Embed Size (px)

Citation preview

1

UKElectricityMarketReformandtheEnergyTransition:

EmergingLessons

MichaelGrubb

ProfessorofInternationalEnergyandClimateChangePolicy,UCL

&Chair,UKPanelofTechnicalExperts,ElectricityMarketReform

and

DavidNewbery

EmeritusProfessor&

Director,EPRG,UniversityofCambridge

*

2

AbouttheAuthors

Michael Grubb is Professor of Energy and Climate Change at University College London (Institute of Sustainable Resources & Energy Institute). From 2011-2016, alongside academic roles, he worked half-time at the UK Office of Gas and Electricity Markets (the energy regulator, Ofgem), initially as Senior Advisor, Sustainable Energy Policy, and subsequently Senior Advisor, Improving Regulation. From Autumn 2016 he moved to Chair the UK government’s Panel of Technical Experts on Electricity Market Reform.

He has combined research and applied roles for many years, bringing research insights into policymaking, and bringing practical experience to bear upon academic studies: before taking up his post at UCL he was part-time Senior Research Associate in Economics at Cambridge University, combined with (prior to joining Ofgem) Chief Economist at the Carbon Trust.

Professor Grubb is author of eight books and, sixty journal research articles, and numerous other publications. His most recent book, Planetary Economics: energy, climate change and the Three Domains of Sustainable Development (Routledge 2014), brought together insights from 25 years of research and implementation of energy and climate policies. He was also founding Editor-in-Chief of the journal Climate Policy, and from 2008-11 served on the UK Climate Change Committee, established under the UK Climate Change Act to advise the government on future carbon budgets and to report to Parliament on their implementation.

Professor David Newbery, CBE, FBA, is the Director of the Cambridge Energy Policy Research Group and Emeritus Professor of Applied Economics at the University of Cambridge. In 2013 he was President of the International Association of Energy Economists. He has managed research projects on utility privatisation and regulation, electricity restructuring and market design, transmission access pricing and has active research on market integration, transmission planning and finance, climate change policies, the design of energy policy and energy taxation

Occasional economic advisor to Ofgem, former chairman of the Dutch Electricity Market Surveillance Committee, member of the Panel of Technical Experts offering quality assurance on the delivery of the UK’s Electricity Market Reform (2014-16). He is currently an independent member of the Single Electricity Market Committee of the island of Ireland and a panel member of Ofgem’s Network Innovation Competition.

Professor Newbery is author of eight books, over one hundred and thirty research articles and numerous other publications. His book, Privatization, Restructuring and Regulation of Network Utilities, published by MIT press provides a definitive empirical cross-country study of de-regulation, liberalization and privatization in electricity, telecoms and gas to assess how structural reforms can enhance productivity.

Both the authors are writing in their independent academic capacities, and drawing only on published materials.

3

ContentsSummary......................................................................................................................................................4

1. Introduction:‘ModelorWarning?’......................................................................................................6

2. UKElectricityincontext.......................................................................................................................6

2.1TheevolutionoftheUKelectricitysupplyindustry–theorigins......................................................6

2.2Theelectricityindustrystructure1990-2001:thepoolandthedash-for-gas...................................8

2.3 Theelectricityindustrystructureafter2001..............................................................................10

2.4Electricitydemandandttheretailmarket.......................................................................................11

3. TheintellectualandpoliticalevolutionofUKElectricityMarketReform..........................................13

4. Afourleggedbeast?TheEMRpackage............................................................................................17

5. Resultstodate....................................................................................................................................22

5.1 CfDAllocationandAuctions.......................................................................................................22

5.2 CapacityMarket.........................................................................................................................26

5.3Carbonpricefloorandemissionsperformancestandard................................................................33

6. Popularcaricature:“Returnofthe‘CentralElectricityGeneratingBoard’?”.....................................36

7.Conclusions:thecollapseofcoal,lessonsofcontractingandfuturechallenges...................................38

References..................................................................................................................................................41

Dataappendix:Notesonconstructionofelectricitybills..........................................................................43

Figure1:UKelectricitygenerationbyfuel,1970-2016...............................................................................7Figure2:UKelectricityconsumptionbyenduse.......................................................................................11Figure3RealIndustrialanddomesticbillsforstandardizedconsumptionlevel.......................................12Figure4ThefourpillarsofUKElectricityMarketReform..........................................................................18Figure5:Carbonpricesupport,asseenbytheUKTreasuryininitialdevelopmentoftheEMR..............18Figure6:StructureoftheContracts-for-Difference...................................................................................20Figure7GrowthofrenewableelectricitygenerationinEUcountriessince2005....................................25Figure8UKoffshorewindcostreductionacrossallocationandauctionrounds.....................................26Figure9:Resultsofmaincapacity(four-yearahead)auctions..................................................................29Figure10:NewcapacityintheCapacitymarket,bidsandapproved,2014-2016.....................................30Figure12GBwholesaleelectricitypriceandthecostofgeneration,2007-17at2011/12prices.............34Figure11CarbonPriceSupportandimpactoncoalgeneration,2012-2017(Q2)....................................35Figure13UKquarterlyelectricitygenerationbyfueltype,1997-2017.....................................................38

Box1:PricingandcapacitypaymentintheElectricityPool........................................................................9Box2:ThehistoryofUKrenewablespolicybeforeEMR..........................................................................16Box3The(almost)‘mostexpensiveobjectontheplanet?’–theHinkleyPointCnuclearcontract........23Box4Transmissionchargingand‘embeddedbenefits’intheCapacityMechanism................................32

4

SummaryUntil1990,theUK-likemanyothercountries-hadanelectricitysystemthatwascentralised,state-owned,anddominatedalmostentirelybycoalandnuclearpowergeneration.Theprivatisationofthesystemthatyearanditscreationofacompetitiveelectricitymarketattractedglobalinterest,helpingtosetapathwhichmanyhavefollowed.

Twodecadeslater,however,theUKgovernmentembarkedonaradicalreformwhichsomecriticsdescribedasareturntocentralplanning.TheUK'sElectricityMarketReform(EMR),enactedin2013,hascorrespondinglybeenatopicofintensedebate,andglobalinterestinthemotivations,components,andconsequences.

ThisreportsummarisestheevolutionofUKelectricitypolicysince1990andexplainstheEMRincontext:itsorigins,rationales,characteristics,andresultstodate.WeexplainwhytheEMRisaconsequenceoffundamentalandgrowingproblemswiththeformofliberalisationadopted,particularlyafter2000,combinedwiththegrowingimperativetomaintainsystemsecurityandcutCO2emissions,whilstdeliveringaffordableelectricityprices.

Thefifteenyearsafterprivatisation,coincidingwiththeeraoflowfossilfuelprices,hadseenmostlyfallingelectricitybills;fromabout2004theystartedtorisesharply,formultiplereasonsincludingincreasingfossilfuelprices,theneedfornewinvestmentinbothgenerationandtransmission,andinefficientrenewablespolicies.

ThefourinstrumentsoftheEMRhaveindeedcombinedtorevolutionisethesector;theyhavealsobothdrawnon,andhelpedtospur,aperiodofunprecedentedtechnologicalandstructuralchange.Competitiveauctionsforbothfirmcapacityandrenewableenergyhaveseenpricesfarlowerthanpredicted,withthefixed-priceauctionsforrenewablesourcesestimatedtosaveover£2bn/yrinthecostoffinancingtheprojectedrenewablesinvestments,comparedtotheprevioussupportsystem.Aminimumcarbonpricelevelhasbroughtcleanergastothefore,displacingcoal.Electricitypricesmayhavepeakedfrom2015,withenergyefficiencyhelpingtoloweroverallconsumerbills.

Newformsofgenerationhaveexpandedrapidlyatallscalesofthesystem.Renewableelectricityinparticularhasgrownfromunder5%ofgenerationin2010,toalmost25%by2016,andisprojectedtoreachover30%by2020despiteapoliticalde-factobanonthecheapestbulkrenewable,ofonshorewindenergy.Theenvironmentalconsequencesoverallhavebeendramatic:coalgenerationhasshrunkfromabout2/3rdofgenerationin1990,to35%in2000,to10%in2016,halvingCO2emissionsfrompowergenerationoverthequartercentury.

Neitherthetechnologicalnorregulatorytransitionsarecomplete,andtheresultstodatehighlightotherchallenges.TheCapacitymechanismhasprovedill-suitedtoencouragingdemand-sideresponse,andincombinationwiththegrowingshareofrenewables,hasunderlinedproblemsintransmissionpricing.Astheshareofvariablerenewablesgrowsfurther,theassociatedcontractswillrequirereformtoimprovesitingefficiencyandavoidadverseimpactsonthewholesalemarket.TheresultstodateshowthatEMRisastepforwards,notbackwards;butitisnottheendofthestory.

5

Acronyms

BEIS DepartmentforBusiness,EnergyandIndustrialStrategy(successortoDECC,establishedin2016)

BETTA BritishElectricityTradingandTransmissionArrangements(extensionofNETAtoincludeScotlandfrom2005)

CfD ContractsforDifference(afixed-priceelectricitycontract)

CCGT CombinedCycleGasTurbine

DECC DepartmentofEnergyandClimateChange

DSR Demand-sideResponse

EMR ElectricityMarketReform

IPP IndependentPowerProducers

NETA NewElectricityTradingArrangements(adoptedin2001)

ROC RenewablesObligationCertificate

PTE PanelofTechnicalExperts(independentadvisorycommitteeestablishedundertheElectricityMarketReformlegislation

RECs RegionalElectricityCompanies(RECs),establishedafterprivatisation

WACC WeightedAverageCostofCapital

6

1. Introduction:‘ModelorWarning?’TheUKwaswidelyseenasoneoftheworld’sleadersonelectricityderegulationintheearly1990s.Thoughthemodelofliberalisationwentthroughsignificantchanges,manyinternationalobserversweresurprisedwhenin2010thenewUKgovernmentembarkedonafundamentalreformtothearchitectureofUKelectricityregulation.Tomany,itseemslikeabandoningtheprinciplesofmarketcompetitionthathadbeenseenasdefiningtheUKapproach.

TheElectricityMarketReformlegislationdidindeedrepresentaradicalchange.Promptedbyunderlyingconcernsaboutalackofinvestmentthatthreatenedtounderminebothsecurityanddecarbonisationgoals,andpoliticallygalvanisedalsobyrisingenergyprices,itneverthelessprovedhighlycontroversial.Thelegislationtookmostofthe5-yearParliamentarytermtocompleteandthefirstauctionsunderthenewsystemonlytookplaceinDecember2014.

TheUK’soriginalliberalisationofelectricitywaswidelyseenasaradicalexperiment,attractingworldwideinterest.TheUK’sElectricityMarketReformhas,similarly,sparkedwidespreadinterest,withwidelydivergentviewsastowhetheritrepresentsapotentialmodelwhichotherscouldfollow,orawarningoftheperilsof–apparently-returningtogreaterstateinvolvementinelectricity.

Itisthusstillrelativelyearlydays,butmanylessonscanalreadybedrawn.Thispaperseeksto:• SummarisebrieflytheevolutionoftheUKelectricitysystemincludingtheunderlying

institutionalandpoliticalcontext;• explainthebasicreasonswhytheUKembarkedonitsElectricityMarketReform–thekey

intellectualdebatesandinstitutionalproponents;• explainthebasicstructureoftheEMRpackageasfinallydefinedinthe2013legislation;• presenttheresultstodate,focusingprimarilyontheresultsofcontractsissuedand

auctionsheldthroughtomid-2017;• drawinitiallessons,addressingconcernsthattheEMRrepresentsa‘returntocentral

planning’.

Finally,wereflectonthefuturechallengesandprospectsforevolutionoftheUKelectricitymarketstructure.

2. UKElectricityincontext

2.1TheevolutionoftheUKelectricitysupplyindustry–theoriginsInEnglandandWalesfrom1947whentheelectricitysupplyindustrywasnationalised,generationandtransmissionwereownedbythepublicCentralElectricityGeneratingBoard.TheCEGBsoldtothe12AreaBoards(thedistributionandretailing)companiesunderaBulkSupplyTariff(forenergyandpeakdemand).InScotlandtheindustrycomprisedtworegionalverticallyintegratedcompanies,andinNorthernIrelandjustoneverticallyintegratedcompany.

7

Figure1showsgenerationoutputbyfuelfrom1970.Until1955almosttheentireoutputwasgeneratedfromcoal,suppliedbytheNationalCoalBoard,but,underpressurefromtheTreasury,oil-firedpowerstationswerebuiltandthefirstgenerationofgas-cooledMagnoxnuclearpowerstationsstartedproducing,andthenuclearshareroseto20%by1990.Theshareofoilpeakedat34%justbeforetheoilshockin1972,andthereaftercoalandnuclearpowergraduallyreplacedoiluntilbytheendofthecenturyitwasdownto1%.

Figure1:UKelectricitygenerationbyfuel,1970-2016Source:BEIS(2017)Note:“other”isallthermalgenerationfromothergenerators(i.e.notthepublicsupplycompanies),non-CCGTgasandthermalrenewables.Pumpedstorage(netnegative)isnotshown.SeenotestoBEIS(2017)

TheConservativeGovernmentunderMargaretThatchercametopowerin1979aftera

“winterofdiscontent”,strikes,stagnationandadrasticreductioninpublicinvestmentfollowingtheoilshocksandavisitoftheIMFurgingausterityin1976.Hermanifestopledgewastoreverseeconomicdecline,rollbackthefrontiersofthestate,andreducethepoweroforganisedlabour.Privatizingstate-ownedenterprisesstartedcautiously,butbetween1979-92some39companieswereprivatized,sothatby1992thetop100companiesincluded17formerlystate-ownedcompanies(Newbery,1999).ThefirstpublicutilitytobesoldwasBritishTelecom(in1984)followedbyBritishGas,thewatercompanies(1989)andfinallythe

8

electricityutilitiesthroughtheElectricityAct1989(from1990on,endingwiththesaleofthemoremodernnuclearplantin1995).

By1989,justbeforerestructuringforprivatisation,around90%oftheconventionalthermalgenerationwasfromcoal,andtheshareofoilfellrapidlyfrom7%to1%in2002(theremainderofthermalgenerationislargelyfromby-productgasesfromiron,cokeandchemicals).Thestoryisquicklytold:theminers’strikein1984wasaccommodatedbyashort-livedswitchbacktooilusingplantbuiltinthe1960’sbutdisplacedbycheapercoalaftertheoilshocksofthe1970s.Atprivatizationin1990theUKwassuppliedbycoalandnuclearpowerwithsomeimports.Shortlyafterprivatizationthecoalsharerapidlydeclinedasnuclearpowerimproveditsperformance,andwiththe“dashforgas”,whichwasallnewentrydespitetheconsiderablesparecapacity.Attheendofthecenturyconsumptionfellwithdeindustrializationandincreaseddemandefficiency,whilerenewablesdisplacedgasand/orcoal,whosesharesdependedontheveryvolatileclean(gas)anddarkgreen(coal)sparkspreads(themarginbetweenthewholesalepriceandthefuelplusCO2cost).

2.2Theelectricityindustrystructure1990-2001:thepoolandthedash-for-gasThestate-ownedcompanieswerereplacedby,inEnglandandWales(E&W),twofossilandonenuclear(initiallystate-owned)generationcompanies,withanunbundledNationalGrid(initiallycollectivelyownedbytheregionalprivatizedRegionalElectricityCompanies,RECs).InScotlandthetwoverticallyintegratedcompaniesweresoldbundled,whileinNorthernIslandthreegenerationcompaniesweresoldwithlong-termpowerpurchaseagreements(PPAs).NationalGridandtheRECswereregulated,andlargecustomerswerefreetobuydirectlyfromthewholesalemarket,whichtooktheformofthemandatorygrossElectricityPool.ThiswascentrallydispatchedwithaSystemMarginalPrice(SMP)setbythemarginalpriceofferedbythemostexpensiveunconstrainedgeneratorrequired,towhichwasaddedacapacitypayment(seeBox1).Oneofthemostdramaticdevelopmentsafterprivatisationwasthe‘dashforgas’;investmentpouredintonewgasgeneratingplants,andasshowninFigure1,gasgenerationgrewfromnexttonothingin1992,toalmostathirdofgenerationby2000.

Multiplefactorsunderpinnedthis.Outsidetheelectricitymarketitself,NorthSeagashadlargelysaturateddomesticmarketswhilstproductionwasstillgrowing,withlowandfallinggasprices.AlegalbanonusinggasforpowergenerationhadbeenliftedandthenewgenerationofCombinedCycleGasTurbines(CCGTs)promisedfargreaterefficiencythanexistingplant.Givenitspoliticalhistorytheconservativegovernmentwashappytoencouragethedeclineofcoal,whilstthebreakingupoftheCEGB,whichhadseentheworldlargelyintermsofeverbiggercoalandnucleargeneration,introducedplayersinterestedinnewapproaches.

9

Inthemarketitself,thelowandfallinggaspriceswereaidedbyhighPoolprices,andrapidlyimprovingandlowcapitalcostCombinedCycleGasTurbines(CCGTs).Withenergypolicylefttothemarkettoguidechoices,politicalriskwasconsideredlowandsubstantialentryby“Independent”PowerProducers(IPPs)occurred.Theseenteredonthebackoflong-termfixedpricecontracts(andoftenshareownership)withtheRECs,whocouldpassontheircoststothecaptivefranchisedomesticmarket.

Thusthecombinationoflong-termgascontracts,longtermIPPcontracts,regulatedpass-throughandperformanceguaranteesontheCCGTs,allreducedrisk,whilstanaddedincentivefortheRECstosignsuchcontractswastoexploittheirnewindependencefromcentralisedgeneration.ThetwofossilgeneratorsdominatedtheEngland&WalesPoolandclearlyhadconsiderablemarketpower(Newbery,1995),whichtheregulatornegotiateddownbyencouragingthemtodivest6GWofcoalplanttoathirdgeneratorin1996.Theresultingtriopolywaslessconstrainedinexercisingmarketpower,withanincentivetodosoastheywishedtodivestcoalplantbeforethedashforgaserodedtheirmarketsharetoodrastically(Sweeting,2007).Indeedby2000,coal-basedgenerationhadshrunkbymorethanathird(andincreasingamountsofcoalwereimportedratherthandomesticallyproduced).

Box1:PricingandcapacitypaymentintheElectricityPool

Theoperationoftheelectricitypoolestablishedafterprivatisationwasdefinedintermsofasinglepriceforelectricitypurchased‘bythepool’fromgenerators(PoolPurchasePrice).TheSystemOperator(ownedbyNationalGrid)receivedoffersfromallindividualgeneratingsetsthedaybefore.Tomeetprojecteddemand,NationalGridestablishedaSystemMarginalPrice(SMP)fromthescheduleofgenerationoffers,dispatchingthegeneratorsaccordinglyuptothemarginalofferwhichdefinedtheSMP.

TothiswasaddedaCapacityPayment,whichwasdesignedtocompensateforthe‘missingmoney’inasystembasedpurelyonshort-runmarginalgeneratingcosts:

CapacityPayment=LoLP*(VoLL–SMP), (1)

whereLoLPistheLossofLoadProbabilityinthathalf-hourandVoLListhevalueofLostLoad(£5,000/MWhin2016£).ThiswouldgivetheefficientscarcitypriceofelectricityiftheSMPwerethesystemmarginalcost,butgeneratorswerefreetoofferanyprice,onlyconstrainedbythethreatofanti-competitivebehaviour.

SMP+CapacityPaymentisthePoolPurchasePrice,,which,withadditionalancillaryserviceandconstraintcostsmadeupthePoolSellingPrice.Theday-aheadbidsreceivedbyNationalGridwerecomplexmulti-partofferswitharaftofadditionalconstraintsandcharacteristics.NationalGridusedtheoldschedulingalgorithmtodetermineafeasibledispatch.Adjustmentsduringthedaywerecalledoffthepreviousday’soffersandchargedouttoconsumersinthesellingprice(GreenandNewbery,1993).

10

2.3 Theelectricityindustrystructureafter2001OncetheyhaddivestedenoughplantthegenerationcompanieswerefreetobuythesupplybusinessesoriginallyintegratedwiththeRECs.ThemarketevolvedtowardsthecurrentBigSixgenerators1plusretailers.ThemarketpowerofthetriopolyleadtoanincreasinggapbetweencostandpriceinthePoolbetween1996-2000,andencouragedtheGovernmenttoreplacethePoolwithNewElectricityTradingArrangements(NETA)-justatthedate(2001)whentheprice-costmargincollapsedundertheweightofcompetitionandexcesscapacity(Newbery,1998;2005).

NETAreplacedcentraldispatchandthePoolwithaself-dispatchedenergy-onlymarket(abolishingcapacitypayments).Theargumentputforwardwasthatgettingridofthepoolinfavourofdirectbilateraltradingwouldrepresentafurthersteptowardscompetition.Tomeetthephysicalneedtobalancesupplyanddemand,NETAcreatedatwo-pricedBalancingMechanism.Theclaimedlogicforthereformwasthatself-dispatchrequiredgeneratorstosubmitabalancedoffer(i.e.outputmatchedbycontractstopurchasebysbuyers)andthatrequiredthemtocontractalloutputaheadoftime,thusremovingtheincentivetomanipulatethespotmarket(under-contractingencouragessellerstoincreasethespotpriceabovethemarginalcost,over-contractingtoreducethepricebelowmarginalcost,Newbery,1995).

Inpracticethebalancingmechanismwassoflawedithasrequiredmanyhundredsofpainfullynegotiatedmodificationstoapproximateanefficientbalancingmarket.Inaddition,theriskofincentivestomanipulatethespotmarketwasreplacedbyaclearincentivetoverticalintegration:themergerofretailingandgenerationcompaniesensuredthattheywereprotectedbothwaysagainstelectricitypriceuncertainties,sincetheywouldthenbesellingwholesaletothemselves.However,thisinturncreatedmajorbarrierstoentry,andaperception–atleast-oftheelectricitysystemasanoligopolyofmajorpowercompaniescontrollingtheentiresystemfromgenerationtoconsumption.

Withoutheedtotheseconcerns,in2005,theretrogressiveprinciplesofNETAwereexpandedtoincorporateScotlandinBETTA-BritishElectricityTradingandTransmissionArrangements,creatingasingleGreatBritainelectricitymarket.2ThiscreatedasinglepricezonedespiteseriouscongestionontheScottishborder,withitsresultinghighredispatchcosts(whichgrewfurtheraswindenergywasincreasinglydeployedinScotland).

TheEUTargetElectricityModelthatcameintoeffectin2014mandatesthatseparatepricezonesarecreatedwhentherearesignificantboundaryconstraints.Hadthisbeenfollowed,ScottishconsumerswouldfrequentlyenjoylowerpricesthantherestofGB,andthe

1Centrica,SSEplc,RWEnpower,E.ON,ScottishPowerandEDFEnergy2LeadingalsotothestrangesituationthatNationalGrid,asTransmissionSystemOwnerandOperatorinEnglandandWales,becametheSystemOperatoroftheScottishgridsthatremainedundertheownershipofthetwoverticallyintegratedcompanies.

11

costsofredispatchwouldhavebeenavoided.Thesecostsrosetohundredsofmillionsofpoundsannually,amountingto£60millioninOctober,2014forasingle(admittedlyhighcost)month.3

2.4ElectricitydemandandtheretailmarketThepatternofelectricityconsumptionhasbeenfarmorestablethatthepatternoffueluseinproduction(figure2):initiallydominatedbyindustryanddomesticuse,theformersincethe1970shasdeclinedrelativelyinfavourof“other”(particularlyservices),whilstoverthepastdecade,overalldemandonthenationalgridhasdeclined.

Industrialelectricitydemandinparticularstabilisedfromabout2000,anddomestic(household)electricitydemandpeakedin2005:by2016,industrialanddomesticelectricitydemandwererespectively21%and14%belowthelevelsadecadeearlier,despiteGBpopulationgrowing10%overtheperiod.4Thisreflectedacombinationofimprovedenergyefficiency(drivenbystrongerefficiencystandardsonbuildingandappliances,andvariousgovernmentprogrammes),slowedeconomicgrowthafterthefinancialcrisis,andthedirectimpactofrisingprices,whichalsoacceleratedstructuralchangeinindustry.

Figure2:UKelectricityconsumptionbyenduseSource:BEIS(2017)Note:“other”includesPublicadministration,transport,agriculturalandcommercialsectors.3NationalGridOperationalandSystemCostUpdate2015atwww2.nationalgrid.com/WorkArea/DownloadAsset.aspx?id=402064DigestofUKEnergyStatistics,2017:Table5.1.2;Populationdata:https://www.ons.gov.uk/peoplepopulationandcommunity/populationandmigration/populationestimates/datasets/populationestimatestimeseriesdataset

Electricity consumption 1970-2016

0

50

100

150

200

250

300

350

400

1970

1971

1972

1973

1974

1975

1976

1977

1978

1979

1980

1981

1982

1983

1984

1985

1986

(4)

1986

(4)

1987

1988

1989

1990

1991

1992

1993

1994

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

2013

2014

2015

2016

TWh

other

Domestic

Industry

fuel industries

12

Incontrast,electricityprices(measuredintermsofaveragebillpaidfor3,800kWh,tocapturefixedcharges)havebeenconsiderablymorevolatile(Figure3).Oncethebigwaveofgasinvestmentsintheearly1990shadbeencompleted,therewasnoneedformorecapacity.Withsurpluscapacity,increasingcompetitionandfallingfossilfuelprices,thepricedeclinedsteadilyfromthemid-1990s.Whenfossilfuelpricesstartedtosoarfrom2004,electricitypricesnaturallyfollowedinthenowcompetitivewholesalemarket.

Figure3RealIndustrialanddomesticbillsforstandardizedconsumptionlevelSource:BEIS(2017)Notes:CCLisclimatechangelevy,PPPisthePoolPurchasePrice(i.e.thewholesalespotprice),MIDPistheMarketIndexDataProviderpromptwholesalepriceafter2001,EUAisEuropean(CO2)emissionallowanceprice.Thefigureshowsinrealterms-£(2015,deflatedbytheConsumerPriceIndex)thebillsfor‘standard’domesticcustomersconsuming3,800kWh,thatforindustrialcustomersbutusingindustrialpricesfor3,800kWh,thewholesalecostofpurchasingthedomesticdemandprofileandthevariablecostofgeneratingthatpower(thegascostfora50%efficientgasturbineplusitscarboncost).Seeappendixfordetails.

Thedeclineinelectricitydemand(in2013Ofgemhadtorevisedownitsdefinitionof“standard”domesticconsumptionto3300kWh3,300kWh/yrperhousehold)helpedtocontainelectricitybills(thesamewastrueforgasconsumption)butofcoursethiswasconfinedtohomesthatbenefitedfromsuchmeasures.Electricityprices,andinparticulartheimpactonpoorhouseholdsandindustry,becameabigpoliticalissueatjustaboutthesametimethatthegovernmentwasembarkingonEMR.

13

Ofgem,theenergyregulator,doesnotcontrolwholesaleorsupplierprices,butdoesregulatethetransmissionanddistributiontariffsthroughincentiveregulation,initiallyproposing5-yearpricecapsforabasketofgoodsthatareindexedtotheretailpriceindex(RPI)andincludeanefficiency(‘X’)factor,henceRPI-X.ThishasevolvedintoRIIO–(Revenue=Incentives+Innovation+Outputs)lastingfor8yearsandstartingin2013forthetransmissionnetwork.Ofgemhasoversightofthewholesaleandretailmarkets,butpreferstoleavethemtocompetitiontodeliverefficiencyimprovementsandtopassthesethroughtofinalcustomers.

Periodically,asdomesticretailpricesrise,politicians,reflectingtabloidheadlines,callforintervention,pricecaps,orevenrenationalization,andinresponseOfgeminitiatesaninvestigation–in2008theEnergySupplyProbe,reportinginitiallylaterthatyear.5Thiswasfollowedin2014byaCompetitionandMarketsAuthority(CMA)investigationintothetradingpracticesandcompetitivenessofthecountry's‘BigSix’energycompanies.WhiletheCMAfoundthatthewholesalemarketwasworkablycompetitive,theyexpressedconcernovertheretailmarkets,andproposedvariousremedies.6Bythen,howevertheUKwasalreadymovingontoyetanotherroundoffundamentalreform.

3. TheintellectualandpoliticalevolutionofUKElectricityMarketReformTheElectricityMarketReform(EMR)thattookeffectin2013was,withhindsight,alongtimeinintellectualgestation,andfedfrommultiplestrandsofintertwinedconcernsaboutinvestment,environment,andenergyprices.7 Thefirstwasagrowingconcernaboutinvestmentandsecurity.Theoretically,anenergy-onlymarketwouldencouragegeneratorstomark-uptheirofferpricesduringperiodsofscarcity,reflectingthepreviouscapacityelementinthepoolprice.Alsotheoretically,investorswouldpredictfuturescarcityandanticipatehigher(scarcity)prices,whichwouldencouragethemtostartinvestmentsnowfordeliveryatthetimeofpredictedhigherprices.

Severalfactorsunderminethistheoreticalhope.Thefirstisthatfuturesmarketsforelectricityareeitherveryilliquidorabsentformuchmorethanayearahead,whileittakes4-8+yearsfromfinalinvestmentdecisiontoplantcommissioning.Investorsthereforeneedtobeconfidentthatthemarketconditionsoverthenext20-30yearsaremoderatelypredictableonthebasisofexistinglawsandpolicies,andthatdemandandsupplyconditionsaresetbycommercialconditions(Newbery,2015).Evenwithoutotherconsiderations,itwouldbeabraveinvestortocommitbillionsofpoundstoaprojectagainsttheprospectofelectricitypricesrisingtoreflectgrowingscarcity,onhighlyuncertaintimescales,tounknowablelevels,

5Seehttps://www.ofgem.gov.uk/publications-and-updates/energy-supply-probe-initial-findings-report6Seehttps://www.gov.uk/cma-cases/energy-market-investigation7Foranoverviewofmanydebatesandperspectivesatthetime,seevariouschaptersinGrubb,JamasbandPollitt(2007).

14

butsetagainstthepredictablepoliticalpressuresthatwouldarisetocurtailpricerises.Theearly2000salreadysawagrowingdebatebetweeneconomists,largelycastbetweenabstracttheoryandthepracticalrealitiesoflikely‘missingmoney’inthecalculationsofcautiousandrisk-averseinvestors.

Thisproblemwas,however,amplifiedinmultiplewaysbyadditionalconsiderations.Investmentrequiredsomeconfidenceinthepoliticallandscapeandthedeterminantsofmarket-drivenfossilfuelprices,againstwhichonecouldatleastplausiblyestimateorhedge.

First,UKenergypolicyhadbeeninturmoilformostofthepost1997periodwhentheLabourPartycametopower,withargumentsovercoal,gas,renewables,andespeciallynuclearpower.TherewerefourEnergyWhitePapersfrom2003-2011(thelastbeingtheprecursortoEMR).Givensuchpolicyuncertainty,itwouldtakeabraveinvestortopredicttheconstraintsonandinterventionsinfutureelectricitymarketsandhencethelikelyfutureprices.

Second,intheory,thegrowingimperativetowardsenvironmentandparticularlydecarbonisationwastobereflectedthroughcarbonpricing.TheUKmodelofwholesaleelectricitymarketcompetitionhadbeguntodominatediscourseinEurope,andthenaturalcomplementofamarketapproachtoelectricitywastheneedtopricetheCO2externality.TheEuropeanCommissionmoveddeftlytoexploitthemoodofthetimesandintroducetheEuropeanEmissionsTradingSystem(ETS),designedtodelivertheEU’sKyotoemissiontargetswithanEU-widecarbonpricecoveringabouthalfoftotalemissions.

However,theEUETShassignallyfailedtodeliveranadequate,durableandcrediblecarbonpricesignal:itwasindeeddrivenbypolicymakerscreatingasystemintheimageoftheUSsulphurtradingsystem,8andforwhomtheimperativeseemedtobedeliveringarelativelyshort-termemissionstargetbasedonideasofstaticefficiencyratherthanprovidinganythingthatinvestorscouldrelyonformajorinvestments.BytheendofthefirsttradingperiodinDecember2007theemissionsallowancepricehadfallentozero,andalthoughitreachedatacredible€30/tonneCO2inthesecondperiodinearly2008,itcrashedto€15/tonnewiththefinancialcrises,oscillatedaroundthatfortwoyears,andthensankfurthertowellbelow€10/tonne,fromwhichithasyettorecover.Theemissiontargetswereachieved,buttheeconomicchoicebetweencoal,gasandzero-carbongeneration(renewablesandnuclear)investmentdependscriticallyonthelevelofthecarbonpriceovercomingdecades,andinvestorshadwatchedastheEUcarbonpricecollapsedthreetimeswithinthespanoffiveyears.

Third,broaderenvironmentalpolicy,particularlyatthedomestic(UK)level,wassimilarlyunstableandhardtopredict.TheEU’sRenewablesDirective(2009/28/EC)9raisedtherequiredshareofrenewableenergy(notjustelectricity)from12%in2010to20%offinal

8TheUSsystemhadalong-termstableplanandallowedbankingofpermitstoencourageinvestments,withconsiderablesuccess(Schmalenseeetal.1998)9http://eur-lex.europa.eu/LexUriServ/LexUriServ.do?uri=CELEX:32009L0028:EN:NOT

15

energydemandby2020,witheachcountryagreeingitstargetshare.TheUKsigneduptoaparticularlychallengingshare;startingfromoneofthelowestcontributions(barely1%),itstargetof15%impliedadramaticgrowthofrenewables.Withelectricitytheeasiestsectortotackle,thisimpliedforeclosingmuchoftheelectricitymarkettoconventionalgeneration(atleast,measuredbyoutput).TheDirectivealsofailedtoremoveallowancesnowdisplacedbyrenewablesfromtheEUETS,puttingdownwardpressureonthecarbonprice.Totheseconflictingsignalswasaddedaslowlygrowingrealisationthatmassiverenewablesentrywould,ifdelivered,crashthewholesalemarketelectricityprice(anoutcomepredictedinfallingutilitysharepricesandrealisedmostobviouslyIntheGermanwholesalemarket).Thecaseforconventionalinvestmentwasthusfurtherunderminedandmiredinuncertainty.

Thegrowingimperativeforlowcarboninvestmentbecametheotherdrivingconcern.Domestically,theUKClimateChangeAct200810waspassedandprovidesalegalframeworkforensuringthatGovernmentmeetsitscommitmentstotackleclimatechange.TheActrequiresthatemissionsarereducedbyatleast80%by2050comparedto1990levels,andthattheGovernmentcommittoaseriesof5-yearcarbonbudgets.11Yet,UKrenewablessupportpolicywasashambles(seebox),andafteradecadeofpoliticaleffortstorehabilitatethereputationofnuclearpower,thegovernmentalsowantedtofindawaytogetnuclearstationsbuilt.

ForBritainfacedtwoadditionalproblems.FirsttheLargeCombustionPlantDirective(LCPD)andthentheEUIndustrialEmissionsDirectivesettighteremissionslimitsthatwouldforcetheretirementofoldercoalplantunlessrefurbished–aprospectthatformanyseemedriskyanduneconomic.Second,Britain’sfirsttwogenerationsofnuclearpowerstations(theMagnoxandAdvancedGas-cooledreactors)werecomingtotheendoftheirlives.Bytheendofthe2000s,itwasexpectedthatsome12GWoftheoldercoal-firedplant(about20%ofpeakdemand)wouldclosebytheendof2015,whileanadditional6.3GWofagingnuclearplantwouldalsocloseby2016.

Asfossilfuelpricessoaredtowardstheirpeakof2008,therefore,theUKelectricitymodelseemedincreasinglyuntenable,asunderlinedbytwoofficialassessments.First,theUKClimateChangeCommittee-thebodysetuptoguideimplementationoftheClimateChangeAct–concluded(CCC2008)thatamarketstructurebuiltpurelyaroundcompetitionforbuyingandsellingelectronscouldnotdeliverlowcarboninvestment.Addedtothegenericconcernsaboutinvestabilityofthemarketatall,andtheinadequacyofcarbonpricing,electricitypricesdrivenbyshort-rungeneratingcostscouldnotconceivablysupportthecapitalintensivebutcheap-to-runinvestmentsthatcharacterisedlowcarbonsources,whetherrenewablesornuclear.Gasinvestmentswouldatleastbehedgedbybeingabletopassthroughfuelpricesintothemarket;zerocarboninvestmentsincontrastwouldtakeallthepricerisk,ofbothfossilfuelandcarbonpriceuncertainties.TheNETA/BETTAmodel,inotherwords,wasindirect10https://www.legislation.gov.uk/ukpga/2008/27/contents11http://www.theccc.org.uk/about-the-ccc/climate-change-act

16

conflictwiththefundamentalaimoftheClimateChangeAct,whosecorerationalewastogivestrategiccertaintyforlowcarboninvestments.

Box2:ThehistoryofUKrenewablespolicybeforeEMR

The UK government first embraced ‘non-fossil’ energy in 1990when the nuclear power stationswereseparated from the CEGB at privatisation but before it became clear that the markets could not bepersuadedtobuynuclearpower.Anenterprisingcivilservantslippedrenewableenergyunderthebannerofsupportfor ‘non-fossilenergy’.NuclearpowerwassubsequentlywithdrawnfromtheNon-FossilFuelObligation,leavingtheNFFOasamechanismtoensurepremiumpaymentsforelectricitygeneratedfromrenewableenergy.

TheNFFOinvitedcompaniestotenderbidsindifferenttechnologycategories.Suchauctionsruntheriskof“winner’scurse”:projectsthatusedthemostoptimisticassumptionswonbids,butthenhadtofacetherealityofriskinghardmoneyonconstruction.Asignificantnumberofwinnersneverproceededtocompletion.Thiscouldhavebeenresolvedbyrerunningauctions,butUKrenewablesincreasinglylaggedtheContinent,fuellingthedesireforchange.

In 2002, the government switchedpolicy to undifferentiated RenewableObligationCertificates(ROCs). Similar to US ‘Portfolio Standards’, this mandated a fixed and increasing share of renewablegeneration. Retailers were obliged to source an increasing share of their sales from renewables, anobligationdischargedeitherbybuyingROCsorpayingabuy-outpriceof£30/MWh(toassuagefearsofexcessivecosts),withrevenuerecycledbacktotherenewablegenerators.Therenewablegeneratorswereresponsibleforsellingtheiroutputinamarketandbeingresponsibleforimbalances,sodevelopersneededtopredictwholesaleprices,imbalancepaymentsandROCpricesoverthefuturelifeoftheirinvestment.GiventhattheROschemewaswidelycriticised(Newbery,2012bandreferencestherein)investorswouldfurthermoreexpectthatitwouldbereformedandhencewasnotaverydurablecommitment.

Finally,sinceallrenewablescompetedequally,mostofthesupportendedupgoingtotheleastrisky,best-establishedtechnologies–mainlyonshorewindprojectsandco-firingbiomassinexistingpowerstations.ThefactthattheUKdomesticrenewablesmanufacturinghadlostoutinthe1990smeantthatforeignmanufacturerswerethemainbeneficiaries.Thefocusononshorewindcombinedwithlackofanyvisible industrial or innovationbenefits weakenedpublic support, andopposition to planning consentsgrew.By2008,UKrenewablecapacityrankedalmostbottomamongstEuropeancountries,despitetheUKhavingsomeofthebestresources.

Facedwithoverwhelmingevidenceoftheseproblems,thegovernmenthadannouncedin2006intenttoreformthesystemandin2009introduced‘banding’– inwhichthelessdevelopedrenewablesreceivedmultiplecreditstofoster innovation–andcomplementedthepricecapwitha ‘ski-slope’thatensured ROC values would be maintained should targets be overachieved, to give investors the priceconfidence they had been saying all alongwas needed. The UK had in effect been dragged into themessiest,mostcomplicated,andmostexpensivewayofdeliveringfeed-intariffsyetconceived.Source: adapted from Grubb et al (2014), Chapter 9: Pushing further, Pulling deeper: Bridging thetechnologyvalleyofdeath

17

ThenOfgem,theenergyregulator,concernedovertheimpendingthreattoenergysecurity,launchedProjectDiscoveryinJune2009.12Theinstitutionseenbymanyasthechampionandguardianoftheliberalizedenergymodelconcluded(Ofgem2010)that“Theunprecedentedcombinationoftheglobalfinancialcrisis,toughenvironmentaltargets,increasinggasimportdependencyandtheclosureofageingpowerstationshascombinedtocastreasonabledoubtoverwhetherthecurrentenergyarrangementswilldeliversecureandsustainableenergysupplies”.Leavingmetaphoricalbloodontheboardroomfloorassomedirectorsresignedinprotest,Ofgemrecommended“farreachingenergymarketreformstoconsumers,industryandgovernment”.

Shortlythereafter,theLabourGovernmentlosttoaConservativeandLiberalDemocratcoalition,andthenewlyformedDepartmentofEnergyandClimateChangeconsultedonElectricityMarketReforminDecember2010(DECC,2010).ItconcurredwithProjectDiscoverythatthecarbonpricewasnowtoolowtosupportunsubsidizednuclearpower;thewholesaleelectricitypricewassetbyfossilfuelprices(andtheETS),thatensuredthatfossilgeneratorshadanaturalhedgeinthatelectricitypricesmirroredgasandcoalpriceswhilenon-fossilgenerationfacedvolatilewholesaleandROCprices.Itwassimilarlyconcernedthatsecurityofsupplywasrapidlybecominganissuewhilethemarketwasnotdeliveringtherequiredvolumeofrenewables.

Inconclusion,theelectricitymarketwasnotwellsuitedtodeliveringeithersecureorsustainableelectricity–andeven‘affordable’ranghollowpoliticallyasretailelectricitypricescontinuedtorise(figure3),andindustrywarnedaboutthehighfinancingcostsarisingfromthemultipleriskssurroundingthesector.TheUK’smuch-vauntedmodelofliberalisationwasseentobefailingonallthreekeyGovernmentobjectives.

4. Afourleggedbeast?TheEMRpackageTheresultingWhitePaper(DECC,2011)setoutanintellectuallycoherentbasisforelectricitymarketreform(EMR),throughacombinationoffourmechanismsasillustratedinFigure4.ThelackofacrediblecarbonpricewouldbeaddressedbyaCarbonPriceFloor,almostimmediatelyenactedbyHMTreasuryintheBudgetinMarch2011.FossilfuelusedtogenerateelectricitywouldbetaxedtobringtheminimumpriceofCO2upto£16/tonnein2013,risinglinearlyto£30/tonnein2020,andprojectedtoriseto£70/tonneby2030(allat2009prices).13

12http://www.ofgem.gov.uk/markets/whlmkts/discovery/Pages/ProjectDiscovery.aspx13HMTreasury,Budget2011,HC836,March2011

18

Figure4ThefourpillarsofUKElectricityMarketReformSource:Ofgem

WhentheEMRlegislationwasfirstbeingdevelopedin2010-11,theEUETSpricehadhoveredaround€12/tCO2(£10/tCO2)forabouttwoyears,andtheratewassetinrelationtolevelstwoyearsbefore.Thisimpliedatop-upofjustafew£/tCO2in2013,withinitialexpectationthatthiswouldriseslowly(Figure5).HoweverwiththecollapseoftheETSpriceduring2011,thetop-uprequiredwhenwrittenintothelegislationby2013actuallyescalatedveryrapidly.

Figure5:Carbonpricesupport,asseenbytheUKTreasuryininitialdevelopmentoftheEMR

Asanytaxcouldbechangedwitheverybudget(andtheCarbonPriceFloorwasindeedsubsequentlycapped,asexplainedlater),thispolicywasbuttressedbyanEmissionsPerformanceStandard(EPS)thatwouldlimitemissionsfromanynewpowerstationto

19

450gm/kWh“atbaseload”,intendedtoruleoutanyunabatedcoal-firedstation(withexemptionsforthedemonstrationCarbonCaptureandStorage,CCS,stationswhichwouldonlyrequireathirdorlessofoutputtobesubjecttocarboncapture).14TheEmissionsPerformanceStandardhadfollowedonfromexperienceofalongbattleoverplansforanewcoalplantatKingsnorthinKent,whichE.Onhadproposedin2006,andservedtoremoveanyambiguityaboutUKpolicytowardscoal.15

Intermsofpolicydesign,thesetwostepswererelativelystraightforward.Thethornyissuesconcernedhowbesttosupportlowcarboninvestment,andhowtoensuresystemsecurity.TheUK’scarbonandrenewablestargetswereestimatedtorequireover£12billioninvestmentperyear(comparedwithlessthan£5billionin2008,whichwasnearly80%abovethepreviousdecadeaverage).16Thiswasconsiderablyabovefinancialanalysts’estimatesofthecapacityoftheBigSixtofinanceandsonewsourcesoffinancewereneeded.Allzero-carbongenerationhasveryhighcapitalcostsandverylowvariablecosts,whichmakestheircosthighlysensitivetotheWeightedAverageCostofCapital(WACC).By2020thecumulativeinvestmentingenerationalonewouldamountto£75billion(DECC,2011)andiftheWACCcouldbereducedby3%(astheauctiondiscussedbelowdemonstrated),theconsumercostwouldbereducedby£2.25billionperyear(ifallattributedtohouseholdsthisisabout15%ofatypicalelectricitybill).Lowerriskenablinghigherdebtmadethiseminentlyfeasible.AstheROschemeplacedallthemarketpriceandpolicyriskondevelopers,replacingthisbyafixed-pricecontractwouldconsiderablyreduceriskandhenceencouragenewfinanceandentry.

14Theforceof“baseload”issomewhatunclear.Ifitistakenas8760hrsperyear,thenaconventionalcoal-firedstationwithemissionsof900gm/kWhcouldoperateatacapacityfactorof50%,andiftheCCSelementemitted90gm/kWhon400MW(gross,300MWnet)ofa1,600MW(gross)supercriticalstation(44%efficient),theremaining1,200MWmightbeabletooperateatacapacityfactorof78%,belowitsnormaldesignrating.TheWhitePaper(at1.22)thereforeallowsforexemptionsforsuchdemonstrationplant.OthergovernmentdocumentsstatethatthePerformanceStandardisintendedtoruleoutanynewcoalwithoutCCS,andtheNationalPolicyStatementforFossilFuelElectricityGeneratingInfrastructure(EN-2)statesthatanynewcoal-firedpowerplantdemonstrateCCSonatleast300MW(net)oftheproposedgeneratingcapacityasaconditionofitsconsent(https://www.gov.uk/government/uploads/system/uploads/attachment_data/file/266882/EPS_Policy_Brief_RA.pdf).15E.Onarguedthatanewcoalplantwouldreduceemissionsbydisplacingolder,lesseffectplant;andlater,thatitwouldbebuild“captureready”(ie.toincludeCCStechnologyasandwhenitbecamecommerciallyviable).Afterthreeyearsofintensecontroversy,theUKgovernment‘deferred’aplanningdecision,andshortlyafterwardstheprojectwasabandoned,withrecognitionofitsincompatibilitywiththeessentialthrustofUKpolicyandtheClimateChangeAct.16£4.3billionat2005prices(OfficeofNationalStatistics)

20

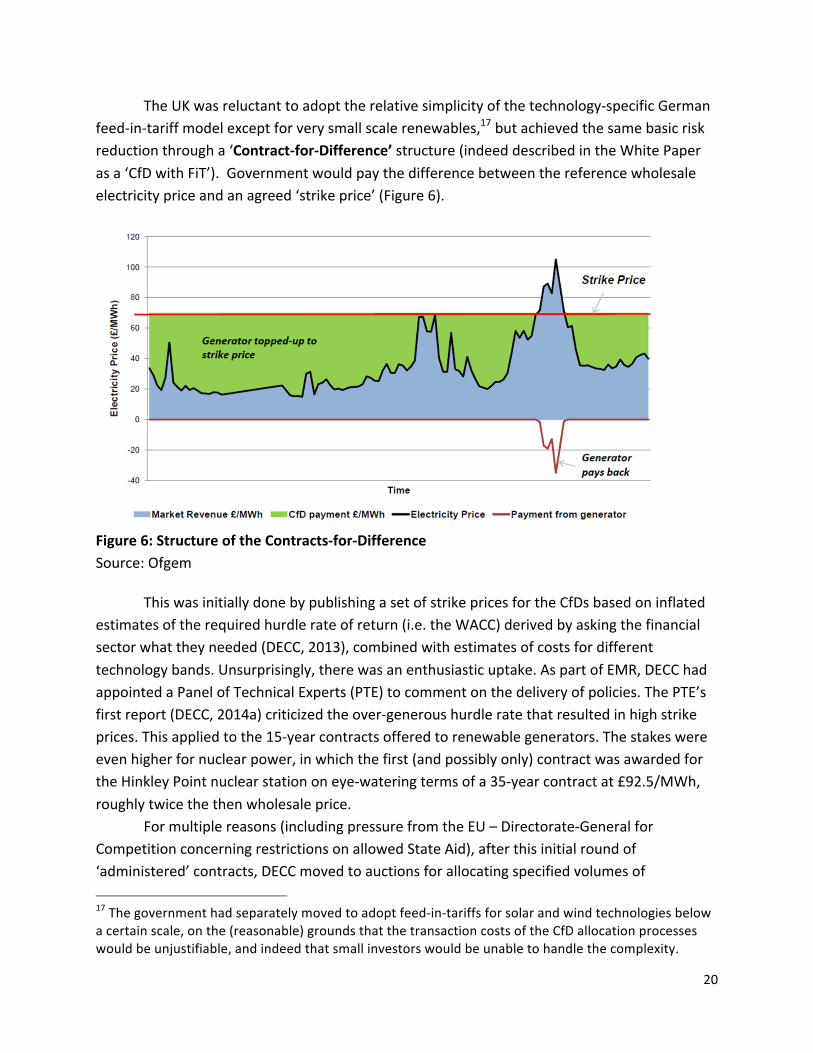

TheUKwasreluctanttoadopttherelativesimplicityofthetechnology-specificGermanfeed-in-tariffmodelexceptforverysmallscalerenewables,17butachievedthesamebasicriskreductionthrougha‘Contract-for-Difference’structure(indeeddescribedintheWhitePaperasa‘CfDwithFiT’).Governmentwouldpaythedifferencebetweenthereferencewholesaleelectricitypriceandanagreed‘strikeprice’(Figure6).

Figure6:StructureoftheContracts-for-DifferenceSource:Ofgem

ThiswasinitiallydonebypublishingasetofstrikepricesfortheCfDsbasedoninflatedestimatesoftherequiredhurdlerateofreturn(i.e.theWACC)derivedbyaskingthefinancialsectorwhattheyneeded(DECC,2013),combinedwithestimatesofcostsfordifferenttechnologybands.Unsurprisingly,therewasanenthusiasticuptake.AspartofEMR,DECChadappointedaPanelofTechnicalExperts(PTE)tocommentonthedeliveryofpolicies.ThePTE’sfirstreport(DECC,2014a)criticizedtheover-generoushurdleratethatresultedinhighstrikeprices.Thisappliedtothe15-yearcontractsofferedtorenewablegenerators.Thestakeswereevenhigherfornuclearpower,inwhichthefirst(andpossiblyonly)contractwasawardedfortheHinkleyPointnuclearstationoneye-wateringtermsofa35-yearcontractat£92.5/MWh,roughlytwicethethenwholesaleprice.

Formultiplereasons(includingpressurefromtheEU–Directorate-GeneralforCompetitionconcerningrestrictionsonallowedStateAid),afterthisinitialroundof‘administered’contracts,DECCmovedtoauctionsforallocatingspecifiedvolumesof17Thegovernmenthadseparatelymovedtoadoptfeed-in-tariffsforsolarandwindtechnologiesbelowacertainscale,onthe(reasonable)groundsthatthetransactioncostsoftheCfDallocationprocesseswouldbeunjustifiable,andindeedthatsmallinvestorswouldbeunabletohandlethecomplexity.

21

renewables,dividedintoone‘pot’fordevelopedtechnologies,andoneforlessdevelopedtechnologies.Asdescribedinthenextsection,Newbery(2016a)estimatesthattheresultingclearingpricesforon-shorewindloweredtheWACCby3%real.Unfortunately,theConservativeGovernment,initsbidforre-electionin2015andtoappealtoitsruralconstituencies,ruledoutsupportingon-shorewind–andalongwithit,alltheotherdeveloped‘pot1’renewabletechnologies-sothedramaticreductioninsupportpricesforon-shorewindonlysurvivedoneauctionround.

ThefourthandfinalstrandofEMRwasdirectedtoensuringsecurityofsupply,throughintroductionofaCapacityMechanism.Afterextensiveinternaldebateandexplorationofinternationalexperience,thegovernmentrejectedtheideaofpaymentstargetedtonewentrants(a‘StrategicReserve’),infavourofsystem-widepaymentstoallgeneratorswhocouldcontracttogeneratewhenevercalleduponbytheSystemOperator,NationalGrid.Wieldingthefearof‘lightsgoingout’,DECCovercameTreasuryscepticismabouttheneedforanycapacitymechanism,whilstOfgemamongstothersarguedthattargetedsupportsfornewentrantswouldcreateperverseincentives,forexample,foracompanytoclosedownoneplantinordertogetsubsidiestoopenanother.Theprevailingviewbecamethatcapacitypaymentswouldineffectbeamarketforreliablecapacity,withafixedpayment(theclearingpriceofthe‘descendingclockreverseauction’)toallwhocouldprovideit.Theassumptionbehindthedesign,however,wasthattheUK’smainneedwasfornewCCGTs,andthesystemwasdesignedaccordinglywithauctionsheldfordelivery4-yearsahead–allowingbothformajorrefurbishmentandnewplant,withthelatterbeingoffered15-yearcapacitycontracts.

TheauctionvolumeswouldbedecidedbytheMinisteronthebasisofadvicefromNationalGridonthecapacityneededtomeettheUK’ssecuritystandard-ofaLossofLoadExpectationof3hrsperyear(onaverageoveralargenumberofyears)–togetherwithestimatesofthe‘de-ratingfactor’toreflecttechnology-specificplantavailability.

Theinstitutionalset-upbehindthisstructurewasitselfachallenge.Thegovernmentcreatedaseparate,government-backedbody(theLowCarbonContractsCompany)tobethecounterpartyforCfDcontracts,whilstNationalGridischargedwithbothrunningtheCapacityandtheCfDauctions.Toprovideaddedscrutinyandaddressfearsofconflictsofinterest,anindependentPanelofTechnicalExperts(PTE)wasestablished,initiallytoadviseonthedetaileddesign,andthentoscrutiniseandchallengeinparticularNationalGrid’sadviceoncapacityprocurement.Theprocesswasunderpinnedwithanefforttoensuretransparency,withforexampletheanalysisforcapacityprocurementofbothNationalGridandthePTEpublishedeachyear(forexampleinthefirstyearasNationalGrid(2014)andDECC(2014)).TheMinisterwouldthenchoosetheamountofde-ratedcapacitytoprocureinaDecemberauctionthatyearfordeliveryinfouryears’time(hencethe“T-4auction”),supplementedbyyear-aheadauctionsforadditionalresources(includingdemand-sideresponse)

22

5. ResultstodateThisreportiswritten(late2017)somefouryearsaftertheUK’sElectricityMarketReformwasenactedandthefirstadministeredcontractsawarded,andalmostthreeyearsafterthefirstauctions.Thissectionsummarisesthemainresultstodate.

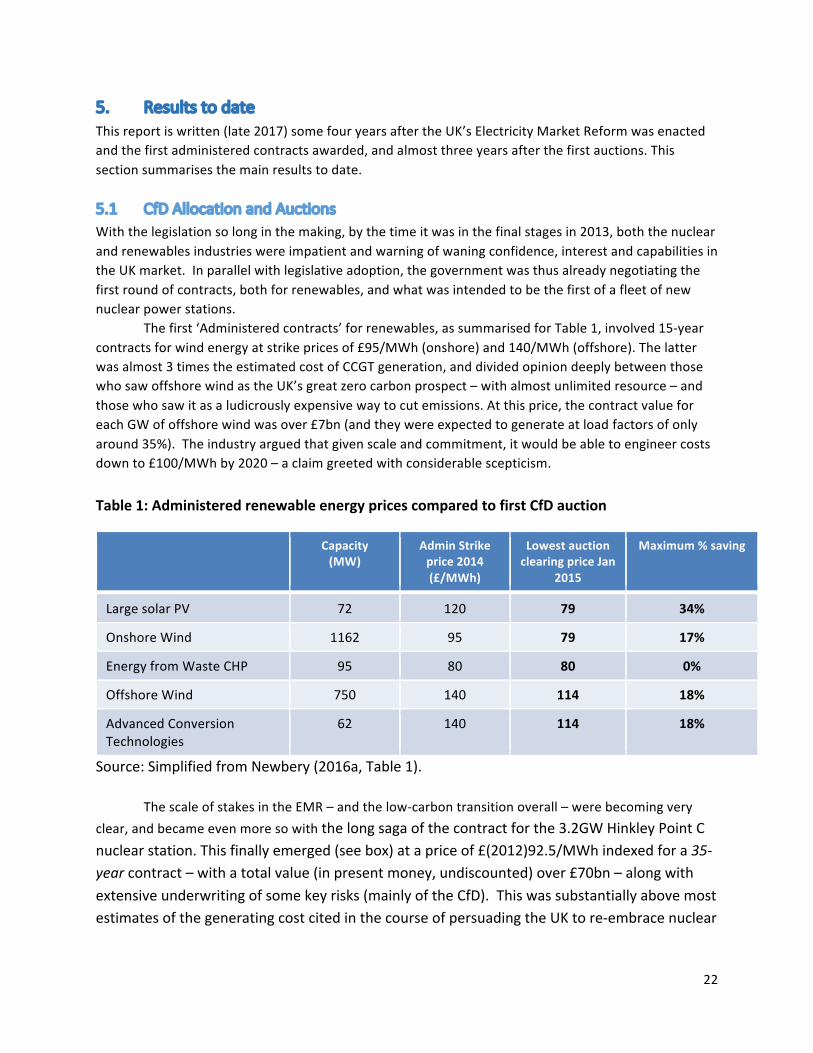

5.1 CfDAllocationandAuctionsWiththelegislationsolonginthemaking,bythetimeitwasinthefinalstagesin2013,boththenuclearandrenewablesindustrieswereimpatientandwarningofwaningconfidence,interestandcapabilitiesintheUKmarket.Inparallelwithlegislativeadoption,thegovernmentwasthusalreadynegotiatingthefirstroundofcontracts,bothforrenewables,andwhatwasintendedtobethefirstofafleetofnewnuclearpowerstations. Thefirst‘Administeredcontracts’forrenewables,assummarisedforTable1,involved15-yearcontractsforwindenergyatstrikepricesof£95/MWh(onshore)and140/MWh(offshore).Thelatterwasalmost3timestheestimatedcostofCCGTgeneration,anddividedopiniondeeplybetweenthosewhosawoffshorewindastheUK’sgreatzerocarbonprospect–withalmostunlimitedresource–andthosewhosawitasaludicrouslyexpensivewaytocutemissions.Atthisprice,thecontractvalueforeachGWofoffshorewindwasover£7bn(andtheywereexpectedtogenerateatloadfactorsofonlyaround35%).Theindustryarguedthatgivenscaleandcommitment,itwouldbeabletoengineercostsdownto£100/MWhby2020–aclaimgreetedwithconsiderablescepticism.Table1:AdministeredrenewableenergypricescomparedtofirstCfDauction

Capacity(MW)

AdminStrikeprice2014(£/MWh)

LowestauctionclearingpriceJan

2015

Maximum%saving

LargesolarPV 72 120 79 34%

OnshoreWind 1162 95 79 17%

EnergyfromWasteCHP 95 80 80 0%

OffshoreWind 750 140 114 18%

AdvancedConversionTechnologies

62 140 114 18%

Source:SimplifiedfromNewbery(2016a,Table1).

ThescaleofstakesintheEMR–andthelow-carbontransitionoverall–werebecomingveryclear,andbecameevenmoresowiththelongsagaofthecontractforthe3.2GWHinkleyPointCnuclearstation.Thisfinallyemerged(seebox)atapriceof£(2012)92.5/MWhindexedfora35-yearcontract–withatotalvalue(inpresentmoney,undiscounted)over£70bn–alongwithextensiveunderwritingofsomekeyrisks(mainlyoftheCfD).ThiswassubstantiallyabovemostestimatesofthegeneratingcostcitedinthecourseofpersuadingtheUKtore-embracenuclear

23

power,andassumedbytheClimateChangeCommitteeinrecommendinganewfleetofnuclearaspartofitsdecarbonisationstrategy.18

Theperceptionthatthemainproponent,ElectricitédeFrance(EdF),hadrunringsaroundthegovernmentandsecuredanoverpricedcontract(Box3)receivedaknockingwhen–

18Seehttps://www.theccc.org.uk/2011/08/09/confused-about-costs-of-nuclear-v-renewables-read-on/wheretherangeofcostswasgivenas£40-100/MWhby2030,whereasrenewableswereexpectedtocost£75-135/MWh.

Box3The(almost)‘mostexpensiveobjectontheplanet?’–theHinkleyPointCnuclearcontract

TheUK’s1980sefforttodevelopa‘newnuclearfamily’,basedonFrenchPressurisedWaterReactortechnology,wasoneofthemajorvictimsofprivatisationin1990,withonlytheonealreadycommittednewplant(theSizewell‘B’reactor)proceeding.Asidefromanyenvironmentorsafetyconcerns,nuclearpowerwasacknowledgedtobeuncompetitiveinaliberalisedelectricitymarketandfellintopublicdisrepute.

ThepoliticalrehabilitationofnuclearpowertookafulldecadefromTonyBlair’selectionin1997,andculminatedthefirstnuclearcontractforageneration,astorydetailedelsewhere(Taylor,2016).TheneedtoreduceCO2emissions,combinedwiththepromiseofeconomicbaseloadpower,formedthetwinplanksofthelong‘charmoffensive.’TheClimateChangeCommittee,abodygenerallywelcomedalsobytheenvironmentalmovement,arguedin2008thatthecountryatminimumneededtore-establishnuclearpowercapabilitiesasoneofthethreecoretechnologyoptionsfordeepdecarbonisation(alongwithrenewablesandCCS).ThenewEuropeanPressurisedWaterReactor,ofwhichtwowereunderconstruction,wasexpectedtocostaround£50-60/MWh.

PublicopiniongraduallyshiftedandnuclearwasfirmlyontheagendaoftheEMRlegislation.Havingbeenburntbyconstructioncostoverrunsinthepast,thestructureofContractsforDifferencewasseenasideal.HistoryhadmadeeveryoneleeryofdirectgovernmentfundingforsuchriskyprojectsandtheCfDstructureenabledthegovernmenttoside-stepdebatesaboutwhetherthiswouldbeasubsidy(orhowbig)–thatwoulddependonfuturewholesaleelectricityprices.Theprivatesectorwouldhavetobearalltheconstructionrisks,inreturnfortheguaranteedelectricityprice.

HinkleyPointC,withtheEPRdesign,waschosentobethefirstofthenewfamily.Withvariousindustrialturmoilamongstthecompaniesinvolved,theUKgovernmentbrokeredChineseinvolvementtoinjectadditionalcapital(withthepromiseoffuturenuclearconstructioncontracts).Bythen,bothoftheEuropean‘demonstration’projectswereintrouble.During2013,variedleaksfromthenegotiationsbetweenthegovernmentandtheEdF-ledconsortiumpointedtopricesfarhigherthanexpected.Thefinalcontractofferedlandedat£92.50/MWh,index-linkedandguaranteedfor35years,withtheplantexpectedtostartgeneratinginthemid-2020s–implyingacontractworthover£70bn(over$100bn)undiscounted,runningtoalmost2060.

Criticssoondubbedit‘themostexpensiveobjectontheplanet’,aclaimdisputedbyEdFpointingtoAustralia’smassiveliquefiedgas(LNG)terminaldevelopments.Theextenttowhichthecontractamountstoasubsidyofcoursedependedonwholesaleelectricitypricesprojectedoutovercomingdecades;withgasandwholesalepricesdeclining,alongwithdecliningrenewableenergycosts,successiveParliamentaryenquiriesratcheteduptheestimatedimpliedsubsidyto£30bn,andevenmoreinmostrecentestimates.ItremainstobeseenwhetherandwhenHinkleyPointCdoesenteroperation,andwhetherit,likeSizewellBagenerationbefore,itturnsouttobeasolitarymemberofthepromised‘family.’

24

despitemajorfinancialinjectionfromaChinesepartnerontheproject–itsplittheEdFBoard,withtwoDirectors(includingtheFinancedirector)resigning,andfinalapprovalonlycarryinga10:7majority.Morethananythingelse,itallunderlinedthecentralityofthefinancechallenge–thoseopposingfearedthatthe£15-20bnconstructioncostwouldbankruptthecompanybeforetheplantbegantogenerate–alongwiththecompleteimplausibilityofanyprivateentitybuildingnuclearwithoutmassivegovernmentinvolvement.

FortheEMRitselfhowever,betternewswasaroundthecornerwiththefirstcompetitiveauctionofrenewableCfDcontracts,heldbarelysixmonthsaftertheadministeredcontracts,withtheresultsshowninthefinalcolumnsofTable1.Newbery(2016a)arguesthattheclosejuxtapositionofthesecontractsprovidesanidealnaturalexperiment.Althoughbothinvolved15-yearcontracts,thefirstwereconductedinparallelwiththeoperationoftheROCssystem,andcompaniescoulduseprojectsconstructedunderthisregimeastheirevidenceforcosts,andrequiredratesofreturn,asindicatedpreviously.Withthemovetoauctions,thisnolongerapplied;thecontractswouldgotothoseofferingthebestvalue,includinglowestcostofcapital,irrespectiveofcostsunderthefarmorevolatileanduncertainROCssystem.UsingtheresultsinTable1,Newberyestimatesthatthemovetocompetitiveauctionsloweredthecostofcapitalfromabout6%to3%-which,translatedtothe£75+bnexpectedinvestmentrequiredoverthedecade,wouldtranslateintoa£2.25bnannualsavingfor15years.19

Levycontrol,thehiatus,andSecondAuction

Shortlyafterthesefirstrenewablesauctioncontractswereawarded,however,aGeneralElectionusheredinreneweduncertainty.Underthecoalitiongovernment,theChancellorGeorgeOsbornehadplacedacapontheoveralllevythatcouldbechargedontoconsumersamountingto£7.6bn/yr(2011/12prices)by2020/21.Heretainedhispost,andalongwithcolleaguesintheConservativepartywasnotamusedasitbecameclearthatthiscapwasgoingtobebreached,formultiplereasons.OverlygenerousPVfeed-in-tariffshadledtoanunexpectedexplosivegrowth(almost10GWcomparedtoanexpected1.5GW),beforetariffreductionscouldkickin.Thepost-2014fallingasandhencewholesaleelectricitypricesincreasedthesubsidyelementintheCfDcontracts.Andtheoffshorewindfarms,inparticular,weregeneratingsubstantiallymoreoutputthanexpected,increasingofcoursethepayoutstothem(Grubb,2015).

19Specifically:“Thedifferencesfromvaryingthetechnologyassumptionsaresmall,suggestingthattheloweringoftheWACCofsome3%realperyearisrobust.ThisismaterialasDECC[49]estimatedthattheWACCforon-shorewindmightfallfrom8.3%undertheROschemeto7.9%withaCfD,orby0.4%(allreal).IftheimpliedWACCisreducedby3.3%throughauctionsthenthesavingongenerationinvestmentof£75billionupto2020[35]wouldbe£2.5billionperyearby2020,continuingfor15years.ThecontraryviewthattheROprovidesabetterhedgethanCfDs[50]mightbetrueforportfolioutilitiesbuttheEMRwasintendedtoencouragenewsourcesoffinanceandappearssuccessful,consistentwiththeexperienceelsewhere”(Newbery2016a,p.1325)

25

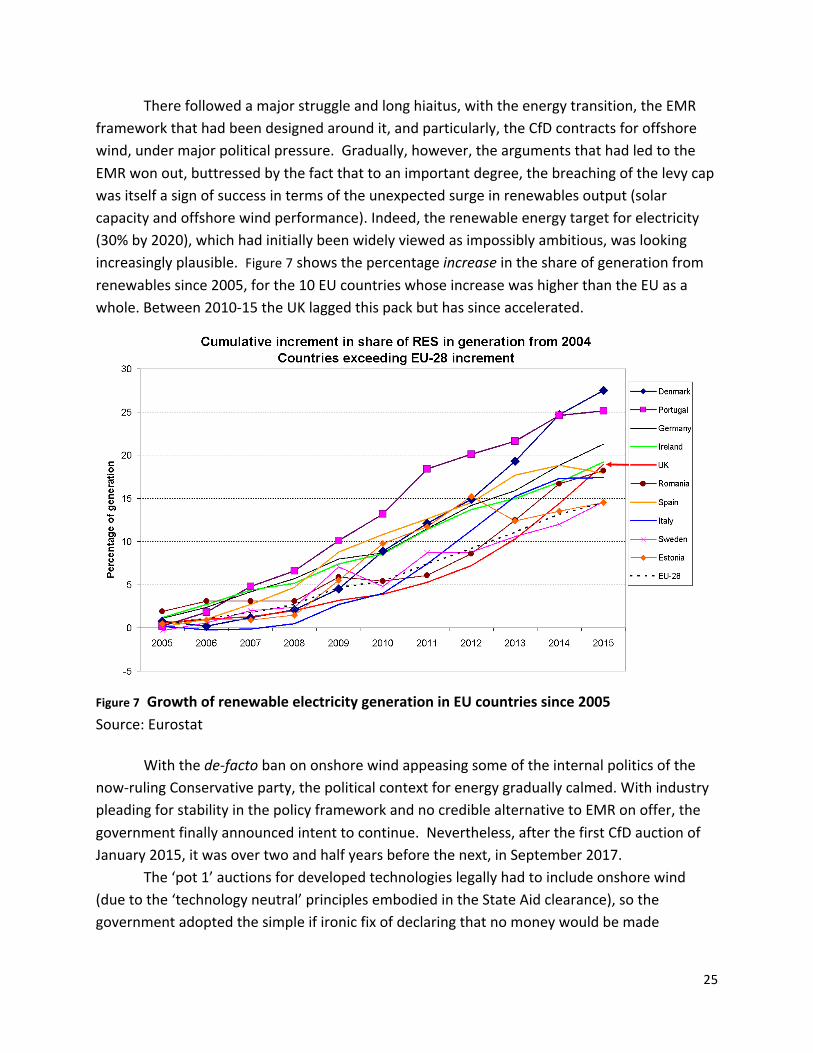

Therefollowedamajorstruggleandlonghiaitus,withtheenergytransition,theEMRframeworkthathadbeendesignedaroundit,andparticularly,theCfDcontractsforoffshorewind,undermajorpoliticalpressure.Gradually,however,theargumentsthathadledtotheEMRwonout,buttressedbythefactthattoanimportantdegree,thebreachingofthelevycapwasitselfasignofsuccessintermsoftheunexpectedsurgeinrenewablesoutput(solarcapacityandoffshorewindperformance).Indeed,therenewableenergytargetforelectricity(30%by2020),whichhadinitiallybeenwidelyviewedasimpossiblyambitious,waslookingincreasinglyplausible.Figure7showsthepercentageincreaseintheshareofgenerationfromrenewablessince2005,forthe10EUcountrieswhoseincreasewashigherthantheEUasawhole.Between2010-15theUKlaggedthispackbuthassinceaccelerated.

Figure7GrowthofrenewableelectricitygenerationinEUcountriessince2005Source:Eurostat

Withthede-factobanononshorewindappeasingsomeoftheinternalpoliticsofthenow-rulingConservativeparty,thepoliticalcontextforenergygraduallycalmed.WithindustrypleadingforstabilityinthepolicyframeworkandnocrediblealternativetoEMRonoffer,thegovernmentfinallyannouncedintenttocontinue.Nevertheless,afterthefirstCfDauctionofJanuary2015,itwasovertwoandhalfyearsbeforethenext,inSeptember2017.

The‘pot1’auctionsfordevelopedtechnologieslegallyhadtoincludeonshorewind(duetothe‘technologyneutral’principlesembodiedintheStateAidclearance),sothegovernmentadoptedthesimpleifironicfixofdeclaringthatnomoneywouldbemade

26

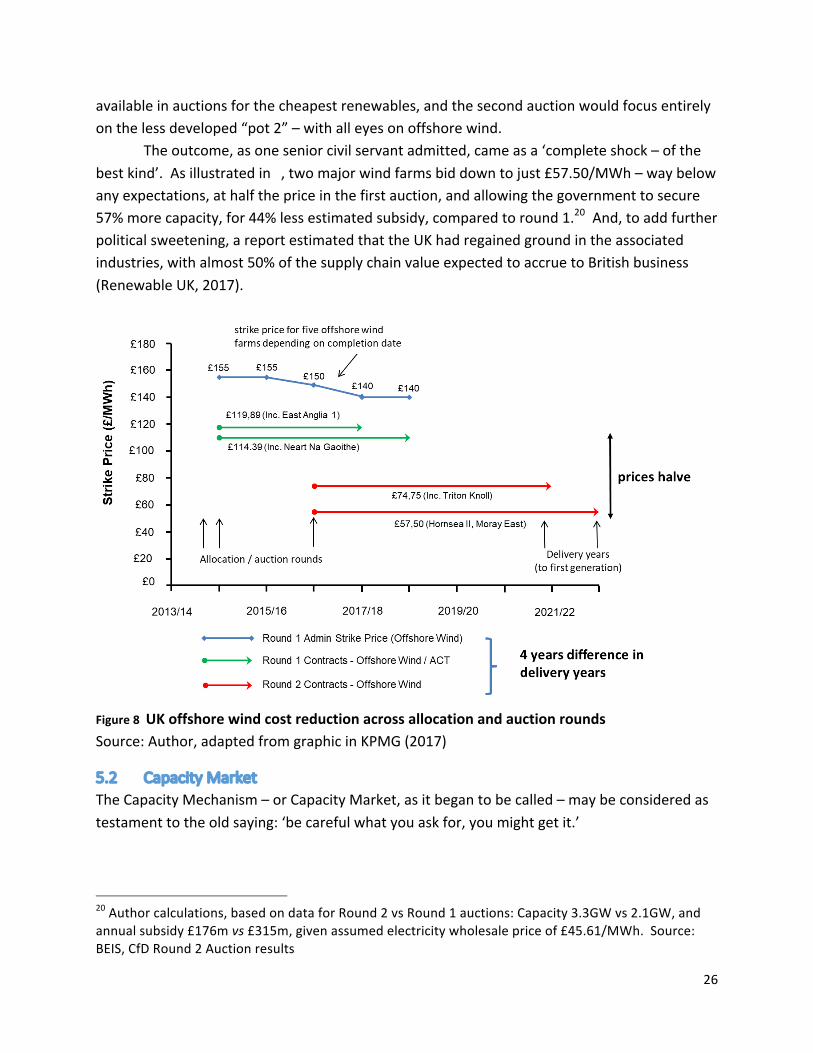

availableinauctionsforthecheapestrenewables,andthesecondauctionwouldfocusentirelyonthelessdeveloped“pot2”–withalleyesonoffshorewind.

Theoutcome,asoneseniorcivilservantadmitted,cameasa‘completeshock–ofthebestkind’.Asillustratedin,twomajorwindfarmsbiddowntojust£57.50/MWh–waybelowanyexpectations,athalfthepriceinthefirstauction,andallowingthegovernmenttosecure57%morecapacity,for44%lessestimatedsubsidy,comparedtoround1.20And,toaddfurtherpoliticalsweetening,areportestimatedthattheUKhadregainedgroundintheassociatedindustries,withalmost50%ofthesupplychainvalueexpectedtoaccruetoBritishbusiness(RenewableUK,2017).

Figure8UKoffshorewindcostreductionacrossallocationandauctionroundsSource:Author,adaptedfromgraphicinKPMG(2017)

5.2 CapacityMarketTheCapacityMechanism–orCapacityMarket,asitbegantobecalled–maybeconsideredastestamenttotheoldsaying:‘becarefulwhatyouaskfor,youmightgetit.’

20Authorcalculations,basedondataforRound2vsRound1auctions:Capacity3.3GWvs2.1GW,andannualsubsidy£176mvs£315m,givenassumedelectricitywholesalepriceof£45.61/MWh.Source:BEIS,CfDRound2Auctionresults

27

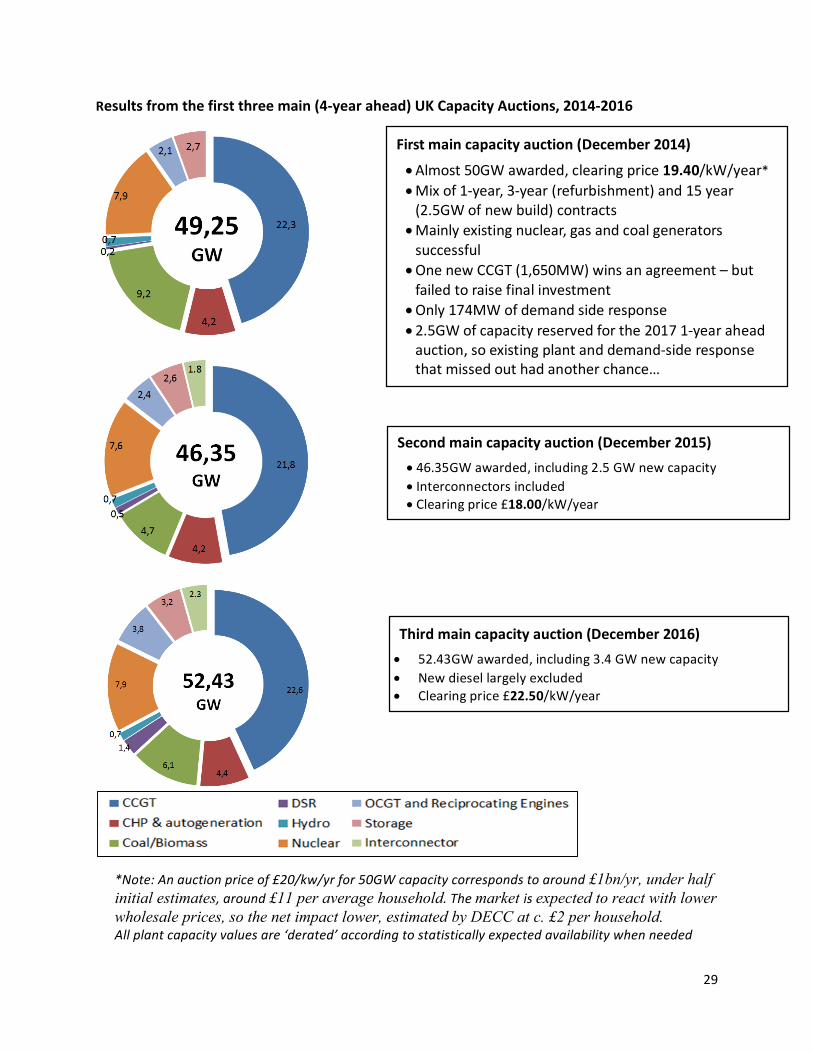

Resultsfromthefirstthreemain(4-yearahead)UKCapacityAuctions,2014-2016

*Note:Anauctionpriceof£20/kw/yrfor50GWcapacitycorrespondstoaround£1bn/yr, under half initial estimates,around£11 per average household.Themarket isexpected to react with lower wholesale prices, so the net impact lower, estimated by DECC at c. £2 per household. Allplantcapacityvaluesare‘derated’accordingtostatisticallyexpectedavailabilitywhenneeded

Figure9showstheresultsofthemaincapacityauctions,heldfordeliveryofcapacityfour-years

28

ahead(“T-4”)overthefirstthreeyears`oftheEMR.

29

Resultsfromthefirstthreemain(4-yearahead)UKCapacityAuctions,2014-2016

*Note:Anauctionpriceof£20/kw/yrfor50GWcapacitycorrespondstoaround£1bn/yr, under half initial estimates,around£11 per average household.Themarket isexpected to react with lower wholesale prices, so the net impact lower, estimated by DECC at c. £2 per household. Allplantcapacityvaluesare‘derated’accordingtostatisticallyexpectedavailabilitywhenneeded

Firstmaincapacityauction(December2014)

•Almost50GWawarded,clearingprice19.40/kW/year*•Mixof1-year,3-year(refurbishment)and15year(2.5GWofnewbuild)contracts•Mainlyexistingnuclear,gasandcoalgeneratorssuccessful•OnenewCCGT(1,650MW)winsanagreement–butfailedtoraisefinalinvestment•Only174MWofdemandsideresponse•2.5GWofcapacityreservedforthe20171-yearaheadauction,soexistingplantanddemand-sideresponsethatmissedouthadanotherchance…

Secondmaincapacityauction(December2015)• 46.35GWawarded,including2.5GWnewcapacity• Interconnectorsincluded• Clearingprice£18.00/kW/year

Thirdmaincapacityauction(December2016)• 52.43GWawarded,including3.4GWnewcapacity• Newdiesellargelyexcluded• Clearingprice£22.50/kW/year

30

Figure9:Resultsofmaincapacity(four-yearahead)auctions

Thefirstauction,heldinDecember2014,wasfordeliveryof50GWcommittedcapacitybywinter2018/19.21Basedontheestimated‘netCostofNewEntry’–whichwasinterpretedasthepricerequiredtosupportanewCCGTinvestmentabovetherevenueearnedinthemarket–thegovernmentprojectedthelikelyclearingpricetobe£49/kW,andfromthisderivedanestimateddemandcurve,andsetapricecapof£75/kW(1.5xnetCoNE).

Intheevent,theauctionclearedat£19.40/kW,andonlyoneCCGTcompany(withtwoturbines)stayedintobeofferedsuchacontract(aftertwoyearsofstrugglingtoraisefinance,itfinallywithdrewinDecember2016).Themajorbeneficiarieswere,ofcourse,existingcoal,gasandnucleargenerators.Thiswasasexpectedbythoseinvolved,butwasthefirstdawningofrealityforthosewhohadnotunderstoodthefullimplicationsofasystem-wideauction,andledtoastormofprotestaboutthegovernmentsubsidisingpreciselythetypeofplant(coal)thatitclaimedtobetryingtogetridof.

AnothersourceofmoreinternaldisquietwasthatInterconnectors(theUKhadabout4GWofconnectionstocontinentalEuropeandmorewasbeinginvestigated)werenotincluded.22Thisbecameasourceofstrongdebatewithinallthebodiesconcerned–theevidencewasunambiguousthatinterconnectorswerenotonlypredominantlyasourceofimports,thuscontributingtosecurity,butthatimportswouldbeevenmorelikelyintimesofsystemstresswhenUKwholesalepriceswouldbeveryhigh(NewberyandGrubb,2015).AdecisiveinterventionthencamefromtheEuropeanCommissionwhichruledthatexcludinginterconnectionwasclearlyagainstEUmarketprinciplesofnon-discrimination,andonlygavestate-aidapprovalforthefirstcapacityauctionprovidedinterconnectorswereincludedinsubsequentrounds.TheirabsenceinthecalculationbuttheircontributionmadeupfortheshortfallfromthewithdrawnnewCCGTplant.

ThenextyearconfirmedagainthatUKelectricitydemandwasactuallyfallingnotrising

(atleastattransmissionlevel),andthecapacityprocuredforthesecondauctionwaslower.However,coalplantwasbeginningtocloseatpace,forreasonsindicatedlater(inadditiontothelowvalueofcapacitypayments)–includingsomewhichhadcapacitycontracts,thuspromptingthegovernmentintoholdinga1-year-aheadauctionearlierthanplanned,andincreasingthevolumetobeprocuredinthenext1-year-aheadauctiontocoverforcancelledcapacitycontracts.

21Ofthetotalprojectedneedforaround52.5GW,2.5GWwasheldasidetoensuresomeroomfora1-yearaheadauctionin2017,toprovidescopefornearer-termadjustment,andshorter-termoptionslikedemand-sideresponse.22Moreprecisely,NationalGridtookthehighendofitscapacityrangeof53.3GWonthebasisthatimportscouldnotbereliedupon(NationalGrid,2014,p10-11).

31

Figure10:NewcapacityintheCapacitymarket,bidsandapproved,2014-2016

Note:Theupperpanel(a)showsthenew-buildcapacitybiddingfor15yearcontracts,dividedbetweenplantsbiggerorsmallerthan100MW.Thelowerpanel(b)showsthetypesofgenerationawardedcontracts,excludinga1.65GWCCGTplantfromthefirstauctionwhichabandonedeffortstosecurefundingtwoyearslater,andabout95MWofOCGTandreciprocatingengineplantsfromthefirsttwoauctionswhichalsodidnotproceed.Someofthelatestnewbuildoptedtotakejustone-yearcontractsfor2020,hopingthatsubsequentcapacitymarketauctionswillyieldhigherprices.

Bythistime,manymoresmallergeneratorshadrealisedtheopportunityofthecapacitymechanism,andalongwithinterconnectors,thesecondauctionsawmanycontractsgoingtosmall-scalegenerators(Figure10b)–notably,reciprocatingenginespoweredbygasordiesel,withanevenlowerclearingpriceof£18/kW.yr.

32

Dieselwasclearlyacarbon-intensivefuelanditsimagewasfurtherworsenedbytheVWvehiclesscandal.Inprinciple,theseplantsareunlikelytobeusedmuch–mostofthisnewbuildisofthecheapcapital,23highrunningcostplantappropriatetoaroleofjustmeetingextremesystemneeds,thoughthiscouldn’tbeguaranteed.Politically,thefactofbeingseentosubsidisedieselpowerstations,insteadoftherelativelycleanandefficientCCGTsexpected,washighlyproblematic. Theexperienceunderlinedtheunexpected:grosscapacityrequirementssofarhaveturnedoutlowerthantheauctionvolumesset,andyetthesystemhadbecomesomewhatmoredependentonyear-aheadauctionsthanoriginallyenvisagedbecauseofcancelledcontractsfornewbuild.The2017PTEreport(DECC2017)arguedthereneededtobemoreattentiontodemandsideresponseandthe‘latentcapacity’ofthesystemtohandlestressevents,togetabetterbalanceofcostsandhencereducetheinevitableinstitutionalandpoliticalpressurestoover-procure. Moreover,amajoranomalysoonbecameapparent,arisingfromthefactthatgenerationconnectedatdistributionlevel(i.e.notfeedingdirectlyintothemaintransmissionnetwork)avoidedbothgenerationandloadtransmissioncharges.Inthepreviouseraofrelativelylowtransmissionchargesandasmallvolumeofsuch‘embeddedgeneration’thishadbeenseenasbothrational,andpositiveasanencouragementtonew,localisedgeneration.Astransmissionchargesgrew,asthevolumesgrew,andwiththeCapacityMechanismpayingcentrallyforsourcesintendedtobeusednationallyineventofneed,whereverconnected,itrapidlycametobeseenasadistortionthataccountedforthedominanceofsmall-scalesourcesatunrealisticallylowprices(seeBox).Theconcernsreachedcrescendowhenastaggering8.7GWof‘embeddedgeneration’registeredforthe3rdCapacityAuction(Figure10a). ThegovernmenthaddesignedtheCapacityMechanismtodeliverreliablegeneratingcapacityatthecheapestprice,givenexistingconditions.Thatisexactlywhatithasdelivered.Thatmighthavebeenfineifpriceandtrueeconomiccostwerealignedbuttheywerenot.TheenvironmentalNGOswereaghasttoseeoldcoalplantsreceivingpayments,andhateddieselevenmore.Thenascentdemand-sidemanagementindustryseestheCapacityMechanismasunbalanced(whichitis)andunderminingtheirmainpotentialmarketofrespondingtoscarcitypricinginthewholesalemarket(theyaremountingalegalchallenge).ThegovernmentreallywantedandexpectedtheCapacityMechanismtobringforthlargeflexiblegas-firedgeneration(whichithasn’t).Andtheincumbentindustrycriedfoul(withreason)atthecompetitionfromdecentralisedgenerationwhichwaseffectivelysubsidisedduetotheexemptionfromthenowveryhighresidualtransmissioncharges.

23ReciprocatingenginesaretypicallymorecostlyperkWthanopencyclegasturbines

33

Thegovernmentmovedtoeffectivelybardieselfromthethirdauctionusingenvironmentalregulation,andthepriceinthat(Dec2016auction)rosesomewhat,bringinganothersurprisewiththescaleofstoragecomingforth.Embeddedgenerationstilldominatedthewinningbids,butdespitehigherprocurementvolumes,clearedatapriceagainmuchtoo

Box4Transmissionchargingand‘embeddedbenefits’intheCapacityMechanism

UKTransmissionchargesareleviedonplantsconnectedtothetransmissionsystem,anddistributioncompaniespayaLoadtarifffortakingpowerfromthegrid,thattheypassontotheircustomers.Bothgenerationandloadtariffshaveanefficiencyelementdesignedtoguidelocationdecisions,andaresidualelementtomakeuptheinitiallysmallshortfallandprovidetheregulatedtotaltransmissionrevenue.1GeneratorsconnectedtothedistributionnetworkthereforereducetheLoadtakenfromthegrid,andsoapparentlyreducethechargetothedistributionnetworks,whopassthisreductiononasan“embeddedbenefit”.Whenthecapacityofdistributedgenerationwassmall,unsubsidised,andconsistingmostlyofindustrialbackupandco-generationofheatandpower,andwhiletheresidualelementinthetariffwassmall,thisseemedreasonable.Decentralisedgenerationwasalsoverymuchinvogue,beingassociatedinparticularwithhouseholdorfarmlevelself-generation. However,astheresidualelementoftransmissionchargesroserapidly(fromabout£10/kW.yrin2006toabout£50/kW.yrin2016andprojectedtoriseto£80/kW.yrin2020)1itbecameclearthatthe“embeddedbenefits”werelargelyavoidedcontributionstothepublicgoodnatureofthenetworks,notproperlyavoidedmarginalcosts.Insomecasestheembeddedgeneration,notablyPVinthesouth-westofEnglishgrewsorapidlyitexceededthelocalexportcapacityofthegridandhadtobecurtailed.AsthewholepointofcapacityprocuredundertheCapacityMechanismwastobeabletosupplynationaldemandwhenneededsuchcurtailmentrenderedsuchembeddedcapacityproblematic.1Analysissoonshowedthattheexemptionfromtransmissionchargescouldrepresentamajordistortion,equivalenttoanythingupto£50/kW.yrofcapacity.Itturnedouttherewasastrongcommercial(ifnoteconomic)reasonwhytheCapacityMechanismwasseeingsomuchdecentralisedgeneration–andatsuchlowprices.

ConcernsexpressedaboutembeddedbenefitswerealreadyclearinDecember2015andofficiallyacknowledgedinJune2016(DECC,2016,§33-34),OfgemfinallyimplementedchangestothechargingregimeinJune2017,phasinginoverthesubsequentthreeyearsrequirementsfordistribution-connectedgenerationtopaytransmissioncharges.Theoutcomeofalegalchallenge,andtheimpactonCapacityMarketvolumesandprices,remains(Dec2017)tobeseen.

34

lowtosupportnewCCGTs,whichmanystillregardedasneededforprovidingbulkpowerthroughthe2020sandbeyond.Despiteconcernsexpressedaboutembeddedbenefits(DECC,2016,§33-34)inJune,2016(andtheevidenceofaproblemalreadyclearinDecember2015),ittookOfgemuntilJune2017toremovethisembeddedbenefitfordistribution-connectedgenerationwithcapacityagreements,24withconsequencesyettobeseen,butpresumablylikelytoraisepricesfurther.

Asidefromthemanydimensionsofconcernaboutthelackofa‘levelplayingfield,theCapacityMechanismfacestwoother,intertwined,worries.OneisthattheincentivesontheMinisterandNationalGridaretoover-procurecapacity-no-onewantstobeheldresponsibleifthe“lightsgoout”,asthetabloidnewspapersfrequentlyannounceisimminent.Astheydonotpay(andNationalGridmaybenefitifmoretransmissioninvestmentisrequired)andconsumersdonotseethecapacitypaymentintheirbills,thereisanadditionalbiastoover-procurement.

Thisinturnexacerbatestheotherworry,aboutthepotentialperverseconsequencesofpayingforcapacity(particularlywithoverprocurement).Ifgeneratorsdonotpassthecapacitypaymentsthroughinreducedwholesaleprices,theyeffectivelygainwindfallprofits.Andiftheydo,thelowerwholesalepricedrivesuptheCapacitypaymentsrequiredtosupportnewinvestment25–and,moreover,thenetcostoftheotherbigpillarofEMR,theCfDsupports-whilstthedampeningeffectonpeak-loadpricinginparticularrobsdemand-sidemanagementofitsprimarypotentialmarket,forwhichtheCapacityMechanismasitstandsissimplynotacrediblesubstitute.

Thusthejudgementismixed.ThepositivecaseisthattheCapacityMechanismisdeliveringcapacitytomaintainsecurity,andhasuncoveredmanyoptionspreviouslynotseriouslyconsidered,atpricesfarlowerthanexpected.Indoingsohoweverithasraisedahostofchallenges,ofwhichonlysomeare,slowly,beingresolved.

5.3CarbonpricefloorandemissionsperformancestandardAsdescribed,theothertwoelementsoftheEMRtargetedcoalmoredirectly.WiththePerformanceStandardeffectivelyremovinganyprospectsofnewcoalinvestment,theissuereallyconcernedoperationoftheexistingfleetandtheincentivesforkeepingcoalpowerstationsopen.Beforetheintroductionofthecarbonpricesupport(CPS),thecarbonpricewasinsufficienttohavemuchoperationalimpact.Atthetimeofitsintroduction,inApril2013,theresultingpricefloorwasstilltoolowtohavemuchimpact,giventhehighgaspriceswhichmaintainedcoalastheeconomicchoiceforbaseloadgeneration.Buttwothingssoonchanged.

24Athttps://www.ofgem.gov.uk/publications-and-updates/embedded-benefits-impact-assessment-and-decision-industry-proposals-cmp264-and-cmp265-change-electricity-transmission-charging-arrangements-embedded-generators25Theevidencesofaristhatcapacitypaymentsarepassedoninlowerwholesaleprices–seetheinterestingeconometricstudyundertakenforOfgemathttps://www.ofgem.gov.uk/system/files/docs/2017/10/final_version_-_technical_appendix.pdf

35

First,thefurthercollapseofEUETSpricealongsidetherisingfloorincreasedthegapbetweenUKandEUcarbonpricesdramatically:thetop-upwritteninwiththefinalEMRlegislationrosefrom£4.94/tCO2intheyearofadoption(2013)to£18.08in2015-16,with‘indicative’projectionsthenrisingabove£20/tCO2.UKindustry,whilstsupportingthefloorinprinciple,becamealarmedatthescaleofthedifferential.Inthesubsequent(2014)budget,theChancellorbowedtothepressureandfrozethemaximumlevelof‘carbonpricesupport’atan£18add-ontotheEUETSprice.26GiventhepersistentlylowEUETSprice,thisineffectbecameatop-uptaxatthislevel,raisingaround£1.5bn/yr.

Theotherfactorwasthatgaspricesbegantodecreaseatlast.Thecombinationmadeiteconomictostartbase-loadinggasinsteadofcoal.Figure11showsthatthecarbon-inclusivecostofgas-firedgenerationfellbelowthatofcoalfromApril2014and,forhighefficiencyCCGTs,hasremainedbelowsince.Indeed,coalhasbeenfrequentlyunprofitabletooperatesincemid-2015(belowzeroinFigure11),promptingaraftofcoalplantclosures.

Figure11GBwholesaleelectricitypriceandthecostofgeneration,2007-17at2011/12prices

Source:https://www.ofgem.gov.uk/data-portal/spark-and-dark-spreads-gbNote:‘Sparkspread’istheutilitytermforthedifferencebetweentheoperatingcostofagasplantandthewholesaleelectricityprice.‘Darkspread’isthecorrespondingtermforcoal..CostsincludetheGBcarbonprice.

26Foranexcellentconcisebriefingseehttp://researchbriefings.files.parliament.uk/documents/SN05927/SN05927.pdf

-20

0

20

40

60

80

100

120

Oct-07

May-08

Dec-08

Jul-0

9 Feb-10

Sep-10

Apr-11

Nov-11

Jun-12

Jan-13

Aug-13

Mar-14

Oct-14

May-15

Dec-15

Jul-1

6 Feb-17

Who

lesalepric

e/spreads,£/M

Wh

Date

Evolutionofwholesalepriceandgenerationspreads,2007-2017

Powerprice(baseload)

Spark(gasloweff)

Spark(gas)

Spark(gashigheff)

Dark(coal)

36

AsillustratedinFigure12anddescribedfurtherintheconclusions,theoverallimpactsontheGBelectricitysystemanditsemissionshavebeendramatic.Asthecombinationoffuelandcarbonpricesincreasinglymadegasplantscheaperthancoaltorun,thismadecoalthemarginalplant,whichmaximisestheimpactofthecarbonpriceonelectricityprices.Domesticelectricitypriceswerealreadypoliticallychargedandin2015thedifferentialwiththerestoftheEU,exacerbatedbyahighexchangerate,pushedcomparativeindustrialelectricitypricesalsohighonthepoliticalagenda.Afterthegeneralelectionof2015,therewasaconcertedpushfromsomeelectro-intensiveindustry,alongwiththe‘climate-sceptic’wingoftheconservativeparty,tocancelthefloorpriceentirelyongroundsofindustrialcompetitiveness.However,strongcounter-lobbying–includingthegasindustryalongsidelargerswathesofUKbusinesspleadingforstabilityinthepolicyenvironment–mergedwiththeevidentself-interestoftheUKTreasurytomaintaintheauctionrevenues.

Figure12CarbonPriceSupportandimpactoncoalgeneration,2012-2017(Q2)

Asthecombinationoffuelandcarbonpricesincreasinglymadegasplantscheaperthancoaltorun,thisTheTreasurydulyannouncedthattheCarbonPriceSupportwouldremain,frozenatthesamelevel,atleastthroughto2021.Therapiddeclineofcoalstartedtocreateperiodswithgasasthemarginalfuel,startingtotempertheimpactofthecarbonpriceonwholesaleprices,whilstthecollapseoftheUKexchangerateaftertheEUreferendumdidmuchtoremovethepricegapwiththerestofEuropeformanyindustrialconsumers.Inautumn2017,thegovernmentannounceditconsideredthattheoverallcarbonpricewasatabouttherightlevel–precludingsignificantnear-termincreasebutalsoprotectingthemarketpriceagainstthepossiblelossoftheEUETSafterBrexit–andwouldbereviewedoncecoalwasremovedfromthesystem.Asthedustbegantosettle,thereforeallfourplanksoftheEMRhad

37

thussurvivedthepoliticalturmoil–but,atthepriceofsacrificingtheintendedstrategicsignalofasteadilyrisingcarbonpricetoguidealllowcarboninvestment.

6. Popularcaricature:“Returnofthe‘CentralElectricityGeneratingBoard’?”Theoriginalvisionthatmotivatedprivatizationwas,toquotethethenenergyministerLawson:“…thebusinessofGovernmentisnotthegovernmentofbusiness”(Lawson,1992,p211).Astoenergypolicy,LawsonstatedataBIEEconferencein1982“Idonotseethegovernment’staskasbeingtotryandplanthefutureshapeofenergyproductionandconsumption.ItisnotevenprimarilytotrytobalanceUKdemandandsupplyforenergy.Ourtaskisrathertosetaframeworkwhichwillensurethatthemarketoperatesintheenergysectorwithaminimumofdistortionandenergyisproducedandconsumedefficiently.”27

CriticshavearguedthatEMRrepresentsareversalofthisideal,withtheGovernmentnowplanningthefutureshapeofenergyproductionandconsumption.SpecificrenewabletechnologiesareprocuredthroughCfDauctions,nuclearpowerissimilarlyprocuredbyabilateralcontractwiththeGovernment,theamountoffossilcapacityconsideredtobeneededtodeliverthereliabilitytargetissetbytheminister,whiletheregulator,Ofgem,issubjecttostrongpoliticalpressuretodelivercheaperdomesticelectricityprices.Criticsfurtherarguethatlong-termcontractsarereplacingthemarketasamechanismtoattractnewinvestmentintotheindustry,seeminglymovingbacktotheSingleBuyerModelthattheFrench,withtheirstate-ownedelectricityindustry,pressedunsuccessfullyforinthefirstEUElectricityDirective.

So,isEMRanadmissionofafailureoftheliberalisedelectricitymarketmodel,oristheGovernment,thoughtheEnergyBill2013,attemptinginsteadtobettercorrectmarketfailures?Wewouldarguethelatter.Long-termcontracts(onlyfornewinvestment)replacetheabsentfuturesmarkets,allthemorenecessarygiventheunpredictabilityoffutureenergypolicy.Mostrenewablescreatelearningspill-oversthatareunrewardedbythemarket,whichjustifysubsidy.28Aslearningspill-oversdependontechnologyandthestateofthetechnology’smaturitythesubsidiesshouldalsobetechnologyspecific(althoughtheformofsubsidyprovidedbyEMRisnotparticularlywell-directedtoaddressingthelearningmarketfailure).

Itismoreoverwrongtoconfusegovernment-ledauctionswithcentralplanning.Asanofficialremarkedin2013,itfeltstrangetobeaccusedofcentralplanningwhentheywereasuncertainabouttheresultsoftheimpendingauctionsaseveryoneelse.Theauctionscreatednewmarkets,andwhichascommonwithnewmarkets,bothunearthedandstimulatedtheunexpected.Butthenewmarkets–andinvestmentsandlearning-couldnothaveoccurredwithoutthegovernmentrecognisingtherewerebiggapsthathadtobefilledifthenationalobjectivesweretobemet.

27NigelLawson,quotedathttps://publications.parliament.uk/pa/ld201617/ldselect/ldeconaf/113/11305.htm28Tidallagoonsarepresumablyanexception,asbuildingdamsinamillennium-oldskill.

38

Providingalong-termcontractfornuclearpoweralsoreflectsthelackofadurablecrediblecarbonprice,aswellasthelackofinsurancemarketsforfuturepowerpricesandnuclearpolicychanges(suchastheEnergiewendeinGermany).WhiletheparticularformofunderwritingforHinkleyPointishighlyunsatisfactory,itseemsinconceivablethatprivatecompanieswouldtakeonnuclearriskwithoutsomeGovernment-backedguaranteetofacilitatefinancing.TheUK,likemanyothercountries,hasstruggledtofindcost-effectivewaystosupportnuclearpower,andyetitremainsunclearwhetherorhowtheUKwillmeetitsambitiousgoalstoalmostentirelydecarbonisethepowersystem,wellbefore2050,withoutit.

ItisalsoworthrememberingthatthemassiveentryofnewCombinedCycleGasTurbinesinthe1990sbyIndependentPowerProducerswasbasedonlong-termpowerpurchaseagreementswiththeRegionalElectricity(distribution)Companies,manyofwhomwereco-sponsorsandshareholdersintheprojects(partlyasawayofreducingtheirrelianceontheduopolygeneratingcompanies).ThedevelopmentofthoseCCGTswasinturnheavilysubsidizedbythedefenceindustrysupportingjetengines.