Embed Size (px)

DESCRIPTION

Laid out by request of UP Junior Philippine Institute of Accountants (JPIA), SY 1314

Citation preview

THE

UNIVERSITY FINANCIAL

TRANSPARENCY REPORTING STANDARDS

UNIVERSITY STUDENT COUNCIL

in partnership with

THE LEAGUE OF COLLEGE COUNCILS

and

UP JUNIOR PHILIPPINE INSTITUTE OF ACCOUNTANTS

Towards Further Transparency

The University Student Council of the University of the Philippines in Diliman, Quezon City is the official student representative body of the Philippines’ premiere institution of higher learning. As such, it represents the interests of the students within and outside the University. The University Student Council, also known as USC, exists to represent UP students in various affairs of the University, acting as the voice of students in the local, national, and international issues.

As the highest student representative body in the university, the USC is composed of members elected amongst the student body, mandated to organize and direct campaigns and activities to defend and promote students’ rights, and improve the students’ general welfare.

Furthermore, it provides direct services to the student body. The USC has the proud and historic tradition of active involvement in the Filipino people’s struggle for their democratic rights and interests.

The UNIVERSITY STUDENT COUNCIL

The League of College Councils (LCC) is the alliance of all local councils in the University of the Philippines, Diliman.

Utilizing the strong potential of a united League of College Councils, the LCC of the Academic Year 2013 – 2014 shall serve as an avenue to forward concrete and sustainable actions to all challenges that hinder genuine development in the education sector and the whole of society. The LCC shall be a bastion of the current student movement that will push for maximum student participation by mainstreaming all possible means to integrate the Iskolar ng Bayan in the challenge of serving the nation.

The LEAGUE OF COLLEGE COUNCILS

The UP Junior Philippine Institute of Accountants (UP JPIA) is the premier Business Administration & Accountancy students’ organization in the Cesar E.A. Virata School of Business in UP Diliman.

Established in 1958, UP JPIA was created for the prime purpose of serving as a medium of expression of the ideals and aspirations of current and former Accountancy students of the University, aimed at creating an atmosphere highly conducive to their moral, social and intellectual development.

Through the years, UP JPIA has built a tradition of excellence, having been recognized as one of the most outstanding organizations in the University and in Quezon City – a three-time winner of the Gawad Chancellor Award for Most Outstanding Organization and the first and only Gawad Chancellor Hall of Fame Awardee in the university, a national finalist in the Ten Accomplished Youth Organizations (TAYO) and a recipient of the Quezon City Youth Achiever’s Award.

Today, UP JPIA continues to provide its members with dynamic opportunities to grow and excel through innovative projects that are relevant to the members, the University and society.

UP JUNIOR PHILIPPINE ASSOCIATION OF ACCOUNTANTS

As mandated by the USC Constitution:

“SEC. 4The Treasurer shall -(d) Submit a financial report at the end of each semester to the Council, which shall be published in the Philippine Collegian;”

The University Student Council (USC), in partnership with the League of College Councils (LCC) and through the expertise provided by the UP Junior Philippine Institute of Accountants (UP JPIA), under the tagline “Responsive and Responsible Finance: Translating Principles into Practice”, has launched the campaign entitled CRAFT: Councils for Responsible Accounting and Financial Transparency.

Spearheaded by the USC Finance Committee, with key proponent Mr. Aaron Letaba, the USC Treasurer, CRAFT will aim to ensure further transparency and accountability in the council’s finances. By implementing a series of seminars for local colleges’ finance councilors, and communicating pronounced rules in creating the local college council’s

financial reporting, CRAFT has the following success metrics:

Coordinated release of relevant and faithfully represented financial statements of all local college councils

Implementation of efficient financial systems for managing internal controls and financial planning

Standardization of financial recording and reporting procedures that will establish transparent and accountable student councils and governments

Implementation of the project covers the whole academic year of 2013-2014, and institutionalization is sought thereafter.

PURPOSE

TABLE ofCONTENTS

5

19

3338

Module 1: Documentation of Transactions

Recording of Cash receiptsRecording of Cash disbursements

Module 2: Statement of Cash Flows

Chart of AccountsStatement of Cash FlowsDisclosureNotes to Financial Statements

Module 3: Internal Control Procedures

Glossary of Terms

DOCUMENTATION OF TRANSACTIONSMODULE 1DOCUMENTATION OF

TRANSACTIONS

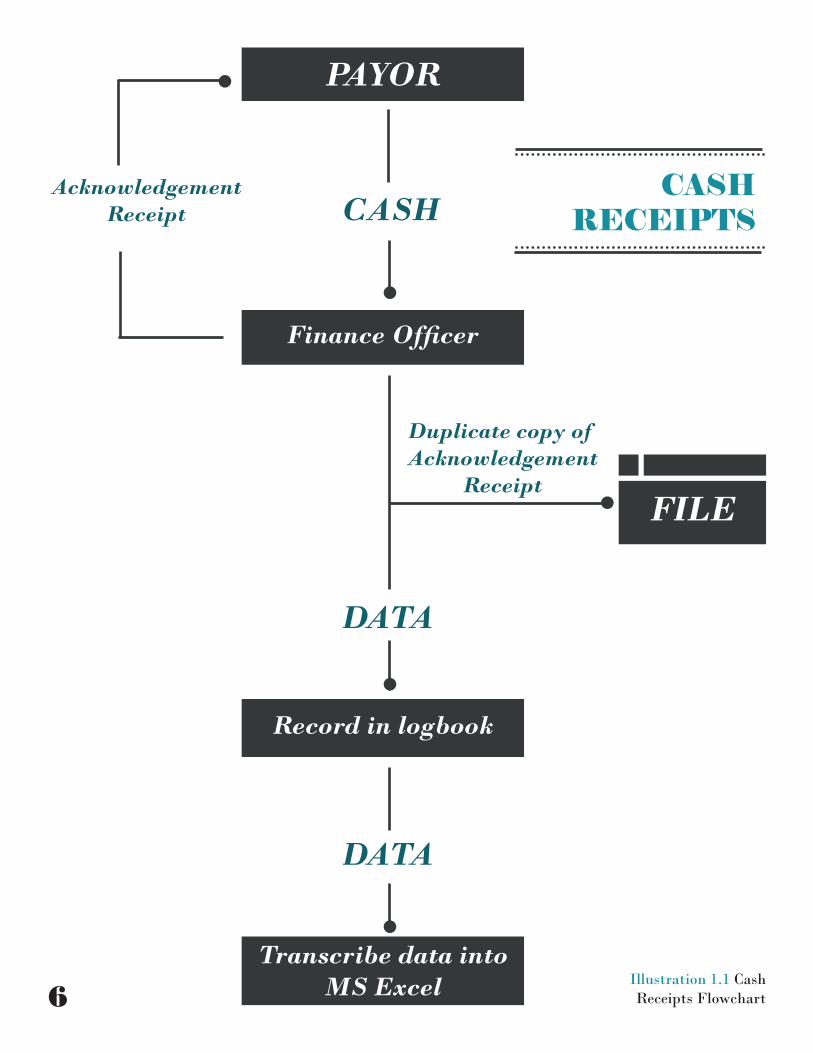

Recording of Cash Receipts

1. Issuance of an Acknowledgment Receipt.

Upon receipt of cash, the finance officer (payee) issues an acknowledgement receipt to the payer. A duplicate copy of the acknowledgement receipt is kept by the finance officer for his/her own record. The said forms shall be pre-numbered and should include the following details: a.) the amount of the cash received, b.) the name of the payer, c.) the source and nature of cash, d.) the date of the transaction, and e.) the name and signature of the finance officer.

2. Recording in the logbook.

Using the duplicate copy of the acknowledgement receipt, the Finance officer thereafter records the transaction in a logbook. The logbook may take the form of a journal or a notebook. Similar to the acknowledgment receipts, the pages of the logbook shall also be pre-numbered. Each page should be signed by the council chairperson to verify that they were pre-numbered. Details to be recorded in the logbook are as follows: a.) the source of cash, b.) the amount received, c.) the date of the transaction, d.) the name and signature of the payer, e.) acknowledgement receipt number and f.) the signature of the Finance officer.

3. Transfer of data from logbook into Excel records.

Information recorded in the logbook is then transferred to a Microsoft Excel worksheet. The worksheet shall contain the same fields as the logbook. The frequency of the transfer of data is left to the discretion of the Finance officer. In determining when to transcribe data into the worksheet factors such as volume of transactions and amount of money received shall be taken into account.

Responsibility for Documentation

The documentation of the local college council’s transactions shall be the sole responsibility of the finance officer.

5

MODULE 1

PAYOR

FILE

Transcribe data into MS Excel

Record in logbook

Finance Officer

CASHAcknowledgement

Receipt

DATA

Duplicate copy of Acknowledgement

Receipt

DATA

Illustration 1.1 Cash Receipts Flowchart

CASH RECEIPTS

6

DOCUMENTATION OF TRANSACTIONS

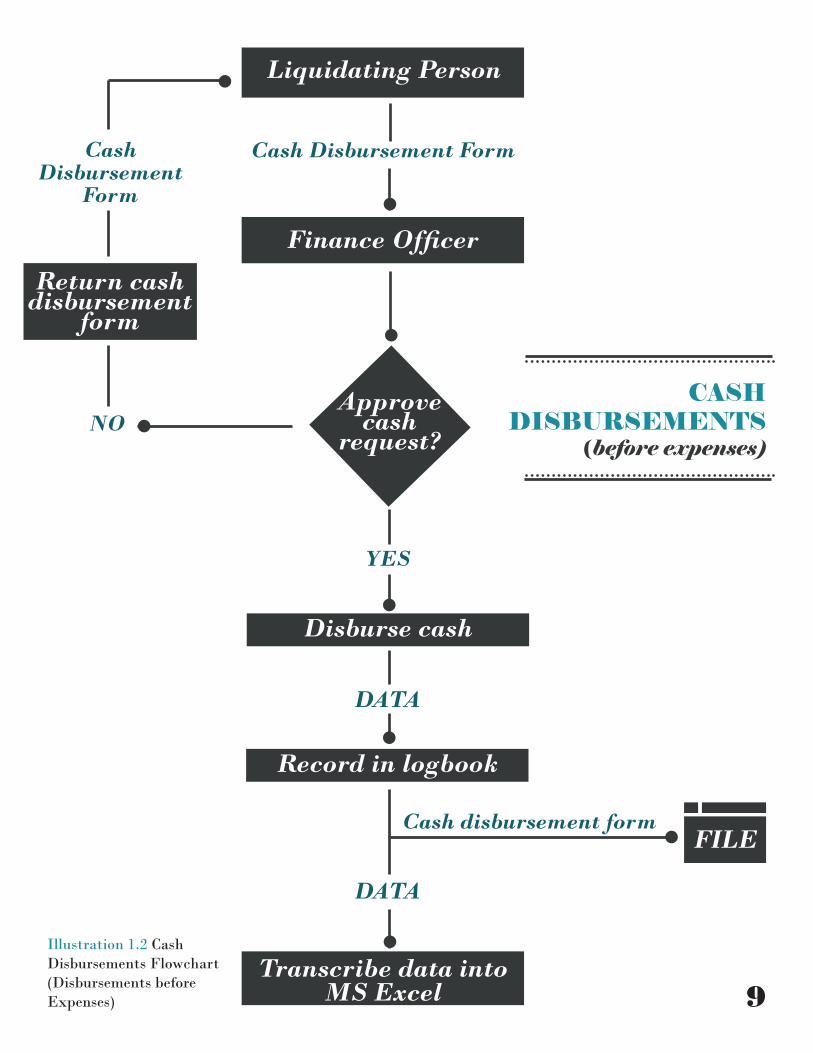

Recording of Cash Disbursements

This section of the documentation module is divided into two parts. The first part applies to transactions wherein disbursements are made before the expenses are incurred or capital request. On the other hand, the second pertains to transactions wherein expenses are made first before the disbursements or reimbursement.

Capital Request

1. Submission of a Cash Disbursement form.

Before disbursement of funds, a cash disbursement form is filled out by the liquidating person. This form should include details such as a.) amount of the money requested, b.) purpose and/or nature of the expenses (includes projection of expenses if request is for a council project), c.) name of the person requesting cash,d.) date of the request and e.) amount disbursed. Only the first four items (a, b, c and d) are to be filled out by the liquidating person.

2. Recording of data in Cash Disbursement Logbook.

After receiving the cash disbursement form, the Finance officer records the information in the logbook. The logbook may take the form of a journal or a notebook. Similar to the acknowledgment receipts, the pages of the logbook shall also be pre-numbered. Each page should be signed by the council chairperson to verify that they were pre-numbered. Details to be recorded are as follows: a.) date of request, b.) date when disbursement was made, c.) nature and purpose of the expense, d.) name of the liquidating person and e.) projection of expenses. Item e (amount disbursed) is only to be filled out if the purpose of the disbursement requires a budget to be submitted. As an additional control, the logbook is also signed by liquidating person.

3. Transfer of data from logbook into Excel records.

Information recorded in the logbook is then transferred to a Microsoft Excel worksheet. The worksheet shall contain the same fields as the logbook. The frequency of the transfer of data is left to the discretion of the Finance officer. In determining when to transcribe data into the worksheet factors such as volume of transactions and amount of money disbursed shall be taken into account.

7

MODULE 1

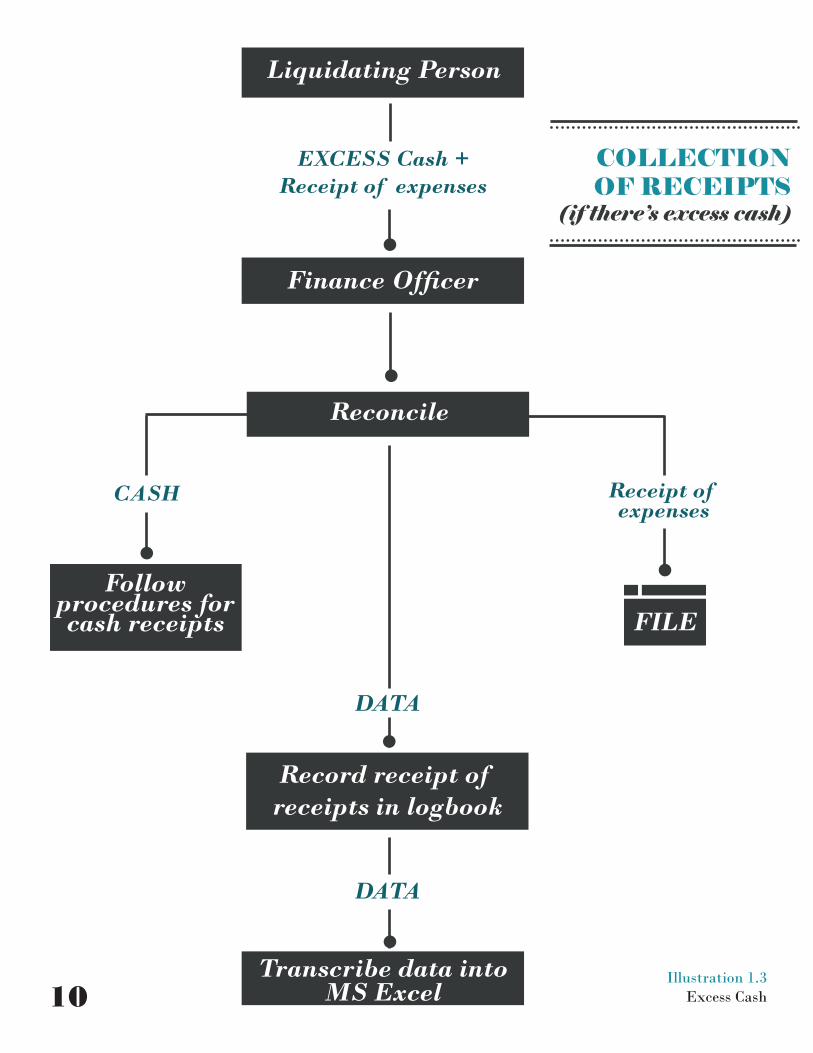

4. Collect all receipts.

After the actual expenses have been incurred, the Finance officer collects the receipts. He must note in the logbook that the receipt/s for a particular disbursement has/have been received. In addition the payee/liquidating person shall countersign to verify the submission of the receipt. The finance officer then reconciles the amount spent indicated in the receipts with the amount disbursed. The receipts are to be kept for audit purposes.

Upon collection of receipts, two possible scenarios might occur:

(a) Deficiency of Funds

If the money previously received/approved is inadequate for the expenses made (as evidenced by the receipts), the steps for reimbursement should be followed.

(b) Excess of Funds

If the money previously disbursed is greater than the amount of expenses made (as evidenced by the receipts), the liquidating person must return the excess money. The steps for cash receipts should be followed thereafter.

8

DOCUMENTATION OF TRANSACTIONSLiquidating Person

FILE

Transcribe data into MS Excel

Record in logbook

Finance Officer

Cash Disbursement Form

Cash disbursement form

DATA

Illustration 1.2 Cash Disbursements Flowchart (Disbursements before Expenses)

Approve cash

request?

Cash Disbursement

Form

NO

Return cash disbursement

form

DATA

YES

Disburse cash

CASH DISBURSEMENTS

(before expenses)

9

MODULE 1Liquidating Person

FILE

Transcribe data into MS Excel

Record receipt of receipts in logbook

Finance Officer

EXCESS Cash +Receipt of expenses

DATA

Illustration 1.3 Excess Cash

Reconcile

CASH

Follow procedures for cash receipts

DATA

COLLECTION OF RECEIPTS

(if there’s excess cash)

Receipt of expenses

10

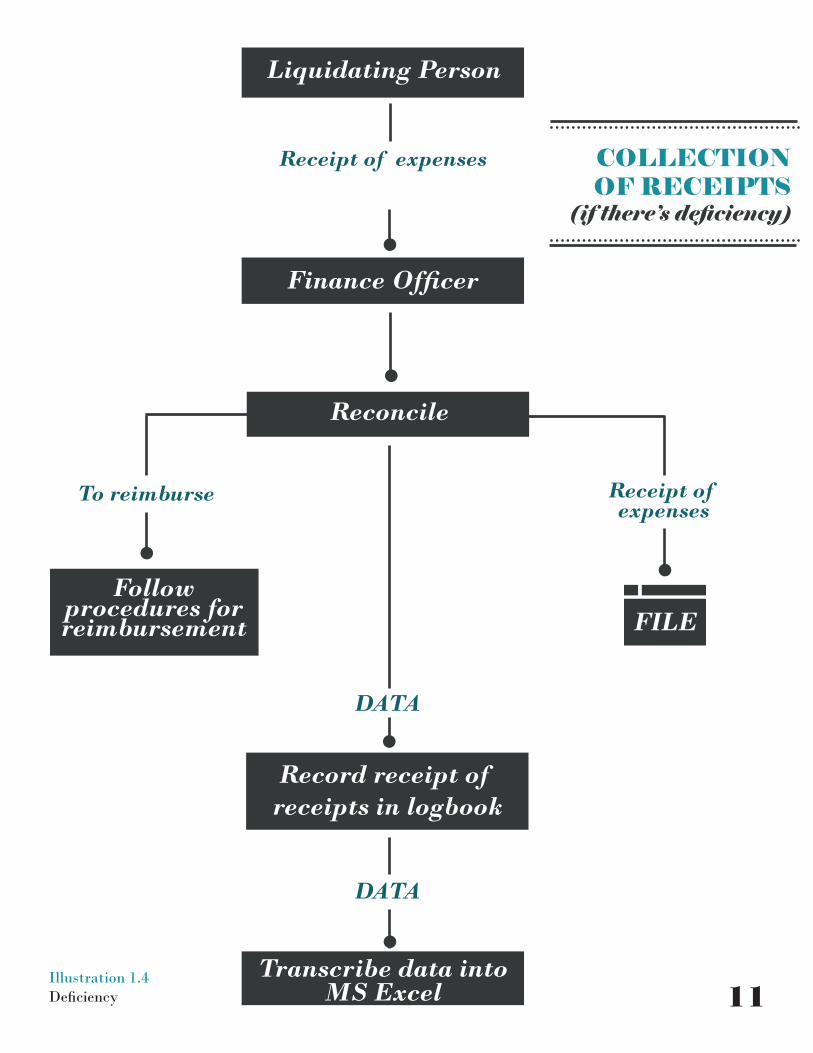

DOCUMENTATION OF TRANSACTIONSLiquidating Person

FILE

Transcribe data into MS Excel

Record receipt of receipts in logbook

Finance Officer

Receipt of expenses

DATA

Illustration 1.4 Deficiency

Reconcile

To reimburse

Follow procedures for reimbursement

DATA

COLLECTION OF RECEIPTS

(if there’s deficiency)

Receipt of expenses

11

MODULE 1

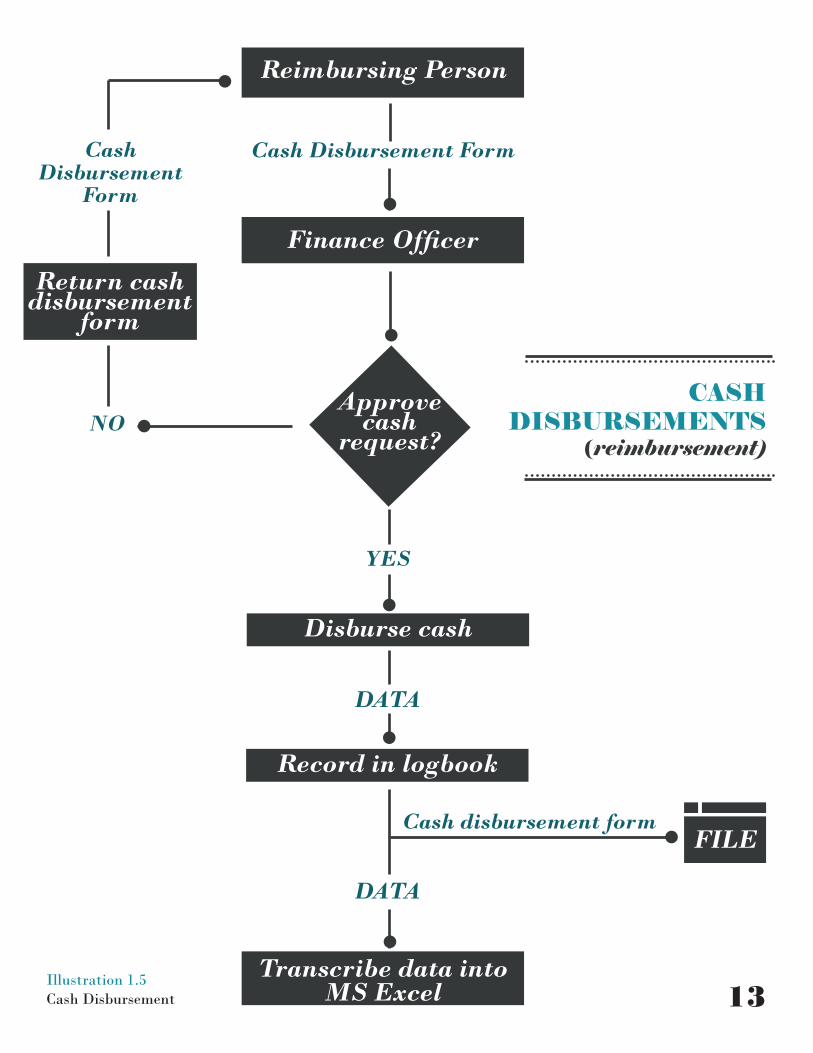

Expenses before Disbursements (Reimbursement)

1. Submission of Cash Disbursement form and Official Receipts.

The person requesting for reimbursement (liquidating person) accomplishes the cash disbursement form. A cash disbursement form shall be filled out by the liquidating person. This form should include details such as a.) amount of the money requested, b.) purpose and/or nature of the expenses (includes projection of expenses if request is for a council project), c.) name of the person requesting cash, d.) date of the request and e.) amount disbursed. Only the first four items (a, b, c and d) are to be filled out by the liquidating person.

2. Recording of data in Cash Disbursement Logbook.

After receiving the cash disbursement form, the Finance officer records the information in the logbook. The logbook may take the form of a journal or a notebook. Similar to the acknowledgment receipts, the pages of the logbook shall also be pre-numbered. Each page should be signed by the council chairperson to verify that they were pre-numbered. Details to be recorded are as follows: a.) date of request, b.) date when disbursement was made, c.) nature and purpose of the expense, d.) name of the liquidating person and e.) projection of expenses. Item e is only to be filled out if the purpose of the disbursement requires a budget to be submitted. As an additional control, the logbook shall also be signed by liquidating person.

3. Transcribe data from logbook into Excel.

Information recorded in the logbook is then transferred to a Microsoft Excel worksheet. The worksheet shall contain the same fields as the logbook. The frequency of the transfer of data is left to the discretion of the Finance officer. In determining when to transcribe data into the worksheet factors such as volume of transactions and amount of money disbursed shall be taken into account.

12

DOCUMENTATION OF TRANSACTIONSReimbursing Person

FILE

Transcribe data into MS Excel

Record in logbook

Finance Officer

Cash Disbursement Form

Cash disbursement form

DATA

Illustration 1.5 Cash Disbursement

Approve cash

request?

Cash Disbursement

Form

NO

Return cash disbursement

form

DATA

YES

Disburse cash

CASH DISBURSEMENTS

(reimbursement)

13

MODULE 1

Payer - MargauxFinance officer - Celine

Situation:

It is enrolment time once again. The super diligent student, Celine Buenaventura, will serve, for the very first time, as the finance officer of College of ABC. Due to her dedication and love for her college and co-UP students, she wants her work to be as organized as possible. She wants every transaction to reflect what really transpired. Then comes Margaux Marasigan. Margaux was taught during her childhood how to value money. For this reason, she’s very conscious about every centavo she spends that’s why she has this habit of asking for a receipt for every transaction, especially those involving high-amount of money.

To complete the validation process, Margaux needs to pay for the following:

Council fee - P300Locker fee - P100

Examples

A. CASH RECEIPT

14

DOCUMENTATION OF TRANSACTIONS

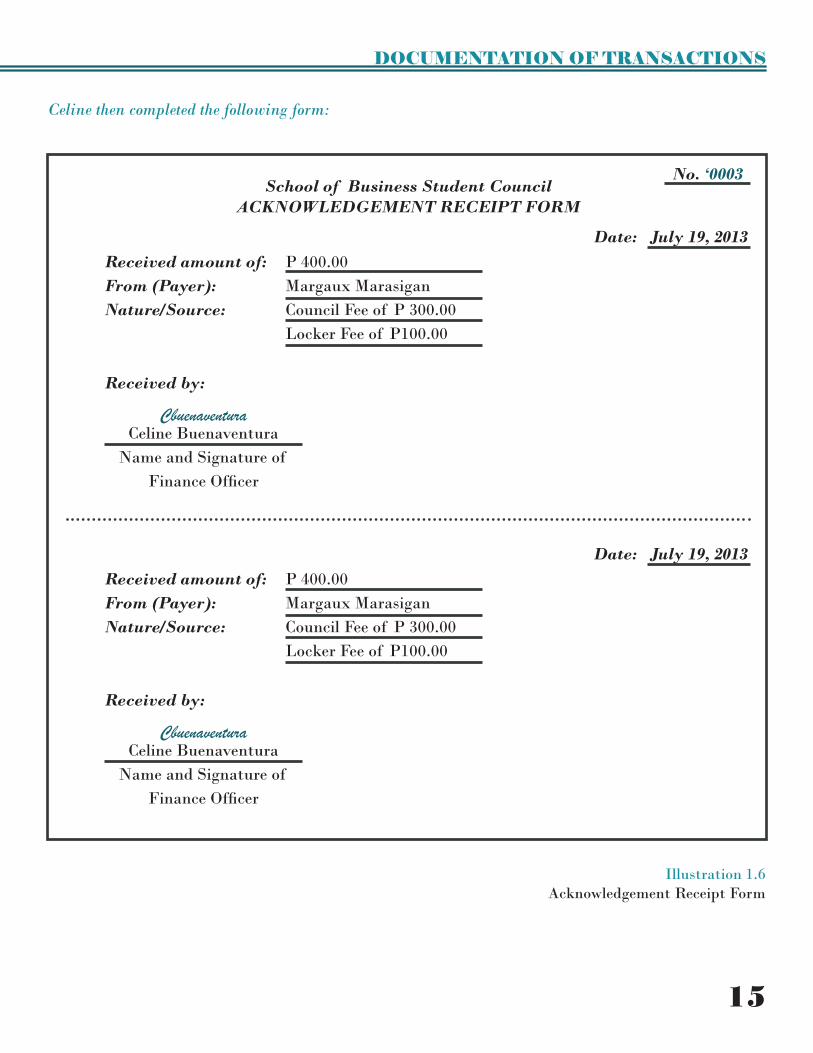

School of Business Student CouncilACKNOWLEDGEMENT RECEIPT FORM

No. ‘0003

Date: July 19, 2013Received amount of:From (Payer):Nature/Source:

P 400.00Margaux MarasiganCouncil Fee of P 300.00Locker Fee of P100.00

Received by:

Celine BuenaventuraName and Signature of

Finance Officer

Cbuenaventura

Date: July 19, 2013Received amount of:From (Payer):Nature/Source:

P 400.00Margaux MarasiganCouncil Fee of P 300.00Locker Fee of P100.00

Received by:

Celine BuenaventuraName and Signature of

Finance Officer

Cbuenaventura

Illustration 1.6 Acknowledgement Receipt Form

Celine then completed the following form:

15

MODULE 1

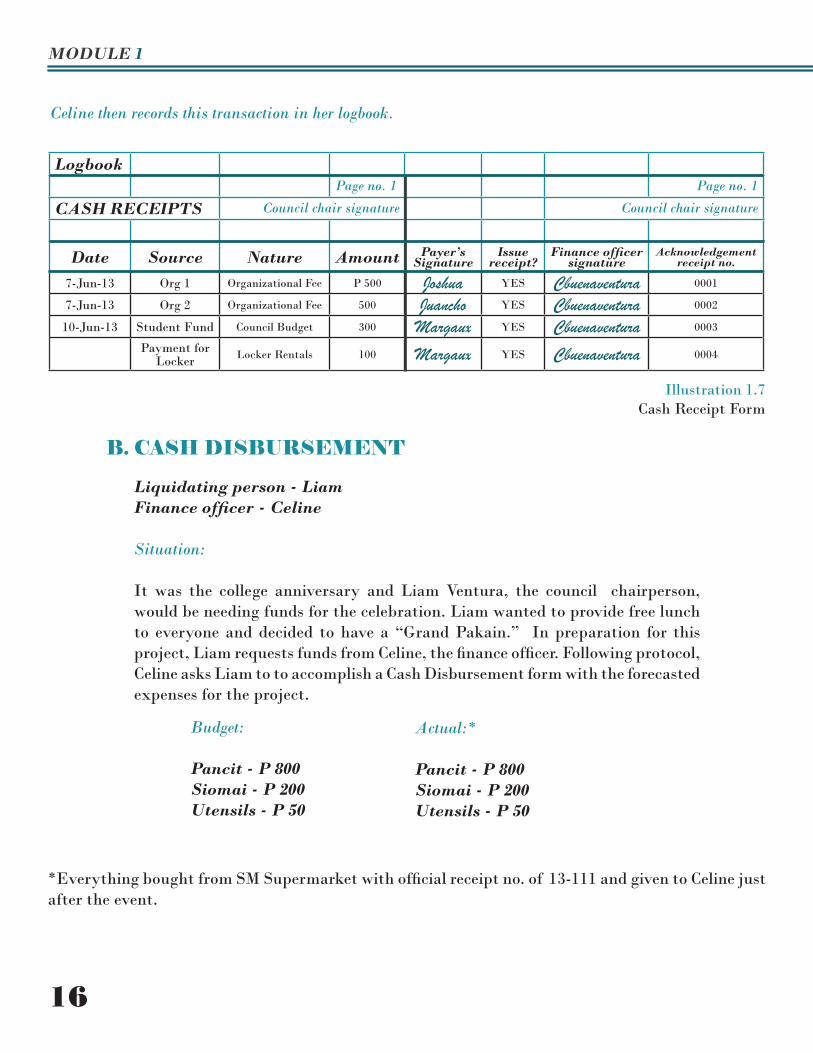

Celine then records this transaction in her logbook.

LogbookPage no. 1 Page no. 1

CASH RECEIPTS Council chair signature Council chair signature

Date Source Nature Amount Payer’s Signature

Issue receipt?

Finance officer signature

Acknowledgement receipt no.

7-Jun-13 Org 1 Organizational Fee P 500 Joshua YES Cbuenaventura 0001

7-Jun-13 Org 2 Organizational Fee 500 Juancho YES Cbuenaventura 0002

10-Jun-13 Student Fund Council Budget 300 Margaux YES Cbuenaventura 0003

Payment for Locker Locker Rentals 100 Margaux YES Cbuenaventura 0004

Illustration 1.7 Cash Receipt Form

Budget:

Pancit - P 800Siomai - P 200Utensils - P 50

Actual:*

Pancit - P 800Siomai - P 200Utensils - P 50

Liquidating person - LiamFinance officer - Celine

Situation:

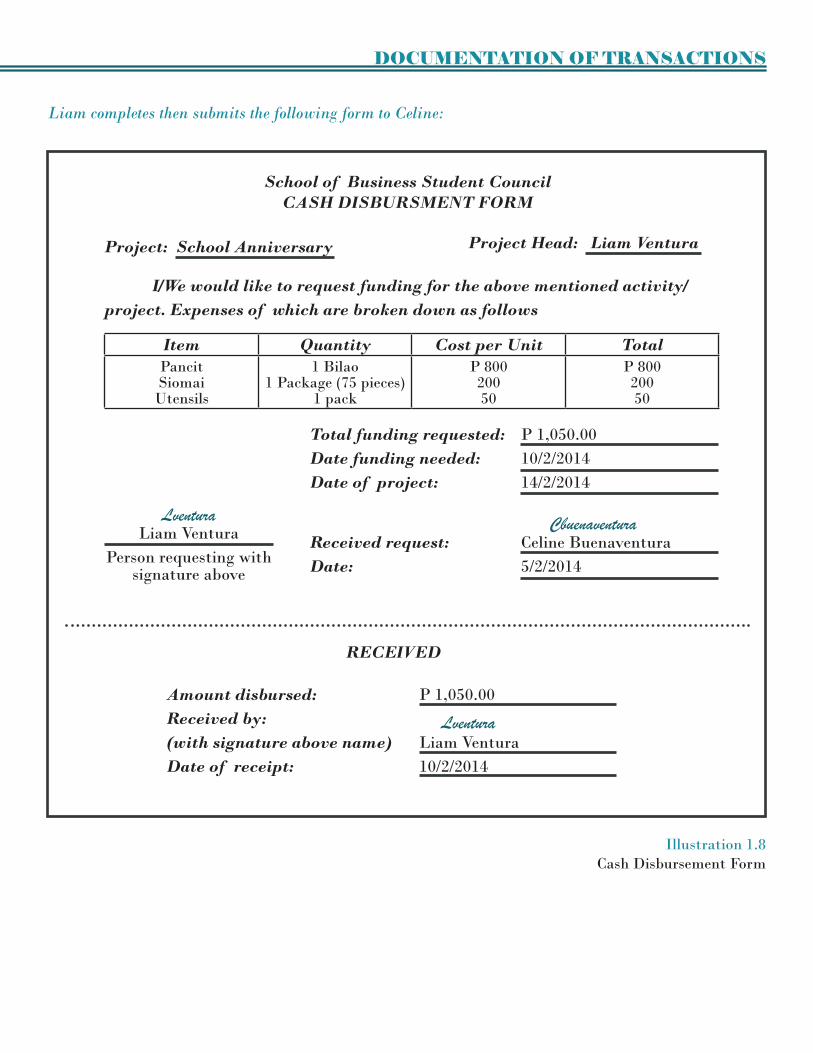

It was the college anniversary and Liam Ventura, the council chairperson, would be needing funds for the celebration. Liam wanted to provide free lunch to everyone and decided to have a “Grand Pakain.” In preparation for this project, Liam requests funds from Celine, the finance officer. Following protocol, Celine asks Liam to to accomplish a Cash Disbursement form with the forecasted expenses for the project.

B. CASH DISBURSEMENT

*Everything bought from SM Supermarket with official receipt no. of 13-111 and given to Celine just after the event.

16

DOCUMENTATION OF TRANSACTIONS

School of Business Student CouncilCASH DISBURSMENT FORM

Project Head: Liam Ventura

I/We would like to request funding for the above mentioned activity/project. Expenses of which are broken down as follows

Liam VenturaPerson requesting with

signature above

Lventura

Project: School Anniversary

Item Quantity Cost per Unit TotalPancitSiomai

Utensils

1 Bilao1 Package (75 pieces)

1 pack

P 80020050

P 80020050

Total funding requested:Date funding needed:Date of project:

P 1,050.0010/2/201414/2/2014

Received request:Date:

Celine Buenaventura5/2/2014

Cbuenaventura

Illustration 1.8 Cash Disbursement Form

RECEIVED

Amount disbursed:Received by: (with signature above name)Date of receipt:

P 1,050.00

Liam Ventura10/2/2014

Lventura

Liam completes then submits the following form to Celine:

MODULE 1

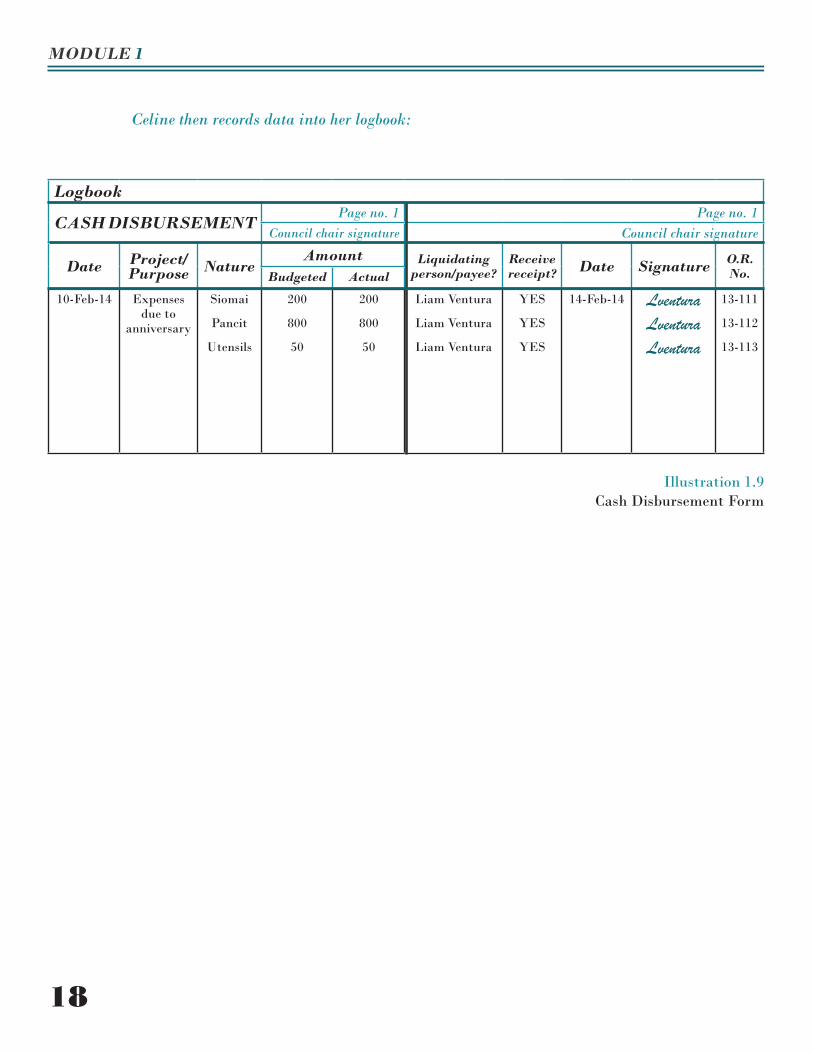

Logbook

CASH DISBURSEMENTPage no. 1 Page no. 1

Council chair signature Council chair signature

Date Project/Purpose Nature

Amount Liquidating person/payee?

Receive receipt? Date Signature O.R.

No.Budgeted Actual

10-Feb-14 Expenses due to

anniversary

Siomai

Pancit

Utensils

200

800

50

200

800

50

Liam Ventura

Liam Ventura

Liam Ventura

YES

YES

YES

14-Feb-14 Lventura Lventura Lventura

13-111

13-112

13-113

Celine then records data into her logbook:

Illustration 1.9 Cash Disbursement Form

18

DOCUMENTATION OF TRANSACTIONSMODULE 2STATEMENT OF

CASH FLOWSStatement of Cash Flows

A. Introduction

1. Purpose of the Statement of Cash Flows

Transparency and Accountability

It is imperative that all foregoing transactions undertaken by any council or body representative of the studentry should keep, at the minimum, a reliable recordkeeping of financial information for the semester and the whole academic year. Such task primarily falls upon the finance councilor (or its equivalent) of every council. Proper recording and relay of financial information to the student population enhances the students’ confidence with their respective council managements, and generates a sense of credibility in their offices.

Additionally, an annexation of the Statement of Finance Councilor’s accountability accompanied with an affirmation of the Council Chair to the Financial Statements furthers the accountability of the council officials lest they misrepresent the information, whether intentionally or inadvertently.

Standardization

In line with the transparency and accountability purpose, standardization is being seen as a means to further enhance the reliability of the Statement of Cash Flows. By implementing uniform mechanisms and procedures applicable to all the councils within the university, there will be a heightened comparability between entities, allowing end users to easily compare the financial performance between colleges. This will also enable an easy identification of unusual deviations in the Statements, as well as finding the uniqueness of each transaction respective to the nature of a college’s operations.

19

MODULE 2

Sound Financial Management

Transparency, accountability, and standardization of the Statements generally relate only to the form and manner that the financial information is handled; managing such finances efficiently and effectively, to the best interests of the students, is another. Thus, another purpose of generating the Financial Statements for the college councils is to make sure that all cash and other assets involved are used in the most worthwhile way possible, setting wastage of funds to a minimum. An introduction for cash budgeting and financial tracking will be annexed to this module as well, for the attainment of this purpose.

Notes: Financial reporting contemplated herein refers to simplified accounting procedures and is independent from the pronouncements of other accounting standard-setting bodies. UP JPIA reserves the right to implement unique accounting standards for the college councils of the University of The Philippines – Diliman , so as to fully achieve practicality and feasibility for all its stakeholders.

20

STATEMENT OF CASH FLOWS

P 500.00 1,050.00 9,000.00 P (10,550.00)

100.00 150.00 (250.00)

500.00 700.00 1,200.00

P (12,000.00) 30,000.00 5,000.00 35,000.00

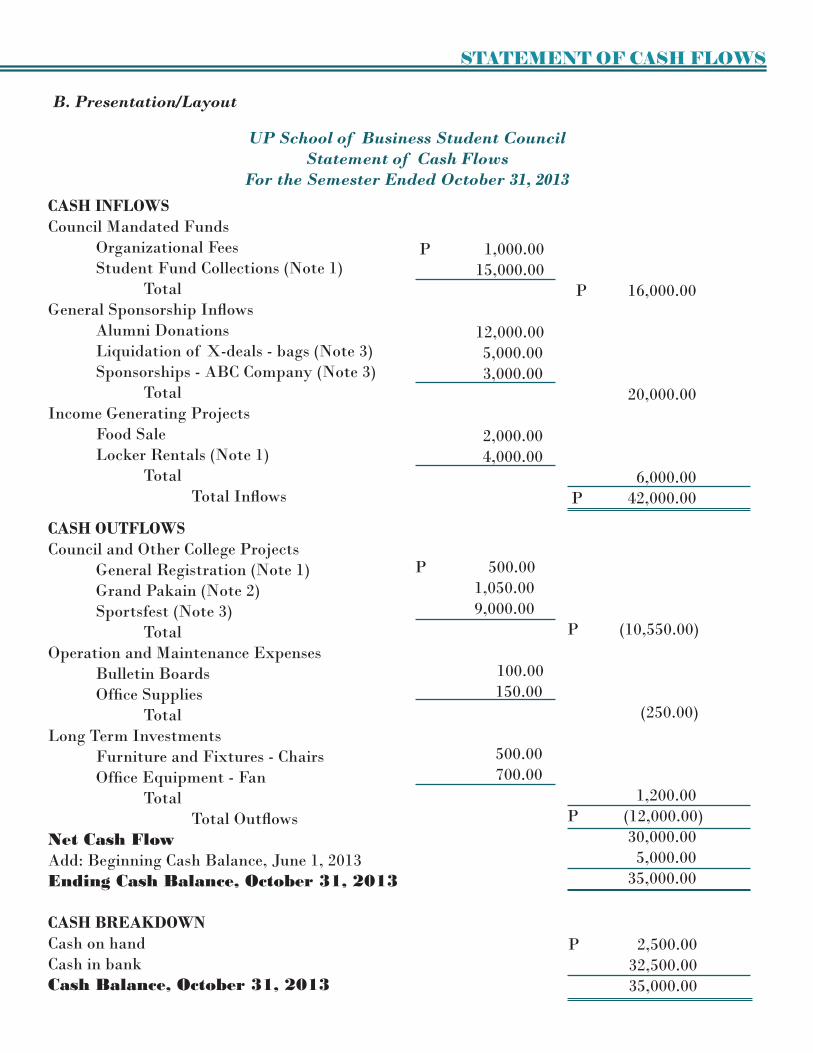

B. Presentation/Layout

UP School of Business Student CouncilStatement of Cash Flows

For the Semester Ended October 31, 2013

CASH INFLOWSCouncil Mandated Funds

Organizational FeesStudent Fund Collections (Note 1) Total

General Sponsorship InflowsAlumni Donations Liquidation of X-deals - bags (Note 3)Sponsorships - ABC Company (Note 3) Total

Income Generating ProjectsFood Sale Locker Rentals (Note 1) Total Total Inflows

CASH OUTFLOWSCouncil and Other College Projects

General Registration (Note 1)Grand Pakain (Note 2)Sportsfest (Note 3) Total

Operation and Maintenance ExpensesBulletin Boards Office Supplies Total

Long Term Investments Furniture and Fixtures - ChairsOffice Equipment - Fan Total Total Outflows

Net Cash Flow Add: Beginning Cash Balance, June 1, 2013Ending Cash Balance, October 31, 2013

CASH BREAKDOWNCash on hand Cash in bank Cash Balance, October 31, 2013

P 1,000.00 15,000.00

P 16,000.00

12,000.00 5,000.00 3,000.00 20,000.00

2,000.00 4,000.00 6,000.00

P 42,000.00

P 2,500.00 32,500.00 35,000.00

MODULE 2

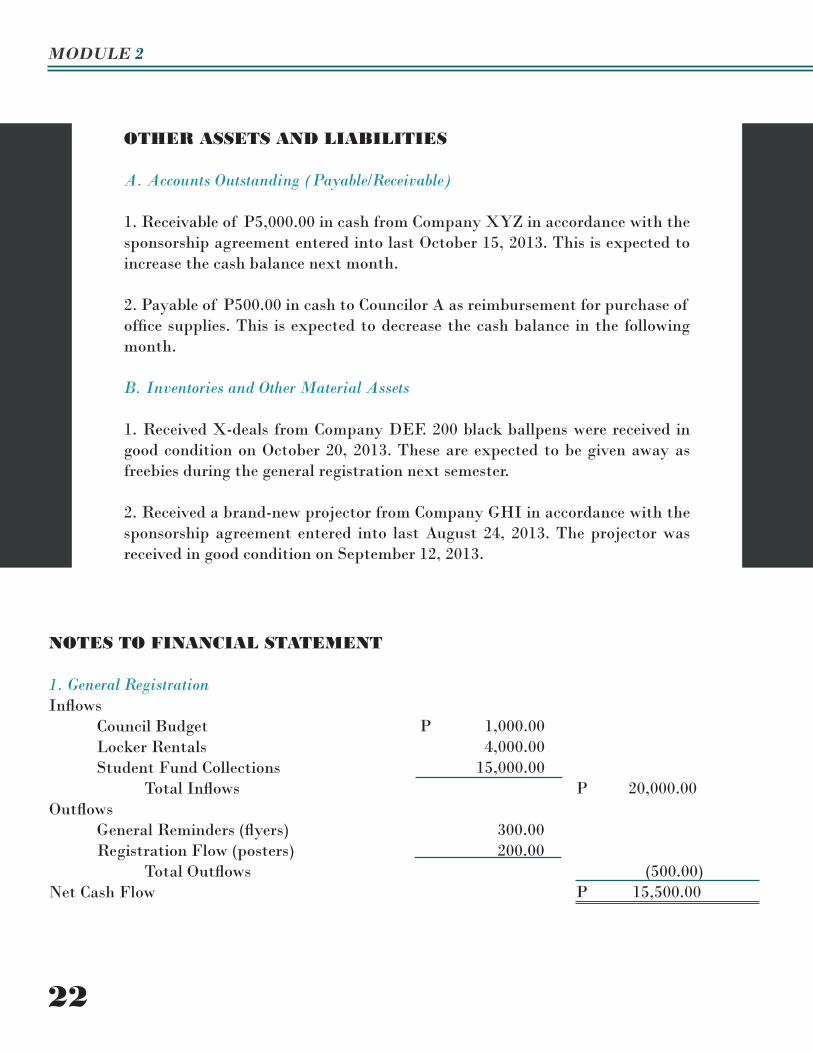

OTHER ASSETS AND LIABILITIES

A. Accounts Outstanding (Payable/Receivable)

1. Receivable of P5,000.00 in cash from Company XYZ in accordance with the sponsorship agreement entered into last October 15, 2013. This is expected to increase the cash balance next month.

2. Payable of P500.00 in cash to Councilor A as reimbursement for purchase of office supplies. This is expected to decrease the cash balance in the following month.

B. Inventories and Other Material Assets

1. Received X-deals from Company DEF. 200 black ballpens were received in good condition on October 20, 2013. These are expected to be given away as freebies during the general registration next semester. 2. Received a brand-new projector from Company GHI in accordance with the sponsorship agreement entered into last August 24, 2013. The projector was received in good condition on September 12, 2013.

NOTES TO FINANCIAL STATEMENT

1. General RegistrationInflows Council Budget Locker Rentals Student Fund Collections Total InflowsOutflows General Reminders (flyers) Registration Flow (posters) Total OutflowsNet Cash Flow

P 1,000.00 4,000.00 15,000.00

P 20,000.00

300.00 200.00 (500.00)

P 15,500.00

22

STATEMENT OF CASH FLOWS

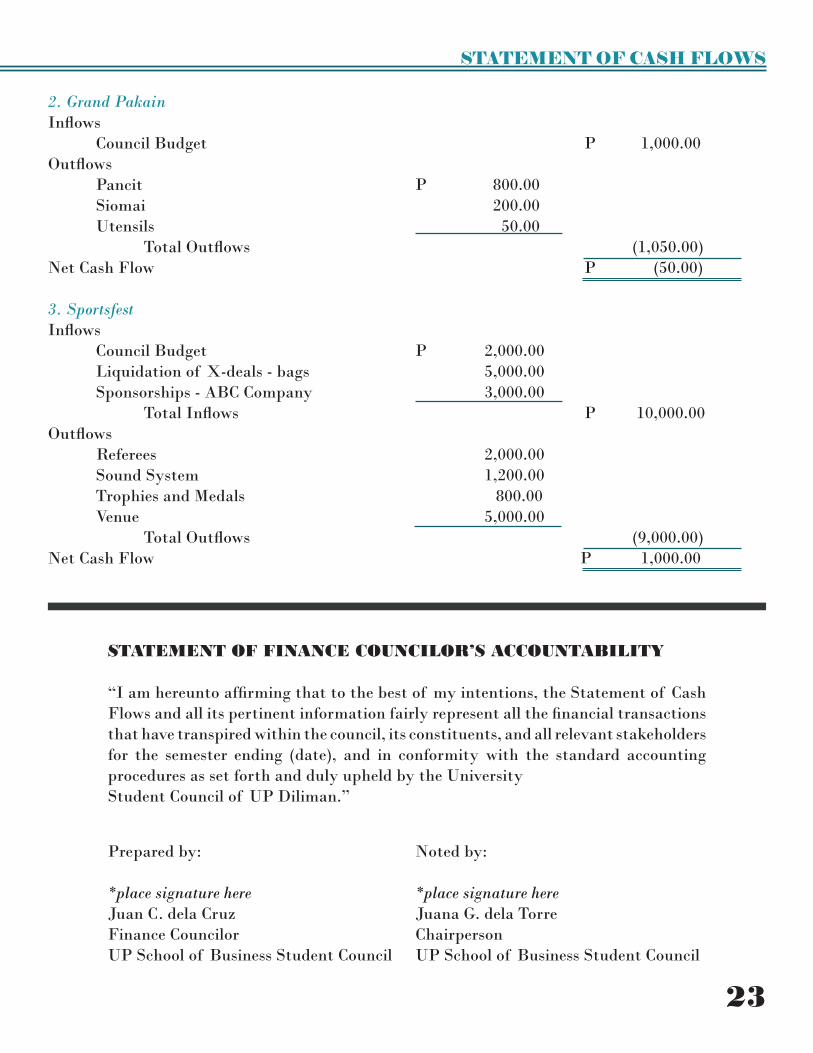

2. Grand PakainInflows Council BudgetOutflows Pancit Siomai Utensils Total OutflowsNet Cash Flow

3. SportsfestInflows Council Budget Liquidation of X-deals - bags Sponsorships - ABC Company Total InflowsOutflows Referees Sound System Trophies and Medals Venue Total OutflowsNet Cash Flow

P 1,000.00

P 800.00 200.00 50.00 (1,050.00)

P (50.00)

P 2,000.00 5,000.00 3,000.00 P 10,000.00 2,000.00 1,200.00 800.00 5,000.00 (9,000.00) P 1,000.00

STATEMENT OF FINANCE COUNCILOR’S ACCOUNTABILITY

“I am hereunto affirming that to the best of my intentions, the Statement of Cash Flows and all its pertinent information fairly represent all the financial transactions that have transpired within the council, its constituents, and all relevant stakeholders for the semester ending (date), and in conformity with the standard accounting procedures as set forth and duly upheld by the University Student Council of UP Diliman.”

Prepared by: *place signature here Juan C. dela Cruz Finance Councilor UP School of Business Student Council

Noted by: *place signature here Juana G. dela Torre Chairperson UP School of Business Student Council

23

MODULE 2

C. Parts

1. Title/Heading

This includes the name of the council, the name of the financial statement and the period covered by the financial statement.

Name of CouncilStatement of Cash Flows

For the Semester Ended Month XX, 20XX

Example:

UP School of Business Student CouncilStatement of Cash Flows

For the Semester Ended October 31, 2013

2. Cash Inflows

These include all inflows discussed in the previous section, alphabetically arranged under the following categories: 1. Council Mandated Funds 2. General Sponsorship Inflows 3. Income Generating Projects 4. Other Income

Example:

CASH INFLOWS

Council Mandated FundsOrganizational FeesStudent Fund Collections (Note 1) Total

General Sponsorship InflowsAlumni Donations Liquidation of X-deals - bags (Note 3)Sponsorships - ABC Company (Note 3) Total

Income Generating ProjectsFood Sale Locker Rentals (Note 1) Total Total Inflows

P 1,000.00 15,000.00

P 16,000.00

12,000.00 5,000.00 3,000.00 20,000.00

2,000.00 4,000.00 6,000.00

P 42,000.0024

STATEMENT OF CASH FLOWS

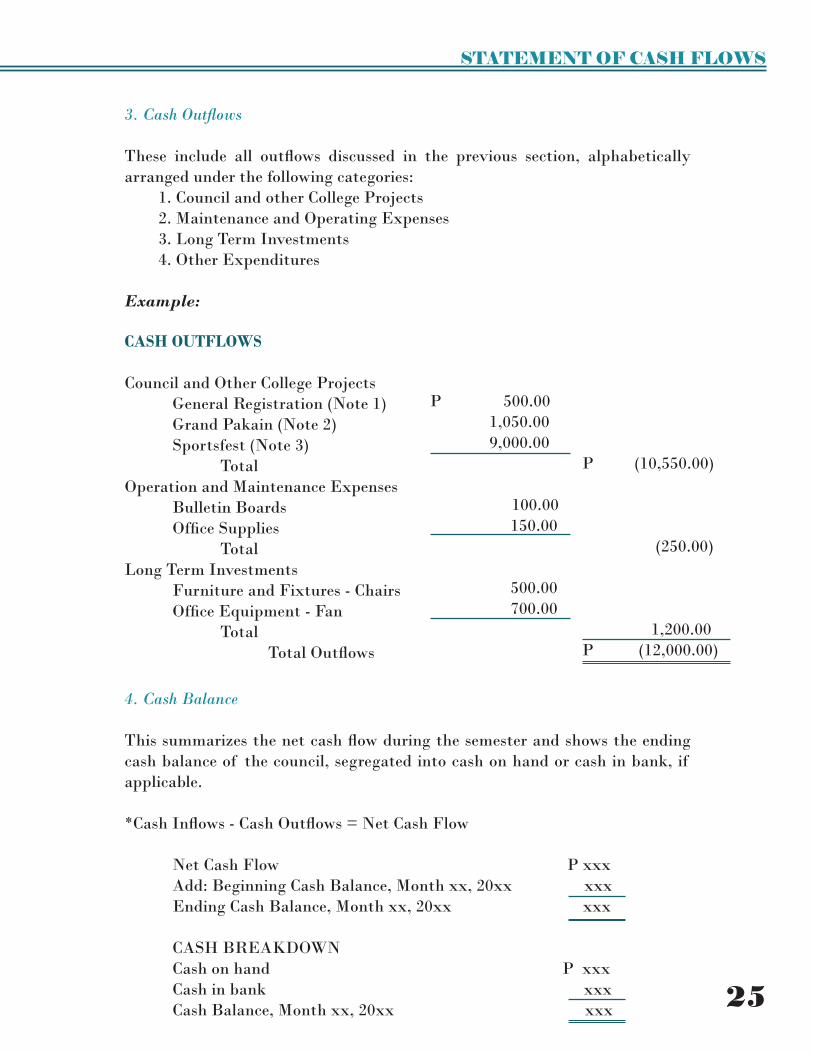

3. Cash Outflows

These include all outflows discussed in the previous section, alphabetically arranged under the following categories: 1. Council and other College Projects 2. Maintenance and Operating Expenses 3. Long Term Investments 4. Other Expenditures

Example:

CASH OUTFLOWS

Council and Other College ProjectsGeneral Registration (Note 1)Grand Pakain (Note 2)Sportsfest (Note 3) Total

Operation and Maintenance ExpensesBulletin Boards Office Supplies Total

Long Term Investments Furniture and Fixtures - ChairsOffice Equipment - Fan Total Total Outflows

P 500.00 1,050.00 9,000.00 P (10,550.00)

100.00 150.00 (250.00)

500.00 700.00 1,200.00

P (12,000.00)

4. Cash Balance

This summarizes the net cash flow during the semester and shows the ending cash balance of the council, segregated into cash on hand or cash in bank, if applicable. *Cash Inflows - Cash Outflows = Net Cash Flow

Net Cash Flow P xxxAdd: Beginning Cash Balance, Month xx, 20xx xxxEnding Cash Balance, Month xx, 20xx xxx CASH BREAKDOWNCash on hand P xxxCash in bank xxxCash Balance, Month xx, 20xx xxx

25

MODULE 2

Example:

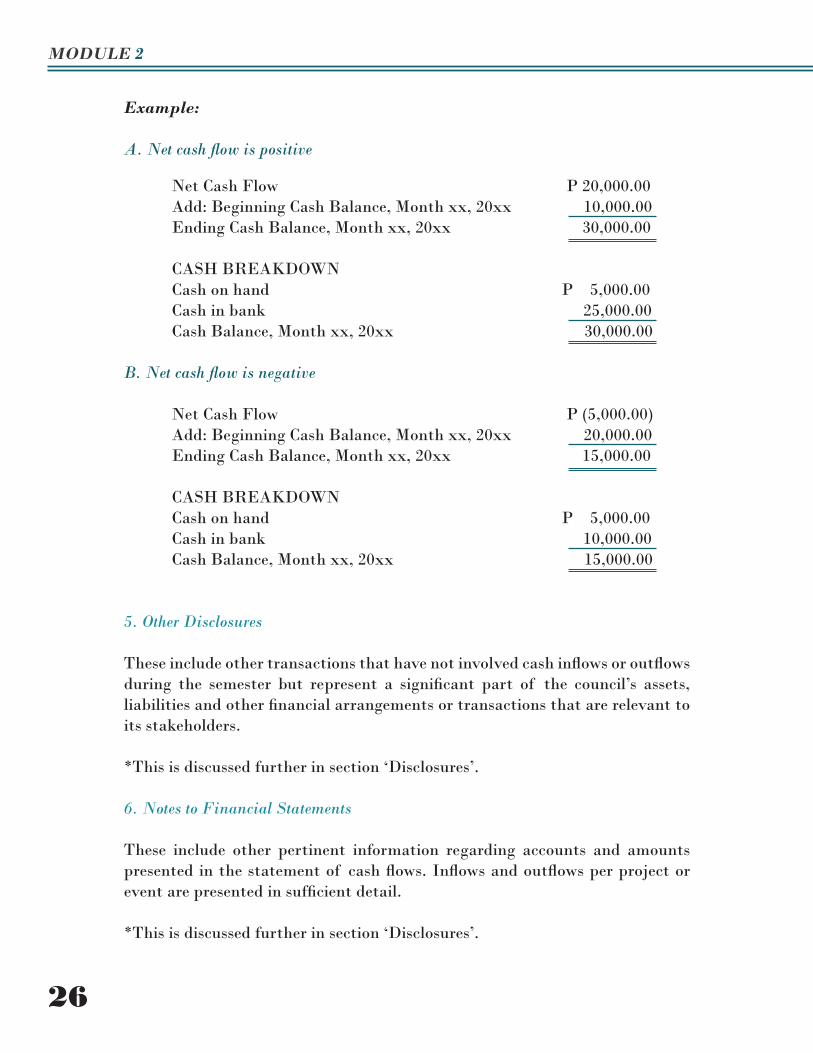

A. Net cash flow is positive

Net Cash Flow P 20,000.00Add: Beginning Cash Balance, Month xx, 20xx 10,000.00Ending Cash Balance, Month xx, 20xx 30,000.00 CASH BREAKDOWNCash on hand P 5,000.00Cash in bank 25,000.00Cash Balance, Month xx, 20xx 30,000.00

B. Net cash flow is negative

Net Cash Flow P (5,000.00)Add: Beginning Cash Balance, Month xx, 20xx 20,000.00Ending Cash Balance, Month xx, 20xx 15,000.00 CASH BREAKDOWNCash on hand P 5,000.00Cash in bank 10,000.00Cash Balance, Month xx, 20xx 15,000.00

5. Other Disclosures

These include other transactions that have not involved cash inflows or outflows during the semester but represent a significant part of the council’s assets, liabilities and other financial arrangements or transactions that are relevant to its stakeholders. *This is discussed further in section ‘Disclosures’.

6. Notes to Financial Statements

These include other pertinent information regarding accounts and amounts presented in the statement of cash flows. Inflows and outflows per project or event are presented in sufficient detail. *This is discussed further in section ‘Disclosures’.

26

STATEMENT OF CASH FLOWS

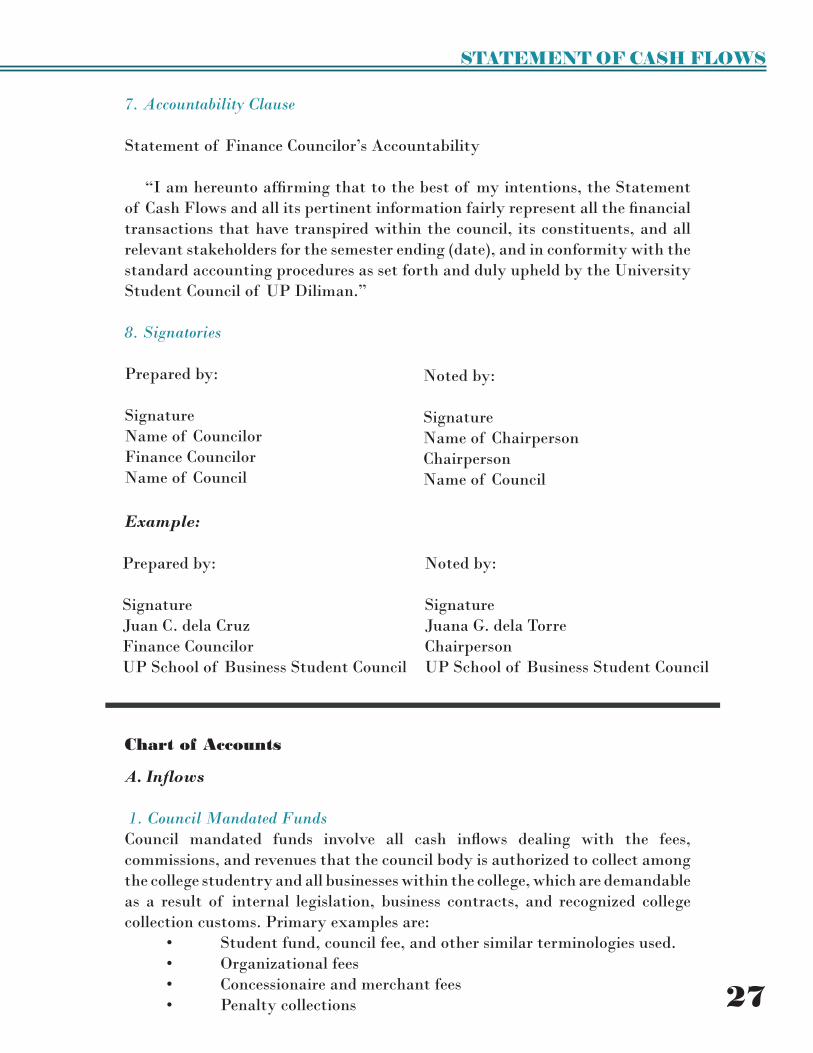

7. Accountability Clause

Statement of Finance Councilor’s Accountability

“I am hereunto affirming that to the best of my intentions, the Statement of Cash Flows and all its pertinent information fairly represent all the financial transactions that have transpired within the council, its constituents, and all relevant stakeholders for the semester ending (date), and in conformity with the standard accounting procedures as set forth and duly upheld by the University Student Council of UP Diliman.”

8. Signatories

Prepared by: SignatureName of CouncilorFinance CouncilorName of Council

Noted by: SignatureName of ChairpersonChairpersonName of Council

Example:

Prepared by: Signature Juan C. dela Cruz Finance Councilor UP School of Business Student Council

Noted by: Signature Juana G. dela Torre Chairperson UP School of Business Student Council

Chart of Accounts

A. Inflows

1. Council Mandated FundsCouncil mandated funds involve all cash inflows dealing with the fees, commissions, and revenues that the council body is authorized to collect among the college studentry and all businesses within the college, which are demandable as a result of internal legislation, business contracts, and recognized college collection customs. Primary examples are:

• Student fund, council fee, and other similar terminologies used. • Organizational fees • Concessionaire and merchant fees• Penalty collections 27

MODULE 2

2. General Sponsorship InflowsGeneral sponsorship inflows are all amounts of cash which are acquired gratuitously from other entities. At the most, such entities might request the promotion of their name or the featuring of their brands in events held within the college, but such event does not preclude retaining the classification of revenues acquired. Inflows only represent all cash, and these include:

• Sponsorships from business organizations• Pledges and donations from studentry/alumni body• Revenues from liquidation/sale of goods acquired in-kind

3. Income Generating Projects Income generating projects are inflows of cash originating from all the events undertaken by the council to raise revenues and generate additional funds supplementary to its operations. Transactions usually involve an initial disbursement of cash for the purchase of goods/merchandise, or setting up of facilities intended to serve as the platform for the eventual collection of cash, with the intention of realizing profits from such. These include:

• Sale of consumable goods/ merchandise (brand sale/ book sale/ food sale)• Rummage sale and revenues from scrap disposal• Ticket sales from college-wide events• Revenues from services (printing and photocopy fees, locker rentals, etc.)

4. Other InflowsAll cash inflows which are not traceable to the three classifications mentioned earlier fall under the other income section. These involve all the unique material transactions that the council has dealt with for the previous semester, and all other kinds of transactions which are special in nature to the council involved. The following is a suggestive list of other inflows:

• Interest income• Loans received from other entities

B. Outflows

1. Council Projects and College EventsThe basic outflow involving all the projects undertaken by the council fall under the “Council Projects and College Events” heading. On a strict accounting format, the council should determine only the single line-item outflow amount, on a per project basis, to be presented in the Statement of Cash Flows, with all the supporting disbursements and sources of funds to be elaborated in the Notes to Financial Statements.

• Staple projects (College Week, Graduation Ball, Christmas Party, etc.)• Other unique council projects• Office renovations• Constitutional amendment and election-related expenses• General registration

28

STATEMENT OF CASH FLOWS

2. Operation and Maintenance Expenses

All recurring expenses required for the operation and upkeep of the council are to be classified under the heading “Operation and Maintenance Expenses”. Outflow of cash that do not involve any particular project, and are done in the usual way of the council’s dealings are likewise included in this classification. These are:

• Council meeting expenses• Bulletin boards and promotional materials• Reimbursements to council officials• Supplies purchases• Sanitation expense

3. Long Term Investments

Long term investments involve all productive assets purchased by the council for the inclusive period of the Financial Statements. Only assets which are intended for use and ownership extending beyond the current academic year, or those which are expected to generate a direct inflow of cash through their usage/ownership are permitted to be classified as long term investments. These include:

• Electronics (Laptops, projectors, photocopying machines, etc.)• Furniture and fixtures (tables, desks, drawers, cabinets, chairs, lockers etc.)• Office equipment (Air conditioner, electric fans, lights, sockets, extension wires, etc.)• Financial instruments (Time deposits, bonds, stocks)

4. Other Outflows

All cash outflows which are not traceable to the three classifications mentioned earlier fall under the other expenditures section. These involve all the unique material transactions that the council has dealt with for the previous semester, and all other kinds of transactions which are special in nature to the council involved. The following is a suggestive list of other outflows:

• Interest expense• Loans paid to other entities• Unaccountable losses

29

MODULE 2

Disclosures

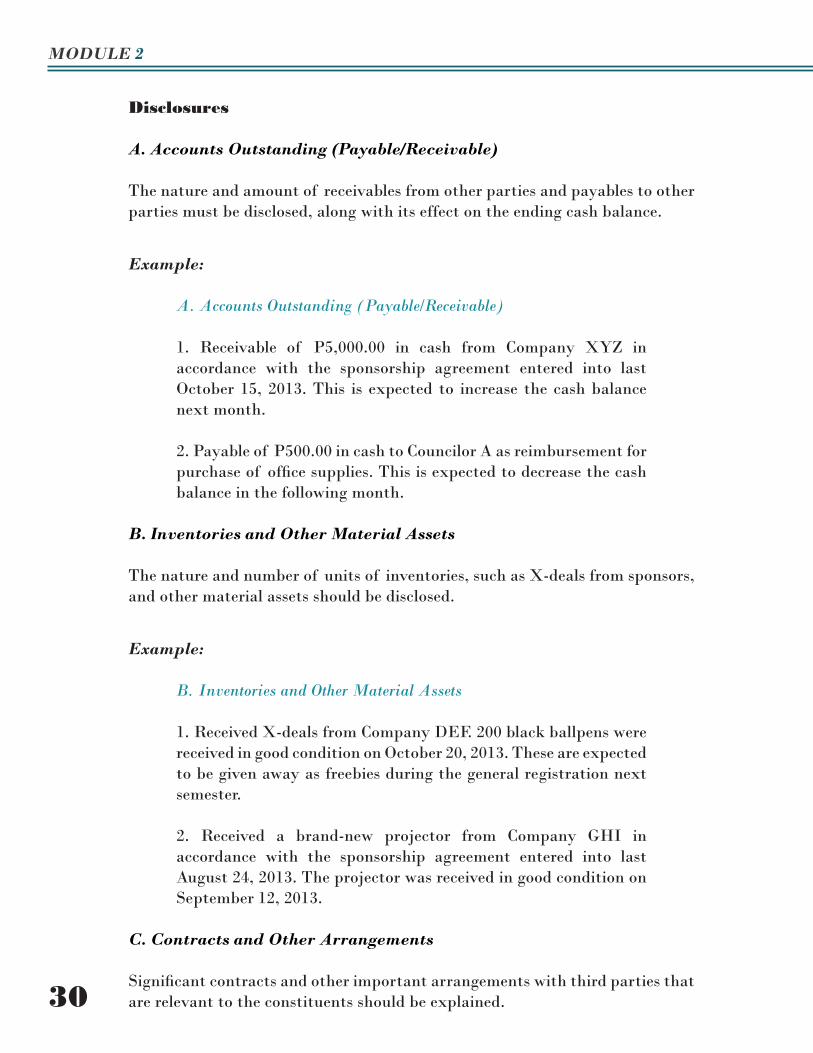

A. Accounts Outstanding (Payable/Receivable)

The nature and amount of receivables from other parties and payables to other parties must be disclosed, along with its effect on the ending cash balance.

Example:

A. Accounts Outstanding (Payable/Receivable) 1. Receivable of P5,000.00 in cash from Company XYZ in accordance with the sponsorship agreement entered into last October 15, 2013. This is expected to increase the cash balance next month.

2. Payable of P500.00 in cash to Councilor A as reimbursement for purchase of office supplies. This is expected to decrease the cash balance in the following month.

B. Inventories and Other Material Assets

The nature and number of units of inventories, such as X-deals from sponsors, and other material assets should be disclosed.

Example:

B. Inventories and Other Material Assets 1. Received X-deals from Company DEF. 200 black ballpens were received in good condition on October 20, 2013. These are expected to be given away as freebies during the general registration next semester. 2. Received a brand-new projector from Company GHI in accordance with the sponsorship agreement entered into last August 24, 2013. The projector was received in good condition on September 12, 2013.

C. Contracts and Other Arrangements

Significant contracts and other important arrangements with third parties that are relevant to the constituents should be explained.30

STATEMENT OF CASH FLOWS

D. Sponsorships

Partnerships with companies and benefits received should be specified.

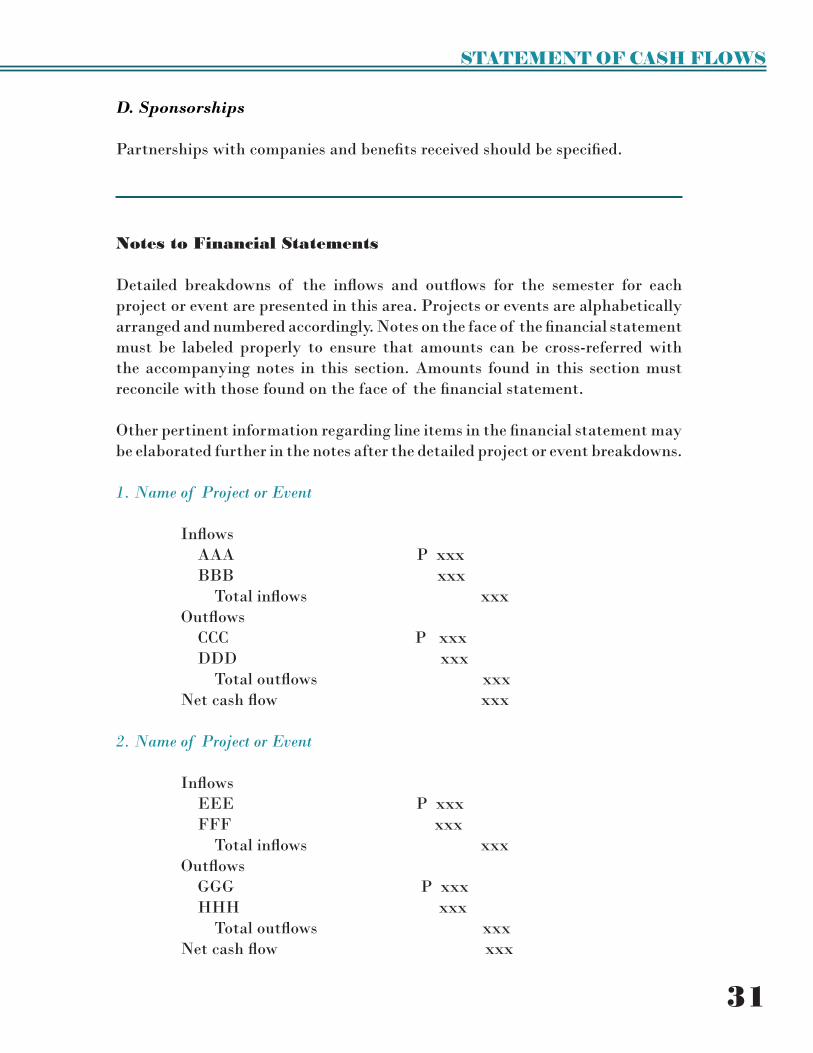

Notes to Financial Statements

Detailed breakdowns of the inflows and outflows for the semester for each project or event are presented in this area. Projects or events are alphabetically arranged and numbered accordingly. Notes on the face of the financial statement must be labeled properly to ensure that amounts can be cross-referred with the accompanying notes in this section. Amounts found in this section must reconcile with those found on the face of the financial statement. Other pertinent information regarding line items in the financial statement may be elaborated further in the notes after the detailed project or event breakdowns.

1. Name of Project or Event

Inflows AAA P xxx BBB xxx Total inflows xxx Outflows CCC P xxx DDD xxx Total outflows xxx Net cash flow xxx

2. Name of Project or Event

Inflows EEE P xxx FFF xxx Total inflows xxx Outflows GGG P xxx HHH xxx Total outflows xxx Net cash flow xxx

31

MODULE 2

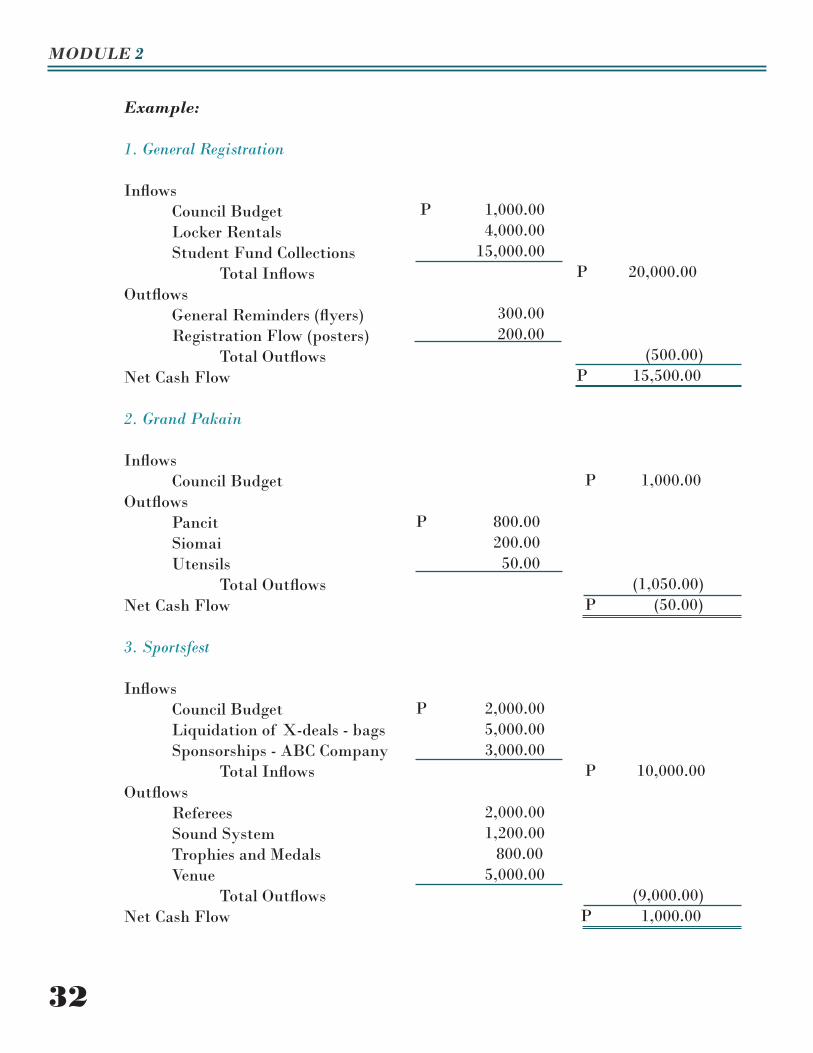

Example:

1. General Registration

Inflows Council Budget Locker Rentals Student Fund Collections Total InflowsOutflows General Reminders (flyers) Registration Flow (posters) Total OutflowsNet Cash Flow

2. Grand Pakain

Inflows Council BudgetOutflows Pancit Siomai Utensils Total OutflowsNet Cash Flow

3. Sportsfest

Inflows Council Budget Liquidation of X-deals - bags Sponsorships - ABC Company Total InflowsOutflows Referees Sound System Trophies and Medals Venue Total OutflowsNet Cash Flow

P 1,000.00 4,000.00 15,000.00

P 20,000.00

300.00 200.00 (500.00)

P 15,500.00

P 1,000.00

P 800.00 200.00 50.00 (1,050.00)

P (50.00)

P 2,000.00 5,000.00 3,000.00 P 10,000.00 2,000.00 1,200.00 800.00 5,000.00 (9,000.00) P 1,000.00

32

STATEMENT OF CASH FLOWSMODULE 3INTERNAL CONTROL

PROCEDURES

Cash: Safekeeping and Recording

Amounts of cash exceeding a materiality threshold duly set by the council must be kept in a savings account named after the duly-recognized student government organization. Signatories must be both the Finance Councilor and the Student Council Chairperson.

Cash deemed nominal in value by the council must be stored in a cashbox with an appropriately secured lock. It must be accompanied by a cashbox ledger noting the inflows and outflows of cash.

The Finance Councilor is mandated to keep a cash ledger record detailing the inflows and ouflows of cash. Items, other than cash, that must be disclosed in a separate portion of the Statement of Cash Flows include:

1. Accounts Receivable (from officers, sponsors)2. Inventory (at net realizable value)3. Accounts Payable (to officers, suppliers)4. Other material items

<See Other Assets and Liabilities Section of the Sample Statement of Cash Flows>

Revenues: Handling the Student Fund & Cash from RGPs

Cash received, while can be kept in one account/ cashbox, must be classified according to their various sources when recorded in the cash ledger document.

<See Sample Statement of Cash Flows>

33

MODULE 3

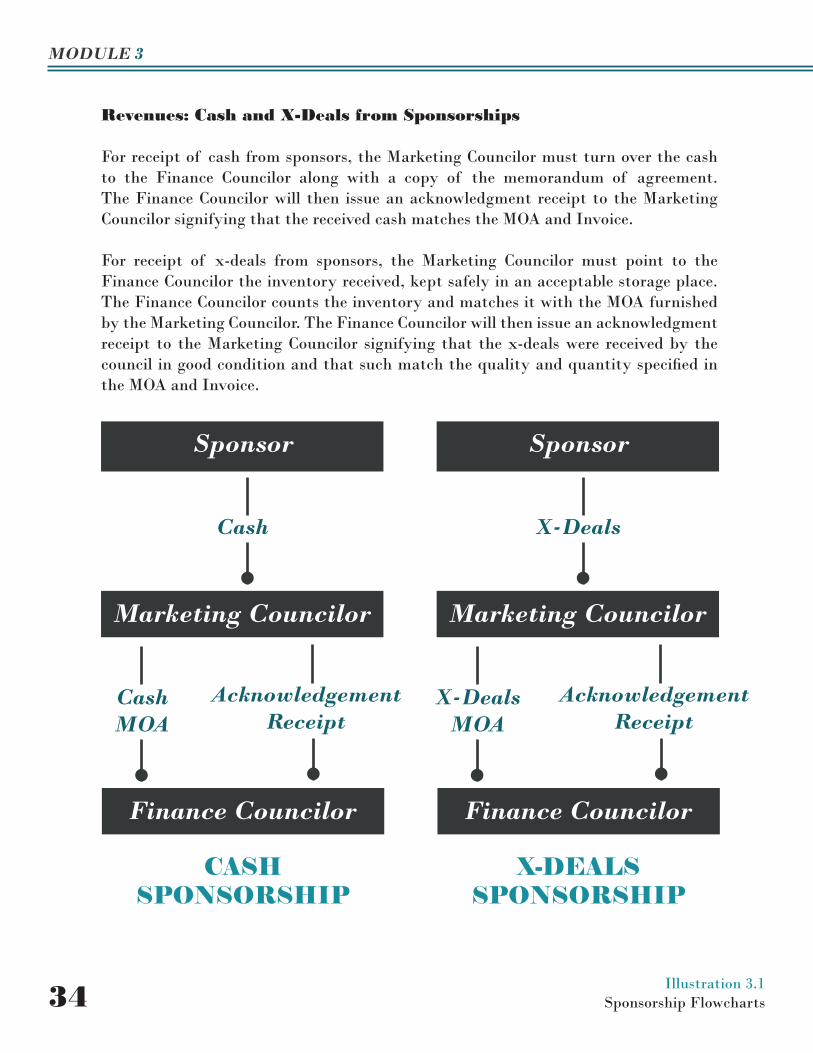

Revenues: Cash and X-Deals from Sponsorships

For receipt of cash from sponsors, the Marketing Councilor must turn over the cash to the Finance Councilor along with a copy of the memorandum of agreement. The Finance Councilor will then issue an acknowledgment receipt to the Marketing Councilor signifying that the received cash matches the MOA and Invoice.

For receipt of x-deals from sponsors, the Marketing Councilor must point to the Finance Councilor the inventory received, kept safely in an acceptable storage place. The Finance Councilor counts the inventory and matches it with the MOA furnished by the Marketing Councilor. The Finance Councilor will then issue an acknowledgment receipt to the Marketing Councilor signifying that the x-deals were received by the council in good condition and that such match the quality and quantity specified in the MOA and Invoice.

Sponsor

Marketing Councilor

Cash

Finance Councilor

Cash MOA

AcknowledgementReceipt

Sponsor

Marketing Councilor

X-Deals

Finance Councilor

X-DealsMOA

AcknowledgementReceipt

CASH SPONSORSHIP

X-DEALSSPONSORSHIP

Illustration 3.1 Sponsorship Flowcharts34

INTERNAL CONTROL PROCEDURES

Expenses: Proper Procedure, Required Forms, Timing

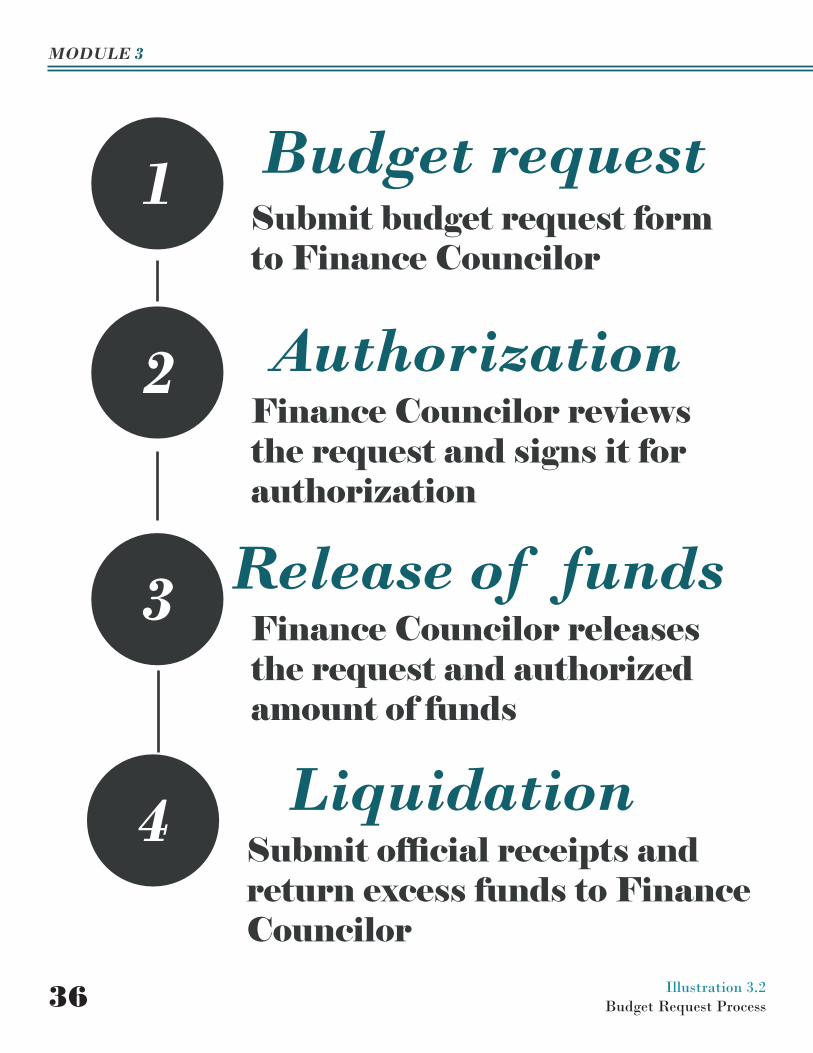

Budget Request Forms

The form must contain, at the minimum, pertinent details such as the date of submission to the Finance Councilor, the name and signature of the council member requesting for funds, a detailed projection of the expenses that will be incurred and the amounts, the total amount requested, the status of the request, and the name and signature of the Finance Councilor.

Authorization& Release of Funds

A standard operating procedure for submission and approval of budget request forms must be established indicating the timeline for submission of the form, approval, and release of funds. Any cash needed in excess of the amount stated in the budget proposal must be included in a separate budget request form.

Liquidation

For liquidation, official receipts must be submitted to and reviewed by the Finance Councilor for any unauthorized disbursements outside of the purpose stated in the budget proposal.

Any unused funds must be returned accordingly to the Finance councilor. The Finance Councilor will then reconcile if the amount of cash returned by the Officer and the total disbursements supported by official receipts would equal the total amount of cash released to the Officer as per the duly approved Budget Proposal.

Unauthorized Disbursements

Cash disbursements that are not in line with the purpose stated in the approved budget request forms must be explained by the officer responsible in a written appeal. To be ratified, the appeal must be reviewed and approved by both the Council President and the Finance Councilor. Otherwise, the unauthorized disbursement will have to be shouldered by the officer responsible.

35

MODULE 3

Budget request1Submit budget request form to Finance Councilor

Authorization2Finance Councilor reviews the request and signs it for authorization

Release of funds3 Finance Councilor releases the request and authorized amount of funds

Liquidation4 Submit official receipts and return excess funds to Finance Councilor

Illustration 3.2 Budget Request Process36

INTERNAL CONTROL PROCEDURES

Documentation

This module encourages the Finance Councilor to use a spreadsheet program in preparing the cash ledger record and the statement of financial position.

During Events

Control must be exercised by the Finance Councilor in making disbursements. Though the module respects the Finance Councilor’s prerogative in doing this, he is mandated to exercise due diligence in ensuring that all disbursements for a project are prudent and well-documented.

Financial Statements: Audit and Turnover

Before turnover of the Statement of Cash Flows (including Accounts Receivable, Inventory, Accounts Payable and Other Material Items) to the next Finance Councilor, the incumbent Finance Councilor must submit his abovementioned files and source documents to the Student Council Chairperson for auditing. Only when the Student Council Chairperson has signed the documents can it be ready for actual turnover to the next Finance Councilor.

37

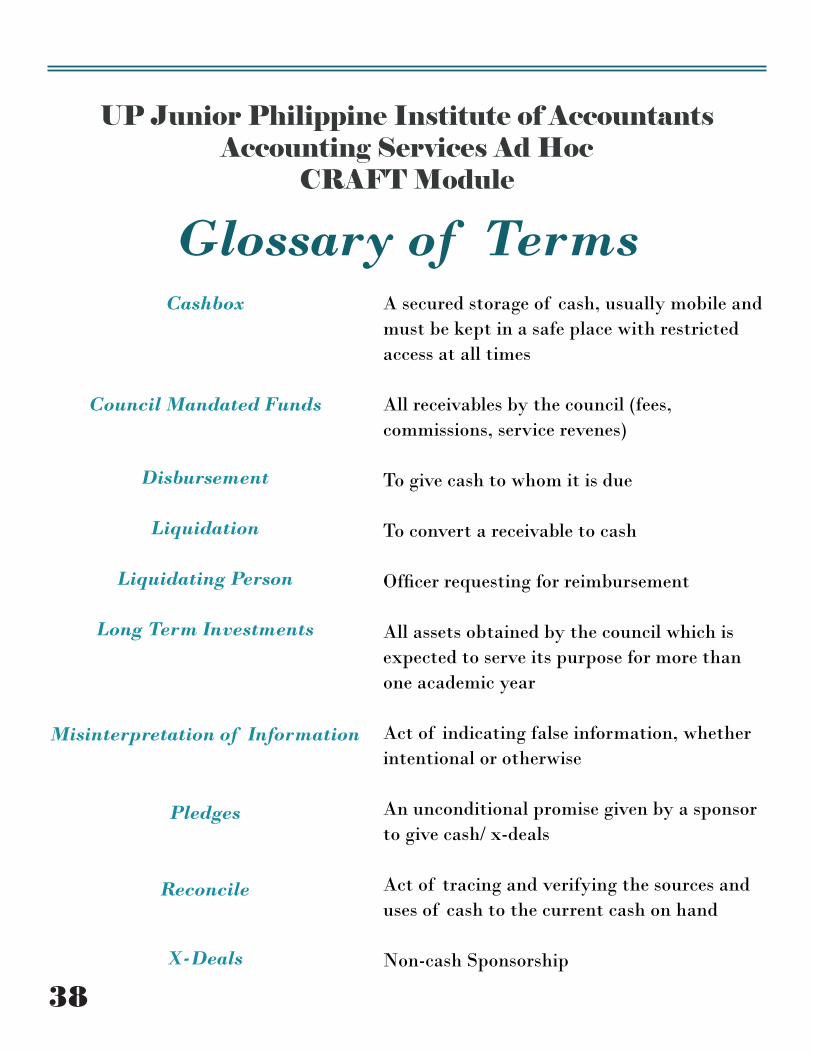

Cashbox

Council Mandated Funds

UP Junior Philippine Institute of AccountantsAccounting Services Ad Hoc

CRAFT Module

Glossary of TermsA secured storage of cash, usually mobile and must be kept in a safe place with restricted access at all times

All receivables by the council (fees, commissions, service revenes)

To give cash to whom it is due

To convert a receivable to cash

Officer requesting for reimbursement

All assets obtained by the council which is expected to serve its purpose for more than one academic year

Act of indicating false information, whether intentional or otherwise

An unconditional promise given by a sponsor to give cash/ x-deals

Act of tracing and verifying the sources and uses of cash to the current cash on hand

Non-cash Sponsorship

Disbursement

Liquidation

Liquidating Person

Long Term Investments

Misinterpretation of Information

Pledges

Reconcile

X-Deals

38

The University Financial Transparency Reporting Standards is a project initiated under the due authorization of the University Student Council, to be implemented in all the College Student Councils of UP Diliman.

While the conceptualization of this public document is wholly undertaken by the UP Junior Philippine Institute of Accountants – the organization at large, and its Accounting Services Adhoc in particular – is responsible only to these standards with respect to the soundness and applicability of the contents embodied herein.

This document is a response and a testimony to the ever increasing need of financial transparency and accountability for public governance.

Approved this 21st day of September, 2013.

Raphael Aaron A. LetabaTreasurer, University Student Council

Miguel Alfonso M. SolidumChairman, Accounting Services Adhoc

Ma. Clarissa Eirene S. TinitiganVice President for Education and Research

Rachelle Annemarie R. Acevedo

Gianni Jasper L. Dazo

Aileen K. Ko

Carmela Jasmine C. Mira

Ramon Carlo L. Pio Roda

Evangeline R. Villajuan

Layout by: Ma. Therese Camille C. Aseoche

Alex CastroChairperson, University Student Council

UP JPIA Representatives

Members

39