Embed Size (px)

Citation preview

Issued by HSBC Asset Management (India) Private Limited

HSBC Equity FundAn open-ended diversified equity Scheme

Abridged Annual Report 2008 - 2009

HSBC Global Asset Management

1

Dear Investor,

We thank you for investing with HSBC Mutual Fund. We are pleased to inform you that HSBCMutual Fund has won prestigious awards* this year at various forums in India.

The awards* won by our schemes in India are

� HSBC Equity Fund has been included in the 5 star rated fund category (“Top rated mutualfunds” by Value Research online) in March, 2009.

� Five-stars indicate that a fund is in the top 10 per cent of its category in terms ofhistorical risk-adjusted returns.

� ICRA Mutual Fund Awards 2009

� HSBC MIP - Savings has been ranked a 5-Star Fund by ICRA Online indicating performanceamong the top 10% in the category of 'Open Ended Marginal Equity' for 3 yearperformance ending 31 December, 2008.

� CNBC TV18 - CRISIL Mutual Fund Awards 2008

� HSBC MIP - Savings was awarded the CNBC TV18 - CRISIL Mutual Fund of the YearAward for the year 2008 in the Monthly Income Plans - Aggressive Category.

(Past performance is no guarantee of future results. * Please refer to Ranking methodologyand disclaimer mentioned at the end of the Abridged Annual Report for the year endedMarch 31, 2009).

At the global level, the HSBC Group won several awards at Euromoney's Awards for Excellence2009. The top awards that HSBC won were the Best Global Bank and the Best Global DebtHouse. It was also honoured as the Best Debt House in 8 locations including Asia and the Bestat Risk Management in Asia. (Past performance may or may not be sustained in the future andis no guarantee of future results). We continue to be one of the leading players in emergingmarkets and remain committed to our asset management business in India.

HSBC Asset Management (India) Private Limited including the mutual fund business as well asthe PMS business (including EPFO money deployed till date) manages assets of about Rs. 26280Crores as at 30 June, 2009. The core to our winning strategy is our endeavour to deliverconsistent performance over the medium to long term for our investors in a risk controlledenvironment and aim for consistent wealth creation under varying market conditions. Throughour product range, we aim to be true to our reputation in India of being a provider ofinternational quality investment products and services.

We remain committed to our philosophy of aiming for consistent wealth creation and serviceexcellence and look forward to your continued investments in HSBC Mutual Fund.

Yours sincerely,

VikramaadityaChief Executive OfficerHSBC Asset Management (India) Private Limited

2

SPONSORHSBC Securities and Capital Markets (India) Private LimitedRegd. Office: 52/60, Mahatma Gandhi Road, Fort, Mumbai 400 001.

TRUSTEEBoard of TrusteesOffice: 314, D. N. Road, Fort, Mumbai 400 001.

ASSET MANAGEMENT COMPANYHSBC Asset Management (India) Private LimitedCorp. & Regd. Office: 314, D. N. Road, Fort, Mumbai 400 001.

CUSTODIANJP Morgan Chase BankCorp. & Regd. Office: Mafatlal Centre, 9th Floor, Nariman Point, Mumbai - 400 021.

AUDITORS TO THE SCHEMEPrice WaterhouseChartered Accountants252, Veer Savarkar Marg, Shivaji Park, Dadar (West), Mumbai - 400 028.

LEGAL ADVISORSBharucha & Partners4th Floor, Cecil Court, Mahakavi Bhushan Marg, Colaba, Mumbai - 400 039.

REGISTRAR & TRANSFER AGENTSComputer Age Management Services (P) Ltd. (CAMS)Rayala Towers, Tower I, III Floor, 158 Anna Salai, Chennai - 600 002.

BOARD OF TRUSTEESMr. N. P. Gidwani - Chairman

Dr. Rudolf ApenbrinkMr. Nasser MunjeeMr. Manu TandonMr. Mehli MistriMr. Dilip J. Thakkar

BOARD OF DIRECTORSMs. Naina Lal Kidwai - Chairman

Mr. Ayaz EbrahimMr. S. P. Mustafa**Mr. Vithal PalekarMs. Kishori J. Udeshi*Mr. Vikramaaditya - Chief Executive Officer***

* Ms. Kishori Udeshi has been appointed as a Director with effect from 14 January 2009 andMr. Jagjit Lal Pasricha has resigned as a Director with effect from 19 January 2009.

** Mr. S. P. Mustafa has been appointed as a Director with effect from 2 September 2008 andMr. Nawshir Khurody has resigned as a Director with effect from 1 September 2008

*** Mr. Vikramaaditya has been appointed as the Chief Executive Officer with effect from 16 July 2008and Mr. Sanjay Prakash has resigned as the Chief Executive Officer with effect from 16 July 2008.

3

Trustees' ReportFor the year ended March 31, 2009

The Trustees present the seventh report and the audited financial statements of the Schemes ofHSBC Mutual Fund (the "Fund"), for the year ended March 31, 2009.

1. SCHEME PERFORMANCE, FUTURE OUTLOOK AND OPERATIONS OF THE SCHEME

a) Operations and Performance of the Scheme

HSBC Equity Fund (HEF) - an open-ended diversified Equity Scheme

To generate long-term capital growth from an actively managed portfolio of equity and equity relatedsecurities. The Scheme offers investors two Options (1) Growth Option (2) Dividend Option. TheDividend Option offers Dividend Payout and Dividend Reinvestment Facilities.

The net assets of the Scheme amounted to Rs. 1092.07 crores as at March 31, 2009 as againstRs. 1052.51 crores as at March 31, 2008. 83% of the net assets were invested in equities, and 17%were invested in debt and money market instruments as at March 31, 2009.

HSBC Equity Fund's approach is to invest across a range of market capitalizations with a preferencefor medium and large companies. Income is not a primary consideration in the investment policies ofHEF.

The fund outperformed the benchmark by approximately 900 bps in FY09 by holding higher thanusual levels of cash and a defensive (low beta) portfolio.

Date of Inception : 10 December, 2002 Compounded Annualized Returns (%)

Schemes (P2P) 1 Year 3 Years 5 Years Since Inception

HSBC Equity Fund - Growth -31.92 -0.41 17.02 32.90

BSE 200 -40.98 -6.88 9.22 18.78

Past performance may or may not be sustained in future. Returns equal to or greater than 1 year arecompounded annualized. 'Since inception' returns are calculated on Rs. 10 invested at inception.Calculations are based on Growth NAVs.

b) Market Overview & Outlook

MARKET OVERVIEW

(as furnished by HSBC Asset Management (India) Private Limited)

Equity Market Overview

The financial year ended 31 March, 2009 was a highly eventful one with long standing institutionsdisappearing from the landscape in the whirlwind of the sub-prime crisis and derivative losses. Theyear can be split into three phases - the first from April 2008 till when Lehman Brothers filed forbankruptcy, which saw a blowout commodity rally (crude oil nudged close to USD 144/barrel) andthe sub-prime situation turning progressively worse. The United States (US) Government / FederalReserve bailed out major institutions thought to be critical to the functioning of the financial system.The second phase from September 2008 till January 2009 saw a spate of bankruptcies most notablyLehman Brothers which saw the appearance of an acute level of risk aversion pushing the creditmarkets into a gridlock. This phase also coincided with the fiscal / monetary stimuli by variousgovernments to take the credit crisis head on. Globally, markets stabilized around their October2008 lows and a semblance of normality started re-appearing in financial markets in this period. Thethird phase from February 2009 onwards witnessed a sharp rally as a weakening US Dollar spewedmoney into emerging markets. The sensex fell by 38% during the financial year.

4

For the financial year 2009, the popular indices viz. BSE Sensex and CNX Nifty were down 37.94%and 36.19% respectively. The BSE Midcap (54.01)% and the broader indices like BSE 200 (40.98)%and BSE 500 (42.77)% also reflected the correction across the markets. Within sectoral indices thebest performing indices were BSE FMCG (11.08)% and BSE Oil and Gas (29.58)% while the worstperforming indices were BSE Realty (79.37)%, due to the high leverage on the balance sheets, BSEMetals (58.67)%, due to slowdown in global growth and BSE Consumer Durables (58.14)% and BSECapital goods (53.84%).

In a year that saw sell-off across emerging markets, FIIs were net sellers of the tune USD 10.4 billionin the Indian equity markets while Domestic Institutional Investors (Insurance & Mutual Funds) werebuyers to the tune of USD 13.1 billion. Further, FIIs were net sellers in the derivative markets ashedge funds, and p-notes unwound positions in a rapidly deleveraging world. Thus, sentimentremained negative as few US based investment banks filed for bankruptcy in the midst of the liquidityand credit crisis and safety took precedence over growth.

Debt Market Overview

Two contrarian forces one inflationary and the other deflationary had been in play since 2007: Onthe one hand strong demand from emerging economies were leading commodities higher and fuellinginflation, while on the other the housing led credit crisis in the US was starting to exert a deflationaryforce. The first force was dominant till early July 2008 leading commodity prices to fresh peaks andinflation to multi year highs. Since then, however, the second force took hold with the result thatcommodity prices fell sharply from the top, growth and inflation numbers toppled worldwide, andcentral bankers shifted focus to achieving financial stability and protecting growth.

The financial crisis hit the domestic markets towards September 2008, leading to acute disruption inmoney markets. The Reserve Bank of India (RBI) acted proactively cutting the cash reserve ratio (CRR)by an unprecedented 400 bps between September 2008 and January 2009. Similarly, the reverserepo rate had been cut by 275 bps since October 2008 while the repo rate had been cut by 425 bpsover the same period.

Bond market yields fell in line with the unprecedented monetary easing up till the first week ofJanuary 2009. Thereon, supply pressures on bond markets rose as a result of government fiscalslippages aimed at stimulating the economy. The RBI, in line with similar measures elsewhere in theworld, started buying government securities to lessen the impact on yields from the rise in governmentborrowing. Although this helped market sentiment, it could not prevent a general rise in yieldstowards fiscal close. As a result, the 10 year benchmark sovereign yield closed the fiscal at 7% froma low of sub 5% hit in early January 2009. Money market rates stabilized after the initial mayhem ofSeptember 2008 and October 2008 and liquidity came back to interbank markets.

MARKET OUTLOOK

(as furnished by HSBC Asset Management (India) Private Limited)

Equity Market Outlook

Financial Year (FY) 2008-09 was a year marked by a strong correlation between the Indian marketand global markets with key indices ending deeply in the red on the back of the subprime crisis andderivative led losses across major financial stocks in the United States (US). Even in India, forex lossesran across corporate India though at a smaller magnitude. FY 10 has begun on a better note onaccount of various fundamental and technical factors.

GDP for FY 09 grew at 6.7% against FY 08 levels of 9%. Agriculture posted a below trend growthrate of 1.6% and industry grew by 3.9% (versus 8.1% in FY 08) with services registering a close to9.7% growth. IIP grew by a mere 2.6%. Although order books of engineering / capital goods wererunning at record high levels, there was possibility of delays in execution as funding sources for thedevelopers (equity, ECB, private equity, FCCB) had dried up. A sharp increase in subsidy on account

Trustees' ReportFor the year ended March 31, 2009 (Contd...)

5

of oil, fertilizers and food led to a cut back in discretionary spending. Inflation rose on the back of asurging crude and higher prices of agricultural commodities to top at 12.91% for the week ending 2August, 2008. A slow down in the growth rates in the US / EU and other markets finally tamed thesurge in crude. As growth rates stumbled, governments / monetary authorities the world over triggeredfiscal stimuli / monetary easing to escape recessionary forces. This was followed in India as wellwhich started monetary easing / fiscal stimuli to keep growth rates buoyant.

On the positive side, India continues to do better in relative terms and we expect GDP growth of6-6.5% for FY10. The broad themes that are driving domestic growth viz. capital expenditure,infrastructure building and domestic consumption are still intact. The key concerns at this pointstems from a ballooning fiscal deficit at the consolidated level (Centre & State) with salary revisionfor Central / State Government employees threatening a cut back in discretionary spending. Inflationis likely to remain benign for the first half of FY10 on a favourable base effect but we anticipate it togo back to trend levels of 5-5.5% for the second half of FY10 as this base effect wears off.

On a valuations perspective, the markets are currently trading at a P/E ratio of around 12 timesFY 2010 earnings. This is well below the 10-year average given the extreme risk aversion prevailing inthe markets. However, the underlying growth in the economy and corporate earnings growth (15%in the long term) makes the market attractive from a longer-term view. The short term could seeenhanced volatility arising from various factors. Increase in commodity prices continues to be a riskin the medium term as the US dollar continues to struggle with the ballooning US fiscal situation.

Debt Market Outlook

Excess supply of government bonds, as a result of fiscal slippages to arrest the downward growthmomentum, has been a reality for bond markets since January 2009. However, this is now compoundedwith some fatigue in buying longer duration as economic data is showing signs of recovery,commodities are showing signs of rally and expectations of incremental monetary easing from theRBI are beginning to unwind. However, system liquidity remains surplus and bank deposits continueto grow thereby providing resistance to bond yields from rising sharply.

Given the above factors, we believe that the market would continue to provide tactical opportunitiesalthough the fundamental bias should be for lower duration. Also, any mitigation of bond supplypressure or a new downturn in the ongoing economic recovery may provide space for opportunisticlonger duration plays. On the other hand, if the recovery cycle continues uninterrupted and commodityprices remain firm, central banks may start to worry about withdrawing the current monetary stimulusby sometime early 2010; with consequent impact on bond markets.

2. BRIEF BACKGROUND OF SPONSORS, BOARD OF TRUSTEES AND ASSETMANAGEMENT COMPANY

a) Sponsor

HSBC Mutual Fund is sponsored by HSBC Securities and Capital Markets (India) Private Limited (HSCI).The Sponsor is the Settler of the Mutual Fund Trust. The Sponsor has entrusted a sum of Rs. 1,00,000(Rupees One Lakh only) to the Trustee as the initial contribution towards the corpus of the MutualFund.

HSCI is a member of the HSBC Group, one of the largest banking and financial services organisations,in the world. Headquartered in London, HSBC operates through long-established businesses in fiveregions: Europe, Asia-Pacific, Middle East, America and Africa. Through its global network of 10,000offices in 86 countries and territories, HSBC provides a comprehensive range of financial services topersonal, commercial, corporate, institutional investment and private banking clients.

HSCI offers integrated investment banking services, securities and corporate finance & advisory. HSCIis a member of The Bombay Stock Exchange Limited and National Stock Exchange (capital and derivativemarket segments) and is also a category I merchant banker and underwriter registered with Securitiesand Exchange Board of India.

HSCI holds 100% of the paid-up equity share capital of the AMC.

Trustees' ReportFor the year ended March 31, 2009 (Contd...)

6

b) HSBC Mutual Fund

HSBC Mutual Fund ("the Mutual Fund" or "the Fund") has been constituted as a Trust in accordancewith the provisions of the Indian Trusts Act, 1882 (2 of 1882) vide a Trust Deed dated February 7,2002 with HSBC Securities and Capital Markets (India) Private Limited, as the Sponsor and the Boardof Individual Trustees. The Trustee has entered into an Investment Management Agreement datedFebruary 7, 2002 with HSBC Asset Management (India) Private Limited (the AMC) to function as theInvestment Manager for all the Schemes of the Fund. The Fund was registered with SEBI videregistration number MF/046/02/5 dated May 27, 2002.

The Trust has been formed for the purpose of pooling of capital from the public for collectiveinvestment in securities / any other property for the purpose of providing facilities for participationby persons as beneficiaries in such properties / investments and in the profits / income arising therefrom.

c) Board of Trustees (the Trustees)

The Board of Trustees are the exclusive owner of the Trust Fund and holds the same in trust for thebenefit of the unitholders. The Trustees have been discharging their duties and carrying out theirresponsibilities as provided in the SEBI (Mutual Funds) Regulations, 1996 and the Trust Deed. TheTrustees seeks to ensure that the Fund and the Schemes floated thereunder are managed by theAMC in accordance with the Trust Deed, the said Regulations, directions and guidelines issued bySEBI, the Stock Exchanges, the Association of Mutual Funds of India and other regulatory agencies.

d) Asset Management Company (the AMC)

HSBC Asset Management (India) Private Limited (the Investment Manager or the AMC) is a privatelimited company incorporated under the Companies Act, 1956 on December 12, 2001 having itsRegistered Office at 314, D. N. Road, Fort, Mumbai 400 001. HSBC Asset Management (India) PrivateLimited has been appointed as the Asset Management Company of the HSBC Mutual Fund by theTrustee vide Investment Management Agreement (IMA) dated February 7, 2002 and executed betweenthe Trustees and the AMC. SEBI approved the AMC to act as the Investment Manager of the Fundvide. its letter No. MFD/BC/163/2002 dated May 27, 2002.

The paid-up equity share capital of the AMC is Rs. 9 crores. HSBC Securities and Capital Markets(India) Private Limited holds 100% of the paid-up equity share capital of the AMC.

3. INVESTMENT OBJECTIVE OF THE SCHEMEThe investment objective of the Scheme has been provided above under the heading "SchemePerformance, Future Outlook and Operation of the Scheme" (refer Section 1).

4. SIGNIFICANT ACCOUNTING POLICIESThe accounting policies are in accordance with Securities and Exchange Board of India (Mutual Funds)Regulations, 1996.

5. UNCLAIMED DIVIDENDS & REDEMPTIONSSummary of number of Investors & corresponding amount

Unclaimed Dividends Unclaimed Redemptions

Scheme Amount No. of Amount No. of(Rs.) Investors (Rs.) Investors

HSBC Equity Fund 2,260,240.73 591 1,092,845.98 34

6. INVESTOR SERVICESDuring the year, the number of official points of acceptance of transactions increased significantly toabout 182 locations. In addition to the offices of the transfer agency, the company has InvestorService Centres in 14 locations at its own offices - namely Mumbai, New Delhi, Kolkata, Chennai,

Trustees' ReportFor the year ended March 31, 2009 (Contd...)

7

Trustees' ReportFor the year ended March 31, 2009 (Contd...)

Bangalore, Hyderabad, Pune, Ahmedabad, Indore, Chandigarh, Kochi, Coimbatore, Lucknow andVadodara. With a view to enhancing customer convenience, the Asset Management Company hasextended the facility of crediting investor bank accounts directly by way of NEFT / RTGS (for credit ofredemption and dividend proceeds). The AMC endeavours to despatch dividend proceeds within 5working days from the Record Date in all Schemes. The internal standards on redemption payoutshave been consistently met, with very few exceptions. The number of locations for the ECS AutoDebit facility for investments through Systematic Investment Plan also increased to about 74 byMarch 2009.

On the distribution front, the number of empanelled distributors increased from 7859 as on 31March, 2008 to 8632 as on 31 March, 2009. During the year, the Asset Management Companyinitiated tie-ups for online distribution of the Mutual Fund's schemes with several channel partnerstaking the total number of such tie-ups to 24 (Angel Capital & Department Market Ltd., Bajaj CapitalLimited, Bonanza Portfolio Limited, Citibank N.A., Citigroup Wealth Advisors India Private Limited,HDFC Bank Limited, Hongkong & Shanghai Banking Corporation Limited, HSBC Corporate InvestmentSolution Services, ICICI Securities Limited, India Infoline Limited, Karvy Stock Broking Limited, KotakMahindra Bank Limited, Kotak Securities Limited, Motilal Oswal Securities Limited, NJ India InvestPrivate Limited, Reliance Securities Limited, RR Investors Capital Services Private Limited, SBICAPSecurities Limited, Sharekhan Limited, SMC Global Securities Limited, Standard Chartered - STCICapital Markets Ltd., Tom Distribution Services Limited, Yes Bank Limited).

Call centre operations have been extended to cover the entire country. The Asset ManagementCompany has outsourced certain back office services including call centre services to HSBC Operationsand Processing Enterprise (India) Private Limited (HOPE).

7. STATUTORY DETAILSa) The Sponsors are not responsible or liable for any loss resulting from the operation of the Schemes

of the Fund beyond initial contribution of Rs. 1 lakh for setting up the Fund.

b) The price and redemption value of the units, and income from them, can go up as well as downwith fluctuations in the market value of its underlying investments.

c) Full / Abridged Annual Report shall be disclosed on the website at www.assetmanagement.hsbc.com/inand shall be available for inspection at the Head Office of the mutual fund. Present and prospectiveunit holder can obtain copy of the trust deed, the Full / Abridged Annual Report of the Scheme(s),the Annual Report of HSBC Asset Management (India) Private Limited and the text of the relevantScheme(s) at a price.

8. ACKNOWLEDGEMENTSThe Trustees wish to thank the Unitholders of the Schemes for their support throughout the year andalso thank the Government of India, the Securities and Exchange Board of India (SEBI), the ReserveBank of India (RBI) and the Association of Mutual Funds in India (AMFI) for the guidance provided bythem. The Trustees also appreciate the service provided by the Registrar and Transfer Agent, FundAccountant, Custodian, Bankers, Distributors and Brokers. The guidance and services provided bythe Auditors and advocates and the ebullience, sincerity and dedication of the employees of HSBCAsset Management (India) Private Limited is also appreciated.

The Trustees look forward to the continued support of everyone.

For and on behalf of the Board of Trustees of HSBC Mutual Fund

Dilip J. Thakkar

Trustee

MUMBAIJuly 6, 2009

8

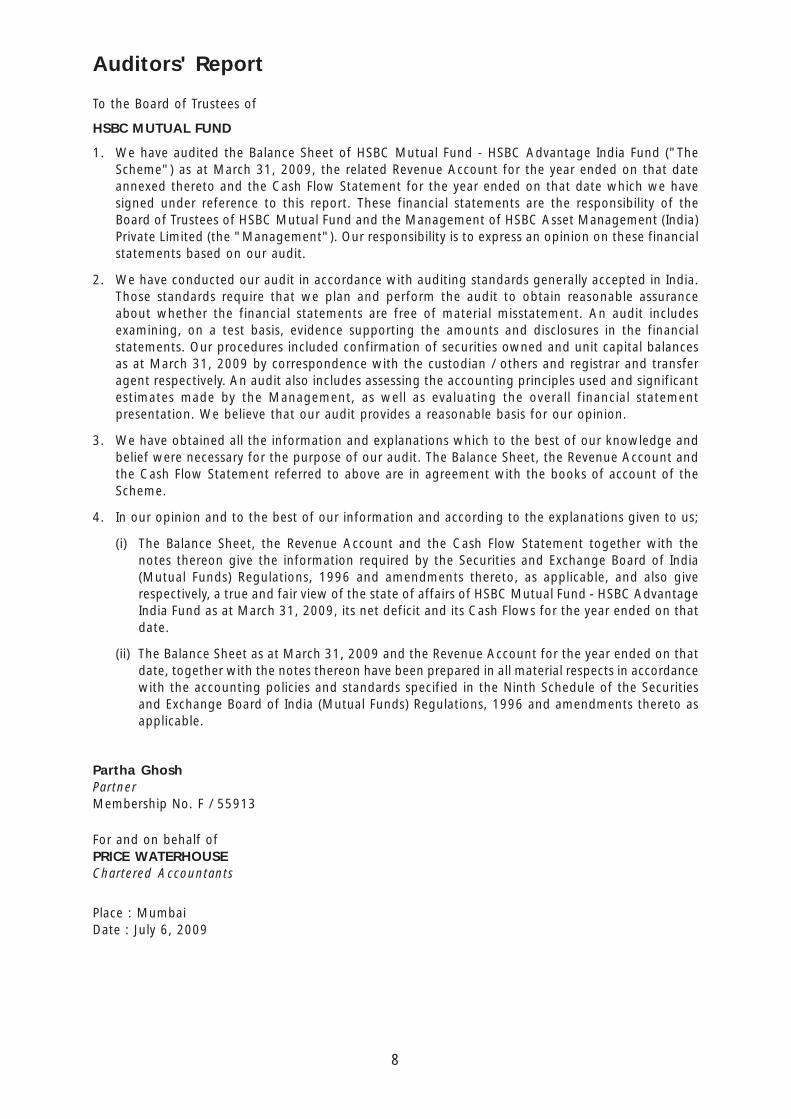

To the Board of Trustees of

HSBC MUTUAL FUND

1. We have audited the Balance Sheet of HSBC Mutual Fund – HSBC Equity Fund (“The Scheme”) asat March 31, 2009, and the related Revenue Account for the year ended on that date annexedthereto and the Cash Flow Statement for the year ended on that date which we have signedunder reference to this report. These financial statements are the responsibility of the Board ofTrustees of HSBC Mutual Fund and the Management of HSBC Asset Management (India) PrivateLimited (the “Management”). Our responsibility is to express an opinion on these financialstatements based on our audit.

2. We have conducted our audit in accordance with auditing standards generally accepted in India.Those standards require that we plan and perform the audit to obtain reasonable assuranceabout whether the financial statements are free of material misstatement. An audit includesexamining, on a test basis, evidence supporting the amounts and disclosures in the financialstatements. Our procedures included confirmation of securities owned and unit capital balancesas at March 31, 2009 by correspondence with the custodian / others and registrar and transferagent respectively. An audit also includes assessing the accounting principles used and significantestimates made by the Management as well as evaluating the overall financial statementpresentation. We believe that our audit provides a reasonable basis for our opinion.

3. We have obtained all the information and explanations which to the best of our knowledge andbelief were necessary for the purpose of our audit. The Balance Sheet and the Revenue Accountreferred to above are in agreement with the books of account of the Scheme.

4. In our opinion and to the best of our information and according to the explanations given to us,

(i) The Balance Sheet, the Revenue Account together with the notes thereon give the informationrequired by the Securities and Exchange Board of India (Mutual Funds) Regulations, 1996 andamendments thereto, as applicable, and also give respectively, a true and fair view of thestate of affairs of HSBC Mutual Fund – HSBC Equity Fund as at March 31, 2009, its net deficitand its Cash Flow for the year ended on that date.

(ii) The Balance Sheet as at March 31, 2009 and the Revenue Account for the year ended on thatdate, together with the notes thereon have been prepared in all material respects in accordancewith the accounting policies and standards specified in the Ninth Schedule of the Securitiesand Exchange Board of India (Mutual Funds) Regulations, 1996 and amendments thereto asapplicable.

Partha GhoshPartnerMembership No. F / 55913

For and on behalf ofPRICE WATERHOUSEChartered Accountants

Place : MumbaiDate : July 6, 2009

Auditors' Report

9

Rs. in Lakhs

HSBC EQUITY FUND

As at As atMarch 31, 2009 March 31, 2008

LIABILITIES1 Unit Capital 39,846.26 27,768.99

2 Reserves & Surplus2.1 Unit Premium Reserves 2,119.08 (1,512.61)2.2 Unrealised Appreciation Reserve 22.03 11,687.792.3 Other Reserves 67,221.65 67,739.38

3 Loans & Borrowings – –

4 Current Liabilities & Provisions4.1 Provision for doubtful Income/Deposits – –4.2 Other Current Liabilities & Provisions 1,337.53 3,546.52

TOTAL 110,546.55 109,230.07

ASSETS1 Investments1.1. Listed Securities:1.1.1 Equity Shares 85,046.83 89,681.441.1.2 Preference Shares – –1.1.3 Equity Linked Debentures – –1.1.4 Other Debentures & Bonds – –1.1.5 Securitised Debt securities – –

1.2 Securities Awaited Listing:1.2.1 Equity Shares – –1.2.2 Preference Shares – –1.2.3 Equity Linked Debentures – –1.2.4 Other Debentures & Bonds – –1.2.5 Securitised Debt securities – –

1.3 Unlisted Securities:1.3.1 Equity Shares – –1.3.2 Preference Shares – –1.3.3 Equity Linked Debentures – –1.3.4 Other Debentures & Bonds – –1.3.5 Securitised Debt securities – –

1.4 Government Securities – –1.5 Treasury Bills – –1.6 Commercial Paper – –1.7 Certificate of Deposits – –1.8 Bill Rediscounting – –1.9 Units of Domestic Mutual Fund – –1.10 Foreign Securities – –

Total Investments 85,046.83 89,681.44

2 Deposits 6,256.03 3,356.03

3 Other Current Assets3.1 Cash & Bank Balance 214.24 112.803.2 CBLO / Reverse Repo Lending 16,548.57 12,696.103.3 Others 2,480.88 3,383.70

4 Deferred Revenue Expenditure – –(to the extent not written off)

TOTAL 110,546.55 109,230.07

Notes to Accounts - Annexure I

Abridged Balance Sheet as at March 31, 2009

10

Rs. in Lakhs

HSBC EQUITY FUND

Current PreviousYear ended Year ended

March 31, 2009 March 31, 2008

1 INCOME1.1 Dividend 1,130.00 607.111.2 Interest 1,426.94 760.991.3 Realised Gain / (Loss) on Foreign Exchange Transactions – (0.26)1.4 Realised Gains / (Losses) on Interscheme

sale of investments – –1.5 Realised Gains / (Losses) on External sale /

redemption of investments (28,846.88) 29,908.861.6 Realised Gains / (Losses) on Derivative Transactions 1,828.55 409.921.7 Other Income – –

(A) (24,461.39) 31,686.62

2 EXPENSES2.1 Management fees 697.59 1,152.012.2 Service tax on Management fees ** – –2.3 Transfer agents fees and expenses 215.56 180.062.4 Custodian fees 58.33 52.722.5 Trusteeship fees 0.45 0.362.6 Commission to Agents * – –2.7 Marketing & Distribution expenses 1,205.76 600.692.8 Audit fees 5.50 7.002.9 Other operating expenses 20.45 282.24

(B) 2,203.64 2,275.08

3 NET REALISED GAINS / (LOSSES)FOR THE YEAR / PERIOD (A - B = C) (26,665.03) 29,411.54

4 Change in Unrealised Depreciation invalue of investments (D) 16,683.17 3,782.43

5 NET GAINS / (LOSSES) FOR THEYEAR /PERIOD [E = (C - D)] (43,348.20) 25,629.11

6 Change in unrealised appreciationin the value of investments (F) – 96.57

7 NET SURPLUS / (DEFICIT) FORTHE YEAR / PERIOD (E + F = G) (43,348.20) 25,725.68

7.1 Add: Balance transfer from UnrealisedAppreciation Reserve – –

7.2 Less: Balance transfer to Unrealised Appreciation Reserve – –7.3 Add / (Less): Equalisation 31,164.97 7,197.26

8 TOTAL (12,183.23) 32,922.94

9 Dividend Appropriation9.1 Income Distributed during the year / period 0.25 23,365.399.2 Tax on income distributed during the year / period – –

10 Retained Surplus / (Deficit) carriedforward to Balance Sheet (12,183.48) 9,557.55

Notes to Accounts - Annexure I* Commission to Agents is included in Marketing & Distribution Expenses.** Service Tax on Management Fees is included in Other Operating Expenses.

Abridged Revenue Account for the year ended March 31, 2009

11

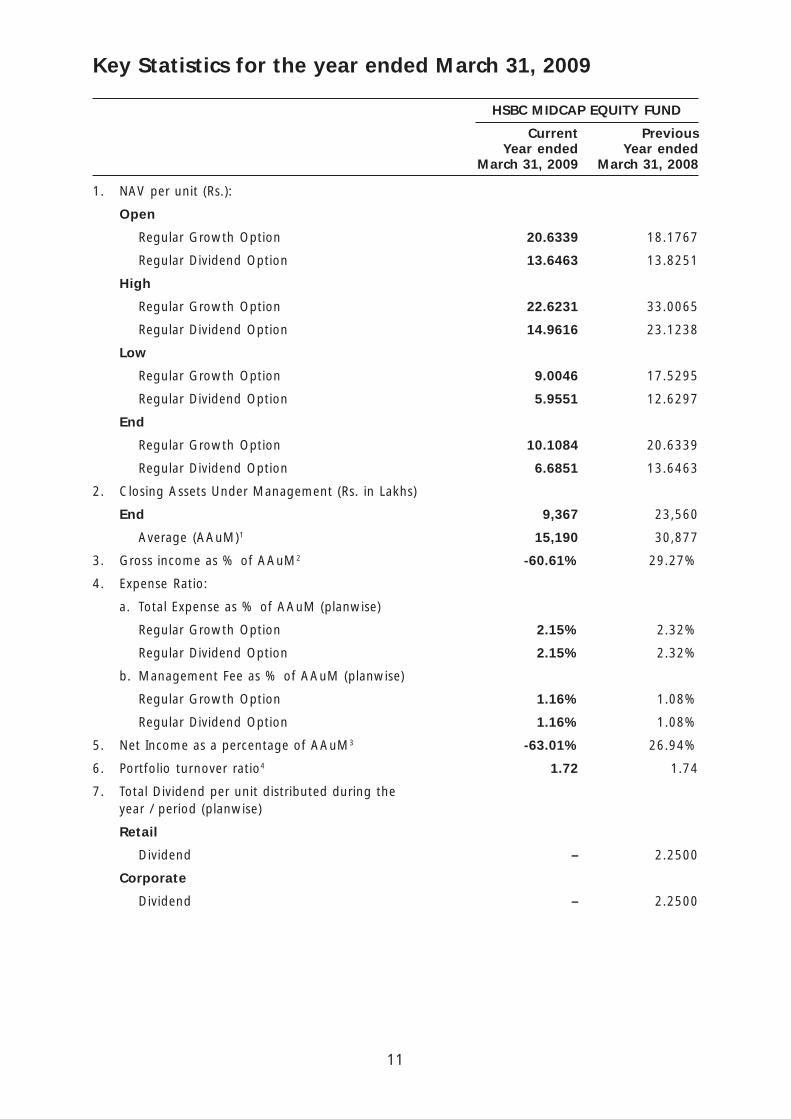

HSBC EQUITY FUND

Current PreviousYear ended Year ended

March 31, 2009 March 31, 2008

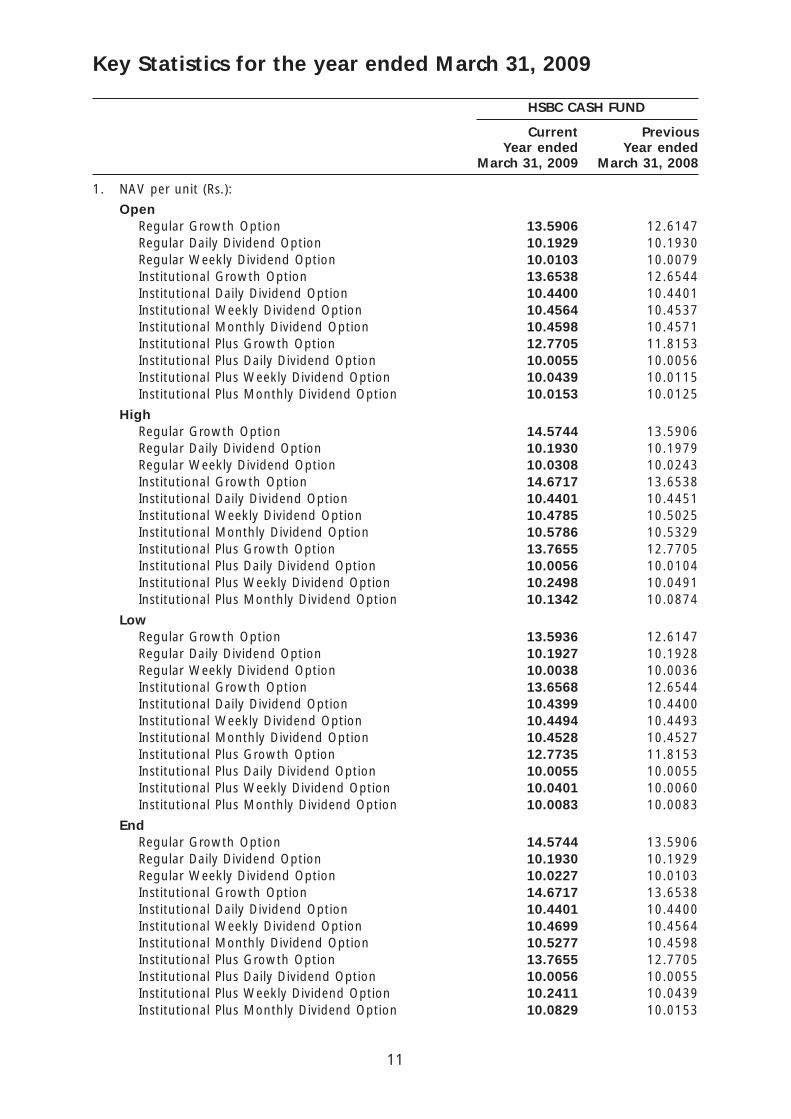

1. NAV per unit (Rs.):

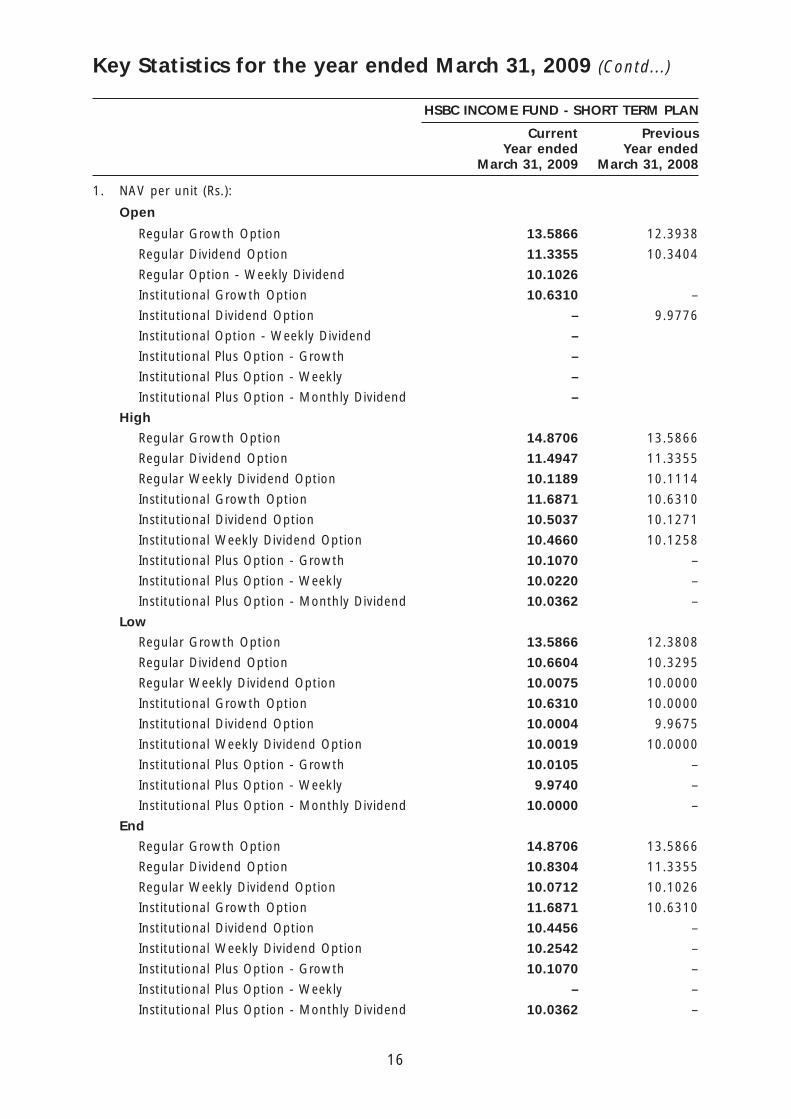

Open

Regular Growth Option 88.3814 67.8614

Regular Dividend Option 27.6286 28.1217

High

Regular Growth Option 97.1612 118.1166

Regular Dividend Option 30.3743 48.9584

Low

Regular Growth Option 52.9573 64.9581

Regular Dividend Option 16.5549 26.3571

End

Regular Growth Option 60.1737 88.3814

Regular Dividend Option 18.8099 27.6286

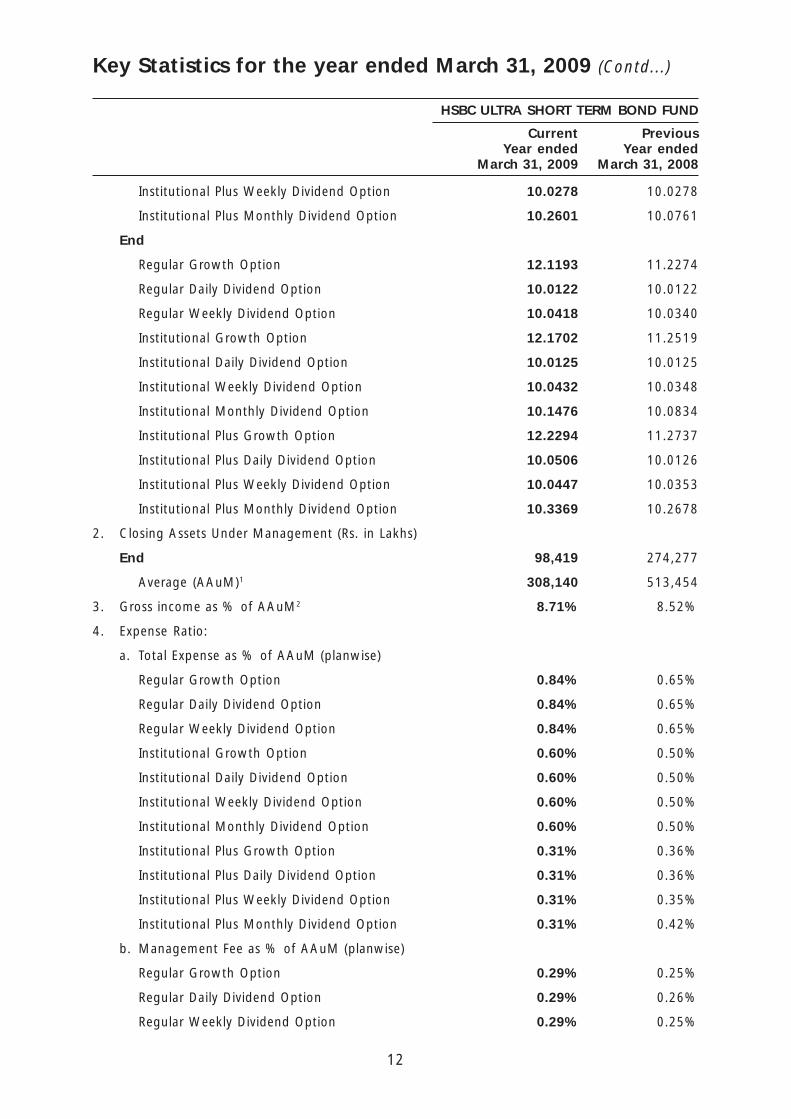

2. Closing Assets Under Management (Rs. in Lakhs)

End 109,209 105,684

Average (AAuM)1 108,793 112,899

3. Gross income as % of AAuM2 -22.48% 28.07%

4. Expense Ratio:

a. Total Expense as % of AAuM (planwise)

Regular Growth Option 2.03% 2.02%

Regular Dividend Option 2.03% 2.01%

b. Management Fee as % of AAuM (planwise)

Regular Growth Option 0.64% 1.02%

Regular Dividend Option 0.64% 1.02%

5. Net Income as a percentage of AAuM3 -24.51% 26.05%

6. Portfolio turnover ratio4 1.10 1.59

7. Total Dividend per unit distributed duringthe year (planwise)

Retail

Regular Dividend Option – 10.00

Corporate

Regular Dividend Option – 10.00

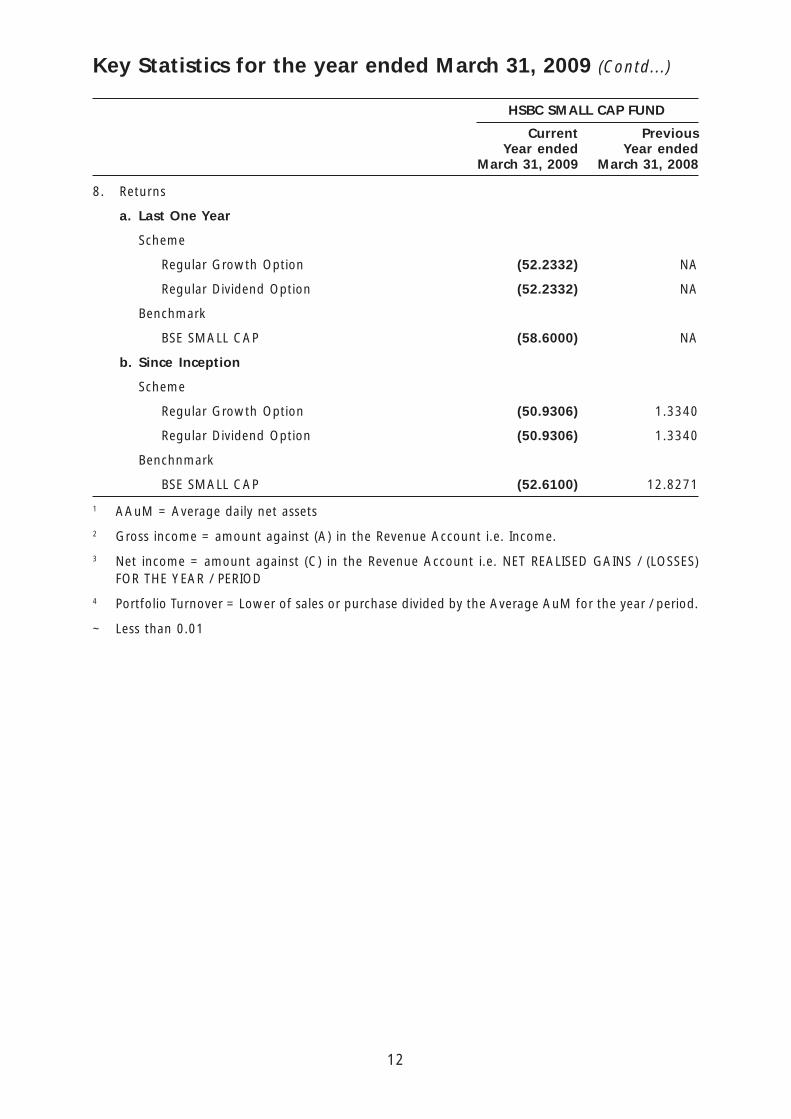

Key Statistics for the year ended March 31, 2009

12

Key Statistics for the year ended March 31, 2009 (Contd...)

HSBC EQUITY FUND

Current PreviousYear ended Year ended

March 31, 2009 March 31, 2008

8. Returns:

a. Last One Year

Scheme

Regular Growth Option (31.9159) 30.0557

Regular Dividend Option (31.9190) 30.0813

Benchmark

BSE 200 (40.9800) 24.1334

b. Since Inception

Scheme

Regular Growth Option 32.9007 50.7427

Regular Dividend Option 32.9640 50.8293

Benchmark

BSE 200 18.7800 35.5069

1 AAuM = Average daily net assets

2 Gross income = amount against (A) in the Revenue Account i.e. Income.

3 Net income = amount against (C) in the Revenue Account i.e. NET REALISED GAINS / (LOSSES)FOR THE YEAR / PERIOD

4 Portfolio Turnover = Lower of sales or purchase divided by the Average AuM for the year / period.

13

HSBC EQUITY FUND

1 Investments:

1.1. It is confirmed that investments of the schemes are registered in the name of the Trustees forthe benefit of the scheme’s unitholders.

1.2. Open Positions of derivatives amount to Rs. (123,697,400) and is 1.13% to Net Assets as ofyear end March 31, 2009. Open Positions of derivatives amount to Rs. 295,319,693 and is2.79% to Net Assets as of year end March 31, 2008.

1.3. Investments in Associates and Group Companies:

(Rupees)

Issuer Instrument Amount Aggregate Amount AggregateType Investments Investments

by all schemes by all schemes

2009 2008

The Hongkong & Fixed deposits – 43,000,000 – 1,654,000,000Shanghai BankingCorporation Ltd.

1.4. Open positions of Securities Borrowed and / or Lent by the scheme as of the Year endedMarch 31, 2009 and March 31, 2008 is NIL.

1.5. NPAs as at years ended March 31, 2009 and March 31, 2008 are NIL.

1.6. Aggregate Unrealised Gain / Loss as at the end of the Financial year 2008-2009 and percentageto net assets.

Company Amount (Rs.) Percentage to Amount (Rs.) Percentage toName Net Assets Net Assets

2009 2008

Equity Shares

– Appreciation 419,474,916 3.8410% 1,520,481,450 14.3871%

– Depreciation 921,216,805 8.4354% 361,734,504 3.4228%

Equity Futures

– Appreciation 2,218,589 0.0203% 10,031,857 0.0949%

– Depreciation 15,363 0.0001% – –

1.7. The aggregate value of investments purchased (excluding accretion of discount ofRs. 14,024,158) and sold during the financial year 2008-2009 is Rs. 20,051,454,038 andRs. 15,984,411,730 respectively being 184.31% and 146.93% of the average daily net assets.

The aggregate value of investments purchased (excluding accretion of discount of Rs. 795,592)and sold during the financial year 2007-2008 is Rs. 16,301,508,784 and Rs. 18,801,319,483respectively being 144.39% and 166.53% of the average daily net assets.

1.8 Non-Traded securities in the portfolio as on March 31, 2009 and March 31, 2008 are Nil.

Notes to Accounts - Annexure ITo the Abridged Balance Sheet and Revenue Account for the year ended March 31, 2009

14

Notes to Accounts - Annexure I (Contd...)To the Abridged Balance Sheet and Revenue Account for the year ended March 31, 2009

2 Disclosure under Regulation 25(8) of the Securities and Exchange Board of India (Mutual Funds)Regulations, 1996 as amended.

Year - 2008-2009HSBC Securities and Capital Markets (India) Private Limited, the Sponsor was paid brokerageaggregating Rs. 1,965,799 on purchase and sale of investments. The Hongkong & ShanghaiBanking Corporation Limited, an associate entity of HSBC Asset Management (India) Private Limitedwas paid collection/bank charges amounting to Rs. 39,751, brokerage amounting toRs. 72,415,284 for procuring unit subscriptions for the Scheme and clearing member charges onderivative transactions Rs. 2,429,235. The brokerage paid was at rates similar to those offered toother brokers / distributors.

Year - 2007-2008HSBC Securities and Capital Markets (India) Private Limited, the Sponsor was paid brokerageaggregating Rs. 1,527,000 on purchase and sale of investments. The Hongkong & ShanghaiBanking Corporation Limited, an associate entity of HSBC Asset Management (India) Private Limitedwas paid collection / bank charges amounting to Rs. 251,447, brokerage amounting toRs. 40,535,389 for procuring unit subscriptions for the Scheme and clearing member charges onderivative transactions Rs. 1,457,655. The brokerage paid was at rates similar to those offered toother brokers / distributors.

Further, The Hongkong and Shanghai Banking Corporation Limited, an associate of the Sponsor,is on the panel of bankers with whom HSBC Mutual Fund places money on fixed deposits andenters into reverse repo transactions from time to time at competitive rates.

3 None of the Investors held more than 25% of the total net assets of the scheme at the yearsended March 31, 2009 and March 31, 2008.

4 Unit Capital movement during the years ended March 31, 2009 and March 31, 2008.

2008-2009

Description Opening Units Subscription Redemption Closing Units Face Value

RegularGrowth Option 47,671,381.108 54,767,475.116 19,616,252.681 82,822,603.543 828,226,035.43

RegularDividend Option 230,018,561.715 146,706,869.491 61,085,405.180 315,640,026.026 3,156,400,260.26

Description 2007-2008

Description Opening Units Subscription Redemption Closing Units Face Value

RegularGrowth Option 51,373,426.727 26,228,151.971 29,930,197.590 47,671,381.108 476,713,811.68

RegularDividend Option 209,212,039.708 149,213,645.273 128,407,123.266 230,018,561.715 2,300,185,617.15

5 Previous year figures have been re-grouped/re-arranged where necessary.

6 No contingent liabilities for the years ended March 31, 2009 and March 31, 2008.

7 Expenses other than Management Fees are inclusive of Service Tax where applicable.

8 The Annual Accounts of the Schemes prepared in accordance with the accounting policies andstandards specified in the Ninth Schedule of The Securities and Exchange Board of India (MutualFunds) Regulations, 1996 has been approved by the Board of Directors of HSBC Asset Management(India) Private Limited and The Board of Trustees of HSBC Mutual Fund at their meeting held onJuly 06, 2009. The audit report attached herewith refers to the said annual accounts. The aforesaidabridged accounts are an extract of the Annual Accounts and are prepared in accordance withSEBI Circular No. IMD/Cir 8/132968/2008 dated July 24, 2008.

15

DISCLAIMERSThe content of this report has been prepared by HSBC Asset Management (India) Private Limited(HSBC) for information purposes only and should not be construed as an offer or solicitation of anoffer for purchase of any of the funds of HSBC Mutual Fund. The information is for general informationonly and does not have regard to specific investment objectives, financial situation and the particularneeds of any specific person who may receive this information. Investments in mutual funds inherentlyinvolve risks and investors should read the relevant documents / information for details and riskfactors and consult their legal, tax and financial advisors before investing. Investors should understandthat statements made herein regarding future prospects may not be realised. Neither this documentnor the units of HSBC Mutual Fund have been registered in any jurisdiction. The distribution of thisdocument in certain jurisdictions may be restricted or totally prohibited and accordingly, personswho come into possession of this document are required to inform themselves about, and to observe,any such restrictions.

Investors may obtain Statement of Additional Information, Combined Scheme Information Documentand Common Key Information Memorandums along with application forms from the office of HSBCMutual Fund, 314, D. N. Road, Fort, Mumbai 400 001. Tel: 022-6666 8819.

Statutory Details:HSBC Mutual Fund has been set up as a trust by HSBC Securities and Capital Markets (India) PrivateLimited (liability restricted to the corpus of Rs. 1 lakh). The Sponsor/associates of the Sponsor/AssetManagement Company (AMC) are not responsible or liable for any loss or shortfall resulting from theoperation of the Schemes. The Trustees of HSBC Mutual Fund have appointed HSBC Asset Management(India) Private Limited as the Investment Manager.

Risk Factors:All investments in mutual funds and securities are subject to market risks and the Net Asset Value(NAV) of the Scheme(s) may go up or down depending on the factors and forces affecting the securitiesmarkets. There can be no assurance that the objectives of the Scheme(s) will be achieved. Pastperformance of the Sponsor, AMC, Mutual Fund or any associates of the Sponsor/AMC does notindicate the future performance of the Scheme(s) of the Mutual Fund. HSBC Equity Fund (HEF) is thenames of the Scheme and does not in any manner indicate the quality of the Scheme or its futureprospects or returns.

Terms of Issue:Units of the Scheme(s) are being offered at NAV based prices, subject to the prevailing loads. TheAMC calculates and publishes NAVs and offers for sale, redemption and switch outs, units of theScheme(s) on all Business Days, at the Applicable NAV for all Schemes (at least once a week, i.e.,every Wednesday and daily during the period of redemption in case of HSCF). HUOF, HSCF & HFTSwill not be open for ongoing subscriptions/ switch ins. HUOF & HSCF would be available for sale onan ongoing basis (after a period of 3 years from the date of allotment). Conversion of HUOF & HSCFto an open-ended scheme will be done only after the balance unamortized amount has been fullyrecovered from the Scheme. Units can be redeemed/switched out on every Business Day at NAVbased prices, subject to prevailing exit loads. In case of HSCF, units can be redeemed / switched outon a monthly basis on the stipulated date i.e. last 3 business days of every month at NAV basedprices, subject to provisions of exit load, if any and recovery of balance proportionate unamortizedNFO expenses.

Load Structure (includes SIP/STP):Entry - 2.25% for investments/switch ins* < Rs. 5 crores, otherwise Nil. For switch transactions fromHCF to HEF (excludes existing & prospective STP transactions) - Nil.

Exit - 1.25% for < Rs. 5 crores, if redeemed/switched out* within 1 year from date of investment,otherwise Nil. For switch transactions from HCF to HEF and subsequent switch transactions from HEFto any other debt or equity scheme (excludes existing & prospective STP transactions) - 2.25% for <Rs. 5 crores, if above switch investments are redeemed / switched out within 1 year from the date ofswitch, otherwise Nil.

*No load in case of switches between equity Schemes of HSBC Mutual Fund.

Consult the nearest investor service centre for details.

The entry/exit load set forth above is subject to change at the discretion of the AMC and suchchanges shall be implemented prospectively.

Mutual Fund investments are subject to market risks. Please read the Statement of AdditionalInformation and Scheme Information Document carefully before investing.

Value Research Online DisclaimerValue Research Fund Ratings: Value Research Fund Ratings are a composite measure of historical risk-adjusted returns. In the case of equity funds this rating is based on the average monthly returns forthe last 3-year and 5-year period. These ratings do not take into account any entry or exit load.

Value Research Fund Ratings are subject to change every month. Current Fund Ratings are as onMarch 31, 2009. 142 open-ended Equity: Diversified Funds were rated. The Rating is based on primarydata provided by respective funds; Value Research does not guarantee the accuracy. Ranking Entity:Value Research Online.

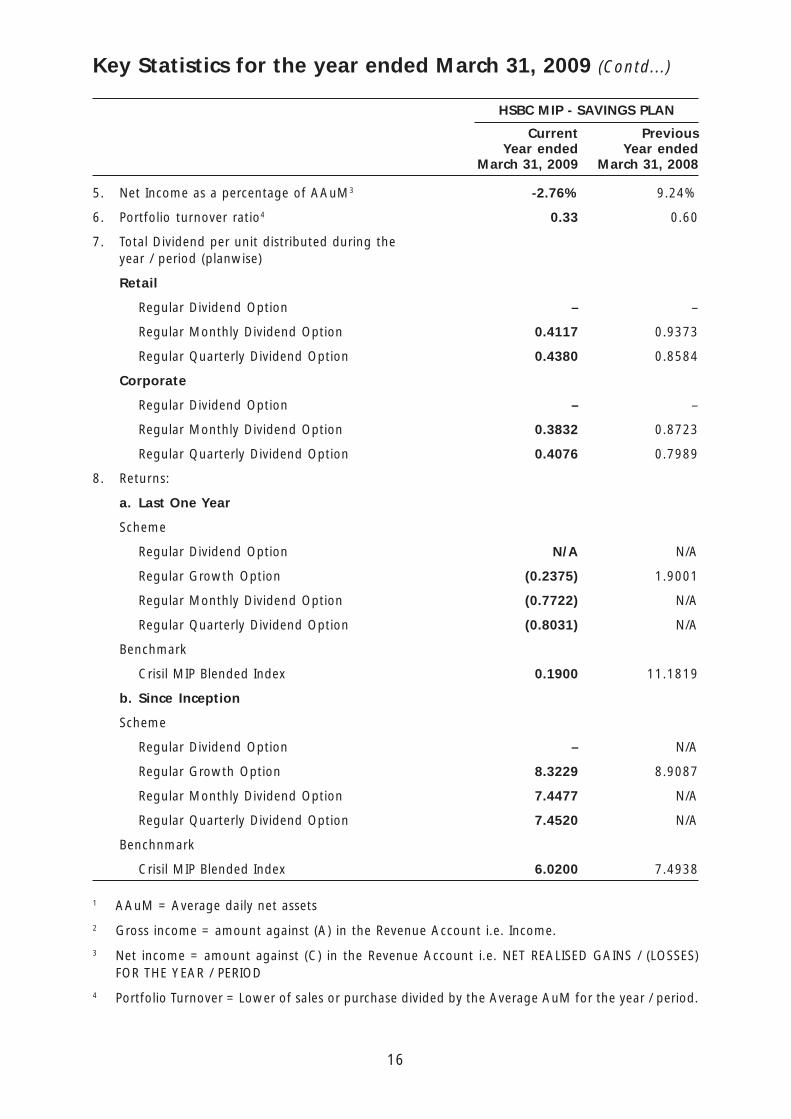

ICRA Online Ranking MethodologyHSBC Monthly Income - Savings Plan has been ranked as a Five Star Fund in the category of 'OpenEnded Marginal Equity' schemes for its 3 year performance till December 31, 2008.

The rank is an outcome of an objective and comparative analysis against various parameters, including:risk adjusted return, fund size, company concentration, portfolio turnover and liquidity. The rankingmethodology did not take into account entry and exit loads imposed by the Fund. There were 27schemes considered in 'Open Ended Marginal Equity' category for the ranking exercise. The rank isneither a certificate of statutory compliance nor any guarantee on the future performance of HSBCMonthly Income - Savings Plan. Ranking Source & Publisher: ICRA Online Limited.

CRISIL Ranking MethodologyThe selection for the awards is based on the CRISIL FundServices' Composite Performance Ranking(CRISIL~CPR) methodology.

The CRISIL Composite Performance Ranking (CRISIL~CPR) is a quarterly ranking of mutual fund schemesbased on two year performance (excepting for the liquid and short term debt categories where a oneyear performance horizon is considered). The methodology is based on global best practices,customized to account for Indian market nuances. Over time, the rankings have become the industrystandard with good acceptance among Investors, Fund Intermediaries, Asset Management Companies,etc. The performance criteria covers not only risk adjusted returns, which are historical, but also theportfolio constitution to make the analysis forward looking.

CRISIL DisclaimerThe overall ranking is assigned to the scheme based on its weighted average score on a range ofparameters: Superior Return Score, Concentration, Liquidity, Asset Quality - Measures the creditquality of the portfolio, Average Maturity and Asset Size. HSBC MIP - Savings was the only schemethat won the CNBC TV18 - CRISIL Mutual Fund of the Year Award in the Category - Monthly IncomePlans - Aggressive. In total 13 schemes were eligible for the award universe. Schemes present in allfour quarterly CRISIL CPRs were considered for the award. The award is based on consistency of thescheme's performance in the four quarterly CRISIL CPR rankings released during the calendar year2008. The individual CRISIL CPR parameter scores averaged for the four quarters were further multipliedby the parameter weights as per the CRISIL CPR methodology to arrive at the final scores. A detailedmethodology of the CRISIL CPR is available at www.crisil.com. Past performance is no guarantee offuture results. Rankings and Award Source: CRISIL Fund Services, CRISIL Ltd. HSBC Monthly Income -Savings Plan has been ranked as a Five Star Fund in the category of 'Open Ended Marginal Equity'schemes for its 3 year performance till December 31, 2008. The rank is an outcome of an objectiveand comparative analysis against various parameters, including: risk adjusted return, fund size,company concentration, portfolio turnover and liquidity. The ranking methodology did not take intoaccount entry and exit loads imposed by the Fund. There were 27 schemes considered in 'OpenEnded Marginal Equity' category for the ranking exercise. The rank is neither a certificate of statutorycompliance nor any guarantee on the future performance of HSBC Monthly Income - Savings Plan.Ranking Source & Publisher: ICRA Online Limited.

16

Issued by HSBC Asset Management (India) Private Limited

HSBC Global Asset Management

HSBC India Opportunities FundAn open-ended flexi-cap equity Scheme

Abridged Annual Report 2008 - 2009

1

Dear Investor,

We thank you for investing with HSBC Mutual Fund. We are pleased to inform you that HSBCMutual Fund has won prestigious awards* this year at various forums in India.

The awards* won by our schemes in India are

� HSBC Equity Fund has been included in the 5 star rated fund category (“Top rated mutualfunds” by Value Research online) in March, 2009.

� Five-stars indicate that a fund is in the top 10 per cent of its category in terms ofhistorical risk-adjusted returns.

� ICRA Mutual Fund Awards 2009

� HSBC MIP - Savings has been ranked a 5-Star Fund by ICRA Online indicating performanceamong the top 10% in the category of 'Open Ended Marginal Equity' for 3 yearperformance ending 31 December, 2008.

� CNBC TV18 - CRISIL Mutual Fund Awards 2008

� HSBC MIP - Savings was awarded the CNBC TV18 - CRISIL Mutual Fund of the YearAward for the year 2008 in the Monthly Income Plans - Aggressive Category.

(Past performance is no guarantee of future results. * Please refer to Ranking methodologyand disclaimer mentioned at the end of the Abridged Annual Report for the year endedMarch 31, 2009).

At the global level, the HSBC Group won several awards at Euromoney's Awards for Excellence2009. The top awards that HSBC won were the Best Global Bank and the Best Global DebtHouse. It was also honoured as the Best Debt House in 8 locations including Asia and the Bestat Risk Management in Asia. (Past performance may or may not be sustained in the future andis no guarantee of future results). We continue to be one of the leading players in emergingmarkets and remain committed to our asset management business in India.

HSBC Asset Management (India) Private Limited including the mutual fund business as well asthe PMS business (including EPFO money deployed till date) manages assets of about Rs. 26280Crores as at 30 June, 2009. The core to our winning strategy is our endeavour to deliverconsistent performance over the medium to long term for our investors in a risk controlledenvironment and aim for consistent wealth creation under varying market conditions. Throughour product range, we aim to be true to our reputation in India of being a provider ofinternational quality investment products and services.

We remain committed to our philosophy of aiming for consistent wealth creation and serviceexcellence and look forward to your continued investments in HSBC Mutual Fund.

Yours sincerely,

VikramaadityaChief Executive OfficerHSBC Asset Management (India) Private Limited

2

SPONSORHSBC Securities and Capital Markets (India) Private LimitedRegd. Office: 52/60, Mahatma Gandhi Road, Fort, Mumbai 400 001.

TRUSTEEBoard of TrusteesOffice: 314, D. N. Road, Fort, Mumbai 400 001.

ASSET MANAGEMENT COMPANYHSBC Asset Management (India) Private LimitedCorp. & Regd. Office: 314, D. N. Road, Fort, Mumbai 400 001.

CUSTODIANJP Morgan Chase BankCorp. & Regd. Office: Mafatlal Centre, 9th Floor, Nariman Point, Mumbai - 400 021.

AUDITORS TO THE SCHEMEPrice WaterhouseChartered Accountants252, Veer Savarkar Marg, Shivaji Park, Dadar (West), Mumbai - 400 028.

LEGAL ADVISORSBharucha & Partners4th Floor, Cecil Court, Mahakavi Bhushan Marg, Colaba, Mumbai - 400 039.

REGISTRAR & TRANSFER AGENTSComputer Age Management Services (P) Ltd. (CAMS)Rayala Towers, Tower I, III Floor, 158 Anna Salai, Chennai - 600 002.

BOARD OF TRUSTEESMr. N. P. Gidwani - Chairman

Dr. Rudolf ApenbrinkMr. Nasser MunjeeMr. Manu TandonMr. Mehli MistriMr. Dilip J. Thakkar

BOARD OF DIRECTORSMs. Naina Lal Kidwai - Chairman

Mr. Ayaz EbrahimMr. S. P. Mustafa**Mr. Vithal PalekarMs. Kishori J. Udeshi*Mr. Vikramaaditya - Chief Executive Officer***

* Ms. Kishori Udeshi has been appointed as a Director with effect from 14 January 2009 andMr. Jagjit Lal Pasricha has resigned as a Director with effect from 19 January 2009.

** Mr. S. P. Mustafa has been appointed as a Director with effect from 2 September 2008 andMr. Nawshir Khurody has resigned as a Director with effect from 1 September 2008

*** Mr. Vikramaaditya has been appointed as the Chief Executive Officer with effect from 16 July 2008and Mr. Sanjay Prakash has resigned as the Chief Executive Officer with effect from 16 July 2008.

3

Trustees' ReportFor the year ended March 31, 2009

The Trustees present the seventh report and the audited financial statements of the Schemesof HSBC Mutual Fund (the "Fund"), for the year ended March 31, 2009.

1. SCHEME PERFORMANCE, FUTURE OUTLOOK AND OPERATIONS OF THE SCHEME

a) Operations and Performance of the Scheme

HSBC India Opportunities Fund (HIOF) - an open-ended flexi-cap Equity Scheme

HIOF is a diversified equity scheme, which seeks long term capital growth through investmentsacross all market capitalisations, including small, mid and large cap stocks. The fund aims to bepredominantly invested in equity and equity related securities. However, it could move asignificant portion of its assets towards fixed income securities if the fund manager becomesnegative on equity markets.

The net assets of the Scheme amounted to Rs. 279.93 crores as at March 31, 2009 as comparedto Rs. 522.72 crores as at March 31, 2008. 92.43% of the net assets were invested in equitiesand 7.57% were invested in debt and money market instruments as at March 31, 2009.

The fund outperformed the benchmark by 600 bps in the past 1 year on higher than normalcash levels and a defensive portfolio. In the Financial Year 2009, the fund completed 5 years ofexistence which is usually a metric tracked by various fund evaluators.

Date of Inception : 24 February, 2004 Compounded Annualized Returns (%)

Schemes (P2P) 1 Year 3 Years 5 Years SinceInception

HSBC India Opportunities Fund - Growth -36.60 -5.10 15.40 14.21

BSE 500 -42.77 -7.94 9.44 9.15

Past performance may or may not be sustained in future. 'Since inception' returns are calculatedon Rs. 10 invested at inception. Calculations are based on Growth NAVs.

b) Market Overview & Outlook

MARKET OVERVIEW

(as furnished by HSBC Asset Management (India) Private Limited)

Equity Market Overview

The financial year ended 31 March, 2009 was a highly eventful one with long standing institutionsdisappearing from the landscape in the whirlwind of the sub-prime crisis and derivative losses. Theyear can be split into three phases - the first from April 2008 till when Lehman Brothers filed forbankruptcy, which saw a blowout commodity rally (crude oil nudged close to USD 144/barrel) andthe sub-prime situation turning progressively worse. The United States (US) Government / FederalReserve bailed out major institutions thought to be critical to the functioning of the financial system.The second phase from September 2008 till January 2009 saw a spate of bankruptcies most notablyLehman Brothers which saw the appearance of an acute level of risk aversion pushing the creditmarkets into a gridlock. This phase also coincided with the fiscal / monetary stimuli by variousgovernments to take the credit crisis head on. Globally, markets stabilized around their October2008 lows and a semblance of normality started re-appearing in financial markets in this period. Thethird phase from February 2009 onwards witnessed a sharp rally as a weakening US Dollar spewedmoney into emerging markets. The sensex fell by 38% during the financial year.

4

For the financial year 2009, the popular indices viz. BSE Sensex and CNX Nifty were down 37.94%and 36.19% respectively. The BSE Midcap (54.01)% and the broader indices like BSE 200 (40.98)%and BSE 500 (42.77)% also reflected the correction across the markets. Within sectoral indices thebest performing indices were BSE FMCG (11.08)% and BSE Oil and Gas (29.58)% while the worstperforming indices were BSE Realty (79.37)%, due to the high leverage on the balance sheets, BSEMetals (58.67)%, due to slowdown in global growth and BSE Consumer Durables (58.14)% and BSECapital goods (53.84%).

In a year that saw sell-off across emerging markets, FIIs were net sellers of the tune USD 10.4 billionin the Indian equity markets while Domestic Institutional Investors (Insurance & Mutual Funds) werebuyers to the tune of USD 13.1 billion. Further, FIIs were net sellers in the derivative markets ashedge funds, and p-notes unwound positions in a rapidly deleveraging world. Thus, sentimentremained negative as few US based investment banks filed for bankruptcy in the midst of the liquidityand credit crisis and safety took precedence over growth.

Debt Market Overview

Two contrarian forces one inflationary and the other deflationary had been in play since 2007: Onthe one hand strong demand from emerging economies were leading commodities higher and fuellinginflation, while on the other the housing led credit crisis in the US was starting to exert a deflationaryforce. The first force was dominant till early July 2008 leading commodity prices to fresh peaks andinflation to multi year highs. Since then, however, the second force took hold with the result thatcommodity prices fell sharply from the top, growth and inflation numbers toppled worldwide, andcentral bankers shifted focus to achieving financial stability and protecting growth.

The financial crisis hit the domestic markets towards September 2008, leading to acute disruption inmoney markets. The Reserve Bank of India (RBI) acted proactively cutting the cash reserve ratio (CRR)by an unprecedented 400 bps between September 2008 and January 2009. Similarly, the reverserepo rate had been cut by 275 bps since October 2008 while the repo rate had been cut by 425 bpsover the same period.

Bond market yields fell in line with the unprecedented monetary easing up till the first week ofJanuary 2009. Thereon, supply pressures on bond markets rose as a result of government fiscalslippages aimed at stimulating the economy. The RBI, in line with similar measures elsewhere in theworld, started buying government securities to lessen the impact on yields from the rise in governmentborrowing. Although this helped market sentiment, it could not prevent a general rise in yieldstowards fiscal close. As a result, the 10 year benchmark sovereign yield closed the fiscal at 7% froma low of sub 5% hit in early January 2009. Money market rates stabilized after the initial mayhem ofSeptember 2008 and October 2008 and liquidity came back to interbank markets.

MARKET OUTLOOK

(as furnished by HSBC Asset Management (India) Private Limited)

Equity Market Outlook

Financial Year (FY) 2008-09 was a year marked by a strong correlation between the Indian marketand global markets with key indices ending deeply in the red on the back of the subprime crisis andderivative led losses across major financial stocks in the United States (US). Even in India, forex lossesran across corporate India though at a smaller magnitude. FY 10 has begun on a better note onaccount of various fundamental and technical factors.

GDP for FY 09 grew at 6.7% against FY 08 levels of 9%. Agriculture posted a below trend growthrate of 1.6% and industry grew by 3.9% (versus 8.1% in FY 08) with services registering a close to9.7% growth. IIP grew by a mere 2.6%. Although order books of engineering / capital goods wererunning at record high levels, there was possibility of delays in execution as funding sources for thedevelopers (equity, ECB, private equity, FCCB) had dried up. A sharp increase in subsidy on account

Trustees' ReportFor the year ended March 31, 2009 (Contd...)

5

of oil, fertilizers and food led to a cut back in discretionary spending. Inflation rose on the back of asurging crude and higher prices of agricultural commodities to top at 12.91% for the week ending 2August, 2008. A slow down in the growth rates in the US / EU and other markets finally tamed thesurge in crude. As growth rates stumbled, governments / monetary authorities the world over triggeredfiscal stimuli / monetary easing to escape recessionary forces. This was followed in India as wellwhich started monetary easing / fiscal stimuli to keep growth rates buoyant.

On the positive side, India continues to do better in relative terms and we expect GDP growth of6-6.5% for FY10. The broad themes that are driving domestic growth viz. capital expenditure,infrastructure building and domestic consumption are still intact. The key concerns at this pointstems from a ballooning fiscal deficit at the consolidated level (Centre & State) with salary revisionfor Central / State Government employees threatening a cut back in discretionary spending. Inflationis likely to remain benign for the first half of FY10 on a favourable base effect but we anticipate it togo back to trend levels of 5-5.5% for the second half of FY10 as this base effect wears off.

On a valuations perspective, the markets are currently trading at a P/E ratio of around 12 timesFY 2010 earnings. This is well below the 10-year average given the extreme risk aversion prevailing inthe markets. However, the underlying growth in the economy and corporate earnings growth (15%in the long term) makes the market attractive from a longer-term view. The short term could seeenhanced volatility arising from various factors. Increase in commodity prices continues to be a riskin the medium term as the US dollar continues to struggle with the ballooning US fiscal situation.

Debt Market Outlook

Excess supply of government bonds, as a result of fiscal slippages to arrest the downward growthmomentum, has been a reality for bond markets since January 2009. However, this is now compoundedwith some fatigue in buying longer duration as economic data is showing signs of recovery,commodities are showing signs of rally and expectations of incremental monetary easing from theRBI are beginning to unwind. However, system liquidity remains surplus and bank deposits continueto grow thereby providing resistance to bond yields from rising sharply.

Given the above factors, we believe that the market would continue to provide tactical opportunitiesalthough the fundamental bias should be for lower duration. Also, any mitigation of bond supplypressure or a new downturn in the ongoing economic recovery may provide space for opportunisticlonger duration plays. On the other hand, if the recovery cycle continues uninterrupted and commodityprices remain firm, central banks may start to worry about withdrawing the current monetary stimulusby sometime early 2010; with consequent impact on bond markets.

2. BRIEF BACKGROUND OF SPONSORS, BOARD OF TRUSTEES AND ASSETMANAGEMENT COMPANY

a) Sponsor

HSBC Mutual Fund is sponsored by HSBC Securities and Capital Markets (India) Private Limited (HSCI).The Sponsor is the Settler of the Mutual Fund Trust. The Sponsor has entrusted a sum of Rs. 1,00,000(Rupees One Lakh only) to the Trustee as the initial contribution towards the corpus of the MutualFund.

HSCI is a member of the HSBC Group, one of the largest banking and financial services organisations,in the world. Headquartered in London, HSBC operates through long-established businesses in fiveregions: Europe, Asia-Pacific, Middle East, America and Africa. Through its global network of 10,000offices in 86 countries and territories, HSBC provides a comprehensive range of financial services topersonal, commercial, corporate, institutional investment and private banking clients.

HSCI offers integrated investment banking services, securities and corporate finance & advisory. HSCIis a member of The Bombay Stock Exchange Limited and National Stock Exchange (capital and derivativemarket segments) and is also a category I merchant banker and underwriter registered with Securitiesand Exchange Board of India.

HSCI holds 100% of the paid-up equity share capital of the AMC.

Trustees' ReportFor the year ended March 31, 2009 (Contd...)

6

b) HSBC Mutual Fund

HSBC Mutual Fund ("the Mutual Fund" or "the Fund") has been constituted as a Trust in accordancewith the provisions of the Indian Trusts Act, 1882 (2 of 1882) vide a Trust Deed dated February 7,2002 with HSBC Securities and Capital Markets (India) Private Limited, as the Sponsor and the Boardof Individual Trustees. The Trustee has entered into an Investment Management Agreement datedFebruary 7, 2002 with HSBC Asset Management (India) Private Limited (the AMC) to function as theInvestment Manager for all the Schemes of the Fund. The Fund was registered with SEBI videregistration number MF/046/02/5 dated May 27, 2002.

The Trust has been formed for the purpose of pooling of capital from the public for collectiveinvestment in securities / any other property for the purpose of providing facilities for participationby persons as beneficiaries in such properties / investments and in the profits / income arising therefrom.

c) Board of Trustees (the Trustees)

The Board of Trustees are the exclusive owner of the Trust Fund and holds the same in trust for thebenefit of the unitholders. The Trustees have been discharging their duties and carrying out theirresponsibilities as provided in the SEBI (Mutual Funds) Regulations, 1996 and the Trust Deed. TheTrustees seeks to ensure that the Fund and the Schemes floated thereunder are managed by theAMC in accordance with the Trust Deed, the said Regulations, directions and guidelines issued bySEBI, the Stock Exchanges, the Association of Mutual Funds of India and other regulatory agencies.

d) Asset Management Company (the AMC)

HSBC Asset Management (India) Private Limited (the Investment Manager or the AMC) is a privatelimited company incorporated under the Companies Act, 1956 on December 12, 2001 having itsRegistered Office at 314, D. N. Road, Fort, Mumbai 400 001. HSBC Asset Management (India) PrivateLimited has been appointed as the Asset Management Company of the HSBC Mutual Fund by theTrustee vide Investment Management Agreement (IMA) dated February 7, 2002 and executed betweenthe Trustees and the AMC. SEBI approved the AMC to act as the Investment Manager of the Fundvide. its letter No. MFD/BC/163/2002 dated May 27, 2002.

The paid-up equity share capital of the AMC is Rs. 9 crores. HSBC Securities and Capital Markets(India) Private Limited holds 100% of the paid-up equity share capital of the AMC.

3. INVESTMENT OBJECTIVE OF THE SCHEMEThe investment objective of the Scheme has been provided above under the heading "SchemePerformance, Future Outlook and Operation of the Scheme" (refer Section 1).

4. SIGNIFICANT ACCOUNTING POLICIESThe accounting policies are in accordance with Securities and Exchange Board of India (Mutual Funds)Regulations, 1996.

5. UNCLAIMED DIVIDENDS & REDEMPTIONSSummary of number of Investors & corresponding amount

Unclaimed Dividends Unclaimed Redemptions

Scheme Amount No. of Amount No. of(Rs.) Investors (Rs.) Investors

HSBC India Opportunities Fund 873,838.13 217 301,902.87 9

6. INVESTOR SERVICESDuring the year, the number of official points of acceptance of transactions increased significantly toabout 182 locations. In addition to the offices of the transfer agency, the company has InvestorService Centres in 14 locations at its own offices - namely Mumbai, New Delhi, Kolkata, Chennai,

Trustees' ReportFor the year ended March 31, 2009 (Contd...)

7

Bangalore, Hyderabad, Pune, Ahmedabad, Indore, Chandigarh, Kochi, Coimbatore, Lucknow andVadodara. With a view to enhancing customer convenience, the Asset Management Company hasextended the facility of crediting investor bank accounts directly by way of NEFT / RTGS (for credit ofredemption and dividend proceeds). The AMC endeavours to despatch dividend proceeds within 5working days from the Record Date in all Schemes. The internal standards on redemption payoutshave been consistently met, with very few exceptions. The number of locations for the ECS AutoDebit facility for investments through Systematic Investment Plan also increased to about 74 byMarch 2009.

On the distribution front, the number of empanelled distributors increased from 7859 as on 31March, 2008 to 8632 as on 31 March, 2009. During the year, the Asset Management Companyinitiated tie-ups for online distribution of the Mutual Fund's schemes with several channel partnerstaking the total number of such tie-ups to 24 (Angel Capital & Department Market Ltd., Bajaj CapitalLimited, Bonanza Portfolio Limited, Citibank N.A., Citigroup Wealth Advisors India Private Limited,HDFC Bank Limited, Hongkong & Shanghai Banking Corporation Limited, HSBC Corporate InvestmentSolution Services, ICICI Securities Limited, India Infoline Limited, Karvy Stock Broking Limited, KotakMahindra Bank Limited, Kotak Securities Limited, Motilal Oswal Securities Limited, NJ India InvestPrivate Limited, Reliance Securities Limited, RR Investors Capital Services Private Limited, SBICAPSecurities Limited, Sharekhan Limited, SMC Global Securities Limited, Standard Chartered - STCICapital Markets Ltd., Tom Distribution Services Limited, Yes Bank Limited).

Call centre operations have been extended to cover the entire country. The Asset ManagementCompany has outsourced certain back office services including call centre services to HSBC Operationsand Processing Enterprise (India) Private Limited (HOPE).

7. STATUTORY DETAILSa) The Sponsors are not responsible or liable for any loss resulting from the operation of the Schemes

of the Fund beyond initial contribution of Rs. 1 lakh for setting up the Fund.

b) The price and redemption value of the units, and income from them, can go up as well as downwith fluctuations in the market value of its underlying investments.

c) Full / Abridged Annual Report shall be disclosed on the website at www.assetmanagement.hsbc.com/inand shall be available for inspection at the Head Office of the mutual fund. Present and prospectiveunit holder can obtain copy of the trust deed, the Full / Abridged Annual Report of the Scheme(s),the Annual Report of HSBC Asset Management (India) Private Limited and the text of the relevantScheme(s) at a price.

8. ACKNOWLEDGEMENTSThe Trustees wish to thank the Unitholders of the Schemes for their support throughout the year andalso thank the Government of India, the Securities and Exchange Board of India (SEBI), the ReserveBank of India (RBI) and the Association of Mutual Funds in India (AMFI) for the guidance provided bythem. The Trustees also appreciate the service provided by the Registrar and Transfer Agent, FundAccountant, Custodian, Bankers, Distributors and Brokers. The guidance and services provided bythe Auditors and advocates and the ebullience, sincerity and dedication of the employees of HSBCAsset Management (India) Private Limited is also appreciated.

The Trustees look forward to the continued support of everyone.

For and on behalf of the Board of Trustees of HSBC Mutual Fund

Dilip J. Thakkar

Trustee

MUMBAIJuly 6, 2009

Trustees' ReportFor the year ended March 31, 2009 (Contd...)

8

To the Board of Trustees of

HSBC MUTUAL FUND

1. We have audited the Balance Sheet of HSBC Mutual Fund - HSBC India Opportunities Fund ("TheScheme") as at March 31, 2009, the related Revenue Account for the year ended on that dateannexed thereto, and the Cash Flow Statement for the year ended on that date which we havesigned under reference to this report. These financial statements are the responsibility of theBoard of Trustees of HSBC Mutual Fund and the Management of HSBC Asset Management (India)Private Limited (the "Management"). Our responsibility is to express an opinion on these financialstatements based on our audit.

2. We have conducted our audit in accordance with auditing standards generally accepted in India.Those standards require that we plan and perform the audit to obtain reasonable assuranceabout whether the financial statements are free of material misstatement. An audit includesexamining, on a test basis, evidence supporting the amounts and disclosures in the financialstatements. Our procedures included confirmation of securities owned and unit capital balancesas at March 31, 2009 by correspondence with the custodian/others and registrar and transferagents respectively. An audit also includes assessing the accounting principles used and significantestimates made by the Management as well as evaluating the overall financial statementpresentation. We believe that our audit provides a reasonable basis for our opinion.

3. We have obtained all the information and explanations which to the best of our knowledge andbelief were necessary for the purpose of our audit. The Balance Sheet, the Revenue Account andthe Cash Flow Statement referred to above are in agreement with the books of account of theScheme.

4. In our opinion and to the best of our information and according to the explanations given to us,

(i) The Balance Sheet, the Revenue Account and the Cash Flow Statement together with thenotes thereon give the information required by the Securities and Exchange Board of India(Mutual Funds) Regulations, 1996 and amendments thereto, as applicable, and also giverespectively, a true and fair view of the state of affairs of HSBC Mutual Fund - HSBC IndiaOpportunities Fund as at March 31, 2009, its net deficit and its cash flows for the year endedon that date.

(ii) The Balance Sheet as at March 31, 2009 and the Revenue Account for the year ended on thatdate, together with the notes thereon have been prepared in all material respects in accordancewith the accounting policies and standards specified in the Ninth Schedule of the Securitiesand Exchange Board of India (Mutual Funds) Regulations, 1996 and amendments thereto asapplicable.

Partha GhoshPartnerMembership No. F / 55913

For and on behalf ofPRICE WATERHOUSEChartered Accountants

Place : MumbaiDate : July 6, 2009

Auditors' Report

9

Rs. in Lakhs

HSBC INDIA OPPORTUNITIES FUND

As at As atMarch 31, 2009 March 31, 2008

LIABILITIES1 Unit Capital 22,075.58 26,248.742 Reserves & Surplus2.1 Unit Premium Reserves (4,967.16) (4,402.00)2.2 Unrealised Appreciation Reserve 12.12 4,824.752.3 Other Reserves 10,872.37 25,566.11

3 Loans & Borrowings – –

4 Current Liabilities & Provisions4.1 Provision for doubtful Income / Deposits – –4.2 Other Current Liabilities & Provisions 500.22 773.45

TOTAL 28,493.13 53,011.05

ASSETS1 Investments1.1. Listed Securities:1.1.1 Equity Shares 23,373.85 46,770.621.1.2 Preference Shares – –1.1.3 Equity Linked Debentures – –1.1.4 Other Debentures & Bonds – –1.1.5 Securitised Debt securities – –1.2 Securities Awaited Listing:1.2.1 Equity Shares – –1.2.2 Preference Shares – –1.2.3 Equity Linked Debentures – –1.2.4 Other Debentures & Bonds – –1.2.5 Securitised Debt securities – –1.3 Unlisted Securities:1.3.1 Equity Shares – –1.3.2 Preference Shares – –1.3.3 Equity Linked Debentures – –1.3.4 Other Debentures & Bonds – –1.3.5 Securitised Debt securities – –1.4 Government Securities – –1.5 Treasury Bills – –1.6 Commercial Paper – –1.7 Certificate of Deposits – –1.8 Bill Rediscounting – –1.9 Units of Domestic Mutual Fund – –1.10 Foreign Securities – –

Total Investments 23,373.85 46,770.62

2 Deposits 2,661.52 1,461.52

3 Other Current Assets3.1 Cash & Bank Balance 8.76 51.573.2 CBLO / Reverse Repo Lending 1,023.25 3,303.593.3 Others 1,425.75 1,423.74

4 Deferred Revenue Expenditure – –(to the extent not written off)

TOTAL 28,493.13 53,011.05

Notes to Accounts - Annexure I

Abridged Balance Sheet as at March 31, 2009

10

Rs. in Lakhs

HSBC INDIA OPPORTUNITIES FUND

Current PreviousYear ended Year ended

March 31, 2009 March 31, 2008

1 INCOME1.1 Dividend 320.06 270.561.2 Interest 367.98 299.911.3 Realised Gain / (Loss) on Foreign Exchange Transactions – –1.4 Realised Gains / (Losses) on Interscheme sale

of investments – –1.5 Realised Gains / (Losses) on External sale /

redemption of investments (11,630.40) 17,909.831.6 Realised Gains / (Losses) on Derivative Transactions 1,184.49 59.291.7 Other Income – –

(A) (9,757.87) 18,539.59

2 EXPENSES2.1 Management fees 407.54 713.212.2 Service tax on Management fees ** – –2.3 Transfer agents fees and expenses 76.41 113.372.4 Custodian fees 24.90 37.442.5 Trusteeship fees 0.16 0.362.6 Commission to Agents * – –2.7 Marketing & Distribution expenses 277.19 460.742.8 Audit fees 5.00 6.502.9 Other operating expenses 86.25 168.00

(B) 877.45 1,499.62

3 NET REALISED GAINS / (LOSSES)FOR THE YEAR / PERIOD (A -B = C) (10,635.32) 17,039.97

4 Change in Unrealised Depreciationin value of investments (D) 1,967.69 –

5 NET GAINS / (LOSSES) FOR THEYEAR / PERIOD [E = (C-D)] (12,603.01) 17,039.97

6 Change in unrealised appreciationin the value of investments (F) (4,812.63) (4,409.29)

7 NET SURPLUS / (DEFICIT) FORTHE YEAR / PERIOD (E + F = G) (17,415.64) 12,630.68

7.1 Add: Balance transfer from Unrealised Appreciation Reserve 4,812.63 4,409.297.2 Less: Balance transfer to Unrealised Appreciation Reserve – –7.3 Add / (Less): Equalisation (2,090.75) (5,422.07)7.4 Transfer from Reserve Fund – 1,252.057.5 Transfer from Unit Premium Reserve – –

8 TOTAL (14,693.76) 12,869.95

9 Dividend Appropriation9.1 Income Distributed during the year / period (0.02) 5,324.389.2 Tax on income distributed during the year / period – –

10 Retained Surplus / (Deficit) carried forwardto Balance Sheet (14,693.74) 7,545.57

Notes to Accounts - Annexure I

* Commission to Agents is included in Marketing & Distribution Expenses.** Service Tax on Management Fees is included in Other Operating Expenses.

Abridged Revenue Account For the year endedMarch 31, 2009

11

HSBC INDIA OPPORTUNITIES FUND

Current PreviousYear ended Year ended

March 31, 2009 March 31, 2008

1. NAV per unit (Rs.):

Open

Regular Growth Option 31.0700 26.7422

Regular Dividend Option 16.4584 16.2416

High

Regular Growth Option 34.4126 46.2473

Regular Dividend Option 18.2294 26.0871

Low

Regular Growth Option 17.4783 25.7935

Regular Dividend Option 9.2599 15.4065

End

Regular Growth Option 19.6995 31.0700

Regular Dividend Option 10.4365 16.4584

2. Closing Assets Under Management (Rs. in Lakhs)

End 27,993 52,238

Average (AAuM)1 38,254 68,891

3. Gross income as % of AAuM2 -25.51% 26.91%

4. Expense Ratio:

a. Total Expense as % of AAuM (planwise)

Regular Growth Option 2.29% 2.18%

Regular Dividend Option 2.29% 2.18%

b. Management Fee as % of AAuM (planwise)

Regular Growth Option 1.07% 1.04%

Regular Dividend Option 1.07% 1.04%

5. Net Income as a percentage of AAuM3 -27.80% 24.73%

6. Portfolio turnover ratio4 1.15 1.82

7. Total Dividend per unit distributed duringthe year / period (planwise)

Retail

Dividend – 2.5000

Corporate

Dividend – 2.5000

Key Statistics for the year ended March 31, 2009

12

8. Returns:

a. Last One Year

Scheme

Regular Growth Option (36.5964) 16.0872

Regular Dividend Option (36.5886) 16.0744

Benchmark

BSE 500 (42.7700) 24.2540

b. Since Inception

Scheme

Regular Growth Option 14.2144 31.8388

Regular Dividend Option 14.2237 31.8482

Benchmark

BSE 500 9.1500 27.7560

1 AAuM = Average daily net assets

2 Gross income = amount against (A) in the Revenue Account i.e. Income.

3 Net income = amount against (C) in the Revenue Account i.e. NET REALISED GAINS / (LOSSES)FOR THE YEAR / PERIOD

4 Portfolio Turnover = Lower of sales or purchase divided by the Average AuM for the year / period.

Key Statistics for the year ended March 31, 2009 (Contd...)

HSBC INDIA OPPORTUNITIES FUND

Current PreviousYear ended Year ended

March 31, 2009 March 31, 2008

13

HSBC INDIA OPPORTUNITIES FUND

1 Investments:

1.1 It is confirmed that investments of the schemes are registered in the name of the Trustees forthe benefit of the scheme’s unitholders.

1.2 Open Positions of derivatives as of March 31, 2009 is Rs. 61,203,450 and is 2.19% to thenet assets. Open Positions of derivatives as of March 31, 2008 is Rs. 124,123,705 and is2.38% to the net assets.

1.3 Investments in Associates and Group Companies(Rupees)