Embed Size (px)

Citation preview

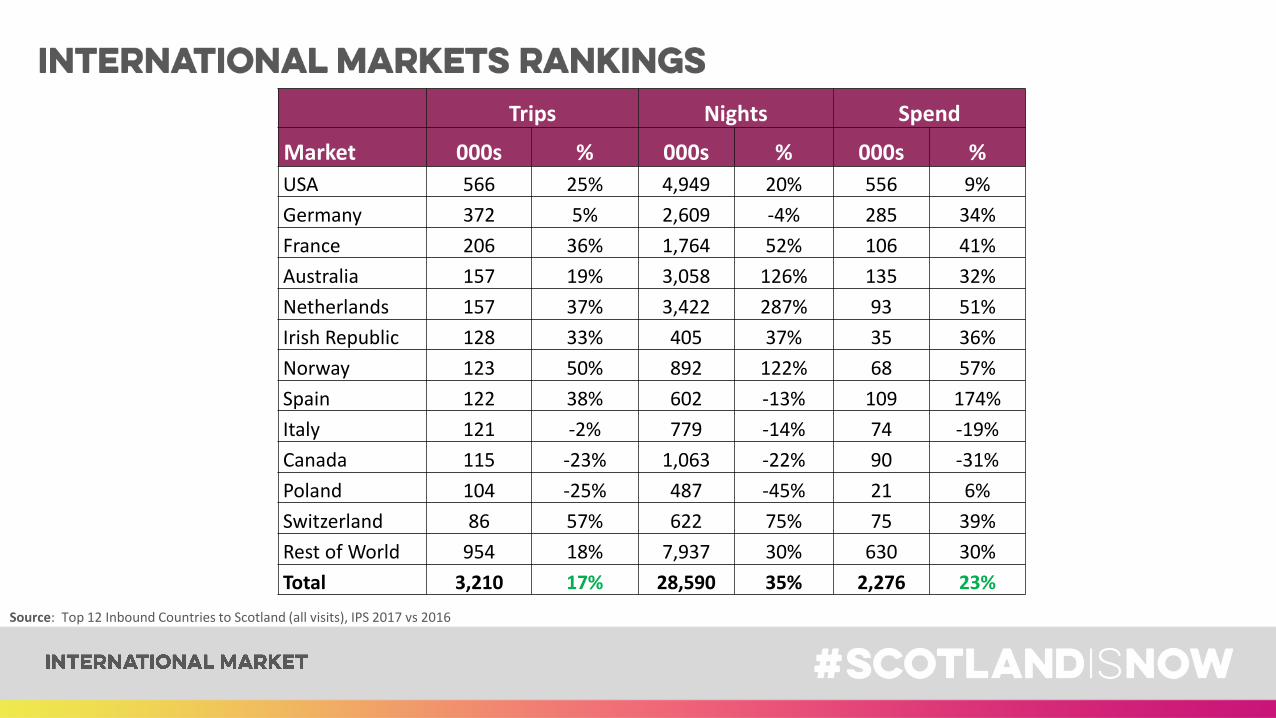

Trips Nights Spend

Market 000s % 000s % 000s %

USA 566 25% 4,949 20% 556 9%

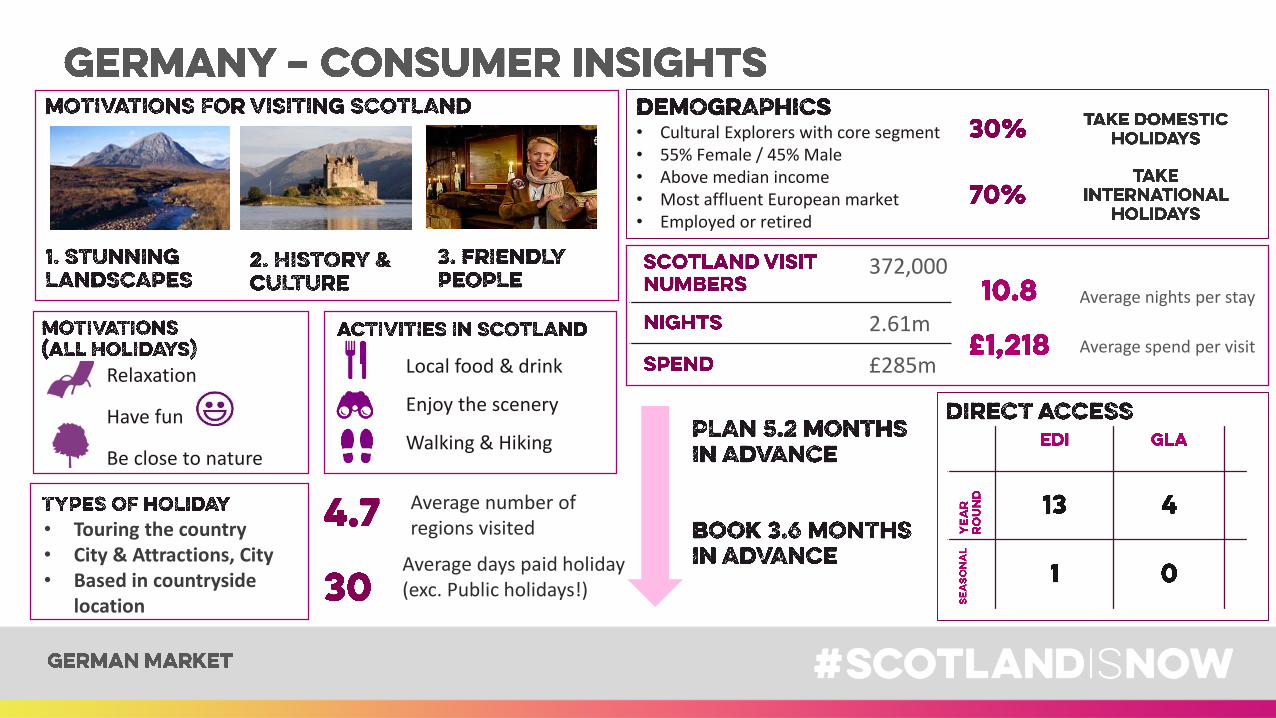

Germany 372 5% 2,609 -4% 285 34%

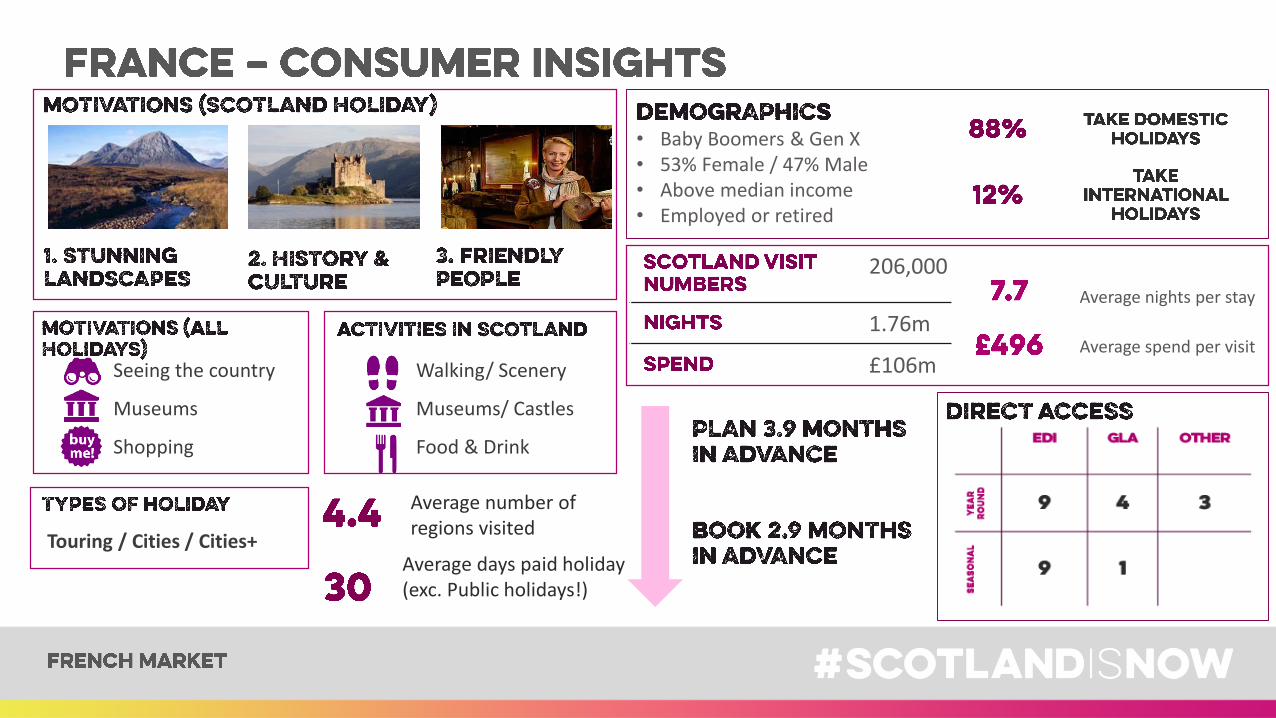

France 206 36% 1,764 52% 106 41%

Australia 157 19% 3,058 126% 135 32%

Netherlands 157 37% 3,422 287% 93 51%

Irish Republic 128 33% 405 37% 35 36%

Norway 123 50% 892 122% 68 57%

Spain 122 38% 602 -13% 109 174%

Italy 121 -2% 779 -14% 74 -19%

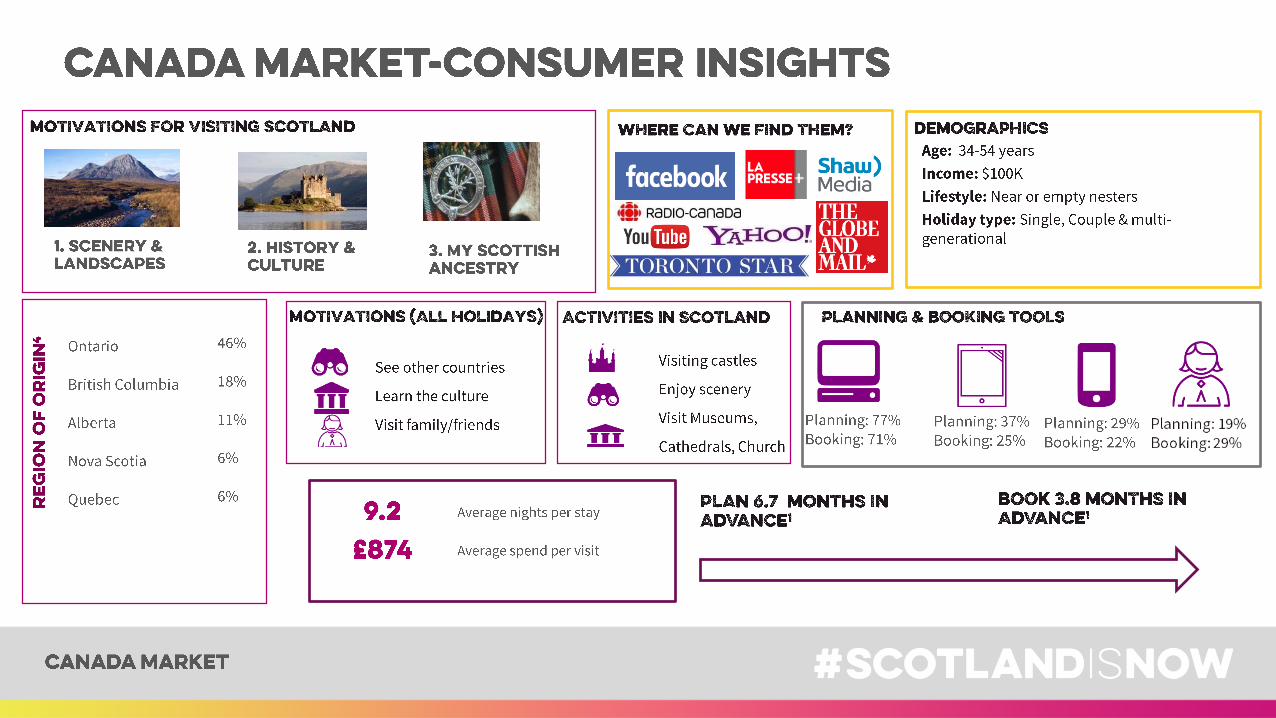

Canada 115 -23% 1,063 -22% 90 -31%

Poland 104 -25% 487 -45% 21 6%

Switzerland 86 57% 622 75% 75 39%

Rest of World 954 18% 7,937 30% 630 30%

Total 3,210 17% 28,590 35% 2,276 23%

Source: Top 12 Inbound Countries to Scotland (all visits), IPS 2017 vs 2016

0

200

400

600

800

1000

1200

1400

1600

1800

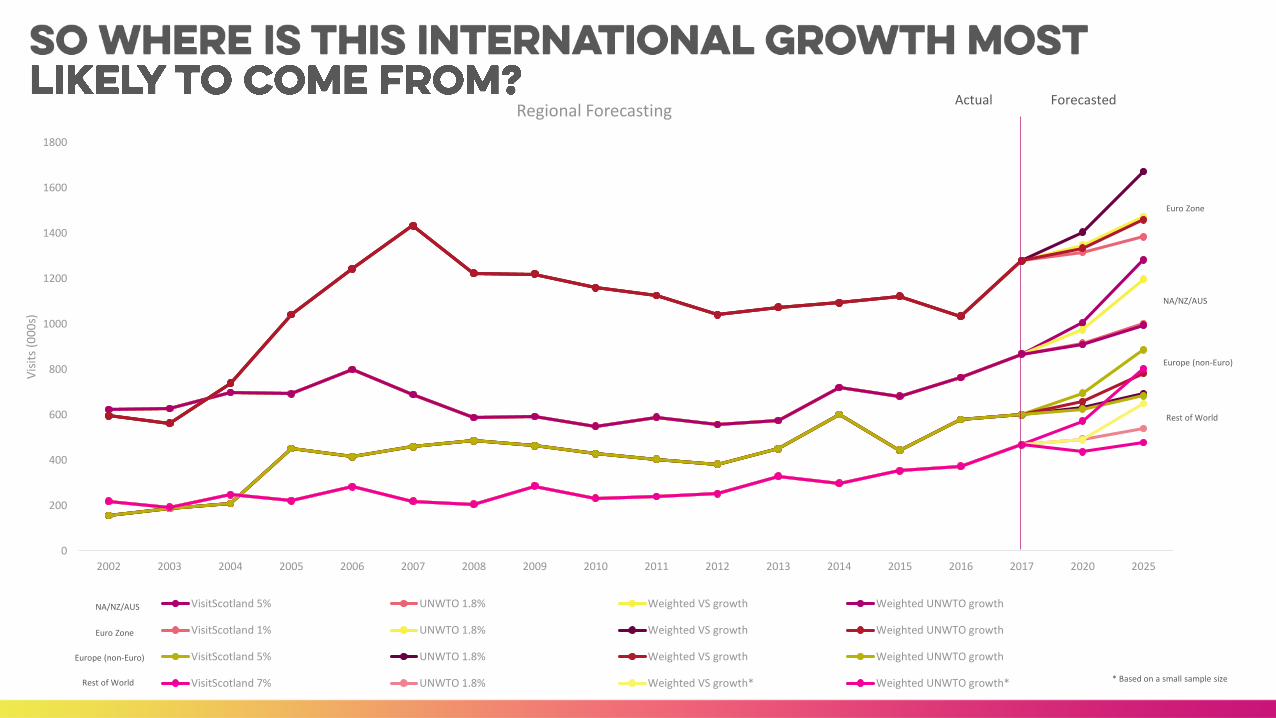

2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 2020 2025

Vis

its

(00

0s)

Regional Forecasting

VisitScotland 5% UNWTO 1.8% Weighted VS growth Weighted UNWTO growth

VisitScotland 1% UNWTO 1.8% Weighted VS growth Weighted UNWTO growth

VisitScotland 5% UNWTO 1.8% Weighted VS growth Weighted UNWTO growth

VisitScotland 7% UNWTO 1.8% Weighted VS growth* Weighted UNWTO growth*

NA/NZ/AUS

Euro Zone

Europe (non-Euro)

Rest of World

NA/NZ/AUS

Euro Zone

Europe (non-Euro)

Rest of World

* Based on a small sample size

Actual Forecasted

Why target international visitors?

Average number of regions visited• Touring the country

• City & Attractions, City • Based in countryside

location

Average days paid holiday (exc. Public holidays!)

Relaxation

Have fun

Be close to nature

Local food & drink

Enjoy the scenery

Walking & Hiking

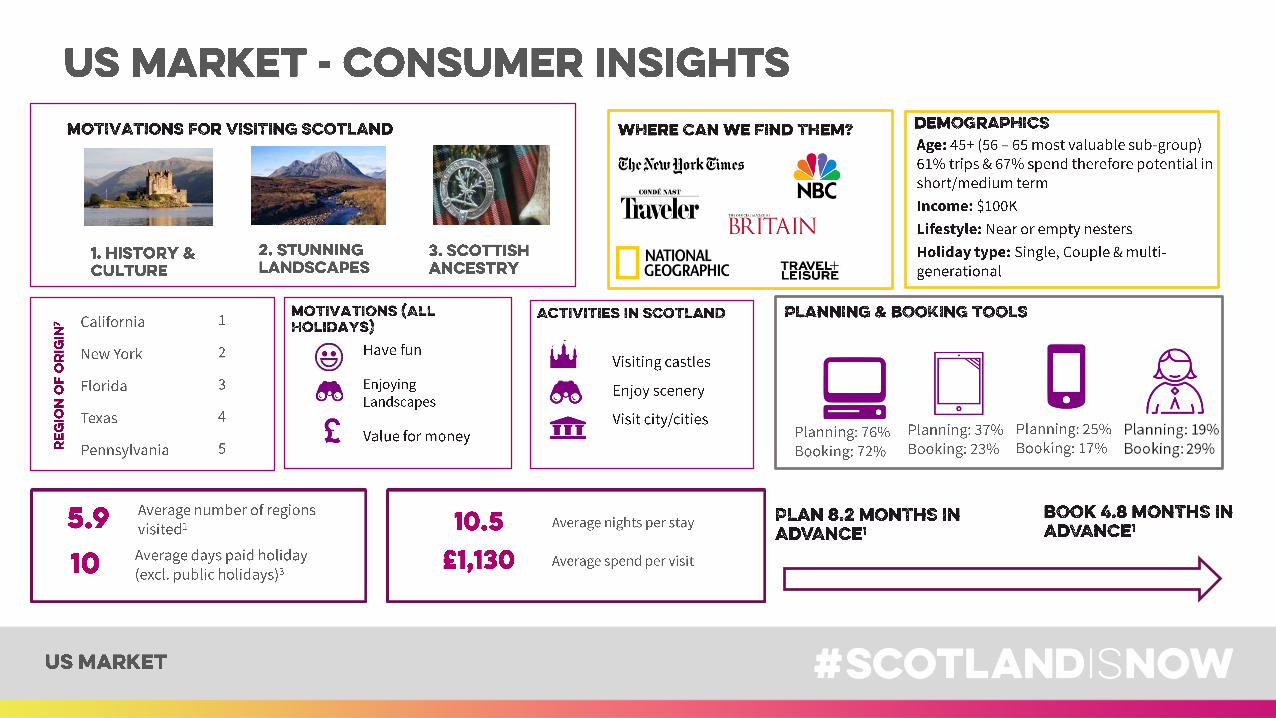

372,000

2.61m

£285m

Average nights per stay

Average spend per visit

• Cultural Explorers with core segment 35+• 55% Female / 45% Male• Above median income• Most affluent European market• Employed or retired

Seeing the country

Museums

Shopping

Average number of regions visited

Walking/ Scenery

Museums/ Castles

Food & Drink

Touring / Cities / Cities+Average days paid holiday (exc. Public holidays!)

• Baby Boomers & Gen X• 53% Female / 47% Male• Above median income• Employed or retired

206,000

1.76m

£106m

Average nights per stay

Average spend per visit

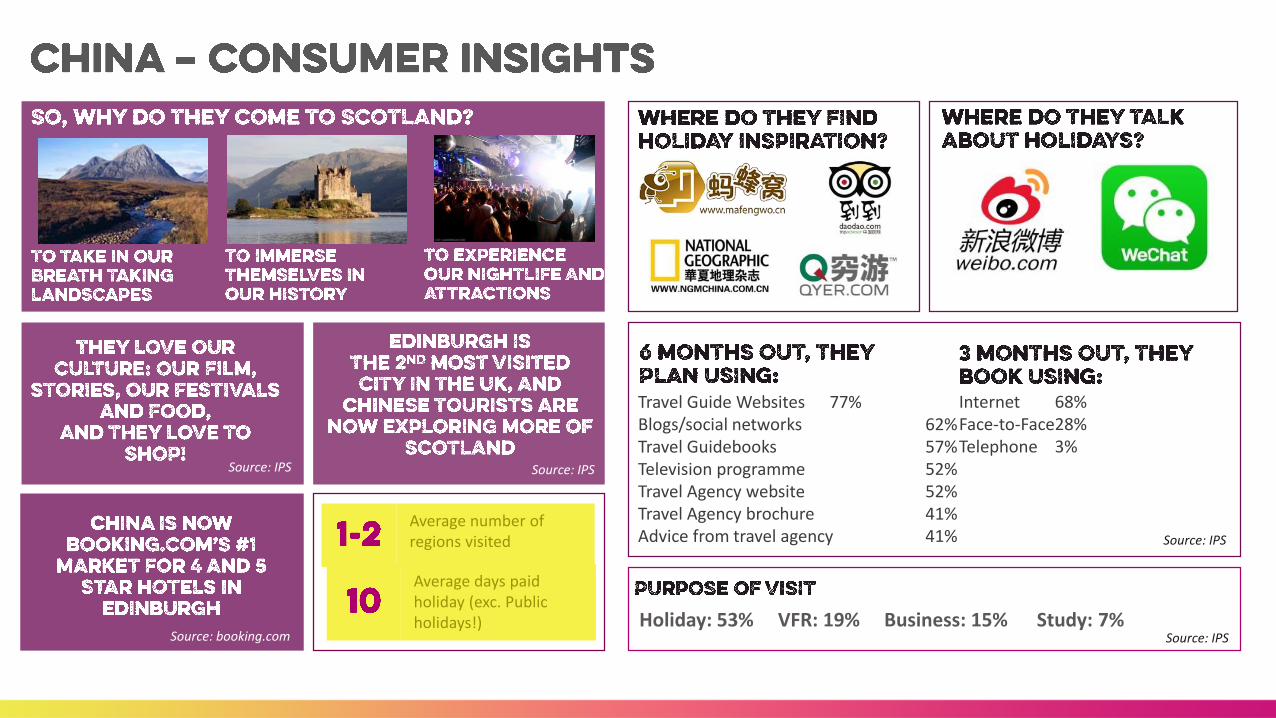

Travel Guide Websites 77%Blogs/social networks 62%Travel Guidebooks 57%Television programme 52%Travel Agency website 52%Travel Agency brochure 41%Advice from travel agency 41%

Internet 68%Face-to-Face28%Telephone 3%

Source: IPS

Source: IPS

Source: booking.com

Source: IPS

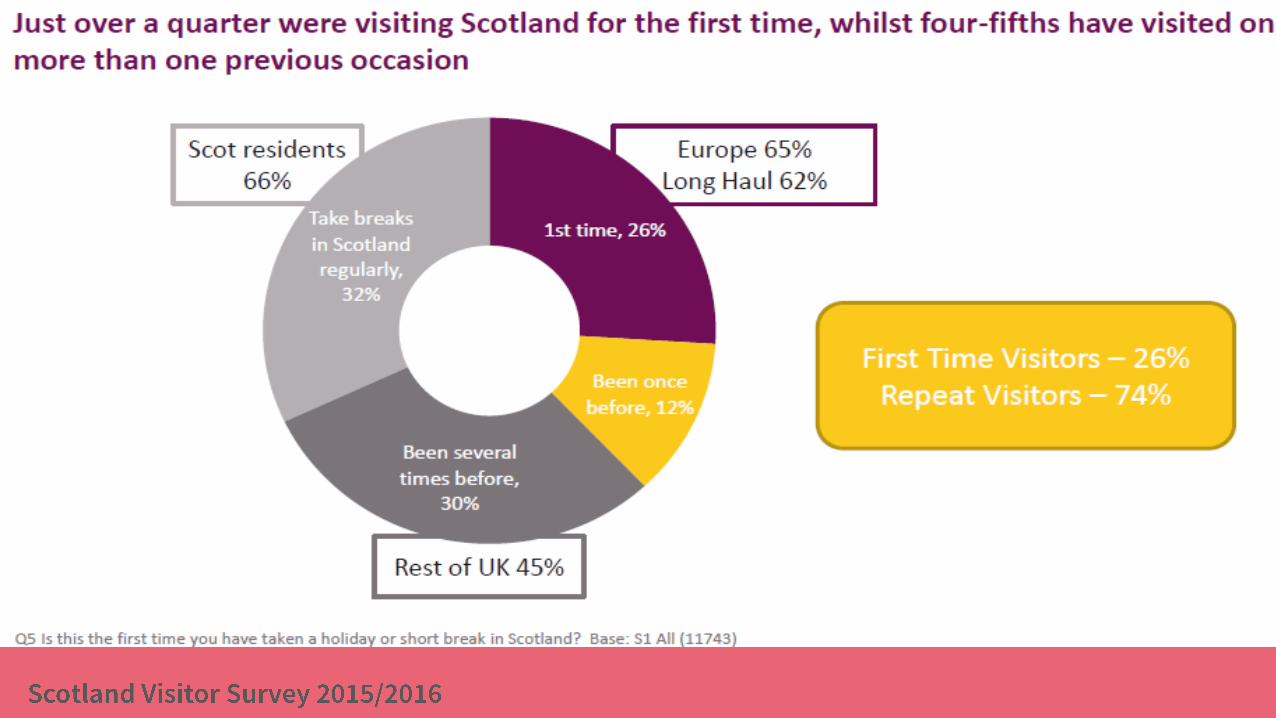

Holiday: 53% VFR: 19% Business: 15% Study: 7% Source: IPS Source: IPS

Average number of regions visited

Average days paid holiday (exc. Public holidays!)

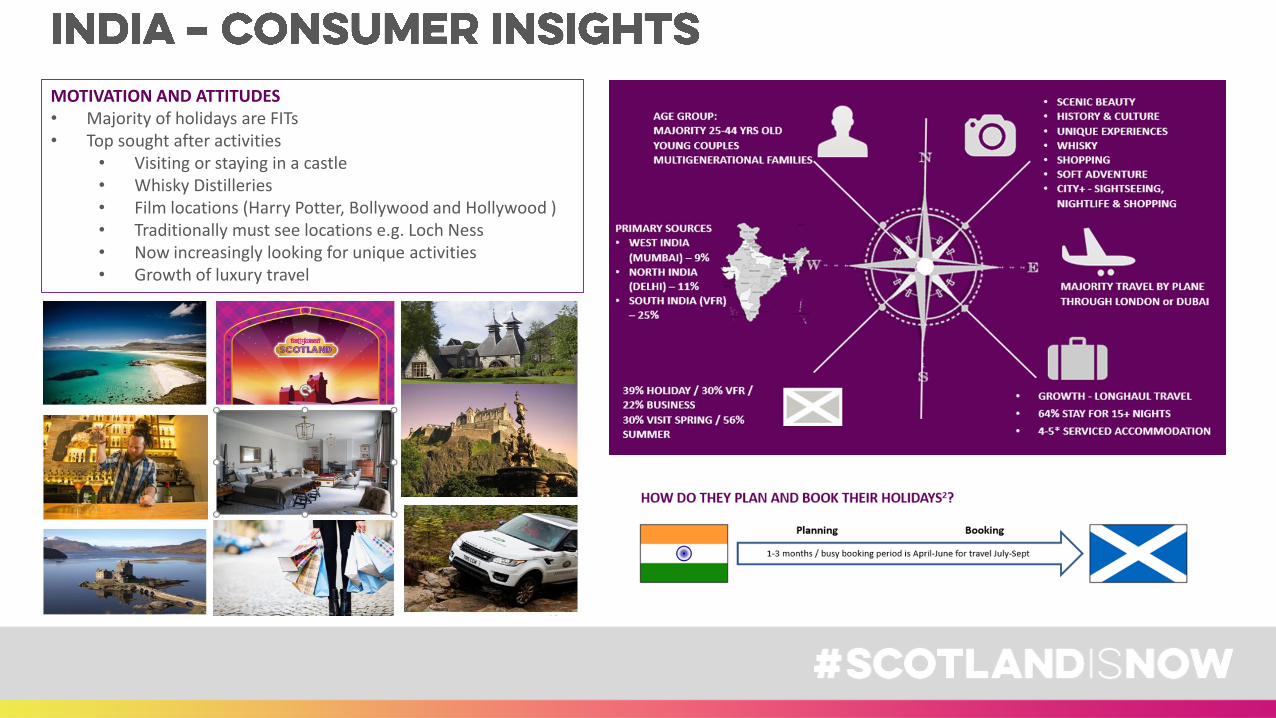

MOTIVATION AND ATTITUDES• Majority of holidays are FITs• Top sought after activities

• Visiting or staying in a castle• Whisky Distilleries • Film locations (Harry Potter, Bollywood and Hollywood )• Traditionally must see locations e.g. Loch Ness• Now increasingly looking for unique activities • Growth of luxury travel

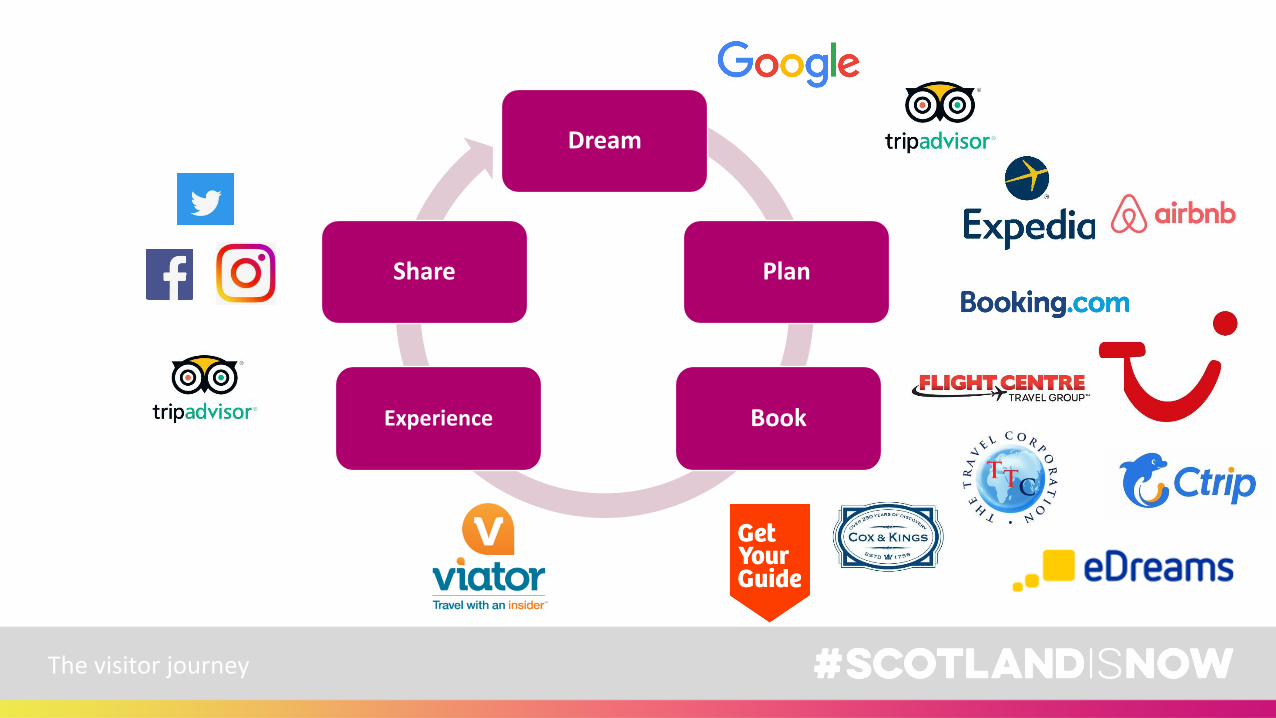

The visitor journey

Dream

Plan

BookExperience

Share

Wholesalers

These organisations have global reach including Destination Management Companies; eg Abbey, JAC, China Holidays, TUI. They have their own brand campaigns and partner with destinations. Often have in house product development and contracting teams.

Niche Tour Operators

Nice operators provide Scotland with clear product development opportunities which often provide suppliers with geographic spread. Product purchase is direct or via an incoming specialist.

OTAs (Online Travel Agents)

OTAs are now seeing a period of stabilisation after unprecedented growth and consolidation –the purchase of niche, specialist online brands by the mega OTAs is a common expansion strategy, recently seen by acquisitions in the tours and activities sector.

Travel agents/smaller operators

This channel still remains important in the emerging and long haul markets for some consumer segments. In recent years they have had to carefully consider how they reach and retain customers. For many, destination or theme specialisation provides a USP.

Who are the key intermediaries

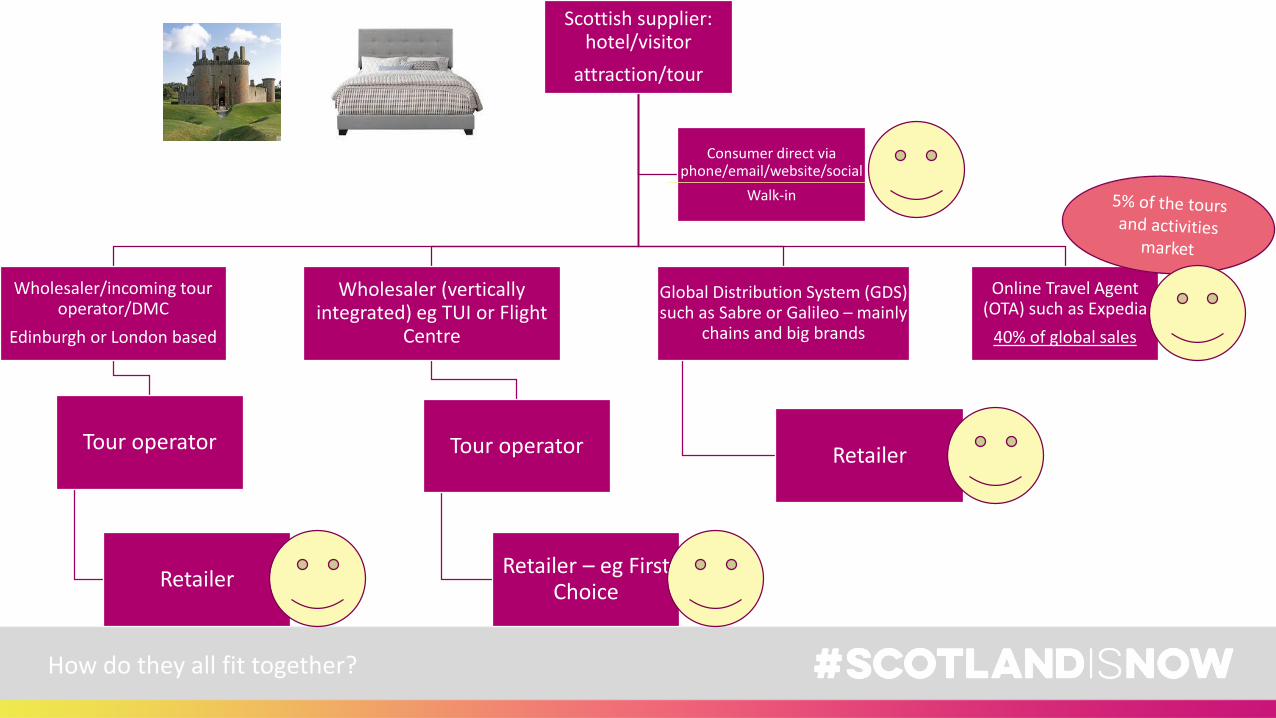

How do they all fit together?

Scottish supplier: hotel/visitor

attraction/tour

Wholesaler/incoming tour operator/DMC

Edinburgh or London based

Tour operator

Retailer

Wholesaler (vertically integrated) eg TUI or Flight

Centre

Tour operator

Retailer – eg First Choice

Global Distribution System (GDS) such as Sabre or Galileo – mainly

chains and big brands

Retailer

Online Travel Agent (OTA) such as Expedia

40% of global sales

Consumer direct via phone/email/website/social

Walk-in

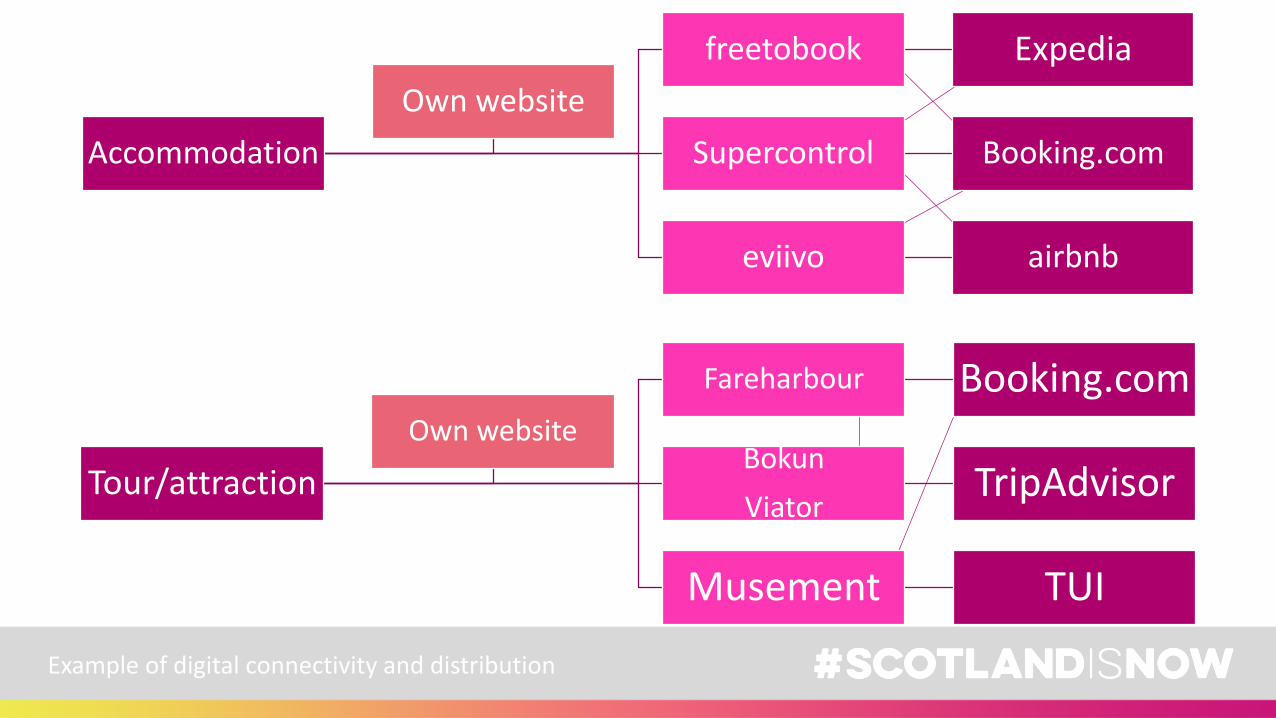

Example of digital connectivity and distribution

Accommodation

freetobook Expedia

Supercontrol Booking.com

eviivo airbnb

Own website

Tour/attraction

Fareharbour Booking.com

Bokun

ViatorTripAdvisor

Musement TUI

Own website

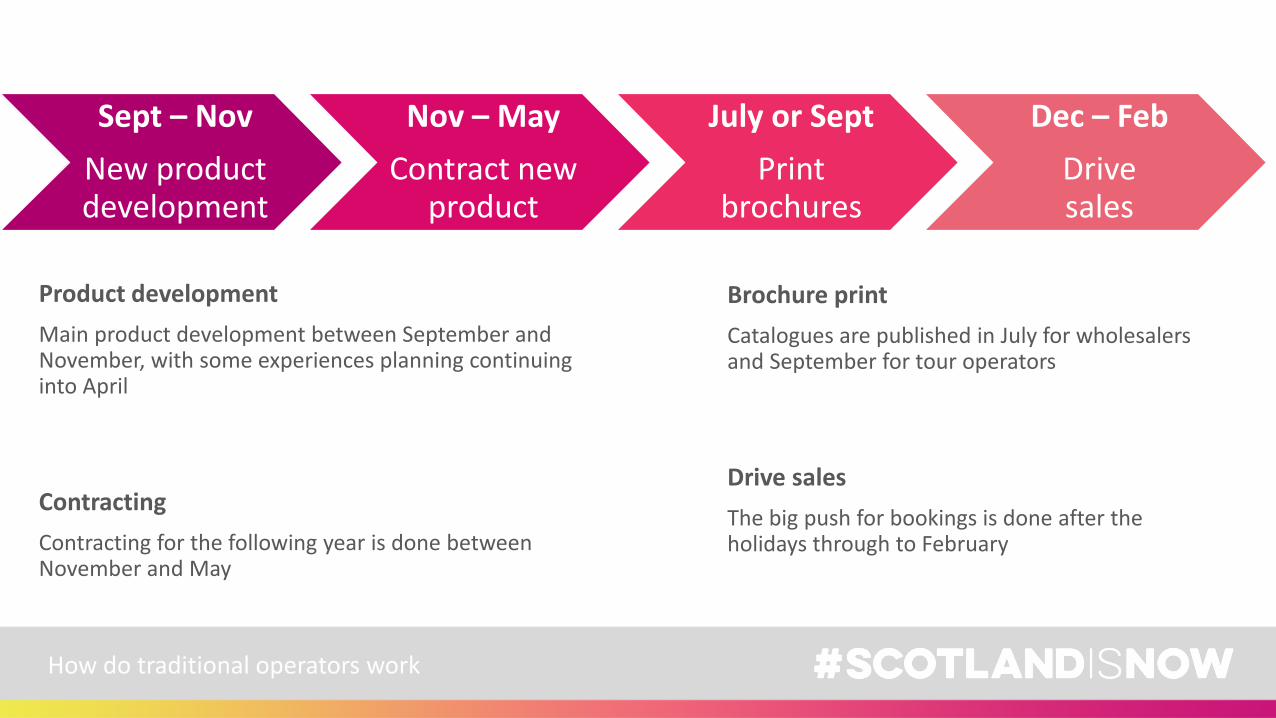

How do traditional operators work

Sept – Nov

New product development

Nov – May

Contract new product

July or Sept

Print brochures

Dec – Feb

Drive sales

Product development

Main product development between September and November, with some experiences planning continuing into April

Contracting

Contracting for the following year is done between November and May

Brochure print

Catalogues are published in July for wholesalers and September for tour operators

Drive sales

The big push for bookings is done after the holidays through to February

Developing a compelling proposition

Developing your

proposition

What is your unique

proposition?

What assets do you have?

Who can you work in partnership

with?

What kind of customer

do you want?

High endFamiliesGroups

Other attractionsDay tour operatorsAccommodation, retailers

Excellent servicePersonalisationUnique experienceFacilities for cyclists/walkers

LocationHistory/heritageLocal food and drinkThematic

• What is your unique propositions?

• What assets do you have?

• Who can you work with to create and develop a thematic proposition?

• Working in partnership -how can you collaborate on a local level to amplify the destination message?

Developing your bookable product for B2B

• VISITSCOTLAND.ORG

• LISTING ON VISITSCOTLANDTRAVELTRADE.COM

• YOUR VISITSCOTLAND INDUSTRY RELATIONS MANAGER

• B2B EVENTS incl VisitScotland Expo