettlement offer over the internet. No traffic. No waiting in line. You get to keep all of your tax savings.

To eFile, you will need the Owner ID and PIN number on your Notice of Appraised Value. See our website atwww.traviscad.org/eservices for more information on how to eFile.

For the fastest resolution, eFile as early as possible. Deadline to eFile May 24, 2017

SAMPLEEXHIBIT C

Appraisal district name Phone (Area code and number)

Address

This document must be filed with the appraisal review board (ARB) for the appraisal district that took the action(s) you want to protest. It must not be filed with the office of the Texas Comptroller of Public Accounts. GENERAL INSTRUCTIONS: Pursuant to Tax Code Section 41.41, a property owner has the right to protest certain actions taken by the appraisal district. This form is for use by a property owner or designated agent who would like the ARB to hear and decide a protest. If you are leasing the property, you are subject to the limitations set forth in Tax Code Section 41.413. FILING DEADLINES: The usual deadline for filing your notice is midnight, May 31. A different deadline will apply to you if: * your notice of appraised value was delivered after May 2; * your protest concerns a change in he use of agricultural, open-space or timber land; * the ARB made a change to the appraisal records that adversely affects you and you received notice o ange; * the appraisal district or the ARB was required by law to send you notice about a property and did n * in certain limited circumstances, you had good cause for missing the May 31 protest filing deadlin Your specific protest filing deadline is printed on the appraisal notice. ASSISTANCE: The Comptroller's office may not advise a property owner, a property owner's agent, or the chief appraiser or employe n appraisal district on a matter that the Comptroller's office knows is the subject of a protest to the ARB.

STEP 1: Owner's or lessee's name and address

Owner's or lessee's full name

Owner's or lessee's current mailing address (number & street, city, town or post offi , zip code)

Daytime Phone (area code and number) Evening Phone (area code and num Mobile Phone area code & number)

STEP 2: Describe property under protest

Give street address and city if different from above, or legal descrip dress

Appraisal district account number (optional)

Mobile homes: (Give make, model and identific ber)

To preserve your right to present each reason for your protest to the ARB ac ng w, be sure ct all boxes that apply. For example, if you select the first box indica ing an incorrect appraised (market) va or y operty, you esenting that the value is incorrect-usually hat the value should be lowered. If you also want to protest that your property is not appraised at the ame level as a sen sample of ble properties appropriately adjusted for condition, size, location and o her factors, you must also select the box indicating he value is unequ pared with o rope Your prope be appraised at its market value, but be unequally appraised. Failure to select the box that corresponds to each reason for yo ay result i inab protest an e that you want to pursue.

STEP 3: Check reason(s) for your protest

Incorrect appraised et) Exemption was denied, modified or cancelled.

Value is unequal compa th oth e Change in use of land appraised as ag-use, open-space, or timber land.

hould not be taxed _______ ____________ Ag-use, open-space or other special appraisal was denied, of taxing unit) modified or cancelled.

to se ed notice. ___ __________________ Owner's name is incorrect. (type)

O _____ _________________________ Property description is incorrect.

Inco sed or market value of land under special Property should not be taxed in this appraisal district or in one or appra ag-use, open-space or other special appraisal. more taxing units.

STEP 4: Give facts that may resolve your case (continue on additional page if needed) What do you think your property's value is? (Optional) $_____________________________________________________

STEP 5: Check to receive ARB hearing procedures

I would like a copy of the CAD evidence packet.

Yes No

STEP 6: Sign the protest

print Date here > Print Name sign here > Signature

8314 CROSS PARK DR, P O BOX 149012 AUSTIN, TX 78714-9012 www.traviscad.org

TRAVIS CENTRAL APPRAISAL DISTRICT

_________________________ Tax Year(s)

May 31, 2017

State the Year(s) for which you are protesting:

(512) 834-9138 or (512) 836-3328 TDD

PROPERTY APPRAISAL - NOTICE OF PROTEST - 2017

Pr erty ID: R 2:

BfY:DwZwqu wYBww:duJVe:fduFFwUEquBwCJUKJEZFfUZbwBffEBwu:equBwBfVwBfY:DwXSAMPLEEXHIBIT C

00 3 88 0 12 900 3 88 0 12 9

4993

#BWNNRFT#R185774409#

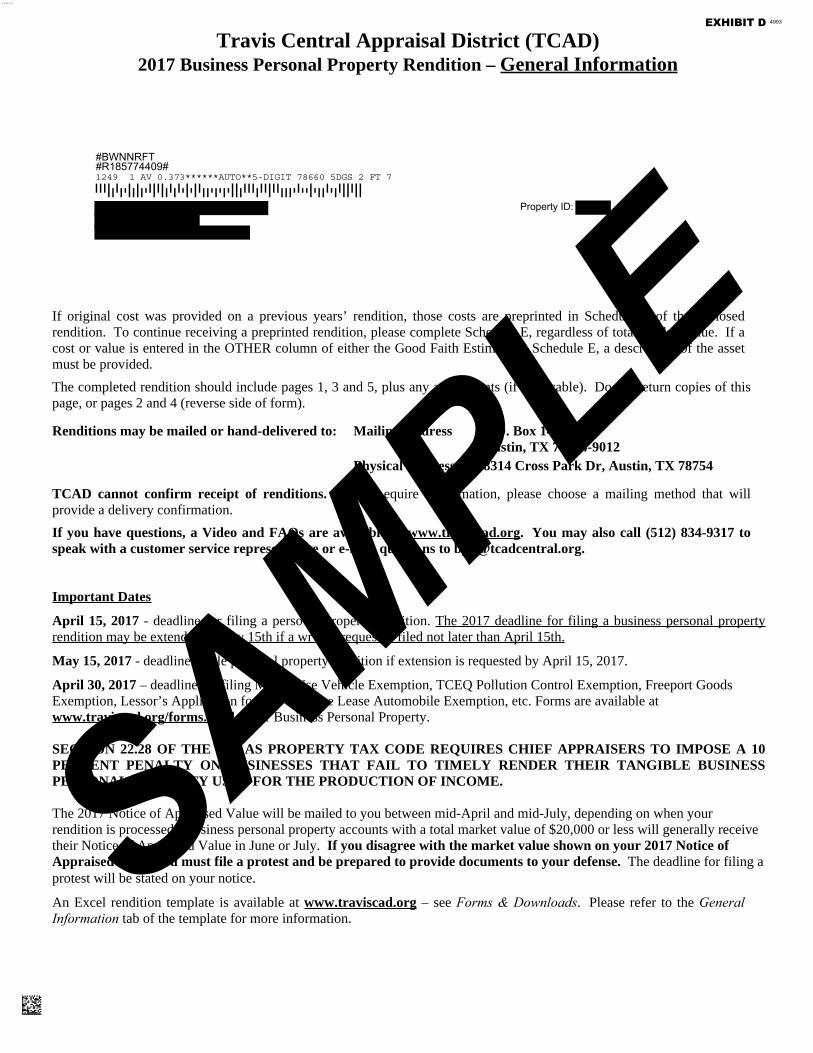

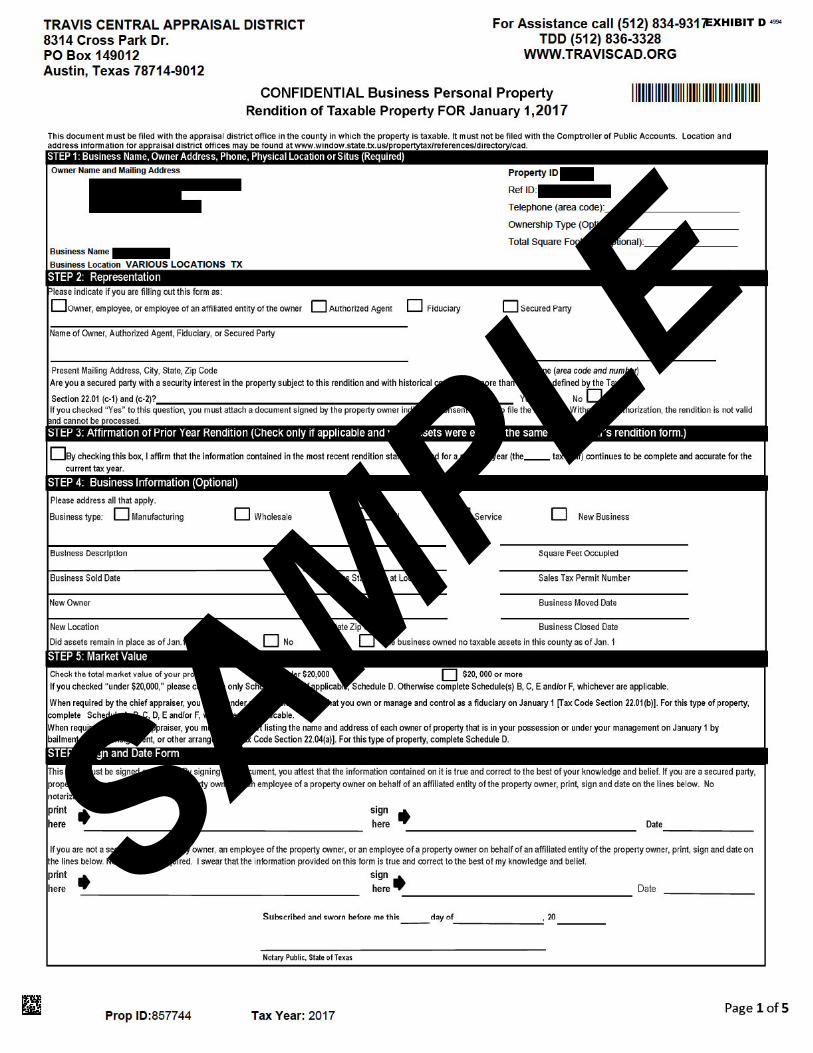

Travis Central Appraisal District (TCAD)2017 Business Personal Property Rendition – General Information

If original cost was provided on a previous years’ rendition, those costs are preprinted in Schedu of th losedrendition. To continue receiving a preprinted rendition, please complete Sche E, regardless of tota k lue. If acost or value is entered in the OTHER column of either the Good Faith Estim Schedule E, a descr of the assetmust be provided.The completed rendition should include pages 1, 3 and 5, plus any a nts (if cable). Do eturn copies of thispage, or pages 2 and 4 (reverse side of form).

Renditions may be mailed or hand-delivered to: Mailin dress O. Box 14ustin, TX 7 4-9012

Physical ess 8314 Cross Park Dr, Austin, TX 78754

TCAD cannot confirm receipt of renditions. equire mation, please choose a mailing method that willprovide a delivery confirmation. If you have questions, a Video and FAQs are av ble www.tr ad.org. You may also call (512) 834-9317 tospeak with a customer service represe ve or e-m qu ns to bp @tcadcentral.org.

Important Dates

April 15, 2017 - deadline f r filing a perso roper ition. The 2017 deadline for filing a business personal propertyrendition may be extend y 15th if a wr reques filed not later than April 15th.

May 15, 2017 - deadline le p l property ition if extension is requested by April 15, 2017.

April 30, 2017 – deadline filing M Use Vehicle Exemption, TCEQ Pollution Control Exemption, Freeport GoodsExemption, Lessor’s Appli on fo e Lease Automobile Exemption, etc. Forms are available atwww.travi d org/forms. ml r Busin ss Personal Property.

SEC ON 22.28 OF THE AS PROPERTY TAX CODE REQUIRES CHIEF APPRAISERS TO IMPOSE A 10PE ENT PENALTY ON USINESSES THAT FAIL TO TIMELY RENDER THEIR TANGIBLE BUSINESSPE ONAL TY US FOR THE PRODUCTION OF INCOME.

The 2017 Notice of Ap sed Value will be mailed to you between mid-April and mid-July, depending on when yourrendition is processed siness personal property accounts with a total market value of $20,000 or less will generally receivetheir Notice f Ap d Value in June or July. If you disagree with the market value shown on your 2017 Notice ofAppraised u must file a protest and be prepared to provide documents to your defense. The deadline for filing aprotest will be stated on your notice.

An Excel rendition template is available at www.traviscad.org – see Forms & Downloads. Please refer to the GeneralInformation tab of the template for more information.

Property ID:

1249 1 AV 0.373******AUTO**5-DIGIT 78660 5DGS 2 FT 7

SAMPLEEXHIBIT D

SAMPLEEXHIBIT D

SAMPLEEXHIBIT D

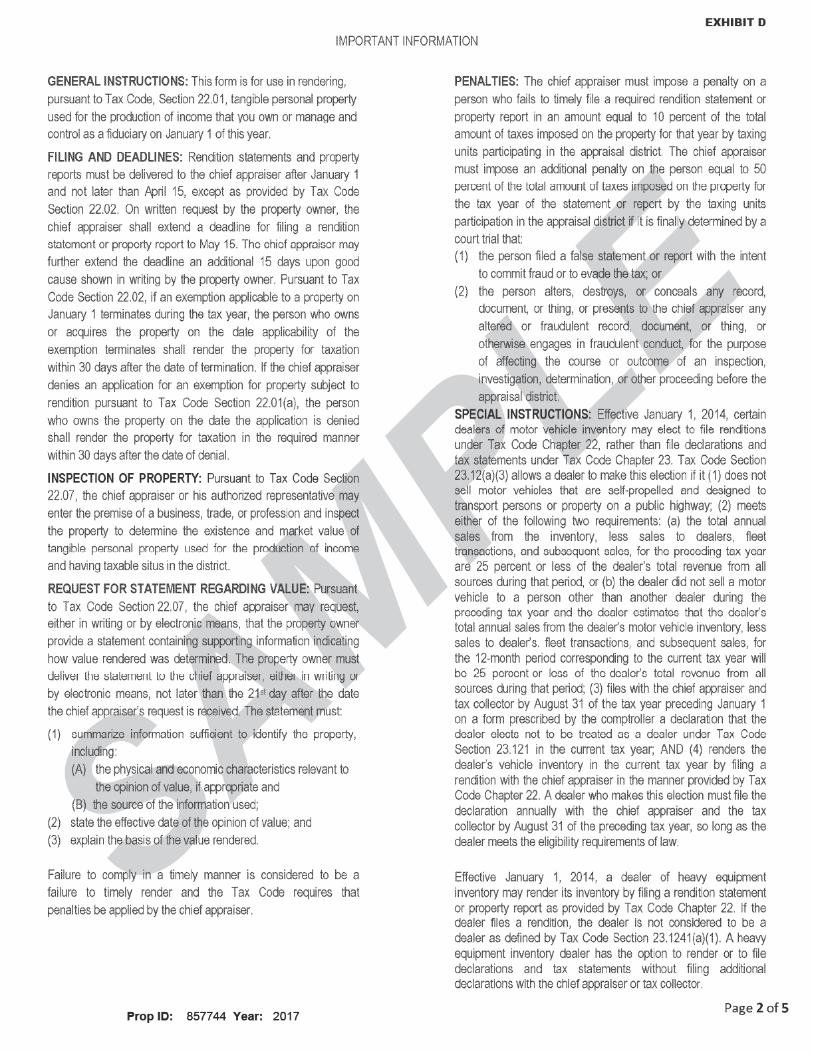

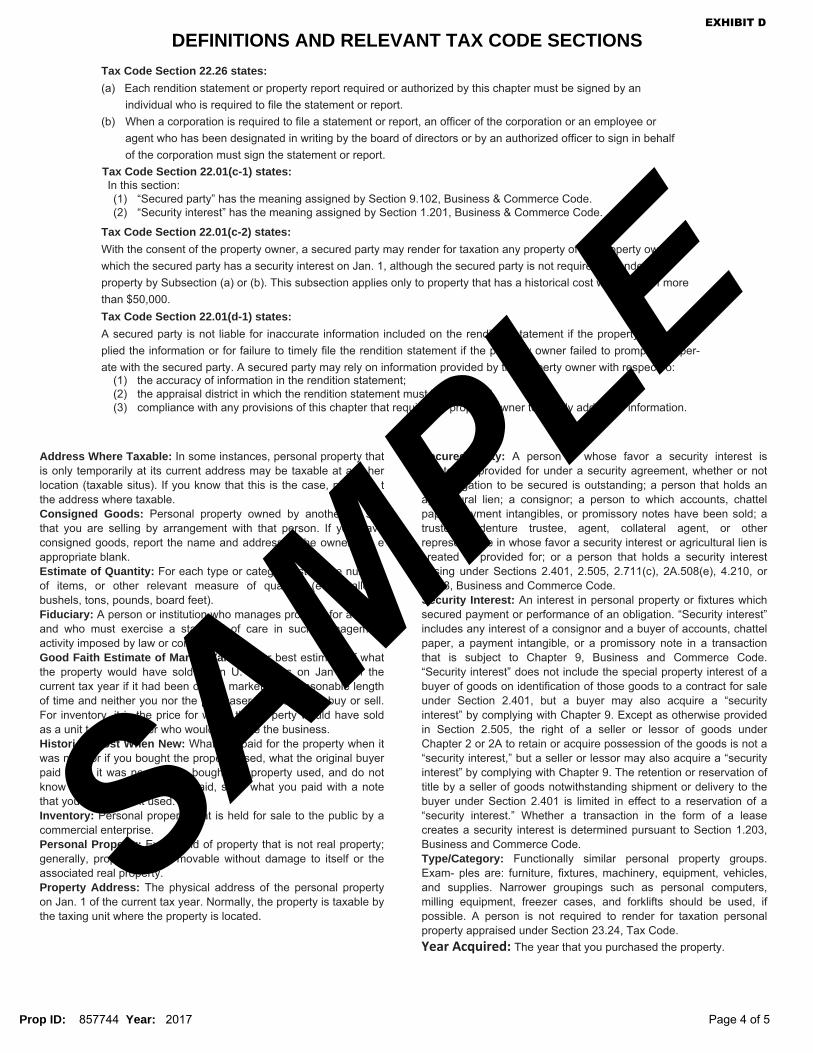

DEFINITIONS AND RELEVANT TAX CODE SECTIONSTax Code Section 22.26 states:(a) Each rendition statement or property report required or authorized by this chapter must be signed by an

individual who is required to file the statement or report.(b) When a corporation is required to file a statement or report, an officer of the corporation or an employee or

agent who has been designated in writing by the board of directors or by an authorized officer to sign in behalf of the corporation must sign the statement or report.

Tax Code Section 22.01(c-1) states: In this section:

(1) “Secured party” has the meaning assigned by Section 9.102, Business & Commerce Code.(2) “Security interest” has the meaning assigned by Section 1.201, Business & Commerce Code.

Tax Code Section 22.01(c-2) states:With the consent of the property owner, a secured party may render for taxation any property of operty ow which the secured party has a security interest on Jan. 1, although the secured party is not require nde property by Subsection (a) or (b). This subsection applies only to property that has a historical cost w f morethan $50,000.Tax Code Section 22.01(d-1) states:A secured party is not liable for inaccurate information included on the rendi tatement if the property eplied the information or for failure to timely file the rendition statement if the p y owner failed to promp per-ate with the secured party. A secured party may rely on information provided by th perty owner with respec o:

(1) the accuracy of information in the rendition statement;(2) the appraisal district in which the rendition statement must b d(3) compliance with any provisions of this chapter that requi prop wner to ly addi information.

ecured ty: A person whose favor a security interest iste provided for under a security agreement, whether or not

gation to be secured is outstanding; a person that holds anag ural lien; a consignor; a person to which accounts, chattelpap yment intangibles, or promissory notes have been sold; atruste denture trustee, agent, collateral agent, or otherreprese e in whose favor a security interest or agricultural lien isreated provided for; or a person that holds a security interest

sing under Sections 2.401, 2.505, 2.711(c), 2A.508(e), 4.210, or8, Business and Commerce Code.

Security Interest: An interest in personal property or fixtures whichsecured payment or performance of an obligation. “Security interest”includes any interest of a consignor and a buyer of accounts, chattelpaper, a payment intangible, or a promissory note in a transactionthat is subject to Chapter 9, Business and Commerce Code.“Security interest” does not include the special property interest of abuyer of goods on identification of those goods to a contract for saleunder Section 2.401, but a buyer may also acquire a “securityinterest” by complying with Chapter 9. Except as otherwise providedin Section 2.505, the right of a seller or lessor of goods underChapter 2 or 2A to retain or acquire possession of the goods is not a“security interest,” but a seller or lessor may also acquire a “securityinterest” by complying with Chapter 9. The retention or reservation oftitle by a seller of goods notwithstanding shipment or delivery to thebuyer under Section 2.401 is limited in effect to a reservation of a“security interest.” Whether a transaction in the form of a leasecreates a security interest is determined pursuant to Section 1.203,Business and Commerce Code.Type/Category: Functionally similar personal property groups.Exam- ples are: furniture, fixtures, machinery, equipment, vehicles,and supplies. Narrower groupings such as personal computers,milling equipment, freezer cases, and forklifts should be used, ifpossible. A person is not required to render for taxation personalproperty appraised under Section 23.24, Tax Code.Year Acquired: The year that you purchased the property.

Address Where Taxable: In some instances, personal property thatis only temporarily at its current address may be taxable at a herlocation (taxable situs). If you know that this is the case, pl tthe address where taxable.Consigned Goods: Personal property owned by another sthat you are selling by arrangement with that person. If yo aveconsigned goods, report the name and address he owner eappropriate blank.Estimate of Quantity: For each type or categ ist e numof items, or other relevant measure of qua (e allobushels, tons, pounds, board feet).Fiduciary: A person or institution who manages pro y for aand who must exercise a sta d of care in such nagemactivity imposed by law or conGood Faith Estimate of Mark Val ur best estim f whatthe property would have sold n U. s on Jan f thecurrent tax year if it had been o e market asonable lengthof time and neither you nor the p haser o buy or sell.For inventory it i the price for w th perty w uld have soldas a unit t er who would e the business.Histori ost When New: What paid for the property when itwas n or if you bought the prope sed, what the original buyerpaid it was ne bough property used, and do notknow aid, s what you paid with a notethat you p it used.Inventory: Personal propert at is held for sale to the public by acommercial enterprise.Personal Prope y: Ev nd of property that is not real property;generally, prop movable without damage to itself or theassociated real property.Property Address: The physical address of the personal propertyon Jan. 1 of the current tax year. Normally, the property is taxable bythe taxing unit where the property is located.

Prop ID: 857744 Year: 2017 Page 4 of 5

SAMPLEEXHIBIT D

SAMPLEEXHIBIT D

SAMPLEEXHIBIT D

2 Texas Comptroller of Public Accounts • Property Tax Assistance Division

Property Taxpayer Remedies

You can appear at the ARB hearing in person, by affidavit or through an agent. If you fail to appear, you may lose the right to be heard by the ARB on the protest and the right to appeal. If you or your agent fails to appear at a hearing, you are entitled to a new hearing if you file with the ARB, not later than four days after your hearing date, a written statement showing good cause for failing to appear and request a new hearing. Good cause is defined as a reason that includes an error or mistake that was not intentional or was not the result of conscious indifference and will not cause undue delay or injury to the person authorized to extend the deadline or grant a rescheduling.

-

-

-