Embed Size (px)

Citation preview

Treaty Series

Treaties and international agreementsregistered

or filed and recordedwith the Secretariat of the United Nations

Recueil des Traitis

Traitis et accords internationaux

enregistrisou classds et inscrits au re'pertoire

au Secrdtariat de l'Organisation des Nations Unies

Copyright © United Nations 2001All rights reserved

Manufactured in the United States of America

Copyright © Nations Unies 2001Tous droits rdserv6s

Imprim6 aux Etats-Unis d'Amdrique

Treaty Series

Treaties and international agreementsregistered

or filed and recordedwith the Secretariat of the United Nations

VOLUME 1920

Recueil des Traitis

Traitis et accords internationaux

enregistrisou classes et inscrits au ripertoire

au Secritariat de I'Organisation des Nations Unies

United Nations * Nations UniesNew York, 2001

Treaties and international agreementsregistered or filed and recorded

with the Secretariat of the United Nations

VOLUME 1920 1996 1. No. 1149H. No. 1149

TABLE OF CONTENTS

I

Treaties and international agreements

registered from 8 April 1996 to 26 April 1996

Page

No. 32783. Denmark and United Kingdom of Great Britain and NorthernIreland:

Memorandum of understanding regarding the billing and collection by the UnitedKingdom of air navigation charges levied by Denmark. Signed at London on2 December 1982

Exchange of notes constituting an agreement amending to the above-mentionedMemorandum of understanding. Copenhagen, 14 June 1993 and 1 March 1994 ... 3

No. 32784. Denmark and Estonia, Finland, Germany, Latvia, Lithuania,Norway, Poland, Russian Federation, Sweden and Commission ofthe European Communities:

Agreement relating to the Secretariat in Copenhagen of the Commissioner of theCouncil of the Baltic Sea States on Democratic Institutions and HumanRights, including the Rights of Persons belonging to Minorities (with proto-col). Signed at Copenhagen on 2 June 1995 ........................................................... 15

No. 32785. Israel and Romania:Agreement in the field of tourism. Signed at Bucharest on 29 March 1995 .............. 37

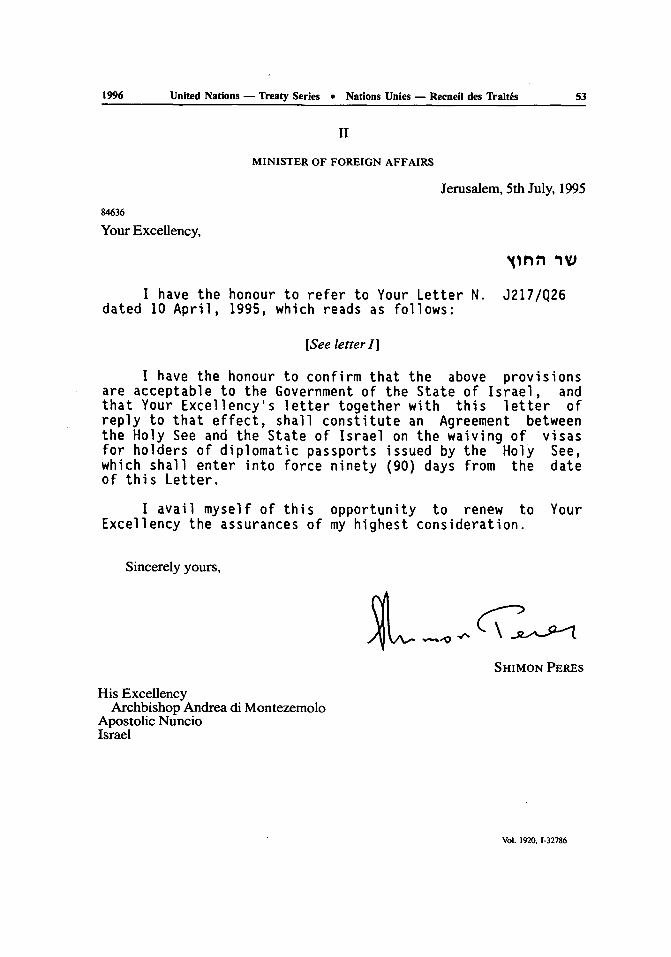

No. 32786. Israel and Holy See:Exchange of letters constituting an agreement on the waiver of the visa require-

ment for holders of diplomatic passports. Tel Aviv, 10 April 1995 and Jerusa-lem , 5 July 1995 .......................................................................................................... 49

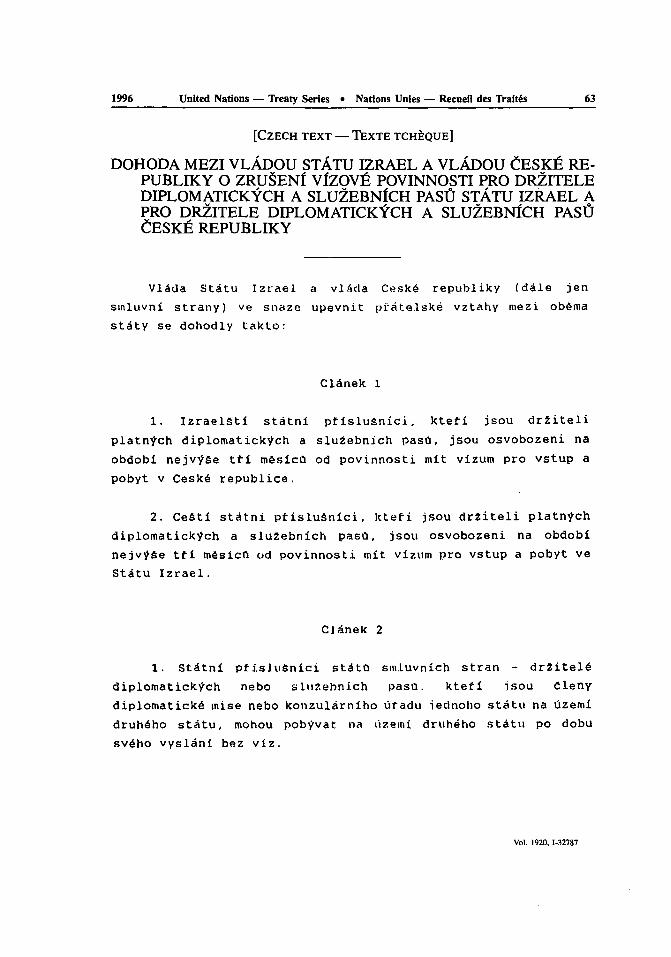

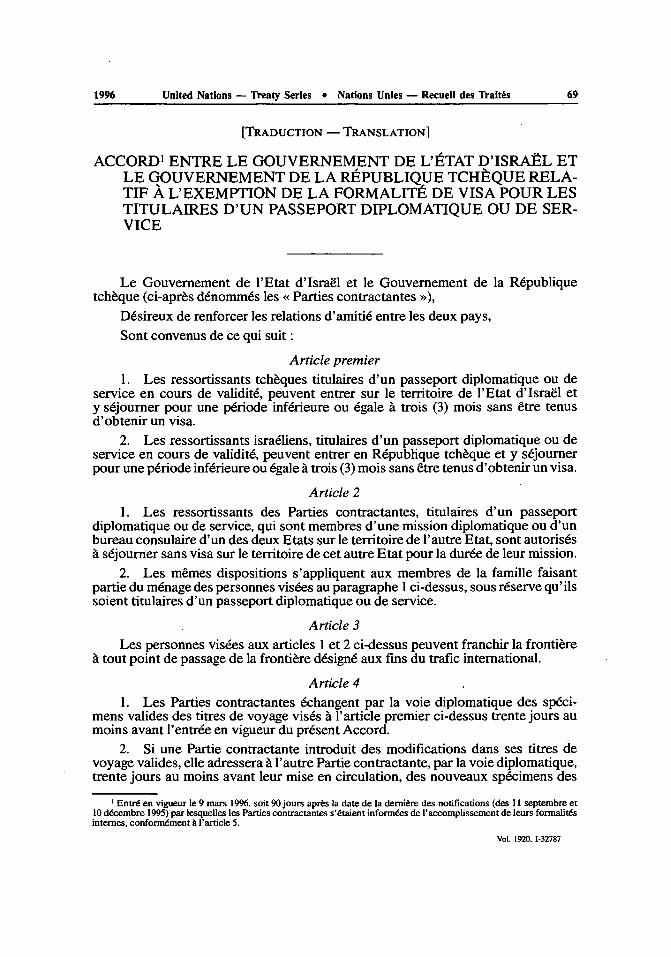

No. 32787. Israel and Czech Republic:Agreement on the waiver of the visa requirement for the holders of diplomatic or

service passports. Signed at Jerusalem on 7 August 1995 ................. 59Vol. 1920

Traitis et accords internationauxenregistris ou classis et inscrits au re'pertoire

au Secritariat de l'Organisation des Nations Unies

VOLUME 1920 1996 1. N s 32783-32822II. NO 1149

TABLE DES MATIERES

I

Traitds et accords internationaux

enregistris du 8 avril 1996 au 26 avril 1996

Pages

NO 32783. Danemark et Royaume-Uni de Grande-Bretagne et d'Irlande duNord:

Mcmorandum d'accord relatif A la facturation et au recouvrement par leRoyaume-Uni de frais de navigation arienne imposs par le Danemark. Sign6A Londres le 2 d6cembre 1982

tchange de notes constituant un accord amendant le M6morandum d'accord sus-mentionn6. Copenhague, 14 juin 1993 et Ier mars 1994 ................... 3

NO 32784. Danemark et Estonie, Finlande, Allemagne, Lettonie, Lituanie,Norv~ge, Pologne, Fid6ration de Russie, Suede et Commission desCommunaut6s europkennes :

Accord relatif au Secrdtariat h Copenhague du Commissaire du Conseil des ltatsde lamer Baltique sur les institutions d6mocratiques et les droits de l'homme,y compris les droits des personnes appartenant A des minorit6s (avec proto-cole). Sign6 A Copenhague le 2 juin 1995 ............................................................... 15

NO 32785. Isra9l et Roumanie :Accord dans le domaine du tourisme. Sign6 A Bucarest le 29 mars 1995 ................. 37

NO 32786. Israel et Saint-Siege :tchange de lettres constituant un accord relatif A 1'exemption de la formalit6 de

visa pour les titulaires d'un passeport diplomatique. Tel-Aviv, 10 avril 1995 etJ rusalem , 5 juilet 1995 ............................................................................................ 49

N0 32787. Israe! et R~publique tchique:Accord relatif A l'exemption de la formalit6 de visa pour les titulaires d'un passe-

port diplomatique ou de service. Signd A Jdrusalem le 7 aoft 1995 .................... 59Vol. 1920

United Nations - Treaty Series * Nations Unies - Recueil des Traitis

Page

No. 32788. United Nations Industrial Development Organization and IslamicRepublic of Iran:

Exchange of letters constituting an agreement concerning the arrangements for thetwelfth session of the UNIDO Leather and Leather Products Industry Panelfrom 27 to 31 August 1995 in Tehran. Vienna, 23 August 1995 ........................... 71

No. 32789. United Nations Industrial Development Organization and Japan:

Exchange of notes constituting an agreement concerning the UNIDO Servicein Japan for the promotion of industrial investment in developing countries(with annexed project document). Vienna, 29 August 1995 ................ 73

No. 32790. United Nations Industrial Development Organization and Bahrain:

Agreement on the establishment of a UNIDO Investment Promotion ServiceOffice in Bahrain (with annexes and exchange of letters of 1 September and19 October 1995). Signed at Manama on 31 October 1995 and at Vienna on7 N ovem ber 1995 ...................................................................................................... . 75

No. 32791. United Nations Industrial Development Organization and China:

Agreement on the establishment of a UNIDO Investment Promotion ServiceOffice for the People's Republic of China in Beijing (with annexes). Signed atVienna on 22 D ecem ber 1995 ................................................................................... 77

No. 32792. International Bank for Reconstruction and Development andChina:

Loan Agreement-Sichuan Power Transmission Project (with schedules and Gen-eral Conditions Applicable to Loan and Guarantee Agreements dated 1 Jan-uary 1985). Signed at Washington on 25 May 1995 .............................................. 79

No. 32793. International Bank for Reconstruction and Development andChina:

Loan Agreement-Inland Waterways Project (with schedules and General Con-ditions Applicable to Loan and Guarantee Agreements for Single CurrencyLoans dated 30 May 1995, and amending letter dated 4 December 1995).Signed at W ashington on 31 August 1995 ............................................................... 81

No. 32794. International Bank for Reconstruction and Development andChina:

Loan Agreement-Ertan II Hydroelectric Project (with schedules and GeneralConditions Applicable to Loan and Guarantee Agreements dated 1 January1985). Signed at Washington on 2 November 1995 ............................................... 83

No. 32795. International Development Association and Benin:Development Credit Agreement-Third Structural Adjustment Credit (with

schedules and General Conditions Applicable to Development Credit Agree-ments dated 1 January 1985). Signed at Washington on 8 June 1995 ................. 85

Vol. 1920

1996 United Nations - Treaty Series * Nations Unies - Recueil des Traitks VII

Pages

NO 32788. Organisation des Nations Unies pour le d6veloppement industriel etR~publique islamique d'Iran :

tchange de lettres constituant un accord relatif aux arrangements en vue de ladeuxi~me session du Groupe de l'industrie du cuir et des produits en cuir deI'ONUDI du 27 au 31 aofit 1995 A Thran. Vienne, 23 aofit 1995 ..................... 71

N0 32789. Organisation des Nations Unies pour le d~veloppement industriel etJapon :

tchange de notes constituant un accord relatif au Service de I'ONUDI au Japonpour la promotion de l'investissement industriel dans les pays en d6veloppe-ment (avec document de projet annex6). Vienne, 29 ao0t 1995 ............. 73

N0 32790. Organisation des Nations Unies pour le d6veloppement industriel etBahrein :

Accord relatif A la creation d'un Bureau de service de I'ONUDI pour la promotionde l'investissement A Bahrein (avec annexes et 6change de lettres des 1er sep-tembre et 19 octobre 1995). Sign6 A Manama le 31 octobre 1995 et A Vienne le7 novem bre 1995 ........................................................................................................ 75

N0 32791. Organisation des Nations Unies pour le dkveloppement industriel etChine :

Accord relatif A la cr6ation d'un Bureau de service de I'ONUDI pour la promotionde l'investissement pour la R4publique populaire de Chine i Beijing (avecannexes). Signd A Vienne le 22 dacembre 1995 ..................................................... 77

NO 32792. Banque internationale pour la reconstruction et le d~veloppement etChine :

Accord de prt - Projet de transport de l'ilectricite de Sichuan (avec annexes etConditions g6n6rales applicables aux accords de pr& et de garantie en date dulerjanvier 1985). Sign6 A Washington le 25 mai 1995 .................... 79

N0 32793. Banque internationale pour la reconstruction et le d6veloppement etChine :

Accord de pr~t - Projet relatif aux voies navigables (avec annexes et Conditionsg6n6rales applicables aux accords de pr~t et de garantie pour les prPts decirculation particuli~re en date du 30 mai 1995, et lettre d'amendement en datedu 4 ddcembre 1995). Sign6 A Washington le 31 aoft 1995 ................ 81

N0 32794. Banque internationale pour la reconstruction et le d~veloppement etChine :

Accord de pret - Projet hydroflectrique II a Ertan (avec annexes et Conditionsg6n6rales applicables aux accords de prt et de garantie en date du let janvier1985). Sign6 A Washington le 2 novembre 1995 ..................................................... 83

NO 32795. Association internationale de dkveloppement et B6nin :Accord de cr&lit de d6veloppement - Troisiame crddit d'ajustement structurel (avec

annexes et Conditions g6n6rales applicables aux accords de crddit de d6veloppe-ment en date du ler janvier 1985). Sign6 A Washington le 8 juin 1995 ........... 85

Vol. 1920

VIII United Nations - Treaty Series * Nations Unies - Recueil des Trait~s 1996

Page

No. 32796. International Development Association and Viet Nam:Development Credit Agreement-Power Sector Rehabilitation and Expansion

Project (with schedules and General Conditions Applicable to DevelopmentCredit Agreements dated 1 January 1985). Signed at Hanoi on 11 July 1995

Agreement amending the above-mentioned Agreement. Signed at Hanoi on12 F ebruary 1996 ....................................................................................................... 87

No. 32797. International Bank for Reconstruction and Development andLithuania:

Loan Agreement-Enterprise and Financial Sector Assistance Project (withschedules and General Conditions Applicable to Loan and Guarantee Agree-ments for Single Currency Loans dated 9 February 1993). Signed at Washing-ton on 19 July 1995 .................................................................................................... 89

No. 32798. International Development Association and Honduras:Development Credit Agreement-Third Social Investment Fund Project (with

schedules and General Conditions Applicable to Development Credit Agree-ments dated 1 January 1985). Signed at Washington on 3 August 1995 ............. 91

No. 32799. International Bank for Reconstruction and Development andRomania:

Guarantee Agreement-Power Sector Rehabilitation and Modernization Project(with General Conditions Applicable to Loan and Guarantee Agreementsdated 1 January 1985). Signed at Washington on 29 August 1995 ...................... 93

No. 32800. International Bank for Reconstruction and Development andRomania:

Loan Agreement-Financial and Enterprise Sector Adjustment Loan (withschedules and General Conditions Applicable to Loan and Guarantee Agree-ments for Single Currency Loans dated 30 May 1995). Signed at Washingtonon 19 January 1996 .................................................................................................... 95

No. 32801. International Development Association and Azerbaijan:Development Credit Agreement-Institution Building Technical Assistance Proj-

ect (with schedules and General Conditions Applicable to DevelopmentCredit Agreements dated 1 January 1985). Signed at Baku on 14 September1995 .............................................................................................................................. 97

No. 32802. International Bank for Reconstruction and Development andParaguay:

Loan Agreement-Secondary Education Improvement Project (with schedulesand General Conditions Applicable to Loan and Guarantee Agreements forSingle Currency Loans dated 30 May 1985). Signed at Washington on 18 Sep-tem b er 1995 ............................................................................................................... 99

Vol. 1920

United Nations - Treaty Series * Nations Unies - Recueil des Traitis

Pages

NO 32796. Association internationale de diveloppement et Viet Nam:Accord de crddit de ddveloppement - Projet de rihabilitation et d'expansion du

secteur de l'Jlectricit (avec annexes et Conditions g~ndrales applicablesaux accords de crddit de ddveloppement en date du ler janvier 1985). Sign6 AHanoi le 11 juillet 1995

Accord modifiant l'Accord susmentionn6. Sign46 A Hanoi le 12 fdvrier 1996........... 87

NO 32797. Banque internationale pour la reconstruction et le diveloppement etLituanie :

Accord de pr~t - Projet d'assistance aux entreprises et au secteurfinancier (avecannexes et Conditions gtndrales applicables aux accords de pr&t et de garantiepour les prts de circulation particuli~re en date du 9 fdvrier 1993). Sign6 AW ashington le 19 juillet 1995 .................................................................................... 89

N0 32798. Association internationale de d~veloppement et Honduras :Accord de crdit de ddveloppement - Troisi me projet defonds d'investissement

social (avec annexes et Conditions gdndrales applicables aux accords de cr6-dit de ddveloppement en date du 1er janvier 1985). Sign6 A Washington le3 ao0 t 1995 .................................................................................................................. 9 1

N0 32799. Banque internationale pour la reconstruction et le diveloppement etRoumanie:

Accord de garantie - Projet de rihabilitation et de modernisation du secteur de1'dlectriciti (avec Conditions gtn6rales applicables aux accords de pret et degarantie en date du lerjanvier 1985). Sign6 A Washington le 29 aofit 1995 ........ 93

N0 32800. Banque internationale pour la reconstruction et le d~veloppement etRoumanie:

Accord de pr~t - Pr.t d'ajustement au secteur financier et des entreprises (avecannexes et Conditions gdnrales applicables aux accords de pr&t et de garantiepour les prets de circulation particulire en date du 30 mai 1995). Sign6 AW ashington le 19 janvier 1996 ................................................................................. 95

N0 32801. Association internationale de diveloppement et Azerbaidjan :Accord de crddit de ddveloppement - Projet d'assistance technique pour le ren-

forcement des institutions (avec annexes et Conditions gdndrales applicablesaux accords de crddit de ddveloppement en date du 1 er janvier 1985). Sign6 AB aku le 14 septem bre 1995 ...................................................................................... 97

N0 32802. Banque internationale pour la reconstruction et le d~veloppement etParaguay:

Accord de prt - Projet d'ame6lioration de l'enseignement secondaire (avecannexes et Conditions gdndrales applicables aux accords de pret et de garantiepour les prts de circulation particuli~re en date du 30 mai 1995). Sign6 AW ashington le 18 septem bre 1995 ........................................................................... 99

Vol. 1920

X United Nations - Treaty Series * Nations Unies - Recueil des Traitis 1996

Page

No. 32803. International Development Association and Ethiopia:Development Credit Agreement-National Fertilizer Sector Project (with sched-

ules and General Conditions Applicable to Development Credit Agreementsdated 1 January 1985). Signed at Washington on 29 September 1995 ................ 101

No. 32804. International Development Association and Armenia:Development Credit Agreement-Highway Project (with schedules and General

Conditions Applicable to Development Credit Agreements dated 1 January1985). Signed at Washington on 2 October 1995 ................................................... 103

No. 32805. International Bank for Reconstruction and Development andMexico:

Guarantee Agreement-Privatization TechnicalAssistance Project (with scheduleand General Conditions Applicable to Loan and Guarantee Agreements dated1 January 1985). Signed at Washington on 8 October 1995 ................................. 105

No. 32806. International Bank for Reconstruction and Development andMauritius:

MMA Guarantee Agreement-Port Development and Environment ProtectionProject (with General Conditions Applicable to Loan and Guarantee Agree-ments for Single Currency Loans dated 30 May 1995). Signed at Washingtonon 8 O ctober 1995 ...................................................................................................... 107

No. 32807. International Development Association and United Republic ofTanzania:

Development Credit Agreement-Financial Institutions Development Project(with schedules and General Conditions Applicable to Development CreditAgreements dated 1 January 1985). Signed at Washington on 27 October1995 .............................................................................................................................. 109

No. 32808. International Bank for Reconstruction and Development andChile:

Loan Agreement-Secondary Education Quality Improvement Project (withschedules and General Conditions Applicable to Loan and Guarantee Agree-ments dated 1 January 1985). Signed at Washington on 31 October 1995 ......... 111

No. 32809. International Bank for Reconstruction and Development andBulgaria:

Guarantee Agreement-Railway Rehabilitation Project (with General ConditionsApplicable to Loan and Guarantee Agreements dated 1 January 1985). Signedat W ashington on 8 N ovem ber 1995 ....................................................................... 113

No. 32810. International Development Association and Uganda:Development Credit Agreement-Environmental Management Capacity Building

Project (with schedules and General Conditions Applicable to DevelopmentCredit Agreements dated 1 January 1985). Signed at Washington on 10 No-vem ber 1995 ................................................................................................................ 115

Vol. 1920

1996 United Nations - Treaty Series * Nations Unies - Recueil des Traitis XI

Pages

NO 32803. Association internationale de d6veloppement et Ikthiopie:Accord de cr6dit de d6veloppement - Projet national relatif au secteur des

engrais (avec annexes et Conditions gdn~rales applicables aux accords decr6dit de d6veloppement en date du 1er janvier 1985). Sign6 b Washington le29 septem bre 1995 ..................................................................................................... 101

N0 32804. Association internationale de d6veloppement et Armknie :Accord de cr6dit de d6veloppement - Projet relatif au riseau routier (avec

annexes et Conditions g6n6rales applicables aux accords de cr6dit de d6velop-pement en date du lerjanvier 1985). Signd A Washington le 2 octobre 1995 ..... 103

N0 32805. Banque internationale pour la reconstruction et le dkveloppement etMexique:

Accord de garantie - Projet d'assistance technique pour la privatisation (avecannexe et Conditions g6nrales applicables aux accords de prat et de garantieen date du lerjanvier 1985). Sign6 A Washington le 8 octobre 1995 ................... 105

NO 32806. Banque internationale pour la reconstruction et le dkveloppement etMaurice :

Contrat de garantie MMA - Projet de diveloppement portuaire et de protectionde l'environnement (avec Conditions g6n6rales applicables aux accords depr& et de garantie pour les prts de circulation particuli~re en date du 30 mai1995). Signd A W ashington le 8 octobre 1995 ......................................................... 107

N0 32807. Association internationale de d6veloppement et Rkpublique-Unie deTanzanie :

Accord de cr&lit de d6veloppement - Projet de diveloppement des institutionsfinancires (avec annexes et Conditions g6n6rales applicables aux accords decr6dit de d6veloppement en date du 1er janvier 1985). Sign6 A Washington le27 octobre 1995 ......................................................................................................... 109

N0 32808. Banque internationale pour la reconstruction et le diveloppement etChili :

Accord de prt - Projet d'amilioration de la qualitj de l'enseignement secon-daire (avec annexes et Conditions g6n6rales applicables aux accords de pr&et de garantie en date du Iet janvier 1985). Sign6 A Washington le 31 octobre1995 .............................................................................................................................. 111

NO 32809. Banque internationale pour la reconstruction et le dkveloppement etBulgarie :

Accord de garantie - Projet de rhabilitation des chemins defer (avec Conditionsg6n6rales applicables aux accords de prt et de garantie en date du ler janvier1985). Sign6 b W ashington le 8 novembre 1995 ..................................................... 113

N0 32810. Association internationale de d6veloppement et Ouganda:Accord de cr6dit de d6veloppement - Projet de renforcement des capacit&s pour

la gestion de I'environnement (avec annexes et Conditions g6n6rales applica-bles aux accords de cr6dit de d6veloppement en date du 1er janvier 1985).Sign6 A W ashington le 10 novembre 1995 ............................................................... 115

Vol. 1920

XII United Nations - Treaty Series * Nations Unies - Recueil des Traitks 1996

Page

No. 32811. International Bank for Reconstruction and Development andBrazil:

Guarantee Agreement-Environmental Conservation and Rehabilitation Project(with General Conditions Applicable to Loan and Guarantee Agreements forSingle Currency Loans dated 9 February 1993). Signed at Washington on14 N ovem ber 1995 ..................................................................................................... 117

No. 32812. International Bank for Reconstruction and Development andPoland:

Guarantee Agreement-Power Transmission Project (with General ConditionsApplicable to Loan and Guarantee Agreements dated 1 January 1985). Signedat W arsaw on 25 January 1996 ................................................................................. 119

No. 32813. International Development Association and Cameroon:Development Credit Agreement-Second Structural Adjustment Credit (with

schedules and General Conditions Applicable to Development Credit Agree-ments dated 1 January 1985). Signed at Washington on 14 February 1996 ....... 121

No.. 32814. International Development Association and Chad:Development Credit Agreement-Capacity Building for Economic Management

Project (with schedules and General Conditions Applicable to DevelopmentCredit Agreements dated 1 January 1985). Signed at Washington on 16 Feb-ruary 1996 ................................................................................................................... 123

No. 32815. International Development Association and Chad:Development Credit Agreement-Structural Adjustment Credit (with schedule

and General Conditions Applicable to Development Credit Agreements dated1 January 1985). Signed at Washington on 16 February 1996 ............... 125

No. 32816. United Nations and Philippines:Exchange of letters constituting an agreement concerning the United Nations/

European Space Agency Workshop on Microwave Remote Sensing Appli-cations, to be held in Manila, Philippines, from 22 to 26 April 1996. Vienna,29 M arch and 18 A pril 1996 ...................................................................................... 127

No. 32817. Italy and Netherlands:Convention for the avoidance of double taxation with respect to taxes on income

and on capital and for prevention of fiscal evasion (with protocol). Signed atThe H ague on 8 M ay 1990 ........................................................................................ 129

No. 32818. Spain and Israel:Agreement on cooperation in the field of desertification (with exchange of notes of

28 December 1993 and 25 January 1994). Signed at Jerusalem on 9 November1993 .............................................................................................................................. 28 1

Vol. 1920

United Nations - Treaty Series * Nations Unies - Recueil des Traitks

Pages

N0 32811. Banque internationale pour la reconstruction et le d~veloppement etBrksil :

Contrat de garantie - Projet de conservation et de rdhabilitation de 1'environne-ment (avec Conditions g6ndrales applicables aux accords de pret et de garan-tie pour les pr&s de circulation particulire en date du 9 f6vrier 1993). Sign6 AW ashington le 14 novem bre 1995 ............................................................................ 117

NO 32812. Banque internationale pour la reconstruction et le d~veloppement etPologne :

Accord de garantie - Projet de transmission d'ilectricitd (avec Conditions gdn6-rales applicables aux accords de pret et de garantie en date du 1er janvier1985). Sign6 A Varsovie le 25 janvier 1996 .............................................................. 119

NO 32813. Association internationale de d6veloppement et Cameroun :Accord de cr6dit de d6veloppement - Deuxime credit d'ajustement structurel

(avec annexes et Conditions g6n6rales applicables aux accords de cr6dit dedtveloppement en date du 1 er janvier 1985). Sign6 A Washington le 14 f6vrier1996 .............................................................................................................................. 12 1

N0 32814. Association internationale de d6veloppement et Tchad :Accord de cr6dit de d6veloppement - Projet de renforcement des capacitds pour

la gestion dconomique (avec annexes et Conditions g6n6rales applicablesaux accords de cr6dit de d6veloppement en date du ler janvier 1985). Sign6 AW ashington le 16 f6vrier 1996 .................................................................................. 123

NO 32815. Association internationale de d~veloppement et Tchad :Accord de cr6dit de daveloppement - Credit d'ajustement structurel (avec

annexe et Conditions g6ndrales applicables aux accords de cr6dit de davelop-pement en date du letjanvier 1985). Sign6 A Washington le 16 f6vrier 1996 ..... 125

NO 32816. Organisation des Nations Unies et Philippines :9change de lettres constituant un accord relatif A la Rdunion de travail des Nations

Unies et de l'Agence spatiale europdenne sur les applications de la t6l6d6tec-tion par ondes ultra-courtes, devant se tenir A Manille (Philippines), du 22 au26 avril 1996. Vienne, 29 mars et 18 avril 1996 ...................................................... 127

NO 32817. Italie et Pays-Bas :Convention tendant A 6viter les doubles impositions en matire d'imp6ts sur le

revenu et sur la fortune et A pr6venir l'6vasion fiscale (avec protocole). Sign6eA L a H aye le 8 m ai 1990 ............................................................................................ 129

N0 32818. Espagne et IsraE!:Accord relatif A la coop6ration dans le domaine de la d6sertification (avec 6change

de notes des 28 d~cembre 1993 et 25 janvier 1994). Sign6 A J.,usalem le 9 no-vem bre 1993 ................................................................................................................ 28 1

Vol. 1920

United Nations - Treaty Series * Nations Unies - Recueil des Traitis

Page

No. 32819. Spain and United States of America:Agreement on scientific and technological cooperation (with annex). Signed at

M adrid on 10 June 1994 ............................................................................................ 309

No. 32820. Spain and Algeria:Agreement on the reciprocal promotion and protection of investments. Signed at

M adrid on 23 Decem ber 1994 .................................................................................. 329

No. 32821. Spain and Romania:Agreement for the reciprocal promotion and protection of investments. Signed at

Bucharest on 25 January 1995 ................................................................................. 369

No. 32822. United Nations and Turkey:Agreement regarding arrangements for the United Nations Conference on Human

Settlements (Habitat II) (with annexes). Signed at Ankara on 23 April 1996... 407

II

Treaties and international agreements

filed and recorded from 1 April 1996 to 26 April 1996

No. 1149. United Nations and World Tourism Organization:

Special Agreement extending the jurisdiction of the Administrative Tribunal of theUnited Nations to the World Tourism Organization with respect to applica-tions by staff members of the World Tourism Organization alleging non-obser-vance of the Regulations of the United Nations Joint Staff Pension Fund.Signed at Madrid on 29 March 1996 and at New York on 26 April 1996 ........... 411

ANNEX A. Ratifications, accessions, subsequent agreements, etc., con-cerning treaties and international agreements registered with theSecretariat of the United Nations

No. 3511. Convention for the Protection of Cultural Property in the Event ofArmed Conflict. Done at The Hague, on 14 May 1954:

A ccession by U zbekistan ................................................................................................. 420

Vol. 1920

1996 United Nations - Treaty Series * Nations Unies - Recueil des Traitis XV

Pages

NO 32819. Espagne et lttats-Unis d'Am~rique:Accord relatif A la cooperation scientifique et technologique (avec annexe). Sign6

A M adrid le 10 juin 1994 ............................................................................................ 309

N0 32820. Espagne et Aigirie:Accord relatif A la promotion et la protection rdciproques des investissements.

Signd hL M adrid le 23 d&cembre 1994 ....................................................................... 329

N0 32821. Espagne et Roumanie:Accord relatif A la promotion et A ]a protection des investissements. Signd A Buca-

rest le 25 janvier 1995 ................................................................................................ 369

N0 32822. Organisation des Nations Unies et Turquie :Accord relatif aux arrangements en vue de la Confdrence des Nations Unies sur

les 6tablissements humains (Habitat II) [avec annexes]. Sign6 A Ankara le23 avril 1996 ................................................................................................................ 407

II

Traitds et accords intemationauxclassis et inscrits au rdpertoire du jer avril 1996 au 26 avril 1996

N0 1149. Organisation des Nations Unies et Organisation mondiale du tou-risme :

Accord spdcial 6tendant la juridiction du Tribunal administratif des Nations UniesA 'Organisation mondiale du tourisme en ce qui concerne les requites defonctionnaires de l'Organisation invoquant l'inobservation des statuts de laCaisse commune des pensions du personnel des Nations Unies. Signd A Ma-drid le 29 mars 1996 et A New York le 26 avril 1996 .................... 411

ANNEXE A. Ratifications, adhdsions, accords ult6rieurs, etc., concernantdes traitis et accords internationaux enregistris au Secretariat de1'Organisation des Nations Unies

N0 3511. Convention pour la protection des biens culturels en cas de conflitarm6. Faite A La Haye, le 14 mai 1954:

A dhdsion de l'O uzbdkistan .............................................................................................. 420

Vol. 1920

XVI United Nations - Treaty Series * Nations Unies - Recueil des Traitis 1996

Page

No. 4789. Agreement concerning the adoption of uniform conditions of ap-proval and reciprocal recognition of approval for motor vehicleequipment and parts. Done at Geneva, on 20 March 1958:

Application by Germany of regulation No. 96 annexed to the above-mentionedA greem ent ................................................................................................................... 421

Application by the Czech Republic of regulations Nos. 69, 70, 80 and 92 to 97annexed to the above-mentioned Agreement ........................................................ 421

Entry into force of regulation No. 98 (Uniform provisions concerning the approvalof motor vehicle headlamps equipped with gas-discharge light sources) as anannex to the above-mentioned Agreement of 20 March 1958 ............................. 422

Entry into force of regulation No. 99 (Uniform provisions concerning the approvalof gas-discharge light sources for use in approved gas-discharge lamp unitsof power-driven vehicles) as an annex to the above-mentioned Agreement of20 M arch 1958 ............................................................................................................ 422

No. 7047. Agreement between the Kingdom of the Netherlands and the ItalianRepublic for the avoidance of double taxation with respect to taxeson income and fortune. Signed at The Hague, on 24 January 1957:

Termination (N ote by the Secretariat) ........................................................................... 425

No. 7515. Single Convention on Narcotic Drugs, 1961. Done at New York, on30 March 1961:

A ccession by G am bia ....................................................................................................... 426

No. 8359. Convention on the settlement of investment disputes between Statesand nationals of other States. Opened for signature at Washington,on 18 March 1965:

R atification by B ahrain ..................................................................................................... 427

No. 8940. European Agreement concerning the International Carriage of Dan-gerous Goods by Road (ADR). Done at Geneva, on 30 September1957:

A ccession by L atvia .......................................................................................................... 428

No. 14151. Protocol amending the Single Convention on Narcotic Drugs, 1961.Concluded at Geneva on 25 Nlarch 1972:

A ccession by Sw itzerland ................................................................................................ 429

No. 14152. Single Convention on Narcotic Drugs, 1961, as amended by the Pro-tocol of 25 March 1972 amending the Single Convention on Nar-cotic Drugs, 1961. Done at New York on 8 August 1975:

R atification by Sw itzerland ............................................................................................. 430

Participation by Gambia to the above-mentioned Convention ................................... 430

Vol. 1920

United Nations - Treaty Series * Nations Unies - Recueil des Traitks

Pages

N0 4789. Accord concernant l'adoption de conditions uniformes d'homologa-tion et la reconnaissance r&iproque de I'homologation des 6quipe-ments et pieces de vkhicules A moteur. Fait A Genve, le 20 mars1958 :

Application par I'Allemagne du r~glement no 96 annex6 A l'Accord susmentionn6 ...... 423

Application par la R6publique tch~que des r~glements nOs 69, 70, 80 et 92 -A 97annexds A l'Accord susm entionn6 .......................................................................... 423

Entrde en vigueur du r~glement no 98 (Dispositions uniformes concernant l'homo-logation des projecteurs de vihicules et moteur munis de sources lumineusest dcharge) en tant qu'annexe A l'Accord susmentionn6 du 20 mars 1958 ...... 424

Entrde en vigueur du r~glement no 99 (Prescription uniformes relatives a l'homo-logation des sources lumineuses t dcharge pour projecteurs homologues devdhicules a moteur) en tant qu'annexe A l'Accord susmentionn6 du 20 mars1958 .............................................................................................................................. 424

NO 7047. Convention entre le Royaume des Pays-Bas et ia Rkpublique italiennetendant A 6viter la double imposition en mati~re d'imp6ts sur lerevenu et sur la fortune. Signke A La Haye, le 24 janvier 1957:

Abrogation (N ote du Secrdtariat) ................................................................................... 425

N0 7515. Convention unique sur les stupffiants de 1961. Faite A New York, le30 mars 1961 :

A dh6sion de G am bie ......................................................................................................... 426

N0 8359. Convention pour, le riglement des diff~rends relatifs aux investis-sements entre Etats et ressortissants d'autres lktats. Ouverte ii lasignature A Washington, le 18 mars 1965 :

Ratification de B ahrern ..................................................................................................... 427

N0 8940. Accord europken relatif au transport international des marchandisesdangereuses par route (ADR). Fait A Genive, le 30 septembre 1957 :

A dhdsion de la L ettonie .................................................................................................... 428

N0 14151. Protocole portant amendement de la Convention unique sur les stu-pffiants de 1961. Conclu A Gen~ve le 25 mars 1972 :

A dhesion de la Suisse ....................................................................................................... 429

NO 14152. Convention unique sur les stupifiants de 1961 telle que modifi&e parle Protocole du 25 mars 1972 portant amendement de la Conven-tion unique sur les stupffiants de 1961. Faite As New York le 8 aofit1975 :

Participation de la Suisse .................................................................................................. 430Participation de la Gambie h la Convention susmentionn~e ...................................... 430

Vol. 1920

XVII

United Nations - Treaty Series * Nations Unies - Recueil des Traitis

Page

No. 14537. Convention on international trade in endangered species of wildfauna and flora. Opened for signature at Washington on 3 March1973:

Accession by Mongolia to the above-mentioned Convention, as amended at Bonnon 22 June 1979 .......................................................................................................... 431

No. 14956. Convention on psychotropic substances. Concluded at Vienna on21 February 1971:

A cce ssion by Sw itzerland ................................................................................................ 432A ccession by G am bia ....................................................................................................... 432

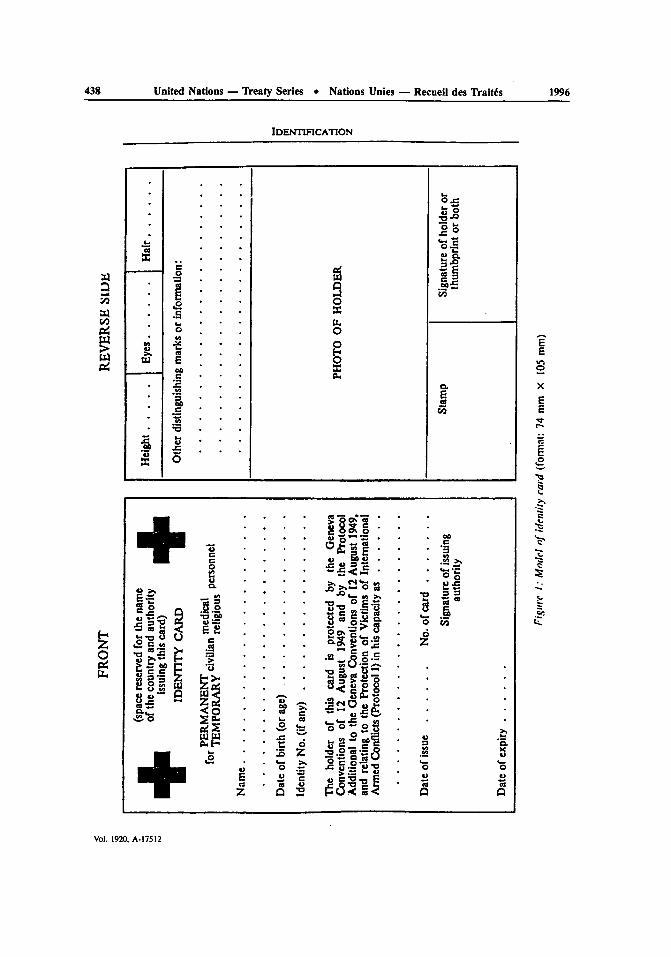

No. 17512. Protocol additional to the Geneva Conventions of 12 August 1949,and relating to the protection of victims of international armedconflicts (Protocol I). Adopted at Geneva on 8 June 1977:

Ratification by M ongolia .................................................................................................. 433Accessions by Swaziland and South Africa .................................................................. 433Annex I (Regulations concerning identification) to the above-mentioned Protocol,

as amended on 30 November 1993 (with communications from Hungary, Jor-dan and Sw eden) ........................................................................................................ 435

No. 17513. Protocol additional to the Geneva Conventions of 12 August 1949,and relating to the protection of victims of non-internationalarmed conflicts (Protocol I). Adopted at Geneva on 8 June 1977:

R atification by M ongolia .................................................................................................. 465Accessions by Swaziland and South Africa .................................................................. 465

No. 26369. Montreal Protocol on Substances that Deplete the Ozone Layer.Concluded at Montreal on 16 September 1987:

Acceptance by Ireland of the amendment to the above-mentioned Protocol,adopted at the Fourth Meeting of the Parties at Copenhagen on 25 November1992 .............................................................................................................................. 466

No. 27627. United Nations Convention against Illicit Traffic in Narcotic Drugsand Psychotropic Substances. Concluded at Vienna on 20 De-cember 1988:

Ratification by the United Republic of Tanzania .......................................................... 467A ccession by G am bia ....................................................................................................... 467

No. 29051. Agreement between the Government of India and the UnitedNations Industrial Development Organization on basic termsand conditions governing UNIDO projects envisaged by the in-terim programme for the International Centre for Genetic Engi-neering and Biotechnology. Signed at Vienna on 25 March 1988:

Exchange of letters constituting an agreement extending and amending the above-mentioned Agreement (with project document). Vienna, 20 April, 15 and29 M ay 1995 ................................................................................................................ 468

Vol. 1920

XVIII

1996 United Nations - Treaty Series * Nations Unies - Recueil des Traitks XIX

Pages

NO 14537. Convention sur le commerce international des espkces de faune etde flore sauvages menac~es d'extinction. Ouverte A la signature AWashington le 3 mars 1973 :

Adhdsion de la Mongolie A la Convention susmentionnde, telle qu'amendte A Bonnle 22 juin 1979 ............................................................................................................. 43 1

N0 14956. Convention sur les substances psychotropes. Conclue A Vienne le21 fivrier 1971 :

A dhdsion de la Suisse ...................................................................................................... 432A dhesion de la G am bie ..................................................................................................... 432

N0 17512. Protocole additionnel aux Conventions de Gen~ve du 12 aofit 1949relatif A la protection des victimes des conflits arm~s internatio-naux (Protocole 1). Adoptk A Gen ve le 8 juin 1977:

R atification de la M ongolie .............................................................................................. 433Adhdsions du Swaziland et de l'Afrique du Sud .......................................................... 433Annexe I (R~glement relatif A l'identification) au Protocole susmentionn6, telle

qu'amendde le 30 novembre 1993 (avec communications de la Hongrie, de laJordanie et de la Su~de) ............................................................................................ 448

NO 17513. Protocole additionnel aux Conventions de Genve du 12 aofit 1949relatif A la protection des victimes des conflits arms non interna-tionaux (Protocole 11). Adoptk h Gen~ve le 8 juin 1977:

R atification de la M ongolie .............................................................................................. 465

Adhesions du Swaziland et de l'Afrique du Sud .......................................................... 465

N0 26369. Protocole de Montreal relatif A des substances qui appauvrissent lacouche d'ozone. Conclu A Montreal le 16 septembre 1987:

Acceptation par l'Irlande de l'amendement au Protocole susmentionn6, adopt6 Ala Quatri~me Rdunion des Parties A Copenhague le 25 novembre 1992 ............ 466

NO 27627. Convention des Nations Unies contre le trafic illicite de stupffiantset de substances psychotropes. Conclue A Vienne le 20 d6cembre1988:

Ratification de la Rdpublique-Unie de Tanzanie ........................................................... 467A dhdsion de la G am bie ..................................................................................................... 467

N0 29051. Accord entre le Gouvernement de l'Inde et i'Organisation desNations Unies pour le d~veloppement industriel relatif aux termeset conditions de base rkgissant les projets de I'ONUDI envisagespar le programme intirimaire pour le Centre international pour leginie gnktique et la biotechnologie. Sign6 A Vienne le 25 mars1988:

tchange de lettres constituant un accord prorogeant et modifiant l'Accord sus-mentionn6 (avec document de projet). Vienne, 20 avril, 15 et 29 mai 1995 ....... 468

Vol. 1920

XX United Nations - Treaty Series * Nations Unies - Recueil des Traitis 1996

Page

No. 29087. Agreement between the United Nations Industrial DevelopmentOrganization and the Government of the Republic of Korea onthe UNIDO Service in the Republic of Korea for promotion ofindustrial investment in developing countries. Signed at Viennaon 15 April 1987:

Exchange of letters constituting an agreement extending and amending the above-mentioned Agreement, as amended (with annexed project document). Vienna,8 and 14 M arch 1995 .................................................................................................. 469

No. 30619. Convention on biological diversity. Concluded at Rio de Janeiro on5 June 1992:

R atification by B ulgaria .................................................................................................... 470

No. 30692. International Cocoa Agreement, 1993. Concluded at Geneva on16 July 1993:

R atification by A ustria ...................................................................................................... 471

No. 30822. United Nations Framework Convention on Climate Change. Con-cluded at New York on 9 May 1992:

A cceptance by C roatia ...................................................................................................... 472Ratification by the United Republic of Tanzania .......................................................... 472A ccession by Q atar ........................................................................................................... 472

No. 31363. United Nations Convention on the Law of the Sea. Concluded atMontego Bay on 10 December 1982:

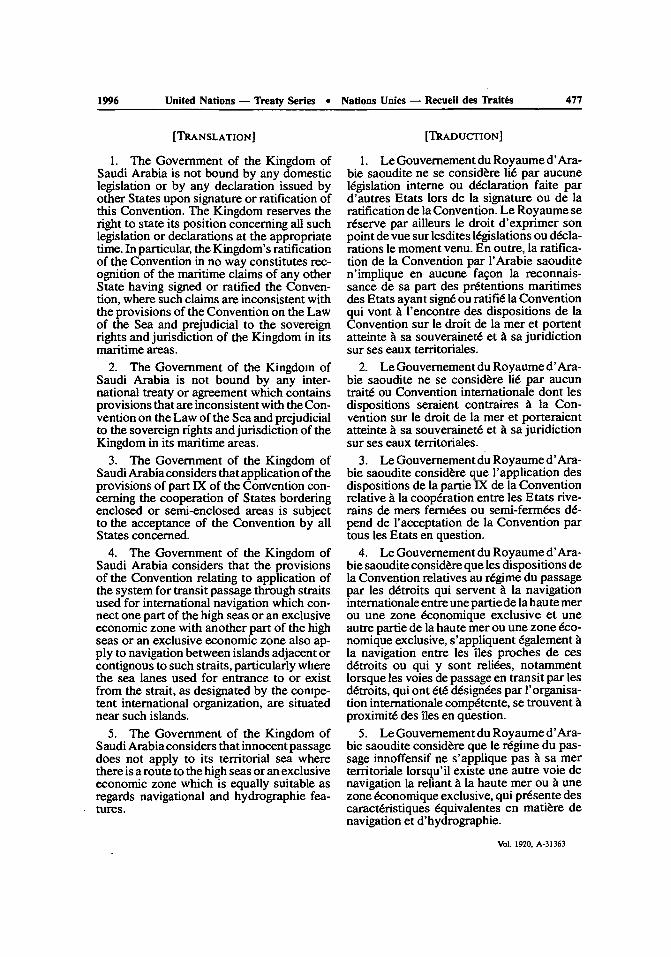

R atification by France ...................................................................................................... 473R atification by Saudi A rabia ............................................................................................ 474

No. 31364. Agreement relating to the implementation of Part XI of the UnitedNations Convention on the Law of the Sea of 10 December 1982.Adopted by the General Assembly of the United Nations on28 July 1994:

R atification by France ...................................................................................................... 479Participation of Saudi Arabia in the above-mentioned Agreement ............................ 479

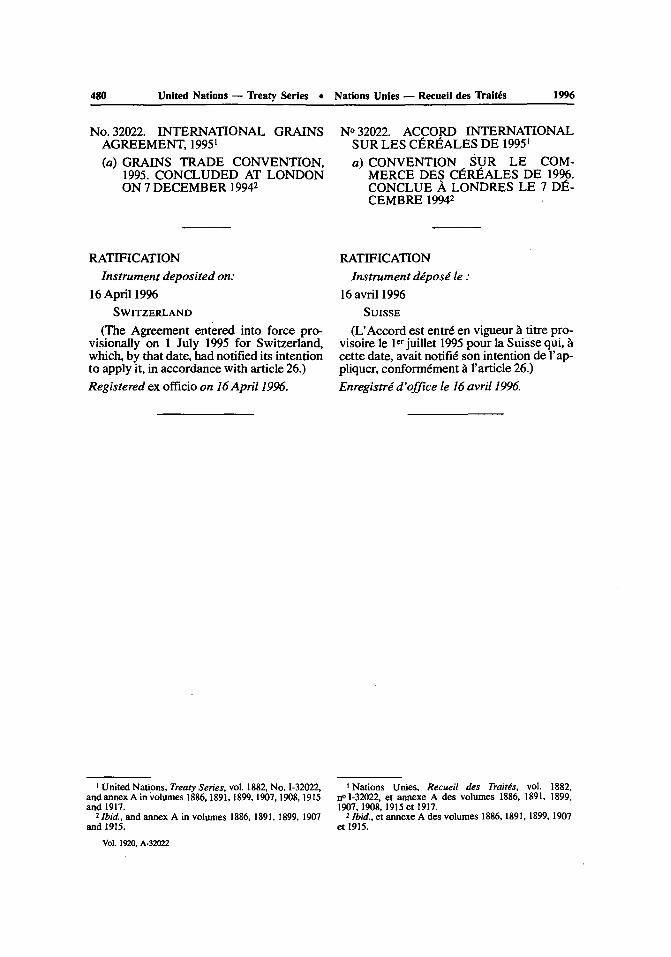

No. 32022. International Grains Agreement, 1995:(a) Grains Trade Convention, 1995. Concluded at London on 7 December

1994:Ratification by Sw itzerland .............................................................................................. 480

Vol. 1920

1996 United Nations - Treaty Series * Nations Unies - Recueil des Trait~s XXI

Pages

NO 29087. Accord entre l'Organisation des Nations Unies pour le d~veloppe-ment industriel et le Gouvernement de la Ripublique de Corkerelatif an Service de I'ONUDI en Rpublique de Cor~e pour lapromotion des investissements industriels dans les pays en dkve-loppement. Sign6 A Vienne le 15 avril 1987:

tchange de lettres constituant un accord prorogeant et modifiant I'Accord sus-mentionn, tel que modifid (avec document de projet annex6). Vienne, 8 et14 m ars 1995 ............................................................................................................... 469

N0 30619. Convention sur la diversit6 biologique. Conclue A Rio de Janeiro le5 juin 1992 :

Ratification de la B ulgarie ................................................................................................ 470

N0 30692. Accord international de 1993 sur le cacao. Conclu t Genive le16 juillet 1993 :

R atification de l'A utriche ................................................................................................. 471

NO 30822. Convention-cadre des Nations Unies sur les changements climati-ques. Conclue t New York le 9 mai 1992:

A cceptation de la C roatie ................................................................................................. 472Ratification de la Rdpublique-Unie de Tanzanie ........................................................... 472A dhdsion du Q atar ............................................................................................................. 472

NO 31363. Convention des Nations Unies sur le droit de la mer. Conclue i Mon-tego Bay le 10 dcembre 1982 :

Ratification de la France ................................................................................................... 473Ratification de l'Arabie saoudite ..................................................................................... 474

NO 31364. Accord relatif A l'application de la Partie XI de la Convention desNations Unies sur le droit de la mer du 10 d~cembre 1982. Adopt6par l'Assembl~e gkn&rale des Nations Unies le 28 juillet 1994:

R atification de la France ................................................................................................... 479Participation de I'Arabie saoudite A 'Accord susmentionn6 ...................................... 479

NO 32022. Accord international sur les c6rkales de 1995 :a) Convention sur le commerce des cirkales de 1995. Conclue A Londres le

7 d6cembre 1994:R atification de la Suisse .................................................................................................... 480

Vol. 1920

NOTE BY THE SECRETARIAT

Under Article 102 of the Charter of the United Nations every treaty and every international agree-ment entered into by any Member of the United Nations after the coming into force of the Charter shall,as soon as possible, be registered with the Secretariat and published by it. Furthermore, no party to atreaty or international agreement subject to registration which has not been registered may invoke thattreaty or agreement before any organ of the United Nations. The General Assembly, by resolution 97 (I),established regulations to give effect to Article 102 of the Charter (see text of the regulations, vol. 859,p. VIII).

The terms "treaty" and "international agreement" have not been defined either in the Charter or inthe regulations, and the Secretariat follows the principle that it acts in accordance with the position of theMember State submitting an instrument for registration that so far as that party is concerned the instru-ment is a treaty or an international agreement within the meaning of Article 102. Registration of aninstrument submitted by a Member State, therefore, does not imply ajudgement by the Secretariat on thenature of the instrument, the status of a party or any similar question. It is the understanding of theSecretariat that its action does not confer on the instrument the status of a treaty or an internationalagreement if it does not already have that status and does not confer on a party a status which it wouldnot otherwise have.

Unless otherwise indicated, the translations of the original texts of treaties, etc., published in thisSeries have been made by the Secretariat of the United Nations.

NOTE DU SECRITARIAT

Aux termes de l'Article 102 de la Charte des Nations Unies, tout traitd ou accord internationalconclu par un Membre des Nations Unies apris l'entr6e en vigueur de la Charte sera, le plus t6t possible,enregistr6 au Secr6tariat et publi6 par lui. De plus, aucune partie h un trait6 ou accord international quiaurait dil 6tre enregistr6 mais ne 'a pas 6t6 ne pourra invoquer ledit trait ou accord devant un organe desNations Unies. Par sa r6solution 97 (I), l'Assembl6e g6n6rale a adopt6 un r~glement destin6 A mettre enapplication l'Article 102 de la Charte (voir texte du r~glement, vol. 859, p. IX).

Le terme « trait6 o et 'expression « accord international o n'ont 6t6 d6finis ni dans la Charte ni dansle r~glement, et le Secr6tariat a pris comme principe de s'en tenir A la position adopt6e A cet 6gard parl'Etat Membre qui a pr6sent6 l'instrument h l'enregistrement, A savoir que pour autant qu'il s'agit de cetEtat comme partie contractante l'instrument constitue un traitt ou un accord international au sens del'Article 102. II s'ensuit que l'enregistrement d'un instrument pr6sent6 par un Etat Membre n'implique,de la part du Secr6tariat, aucun jugement sur la nature de l'instrument, le statut d'une partie ou touteautre question similaire. Le Secr6tariat considare donc que les actes qu'il pourrait &re amen6 A accomplirne confirent pas b un instrument la qualitd de « trait6> ou d'< accord international si cet instrumentn'a pas d6jA cette qualit6, et qu'ils ne confirent pas A une partie un statut que, par ailleurs, elle neposs6derait pas.

Sauf indication contraire, les traductions des textes originaux des trait6s, etc., publi6s dans ce Re-cueil ont 6t6 6tablies par le Secr6tariat de l'Organisation des Nations Unies.

Treaties and international agreements

registered

from 8 April 1996 to 26 April 1996

Nos. 32783 to 32822

Traitis et accords internationaux

enregistris

du 8 avril 1996 au 26 avril 1996

NOs 32783 h1 32822

Vol. 1920

No. 32783

DENMARKand

UNITED KINGDOM OF GREAT BRITAINAND NORTHERN IRELAND

Memorandum of understanding regarding the billing andcollection by the United Kingdom of air navigationcharges levied by Denmark. Signed at London on 2 De-cember 1982

Exchange of notes constituting an agreement amending tothe above-mentioned Memorandum of understanding.Copenhagen, 14 June 1993 and 1 March 1994

Authentic texts: English.

Registered by Denmark on 16 April 1996.

DANEMARKet

ROYAUME-UNI DE GRANDE-BRETAGNEET D'IRLANDE DU NORD

Memorandum d'accord relatif ii la facturation et au recou-vrement par le Royaume-Uni de frais de navigationaerienne imposes par le Danemark. Sign6 i Londres le2 d~cembre 1982

Echange de notes constituant un accord amendant le Mkmo-randum d'accord susmentionn6. Copenhague, 14 juin1993 et ler mars 1994

Textes authentiques : anglais.

Enregistris par le Danemark le 16 avril 1996.

Vol. 1920, 1-32783

United Nations - Treaty Series o Nations Unies - Recueil des Traitis

MEMORANDUM OF UNDERSTANDING' BETWEEN THE GOV-ERNMENT OF THE KINGDOM OF DENMARK AND THE GOV-ERNMENT OF THE UNITED KINGDOM OF GREAT BRITAINAND NORTHERN IRELAND REGARDING THE BILLING ANDCOLLECTION BY THE UNITED KINGDOM OF AIR NAVIGA-TION CHARGES LEVIED BY DENMARK

The Government of the Kingdom of Den-mark and the Government of the UnitedKingdom of Great Britain and Northern Ire-land. desiring to draw up arrangements forthe billing and collection of charges imposedby the Government of Denmark at the re-quest of the Council of the InternationalCivil Aviation Organisation ('ICAO") pur-suant to Article XIV of the Agreement onthe Joint Financing of Certain Air Naviga-tion Services in Greenland and the FaroeIslands. opened for signature at Geneva on25 September 1956.2 as amended by the Pro-tocol opened for signature at Montreal on 3November 19823 (-the Agreement") and ascalled for in Recommendation 7 of the Sec-ond Conference on 1956 Danish and Ice-landic Joint Financing Agreements. have en-tered into this Memorandum of Understand-ing.

1.1. The Government of the United King-dom will. subject to the necessary approvalof Parliament. make regulations for requiringcharges (including the fee referred to in pa-ragraph 2.S.1 in respect of air navigationservices provided by the Government ofDenmark in pursuance of the Agreement tobe paid to the Civil Aviation Authority ofthe United Kingdom ("the Authority") bythe operator of every aircraft wherever regis-tered. which(a) makes a crossing between Europe and

North America: and(b) at any time during the crossing is in an

area north of the 45th parallel North be-tween the meridians of 15 West and 500West: and

tci in respect of which a flight plan is com-municated to the appropriate air traffic

control unit. being a flight plan involv-ing the flight of the aircraft in that area.

1.2. Flights between the following areaswill. subject to subparagraph (c) of the pre-ceding paragraph, also be taken into accountas follows:

Greenland and Canada. Greenland andthe United States of America, Greenland andIceland or Iceland and Europe - one thirdof a crossing: Greenland and Europe. Ice-land and Canada or Iceland and the UnitedStates of America - two thirds of a crossing:a crossing to or from Europe or Iceland notcrossing the coast of North America butwhich crosses the meridian of 300 Westnorth of the 45th parallel North - one thirdof a crossing.

For the purposes of this paragraph andthe preceding paragraph(a) a crossing will be counted even if the

point of take-off or landing is not in theareas mentioned in this or the precedingparagraph:

(b) "Europe" does not include Iceland orthe Azores.

2.1. Subject as aforesaid, the Authoritywill bill and collect charges and fees underthese arrangements in respect of flights madeon or after I January 1983.

2.2. The rate of the charge for each cross-ing made on or after I January 1983 will be£ 8 81 p being the rate notified, by the Gov-ernment of Denmark to the Government ofthe United Kingdom as the sterling equiva-lent of the rate determined by the Council ofICAO.

2.3. For each year subsequent to 1983 therate of the charge determined unoer the pre-

I Came into force on 1 January 1983, in accordance with section 2.1.I United Nations, Treaty Series, vol. 334, p. 89.3 Ibidl, vol. 1550, p. 299.

Vol. 1920, 1-32783

1996

1996 United Nations - Treaty Series * Nations Unies - Recuell des Trait6s 5

ceding paragraph will apply unless it ischanged in accordance with paragraph 2.4.

2.4. Should the Council of ICAO deter-mine that the rate of the charge is to bechanged, the Government of Denmark willnotify the Government of the United King-dom of the sterling equivalent of the newrate. Furthermore, should there at any timehe a substantial change in the rate of ex-change between the Danish krone and ster-ling, the Government of Denmark 'may noti-fy the Government of the United Kingdomof the new sterling equivalent of the rate ofcharge. For this purpose a change of lessthan 10 % in the value of the pound in rela-tion to Danish kroner will not be consideredsubstantial. It is recognised that at least threemonths must elapse between the notificationof a change and the coming into force of thenecessary amendment to the regulations re-ferred to in paragraph 1.1.

2.5. On billing the operator, the Authoritywill add to the charge a fee, not exceeding 5% of the charge, in respect of the Authority'sservices in collecting and accounting for thecharges (other than costs and expenses refer-red to in paragraph 4.4.). The Authority willfrom time to time inform the Directorate ofCivil Aviation in Denmark ("the DCA") ofthe basis on which the fee is calculated.

3.1. Payment by the operator will becomedue at the time of the flight in question andwill be payable in sterling to the Authorityby the person who is the operator of the air-craft at the time of that flight, if there isdoubt as to who is the operator the Authoritymay give notice to the person who it believeswas the owner of the aircraft at the time ofthe flight that it will treat him as the operatoruntil he can establish that some other personis the operator and that until he does so he isliable to make the payment. All references inthis Memorandum to the operator will beconstrued accordingly.

3.2. All sums received by the Authority inpursuance of these arrangements (exclusiveof the fees referred to in paragraph 2.5.) willbe remitted in sterling at monthly intervalsby the Authority to the DCA, and with anindication of the total amount remitted, sub-divided according to the nationality of theoperators. The Government of the UnitedKingdom will facilitate the remission to Den-mark in sterling of the sums in question.

4.1. The DCA will inform the Authority atweekly intervals of flights made through the

Sondrestrom Flight Information Region, giv-ing the following particulars:(a) the name of the operation or owner:(b) the date of the flight.(c) the flight number, if possible, or failing

that the registration and nationalitymarks of the aircraft:

(d) the origin and destination of the flight;(e) the type of the aircraft, where known:provided that such information need not befurnished if in the course of the flight theaircraft enters the Shanwick Oceanic FlightInformation Region.

4.2. The two Governments will endeavourto obtain similar information for the Author-ity in respect of flights to which these ar-rangements apply which pass through FlightInformation Regions administered by othergovernments and extending north of the 45thparallel North, other than flights in thecourse of which the aircraft enters the Son-drestrom or Shanwick Oceanic Flight In-formation Region.

4.3. The Government of the United King-dom will ensure that the Authority will useits best efforts to collect the sums due underthe regulations referred to in paragraph 1.1.,and that in the event of any difficulty in col-lecting the sums due the Authority will con-sult with the DCA as to the best method ofproceeding. The Government of Denmarkhas no objection to the exercise of jurisdic-tion by the courts of the United Kingdomfor the collection of the sums due whateverthe nationality of the aircraft in question orof its operator, and whatever the place wherethe liability arose.

4.4. The Authority will not be obliged todetain any aircraft or to engage in litigationfor the recovery of any sums due, and willnot take either course of action without theconsent of the DCA. If the Authority does sowith that consent, the Government of Den-mark will indemnify the Authority against allcosts and other expenses incurred by it andagainst any legal liability in respect of thedetention of the aircraft, howsoever suchcosts, expenses or liability may arise.

4.5. The two Governments may decide thatefforts under these arrangements to collect aparticular sum due should be suspended, inwhich event the matter will be dealt with inaccordance with arrangements made or to bemade in pursuance of the Agreement.

5. The Government of the United King-dom will cause the Authority to keep proper

Vol. 1920, 1-32783

6 United Nations - Treaty Series * Nations Unies - Recueil des Traitis 1996

accounts of its receipts under these arrange-ments and to permit the DCA and ICAO toverify those accounts with the relevantvouchers at reasonable intervals. The ac-counts and vouchers will be retained by theAuthority for that purpose for a period ofthree years after payment by the operatorbecomes due.

6. Nothing herein applies to military air-craft. An aircraft on the civil register of anyState will not be considered to be a militaryaircraft.

7.1. These arrangements may be terminat-ed by either Government giving to the othernot less than twelve months notice in writing,such notice to expire not earlier than the lastday of the year which follows the year inwhich the notice is received.

7.2. Upon the giving of notice of termina-tion of the Agreement by any party thereto

or on the occurrence of any substantialchange in its operation, these arrangementswill be reviewed by the two Governments atthe request of either of them.

8. Any dispute between the two Govern-ments arising out of the interpretation or ap-plication of these arrangements will be deter-mined by referring it to an arbitrator ap-pointed by both Governments jointly, or, ifthe Governments cannot decide on a mutual-ly acceptable arbitrator, by the President ofthe European Court of Justice provided thathe is neither a United Kingdom nor Danishnational or, if he is such a national, by thenext Senior Judge of that Court, in the orderof precedence established by Article 6 of theRules of Procedure of that Court, who is notsuch a national. The two Governments willabide by the decision of the arbitrator.

London, 2 December 1982

For the Governmentof the Kingdom of Denmark:

I. J. KELLAND

For the Governmentof the United Kingdom of Great Britain and Northern Ireland:

J. W. D. GRAY

Vol. 1920. 1-32783

United Nations - Treaty Series * Nations Unies - Recueil des Traitks

[TRADUCTION - TRANSLATION]

MIMORANDUM D'ACCORD 1 ENTRE LE GOUVERNEMENT DUROYAUME DU DANEMARK ET LE GOUVERNEMENT DUROYAUME-UNI DE GRANDE-BRETAGNE ET D'IRLANDE DUNORD RELATIF A LA FACTURATION ET AU RECOUVRE-MENT PAR LE ROYAUME-UNI DE FRAIS DE NAVIGATIONAIfRIENNE IMPOStS PAR LE DANEMARK

Le Gouvernement du Royaume du Danemark et le Gouvernement duRoyaume-Uni de Grande-Bretagne et d'Irlande du Nord, d6sireux de fixer les arran-gements relatifs A la facturation et au recouvrement des frais impos6s par le Dane-mark A la demande du Conseil de l'Organisation de l'aviation civile internationale(< OACI >>), conformment A l'article XIV de l'Accord sur le financement collectifde certains services de navigation a6rienne du Groenland et des iles Fro6 ouvert Ala signature A Gen~ve le 25 septembre 19562, tel que modifil par le Protocole ouvertA la signature a Montr6al le 3 novembre 19823 (« l'Accord > ), et tel que pr6vu A larecommandation 7 de la deuxi~me Conf6rence sur l'Accord de 1956 sur le finance-ment collectif entre l'Islande et le Danemark, ont conclu le pr6sent M6morandumd'accord.

1.1. Sous r6serve de l'approbation n6cessaire du Parlement, le Gouvemementdu Royaume-Uni, s'engage A adopter une r6glementation relative A la facturation desfrais (y compris les frais vis6s au paragraphe 2.5) relatifs aux services de navigationa6rienne assur6s par le Gouvernement du Danemark, conform6ment A l'Accord quiseront vers6s a l'administration de l'aviation civile du Royaume-Uni (<< l'Adminis-tration >) par l'exploitant de tout a6ronef quel que soit le lieu d'immatriculation decelui-ci, qui

a) Relie l'Europe A l'Am6ique du Nord; et qui

b) A un ou l'autre moment de son vol se trouve dans une zone situ6e au norddu 45e parall~le Nord entre les m6ridiens 150 et 50' ouest; et

c) Concernant lequel un plan de vol a 6t6 communique aux autorit6s charg6esdu contr6le de la circulation a6rienne s'agissant du vol de l'a6ronef dans ladite zone.

1.2. Sous r6serve de dispositions de 'alin6a c du pr6c&lent paragraphe, il sera6galement tenu compte des vols entre les endroits suivants de la fagon suivante :

Groenland et Canada, Groenland et Etats-Unis d'Am6rique, Groenland etIslande ou Islande et Europe - un tiers de parcours; Groenland et Europe, Islandeet Canada ou Islande et Etats-Unis d'Amdrique - deux tiers du parcours; un par-cours en direction ou en provenance de l'Europe ou d'Islande qui ne franchit pas lesc6tes de l'Am6rique du Nord mais qui traverse les mdridiens 30 ouest au nord du45e parall~le - un tiers du parcours.

Aux fins du pr6sent paragraphe et du pr6c&tent paragraphe:

I Entrd en vigueur le Iet janvier 1983, conformdment A la section 2.1.2 Nations Unies, Recueil des Trait~s, vol. 334, p. 89.3 Ibid., vol. 1550, p. 305.

Vol. 1920, 1-32783

8 United Nations - Treaty Series * Nations Unies - Recueil des Traitis 1996

a) Une traversde sera prise en compte m8me si le point de depart ou d'atterris-sage ne sont pas situds dans les zones visdes au prdsent ou au prc&dent paragraphe;

b) Le terme « Europe > ne comprend pas l'Islande ou les Agores.

2.1. Sous reserve des dispositions ci-avant, l'Administration facture et pergoitles frais et les taxes en vertu des pr6sents arrangements en ce qui concerne les volseffecturs A compter du ler janvier 1983 ou apr~s cette date.

2.2. Le taux des frais pour chaque traversde effectude A compter du lerjanvier1983 ou apres cette date s'61vera A £ 8,81 pence correspond au taux notifi6 par leGouvernement du Danemark au Gouvernement du Royaume-Uni, 6tant 1'6quiva-lent en sterling du taux fix6 par le Conseil de I'OACI.

2.3. S'agissant de chaque annde suivant l'anne 1983, le taux des frais 6tabliconformrment aux dispositions du paragraphe prrcrdent s'appliquera aux disposi-tions du paragraphe 2.4.

2.4. Si le Conseil de I'OACI devait drcider d'un changement du taux des frais,le Gouvernement du Danemark notifiera le Gouvernement du Royaume-Uni del'6quivalent en sterling du nouveau taux. En outre, si une modification impor-tante du taux de change devait apparaitre entre la couronne danoise et la livre ster-ling, il sera loisible au Gouvernement du Danemark de notifier le Gouvernement duRoyaume-Uni du nouvel &quivalent en sterling du taux de change. A cet 6gard, unemodification inf6rieure A 10% de la valeur de la livre par rapport A la couronnedanoise ne sera pas consid~re comme importante. I1 est admis qu'une priode detrois mois devra s'6couler entre la notification d'une modification et l'entr6e envigueur de l'amendement ncessaire A la rdglementation visde au paragraphe 1.1.

2.5. Lorsqu'elle facture 1'exploitant, l'Administration ajoute aux frais uneredevance n'excrdant pas 5 % des frais, au titre des services rendus par l'Adminis-tration aux fins de la perception et de la comptabilisation des frais (autres que lescofots et les d6penses visdes au paragraphe 4.4). De temps A autre, l'Administrationinformera la Direction de 'aviation civile du Danemark (« DAC ) de la base surlaquelle la redevance est calculre.

3.1. Le paiement par l'exploitant est exigible au moment du vol concern6 etrrglable en sterling A l'Administration par la personne qui exploite l'adronef aumoment du vol. S'il existe un doute s'agissant de l'identit6 de l'exploitant, l'Admi-nistration peut notifier la personne qu'elle estime 8tre le propridtaire de l'arronef aumoment du vol qu'elle le consid~re comme 6tant l'exploitant jusqu'h ce que leditpropri6taire ait W en mesure de ddmontrer qu'une autre personne est l'exploitant;aussi longtemps que cela n'aura pas 6t6 fait, ledit propridtaire demeure responsabledu paiement. Toutes les mentions relatives A l'exploitation au prdsent Mdmorandumseront ainsi interprdtres.

3.2. Tous les montants pergus par l'Administration en vertu des presentsarrangements (A l'exclusion des frais vises au paragraphe 2.5) seront versds en ster-ling mensuellement par 1'Administration A la DAC, avec une indication du mon-tant total vers6, ventilM selon la nationalit6 des exploitants. Le Gouvernement duRoyaume-Uni facilitera la remise au Danemark, en sterling, des montants dont ils'agit.

4.1. La DAC informera l'Administration hebdomadaire des vols effectus Atravers la r6gion de renseignements sur les vols de Sondrestrom, en fournissant les616ments suivants:

Vol. 1920, 1-32783

1996 United Nations - Treaty Series * Nations Unies - Recueil des Traitks 9

a) Le nom de l'exploitant ou du propridtaire;

b) La date du vol;

c) Si possible, le num6ro de vol ou, A d6faut, les marques d'enregistrement etde la nationalitd de l'aronef;

d) Les points d'origine et de destination du vol;

e) Le type d'a6ronef, s'il est connu;6tant entendu que lesdits renseignements n'auront pas A &re fournis si, au coursdu vol, l'a~ronef traverse la r6gion des renseignements sur les vols oc6aniques deShanwick.

4.2. Les deux gouvernements s'efforceront d'obtenir des renseignementssimilaires A l'intention de l'Administration s'agissant des vols auxquels les presentsarrangements s'appliquent et qui traversent les r6gions de renseignements sur lesvols g6rds par d'autres gouvernements et qui s'6tendent au nord du 45e paralllenord, autres que les vols au cours desquels les a6ronefs traversant la rgion derenseignements des vols de Sondrestrom ou la r6gion de renseignements des volsocaniques de Shanwick.

4.3. Le Gouvernement du Royaume-Uni veillera A ce que l'Administrations'efforce de percevoir les montants dus en vertu de la r6glementation vis6e au para-graphe 1.1, et qu'en cas de difficult6 A percevoir les montants dus, l'Administrationengagera des consultations avec le DAC concernant les meilleures dispositions Aprendre. Le Gouvernement du Danemark ne s'oppose pas A l'exercice d'unejuridic-tion des tribunaux du Royaume-Uni s'agissant de la perception des montants dusquelle que soit la nationalit6 de l'a~ronef concern6 ou de son exploitant, et quel quesoit 1'endroit oit la responsabilit6 a pris naissance.

4.4. L'Administration ne sera pas oblig6e de ddtenir un a6ronef ou d'engagerdes proc&lures judiciaires aux fins du recouvrement des montants dus, et n'en-treprendra aucune de ces d6marches sans le consentement de la DAC. Au cas oal'Administration proc&lerait ainsi A d6faut dudit consentement, le Gouvernementdu Danemark indemnisera l'Administration des coots et autres d6penses encouruspar celle-ci et la mettra hors de cause s'agissant de toute responsabilit6 concernantla d6tention de l'a~ronef, quelle que soit l'importance desdits coats, d6penses etresponsabilit6.

4.5. Il sera loisible aux deux gouvernements de d6cider de suspendre lesefforts pr6vus par les pr6sents arrangements aux fins de la perception d'un montantdonn6; en pareil cas, la question sera trait6e conformdment aux arrangements fix6sou A fixer conform6ment A l'Accord.

5. Le Gouvernement du Royaume-Uni veillera A ce que l'Administrationmaintienne des livres de compte en bon dtat concernant la perception des montantsen vertu des pr6sents arrangements et autorise le DAC et I'OACI t v6rifier lesditscomptes A intervalles raisonnables ainsi que les quittances pertinentes. A cette fin,lesdits comptes et quittances seront conserves par l'Administration pendant unep6riode de trois ans suivant 'exigibilit6 du paiement par l'exploitant.

6. Aucune des pr6sentes dispositions ne s'applique aux a~ronefs militaires.Un a6ronef qui figure sur le registre civil d'un Etat ne sera pas consid6r6 comme6tant un adronef militaire.

Vol. 1920, 1-32783

United Nations - Treaty Series * Nations Unies - Recueil des Traitks

7.1. L'un ou l'autre des gouvernements peut d6noncer les pr6sents arrange-ments moyennant un prAavis 6crit d'au moins 12 mois adress6 A l'autre gouverne-ment ledit pr6avis devant expird au plus t6t le dernier jour de l'ann6e qui suit l'ann6eau cours de laquelle il a 6t6 recu.

7.2. A la suite de la d6nonciation de l'Accord par l'une ou l'autre des PartiesA 1'occasion de toute modification importante touchant son ex6cution, lesdits arran-gements feront l'objet d'une 6valuation par les deux gouvernements A la suite d'unedemande de l'un ou l'autre d'entre eux.

8. Tout diff6rend qui pourrait surgir entre les deux gouvernements s'agissantde l'interpr6tation ou de l'application des presents arrangements sera soumis A unarbitre d6sign6 conjointement par les deux gouvernements ou, si les gouvernementsne peuvent se mettre d'accord sur la d6signation d'un arbitre mutuellement accep-table, par le Pr6sident de la Cour europ6enne de Justice sous r6serve que celui-ci nesoit pas un ressortissant du Royaume-Uni ou du Danemark ou, en pareil cas, par lejuge le plus ancien de ladite Cour, conform6ment A l'ordre de pr6s6ance 6tabli parl'article 6 du rglement intdrieur de ladite Cour et qui n'est pas un tel ressortissant.Les deux gouvernements se conforment A la d6cision de l'arbitre.

Londres, le 2 d6cembre 1982

Pour le Gouvernementdu Royaume du Danemark:

I. J. KELLAND

Pour le Gouvernementdu Royaume-Uni de Grande-Bretagne et d'Irlande du Nord:

J. W. D. GRAY

Vol. 1920, 1-32783

United Nations - Treaty Series * Nations Unies - Recueil des Trait~s

EXCHANGE OF NOTES CONSTITUTING AN AGREEMENT' BE-TWEEN DENMARK AND THE UNITED KINGDOM OF GREATBRITAIN AND NORTHERN IRELAND AMENDING THEMEMORANDUM OF UNDERSTANDING OF 2 DECEMBER 1982REGARDING THE BILLING AND COLLECTION BY THEUNITED KINGDOM OF AIR NAVIGATION CHARGES LEVIEDBY DENMARK

MINISTRY OF FOREIGN AFFAIRS

Note verbale

The Ministry of Foreign Affairs has the hon-our to refer to the Joint Financing Agreementcovering Air Navigation Services between theInternational Civil Aviation Organization(ICAO) and the Government of the Kingdomof Denmark2 and to the decision of the Councilof ICAO on 9 July 1992 to propose amend-ments to the said Agreement in order to recoverthe full costs of facilities and services providedby ICAO to administer the said Agreementthrough an administrative fee to be included inthe user charges collected by the United King-dom Civil Aviation Authority on behalf of theGovernment of Denmark.

As a consequence, it will be necessary tomodify the terms of the Memorandum ofUnderstanding between our two countriesdated 2 December 19823 and accordingly I have

the honour to propose that the said Memoran-dum be amended by the addition of the follow-ing new paragraph 3.3.:-

3.3. Notwithstanding the provisions ofparagraph 3.2, the Authority will remit toICAO that proportion of the charges, to bedetermined by the Council of ICAO, represent-ing the fee for the administration of the agree-ment by ICAO.,i

If the foregoing is applicable to your Gov-ernment, the Ministry has the honour to pro-pose that this letter and your reply should con-stitute an amendment to the Memorandum ofUnderstanding dated 2 December 1982 whichwill take effect with respect to charges collectedon and after I January 1993.

Copenhagen, 14 June 1993