Embed Size (px)

Citation preview

UBS Best of Germany

One-on-One Conference New York, 17 & 18 September 2015

METRO GROUP, Investor Relations

17 & 18 September 2015 | © METRO AG 2015 1

DISCLAIMER AND NOTES To the extent that statements in this presentation do not relate to historical or current facts, they constitute forward-looking statements. All forward-looking statements

herein are based on certain expectations and assumptions at the time of publication of this presentation and are subject to risks and uncertainties that could cause actual

results, performance or financial position to differ materially from any future results, performance or financial position expressed or implied in this presentation. Many of

these risks and uncertainties relate to factors that are beyond METRO GROUP’s ability to control or estimate precisely. The risks and uncertainties to which these forward-

looking statements may be subject include (without limitation) future market and economic conditions, the behaviour of other market participants, investments in innovative

sales formats, expansion in online and multichannel sales activities, integration of acquired businesses and achievement of anticipated cost savings and productivity gains,

and the actions of government regulators. Readers are cautioned not to place too much reliance on these forward-looking statements. See also “Risk and Opportunity

Report” on pages 145 - 167 of the METRO GROUP Annual Report 2013/14 for risks as of the date of such Annual Report. METRO GROUP does not undertake any

obligation to publicly update any forward-looking statements or to conform them to events or circumstances after the date of this presentation.

This presentation is intended for information only. It is not intended as an offer for sale, or as a solicitation of an offer to purchase, any securities in any jurisdiction.

This presentation may not be reproduced, distributed or published without prior written consent of METRO AG.

All numbers are before special items, unless otherwise stated.

The consolidated financial statements have been prepared in euros. All amounts are stated in million euros (€ million) unless otherwise indicated. Amounts below €0.5

million are rounded and reported as 0. Since 2012, only the amounts in the income statement, the reconciliation from profit or loss for the period to total comprehensive

income, the balance sheet, the statement of changes in equity and the cash flow statement were rounded to produce the respective totals. In all other tables, the individual

amounts and the totals were rounded separately. This may entail rounding differences.

Due to the sale to Hudson’s Bay Company, Galeria Kaufhof will no longer be shown as a separate segment, but as a discontinued operations. Accordingly,

METRO GROUP's financials have been recalculated to account for the disposal of Galeria Kaufhof and the previous year's figures have been adjusted. The sale is

scheduled to close in September 2015.

METRO GROUP, Investor Relations

17 & 18 September 2015 | © METRO AG 2015 2

AGENDA

01 Active Portfolio Management@ METRO GROUP 3

02 METRO GROUP @ a Glance 11

03 Three Market Leading Sales Lines 16

04 Performance in Q3 2014/15 & Outlook FY 2014/15 26

05 Key takeaways 32

METRO GROUP, Investor Relations

17 & 18 September 2015 | © METRO AG 2015 3

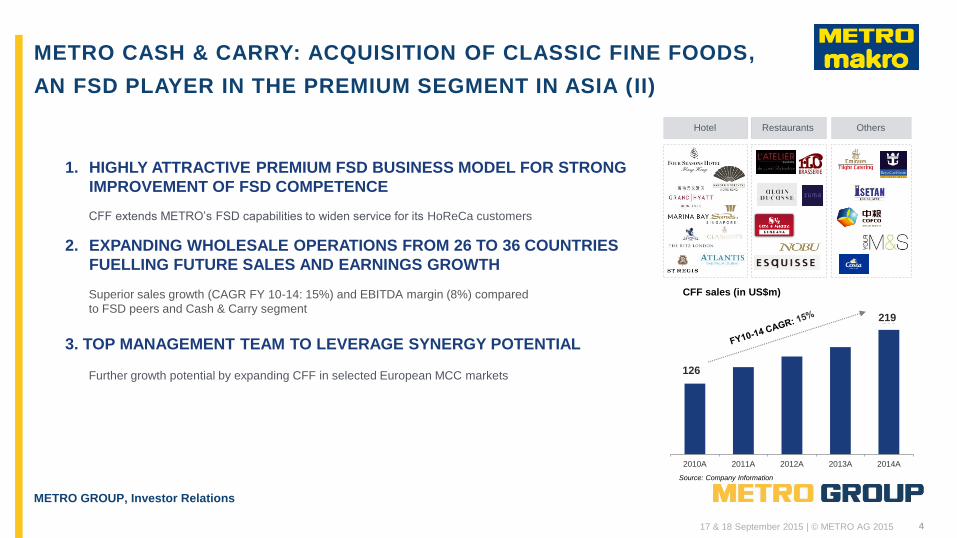

METRO CASH & CARRY: ACQUISITION OF CLASSIC FINE FOODS,

AN FSD PLAYER IN THE PREMIUM SEGMENT IN ASIA (I)

UK

France

UAE

China KoreaJapan

Hong Kong

Vietnam

Thailand Philippines

MalaysiaSingaporeIndonesia

Leading FSD player in the high-margin premium segment:

Access to high growth markets

Unique service offering

Highly niche premium product portfolio

Presence in 25 mainly Asian cities across 14 countries

~6,000 active customers with focus on HoReCa customer

group

c. 800 full-time employees

Financials 2014: sales US$219m

EBITDA US$18m (margin 8%)

METRO GROUP, Investor Relations

17 & 18 September 2015 | © METRO AG 2015 4

2. EXPANDING WHOLESALE OPERATIONS FROM 26 TO 36 COUNTRIES

FUELLING FUTURE SALES AND EARNINGS GROWTH

METRO CASH & CARRY: ACQUISITION OF CLASSIC FINE FOODS,

AN FSD PLAYER IN THE PREMIUM SEGMENT IN ASIA (II)

Superior sales growth (CAGR FY 10-14: 15%) and EBITDA margin (8%) compared

to FSD peers and Cash & Carry segment

1. HIGHLY ATTRACTIVE PREMIUM FSD BUSINESS MODEL FOR STRONG

IMPROVEMENT OF FSD COMPETENCE

CFF sales (in US$m)

118

208

0k

0k

0k

0k

0k

0k

2010A 2011A 2012A 2013A 2014A

Source: Company Information

Hotel Restaurants Others

CFF extends METRO’s FSD capabilities to widen service for its HoReCa customers

3. TOP MANAGEMENT TEAM TO LEVERAGE SYNERGY POTENTIAL

Further growth potential by expanding CFF in selected European MCC markets

219

126

METRO GROUP, Investor Relations

17 & 18 September 2015 | © METRO AG 2015 5

MEDIA-SATURN: ACQUISITION OF RTS GROUP, A FULL-SERVICE &

REPAIRS PROVIDER FOR ELECTRONIC PRODUCTS (I)

Full-service and repairs provider

for electronic products

Founded in 1989 by Josef Raith

Headquartered in Wolnzach,

Bavaria

Further locations in Germany:

Augsburg, Nürnberg, Regensburg,

Sömmerda, Straubing

Cooperation with > 50 service

partners across Europe

Around 1,200 employees

Financials 2014: Sales ~€136m;

EBITDA ~€8 m.

CE service & repairs

• Multiple device repairs and

customer service solutions

Technical after-sales

service (Profectis)

• Only on-site (home) service

provider for white goods

covering the whole of Germany

• Warranty-buy-out

Smart home installations

• Smart home installations and

support in-store and on-site

(home/B2B)

Spare parts

• Spare parts logistics &

management

• Online spare parts sales

B2B/B2C

METRO GROUP, Investor Relations

17 & 18 September 2015 | © METRO AG 2015 6

Valuation and deal structure

Sellers: Josef Raith (Founder) & Capiton AG

Share deal

In a first step, acquisition of 90% of the shares

Full exit of Capiton AG

Founder Raith to keep 10% of the shares

Transaction subject to approval by the cartel offices

MEDIA-SATURN: ACQUISITION OF RTS GROUP, A FULL-SERVICE &

REPAIRS PROVIDER FOR ELECTRONIC PRODUCTS (II)

Deal rationale for MSH

Acquisition enables MSH to transform from a

transaction-/product-driven CE retailer to a

customer-solution-focused CE retailer

Added value service throughout the entire

customer journey (beyond the buying process)

Dedicated service offering as a new product

Consistent quality standards

From a single source

Unique opportunity to work with suppliers on back-

end process optimization, service and repairs

METRO GROUP, Investor Relations

17 & 18 September 2015 | © METRO AG 2015 7

GALERIA KAUFHOF: KEY TRANSACTION FACTS

Disposal of department store operations in Germany

and Belgium together with the related real estate

portfolio to Hudson’s Bay Company

Enterprise value of €2.825bn

Substantial assurances for around 21,500 employees,

HQ and stores

Significant reduction in rating-relevant1 net debt by

c.€2.7bn, including cash inflow of c. €1.6bn

Net book gain on sale of c. €0.7bn

Closing expected by end of FY 2014/15

Germany

Belgium

Total € million

FY Sales 2013/14 2,920 178 3,099

FY EBIT 2013/142 193

Stores per 31/3/2015 119 16 135 1Standard & Poor‘s methodology

2 before special items

METRO GROUP, Investor Relations

17 & 18 September 2015 | © METRO AG 2015 8

Increase overall capex budget to ca. €2bn over the

next few years

Intensify investment activity

▪ Growth countries (METRO Cash & Carry and Media-

Saturn)

▪ Store remodellings and new store formats in inner

city locations (METRO Cash & Carry and Media-

Saturn)

▪ Complementary assets to accelerate growth in Cash

& Carry (FSD) and Media-Saturn (multi-channel)

Digital penetration of the HoReCa sector

(METRO Cash & Carry)

Strengthen financial profile

GALERIA KAUFHOF: USE OF PROCEEDS FROM SALE

RoCE* 2013/14 vs. Cost of Capital

* lease-adjusted

METRO GROUP, Investor Relations

17 & 18 September 2015 | © METRO AG 2015 9

SUCCESSFUL PORTFOLIO STREAMLINING AND FOCUS ON CORE OPERATIONS

Freeing up capital to focus on and grow the core business and strengthen the balance sheet

Disposals

METRO Cash &

Carry Morocco

Saturn France

Media-Markt China

Real Eastern Europe

MAKRO Cash &

Carry UK

&

Booker stake

&

METRO Cash & Carry

Denmark & Vietnam *)

MAKRO Cash & Carry

Egypt & Greece

Real Turkey

GALERIA Kaufhof

2010 - 2011 2012 - 2013 2014 2015

*) Vietnam pending

METRO GROUP, Investor Relations

17 & 18 September 2015 | © METRO AG 2015 10

AGENDA

01 Active Portfolio Management@ METRO GROUP 3

02 METRO GROUP @ a Glance 11

03 Three Market Leading Sales Lines 16

04 Performance in Q3 2014/15 & Outlook FY 2014/15 26

05 Key takeaways 32

METRO GROUP, Investor Relations

17 & 18 September 2015 | © METRO AG 2015 11

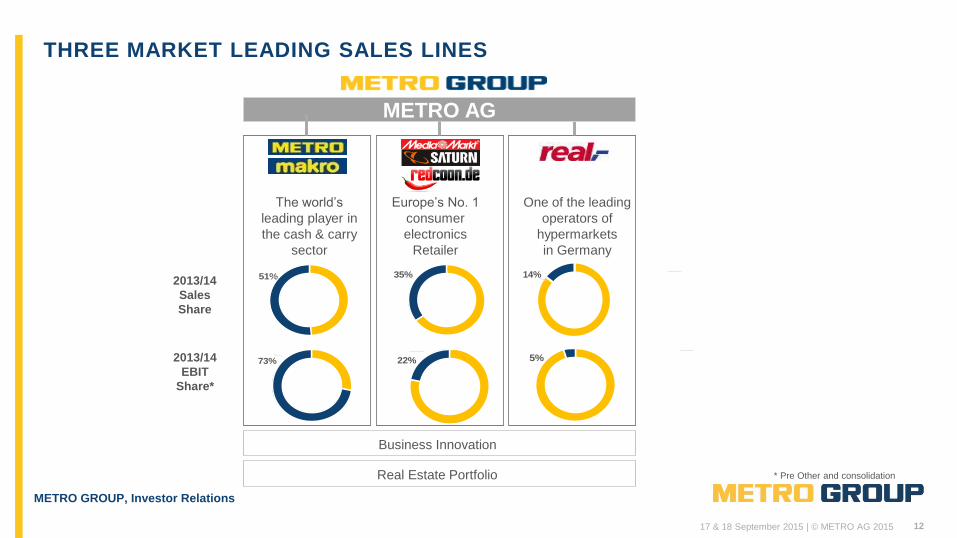

ONE OF THE LARGEST RETAILERS IN THE WORLD

Sales: €60 billion

EBIT: €1.5 billion

Stores: 2,063

Countries: 31

Employees: 230,000

DATA BASE: FY 2013/14 ADJUSTED FOR GALERIA KAUFHOF

METRO GROUP, Investor Relations

17 & 18 September 2015 | © METRO AG 2015 12

5%

73%

51%

METRO AG

2013/14

Sales

Share

2013/14

EBIT

Share*

* Pre Other and consolidation

22%

14% 35%

Europe’s No. 1

consumer

electronics

Retailer

One of the leading

operators of

hypermarkets

in Germany

The world’s

leading player in

the cash & carry

sector

THREE MARKET LEADING SALES LINES

Business Innovation

Real Estate Portfolio

METRO GROUP, Investor Relations

17 & 18 September 2015 | © METRO AG 2015 13

Germany

Western

Europe

Eastern

Europe Asia/Africa

METRO

GROUP

1 11 14 5 31 2013/14

Countries

2013/14

Sales

Share

We generate approximately 30% of Group sales in emerging markets

37% 32% 25%

STRONG INTERNATIONAL PRESENCE

6% 100%

METRO GROUP, Investor Relations

17 & 18 September 2015 | © METRO AG 2015 14

FY 2013/14* – ALL TARGETS ACHIEVED

Better sales, higher earnings, stronger balance sheet

LFL Sales

Dividend

EPS

Net Debt

Major challenges

Sluggish economic environment

Geopolitical crisis

Weak emerging market currencies

Major achievements

Consequent focus on our customers in terms of

Assortment

Services

Solution Competences

Improved company culture

Active portfolio management

+0.1%

€0.90 per

ordinary

share

+25%

to €1.84

-€0.7bn

to €4.7bn

* Includes Galeria Kaufhof

METRO GROUP, Investor Relations

17 & 18 September 2015 | © METRO AG 2015 15

AGENDA

01 Active Portfolio Management@ METRO GROUP 3

02 METRO GROUP @ a Glance 11

03 Three Market Leading Sales Lines 16

04 Performance in Q3 2014/15 & Outlook FY 2014/15 26

05 Key takeaways 32

METRO GROUP, Investor Relations

17 & 18 September 2015 | © METRO AG 2015 16

THE WORLD‘S LEADING PLAYER IN THE CASH & CARRY SECTOR

Focused on B2B self-service wholesaling to

3 customer groups: HoReCa, Trader and SCO

High performance internationally replicable concept

International share of sales of 84%

766 stores in 28 countries

Profitable Growth Drivers:

▪ Outstanding freshness & quality in food

▪ Dedicated sales force

▪ Innovative store concepts

▪ Delivery

▪ Own brands

▪ Expansion Focus on Russia, China, India and Turkey

€ million FY 2012/13 FY 2013/14

Sales 31,165 30,513

RoCE 15.7% 13.3%

EBIT 1,379 1,125

EBIT Margin 4.4% 3.7%

METRO GROUP, Investor Relations

17 & 18 September 2015 | © METRO AG 2015 17

STRATEGIC AMBITIONS

Being the “Champion for Independent Business”

Strong differentiation through exceptional food competence

Development and roll-out of innovative wholesale concepts

Ongoing cost structure review

Overall Ambition:

Market Leadership in well defined sectors through unique product ranges and strong focus on B2B

solutions that make our customers more competitive

METRO GROUP, Investor Relations

17 & 18 September 2015 | © METRO AG 2015 18

MCC’S NEW OPERATING MODEL FOSTERS ENTREPRENEURSHIP

Our new approach includes:

Countries are fully empowered for value creation

Certain functions are shared based on common needs

Utilization of best practices and expertise will be increased

Commercial Intelligence is close to operations

The center takes an active ownership approach

▪ through Operating Partners

▪ with much higher proximity to the business and

▪ much more intensive interactions

Effectiveness and intensity of leadership grow

METRO GROUP, Investor Relations

17 & 18 September 2015 | © METRO AG 2015 19

MAJOR CHANGES EXPECTED

From past … … to new operating model

Standard approach across all countries Significant localization based on country

situation

Multi project management across

all countries

Dedicated focus on locally selected

CTGs and selected key initiatives

Heavy expansion across many countries Focused expansion in selected countries

“Most international” country portfolio Optimized portfolio to create value

Classic planning and budgeting process Value Creation plan as the central

steering component

METRO GROUP, Investor Relations

17 & 18 September 2015 | © METRO AG 2015 20

ESSENCE OF OUR NEW OPERATING MODEL

Our Aspiration: Increase effectiveness & proximity

METRO GROUP, Investor Relations

17 & 18 September 2015 | © METRO AG 2015 21

EUROPE’S NO. 1 IN CONSUMER ELECTRONICS RETAILING

Pan-European market leader with 986 stores in 15 countries

and online presence

Large-scale, full assortment store base with entrepreneurial

store managers

Very competitive EDLP pricing strategy

Innovative merchandising and marketing concepts

Profitable Growth Drivers:

Business model transformation

Multi-channel sales activities in 14 countries

Online sales

Own brands

€ million FY 2012/13 FY 2013/14

Sales 21,053 20,981

RoCE 15.5% 14.9%

EBIT 299 335

EBIT Margin 1.4% 1.6%

METRO GROUP, Investor Relations

17 & 18 September 2015 | © METRO AG 2015 22

STRATEGIC AMBITIONS

Continue transformation to seamless multichannel approach

Enhance position as “partner of choice” for suppliers

Further improving cost position: Target cost ratio of 19%

Overall Ambition:

Media Markt and Saturn:

Europe’s leading seamless shopping experience in consumer electronics

Redcoon:

Europe’s leading online pure player with a big product range and the lowest prices

METRO GROUP, Investor Relations

17 & 18 September 2015 | © METRO AG 2015 23

LEADING OPERATOR OF HYPERMARKETS IN GERMANY

Following the divestment of activities in Eastern Europe and

Turkey focus is on Germany with 307 stores

Food accounts for approx. 75% of sales

Comprehensive product range of 80,000 different articles

Member of Germany’s leading loyalty card programme

PAYBACK

Profitable Growth Drivers:

▪ Store remodellings

▪ Own brands

▪ Entrepreneurial store management

▪ Multichannel activities: Webshop www.real-onlineshop.de

with more than 20,000 products

€ million FY 2012/13 FY 2013/14

Sales 10,366 8,432

RoCE 5.8% 4.1%

EBIT 145 81

EBIT Margin 1.4% 1.0%

METRO GROUP, Investor Relations

17 & 18 September 2015 | © METRO AG 2015 24

STRATEGIC AMBITIONS

Capturing market share by offering best customer propositions

Extending own brand offering and multichannel activities

Continuing remodeling program

Strict cost control

Overall Ambition:

Unique choice and quality in food retail complemented by a compelling non-food range.

Well-adjusted to serve our key customer groups. Enhanced through multichannel.

METRO GROUP, Investor Relations

17 & 18 September 2015 | © METRO AG 2015 25

AGENDA

01 Active Portfolio Management@ METRO GROUP 3

02 METRO GROUP at a Glance 11

03 Three Market Leading Sales Lines 16

04 Performance in Q3 2014/15 & Outlook FY 2014/15 26

05 Key takeaways 32

METRO GROUP, Investor Relations

17 & 18 September 2015 | © METRO AG 2015 26

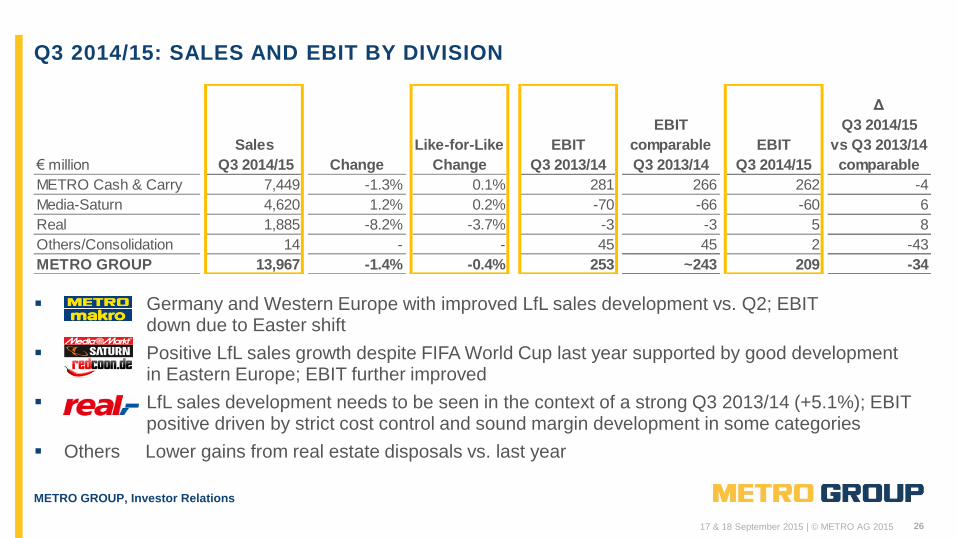

Q3 2014/15: SALES AND EBIT BY DIVISION

Germany and Western Europe with improved LfL sales development vs. Q2; EBIT down due to Easter shift

Positive LfL sales growth despite FIFA World Cup last year supported by good development in Eastern Europe; EBIT further improved

LfL sales development needs to be seen in the context of a strong Q3 2013/14 (+5.1%); EBIT positive driven by strict cost control and sound margin development in some categories

Others Lower gains from real estate disposals vs. last year

€ million

METRO Cash & Carry 7,449 -1.3% 0.1% 281 266 262 -4

Media-Saturn 4,620 1.2% 0.2% -70 -66 -60 6

Real 1,885 -8.2% -3.7% -3 -3 5 8

Others/Consolidation 14 - - 45 45 2 -43

METRO GROUP 13,967 -1.4% -0.4% 253 ~243 209 -34

Δ

Q3 2014/15

vs Q3 2013/14

comparable

Sales

Q3 2014/15 Change

Like-for-Like

Change

EBIT

Q3 2013/14

EBIT

comparable

Q3 2013/14

EBIT

Q3 2014/15

METRO GROUP, Investor Relations

17 & 18 September 2015 | © METRO AG 2015 27

Q3/9M 2014/15 INCOME STATEMENT (EBIT TO EPS)

Ongoing improvement of net financial result driven by lower net debt and interest level

The high tax rate in Q3 results from our integral approach thus the adjustments for the

9M period affect Q3

Tax rate for continuing operations of 56.6% in 9M 2014/15 (9M 2013/14: 56.8%) in line

with expectations

€ million

Q3 2013/14

Q3 2014/15

9M 2013/14

9M 2014/15

EBIT 253 209 1,127 1,076

Net financial result -102 -94 -376 -269

EBT 151 115 751 807

Income Taxes -73 -113 -426 -456

Profit or loss for the period from continuing operations 78 2 325 351

Profit or loss for the period from disconinued operations 17 5 181 94

Profit or loss for the period 95 7 506 445

EPS in € from continuing operations 0.27 0.05 0.84 0.94

EPS in € 0.32 0.07 1.39 1.23

METRO GROUP, Investor Relations

17 & 18 September 2015 | © METRO AG 2015 28

APPRECIATION OF EBIT 9M 2014/15

487

872

590

255

1,127

Special Items 9M 2013/14

(Reported)

Negative

FX Impact

~-100

9M 2013/14

(Before

Special Items)

9M 2014/15

(Before

Special Items)

~301)

9M 2014/15

(Reported)

Special Items 9M 2013/14

(Comparable

Before

Special Items)

~601)

in € million +49

1) Real Estate Gains from Divestments

~1,027 1,076

METRO GROUP, Investor Relations

17 & 18 September 2015 | © METRO AG 2015 29

9M 2014/15: OTHER KEY FINANCIALS

Net debt further reduced by around €0.4bn to €5.1bn due to portfolio optimization and real estate

divestments

Net working capital and cash flow from operating activities impacted by FX and negative NWC

development at Media-Saturn, cash flow additionally impacted by higher tax cash out

Capex of €656m mainly invested in modernisation, expansion and remodellings

€ million

9M 2014/15 Change

Net debt (as at 30/06) 5,795 5,530 5,130 -400

Net working capital (as at 30/06) -1,776 -1,982 -1,700 282

Change in net working capital

(cash flow impact)-456 -403 -682 -279

Cash flow from operating activities 958 791 474 -317

Capex 701 558 656 98

Number of new store openings 57 57 42 -15

9M 2013/14

reported

9M 2013/14

METRO GROUP, Investor Relations

17 & 18 September 2015 | © METRO AG 2015 30

OUTLOOK 2014/15: FINANCIAL TARGETS

€ billlion

Reported

FY 2013/143

Guidance

FY 2014/15

Sales growth1.2 +1.3% >0%

LFL sales growth +0.1% >0%

EBIT before special items 1,531 >1,5312

Capex 1.0 ~1.5

Net debt 4.7flat <3.2

Number of new store openings 68flat ~501Adjusted for portfolio changes 2Based on constant foreign exchange rates3Adjusted for Galeria Kaufhof

METRO GROUP, Investor Relations

17 & 18 September 2015 | © METRO AG 2015 31

AGENDA

01 Active Portfolio Management@ METRO GROUP 3

02 METRO GROUP @ a Glance 131

03 Three Market Leading Sales Lines 16

04 Performance in Q3 2014/15 & Outlook FY 2014/15 26

05 Key takeaways 32

METRO GROUP, Investor Relations

17 & 18 September 2015 | © METRO AG 2015 32

CUSTOMER VALUE clearly in focus, relevance further increased

BUSINESS MODEL UPGRADE on track and to be intensified

EFFECTIVENESS enhanced with new Operating Model (MCC)

Successful PORTFOLIO MANAGEMENT to be continued

Fast growing new sales CHANNELS and SERVICES

Strengthened BALANCE SHEET

INNOVATION as a catalyst for further growth

Creating value for all METRO GROUP stakeholders

METRO GROUP’S TRANSFORMATION IS ON TRACK

METRO GROUP, Investor Relations

17 & 18 September 2015 | © METRO AG 2015 33

APPENDIX

METRO GROUP, Investor Relations

17 & 18 September 2015 | © METRO AG 2015 34

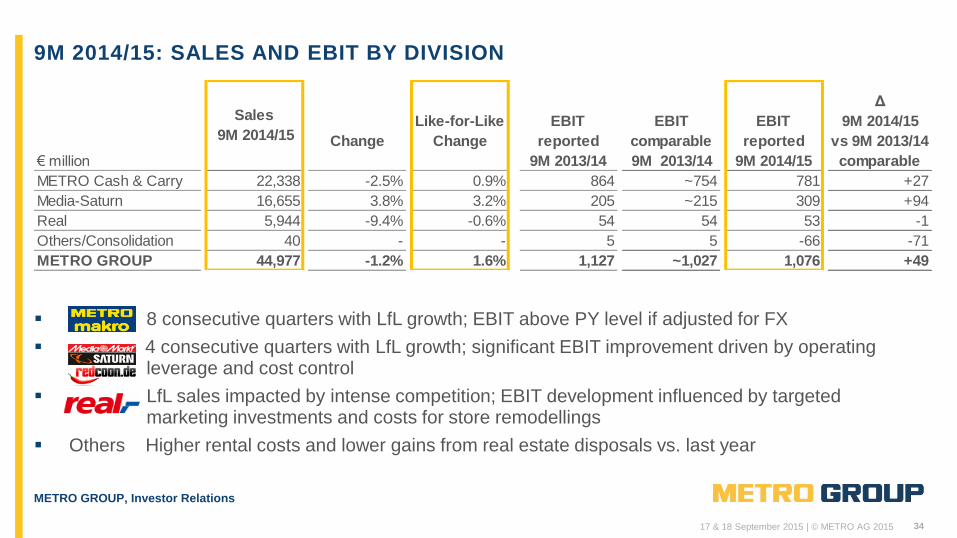

9M 2014/15: SALES AND EBIT BY DIVISION

8 consecutive quarters with LfL growth; EBIT above PY level if adjusted for FX

4 consecutive quarters with LfL growth; significant EBIT improvement driven by operating leverage and cost control

LfL sales impacted by intense competition; EBIT development influenced by targeted marketing investments and costs for store remodellings

Others Higher rental costs and lower gains from real estate disposals vs. last year

Change

Like-for-Like

Change

€ million

METRO Cash & Carry 22,338 -2.5% 0.9% 864 ~754 781 +27

Media-Saturn 16,655 3.8% 3.2% 205 ~215 309 +94

Real 5,944 -9.4% -0.6% 54 54 53 -1

Others/Consolidation 40 - - 5 5 -66 -71

METRO GROUP 44,977 -1.2% 1.6% 1,127 ~1,027 1,076 +49

Sales

9M 2014/15EBIT

reported

9M 2013/14

EBIT

comparable

9M 2013/14

EBIT

reported

9M 2014/15

Δ

9M 2014/15

vs 9M 2013/14

comparable

METRO GROUP, Investor Relations

17 & 18 September 2015 | © METRO AG 2015 35

APPRECIATION OF EBIT Q3 2014/15

175

253

171

Q3 2014/15

(Before

Special Items)

209

Special Items

35

Q3 2014/15

(Reported)

Q3 2013/14

(Comparable

Before

Special Items)

~243

Negative

FX Impact

~-10

Q3 2013/14

(Before

Special Items)

Special Items

83

Q3 2013/14

(Reported)

in € million -34

~601)

~301)

1) Real Estate Gains from Divestments

METRO GROUP, Investor Relations

17 & 18 September 2015 | © METRO AG 2015 36

METRO CASH & CARRY: HIGHLIGHTS Q3 2014/15

8th consecutive quarter with LfL sales growth

▪ Germany improved vs. Q2 despite shift of Easter

business

▪ Western Europe: Italy and Spain with positive LfL

sales growth

▪ Eastern Europe: esp. Russia and Turkey with positive

LfL sales development

▪ Asia: China LfL sales development impacted by giving

up low-margin volume business

Delivery sales increased by 15% (representing more

than 10% of total Cash & Carry sales)

7 new store openings, 2 store closures

Sale of METRO Cash & Carry Vietnam on track

Q3 Q2

1.1

Q1

1.4

Q4

0.1

Q3

2.0

Q2

0.8

Q1

0.9 0.1

2013/14 2014/15

Like-for-Like Sales Development in %

Q3 Q2

10.1

Q1

8.6

Q4

10.0

Q3

9.4

Q2

9.4

Q1

7.9 10.9

2013/14 2014/15

Delivery Sales Share in %

METRO GROUP, Investor Relations

17 & 18 September 2015 | © METRO AG 2015 37

METRO CASH & CARRY: STRATEGIC UPDATE

Implementation of the New Operating Model to foster

entrepreneurship well on track

▪ New organizational structure “live” since 1 July 2015, teams

almost fully staffed

▪ Pieter Boone took his office as member of the Management Board

of METRO AG

▪ Countries currently working on the Value Creation Plans (VCPs)

together with their Operating Partners (OPs)

▪ Full implementation of the New Operating Model by October 2016

Techstars METRO Accelerator well on track

METRO Cash & Carry business in Russia under control

METRO Cash & Carry Germany

▪ Improved development of important HoReCa customer group

▪ Upgrading and rebranding of Schaper stores to METRO GASTRO

started

▪ First promising results from FSD pilot in Weiterstadt

METRO GROUP, Investor Relations

17 & 18 September 2015 | © METRO AG 2015 38

Deal rationale for MCC Valuation and deal structure

Acquire full FSD capabilities

Accelerate growth in the HoReCa sector

Expand into additional countries

Add strong management capabilities

Capture additional value through

▪ Strengthened access to exclusive

assortment

▪ Support of international expansion

▪ Capture opportunities for selected store

operations in new regions

Seller: Klassisk Holding Limited (EQT)

Share deal

Enterprise value of US$290m + earn-out

Valuation multiple of 11.6x (EV/2015E EBITDA)

in line with peers (MARR1)12.3x; Sysco1)10.1x)

METRO CASH & CARRY: ACQUISITION OF CLASSIC FINE FOODS,

AN FSD PLAYER IN THE PREMIUM SEGMENT IN ASIA (III)

1) Valuation as at 28 July 2015 based on factset

METRO GROUP, Investor Relations

17 & 18 September 2015 | © METRO AG 2015 39

MEDIA-SATURN: HIGHLIGHTS Q3 2014/15

4th consecutive quarter with positive LfL sales growth

▪ Germany impacted by missing sales from FIFA

World-Cup last year

▪ Western Europe: All major countries grew

▪ Eastern Europe: Positive despite Russia suffering

from crisis

Continued strong growth in online sales of +24%

(representing 9% of total Media-Saturn sales)

Internet product offering further increased to

▪ about 130,000 SKUs at www.mediamarkt.de

▪ about 120,000 SKUs at www.saturn.de

4 new store openings, 5 store closures

Q3

0.2

Q2

5.2

Q1

3.8

Q4

1.7

Q3

-0.2

Q2

-3.7

Q1

-1.0

2013/14 2014/15

Like-for-Like Sales Development in %

404436512

353328358398

Q3 Q2 Q1 Q4 Q3 Q2 Q1

2013/14 2014/15

Online Sales in € million

1 1

1Adjusted for Redcoon Denmark and France

METRO GROUP, Investor Relations

17 & 18 September 2015 | © METRO AG 2015 40

MEDIA-SATURN: STRATEGIC UPDATE

Business transformation well on track

▪ European market leadership extended by 0.6%pt to 13.4% (highest market share ever!)

▪ Market leadership in 9 countries, market share increased in 11 countries

▪ Market share gains in all categories

▪ All countries contribute to improved operating performance

Implementation of electronic shelf labelling (ESL)

Further roll-out of city center formats to meet customer needs

Ongoing portfolio optimisation

(space reductions / store closings)

METRO GROUP, Investor Relations

17 & 18 September 2015 | © METRO AG 2015 41

MEDIA-SATURN LAUNCHES NEW ENTERTAINMENT PORTAL JUKE

German launch of JUKE (joint digital entertainment platform)

on 3rd August 2015

Strategic expansion of Media-Saturn’s digital business through

comprehensive digital offering:

▪ >30 million songs

▪ >15,000 movies and TV series

▪ 1.5 million e-books

▪ 2,400 PC games

▪ 2,400 PC software applications

Free JUKE app pre-installed on various devices and available for

download on Google Play and iOS App Store

METRO GROUP, Investor Relations

17 & 18 September 2015 | © METRO AG 2015 42

REAL GERMANY: HIGHLIGHTS Q3 2014/15

+1.4% LfL sales growth over two years

Good performance of fruit & vegetables as well as

household goods

Online sales with strong improvement

EBIT with stable development driven by tight cost

control and sound margin development in some

categories

Joint venture with Carlton Investment to further

enhance attractiveness and footfall of 10 Real

hypermarkets

1 store closure

0.9

Q2 Q3 Q1

5.1

0.2

Q4

-6.6

Q2 Q1

1.1

-2.1

Q3

-3.7

2013/14 2014/15

Like-for-Like Sales Development in Germany in %

METRO GROUP, Investor Relations

17 & 18 September 2015 | © METRO AG 2015 43

REAL GERMANY: STRATEGIC UPDATE

Additional initiatives to further improve performance

▪ Service agreement with Markant for complete settlement

▪ Striving for in-house collective agreement

Commercial Model will drive top-line performance

▪ 82 stores already remodeled, 25 to follow in Q4 2014/15

▪ Remodeled stores continue to outperform the other stores by round

about 2%

Supply chain optimization moving forward

METRO GROUP, Investor Relations

17 & 18 September 2015 | © METRO AG 2015 44

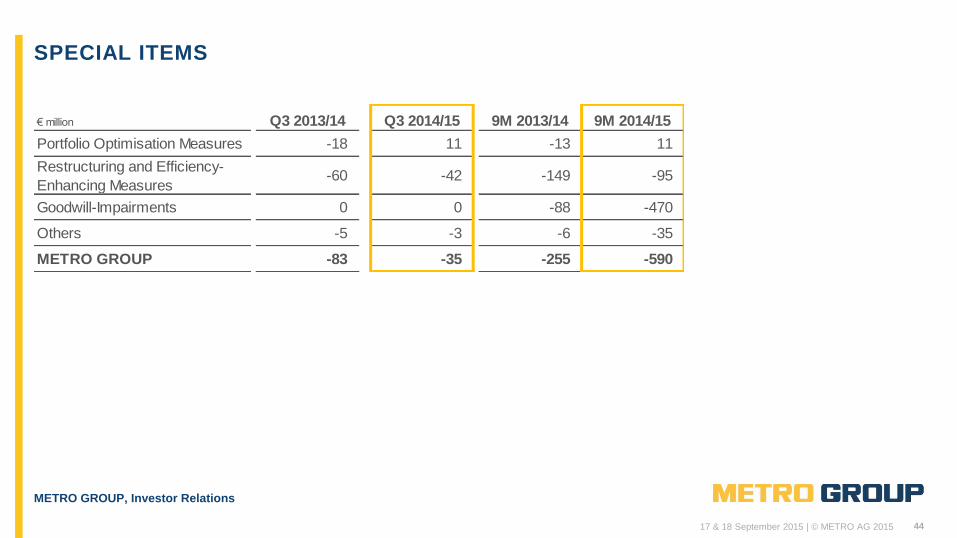

SPECIAL ITEMS

€ million

Q3 2013/14

Q3 2014/15

9M 2013/14

9M 2014/15

Portfolio Optimisation Measures -18 11 -13 11

Restructuring and Efficiency-

Enhancing Measures-60 -42 -149 -95

Goodwill-Impairments 0 0 -88 -470

Others -5 -3 -6 -35

METRO GROUP -83 -35 -255 -590

METRO GROUP, Investor Relations

17 & 18 September 2015 | © METRO AG 2015 45

STORES BY DIVISION AND COUNTRY

*including 4 stores in the Others segment

METRO GROUP, Investor Relations

17 & 18 September 2015 | © METRO AG 2015 46

METRO TECHSTARS ACCELERATOR (1)

BEST DIGITAL INNVOATIONS FOR HORECA

Seeking the best digital innovations for

hotels and restaurants.

Intensive start-up-bootcamp

Broad network of experienced mentors

3 prestigious partners

10 companies to be chosen

techstars METRO ACCELERATOR with

R/GA

Berlin – 2015/2016

METRO GROUP, Investor Relations

17 & 18 September 2015 | © METRO AG 2015 47

METRO TECHSTARS ACCELERATOR (2)

APPLICANTS FROM AROUND THE GLOBE

METRO GROUP, Investor Relations

17 & 18 September 2015 | © METRO AG 2015 48

CULINARY AGENTS (1)

The Vision:

the networking platform enabling talent and

supporting businesses in the hospitality industry

The mission:

is to connect, develop and educate the world’s

existing and aspiring hospitality professionals.

Focusing on the problem of talent sourcing first.

METRO GROUP, Investor Relations

17 & 18 September 2015 | © METRO AG 2015 49

CULINARY AGENTS (2)

Become the leading professional network

for the Hospitality Community

Support of European roll-out by METRO

Italy & France to launch with major events in Oct 15;

Spain, Portugal & Germany to follow

Pre-launch piloting with key hospitality

schools and opinion leaders

Partnership agreement with Guide

Michelin (USA, France, Italy)

METRO GROUP, Investor Relations

17 & 18 September 2015 | © METRO AG 2015 50

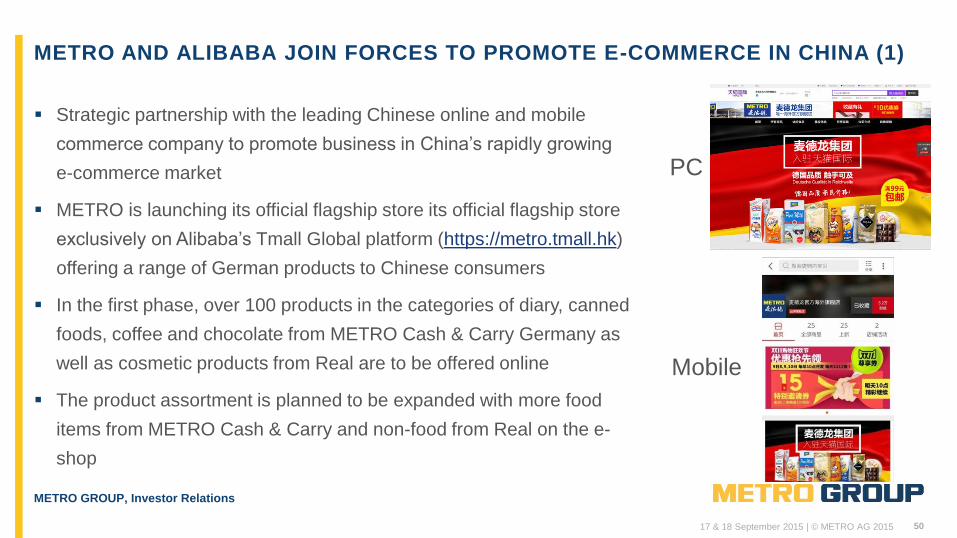

METRO AND ALIBABA JOIN FORCES TO PROMOTE E-COMMERCE IN CHINA (1)

Strategic partnership with the leading Chinese online and mobile

commerce company to promote business in China’s rapidly growing

e-commerce market

METRO is launching its official flagship store its official flagship store

exclusively on Alibaba’s Tmall Global platform (https://metro.tmall.hk)

offering a range of German products to Chinese consumers

In the first phase, over 100 products in the categories of diary, canned

foods, coffee and chocolate from METRO Cash & Carry Germany as

well as cosmetic products from Real are to be offered online

The product assortment is planned to be expanded with more food

items from METRO Cash & Carry and non-food from Real on the e-

shop

PC

Mobile

METRO GROUP, Investor Relations

17 & 18 September 2015 | © METRO AG 2015 51

7 5 2 1 0 1 1

6 4 0

21

39

35

31

23 21

25

40

21

28

31

41

32 33

1,335 763

426 250 222 375 1,060 1,311 1,516

2,013

4,369 4,982

4,014 3,741 3,367 3,275

4,464 5,711

4,969

6,930

8,675

11,078

11,706

9,368

00:00 01:00 02:00 03:00 04:00 05:00 06:00 07:00 08:00 09:00 10:00 11:00 12:00 13:00 14:00 15:00 16:00 17:00 18:00 19:00 20:00 21:00 22:00 23:00

Orders

Visitor

Time

METRO & Alibaba

Announcement

METRO AND ALIBABA JOIN FORCES TO PROMOTE E-COMMERCE IN CHINA (2)

METRO GROUP, Investor Relations

17 & 18 September 2015 | © METRO AG 2015 52

CONTACT

Investor Relations

Metro-Straße 1

40235 Duesseldorf

Germany

Tel.: +49 (0)211 6886-1051

Fax: +49 (0)211 6886-3759

Email: [email protected]

Internet: www.metrogroup.de