Embed Size (px)

DESCRIPTION

Covering high quality, high yield shares for defensive value investors.

Citation preview

Page 1Photo credit: George Rex

UK Value Investor is for investors who want to make their own investment decisions and are capable of doing so withoutprofessional advice. If you think you need advice then you should seek a professional advisor. Please see the importantnotes on the back page for further information.

October 2012

UK Value InvestorValue Investing for Income and Growth

Contents

Market forecast and tactical asset allocation Page 2

Model portfolio review Page 3

Selling: The latest sale will generate annualised returns of around 35% Page 6

FTSE 350 Rankings: The easy way to find high income and growth Page 9

Of Mergers and AcquisitionsJohn Kingham, Editor

When I invest in a company my expectation is that I’ll be holding it for at least five years. So of course I wantthe business to be able to last the next five years and if possible for it to be bigger in five years than it is today.This means that I look for reasons as to why the company might fail or shrink, and if the case doesn’t lookstrong enough then I will move on to the next opportunity.

However, there is one type of corporate event that pops up occasionally and unpredictably, and yet it can havea massive impact on investment returns. These events are mergers and acquisitions, or M&A as it’s oftenknown.

So far in the life of the UKVI model portfolio things have worked out well on this front. Robert WisemanDairies, one of the UK’s leading suppliers of fresh milk, was in the portfolio when it was taken over by MullerDairies. It was an unexpected event because the shares jumped from about 245p up to the offer price of 390palmost instantly. Nobody saw it coming, but that was okay as it resulted in a 27% gain for the portfolio.

Now we have a similar situation occurring with both Chemring and BAE Systems, although in both these casesa takeover or merger has been publicly mentioned, but neither one is a done deal just yet. Once again, exactlyhow this will work out is unclear.

M&A provides a good example of the kind of randomness that equity investments are subject to all the time.They may turn out well or badly, but the best defence against this uncertainty is a well diversified portfolio.

Page 2

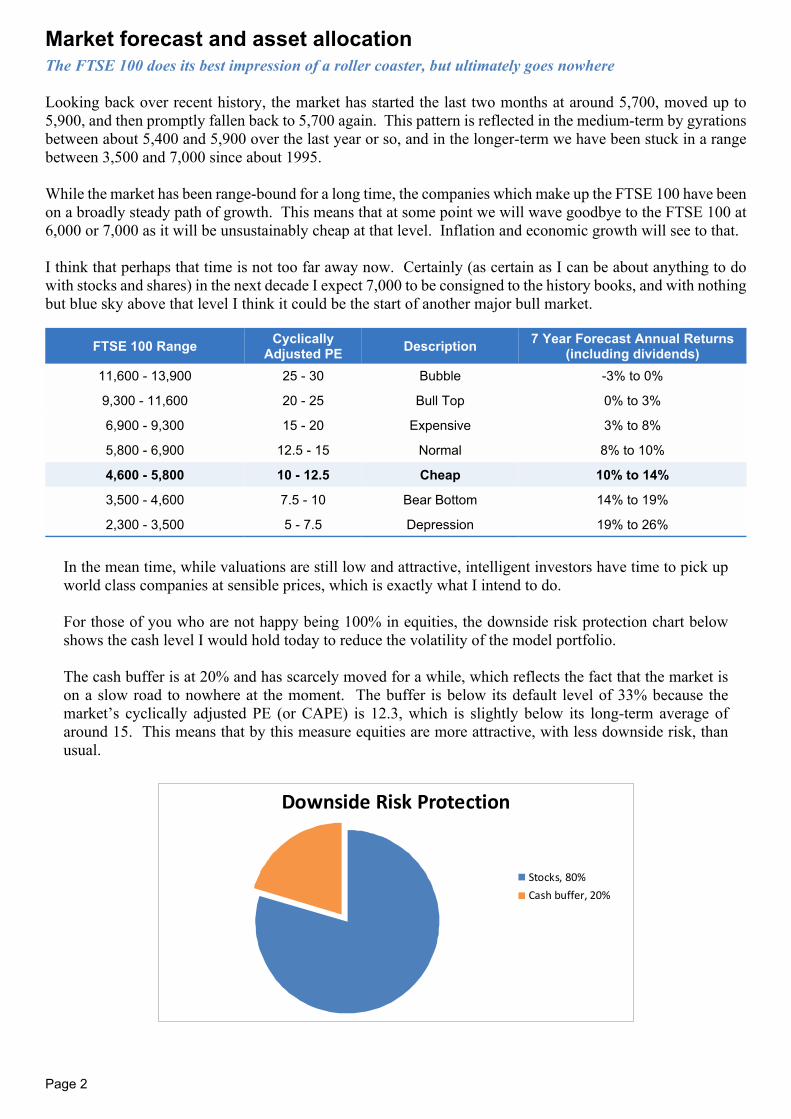

Market forecast and asset allocationThe FTSE 100 does its best impression of a roller coaster, but ultimately goes nowhere

Looking back over recent history, the market has started the last two months at around 5,700, moved up to5,900, and then promptly fallen back to 5,700 again. This pattern is reflected in the medium-term by gyrationsbetween about 5,400 and 5,900 over the last year or so, and in the longer-term we have been stuck in a rangebetween 3,500 and 7,000 since about 1995.

While the market has been range-bound for a long time, the companies which make up the FTSE 100 have beenon a broadly steady path of growth. This means that at some point we will wave goodbye to the FTSE 100 at6,000 or 7,000 as it will be unsustainably cheap at that level. Inflation and economic growth will see to that.

I think that perhaps that time is not too far away now. Certainly (as certain as I can be about anything to dowith stocks and shares) in the next decade I expect 7,000 to be consigned to the history books, and with nothingbut blue sky above that level I think it could be the start of another major bull market.

FTSE 100 Range CyclicallyAdjusted PE Description 7 Year Forecast Annual Returns

(including dividends)11,600 - 13,900 25 - 30 Bubble -3% to 0%

9,300 - 11,600 20 - 25 Bull Top 0% to 3%

6,900 - 9,300 15 - 20 Expensive 3% to 8%

5,800 - 6,900 12.5 - 15 Normal 8% to 10%

4,600 - 5,800 10 - 12.5 Cheap 10% to 14%

3,500 - 4,600 7.5 - 10 Bear Bottom 14% to 19%

2,300 - 3,500 5 - 7.5 Depression 19% to 26%

In the mean time, while valuations are still low and attractive, intelligent investors have time to pick upworld class companies at sensible prices, which is exactly what I intend to do.

For those of you who are not happy being 100% in equities, the downside risk protection chart belowshows the cash level I would hold today to reduce the volatility of the model portfolio.

The cash buffer is at 20% and has scarcely moved for a while, which reflects the fact that the market ison a slow road to nowhere at the moment. The buffer is below its default level of 33% because themarket’s cyclically adjusted PE (or CAPE) is 12.3, which is slightly below its long-term average ofaround 15. This means that by this measure equities are more attractive, with less downside risk, thanusual.

Downside Risk Protection

Stocks, 80%Cash buffer, 20%

Page 3

Model portfolio reviewOne of the nice things about owning a portfolio of shares versus a collective fund is the continuous paymentof dividends. Now that the model portfolio has been fully invested for a while there are new dividend paymentscoming in every month, rather than the two or four payments a year that a typical fund would pay.

For example, this month we’ve had payments from AstraZeneca, SSE, BP, Reckitt Benckiser and BHPBilliton. This steady stream of cash shows the true economic value of a portfolio much better than whether ornot the capital value (i.e. the share prices) went up or down in a given period.

These dividends are then available to be reinvested into more high quality businesses at attractive, highyielding valuations. In my opinion the growth of the income stream is the best way to gauge the success of aninvestment fund.

Rio Tinto

Following last month’s buy alert I’ve added Rio Tinto to the portfolio at 2,988p with the usual weighting ofaround 1/30th of the total.

Performance (%) Yield 1y YTD 2011 From inceptionModel Portfolio 4.5 14.1 17 -6.9 8.9

Index Tracker 3.3 19.4 10.4 -3.4 6.6

Relative to Index Tracker + 1.2 - 5.3 + 6.6 - 3.5 + 2.3

Cash Results (started at £50,000) Current Capital Value Rolling 12 Month IncomeModel Portfolio £54,438 £2,437

Index Tracker £53,309 £1,742

Relative to Index Tracker £1,129 £695

-15.0%

-10.0%

-5.0%

0.0%

5.0%

10.0%

15.0%

Mar-11 May-11 Jul-11 Sep-11 Nov-11 Jan-12 Mar-12 May-12 Jul-12 Sep-12

Model Portfolio Total Return FT SE 100 Tracker Total Return

Page 4

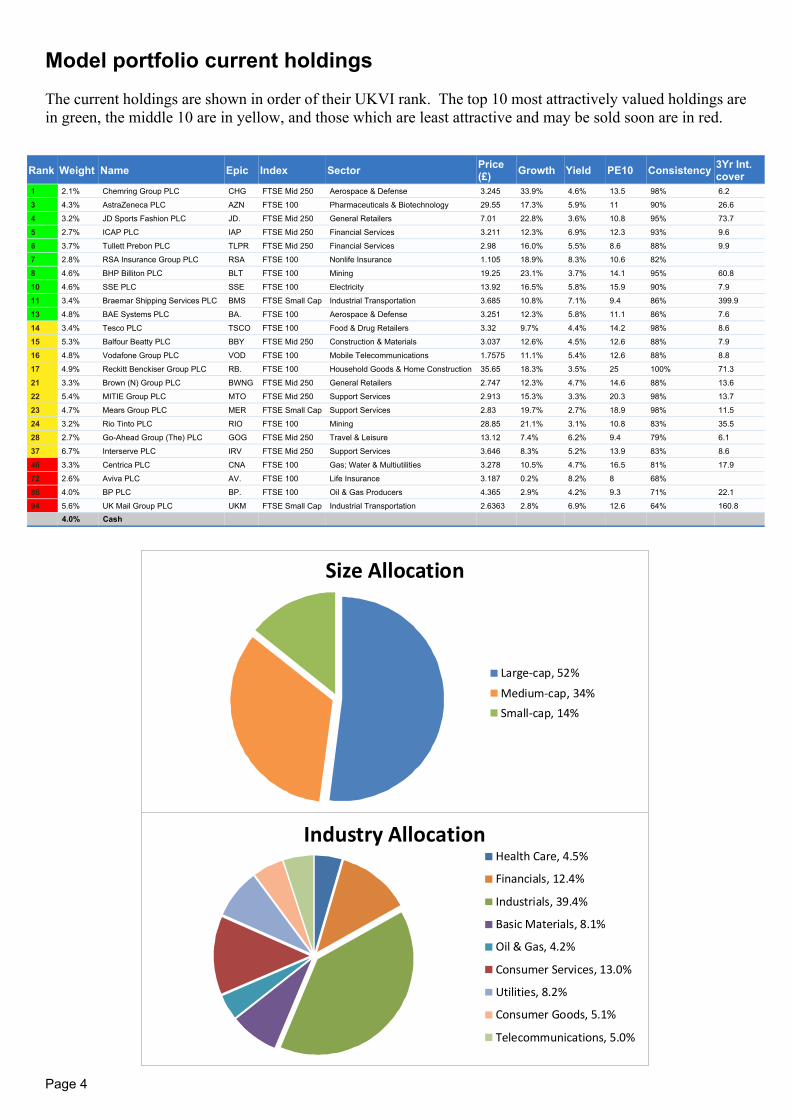

Model portfolio current holdings

Rank Weight Name Epic Index Sector Price(£) Growth Yield PE10 Consistency 3Yr Int.

cover1 2.1% Chemring Group PLC CHG FTSE Mid 250 Aerospace & Defense 3.245 33.9% 4.6% 13.5 98% 6.2

3 4.3% AstraZeneca PLC AZN FTSE 100 Pharmaceuticals & Biotechnology 29.55 17.3% 5.9% 11 90% 26.6

4 3.2% JD Sports Fashion PLC JD. FTSE Mid 250 General Retailers 7.01 22.8% 3.6% 10.8 95% 73.7

5 2.7% ICAP PLC IAP FTSE Mid 250 Financial Services 3.211 12.3% 6.9% 12.3 93% 9.6

6 3.7% Tullett Prebon PLC TLPR FTSE Mid 250 Financial Services 2.98 16.0% 5.5% 8.6 88% 9.9

7 2.8% RSA Insurance Group PLC RSA FTSE 100 Nonlife Insurance 1.105 18.9% 8.3% 10.6 82%

8 4.6% BHP Billiton PLC BLT FTSE 100 Mining 19.25 23.1% 3.7% 14.1 95% 60.8

10 4.6% SSE PLC SSE FTSE 100 Electricity 13.92 16.5% 5.8% 15.9 90% 7.9

11 3.4% Braemar Shipping Services PLC BMS FTSE Small Cap Industrial Transportation 3.685 10.8% 7.1% 9.4 86% 399.9

13 4.8% BAE Systems PLC BA. FTSE 100 Aerospace & Defense 3.251 12.3% 5.8% 11.1 86% 7.6

14 3.4% Tesco PLC TSCO FTSE 100 Food & Drug Retailers 3.32 9.7% 4.4% 14.2 98% 8.6

15 5.3% Balfour Beatty PLC BBY FTSE Mid 250 Construction & Materials 3.037 12.6% 4.5% 12.6 88% 7.9

16 4.8% Vodafone Group PLC VOD FTSE 100 Mobile Telecommunications 1.7575 11.1% 5.4% 12.6 88% 8.8

17 4.9% Reckitt Benckiser Group PLC RB. FTSE 100 Household Goods & Home Construction 35.65 18.3% 3.5% 25 100% 71.3

21 3.3% Brown (N) Group PLC BWNG FTSE Mid 250 General Retailers 2.747 12.3% 4.7% 14.6 88% 13.6

22 5.4% MITIE Group PLC MTO FTSE Mid 250 Support Services 2.913 15.3% 3.3% 20.3 98% 13.7

23 4.7% Mears Group PLC MER FTSE Small Cap Support Services 2.83 19.7% 2.7% 18.9 98% 11.5

24 3.2% Rio Tinto PLC RIO FTSE 100 Mining 28.85 21.1% 3.1% 10.8 83% 35.5

28 2.7% Go-Ahead Group (The) PLC GOG FTSE Mid 250 Travel & Leisure 13.12 7.4% 6.2% 9.4 79% 6.1

37 6.7% Interserve PLC IRV FTSE Mid 250 Support Services 3.646 8.3% 5.2% 13.9 83% 8.6

46 3.3% Centrica PLC CNA FTSE 100 Gas; Water & Multiutilities 3.278 10.5% 4.7% 16.5 81% 17.9

72 2.6% Aviva PLC AV. FTSE 100 Life Insurance 3.187 0.2% 8.2% 8 68%

86 4.0% BP PLC BP. FTSE 100 Oil & Gas Producers 4.365 2.9% 4.2% 9.3 71% 22.1

94 5.6% UK Mail Group PLC UKM FTSE Small Cap Industrial Transportation 2.6363 2.8% 6.9% 12.6 64% 160.84.0% Cash

The current holdings are shown in order of their UKVI rank. The top 10 most attractively valued holdings arein green, the middle 10 are in yellow, and those which are least attractive and may be sold soon are in red.

Size Allocation

Large-cap, 52%

Medium-cap, 34%Small-cap, 14%

Industry AllocationHealth Care, 4.5%

Financials, 12.4%

Industrials, 39.4%

Basic Materials, 8.1%

Oil & Gas, 4.2%

Consumer Services, 13.0%

Utilities, 8.2%

Consumer Goods, 5.1%

Telecommunications, 5.0%

Page 5

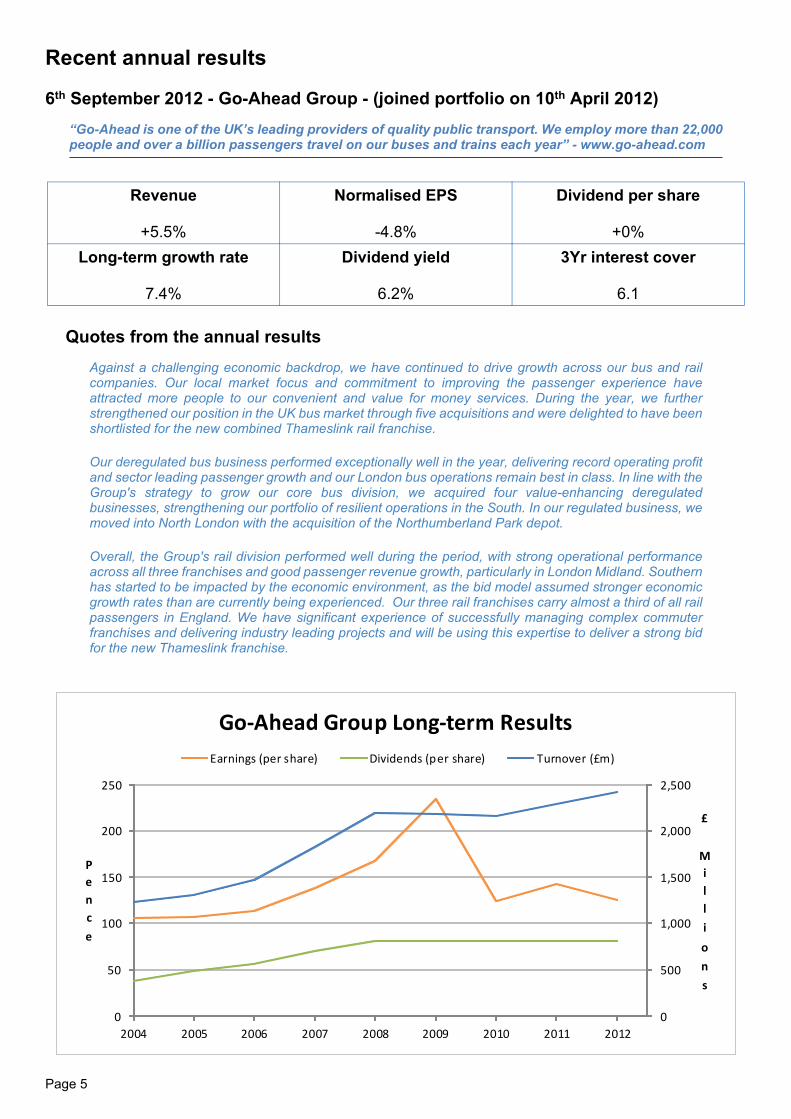

Recent annual results

6th September 2012 - Go-Ahead Group - (joined portfolio on 10th April 2012)“Go-Ahead is one of the UK’s leading providers of quality public transport. We employ more than 22,000people and over a billion passengers travel on our buses and trains each year” - www.go-ahead.com

Revenue

+5.5%

Normalised EPS

-4.8%

Dividend per share

+0%Long-term growth rate

7.4%

Dividend yield

6.2%

3Yr interest cover

6.1

Quotes from the annual resultsAgainst a challenging economic backdrop, we have continued to drive growth across our bus and railcompanies. Our local market focus and commitment to improving the passenger experience haveattracted more people to our convenient and value for money services. During the year, we furtherstrengthened our position in the UK bus market through five acquisitions and were delighted to have beenshortlisted for the new combined Thameslink rail franchise.

Our deregulated bus business performed exceptionally well in the year, delivering record operating profitand sector leading passenger growth and our London bus operations remain best in class. In line with theGroup's strategy to grow our core bus division, we acquired four value-enhancing deregulatedbusinesses, strengthening our portfolio of resilient operations in the South. In our regulated business, wemoved into North London with the acquisition of the Northumberland Park depot.

Overall, the Group's rail division performed well during the period, with strong operational performanceacross all three franchises and good passenger revenue growth, particularly in London Midland. Southernhas started to be impacted by the economic environment, as the bid model assumed stronger economicgrowth rates than are currently being experienced. Our three rail franchises carry almost a third of all railpassengers in England. We have significant experience of successfully managing complex commuterfranchises and delivering industry leading projects and will be using this expertise to deliver a strong bidfor the new Thameslink franchise.

0

500

1,000

1,500

2,000

2,500

0

50

100

150

200

250

2004 2005 2006 2007 2008 2009 2010 2011 2012

£

Millions

Pence

Go-Ahead Group Long-term ResultsEarnings (per share) Dividends (per share) Turnover (£m)

Page 6

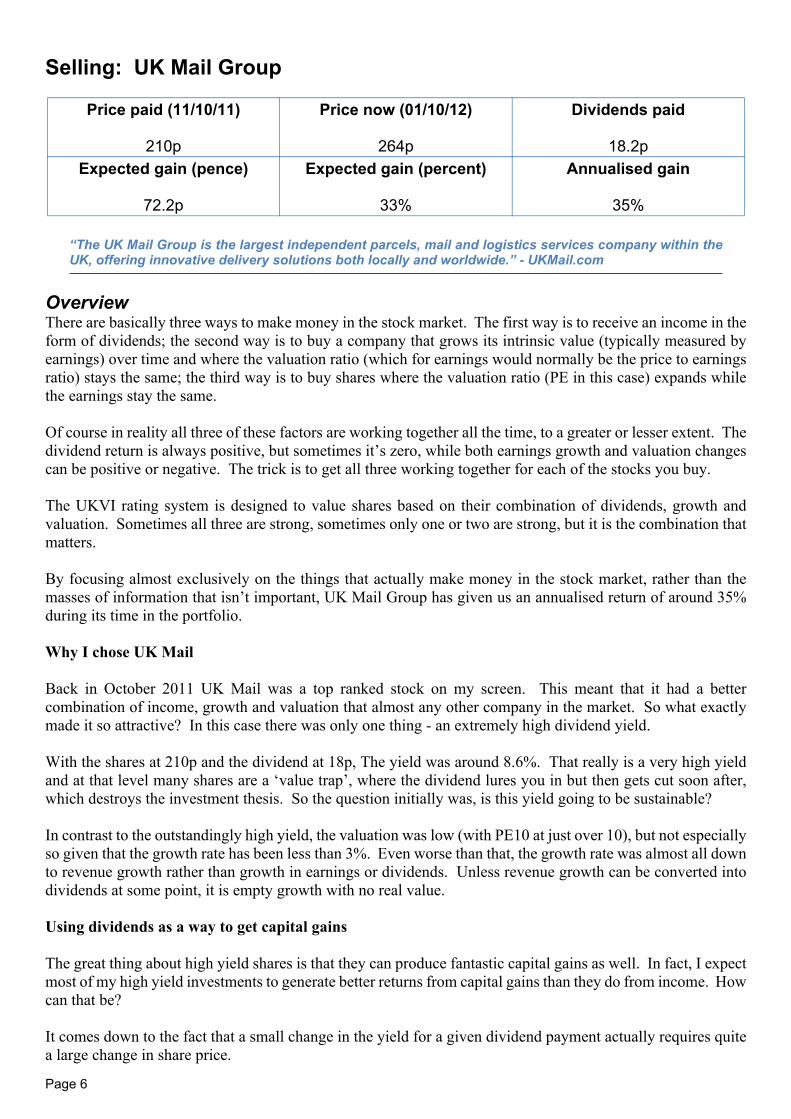

Selling: UK Mail Group

Price paid (11/10/11)

210p

Price now (01/10/12)

264p

Dividends paid

18.2pExpected gain (pence)

72.2p

Expected gain (percent)

33%

Annualised gain

35%

“The UK Mail Group is the largest independent parcels, mail and logistics services company within theUK, offering innovative delivery solutions both locally and worldwide.” - UKMail.com

OverviewThere are basically three ways to make money in the stock market. The first way is to receive an income in theform of dividends; the second way is to buy a company that grows its intrinsic value (typically measured byearnings) over time and where the valuation ratio (which for earnings would normally be the price to earningsratio) stays the same; the third way is to buy shares where the valuation ratio (PE in this case) expands whilethe earnings stay the same.

Of course in reality all three of these factors are working together all the time, to a greater or lesser extent. Thedividend return is always positive, but sometimes it’s zero, while both earnings growth and valuation changescan be positive or negative. The trick is to get all three working together for each of the stocks you buy.

The UKVI rating system is designed to value shares based on their combination of dividends, growth andvaluation. Sometimes all three are strong, sometimes only one or two are strong, but it is the combination thatmatters.

By focusing almost exclusively on the things that actually make money in the stock market, rather than themasses of information that isn’t important, UK Mail Group has given us an annualised return of around 35%during its time in the portfolio.

Why I chose UK Mail

Back in October 2011 UK Mail was a top ranked stock on my screen. This meant that it had a bettercombination of income, growth and valuation that almost any other company in the market. So what exactlymade it so attractive? In this case there was only one thing - an extremely high dividend yield.

With the shares at 210p and the dividend at 18p, The yield was around 8.6%. That really is a very high yieldand at that level many shares are a ‘value trap’, where the dividend lures you in but then gets cut soon after,which destroys the investment thesis. So the question initially was, is this yield going to be sustainable?

In contrast to the outstandingly high yield, the valuation was low (with PE10 at just over 10), but not especiallyso given that the growth rate has been less than 3%. Even worse than that, the growth rate was almost all downto revenue growth rather than growth in earnings or dividends. Unless revenue growth can be converted intodividends at some point, it is empty growth with no real value.

Using dividends as a way to get capital gains

The great thing about high yield shares is that they can produce fantastic capital gains as well. In fact, I expectmost of my high yield investments to generate better returns from capital gains than they do from income. Howcan that be?

It comes down to the fact that a small change in the yield for a given dividend payment actually requires quitea large change in share price.

Page 7

So for example, UK Mail was paying out a dividend of 18p, and with the share price at 210p it had a yield of8.6%. If the dividend was sustained then it seemed highly likely that the high yield would attract otherinvestors who would bid up the price until the yield became less attractive.

To push the yield up to 7%, which is still a very attractive level, the share price would have to rise to 257p,which is a 22.4% capital gain. That return dwarfs the expected dividend income and that’s the hidden value inhigh yield shares.

0

50

100

150

200

250

300

350

400

450

500

0

5

10

15

20

25

30

35

40

45

50

2004 2005 2006 2007 2008 2009 2010 2011 2012

£Million

Pence

UK Mail long-term resultsEarnings (per share) Dividend (per share) Turnover (£m)

But at the time the most important thing was to see if the yield would be sustainable, which for me starts witha review of how the company has done in the last decade.

Looking for a successful past

I want to invest in good businesses with proven track records, and UK Mail only just make the grade. It’scertainly a leading company in its industry, but what really matters is results and on this front they are far lesssuccessful than many other companies in the portfolio.

Still, they’re not a basket case - far from it in fact. And even though the dividend is barely covered by earnings,it had been sustained at around 18p for many years, with no obvious signs that it was about to be cut.

Of course the management focused on their success in growing revenues, but as I said before, unless revenuescan be converted into cash they add little value.

A survivable present

Most of the time investments are attractive because they’re out of favour with the mainstream. Sometimesthere are obvious reasons why, such as when Tesco’s recent like-for-like results missed estimates and triggereda fall of more than 15% in the share price.

But sometimes the reasons are not so obvious, and with UK Mail it seemed like a combination of factors, noneof which really stood out. Of course, we are in an environment that is quite negative for equities, and thecompany’s results haven’t exactly set the world on fire. There were also some worries about falling profits in2011 and the share price has been on a long fall from 700p in 2005 to 200p in 2011.

Page 8

Whatever the reason, the underlying business looked steady, debts were low (and the company now has morecash than borrowings), and at least to me, the dividend looked sustainable.

A rosy future

Shares are risky, we all know that. Nobody can know where the share price is going to be tomorrow, or nextyear. So I always invest with the expectation that I will be holding for at least 5 years, which means that I wantthe company to survive and thrive in that time.

As a mail and parcel delivery company, I certainly didn’t think that the industry was going to see the kind ofrevolution that the music industry has seen. 5 years from now UK Mail will very probably still be hauling truckloads of letters and packages all over the country. And even if we faced a severe recession, parcels would stillneed to be sent no matter what, so there seemed to be little threat to the company from the ups and downs ofthe business cycle.

How did it all turn out?

In hindsight I can see that things have turned out pretty much as I hoped for. In terms of the company, nothingmuch has really happened. We’ve had a new annual report in which the results were much as they have beenfor many years. The important thing was that the dividend was maintained and this seems to have giveninvestors more confidence that it will not be cut.

The confidence of other investors is shown in the rising share price, which is good for the portfolio as itproduces gains, at least on paper. Just as importantly, because the price has increased but the company’sintrinsic value hasn’t, there may be fewer returns on offer in future and at the same time there is more risk ofa share price fall. Both of those factors are good reasons to sell.

Knowing when to sell

Selling is a difficult subject; it’s every bit as difficult as buying. In my case I buy and sell using much the samecriteria, so if a stock doesn’t have an outstanding combination of yield, growth and valuation then I will sellup and move to another one that does.

When I bought UK Mail Group a year ago at 210p the yield was 8.6%, PE10 was 10.2 and growth was 2.8%.

Now the shares are at 264p the yield is 6.9%, PE10 is 12.6 and growth is much the same. Although these arestill reasonable values they are far less attractive than they were before, to the extent that I now think there arebetter places that this money can be put to work.

Does that mean I think the shares won’t go any higher? No, I think at current levels the shares could still easilydouble. But I don’t want to speculate about how high the shares might go. I want to buy only the mostattractive shares in the market and sell them when they are no longer the most attractive shares. For UK Mailthat means the time to go is now.

I will be selling UK Mail Group in a few days and the cash will be used to buy two new holdings over the nextcouple of months, after which I will be selling another holding to recycle the cash into the most attractiveopportunities.

Page 9

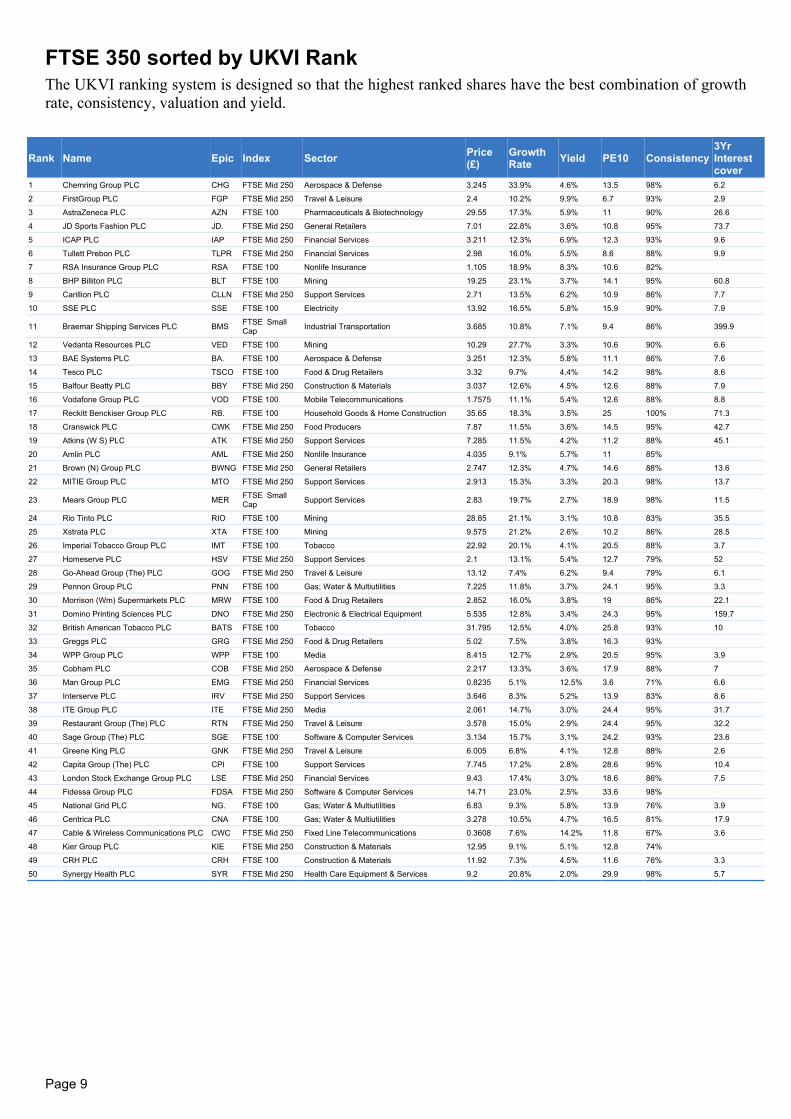

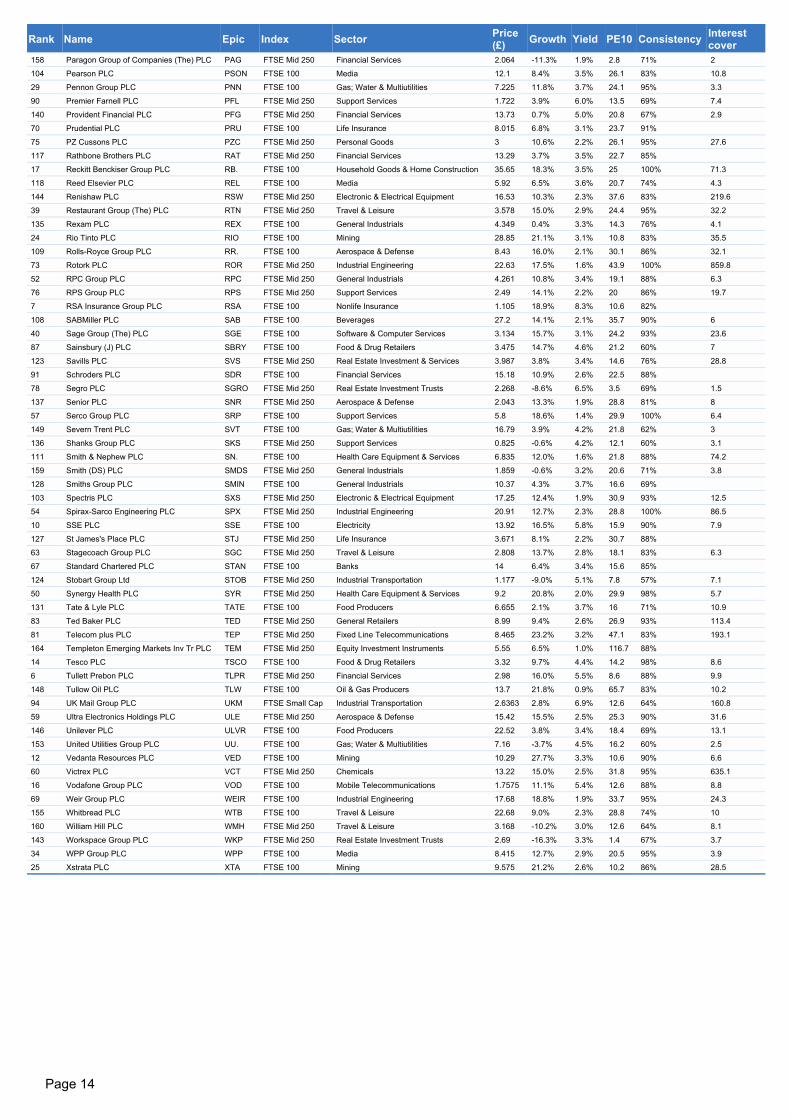

FTSE 350 sorted by UKVI RankThe UKVI ranking system is designed so that the highest ranked shares have the best combination of growthrate, consistency, valuation and yield.

Rank Name Epic Index Sector Price(£)

GrowthRate Yield PE10 Consistency

3YrInterestcover

1 Chemring Group PLC CHG FTSE Mid 250 Aerospace & Defense 3.245 33.9% 4.6% 13.5 98% 6.2

2 FirstGroup PLC FGP FTSE Mid 250 Travel & Leisure 2.4 10.2% 9.9% 6.7 93% 2.9

3 AstraZeneca PLC AZN FTSE 100 Pharmaceuticals & Biotechnology 29.55 17.3% 5.9% 11 90% 26.6

4 JD Sports Fashion PLC JD. FTSE Mid 250 General Retailers 7.01 22.8% 3.6% 10.8 95% 73.7

5 ICAP PLC IAP FTSE Mid 250 Financial Services 3.211 12.3% 6.9% 12.3 93% 9.6

6 Tullett Prebon PLC TLPR FTSE Mid 250 Financial Services 2.98 16.0% 5.5% 8.6 88% 9.9

7 RSA Insurance Group PLC RSA FTSE 100 Nonlife Insurance 1.105 18.9% 8.3% 10.6 82%

8 BHP Billiton PLC BLT FTSE 100 Mining 19.25 23.1% 3.7% 14.1 95% 60.8

9 Carillion PLC CLLN FTSE Mid 250 Support Services 2.71 13.5% 6.2% 10.9 86% 7.7

10 SSE PLC SSE FTSE 100 Electricity 13.92 16.5% 5.8% 15.9 90% 7.9

11 Braemar Shipping Services PLC BMS FTSE SmallCap Industrial Transportation 3.685 10.8% 7.1% 9.4 86% 399.9

12 Vedanta Resources PLC VED FTSE 100 Mining 10.29 27.7% 3.3% 10.6 90% 6.6

13 BAE Systems PLC BA. FTSE 100 Aerospace & Defense 3.251 12.3% 5.8% 11.1 86% 7.6

14 Tesco PLC TSCO FTSE 100 Food & Drug Retailers 3.32 9.7% 4.4% 14.2 98% 8.6

15 Balfour Beatty PLC BBY FTSE Mid 250 Construction & Materials 3.037 12.6% 4.5% 12.6 88% 7.9

16 Vodafone Group PLC VOD FTSE 100 Mobile Telecommunications 1.7575 11.1% 5.4% 12.6 88% 8.8

17 Reckitt Benckiser Group PLC RB. FTSE 100 Household Goods & Home Construction 35.65 18.3% 3.5% 25 100% 71.3

18 Cranswick PLC CWK FTSE Mid 250 Food Producers 7.87 11.5% 3.6% 14.5 95% 42.7

19 Atkins (W S) PLC ATK FTSE Mid 250 Support Services 7.285 11.5% 4.2% 11.2 88% 45.1

20 Amlin PLC AML FTSE Mid 250 Nonlife Insurance 4.035 9.1% 5.7% 11 85%

21 Brown (N) Group PLC BWNG FTSE Mid 250 General Retailers 2.747 12.3% 4.7% 14.6 88% 13.6

22 MITIE Group PLC MTO FTSE Mid 250 Support Services 2.913 15.3% 3.3% 20.3 98% 13.7

23 Mears Group PLC MER FTSE SmallCap Support Services 2.83 19.7% 2.7% 18.9 98% 11.5

24 Rio Tinto PLC RIO FTSE 100 Mining 28.85 21.1% 3.1% 10.8 83% 35.5

25 Xstrata PLC XTA FTSE 100 Mining 9.575 21.2% 2.6% 10.2 86% 28.5

26 Imperial Tobacco Group PLC IMT FTSE 100 Tobacco 22.92 20.1% 4.1% 20.5 88% 3.7

27 Homeserve PLC HSV FTSE Mid 250 Support Services 2.1 13.1% 5.4% 12.7 79% 52

28 Go-Ahead Group (The) PLC GOG FTSE Mid 250 Travel & Leisure 13.12 7.4% 6.2% 9.4 79% 6.1

29 Pennon Group PLC PNN FTSE 100 Gas; Water & Multiutilities 7.225 11.8% 3.7% 24.1 95% 3.3

30 Morrison (Wm) Supermarkets PLC MRW FTSE 100 Food & Drug Retailers 2.852 16.0% 3.8% 19 86% 22.1

31 Domino Printing Sciences PLC DNO FTSE Mid 250 Electronic & Electrical Equipment 5.535 12.8% 3.4% 24.3 95% 159.7

32 British American Tobacco PLC BATS FTSE 100 Tobacco 31.795 12.5% 4.0% 25.8 93% 10

33 Greggs PLC GRG FTSE Mid 250 Food & Drug Retailers 5.02 7.5% 3.8% 16.3 93%

34 WPP Group PLC WPP FTSE 100 Media 8.415 12.7% 2.9% 20.5 95% 3.9

35 Cobham PLC COB FTSE Mid 250 Aerospace & Defense 2.217 13.3% 3.6% 17.9 88% 7

36 Man Group PLC EMG FTSE Mid 250 Financial Services 0.8235 5.1% 12.5% 3.6 71% 6.6

37 Interserve PLC IRV FTSE Mid 250 Support Services 3.646 8.3% 5.2% 13.9 83% 8.6

38 ITE Group PLC ITE FTSE Mid 250 Media 2.061 14.7% 3.0% 24.4 95% 31.7

39 Restaurant Group (The) PLC RTN FTSE Mid 250 Travel & Leisure 3.578 15.0% 2.9% 24.4 95% 32.2

40 Sage Group (The) PLC SGE FTSE 100 Software & Computer Services 3.134 15.7% 3.1% 24.2 93% 23.6

41 Greene King PLC GNK FTSE Mid 250 Travel & Leisure 6.005 6.8% 4.1% 12.8 88% 2.6

42 Capita Group (The) PLC CPI FTSE 100 Support Services 7.745 17.2% 2.8% 28.6 95% 10.4

43 London Stock Exchange Group PLC LSE FTSE Mid 250 Financial Services 9.43 17.4% 3.0% 18.6 86% 7.5

44 Fidessa Group PLC FDSA FTSE Mid 250 Software & Computer Services 14.71 23.0% 2.5% 33.6 98%

45 National Grid PLC NG. FTSE 100 Gas; Water & Multiutilities 6.83 9.3% 5.8% 13.9 76% 3.9

46 Centrica PLC CNA FTSE 100 Gas; Water & Multiutilities 3.278 10.5% 4.7% 16.5 81% 17.9

47 Cable & Wireless Communications PLC CWC FTSE Mid 250 Fixed Line Telecommunications 0.3608 7.6% 14.2% 11.8 67% 3.6

48 Kier Group PLC KIE FTSE Mid 250 Construction & Materials 12.95 9.1% 5.1% 12.8 74%

49 CRH PLC CRH FTSE 100 Construction & Materials 11.92 7.3% 4.5% 11.6 76% 3.3

50 Synergy Health PLC SYR FTSE Mid 250 Health Care Equipment & Services 9.2 20.8% 2.0% 29.9 98% 5.7

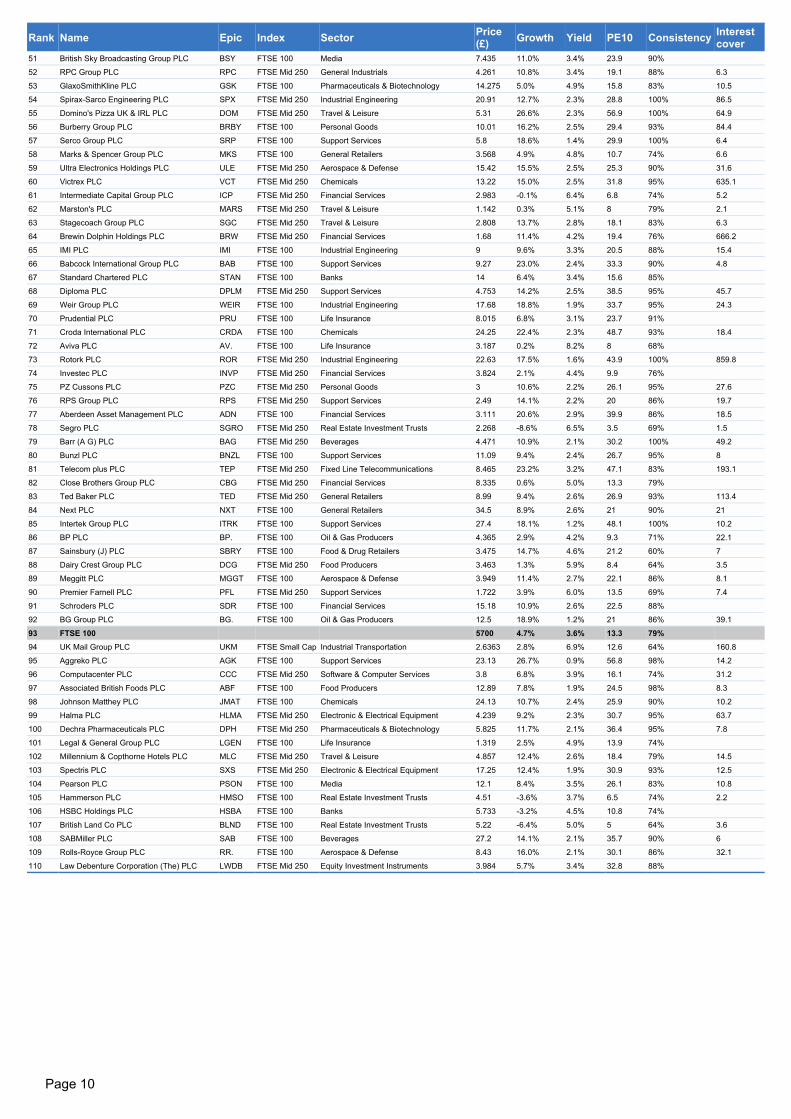

Page 10

Rank Name Epic Index Sector Price(£) Growth Yield PE10 Consistency Interest

cover51 British Sky Broadcasting Group PLC BSY FTSE 100 Media 7.435 11.0% 3.4% 23.9 90%

52 RPC Group PLC RPC FTSE Mid 250 General Industrials 4.261 10.8% 3.4% 19.1 88% 6.3

53 GlaxoSmithKline PLC GSK FTSE 100 Pharmaceuticals & Biotechnology 14.275 5.0% 4.9% 15.8 83% 10.5

54 Spirax-Sarco Engineering PLC SPX FTSE Mid 250 Industrial Engineering 20.91 12.7% 2.3% 28.8 100% 86.5

55 Domino's Pizza UK & IRL PLC DOM FTSE Mid 250 Travel & Leisure 5.31 26.6% 2.3% 56.9 100% 64.9

56 Burberry Group PLC BRBY FTSE 100 Personal Goods 10.01 16.2% 2.5% 29.4 93% 84.4

57 Serco Group PLC SRP FTSE 100 Support Services 5.8 18.6% 1.4% 29.9 100% 6.4

58 Marks & Spencer Group PLC MKS FTSE 100 General Retailers 3.568 4.9% 4.8% 10.7 74% 6.6

59 Ultra Electronics Holdings PLC ULE FTSE Mid 250 Aerospace & Defense 15.42 15.5% 2.5% 25.3 90% 31.6

60 Victrex PLC VCT FTSE Mid 250 Chemicals 13.22 15.0% 2.5% 31.8 95% 635.1

61 Intermediate Capital Group PLC ICP FTSE Mid 250 Financial Services 2.983 -0.1% 6.4% 6.8 74% 5.2

62 Marston's PLC MARS FTSE Mid 250 Travel & Leisure 1.142 0.3% 5.1% 8 79% 2.1

63 Stagecoach Group PLC SGC FTSE Mid 250 Travel & Leisure 2.808 13.7% 2.8% 18.1 83% 6.3

64 Brewin Dolphin Holdings PLC BRW FTSE Mid 250 Financial Services 1.68 11.4% 4.2% 19.4 76% 666.2

65 IMI PLC IMI FTSE 100 Industrial Engineering 9 9.6% 3.3% 20.5 88% 15.4

66 Babcock International Group PLC BAB FTSE 100 Support Services 9.27 23.0% 2.4% 33.3 90% 4.8

67 Standard Chartered PLC STAN FTSE 100 Banks 14 6.4% 3.4% 15.6 85%

68 Diploma PLC DPLM FTSE Mid 250 Support Services 4.753 14.2% 2.5% 38.5 95% 45.7

69 Weir Group PLC WEIR FTSE 100 Industrial Engineering 17.68 18.8% 1.9% 33.7 95% 24.3

70 Prudential PLC PRU FTSE 100 Life Insurance 8.015 6.8% 3.1% 23.7 91%

71 Croda International PLC CRDA FTSE 100 Chemicals 24.25 22.4% 2.3% 48.7 93% 18.4

72 Aviva PLC AV. FTSE 100 Life Insurance 3.187 0.2% 8.2% 8 68%

73 Rotork PLC ROR FTSE Mid 250 Industrial Engineering 22.63 17.5% 1.6% 43.9 100% 859.8

74 Investec PLC INVP FTSE Mid 250 Financial Services 3.824 2.1% 4.4% 9.9 76%

75 PZ Cussons PLC PZC FTSE Mid 250 Personal Goods 3 10.6% 2.2% 26.1 95% 27.6

76 RPS Group PLC RPS FTSE Mid 250 Support Services 2.49 14.1% 2.2% 20 86% 19.7

77 Aberdeen Asset Management PLC ADN FTSE 100 Financial Services 3.111 20.6% 2.9% 39.9 86% 18.5

78 Segro PLC SGRO FTSE Mid 250 Real Estate Investment Trusts 2.268 -8.6% 6.5% 3.5 69% 1.5

79 Barr (A G) PLC BAG FTSE Mid 250 Beverages 4.471 10.9% 2.1% 30.2 100% 49.2

80 Bunzl PLC BNZL FTSE 100 Support Services 11.09 9.4% 2.4% 26.7 95% 8

81 Telecom plus PLC TEP FTSE Mid 250 Fixed Line Telecommunications 8.465 23.2% 3.2% 47.1 83% 193.1

82 Close Brothers Group PLC CBG FTSE Mid 250 Financial Services 8.335 0.6% 5.0% 13.3 79%

83 Ted Baker PLC TED FTSE Mid 250 General Retailers 8.99 9.4% 2.6% 26.9 93% 113.4

84 Next PLC NXT FTSE 100 General Retailers 34.5 8.9% 2.6% 21 90% 21

85 Intertek Group PLC ITRK FTSE 100 Support Services 27.4 18.1% 1.2% 48.1 100% 10.2

86 BP PLC BP. FTSE 100 Oil & Gas Producers 4.365 2.9% 4.2% 9.3 71% 22.1

87 Sainsbury (J) PLC SBRY FTSE 100 Food & Drug Retailers 3.475 14.7% 4.6% 21.2 60% 7

88 Dairy Crest Group PLC DCG FTSE Mid 250 Food Producers 3.463 1.3% 5.9% 8.4 64% 3.5

89 Meggitt PLC MGGT FTSE 100 Aerospace & Defense 3.949 11.4% 2.7% 22.1 86% 8.1

90 Premier Farnell PLC PFL FTSE Mid 250 Support Services 1.722 3.9% 6.0% 13.5 69% 7.4

91 Schroders PLC SDR FTSE 100 Financial Services 15.18 10.9% 2.6% 22.5 88%

92 BG Group PLC BG. FTSE 100 Oil & Gas Producers 12.5 18.9% 1.2% 21 86% 39.1

93 FTSE 100 5700 4.7% 3.6% 13.3 79%94 UK Mail Group PLC UKM FTSE Small Cap Industrial Transportation 2.6363 2.8% 6.9% 12.6 64% 160.8

95 Aggreko PLC AGK FTSE 100 Support Services 23.13 26.7% 0.9% 56.8 98% 14.2

96 Computacenter PLC CCC FTSE Mid 250 Software & Computer Services 3.8 6.8% 3.9% 16.1 74% 31.2

97 Associated British Foods PLC ABF FTSE 100 Food Producers 12.89 7.8% 1.9% 24.5 98% 8.3

98 Johnson Matthey PLC JMAT FTSE 100 Chemicals 24.13 10.7% 2.4% 25.9 90% 10.2

99 Halma PLC HLMA FTSE Mid 250 Electronic & Electrical Equipment 4.239 9.2% 2.3% 30.7 95% 63.7

100 Dechra Pharmaceuticals PLC DPH FTSE Mid 250 Pharmaceuticals & Biotechnology 5.825 11.7% 2.1% 36.4 95% 7.8

101 Legal & General Group PLC LGEN FTSE 100 Life Insurance 1.319 2.5% 4.9% 13.9 74%

102 Millennium & Copthorne Hotels PLC MLC FTSE Mid 250 Travel & Leisure 4.857 12.4% 2.6% 18.4 79% 14.5

103 Spectris PLC SXS FTSE Mid 250 Electronic & Electrical Equipment 17.25 12.4% 1.9% 30.9 93% 12.5

104 Pearson PLC PSON FTSE 100 Media 12.1 8.4% 3.5% 26.1 83% 10.8

105 Hammerson PLC HMSO FTSE 100 Real Estate Investment Trusts 4.51 -3.6% 3.7% 6.5 74% 2.2

106 HSBC Holdings PLC HSBA FTSE 100 Banks 5.733 -3.2% 4.5% 10.8 74%

107 British Land Co PLC BLND FTSE 100 Real Estate Investment Trusts 5.22 -6.4% 5.0% 5 64% 3.6

108 SABMiller PLC SAB FTSE 100 Beverages 27.2 14.1% 2.1% 35.7 90% 6

109 Rolls-Royce Group PLC RR. FTSE 100 Aerospace & Defense 8.43 16.0% 2.1% 30.1 86% 32.1

110 Law Debenture Corporation (The) PLC LWDB FTSE Mid 250 Equity Investment Instruments 3.984 5.7% 3.4% 32.8 88%

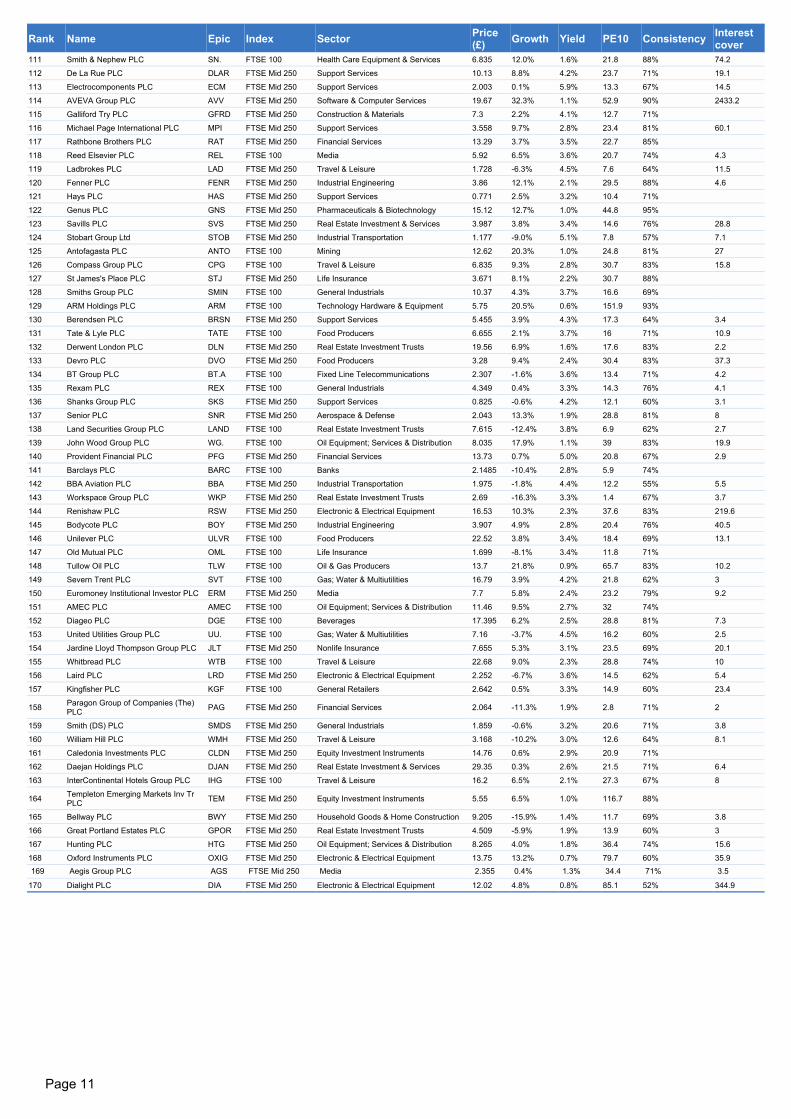

Page 11

Rank Name Epic Index Sector Price(£) Growth Yield PE10 Consistency Interest

cover111 Smith & Nephew PLC SN. FTSE 100 Health Care Equipment & Services 6.835 12.0% 1.6% 21.8 88% 74.2

112 De La Rue PLC DLAR FTSE Mid 250 Support Services 10.13 8.8% 4.2% 23.7 71% 19.1

113 Electrocomponents PLC ECM FTSE Mid 250 Support Services 2.003 0.1% 5.9% 13.3 67% 14.5

114 AVEVA Group PLC AVV FTSE Mid 250 Software & Computer Services 19.67 32.3% 1.1% 52.9 90% 2433.2

115 Galliford Try PLC GFRD FTSE Mid 250 Construction & Materials 7.3 2.2% 4.1% 12.7 71%

116 Michael Page International PLC MPI FTSE Mid 250 Support Services 3.558 9.7% 2.8% 23.4 81% 60.1

117 Rathbone Brothers PLC RAT FTSE Mid 250 Financial Services 13.29 3.7% 3.5% 22.7 85%

118 Reed Elsevier PLC REL FTSE 100 Media 5.92 6.5% 3.6% 20.7 74% 4.3

119 Ladbrokes PLC LAD FTSE Mid 250 Travel & Leisure 1.728 -6.3% 4.5% 7.6 64% 11.5

120 Fenner PLC FENR FTSE Mid 250 Industrial Engineering 3.86 12.1% 2.1% 29.5 88% 4.6

121 Hays PLC HAS FTSE Mid 250 Support Services 0.771 2.5% 3.2% 10.4 71%

122 Genus PLC GNS FTSE Mid 250 Pharmaceuticals & Biotechnology 15.12 12.7% 1.0% 44.8 95%

123 Savills PLC SVS FTSE Mid 250 Real Estate Investment & Services 3.987 3.8% 3.4% 14.6 76% 28.8

124 Stobart Group Ltd STOB FTSE Mid 250 Industrial Transportation 1.177 -9.0% 5.1% 7.8 57% 7.1

125 Antofagasta PLC ANTO FTSE 100 Mining 12.62 20.3% 1.0% 24.8 81% 27

126 Compass Group PLC CPG FTSE 100 Travel & Leisure 6.835 9.3% 2.8% 30.7 83% 15.8

127 St James's Place PLC STJ FTSE Mid 250 Life Insurance 3.671 8.1% 2.2% 30.7 88%

128 Smiths Group PLC SMIN FTSE 100 General Industrials 10.37 4.3% 3.7% 16.6 69%

129 ARM Holdings PLC ARM FTSE 100 Technology Hardware & Equipment 5.75 20.5% 0.6% 151.9 93%

130 Berendsen PLC BRSN FTSE Mid 250 Support Services 5.455 3.9% 4.3% 17.3 64% 3.4

131 Tate & Lyle PLC TATE FTSE 100 Food Producers 6.655 2.1% 3.7% 16 71% 10.9

132 Derwent London PLC DLN FTSE Mid 250 Real Estate Investment Trusts 19.56 6.9% 1.6% 17.6 83% 2.2

133 Devro PLC DVO FTSE Mid 250 Food Producers 3.28 9.4% 2.4% 30.4 83% 37.3

134 BT Group PLC BT.A FTSE 100 Fixed Line Telecommunications 2.307 -1.6% 3.6% 13.4 71% 4.2

135 Rexam PLC REX FTSE 100 General Industrials 4.349 0.4% 3.3% 14.3 76% 4.1

136 Shanks Group PLC SKS FTSE Mid 250 Support Services 0.825 -0.6% 4.2% 12.1 60% 3.1

137 Senior PLC SNR FTSE Mid 250 Aerospace & Defense 2.043 13.3% 1.9% 28.8 81% 8

138 Land Securities Group PLC LAND FTSE 100 Real Estate Investment Trusts 7.615 -12.4% 3.8% 6.9 62% 2.7

139 John Wood Group PLC WG. FTSE 100 Oil Equipment; Services & Distribution 8.035 17.9% 1.1% 39 83% 19.9

140 Provident Financial PLC PFG FTSE Mid 250 Financial Services 13.73 0.7% 5.0% 20.8 67% 2.9

141 Barclays PLC BARC FTSE 100 Banks 2.1485 -10.4% 2.8% 5.9 74%

142 BBA Aviation PLC BBA FTSE Mid 250 Industrial Transportation 1.975 -1.8% 4.4% 12.2 55% 5.5

143 Workspace Group PLC WKP FTSE Mid 250 Real Estate Investment Trusts 2.69 -16.3% 3.3% 1.4 67% 3.7

144 Renishaw PLC RSW FTSE Mid 250 Electronic & Electrical Equipment 16.53 10.3% 2.3% 37.6 83% 219.6

145 Bodycote PLC BOY FTSE Mid 250 Industrial Engineering 3.907 4.9% 2.8% 20.4 76% 40.5

146 Unilever PLC ULVR FTSE 100 Food Producers 22.52 3.8% 3.4% 18.4 69% 13.1

147 Old Mutual PLC OML FTSE 100 Life Insurance 1.699 -8.1% 3.4% 11.8 71%

148 Tullow Oil PLC TLW FTSE 100 Oil & Gas Producers 13.7 21.8% 0.9% 65.7 83% 10.2

149 Severn Trent PLC SVT FTSE 100 Gas; Water & Multiutilities 16.79 3.9% 4.2% 21.8 62% 3

150 Euromoney Institutional Investor PLC ERM FTSE Mid 250 Media 7.7 5.8% 2.4% 23.2 79% 9.2

151 AMEC PLC AMEC FTSE 100 Oil Equipment; Services & Distribution 11.46 9.5% 2.7% 32 74%

152 Diageo PLC DGE FTSE 100 Beverages 17.395 6.2% 2.5% 28.8 81% 7.3

153 United Utilities Group PLC UU. FTSE 100 Gas; Water & Multiutilities 7.16 -3.7% 4.5% 16.2 60% 2.5

154 Jardine Lloyd Thompson Group PLC JLT FTSE Mid 250 Nonlife Insurance 7.655 5.3% 3.1% 23.5 69% 20.1

155 Whitbread PLC WTB FTSE 100 Travel & Leisure 22.68 9.0% 2.3% 28.8 74% 10

156 Laird PLC LRD FTSE Mid 250 Electronic & Electrical Equipment 2.252 -6.7% 3.6% 14.5 62% 5.4

157 Kingfisher PLC KGF FTSE 100 General Retailers 2.642 0.5% 3.3% 14.9 60% 23.4

158 Paragon Group of Companies (The)PLC PAG FTSE Mid 250 Financial Services 2.064 -11.3% 1.9% 2.8 71% 2

159 Smith (DS) PLC SMDS FTSE Mid 250 General Industrials 1.859 -0.6% 3.2% 20.6 71% 3.8

160 William Hill PLC WMH FTSE Mid 250 Travel & Leisure 3.168 -10.2% 3.0% 12.6 64% 8.1

161 Caledonia Investments PLC CLDN FTSE Mid 250 Equity Investment Instruments 14.76 0.6% 2.9% 20.9 71%

162 Daejan Holdings PLC DJAN FTSE Mid 250 Real Estate Investment & Services 29.35 0.3% 2.6% 21.5 71% 6.4

163 InterContinental Hotels Group PLC IHG FTSE 100 Travel & Leisure 16.2 6.5% 2.1% 27.3 67% 8

164 Templeton Emerging Markets Inv TrPLC TEM FTSE Mid 250 Equity Investment Instruments 5.55 6.5% 1.0% 116.7 88%

165 Bellway PLC BWY FTSE Mid 250 Household Goods & Home Construction 9.205 -15.9% 1.4% 11.7 69% 3.8

166 Great Portland Estates PLC GPOR FTSE Mid 250 Real Estate Investment Trusts 4.509 -5.9% 1.9% 13.9 60% 3

167 Hunting PLC HTG FTSE Mid 250 Oil Equipment; Services & Distribution 8.265 4.0% 1.8% 36.4 74% 15.6

168 Oxford Instruments PLC OXIG FTSE Mid 250 Electronic & Electrical Equipment 13.75 13.2% 0.7% 79.7 60% 35.9169 Aegis Group PLC AGS FTSE Mid 250 Media 2.355 0.4% 1.3% 34.4 71% 3.5

170 Dialight PLC DIA FTSE Mid 250 Electronic & Electrical Equipment 12.02 4.8% 0.8% 85.1 52% 344.9

Page 12

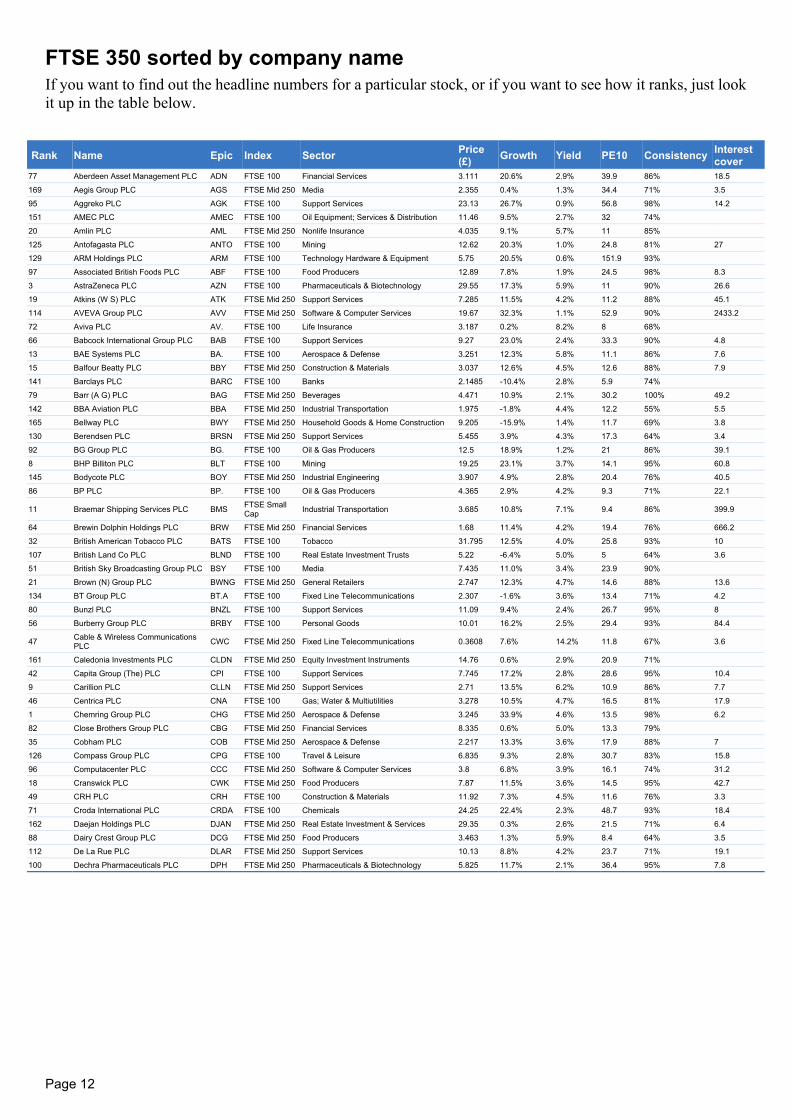

FTSE 350 sorted by company nameIf you want to find out the headline numbers for a particular stock, or if you want to see how it ranks, just lookit up in the table below.

Rank Name Epic Index Sector Price(£) Growth Yield PE10 Consistency Interest

cover77 Aberdeen Asset Management PLC ADN FTSE 100 Financial Services 3.111 20.6% 2.9% 39.9 86% 18.5

169 Aegis Group PLC AGS FTSE Mid 250 Media 2.355 0.4% 1.3% 34.4 71% 3.5

95 Aggreko PLC AGK FTSE 100 Support Services 23.13 26.7% 0.9% 56.8 98% 14.2

151 AMEC PLC AMEC FTSE 100 Oil Equipment; Services & Distribution 11.46 9.5% 2.7% 32 74%

20 Amlin PLC AML FTSE Mid 250 Nonlife Insurance 4.035 9.1% 5.7% 11 85%

125 Antofagasta PLC ANTO FTSE 100 Mining 12.62 20.3% 1.0% 24.8 81% 27

129 ARM Holdings PLC ARM FTSE 100 Technology Hardware & Equipment 5.75 20.5% 0.6% 151.9 93%

97 Associated British Foods PLC ABF FTSE 100 Food Producers 12.89 7.8% 1.9% 24.5 98% 8.3

3 AstraZeneca PLC AZN FTSE 100 Pharmaceuticals & Biotechnology 29.55 17.3% 5.9% 11 90% 26.6

19 Atkins (W S) PLC ATK FTSE Mid 250 Support Services 7.285 11.5% 4.2% 11.2 88% 45.1

114 AVEVA Group PLC AVV FTSE Mid 250 Software & Computer Services 19.67 32.3% 1.1% 52.9 90% 2433.2

72 Aviva PLC AV. FTSE 100 Life Insurance 3.187 0.2% 8.2% 8 68%

66 Babcock International Group PLC BAB FTSE 100 Support Services 9.27 23.0% 2.4% 33.3 90% 4.8

13 BAE Systems PLC BA. FTSE 100 Aerospace & Defense 3.251 12.3% 5.8% 11.1 86% 7.6

15 Balfour Beatty PLC BBY FTSE Mid 250 Construction & Materials 3.037 12.6% 4.5% 12.6 88% 7.9

141 Barclays PLC BARC FTSE 100 Banks 2.1485 -10.4% 2.8% 5.9 74%

79 Barr (A G) PLC BAG FTSE Mid 250 Beverages 4.471 10.9% 2.1% 30.2 100% 49.2

142 BBA Aviation PLC BBA FTSE Mid 250 Industrial Transportation 1.975 -1.8% 4.4% 12.2 55% 5.5

165 Bellway PLC BWY FTSE Mid 250 Household Goods & Home Construction 9.205 -15.9% 1.4% 11.7 69% 3.8

130 Berendsen PLC BRSN FTSE Mid 250 Support Services 5.455 3.9% 4.3% 17.3 64% 3.4

92 BG Group PLC BG. FTSE 100 Oil & Gas Producers 12.5 18.9% 1.2% 21 86% 39.1

8 BHP Billiton PLC BLT FTSE 100 Mining 19.25 23.1% 3.7% 14.1 95% 60.8

145 Bodycote PLC BOY FTSE Mid 250 Industrial Engineering 3.907 4.9% 2.8% 20.4 76% 40.5

86 BP PLC BP. FTSE 100 Oil & Gas Producers 4.365 2.9% 4.2% 9.3 71% 22.1

11 Braemar Shipping Services PLC BMS FTSE SmallCap Industrial Transportation 3.685 10.8% 7.1% 9.4 86% 399.9

64 Brewin Dolphin Holdings PLC BRW FTSE Mid 250 Financial Services 1.68 11.4% 4.2% 19.4 76% 666.2

32 British American Tobacco PLC BATS FTSE 100 Tobacco 31.795 12.5% 4.0% 25.8 93% 10

107 British Land Co PLC BLND FTSE 100 Real Estate Investment Trusts 5.22 -6.4% 5.0% 5 64% 3.6

51 British Sky Broadcasting Group PLC BSY FTSE 100 Media 7.435 11.0% 3.4% 23.9 90%

21 Brown (N) Group PLC BWNG FTSE Mid 250 General Retailers 2.747 12.3% 4.7% 14.6 88% 13.6

134 BT Group PLC BT.A FTSE 100 Fixed Line Telecommunications 2.307 -1.6% 3.6% 13.4 71% 4.2

80 Bunzl PLC BNZL FTSE 100 Support Services 11.09 9.4% 2.4% 26.7 95% 8

56 Burberry Group PLC BRBY FTSE 100 Personal Goods 10.01 16.2% 2.5% 29.4 93% 84.4

47 Cable & Wireless CommunicationsPLC CWC FTSE Mid 250 Fixed Line Telecommunications 0.3608 7.6% 14.2% 11.8 67% 3.6

161 Caledonia Investments PLC CLDN FTSE Mid 250 Equity Investment Instruments 14.76 0.6% 2.9% 20.9 71%

42 Capita Group (The) PLC CPI FTSE 100 Support Services 7.745 17.2% 2.8% 28.6 95% 10.4

9 Carillion PLC CLLN FTSE Mid 250 Support Services 2.71 13.5% 6.2% 10.9 86% 7.7

46 Centrica PLC CNA FTSE 100 Gas; Water & Multiutilities 3.278 10.5% 4.7% 16.5 81% 17.9

1 Chemring Group PLC CHG FTSE Mid 250 Aerospace & Defense 3.245 33.9% 4.6% 13.5 98% 6.2

82 Close Brothers Group PLC CBG FTSE Mid 250 Financial Services 8.335 0.6% 5.0% 13.3 79%

35 Cobham PLC COB FTSE Mid 250 Aerospace & Defense 2.217 13.3% 3.6% 17.9 88% 7

126 Compass Group PLC CPG FTSE 100 Travel & Leisure 6.835 9.3% 2.8% 30.7 83% 15.8

96 Computacenter PLC CCC FTSE Mid 250 Software & Computer Services 3.8 6.8% 3.9% 16.1 74% 31.2

18 Cranswick PLC CWK FTSE Mid 250 Food Producers 7.87 11.5% 3.6% 14.5 95% 42.7

49 CRH PLC CRH FTSE 100 Construction & Materials 11.92 7.3% 4.5% 11.6 76% 3.3

71 Croda International PLC CRDA FTSE 100 Chemicals 24.25 22.4% 2.3% 48.7 93% 18.4

162 Daejan Holdings PLC DJAN FTSE Mid 250 Real Estate Investment & Services 29.35 0.3% 2.6% 21.5 71% 6.4

88 Dairy Crest Group PLC DCG FTSE Mid 250 Food Producers 3.463 1.3% 5.9% 8.4 64% 3.5

112 De La Rue PLC DLAR FTSE Mid 250 Support Services 10.13 8.8% 4.2% 23.7 71% 19.1

100 Dechra Pharmaceuticals PLC DPH FTSE Mid 250 Pharmaceuticals & Biotechnology 5.825 11.7% 2.1% 36.4 95% 7.8

Page 13

Rank Name Epic Index Sector Price(£) Growth Yield PE10 Consistency Interest

cover132 Derwent London PLC DLN FTSE Mid 250 Real Estate Investment Trusts 19.56 6.9% 1.6% 17.6 83% 2.2

133 Devro PLC DVO FTSE Mid 250 Food Producers 3.28 9.4% 2.4% 30.4 83% 37.3

152 Diageo PLC DGE FTSE 100 Beverages 17.395 6.2% 2.5% 28.8 81% 7.3

170 Dialight PLC DIA FTSE Mid 250 Electronic & Electrical Equipment 12.02 4.8% 0.8% 85.1 52% 344.9

68 Diploma PLC DPLM FTSE Mid 250 Support Services 4.753 14.2% 2.5% 38.5 95% 45.7

31 Domino Printing Sciences PLC DNO FTSE Mid 250 Electronic & Electrical Equipment 5.535 12.8% 3.4% 24.3 95% 159.7

55 Domino's Pizza UK & IRL PLC DOM FTSE Mid 250 Travel & Leisure 5.31 26.6% 2.3% 56.9 100% 64.9

113 Electrocomponents PLC ECM FTSE Mid 250 Support Services 2.003 0.1% 5.9% 13.3 67% 14.5

150 Euromoney Institutional Investor PLC ERM FTSE Mid 250 Media 7.7 5.8% 2.4% 23.2 79% 9.2

120 Fenner PLC FENR FTSE Mid 250 Industrial Engineering 3.86 12.1% 2.1% 29.5 88% 4.6

44 Fidessa Group PLC FDSA FTSE Mid 250 Software & Computer Services 14.71 23.0% 2.5% 33.6 98%

2 FirstGroup PLC FGP FTSE Mid 250 Travel & Leisure 2.4 10.2% 9.9% 6.7 93% 2.9

93 FTSE 100 57 4.7% 3.6% 13.3 79%115 Galliford Try PLC GFRD FTSE Mid 250 Construction & Materials 7.3 2.2% 4.1% 12.7 71%

122 Genus PLC GNS FTSE Mid 250 Pharmaceuticals & Biotechnology 15.12 12.7% 1.0% 44.8 95%

53 GlaxoSmithKline PLC GSK FTSE 100 Pharmaceuticals & Biotechnology 14.275 5.0% 4.9% 15.8 83% 10.5

28 Go-Ahead Group (The) PLC GOG FTSE Mid 250 Travel & Leisure 13.12 7.4% 6.2% 9.4 79% 6.1

166 Great Portland Estates PLC GPOR FTSE Mid 250 Real Estate Investment Trusts 4.509 -5.9% 1.9% 13.9 60% 3

41 Greene King PLC GNK FTSE Mid 250 Travel & Leisure 6.005 6.8% 4.1% 12.8 88% 2.6

33 Greggs PLC GRG FTSE Mid 250 Food & Drug Retailers 5.02 7.5% 3.8% 16.3 93%

99 Halma PLC HLMA FTSE Mid 250 Electronic & Electrical Equipment 4.239 9.2% 2.3% 30.7 95% 63.7

105 Hammerson PLC HMSO FTSE 100 Real Estate Investment Trusts 4.51 -3.6% 3.7% 6.5 74% 2.2

121 Hays PLC HAS FTSE Mid 250 Support Services 0.771 2.5% 3.2% 10.4 71%

27 Homeserve PLC HSV FTSE Mid 250 Support Services 2.1 13.1% 5.4% 12.7 79% 52

106 HSBC Holdings PLC HSBA FTSE 100 Banks 5.733 -3.2% 4.5% 10.8 74%

167 Hunting PLC HTG FTSE Mid 250 Oil Equipment; Services & Distribution 8.265 4.0% 1.8% 36.4 74% 15.6

5 ICAP PLC IAP FTSE Mid 250 Financial Services 3.211 12.3% 6.9% 12.3 93% 9.6

65 IMI PLC IMI FTSE 100 Industrial Engineering 9 9.6% 3.3% 20.5 88% 15.4

26 Imperial Tobacco Group PLC IMT FTSE 100 Tobacco 22.92 20.1% 4.1% 20.5 88% 3.7

163 InterContinental Hotels Group PLC IHG FTSE 100 Travel & Leisure 16.2 6.5% 2.1% 27.3 67% 8

61 Intermediate Capital Group PLC ICP FTSE Mid 250 Financial Services 2.983 -0.1% 6.4% 6.8 74% 5.2

37 Interserve PLC IRV FTSE Mid 250 Support Services 3.646 8.3% 5.2% 13.9 83% 8.6

85 Intertek Group PLC ITRK FTSE 100 Support Services 27.4 18.1% 1.2% 48.1 100% 10.2

74 Investec PLC INVP FTSE Mid 250 Financial Services 3.824 2.1% 4.4% 9.9 76%

38 ITE Group PLC ITE FTSE Mid 250 Media 2.061 14.7% 3.0% 24.4 95% 31.7

154 Jardine Lloyd Thompson Group PLC JLT FTSE Mid 250 Nonlife Insurance 7.655 5.3% 3.1% 23.5 69% 20.1

4 JD Sports Fashion PLC JD. FTSE Mid 250 General Retailers 7.01 22.8% 3.6% 10.8 95% 73.7

139 John Wood Group PLC WG. FTSE 100 Oil Equipment; Services & Distribution 8.035 17.9% 1.1% 39 83% 19.9

98 Johnson Matthey PLC JMAT FTSE 100 Chemicals 24.13 10.7% 2.4% 25.9 90% 10.2

48 Kier Group PLC KIE FTSE Mid 250 Construction & Materials 12.95 9.1% 5.1% 12.8 74%

157 Kingfisher PLC KGF FTSE 100 General Retailers 2.642 0.5% 3.3% 14.9 60% 23.4

119 Ladbrokes PLC LAD FTSE Mid 250 Travel & Leisure 1.728 -6.3% 4.5% 7.6 64% 11.5

156 Laird PLC LRD FTSE Mid 250 Electronic & Electrical Equipment 2.252 -6.7% 3.6% 14.5 62% 5.4

138 Land Securities Group PLC LAND FTSE 100 Real Estate Investment Trusts 7.615 -12.4% 3.8% 6.9 62% 2.7

110 Law Debenture Corporation (The) PLC LWDB FTSE Mid 250 Equity Investment Instruments 3.984 5.7% 3.4% 32.8 88%

101 Legal & General Group PLC LGEN FTSE 100 Life Insurance 1.319 2.5% 4.9% 13.9 74%

43 London Stock Exchange Group PLC LSE FTSE Mid 250 Financial Services 9.43 17.4% 3.0% 18.6 86% 7.5

36 Man Group PLC EMG FTSE Mid 250 Financial Services 0.8235 5.1% 12.5% 3.6 71% 6.6

58 Marks & Spencer Group PLC MKS FTSE 100 General Retailers 3.568 4.9% 4.8% 10.7 74% 6.6

62 Marston's PLC MARS FTSE Mid 250 Travel & Leisure 1.142 0.3% 5.1% 8 79% 2.1

23 Mears Group PLC MER FTSE Small Cap Support Services 2.83 19.7% 2.7% 18.9 98% 11.5

89 Meggitt PLC MGGT FTSE 100 Aerospace & Defense 3.949 11.4% 2.7% 22.1 86% 8.1

116 Michael Page International PLC MPI FTSE Mid 250 Support Services 3.558 9.7% 2.8% 23.4 81% 60.1

102 Millennium & Copthorne Hotels PLC MLC FTSE Mid 250 Travel & Leisure 4.857 12.4% 2.6% 18.4 79% 14.5

22 MITIE Group PLC MTO FTSE Mid 250 Support Services 2.913 15.3% 3.3% 20.3 98% 13.7

30 Morrison (Wm) Supermarkets PLC MRW FTSE 100 Food & Drug Retailers 2.852 16.0% 3.8% 19 86% 22.1

45 National Grid PLC NG. FTSE 100 Gas; Water & Multiutilities 6.83 9.3% 5.8% 13.9 76% 3.9

84 Next PLC NXT FTSE 100 General Retailers 34.5 8.9% 2.6% 21 90% 21

147 Old Mutual PLC OML FTSE 100 Life Insurance 1.699 -8.1% 3.4% 11.8 71%168 Oxford Instruments PLC OXIG FTSE Mid 250 Electronic & Electrical Equipment 13.75 13.2% 0.7% 79.7 60% 35.9

Page 14

Rank Name Epic Index Sector Price(£) Growth Yield PE10 Consistency Interest

cover158 Paragon Group of Companies (The) PLC PAG FTSE Mid 250 Financial Services 2.064 -11.3% 1.9% 2.8 71% 2

104 Pearson PLC PSON FTSE 100 Media 12.1 8.4% 3.5% 26.1 83% 10.8

29 Pennon Group PLC PNN FTSE 100 Gas; Water & Multiutilities 7.225 11.8% 3.7% 24.1 95% 3.3

90 Premier Farnell PLC PFL FTSE Mid 250 Support Services 1.722 3.9% 6.0% 13.5 69% 7.4

140 Provident Financial PLC PFG FTSE Mid 250 Financial Services 13.73 0.7% 5.0% 20.8 67% 2.9

70 Prudential PLC PRU FTSE 100 Life Insurance 8.015 6.8% 3.1% 23.7 91%

75 PZ Cussons PLC PZC FTSE Mid 250 Personal Goods 3 10.6% 2.2% 26.1 95% 27.6

117 Rathbone Brothers PLC RAT FTSE Mid 250 Financial Services 13.29 3.7% 3.5% 22.7 85%

17 Reckitt Benckiser Group PLC RB. FTSE 100 Household Goods & Home Construction 35.65 18.3% 3.5% 25 100% 71.3

118 Reed Elsevier PLC REL FTSE 100 Media 5.92 6.5% 3.6% 20.7 74% 4.3

144 Renishaw PLC RSW FTSE Mid 250 Electronic & Electrical Equipment 16.53 10.3% 2.3% 37.6 83% 219.6

39 Restaurant Group (The) PLC RTN FTSE Mid 250 Travel & Leisure 3.578 15.0% 2.9% 24.4 95% 32.2

135 Rexam PLC REX FTSE 100 General Industrials 4.349 0.4% 3.3% 14.3 76% 4.1

24 Rio Tinto PLC RIO FTSE 100 Mining 28.85 21.1% 3.1% 10.8 83% 35.5

109 Rolls-Royce Group PLC RR. FTSE 100 Aerospace & Defense 8.43 16.0% 2.1% 30.1 86% 32.1

73 Rotork PLC ROR FTSE Mid 250 Industrial Engineering 22.63 17.5% 1.6% 43.9 100% 859.8

52 RPC Group PLC RPC FTSE Mid 250 General Industrials 4.261 10.8% 3.4% 19.1 88% 6.3

76 RPS Group PLC RPS FTSE Mid 250 Support Services 2.49 14.1% 2.2% 20 86% 19.7

7 RSA Insurance Group PLC RSA FTSE 100 Nonlife Insurance 1.105 18.9% 8.3% 10.6 82%

108 SABMiller PLC SAB FTSE 100 Beverages 27.2 14.1% 2.1% 35.7 90% 6

40 Sage Group (The) PLC SGE FTSE 100 Software & Computer Services 3.134 15.7% 3.1% 24.2 93% 23.6

87 Sainsbury (J) PLC SBRY FTSE 100 Food & Drug Retailers 3.475 14.7% 4.6% 21.2 60% 7

123 Savills PLC SVS FTSE Mid 250 Real Estate Investment & Services 3.987 3.8% 3.4% 14.6 76% 28.8

91 Schroders PLC SDR FTSE 100 Financial Services 15.18 10.9% 2.6% 22.5 88%

78 Segro PLC SGRO FTSE Mid 250 Real Estate Investment Trusts 2.268 -8.6% 6.5% 3.5 69% 1.5

137 Senior PLC SNR FTSE Mid 250 Aerospace & Defense 2.043 13.3% 1.9% 28.8 81% 8

57 Serco Group PLC SRP FTSE 100 Support Services 5.8 18.6% 1.4% 29.9 100% 6.4

149 Severn Trent PLC SVT FTSE 100 Gas; Water & Multiutilities 16.79 3.9% 4.2% 21.8 62% 3

136 Shanks Group PLC SKS FTSE Mid 250 Support Services 0.825 -0.6% 4.2% 12.1 60% 3.1

111 Smith & Nephew PLC SN. FTSE 100 Health Care Equipment & Services 6.835 12.0% 1.6% 21.8 88% 74.2

159 Smith (DS) PLC SMDS FTSE Mid 250 General Industrials 1.859 -0.6% 3.2% 20.6 71% 3.8

128 Smiths Group PLC SMIN FTSE 100 General Industrials 10.37 4.3% 3.7% 16.6 69%

103 Spectris PLC SXS FTSE Mid 250 Electronic & Electrical Equipment 17.25 12.4% 1.9% 30.9 93% 12.5

54 Spirax-Sarco Engineering PLC SPX FTSE Mid 250 Industrial Engineering 20.91 12.7% 2.3% 28.8 100% 86.5

10 SSE PLC SSE FTSE 100 Electricity 13.92 16.5% 5.8% 15.9 90% 7.9

127 St James's Place PLC STJ FTSE Mid 250 Life Insurance 3.671 8.1% 2.2% 30.7 88%

63 Stagecoach Group PLC SGC FTSE Mid 250 Travel & Leisure 2.808 13.7% 2.8% 18.1 83% 6.3

67 Standard Chartered PLC STAN FTSE 100 Banks 14 6.4% 3.4% 15.6 85%

124 Stobart Group Ltd STOB FTSE Mid 250 Industrial Transportation 1.177 -9.0% 5.1% 7.8 57% 7.1

50 Synergy Health PLC SYR FTSE Mid 250 Health Care Equipment & Services 9.2 20.8% 2.0% 29.9 98% 5.7

131 Tate & Lyle PLC TATE FTSE 100 Food Producers 6.655 2.1% 3.7% 16 71% 10.9

83 Ted Baker PLC TED FTSE Mid 250 General Retailers 8.99 9.4% 2.6% 26.9 93% 113.4

81 Telecom plus PLC TEP FTSE Mid 250 Fixed Line Telecommunications 8.465 23.2% 3.2% 47.1 83% 193.1

164 Templeton Emerging Markets Inv Tr PLC TEM FTSE Mid 250 Equity Investment Instruments 5.55 6.5% 1.0% 116.7 88%

14 Tesco PLC TSCO FTSE 100 Food & Drug Retailers 3.32 9.7% 4.4% 14.2 98% 8.6

6 Tullett Prebon PLC TLPR FTSE Mid 250 Financial Services 2.98 16.0% 5.5% 8.6 88% 9.9

148 Tullow Oil PLC TLW FTSE 100 Oil & Gas Producers 13.7 21.8% 0.9% 65.7 83% 10.2

94 UK Mail Group PLC UKM FTSE Small Cap Industrial Transportation 2.6363 2.8% 6.9% 12.6 64% 160.8

59 Ultra Electronics Holdings PLC ULE FTSE Mid 250 Aerospace & Defense 15.42 15.5% 2.5% 25.3 90% 31.6

146 Unilever PLC ULVR FTSE 100 Food Producers 22.52 3.8% 3.4% 18.4 69% 13.1

153 United Utilities Group PLC UU. FTSE 100 Gas; Water & Multiutilities 7.16 -3.7% 4.5% 16.2 60% 2.5

12 Vedanta Resources PLC VED FTSE 100 Mining 10.29 27.7% 3.3% 10.6 90% 6.6

60 Victrex PLC VCT FTSE Mid 250 Chemicals 13.22 15.0% 2.5% 31.8 95% 635.1

16 Vodafone Group PLC VOD FTSE 100 Mobile Telecommunications 1.7575 11.1% 5.4% 12.6 88% 8.8

69 Weir Group PLC WEIR FTSE 100 Industrial Engineering 17.68 18.8% 1.9% 33.7 95% 24.3

155 Whitbread PLC WTB FTSE 100 Travel & Leisure 22.68 9.0% 2.3% 28.8 74% 10

160 William Hill PLC WMH FTSE Mid 250 Travel & Leisure 3.168 -10.2% 3.0% 12.6 64% 8.1

143 Workspace Group PLC WKP FTSE Mid 250 Real Estate Investment Trusts 2.69 -16.3% 3.3% 1.4 67% 3.7

34 WPP Group PLC WPP FTSE 100 Media 8.415 12.7% 2.9% 20.5 95% 3.9

25 Xstrata PLC XTA FTSE 100 Mining 9.575 21.2% 2.6% 10.2 86% 28.5

Page 15

IMPORTANT DISCLAIMER: The author is not registered as an investment advisor or as an independent financialadvisor and does not provide individual investment advice. Neither the author nor this document are regulated by theFinancial Services Authority. No information provided in this document should ever be construed as investment advice.It is prepared for education and information only. The specific needs, investment objectives and financial situation of anyparticular reader have not been taken into consideration and the investments mentioned may not be suitable for anyindividual. The information contained in this document is not intended to be an offer to buy or sell or a solicitation of anoffer to buy or sell any securities. Readers must not base any investment decision solely on the basis of this document;instead they should seek independent financial advice. The information in this document and any expression of opinionby the author have been obtained from or are based on sources believed to be reliable but the accuracy or completenessof any such sources or the author’s interpretation of them cannot be guaranteed although the author believes thedocument to be clear, fair and not misleading. The author receives no compensation from and is not affiliated with anycompany mentioned in this document other than possibly receiving advertising revenue via a third party. The viewsreflected in this document may be wrong and may change without notice. To the maximum extent possible at law, theauthor does not accept any liability whatsoever arising from the use of the material or information contained herein.

INVESTMENT RISK: The value of shares can fall as well as rise. Dividend payments can fall as well as rise. Anyinformation relating to past performance of an investment or investment service is not necessarily a guide to futureperformance. There is an additional risk of making a loss when you buy shares in certain smaller companies. There is abig difference between the buying price and the selling price of some shares and if you have to sell quickly you may getback much less than you paid. Share prices may go down as well as up and you may not get back the original amountinvested. It may be difficult to sell or realize an investment. You should not buy shares with money you cannot afford tolose.

DISCLOSURE RULES: When content is published about a company and the author has a position or beneficial interestin it, that fact will be disclosed.

In addition to the above disclosure requirement, the author follows additional trading restrictions and guidelines. Theserestrictions require that the author:

· Hold any stocks owned for at least 10 full market business days.

· Cannot write about a stock for 2 business days before and after purchasing or selling the stock.

DISCLOSURE: The author owns shares in all of the companies in the model portfolio and intends to buy shares in anynew model portfolio investments, and sell the shares of any model portfolio holdings which are sold.

CONFIDENTIALITY: This document is for subscribers only. Please retain it for your own exclusive use and treat it asconfidential.

© John Kingham, 2012. Offices at Unit 5, Pluto House, 19-33 Station Road, Ashford, Kent, TN23 1PP.

Subscribe online at ukvalueinvestor.com