Embed Size (px)

Citation preview

Treasury Management in the Nonprofit World : Best Practices from

Christian Children’s Fund

John Zietlow, D.B.A., CCMProf. of Finance, Lee University

William J. Hopkins, CCM

Treasurer, Christian Children’s Fund, Inc.

Copyright 2002 John Zietlow. Portions Copyright William Hopkins, 2002.

Today’s Agenda

Let’s decide on the primary financial objective(s)

Let’s think about how cash flow patterns differ in the nonprofit arena

Let’s determine how you can make a difference to a nonprofit

Let’s hear from some financial institutions about areas for improvement

Your Turn Now: What is the Primary Financial Objective of a Charity?

Can you arrive at a consensus at your table about this? First, each of you write down what you think the objective is. Then, discuss it with others at your table. Appoint a spokesperson.

Now, what do nonprofit managers say is their financial objective?

Many say “financial break-even” – revenues should cover costs

Some say maximizing revenue, reducing risk, or increasing funds raised

Christian Children’s Fund, Inc.

Cost Effectiveness Financial Accountability Maximization and Protection of Cash Flows Maintaining Liquidity that ensures the

future of the organization.

And academics say…

Richard Wacht: “purely financial decisions” to be driven by “cost minimization, subject to the absolute constraint of maintaining organizational liquidity and solvency over time”

My view: strive to meet an “approximate liquidity target” over time (cash flow and cash position management are keys)

Main Defining Characteristics:Nonprofit Treasury Management

Liquidity management (just documented) Organizational size and structure Main source of revenue Importance of cash and cash flow

management

CHRISTIAN CHILDREN'S FUND, INC.Global Cash Management

June 2002

$23 million $18 million REVENUE $28 million $86 million

100,000 Eight Contributions 300,000International International Source Country London Grants U.S.

Sponsors Affiliates Currency 5 accounts Other Sponsors5 currencies

EXPENSES BANKS

International 2 banks InternationalOffice 8 accounts Office

$28 million Richmond

National & 34 banks 23 National 6 Regional 7 Fund 4 GrantOther Offices 84 accounts Offices Offices Raising Centers$14 million 21 currencies Offices

Program 719 banksExpenses 1137 accounts Projects Projects Projects Projects$92 million 21 currencies

Operating CashFiscal Years 2001 and 2002

($2,000,000.00)

($1,000,000.00)

$0.00

$1,000,000.00

$2,000,000.00

$3,000,000.00

$4,000,000.00

$5,000,000.00

$6,000,000.00

$7,000,000.00

$8,000,000.007/

1/00

8/1/

00

9/1/

00

10/1

/00

11/1

/00

12/1

/00

1/1/

01

2/1/

01

3/1/

01

4/1/

01

5/1/

01

6/1/

01

7/1/

01

8/1/

01

9/1/

01

10/1

/01

11/1

/01

12/1

/01

1/1/

02

2/1/

02

3/1/

02

4/1/

02

5/1/

02

6/1/

02

Operating Account Ledger Balance Overnight Investments

Christian Children's Fund, Inc.Total Cash

End of Fiscal Year 1994 through 2002

$0

$2,000,000

$4,000,000

$6,000,000

$8,000,000

$10,000,000

$12,000,000

$14,000,000

FY '95 FY '96 FY '97 FY '98 FY '99 FY '00 FY '01 FY '02

Cash in Offices Abroad

In Transit Cash

Operating Cash

Project Cash

$5,000,000.00

$5,500,000.00

$6,000,000.00

$6,500,000.00

$7,000,000.00

$7,500,000.00

$8,000,000.00

$8,500,000.00

$9,000,000.00

$9,500,000.00

May-01 Jun-01 Jul-01 Aug-01 Sep-01 Oct-01 Nov-01 Dec-01 Jan-02 Feb-02 Mar-02 Apr-02 May-02 Jun-02

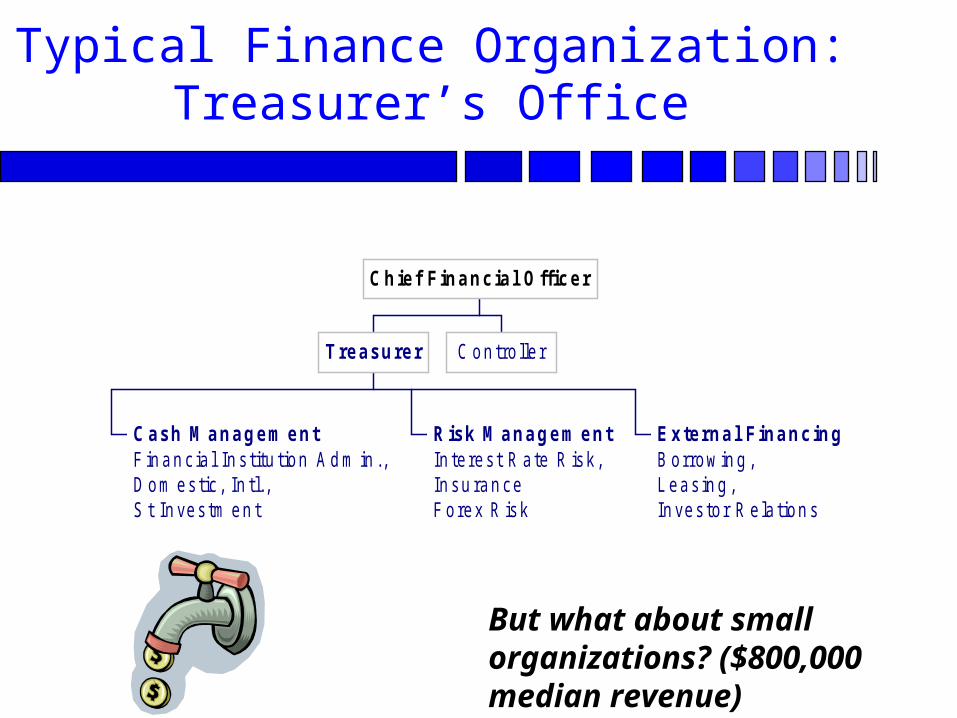

Typical Finance Organization:Treasurer’s Office

Cash M anagem entF in an c ia l In s titu t ion A d m in .,D om es tic , In tl. ,S t In ves tm en t

Risk M anagem entIn te res t R a te R isk ,In su ran ceF orex R isk

External FinancingB orrow in g ,L eas in g ,In ves to r R e la tion s

T reasurer C on tro lle r

Chief Financial Officer

But what about small organizations? ($800,000 median revenue)

Typical Finance Organization:Controller’s Office

Treasu rer

AccountingG en era l L ed g er,R ep orts ,Taxes

Auditing Budgeting& FinancialReporting

Credit& Accounts Receivable

Disbursem entsA ccou n ts P ayab leP ayro ll

Controller

Chief Financial Officer

DIRECTOR, FOUNDATION FINANCIAL MANAGEMENT

Position: Acting as the chief accounting officer for the University of Maryland College Park Foundation, the Director is responsible for all accounting functions of a rapidly growing organization. Supervising a staff of two, you will determine the appropriate delegation of duties, insure that all accounts are reconciled in a timely manner, approve journal entries, operate a computerized fund accounting system and produce financial statements for fund holders and external constituents. You will coordinate the annual audit process and prepare the F.A.S.B. conforming financials. Working with other staff members, you will insure the proper recording of receipts and disbursements and help to determine internal control policies.

What are the main sources of revenue for charities?

Why is this important?

N onprofi t O rga ni za tions a s Ca sh F low System s

Cash D isbursedto Cl ient/Benefi ciary

N o Transfo rm ation(P ure D is tribution)

S ervice or P roduct P rovidedto Cl ient/Benefi ciary

T ransfo rm ation(Service or P roduct P rovision)

N onprofi t Organiza tionCash M anagem ent

Cash from Gifts and Grants

CONDUITS TRANSFORMERS

“THE BIG FIVE” Areas for Treasury Improvement

Cash forecasting Positive pay and other fraud prevention Sweep accounts, Segregated ST

Investments Portfolios More liquidity! Harness the Internet

How Can I Assist a Nonprofit?

Go to work for one! Serve on a board

Donate Sponsor an intern

at a local nonprofit (Lenders) Understand their world

In Conclusion…