Embed Size (px)

Citation preview

Chapter 3 reviewed the trends, opportunities,and policy challenges associated with inter-national migration. It also introduced theeconomic importance of the funds that inter-national migrants send back to their countryof origin. In recent years, those funds haveemerged as a major source of external financ-ing in developing countries. Although there isno universal agreement yet on how to measureinternational migrants’ remittances to devel-oping countries, a comprehensive measure ofcertain officially recorded flows—workers’remittances, compensation of employees, andmigrant transfers—produced an estimate of$167 billion for 2005, up from $160 billion in2004. Given measurement uncertainties,notably the unknown extent of unrecordedflows through formal and informal channels,the true size of remittance flows may be muchhigher—perhaps 50 percent or more. Becauseof their volume and their potential to reducepoverty, remittances are attracting growingattention from policymakers at the highestlevels in both developed and developingcountries.1

This chapter and chapters 5 and 6 considerremittances from several angles. The organiz-ing framework is driven by three items on theinternational policy agenda: (1) understandingthe true size and trends in remittance flows todeveloping countries, as well as their macro-economic impact; (2) evaluating the impact ofremittances on the households that receive

them; and (3) designing policies to reduce thetransaction costs of remittances, strengthenthe formal financial infrastructure supportingremittances, and leverage remittances to im-prove access to financial services in recipienteconomies.

Officially recorded remittance estimatesmay significantly underestimate the real mag-nitude of remittances. Model-based estimatesand household surveys suggest that informalflows could add at least 50 percent to the offi-cial estimate, with significant regional andcountry variation. The true size of remittanceflows could be even larger, in view of substan-tial underrecording of flows through formalchannels.

Despite the prominence given to remit-tances from developed countries, South–Southremittance flows make up 30–45 percent oftotal remittances received by developing coun-tries, reflecting the fact that over half ofmigrants from developing countries migrate toother developing countries. Remittance flowsto poor countries originate largely in themiddle-income developing countries.

Recorded remittance flows have surged inrecent years, driven by a combination offactors—among them better data collection,reflecting greater awareness of the develop-ment potential of remittances, as well as con-cerns about money laundering and terroristfinancing; lower costs and wider networks inthe industry that supports remittance; and

85

Trends, Determinants, andMacroeconomic Effects of Remittances

4

growth in the number of migrants and theirincomes. Government policies to improvebanking access and the technology of moneytransfers have also helped increase the flow ofremittances and promote their transferthrough formal channels.

Efforts to encourage remittances, however,sometimes generate unwanted effects. Taxincentives may attract remittance inflows, forexample, but they also create opportunitiesfor tax evasion. Likewise, matching-fundprograms for migrant associations may chan-nel collective remittances to developmentprojects, but in so doing they may divert fundsfrom other local funding priorities.

For some recipient countries, remittancesare large enough to have broader macroeco-nomic implications. By generating a steadystream of foreign-exchange earnings, theycan improve a country’s creditworthiness forexternal borrowing, and through innovativefinancing mechanisms (such as securitization),they can expand access to capital and lowerborrowing costs. While large and sustainedremittance inflows can contribute to currencyappreciation and so affect the production ofcost-sensitive tradables (such as labor-intensive manufactures), this outcome maybe less severe than it is in the case of natural-re-source earnings (since remittances are distrib-uted more widely and may avoid exacerbatingthe strains on institutional capacity that areoften associated with natural-resourcebooms). Furthermore, the “Dutch disease”effects of remittances are of relatively minorconcern insofar as remittances grow graduallyover long periods. Remittances have a largepositive effect on national income in many de-veloping countries, and there is compellingevidence that they contribute significantly topoverty reduction (see chapter 5). Althoughthe evidence on the effect of remittances onlong-term growth remains inconclusive, ineconomies where the financial system is under-developed, remittances appear to alleviatecredit constraints and may stimulate economicgrowth.

The plan of this chapter is as follows. In thenext section, trends in remittance flows to de-veloping countries are presented along with arange of estimates for their true size—that is,with informal flows included. We identify themajor sending and receiving countries, includ-ing those in the South. In the following sec-tion, we examine the factors affecting remit-tance flows, including the prospects for futureremittance growth, and policies and regula-tions in source and destination countries thataffect the cost of remittances. In the final sec-tion, we consider the macroeconomic effectsof remittances, including the effects on sta-bility, country creditworthiness, internationalcapital-market access, the real exchange rate,and competitiveness.

Remittance data and trends

The quality and coverage of data on remit-tances leave much to be desired. First, there

is no consensus on the boundaries of the phe-nomenon under study. Should only workers’ re-mittances be counted, or should we includecompensation of employees and migrant trans-fers? (See annex 4A.1 for more details on thesenomenclatural disputes.) Second, in severalcountries, many types of formal remittanceflows go unrecorded, due to weaknesses in datacollection (related to both definitions and cov-erage).2 Reporting of “small” remittance trans-actions made through formal channels is notmandatory in most countries,3 and remittancessent through post offices, exchange bureaus,and other agents of money transfer operators(MTOs) are often not reflected in official statis-tics (de Luna Martinez 2005). Third, flowsthrough informal channels (such as unregulatedmoney transfer firms or family and friends whocarry remittances) are rarely captured. Finally,remittances are often misclassified as exportrevenue, tourism receipts, nonresident deposits,or even foreign direct investment (FDI). Im-proving the quality of remittance statistics is thefocus of ongoing cooperative internationalefforts (see box 4.1).

G L O B A L E C O N O M I C P R O S P E C T S 2 0 0 6

86

Officially recorded remittance flows are surgingIn this report (as in past editions of the WorldBank’s annual Global Development Financeand the IMF’s 2005 World Economic Out-look), migrant remittances are calculated asthe sum of workers’ remittances, compensa-tion of employees, and migrant transfers (seeannex 4A.1). Thus defined, remittances re-ceived by developing countries, estimated

using officially recorded data, rose to$167 billion in 2005, up 73 percent from2001 (table 4.1). More than half of that in-crease occurred in China, India, and Mexico.Low-income countries, led by India, registeredan increase of $18 billion during this period(box 4.2). Of 34 developing countries that re-ceived remittances in excess of $1 billion in2004, 26 countries registered more than30 percent growth during 2001–4: Algeria

T R E N D S , D E T E R M I N A N T S , A N D M A C R O E C O N O M I C E F F E C T S O F R E M I T T A N C E S

87

Box 4.1 International working group on improvingdata on remittances

resident households to or from nonresident house-holds, and “net” compensation of employees frompersons working abroad for short periods of time(less than one year).

The TSG also recommended that institutionalremittances—those involving government, cor-porations, and nonprofit institutions serving households—should also be reported as a new mem-orandum item in the standard presentation ofbalance-of-payments statistics. That item would leadto a further memorandum item, “total remittances,”the sum of personal and institutional remittances.

Because the concepts of personal transfers andremittances are based on the concept of residencerather than migration status, the TSG recommendedthat the concept of “migrant” be replaced by theconcept of “residence” in the balance-of payments-framework. Reporting of bilateral remittance flowsis not currently required in the balance of payments,but the recommendation of the TSG is that flows toand from major partner countries be identified.

The TSG is expected to produce a final report inspring 2006.a

aA concurrent effort to improve remittance statistics isunder way at the Center for Latin America Monetary Studies(CEMLA) with support from the Multilateral Investment Fundof the Inter-American Development Bank and technical advicefrom an international advisory council that includes the IMFand World Bank.

At its meeting in Sea Island in April 2004, the G-8called upon the international financial institu-

tions (IFIs) to lead a global effort to improve remit-tance statistics. In January 2005, the World Bankand International Monetary Fund (IMF) held aninternational meeting of data users and compilerswho agreed that balance-of-payments statistics werethe appropriate framework for collecting, reporting,and improving official statistics on remittances; thatbalance-of-payments concepts and definitions relat-ing to remittances should be reviewed; and thatimproved guidance for collecting and compilingremittance statistics, including through the use ofhousehold surveys, was needed. Participants at theinternational meeting also agreed that improvementsto relevant statistical concepts and definitions shouldbe discussed in a Technical Sub-Group on the Move-ment of Persons (TSG), chaired by the UN StatisticsDivision with membership from central banks andnational and international statistical agencies.

The TSG recommended that the “workers’ remit-tances” item in the balance of payments be replacedby “personal transfers.” The new term would coverall current transfers in cash or in kind made orreceived by resident households to or from othernonresident households. It went on to recommendthat a new aggregate, “personal remittances,” bereported in the standard balance-of-payments presen-tation as a memorandum item. It was proposed thatpersonal remittances comprise current and capitaltransfers in cash or in kind, made or received, by

and Guatemala reported more than a tripling ofremittance inflows; Brazil, China, Honduras,Nigeria, Pakistan, and Serbia and Montenegroreported growth in the range of 101–170 per-cent. (Also, five high-income countries—Austria, Australia, Belgium, Germany, andSpain—reported 45–79 percent growth inremittance inflows during 2001–4.)

The growing importance of remittances asa source of foreign exchange is reflected in thefact that remittance growth has outpacedprivate capital flows and official develop-ment assistance (ODA) over the last decade(table 4.2). Recorded remittance receipts wereequivalent to about 6.7 percent of developingcountries’ imports and 7.5 percent of domes-tic investment. They also were larger than of-ficial flows and private equity (non-FDI) flowsin 2004. Remittances were larger than publicand private capital inflows in 36 developingcountries in 2004 and larger than totalmerchandise exports in Albania, Bosnia and

Herzegovina, Cape Verde, Gaza, Haiti,Jamaica, Kiribati, Lebanon, Nepal, Samoa,Serbia and Montenegro, and Tonga. In an-other 28 countries, they were larger than theearnings from the most important commodityexport; for example, in Mexico, remittancesare larger than FDI; in Sri Lanka, they arelarger than tea exports; and in Morocco, theyare larger than tourism receipts.

G L O B A L E C O N O M I C P R O S P E C T S 2 0 0 6

88

Table 4.1 Workers’ remittances to developing countries, 1990–2005 $ billions

Change (%)1990 1995 2000 2001 2002 2003 2004e 2005e 2005–2001

Developing countries 31.2 57.8 85.6 96.5 113.4 142.1 160.4 166.9 73Lower middle income 13.9 30.0 42.6 47.4 57.3 72.5 83.5 88.0 86Upper middle income 9.1 14.5 20.0 22.3 23.0 27.8 33.0 33.8 52Low income 8.1 13.3 22.8 26.8 33.1 41.8 43.9 45 68Latin America and the 5.8 13.4 20.1 24.4 28.1 34.8 40.7 42.4 74

CaribbeanSouth Asia 5.6 10.0 17.2 19.2 24.2 31.1 31.4 32.0 67East Asia and the 3.3 9.7 16.7 20.1 27.2 35.8 40.9 43.1 114

PacificMiddle East and North 11.4 13.4 13.2 15.1 15.6 18.6 20.3 21.3 41

AfricaEurope and Central 3.2 8.1 13.4 13.0 13.3 15.1 19.4 19.9 53

AsiaSub-Saharan Africa 1.9 3.2 4.9 4.7 5.2 6.8 7.7 8.1 72

World (developing & 68.6 101.6 131.5 147.1 166.2 200.2 225.8 232.3 58industrial)

Outward remittances from 6.1 12.5 12.1 14.3 18.7 20.2 24.1 – –developing countries

Outward remittances from 11.2 16.6 15.4 15.1 15.9 14.8 13.6 – –Saudi Arabia

Source: World Bank staff estimates based on IMF BoP Yearbook 2004 and country sources.Note: Remittances are defined as the sum of workers’ remittances, compensation of employees, and migrant transfers (seeannex 4A.1). e � estimate.– Data not available.

Table 4.2 Recorded remittances havegrown faster than private capital flows and ODA$ billions

1995 2004

Workers’ remittances 58 160Foreign direct investment 107 166Private debt and portfolio equity 170 136Official development assistance 59 79

Source: World Bank (2005).

T R E N D S , D E T E R M I N A N T S , A N D M A C R O E C O N O M I C E F F E C T S O F R E M I T T A N C E S

89

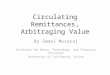

India has reported a spectacular increase in remit-tance inflows—from $13 billion in 2001 to more

than $20 billion in 2003 (see figure). Several factorsaccount for this remarkable increase. First, the num-ber of migrants has grown sharply. During the oilboom in the 1970s and 1980s, thousands of low-skilled Indian workers migrated to the Persian Gulfcountries. In the 1990s, migration to Australia,Canada, and the United States, increased signifi-cantly, particularly among information technology(IT) workers on temporary work permits.a

Second, the swelling of migrants’ ranks coincidedwith (a) better incentives to send and invest money

Box 4.2 The recent surge in remittance flows to Indiain India’s growing economy and (b) an easing of theregulations and controls, more flexible exchangerates, and gradual opening of the capital account.The elimination of the black-market premium on therupee and convenient remittance services provided byIndian and international banks have no doubt shiftedsome remittance flows from informal hawala chan-nels to formal channels.

Third, nonresident Indians have also respondedto several attractive deposit schemes and bondsoffered by the government of India. These offerattractive interest rates and an appreciating rupee.While nonresident deposits are conceptually differ-ent from remittances (they are a liability item inthe capital account), evidence suggests that a largepart of such deposits is converted to local currency.For example, for the Resurgent India Bond thatmatured in 2003, most of the redemption valuestayed in India to meet various local currencyneeds of the nonresident depositors and their fami-lies. Nevertheless, remittances in the form of for-eign-currency deposits can be speculative and mayreverse in the event of deterioration in theinvestment sentiment.

aIn particular, migration to United States doubled duringthe 1990s. Remittances from United States as a share of totalremittances to India grew from 37 percent in 1997 to 51 per-cent in 2003.

Remittance flows to India

1987

$ billions

0

5

10

15

20

25

1988

1989

1990

1991

1992

1993

1994

1995

1996

1997

1998

1999

2000

2001

2002

2003

Figure 4.1 identifies the top 20 remittancerecipients in 2004. Among developing coun-tries, China, India, Mexico, and the Philippineswere among the top recipients. Several indus-trial countries appear in this list as well.

When remittances are calculated in percapita terms or as a share of GDP, a differentpicture emerges. The top 20 recipients inshares of GDP are all developing countries;all receive more than 10 percent of GDP asremittance flows (figure 4.1). Small countries(Bosnia and Herzegovina, Haiti, Lesotho,Moldova, and Tonga) are among the most de-pendent on remittances.

High-income countries are the dominantsource of global remittance flows (figure 4.2).The United States was the largest sourcecountry with nearly $39 billion in outwardremittances in 2004. However, outwardremittances from developing countriesamounted to $24 billion in the same year.4

When expressed in terms of GDP shares, out-ward remittances play the largest role in theupper-middle-income developing countries(0.7 percent of GDP in these countriescompared to 0.2–0.4 percent in other devel-oping countries and in high-income countries;figure 4.2).

G L O B A L E C O N O M I C P R O S P E C T S 2 0 0 6

90

Figure 4.1 Top 20 remittance-recipient countries, 2004

21.7

21.3

18.1

12.7

11.6

6.9

6.8

6.5

6.4

4.2

4.1

3.9

3.6

3.4

3.3

3.2

3.2

3.2

3.0

2.8

0 5 10 15 20 25 0 15 30 45

31.1

27.1

25.8

24.8

22.5

20.4

17.4

17.2

16.2

15.5

13.5

13.2

12.4

12.4

12.1

11.9

11.7

11.7

11.3

10.0

Tonga

Moldova

Lesotho

Haiti

Bosnia and Herzegovina

Jordan

Jamaica

Serbia and Montenegro

EI Salvador

Honduras

Philippines

Dominican Rep.

Lebanon

Samoa

Tajikistan

Nicaragua

Albania

Nepal

Kiribati

Yemen, Rep.

Billions of dollars Share of GDP

Source: IMF BoP Yearbook, 2004, and World Bank staff estimates.

India

China

Mexico

France

Philippines

Spain

Belgium

Germany

United Kingdom

Morocco

Serbia

Pakistan

Brazil

Bangladesh

Egypt, Arab Rep.

Portugal

Vietnam

Colombia

United States

Nigeria

South–South remittance flows are considerableOfficial data show that several developingcountries (China, Malaysia, and the RussianFederation) are among the top 20 sources ofremittances. Anecdotally, outward remittancesfrom India and South Africa are also believedto be large, although this is not reflected in theofficial data (Genesis Analytics 2005). TheWorld Bank (2005a) points out a strong asso-ciation between remittance receipts and thelength of the border shared with more pros-perous neighbors. Harrison and others (2004)also report that most remittance flows occurwithin the same region.

These factors all point to the conclusionthat South–South remittance flows are sub-stantial. But placing more precision on theseflows is hard to do. First, relatively little isknown about bilateral migration flows—thatis, about how many migrants (or what share)in each receiving country come from each

sending country. Comprehensive global dataare not available,5 but estimates are that inpoor countries of East Asia, South Asia, andSub-Saharan Africa, more than two-thirds ofemigrants migrate to a country in the same re-gion. In South Asia and Sub-Saharan Africa,most migrate to another developing country.

Second, even less is known about how bi-lateral remittance patterns differ. We do notknow, for example, how much, in total, is sentfrom one country to another, or how remit-tance propensities differ across sending andreceiving countries. But by making plausibleassumptions about these flows (in particular,that bilateral remittances are a function of thestock of migrants in the sending country), itis possible to estimate bilateral remittanceflows and to calculate what proportioncomes through South–South links.6 Using thismethod, we estimate that nearly 30 percent oftotal remittance flows to developing countriesoriginate in other developing countries. This

estimate is consistent with the fact that nearlyhalf of the migrant stock from the South mi-grate to another country in the South.7

One of the challenges of understandingremittance flows is that their characteristics,costs, and channels can vary widely from onebilateral corridor to another (and also widelyfrom different locations within each country).Understanding how remittance corridorsdiffer in the kinds of migrants they serve andtheir means of transferring money is useful forproviders of remittance services as well as pol-icymakers (Hernandez-Coss 2004; Terry2005; and chapter 6 of this volume). Some ofthe major remittance corridors are those thatconnect Canada and the United States to LatinAmerica and Asia; the European Union to

Eastern Europe, Turkey, and North Africa;and the Persian Gulf to South and SoutheastAsia.

Informal remittances are largeRemittances transferred through informaloperators or hand carried by travelers areunlikely to be captured in official statistics,although they may represent a substantialaddition to remittances sent through officialchannels. While it is extremely difficult to es-timate the flows through informal channels,they appear to be large. First, the fact thatrecorded remittances to several countriesthrough formal channels doubled, tripled, orquadrupled between 2001 and 2003 suggeststhat a significant part of the increase is likelyto reflect a shift from informal to formal chan-nels in response to the tightened regulatoryscrutiny that has occurred since September 11,2001.

Second, evidence from household surveyssuggests widespread use of informal remit-tance channels (table 4.3).8 Household sur-veys also help identify factors affecting the useof remittance channels. In the presence of awell-developed formal sector, regular remittersand large remitters are unlikely to use theinformal sector. Trust in the financial system isan important prerequisite for a growing bankpresence in the (formal) remittance market.

High remittance costs and the presence ofdual exchange rates are two key factorsaffecting the choice of informal remittance

T R E N D S , D E T E R M I N A N T S , A N D M A C R O E C O N O M I C E F F E C T S O F R E M I T T A N C E S

91

Billions of dollars

Share of GDP

Low-incomecountries

Lower-middle-income

countries

Upper-middle-income

countries

High-incomecountries

Figure 4.2 Estimated remittance payment,by country group, 2004

125.3

15.45.73.0

Low-incomecountries

Lower-middle-income

countries

Upper-middle-income

countries

High-incomecountries

0.4

0.7

0.2

0.3

Table 4.3 Choice of remittance channel in selected countries % remittances

Formal Informal

Dominican Republic 96 4Guatemala 95 5El Salvador 85 15Armenia 62 38Moldova 53 47Bangladesh 46 54Uganda 20 80

Source: World Bank staff estimates based on householdsurveys. See also Freund and Spatafora 2005.

channels.9 If there were no cost advantages tousing informal channels, there would be littleincentive to use them, and remittances couldarguably shift entirely to formal channels.Thus if the costs of formal transfers werereduced to the range reported in the informalsector (2–5 percent), and if official and paral-lel exchange rates were unified, the resultantincrease in recorded remittance flows couldbe interpreted as an estimate of the size ofinformal flows.

Table 4.4 reports the results of an exerciseto estimate the size of the informal remittancesector (see annex 4A.2 for a fuller explana-tion). Cross-country regression analysisshows that reported remittances are lower,and informal flows higher, in corridors whereremittance costs are higher and where thereare significant black-market premiums overthe official exchange rate. Using the estimatedcoefficients from these regressions, thepredicted increase in officially recorded remit-tances is calculated in response to a 2–5 per-cent decline in remittance costs and elimina-tion of the exchange-rate premium. Thesecalculations suggest that the informal remit-tance sector is at least 50 percent of the

official sector.10 They also show significantregional variation. Informal remittances ap-pear to be larger in Sub-Saharan Africa, theMiddle East and North Africa, and Europeand Central Asia than in other regions.11

While the magnitude of the regional estimatesvaries across methods, the relative ranking ofregional effects is more robust.

Factors affecting remittance flows

The surge in remittance flows over the pastfew years reflects a mix of factors, as

noted. In some areas, there have been signifi-cant reductions in remittance costs—60 per-cent in the United States–Mexico corridorsince 1999. On the measurement side, the size-able depreciation of the dollar against mostother major currencies (the euro in particular)since 2002 has increased the dollar value ofnondollar remittances over time.12 Improve-ments in data recording by central banks—inresponse to growing recognition of the impor-tance of remittances by national authorities,and as a result of broader efforts to improvedata quality—have generated sharp increasesin remittance flows in some cases. In addition,heightened security and scrutiny by immigra-tion and finance authorities in many high-income countries may have encouraged out-ward surges in remittances, as undocumentedmigrants responded to increased uncertaintyand risk of deportation or other legal action byremitting a larger share of their savings orincome. This factor has reportedly been im-portant in Pakistan, which recorded a triplingof remittance receipts from 2001 to 2003.

The surge in remittances is likely tocontinue in the medium termIn addition to these special factors, powerfuleconomic factors also influence the growthof remittances. Increases in the number ofmigrants will have the greatest and most directimpact, of course, along with compositionalfeatures, such as the mix between temporaryand permanent workers (temporary workers

G L O B A L E C O N O M I C P R O S P E C T S 2 0 0 6

92

Table 4.4 Estimated increase in formalremittances if transaction costs werereduced to 2 to 5 percent and dualexchange rates were eliminatedPercent

Cross-sectional PanelRegion estimates estimates

All developing countries 69 54Sub-Saharan Africa 201 122Eastern Europe and Central Asia 151 73East Asia and the Pacific 56 ..South Asia 25 55Middle East and North Africa 165 ..Latin America and the Caribbean 51 99

Source: Freund and Spatafora 2005.Note: Results averaged over 1995–2003. See annex 4A.2 fora fuller explanation of the procedures used. In column 3,a reduced form equation is estimated on the basis of theexplanatory variables used in the cost regression reported intable 4A.2.2... Negligible.

are believed to remit a larger share of theirincome) and the skill mix (low-skilled workerstend to send a higher proportion of their lowerincomes). Employment opportunities in thehost country affect income, and thereforeremittances, while changes in the cost of livingmay affect the size of the surplus that remittersare able to send.

The complex interplay of these factorsmakes assessing the future growth potential ofremittance flows quite difficult. It is plausiblethat in the coming years, official remittanceflows will continue to rise at the 7–8 percentannual rate seen during the 1990s. With boththe supply and demand for migrants grow-ing, migration flows—especially temporarymigration—are likely to continue to be strong.Growing income levels in source countries andrising costs of living in receiving countries,together with the falling costs of remittances,would also imply larger remittances, espe-cially through recorded channels.

It is unlikely, however, that the surge inremittance flows seen in some countries since2001 will continue much longer. The shift inflows from informal to formal channels, to theextent that it occurred in response to tightenedscrutiny, is likely to dwindle. (In Pakistan,for example, remittance flows have flattenedsince 2003.) In the more mature UnitedStates–Mexico corridor, where remittancecosts have already fallen drastically (by 60 per-cent since 1999), the effect of further costreduction will not be as large as it was fiveyears ago.

Some analysts argue that in the more maturemarkets, “remittance decay” may set in, espe-cially if temporary or undocumented workersare allowed permanent and legal residence.While it is true that the marginal propensity toremit tends to decline with the length of a mi-grant’s stay in a host country, and ties with thehome country weaken over time, there is noempirical evidence that the dollar amount ofremittances actually declines in these circum-stances.13 On the contrary, the effect of risingincomes of the migrant sender may show up asan increase in remittances over time.

Government policies can affect remittance flowsMany sending and receiving governmentsare only now beginning to think about policiesto increase remittance flows and promotetransfers through formal channels. In theremittance-receiving countries, these policiesinclude tax exemptions for remittance in-come; improved access to banking services byrecipients; incentives to attract investmentsby the diaspora; access to foreign exchangeor lower duties on imports; support for theprojects of migrant associations; and help formigrants in accessing financial systems. In theremittance-source countries, they include poli-cies affecting access to banks, access to foreignexchange, support to migrant groups, types ofimmigration regimes, and cooperation withreceiving countries.14

Policies in remittance-receiving countriesTaxes on incoming remittances. Mostremittance-receiving countries today do notimpose taxes on incoming remittances. Theremay be some implicit tax on remittances, how-ever, in the form of a general financial servicestax15 or on remittances in kind (for example,food, clothing, electronic items, or vehicles).When Vietnam removed its 5 percent tax onremittances in 1997, it found that the flow ofremittances through formal channels in-creased. Such tax exemptions may well in-crease remittance inflows,16 but they also raisethe possibility of misuse for tax evasion.

Travel and customs privileges for returns andimported goods. Many remittance-receivingcountries give preferential treatment tomigrants sending home or bringing with themgoods and equipment. For example, once ayear Tunisians are entitled to import goodsand/or services up to a customs value ofTD1,000 without paying tax, and a privatevehicle, home equipment, and furniture aretax free when they return; Guatemala permitsa once-a-year tax-free remittance of any com-modity valued up to $500. Pakistan, Turkey,Vietnam, and many other countries also offersuch import privileges.17

T R E N D S , D E T E R M I N A N T S , A N D M A C R O E C O N O M I C E F F E C T S O F R E M I T T A N C E S

93

Relaxation of exchange and capital controls.Unification of exchange rates and allowingmore banks and financial institutions to un-dertake foreign exchange transactions havebeen among the most successful ways of at-tracting remittances to formal channels andexpanding remittance services in many coun-tries. Also, allowing residents to hold foreigncurrency deposits using remittances fromabroad is believed to have resulted in a largeincrease in formal remittances in many coun-tries in South Asia and Africa (Siddiqui 2004).India’s liberalization of the exchange rate in1991 has been linked to a decrease in the useof illegal transfer channels to the state ofKerala; and the Philippines found that byabolishing exchange controls it quadrupled itsformal inward remittances in the same year(Buencamino and Gorbunov 2002). Allowingthe market to decide exchange rates in 2002also helped the Bangladesh Bank to curb theinformal hundi business significantly (Siddiqui2004). In 2004, an increase in foreign cur-rency reserves in Zimbabwe was ascribed, inpart, to the introduction of a new moneytransfer system (Homelink) set up by the gov-ernment to facilitate formal transfers.

Allowing domestic banks to operate overseas.Governments have allowed more of theirdomestic financial institutions (includingmicrofinance institutions in some countries) toopen branches and provide services to theirmigrants working in other countries. Thesedomestic banks bring trust and offer remit-tance services at competitive prices. For exam-ple, the Groupe Banques Populaires haspicked up 66 percent of total remittances toMorocco by offering low fees, simple proce-dures, and other nonfinancial services toMoroccans abroad (Amin and Freund 2005).Two small Armenian banks specializing in re-mittance transfers, Anelik and Unibank, havecome to dominate the formal transfer systemfor Armenians in parts of Europe; andFonkoze in Haiti has expanded its U.S.–basedclientele in partnership with the City National

Bank of New Jersey. In Bangladesh the dra-matic increase in formal remittances since2001 is, in part, the result of the improved ser-vices of the banking sector (Siddiqui 2004).

ID cards for migrants. Providing identificationcards to migrants (regardless of their legal mi-gration status) to access banking facilities hasalso opened up more opportunities for formalremittance transfer. Mexican immigrants, forexample, can obtain a photo-identificationcard in the form of a matricula consular fromthe Mexican consulates abroad. This card iswidely accepted by commercial banks in theUnited States to open bank accounts (and inmany states, for issuing driving licenses, seebox 6.1). Other Latin American governmentsare discussing similar arrangements for theirnationals in the United States. Most sendingcountries require legal documentation for anybank transaction. Some receiving countriesissue ID cards to expedite domestic servicesfor their emigrants, for example, the Tunisiancarte consulaire for special customs clearance,reduced airfares, and foreign currency bankaccounts in Tunisia.18

Support to hometown associations (HTAs)and matching grants. Providing funds tosupplement or match collective remittancesmade by emigrant groups is another means toengage migrants in the development of homecommunities. With enhanced institutionalcapacities, HTAs could be valuable develop-ment partners for governments, the privatesector, and communities, but importantly as acomplement to, not a substitute for, strength-ened financial and investment systems on theground (Gubert 2005). A careful evaluation ofsupport to HTAs through matching grantschemes and other means is yet to be under-taken (see box 4.3).

Loans/pension schemes and bonds targeted atthe diasporas. These measures can expandopportunities for investment and provide in-centives for the formal transfer of money fromabroad (see also chapter 6). While investments

G L O B A L E C O N O M I C P R O S P E C T S 2 0 0 6

94

T R E N D S , D E T E R M I N A N T S , A N D M A C R O E C O N O M I C E F F E C T S O F R E M I T T A N C E S

95

Box 4.3 Collective remittances through hometownassociations and matching schemes

distribution of consumer goods (as in general storesor grain banks) or the purchase of farming equip-ment (Gubert 2005). In Latin America, it is observedthat when at least 30 percent of households in atown receive remittances, HTAs can help improvethe quality of life of households (IOM 2005). But thefocus of HTAs is expanding to include more invest-ment in economic infrastructure and income-generating projects managed by the community andlocal NGOs or banks (Orozco 2003).

Governments have, on occasion, offeredmatching grants for remittances from diasporagroups or HTAs to attract funding for specificcommunity projects.c The best known of thesematching schemes is Mexico’s 3-for-1 program,started in 1997, under which the local, state, andfederal governments all contribute $1 for every $1of remittances sent to a community for a designateddevelopment project. By 2002, the 3-for-1 programhad established projects totaling $43.5 million, two-thirds of which benefited labor-intensive agriculturaleconomies in four high emigration states (IOM2005). In the period 2002–4, more than 3,000 suchprojects benefited some 1 million inhabitants in23 Mexican states.d

Evidence from Mexico suggests, however, thatHTAs have not been very successful. But in somecases (for example, Zacatecas) where HTAs haveexchanged or debated project ideas and investment

Many migrants are increasingly pooling theirresources and investing collectively in

development-related activities in home communities,either through hometown associations (HTAs) orother migrant group schemes.a HTAs are the mostprominent, because of their proliferation among theLatin American and Caribbean diaspora in Canadaand the United States since the late 1990s. Similarassociations exist in France (some 1,000 organiza-tions de solidarite internationale issues de migrationsor OSIMs), the United Kingdom, and Africa.b Theactivities of HTAs are mixed and poorly docu-mented, but they range from diaspora support inthe host country to community investment projectsin villages in the home country.

Collective remittances via HTAs currently accountfor only 1 percent of all remittances in CentralAmerica, but it is estimated that they could rise to3–5 percent in ten years if their management andinstitutional capacity improves (IFAD 2005).

Most HTAs tend to be small scale and philan-thropic in orientation, and they invest in projects ofno more than $10,000. They have traditionallyfocused on infrastructure and social projects(schools, churches, recreational parks, medical out-reach clinics, and household support) and on chan-neling post-disaster humanitarian aid (for example,in El Salvador). In Africa, there is evidence that themore sustainable projects tend to facilitate household

in the form of nonresident deposits or dias-pora bonds are not, strictly speaking, remit-tances (because they involve the purchase ofassets, rather than transfers to households),they may indirectly encourage remittances.Many countries have successfully issued pre-mium bonds to their diaspora (forBangladesh, China, Eritrea, India, Israel,Lebanon, Pakistan and the Philippines, seeCarling 2005). Even when investments inthese bonds are in foreign currency terms,after maturity some portion is likely to remain

in the country. Such schemes were a major fac-tor behind the doubling of remittance flows toIndia between 2002 and 2003 (box 4.2).

Active policies and institutional arrangementsto support the diaspora. Countries likeMexico and the Philippines with more suc-cessful remittance programs tend to have wellestablished institutional frameworks to train,support, and ensure the welfare of their expa-triates abroad. There is also a broad range ofoutreach activities to assist migrant welfare

G L O B A L E C O N O M I C P R O S P E C T S 2 0 0 6

96

climate issues with the local and state governments,they are believed to have been successful.e

On the positive side, HTA involvement in projectsis argued to ensure that programs are focused oncommunity needs. Resources have gone primarily torural areas, where they have increased the supply ofessential services (health, education, roads, and elec-tricity). Donations by HTAs are often as much as ormore than the municipal budget for public works,particularly in towns with small populations (Orozco2003). HTAs can promote higher standards of trans-parency and accountability among local authorities,and higher labor standards.

There are obviously limitations on the potentialfor HTAs to serve as conduits for broader develop-ment projects. They may not have the best informa-tion about the needs of the local community, or theymay have different priorities. The capacity of HTAsto scale up or form partnerships is limited by the factthat their members are volunteers, and theirfundraising ability finite. They can also becomedivided and weaken their own advocacy potential(Newland and Patrick 2004). When matching fundscome from fiscally constrained governments, there isalso the problem that they may be diverted fromother—perhaps higher priority—development

Box 4.3 (continued)projects, or from other regions with a greater needfor assistance.

aHTAs are grassroots migrant organizations, usually formedaround the interests and needs of a mutual hometown. Theterm has been coined in the United States, where many thou-sands of Latin American and Caribbean HTAs have sprung upin the past 15 years or so (Orozco and Welle 2004).

bMigrant associations exist in many countries, but aremostly concerned with the conditions of the diaspora and net-working abroad. Some, like the Sierra Leonean Women’s Forumin the United Kingdom, are concerned with immediate survivalneeds (food, clothing) back home (Black and others 2004).

cIn addition to Mexico, the Salvadoran government partnerswith HTAs in rural development projects in El Salvador. In2001, the federation of HTAs (COMUNIDADES) and the Na-tional Corporation of Municipalities created the Social Invest-ment for Local Development Fund (FISDL) to providematching project funding. In France, the Osims can alsoreceive institutional and financial subsidies from the govern-ment for social and economic development projects back home(Magoni 2004).

dSee “3 por 1. Proyectos Compartidos,” prepared for theseminar “Migracion, remesas y el Programa 3 por 1 para Mi-grantes,” Secretaria de Desarollo Social, Mexico and IADB,Washington DC, June 2005.

eSee Gubert 2005, Iskander 2005, and Orozco 2004. Theliterature is not clear on what “success” means in these cases(beyond mere survival of the HTAs).

and promote remittances and investment inthe home country, from pre-migration infor-mation and orientation (Philippines), IDs forcustoms and other purposes (Colombia,Tunisia), finance for study (Tunisia), support inlegal and administrative disputes (Morocco),fairs and re-orientation visits for émigrés andtheir families (Colombia, Tunisia), shortenedmilitary service (and payment of fee in lieu,Turkey), hotline for migrant investors(Tunisia), and a diaspora trust fund (Nigeria).Some countries like Bangladesh, Egypt,Eritrea, Pakistan, Philippines, and Thailand(and Mexico and Turkey in the 1960s) havetried to impose mandatory remittance require-

ments on their émigrés, but with little success.Also, restrictive emigration policies have dri-ven migrants into using clandestine remittancechannels.19

Policies in remittance-source countriesOnly a handful of remittance-sending coun-tries have proactive remittance-supportingpolicies. Most are noninterventionist or havehad little engagement to date, but this ischanging with the growing appreciation of thesignificance of remittances for development incountries such as Australia, Canada, theUnited States, and most West European states(Ellerman 2003, Carling 2005). USAID has

undertaken extensive research on remittances,as has the United Kingdom’s Department forInternational Development (DFID) and theNorwegian International Peace Institute(PRIO). All propose ways forward for moreproactive policies by sending countries—forexample, to support migrant associations, fa-cilitate low cost, reduce bureaucratic remit-tance transfer, greater competition in the re-mittance market, and inform decision makingby migrants and affected communities.

Immigration policies. Policies that affect thesize, type, and tenure of migration flows alsoaffect remittance patterns. A larger migrationstock would in general imply larger remittanceflows to the country of origin. Given the mi-gration stock, a larger share of temporary

migrants is likely to lead to larger remittances.Also, as discussed above, the ties of migrantsto their home country weaken with the pas-sage of time, causing remittances to decline.

Given the personalized nature of remit-tances, governments are unlikely to have muchsuccess in using remittance policies to steermigration differently. Some countries, likeCanada, France, and Germany, have tried todirect remittance flows to investments in thehome country to encourage return migration,but these efforts have met with little success.There are also some examples of “forced” re-mittance transfer programs between sendingand receiving countries, although these raisevexing legal issues and do not appear to be ef-fective either in encouraging migrant return ormobilizing resources (box 4.4).

T R E N D S , D E T E R M I N A N T S , A N D M A C R O E C O N O M I C E F F E C T S O F R E M I T T A N C E S

97

While it is generally assumed that migrantworkers are free to choose how much, when,

and to whom to send money, there have been caseswhen sending or receiving governments, banks inthe home country, or employers have decided to re-tain a certain proportion of pay for remittances. Therationale for such “forced” remittances is to ensurethat temporary migrant workers do not stay on, butreturn home after the end of their contract. Some-times, the objective of such measures is to steer theuse of remittances to investment in the country oforigin.

For example, from 1942 to 1964 the “Braceroprogram” regulated migration of 4.6 million farmworkers between Mexico and the United States.From 1942–9, a tenth of the wages earned by thesebraceros was deducted from their pay by the U.S.employers and paid into accounts held by the Bankof Mexico at two commercial banks in San Fran-cisco. From there it was transferred to the Bank ofMexico and then on to the Banco de Credito Agri-cola. Alternatively, the employers gave the worker acheck for the deducted amount at the end of the con-tract to be cashed back home in Mexico. A 1946 re-port by the Mexican government claimed that

Box 4.4 Forced remittances $8 million in forced savings had been paid out to ex-braceros and only $6 million was unaccounted for;but the LA Times reported (on March 30, 2001) thata total of $34 million in forced savings was collectedduring 1942–6. The loss of the money was explainedby successive bank consolidations and restructuring,and as a result, records of accounts had disappeared(Migration News, http://migration.ucdavis.edu/mn).The braceros were mostly poorly educated peasants,who did not even know about the deductions andwho later were intimidated by the forms and corre-spondence needed to claim their money (LA Times).op.cit.). In March 2001, a class action suit was filedon behalf of former braceros at a San Francisco dis-trict court claiming $30 million–$50 million in sav-ings not returned and additional punitive damages.This claim was rejected because of the statute of lim-itations (San Francisco Chronicle, August 29, 2002).In 2003, the Mexican government agreed to reim-burse, within six months, an upfront sum of $150per person and then monthly rates of pesos 200 forup to pesos 60,000, provided the ex-braceros couldproduce identification (the Bracero Net program).

Forced remittances may also be used by a gov-ernment to encourage the use of remittances for

G L O B A L E C O N O M I C P R O S P E C T S 2 0 0 6

98

investment in the domestic economy. Under theDeferred Pay Scheme, mine workers from Lesothohave 30 percent (initially 60 percent, until 1990) oftheir pay deposited at a Lesotho bank and the bal-ance into a savings account at TEBA (The Employ-ment Bureau of Africa) Bank. The certificate con-firming the identity of the account holder is handedout by the TEBA Bank at the end of the contract,before the mine worker goes home to collect thebalance from the deferred pay scheme.

A similar arrangement is foreseen in the memo-randum of understanding between the Governmentsof Thailand and Laos on employment cooperation.All Laotian guest workers are obliged to pay 15 per-cent of their earnings into a “deportation fund” setup by the host country, Thailand. Workers who wishto return home can claim their contribution in fullwith interest. The request must be filed three monthsbefore the return date, and the money is to be paidto the workers within 45 days after the last day ofemployment (articles 11 and 12).

A milder form of induced remittances has beenintroduced for temporary Mexican farm workers inthe United States and Canada. Before their departurevisas and work permits are issued, the temporaryfarm workers register with the Ministry of Labor inMexico. After the papers are delivered, migrantsopen a savings account with the subsidiary or anassociated institution of a North American bank inMexico. Once they arrive in the United States orCanada, the temporary workers either make theremittance transaction themselves or arrange with

Box 4.4 (continued)the farmer-employer to pay directly into their savingsaccount via payroll deduction.

Forced savings of this type raise legal issues inthat they violate an accepted principle of wage pro-tection, that is, the idea that “wages shall be paid di-rectly to the worker concerned” (article 5 ILO Con-vention 95 of 1949). The only exception providedfor is that the “worker concerned has agreed to thecontrary.” It is not clear whether that has been thecase with the braceros or with the other examplescited here. Convention 95 states that “employersshall be prohibited from limiting in any manner thefreedom of the worker to dispose of his/her wages.”Article 8.2 further spells out that “workers shall beinformed of the conditions under which suchdeductions may be made.” (Mexico ratified thisconvention in 1955. The United States has notratified it.)

Forced remittances are also probably not the mosteffective measure to ensure that temporary migrantworkers return home. If they return, it is likely notdriven by their desire to reclaim their savings. Whenoffered a choice, migrants avoid such systems. InSouth Africa a considerable number of mine workersfrom Lesotho did not participate in the deferred payscheme, often in complicity with the mining compa-nies (Sparreboom 1996, p. 13). If the Lesotho de-ferred pay scheme was voluntary, then the volume ofsavings would drop to a level of the voluntaryschemes of workers from Botswana and Swaziland,namely 1 percent of the levels of the obligatoryscheme (TEBA 1995).

Banking and financial markets. Greater relax-ation and competition in money transfer mar-kets leads to reduced prices and more moneyreaching the beneficiaries. This process is fa-cilitated further by improving access of remit-tance service providers to national paymentand settlement systems. This seems to haveworked well within framed agreements suchas the United States–Mexican Partnership forProsperity program of 2001, involving thematricula consular to improve banking access

of Mexican immigrants in the United Statesand low-cost electronic transfers through theFederal Reserve Bank’s automated clearing-house system for Mexico (see chapter 6).Spain has initiated agreements betweenSpanish and Latin American financial institu-tions to reduce transfer fees and foster theentry of new agents into the financial market,particularly in rural areas. In the past,Germany worked closely with Turkey to en-courage remittances into formal channels

(UN 2005). In some remittance-source coun-tries, outward remittance flows are affected byexchange controls. For example, SouthAfrica’s policy of limiting foreign exchangedealings only to banks has prompted (un-banked) remitters to use informal channels—only 5 percent of remittances to other South-ern African Development Community (SADC)countries are being sent via formal channels,according to Genesis Analytics (2005).20

ID arrangements for migrants. The U.S. facil-itation of banking for both regular and irreg-ular migrants from Mexico through the ma-tricula consular mechanism has been highlysuccessful in drawing more migrants intosafer and cheaper remittance modes. The Fed-eral Deposit Insurance Corporation (FDIC)through its New Alliance Task Force initiative,in collaboration with the Mexican consulatesand commercial banks, has been successful inimproving banking access as well as the finan-cial literacy of immigrants.21

Support to HTAs or migrant associations.HTAs and similar entities receive some supportfrom host governments in the United States,France, and parts of Africa in recognition oftheir development assistance potential. WhileHTAs could potentially play a useful role incommunity infrastructure and other collectivelyfunded projects, their ability to effectively chan-nel large amounts of aid remains untested.22

Macroeconomic effects of remittances

Until recently most of the discussion andresearch on remittances was focused on

the (microeconomic) end use by the recipienthouseholds, including the effects on poverty(see chapter 5). But as outlined earlier in thischapter, the large size of remittances relative toother external flows and to the GDP in manycountries suggests that the macroeconomiceffects of remittances may be of critical impor-tance in many countries (recall that the top 19remittance recipients receive more than 10 per-cent of their GDP in remittances).

High levels (or large increases) in remit-tance flows can be expected to have directrepercussions on foreign exchange rates, do-mestic interest rates, and the balance of pay-ments, and indirect repercussions on macro-variables. Because of their relative stabilityand targeting (directly to households), theymay bring some additional benefits. However,as the experience with and analysis of naturalresource booms have shown, large inflows canalso have some undesirable side effects (seealso box 4.5). And to the extent that remit-tance flows may naturally just go to countriesthat are doing poorly or respond anticyclically(increase during downturns, due to a drought,for example), it may be hard to disentanglehow remittances affect macro-performance. Inthis section, we consider some of the macro-economic channels through which remittancesaffect recipient countries.

Remittances are stable and may be countercyclicalRemittances may move countercyclically rela-tive to the economic cycle of the recipientcountry. Remittances may rise when the recip-ient economy suffers a downturn in activity ormacroeconomic shocks due to financial crisis,natural disaster, or political conflict, becausemigrants may send more funds during hardtimes to help their families and friends. Re-mittances may thus smooth consumption andcontribute to the stability of recipient eco-nomies by compensating for foreign exchangelosses due to macroeconomic shocks.

Many authors have observed an increase inremittance inflows following a natural dis-aster (Clarke and Wallsten 2004) or an eco-nomic downturn (Kapur 2003). Yang (2004)showed that remittance receipts by Filipinohouseholds increased following the 1997 fi-nancial crisis. A 10 percent appreciation of amigrant’s currency against the Philippine pesoled to increases in household remittance re-ceipts and a 0.6 percentage point decline in thepoverty rate in migrant households. He alsofound evidence of positive spillover effects onhouseholds without migrant members due to

T R E N D S , D E T E R M I N A N T S , A N D M A C R O E C O N O M I C E F F E C T S O F R E M I T T A N C E S

99

increases in remittance-driven economic activ-ity as well as by direct transfers from the mi-grant’s origin household. Mishra (2005) findsthat a 1 percent decrease in real GDP was as-sociated with a 3 percent increase in remit-tances after a two-year lag in 13 Caribbeancountries during 1980–2002. To the extent thatremittances are used for investment purposes,however, they may behave procyclically just asother investment flows do. In Turkey and thePhilippines, remittances were more volatile andprocyclical in the 1990s than in the 1980s.23

Remittance flows (as a share of personalconsumption) continued to rise after naturaldisasters in Bangladesh, Dominican Republic,Haiti, and Honduras (figure 4.3). In Albania,after an initial disruption in remittanceinflows (as a share of personal consumption)in the year of conflict, remittance flows recov-ered quickly (figure 4.4). In Sierra Leone,remittances increased in the year of the con-flict.24 Remittances as a share of personalconsumption rose in response to the financialcrisis in Mexico in 1995 and in Indonesia andThailand in 1997 (figure 4.5).

Yang (2005) found that the increase in re-mittances makes up for 13 percent of incomelosses in the current year and 28 percent

within four years of a hurricane. In contrast,increases in ODA and FDI make up forroughly 26 and 21 percent, respectively,within four years.

Remittances can improve countrycreditworthinessRemittances can improve a country’s credit-worthiness and thereby enhance its access tointernational capital markets. The ratio of

G L O B A L E C O N O M I C P R O S P E C T S 2 0 0 6

100

Figure 4.3 Remittances as percent of private consumption, two years before and two yearsafter natural disasters

Bangladesh

�2 �1 0 �1 �2

Percent

�2 �1 0 �1 �2 �2 �1 0 �1 �2 �2 �1 0 �1 �2

Dominican Republic Haiti Honduras

0

2

4

6

8

10

12

14

20

16

18

Note: The bar marked 0 is the year of the natural disaster.

3.8 4.2 4.4 4.7 5.1

7.98.9

10.411.3 10.8

5.7 5.2 5.5 5.6

7.78.48.4

9.6

11.3

15.5

Albania

20

15

10

5

0

Sierra Leone

Figure 4.4 Remittances as a share ofpersonal consumption, two years beforeand two years after conflict

Percent

�2 �1 0 �1 �2 �2 �1 0 �1 �2

Note: The bar marked 0 is the year of the conflict.

2.9 3.2

0.7

16.9 16.9

12.7

17.0

12.3

1.0 0.8

debt to exports of goods and services, a keyindebtedness indicator, would increase signifi-cantly if remittances were excluded fromthe denominator (figure 4.6). Country creditratings by major international rating agenciesoften fail to account for remittances.25 Model-based calculations using debt-to-exportratios that include remittances in the denomi-nator indicate that including remittances increditworthiness assessments would improve

T R E N D S , D E T E R M I N A N T S , A N D M A C R O E C O N O M I C E F F E C T S O F R E M I T T A N C E S

101

Mexico Indonesia

2.5

2

1

1.5

0.5

0

Thailand

Figure 4.5 Remittances as a share ofpersonal consumption, two years beforeand two years after financial crises

1.2 1.1

2.0 2.11.9

0.5 0.5

�2 �1 0 1 2 �2 �1 0 1 2 �2 �1 0 1 2

1.4

1.01.1

1.51.7

2.01.8

2.0

Percent

Note: The bar marked 0 is the year of the financial crisis.

Lebanon Ecuador

Excluding remittances

Including remittances

Pakistan Philippines Jamaica Morocco Jordan El Salvador

700

800

600

500

400

300

200

100

0Guatemala

Figure 4.6 Indebtedness classification including and excluding remittances, 2003

Debt as percent of exportsa

732

355

257208

245193

151 127167

121 145114

190

126178

116 12482

Note: a. Present value of external debt as percent of exports of goods and services, and remittances.

Source: World Development Indicators, and World Bank staff calculations.

credit ratings for Lebanon and Haiti by twonotches; these would result in implied sover-eign spread reductions ranging from 130 to334 basis points (table 4.5).26

Remittance securitization can helpcountries raise external financingAnother way in which remittances affectinternational capital market access is throughthe use of structured finance techniques.Several banks in developing countries (forinstance, Brazil) have been able to raise rela-tively cheap and long-term financing frominternational capital markets via securitizationof future remittance flows.

Remittance securitization typically involvesthe borrowing entity (such as a bank) pledgingits future remittance receivables to an offshorespecial purpose vehicle (SPV). The SPV issuesthe debt (figure 4.7). Designated correspon-dent banks are directed to channel remittanceflows of the borrowing bank through an off-shore collection account managed by atrustee. The collection agent makes principaland interest payments to the investors andsends excess collections to the borrowingbank. Since remittances do not enter the is-suer’s home country, the rating agencies

believe that the structure mitigates the usualsovereign transfer and convertibility risks.Such transactions also often resort to excesscoverage to mitigate the risk of volatility andseasonality in remittances.

By mitigating currency convertibility risk,a key component of sovereign risk, the futureflow securitization structure allows securitiesto be rated better than the sovereign credit rat-ing. These securities are typically structured toobtain an investment grade rating. In the caseof El Salvador, for example, the remittance-backed securities were rated investment grade,two to four notches above the sub-investmentgrade sovereign rating. Investment-grade rat-

ing makes these transactions attractive to awider range of “buy-and-hold” investors (forexample, insurance companies) that face limi-tations on buying sub-investment grade. As aresult, the issuer can access international cap-ital markets at a lower interest rate spread andlonger maturity. Moreover, by establishing acredit history for the borrower, these dealsenhance the ability and reduce the costs ofaccessing capital markets in the future.

The first major securitization deal in-volving international migrant remittancesoccurred in 1994 in Mexico. The volume ofremittance securitization has grown rapidlysince then (figure 4.8a). Using this instrument,

G L O B A L E C O N O M I C P R O S P E C T S 2 0 0 6

102

Table 4.5 Impact of remittances on country credit rating and sovereign spread

Remittances as % Rating excluding Rating including Spread savingof GDP, 2004 remittances remittancesa (basis points)

Serbia and Montenegro 7 B� BB� 150Lebanon 14 B� B� 130Haitia 28 CCC B� 334Nicaraguaa 11 CCC� B� 209Ugandaa 5 B� B 161

Sources: Standard and Poors and World Bank staff calculations. Note: a. Calculated using a model similar to Cantor and Packer (1995); see Ratha and De (2005).

Figure 4.7 Remittance securitization structure

Beneficiary’saccountRemittance senders

International investors

Remittancepayments(foreign currency)

Remittance flows (foreign currency)

Excess cash

(foreign currency)

Debt service payment

Trustee collateralaccount

Issuing bank’saccount atcorrespondent bank

Correspondent banks

Issuing bank creditsbeneficiary’s accountin domestic currency

MessageIssuing bank

Offshore Domestic

Mexico, El Salvador, and Turkey raised about$2.3 billion during 1994–2000. As electronictransfers became more widespread, it waseasier to track complex transactions, andremittances securitization gave way tosecuritization of diversified payment rights(DPRs), including migrant remittances, butalso payments related to exports and FDI.During 2000–4, a total of $10.4 billion wasraised through securitization of DPRs byBrazil ($5.3 billion), Turkey ($4.1 billion), ElSalvador, Kazakhstan, Mexico, and Peru (fig-ure 4.8b). Following a sharp increase in bor-rowing costs in 2002 (in part because ofelection-year uncertainties), Brazil has raisedover $4 billion by issuing bonds backed by di-

versified payment rights. These bonds resultedin a spread saving of more than 700 basispoints compared to Brazil’s sovereign spread.

As experience with this instrument broad-ens, and investors become more comfortablewith its characteristics, it is possible that itcould be used by a wider range of countries (in-cluding poor countries) and for a broader rangeof external flows (remittances, tourism re-ceipts, and commodity earnings). It is not easyto estimate the potential size of such future-flow securitization. But preliminary calcula-tions, assuming an over-collateralization ratioof 5:1 and using migrant remittance figures for2003, show that developing countries couldpotentially issue nearly $9 billion and low-income countries could raise up to $3 billionannually from international capital markets.

Several policy hurdles need to be crossedbefore securitization deals can proceed. Highfixed costs of legal, investment banking, andcredit-rating services and long lead times canpose difficulties for developing countries withfew large entities and high borrowing needs. Amaster trust arrangement can permit issuers tostructure a large deal but to tap the market inseveral tranches. Pooling receivables of severalbranches (or even several borrowers) couldalso help increase the deal size to justify largefixed costs. While the absence of an appro-priate legal infrastructure can also constrainissuance, this need not require an overhaulof the entire legal system. A more focusedapproach that concentrates on bankruptcylaw may suffice, by making sure that pledgedassets remain pledged in the event of default.

So far, only the top-rated (in local currencyterms) financial institutions have issued futureremittance-backed bonds in an effort to piercethe sovereign foreign currency rating ceiling(that is, to obtain a higher rating for thesebonds than the sovereign foreign currency rat-ing). The securitization transactions typicallydo not affect financial institutions’ ability todeliver remittances to the ultimate beneficia-ries. Loosely speaking, the financial institu-tions that undertake a securitization transac-tion are pledging their rights to foreign

T R E N D S , D E T E R M I N A N T S , A N D M A C R O E C O N O M I C E F F E C T S O F R E M I T T A N C E S

103

1994

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

Figure 4.8 Securitization of remittances,1994–2004

a. Millions of dollars

b. By country

65206

350115

540

1,1751,170

1,6001,690

2,837

1,055

Brazil 31%

Peru2%

Turkey35%

Panama1%

Mexico24%

El Salvador6%

Kazakhstan1%

Note: Applies to the first half of 2004 only.

currency, but not their obligations to deliverremittances (typically in local currency terms).Potential issuers should be reminded, how-ever, of significant risks—currency devalua-tion and, in the case of flexible rate debt, un-expected increases in interest rates—that areassociated with market-based foreign currencydebt. Moreover, securitized debt is inflexibledebt. Securitization of remittances (and otherfuture flows) by public sector entities reducesthe government’s flexibility in managing itsexternal payments and can conflict with thenegative pledge provision included in multilat-eral agencies’ loan and guarantee agreements,which prohibit the establishment of a priorityfor other debts over the multilateral debts.

Large remittance inflows can lead to exchange rate appreciation and lower export competitiveness Large and sustained remittance inflows cancause an appreciation of the real exchangerate and make the production of cost-sensitivetradables, including cash crops and manufac-turing less profitable. Although empirical evi-dence on the adverse effect of large inflows offoreign exchange in terms of trade and growthis limited,27 it is plausible that this effect existsand is significant for some small economieswhere remittances are very high. Amuedo-Dorantes and Pozo (2004) found that a dou-bling of workers’ remittances resulted in realexchange rate appreciation of about 22 per-cent in a panel of 13 LAC countries (see alsoWinters and Martins 2004). Rajan andSubramanian (2005), however, did not findany evidence that remittance flows slow downgrowth by affecting competitiveness.28 More-over, as remittances tend to be relatively stableand persistent over long periods, the “Dutchdisease” effects of remittances are less of aconcern than similar effects of natural re-source windfalls and other cyclical flows, andthe real exchange rate level achieved throughsensible policies may be sustainable (IMF2005). Governments in countries receivinglarge remittances can mitigate the effects ofreal exchange rate appreciation by allocating a

larger portion of government expenditures oninfrastructure and also practicing more liberaltrade policies; both these measures wouldtend to increase exports and also contributeto improved labor productivity andcompetitiveness.

A related concern is whether reliance on un-earned income in the form of remittances hasadverse effects on the incentives to work, aswell as on the quality of economic policies andgovernance, similar to the well-documentedeffects of windfall gains from natural re-sources such as oil. While oil exports are al-most always found to have a strong negativeimpact on various governance indicators, suchas control of corruption and rule of law, pre-liminary cross-country analysis suggests thatremittance flows may not have such negativeeffects (box 4.5).29

The evidence on the effect of remittanceson long-term growth is inconclusiveTo the extent that they finance education andhealth and increase investment, remittancescould have a positive effect on economicgrowth. Remittances may relieve credit con-straints in the recipient community and spurentrepreneurial activity (Funkhouser 1992,Yang 2004, Woodruff and Zenteno 2004).Faini (2002) finds that the impact of remit-tances on growth is positive. He argues thatremittances overcome capital market imper-fections and allow migrant households to ac-cumulate positive assets, as claimed by Starkand Lucas (1988) and Taylor (1994). Mishra(2005) found that a 1 percentage point in-crease in remittance inflows in 13 Caribbeancountries increased private investment by0.6 percentage point (all measured relative toGDP). To the extent that they increaseconsumption, remittances may increase percapita income levels and reduce poverty andincome inequality, even if they do not directlyimpact growth (see chapter 5).

On the other hand, large outflow of work-ers, especially skilled workers, can reducegrowth in labor-sending countries. Remit-tances may also indirectly affect labor supply,

G L O B A L E C O N O M I C P R O S P E C T S 2 0 0 6

104

by encouraging some remittance-recipienthouseholds to choose more leisure thanlabor. Chami, Fullenkamp, and Jahjah (2005)argue that remittances may slow down growthby reducing work efforts by remittancerecipients.30

One recent study of the impact of remit-tances on growth over an extended period(1970–2003) for 101 developing countriesfound no significant link between remittancesand per capita output growth, or betweenremittances and other variables such as educa-tion or investment rates (IMF 2005). Thisstudy, however, attributed this inconclusive re-sult to measurement difficulties arising fromthe fact that remittances may behave counter-cyclically with respect to growth.31 Also, em-pirically it is difficult to measure the effects ofremittances on human capital formation,which may occur over a very long period oftime.

Remittances, like aid, may be more effec-tive in a good policy environment. Forinstance, a good investment climate with well-

developed financial systems and sound institu-tions is likely to imply that a higher share ofremittances is invested in physical and humancapital (IMF 2005). Indeed, Giuliano andRuiz-Arranz (2005) show that in theeconomies where the financial system is un-derdeveloped, remittances alleviate creditconstraints and work as a substitute for finan-cial development, improving the allocation ofcapital and therefore accelerating economicgrowth. Recent research also shows thatremittances may promote financial develop-ment (Aggarwal and others 2005), which inturn can enhance growth and reduce poverty(Beck and others 2004).

Annex 4A.1 World Bank data on remittances

Using the definition in chapter 7 of GlobalDevelopment Finance 2003, migrant re-

mittances are considered the sum of workers’remittances, compensation of employees, andmigrants’ transfers. Data for these variables

T R E N D S , D E T E R M I N A N T S , A N D M A C R O E C O N O M I C E F F E C T S O F R E M I T T A N C E S

105

The economic performance of most mineral ex-porters, in particular oil exporters, has been far

less impressive than that of resource-poor countries (Gelb and others 1988; Auty 2001; Gelb, Eifert, andTallroth 2002). To a large extent this outcome seemsdriven by mismanagement of the economy and weakinstitutions. Sala-i-Martin and Subramanian (2003)show empirically that concentration of resourceflows has deleterious effects on the institutionalframework and capacity of a country. Natural re-source windfalls—oil rents, for example—often fos-ter weak institutions because they allow the authori-ties to pursue arbitrary, costly, and inefficient policies(Ross 2001). States that control such resources mayresist secular modernization pressures because theycreate alternative sources of power (Isham andothers 2003). These rents also perpetuate economic

Box 4.5 Unlike oil windfalls, remittance inflows donot weaken institutional capacity

inequality, which results in nepotism and a weakcivil society. Resource rents are also believed to beassociated with civil conflict (Collier and Hoeffler2002).

In contrast, remittances are widely dispersed, thegreat bulk of them is allocated in small amounts, andfor the most part, remittances avoid the government“middleman.” Hence the expectation is that they canavoid the negative effects of natural resource wind-falls on poverty, growth, and institutional capacity.This is similar to an argument by Birdsall and Subra-manian (2004) that countries would be better off ifthey distributed the bulk of the returns from resourceflows to the general population, who would use thefunds more effectively than a highly centralized gov-ernment, and also greatly reduce the incentives forcorruption.

are taken mostly from the balance of payments(BoP) data file of the IMF (see also Ratha2003). However, many countries do not reportdata on remittances in the IMF BoP statistics,even though it is known that emigration fromthose countries took place (see table 4A.1.1 fora list of these countries). In 2003 about 87countries did not report any remittances’ data.Further, there was no consistency in reportingthe data. For example, only 28 countries re-port workers’ remittances, compensation ofemployees, and migrants’ transfers. Forty-fivecountries report both workers’ remittancesand compensation of employees; 11 countriesreport compensation of employees and mi-grants’ transfers; and 3 countries report work-ers’ remittances and migrants’ transfers. Thereare 14 countries that report only workers’ re-mittances and 19 countries that report onlycompensation of employees.

Reported data for developing countriesshow only $113.4 billion in total remittancesfor the year 2003 (workers’ remittances$97.3 billion, compensation of employees$14.8 billion, and migrants’ transfers $1.3 bil-lion), and 83.8 billion in 2004 (workers’ re-mittances $68.7 billion, compensation of em-ployees $13.5 billion, and migrants’ transfers$1.5 billion). By filling in gaps for some devel-oping countries for which remittance datawere missing, we arrived at an estimate of$142 billion in 2003, and $160 billion in

2004 (the latest year for which BoP data arecurrently available). The gap-filling methodsfollowed, and the reasons for making theadjustments are documented below.

Workers’ remittances, as defined in theIMF Balance of Payments manual, publishedin 1993 (fifth edition), are current privatetransfers from migrant workers who are con-sidered residents of the host country to recipi-ents in their country of origin. If the migrantslive in the host country for a year or longer,they are considered residents, regardless oftheir immigration status. If the migrants havelived in the host country for less than a year,their entire income in the host country shouldbe classified as compensation of employees.Workers’ remittances are transfers, whereascompensation of employees is considered fac-tor income. In the earlier, fourth edition of theBoP manual, compensation of employees wascalled labor income and was classified as non-factor services (referred to just as services inthe fifth edition).

Although the residence guideline in themanual is clear, this rule is often not followedfor various reasons. Many countries compiledata based on the citizenship of the migrantworker rather than on their residency status.Further, data are shown entirely as eithercompensation of employees or as worker re-mittances, although they should be split be-tween the two categories if the guidelineswere correctly followed; for example, SaudiArabia and Israel record only compensationof employees. India shows very little com-pensation of employees, but large workers’remittances, although it is well known thatIndia supplies a large number of temporaryIT workers to the United States and Euro-pean countries. On the other hand, thePhilippines shows large compensation ofemployees and very few migrants’ transfers.The distinction between these two categoriesappears to be entirely arbitrary, dependingon country preference, convenience, and taxlaws or data availability. This fact has beenrecognized at the World Bank since the1980s, and worker remittances have been

G L O B A L E C O N O M I C P R O S P E C T S 2 0 0 6

106

Table 4A.1.1 Countries with alternativeestimates in 2004 $ millions

Algeria 2,460China 21,283Gambia 8Iran 1,032Kenya 464Lebanon 2,700Malaysia 987Mauritious 215Nigeria 2,751Serbia and Montenegro 4,129Vietnam 3,200

Total $39,259

treated as part of labor income and added toexports of goods and services in calculatingdebt service ratios.