Embed Size (px)

Citation preview

4251

UC Tax Issues

Office of the Controller

Financial Management Certificate Program

December 2014

4251

04/19/23 2

Is UC “Tax Exempt”?

UC is an exempt organization for income tax purposes only under Section 501(c)(3) of the Internal Revenue Code

CA BOE considers UC subject to Sales/Use Tax

UC also must do non-payroll income tax information reporting (1099) and nonresident withholding

4251

04/19/23 3

Agenda

Sales & Use Tax Unrelated Business Income Employee vs. Non-employee Relations Employee Fringe Benefits Taxable Payments through the A/P System Tax Treatment of Moving Expenses Tax Treatment of Travel Expenses

4251

04/19/23 4

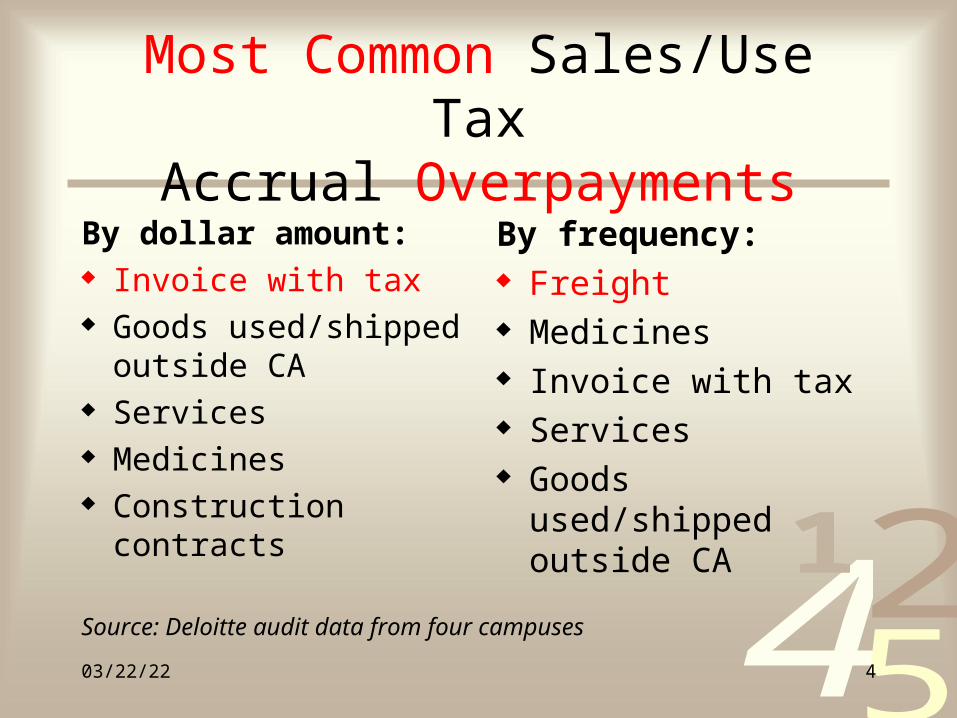

Most Common Sales/Use TaxAccrual Overpayments

By dollar amount: Invoice with tax Goods used/shipped

outside CA Services Medicines Construction contracts

By frequency: Freight Medicines Invoice with tax Services Goods used/shipped

outside CA

Source: Deloitte audit data from four campuses

4251

04/19/23 5

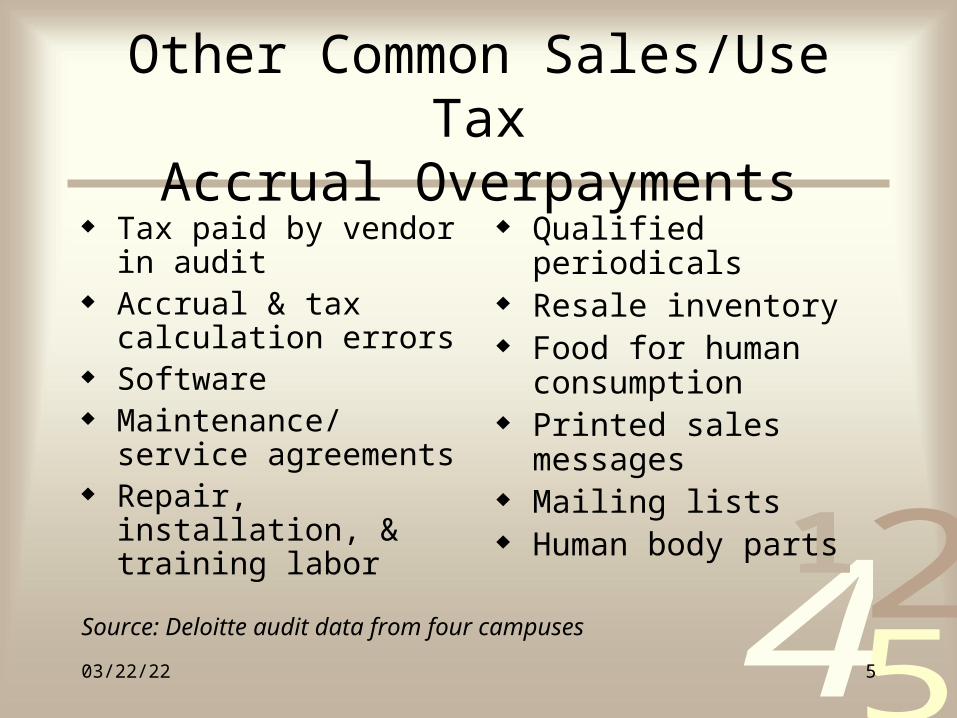

Other Common Sales/Use TaxAccrual Overpayments

Tax paid by vendor in audit

Accrual & tax calculation errors

Software Maintenance/service

agreements Repair, installation, &

training labor

Qualified periodicals Resale inventory Food for human

consumption Printed sales messages Mailing lists Human body parts

Source: Deloitte audit data from four campuses

4251

04/19/23 6

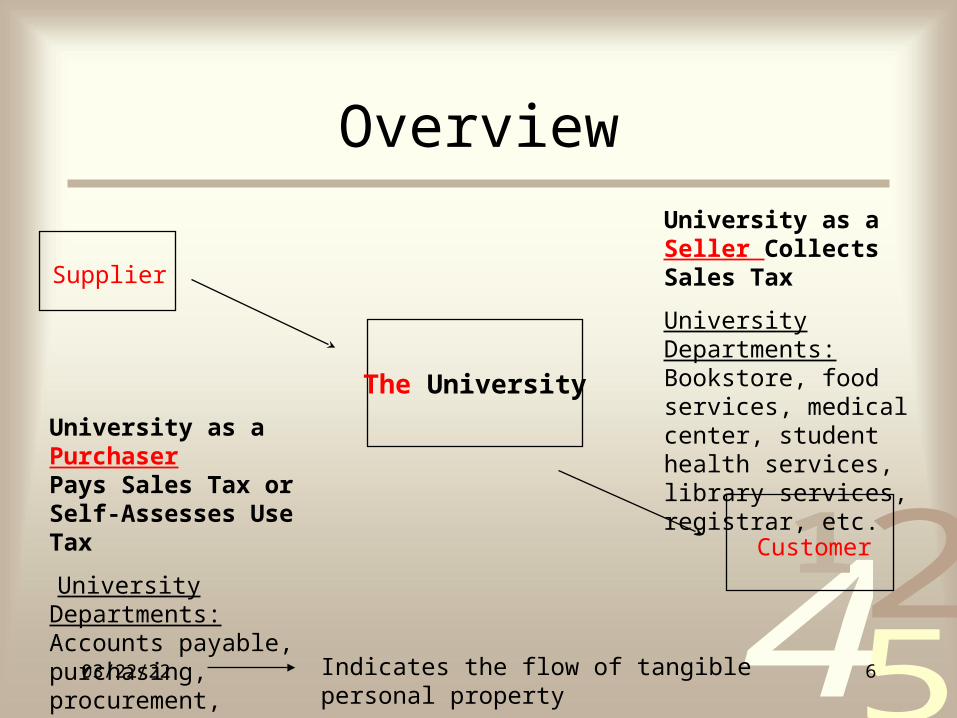

Overview

The University

Supplier

Customer

University as a PurchaserPays Sales Tax or Self-Assesses Use Tax

University Departments:Accounts payable, purchasing, procurement,medical center, cafeteria, etc.

University as a Seller Collects Sales Tax

University Departments:Bookstore, food services, medical center, student health services, library services, registrar, etc.

Indicates the flow of tangible personal property

4251

04/19/23 7

Sales Tax – Retail Perspective

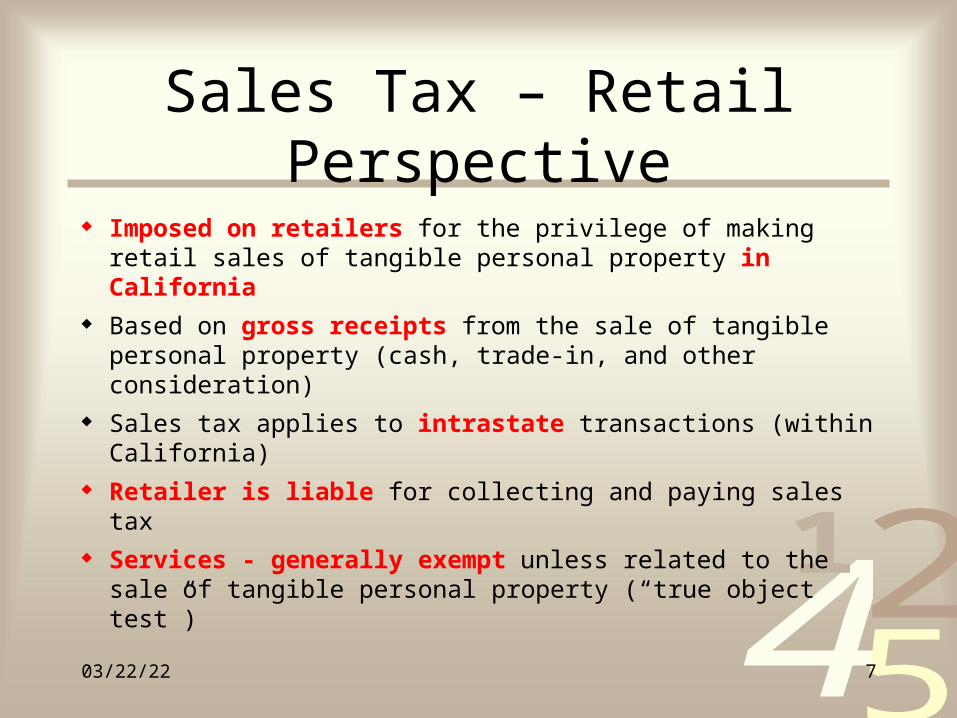

Imposed on retailers for the privilege of making retail sales of tangible personal property in California

Based on gross receipts from the sale of tangible personal property (cash, trade-in, and other consideration)

Sales tax applies to intrastate transactions (within California)

Retailer is liable for collecting and paying sales tax Services - generally exempt unless related to the sale of

tangible personal property (“true object test”)

4251

04/19/23 8

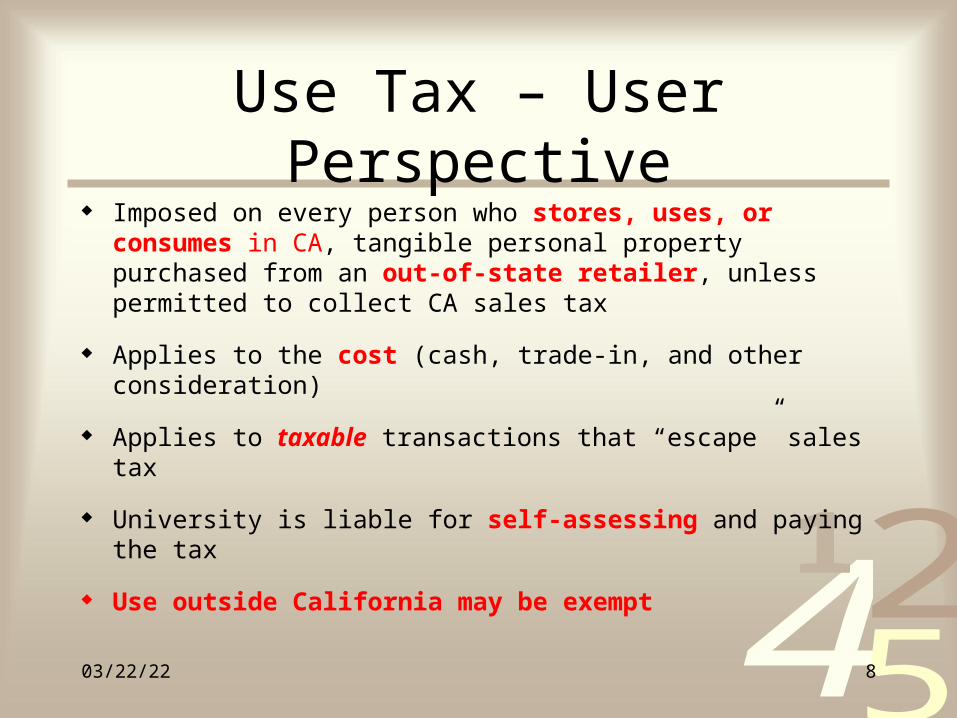

Use Tax – User Perspective Imposed on every person who stores, uses, or consumes in CA,

tangible personal property purchased from an out-of-state retailer, unless permitted to collect CA sales tax

Applies to the cost (cash, trade-in, and other consideration)

Applies to taxable transactions that “escape” sales tax

University is liable for self-assessing and paying the tax

Use outside California may be exempt

4251

04/19/23 9

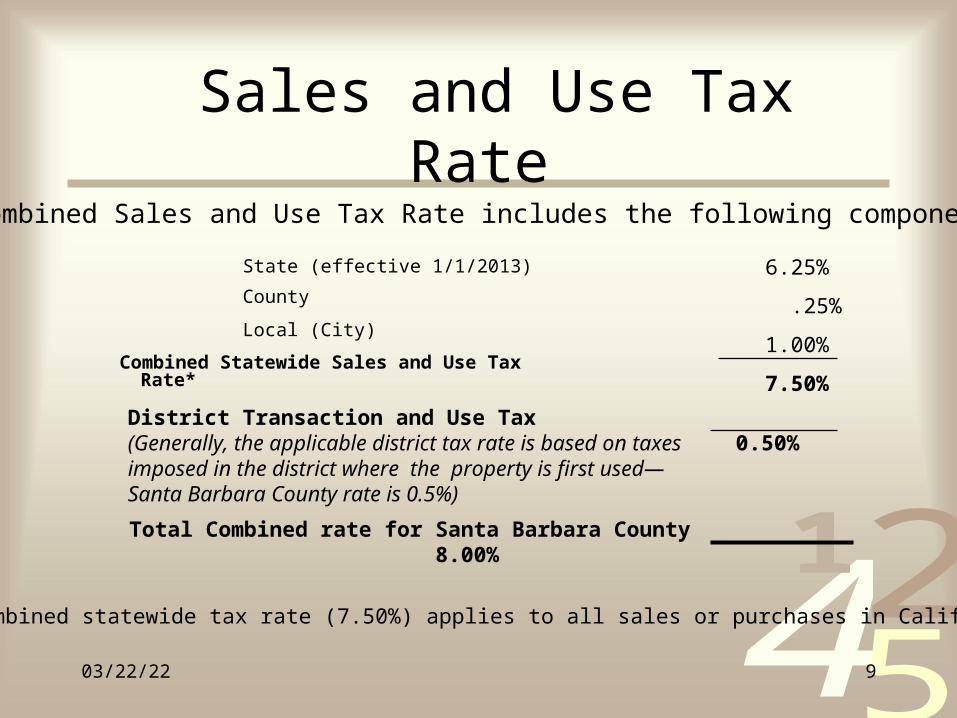

Sales and Use Tax Rate

State (effective 1/1/2013)

County

Local (City)

Combined Statewide Sales and Use Tax Rate*

* The combined statewide tax rate (7.50%) applies to all sales or purchases in California

6.25%

.25%

1.00%

7.50%

District Transaction and Use Tax

(Generally, the applicable district tax rate is based on taxes imposed in the district where the property is first used—Santa Barbara County rate is 0.5%)

0.50%

The combined Sales and Use Tax Rate includes the following components:

Total Combined rate for Santa Barbara County 8.00%

4251

04/19/23 10

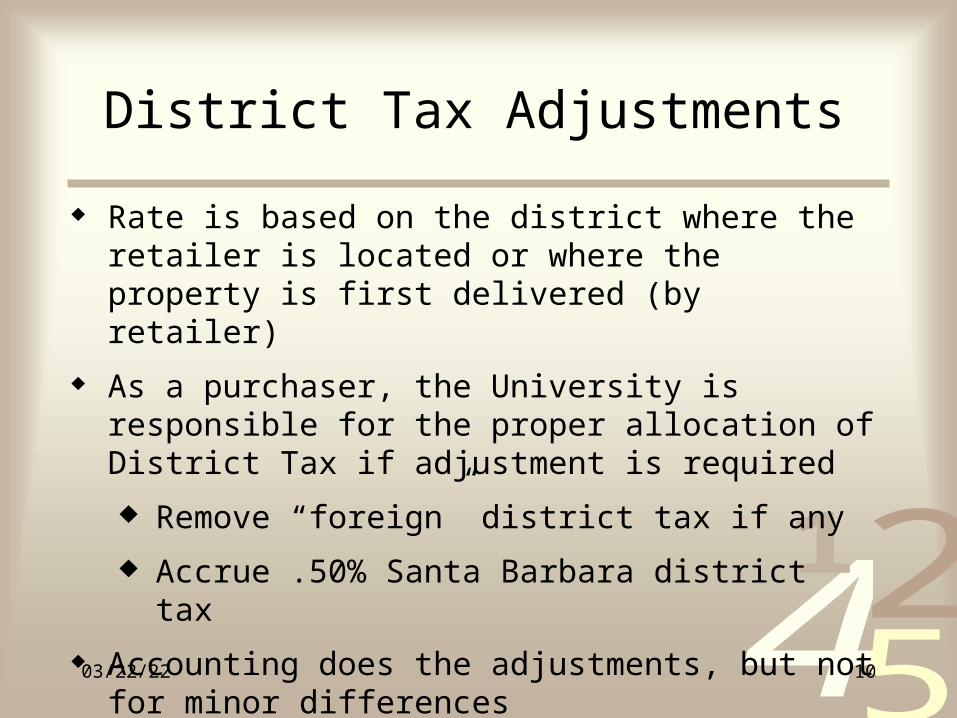

Rate is based on the district where the retailer is located or where the property is first delivered (by retailer)

As a purchaser, the University is responsible for the proper allocation of District Tax if adjustment is required

Remove “foreign” district tax if any

Accrue .50% Santa Barbara district tax

Accounting does the adjustments, but not for minor differences

District Tax Adjustments

4251

04/19/23 11

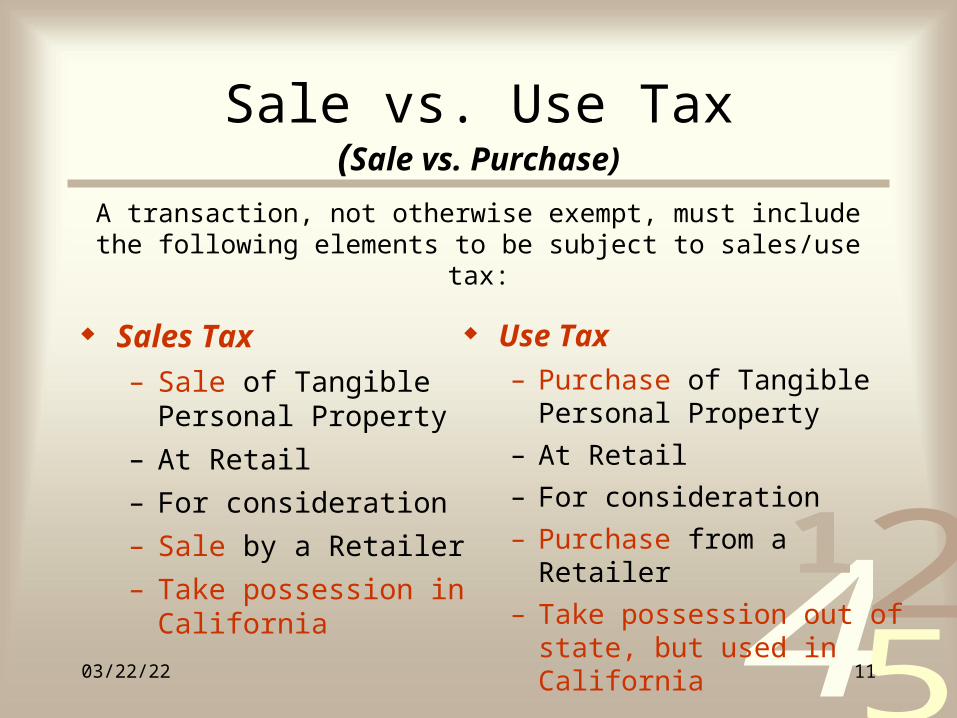

Sale vs. Use Tax(Sale vs. Purchase)

A transaction, not otherwise exempt, must include the following elements to be subject to sales/use tax:

Sales Tax– Sale of Tangible Personal

Property

– At Retail

– For consideration

– Sale by a Retailer

– Take possession in California

Use Tax– Purchase of Tangible Personal

Property

– At Retail

– For consideration

– Purchase from a Retailer

– Take possession out of state, but used in California

4251

04/19/23 12

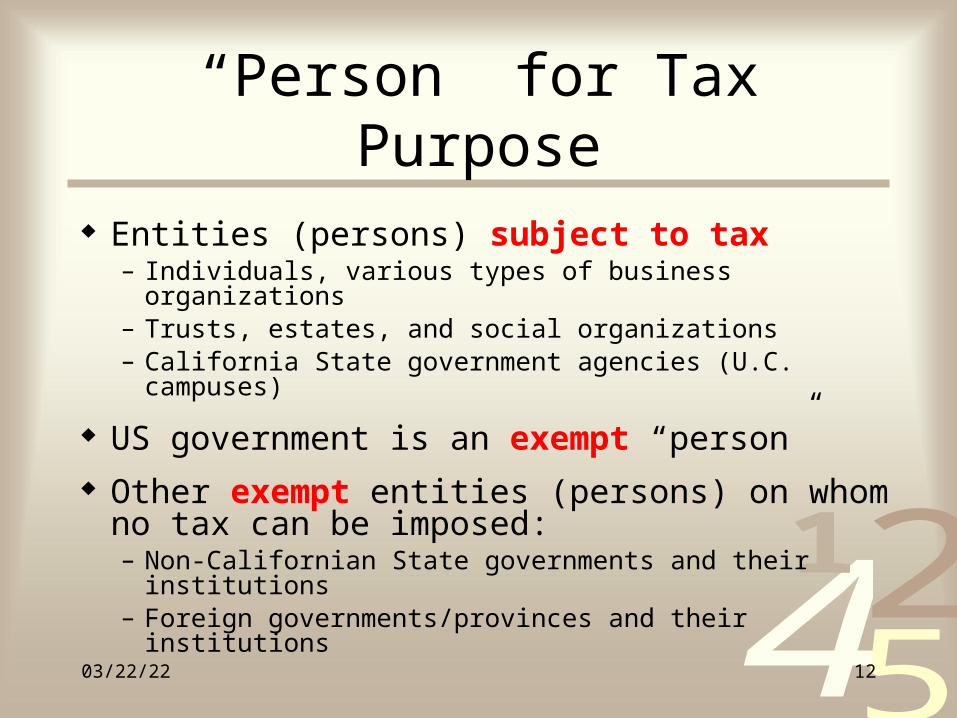

“Person” for Tax Purpose

Entities (persons) subject to tax – Individuals, various types of business organizations– Trusts, estates, and social organizations– California State government agencies (U.C. campuses)

US government is an exempt “person”

Other exempt entities (persons) on whom no tax can be imposed:– Non-Californian State governments and their institutions– Foreign governments/provinces and their institutions

4251

04/19/23 13

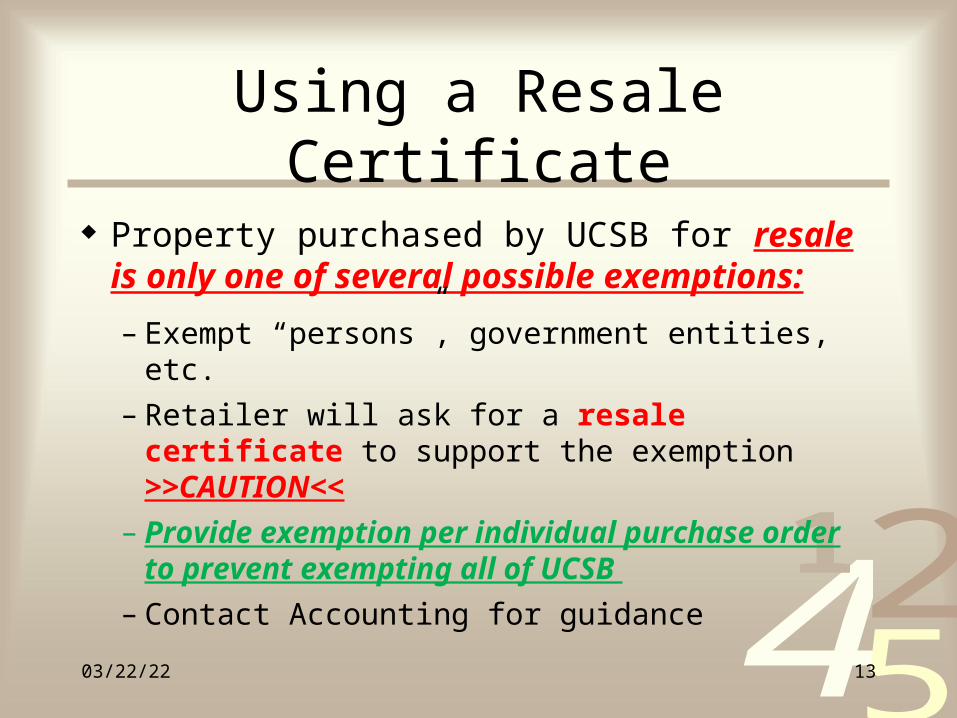

Using a Resale Certificate

Property purchased by UCSB for resale is only one of several possible exemptions:

– Exempt “persons”, government entities, etc.

– Retailer will ask for a resale certificate to support the exemption >>CAUTION<<

– Provide exemption per individual purchase order to prevent exempting all of UCSB

– Contact Accounting for guidance

4251

04/19/23 14

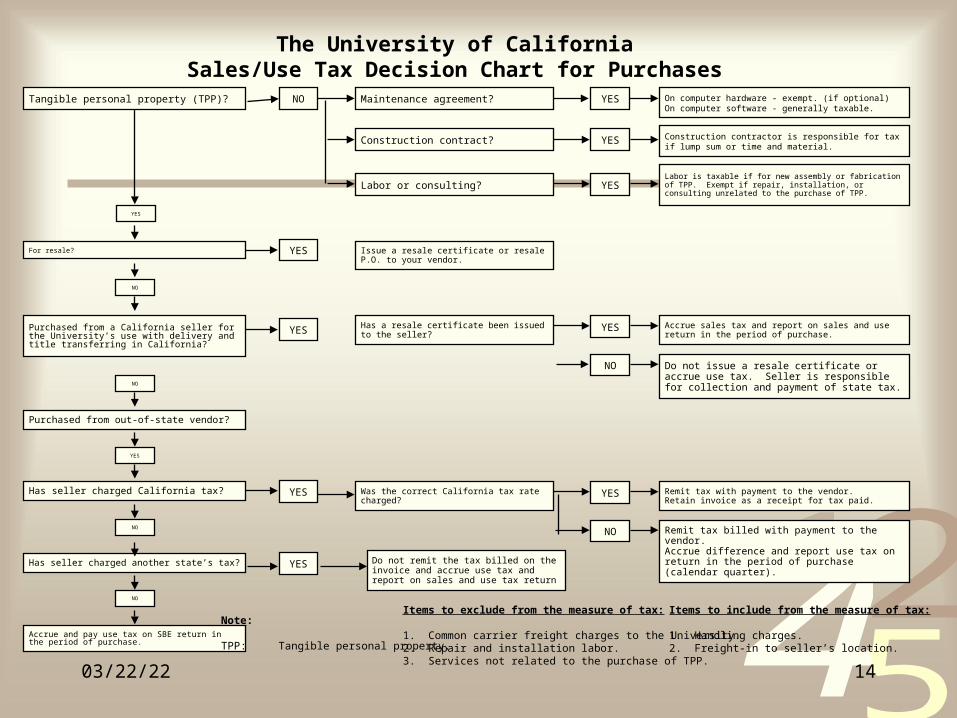

The University of CaliforniaSales/Use Tax Decision Chart for Purchases

Accrue sales tax and report on sales and use return in the period of purchase.

YES

YES

On computer hardware - exempt. (if optional)On computer software - generally taxable.

Construction contractor is responsible for tax if lump sum or time and material.

Labor is taxable if for new assembly or fabrication of TPP. Exempt if repair, installation, or consulting unrelated to the purchase of TPP.

Tangible personal property (TPP)? NO Maintenance agreement?

Construction contract?

Labor or consulting?

YES

For resale?

Purchased from a California seller for the University’s use with delivery and title transferring in California?

Purchased from out-of-state vendor?

YES

NO

YES

YES

NO

Has seller charged California tax?

Has seller charged another state’s tax?

Accrue and pay use tax on SBE return in the period of purchase.

YES

NO

NO

Note:

TPP: Tangible personal property.

YES

Issue a resale certificate or resale P.O. to your vendor.

Has a resale certificate been issued to the seller?

Was the correct California tax rate charged?

Items to exclude from the measure of tax:

1. Common carrier freight charges to the University.2. Repair and installation labor.3. Services not related to the purchase of TPP.

Do not issue a resale certificate or accrue use tax. Seller is responsible for collection and payment of state tax.

NO

Remit tax with payment to the vendor.Retain invoice as a receipt for tax paid.

YES

Remit tax billed with payment to the vendor.Accrue difference and report use tax on return in the period of purchase (calendar quarter).

NO

Items to include from the measure of tax:

1. Handling charges.2. Freight-in to seller’s location.

YES

YES Do not remit the tax billed on the invoice and accrue use tax and report on sales and use tax return

4251

04/19/23 15

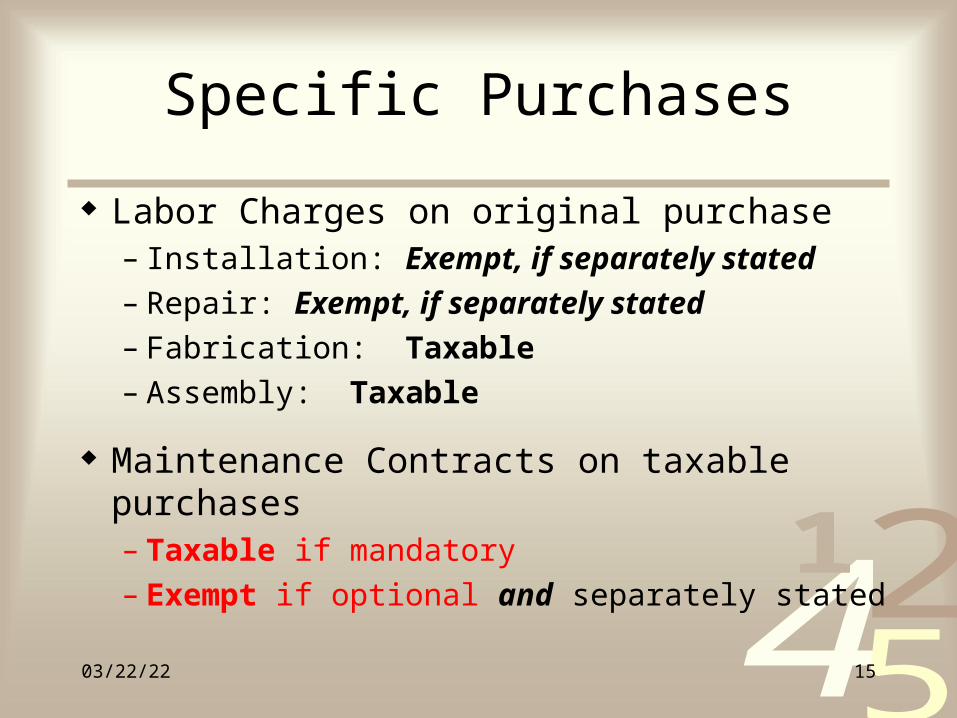

Specific Purchases

Labor Charges on original purchase– Installation: Exempt, if separately stated– Repair: Exempt, if separately stated– Fabrication: Taxable– Assembly: Taxable

Maintenance Contracts on taxable purchases– Taxable if mandatory– Exempt if optional and separately stated

4251

04/19/23 16

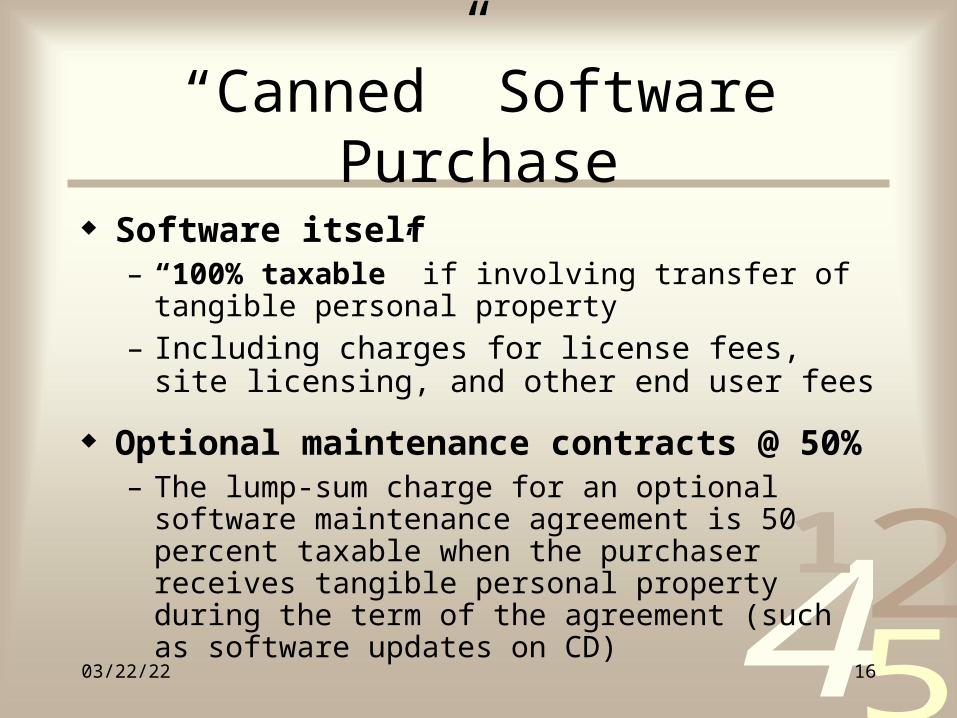

“Canned” Software Purchase

Software itself– “100% taxable” if involving transfer of tangible

personal property

– Including charges for license fees, site licensing, and other end user fees

Optional maintenance contracts @ 50%– The lump-sum charge for an optional software

maintenance agreement is 50 percent taxable when the purchaser receives tangible personal property during the term of the agreement (such as software updates on CD)

4251

04/19/23 17

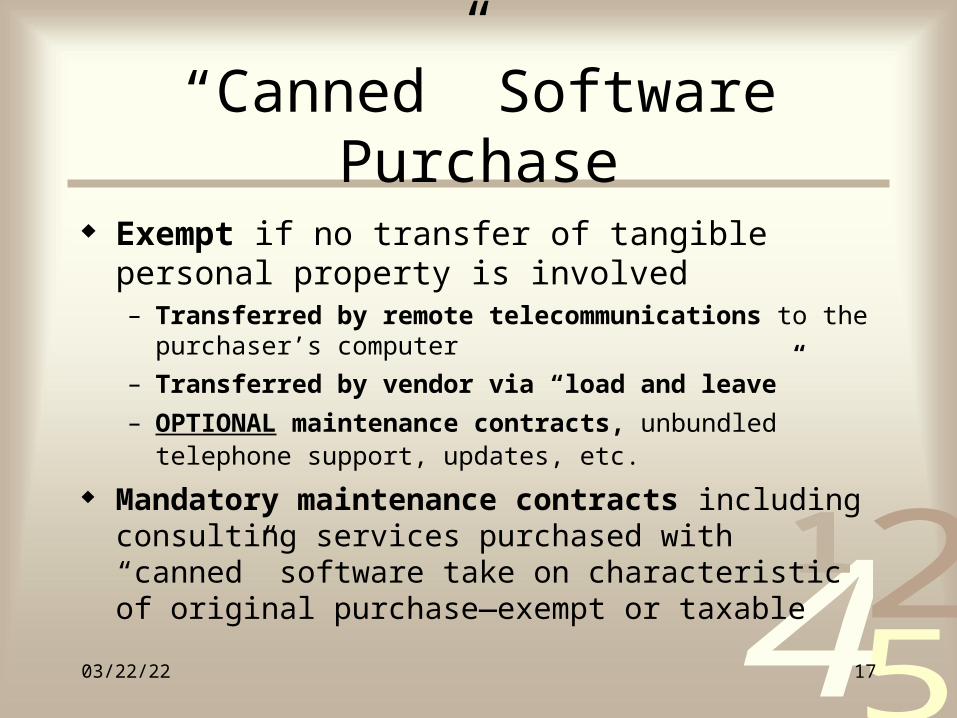

“Canned” Software Purchase

Exempt if no transfer of tangible personal property is involved– Transferred by remote telecommunications to the purchaser’s

computer

– Transferred by vendor via “load and leave”

– OPTIONAL maintenance contracts, unbundled telephone support, updates, etc.

Mandatory maintenance contracts including consulting services purchased with “canned” software take on characteristic of original purchase—exempt or taxable

4251

04/19/23 18

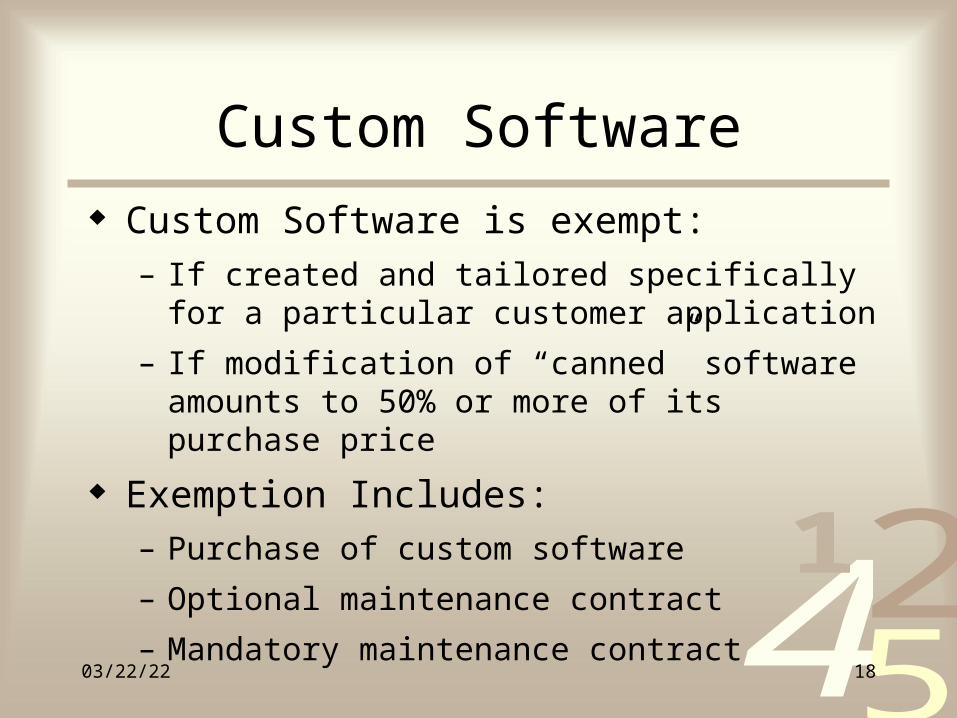

Custom Software Custom Software is exempt:

– If created and tailored specifically for a particular customer application

– If modification of “canned” software amounts to 50% or more of its purchase price

Exemption Includes:– Purchase of custom software

– Optional maintenance contract

– Mandatory maintenance contract

4251

04/19/23 19

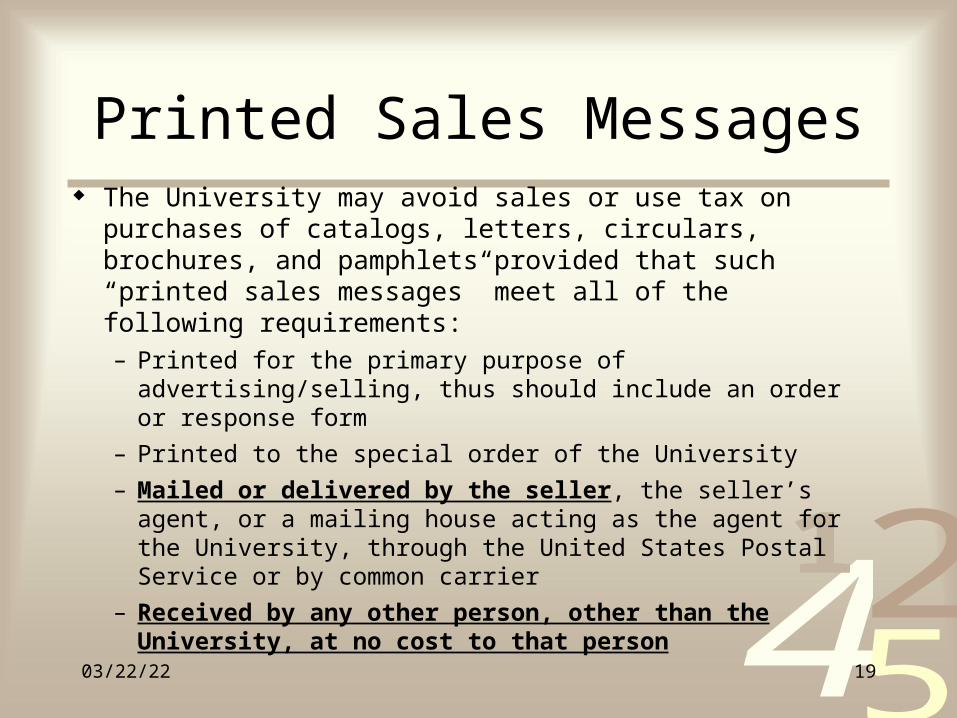

Printed Sales Messages The University may avoid sales or use tax on purchases of

catalogs, letters, circulars, brochures, and pamphlets provided that such “printed sales messages” meet all of the following requirements:– Printed for the primary purpose of advertising/selling, thus

should include an order or response form

– Printed to the special order of the University

– Mailed or delivered by the seller, the seller’s agent, or a mailing house acting as the agent for the University, through the United States Postal Service or by common carrier

– Received by any other person, other than the University, at no cost to that person

4251

04/19/23 20

University as a Seller

California law holds University responsible for collecting sales tax

Departments need to collect sales tax when selling any tangible personal propertyBookstore sales, used furniture, cataloguesIncluding student organization fund raising (sale of lab

notebooks, candy-filled coffee mugs, etc.)Maintain proper records Deposit tax collected into proper liability accountContact Accounting for guidance

4251

04/19/23 21

Sales and Use Tax

Where to go for help?– UC Sales and Use Tax Manual (243 pages)http://www.ucop.edu/financial-accounting/_files/sutm.pdf

http://policy.ucop.edu/doc/3410313/AM-T182-73

– Call Steve Kriz, x3480 [email protected]

4251

04/19/23 22

Sales and Use Tax

DISCUSSION ITEMSyellow handouts

4251

04/19/23 23

Unrelated Business Income

Unrelated Business Activity:

– If the activity is a trade or business– Regularly carried on– Not substantially related to exempt purpose (i.e.

education, research, public service, or patient care)

4251

04/19/23 24

Examples ofUnrelated Business Income

Recreation: – Sale of recreation membership cards to the general

public and alumni

Athletics: – Sale of advertising space in sporting event programs

Scanning Transmission Electron Microscope (STEM) Facility: – Sale of STEM services to non-University users

Other?: – Name one more

4251

04/19/23 25

Activities Exempt from Tax

General Rule = Income from an unrelated business activity is taxable unless it meets one of several specific exemptions:

– Convenience of members – Passive income – Research – Real estate rents

4251

04/19/23 26

Determining Unrelated Business

Contact General Accounting

Complete a non-financial questionnaire describing your activity

If it is unrelated business, UCOP will send a financial worksheet to be completed by the department

4251

04/19/23 27

Employee vs.Non-Employee Relations

Federal (IRS Code) and state laws (Unemployment Insurance Code) govern use of independent contractors

Significant consequences of incorrectly classifying workers

Use the 11 Questions of the Pre-Hire Worksheet, Exhibit D, BUS-77*

*Business & Finance Bulletins, BUS-77: Independent Contractor Guidelines

http://policy.ucop.edu/doc/3220483/BFB-BUS-77

4251

04/19/23 28

What is an Independent Contractor/Consultant?

A Person who:– Is in business for themselves– Is hired to perform specific, one-time tasks– Is NOT a University employee– Is ineligible for employee benefits– Signs a contract/agreement issued/authorized by

Contracts & Property

The University determines the final result, but does not direct how the work is to be accomplished

4251

04/19/23 29

Can a Student Employee Also Be an Independent Contractor?

YES—law allows IC status for activities traditionally provided by independent contractors, for example event performances

NO— student employees performing services under the direction and supervision of the University must be compensated through Payroll, even for onetime services unrelated to regular work.

4251

04/19/23 30

What is an Independent Contractor/Consultant?

For more information about– Conflict of Interest, – Successor Contracts, – Employee Vendors, – Contractors Who Are Former Employees:

http://www.bfs.ucsb.edu/contracts-property

4251

04/19/23 31

Independent Contractor

UC Business and Finance Bulletins, BUS-34 and BUS-77, outline the University’s policies and procedures with respect to retention of independent contractors

Business and Finance Bulletins library at:http://policy.ucop.edu/manuals/business-and-finance-bulletins.html

4251

04/19/23 32

Nonresident AlienIndependent Contractors

Determination of independent contractor or employee is the same for a U.S. resident and nonresident alien

Federal income taxation, reporting and withholding for nonresident alien independent contractors, depends on:

– worker’s visa type

– immigration status

– worker’s residency status for U.S. tax purposes

– availability of tax treaty benefits, etc.

4251

04/19/23 33

Independent Contractor Status

Incorrectly classifying employees can result in University-specific consequences, such as:

– Possible loss of reimbursement from Contract and Grant funds

– Failure to comply with patent agreement requirements– Violation of state financial conflict of interest rules

4251

04/19/23 34

Independent Contractor Status

Tax consequences:– Assessed back state and federal employment

taxes, income tax withholding, interest, and penalties

– Penalties can be assessed for not paying minimum wage and mandated benefits

4251

04/19/23 35

Contractor vs. Employee

If in doubt whether an individual is a contractor or an employee, contact – Contracts & Property:

• http://www.bfs.ucsb.edu/contracts-property

– Other resources:

• Business & Financial Services: Jim Corkill, x5882

• Human Resources: Melinda Crawford, x5781

4251

04/19/23 36

Independent Contractor

Scenario #1

Tom Jones works 100% for Biology as a word processor. In his free time, he has a graphic design business.

Professor Newton, from Chemistry, has asked Tom to do a small graphic design job. Professor Newton would like to pay him by a non-payroll Form 5. Is this ok? If not, what steps should you take to get him paid?

4251

04/19/23 37

Independent Contractor

Scenario #2

Harmony works 10 hour per week as a student employee at the UCEN. Occasionally this music major also sings with jazz and rock bands.

Harmony performs at an alumni event during All Gaucho Reunion. Can she be paid by a non-payroll Form 5 or should she be set up as an employee of Alumni Association as well?

4251

04/19/23 38

Employee Fringe Benefits

The fair market value of a fringe benefit must be included in an employee’s income unless excluded under a specific exception

4251

04/19/23 39

Employee Fringe Benefits

Examples of potentially taxable benefits:– Parking - up to $245/month reported as pre-tax income– Van Pool/Transportation - up to $245/month reported as

pre-tax income– Housing - unless employee is required to live on or

nearby campus– Loans - forgone interest is taxable unless exempt loan– Discounts - taxable if more than 20% of price offered to

public

4251

04/19/23 40

Payments Subject to Tax and Information Reporting

Accounting for and Tax Reporting of Payments Made Through the Vendor System — AMC* D-371-12.1

State Withholding from Non-Wage Payments to Nonresidents of California — AMC* D-371-77

Taxation of Scholarship and Fellowship Grants and Educational Assistance — AMC* T-182-77

Federal Taxation of Aliens — AMC* T-182-27

*Accounting Manual Chapters: http://policy.ucop.edu/manuals/accounting-manual.html

4251

04/19/23 41

Accounting for and Tax Reporting of Payments Made Through the Vendor System

Chapter provides overview including table of payments subject to tax reporting

Generally payments to corporations are exempt from reporting

Payment to legal and medical corporations are reportable

Tax coding is Accounting’s responsibility, but departments must supply Form-5 data

Accounting Manual: http://policy.ucop.edu/manuals/accounting-manual.htmlChapter D-371-12.1

4251

04/19/23 42

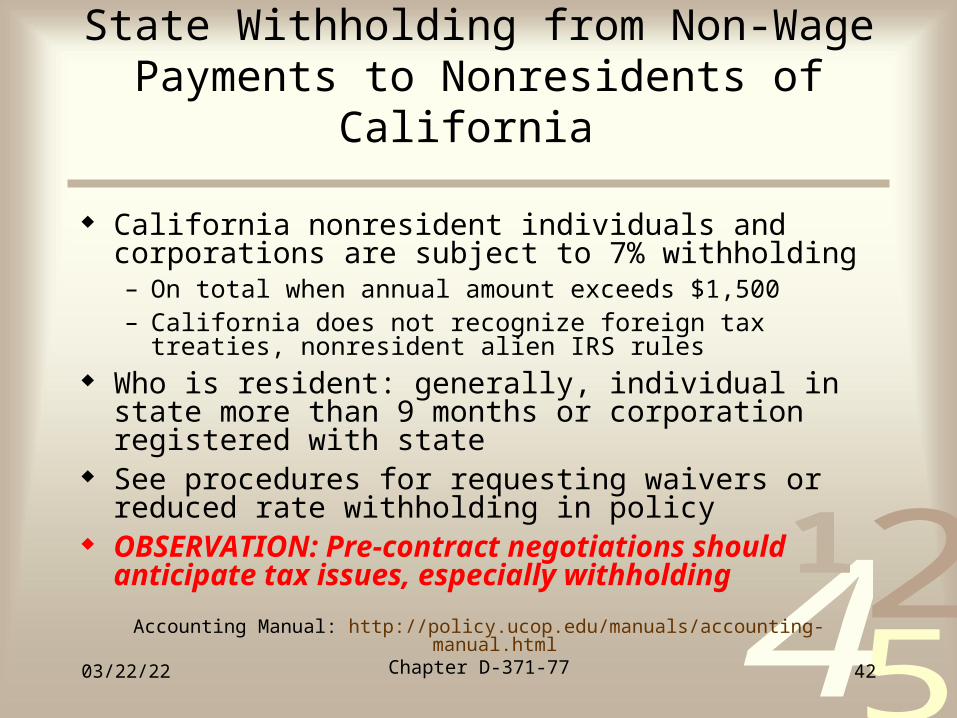

State Withholding from Non-Wage Payments to Nonresidents of California

California nonresident individuals and corporations are subject to 7% withholding– On total when annual amount exceeds $1,500– California does not recognize foreign tax treaties, nonresident

alien IRS rules Who is resident: generally, individual in state more than

9 months or corporation registered with state See procedures for requesting waivers or reduced rate

withholding in policy OBSERVATION: Pre-contract negotiations should

anticipate tax issues, especially withholding

Accounting Manual: http://policy.ucop.edu/manuals/accounting-manual.htmlChapter D-371-77

4251

04/19/23 43

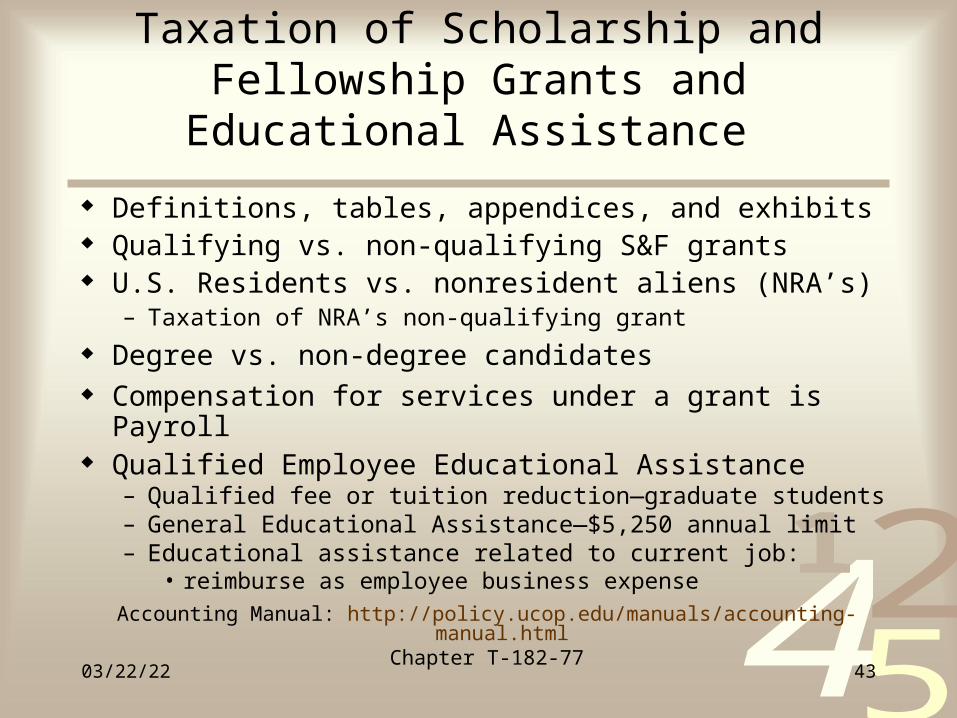

Taxation of Scholarship and Fellowship Grants and Educational Assistance

Definitions, tables, appendices, and exhibits Qualifying vs. non-qualifying S&F grants U.S. Residents vs. nonresident aliens (NRA’s)

– Taxation of NRA’s non-qualifying grant

Degree vs. non-degree candidates Compensation for services under a grant is Payroll Qualified Employee Educational Assistance

– Qualified fee or tuition reduction—graduate students– General Educational Assistance—$5,250 annual limit– Educational assistance related to current job:

• reimburse as employee business expense

Accounting Manual: http://policy.ucop.edu/manuals/accounting-manual.htmlChapter T-182-77

4251

04/19/23 44

Federal Taxation of Aliens

Chapter discusses issues relevant to both payroll and non-payroll payments

Residency rules, definitions, calculations Terms and conditions of nonresident visas Withholding and reporting obligations See Exhibits and Appendices

Accounting Manual: http://policy.ucop.edu/manuals/accounting-manual.html

Chapter T-182-27

4251

04/19/23 45

Nonresident Alien Issues

Honoraria and/or Associated Incidental Expenses associated with “usual academic activity”:

Restrictions on such payments to B-1, B-2, WB, and WT visas holders:– Cannot exceed nine days at a single institution– Cannot have accepted honoraria from more than five

institutions in the previous six months Exception—no restrictions apply to travel

reimbursements for B-1, WB visa holders as long as associated with “usual academic activity”.

4251

04/19/23 46

Nonresident Alien Issues

UC system now uses GLACIER online software for documenting nonresident alien visitorsDifferent rules, procedures, and US TINs

–Employees: must apply for SSNs–Students: must apply for ITIN if not employed –Visitors: often subjected to withholding if no US TIN

Information at Business & Financial Services web page: http://www.bfs.ucsb.edu/accounts-payable/non-resident-alien-information

Procedures for international graduate students–OISS: http://oiss.sa.ucsb.edu/Home/OISSForms.aspx

–Graduate Division: http://www.graddiv.ucsb.edu/financial/tax-information.aspx

4251

04/19/23 47

Tax Treatment ofMoving Expenses

Moving expenses are excludable from income if they meet all three requirements:– Related to the start of work, i.e. in connection with

commencement of work and incurred within 1 year – Distance test - new job location must be at least 50 miles

farther than former principal job location – Time test - must be employed full time for at least 39

weeks in 12 month period immediately following the move

Business and Finance Bulletin: http://policy.ucop.edu/doc/3420347/BFB-G-13

4251

04/19/23 48

Nontaxable Moving Expenses

Cost of moving household goods

Expenses incurred in traveling from former residence to new residence (excluding meals)

See pink handout

4251

04/19/23 49

Taxable Moving Expenses

Examples (see pink handout):– Meals, lodging, expenses for pre-move house

hunting trips– Meal reimbursements during travel from former

residence to work location – Temporary lodging and meals at work location– Mileage reimbursement in excess of 24.0

cents/mile as of 1/1/2013

Business & Finance Bulletin: http://policy.ucop.edu/doc/3420365/BFB-G-28Appendix A

4251

04/19/23 50

Tax Treatment of Some Travel Expenses

Timely Claiming Expenses and Clearing Advances:

– Failure by the employee to substantiate expenses and return any unused advances within 60 days after the completion of a trip obligates the University, under IRS regulations, to consider the unsubstantiated amounts as income to the employee

– At 120 days unsubstantiated expenses/advances are transferred to payroll as part of the employee’s income

Business & Finance Bulletin: http://policy.ucop.edu/doc/3420365/BFB-G-28

4251

04/19/23 51

Tax Treatment of Some Travel Expenses

Claiming expenses—missing receipts: When receipts are required but cannot be obtained or have been lost, the reimburse-ment of these expenses may be taxable

Business & Finance Bulletins: G-28, Policy and Regulations Governing Travelhttp://policy.ucop.edu/doc/3420365/BFB-G-28

4251

04/19/23 52

Travel Subsistence: Indefinite assignments that exceed one year

Under the IRS rules, travel away from home that lasts more than one year in a single location is considered indefinite:– Any travel expenses reimbursed during that period

must be treated as taxable income, subject to withholding of income and social security taxes

Business & Finance Bulletin: http://policy.ucop.edu/doc/3420365/BFB-G-28

4251

04/19/23 53

Travel—Special Situations

Inbound travelers* hired by UCSB for temporary assignments that do not exceed one year are considered nontaxable expense

Inbound travel assignments that exceed one year are taxable and require exception approval

Business & Finance Bulletin: http://policy.ucop.edu/doc/3420365/BFB-G-28

*Includes employees, independent contractors, and consultants at UCSB

4251

04/19/23 54

Travel Status vs. Residency

Employees who reside outside the SB area (for example Bay Area)– If they travel to Santa Barbara, the reimburse-

ment for travel expenses is taxable– If the University asked you to work on a project

outside SB, then those reimbursable expenses are not taxable

Business & Finance Bulletin: http://policy.ucop.edu/doc/3420365/BFB-G-28

4251

04/19/23 55

Recruitment Travel

On the first visit to campus:

– If a candidate’s spouse is given approval to travel to UCSB, the spouse’s expenses will be considered taxable income

– If the spouse has a valid business purpose there is no tax issue

Business & Finance Bulletin: http://policy.ucop.edu/doc/3420365/BFB-G-28

4251

04/19/23 56

Taxable Moving Expenses

Scenario #3A professor moves from New York to Santa Barbara. He submits a travel voucher for the following expenses:

- Private Car mileage: 3000 miles at 56.5* cents/mile (an approved Exception)- All lodging and meals for family (spouse and child) en-route- Temporary meals and lodging in SB for 5 days (Approved Exception)

Which expenses are taxable?* as of 4/17/2012

4251

04/19/23 57

Tax Issues – In General

Be aware of tax implications of various payments

Anticipate tax issues in contracts, agreements, and invitations

Don’t wait for the issue to come up when processing payment requests

Call Asger Pedersen, x3919

4251

04/19/23 58

UC Tax Issues

Office of the ControllerFinancial Management Certificate Program

Questions?