Embed Size (px)

Citation preview

0 EDGARS

UNAUDITED CONSOLIDATED RESULTSQ1:FY18

18 AUGUST 2017

1

AGENDA

1. Q1:FY18 OVERVIEW

2. MACRO ECONOMIC ENVIRONMENT

3. FINANCIAL REVIEW

4. STRATEGY AND TURNAROUND INITIATIVES

5. WAY FORWARD

2

Q1:FY18 OVERVIEW

• Edcon Group trading profit up 165.4% to R89 million from a loss of R136 million

• Pro-forma adjusted EBITDA increased by 12.7% to R354 million

• Like-for-like retail sales decreased by 1.4% while Edgars like-for-like sales rose 1.6% over the quarter

• Improved results delivered despite retail credit sales decreasing by 7.4% and cash sales down 8.0%

• Gross profit margin up 60 bps from 38.3% to 38.9%

• Overall sales performance impacted by the removal of certain international brands, sale of Legit and closure of stores and trading environment

• Compared to this time last year, Edcon traded with 219 less stores and a 4% reduction in square meterage

• Once off costs removed from the system following the exit of 27 international brands, non-productive space and the clearance of aged stock

EDGARS

3

Q1:FY18 OVERVIEW

• Stock disciplines resulting in inputs and clearance shifts into anormal retail cycle

• Strategy implementation well underway in Jet and Edgars, with improved sales performance

• Merchandise strategy of range rationalisation, focused supplier management, fresher stock and more competitive pricing

• Business model ‘test and learn’ process completed in CNA and Active

• The R1.5 billion investment in IT is underway to halve the IT costs by year three, and transform the Edcon IT infrastructure

• Staff retention improved with the stabilisation of the balance sheet and strategic transformation process

• Transition of company leadership progressing seamlessly

• Results validates turnaround strategy

EDGARSJET

4

EDCON HAS UNDERGONE A RESTRUCTURE TO STREAMLINE OPERATIONS ON CORE BUSINESS

SPECIALTY

CellularInternational Brands

We have made the strategic decision to re-align corporate divisions in order to streamline operations and optimise scale efficiencies found in the larger Edcon Brands.

PREVIOUS STRUCTURE: NEW STRUCTURE

SPECIALTY

International Brands Cellular*

Boardmans & Red Square have moved into the Edgars division

Edgars Active has moved into the Jet division

*Cellular is allocated to chains for reporting purposes

5

2. MACRO ECONOMIC ENVIRONMENTRICHARD VAUGHAN - CFO

6

22232425262728

(1)

-

1

2

3

06-2

016

07-2

016

08-2

016

09-2

016

10-2

016

11-2

016

12-2

016

01-2

017

02-2

017

03-2

017

04-2

017

05-2

017

06-2

017

Real GDP (y-o-y %) Unemployment rate (%)

GDP GROWTH AND UNEMPLOYMENT RATE

456789

06-2

016

07-2

016

08-2

016

09-2

016

10-2

016

11-2

016

12-2

016

01-2

017

02-2

017

03-2

017

04-2

017

05-2

017

06-2

017 4

5.5

7

8.5

10

11.5

06-2

015

08-2

015

10-2

015

12-2

015

02-2

016

04-2

016

06-2

016

08-2

016

10-2

016

12-2

016

02-2

017

04-2

017

06-2

017

EXCHANGE RATES

PRIVATE SECTOR CREDIT EXTENSION (Y-O-Y %) REPO AND PRIME RATE

EXCHANGE RATES

06-2

016

07-2

016

08-2

016

09-2

016

10-2

016

11-2

016

12-2

016

01-2

017

02-2

017

03-2

017

04-2

017

05-2

017

06-2

017

USDZAR EURZAR

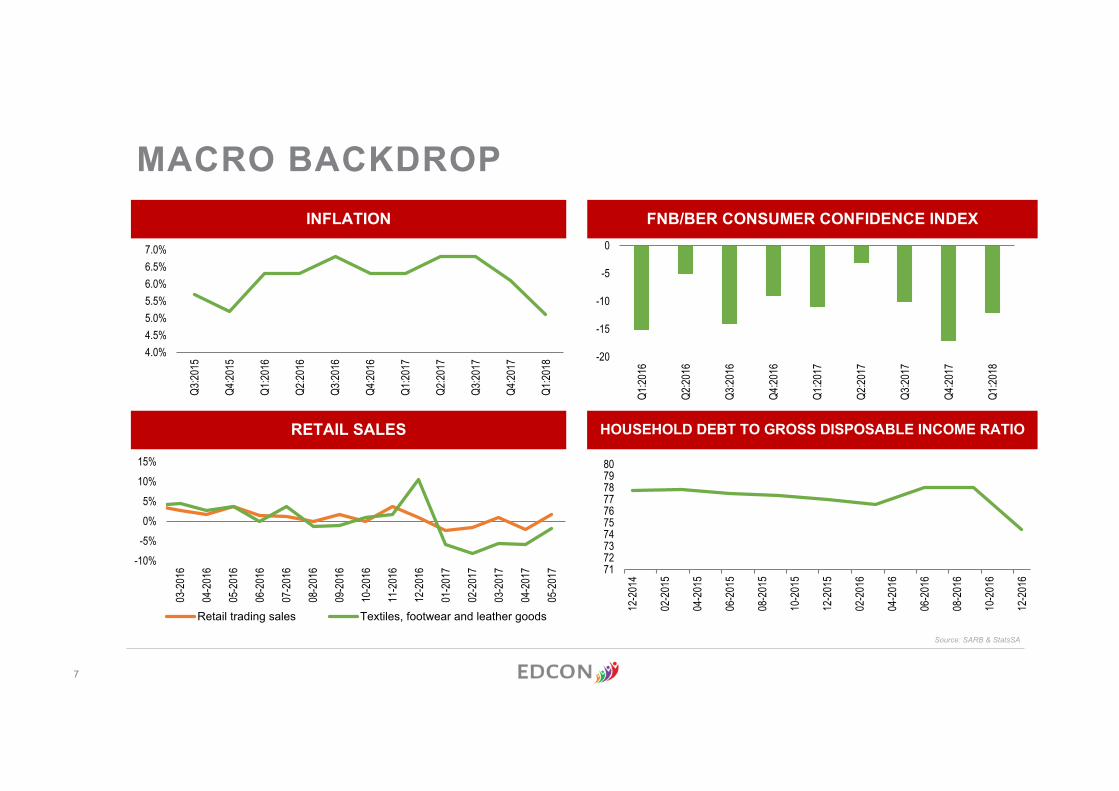

MACRO BACKDROP

Source: SARB & StatsSA

7

4.0%4.5%5.0%5.5%6.0%6.5%7.0%

Q3:20

15

Q4:20

15

Q1:20

16

Q2:20

16

Q3:20

16

Q4:20

16

Q1:20

17

Q2:20

17

Q3:20

17

Q4:20

17

Q1:20

18

INFLATION

-20

-15

-10

-5

0

Q1:20

16

Q2:20

16

Q3:20

16

Q4:20

16

Q1:20

17

Q2:20

17

Q3:20

17

Q4:20

17

Q1:20

18

-10%-5%0%5%

10%15%

03-2

016

04-2

016

05-2

016

06-2

016

07-2

016

08-2

016

09-2

016

10-2

016

11-2

016

12-2

016

01-2

017

02-2

017

03-2

017

04-2

017

05-2

017

Retail trading sales Textiles, footwear and leather goods

71727374757677787980

12-2

014

02-2

015

04-2

015

06-2

015

08-2

015

10-2

015

12-2

015

02-2

016

04-2

016

06-2

016

08-2

016

10-2

016

12-2

016

FNB/BER CONSUMER CONFIDENCE INDEX

RETAIL SALES HOUSEHOLD DEBT TO GROSS DISPOSABLE INCOME RATIO

Source: SARB & StatsSA

MACRO BACKDROP

8

3. FINANCIAL REVIEWBERNIE BROOKES – CEORICHARD VAUGHAN - CFO

9

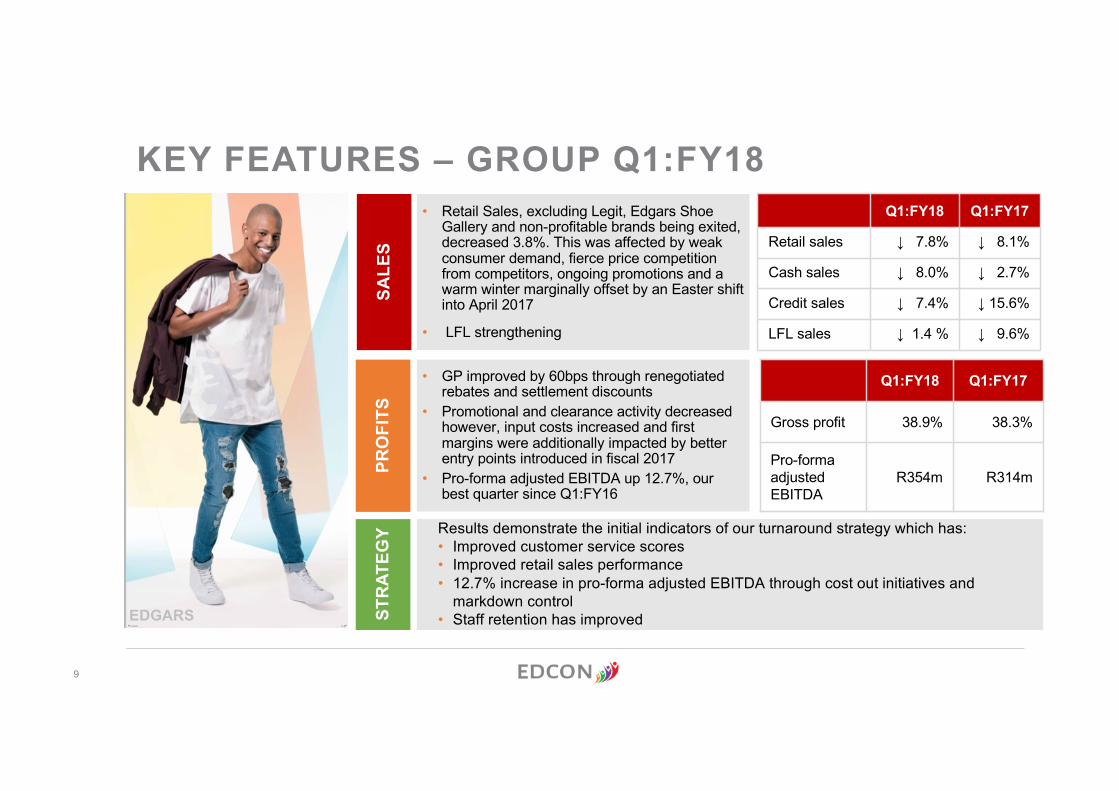

• Retail Sales, excluding Legit, Edgars Shoe Gallery and non-profitable brands being exited, decreased 3.8%. This was affected by weak consumer demand, fierce price competition from competitors, ongoing promotions and a warm winter marginally offset by an Easter shift into April 2017

• LFL strengthening

• GP improved by 60bps through renegotiated rebates and settlement discounts

• Promotional and clearance activity decreased however, input costs increased and first margins were additionally impacted by better entry points introduced in fiscal 2017

• Pro-forma adjusted EBITDA up 12.7%, our best quarter since Q1:FY16

Results demonstrate the initial indicators of our turnaround strategy which has:• Improved customer service scores• Improved retail sales performance • 12.7% increase in pro-forma adjusted EBITDA through cost out initiatives and

markdown control• Staff retention has improved

SALE

SPR

OFI

TSST

RAT

EGY

KEY FEATURES – GROUP Q1:FY18Q1:FY18 Q1:FY17

Retail sales ↓ 7.8% ↓ 8.1%

Cash sales ↓ 8.0% ↓ 2.7%

Credit sales ↓ 7.4% ↓ 15.6%

LFL sales ↓ 1.4 % ↓ 9.6%

Q1:FY18 Q1:FY17

Gross profit 38.9% 38.3%

Pro-forma adjusted EBITDA

R354m R314m

EDGARS

10

• Retail sales decreased 2.9%

- Improved customer experience, focused category management, driving credit and financial services products and change management is starting to show benefits to our customers with a positive 1.6% - LFL sales growth in Q1:FY18- Ladieswear, childrenswear, footwear and

cosmetics had positive retail sales growth- Cash sales decreased 0.5% and credit

sales decreased 5.5%- Easter shift to April 2017

• Gross margin of 42.4% up from 41.8%- Increased supplier discounts- Reduced markdown activity

• 3 new Edgars stores and 3 new Edgars Cosmetics Emporium stores opened

• 5 Edgars stores, 9 Edgars Cosmetics Emporium stores closed

Q1:FY18 Q1:FY17

Retail sales growth (%) (2.9) (8.5)

LFL sales growth (%) 1.6 (12.3)

GP margin (%) 42.4 41.8

Total number of stores 308 306

Capex spend (R’m) 66 61

Av space (‘000sqm) 765 765

EDGARS DIVISION – Q1:FY18219 stores* · LSM 6-10

*Includes 202 Edgars Stores, 1 Edgars sales store ,16 Edgars Cosmetics Emporium

40 stores · LSM 7-10

49 stores · LSM 5-10

11

• Retail sales decreased 2.3%- LFL sales growth decreased by 1.6% as

strategic initiatives started to show benefits through improved in-store experience, re-freshed business model, lay-bye offers, customer service and merchandise assortment improvements- Cash sales decreased 2.6% and credit sales

decreased by only 1.8%- Easter moved to April in 2017 from March

last year- Gross margin of 34.7% from 34.2%- Improved supplier rebates and discounts- Reduced markdown activity

• 20 new Jet stores and 2 Jet Mart stores opened

• 4 Jet stores, 3 Jet Mart stores and 1 Edgars Active Store closed

Q1:FY18 Q1:FY17

Retail sales growth (%) (2.3) (8.9)

LFL sales growth (%) (1.6) (8.4)

GP margin (%) 34.7 34.2

Total number of stores 711 700

Capex spend (R’m) 34 24

Av space (‘000sqm) 652 657

408 stores · LSM 4-7

122 stores · LSM 4-7

JET DIVISION – Q1:FY18

181 stores · LSM 4-7

12

• Includes CNA, mono-branded stores and Legit in Q1:FY18. Q1:FY17 additionally includes the entire Legit business and Edgars Shoe Gallery

• Excluding Legit, Edgars Shoe Gallery and unprofitable international brands, retail sales decreased 12.7% ( 37% reduction in meterage)- Cash sales decreased 40.8% (18.3% excl. Legit

and Edgars Shoe Gallery)- Credit sales decreased 39.4% (12.6% excl.

Legit and Edgars Shoe Gallery)• Margin improvement through:- Renegotiated supplier rebates and discounts- Excluding Legit, Edgars Shoe Gallery and

international brands being exited, gross margin % increased 340 bps to 39.5% from 36.1%

• 2 mono-branded opened

• 5 stores closed- 1 CNA and 4 mono-branded stores

• 10 Legit stores in Botswana disposed during the quarter

Q1:FY18 Q1:FY17

Retail sales growth (%) (40.5) (6.9)

LFL sales growth (%) (10.6) (7.0)

GP margin (%) 38.7 37.9

Total number of stores 266 496

Capex spend (R’m) 14 17

Av space (‘000sqm) 97 156

MONO-BRANDED STORES

195* stores · LSM 7-10

71 stores · LSM 5-10

*Includes 11 Samsung stores

10* stores · LSM 5-8*Stores in Botswana sold effective April 2017

SPECIALTY DIVISION – Q1:FY18

13

STATEMENT OF COMPREHENSIVE INCOME

(R millions) Q1:FY18 Q1:FY17 % change

Retail sales 5 508 5 973 (7.8)

Gross profit 2 142 2 286 (6.3)

Gross profit margin 38.9 38.3 0.6pts

Other income 327 454 (28.0)

Store costs (1 559) (1 703) (8.5)

Other operating costs(1) (1 003) (1 169) (14.2)

Share of profits of associates and insurance business 182 (4)

Trading profit 89 (136) 165.4

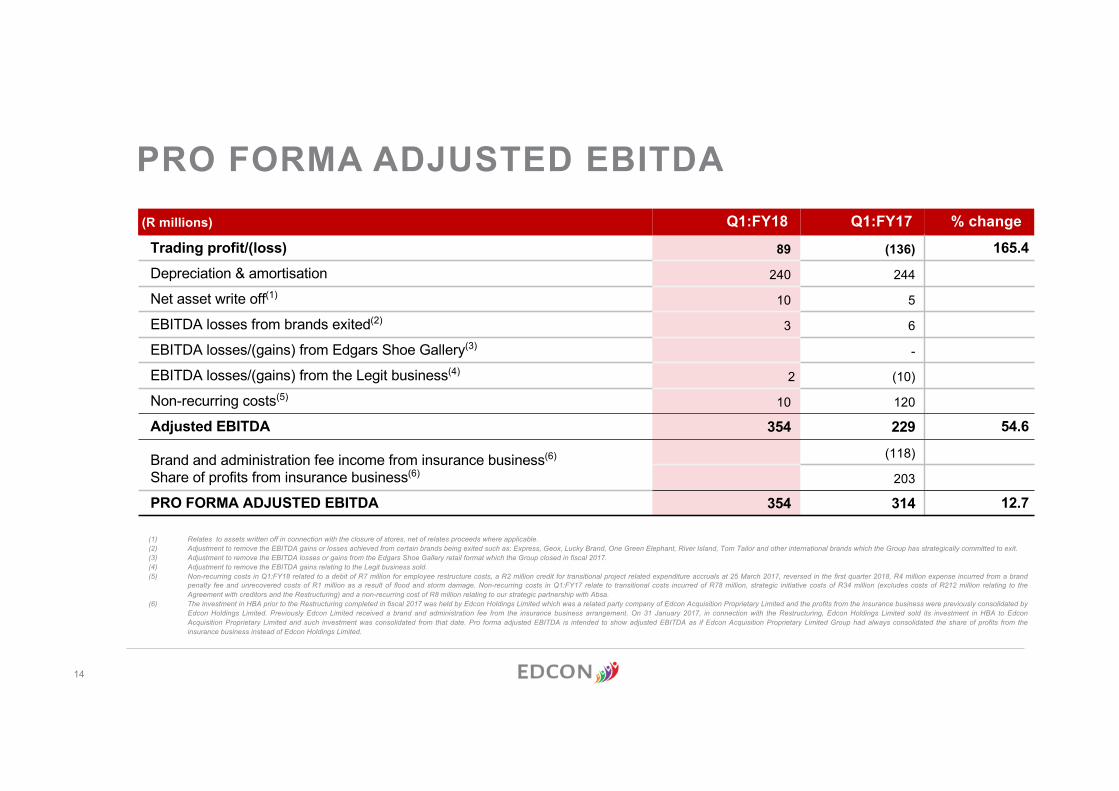

PROFORMA ADJUSTED EBITDA 354 314 12.7(1) Includes non-recurring costs of R10 million in Q1: FY18 (Q1: FY17 – R120 million). See cost analysis –Q1: FY18

14

(R millions) Q1:FY18 Q1:FY17 % change Trading profit/(loss) 89 (136) 165.4Depreciation & amortisation 240 244

Net asset write off(1) 10 5

EBITDA losses from brands exited(2) 3 6

EBITDA losses/(gains) from Edgars Shoe Gallery(3) -

EBITDA losses/(gains) from the Legit business(4) 2 (10)

Non-recurring costs(5) 10 120

Adjusted EBITDA 354 229 54.6

Brand and administration fee income from insurance business(6)

Share of profits from insurance business(6)

(118)

203

PRO FORMA ADJUSTED EBITDA 354 314 12.7

(1) Relates to assets written off in connection with the closure of stores, net of relates proceeds where applicable.(2) Adjustment to remove the EBITDA gains or losses achieved from certain brands being exited such as: Express, Geox, Lucky Brand, One Green Elephant, River Island, Tom Tailor and other international brands which the Group has strategically committed to exit.(3) Adjustment to remove the EBITDA losses or gains from the Edgars Shoe Gallery retail format which the Group closed in fiscal 2017.(4) Adjustment to remove the EBITDA gains relating to the Legit business sold.(5) Non-recurring costs in Q1:FY18 related to a debit of R7 million for employee restructure costs, a R2 million credit for transitional project related expenditure accruals at 25 March 2017, reversed in the first quarter 2018, R4 million expense incurred from a brand

penalty fee and unrecovered costs of R1 million as a result of flood and storm damage. Non-recurring costs in Q1:FY17 relate to transitional costs incurred of R78 million, strategic initiative costs of R34 million (excludes costs of R212 million relating to theAgreement with creditors and the Restructuring) and a non-recurring cost of R8 million relating to our strategic partnership with Absa.

(6) The investment in HBA prior to the Restructuring completed in fiscal 2017 was held by Edcon Holdings Limited which was a related party company of Edcon Acquisition Proprietary Limited and the profits from the insurance business were previously consolidated byEdcon Holdings Limited. Previously Edcon Limited received a brand and administration fee from the insurance business arrangement. On 31 January 2017, in connection with the Restructuring, Edcon Holdings Limited sold its investment in HBA to EdconAcquisition Proprietary Limited and such investment was consolidated from that date. Pro forma adjusted EBITDA is intended to show adjusted EBITDA as if Edcon Acquisition Proprietary Limited Group had always consolidated the share of profits from theinsurance business instead of Edcon Holdings Limited.

PRO FORMA ADJUSTED EBITDA

15

OTHER OPERATING COSTS STORE COSTS

COST ANALYSIS Q1:FY18

• Other operating costs excl. non-recurring costs decreased by 5.3% attributable to renegotiated contracts offset by additional manpower costs for IT as the Group embarks on its IT strategy

• Store costs well managed decreasing by 8.5% - Closure of unprofitable stores during the

quarter - Rental and manpower constitute 61.7% of

total costs for Q1:FY18 (59.9% in Q1:FY17)

(R millions) Q1:FY18 Q1: FY17 % change

Other operating costs(excl. non-recurring costs)

993 1 049 (5.3)

Non-recurring costs10 120

TOTAL 1 003 1 169 (14.2)

16

CASH FLOW – Q1:FY18

198

117280

63101

OPERATING ACTIVITIES

OPENING CASH BALANCE

WORKING CAPITAL

MOVEMENT

CAPEX NET FINANCING COSTS

FINANCING ACTIVITIES

7

TAX

1 651

CLOSING CASH

BALANCE

455

(315)Trade and other

revceivables1Inventories

(23)

Trade and other payables

(1) Includes R39 million proceeds relating to the sale of the written down trade receivables book sold in fiscal 2017.

1 787

R’m Working capital

17

(R millions)(1) Cash PIK Q1:FY18 Q1:FY17Super Senior Secured debt

EUR Refinanced Facility A1 due 31 December 2017(2) E+4.00% 8.00% 632EUR Super Senior Facility due 31 December 2017 – Facility A2(2,3) E+4.00% 8.00% 1 972 2 075ZAR Super Senior RCF Term Loan due 31 December 2019(4) J+5.00% 3.00% 2 131 3 297

ZAR Converted revolving credit Facility until 31 December 2019(4,5)J+5.00% 3.00% 1 250

ZAR Super Senior Hedging Debt due 31 December 2017(6)JIBAR 8.00% 675

EUR Super Senior Term Loan due 31 December 2017(6) EURIBOR 8.00% 633EUR Super Senior PIK notes due 30 June 2019(6) 8.00% 1 842

Senior Secured debtZAR term loan due 31 December 2017(6) J+7.00% 3.00% 3 020EUR fixed rate note due 1 March 2018(6) 9.50% 10 244USD fixed rate note due 1 March 2018(6) 9.50% 3 780Lease liabilities 302 319

EUR Senior secured PIK Toggle notes due 30 June 2019(6) 9.75%(no toggle)

12.75%(toggle) 481

Other Loans (7) 206 304Gross third party debt 6 493 26 670Derivatives 50Cash held in escrow on Legit sale (634)Cash and cash equivalents (1 651) (1 111)

Net third party debt 4 208 25 609(1) FX rates at end Q1:FY17 were R15.19:$ and R16.81:€; and at the end of Q1:FY18 were R12.97:$ and R14.48:€.(2) The maturities may be extended in exchange for a cash margin uplift from 4.0% to 9.0% if certain leverage conditions are satisfied.(3) The maturity may be extended to 30 September 2018 or 31 December 2018 if certain leverage conditions are satisfied.(4) The maturity may be extended to 31 December 2020 if certain refinancing conditions are satisfied.(5) The total available facility is R1,825 million of which R575 million was undrawn at 24 June 2017. (6) This debt was restructured or amended as part of the Restructuring.(7) The portion of this debt relating to Zimbabwe was R137 million in Q1:FY18 and R229 million in Q1:FY17.(8) At the end of the period R204 million of a Super Senior LC facility were utilised for guarantees and LC’s.

EDGARS | WINTER 16

NET THIRD PARTY DEBT

JET

18

4. STRATEGY & TURNAROUND INITIATIVESBERNIE BROOKES - CEO

19

ROADMAP WITH STRATEGIC INITIATIVES2016 2017

INITIATIVESTATUS UPDATE

OCT NOV DEC JAN FEB MAR APR MAY JUN JUL AUG SEP

GROWTH

ENABLERS

COST

LEAN HQ & OPERATING MODEL

GNFR

COGS REDUCTION

PROPERTY

EDGARS CHAIN: TURNAROUND/CUSTOMER CENTRICITY

JET CHAIN: LEAN DISCOUNT RE-POSITIONING

SPECIALTY CHAINS: STRATEGY REVIEW AND REFRESH

CREDIT SALES

LOYALTY PROGRAM

CUSTOMER CENTRICITY

IT STRATEGY AND RENEWAL PLAN

SUPPLY CHAIN & LOGISTICS ROADMAP

SUPPLIER ENGAGEMENT

INVENTORY

Savings realized and locked in

Savings being realized

Savings being realized

Savings being realized

Initiatives underway – customer experience,category management, change management

Initiatives underway – In-store experience, every day low price & cost savings

Legit sale completePortfolio strategy review underway

Own book sales picking up ( over R400m)

Strategy developed and initial value target identified

NPS roll-out underway

Strategy and roadmap complete. RFP’s launched

Strategy and roadmap complete. Roll-out underway

Review underway

Review underway

1

2

3

4

5

6

7

8

9

10

11

12

13

14

20

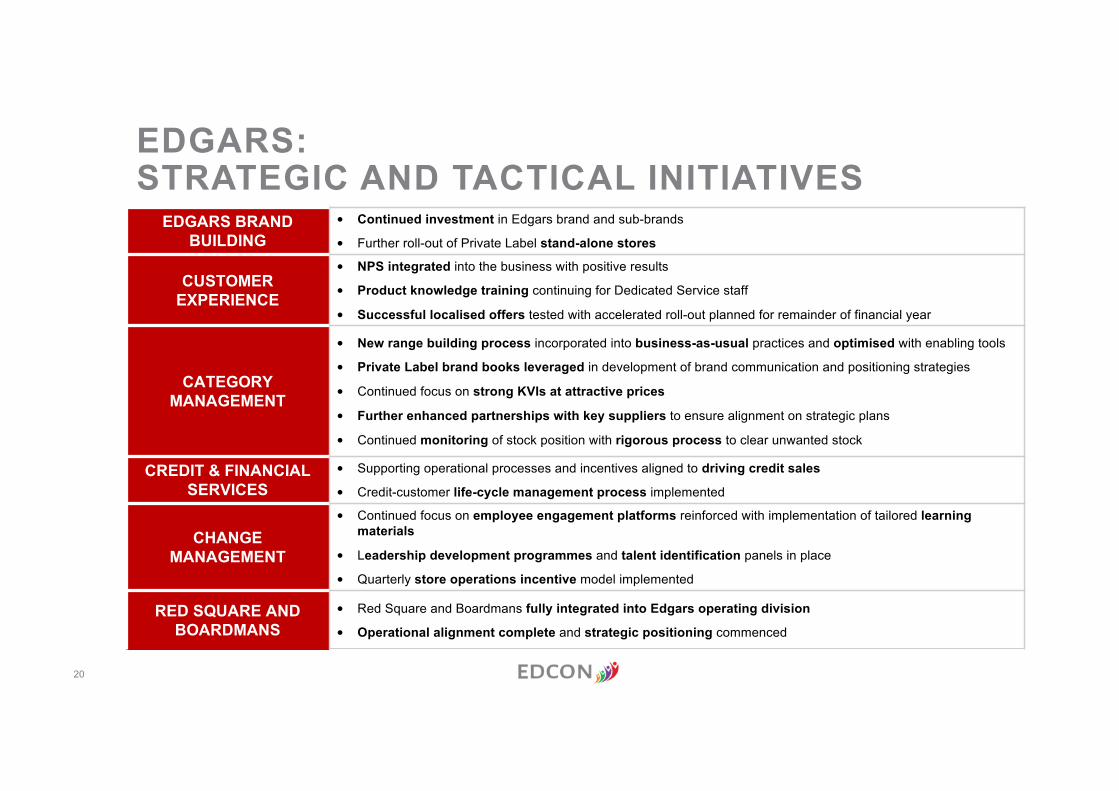

EDGARS: STRATEGIC AND TACTICAL INITIATIVES

EDGARS BRAND BUILDING

• Continued investment in Edgars brand and sub-brands

• Further roll-out of Private Label stand-alone stores

CUSTOMER EXPERIENCE

• NPS integrated into the business with positive results

• Product knowledge training continuing for Dedicated Service staff

• Successful localised offers tested with accelerated roll-out planned for remainder of financial year

CATEGORYMANAGEMENT

• New range building process incorporated into business-as-usual practices and optimised with enabling tools

• Private Label brand books leveraged in development of brand communication and positioning strategies

• Continued focus on strong KVIs at attractive prices

• Further enhanced partnerships with key suppliers to ensure alignment on strategic plans

• Continued monitoring of stock position with rigorous process to clear unwanted stock

CREDIT & FINANCIALSERVICES

• Supporting operational processes and incentives aligned to driving credit sales

• Credit-customer life-cycle management process implemented

CHANGEMANAGEMENT

• Continued focus on employee engagement platforms reinforced with implementation of tailored learning materials

• Leadership development programmes and talent identification panels in place

• Quarterly store operations incentive model implemented

RED SQUARE AND BOARDMANS

• Red Square and Boardmans fully integrated into Edgars operating division

• Operational alignment complete and strategic positioning commenced

21

JET: STRATEGIC AND TACTICAL INITIATIVES

SALES GROWTH

• Optimise store footprint: improve store productivity & profitability by identifying opportunities for consolidations, carve outs & reductions

• Turnaround JetMart: through localisation, changed customer perception and exiting categories that don’t fit with the brand

• New Growth: continued roll out of small store formats

• Category Management: recapture lost market share in key categories while remaining price competitive

• Redefine Active: stabilise and grow active to capture the youth market while improving profitability

• In-store experience: improved store shopping experience for customers through layout & visual changes

• Customer Centricity: embedded a truly effective customer centric marketing strategy that is right for the brand and rolled out NPS to all stores

GP IMPROVEMENT• Markdowns: improved GP through better markdown management

• Pricing: Continued focus on everyday low price items and key entry price points

CREDIT & FINANCIAL SERVICES

• Credit: Revised agreement with ABSA resulting in more control over new business credit sales• FS: Continue to drive additional income on insurance products through the operations channel

COST SAVINGS• Advertising: Revised strategy in place and has been realising media, cost and ROI efficiencies

• Lean operating model: Continued focus on cost savings

PEOPLE• Improving employee engagement: Continued focus on people initiatives to improve the employee experience that

empowers employees to deliver on business results• Improving strategic capability: Continued focus on leadership capability, through the launch of the Jet Retail and

Leadership Academy to improve leadership and functional competencies to deliver on business results

22

SPECIALTY: STRATEGIC AND TACTICAL INITIATIVES

• Consolidation of supplier base completed• Pilot revised product range and layout – CNA aims to re-establish itself as the dominant

stationery retailer through an expanded stationery range that includes a greater selection of fun and trendy products. This will be associated with a revised store layout to emphasise these changes

• Pilot of localised ranges under way to refine product offering by location• Ongoing evaluation of store network, including a potential revision in location strategy

CELLULAR

• Optimize range – Establish a top selling core range of products with localised supporting ranges of higher and lower selling price products tailored by geographic node

• Improved allocation - reduced store grids, to increase customer journey consistency and simplify processes

• Improve in-store visibility through in store advertising, and where possible relocating the Cellular pad closer to financial services

• Increase connections and improve customer life cycle management• Drive online sales

INTERNATIONAL BRANDS

• Continue exit of River Island and other underperforming in-store brands (River Island will continue to be available via their website)

• Continually engage on-going brands to collaboratively improve go to market propositions that deliver brand equity, aspirational product and customer experience while strengthening and enhancing the fashion credibility of the Edgars brand

• Right-size store footprint

23

SHIFTS & SAVINGS

• Increased collaboration, commitment and trust across the entire demand chain to achieve full potential.

• Focused on a lean sourcing operation through innovation, transparency and sustainabilityresulting in increased productivity per headcount

• On track to reduce reliance on indirect vendors (3rd party imports) from 44% to 17% by Winter 2018 • Shifts & vendor management across our direct vendor base to achieve estimated savings of 4% to

6%• Consolidation, across programs to maximise scale and drive volume• Increased vendor support for capability and capacity management• Reallocating sourcing geographies and vendors to align with market trends

LOCAL/REGIONAL FOCUS

• Total Direct Local / Regional spend to increase by 4% to 6% versus FY17• South African production estimated at 68 -72% of total Local / Regional spend • Increase Regional sourcing to support our Africa growth strategy• Achieve shorter lead-times by pursuing fabric bundling

CELROSE & EDDELS

• New denim plant fully operational, creating 150 new jobs • Established a dedicated knits line for ladieswear resulting in an additional 60 machinists• Product expansion to heels and boots together with 4 dedicated pump lines has resulted to 330 new

jobs

COGS: SAVINGS AND INITIATIVES

24

EFFICIENT LOGISTICS

• “Speedlining” initiative fully implemented and DC to store lead-times have reduced by 2.5 days• 80% of DC deliveries processed and dispatched to the depot on the same day• DC delivery windows for non replenishment product (Fashion) have been adjusted to ensure no stock

is held in the DC’s over weekends resulting in positive working capital benefit

• Continued collaboration with the chains to smooth weekly flow of inputs are yielding positive results with Merchant groups

• Design & implementation of the lead-time cube has increased visibility of lead-times across the Supply Chain network

MINIMAL STOCK ROOM PROCESSING

• Ramping up delivery of floor ready merchandise to stores i.e. Hanger Value Added Service (VAS), which helps free up store staff to focus on customer service

• The delivery of floor ready merchandise not only reduces processing times (store receipt to floor) but also stock losses/damages as merchandise is sent directly to the sales floor

IMPROVED ALLOCATION

• Hold back initiative has been rolled out with holdback styles performing well above the 15% markdown reduction target

• Shifting focus to multiple orders thereby reducing interest on inventory and improve working capital

SUPPLY CHAIN: STRATEGIC AND TACTICAL INITIATIVES

25

IT TRANSFORMATION UPATE

• Networks, Service Desk and Desktop renegotiations finalised

• Data Centre to be finalised by year endINFRASTRUCTURE

• RFP activity completed with contract awarded • Software license negotiations expected to be

finalised by end AugustINTEGRATION

• RFP activity nearing completion• Short-listed vendors selected and final

negotiations underwayPOS

MERCHANDISE AND PLANNING

FINANCE

BUSINESS INTELLIGENCE

• RFP activity nearing completion• Short-listed vendors selected and final

negotiations underway

• RFP activity nearing completion• Short-listed vendors selected and final

negotiations underway

• RFP activity nearing completion• Short-listed vendors selected and final

negotiations underway

IT ROADMAP DEVELOPED

3 year timeline for primary project delivery, starting with systems implementation mid-2017 after

completion of vendor contracting period

26

CREDIT, FINANCIAL SERVICES & COMMERCIAL SALES

CREDIT PORTFOLIO

• Revised Absa acquisition strategy positively driving credit sales: The revised strategy, which was implemented in November 2016, has resulted in stronger credit sales growth across all Chainsand is expected to gain further momentum over FY18 festive trade period

• Reintroduction of Regulatory compliant automated credit limit increases: The reintroduction of ACLI’s has resulted in positive growth in credit sales with the real benefit expected over the festive trade period

• Positive progress with revised compliance, new account application and credit limit increase processes: First phase of process expected to be implemented by October 2017 focused on improved customer experience

• Introduce targeted credit marketing campaigns, resulting in increased shopping frequency• Continuous focus collections efficiency, resulting in improved portfolio performance• Continue to consider various funding option for Edcon funded portfolio to support continuous

growth

FINANCIAL SERVICES PRODUCTS

• Continued strong performance of Hollard insurance partnership • Introduction of revised Legal product expected to further support growth

COMMERCIAL SALES GROWTH

• Commercial sales unit continues to positively contribute to Group sales• Gift card sales continue to show strong growth though new corporate partnerships• More focused 3rd party credit offering positively contributing to credit sales• Piloting corporate sales offering with strong future growth prospects• Piloting term loan financing model in selected CNA and JetMart stores to support big ticket item

sales

27

5. WAY FORWARDBERNIE BROOKES - CEO

28

WAY FORWARDThe roll-out of the strategic and tactical initiatives for all areas of the business will continue, which include:

• Enhancing the rationalisation of the overall range• Accelerating the store optimisation and service delivery model across

additional stores• Being even more competitive on price• Initiating faster stock turns• Improving the private label offering• Deliver floor ready merchandise to stores • Improved stock allocations• Completing the implementation of the Net Promotor Score (NPS) system,

while further embedding customer service into the various chains• Continue to develop Jet small store concept• Advancing the plans for the turn-around of CNA, Cellular and other

businesses.• Promote and support local manufacturing• Launch the new Thank U Loyalty Programme• Focus on preparation for Christmas

EDGARS

29 EDGARS

UNAUDITED CONSOLIDATED RESULTSQ1:FY18

18 AUGUST 2017

For more information: www.edcon.co.za | [email protected]

EDGARS