Embed Size (px)

Citation preview

UNCLASSIFIED

UNCLASSIFIED

Activity and Cost Analysis of a Scheduling Problem

Terry WeirJoint Operations Division

UNCLASSIFIED

UNCLASSIFIED

Outline

Introduction Background Problem Data Regression Analysis Simulations Summary

UNCLASSIFIED

UNCLASSIFIED

Introduction

A sample of previous activity and costing studies

Topic Theme Client Report

RAN Fleet Aviation Management Study 1999 Rate of Effort Costs RAN NAFMR

Collins Class Cost of Ownership Sustainment COLSPO DSTO-TR-2131

Collins Class Activity Analysis Readiness CDG DSTO-CR-2012-0230

Parameterisation of the ASW Mission Operational Planning ALG DSTO-TR-2413

Preparedness Modelling and Analysis Tool - Phase 1 Preparedness Management DGDPREP DSTO-TR-2011-0314

Fleet Costing Study 2000 Fleet Options Costing FASRFP

Quantifying Current Aggregate Sea Training Requirements of the Fleet 2010 Collective Training FHQ

KPMG PAL Review (ANZAC Detailed Force Element Review) 2009 Preparedness Management DGDPREP

Productivity Measurement in the Royal Australian Navy: A Preliminary Analysis (CEPA) Productivity Management SCFEG

A Statistical Activity Cost Analysis of a Fleet Scheduling Problem 2010 Fleet Activity Costing NHQ

Engineering Asset Management and

Infrastructure Sustainability

UNCLASSIFIED

UNCLASSIFIED

ReferencesCooper, R., (1988) The rise of activity-based costing – part one: what is an activity-based cost system? Journal of Cost Management, 2, 45-54

Noreen, E., (1991) Conditions under which activity-based cost systems provide relevant costs, J. Man. Acc. Res, Fall, 159-168

Willett, R.J. (1987). An axiomatic theory of accounting measurement. Acc. Bus. Res., 17, 155–171

Willett, R.J. (1988). An axiomatic theory of accounting measurement—part II. Acc. Bus. Res., 19, 79–91

Colin, A., Lambrineas, P., Weir, T. and Willet, R.J. (2011) Statistical Activity Cost Regression Analysis of a Scheduling Problem, in J. Mathew et al. (eds.), Engineering Asset Management and Infrastructure Sustainability, pp 121-131, Springer-Verlag London Limited

Amadi-Echendu , J., Willett, R. J., Brown, K., Matthew, J., Vyas, N. and Yang, B-S. (2010) What Is Engineering Asset Management? In Amadi-Eschendu et al. (eds) Engineering Asset Management Review 1, Definitions, concepts and scope of engineering asset management pp 3-16, Springer-Verlag London Limited.

UNCLASSIFIED

UNCLASSIFIED

Background to this studyTraditional cost accounting

Costs allocated to products based on volume of product or output

Simple to use Little computing power needed

Activity based costing (see eg Cooper 1988) Activities generate costs Two stage allocation

– Activities– Products or outputs

Greater segmentation of costs & fidelity Higher computation requirements Questions over appropriateness of activities Conditions for accuracy and cost separation are very

strong (Noreen 1991)

Both methods suffer from arbitrary allocations and assume recorded costs are deterministic

UNCLASSIFIED

UNCLASSIFIED

Statistical Activity Cost Analysis (Willett 1987, 1988) Axiomatic model addresses:

– Transaction costs– Continuity of production relations– Separability of production relations

Background

C

t

Activity

Costs

timett -1

a0

a2

a1

Asset at t-1

Equity at t

Asset at t

Asset at t-1

Asset at t

Can recover all accounting arithmeticCosts are random variablesApplication to earnings, depreciation and goodwillApplication to reliability analysis, portfolio budgeting and scheduling

R. Willet 2004

UNCLASSIFIED

UNCLASSIFIED

Problem – can we relate Navy fleet activities to costs

A key question in Defence planning is “how much does it cost to conduct an exercise, event or activity?”

Our question is can the cost of activities be estimated, based on a knowledge of past activity levels?

If we can do this this we can use this to better estimate costs for budgeting, risk analysis etc

By product : better preparedness management

Typical costing approaches tend to be subjective and deterministic. We aim for a statistical approach.

UNCLASSIFIED

UNCLASSIFIED

Data Navy Activities

FAMT provides data for the ‘activity’ dimension

Fleet activities generate Navy outputs

Activity data can be described by multiple parameters: duration, type, location, operation….

UNCLASSIFIED

UNCLASSIFIED

DataCosts

Data sourced from Defence ERP systems ROMAN, JFL, SDSS/MILIS, COMSARM, PMKEYS, ADFPAY, CENRESPAY

Consolidated in Navy’s Activity Based Management System

Costs categorised by ship class and expense type

Costs aggregated by quarter

UNCLASSIFIED

UNCLASSIFIED

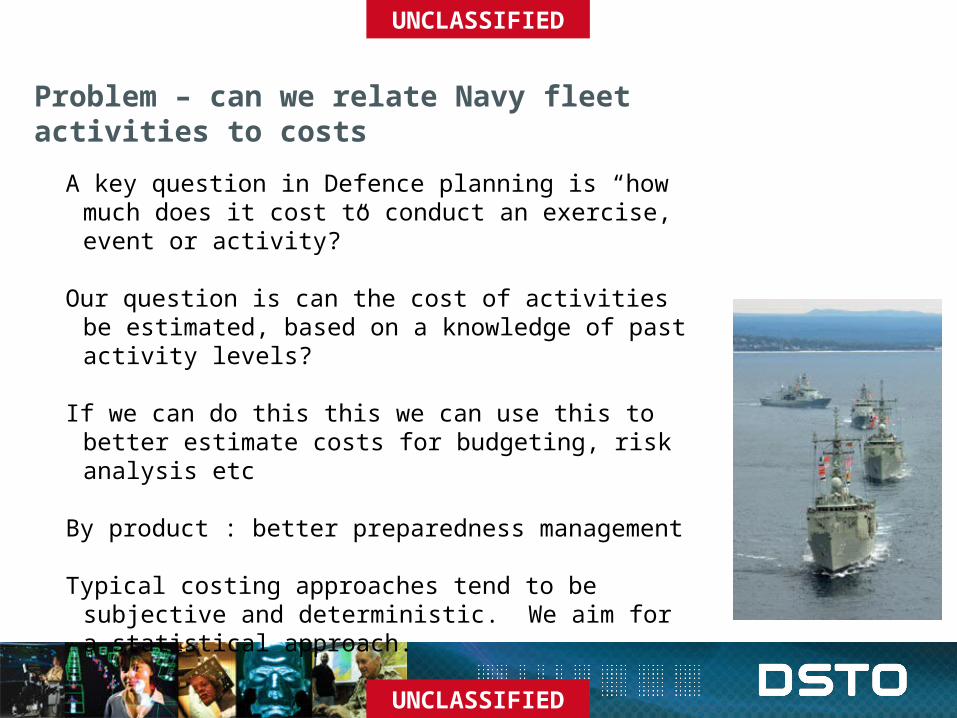

Sample Data

4 platforms, P1..P4, same class, 6 cost categories, direct costs only, 26 quarters

Proportional Standard Deviations

Personnel 0.02

Maintenance 0.04

Fuel 0.02

Expenses 0.02

Inventory 0.08

Ordnance 0.04

Average Quarterly Cost Proportions

47%

28%

14%

5% 2% 4%Personnel

Maintenance

Fuel

Expenses

Inventory

Ordnance

Average cost per quarter $7.59m

Standard deviation per quarter $1.39m

UNCLASSIFIED

UNCLASSIFIED

Observed correlations

Average correlations between cost categories

Total Fuel Expenses

Inventory

Ordnance

Personnel Maintenance

Total 1.00

Fuel 0.30 1.00

Expenses 0.17 0.22 1.00

Inventory 0.39 -0.15 -0.28 1.00

Ordnance 0.46 0.03 -0.02 0.39 1.00

Personnel 0.61 0.13 0.51 -0.05 0.32 1.00

Maintenance

0.51 -0.23 -0.13 0.28 0.05 -0.19 1.00

Cost

Cost

M

I ?

EF

PO ?

UNCLASSIFIED

UNCLASSIFIED

RegressionWhen durations of events are included: No simple contemporaneous relationship between

costs and events in current time periods But if lags are considered, a systematic pattern

emerges Simple model:

, , , , 1 , 1 , 2 , 2 , 3 , 3i t i i t i t i t i t i t i t i t i t iY A A A A

Yi,t are the costs in each category

Ai,t are the away from home port times

i are the fixed costs

i,t are prices of variable away times

Current costs depend on past activities! This is not what is expected from ABC!

UNCLASSIFIED

UNCLASSIFIED

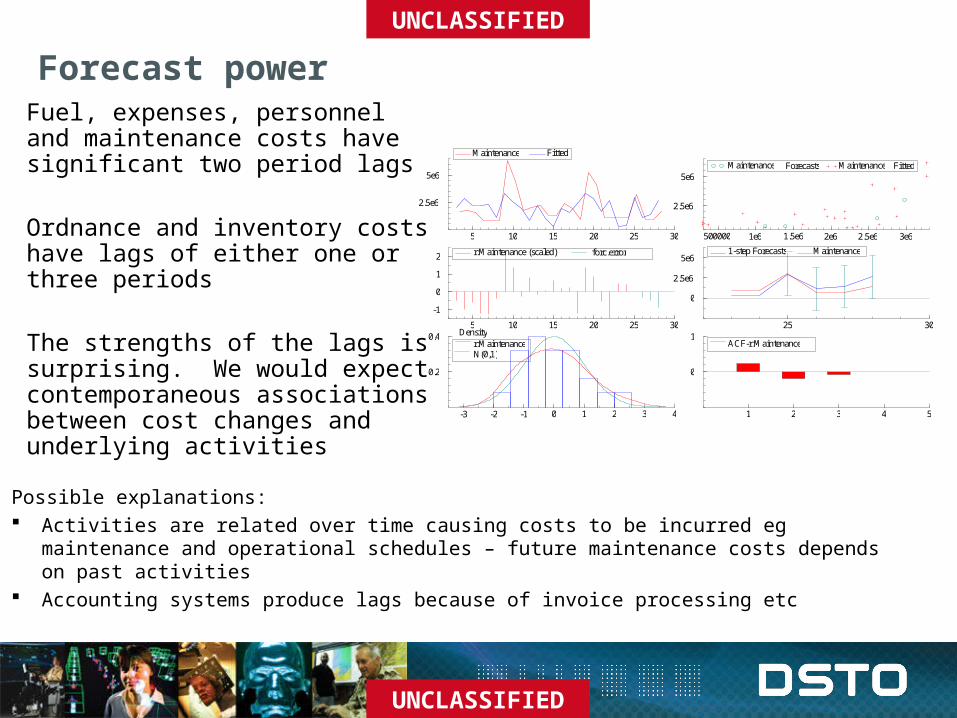

Forecast powerFuel, expenses, personnel and maintenance costs have significant two period lags

Ordnance and inventory costs have lags of either one or three periods

The strengths of the lags is surprising. We would expect contemporaneous associations between cost changes and underlying activities

5 10 15 20 25 30

2.5e6

5e6

Maintenance Fitted

500000 1e6 1.5e6 2e6 2.5e6 3e6

2.5e6

5e6 Maintenance Forecasts Maintenance Fitted

5 10 15 20 25 30 -1 0 1 2 r:Maintenance (scaled) forc.error

25 30

0

2.5e6

5e6 1-step Forecasts Maintenance

-3 -2 -1 0 1 2 3 4

0.2

0.4 Density r:Maintenance N(0,1)

1 2 3 4 5

0

1 ACF-r:Maintenance

Possible explanations: Activities are related over time causing costs to be incurred eg maintenance and

operational schedules – future maintenance costs depends on past activities Accounting systems produce lags because of invoice processing etc

UNCLASSIFIED

UNCLASSIFIED

Forecast powerMore advanced model Costs as a function of alongside time, at sea time, maintenance

time Again statistically significant lagged relationships But the improvement is not remarkable

Simply adding more data does not necessarily improve forecast power

2000 2005 0

1e6

2e6

C f , t = 1 6 1 5 0 2 0 - 1 2 4 6 4 A a , t - 1

- 1 5 0 7 3 A m , t - 1 FuelDeflated Fitted

250000 500000 750000 1e6 1.25e6 1.5e6 0

1e6

2e6 FuelDeflated Fitted

FuelDeflated Forecasts

2000 2005 -1 0 1 2 Residuals:

FuelDeflated (scaled) Forecast error

2005 2006 2007 0

1e6

2e6 1-step Forecasts FuelDeflated

-2 -1 0 1 2 3 4

0.2

0.4

Density Residuals:FuelDeflated N(0,1)

0 5

0

1 ACF-Residuals:FuelDeflated

UNCLASSIFIED

UNCLASSIFIED

Simulations

SACA is based upon the objective of providing an improved description of the relationships between physical processes and financial measurements.

In this it is similar to activity based costing.

SACA integrates statistical theory into the analysis of these relationships.

If alternate attributes such as capability or risk measures can be related to physical tasks, then we can model the interaction of costs, capability and risk

UNCLASSIFIED

UNCLASSIFIED

Example Simple Simulation

We assume ‘Capability’ is a decaying function of time from last major maintenance. Capability is refreshed in maintenance

The simulator generates events

Maintenance periods are quarterly or biannual

Platform activities are uniformly distributed over a six month period beginning with the start of maintenance

The duration of maintenance periods are randomly generated from a beta distribution

Platform activities arrive randomly conditional upon their planned maintenance; non-zero probabilities of multiple platforms in maintenance simultaneously

Costs are generated using the away times generated by the maintenance schedules

Overall fleet capability is measured on a daily basis by averaging individual daily capability

Ships

P1

P2

P3

P4

Simulated Maintenance and Away Periods

Time

Beta Distribution

0

0.5

1

1.5

2

2.5

3

0 0.2 0.4 0.6 0.8 1

UNCLASSIFIED

UNCLASSIFIED

Example Sample Simulation

22.5

23

23.5

24

24.5

25

0 0.1 0.2 0.3 0.4 0.5 0.6 0.7 0.8 0.9 1

Capability

Cost (Arb. $)

Three month schedule Six month schedule

UNCLASSIFIED

UNCLASSIFIED

Summary & ConclusionsGood results exhibit potential to use SACA in modelling cost and activity data

The model demonstrated here has a fixed and variable component. Better understanding of ‘cost drivers’ will enable models to eliminate lags as much as possible

Capability and capacity metrics can be utilised in simulations based on SACA

Automation of data capture etc should allow for decision support tools

Direct applicability to cost generation in FAMT

5 10 15 20 25 30

2.5e6

5e6

Maintenance Fitted

500000 1e6 1.5e6 2e6 2.5e6 3e6

2.5e6

5e6 Maintenance Forecasts Maintenance Fitted

5 10 15 20 25 30 -1 0 1 2 r:Maintenance (scaled) forc.error

25 30

0

2.5e6

5e6 1-step Forecasts Maintenance

-3 -2 -1 0 1 2 3 4

0.2

0.4 Density r:Maintenance N(0,1)

1 2 3 4 5

0

1 ACF-r:Maintenance

, , , , 1 , 1 , 2 , 2 , 3 , 3i t i i t i t i t i t i t i t i t i t iY A A A A

22.5

23

23.5

24

24.5

25

0 0.1 0.2 0.3 0.4 0.5 0.6 0.7 0.8 0.9 1

Capability

Cost (Arb. $)

Three month schedule Six month schedule